Quality Control Hell: Tesla’s Model 3 Bumper Is Falling Off “More Than Expected” Tyler Durden

Mon, 07/20/2020 – 08:46

We’re not sure exactly how expected it should be that a bumper should randomly fall off of a car at any given time, but we digress.

Let’s just ignore that bit of common sense and focus on the fact that Elon Musk – the man who wants to implant chips into people’s brains to cure cognitive diseases – seems to be having an awful lot of trouble manufacturing a car that doesn’t disintegrate while it’s being driven down the street.

Our friends over at InsideEVs released a scathing piece this weekend about Tesla’s Model 3, noting that the car’s bumper has a tendency to fall off at a rate that is “more widespread than expected”. And we credit the blog for posting the story despite getting obvious pushback from Tesla cultists.

“Any article that exposes issues from Tesla gets apologists claiming it is irrelevant, regardless of what it is. The story would be an attempt to harm the company. As we already explained, it is the opposite: it is an effort to convince it to do the right thing,” the blog said.

The blog shares three different horror stories of bumpers flying off that were sent to the blog after they posted their first article about a Model 3 bumper flying off. In all three cases, the owners were told by Tesla that the repairs would not be covered.

The first owner recalled:

“I was driving through a puddle that was about ankle deep when I heard a loud thud coming from the back of my car. When I looked out through my rear-view mirror, I could see my bumper laying on the road behind me. My friend, who was in another car driving in front of me, went through the same puddle without issue. I was able to get the parts that fell off my car home through the help of my friend and some people who were in the area at the time who loaned me their tools. The next day at home I assessed the damage and reattached the bumper fascia more securely.”

When he brought the issue to Tesla, who seemed at first like they would help him, they eventually “told me that they actually wouldn’t be able to fix it, despite having ‘ordered all the parts.’”

A second owner wrote about his bumper:

“Just another statistic for you: the same thing happened to my early Model 3 LR RWD, VIN 26xxx, last month (June) when I drove through a puddle a little larger than this on a one-way road. Both lanes were flooded, there was no place to turn around, and not really enough warning to make a turn prior to encountering it, with heavy traffic behind me. My car is still sitting at the body shop…”

“They simply told me that it wasn’t something Tesla would cover,” the second owner said after he took his vehicle to try and get repaired under warranty.

A third owner, Luis Terceiro, said:

“I was driving to work in low traffic and heavy rain. I take two major highways to get to work (I-35 and President George w. Bush Turnpike tollway, both in Dallas, Texas). After parking my car, I saw that my rear bumper was hanging by one bolt on the left side. The whole bumper was dragging on the road for who knows how long!”

Tesla claimed they couldn’t make repairs to his vehicle because he was “driving 100mph” when the bumper came off. “How I can drive 100 mph in heavy rain and live to tell the tale is beyond me,” Terceiro said.

Recall, just a few days ago we posted a viral video perfectly demonstrating exactly the type of quality one would expect from a vehicle made in an outdoor tent.

A video of a Model 3’s bumper flying off while driving in the rain went viral last week. Hilariously, pro-Tesla blog electrek describes the bumper flying off as a “known issue”, as if when it rains the bumpers of Fords and GMs fly off randomly while driving all the time.

The video has garnered over 1 million YouTube views in just a matter of days.

“In 2018, when Tesla was still ramping up production of the Model 3, we reported on several owners who had issues with their rear bumpers falling off after driving through rain or water puddles,” the blog wrote last Wednesday.

Although the company said they were investigating it, here we are in 2020 and it still appears to be a major issue. The video description says:

I was driving my Tesla Model 3 in the rain with 2 other people in the car when all of a sudden we heard a big BOOM! I pulled into the nearest parking lot, went out of my car to check what happened and I was in total shock.

Recall back in 2019 we wrote about a flaw that had allowed 35 pounds of dirt to get trapped under a Model 3 bumper in Canada. The Model 3 was found to have a design flaw in its underbody that causes the car to trap and retain dirt, water and sand from roadways.

Back in 2019, electrek was making excuses for Tesla still, saying that the company has “often been accused of designing cars for the Californian climate” and that water, dirt and sand used to de-ice roads in colder climates are susceptible to getting trapped in the underbody of Model 3 cars.

“I wish Tesla would address this, but the automaker doesn’t seem to respond to media inquiries anymore,”electrek editor Fred Lambert bemoaned at the end of his article about the issue.

Now you know how we feel, Fred.

via ZeroHedge News https://ift.tt/3joiWGw Tyler Durden

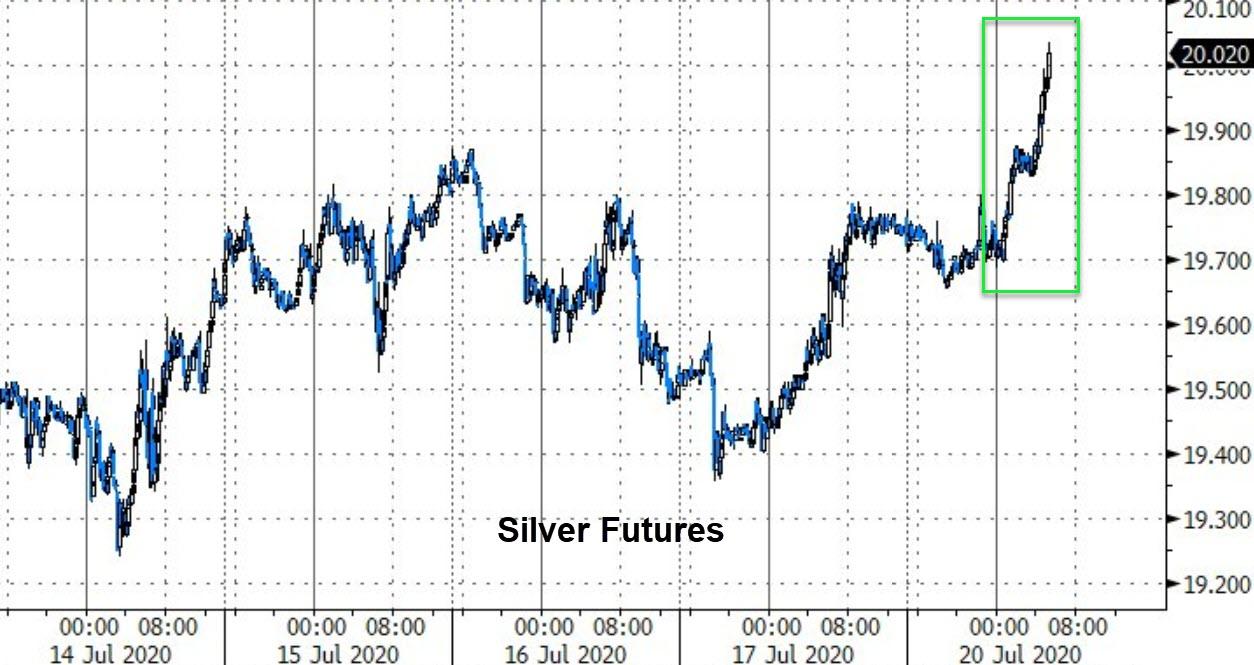

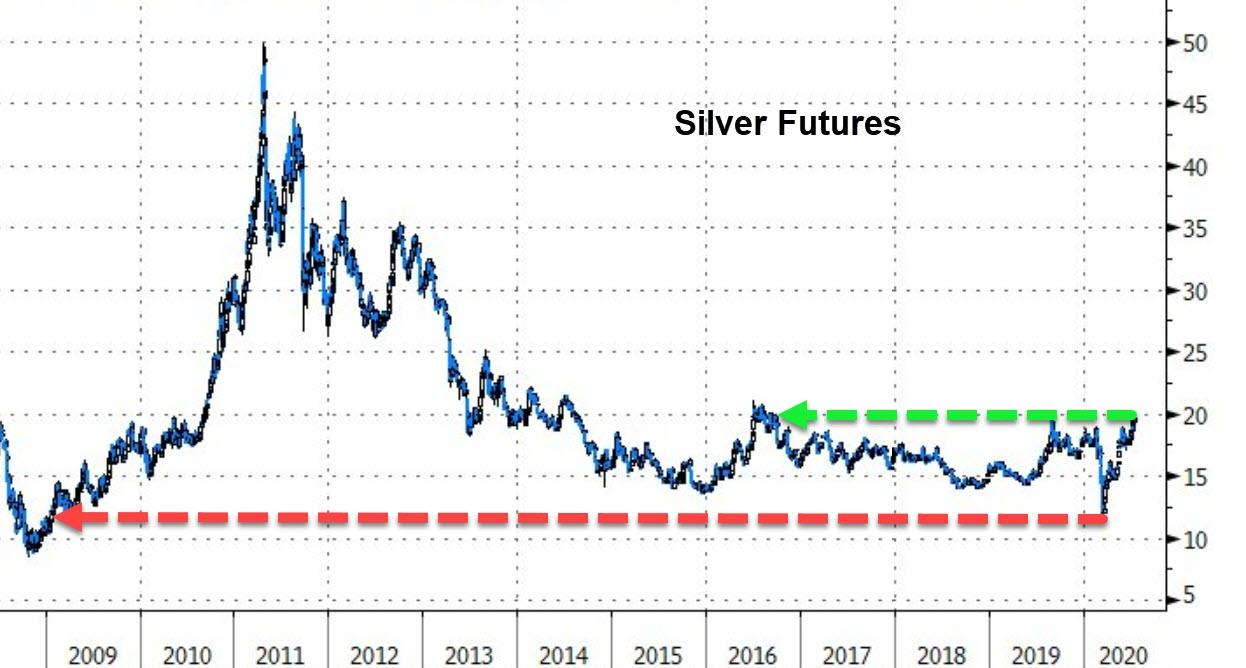

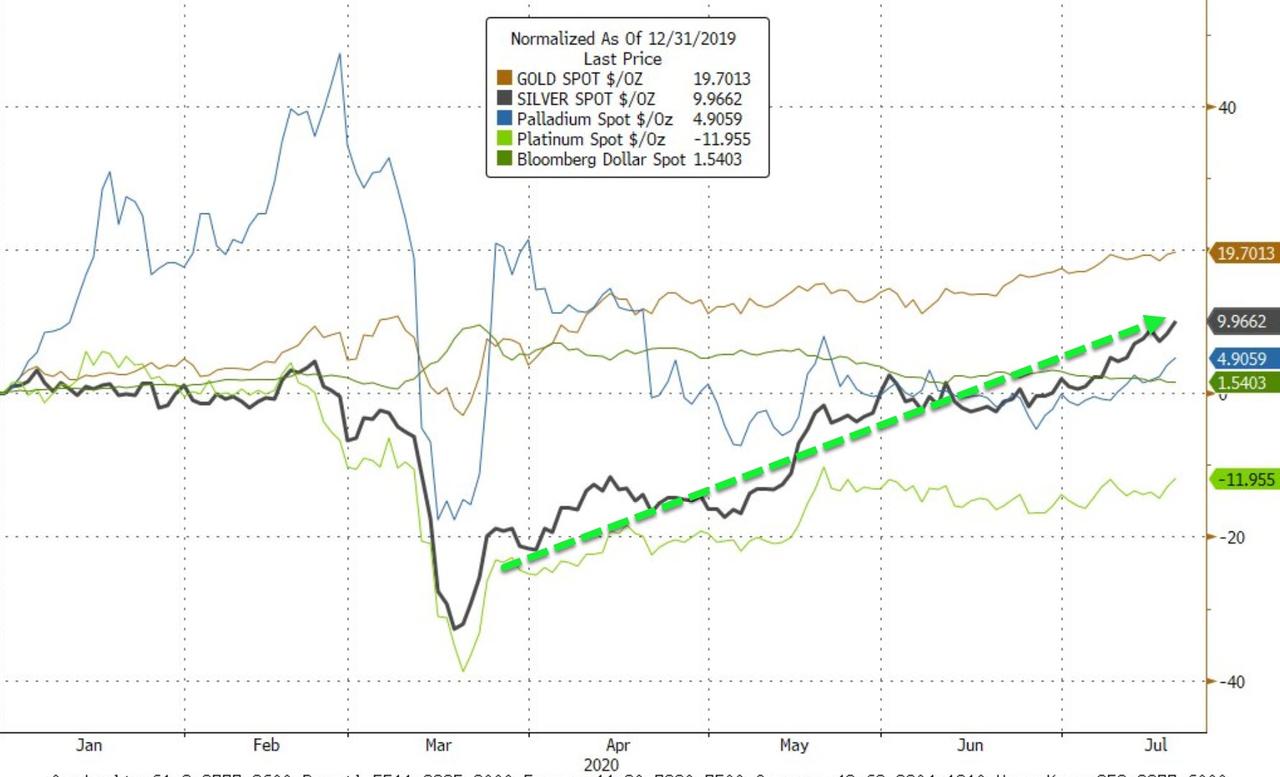

Silver Hits $20 For The First Time Since 2016… And Why It Will Go Much Higher Tyler Durden

Mon, 07/20/2020 – 08:32

For the first time since September 2016, Silver futures just broke above $20…

Just a few short months after dropping to the lowest since 2009…

As the gold/silver ratio reverses from its record high spike…

Though gold is still outperforming YTD for now…

But, as tsi-blog.com explains, silver is set to continue outperforming over the next year.

Gold is more money-like and silver is more commodity-like. Consequently, the relationships that we follow involving the gold/GNX ratio (the gold price relative to the price of a basket of commodities) also apply to the gold/silver ratio. In particular, gold, being more money-like, tends to do better than silver when inflation expectations are falling (deflation fear is rising) and economic confidence is on the decline.

Anyone armed with this knowledge would not have been surprised that the collapse in economic confidence and the surge in deflation fear that occurred during February-March of this year was accompanied by a veritable moon-shot in the gold/silver ratio. Nor would they have been surprised that the subsequent rebounds in economic confidence and inflation expectations have been accompanied by strength in silver relative to gold, leading to a pullback in the gold/silver ratio. The following charts illustrate these relationships.

The first chart compares the gold/silver ratio with the IEF/HYG ratio, an indicator of US credit spreads. It makes the point that during periods when economic confidence plunges, the gold/silver ratio acts like a credit spread (credit spreads rise (widen) when economic confidence falls).

The second chart compares the silver/gold ratio (as opposed to the gold/silver ratio) with the Inflation Expectations ETF (RINF). It makes the point that silver tends to outperform gold when inflation expectations are rising and underperform gold when inflation expectations are falling.

We are expecting a modest recovery in economic confidence and a big increase in inflation expectations over the next 12 months, meaning that we are expecting the fundamental backdrop to shift in silver’s favour. As a result, we are intermediate-term bullish on silver relative to gold. We don’t have a specific target in mind, but, as mentioned in the 16th March Weekly Update when the gold/silver ratio was 105 and in upside blow-off mode, it isn’t a stretch to forecast that at some point over the next three years the gold/silver ratio will trade in the 60s.

Be aware that before silver commences a big up-move in dollar terms and relative to gold there could be another deflation scare. If this is going to happen it probably will do so within the next three months, although we hasten to add that any deflation scare over the remainder of this year will be far less severe than what took place in March.

via ZeroHedge News https://ift.tt/2Bjre1m Tyler Durden

One Hedge Fund Manager’s Lesson On When To Take Profits Tyler Durden

Mon, 07/20/2020 – 08:20

Authored by Eric Peters, CIO of One River Asset Management, who has written the following anecdote about learning to take a profit, a lesson learned in 1992.

Black Wednesday – 16 September 1992. How the newspapers reported the sterling crisis.

“Let’s step into my office,” he said. So I did. He was my boss. “The firm’s most important client needs help,” he said. I listened, uninterested, unconcerned about clients, their problems. Barely cared about my boss. I had a game to play, solo sport, and loved it to the exclusion of all else.

“They need to do a very large trade,” he explained. A twenty-six-year-old proprietary trader’s mind is rather primitive. Which is good and bad. Being young and dumb allows you to see things elders can’t. And take risks one rarely should. In 1992, I’d done both.

“They need to buy three hundred million Mark/Lira.” The Europeans established a mechanism to lock their exchange rates into narrow ranges to reduce market volatility and promote economic convergence. In theory it worked, in practice it didn’t. Politicians named it the ERM.

“What would you like to do?” he asked, calm. I stood there, processing. Such a sum was extraordinary even before the ERM blew up, which it just had. For months, I’d bought options in anticipation of its demise. Honestly, it was obvious. The ERM encouraged speculators to build massive leveraged carry positions, discouraged corporations from hedging exchange rate risk, suppressing volatility and interest rate spreads everywhere. The process was reflexive. Today’s central bank volatility suppression regime resembles it and will end in spectacular fashion. All such things do.

“I want to buy more!” I answered. My foreign-exchange options left me long the exact amount our client needed to buy. No other bank would sell them such a large sum. So naturally, I wanted to own even more.

“You should sell them your whole position,” he told me, firmly. I couldn’t understand, it made no sense.

“Big customer orders like this usually mark the highs – never forget it,” he said. I left his office angry, irate, sold my whole position. And he was right.

via ZeroHedge News https://ift.tt/2CQa384 Tyler Durden

But that was before we learned that the judge targeted in the attack – Newark-based US federal judge Esther Salas – had been assigned to the Deutsche Bank/Epstein case just four days before the attack.

The shooting occurred Sunday night at around 5pmET. Salas 20-year-old son Daniel Anderl, a student, opened the door at the family home in North Brunswick after hearing the doorbell ring. The man outside appeared to be a FedEx employee, according to media reports.

Almost immediately, the gunman started blasting, shooting and killing Anderl, and badly wounding his father, Mark Anderl, 63, a prominent defense attorney in the area. Salas has reportedly received threats from time to time, but local press reported that Salas hadn’t received any threats recently.

Seated in Newark, Salas’ most high-profile cases recently involved the tax evasion prosecution of Joe Giudice, the husband of RHNJ star Theresa Giudice. She also spared a murderous gang leader from the death penalty over what she ruled was an intellectual disability that made him ineligible for capital punishment.

But Salas is now presided over an ongoing lawsuit brought by Deutsche Bank investors who claim the company made false and misleading statements about its AML policies while failing to monitor “high-risk” customers like sex offender Jeffrey Epstein. After all, how would Epstein have managed to run his international child-sex-trafficking ring without banks to move the money around for him.

The FBI revealed last night that it would be taking over the case.

Investigators said they’re looking into any connections to the Epstein/DB lawsuit, while also investigating any connections to her husband’s work as a criminal defense attorney.

The FBI’s announcement was met with a sarcastic response by many on twitter.

If there is one organization in the country that can stand up to the Epstein-linked mob and keep democratic society on track, this is that group. https://t.co/xCb5SYUqP7

The FBI says it’s looking for one suspect. The Marshals Service is also carrying out its own investigation, since the agency takes its responsibility to protect federal officials “very seriously”.

So far, authorities have refused to confirm that the Epstein connection might have been a motive. A friend of the judge’s said Salas hadn’t received any threats recently.

Salas, 51, was New Jersey’s first Hispanic woman to serve as a US district judge. She was nominated by Barack Obama in 2010, and confirmed by the Senate the following year.

via ZeroHedge News https://ift.tt/3jlJLez Tyler Durden

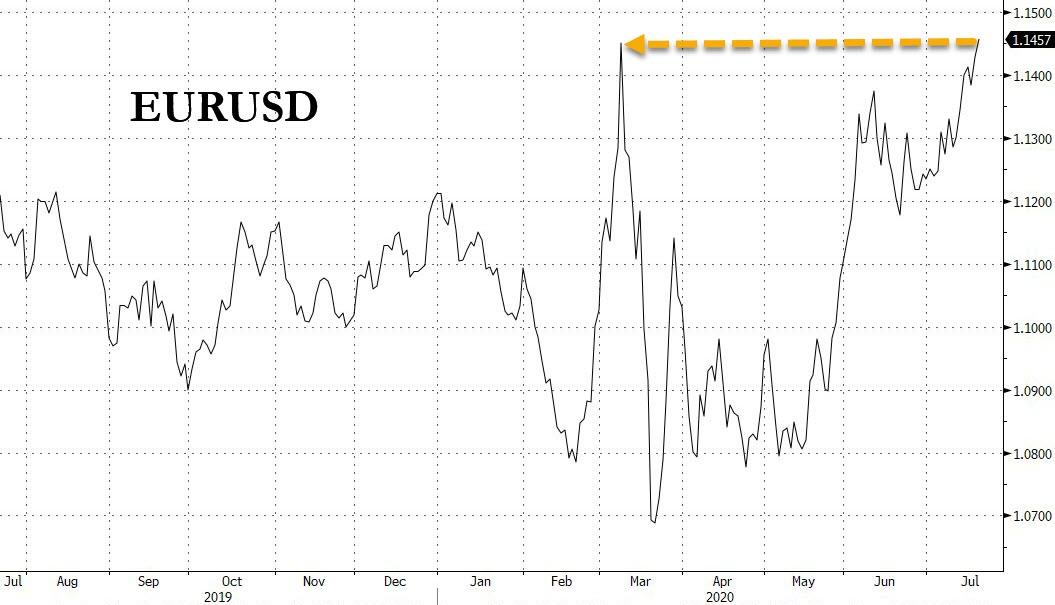

Futures Reverse Losses, Euro Jumps To 4 Month High On Hopes Of EU Rescue Package Deal Tyler Durden

Mon, 07/20/2020 – 07:52

S&P500 futures pared earlier losses, as European stocks gained and European bond spreads narrowed while the euro strengthened to a four-month high as leaders reportedly made progress in negotiating a historic stimulus package which was still missing after three days of tense, deadlocked weekend negotiations.

US equity futures traded -0.1% lower after dropping -0.6% earlier. In Merger Monday news, Chevron agreed to buy Noble Energy for about $5 billion in shares, the first major deal since the coronavirus triggered a severe oil slump. “Our strong balance sheet and financial discipline gives us the flexibility to be a buyer of quality assets during these challenging times,” Chevron Chief Executive Officer Michael Wirth said in a statement on Monday. “This is a cost-effective opportunity for Chevron to acquire additional proved reserves and resources.“ The deal values Noble at $10.38 a share, or 0.1191 of a Chevron share, equivalent to a 7.5% premium over Friday’s closing price. The total enterprise value, including debt, is $13 billion.

The single currency hit its highest levels against the dollar since March 9, at $1.1467 after early Monday reports of progress following three days of negotiations towards the proposed 750 billion-euro fund. The four governments that have been holding up negotiations are ready to agree on a key plank of the deal, two officials said. The Netherlands, Austria, Denmark and Sweden, also known as the “Frugal Four” are satisfied with €390 billion of the fund being made available as grants with the rest coming as low-interest loans. Still, that number is about €110BN below the €500BN that was originally expected to be made available in the form of grants. A deal envisaging €400 billion in grants – down from a proposed €500 billion – was also rejected by the north, which said it saw €350 billion as the maximum.

Talks on the fund were adjourned on Monday until 1600 CET (1400 GMT). After the adjournment was announced, both the Austrian Chancellor Sebestian Kurz and Dutch Prime Minister Mark Rutte said progress was being made.

“The euro has gained on the likelihood that they do come up with some solution at this meeting,” said Marshall Gittler, head of investment research at BDSwiss Group. “I had expected them to fail, or at best to come to only a partial agreement, but the fact that they’ve kept at it for this long shows that they really are determined to succeed,” Gittler said. A successful agreement would probably give the euro a further boost, he added.

“The chances of a deal appear higher now than before the weekend, with the Frugal Four winning concessions while also acknowledging grants must be part of the deal,” strategists at UBS Global Wealth Management said in a note to clients. “While it remains to be seen if a deal can be done today, we continue to expect an eventual agreement, which would act as a catalyst for the euro and support Eurozone equities and bonds.”

Bond markets also cheered the progress, with Italy’s 10-year bond yield spread over Germany, a key gauge of risk in the region, falling to 161 bps, the lowest level since March.

Stock markets were more reserved in their optimism, however. The pan-European Stoxx 600 index 0.2% higher by mid-morning trade in London, reversing an earlier loss of -0.8% with a risk-off tone expressed in sectoral gainers and losers. Shares of chemical and construction companies led the gains, while the region’s travel and leisure stocks retreated on continued worries over the coronavirus pandemic. AstraZeneca Plc gained ahead of highly anticipated results from early vaccine studies.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan gained 0.26%, reversing loses earlier in the day, led by materials and IT, after rising in the last session. Most markets in the region were down, with Jakarta Composite dropping 0.6% and Australia’s S&P/ASX 200 falling 0.5%, while Shanghai Composite resumed its bubbly ways, closing at session highs, up 3.1% after regulators raised the equity investment cap for insurers and encouraged mergers and acquisitions among brokerages and mutual fund houses. China’s Chalco and Changjiang & Jinggong posting the biggest advances. Japan’s Topix gained 0.2%, with Japan Communications and Takara & Co Ltd rising the most. Australia’s S&P/ASX 200 index dropped 0.5% after authorities warned that a surge in COVID-19 cases in the country’s second most populous state could take weeks to tame.

More than 14 million people have been infected by the novel coronavirus globally and nearly 602,000 have died, according to a Reuters tally.

South Korea’s KOSPI pared gains to fall 0.1%. Japan’s Nikkei was also down 0.1% after data showed the country’s exports suffered a double-digit decline for the fourth month in a row in June.

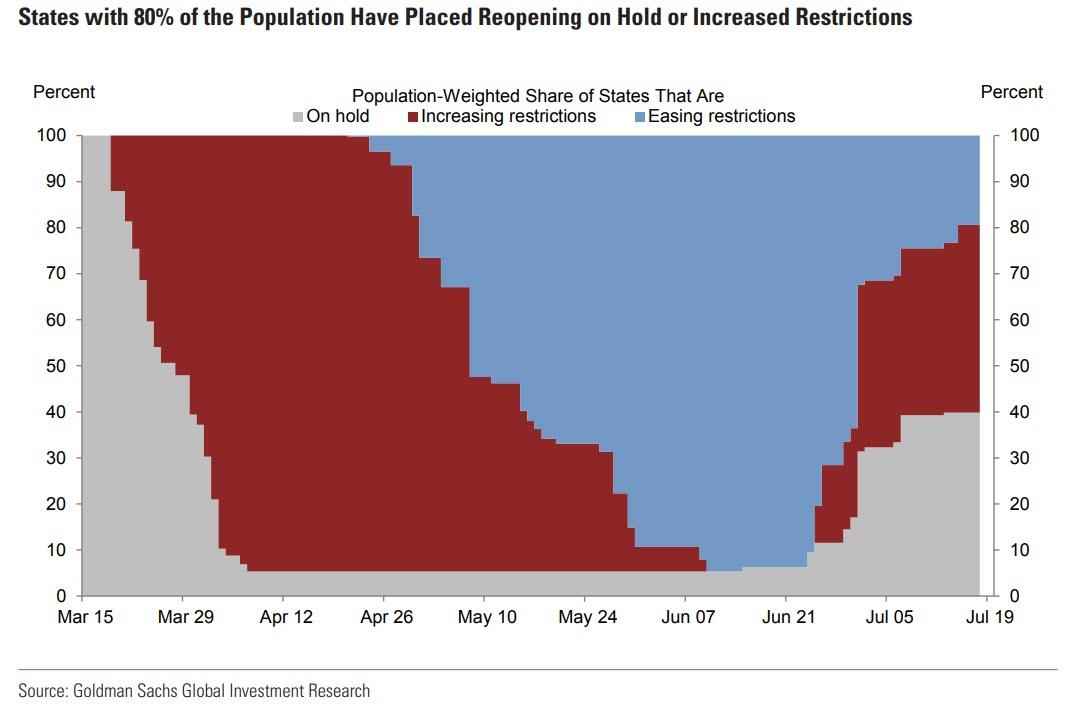

Meanwhile, in the US talks on a new stimulus package will start on Monday with with Mitch McConnell, Steven Mnuchin and others as several states in the country’s South and West imposed new lockdowns to curb the virus and 80% of states now stopping or reversing reopening according to Goldman.

With the virus spreading rapidly in parts of the U.S., there are still plenty of worries about the health of the global economy. Los Angeles Mayor Eric Garcetti has warned that the city is on the brink of another stay-at-home order. Hong Kong added a record 108 infections, will require civil servants to work from home and plans to mandate wearing of masks in all shared indoor areas.

”The economic dislocation of Covid-19 triggered a tremendous response by fiscal and monetary policy makers as well as central banks,” said Gene Tannuzzo, a portfolio manager at Columbia Threadneedle. “These measures helped to stabilise markets, yet we still find ourselves in an environment of continuous low growth.”

While stock markets have inched higher in recent weeks, there are still plenty of worries about the health of the global economy, especially with the virus spreading unabated in parts of the U.S. In the euro area, unemployment could hit almost 10% by the end of the year as the economy slumps, according to a Bloomberg survey.

In rates, Treasury yields were slightly richer across the curve, outperforming bunds following report that EU leaders are set to resume deadlocked recovery-fund talks. Treasury yields were lower by 0.5bp to 1.1bp across the curve with 2s10s, 5s30s flatter by 0.6bp and 0.2bp; 10-year yields around 0.618%, richer by less than 1bp vs Friday’s close. Bunds cheaper by 2.2bp, gilts by 1.2bp vs Treasuries.

In currencies, the Bloomberg Dollar Spot Index shrugged off early gains to slip as the euro rallied to 4 month highs. Italian bonds climbed and U.S. equity futures pared losses as European stocks gained. Meanwhile, the Japanese yen rose to 107.22. while Sterling gained 0.4% to trade as high as $1.2618. The risk-sensitive Australian dollar was down 0.1% at $0.6989.

In commodities, spot gold traded flat at $1,809.58 an ounce, still near a nine-year top. Oil extended losses toward $40 a barrel, unnerved by the prospect of rising coronavirus cases halting a recovery in fuel demand. WTI and Brent were both down 1% each to $40.14 per barrel and $42.71 per barrel, respectively. Prices for copper, a barometer of economic growth, fell on Monday after data showed rising inventories in Chinese warehouses and on concern the climbing coronavirus cases threatened a sustainable global recovery.

Halliburton and IBM are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.2% to 3,207.75

STOXX Europe 600 down 0.5% to 370.93

MXAP up 0.2% to 164.86

MXAPJ up 0.2% to 542.42

Nikkei up 0.09% to 22,717.48

Topix up 0.2% to 1,577.03

Hang Seng Index down 0.1% to 25,057.99

Shanghai Composite up 3.1% to 3,314.15

Sensex up 1% to 37,387.70

Australia S&P/ASX 200 down 0.5% to 6,001.57

Kospi down 0.1% to 2,198.20

German 10Y yield rose 0.2 bps to -0.445%

Euro up 0.4% to $1.1468

Italian 10Y yield fell 1.7 bps to 1.043%

Spanish 10Y yield fell 1.4 bps to 0.396%

Brent futures down 0.6% to $42.90/bbl

Gold spot up 0.1% to $1,812.34

U.S. Dollar Index down 0.2% to 95.80

Top Overnight News

The four EU governments holding up negotiations over 390Bn stimulus package to reboot the bloc’s economy are ready to agree on a key plank of the deal, officials said

Informal Brexit meetings between the U.K. and EU’s chief negotiators in recent weeks have failed to make progress

U.K. is set to halt its extradition pact with Hong Kong, marking a further diplomatic escalation with China

Saudi Arabian King Salman bin Abdulaziz of has beenadmitted to a hospital in Riyadh early Monday for medical tests, the second elderly ruler of an oil-rich Gulf Arab nation to be hospitalized in less than a week

APAC stocks traded choppy after the region initially took its cue from Wall Street’s mixed close on Friday as the decline in Netflix shares kept other large tech stocks at bay ahead of another earnings-abundant week, with 92 S&P 500 companies alongside eight Dow 30 constituents bracing to report their numbers – including the likes of Tesla, Microsoft, Twitter, IBM and some major US airlines. ASX 200 (-0.5%) lost steam after the open as Australia remained subdued by the outbreak in its second largest state of Victoria– which prompted authorities to announce a mandatory mask-wearing rule over the weekend. Nikkei 225 (+0.1%) swung between gains and losses after seeing initial pressure as Japan’s June trade balance printed a significantly wider-than-expected deficit in JPY terms, but with losses somewhat cushioned on currency dynamics. Meanwhile, Hang Seng (-0.1%) conformed to the downside across the region at the open and as Hong Kong is set to tighten restrictions following a spike in COVID-19 cases, but later erased losses, whilst Shanghai Comp (+3.1%) outperformed as reports noted that Beijing is to lower its COVID-19 alert level as cases are back under control, whilst the PBoC also injected a net CNY 50bln via 7-day reverse repos. Finally, JGB futures traded lower in early Tokyo trade, whilst most of the curve saw some cheapening, but the longer-end held despite 20yr supply tomorrow.

Top Asian News

Hong Kong Growth to Halve as City Loses Distinctiveness: S&P

China Condemns U.K.’s ‘Wrong Words and Actions’ on Hong Kong

BP Singapore Oil Traders Placed on Leave Amid Disputed Deals

European equities (Eurostoxx 50 +0.3%) kicked the session off on the backfoot before paring losses as market participants eye events in Brussels and the COVID situation in the US. Despite some of the harsh words spoken between EU leaders over the weekend, the latest state of play indicates that some form of agreement on the recovery fund could be on the cards as the so-called “frugal four” appear to have settled on a figure of EUR 390bln for the grants component of the fund (subject to pushing for additional rebates from the EU budget). As such, it is now on EU members external to the frugals to meet the group “halfway”. Talks have currently taken a pause and will resume once again later today at 1500BST. Despite a potential agreement being on the horizon and upside for the EUR currency (suggesting the market is taking a favourable view of the situation), stocks took a little while to recover off lows with indices now broadly flat/marginally firmer. Stateside, COVID concerns remain at the forefront with the US reporting +67k cases yesterday and as according to Fulcrum economists, the r-rate is above 1 in 45 of the 50 US states, which between them account for 95% of U.S. GDP. From a sectoral standpoint, sectors trade mixed with some of the more cyclical names such as travel & leisure and autos faring worse than peers. For the former, it is worth noting that reports suggest Barcelona could have to return to lockdown within the next two weeks, such a development would be troubling given it is such a tourist hotspot for Europe and a potential sign of things to come for other such destinations. Elsewhere, losses for health care names are shallower than most with AstraZeneca (+3.2%) lending some support after signing an in-principal agreement with Britain’s business ministry for 1mln doses of a treatment containing COVID-19 neutralising antibodies for those who cannot receive a vaccine. Note, markets also await data from the Co.’s early-stage human trials due to be published in The Lancet later today (timing TBC). Other notable movers include Natixis (-7.3%) after BPCE pushed back on FT speculation that it was looking to purchase the remaining 30% shares of Natixis they do not already control. To the upside, UBI Banca (+12.4%) sit at the top of the Stoxx 600 after reports noted that Intesa Sanpaolo increased its bid for UBI, offering EUR 0.57/shr in addition to 1.7 shares for each UBI share.

Top European News

Glaxo to Invest Up to $1 Billion in CureVac Vaccine Pact

U.K. Orders 90 Million Vaccine Doses from Pfizer, Valneva

Europe’s Climate Laggard Plans Green Revolution With Oil Company

In FX, the Dollar is mixed vs major rivals and seems to be settling into relatively narrow ranges that often mark the start of a new week, albeit after some volatility in certain Usd/G10 pairings overnight and in early EU trade. The index is rotating around 96.000 within a 95.792-96.183 band and maintaining an underlying bid on broad risk aversion to counter losses against a few counterparts and the latest more specific US COVID-19 developments that include record rises of confirmed cases in some states again.

EUR – Renewed hope of a deal on the EU Recovery Fund at the next meeting of leaders is keeping the Euro elevated amidst stops on a break of last week’s peak vs the Greenback that pushed the pair up to circa 1.1467 at one stage. However, an agreement is far from certain as the so called ‘frugals’ continue to contest the total size of the crisis package and composition between grants and loans – for a more in depth look at the current state of play and latest proposals check out the headline feed at 9.03BST. In terms of technical factors, Eur/Usd resistance is seen at the 1.1495 ytd high from March 9 ahead of 1+ bn expiries at 1.1500, while even heftier option expiry interest at the 1.1400 strike (2.6 bn) should add to psychological support and underlying bids.

CHF/JPY – Both weaker vs the Buck, with the Franc back below 0.9400 and Yen under 107.00, albeit off worst levels through 107.50 on the back of worse than forecast Japanese trade data, while the former will have taken note of a Chf 5 bn or so jump in Swiss domestic bank sight deposits. Indeed, Eur/Chf is also higher alongside Eur/Jpy, eyeing 1.0775 and 123.00 ahead of CPI and trade respectively on Tuesday.

GBP/NZD/CAD/AUD – All essentially flat relative to the US Dollar, with Sterling gleaning some traction from the single currency’s advance as Eur/Gbp fails to extend beyond last Friday’s high and drifts back down towards 0.9100, while the Kiwi rotates around 0.6550 on marginally favourable Aud/Nzd cross flows in the run up to RBA minutes and a speech from Governor Lowe that are keeping the Aussie contained/capped at 1.0675 and near 0.7000. Elsewhere, the Loonie is meandering between 1.3600 and 1.3570 awaiting Canadian housing data, retail sales and CPI over the next 48 hours for some independent impetus following the BoC and July MPR that was bereft of economic estimates.

EM – Another strong rally in Chinese equities, a firmer PBoC Usd/Cny midpoint fix and net injection of 7-day liquidity all keeping the Yuan afloat above 7.0000 and close to resistance near 6.9800 that has been tested twice so far in July, but the Lira remains rigid between 6.8500-8600 ahead of Thursday’s CBRT policy meeting even though the Turkish CB jacked up the FX RRR by 300 bp to raise reserves by some Usd 9 bn.

In commodities, WTI and Brent have begun the week on the backfoot, as sentiment in general has been subdued for much of the session after a choppy APAC handover following a mixed US close and a number of updates from the EU Council meeting. For the crude complex itself newsflow has been slow, attention was grabbed by reports that the Saudi King Abdulaziz was admitted to hospital; but, ultimately did not cause a price reaction as the reason was testing for an infection. For the week itself there isn’t anything scheduled on the crude front of note, aside from the usual weekly private inventories, DoE’s & Baker Hughes updates. As such, the complex may well itself more at the whim of broader sentiment/USD action – barring any unscheduled updates of course. Most recently, Sinopec are cutting refining rates for July due to demand being impacted by severe flooding, according to sources. Moving to metals where spot gold is currently little changed on the day and is comfortably above USD 1800/oz handle and withing proximity to the high of circa USD 1812/oz. Citi, on the precious metal, writes that a rally to record prices is only a matter of time and ascribes a 30% chance to USD 2000/oz by Christmas; given, record ETF inflows, increased gold asset allocations & low real yields among other factors.

US Event Calendar

Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

After 3 days and long nights of the extended EU recovery fund summit, the diplomatic lake in Brussels remains frozen over even if there does seem to be signs that we’ll see a thaw today.

The very latest reports this morning (although this could be out of date by the time you read) are pointing towards a possible compromise for €390bn in grants in the recovery fund. It seems much depends on whether Macron believes this to be ambitious enough. The wires have just quoted a French official as saying “France now see a path to a recovery fund deal”. It seems we may be on hold until this afternoon though but the fact that we are still going well into a fourth day suggests a desire to get something done.

The Euro is largely unchanged this morning against the greenback at 1.1424 even as the US dollar index is up +0.20%. Meanwhile, Asian markets are trading mixed with the Shanghai Comp (+2.62%) and Hang Seng (+0.35%) up while the Nikkei (+0.05%) and Kospi (-0.05%) are flat and the Asx (-0.48%) is down. Chinese markets have danced to a different beat over the last couple of weeks so not much read through for other global markets here. Elsewhere, futures on the S&P 500 are trading down -0.32%.

Moving onto the coronavirus, globally reported cases crossed the 14 million mark over the weekend with fatalities above 605k. Sao Paulo crossed New York to become the most infected state globally with 415,049 confirmed cases. In the US, cases rose at an average of +1.72% per day this weekend above the +1.53% rise per day registered in the previous 5 weekends while fatalities rose at +0.47% vs. previous 5 weekend average of 0.34%. In terms of state level data new case growth slowed in Texas, Florida and Arizona over the weekend compared to previous weekends indicating that renewed lockdown measures are helping. However, in California new case growth was at an average of +2.47% vs. the previous 5 weekend average of +2.20%. Meanwhile, fatalities picked up with Texas registering an average per day growth of +2.21% as against +1.07% per day over the previous 5 weekends. Likewise, Florida (at +1.83% vs. +0.99%), California (at +1.26% vs. +0.74%) and Arizona (at +3.41% vs. +1.77%) all registered rises.

In Asia, Hong Kong is planning to extend mandatory wearing of masks to more public spaces after registering a record 108 new infections yesterday and has extended restaurant restrictions and gym closures for another week. Melbourne has also mandated its residents to wear masks as Victoria state added another 275 cases. China’s Xinjiang province is also seeing a small spike in new cases (17) leading to concerns around a second wave.

In other overnight news, talks on a new coronavirus stimulus package will start at the White House today with Senate Majority Leader Mitch McConnell, Treasury Secretary Steven Mnuchin and others. Bloomberg reported that priorities for the talks include funding to expedite development of therapeutics and vaccines for the coronavirus, “protections for the American worker and those that employ individuals” and the manufacturing sector, particularly bringing jobs back to the US from abroad. President Donald Trump’s chief of staff said that “It looks like that new package will be in the trillion-dollar range, as we have started to look at it, whether it’s a payroll tax deduction, whether it’s making sure that unemployment benefits continue without a disincentive to return to work.”

The data highlight this week will be the flash PMIs for July on Friday (Japan Wednesday). Elsewhere earnings season picks up a bit more, with 88 releases from S&P 500 companies and another 76 from the STOXX 600.

For the flash PMIs for July, the highlight will be whether US progress has stalled given the increased spread of the virus over the last few weeks. In terms of expectations the US numbers are expected to tick up from the high 40s to the 51-52 range. In Europe there is more of a spread but the composite is expected to be at 51. It will be interesting to see if the European numbers can edge ahead of the US given the clearer run of reopenings. However Europe did see lower troughs and could have more scarring as a result. We will see over the months ahead as to whether the US – that didn’t ever totally lockdown – will see that offset by not fully controlling the virus.

Speaking of the US, another data highlight of note will be the weekly initial jobless claims for the week through July 18. Last week it fell by a smaller-than-expected -10k to 1.3m, which is the smallest weekly decline since they reached their peak back in late March, raising concerns over the speed of the labour market recovery. Over in Europe, another release will be the European Commission’s advance consumer confidence indicator for July (Thursday). The last couple of months have seen a rebound from its April low, but it still remains well below its levels at the start of the year, so it’ll be interesting to see if this upward momentum is sustained.

Earnings season moves into full flow this week, with 88 releases from S&P 500 companies and another 76 from the STOXX 600. In terms of the highlights to look out for, today we have IBM. Then tomorrow, that’s followed by Novartis, The Coca-Cola Company, Texas Instruments, Philip Morris, Lockheed Martin and UBS. Then on Wednesday, we have Microsoft, Thermo Fisher Scientific and Tesla. Thursday sees Roche, Intel, AT&T, Unilever, Union Pacific, Daimler, Twitter and Hyundai release earnings. Finally on Friday, we’ll hear from Verizon, NextEra Energy, T-Mobile and American Express.

It’s a quieter week on the central bank front, with Fed speakers now in their blackout period ahead of next week’s meeting. However, we will get decisions from some EM central banks, including Turkey and South Africa on Thursday and Russia on Friday. Otherwise, the Bank of Japan will be releasing the minutes of their June meeting today, and we’ll also hear from the BoE’s Haldane, Tenreyro and Haskel this week.

Looking back at last week now and markets were generally constructive even though the outlook for the virus in the U.S. has caused a great deal of uncertainty after more states paused and rolled back reopening plans. The S&P 500 gained +1.25% (+0.28% Friday) on the week, and finished at the highest end-of-week close of the pandemic. The tech-focused Nasdaq underperformed this week as earnings season got underway, falling -1.08% (+0.28% Friday) as the mega-cap growth NYSE FANG index saw its worst week (-4.91%) since the height of the market turmoil in March. European equities slightly outperformed the S&P with the Stoxx 600 gaining +1.60% (+0.16% Friday) over the five days. It was the third straight weekly advance, tied for the longest streak since November 2019. Major European bourses were all strongly higher on the week with the DAX (+2.26%), CAC (+1.99%), FTSE (+3.20%) and FTSE MIB (+3.30%) gaining ground. Asian indices were fairly mixed as Chinese stocks saw a large pullback after the over +7.5% rally the prior week with the CSI 300 down -4.29%, while the Nikkei (+1.82%) and Kospi (+2.37%) were higher over the week.

Core sovereign bonds were mixed even as risk assets generally rose. US 10yr Treasury yields fell -1.8bps (+1.0bps Friday) to finish at 0.627%, while 10yr Bund yields gained +1.8bps (+1.8bps Friday) to -0.45%. In other fixed income, HY cash spreads continued tightening both in Europe and the U.S. as sentiment improves and more stimulus seems on the way. US HY cash spreads tightened -39bps (-3bps Friday) and Europeans ones tightened -14bps (-4bps) Friday. The dollar fell -0.73% on the week to its lowest weekly close since February 2019, while the Euro gained +1.13% to the highest point early March.

via ZeroHedge News https://ift.tt/3jtBeXd Tyler Durden

Russian Elite Received ‘Experimental’ COVID-19 Vaccine As Early As April Tyler Durden

Mon, 07/20/2020 – 07:22

Last week, we shared news of what Russia’s scientific community had touted as a major breakthrough in the development of a vaccine for SARS-CoV-2: A vaccine trial at Moscow’s Sechenov First Moscow State Medical University had yielded the first successful human trials. The American business press slavishly parrots every Moderna press release as the company regurgitates its Phase 1 trial results, despite the fact that the politically-connected biotech company’s stage 3 clinical trials won’t begin until later this month. Meanwhile, its CEO Stephane Bancel and other executives have cashed in on their Moderna shares, prompting SEC chief Jay Clayton to sheepishly caution against credibility-destroying insider selling.

Despite all of this, we didn’t hear a peep out of the western press about the Sechenov trial’s accomplishments. However, a few days later, with anxieties about Russia-backed electoral interference intensifying and ‘national polls’ hinting at a Biden landslide, the British press reported on a new ‘policy paper’ accusing those pesky Ruskies of trying to steal British research involving COVID-19 vaccines. Intel shared by Canada and the US purportedly supported this conclusion, though Russia has vehemently denied the accusations.

But that’s not all: Around the same time, Foreign Secretary Dominic Raab accused Russia of trying to meddle in the UK’s December election (which returned the Tories to power and ended the reign of opposition leader Jeremy Corbyn).

Were these reports about Russia’s vaccine-trial successes merely a smokescreen? The British might see it that way, but on Monday, US-based Bloomberg News published an interesting report claiming that certain Russian VIPs had been administered experimental doses of a vaccine prototype as early as April. Reportedly developed by Moscow’s Gamaleya Institute and financed by the state-run Russian Direct Investment Fund, this Russian vaccine candidate is a so-called “viral vector vaccine” based on human adenovirus – a common cold virus fused with the spike protein of SARS CoV-2 to stimulate a human immune response.

It’s similar to a vaccine being developed by China’s CanSino Biologics, according to Bloomberg.

Scores of members of Russia’s business and political elite have been given early access to an experimental vaccine against Covid-19, according to people familiar with the effort, as the country races to be among the first to develop an inoculation.

Top executives at companies including aluminum giant United Co. Rusal, as well as billionaire tycoons and government officials began getting shots developed by the state-run Gamaleya Institute in Moscow as early as April, the people said. They declined to be identified as the information isn’t public.

The Gamaleya vaccine, financed by the state-run Russian Direct Investment Fund and backed by the military, last week completed a phase 1 trial involving Russian military personnel. The institute hasn’t published results for the study, which involved about 40 people, but has begun the next stage of trials with a larger group.

Gamaleya’s press office couldn’t be reached by phone Sunday. Kremlin spokesman Dmitry Peskov didn’t respond to a text message asking whether President Vladimir Putin or others in his administration have had the shots. A government spokesman couldn’t immediately comment.

Wait… so the Russians hacked the British vaccine research, traveled back in time, then decided to test their vaccine prototype on some of the most powerful people in Russia’s (highly unequal) society? Well, they had to first travel to the future to steal the time-travel technology from the Americans (bear with us…we’re still piecing it all together).

The program under which members of Russia’s business and political elite have been given the chance to volunteer for doses of the experimental vaccine is legal but kept under wraps to avoid a crush of potential participants, according to a researcher familiar with the effort. He said several hundred people have been involved. Bloomberg confirmed dozens who have had the shots but none would allow their names to be published.

It’s not clear how participants are selected and they aren’t part of the official studies, though they are monitored and their results logged by the institute. Patients usually get the shots – two are needed to produce an immune response Gamaleya says will last for about two years – at a Moscow clinic connected to the institute. Participants aren’t charged a fee and sign releases that they know the risks involved.

Dmitriev of the RDIF said he and his family had taken the shots and noted that a significant number of other volunteers have also been given the opportunity. He declined to provide further details. The Gamaleya Institute said it vaccinated its director, as well as the team working on the trial, when it started. In May, state-controlled Sberbank recruited volunteers among employees to test the institute’s vaccine.

One top executive who had the vaccine said he experienced no side effects. He said he decided to risk taking the experimental shots in order to be able to live a normal life and have business meetings as usual. Other participants have reported fever and muscle aches after getting the shots.

Is it so hard to believe that Russia had enough faith in its vaccine prototype that it would allow certain individuals the choice of receiving an early dose? After all, EU governments are already buying up millions of doses of Moderna’s still-largely-untested vaccine candidate.

Similarly, is it possible that Russian spies were simply monitoring the competition?

Who knows? When it comes to the shadowy world of espionage, the public rarely hears the full story. Russia’s outbreak has slowed in recent weeks as it has been overtaken by India, which now counts more than 1 million confirmed cases. Meanwhile Russia has confirmed more than 750,000 cases of Covid-19, the fourth-largest total in the world.

via ZeroHedge News https://ift.tt/2ZMJU33 Tyler Durden

20,000 Robinhood Traders Are In For Rude Surprise As CBL Prepares To File Chapter 11 Tyler Durden

Mon, 07/20/2020 – 05:30

Bloomberg reports mall operator CBL & Associates Properties Inc. is preparing to file for bankruptcy. The headline hit after hours on Friday, sinking shares by at least 20%.

Sources told Bloomberg the company “has been negotiating with its lenders in an effort to enter Chapter 11 with a consensual restructuring agreement in place…the plans aren’t final, and elements could change.”

CBL’s portfolio has 108 properties totaling 68.2 million square feet across 26 states. Many of the properties are classified as “Class B malls,” supported by a middle-market customer base that has been crushed by the virus-induced recession.

CBL fired a warning shot on June 5 and said tenants across 108 of its properties paid just 27% of April’s rent. The loss of rental income forced the mall operator to skip interest payments due on $3 billion in debt. On July 16, it entered forbearance agreements with debt-holders concerning 2023 and 2026 notes.

CBL bonds maturing in 2023 traded a bid/ask around 24.6 to 25.4 cents on Friday, according to the latest bond quotes via Refinitiv.

When CBL files, it would mark the largest commercial real estate bankruptcy of the pandemic. Thousands of stores are closing this year, further accelerating retail apocalypse, expected to be a record year.

Meanwhile, Robinhood daytraders, with no concern about the unprecedented surge in new CMBS delinquencies, have been panic buying CBL shares. From the start of lockdowns (mid-March), new account holdings surged from 8,000 to more than 20,000 on Friday, a 1.5x increase in four months.

Come Monday morning, thousands of Robinhood traders who panic bought, yet another bankrupt company, are going to be transformed into instant bagholders.

via ZeroHedge News https://ift.tt/2OD5QXS Tyler Durden

There is no solidarity without responsibility. The European Union Recovery Fund cannot be used as an excuse to perpetuate bloated political spending and create a transfer union where governments use taxpayers’ money to increase bureaucracy, because it would be the end of the European project. A union based on excess spending, debt and extractive policies would be destroyed in a few years. The strength of a unified group of countries comes from diversity and responsibility.

No one denies the challenges created by the Covid-19 crisis, but there are countries that have used the excuse of the pandemic to inflate political spending and now demand free money. The Spanish government has doubled the cost of government, maintained all the spending it increased during the growth period and increased the number of ministerial seats and advisors despite the crisis. Additionally, the government has approved a basic income plan that had no budget or fiscal space. There has been no management of costs whatsoever to allow budget room for automatic stabilizers, health, and unemployment costs. A government that increased the deficit in 2019 by 24% in a year of 2% GDP growth and record tax revenues has doubled the cost of government in the crisis and now demands no conditions or scrutiny from other member states.

Why would a serious government oppose a detailed scrutiny of the funds received? It should welcome it. Why would a government that calls itself reformist and states its commitment to budget stability reject any structural reform proposed by other member states? They should be implementing them now. Furthermore, why would a government that talks about an unprecedented emergency prefer to receive less funds than to accept the member states’ monitoring of grants? One could suspect that they are not aiming to use the funds in the most effective way.

These are important questions that need to be addressed in the European summit because this crisis cannot be solved if governments use the money of a recovery fund to perpetuate imbalances and squander resources for political purposes. If we want the EU to survive, it can only be based on competitiveness, trust and, most of all, credit responsibility.

If we want a united Europe we must listen more to the most dynamic countries and stop using the bureaucratic steamroller to turn all the member states into interventionist satellites.

The European Union faces a deep crisis. It cannot become a depression by using important funds that should boost competitiveness and strengthen the recovery to finance massive political transfer plans that serve as a political tool to keep bloated administration and political budgets.

The Spanish government has made serious mistakes in its objective of getting massive grants without conditionality.

The first one was not giving serious estimates of spending ceiling, deficit and debt for 2020 and not providing any for 2021 when Spain had already tested the patience of the European Commission in 2019 by missing an already revised deficit target in a period of record tax revenues.

The second mistake was assuming that Spain’s European partners were going to accept things that the Spanish government itself would not have accepted in different circumstances. Everyone knows that the government of Spain would have refused an unconditional fund if it had been only for another country, since it would mean a greater contribution to the EU budget, and a greater deficit for Spain. We know this because it was exactly the Spanish government’s position in the Greek crisis, when Prime Minister Zapatero stated that the Greek opposition parties should agree to the agenda of reforms in order to receive bailout funds (24th June 2011, La Vanguardia). It is easy to demand solidarity when you are the recipient of it.

Third mistake: It is not convenient to demand from the most responsible countries free money when the government goes to the negotiation table having missed the 2019 deficit target in a year of record tax revenues, with the largest deficit in the eurozone in 2020, being the only country that has not reduced non-essential expenses to accommodate the increase in health spending and with the most expensive government, with more ministers and higher officials in four decades.

The fourth error: It is also not easy to convince others to provide tens of billions of euros, unconditionally and with greater weight of subsidies when Spain has in the government coalition a party that has voted in Europe in favour of breaking the euro and whose leaders, including a vice president and two ministers, defended a massive default on the debt.

Podemos and Izquierda Unida voted on December 14, 2015 an amendment proposing “facilitating withdrawal mechanisms” from the monetary union and “an alternative plan for an orderly break-up of the euro area” and have never withdrawn or modified it.

The final and fifth mistake: The Spanish Government constantly repeats that the economy is recovering in a V-shape and that they will not cut any spending under any circumstance, just implement massive tax hikes that will erode competitiveness, growth, job creation, tax revenues and increase future deficit and debt. At the same time, they demand donations with no conditions.

Many Spanish and European citizens like me are more than happy to commit to a strong set of reforms to improve competitiveness and boost economic growth and jobs. We do not want funds to be squandered in political spending.

The failure to approve a no-condition all-grant recovery fund is not a European failure. It is the confirmation that the European project will only be strengthened if it becomes a union where solidarity is given with responsibility and where strength comes from the prudent management of so-called “frugal” – or rather, responsible – leaders.

There will be a Recovery Fund, it will have conditions and it will be good for all if it does. However, the Recovery Fund is not the solution for many European states’ structural problems. Structural reforms must be adopted to solve the long-term imbalances of European economies and conditionality should be viewed as a positive, not a negative. If countries want to show to the world that they are reliable partners committed to budgetary stability, reforms must be embraced, not rejected.

via ZeroHedge News https://ift.tt/2WEjD4R Tyler Durden

Class 8 Orders 'Dead Cat Bounce' 2 Months After Hitting Their Lowest Level In 25 Years Tyler Durden

Mon, 07/20/2020 – 04:15

Class 8 trucking orders – often seen as a gauge of how the U.S. production economy is faring, have been brutalized for almost all of 2020 so far due to the ongoing pandemic. But June’s data appears to suggest a slight respite in orders, despite crashing retail sales, even though we’re not quite certain that it’s going to carry into the second half of the year.

Regardless, June is traditionally a tough month for Class 8 orders and the industry (and its analysts) are optimistic.

Final Class 8 truck data for June has been released and retail sales were down 41% YoY to 17,055 units. Orders were up 23.2% for the month, marking a small bounce back for the industry.

This comes after two incredible poor months that we highlighted (ZH Class 8 report April, ZH Class 8 report May) where orders hit their lowest level in 25 years. In May, new orders “recovered” slightly to a dismal 6,687 number before taking off this June.

Regardless, Class 8 orders remain down 24.7% YTD, mostly as a result of a continued lagging economy and pressured supply chain due to the coronavirus pandemic. In the first half of 2020, 65,814 trucks were ordered, compared with 87,466 in the first half of 2019.

Retail sales are also lagging YTD, still down 39%, according to data from JP Morgan. Builds have appears to make somewhat of a V-shape recovery, but were down 39% YoY in June and have fallen 70% in Q2. Builds remain down 52% year to date.

But that hasn’t stopped the industry’s perpetually bullish analysts, who weigh in on the numbers every month and – somehow – can find the positive in almost the most dismal of reports.

Don Ake, FTR’s vice president of Commercial Vehicles said: “The Class 8 market is on the slow, steady recovery that matches our forecast. It is also encouraging that fleets are showing enough confidence in the economy to begin placing some viable orders. The trend should continue, but a significant increase is not expected until October when the big fleets begin placing orders for 2021 delivery.”

He continued: “June’s order activity is good news, after last month’s disappointing number. We expected orders to average around 10,000 units for a few months. Now they have averaged 11,000 for the past two months.”

Kenny Vieth, ACT president and senior analyst commented: “North American Class 8 net orders were up against an easy year-ago comparison, when orders were under pressure from still large backlogs and rising equipment overcapacity.”

ISM New Orders Index posted its strongest jump on record (up 24.6pts MoM) to 56.4 in June, up 11.7% YoY to its highest level since January 2019, JP Morgan noted.

JP Morgan is still, however, forecasting Class 8 builds of ~165,000 (down 52%) for the year.

via ZeroHedge News https://ift.tt/30tzrIL Tyler Durden

The current fiat international monetary system is ending—unconventional monetary policy has entered a dead end street and can’t reverse. I have written about this before, and will not repeat this message in today’s article. Instead, we will discuss a topic that deserves more attention, namely that European central banks saw this coming decades ago when the world shifted to a pure paper money standard. Accordingly, European central banks have carefully prepared a new monetary system based on gold.

When the last vestige of the gold standard was terminated by the U.S. in 1971, circumstances forced European central banks go along with the dollar hegemony, for the time being. Sentiment in Europe, however, was to counter dollar dominance and slowly prepare a new arrangement. Currently, central banks in Europe are signaling that a new system that incorporates gold is approaching.

If you want to read a summary of this article you can skip to the conclusion.

Contents:

The Rise and Fall of Bretton Woods

Europe Equalizes Gold Reserves Internationally

Private Gold Ownership Distribution

Setting the Stage for a Gold Standard

Conclusion

Sources

The Rise and Fall of Bretton Woods

At the end of the Second World War, a new international monetary system called Bretton Woods was ratified. Under Bretton Woods, the U.S. dollar was officially the world reserve currency, backed by gold at a parity of $35 per ounce. The United States owned 60% of all monetary gold—more than 18,000 tonnes—and promised the dollar to be “as good as gold.” All other participating countries committed to peg their currencies to the dollar. Bretton Woods was a typical gold exchange standard.

It didn’t take long for the U.S. to print and export more dollars than it had gold backing them, which raised concern about the parity of $35 dollars per ounce. As a consequence, foreign central banks started redeeming dollars for gold at the U.S. Treasury. The vast gold reserves of the U.S. began flowing out and ended up mainly in Western Europe.

In an attempt to stabilize the international monetary system, a consortium of eight Western central banks set up the London Gold Pool in 1961 to keep the gold price in the free market at $35. Despite being a member of the Pool, France—that was very critical of U.S. monetary policy—repeatedly redeemed dollars at the Treasury. France thus bought gold at the Treasury, to sell in the free market through the Pool.

In 1965 pressure on the dollar increased and the Pool had to supply huge amounts of gold to sustain the peg. European central bankers started deliberating how to get out of the Pool agreement. Europe didn’t want to defend the peg indefinitely for what was in essence a problem caused by the United States. In 1967 the British pound devalued, which injured confidence in the entire system and France withdrew from the Pool. The situation escalated quickly. Famous gold author Timothy Green writes in The New World of Gold (1982):

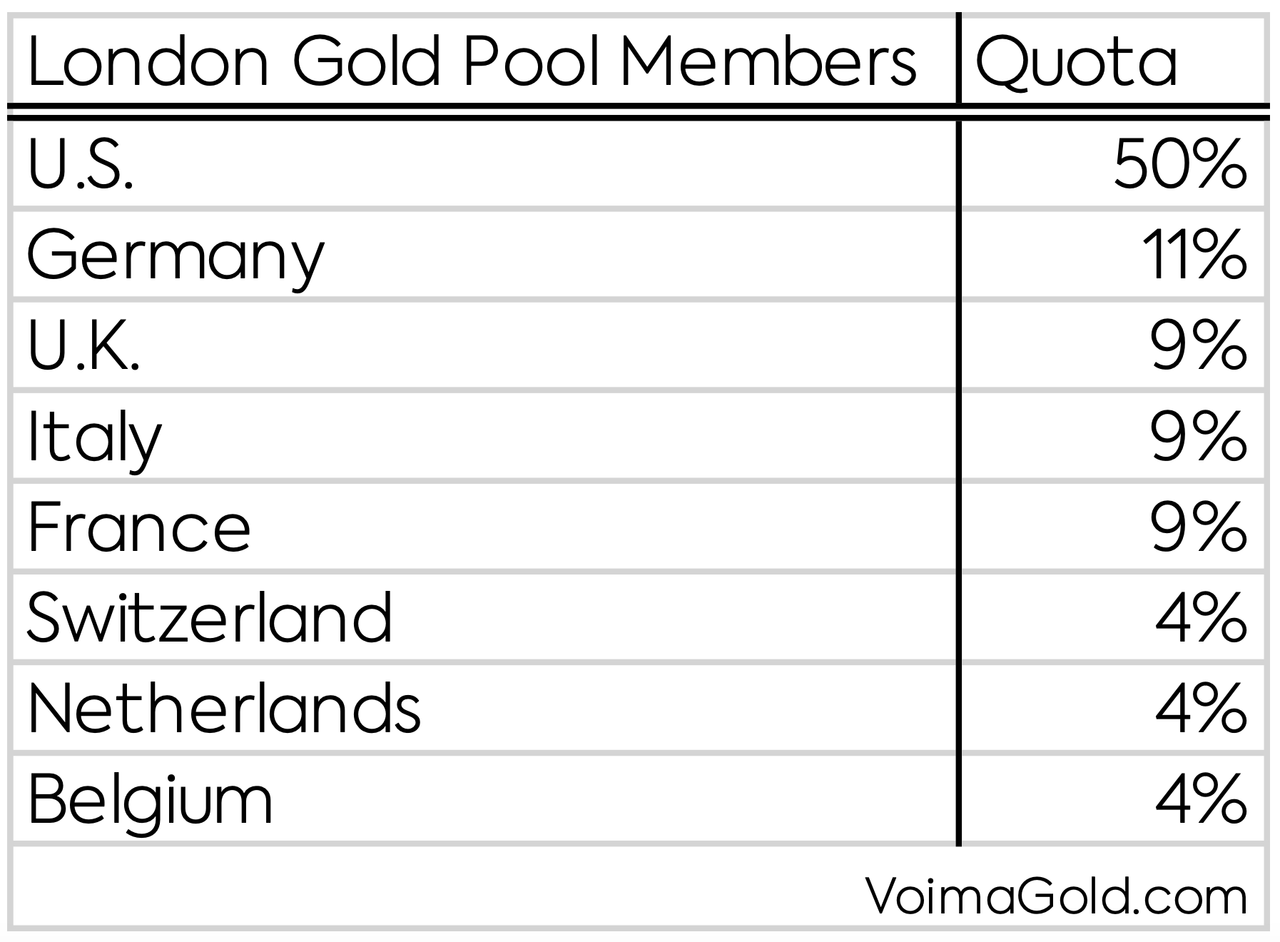

Could $35 gold be maintained? The gold pool, except for France (under de Gaulle who shrewdly opted out), thought it could. They had nearly twenty-four thousand tons of gold at their disposal. And William McChesney Martin of the Federal Reserve Board rashly said they would defend the $35 price “to the last ingot.” But the Tet offensive in Vietnam crushed that pledge. Between March 8 and March 15, 1968, the pool had to provide nearly one thousand tons to hold the price at the fix. U.S. air force planes rushed more and more Fort Knox gold to London, and so much piled up in the Bank Of England’s weighing room that the floor collapsed.

On March 15, 1968, the Pool ceased its operations and the gold price in the free market was allowed to float. Though central banks agreed to keep trading gold among each other at $35 and not buy and sell in the free market. A “two-tier gold market” had emerged.

Foreign central banks could still redeem dollars at the Treasury—at the official gold price that was lower than the free market price—but it was seen as “unfriendly.” Early August, 1971, France, again, sent a battleship to New York to load up on gold in exchange for dollars. A few days later, on August 15, the United States unilaterally decided to end Bretton Woods by suspending dollar convertibility. Europe, Japan, and other countries, were not amused. Dollar reserves, previously backed by gold, had turned into pieces of paper plummeting in value against gold. What followed was a diplomatic conflict between Europe and the U.S.

Since the 1960s, America seduced foreign central banks to reinvest their dollar reserves in U.S. government bonds (Treasuries), instead of redeeming them for gold. If Treasuries would replace gold in the international monetary system, the United States could continue to print money for imports, and have savers abroad finance their fiscal deficits. Such a dollar standard would yield the U.S. unprecedented power, though it wouldn’t be an equitable system.

One of the reasons the euro was created was to counter dollar dominance. Many decades before it was launched, Western Europe started to integrate. The first seed was the Treaty of Rome in 1957 that gave birth to the European Economic Community (EEC). From classified documents that have been released in recent years, we know the U.S. opposed monetary cooperation in Europe, for the simple reason it didn’t want competition for the dollar hegemony. Below are excerpts from a telephone call between U.S. National Security Advisor, Henry Kissinger, and Deputy Secretary of the Treasury, William Simon, on March 14, 1973.

Kissinger: … I basically have only one view right now which is to do as much as we can to prevent a united European position without showing our hand. … I don’t think a unified European monetary system is in our interest.

… You understand, my reason’s entirely political, but I got an intelligence report of the discussions in the German Cabinet and when it became clear to me that all our enemies were for the European solution that pretty well decided me.

The “European solution” was to fix the exchange rates of the EEC’s currencies, and float as a bloc against the dollar. The “common float” would enhance trade within Europe and show the world Europe’s unity and leadership. This was not in the interest of the U.S. According to Under Secretary of the Treasury for Monetary Affairs, Paul Volcker, the European solution was a euphemism for saying: “Let’s leave the United States out of the world and go our independent course.”

Furthermore, the EEC took the stance that central banks should be able to buy and sell gold at a market-related price, both among themselves and on the free market. Also, in 1973 the EEC publicly stated in the New York Times: “[Europe] will promote agreement on international monetary reform to achieve an equitable and durable system taking into account the interests of the developing countries.” This statement can be traced to what Georges Pompidou, President of France, said in a meeting with Richard Nixon, President of the U.S., in 1970: “Power thus established never lasts long. The existence of more centers of economic and political power makes things more complicated but in the longer term has greater advantages.” France’s view was that if there were more centers of economic and political power, the world would be more stable.

The U.S. opposed the end of the two-tier system, because this would increase the official price of gold and put it back in the center of the international monetary system. America pushed for “phasing gold out of the international monetary system,” all the more because Europe was holding more gold than the U.S. since the 1960s.

A historic document that pointedly illustrates the aforementioned dynamics is, “Minutes of Secretary of State Kissinger’s Principals and Regionals Staff Meeting, Washington, April 25, 1974”. From the American meeting in 1974:

Mr. Enders: … It’s been in the newspapers now—the EC [EuropeanCommunity] proposal.

Secretary Kissinger: On what—revaluing their gold?

Mr. Enders: Revaluing their gold—in the individual transaction between the central banks [meaning the end of the two-tier system].

Mr. Enders: Arthur Burns—I talked to him last night on it, and he didn’t define a general view yet. He was unwilling to do so. He said he wanted to look more closely on the proposal. Henry Wallich, the international affairs man, this morning indicated he would probably adopt the traditional position that we should be for phasing gold out of the international monetary system; but he wanted to have another look at it.

Secretary Kissinger: … my understanding of this proposal would be that they—by opening it up to other countries, they’re in effect putting gold back into the system at a higher price.

Mr. Enders: Correct.

Secretary Kissinger: Now, that’s what we have consistently opposed.

Mr. Enders: Yes, we have. You have convertibility if they—

Secretary Kissinger: Yes.

Mr. Enders: Both parties have to agree to this. But it slides towards and would result, within two or three years, in putting gold back into the centerpiece of the system—one. Two—at a much higher price. Three—at a price that could be determined by a few central bankers in deals among themselves.

…

Secretary Kissinger: Why are we so eager to get gold out of the system?

Mr. Enders: It’s against our interest to have gold in the system because for it to remain there it would result in it being evaluated periodically. Although we have still some substantial gold holdings—about 11 billion [USD]—a larger part of the official gold in the world is concentrated in Western Europe. This gives them the dominant position in world reserves and the dominant means of creating reserves. We’ve been trying to get away from that into a system in which we can control—

Secretary Kissinger: But that’s a balance of payments problem.

Mr. Enders: Yes, but it’s a question of who has the most leverage internationally. If they have the reserve-creating instrument, by having the largest amount of gold and the ability to change its price periodically, they have a position relative to ours of considerable power.

…

Secretary Kissinger: O.K. My instinct is to oppose it. What’s your view, … Ken?

[Ken] Rush: Well, I think probably I do. The question is: Suppose they go ahead on their own anyway. What then?

Secretary Kissinger: We’ll bust them.

Mr. Enders: I think we should look very hard then, Ken, at very substantial sales of gold—U.S. gold on the market—to raid the gold market once and for all.

The above goes to show the distaste of the U.S. with respect to gold, and their ambition to maintain the dollar hegemony.

For informative comments by Arthur Burns we will turn to a “Memorandum For The President” he wrote on June, 3, 1975. From Burns:

… removal of the present restraints on inter-governmental gold transactions and on official purchases from the private market [meaning the end of the two-tier system] could well release forces and induce actions that would increase the relative importance of gold in the monetary system. In fact, there are reasons for believing that the French, with some support from one or two smaller countries, are seeking such an outcome.

…

It is an open secret among central bankers that, at a later date, the French and some others may well want to stabilize the market [gold] price within some range.

All in all, I am convinced that by far the best position for us to take at this time is to resist arrangements that provide wide latitude for central banks and governments to purchase gold at a market-related price.

The French, and some of its allies, wanted gold’s importance to increase in the international monetary system and stabilize its price “at a later date.” Which boils down to a gold standard. The Federal Reserve favored a continuation of the two-tier market, which in practice meant gold’s demonetization.

Finally, the EMS may also turn out to be a first step toward rehabilitating gold as an integral part of the international monetary system.

In 1998 the EMS was annulled and replaced by the Eurosystem.

Although France, and some other European countries, were surely in favor of gold and against the dollar hegemony in the 1970s, I don’t know if this group had a solid plan from the start. Perhaps, they had a direction in mind and adjusted their policies throughout the years.

The U.S. never did “raid the gold market once and for all.” They sold roughly 500 tonnes in the late 1970s and 1980s in an attempt to lower the price in the free market. Gold traded more or less sideways throughout in the 1980s and 1990s, but didn’t get phased out of the international monetary system. However, the Americans succeeded in imposing the paper dollar standard on the world. There was a lot of discussion in the 1970s about the Special Drawing Right (SDR), a reserve asset issued by the International Monetary Fund, but it didn’t function (and still doesn’t). The U.S. could continue to print and export dollars, and Treasuries became the main international reserve asset. As a result, the U.S. has been running a trade and fiscal deficit since 1971.

Europe Equalizes Gold Reserves Internationally

As mentioned, Europe preferred a new “equitable and durable system taking into account the interests of the developing countries,” and France, supported by allies, was aiming for something of a gold standard “at a later date.” Remarkably, what I discovered is that European central banks started selling gold in the 1990s to equalize their gold reserves relative to other nations. A new gold standard would be equitable if all gold was distributed evenly, which is what European central banks have been managing.

After the Great Financial Crisis (GFC) in 2008, the Minister of Finance of the Netherlands, Jan Kees de Jager, was asked in parliament for the main reason why the Dutch central bank had sold 1,100 tonnes of gold since 1993, and if storage costs had been a motivation. His answer:

Through gold sales in the past, the Dutch central bank brought its relative gold holdings more in line with other important gold holding nations. Storage costs didn’t play any part in the decision to sell gold…

At the time DNB [Dutch central bank] determined that from an international perspective it owned a lot of gold proportionally.

Another question directed at de Jager, was if he could confirm if other nations—in contrast to the Netherlands—had increased their official gold reserves in the past years. His answer:

The buyers are developing nations whose international reserves are growing, or historically have a small gold stock.

According to de Jager, the Dutch central bank sold gold to equalize reserves internationally. He mentioned no other reason for the sales. (De Jager denied the Dutch central bank sold gold for paying off the national debt of the Netherlands, which is a frequently mentioned reason for European gold sales.) In addition, Dutch newspaper NRC Handelsblad reported in 1993 that the Dutch central bank had sold 400 tonnes through the Bank for International Settlement, and this was partially bought by the Chinese central bank. I conclude that the Netherlands sold 1,100 tonnes to help developing nations get equal in terms of gold reserves proportionally and prepare for a new monetary system that incorporates gold. Why else—than to reposition gold in the international monetary system—would the Netherlands want to equalize their gold reserves with other “important gold holding nations”?

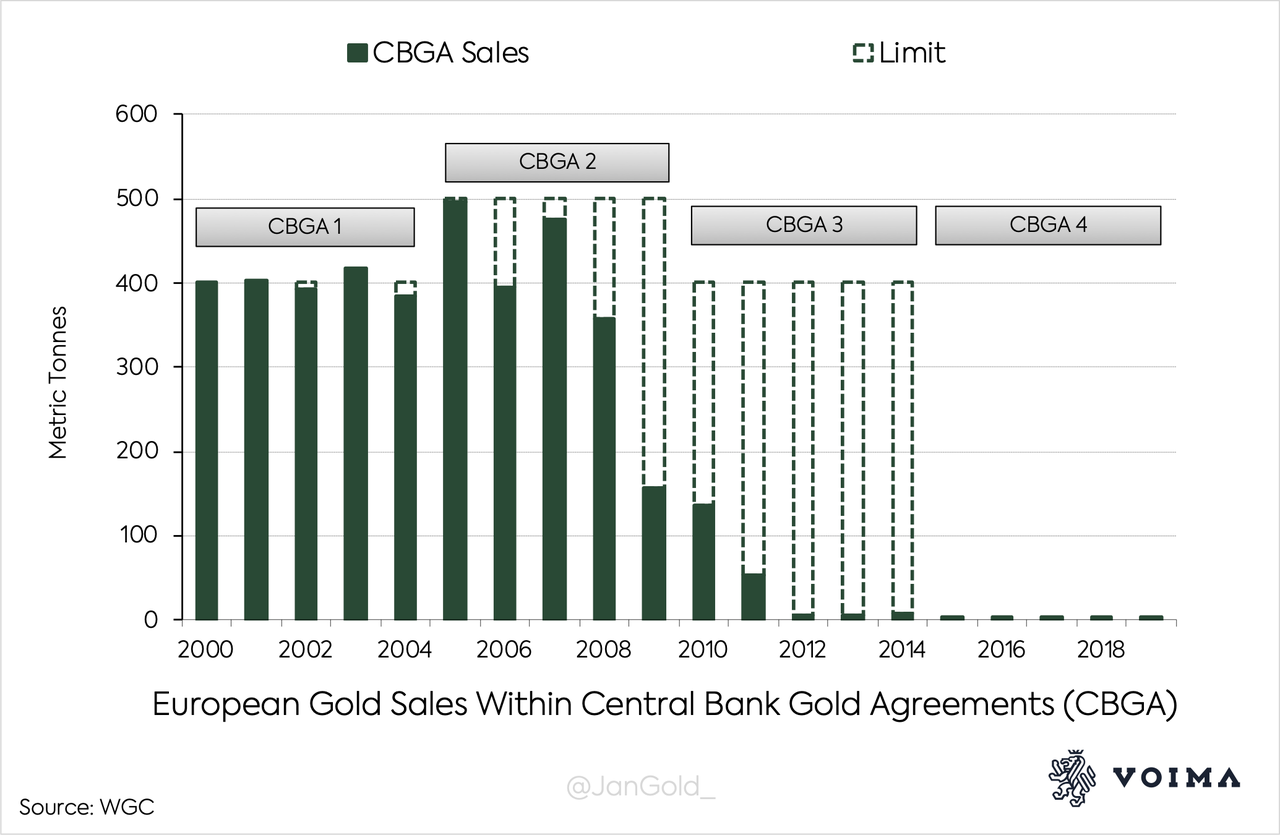

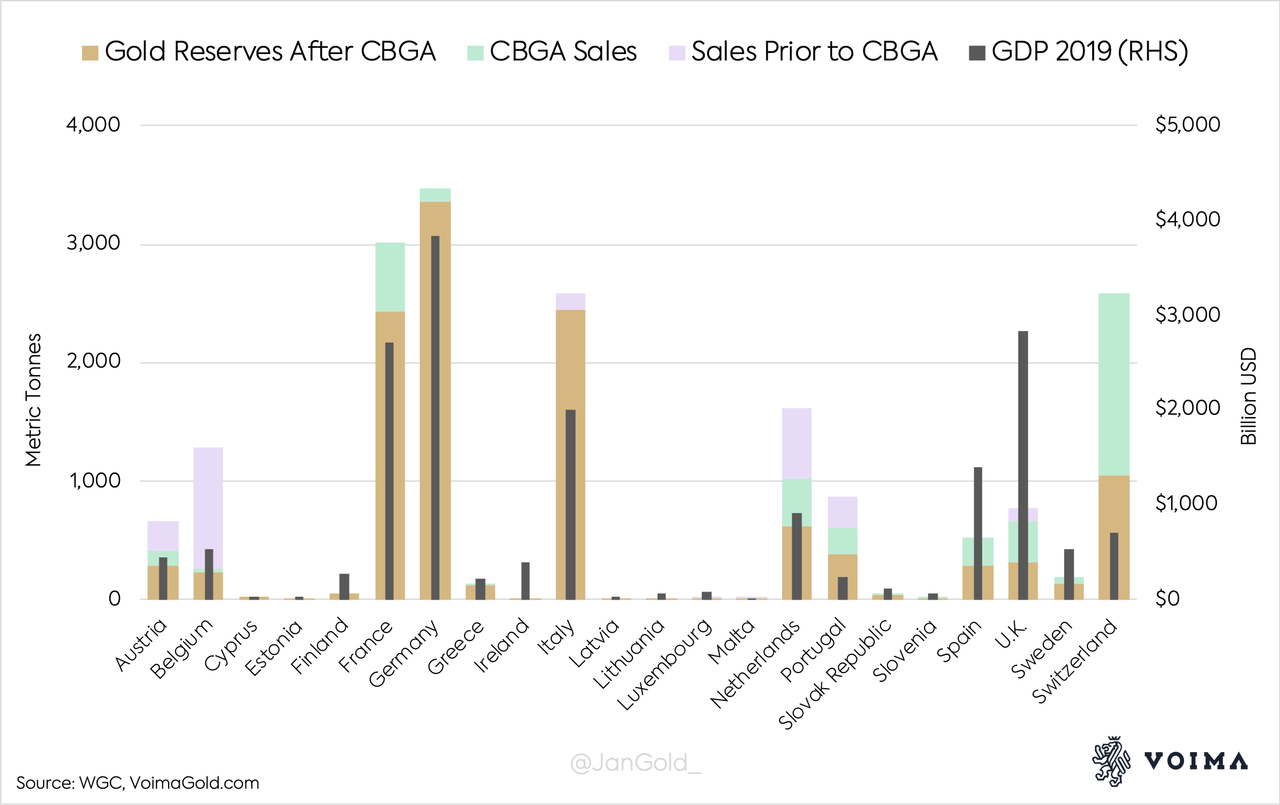

Other central banks in Europe have done the same as the Dutch central bank. In 1999, fourteen (Western) European central banks surprised the gold market with a statement regarding a “concerted programme of [gold] sales over the next five years.” The program was dubbed the Central Bank Gold Agreements (CBGA), and the signatories declared:

Gold will remain an important element of global monetary reserves. … Annual [aggregated] sales will not exceed approximately 400 tons and total sales over this period will not exceed 2,000 tons. … This agreement will be reviewed after five years.

Gold sales were tightly coordinated. In the knowledge Europe wanted to balance gold reserves internationally (more proof below) this statement makes perfect sense.

The World Gold Council interpreted CBGA as removing “concern that uncoordinated central bank gold sales were destabilising the market, driving the gold price sharply down.” It’s true that some European countries sold significant amounts of gold before CBGA, which drove the price down, and right after CBGA was announced the gold price started to rise. Mission accomplished, I would say.

Eventually, CBGA was extended three times, and ten more European countries joined. During CBGA 1-4 a little over 4,000 tonnes were sold, virtually all of which before 2009.

One of the members of Voima Gold’s Advisory Board is Pentti Pikkarainen, who was Head of Banking Operations at the central bank of Finland—one of the signatories of CBGA—from 2001 until 2010. When I asked Pikkarainen if in addition to the Dutch central bank, others had sold to bring their “relative gold holdings more in line with other important gold holding nations” as well, he answered:

It is true that some central banks compared their gold holdings with those of other central banks and came to that type of conclusion.

So,multiple central banks in Europe sold gold to equalize reserves internationally.

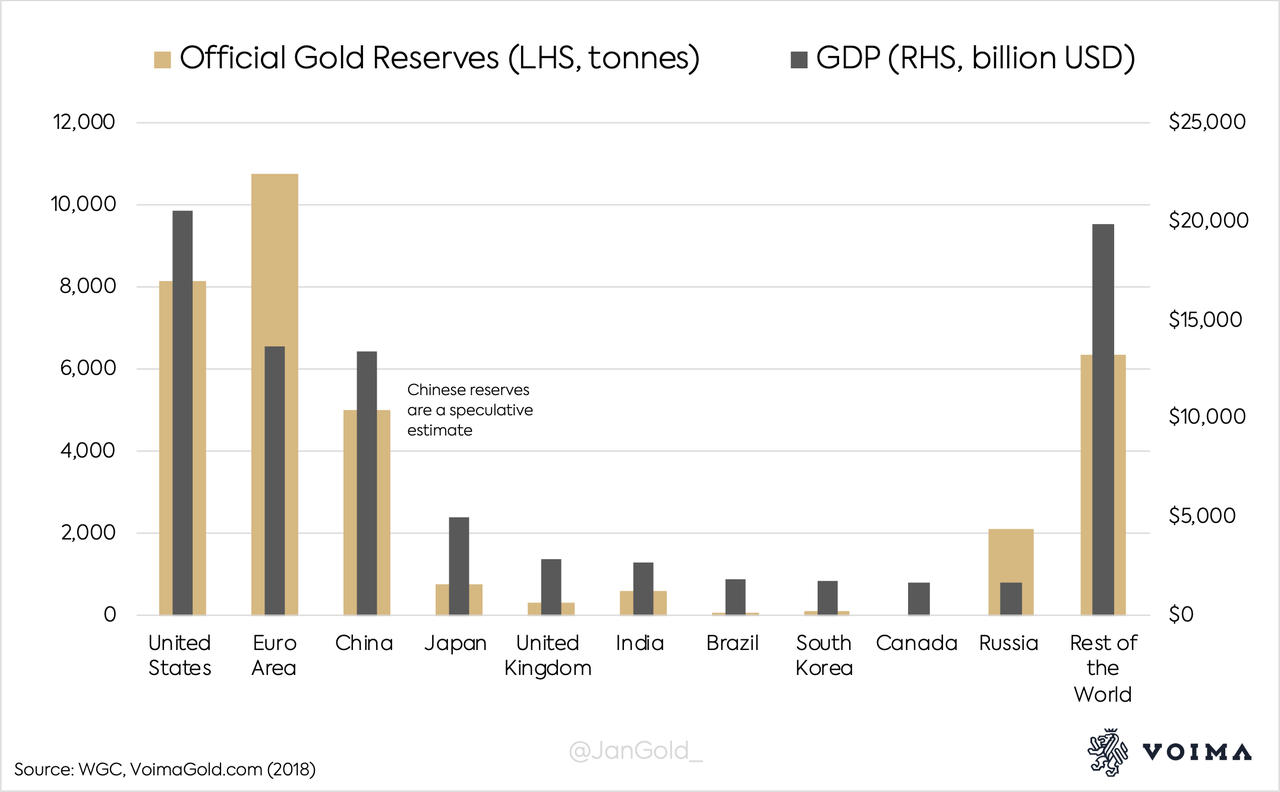

To get a sense of the equalization process within Europe, I have made a chart showing gold sales per country before and during CBGA, current gold reserves, and Gross Domestic Product (GDP).

Before and during CBGA, mainly medium sized economies sold gold to have an equal share relative to others. It’s not a perfect fit, but striking nonetheless. Still more, because Cyprus, Estonia, Italy, and Lithuania were signatories of CBGA, but didn’t sell an ounce of gold during the “concerted programme of sales.” Finland and Ireland were buyers during CBGA, albeit of small weights, which makes sense when comparing reserves across the board. It appears CBGA was not a concerted programme of gold sales, but a concerted programme of equalizing gold reserves. The main outlier is the U.K.

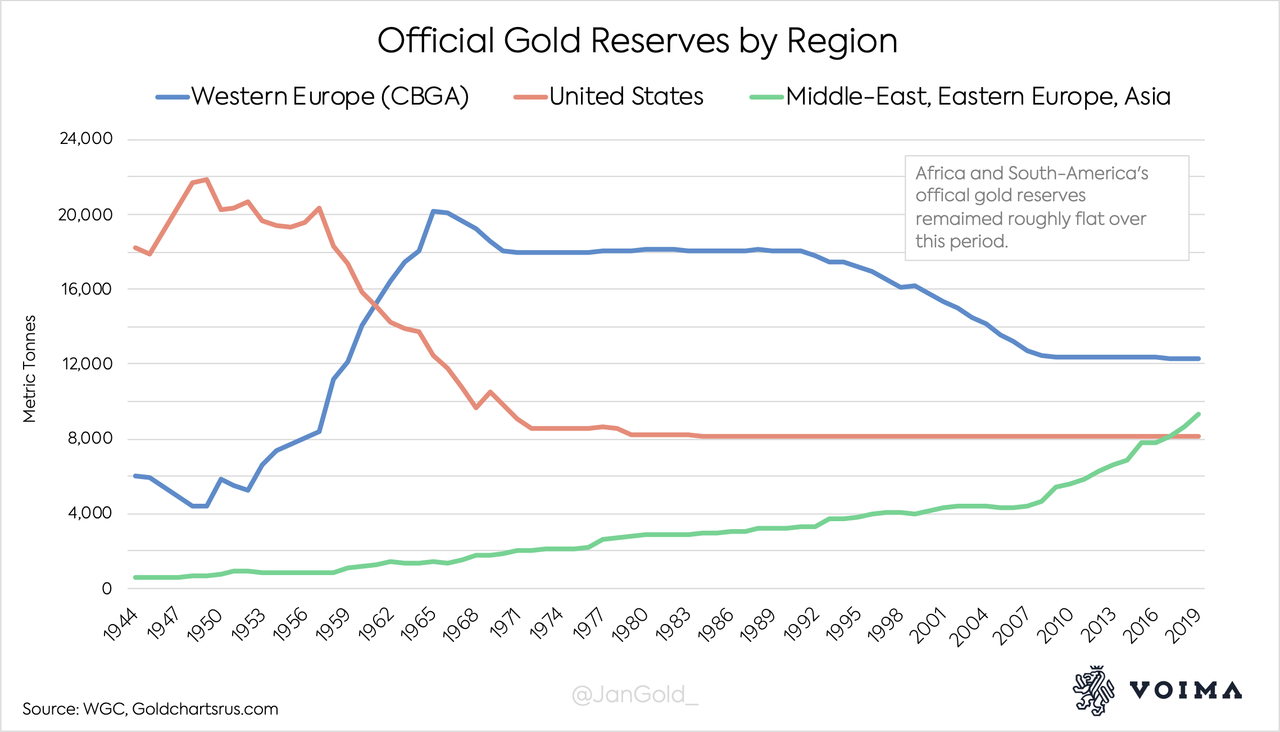

Official gold reserves around the world are spread more evenly since the 1970s. Eurasia minus Western Europe held 2,000 tonnes in 1971, versus 9,300 tonnes currently.

The equalization process continues until this day. In 2018, the central bank of Hungary (MNB) purchased 31.5 tonnes of gold, a tenfold in their official reserves. MNB disclosed it bought gold because “it may play a stabilising role … in times of structural changes in the international financial system,” but also to bring their gold reserves more in line to its peers. The Polish central bank (NBP) bought 125.7 tonnes in 2019 and stated the same:

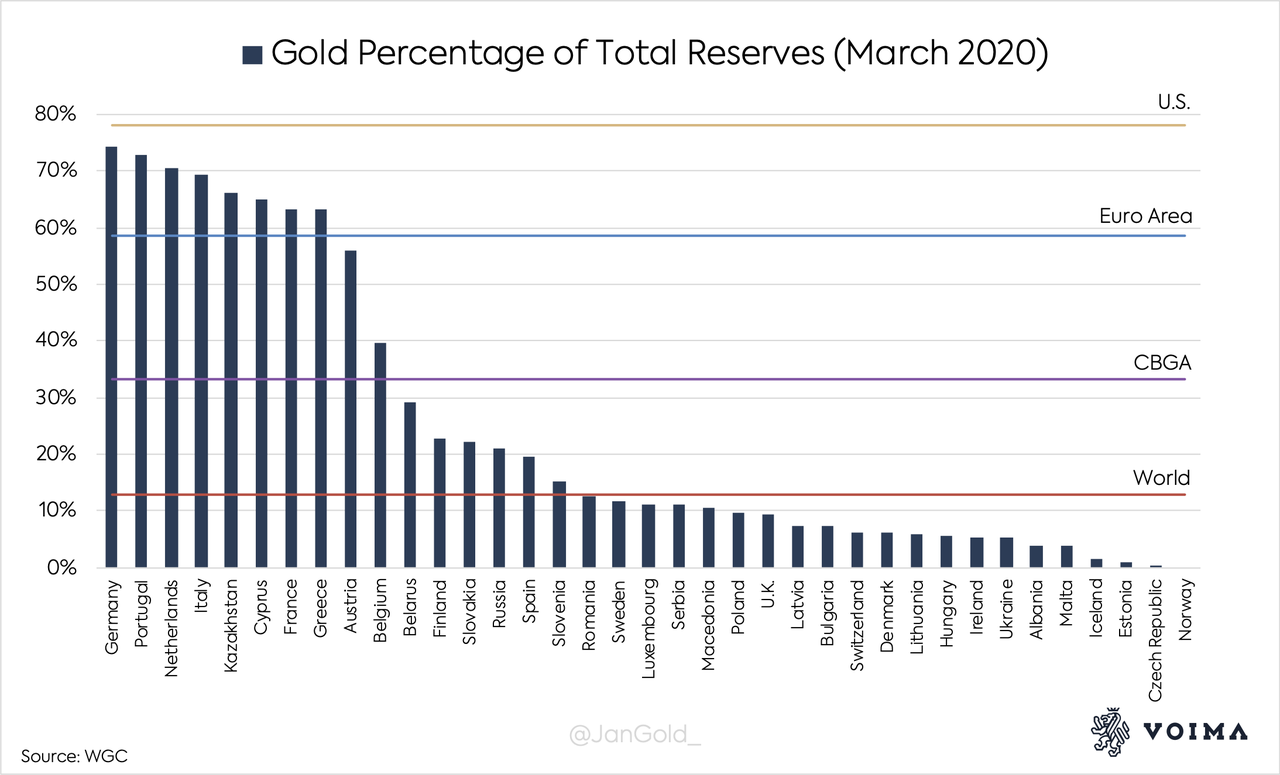

the share of gold in NBP foreign exchange reserves was below the average for all central banks (10.5%) and significantly below the average in European countries (20.5%). The purchase of gold allowed not only to increase the strategic financial buffer of the country, but also to bring the NBP closer in terms of the share of gold in foreign exchange reserves to the average of all central banks (10.5%).

We undoubtedly read about preparing for a change in the international financial system, and balancing gold reserves proportionally. I’m aware de Jager, MNB, and NBP talk about leveling “gold reserves as a percentage of total reserves,” but I see a more significant pattern in gold reserves versus GDP. To be complete, below is a chart showing official gold reserves as a percentage of total reserves (foreign exchange, gold, and SDRs) for European countries.

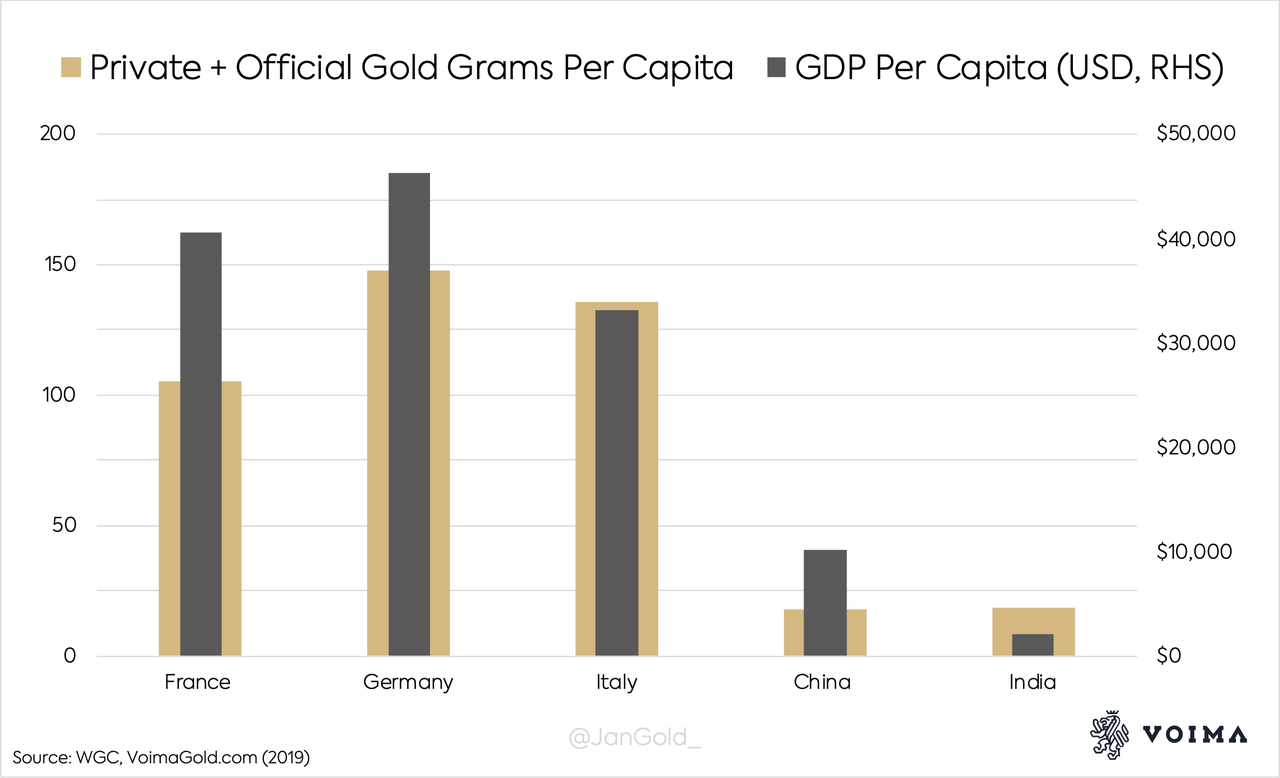

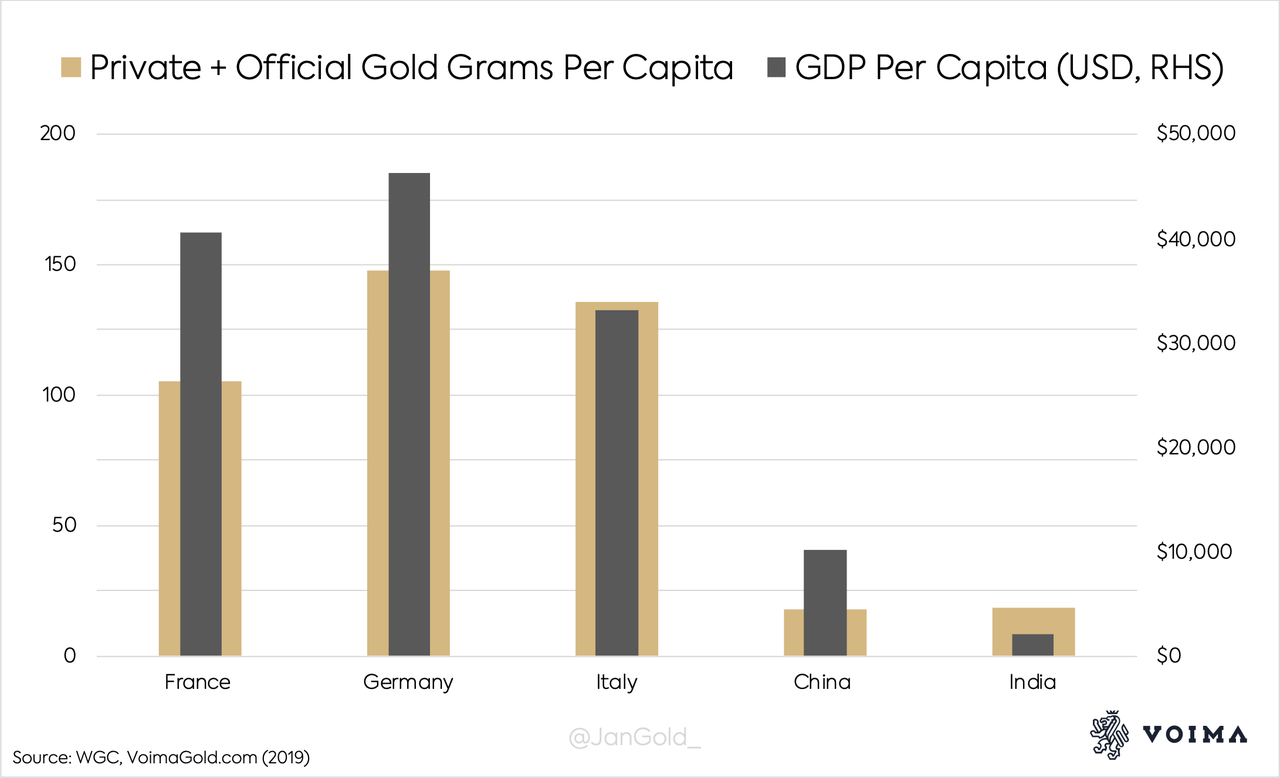

Private Gold Ownership Distribution

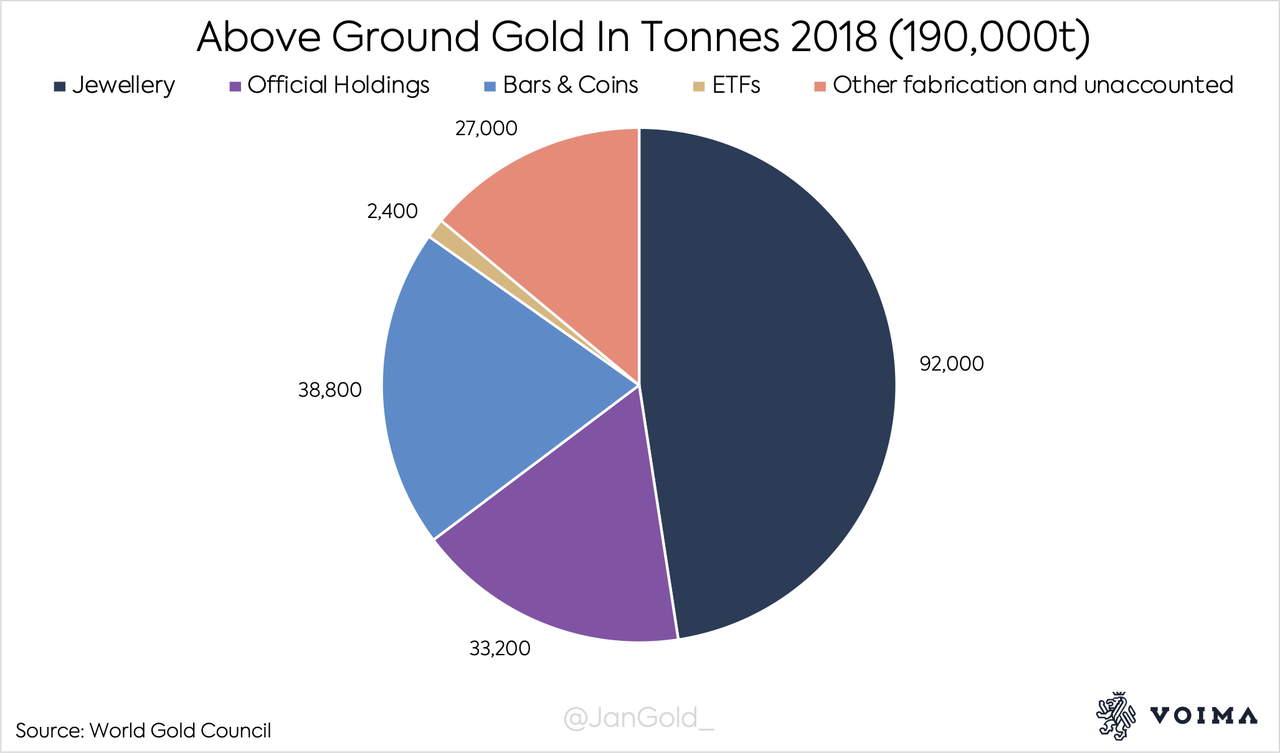

Private gold holdings make up a larger portion of total above ground stocks than official holdings, but it’s a lot harder to localize. Although the data is limited, private gold distribution shows to be roughly equal for “important gold holding nations.” (Of course, it can never be exactly equal.)

Official gold reserves make up less than 20% of total above ground reserves.

When the Chinese Communist Party (CCP) took control over China in 1949 it effectively banned the private use of gold. Since the 1980s, Chinese citizens were slowly allowed to buy gold jewelry, and in 2002 the Chinese gold market was fully liberalized with the launch of the Shanghai Gold Exchange. Gradually, the CCP began stimulating its citizens to accumulate gold. In 2012, President of the China Gold Association, Sun Zhaoxue, elaborated on the importance of private gold ownership in the leading academic journal of the CCP’s Central Committee, Qiushi:

Practice shows that gold possession by citizens is an effective supplement to national reserves and is very important to national financial security. … We should advocate to ‘store gold among the people’ …

A year later Sun made a statement in the Wall Street Journalon how much gold Chinese people own on average:

Meanwhile, the average Chinese person “only holds 4.5gram of gold,” Mr. Sun said. “That is far below an average of 24 grams per person globally …

The Chinese government aims to elevate the amount of private gold per capita, to bring it more in line to the global average. China’s gold strategy matches Europe’s gold strategy in terms of equalizing reserves (next to the obvious reasons to own gold in the first place).

From previous research, I know approximately how much private gold is in India, China, France, Italy, and Germany. When I combine the private and official gold reserves of these countries, and compare it to GDP per capita, these measures appear to be quite close to each other.

The amount of gold each citizen owns on average, directly and via their central bank, is roughly equal to their economic income. At a gold price of about $10,000 dollars per ounce, that is. The biggest difference is between China and India.

For China’s official gold reserves I have used a speculative estimate of 5,000 tonnes. According to my calculations China currently is at 18 grams of gold per capita.

It goes without saying that partially the gold distribution in recent decades has been organic.

The story of China and gold goes back further than many people think. On the website of Bank of China—a state owned bank—we can read:

From 1973 to 1974, Vice Premier Chen Yun … carried out special research on foreign trade issues. On June 7, 1973, when listening to a bank report, Vice Premier Chen Yun raised ten important questions in international economy and finance, … The ten research topics assigned by Chen Yun covered economy, finance, currency and other important aspects in the contemporary capitalist world, which were:

(1) How much money was issued in the U.S., Japan, UK, Federal Republic of Germany and France from 1969 to 1973? How much were their foreign currency reserves and gold reserves?

…