McConnell Slams Dem Coronavirus Bill As “Ideological Wish List”

Senate Majority Leader Mitch McConnell (R-KY) has slammed legislation introduced by House Democrats to tackle coronavirus as an “ideological wish list” which he vowed to block because it creates a “needless thicket of bureaucracy.”

“Instead of focusing on immediate relief to affected individuals, families and businesses, the House Democrats chose to wander into various areas of policy that are barely related, if at all, to the issue before us.” he said.

McConnell said that instead he wants a smaller, non-controversial coronavirus response package.

House Majority Leader Kevin McCarthy (R-CA) also signaled his opposition to the Democratic proposal.

House Democrats are hoping to vote for their economic stimulus bill on Thursday, which would include provisions that mandate paid sick leave for workers, provide over $1 billion in aid to state and local governments for food programs and unemployment.

The new Dem plan rests on four principles:

* Anyone who needs a test must get it

* Aid must be targeted to most vulnerable

* We need a much stronger safety net

* Our biggest problem is the virus is already here and spreading

House Majority Leader Steny Hoyer (D-MD) said on Thursday morning that the House is still working with the Trump administration and a vote on the bill is still possible later in the day.

“Further information regarding the exact timing of votes will be announced as soon as it becomes available,” he said.

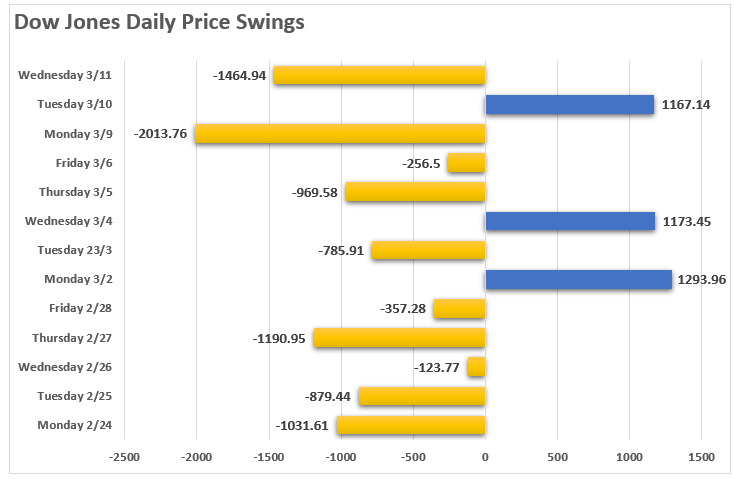

Dow sinks 2,000 points in worst day since 2008, S&P 500 drops more than 7%

Dow rallies more than 1,100 points in a wild session, halves losses from Monday’s sell-off

Dow drops 1,400 points and tumbles into a bear market, down 20% from last month’s record close

It has, been a heck of a couple of weeks for the market with daily point swings running 1000, or more, points in either direction.

However, given Tuesday’s huge rally, it seemed as if the market’s recent rout might be over with the bulls set to take charge? Unfortunately, as with the two-previous 1000+ point rallies, the bulls couldn’t maintain their stand.

But with the markets having now triggered a 20% decline, ending the “bull market,” according to the media, is all “hope” now lost? Is the market now like an “Oriental Rug Factory” where “Everything Must Go?”

It certainly feels that way at the moment.

“Virus fears” have run amok with major sporting events playing to empty crowds, the Houston Live Stock Show & Rodeo was canceled, along with Coachella, and numerous conferences and conventions from Las Vegas to New York. If that wasn’t bad enough, Saudi Arabia thought they would start an “oil price” war just to make things interesting.

What is happening now, and what we have warned about for some time, is that markets needed to reprice valuations for a reduction in economic growth and earnings.

It has just been a much quicker, and brutal, event than even we anticipated.

The questions to answer now are:

Are we going to get a bounce to sell into?

Is the bear market officially started – from a change in trend basis; and,

Just how bad could this get?

A Bounce Is Likely

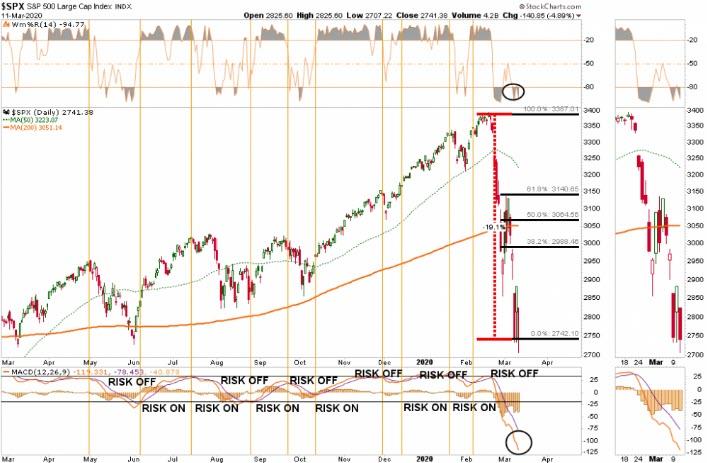

In January, when we discussed taking profits out of our portfolios, we noted the markets were trading at 3-standard deviations above their 200-dma, which suggested a pullback, or correction, was likely.

Now, it is the same comment in reverse. The correction over the last couple of weeks has completely reversed the previous bullish exuberance into extreme pessimism. On a daily basis, the market is back to oversold. Historically, this condition has been sufficient for a bounce. Given that the oversold condition (top panel) is combined with a very deep “sell signal” in the bottom panel, it suggests a fairly vicious reflexive rally is likely. The question, of course, is how far could this rally go.

Looking at the chart above, it is possible we could see a rally back to the 38.2%, or the 50% retracement level where the 200-dma currently resides. A rally to that level will likely reverse much of the current oversold condition, and set the market up for a retest of the lows.

The deep deviation from the 200-dma also supports this idea of a stronger reflexive rally. If we rework the analysis a bit, the 3-standard deviation discussed previously has now reverted to 3-standard deviations below the 200-dma. The market found support there, and with the deeply oversold condition, it again suggests a rally to the 200-dma is likely.

Given that rally could be sharp, it will be a good opportunity to reduce risk as the impact from the collapse in oil prices, and the shutdown of the global supply chain, has not been fully factored in as of yet.

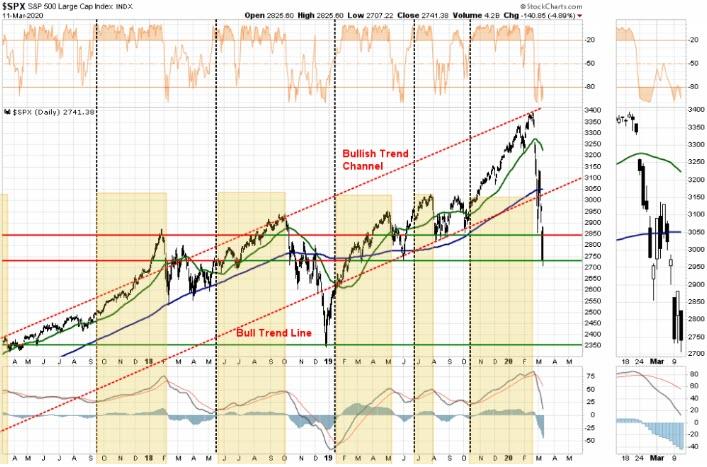

The following chart is a longer-term analysis of the market and is the format we use for “onboarding” our clients into their allocation models. (Vertical black lines are buy periods)

The triggering of the “sell signals” suggests we are likely in a larger correction process. With the “bull trend” line now broken, a rally toward the 200-dma, which is coincident with the bull trend line, will likely be an area to take additional profits, and reduce risk accordingly.

The analysis becomes more concerning as we view other time frames.

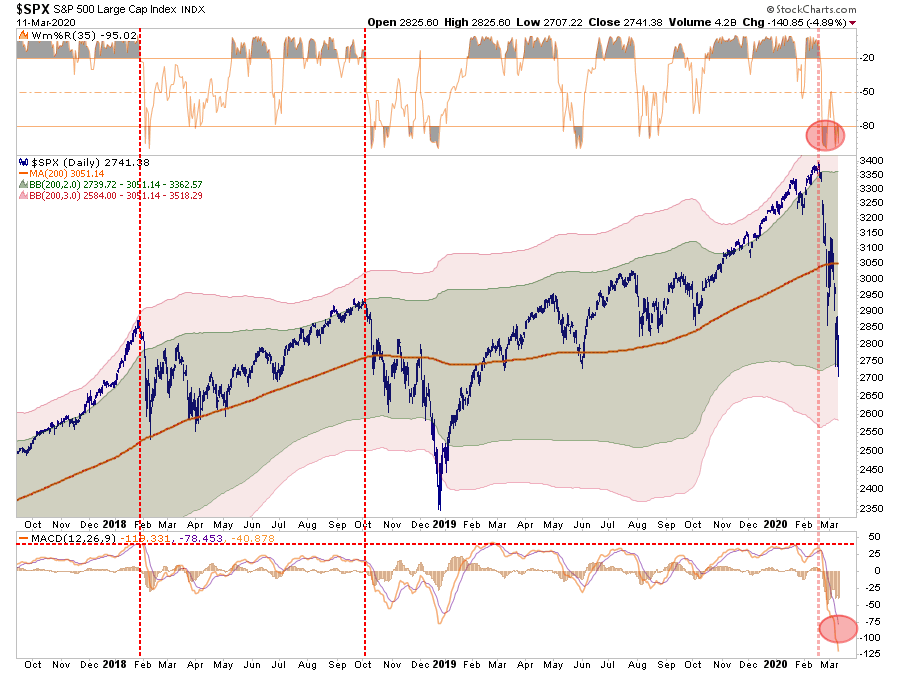

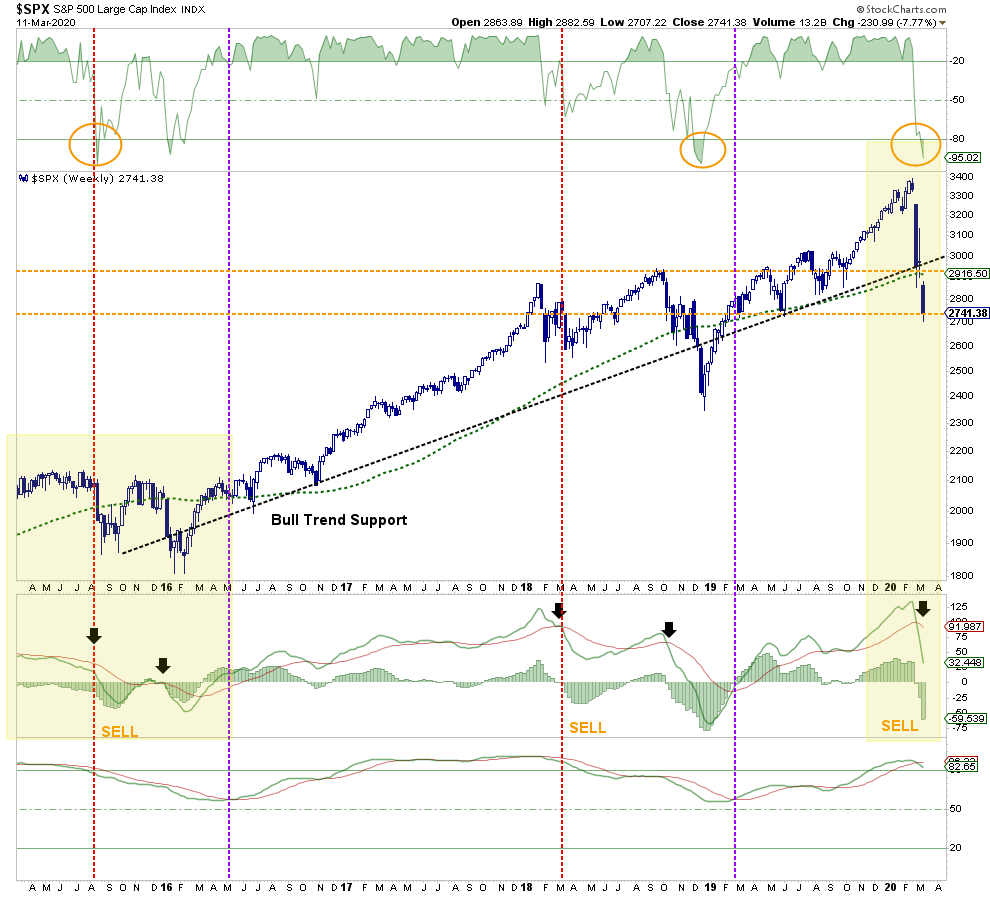

Has A Bear Market Started?

On a weekly basis, the rising trend from the 2016 lows is clear. The market has NOW VIOLATED that trend, which suggests a “bear market” has indeed started. This means investors should consider maintaining increased cash allocations in portfolios currently. With the two longer-term sell signals, bottom panels, now triggered, it suggests that whatever rally may ensue short-term will likely most likely fail. (Also a classic sign of a bear market.)

With the market oversold on a weekly basis, a counter-trend, or “bear market” rally is likely. However, as stated, short-term rallies should be sold into, and portfolios hedged, until the correction process is complete.

With all of our longer-term weekly “sell signals” now triggered from fairly high levels, it suggests the current selloff is much like what we saw in 2015-2016. (Noted in the chart above as well.) In other words, we will see a rally, followed by a secondary failure to lower lows, before the ultimate bottom is put in. If the market fails to hold current levels, the 2018 lows are the next most likely target.

Just How Bad Can It Get?

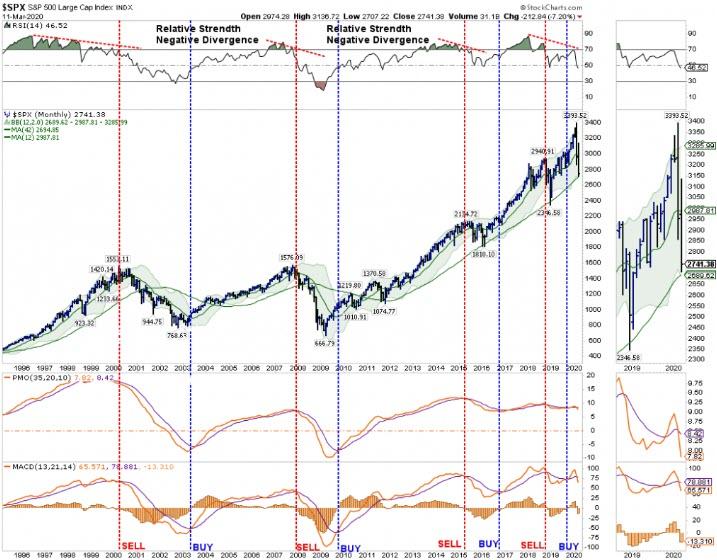

The idea of a lower bottom is also supported by the monthly data.

NOTE: Monthly Signals Are ONLY Valid At The End Of The Month.

On a monthly basis, sell signals have also been triggered, but we will have to wait until the end of the month for confirmation. However, given the depth of the decline, it would likely take a rally back to all-time highs to reverse those signals. This is a very high improbability.

Assuming the signals remain, there is an important message being sent, as noted in the top panel. The “negative divergence” of relative strength has only been seen prior to the start of the previous two bear markets, and the 2015-2016 slog. While the current sell-off resembles what we saw in late 2015, there is a risk of this developing into a recessionary bear market later this summer. The market is very close to violating the 4-year moving average, which is a “make or break” for the bull market trend from the 2009 lows.

How bad can the “bear market” get? If the 4-year moving average is violated, the 2018 lows become an initial target, which is roughly a 30% decline from the peak. However, the 2016 lows also become a reasonable probability if a “credit event” develops in the energy market which spreads across the financial complex. Such a decline would push markets down by almost 50% from the recent peak, and not unlike what we saw during the previous two recessions.

Caution is advised.

What We Are Thinking

Since January, we have been regularly discussing taking profits in positions, rebalancing portfolio risks, and, most recently, moving out of areas subject to slower economic growth, supply-chain shutdowns, and the collapse in energy prices. This led us to eliminate all holdings in international, emerging markets, small-cap, mid-cap, financials, transportation, industrials, materials, and energy markets.(RIAPRO Subscribers were notified real-time of changes to our portfolios.)

While there is “some truth” to the statement “that no one” could have seen the fallout of the “coronavirus” being escalated by an “oil price” war, there has been mounting risks for quite some time from valuations, to price deviations, and a complete disregard of risk by investors. While we have been discussing these issues with you, and making you aware of the risks, it was often deemed as “just being bearish” in the midst of a “bullish rally.”However, it is managing these types of risks, which is ultimately what clients pay advisors for.

It isn’t a perfect science. In times like these, it gets downright messy. But this is where working to preserve capital and limit drawdowns becomes most important. Not just from reducing the recovery time back to breakeven, but in also reducing the “psychological stress” which leads individuals to make poor investment decisions over time.

Given the extreme oversold and deviated measures of current market prices, we are looking for a reflexive rally that we can further reduce risk into, add hedges, and stabilize portfolios for the duration of the correction. When it is clear, the correction, or worse a bear market, is complete, we will reallocate capital back to equities at better risk/reward measures.

We highly suspect that we have seen the highs for the year. Most likely,,we are moving into an environment where portfolio management will be more tactical in nature, versus buying and holding. In other words, it is quite probable that “passive investing” will give way to “active management.”

Given we are longer-term investors, we like the companies we own from a fundamental perspective and will continue to take profits and resize positions as we adjust market exposure accordingly. The biggest challenge coming is what to do with our bond exposures now that rates have gotten so low OUTSIDE of a recession.

BofA’s Shocking Warning: The Treasury Market Is No Longer Functioning Normally

In a stunning report published this morning by BofA’s Marc Cabana, the rates strategist warns that the US Treasury market is no longer functioning properly, and will “likely requires a rapid & large near-term policy response from the US Treasury or Federal Reserve” to get back to normal.

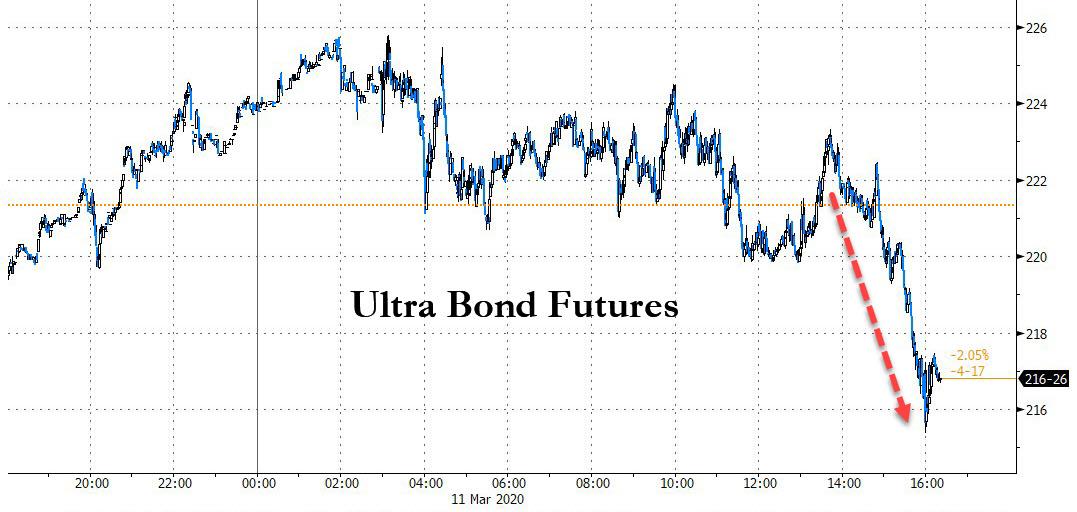

Prompting BoA’s stunning admission that the world’s most liquid market appears broken, was the unexpected plunge in Treasury futures which we discussed yesterday…

… with Cabana perplex by the 11bps surge in 30Y bond yield even as the S&P declined 5%: “In a risk off environment it would be expected to see UST yields decline; yields appear to have been overwhelmed by liquidity concerns yesterday.“

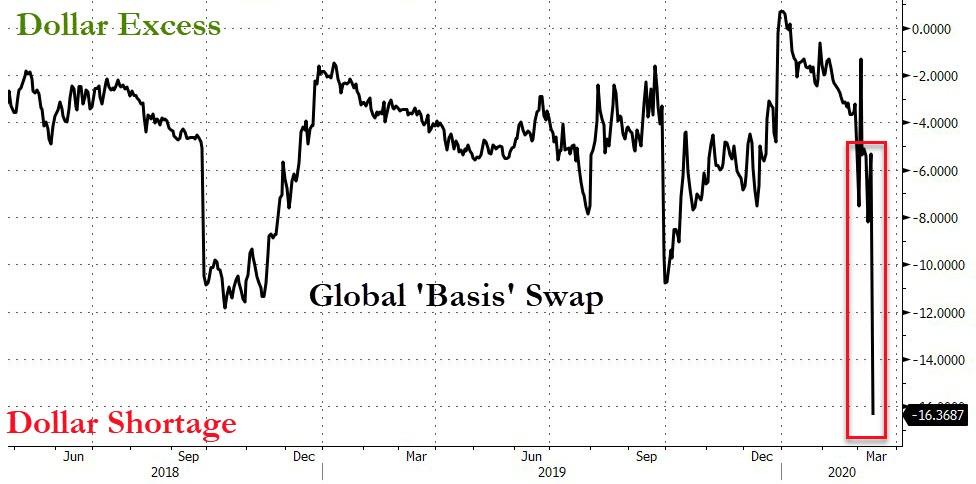

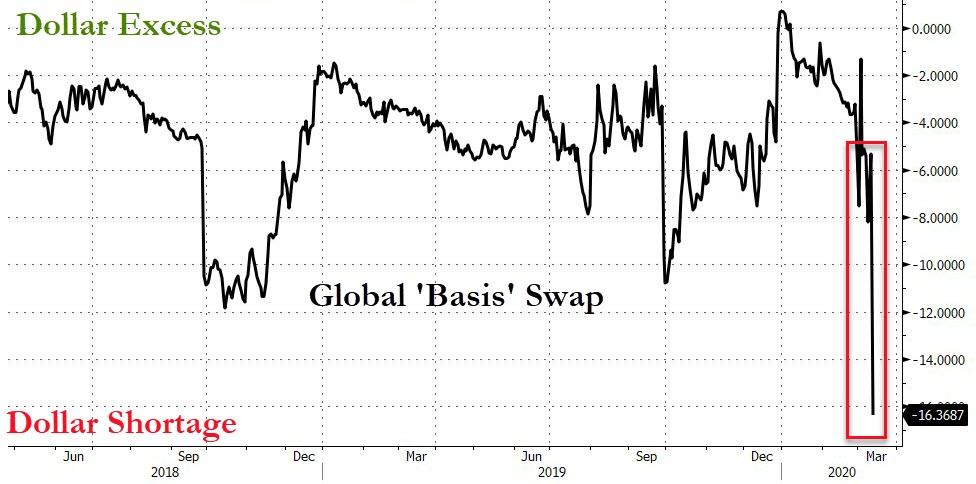

Of course, it’s not just yesterday’s late day puke: as we noted earlier, the funding market itself is starting to freeze up, with the FRA/OIS, i.e., bank dollar funding stress indicator, exploding to the highest since the financial crisis…

… and global FX basis swap cratering amid a sudden shortage in dollars.

All of this ties back to the increasingly imbalanced Treasury market, which itself is starting to break.

As a result, BofA believes that only two things could help restore functioning to the bond market:

Fed re-starting UST QE

US Treasury conducting buyback operations.

For what it’s worth, Cabana favors the latter. In the below excerpt from his full note, he explains what is going on, and what has to be done to make sure the world’s most important market does not freeze.

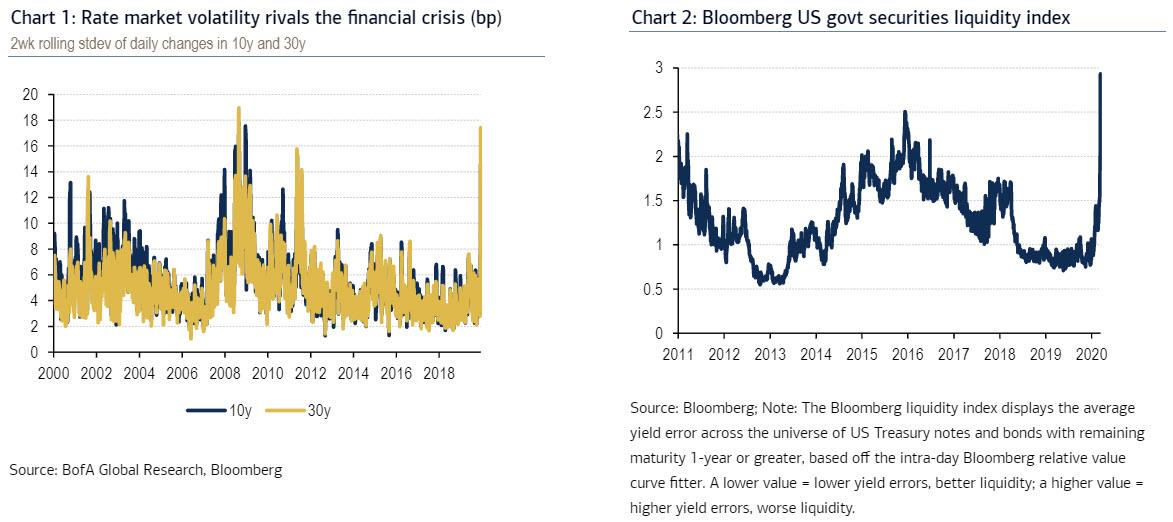

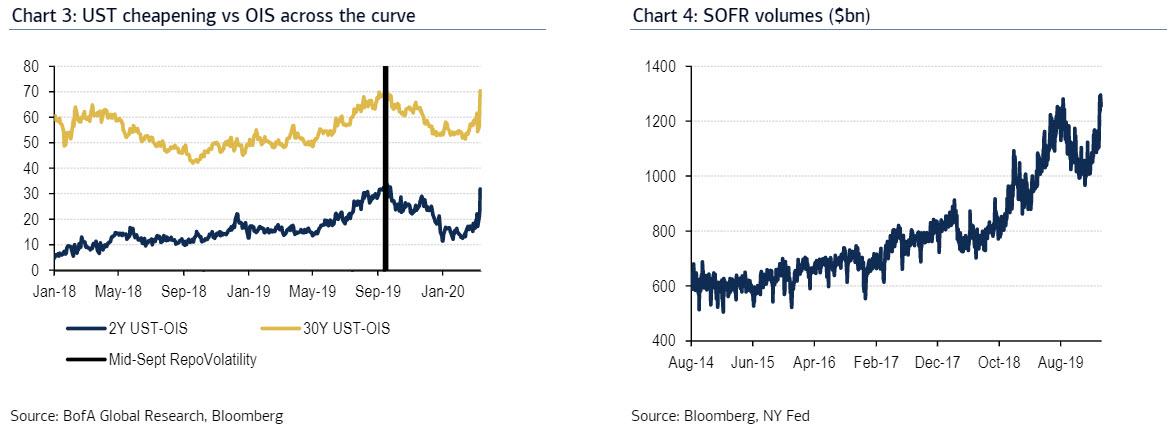

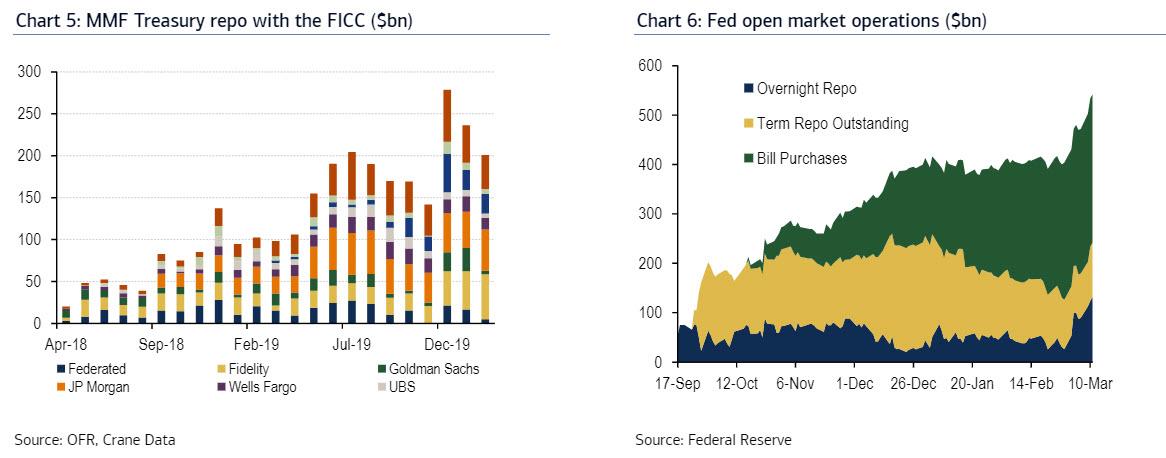

What happened? – The US Treasury market has been very volatile due to macro uncertainty. Realized volatility in the Treasury market is at the highest levels since EU breakup concerns in ’11 & the financial crisis in ’08 (Chart 1). This has caused dealers to widen their bid-offer spreads and limited their ability to transfer risk. These dynamics have materially worsened market functioning (Chart 2), and led to a large cheapening of USTs vs OIS across the curve (Chart 3).

Why should you care? -Sustained illiquidity in the US Treasury market threatens the ability for certain actors to retain their UST positions and could result in large scale position liquidation. The investor community most at risk is leveraged UST investors. These investors typically invest in US Treasury securities and hedge their interest rate exposure with Treasury futures; this is a profitable strategy since UST securities trade “cheap” to futures due to the associated balance sheet cost of holding the UST security vs the futures hedge. This activity supports elevated UST debt issuance by providing a significant source of demand while keeping on & off the run USTs at relatively tight spreads.

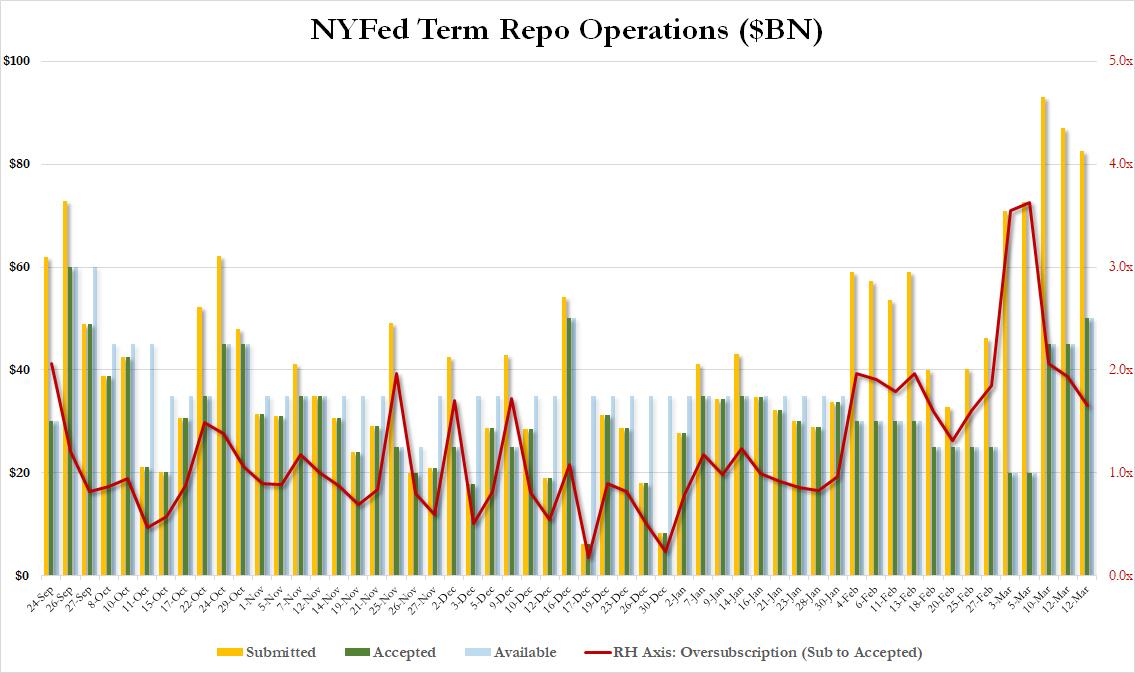

The size of the leveraged UST community is difficult to estimate but the extent of its growth can be seen via growth of the US Treasury repo market. The overnight Treasury repo market has doubled in size since 2016 (Chart 4, Chart 5). The US Treasury repo market is essentially comprised of real money investors lending cash to dealers who then pass this cash along to leveraged investors. The growth of the US Treasury repo market can then be a proxy for the growth of leverage in the UST market.

The risk in the current environment is that sustained illiquidity of the UST market and cheapening of USTs vs OIS could cause leveraged UST investors to reduce their Treasury positions on a large scale. This would essentially result in a Treasury “supply shock” as these funds reduce their positions & force dealers to sell those positions in a very illiquid market. Significant position reduction from one large leveraged UST investor would likely lead to a cascading effect whereby US Treasury yields rise sharply and force liquidations from other similar investors. This would worsen conditions for dealers to intermediate risk in the US Treasury market, exacerbate the rise in US Treasury yields, and further cheapen Treasuries vs OIS or swaps.

Where are the other investors? – Other real money investors should theoretically use Treasury market illiquidity as a buying opportunity. However, real money investors appear hesitant to re-engage in the market due to the elevated illiquidity and fear that conditions could get worse. These real money investors don’t want to “catch the falling knife” especially if there are large scale and disorderly UST position unwinds. They likely believe there may be better buying opportunities in the near future.

What is the bigger picture? – The US Treasury market is the bedrock for all other financial markets; it is the world’s risk free rate and allows the US government to fund itself. If the US Treasury market experiences large scale illiquidity it will be difficult for other markets to price effectively and could lead to large scale position liquidations elsewhere, ex. agency MBS, credit, equities. It would also increase the cost and reduce the ability for the US government to fund itself. This would make it increasingly difficult to provide much needed fiscal help to combat the COVID-19 public health emergency.

What is the policy response? – The Fed today extended the tenor of its repo operations from overnight & 2 week tenors out to 1 month (Chart 6). The first 1-month repo operation is $50 bn in size, slated for Thursday morning, and priced at 1-month fed funds OIS + 5 bps. This repo operation will help provide certainty over dealer funding costs that can be passed along to the leveraged UST community and should assist in stabilizing funding costs. The action shows that the Fed is sensitive to underlying market conditions and working to improve market functioning. However, it may not be enough.

We are concerned that the size of this repo operation may not be large enough to stabilize the cheapening in UST securities and materially improve Treasury market liquidity. We believe it may take a more forceful action from the US Treasury or Federal Reserve to act as a “circuit breaker” in these illiquid Treasury markets. Specifically, we think there is a case for official sector policy action to support market functioning. Two options for consideration include: (1) the Fed re-starting UST quantitative easing (2) the US Treasury conducting “buyback” operations. We favor the latter option.

How does a Treasury buyback work? – In a buyback operation the US Treasury redeems USTs outstanding. This is the same process by which any other private issuer could choose to extinguish outstanding debt or equity. In a Treasury buyback the US Treasury Department would instruct the New York Fed (NY Fed = US Treasury fiscal agent) to buy USTs from primary dealers and pay for these purchases by drawing down its cash balance. To offset the cash balance decline, the US Treasury could increase its debt outstanding at other tenors. The US Treasury engaged in buyback operations from 2000-2002 as a means to manage debt stemming from a budget surplus & strong tax receipts; the US Treasury has done a number of small value buyback operation tests since the fall of 2014 but not done any large scale buyback operations recently.

We expect that the US Treasury would target its buyback operations at tenors across the US Treasury curve and finance these operations by increasing short-term bill issuance. The Treasury has the benefit of the Fed currently conducting 1-month repo operations which should limit the extent of upward pressure on short-dated bills.

The buybacks across the curve would represent a strong real money investor that could aid dealer risk transfers and improve two-way market making activity. We are not sure how large such a buyback program would need to be but we might imagine it could take $50-$100 bn to stabilize market conditions and result in more orderly market making. The Treasury would likely signal that these buyback operations are being done to promote market functioning and will remain open ended until more orderly market conditions prevail.

Why not just do Fed UST QE? – The mechanics of Fed UST QE & Treasury buybacks are very similar but their intentions are fundamentally different. Fed UST QE is designed for monetary policy purposes; the intention of QE is to lower overall borrowing costs, reinforce forward guidance for low interest rates, and have a “portfolio balance impact” by removing duration risk from the private market (Table 1). The Fed likely does not believe it should expand its balance sheet and engage in QE to support market functioning. The Fed likely believes this resides more in the remit of the US Treasury Department.

What about moral hazard? – Such an official sector policy response raises important questions about moral hazard regarding UST leverage and US fiscal deficits; however, these moral hazard risks likely pale in comparison to the acute risks stemming from illiquid Treasury market functioning and the challenges it poses for US government financing of the COVID-19 public health response. A Treasury buyback or Fed UST QE program designed to support market functioning will almost certainly raise questions from Congress. The necessity of these actions will likely increase scrutiny around the extent to which certain investors have been able to deploy leverage and the sustainability of US government deficits. These are important and serious questions to address; however, the more pressing issue is likely to re-establish US Treasury market functioning and provide the US government with an ability to raise cash for the current public health emergency.

Market implications? – Any such Treasury buyback or Fed UST QE response would result in a material richening of UST vs OIS & widening of swap spreads across the curve. Market participants are likely reluctant to take such positions at present due to liquidity concerns. However, the acute illiquidity in the US Treasury market is likely to increasingly drive an official sector policy response. Time is of the essence.

‘They Know Nothing’ (Again): Jim Cramer Calls For Government To Suspend Taxes, Print Way Out Of COVID-19

Jim Cramer on Thursday called for the federal government to immediately print $500 billion to address the coronavirus outbreak, and suspend all taxation during the crisis.

“Everyone owes the government at all time. Everyone in this country, individuals, corporations. That has to be suspend right now so they have more money,” he said.

“Are these radical actions? You bet they are,” Cramer added. “This is the time for radical action and the action can be done by the federal government.“

“They know nothing,” the CNBC host began to rant, referring to the government’s response to the crisis, “I know more than they do, which shouldn’t be – there are no signs anyone in government understands problem.”

“We know more than they do, and that’s not acceptable either,” he added.

Cramer also recommended that companies tap their credit revolvers and that there should be no stigma attached to it when they do so.

This is a DIFFERENT TIME. Only the Federal government can get us through this. ONLY. NO ONE else is big enough. This is my last shot to help this situation. The laughed in 2007 at me. NO MORE LAUGHING

His comments come on the heels of President Trump’s prime-time Wednesday address in which he announced that travel would be suspended to most of Europe for 30 days in an attempt to slow the spread of coronavirus. He said he will also ask Congress to provide payroll tax relief for Americans – and would instruct the Small Business Administration to “provide capital and liquidity” to small businesses.

Cramer’s Thursday comments were reminiscent of his infamous “They know nothing!” rant in 2007.

‘They haveno Idea how bad it is out there… NO IDEA. They know NOTHING!’

Of course in 2008: ‘Bear Stearns is fine‘

Investor Peter Schiff disagrees with Cramer, big time:

Crazy @jimcramer just advocated live on @CNBC that the Federal Government suspend all taxation and just “print the darn money.” A new low for economic thinking from the network that claims to be number 1 in finance!

Has @JimCramer ever considered what would happened if everyone stayed home from work, no one produced anything, no one paid taxes, but the government just printed trillions of dollars out of thin air and effectively dropped them on the populace from helicopters?

S&P Opens Down 7%, Triggers Circuit-Breaker – Halted For 15 Mins

It’s a Monday morning replay. S&P cash markets have opened down 6.7%, bounced a little, before tumbling back down to a 7% loss, triggering the first system-wide circuit-breaker, causing markets to halt trading for 15 minutes.

Where are the circuit-breakers:

During US trading hours (Cash)

Level 1: 7% fall to 2549.48 before 15:25EDT/19:25GMT will prompt a 15-minute pause.

Level 2: 13% drop to 2385.00 before said time will introduce another 15-minute pause.

Level 3: 20% decline to 2193.10 within the time will shut the markets

NOTE: Only the 20% rule applies to the final 35 minutes of trading.

Carnival Halts Global Cruise Operations For 60 Days

Shares of Carnival Corp. plunged by more than 20% on Thursday morning after it announced its Princess Cruises Line would halt operations for 60 days amid the Covid-19 outbreak.

This comes after all confirmed cases of the new coronavirus aboard cruise ships have been on Princess vessels. The Diamond Princes has been docked in Yokohama, Japan, with at least 700 confirmed cases. The Grand Princess docked Monday in Oakland, California, has about 21 confirmed cases.

Princess Cruises announces it will “voluntarily pause global operations of its 18 cruise ships for two months (60 days), impacting voyages departing March 12 to May 10.” https://t.co/JDwgJwbtEKpic.twitter.com/smhLBIL6cL

In proactive response to the unpredictable circumstances evolving from the global spread of COVID-19 and in an abundance of caution, Princess Cruises announced that it will voluntarily pause global operations of its 18 cruise ships for two months (60 days), impacting voyages departing March 12 to May 10.

“Princess Cruises is a global vacation company that serves more than 50,000 guests daily from 70 countries as part of our diverse business, and it is widely known that we have been managing the implications of COVID-19 on two continents,” said Jan Swartz, president of Princess Cruises.

“By taking this bold action of voluntarily pausing the operations of our ships, it is our intention to reassure our loyal guests, team members and global stakeholders of our commitment to the health, safety and well-being of all who sail with us, as well as those who do business with us, and the countries and communities we visit around the world,” added Swartz.

While this is a difficult business decision, we firmly believe it is the right one and is in alignment with our company’s core values. Rest assured the long-serving and dedicated professionals at with our company’s core values. Rest assured the long-serving and dedicated professionals at our company will make best use of this time to prepare Princess Cruises’ fleet of cruise ships for a successful return.

Those currently onboard a cruise that will end in the next five days will continue to sail as expected through the end of the itinerary so that onward travel arrangements are not disrupted. Current voyages that are underway and extend beyond March 17 will be ended at the most convenient location for guests, factoring in operational requirements. Princess will do everything possible to return each guest home with the greatest amount of care possible. During this time, our operations and medical teams across the fleet will remain vigilant in their care and service for guests and crew onboard.

For those who are impacted by this business decision, Princess is offering guests the opportunity to transfer 100% of the money paid for their cancelled cruise to a future cruise of their choice. To add a bonus incentive for guests to accept this offer, the company will add an additional generous future cruise credit benefit which can be applied to the cruise fare or onboard expenses. In addition, Princess will honor this offer for those guests who had made final payment and cancelled their booking on or after February 4, 2020. The future cruise credit can be used on any voyage departing through May 1, 2022.

We wonder how many will actually transfer the credit or demand their money back? Is the cruise industry as we know it about to die?

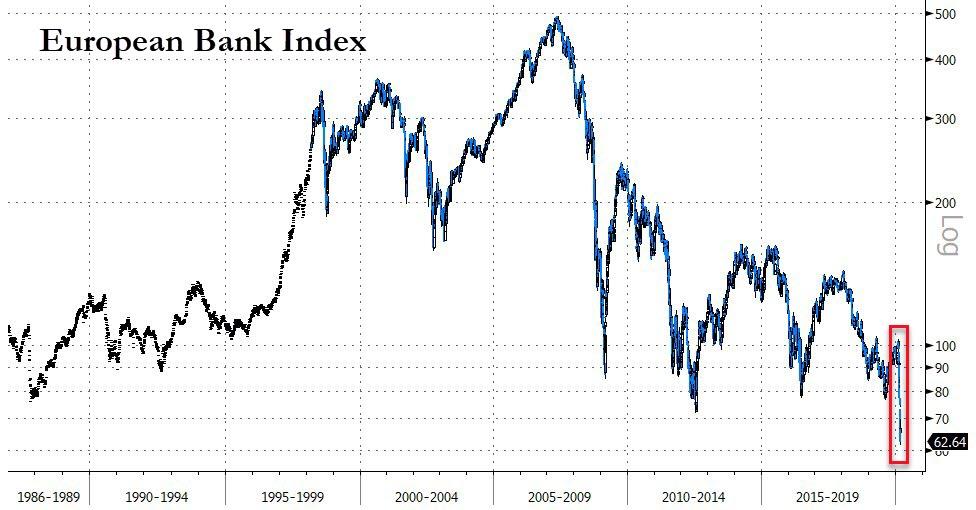

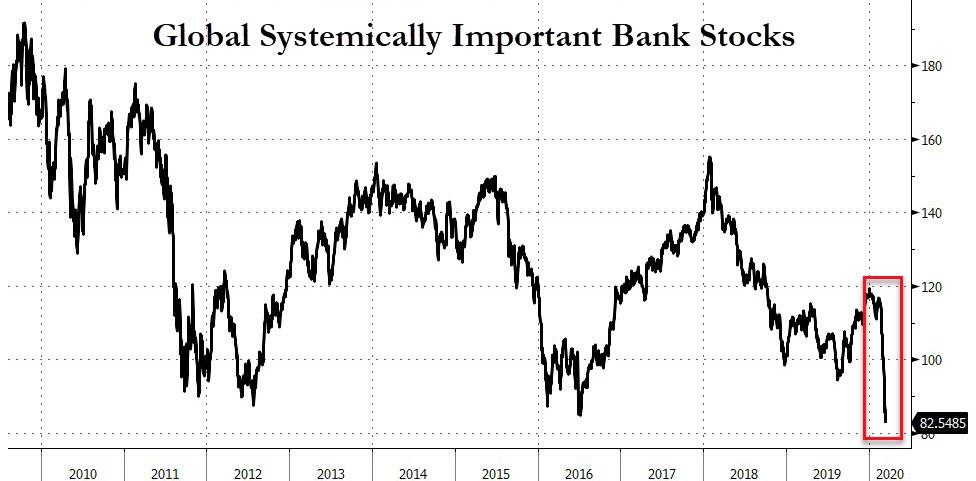

The problem is – judging by the markets – it didn’t work. European bank stocks have crashed to record lows and peripheral bond yields are exploding higher.

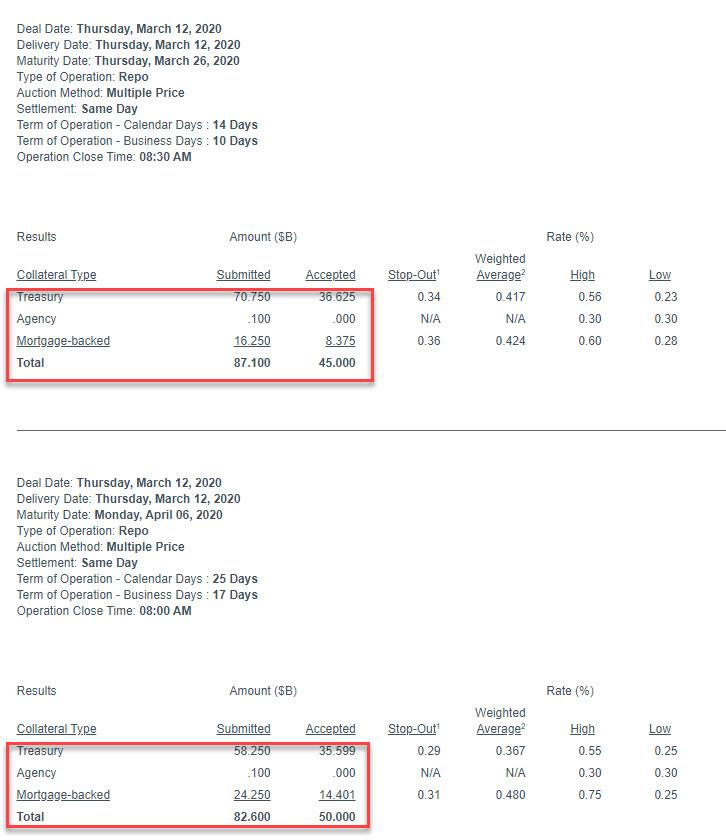

Fed Injects $198 Billion Via Repos To Unfreeze Paralyzed Funding Markets

Update: shortly after the Fed injected $95BN in liquidity via two term reports (a 2-week and the first 1-month op), it also announced $103.1BN injected via the overnight operation, which means that the Fed has injected a combined $198BN in liquidity as funding markets freeze.

Between today’s surge in FRA/OIS which briefly rose to the highest level since the financial crisis, confirming the biggest dollar funding shortage in the interbank market in over a decade…

… to the explosion in the 3-month EUR cross-currency basis is 36 basis points wider, the largest move since 2008 on a closing basis which send the global basis swap crashing…

… the Fed has found itself woefully behind the curve. As a result, moments ago, the Fed announced that it has injected the maximum possible liquidity via today’s 2 term repos, including the just announced 1-month, $50bn term repo, for a total of $45BN + $50BN.

The bank also lowered the minimum bid rate on the 2-week term repo to 0.23% from 0.59% at the original announcement.

As has been the case in the past week, both term repos were oversubscribed, with the 2-week term 1.9x oversubscribed while the 1 month was 1.7x.

Unfortunately, these operations do nothing to fix the funding squeeze and the Fed is now dangerously behind the curve meaning Powell will need to unleash a far more aggressive liquidity injection if he wants to unfreeze the funding markets which appear to be locking up by the hour.