Trump Threatens “Very Strong Reaction” If Beijing “Interferes” With Hong Kong Tyler Durden

Thu, 05/21/2020 – 13:00

Did President Trump just crank the belligerent rhetoric up to ’11’?

During a briefing with reporters, President Trump answered questions about the MSM fixations du jour, including his feelings on mail-in ballots and his current COVID-19 infection status (still negative). But amid the fluff, one reporter asked an important question referencing Thursday’s decision to adopt a new “national security” resolution opening the door to new laws allowing Beijing to punish political dissidents with impunity.

Trump replied that if this happens, the US would respond with a “very strong reaction.” You’ll remember that last year, President Xi warned in a speech that any foreign powers who screwed with China’s relationship with Hong Kong and Taiwan would face serious consequences.

TRUMP, ASKED ABOUT CHINA’S MOVE ON HONG KONG, SAYS IF IT HAPPENS U.S. WILL HAVE A VERY STRONG REACTION

A few hours ago, Chinese tech giant Baidu became the first major Chinese company to delist from an American exchange (it de-listed from the Nasdaq) in retaliation against a bill passed by the Senate that would require Chinese companies to submit to certain auditing conditions that Beijing currently resists, for dubious reasons.

With the WHA agreeing to an “independent” investigation of China’s early response to the coronavirus, and President Trump embracing increasingly belligerent rhetoric as his administration pins its reelection hopes on vilifying China as an ascendant American foe that effectively – even if inadvertently – unleashed a potent biological weapon on the world, investors including David Tepper have said they see a tail risk of an armed conflict between the world’s two largest economies.

Fortunately for the Fed, investors haven’t really woken up the possibility yet.

via ZeroHedge News https://ift.tt/36v3Hpv Tyler Durden

Alex Jones exclusively revealed Thursday that Joe Rogan signed an exclusivity contract for his podcast with Spotify as a way of striking back against YouTube censorship.

Jones, who has been friends with Rogan for 22 years, spoke at length with the podcast king, with Rogan telling him that he should announce to the world that the move is a direct strike against Google, that the “gloves are off” and he is “going to war” against big tech tyranny.

Jones told his audience that Rogan had encouraged him to go on air and “put it all out there.”

The deal, suggested to be worth $100 million was announced earlier this week. Analysts are saying that it will change the face of media forever.

Jones, who has appeared on The Joe Rogan Experience numerous times, also announced that Rogan had specifically requested in his contract with Spotify that the Infowars host will be allowed to appear uncensored on the podcast on Spotify.

Jones said Rogan wants him as the first guest on the show when it arrives on Spotify on the 1st of September, followed by Elon Musk, who is also currently speaking out against big tech censorship and cancel culture.

Jones said Rogan told him he is sick of being treated poorly by Google, and the straw that broke the camel’s back was that Rogan wanted to interview doctors and experts who have differing opinions on the coronavirus to the officially sanctioned narrative, and was told by YouTube that they would not allow such content on their platform.

Rogan also told Jones that the lockdown has provided him more clarity on the situation.

Rogan has noted on his podcast that YouTube is consistently demonetising his content and removing videos. He told Jones that he sees it not only as ‘un-American’, but also ‘anti-human’.

An excited Jones descried the move by Rogan as “peak internet”.

Rogan’s podcast was downloaded 190 million times per month last year. His YouTube channel has 8.42 million subscribers, and the move away is sure to be a huge strike against big tech thought control.

via ZeroHedge News https://ift.tt/2A2oy75 Tyler Durden

Trump In ‘Desperate Effort To Steal Election’ By Opposing Vote-By-Mail, Says DNC’s Perez Tyler Durden

Thu, 05/21/2020 – 12:30

President Trump is ‘in a desperate effort to steal an election’ by opposing vote-by-mail during the coronavirus pandemic, according to Democratic National Committee chairman Tom Perez.

In a Wednesday appearance on MSNBC, host Chris Hayes referenced recent comments and tweets by Trump attacking vote-by-mail, saying: “For more on the president’s efforts to subvert the democratic process, I’m joined by the chair of the Democratic National Committee. I’m always conflicted about, you know, stories of the variety the president tweeted.”

State of Nevada “thinks” that they can send out illegal vote by mail ballots, creating a great Voter Fraud scenario for the State and the U.S. They can’t! If they do, “I think” I can hold up funds to the State. Sorry, but you must not cheat in elections. @RussVought45@USTreasury

“He tweets a lot of things and most of it is nonsense or lies or liable or slander or whatever. But the way he attacked absentee voting today struck me as genuinely dangerous and genuinely sort of threatening to democracy. How high on the priority list is it for you to do what you can to the safeguard administration of free and fair elections this fall?” Hayes continued.

To which Perez replied: “It’s the highest priority, Chris because we know that you’re going to see voter suppression on steroids in the months ahead. We had a conversation I know about the election in Wisconsin recently where they tried to weaponize the pandemic to suppress the vote and steal the state supreme court race. It failed miserably. That’s what you’re going to see.”

Hayes said, “I want to play for you something the president just said about voting, which struck me as deeply pernicious, this sort of voting is an honor and going off about how he doesn’t want people mail-in voting. Take a listen.”

In a clip, Trump said, “Common sense would tell you it’s massive manipulation can take place, massive. They — and you do —you have cases of fraudulent ballots where they actually print them and give them to people to sign, maybe the same person signs them with different writing, different pens. I don’t know. A lot of things can happen. If you can, you should go and vote. Voting is an honor. It shouldn’t be something where they send you a pile of stuff, and you send it back.” –Breitbart

Perez responded to the clip, saying: “Voting isn’t simply an honor, Chris, voting is a fundamental right. People pay the ultimate price to exercise the right to vote. And in a pandemic, the notion that you have a president going after Republican and Democratic secretaries of state in the middle of a pandemic, Secretary Benson is trying to make it easier for eligible people to exercise their right to vote. She’s trying to allow them to exercise the choice that the Michigan Constitution provides them.”

“What we have to do between now and November is make sure that every single voter in every single state has a choice. The choice to vote on election day. So the choice to early vote, the more days of early voting, the more social distancing you do and the right to vote absentee with no excuse, the right to vote by mail. Republicans and Democrats agree on that. This president, in a desperate effort to steal an election, is going to stop at nothing.”

via ZeroHedge News https://ift.tt/2ZvyVvb Tyler Durden

Dear Corporate America: maybe you remember the old Johnny Paycheck tune? Let me refresh your memory: take this job and shove it.

Put yourself in the shoes of a single parent waiting tables in a working-class cafe with lousy tips, a worker stuck with high rent and a soul-deadening commute–one of the tens of millions of America’s working poor who have seen their wages stagnate and their income becoming increasingly precarious / uncertain while the cost of living has soared.

Unemployment and the federal stimulus bonus of $600 a week are far more than your regular wages, including tips. Exactly why do you want to go back to your miserable job and low pay? Why wouldn’t you take time off and enjoy life a little, which is what you’ve been wanting to do for years?

Indeed–why not? The pandemic is giving many permission to get what they always wanted. Consider these examples:

1. The Federal Reserve has always pined for the power to bail out the top .01% / the New Nobility the way they deserve, with unlimited money-printing and the Fed being able to buy every rigged, fraudulent asset spewed by the New Nobility’s financial and corporate predators and parasites.

Yee-haw, the pandemic genie granted your wish: there’s no limits on how many trillions you can shove into the greedy maw of the top .01%, and bail out every single one of their predatory, exploitive, legalized looting bets that went south.

2. Local officials always wanted to commandeer some motels and shove the homeless into them, to clear the sidewalks and parks and then claim “homeless problem solved.” Presto, your wish has been granted.

3. Central government authorities have always resented all those pesky civil liberties restraints on their unquenchable desires to control every tiny aspect of life, public and private, and now–voila, the doors to Petty Authoritarian Heaven have opened. Question our authority? A tenner in the gulag for you, Doubter of All That Is Great and Good.

4. Restaurant owners who on camera always have to say how much they love their customers and business, never mind the money, who secretly have come to loathe their over-entitled, self-absorbed, dilettante customers and are sick and tired of the soaring rent, business licenses, insurance, payroll taxes and costs of ingredients.

You know what, pal? Here’s the keys, you can re-open whatever the heck you want, I’m outta here. I’ve been secretly wishing I could get out from underneath this crushing burden and get my life back. Yes, it was exciting way back when, but now it’s nothing but an endless grind that wasn’t making money even before the pandemic.

5. Since the financiers, Big Tech mini-gods and stock buyback crowd have looted and pillaged their way to immense fortunes by lying, cheating, conniving and gaming, why not follow the money just like the predators and parasites at the top of the heap?

Indeed, why not fudge the application for a federal small business loan and use the “free money” to lease that shiny new Rolls Royce you always desired? Well, haven’t the authorities been begging us to borrow and spend like there’s no tomorrow?

6. Dear Corporate America: maybe you remember the old Johnny Paycheck tune? Let me refresh your memory: take this job and shove it, I ain’t working here no more. If there’s a will, there’s a way, and I’m stepping off the rat race merry-go-round, thank you very much. You can find some other sucker to do your dirty work and BS work, all for the greater glory and wealth of your New Nobility shareholders. I’m outta here. So I won’t get rich, that dream died a long time ago. What I’m interested in now is getting my life back.

The pandemic might not follow the Central Casting script of a V-shaped return to debt-serf, BS-work wonderfulness. Everyone who was sick and tired of their pre-pandemic life and the endless exploitation has had time to think things over, and some consequential percentage of them will welcome “good-bye to all that” and others will decide not to go back, even if that is still an option.

It’s called opting out, and it has always characterized the end of imperial pretensions, pillaging, propaganda and predation. Financial parasites, beware the second-order effects of your overweening dominance and limitless greed.

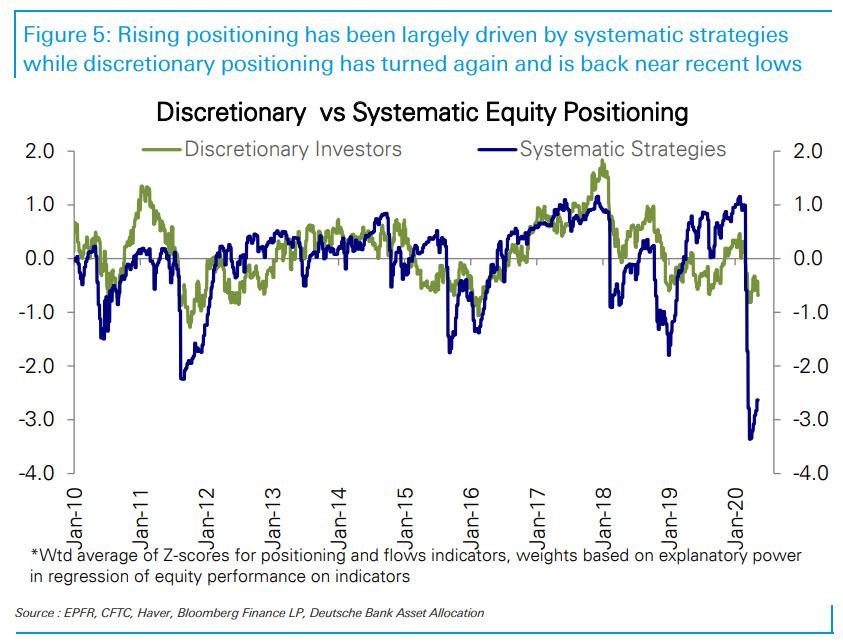

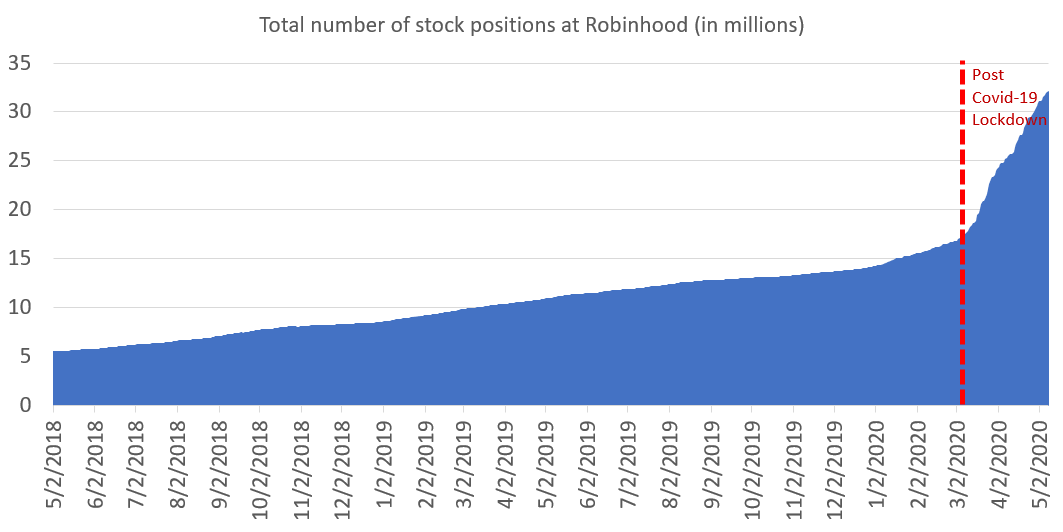

How Retail Investors Took Over The Stock Market Tyler Durden

Thu, 05/21/2020 – 11:50

Two weeks ago, we showed a bizarre breakdown of the main market participants during the latest market meltup/massive short squeeze phase: whereas institutional, hedge fund, CTA, quant and other institutional and systematic funds were refusing to chase the rally…

… retail investors were not only all-in but had literally doubled down since the Covid lockdown.

But how? And where were they getting the money from to chase stocks with such reckless abandon.

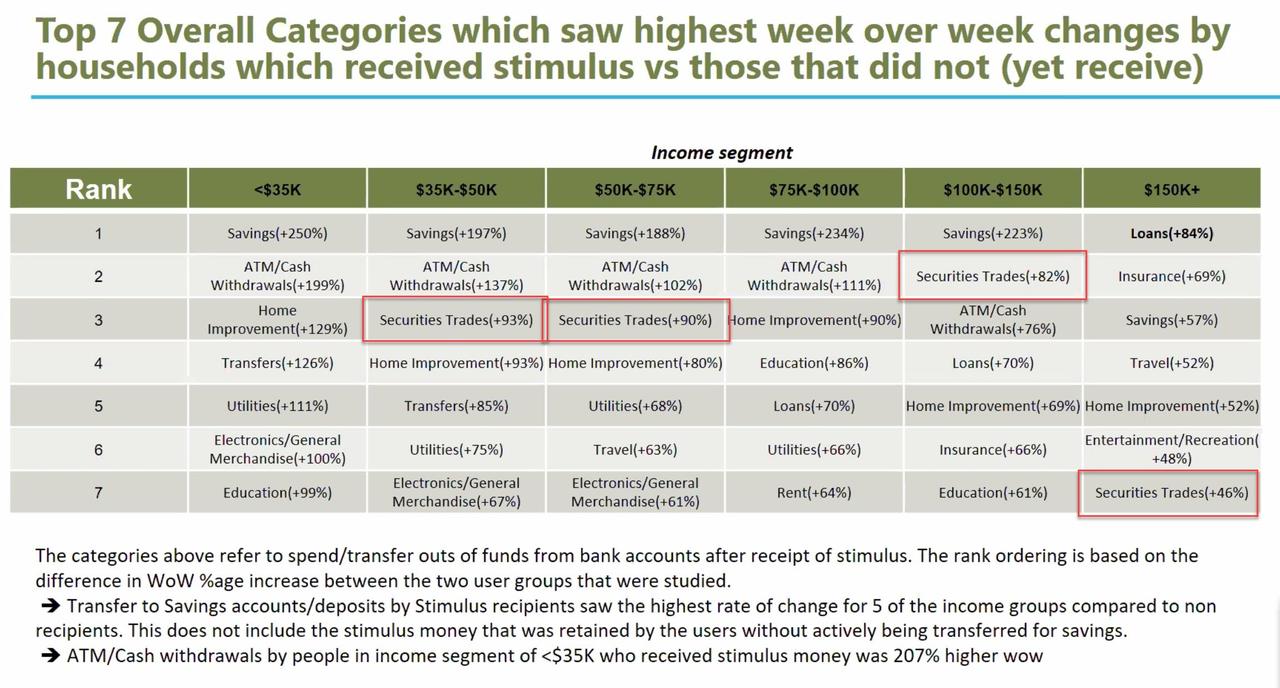

We now know the answer: according to credit card data analytics company Yodlee, after putting some money into savings and withdrawing cash (confirming some of those nascent rumors about ATM runs in March), the third most popular activity for most income segments was “securities trades” – i.e., buying stocks – especially among the pure middle class, those making between $35K and $75K.

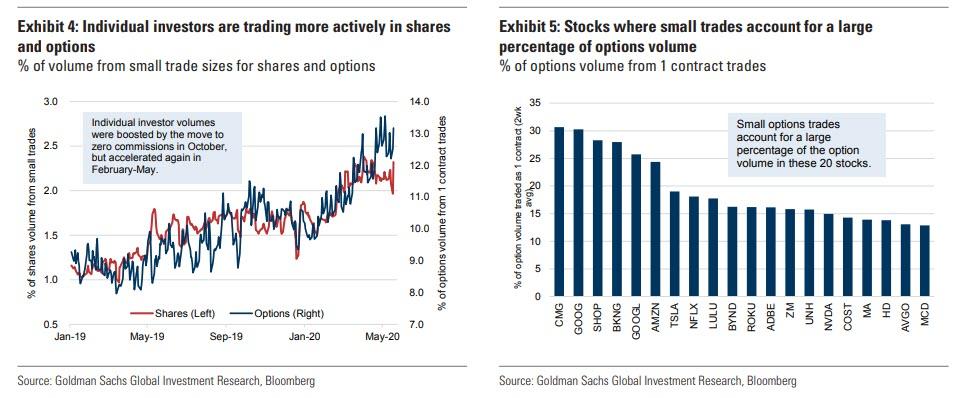

Meanwhile, separate data from Goldman only confirms the surge of small trades, i.e., retail participation, in the past three months.

A few months ago, in response to inbound client inquiries about the participation of individual investors in the share and options market, Goldman started tracking the percentage of volume that is driven by trades of small size as a proxy for assessing the percentage of activity attributable to individual investors.

We monitor the percentage of volume that is attributable to trades of $2,000 or less in the largest 100 stocks. In single stock options, we monitor the percentage of volume that occurs in 1 contract (1 contract provides optionality on 100 shares) for the 50 stocks with the most liquid options.

Not surprisingly, according to Goldman strategists, the proportion of volume driven by small trades over the past three months, in both the shares and options market, has been rising rapidly, with the most significant increase in percentage of volume driven by small trades occurred in February, before the broad decline in liquidity, but has remained at an elevated level.

This data supports the view that individual investor active trading is playing an increased role in market volatility, particularly in select stocks. In the shares market, 2.3% of all volume is made up of trades for $2,000 or less. The increase in small trades has been even more notable in the options market, where 13% of all trades are for 1 contract.

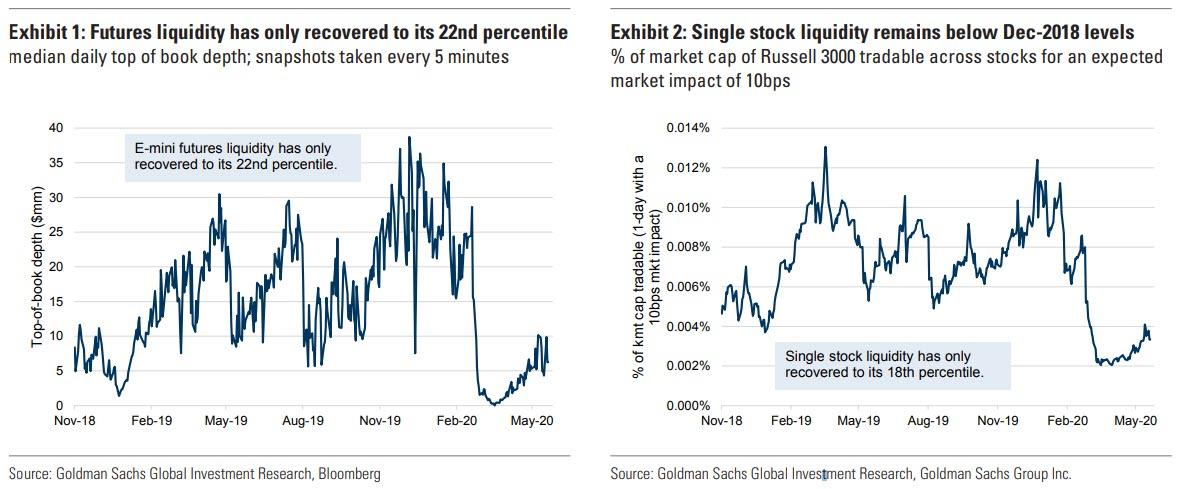

But wait, if individual investors who barely register in the grand scheme of the market, have enough of an impact to move not only single names but entire indexes, that would mean that liquidity in the broader market is non-existent. And that’s precisely the case because as Goldman notes, futures liquidity has only recovered to its 22nd percentile, while single-stock liquidity remains below Dec-2018 levels.

In other words, with most other investor classes sitting this one out and thus making sure market liquidity remains dismal, retail investors – who have been chasing upward momentum in the past three months as they flooded their $0-trade cost online discount brokers with trades – basically took over the market, which also explains why this particular bear market rally from the March 23 low to 3,000 has been especially hated by institutions.

via ZeroHedge News https://ift.tt/2Tt4rWF Tyler Durden

The CDC’s National Center for Health Statistics released some alarming data earlier this week that surprisingly had absolutely nothing to do with Covid for a change.

The report showed that the birthrate in the United States last year declined to its lowest level on record ever since the government began collecting data more than 110 years ago.

This new record low birth rate breaks the previous record set in 2018, which broke the previous record set in 2017, which broke the previous record set in 2016. . .

You get the idea. This has been a long-term issue: people just aren’t having babies anymore. And it’s not just in the Land of the Free.

Fertility rates are low all over the developed world– far below the ‘population replacement level’ of around 2.2 children per mother.

(This is the number of children that demographers say will maintain a steady population.)

In the United States, the average number of births per mother is currently about 1.7. In Australia it’s also around 1.7. In Spain, it’s just 1.5. In Japan, 1.44. In Italy, 1.31. In South Korea, 0.92. And in Singapore, just 0.83.

This list goes on and on. And the fertility rates in most of these countries are hovering near record lows.

Even many large, developing countries have low or declining fertility rates.

In Brazil, for example, the average woman has 1.74 children, which is below the population replacement level. And the rate has been falling steadily for decades.

Even India’s birth rate has been declining, down to just 2.24– less than half the level from the 1980s.

And these statistics were pre-Covid. It certainly stands to reason that with all the economic uncertainty and virus fears, people will delay having children, and potentially have fewer.

This is pretty normal in any economic crisis; according to IMF data, birth rates worldwide plunged following the Great Recession of 2008/2009.

Now, it’s not like a low fertility rate means that some country is going to vanish into the history books.

In Spain, the population declines by an average of just 0.21% per year. And Japan’s population declines by roughly 0.12% per year.

These are trivial numbers… unless you’re thinking about Social Security and national pension funds.

The idea behind most social security programs around the world is that everyone with a job gives up a portion of his/her wages to pay monthly benefits to people who are currently retired.

We do this for our entire careers, with the promise that, when we reach retirement age, the younger generations will pay for our benefits.

This scheme clearly requires a steadily rising population in order to be sustainable:

If you have 1 person receiving benefits today, you’d need 3-4 people paying taxes to support that single beneficiary.

After a few decades, those 3-4 would be retired, requiring around 10-15 workers to support them. And when those 10-15 people retire, you’d need 30-50 workers to support them.

It’s easy to see why low birth rates and declining populations can cause these social security programs to fail.

But Covid is having an even deeper impact on these programs. Because in addition to making the fertility problem worse, Covid has also vanquished tax revenue.

In the US, for example, Social Security is funded almost exclusively by payroll taxes. So when tens of millions of people lose their jobs, payroll tax revenue declines, and Social Security runs a big deficit.

I’ve been writing about this for years: Social Security is already in deep trouble.

The program’s Trustees (which include the Treasury Secretary of the United States) write in their most recent annual report that Social Security’s trust funds will run out of money by 2035.

Again, though, that was pre-Covid. Financial crises tend to make these things a lot worse.

Back in 2007, the last year before the Great Recession, Social Security projected it would run out of money in 2041.

But the financial crisis took such a toll that, after it was over, they revised their projected insolvency date down to 2035.

Social Security hasn’t updated its projection yet to incorporate the Covid impact, and they probably won’t until next year.

But the Bipartisan Policy Center ran the numbers using Social Security’s own financial model. And according to their analysis, Social Security is now set to run out of money in 2029.

That might seem like a long time from now, but from a retirement prospective, it’s just around the corner.

And options for Social Security are extremely limited; the government will either have to (a) radically increase payroll tax rates, and/or (b) make drastic cuts to the monthly benefit they’ve been promising people for decades.

Neither option is good, and most likely they’ll end up doing a combination of both. But not yet.

As this pandemic has proven, they’ll wait until it becomes a major catastrophe before even acknowledging the problem, and then they’ll overreact with worst Draconian measures imaginable.

But any rational person who thinks long-term, however, still has time to plan.

Trump To Void ‘Open Skies’ Treaty With Russia On Friday Tyler Durden

Thu, 05/21/2020 – 11:15

The Trump administration is finally moving to pull the trigger on voiding the three-decade long Open Skies Treaty with Russia, after over much of the past year blasting Moscow’s ‘non-compliance’ and threatening pullout along with other mutual defense treaties like New START.

“President Trump has decided to withdraw from another major arms control accord, according to senior administration officials, and will inform Russia on Friday that the United States is pulling out of the Open Skies Treaty,” reports The New York Times.

US ‘Open Skies’ flight, file image.

The post Cold War treaty, initiated in 1992 and then ratified in 2002, allows its now 35 member states to conduct short-notice, unarmed observation flights to monitor other countries’ military operationsin mutual verification of arms-control agreements.

The treaty even allows Russian recon flights over tightly restricted Washington D.C. airspace — in past years Russian Tupolev Tu-154s have even flown at low altitude over such sensitive sites as Andrews Air Force Base in Maryland, the US Capitol, the Pentagon, and CIA headquarters in Langley.

Senior administration officials previously said of Open Skies, “This is a U.S. position—that we think this treaty is a danger to our national security. We get nothing out of it. Our allies get nothing out of it, and it is our intention to withdraw.”

The Pentagon has in recent years complained that Russia curtails ability to fly over key Russian cities where it’s believed nuclear defense capabilities related to Europe are readied.

In NYT’s Thursday reporting another rationale has been put forth based on intelligence soures, namely—

“…in classified reports, the Pentagon and American intelligence agencies have contended the Russians are also using flights over the United States to map out critical American infrastructure that could be hit by cyberattacks.”

Meanwhile, European allies are actually more fearful this signals the White House is seriously mulling a near-future exit from New START, the last major defense pact between Washington and Moscow which seeks to limit and greatly reduce nuclear arms proliferation.

via ZeroHedge News https://ift.tt/36hUFfn Tyler Durden

Over the last few days we’ve seen two companies make coronavirus-curing headlines without even remotely having the data to back it up. The most impactful headlines were about Moderna, a company that claimed its vaccine was getting a positive immune response in human trials on Monday morning.

The market lost it’s mind on that news. The company’s stock jumped 26%. Moderna’s CEO, Stephane Blancel, did a victory lap interview for a credulous Joe Kernan on CNBC. Literally overnight the company raised $1.4 billion. The whole market rallied. It was a true Cinderella story.

It took a full 24 hours before the market actually read Moderna’s clinical trial, which cited COVID-19 antibodies forming in only eight subjects. The market also noticed that the National Institute for Allergy and Infectious Diseases, which was partnering with the company, did not release an endorsement of the company’s findings as it usually does.

Once the market digested all of that Moderna’s stock fell over 10% and the market went with it. No one did their homework, and no one has since apologized. Welcome to Wall Street. The market didn’t learn its lesson either. On Wednesday Inovio Pharmaceuticals announced that its COVID-19 vaccine was producing positive results in animals and that it expected data in the coming weeks. The stock jumped over 8%.

The pharmaceutical industry was already opaque and scammy. Now suddenly everyone in the stock market is invested in a specific outcome from the sector. They want to be the person who scores big on a life saving treatment. In fact, they’ll be afraid to miss out opportunities. I have an extremely active subconscious, and I could not have dreamt a more perfect condition for separating investors from their money if I tried.

via ZeroHedge News https://ift.tt/3e1zdh2 Tyler Durden

It may well be the case that the U.S. shale sector has cut over US$50 billion from its planned spending this year, the number of operating rigs has fallen by 40 per cent in the past four weeks, and output has fallen by nearly one million barrels per day (bpd) over the same period.

It is equally true, though, that what all these reports overlook is that the shale oil (and gas) sector is too important from a geopolitical and economic perspective to the world standing of the U.S. for it to be allowed to fail, and all other considerations are secondary. In reality, the U.S. shale sector is set to emerge stronger, and earlier, than the vast majority of people think.

Ever since the 1973 Oil Crisis – when Saudi Arabia pressured OPEC members plus Egypt, Syria, and Tunisia to embargo oil exports to the U.S. (and the U.K., Japan, Canada, and the Netherlands) in response to the U.S.’s supplying of arms to Israel in the Yom Kippur War – the U.S. had been itching for a way to end its energy dependence on other countries. Up to that point in October 1973, the U.S. had largely believed that the Saudis could be trusted to adhere to the multi-generational deal that U.S. President Franklin D. Roosevelt and the Saudi King at the time, Abdulaziz, had struck in 1945, as analysed in depth in my new book on the global oil market. Specifically, this deal made in the Great Bitter Lake segment of the Suez Canal was that the U.S. would receive all of the oil supplies it needed for as long as Saudi Arabia had oil in place, in return for which the U.S. would guarantee the security of the ruling House of Saud. By the end of the Saudi-supported embargo in March 1974, the price of oil had risen from US$3 per barrel to nearly US$12 per barrel and, as the Saudi Minister of Oil and Mineral Reserves at the time, Sheikh Ahmed Zaki Yamani (widely credited with formulating the embargo strategy) unequivocally highlighted at that point: the extremely negative effects on the global economy marked a fundamental shift in the world balance of power between the emerging nations that produced oil and the developed nations that consumed it.

When the U.S. shale industry began in earnest in 2006 with natural gas, and in 2010 with crude oil, it offered the U.S. the long-awaited opportunity to finally shrug off any shackles to Saudi that remained by dint of the Kingdom’s petro-power. Within a relatively short time, the U.S. had become the number one oil producer in the world, pushing Saudi frequently into third place behind Russia, and producing an average of around 13 million bpd, with around 60-70 per cent of that coming from the shale sector. In short, it meant that the U.S. did not have to put up with any nonsense from the Saudis anymore, or from anyone else for that matter, with a new-found ability to sanction major oil producing nations that fell foul of it for one reason or another – most notably including Iran, Venezuela, and Russia – without fear of the repercussions for its own energy security.

Given this massive geopolitical reason alone, it should be blatantly obvious to anyone that the U.S. will never capitulate on its shale-centric power, or even allow it to be materially damaged. Even more immediate domestic political reasons militate into shale continuing to function as it was before Crown Prince Mohammed bin Salman (MbS) ignored recent historical precedent and launched the second oil price war against the U.S. shale sector in less than a decade, with the disastrous fallout for it that has resulted. Senior U.S. politicians believe that if the Saudis are ever able to meaningfully reduce the U.S.’s oil output (which has effectively made it the new global ‘swing’ producer, instead of Saudi Arabia), then longer-term not only would the U.S. have to toe the Saudi line on whatever hare-brained schemes MbS might dream up but also it would allow Saudi Arabia over time to manipulate prices back up to levels that would allow it to avoid the imminent bankruptcy that it faces. At the moment, Saudi’s official budget breakeven price per barrel of Brent is US$84 (although after the latest oil price war it is in reality nearer US$100).

The threat of this power, and the resultant oil price levels, is intolerable to U.S. politicians, and particularly those right now whose power is up for grabs in an election year. In this context, any sustained Brent price above US$70 per barrel is regarded by the current Presidential Administration as being in a pricing area where the benefits to U.S. shale producers of higher prices are outweighed by the relative damage done to the U.S. economy. More specifically, it is estimated that every US$10 per barrel change in the price of crude oil results in a 25-30 cent change in the price of a gallon of gasoline, and for every 1 cent that the average price per gallon of gasoline rises, more than US$1 billion per year in consumer spending is lost. As Bob McNally, the former energy adviser to the former President George W. Bush put it: “Few things terrify an American president more than a spike in fuel [gasoline] prices.”

At least as bad for a sitting president is the effect of rising gasoline prices on an already ailing U.S. economy due to the COVID-19 pandemic. According to U.S. NBER statistics, since World War I, the sitting U.S. president has won re-election 11 times out of 11 if the U.S. economy was not in recession within 24 months ahead of an election but presidents who went into a re-election campaign with the economy in recession won only once out of seven times (Calvin Coolidge in 1924). As it stands, according to the American Petroleum Institute, the oil sector also accounts for 10 per cent of U.S. gross domestic product, although this has to be put in context of it being a lobby group for oil companies.

As it stands, the U.S. shale sector benefits in its trajectory of recovery from the after-effects of the previous (2014-2016) oil price war launched against it by the Saudis.

“Prior to that, it was the consensus that the breakeven price for U.S. shale producers was around US$70 per barrel but this was reduced by around half or even more in some cases,” Andrew Dittmar, a Houston-based senior M&A analyst for Enverus exclusively told OilPrice.com last week.

“They did so mainly through the advancement of technology that enabled them to drill longer laterals, manage the fracking stages closer and maintain the fracks with higher, finer, sand to allow for increased recovery for the wells drilled, in conjunction with faster drill times, and these improvements remain in place,” he said.

“They gained further cost benefits from multi-pad drilling and well spacing theory and practice, and for some time the only factor holding back further improvements in output and pricing were infrastructure constrains but even these have now improved, so they are in a much better position to bounce back now than they were after the 2014-2016 war,” he added.

So quickly, in fact, that from a standing start right now some of the best operations can be back online in as little as a week, although the refinery-related lead time is slightly longer.

“Typically, you buy the majority of your crude supplies 30-45 days out so what will happen is refineries will start to increase their run rates and will start buying, then buyers show up to start buying the crude from the producers and then the producers turn it back on – so there will be some advanced warning but it will be very dependent on refinery runs,” Bernadette Johnson, Enverus’ Denver-based vice president of strategic analytics exclusively told OilPrice.com last week.

“There are some risks associated with a shut-in, of course – such as water encroachment in the reservoir, and well bore or surface facility damage, everything we leave in the well will be subject to rusting, corrosion, and deterioration – and these will all have to be tested for, but within those parameters for the vast majority of the wells one week is absolutely sufficient to bring them back to full production capacity, particularly for unconventional wells,” she said.

“In fact, contrary to what many people think, the reservoir damage is actually fairly minimal for the most part and typically when the well has been shut-in pressure rebuilds and when we bring the well back online it actually performs a little better for a while and then it settles back to what it was before,” she added.

“In terms of pricing, US$25-30 per barrel of WTI is enough to get the existing production back up and running, as long as operators believe prices won’t crash back down below US$20 per barrel,” she underlined.

Fears as well of permanently losing the crews look as overblown this time as they were last time: “The idea that these crews will just stay away from a sector that pays much bigger money than they can get elsewhere to go and re-train as coders or something is just not true and didn’t play out last time either,” said Dittmar.

“In sum what we have seen is just another phase of the Business Cycle, with the first phase marked by the rush for volume and the second phase marked by some demand for capital repayment from Wall Street in a broadly lower price environment after 2016,” said Dittmar. “Now, we are entering a third phase that will be marked by more M&A activity, particularly by the acquisition of smaller shale operations by bigger firms, probably with a heavy equity-funded element, given that the stocks of the bigger oil firms have started to rebound whilst the smaller firms still have very low valuations,” he added.

“For the big firms – particularly such as Exxon, Chevron, BP, Shell, and Total, having a good-sized shale operation is a very good fit in the overall business model,” he told OilPrice.com. “It sits well in the short-cycle perspective so that when prices are rising they can ramp up production quickly to take advantage of that and when they are falling they can just cut capex quickly and trim back production,” he underlined.

via ZeroHedge News https://ift.tt/3cTnrFr Tyler Durden

For 2nd Week Jobless Claims Spiked By Major Data-Entry Error; Real Claims Much Lower Than Reported Tyler Durden

Thu, 05/21/2020 – 10:45

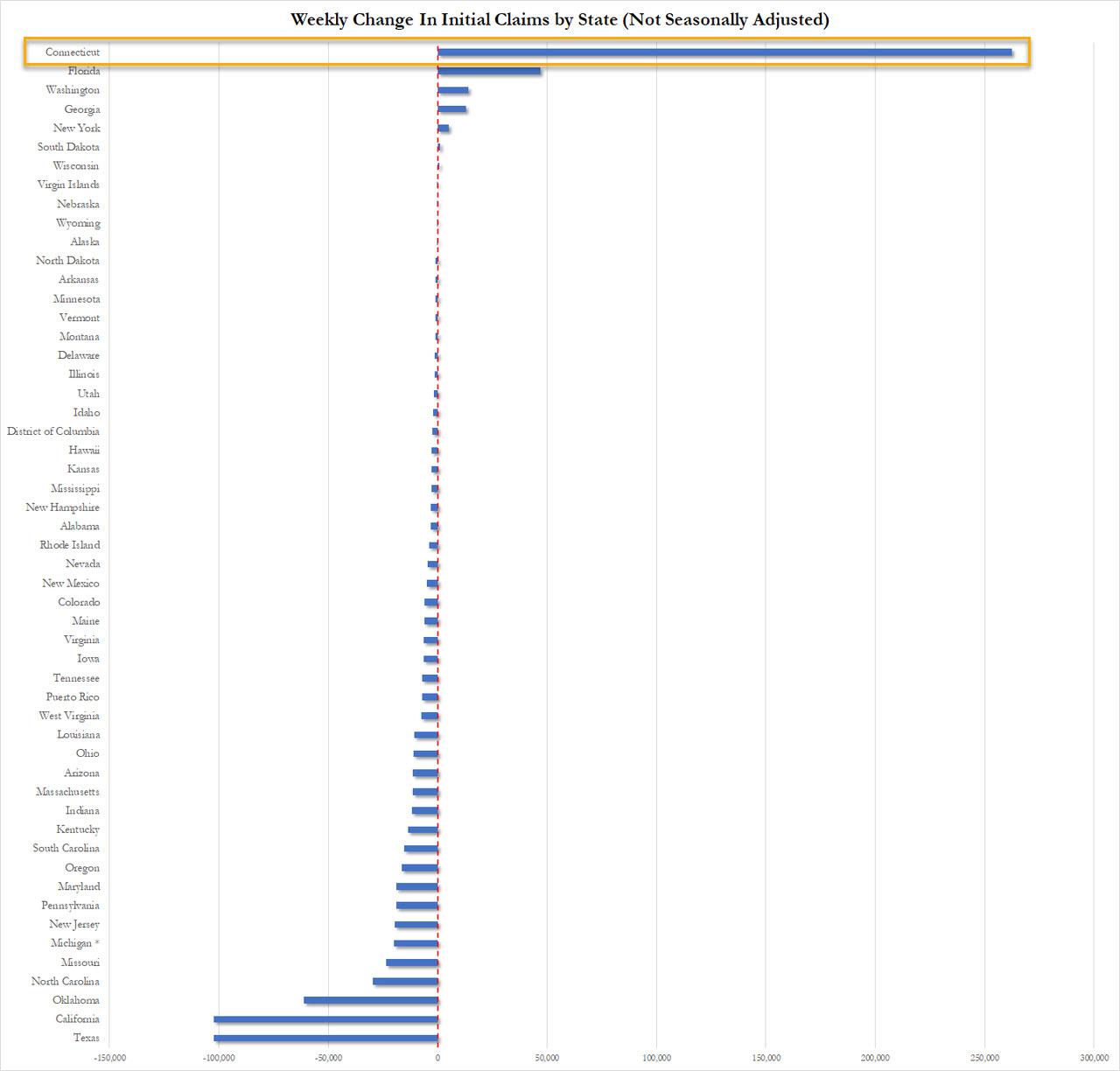

When we reported the initial claims data last week, one number stood out: the 298,680 initial jobless claims reported by Connecticut, which we speculated may have been a simple error.

A few hours later,our suspicion was wrong, as Connecticut confirmed of an embarrassing fat finger error, because instead of reporting 298,680 initial jobless claims, the Constitution state meant to type in 29,846.

One week later, after today’s initial claims report which found that over 2.4 million workers were laid off in the past week, there was a second consecutive data error, with the actual level of claims in a federal program 1 million lower than initially reported.

According to a Massachusetts official, the state had 115,952 initial claims last week under the federal Pandemic Unemployment Assistance program, not the 1,184,792 shown in the U.S. Labor Department’s report earlier Thursday. That means the 2.23 million reported figure for nationwide PUA claims was likely about half that number in reality.

And while those figures, as Bloomberg notes, are separate from the principal number tallying initial claims under regular state programs, it still prompts questions if states are gaming the data to represent the worst possible picture for themselves in hopes of getting a state bailout.

Which brings us to a point made by Southbay Research, namely that even ignoring fat fingers, the true jobless claims data is far lower than what is reported.

First, keep in mind that the number of Ongoing Claims is the most important data point to track COVID’s peak economic pain, as it represents the most concurrent data available. Alas, it now appears that the Jobless Claims data has been misreported, whether for political reasons or simply due to statistical error.

As Southbay notes, what we should see at current levels, is that there should be almost no difference between Seasonally Adjusted (SA) and Not Seasonally Adjusted data (NSA). Historically, ongoing Claims run in the 2M~3M range and that figure shifts ~150K per week depending on various seasonal factors. For example, Spring hiring pushes down ongoing claims.

But COVID has created 22M+ Ongoing Claims. Against that background, a shift of 150K jobs is noise.

What actually happened: Ongoing Claims were adjusted 2.2M. Not even close to any historical seasonal shift.

The Methodology Mistake

In the latest release on Unemployment Claims, the Dept. of Labor reported the following

Ongoing Claims (Seasonally Adjusted): 25.1M

Ongoing Claims (Not Seasonally Adjusted): 22.9M

Seasonal Adjustment factor: 9.3%

Compare that to the same week last year:

Ongoing Claims (Seasonally Adjusted): 1.68M

Ongoing Claims (Not Seasonally Adjusted): 1.54M

Seasonal Adjustment factor: 9.1%

See the problem? The model is plugging a multiplier (9%) instead of using the actual historical nominal level. That’s ok in normal conditions when the underlying figure is ~2M. But when the data is an order of magnitude higher at 23M, using a rate makes no sense. And it’s a methodological error that unnecessarily adds 2.2M to the Ongoing Claims count.

The correct approach would be to use the underlying data (hey, this week typically sees a median drop of 200K in ongoing claims, so we should use that figure.

Use the median actual: 23M Ongoing Claims

Use the rate: 25M Ongoing Claims

2 million “jobs” due to statistical adjustments is big distortion.

What is notable is that the BLS Nonfarm Payrolls Did it Correctly. Consider the recent Nonfarm Payrolls report for April:

Nonfarm Payrolls (SA): -20.5M

Nonfarm Payrolls (NSA): -19.5M

Delta: -1M

Historically, April payrolls grow ~0.9M (warm weather boosts jobs). To offset that seasonal expansion in jobs, the seasonal adjustment factor reduces the NSA figure by -0.9M. Under normal circumstances, that 0.9M is reduced to a rate and would be applied. But COVID is far from normal conditions. Instead, it would appear that the BLS tossed the rate and went with the core data. But the team responsible for Ongoing Jobless Claims missed this step.

Bottom line: The NSA data shows that not only is the number of claims much lower, but that the US has reached peak ongoing unemployment.

via ZeroHedge News https://ift.tt/2LJMzTh Tyler Durden

{kind=link}