Crude Prices Are Collapsing To 5-Month Lows After Lagarde Comments Tyler Durden

Thu, 10/29/2020 – 09:48

The last three days have seen a total bloodbath in black gold as WTI plunges to a $34 handle and Brent drops below $37.

“It’s all about the coronavirus still, and the reaction to the rise in cases, especially in Europe,” said John Kilduff, a partner at Again Capital LLC. “These lockdowns are serious and a blow to what’s been seen as good progress in terms of demand coming back.”

Some have blamed this last leg on the ECB:

Lagarde warned that there’s a clear deterioration in the outlook and the recovery in the euro area is “losing momentum more rapidly than expected.”

And that just added to demand woes as oil is also contending with supply issues.

American crude inventories rose the most since July last week, while Libyan output is also gaining rapidly. As a result, the size of expected inventory declines in the fourth quarter is falling rapidly, according to JPMorgan Chase & Co.

“The recovery of oil demand in Europe has stalled in recent weeks,” said Giovanni Staunovo, commodity analyst at UBS Group AG.

“We previously forecast the oil market to be in deficit in 4Q. It now will likely be balanced and might even flip into oversupplied in November and December.”

Four big legs lower have dragged the price of WTI from $42 to $34…

And Brent plunged to a $36 handle – its lowest since May…

Currently, the only bright spot in demand is China, which is expected to sustain solid demand in the fourth quarter and into the start of 2021, Aramco Trading’s Al-Buainain told Gulf Intelligence… but how long will that last if we get a second wave in Asia?

via ZeroHedge News https://ift.tt/3mAZEyK Tyler Durden

“All Hell Could Break Loose”: Wednesday’s “Liquidation Combination Of Doom” Has Taken Place On Only Two Prior Occasions In History Tyler Durden

Thu, 10/29/2020 – 09:32

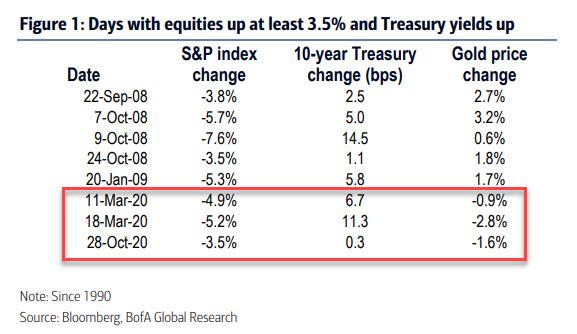

Yes, yesterday’s furious 3.5% equity selloff – the biggest since June 11 – was painful, but in isolation it should have been manageable for investors using legacy balanced 60/40 (or risk parity) portfolios. However that was not the case because as BofA’s Hans Mikkelsen writes overnight, what was truly unique about the Wednesday rout is that as stocks cratered, Treasury yields were up and gold is down, or as the BofA strategist puts it “everything on sale”, in other words a perfect liquidation.

Such a selloff is so against the core tenets of conventional market flows, that this combination – of stocks, bonds and gold down on the same day – only happened twice in market history – on March 11 and March 18th – during the liquidity crisis where nearly all assets where liquidated as risk-parity funds were hammered.

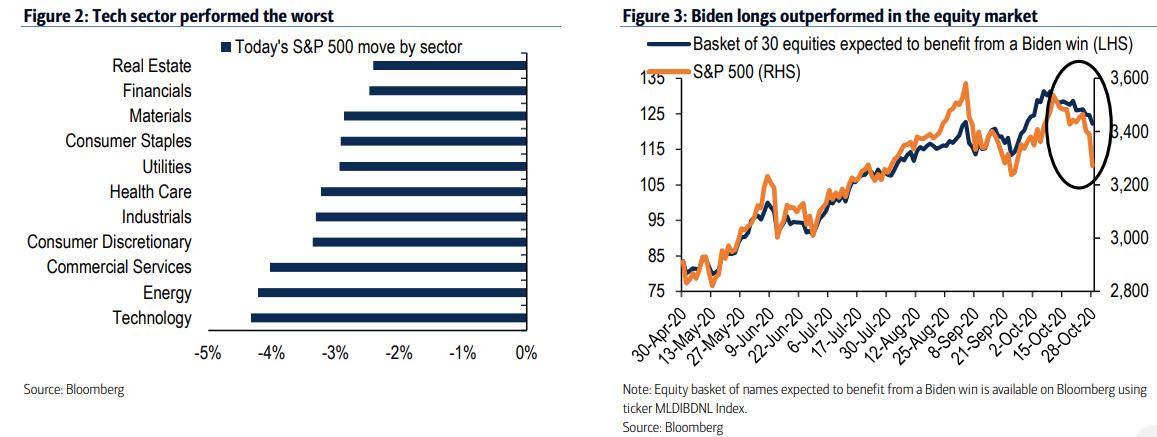

As BofA notes, while Wednesday moves were to some extent in reaction to a deteriorating Covid-19 situation globally and lockdown-type measures being re-imposed in Europe “that can’t be the only story as the Technology sector, which benefits from stay-at-home, performed the worst.” It also can’t be that polls suggesting improving odds for President Trump for next week’s election got investors worried about less fiscal support as Biden longs outperformed in the equity market.

So according to BofA what happened on Wednesday was that investors already positioned for either outcomes for the various near term risks decided to “dial it down a touch in order to reduce risk” and deleverage, a move that hit “balanced portfolio” investors the hardest.

And in the latest ominous development for risk-parity funds, BofA warned that “at these low yields the Treasury market does not offer attractive hedging properties for a risk-off environment” especially since increased Corona risk would lead to more fiscal stimulus and higher supply of Treasuries.

Which brings us to the risk-parity “matrix of doom”, which we have discussed previously and which shows at what drops in both bonds and stocks risk parity portfolios are forced to delever aggressively.

As the chart shows, another -3.5% day coupled with a modestly bigger jump in yields and all hell can break loose.

via ZeroHedge News https://ift.tt/3oFQX7O Tyler Durden

Watch Live: ECB’s Christine Lagarde Explain How She’ll Save The World Again (If Needed) Tyler Durden

Thu, 10/29/2020 – 09:25

ECB President Christine Lagarde and her colleagues are walking a fine line as they likely believe they can get away with holding steady for now; but in the face of resurging COVID and re-lockdowns, she will need to send a strong signal that more stimulus is coming… “whatever it takes.”

“I don’t think the Governing Council is ready” to agree new measures, said Florian Hense, an economist at Berenberg.

“Maybe we’ll hear more clearly that something is coming.”

The statement confirmed the “more to come” narrative:

On the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation and to ensure that financing conditions remain favourable to support the economic recovery and counteract the negative impact of the pandemic on the projected inflation path.

Watch Live (due to start at 0930ET):

via ZeroHedge News https://ift.tt/2HL9DlT Tyler Durden

“In light of his comments made today and his failure to retract them subsequently, the Labour Party has suspended Jeremy Corbyn pending investigation. He has also had the whip removed from the Parliamentary Labour Party.”

More problematic was the fact that the report found Corbyn’s office interfered in the report…

How Jeremy Corbyn’s office interfered in the complaints process “throughout” the period investigated not just March-April 2018 when they were sent all cases and this was “not legitimate” and is “indirectly discriminatory” pic.twitter.com/RrMrGSDl5E

Sky News reports that Corbyn gave a press conference in which he repeated his previous “overstated” comments and insisted “I’m not part of the problem”.

via ZeroHedge News https://ift.tt/3e9QlT2 Tyler Durden

The 2020 campaign is down to its final week, with each party and pundit preparing the ammo they need to either take a victory lap or explain away their defeat. In the age of covid, the Democratic Party has pushed heavily a vote-by-mail campaign that places their successes in the hands of the ability of voters to successfully negotiate the postal system, while Trump’s team is relying on MAGA rallies to motivate in-person early voting. The combination of the two has the race projected to be the largest projected voter turnout in over a century.

According to conventional wisdom, this is a major win for Joe Biden’s team. In fact, strong voter turnout in states like Texas and Georgia has anxious pundits questioning whether this is finally the year these red state stalwarts flip blue. But is conventional wisdom correct?

If we do in fact see a major surge of voter behavior, it’s useful to consider the sort of voter who may be turning out to cast a vote for the first time. Both sides have their own preferred narrative here: Democrats see a nation of politically oppressed groups that can be activated by tapping into their sense of injustice, while Republicans see a “silent majority” that wants, to quote @realDonaldtrump, “LAW AND ORDER!”

Historically, the demonstrated preference of American voters has firmly been political apathy. In 2016, if Did Not Vote had been a candidate, it would have won with an impressive 471 votes. As such, to the extent that the “silent majority” exists, we can perhaps view it as “antipolitical.”

The question, then, is which candidate makes the best appeal to the “antipolitical”?

If you were to listen to the corporate press, the obvious answer would be that President Trump is so uniquely bad that any decent person would be motivated to fire him. Helping this argument is general disapproval of the president’s handling of covid (though specific criticisms are not made clear in the poll), as well as the fact his favorability rating is below 50 percent (though no worse than in 2016). Working against this narrative is the fact that, in spite of what 2020 has brought, 56 percent of voters told Gallup that they are better off now than where they were four years ago.

Considering the amount of money that was spent in 2016 unsuccessfully making the case that Donald Trump was a uniquely unacceptable outcome for American democracy, it’s fair to question whether four years of “Orange Man Bad” is a political message that would electrify new votes.

So what has changed in four years?

Well, one obvious change is social media and the willingness of Big Tech to leverage their platforms for purely partisan purposes. In 2016, Americans were able to find and read and share materials such as leaked campaign emails, or episodes of The Alex Jones Show. American democracy allowed for voters to make their own judgments on these matters.

Now we’re told that American democracy depends on protecting voters from potential “disinformation.” The most obvious example is social media’s treatment of files allegedly found on a lost laptop, which Big Tech has desperately tried to hide from American voters. The New York Post, one of America’s oldest newspapers, remains locked out of their Twitter account for daring to publish the content.

While this episode highlights important questions about the relationship between Big Tech and society, this is simply an example of a larger trend of the progressive left pushing politics beyond elections. While the political agenda of Facebook and Twitter may have a more direct impact on how we use the product than how Gillette targets its advertising or what the next woke flavor of Ben and Jerry’s is, the Left and its corporate allies have made the decision that politics is too important to not be talked about.

But what if normal Americans do not want to be lectured to? Particularly when those lectures come from the people who engage in such performative hypocrisy as celebrating massive protests in the name of “social justice” while scolding you for going to church?

If “bread and circuses” really are all that is needed to keep the masses content, what happens when you pervert pastimes into “soy and political lectures”?

What if there is a large section of the country that did not vote for Trump in 2016, sees plenty of faults with the man and his policies, but sees him and his tweets as far less dangerous than self-righteous lefties who use their social media to get random people fired? If polling trends are accurate, we’ve already seen President Trump greatly enhance his position with minority voters, whose communities tend to be the most hostile to the Left’s fetish for political correctness. In particular, Biden may win 100 percent of the self-identified Latinx demographic, but Trump appears set to perform significantly better with Hispanic voters in both Florida and the Sun Belt.

Perhaps real populism in America is simply letting people raise a family and grill in peace?

If so, maybe Murray Rothbard was right about the potential for a uniquely libertarian brand of populism in America.

One thing is for sure if this theory holds: political pundits in New York and Washington, DC will find themselves looking foolish in 2020. Again.

via ZeroHedge News https://ift.tt/34BcXce Tyler Durden

ECB Holds Rates, QE Unchanged, Risks Still “Tilted To Downside” Tyler Durden

Thu, 10/29/2020 – 08:48

While tougher pandemic restrictions are amplifying the pressure on the ECB to act at a time when it faces its own credibility crisis (unable to raise inflation expectations ‘whatever’ they do), they do have plenty of ammunition left in existing pandemic programs so not much was expected in actual ‘actions’ from Lagarde… but plenty of optimistic jawboning at the press conference we are sure.

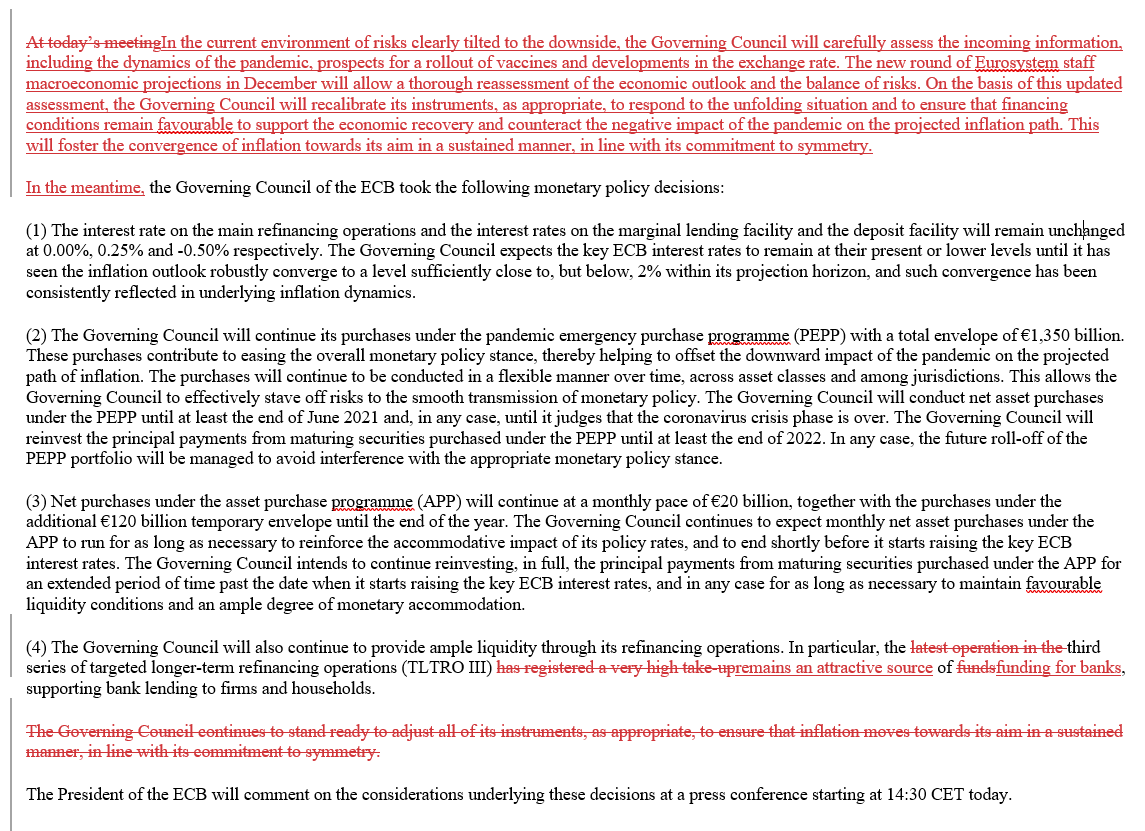

And so, as expected, The ECB held rates and their bond-buying programs unchanged and signaled more to come…

In the current environment of risks clearly tilted to the downside, the Governing Council will carefully assess the incoming information, including the dynamics of the pandemic, prospects for a rollout of vaccines and developments in the exchange rate. The new round of Eurosystem staff macroeconomic projections in December will allow a thorough reassessment of the economic outlook and the balance of risks.

On the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation and to ensure that financing conditions remain favourable to support the economic recovery and counteract the negative impact of the pandemic on the projected inflation path. This will foster the convergence of inflation towards its aim in a sustained manner, in line with its commitment to symmetry.

In the meantime, the Governing Council of the ECB took the following monetary policy decisions:

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

The Governing Council will continue its purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,350 billion. These purchases contribute to easing the overall monetary policy stance, thereby helping to offset the downward impact of the pandemic on the projected path of inflation. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows the Governing Council to effectively stave off risks to the smooth transmission of monetary policy. The Governing Council will conduct net asset purchases under the PEPP until at least the end of June 2021 and, in any case, until it judges that the coronavirus crisis phase is over. The Governing Council will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Net purchases under the asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. The Governing Council continues to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates. The Governing Council intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when it starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

The Governing Council will also continue to provide ample liquidity through its refinancing operations. In particular, the third series of targeted longer-term refinancing operations (TLTRO III) remains an attractive source of funding for banks, supporting bank lending to firms and households.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today.

Notably, that entire narrative-defining first paragraph is new to The ECB’s statement:

Now all eyes are on the presser, where we assume Lagarde promises more “whatever it takes.”

via ZeroHedge News https://ift.tt/2TGGcnr Tyler Durden

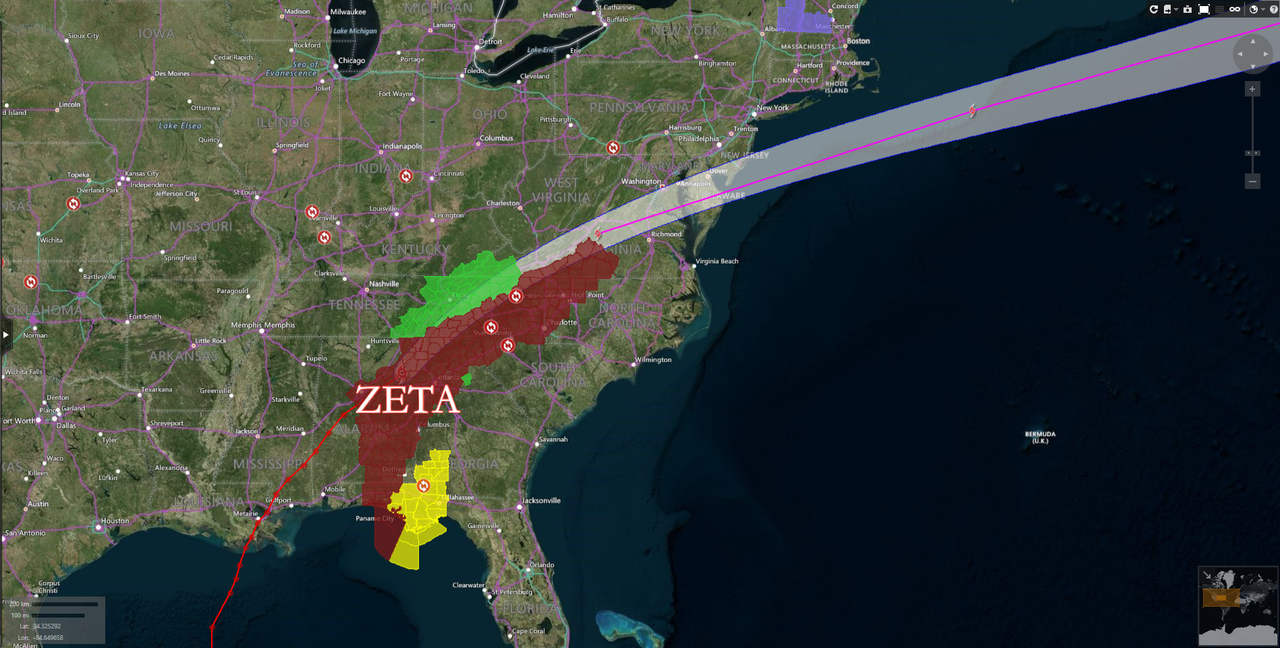

According to power outage.us, by 0553 ET Thursday, more than 1.7 million customers were without power across four states. Georgia 708k, Louisiana 508k, Alabama 273k, and Mississippi 231k.

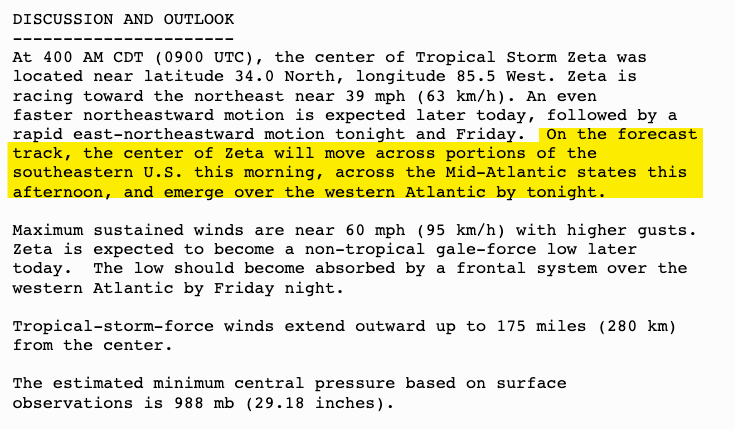

Zeta has picked up momentum, racing through central Alabama and northern Georgia this morning and then the Mid-Atlantic by evening.

“On the forecast track, the center of Zeta will move across portions of the southeastern US this morning, across the mid-Atlantic states this afternoon, and emerge over the western Atlantic by tonight,” the National Hurricane Center said.

CNN Meteorologist Michael Guy said Zeta’s fast track suggests the storm won’t lose much energy as it traverses the Southeast today and Mid-Atlantic by evening.

“This will allow Zeta to keep tropical storm intensity with strong winds throughout its course to the Atlantic,” Guy said.

Zeta is the 11th named storm and 6th hurricane to make landfall in 2020. “Both are seasonal records (the six hurricane landfalls ties with 1985 and 1886). Louisiana is the first state with five named storm landfalls in a season,” said Aon PLC.’s meteorologist and head of catastrophe insight Steve Bowen.

Bowen also said the super active hurricane season has already cost more than $30 billion in damage.

via ZeroHedge News https://ift.tt/3jBqrc5 Tyler Durden

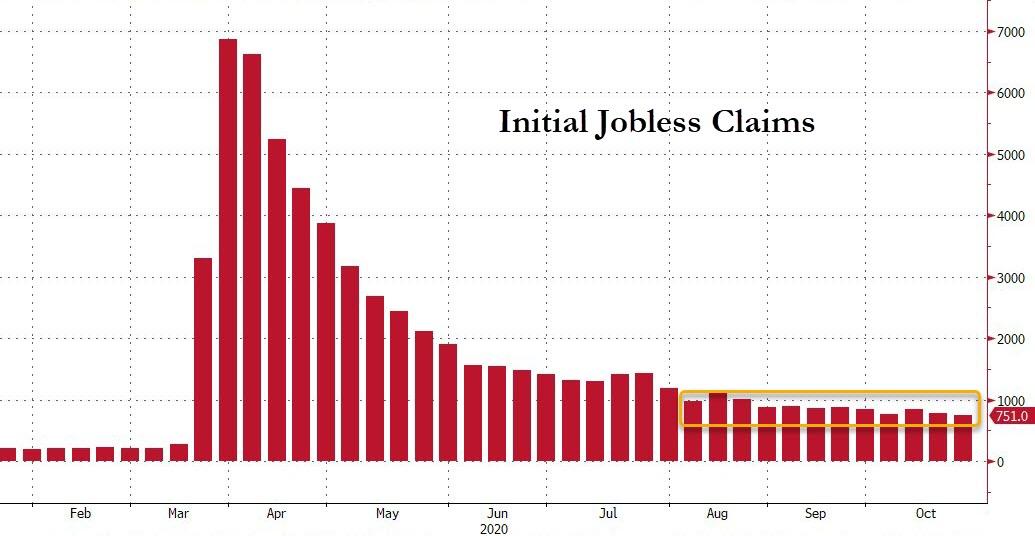

Pandemic Emergency Jobless Claims Soar To Record High Tyler Durden

Thu, 10/29/2020 – 08:39

With California’s fraudulent data issues ‘fixed’, initial jobless claims data is at least a little cleaner and printed a better than expected 751k – that’s the best level since pre-lockdown. Reminder, however, that this is still around 4x the pre-lockdown normal.

Source: Bloomberg

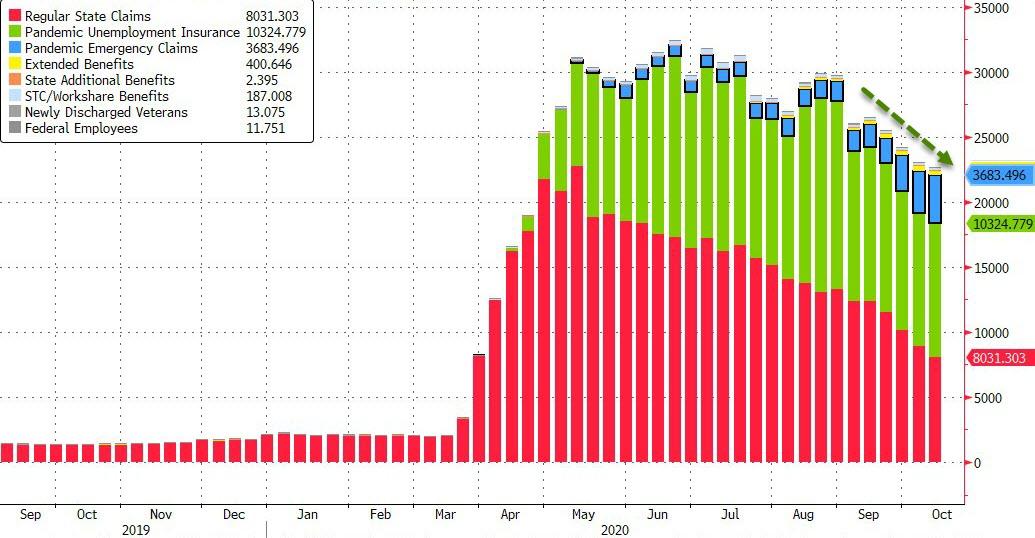

Continuing claims fell back below 8 million, its lowest level since pre-lockdowns…

Source: Bloomberg

Total Claims fell WoW…

Source: Bloomberg

But Pandemic Emergency Jobless Claims surged once again…

Source: Bloomberg

Sadly, as Peter Schiff recently noted, a lot of the people who have gone back to work in recent weeks will eventually find themselves in the unemployment line again.

I think a lot of these people who have been recalled, who have come back to work, I think ultimately their employers are going to realize, after the fact, that they don’t really need a lot of these workers, and a lot of these workers are going to be re-fired. Except next time it is going to be permanent, not temporary.”

Lockdowns and the government/central bank response to the ensuing economic fallout may havepermanently scarred the labor market and there are signs of deep wounds that won’t quickly heal. In a nutshell, a lot of people will likely never return to work.

via ZeroHedge News https://ift.tt/3e8gphJ Tyler Durden

US GDP Soars By A Record 33.1% In Q3, Smashing Expectations Tyler Durden

Thu, 10/29/2020 – 08:36

What goes down, must come up, and one quarter after US GDP collapsed by a record 31.4% annualized, moments ago the BEA reported that in Q3 the US economy rebounded by a similarly record high 33.1%, the biggest annualized increase in history.

And while on a Y/Y basis the rebound was not nearly as impressive, with the US economy still showing a 2.9% decline compared to a year ago following trillions in stimulus…

… one can be certain that Trump will parade with this “blockbuster” number for the next 4 days.

via ZeroHedge News https://ift.tt/2TGEeU5 Tyler Durden

Rabobank: Opinion Polls Are Saying Whatever *You* Want Them To Say, To A Tragicomic Degree Tyler Durden

Thu, 10/29/2020 – 08:26

By Michael Every of Rabobank

Always blindingly obvious

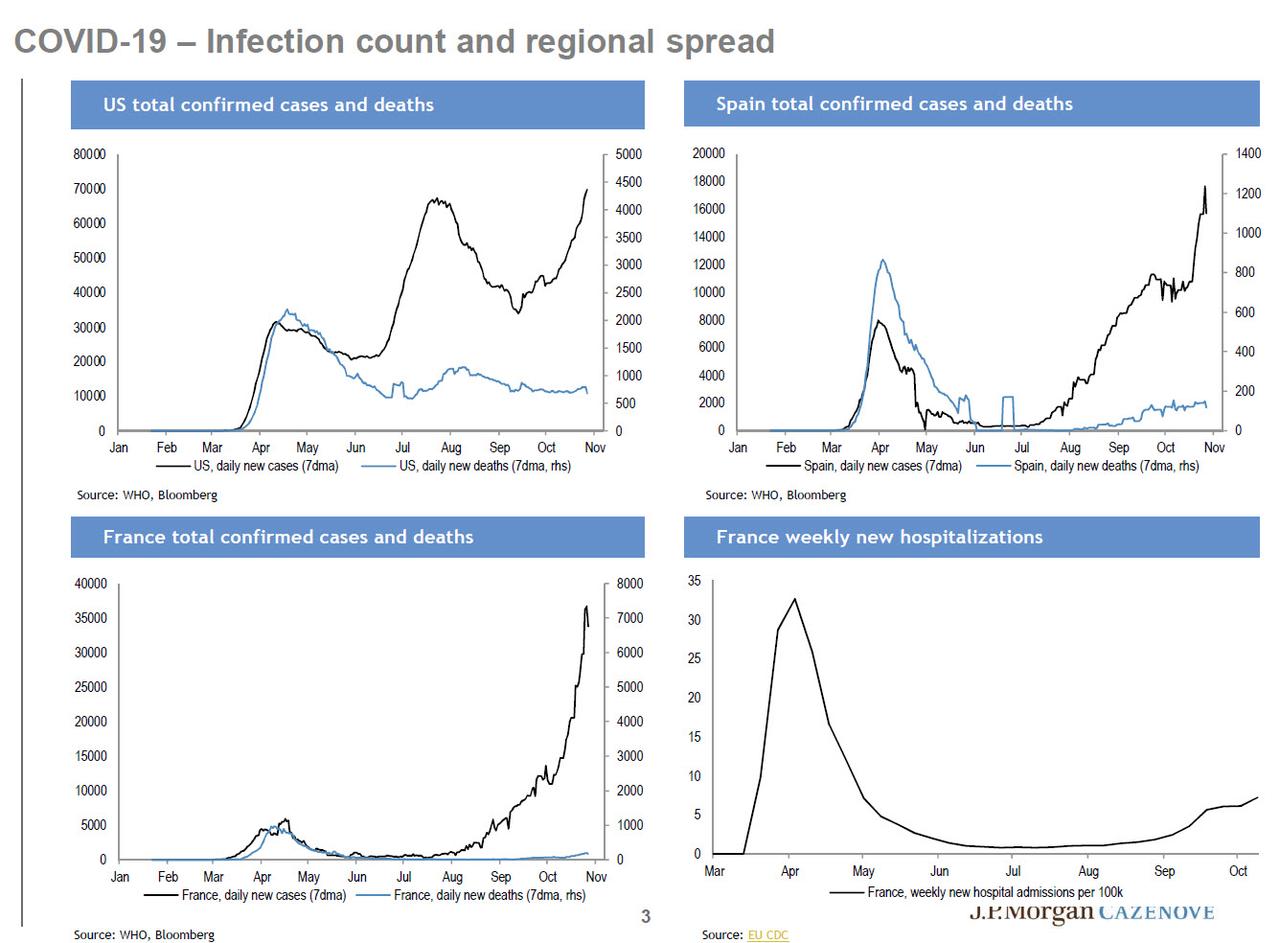

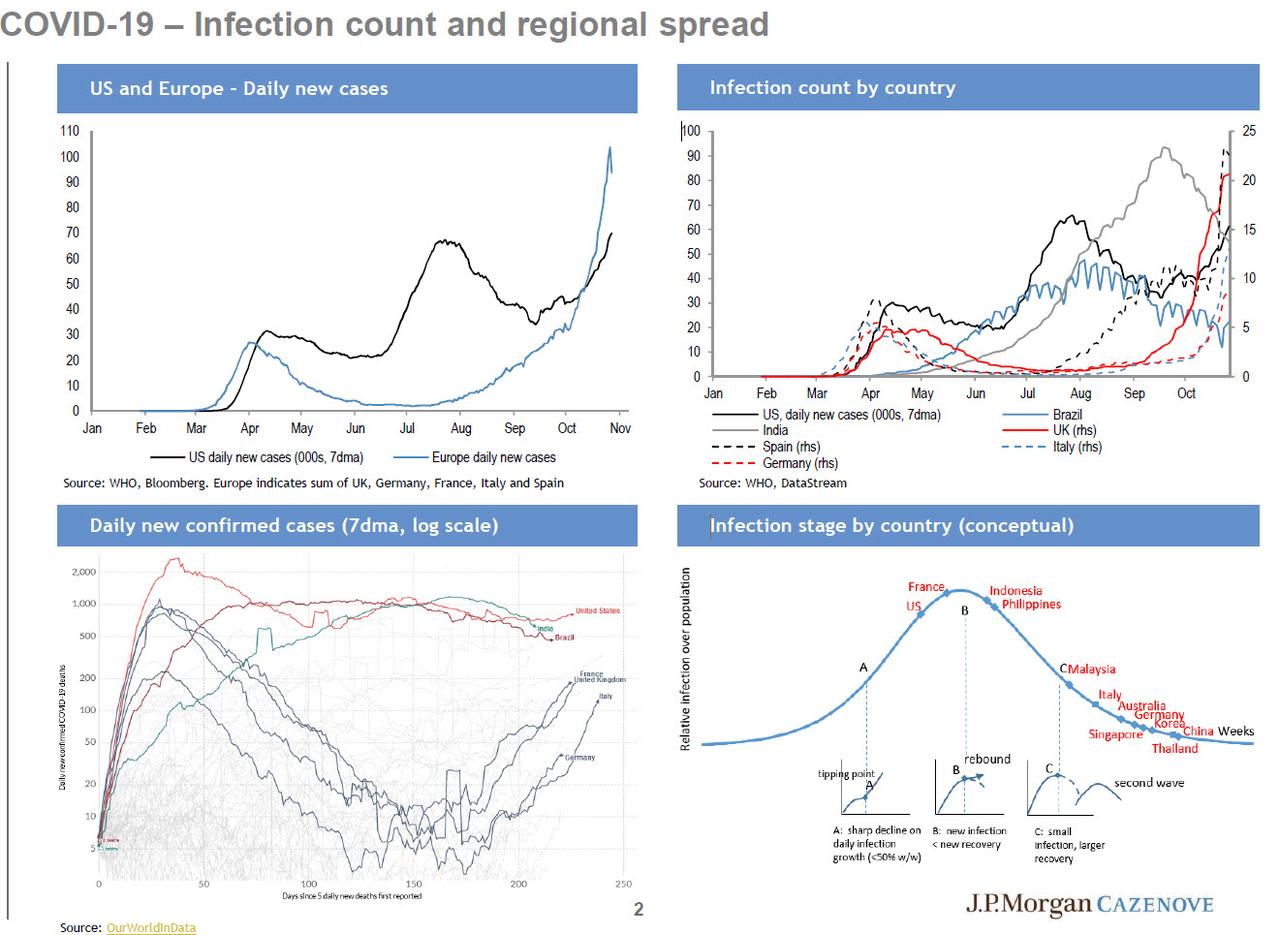

France is partially locked down from tomorrow until 1 December; super-efficient Germany has a limited lockdown for a month too; Italy may follow imminently; and Ireland has had one for a while. In the UK pubs are either open but can’t serve alcohol, or are open if they put a lettuce leaf next to a Cornish pasty on a plate, because that obviously controls the virus completely, or are closed; and the threat is being bandied about that the British police could even come into homes and arrest families over Christmas if more than six people are gathered together for a slice of Xmas pudding. Is it any wonder that the UK’s three virus ‘tiers’ were recently dubbed by its tabloid press as “stuffed”, “nearly stuffed”, and “soon to be stuffed”. Meanwhile, US cases are spiking up again, in the Mid-West this time.

Of course, Covid-19 has been rampaging across swathes of the developing world for months, such as India with its 8m cases. Yet that didn’t seem to matter at all to ebullient markets at all until this week, and yesterday in particular. Suddenly it all does matter, however. I mean, just imagine a European not being able to go to a restaurant on a Wednesday night and having to cook at home! Imagine a skiing holiday being cancelled! Thus risk is now off and sentiment has turned and equities have tumbled.

Should we be surprised? After all, whoever said markets were either rational in the short term or moral? They love to ignore the blindingly obvious until it is literally right in their own faces.

This is in no way to underplay the serious economic hardship and real physical and psychological damage that is being wrought in developed economies by Covid-19, which in many ways is only just getting started: how many small businesses and jobs are going to be able to survive another lockdown? How many are going to be able to cope with a potential future of rolling biannual lockdowns? As this report shows, one in seven adults with kids in the US is already going short of food; and nearly one in four renters with kids is behind on rent payments.

However, the suffering in many emerging markets has been very high for a long time too, and is still rising. Scientists made clear a second wave would arrive with autumn. Markets just weren’t that interested. All that supposed economic muscle in EM still pales in comparison to DM when push comes to actual shove, it seems. As does’ following the science’.

So let’s now follow on to scientifically focusing on the travails of some of the richest countries with the best public health systems in the world: yes, it’s ECB day.

As our ECB team note, the Governing Council meets amidst a resurgence of Covid-19 across Europe. Many Council members have expressed their support for new or prolonged easing as the outlook for the economy and inflation remains weak, but there has still been some pushback on the timing. (Could they not wait until inflation is firmly negative y/y, cynics might ask?)

Last week, the team’s view was that considering calm markets and the stimulus still being provided by previous measures, they did not think that the downside risks warranted immediate ECB intervention, but they openly acknowledged there was a substantial risk of an announcement today. Will Europe back in partial lockdown and markets falling this week have changed a few minds? Or will the majority of the ECB still favour the December meeting as more propitious to take the next step on the ongoing journey of not meeting its inflation target?

In terms of policy expectations, they expect interest rates on hold for the foreseeable future. There are only risks of a cut, which would be effective in weakening EUR. However, they think EUR/USD would still need to be closer to 1.20 before the ECB sees it as restrictively strong and acts in that regard. They still foresee a higher tiering multiplier, but expect the ECB to wait until more of the PEPP has been implemented (or a rate cut does materialise). A rate cut, if seen, may also require a tweak in the TLTRO modalities to limit the potential downside. On the once-unthinkable and now life-is-unthinkable-without-them Asset Purchase Programmes, they expect no changes or PEPP just yet, but still call for an extension of PEPP to end-2021 in December, paired with a EUR ~250bn increase in the envelope.

In short, Europe is seemingly heading for a very difficult winter on multiple fronts: and the ECB is not going to be providing much light or heat, just the usual acronyms. The EU’s fiscal-Rubicon-crossing virus spending measures might even need review, one might imagine, before the ink is dry on the document and a single Euro flows out.

Similar sentiments of course apply to Japan, where retail sales dipped 0.1% m/m in September vs. a projected 1.0% rise and are still -8.7% y/y, but where the BOJ did nothing new at its monthly meeting. Apart from raising its forecast for growth next year to 3.6% to 3.3% y/y.

Meanwhile in US news, the opinion polls are still saying whatever *you* want them to, to a quite tragicomic degree – but somebody is going to be tragically wrong, however, and soon; new Supreme Court rulings mean we could indeed have a post-election delay for late-arriving ballots in a few key states after all – or that mail in votes in Pennsylvania could be discarded after Election Day; Tech CEOs testified to Congress again over the contentious Section 230 issue, which included Mark Zuckerberg having to delay because he couldn’t get a decent Wi-Fi Signal(!), and the Twitter CEO’s view being that if they don’t like his communication channel, all 300m users can always use alternatives to get their political messages out; that as Fox News’ Tucker Carlson claimed on TV that important Biden-related documents sent to him by a courier service simply disappeared – a story which, like so many others recently, it is equally worrying if it is or isn’t true.

And regardless of the election, some things don’t seem to change in the US. The Senate has seen a bill introduced “that would prohibit malign Chinese companies — including the parent, subsidiary, affiliate, or a controlling entity — that are listed on the US Department of Commerce Entity List or the US Department of Defence list of Communist Chinese military companies from accessing US capital markets.” It would prohibit such firms listing and trading on a US securities exchange; the use of federal funds to deal with such entities; all investments by insurance companies in them; all IRAs from investing in them; and remove the tax-exempt status for qualified trusts that invest in them. Notably, there is still no reference to stopping US capital flowing into Chinese bonds or Chinese government bonds, but given that a share of public spending in every country goes into the military that this bill rails against, one wonders how long until that loophole is also closed.

Something else for markets not to worry about, no doubt, until the blindingly obvious –like the fact that this Covid second wave would happen in DM too– suddenly looms ahead ad ski-trips have to be postponed.

via ZeroHedge News https://ift.tt/2HAwz7J Tyler Durden