NYPD Braces For Protests ‘Growing In Size, Frequency And Intensity’ Surrounding ‘Most Highly Contested Election In Modern Era’ Tyler Durden

Tue, 10/13/2020 – 17:20

The New York Police Department is preparing for widespread protests “growing in size, frequency, and intensity” over the presidential election and the confirmation hearings of Supreme Court nominee Amy Coney Barrett, according to a memo obtained by the New York Post.

In it, Police Commissioner Dermot Shea warns “this November 3rd will be the one of the most highly contested presidential elections in the modem era,” adding that there is a “strong likelihood” that the winner won’t be declared for several weeks.

All uniformed officers of every rank will be expected to “perform duty in the uniform of the day and be prepared for deployment” beginning October 25 – whole officers who don’t typically wear uniforms, such as detectives, are being told to have their uniform and equipment on hand.

In fact, Americans around the country are similarly anticipating unrest surrounding the election, according to Reuters.

Some people are planning foreign vacations around Election Day or heading to rural retreats. Others have bought guns for defense. Firearm sales hit a monthly record of 3.9 million in June, according to FBI data. Ammunition for AR-15-style rifles is on back order in states like Washington and Colorado.

“I bought an AK-47,” said a Denver-based lawyer who identified himself as Ewing, and asked that his full name not be used. “The ammo is inexpensive and I can still get it.” –Reuters (via Yahoo!)

Another factor in New York City not mentioned in Shea’s letter is the growing unrest among Hasidic Jews protesting coronavirus restrictions in the streets by the hundreds despite Governor Andrew Cuomo’s edict that houses of worship located in so-called ‘red zones’ where COVID-19 is spreading most rapidly are limited to 25% capacity, or a maximum of 10 people. In the city’s “orange zones,” it’s limited to 33 percent capacity, while “yellow zones” are at 50 percent.

Hundreds of demonstrators took to the streets in Brooklyn’s Borough Park neighborhood, where themostly Orthodox male gathering burned masks in the street.

NEW YORK: Orthodox Jews burn a pile of masks in protest against the continued lockdowns in the city

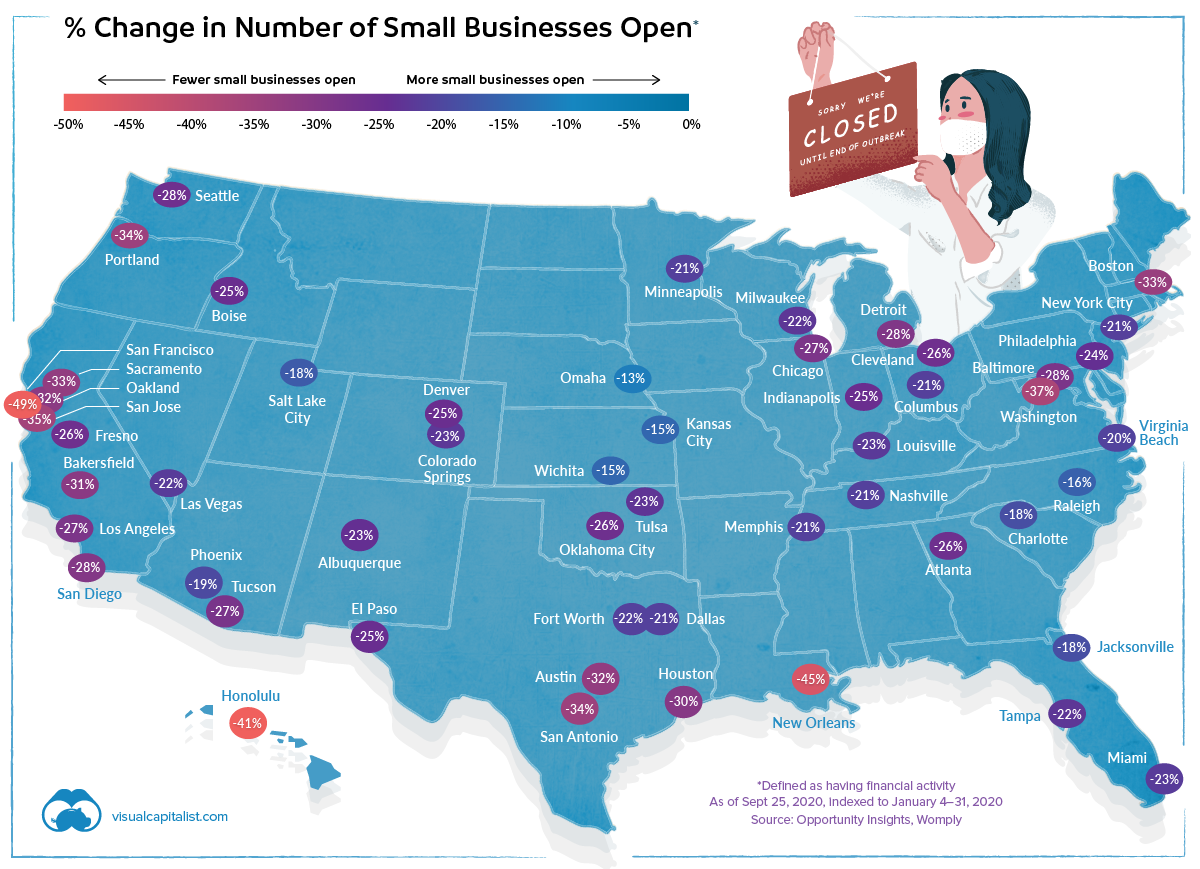

Mapping The Uneven Recovery Of US Small Businesses Tyler Durden

Tue, 10/13/2020 – 16:40

Small businesses are the backbone of the U.S. economy, employing nearly half of the private sector workforce.

Unfortunately, as Visual Capitalist’s Nick Routley details below, lockdown and work-from-home measures brought about by COVID-19 have disproportionately affected small businesses – particularly in the leisure and hospitality sectors.

As metro-level data from Opportunity Insights points out, geography makes a great deal of difference in the proportion of U.S. small businesses that have flipped their open sign. While some cities are mostly back to business as usual, others are in a situation where the majority of small businesses are still shuttered.

The Big Picture

In the U.S. as a whole, data suggests that nearly a quarter of all small businesses remain closed. Of course, the situation on the ground differs from place to place. Here’s how cities around the country are doing, sorted by percentage of small businesses closed as of September 2020:

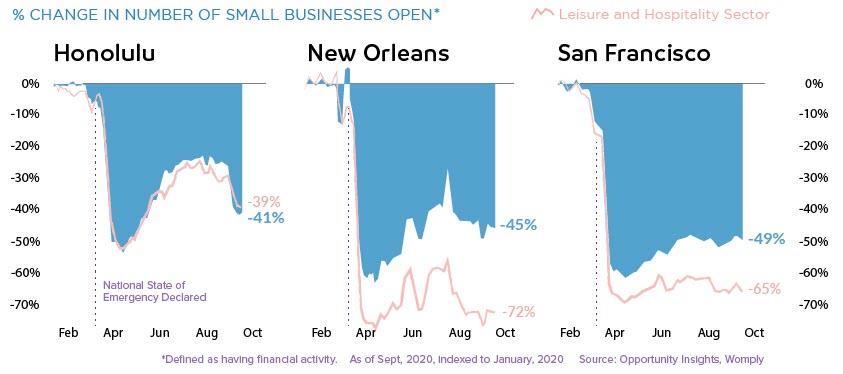

New Orleans and the Bay Area are still experiencing rates of small business closures that are almost double the national median.

Small businesses in the leisure and hospitality sector have been particularly hard hit, with 37% reporting no transaction data.

Getting Back to Business

Some cities are seeing rates of small business operation that are nearing pre-pandemic levels.

Of the cities covered in the data set, Omaha had the highest rate of small businesses open.

Still Shuttered

In cities with a large technology sector, such as San Francisco and Austin, COVID-19 is shaking up the economic patterns as entire companies switched to remote working almost overnight. This is bad news for the constellation of restaurants and services that cater to those workers.

Likewise, cities that have an economy built around serving visitors – Honolulu and New Orleans, for example – have seen a very high rate of small business closures as vacations and conferences have been paused indefinitely.

As the pandemic drags on, many of these temporary closures are looking to be permanent. Yelp recently reported that of the restaurants marked as closed on their platform, 61% are shut down permanently. As well, businesses in the retail and nightlife categories also saw more than half of closures become permanent.

In Remembrance of Revenue

A business being completely closed is a definitive measure, but it doesn’t tell the whole story. Even for businesses that remained open, revenue is often far below pre-pandemic rates.

Once again, businesses in the leisure and hospitality sector have been hit the hardest, with revenue falling by almost half since the beginning of 2020.

At present, it’s hard to predict when, or even if, economic activity will completely recover. Though travel and some level of in-office work will eventually ramp back up, the small business landscape will continue to face major upheaval in the meantime.

via ZeroHedge News https://ift.tt/359KCJd Tyler Durden

In the hyper-real casino, everyone has access to the terrors of losing, but only a few know the joys of the rigged games that guarantee a few big winners by design.

Readers once routinely chastised me for over-using simulacrum to describe our economy and society. The problem is this word perfectly describes the hollowed-out, rigged economy and social order we inhabit and so synonyms don’t quite cut it: it’s not the same as simulation or imitation or counterfeit.

My use (or over-use) dates back to the 2009 publication of my book Survival+, which included a chapter titled Simulacrum and the Politics of Experience. I use simulacrum to describe a carefully constructed representation of a once-authentic system that is intended to shape our behavior to suit the interests of those constructing the simulacrum.

The simulacrum has the look and feel of the once-authentic system but it’s rigged to benefit the few whose interests are better served by the simulacrum than they could ever be served by an authentic system.

As I wrote in Survival+: A simulacrum is used to distort a reality that, once revealed, would cause the target audience to act in ways that would not serve the interests of those deploying the simulacrum.

The point of a simulacrum is to mimic an authentic system realistically enough so nobody notices it’s rigged to benefit the few at the expense of the many. This is different from a simulation–for example, a flight simulator–that models the actual experience.

It’s also not a faux copy or counterfeit of the authentic system; it is a replacement that’s real in every way.

French Postmodernist Jean Baudrillard’s 1981 book Simulacra and Simulation attempts to differentiate Simulacra and Simulation by noting that a simulacrum is not a copy of an original (i.e. a counterfeit) because the original is no longer accessible. As a result, the simulacrum becomes not just real but hyper-real.

For an example, consider capitalism which in its classical form is the risking of capital to generate financial and social gains that were not possible in a pre-capital economy.

The labor and materials needed to construct a major canal, for example, were beyond the reach of villages or even towns, and so their economies remained localized and poor due to the inability to reach distant, more lucrative markets.

Once capital could be assembled in sufficient size, the localized, fragmented economies were unified by the canal, and commerce expanded exponentially as a result, benefiting everyone with access to the canal: laborers, farmers, craftspeople, traders and those who risked the money to construct the canal.

Contrast this authentic form of capitalism with the monopoly-finance-state version we inhabit, a simulacrum of authentic capitalism that retains enough superficial similarities to the original that the vast majority of participants don’t even realize that their experience of this simulacrum is entirely different from an experience of authentic capitalism.

Rather than draw benefits from this hyper-real monopoly-finance-state version, the vast majority of participants are exploited, as the value of their labor and capital is extracted by the simulacrum version of “capitalism” which divvies up the extracted value between the monopolies / cartels who control most of the valuable economic activity, the financial sector that parasitically feeds on the real economy and the state, which extracts wealth to feed its vast network of dependents, enforcers and minders of the entire system.

In this hyper-real simulacrum, a vast fortune is never more than a couple of stock gambles, TikTok clips or YouTube videos away. Or for those wary of the casino, the enormous mortgage taken on for life promises access to the riches of the Everything Bubble.

In the hyper-real casino, everyone has access to the terrors of losing, but only a few know the joys of the rigged games that guarantee a few big winners by design and a fortunate few who stumbled into the game at a propitious moment.

As Baudrillard anticipated, the authentic original version of capitalism is no longer accessible. The simulacrum that we call capitalism is rigged, and the mechanisms are so cleverly obscured that the vast majority of participants willingly allow themselves to be exploited, disempowered or marginalized because they have no experience or even reference point to the authentic original version, as it no longer exists.

Everything they know and experience–the economic models, symbols, signifiers, narratives, adverts, etc., and their own conceptions of value and agency, have all been so thoroughly debauched that they have no idea that the authentic original has been lost.

The problem is our system only survives by cannibalizing its weakest parts, and once they’ve been consumed, the system can no longer sustain itself and it expires.

Simulacra are not fake, but they are profoundly unstable and prone to collapse. Everything gluing the monopoly-finance-state system together is unraveling due to the excesses of extraction and exploitation the system has perfected.

Banks Bust, Bullion Battered, But Big-Tech Bid (Again) Tyler Durden

Tue, 10/13/2020 – 16:02

Another day, another Nasdaq-Whale-driven gamma-squeeze in Nasdaq as the rest of the market deteriorated, giving back a lot (if not all) of yesterday’s gains (Small Caps red from Friday)…

Nasdaq faces record delta and surging gamma into this Friday’s Op-Ex…

Source: Nomura

And if you don’t know what gamma is – probably better not to play at this point in the farce…

Nasdaq outperformed Small Caps once again, but also gave back a lot of the early day outperformance…

The S&P 500 was unable to take out its recent highs…

Source: Bloomberg

Despite claims by the great and the good that earnings were awesome (thanks to cuts in provisions, despite no optimism on the economy?), bank stocks were battered today…

Source: Bloomberg

With Citi hit hardest…

Source: Bloomberg

AAPL tumbled during its iPhone launch as China killed the livestream…

VIX did not rise with the underlying market today, suggesting the (call-buying) whale is starting to leave the market…

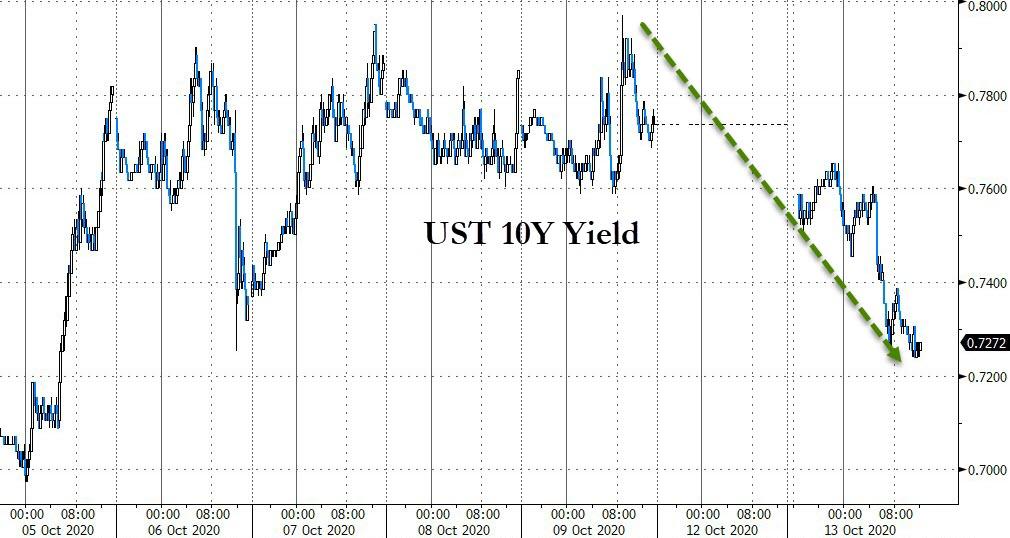

Having been closed yesterday, bond yield tumbled today…

Source: Bloomberg

With 10Y back down to 72bps…

Source: Bloomberg

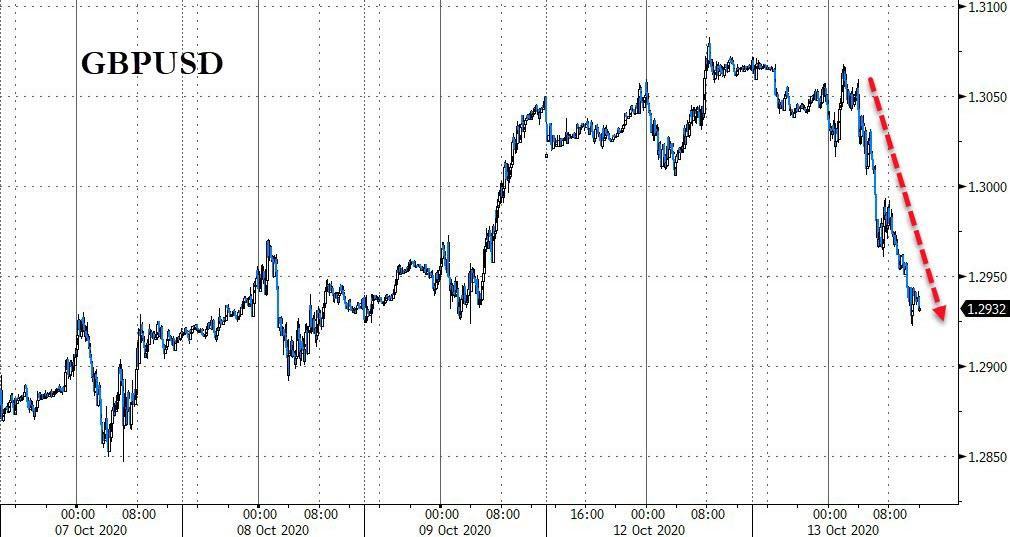

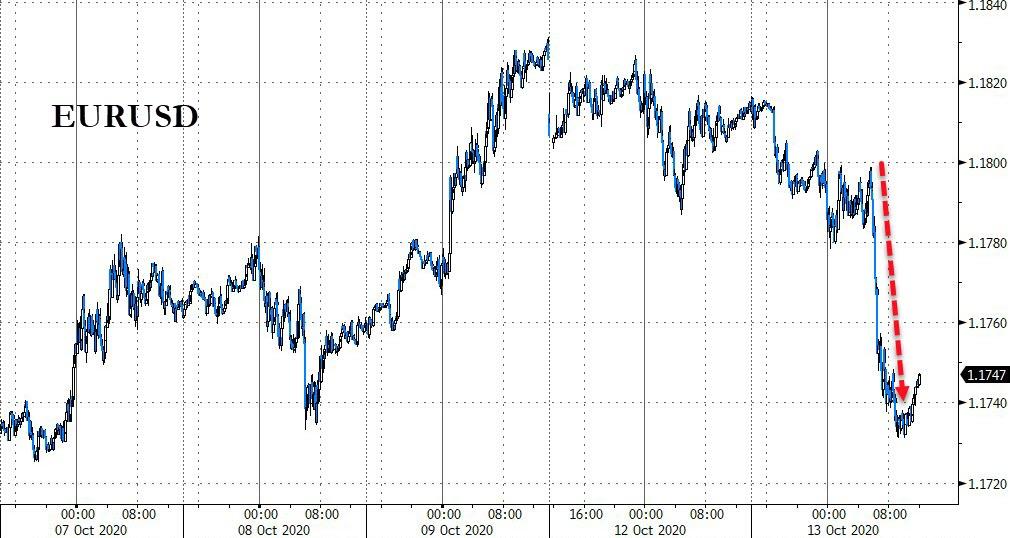

EUR and GBP dropped as Brexit talks breakdown…

Source: Bloomberg

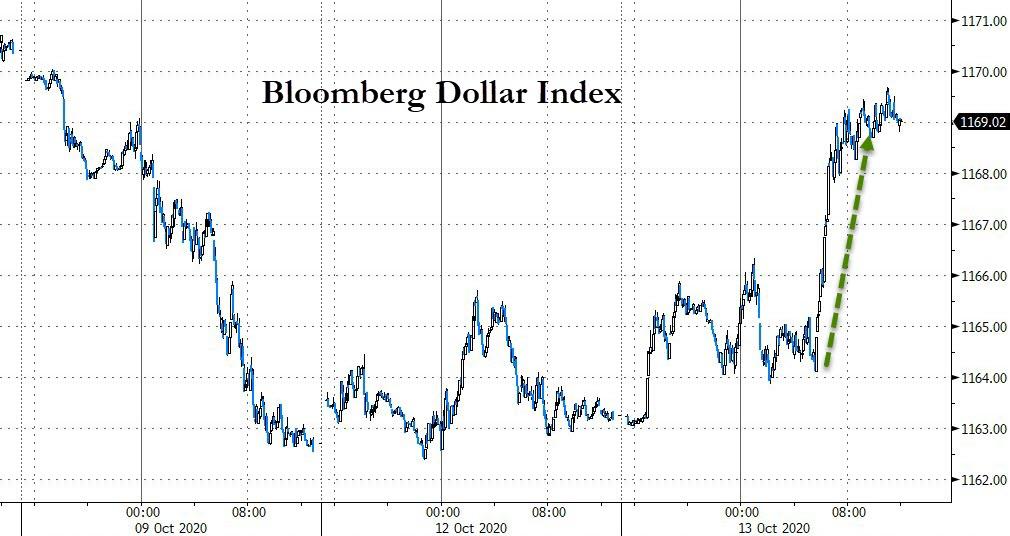

Sending the dollar spiking higher…

Source: Bloomberg

Cryptos slipped lower as the USD rallied…

Source: Bloomberg

The dollar spike sparked a plunge in precious metals.

Gold futs tumbled back below $1900…

Silver tanked below $25…

Oil price rebounded modestly today with WTI back above $40 ahead of tonight’s API inventory data…

Finally, in case you were wondering what – aside from Softbank’s Whale call-buying malarkey – is driving this meltup… it’s “hope”…

Source: Bloomberg

…and everyone knows “hope is not a strategy!”

via ZeroHedge News https://ift.tt/370RcnA Tyler Durden

“Unconstitutional”: Michigan Supreme Court Denies Gov. Whitmer Request For Extension Of Pandemic Executive Powers Tyler Durden

Tue, 10/13/2020 – 15:45

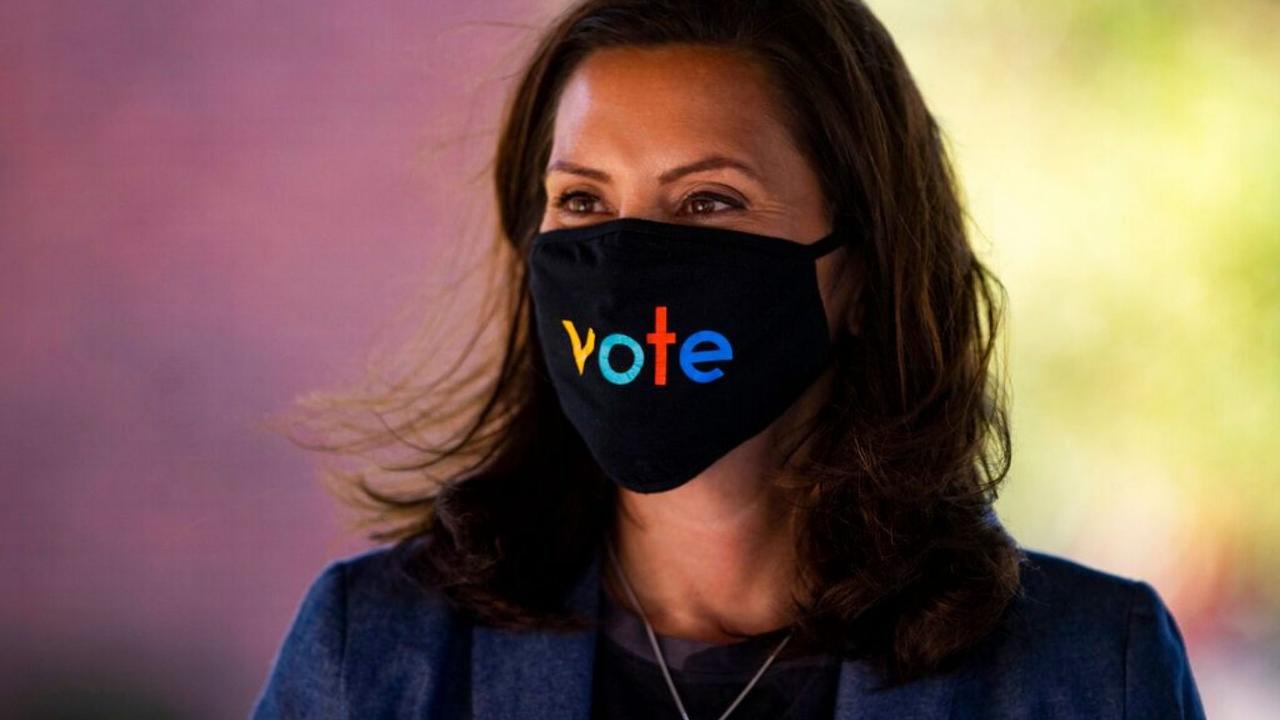

Fresh from her “ordeal” of almost being kidnapped by a couple of white supremacists leftist, BLM-supporting militia nuts, overnight there was more bad news for Michigan Gov. Gretchen Whitmer when on Monday a conservative majority in the Michigan Supreme Court denied her request to extend the emergency powers which she invoked to curb the spread of the coronavirus, declaring it unconstitutional.

Michigan Gov. Gretchen Whitmer wears a mask with the word “vote”.

The justices reversed a lower court’s opinion that supported the governor’s use of executive powers amid the pandemic when they voted 6-1 against halting the precedential effect of its Oct. 2 opinion until Oct. 30. They reaffirmed their initial 4-3 ruling that declared unconstitutional her use of the 1945 emergency powers law.

Michigan Supreme Court justices are elected on the nonpartisan portion of the Michigan ballot, but they are nominated at state political party conventions. The four Republican-nominated justices — Stephen Markman, Brian Zahra, David Viviano and Elizabeth Clement — all ruled that the Emergency Powers of Governor Act that the governor relied on in issuing her orders is unconstitutional. The three Democratic-nominated justices — McCormack, Bernstein, and Cavanagh — all said that both the law and Whitmer’s orders under the 1945 law should be ruled valid.

In striking down her attempt to continue usurping power, the court wrote that executive orders issued under the law “are of no continuing legal effect. This order is effective upon entry.”

But new emergency orders that the Whitmer administration has issued through the state health department director — which replicate mask requirements, restrictions on gathering sizes and restaurant capacity, among other features — are not affected by the court’s ruling.

Monday’s Supreme Court ruling is in response to a lawsuit brought by the Michigan Legislature. The Oct. 2 ruling, which was a 4-3 decision striking down the Emergency Powers of Governor Act of 1945, was in response to questions sent to the court by a federal judge handling a lawsuit brought by medical service providers in western Michigan.

Whitmer had asked the justices to give her administration, lawmakers and local health departments 28 days to transition in the wake of the major decision. Last week, her administration quickly reinstituted mask requirements, gathering limits and other restrictions with orders issued by the state health department under a different law.

Separately, Fox News reported that legislators and Whitmer are negotiating legislation related to other orders negated by the decision, including an extension of unemployment benefits to 26 weeks from 20 weeks.

The ruling caused some confusion because it reached the Supreme Court in an unconventional way. A federal judge overseeing a lawsuit that makes state and federal claims about Whitmer’s powers asked for an opinion on the constitutionality of two laws related to gubernatorial emergency powers. The Supreme Court ruled in a similar case brought by the GOP-controlled House and Senate and said in an order that the decision is effective immediately.

via ZeroHedge News https://ift.tt/34TjVs3 Tyler Durden

Wall Street October Survey: Most Expect A Contested Election, February Vaccine And W-Shaped Recovery Tyler Durden

Tue, 10/13/2020 – 15:30

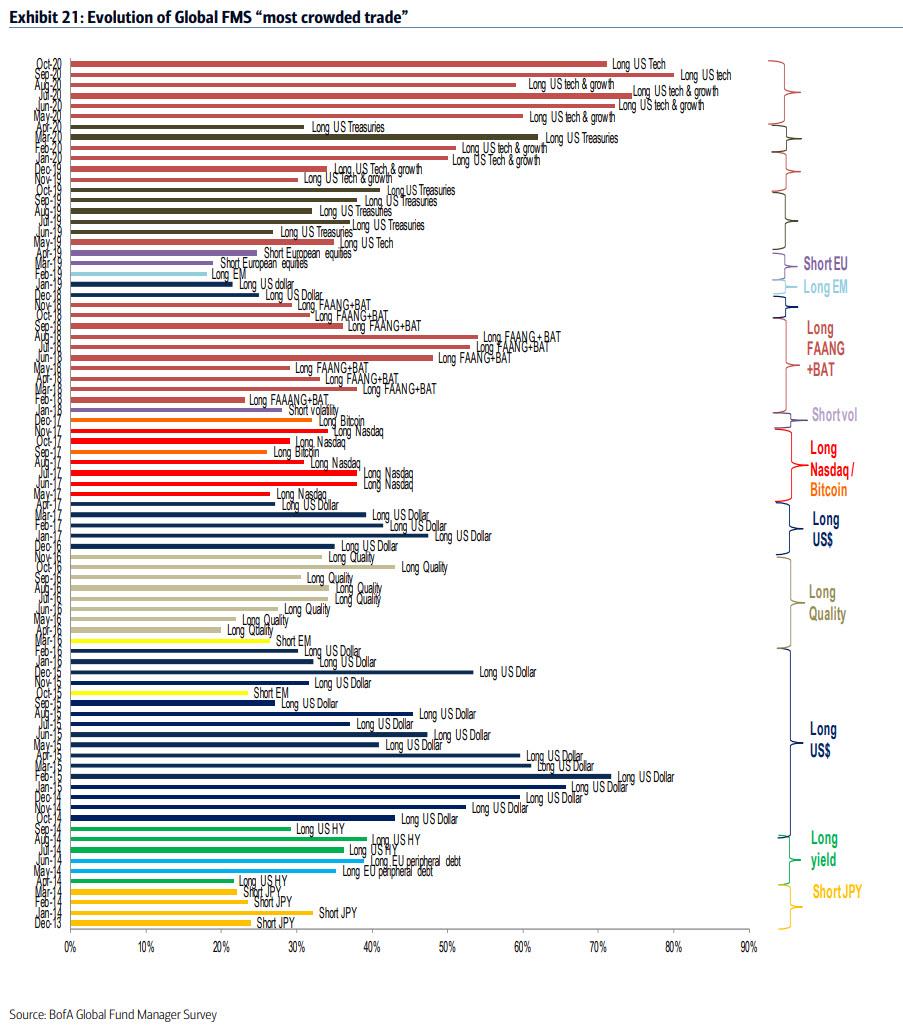

Today Bank of America released its latest Fund Mangers Report, which is perhaps best known for capturing the sheer schizophrenia gripping Wall Street professionals (case in point, last month a record majority of respondents said “Long US Tech” was the most crowded trade on Wall Street, even as most professionals admitted to flooding into Long US Tech trades).

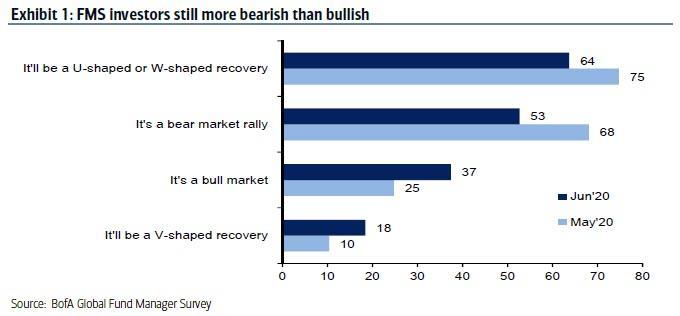

So what is the take home message from the latest survey of 224 pangelists managing some $624 billion in AUM? First and foremost, last month’s consensus that the current recovery is U-shaped (a view held by 32% of respondents in September) giving way to a majority view that the recovery will be a bumpy, double-dip, or W-shaped, held by 30% of respondents while the U-shaped crowd drops to 29%. Meanwhile the V-shaped optimists are far back in 3rd place with just 19% of the responses.

Alas, this question has now become a running joke where the answers are entirely dependent only on the market’s last up or downtick: as a reminder back in May it was nearly consensus that the Fed-inspired ramp in stocks was a bull market rally, while the U and W-shaped crowd was lumped into one category.

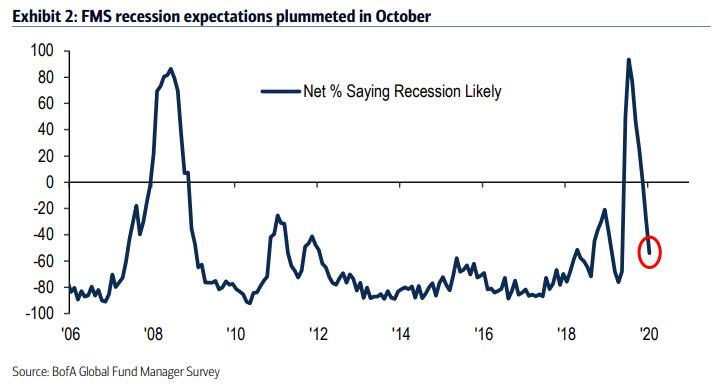

Even poll organizer Michael Hartnett hoped to gloss over these responses, and instead pointed out that the big change in the Oct FMS was a collapse in recession expectations, as the net % of investors expecting recession in the next 12 months plummeted to -54% from -28% in Sept. And to think that this respond hit an all time high back in March and April, shows just how much sentiment is influenced not by fundamentals but by the S&P500, something the Fed knows very well.

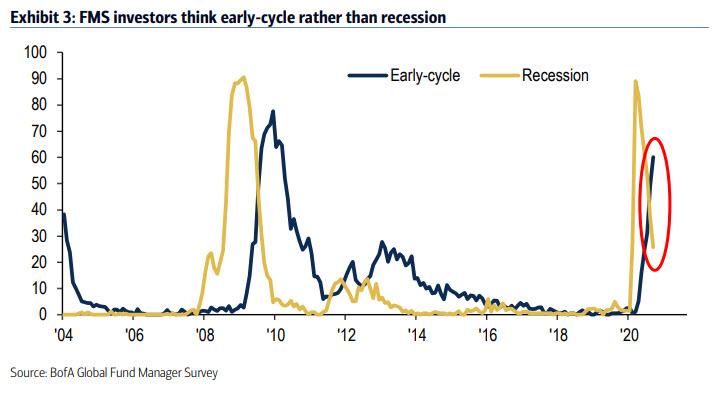

While we expect a prompt and violent reversal in this series as soon as stocks swoon lower, it was amusing to note just how eager Wall Street is to delude itself that all is well with the next question, in which we find that many more investors said the global economy is in an early-cycle phase (60%) as opposed to recession (26%). Just 4 months ago, the vast consensus was just the opposite: recession, with nobody even dreaming of “early-cycle.”

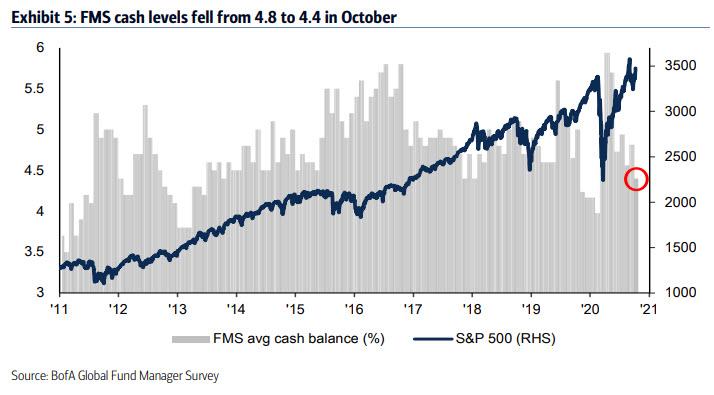

The survey next shifts to cash use, with Hartnett reporting that FMS cash levels fell to 4.4% from 4.8%; As a reminder, according to the BofA model, cash <4% = greed, >5% = fear. As a result, cash levels have collapsed 1.5% in past 6 months, the fastest drop since 2003 as everyone was forced to chase markets thanks to the Fed.

Curiously, there has once again been a divergence between retail and institutional sentiment, with retail funds (i.e. mutual funds) reducing elevated cash levels this month to 4.3% while institutional funds (i.e. pension, insurance) reduced cash levels to 3.6%.

As they turned even more bullish, FMS investors naturally increased their equity overweight to net 27% (from 18%); the net % saying equities markets are overvalued fell to 28% (from 41%) following the September pullback in stock prices. Notably, the October equity overweight of net 27% shows investors are optimistic on stocks but not “dangerously optimistic”, because according to BofA, a net equity overweight of >50% is dangerously optimistic.

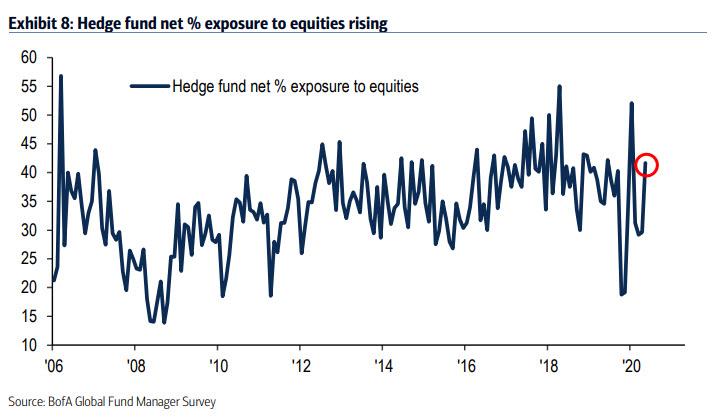

At the same time, Hedge funds appears to be on the verge of “dangerous optimism” as they increased their net equity exposure to 42% (from 30%), the highest level since Jun’20.

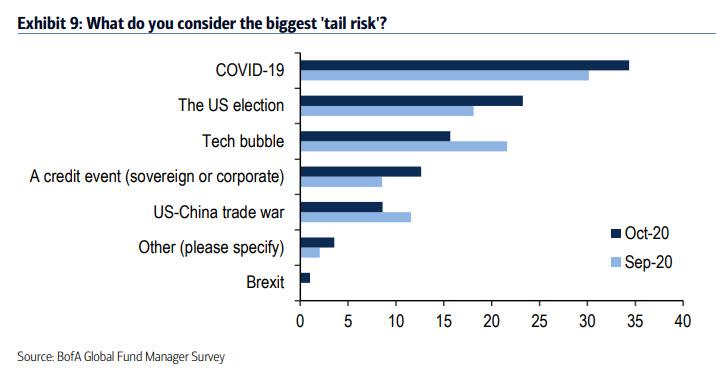

Shifting topics, when discussing COVID-19, the respondents still view pandemic as the #1 “tail risk”…

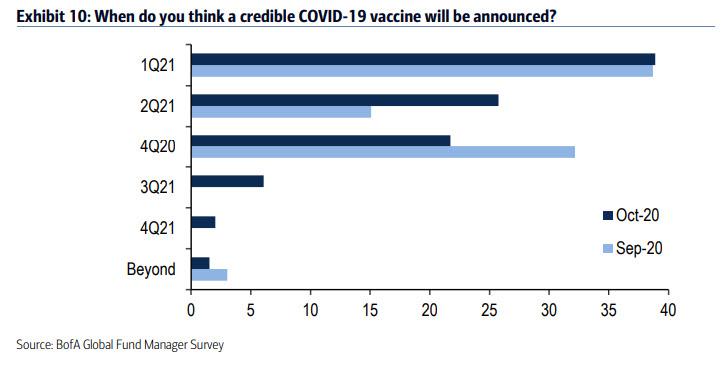

… while the timing of credible vaccine pushed back from Jan’21 to Feb’21.

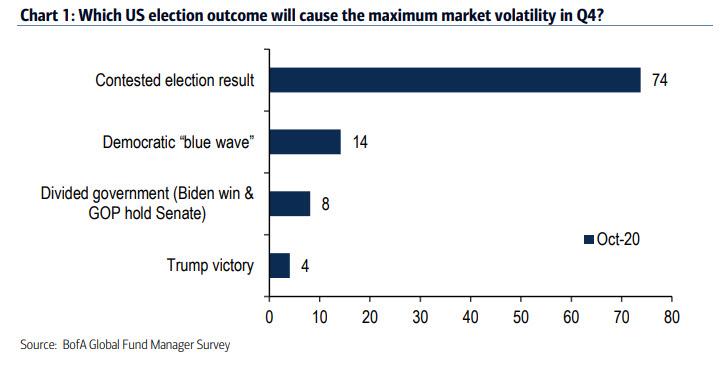

Meanwhile, the US election is viewed as the 2nd largest tail risk, and when asked what outcome causes volatility 74% say “contested election”, 14% “blue wave”, 8% divided Congress, 4% say Trump victory.

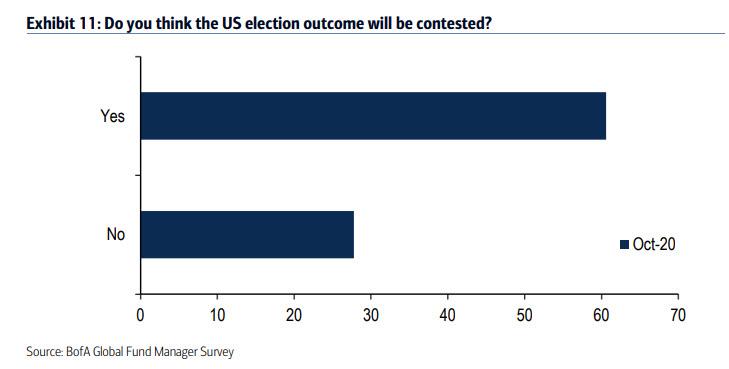

Oddly, even though most investors are bullish, with the US election now just 4 weeks away; 61% of FMS investors believe the US election result will be contested.

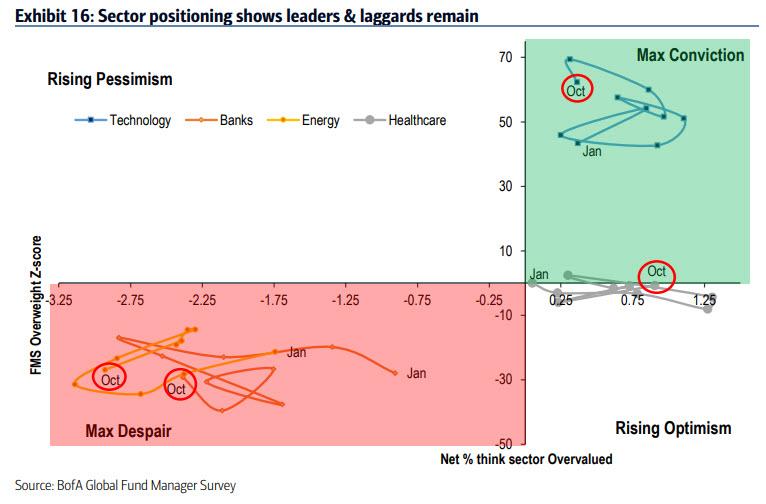

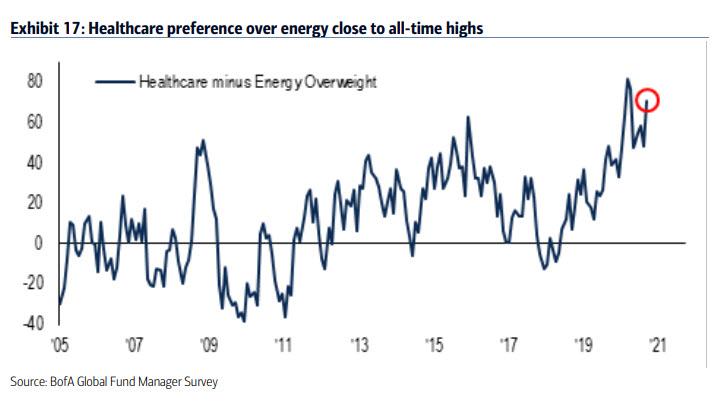

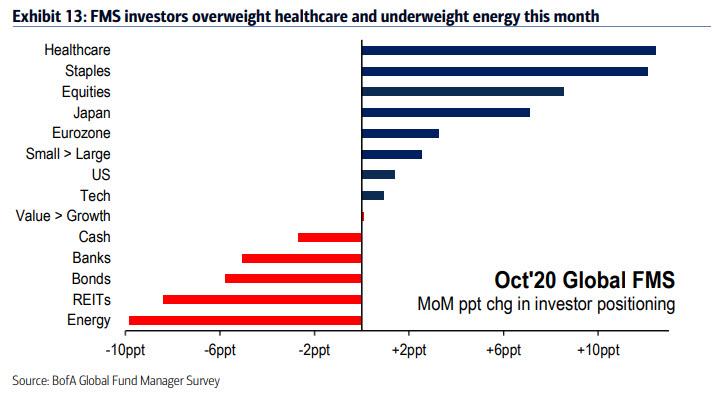

Finally, when looking at positioning, BofA finds the 5th largest short in energy in 20 years; while healthcare overweight surges to #1…

… as FMS investor preference for healthcare over energy is close to all-time highs (high was Apr’20). The spread was net +41% overweight for healthcare and -30% underweight for energy.

… even as long tech is still deemed #1 “crowded trade” by big margin;

Separately, the “cyclical rotation” paused in Oct due to a “sellers strike” in tech, “buyers strike” in energy & banks. As shown below, there was a big increase in exposure to healthcare, staples, stocks & Japan; at the same time, a big reduction in expsoure to energy, REITs, bonds, banks.

Oct FMS contrarian trades: long UK, energy, bank stocks, short US, healthcare, tech, and consumer discretionary stocks.

In other words, one of these days, Exxon may even go up, although if it is red on the day Goldman upgraded it, we wouldn’t get our hopes up too high.

Hartnett’s bottom line: “respondents in our October Fund Manager Survey (FMS) said the recession is over, reduce cash, pause cyclical rotation, and price in contested election & February vaccine; we say sell SPX >3600 and cyclical rotation via banks/energy to resume in Q4.”

via ZeroHedge News https://ift.tt/3dnMVff Tyler Durden

NYC Vacuum Trains Called “Time Bombs” At Risk Of Sparking “Catastrophic Subway Fires” Tyler Durden

Tue, 10/13/2020 – 15:15

Trains that have been designed to literally vacuum New York’s 665 miles of subway tracks could actually be doing more harm than good. We know, you’re surprised that the MTA could be doing anything that winds up being counter-intuitive, right?

Even better, they are (of course), doing it with taxpayer money, according to The Daily News.

The “VakTraks”, as the trains are called, were bought using $23 million worth of taxpayer money in 2017 as part of Governor Cuomo’s “Subway Action Plan”. And what did this $23 million buy the city? Trains that the MTA are literally referring to as “time bombs” due to safety and reliability concerns.

One MTA worker noted that its only a matter of time before they spark a catastrophic subway fire. The French built trains have filters that can easily handle European subway tracks, but that can be “overwhelmed by New York’s filth” sometimes.

When filters tear, the trains can spew out clouds of dust and dirt that, when combined with diesel engines, can “make the air so bad it burns your eyes,” according to one MTA worker.

Another worker said: “These filters are humongous, made out of a Gore-Tex-like material, and after a year they were already ripping and failing.”

And the failsafes on the trains for fires – 12 vent doors that are supposed to shut in the case of fire – “do not fit into their designed slots”, crews said. Crews at Coney Island have been complaining about the potential for catastrophe for “months”.

One MTA worker said: “You ever see a semi truck down the road engulfed in flames? That’s what it’d be like if one of these caught fire.”

MTA spokesman Ken Lovett pointed to the fact that track fires are down 44% between 2017 and 2019 and that the arrival of the VakTraks allowed the MTA to cut 30 jobs and save $3 million annually. “Any claims that the vacuum trains are not working effectively are categorically false,” he said.

Mike Carube, president of the Subway Surface Supervisors Association, called it a “cover up” by the MTA. And some Coney Island workers said they were even disciplined for speaking out. One supervisor said:

“I try to explain to my manager that my job is to put out safe equipment into the public. He said, ‘Don’t worry about it, we know about all the issues, our main prerogative is to keep the trains rolling.’ They want to show the trains are out there even if they’re unsafe because it’s the governor’s pet project.”

via ZeroHedge News https://ift.tt/36YENRj Tyler Durden

House Financial Services Chair Maxine Waters and Senator Elizabeth Warren have introduced the Federal Reserve Racial and Economic Equity Act. This legislation directs the Federal Reserve to eliminate racial disparities in income, employment, wealth, and access to credit.

“Eliminating racial disparities in access to credit” is code for forcing banks and other financial institutions to approve loans based on the applicants’ race, instead of based on their income and credit history. Overlooking poor credit history or income below what would normally be required to qualify for a loan results in individuals ending up with ruinous debt. These individuals will end up losing their homes, cars, or businesses because banks disregarded sound lending practices in an effort to show they are meeting race-based requirements.

Forcing banks to make loans based on political considerations damages the economy by misallocating resources. This reduces economic growth and inflicts more pain on lower-income Americans.

The Carter-era Community Reinvestment Act has already shown what happens when the government forces banks to give loans to unqualified borrowers. This law played a significant role in the housing boom and subsequent economic meltdown. The Federal Reserve Racial and Economic Equity Act will be the Community Reinvestment Act on steroids.

This legislation also requires the Fed to shape monetary policy with an eye toward eliminating racial disparities. This adds a third mandate to the Fed’s current “dual mandate” of promoting a stable dollar and full employment.

Federal Reserve Chair Jerome Powell has already publicly committed to using racial disparities as an excuse to continue the Fed’s current policy of perpetual money creation. Since inflation occurs whenever the Fed creates new money, Powell and his supporters want a policy of never-ending inflation.

Supporters of this scheme say that inflation raises wages and creates new job opportunities for those at the bottom of the economic ladder. However, these wage gains are illusory, as wages rarely, if ever, increase as much as prices. So, workers’ real standard of living declines even as their nominal income increases. By contrast, those at the top of the income ladder tend to benefit from inflation as they receive the new money — and thus an increase in purchasing power — before the Fed’s actions cause a general rise in the price level. The damage done by inflation is hidden and regressive, which is part of why the inflation tax is the most insidious of all taxes.

When the Fed creates new money, it distorts the market signals sent by interest rates, which are the price of money. This leads to a bubble. Many people who find well-paying jobs in bubble industries will lose those jobs when the bubble inevitably bursts. Many of these workers, and others, will struggle because of debt they incurred because they listened to “experts” who said the boom would never end.

The Federal Reserve’s manipulation of the money supply lowers the dollar’s value, creates a boom-and-bust business cycle, facilitates the rise of the welfare-warfare state, and enriches the elites, while impoverishing people in the middle and lower classes. Progressives who want to advance the wellbeing of people in the middle and lower classes should stop attacking free markets and join libertarians in seeking to restore a sound monetary policy, The first step is to let the people know the full truth about the central bank by passing the Audit the Fed bill.

Once the truth about the Fed is exposed, a critical mass of people will join the liberty movement and force Congress to end the Fed’s money monopoly.

via ZeroHedge News https://ift.tt/2GSZO52 Tyler Durden

Demand Hell: Tesla Cuts Prices In China For The Seventh Time This Year Tyler Durden

Tue, 10/13/2020 – 14:45

Tesla has once again cut prices for cars in China. This time, the company slashed prices for its longer-range and performance Model S by 23,000 yuan for each model, according to Bloomberg. Including today’s cuts, it is the seventh price cut for Tesla in China alone this year, according to GLJ Research’s Gordon Johnson.

Perhaps the company’s newly released September sales numbers in China were the driving force behind the cuts. As Johnson notes in his latest report on the company from Tuesday, October 13, Tesla actually lost market share in China and unsold inventory doubled. Johnson writes:

TSLA sold 11,329 made in China (“MIC”) Model 3 cars in Sep. 2020, bringing quarterly totals to 34,333. This compares to 30,494 in 2Q20, a growth of +12.6%, while production grew 13.2%, and unsold inventory roughly doubled q/q (i.e., up +75.5% q/q). Interestingly, while the Chinese NEV market grew 26% m/m in Sep. 2020 (link), TSLA’s MIC M3 sales were down -2% over the same time frame (TSLA’s Model 3 MIC market share fell from 10.5% in Aug. to 8.3% in Sep.).

As Johnson notes, the company did stop production the last 10 days of September in China, but still saw its inventory nearly double. Johnson says this could be why the company plans on exporting cars it has made in China to the Asia Pacific and Europe.

Johnson also noted that Tesla (purple line) is losing market share in the EU:

Meanwhile as Tesla looks to stoke demand in Asia, and while the market continues to ascribe a valuation to Tesla as though it is not a traditional auto manufacturer, people can’t help pointing out the obvious: that they are still behind legacy automakers like GM. For example, GM has sold more than 2x the amount of EVs in China than Tesla did last month:

GM sold more than TWICE the amount of electric vehicles than $TSLA sold in China last month, and far more than Tesla’s peak China sales in any month ever.

Johnson concluded, stating about the price cuts: “That’s quite a few price cuts for a company that is said to be supply constrained (by definition, if you continuously have to lower the price of the item you’re selling, and have failed to sell out production for three straight months and running, you have a demand problem… not a supply problem).”

via ZeroHedge News https://ift.tt/33V1CTR Tyler Durden

Eli Lilly Suspends COVID-19 Antibody Therapy Trial Over “Potential Safety Concern” Tyler Durden

Tue, 10/13/2020 – 14:41

Barely a week after applying for emergency use approval from the FDA for one of its COVID-19 antibody therapeutics, it appears trials for one of Eli Lilly’s therapeutic drugs focused on the virus (Eli Lilly is working on more than just one) have been paused, according to an NYT report.

Per the NYT report, the government-sponsored clinical trial has been paused because of a “potential safety concern.” The report cited emails that government officials sent on Tuesday to researchers at testing sites, which the company confirmed. The trial was designed to test the benefits of the therapy on hundreds of people already infected with the virus. The company did not say how many volunteers were sick, or any details about their illness.

This comes after Johnson & Johnson confirmed that it had voluntarily paused its Phase 3 vaccine trials after a participant in the 60k person trial came down with an unusual and unspecified illness. An AstraZeneca trial in the US has still not restarted.

As we noted last night, convincing the public to trust the vaccines is critically important, according to a team of analysts at Goldman Sachs, who recently warned that convincing the public to accept the vaccine is an understated risk.

Stocks tumbled on the news.

via ZeroHedge News https://ift.tt/2H28MNj Tyler Durden

{kind=link}