They’ll “Get What They Deserve” – Trump Blasts “Pathetic” Supremes As Biden Court-Packing Looms

In what is likely to go down as one of his greatest rants yet (and longest run-on sentences), former President Trump weighed in tonight on President Biden’s court-packing commission – and in the process took a jab at the Justices, the Radical Left, Mitch McConnell, and dared to exercise his free speech a little further by reminding Americans of his beliefs that the election was fraudulent.

As a reminder, in an executive order on Friday, President Biden createda 36-member commission charged with examining the history of the court, past changes to the process of nominating justices, and the potential consequencesto altering the size of the nation’s highest court.

The panel will beled by Bob Bauer, who served as White House counsel for former President Barack Obama,and Cristina Rodriguez, a Yale Law School professor who served as deputy assistant attorney general in the Office of Legal Counsel under Mr. Obama.

The issue of whether to alter the size of the court, which has beenset at nine members since just after the Civil War,is highly charged, particularly at a moment when Congress is almost evenly divided between the two parties. An attempt by Mr. Biden to increase the number of justices would require approval of Congress and would be met by fierce opposition.

As Jonathan Turley recently noted, the Commission is set to consider a litany of truly looney ideas to prevent the conservative majority from deciding cases, including creating a new specialized court or limiting jurisdiction to remove certain cases from their docket.

The commission includes such individuals as Harvard University professor Laurence Tribe, who called Donald Trump a “terrorist” and has a history of personal and vulgar attacks on Senate Minority Leader Mitch McConnell and others, myself included, who maintain views that he opposes.

Tribe once ridiculed former Attorney General William Barr for his Catholic faith.

The only ire Tribe has drawn from the left, however, was when he referred to the possible selection of an African American like then Senator Kamala Harris to be vice president as mere “cosmetics” for the party.

Tribe has not been subtle about his sudden interest in court packing. After the election he declared:

“The time is overdue for a seriously considered plan of action from those of us who believe McConnell and Republicans, abetted by and abetting the Trump movement, have prioritized expansion of their own power over the safeguarding of our American democracy and the protection of the most vulnerable who are among us.”

And so, with all that said, here are Trump’s thoughts:

Statement by Donald J. Trump, 45th President of the United States of America

(emphasis ours)

Wouldn’t it be ironic if the Supreme Court of the United States, after showing that they didn’t have the courage to do what they should have done on the Great Presidential Election Fraud of 2020, was PACKED by the same people, the Radical Left Democrats (who they are so afraid of!), that they so pathetically defended in not hearing the Election Fraud case.

Now there is a very good chance they will be diluted (and moved throughout the court system so that they can see how the lower courts work), with many new Justices added to the Court, far more than has been reported.

There is also a good chance that they will be term-limited.

We had 19 states go before the Supreme Court who were, shockingly, not allowed to be heard. Believe it or not, the President of the United States was not allowed to be heard based on “no standing.” not based on the FACTS.

The Court wouldn’t rule on the merits of the great Election Fraud, including the fact that local politicians and judges, not State Legislatures, made major changes to the Election – which is in total violation of the United States Constitution.

Our politically correct Supreme Court will get what they deserve – an unconstitutionally elected group of Radical Left Democrats who are destroying our Country.

With leaders like Mitch McConnell, they are helpless to fight. He didn’t fight for the Presidency, and he won’t fight for the Court.

If and when this happens, I hope the Justices remember the day they didn’t have courage to do what they should have done for America.

We can only imagine the liberal media uproar that is about to be unleashed… and demands for Trump to be banned from the entire internet will be imminent.

Investigative site Bellingcat is the toast of the popular press. In the past month alone, it has been described as “an intelligence agency for the people” (ABC Australia), a “transparent” and “innovative” (New Yorker) “independent news collective,” “transforming investigative journalism” (Big Think), and an unequivocal “force for good” (South China Morning Post). Indeed, outside of a few alternative news sites, it is very hard to hear a negative word against Bellingcat, such is the gushing praise for the outlet founded in 2014.

This is troubling, because the evidence compiled in this investigation suggests Bellingcat is far from independent and neutral, as it is funded by Western governments, staffed with former military and state intelligence officers, repeats official narratives against enemy states, and serves as a key part in what could be called a “spook to Bellingcat to corporate media propaganda pipeline,” presenting Western government narratives as independent research.

Citizen journalism staffed with spies and soldiers

An alarming number of Bellingcat’s staff and contributors come from highly suspect backgrounds. Senior Investigator Nick Waters, for example, spent three years as an officer in the British Army, including a tour in Afghanistan, where he furthered the British state’s objectives in the region. Shortly after leaving the service, he was hired by Bellingcat to provide supposedly bias-free investigations into the Middle East.

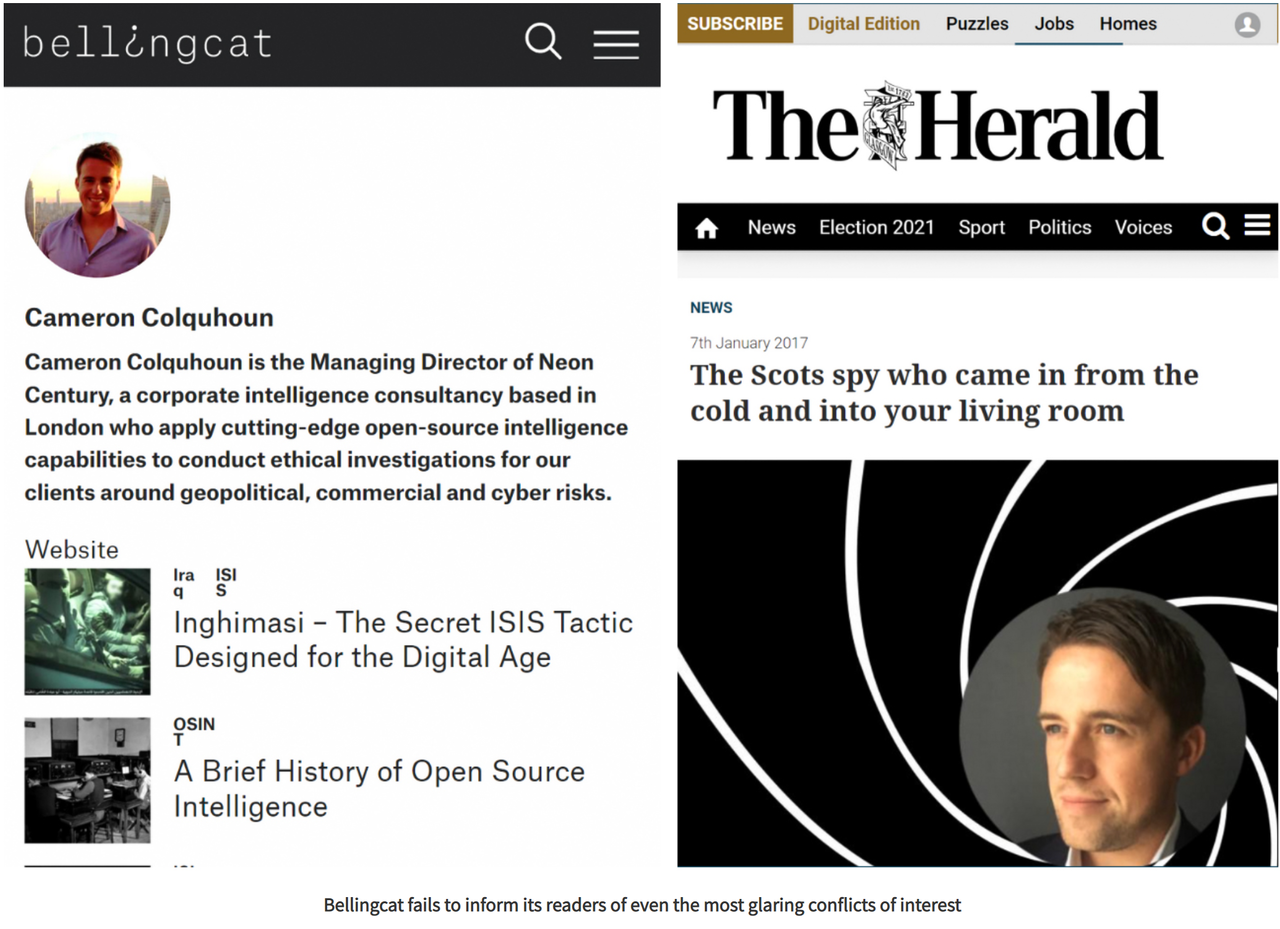

Former contributor Cameron Colquhoun’s past is even more suspect. Colquhoun spent a decade in a senior position in GCHQ (Britain’s version of the NSA), where he ran cyber and Middle Eastern terror operations. The Scot specializes in Middle Eastern security and also holds a qualification from the US State Department. None of this, however, is disclosed by Bellingcat, which merely describes him as the managing director of a private intelligence company that “conduct[s] ethical investigations” for clients around the world — thus depriving readers of key information they need to make informed judgments on what they are reading.

There are plenty of former American spooks on Bellingcat’s roster as well. Former contributor Chris Biggers, who penned more than 60 articles for the site between 2014 and 2017, previously worked for the National Geospatial-Intelligence Agency — a combat support unit that works under the Department of Defense and the broader Intelligence Community. Biggers is now the director of an intelligence company headquartered in Virginia, on the outskirts of Washington (close to other semi-private contractor groups like Booz Allen Hamilton), that boasts of having retired Army and Air Force generals on its board. Again, none of this is disclosed by Bellingcat, where Biggers’s bio states only that he is a “public and private sector consultant based in Washington, D.C.”

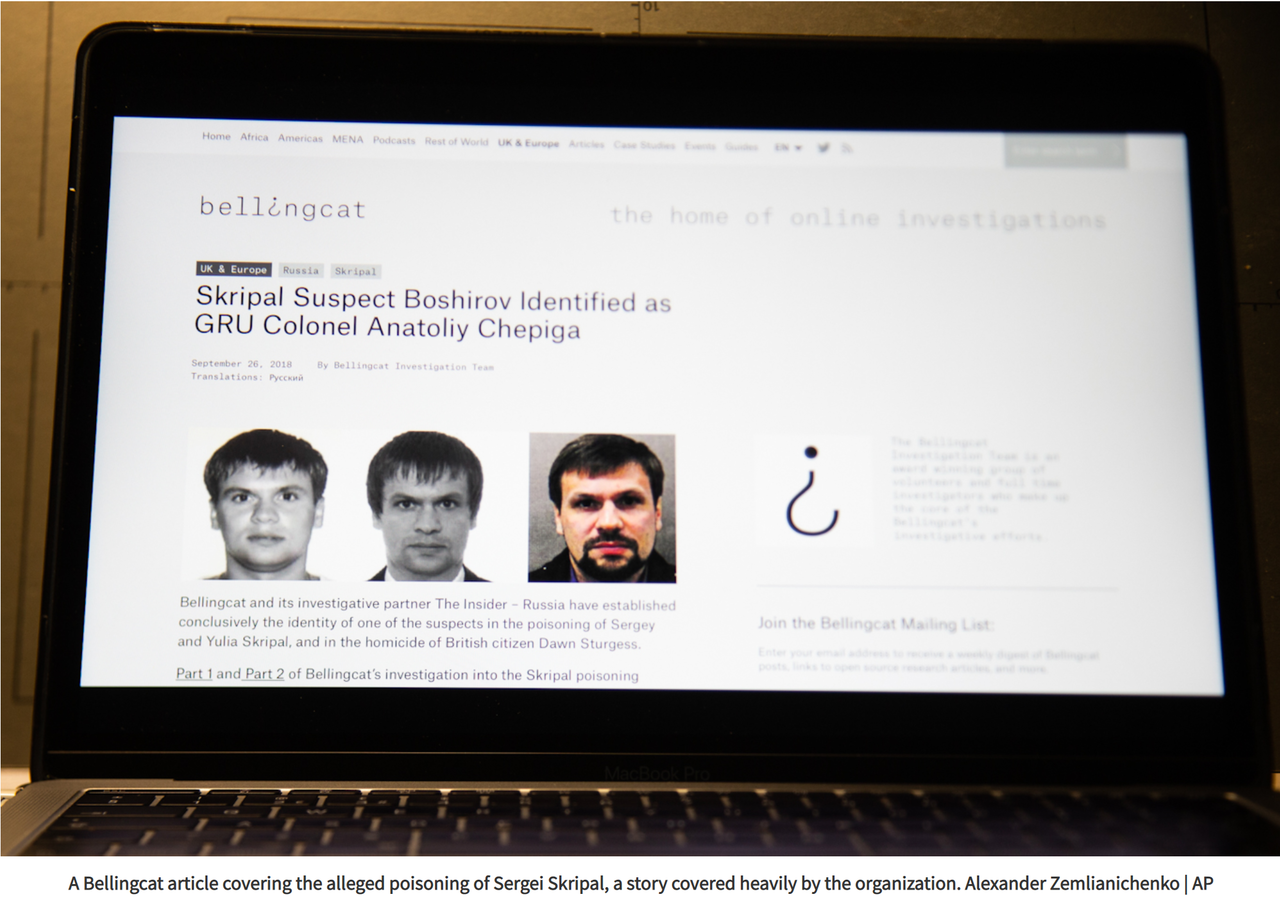

For six years, Dan Kaszeta was a U.S. Secret Service agent specializing in chemical, biological and nuclear weapons, and for six more he worked as program manager for the White House Military Office. At Bellingcat, he would provide some of the intellectual ammunition for Western accusations about chemical weapons use in Syria and Russia’s alleged poisoning of Sergei Skripal.

Kaszeta is also a fellow at the Royal United Services Institute, a think tank funded by a host of Western governments as well as weapons contractors such as Airbus, Lockheed Martin and Raytheon. Its president is a British field marshal (the highest attainable military rank) and its senior vice president is retired American General David Petraeus. Its chairman is Lord Hague, the U.K.’s secretary of state between 2010 and 2015.

All of this matters if a group is presenting itself as independent when, in reality, their views align almost perfectly with the governments funding them. But yet again, Bellingcat fails to follow basic journalism ethics and inform readers of these glaring conflict of interests, describing Kaszeta as merely the managing director of a security company and someone with 27 years of experience in security and antiterrorism. This means that unless readers are willing to do a research project they will be none the wiser.

Other Bellingcat contributors have similar pasts. Nour Bakr previously worked for the British government’s Foreign and Commonwealth Office while Karl Morand proudly served two separate tours in Iraq with the U.S. 82nd Airborne Division.

Government and intelligence officials are the opposite of journalists. The former exist to promote the interests of power (often against those of the public) while the latter are supposed to hold the powerful to account on behalf of the people. That is why it is so inappropriate that Bellingcat has had so many former spooks on their books. It could be said that ex-officials who have renounced their past or blown the whistle, such as Daniel Ellsberg or John Kiriakou, have utility as journalists. But those who have simply made the transition into media without any change in positions usually serve only the powerful.

Who pays the piper?

Just as startling as its spooky staff is Bellingcat’s source of funding. In 2016 its founder, Eliot Higgins, dismissed the idea that his organization got money from the U.S. government’s National Endowment for Democracy (NED) as a ludicrous conspiracy theory. Yet, by the next year, he openly admitted the thing he had laughed off for so long was, in fact, true (Bellingcat’s latest available financial report confirms that they continue to receive financial assistance from the NED). As many MintPress readers will know, the NED was explicitly set up by the Reagan administration as a front for the CIA’s regime-change operations. “A lot of what we do today was done covertly 25 years ago by the CIA,”said the organization’s co-founder Allen Weinstein, proudly.

Higgins himself was a senior fellow at the Atlantic Council, NATO’s quasi-official think tank, from 2016 to 2019. The Atlantic Council’s board of directors is a who’s who of state power, from war planners like Henry Kissinger, Condoleezza Rice and Colin Powell to retired generals such as James “Mad Dog” Mattis and H.R. McMaster. It also features no fewer than seven former CIA directors. How Higgins could possibly see taking a paid position at an organization like this while he was still the face of a supposedly open and independent intelligence collective as being at all consistent is unclear.

Other questionable sources of income include the Human Rights Foundation, an international organization set up by Venezuelan activist Thor Halvorssen Mendoza. Halvorssen is the son of a former government official accused of being a CIA informant and a gunrunner for the agency’s dirty wars in Central America in the 1980s and the cousin of convicted terrorist Leopoldo Lopez. Lopez in turn was a leader in a U.S.-backed coup in 2002 and a wave of political terror in 2014 that killed at least 43 people and caused an estimated $15 billion worth of property damage. A major figure on the right-wing of Venezuelan politics, Lopez told journalists that he wants the United States to formally rule the country once President Nicolas Maduro is overthrown. With the help of the Spanish government, Lopez escaped from jail and fled to Spain last year.

Imagine, for one second, the opposite scenario: an “independent” Russian investigative website staffed partially with ex-KGB officials, funded by the Kremlin, with most of their research focused on the nefarious deeds of the U.S., U.K. and NATO. Would anyone take it seriously? And yet Bellingcat is consistently presented in corporate media as a liberatory organization; the Information Age’s gift to the people.

The Bellingcat to journalism pipeline

The corporate press itself already has a disturbinglyclose relationship with the national security state, as does social media. In 2019, a senior Twitter executive was unmasked as an active duty officer in the British Army’s online psychological operations unit. Coming at a time when foreign interference in politics and society was the primary issue in U.S. politics, the story was, astoundingly, almost completely ignored in the mainstream press. Only one U.S. outlet of any note picked it up, and that journalist was forced out of the profession weeks later.

Increasingly, it seems, Bellingcat is serving as a training ground for those looking for a job in the West’s most prestigious media outlets. For instance, former Bellingcat contributor Brenna Smith — who was recently the subject of a media storm after she successfully pressured a number of online payment companies to stop allowing the crowdfunding of the Capitol Building insurrectionists — announced last month she would be leaving USA Today and joining The New York Times. There she will meet up with former Bellingcat senior investigator Christiaan Triebert, who joined the Times’ visual investigations team in 2019.

The Times, commonly thought of as the United States’ most influential media outlet, has also collaborated with Bellingcat writers for individual pieces before. In 2018, it commissioned Giancarlo Fiorella and Aliaume Leroy to publish an op-ed strongly insinuating that the Venezuelan state murdered Oscar Perez. After he stole a military helicopter and used it to bomb government buildings in downtown Caracas while trying to ignite a civil war, Perez became the darling of the Western press, being described as a “patriot” (The Guardian), a “rebel” (Miami Herald), an “action hero” (The Times of London), and a “liberator” (Task and Purpose).

Until 2020, Fiorella ran an opposition blog called “In Venezuela” despite living in Canada. Leroy is now a full-time producer and investigator for the U.K.-government network, the BBC.

Bad news from Bellingcat

What we are uncovering here is a network of military, state, think-tank and media units all working together, of which Bellingcat is a central fixture. This would be bad enough, but much of its own research is extremely poor. It strongly pushed the now increasingly discredited idea of a chemical weapons attack in Douma, Syria, attacking the members of the OPCW who came forward to expose the coverup and making some bizarre claims along the way. For years, Higgins and other members of the Bellingcat team also signal-boosted a Twitter account purporting to be an ISIS official, only for an investigation to expose the account as belonging to a young Indian troll in Bangalore. A leaked U.K. Foreign Office document lamented that “Bellingcat was somewhat discredited, both by spreading disinformation itself, and by being willing to produce reports for anyone willing to pay.”

Ultimately, however, the organization still provides utility as an attack dog for the West, publishing research that the media can cite, supposedly as “independent,” rather than rely directly on intelligence officials, whose credibility with the public is automatically far lower.

Oliver Boyd-Barrett, professor emeritus at Bowling Green State University and an expert in the connections between the deep state and the fourth estate, told MintPress that “the role of Bellingcat is to provide spurious legitimacy to U.S./NATO pretexts for war and conflict.” In far more positive words, the CIA actually appears to agree with him.

“I don’t want to be too dramatic, but we love [Bellingcat],” said Marc Polymeropoulos, the agency’s former deputy chief of operations for Europe and Eurasia. “Whenever we had to talk to our liaison partners about it, instead of trying to have things cleared or worry about classification issues, you could just reference [Bellingcat’s] work.” Polymeropoulos recently attempted to blame his headache problems on a heretofore unknown Russian microwave weapon, a claim that remarkably became an international scandal. “The greatest value of Bellingcat is that we can then go to the Russians and say ‘there you go’ [when they ask for evidence],”added former CIA Chief of Station Daniel Hoffman.

Bellingcat certainly seems to pay particular attention to the crimes of official enemies. As investigative journalist Matt Kennard noted, it has only published five stories on the United Kingdom, 17 on Saudi Arabia, 19 on the U.S. (most of which are about foreign interference in American society or far-right/QAnon cults). Yet it has 144 on Russia and 244 under its Syria tag.

In his new book “We Are Bellingcat: An Intelligence Agency for the People,” the outlet’s boss Higgins writes: “We have no agenda but we do have a credo: evidence exists and falsehoods exist, and people still care about the difference.” Yet exploring the backgrounds of its journalists and its sources of funding quickly reveals this to be a badly spun piece of PR.

Bellingcat looks far more like a bunch of spooks masquerading as citizen journalists than a people-centered organization taking on power and lies wherever it sees them. Unfortunately, with many of its proteges travelling through the pipeline into influential media outlets, it seems that there might be quite a few masquerading as reporters as well.

Japan Decides To Dump One Million Tons Of Radioactive Fukushima Water Into The Pacific; IAEA Approves

We live in a bizarre world: one where the the Keystone XL pipeline must be shut in case of a hypothetical (and extremely unlikely) leak, but where Japan is allowed to dump over one million tons of radioactive water into the Pacific Ocean. Well… it’s either bizarre or simply exposing just how profoundly hypocritical, self-serving and corrupt the “green”/ESG/Greta Thunberg narrative truly is.

Last week we wrote that ten years after the Fukushima disaster, Japan had finally come “clean”, and admitted that it is “unavoidable” that it would have to dump radioactive Fukushima water in the Pacific Ocean.

Fast forward to today when moments ago Kyodo confirmed what we already knew: the Japanese government decided to release treated radioactive water accumulating at the crippled Fukushima Daiichi nuclear power plant into the sea, having determined “it poses no safety concerns to humans or the environment” despite worries of local fishermen and neighboring countries.

So an oil pipeline whose odds of leaking are virtually zero must be shuttered immediately, but a million tons of radioactive water is “safe” and can be released into the Pacific Ocean, from where it will eventually finds its way into billions of humans around the globe.

But wait, the insanity gets better: Japan’s decision to release all this radioactivity into the ocean was backed by none other than the “scientists” at the International Atomic Energy Agency, with Director General Rafael Grossi saying it is “scientifically sound” and in line with standard practice in the nuclear industry around the world.

So… the IAEA has a standard practice of what exploded nuclear power plants do with their fallout water? And how often has this particular standard practice been invoked we wonder?

Between this and the covid debacle, one can almost see why nobody trusts the world’s so-called whores for hire scientists any more.

Anyway, back to the cartoonish nation of Japan, whose Prime Minister Yoshihide Suga met with members of his Cabinet including industry minister Hiroshi Kajiyama to formalize the decision, which comes a decade after a massive earthquake and tsunami triggered a triple meltdown in March 2011.

It is here that over the past decade, water pumped into the ruined reactors at the Fukushima plant to cool the melted fuel, mixed with rain and groundwater that has also been contaminated, has been treated using a liquid processing system, or ALPS, which in theory removes most radioactive materials including strontium and cesium but leaves behind tritium, which according to scientists poses little risk to human health in low concentration. The water is being stored in tanks on the plant’s premises — more than 1.25 million tons in total.

Of course, if the water is so safe, we wonder when the “scientists” will demonstrate that there is nothing to be concerned about by chugging a gallon of the “ALPS-treated” radioactive sludge. We won’t be holding our breath.

The real reason why Japan has no choice but to dump the toxic fallout into the ocean is that plant operator TEPCO (Tokyo Electric Power Company Holdings) expects to run out of storage capacity as early as fall next year, and the government had been looking for ways to safely dispose of the tritiated water. Having found no viable alternative, it decided to do the simplest possible thing: dump it.

“Disposing of the treated water is an unavoidable issue in decommissioning the Fukushima Daiichi plant,” Suga said at the meeting, adding the plan will be implemented “while ensuring that safety standards are cleared by a wide margin and firm steps are taken to prevent reputational damage.”

A Ministry of Economy, Trade and Industry subcommittee concluded in February 2020 that releasing the tritiated water into the sea and evaporating it were both realistic options, with the former more technically feasible. Hilariously, and as noted above, the International Atomic Energy Agency has backed the move, with Director General Rafael Grossi saying it is scientifically sound and in line with standard practice in the nuclear industry around the world.

Yet despite Japan’s and the IAEA’s assurance, China and South Korea on Monday voiced deep concern over Japan’s plan – and now decision – to release treated radioactive water that has accumulated at the crippled Fukushima nuclear plant, saying discharging it into the sea would have a negative impact on its neighbors. Apparently they have not been briefed by the ALPS “experts” that there is nothing to worry about.

China said it has conveyed its “serious concern” to Japan, calling on Prime Minister Yoshihide Suga’s government to make a cautious decision to protect the public interest of international society as well as the health and safety of Chinese citizens. Arguing Tokyo has come under criticism globally over the issue, “Japan cannot overlook or shrug off” such a fact and “should not hurt the marine environment, food safety and human health anymore,” the Chinese Foreign Ministry said.

A South Korean Foreign Ministry spokesman, meanwhile, said Monday that releasing treated water from the Fukushima plant would “directly and indirectly affect the safety of the people and the neighboring environment.”

“It would be difficult to accept the release into the sea if the Japanese side makes a decision without sufficient consultation,” the spokesman said, adding South Korea will “respond by strengthening cooperation” with the International Atomic Energy Agency. Apparently he was unaware that the IAEA was already bribed convinced by Japan that there is nothing wrong what what is about to take place.

But wait… we thought that “scientists” said it was safe: does China and South Korea practice a different “science” – one where a million tons of radioactive water getting dumped into the ocean is actually – gasp – dangerous.

Could it be that we have two “scientific” camps, one of which is motivated by things far more mundane than the scientific method to reach its conclusion. Things such as money?

Of course, for Japan which prints trillions of said money every months, it’s not a concern, and that’s music to the “scientists” ears. Suga said the IAEA and other third parties will be involved in the plan, ensuring it is carried out with transparency. We can only assume that the “third parties” will also receive copious amounts of money to find that nothing is wrong here.

In any case, the poisoning of the Pacific Ocean won’t take place for another two years: that’s when the the tritiated water is actually released into the sea due to the need to build new facilities and conduct safety screenings. The government had initially hoped to make the decision last October, viewing it as necessary to clear up space at the Fukushima plant in order to move forward with the decades-long decommissioning process, but decided it needed more time to convince local fishermen who have voiced strong opposition.

Apparently the local fishermen have also not heard of this thing called “science” according to which there is nothing to worry about.

The good news is that with a two year lead time, such aspiring eco-saints as Greta Thunberg will have more than enough time to prevent this plan from being realized. Unless, of course, Greta’s entire eco spiel is one giant lie. Failing that, and should Greta also be convinced by money the IAEA that there is nothing wrong with the water, we can only hope that she will drink several gallons of the radioactive substance on live TV.

Meanwhile, we wonder how those other eco-saints at Blackrock will respond: having banned investments in such devious, diabolical industries as coal and shale, we can only imagine the loophole Larry Fink’s henchmen will have to come up with to continue investing in Japan without looking like total sellouts. One suggestion has already emerged: the “Blackrock Nuclear Treated Water Socially Responsible Inclusion Oil Sands Exclusion ETF”

That Rep. Matt Gaetz (R-FL) is a pedophile, a sex trafficker, and an abuser of women who forces them to prostitute themselves and use drugs with him is a widespread assumption in many media and political circles. That is true despite the rather significant fact that not only has he never been charged with (let alone convicted of) such crimes, but also no evidence has been publicly presented that any of it is true. He has also vehemently denied all of it. All or some of these accusations very well may be true and, one day — perhaps imminently — there will be ample publicly available evidence demonstrating this.

But that day has not yet arrived. As of now, we know very little beyond what The New York Timesinitially reported about all of this on March 30: that “people close to the investigation” told the paper that “a Justice Department investigation into Representative Matt Gaetz and an indicted Florida politician is focusing on their involvement with multiple women who were recruited online for sex and received cash payments.” The article also said the DOJ “inquiry is also examining whether Mr. Gaetz had sex with a 17-year-old girl and whether she received anything of material value.” Both the NYT and, later, The Daily Beast, indicated the existence of financial transactions involving payments by Gaetz to his associate Joel Greenberg, currently charged with multiple felonies. The New York Times article made clear: “No charges have been brought against Mr. Gaetz, and the extent of his criminal exposure is unclear.” That is still true..

But no matter. One is hard-pressed to find people willing to urge that his guilt not be assumed before evidence of it is presented (amazingly, just six months ago, many of the same people now treating these accusations as proven fact had no troublecasually asserting or stronglyimplying that Gaetz was having sex with a 19-year-old male whom he said he had been parentally raising for years, all without the slightest regard for the impact of such innuendo on that other person). So reckless is the discourse around this case that it is now frequently asserted in major outlets that Rep. Gaetz faces “charges” of sex trafficking and sex with a minor, even though that claim is, at least as of now, blatantly untrue. Rep. Liz Cheney (R-WY) said that explicitly this morning without contradiction on CBS News’ Face the Nation, and it was then repeated without contradiction by numerous media outlets:

That is because — as many people learned in the case of 31-year-old Mayor Alex Morse, accused by the left’s creepy sexual morality police of the moral crime of consensually dating young adults only to be subsequently vindicated as the victim of a political hit — those who urge caution or basic precepts of due process are immediately accused of sympathy for the crimes themselves. Like free speech, “due process” is both a Constitutional guarantee (i.e., the state may not deprive someone of life, liberty or property without it) as well as a vital cultural norm (i.e., people should not be assumed guilty of heinous crimes without evidence being publicly presented). It is that latter sense of due process being mauled by prevailing discourse surrounding this case.

But this case also raises interesting and important questions of sexual morality and political ideology about the right of adults to engage in consensual behavior without the state and societal moral judgments intervening to punish or castigate them for it — once a foundational view of left-wing, libertarian and even some strains of right-wing politics. It goes without saying that if Rep. Gaetz or the adult women he hired violated prostitution or drug laws, then they should be treated like anyone else who does so (in 38 of 50 states and the District of Columbia, the age of consent for sex is 16 or 17; only in 12 states is it 18, though Florida, Gaetz’s home state, is one of those; prostitution remains illegal in all U.S. jurisdictions except parts of Nevada).

But legality aside, what are the moral principles that ought to govern how consenting adults have sex with one another, choose to engage in or patronize sex work, or ingest substances into their own body? That “sex work” should neither be criminalized nor stigmatized has been a growing view within leftist politics for years now (it is a major cause of the ACLU), and has long had significant support among libertarians and even some “limited government” conservatives.

To explore all of these complex and quite fascinating legal, political and cultural issues, I discuss this case in the video below, roughly 30 minutes in length. In addition to the above-referenced questions, I examine how the liberal-left view of private adult consensual behavior has radically shifted within the last ten-to-fifteen years (the USA Today article I referenced about the 1994 sexual relationship between the married-but-separated California House Speaker Willie Brown, 60, and county prosecutor Kamala Harris, 31 years his junior, is here). My discussion in this video also explores the state of the law and relevant moral principles applicable to Rep. Gaetz’s case and those like it:

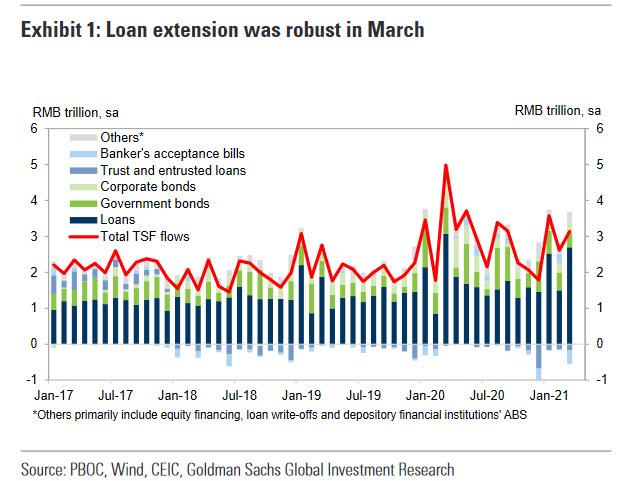

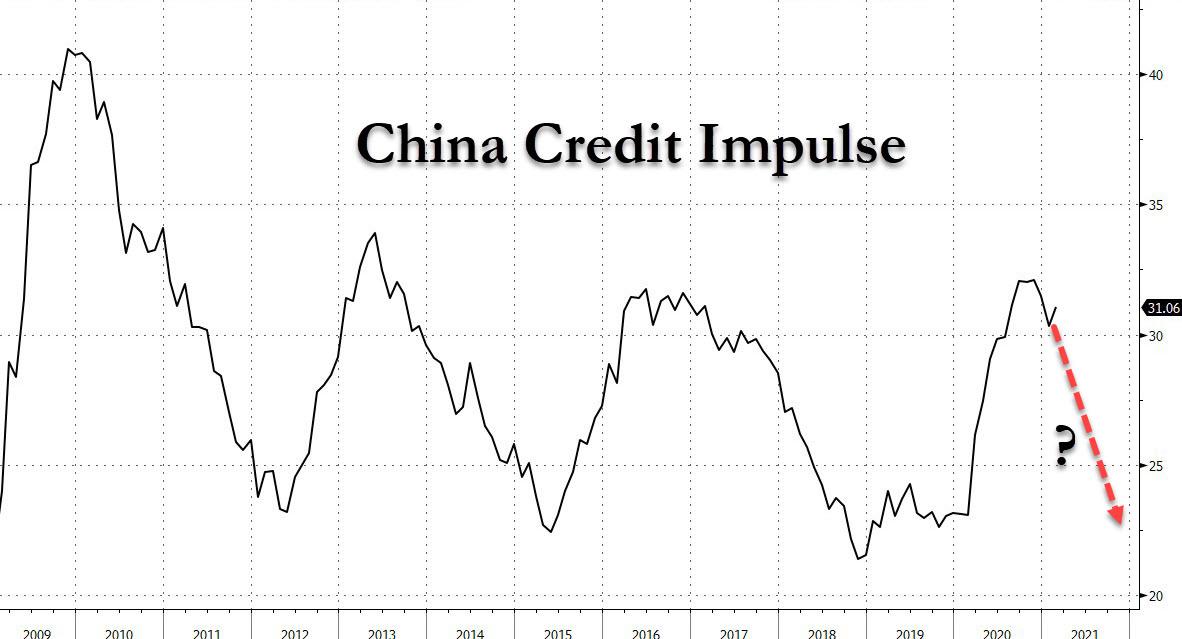

Overnight, China reported that the sequential growth of total social financing (TSF) moderated in March following a strong rebound in January and February, with robust loan growth offset by a contraction in shadow lending.

Reflecting the normalization in monetary policy in past months, and the PBOC’s most recent attempt to rein in runaway debt, Goldman believes that credit growth should moderate this year but remain broadly in line with nominal GDP growth. This would be primarily driven by moderation in government bond and corporate bond issuance, and slower loan growth. On the other hand, a big test to China’s commitment to contain debt will emerge in the coming months, when issuance in local government new special bonds will increase significantly, which would be supportive of credit growth in the near term, but would once again put into question Beijing’s dedication lowering or even containing the country’s debt.

Here are the key numbers:

New CNY loans: RMB 2,730bn in March, beating consensus est. RMB 2,300bn.

Outstanding CNY loangrowth: 12.6% yoy in March; down from February:12.9% yoy

Total social financing: RMB 3340bn in March, missing consensus est. RMB 3700bn.

TSF stock growth was 12.6% yoy in March, lower than 13.5% in February. The implied month-on-month growth of TSF stock moderated to 10.6% from 13.5% in February.

M2: 9.4% yoy in March (11.9% SA ann mom), missing consensus est. 9.5% yoy., and down from February’s 10.1% yoy

Key points:

The sequential growth of TSF slowed to 10.6% M/M annualized in March,following the acceleration in January and February. This is roughly similar to the average of sequential growth of TSF stock in November-February. In year-on-year terms, TSF stock growth moderated to 12.6% yoy in March from 13.5% yoy. M2 growth slowed to 9.4% yoy in March from 10.1% in February.

Among major TSF components, new Rmb loans was robust in March. This was driven by strong mid-to-long term loans to corporates. It may reflect strength in investment demand, which was echoed by significant pickup in business expectation sub-index under construction PMI and Cheung Kong Graduate School of Business’s business condition index on investment outlook in recent two months. And while household mid-to-long term loans growth remained robust, Goldman notes that average growth for short-term household loans weakened notably, probably related to regulations on consumer credit. Meanwhile, the drag from shadow lending widened: banks’ undiscounted acceptance bills fell significantly in March (after seasonal adjustment), and contraction in trust also widened. Corporate bond issuance in March was similar as the average in January and February, and net government bonds issuance has been relatively mild so far this year.

According to Goldman, reflecting the normalization in monetary policy in past months, credit growth should moderate this year but remain broadly in line with nominal GDP growth (the bank forecasts TSF growth to moderate to 11.5% this year). This would be primarily driven by moderation in government bonds as suggested in the budget, milder corporate bond issuance reflecting normalization of liquidity conditions, and slower loan growth (due to slower public investment and smaller liquidity demand which increased notably last year amid the pandemic shock). For instance, policy bank loans, which may have increased significantly by around Rmb 2.5tr last year to support public investment, would probably slow this year. And inclusive SMEs lending, which increased by around Rmb 3.6tr, could also moderate (big five banks’ inclusive SMEs lending increased sharply by around 55% last year, and was required to increase by more than 30% this year). In coming months,issuance in local government new special bonds, which only started in March, will increase significantly, with the majority of pre-allocated quota of Rmb 1.77tr likely being issued in Q2, and this would support credit growth in the near term.

Details aside, as Bloomberg’s Ye Xie notes when looking at the continued slowdown in growth in both TSF and M2, “at this rate, the credit impulse, or the change of new credit as a percentage of GDP, could start to shrink by July or August just as the Fed may lay the groundwork for its own tapering.” This confirms what we discussed last week…

… when we said that a slowdown in credit creation would have dire consequences on China’s all-important credit impulse which, as we have profiled repeatedly in the past, is arguably the biggest driving force behind global reflation (or disinflation, as the case may be).

… will be validated. And as this all too critical metric fades, virtually every asset across the globe will be affected (especially if it is joined by the double whammy of the Fed also tapering in late 2021/early 2022).

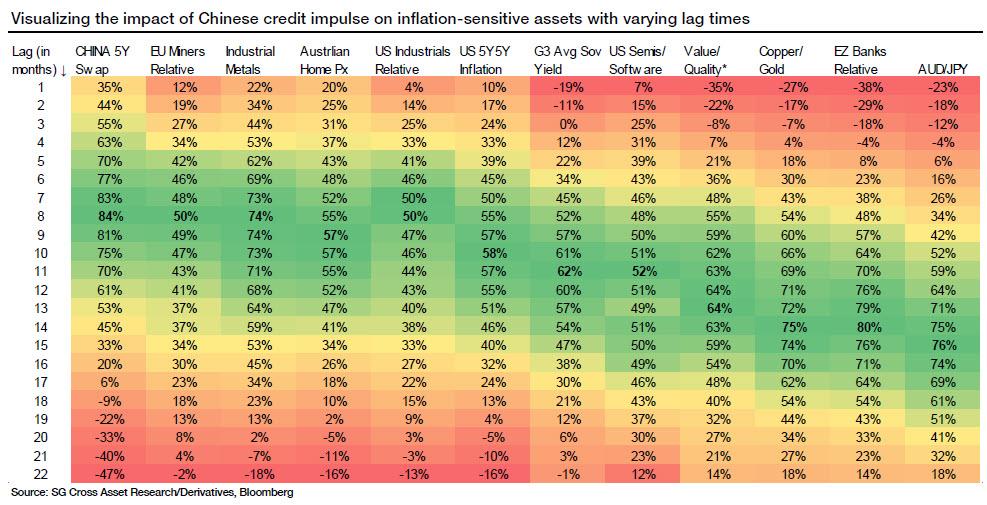

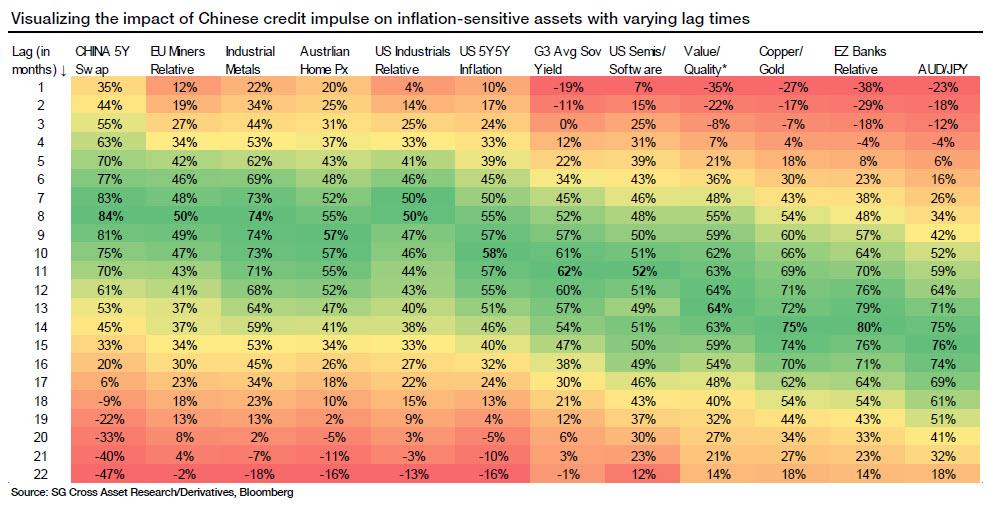

As a reminder, the credit impulse first reaches assets that are driven primarily by the Chinese economy (Chinese bond yields and industrial metals). Next to be impacted are inflation breakevens and sovereign yields in Western economies. The peak correlation for other growth-sensitive assets such as eurozone banks and AUD/JPY arrives with bigger lag of around 4-5 quarters. This result, while logical, is quite significant, as it gives us a playbook for the ebb and flow in Chinese credit impulse.

The table above shows the correlation between different assets and Chinese credit impulse for varying lag times. The extent of the differences between lags in correlations is exemplified in the left-hand chart below. While peak correlation for Chinese interest rate swaps arrives with an eight-month lag, the peak correlation for eurozone banks manifests itself with a lag of 14 months (read more here “In Historic Reversal, China’s Credit Impulse Just Peaked: What This Means For Global Markets“).

Looking ahead, with high correlations and short lag times, Chinese interest rate swaps and industrial metals should be the first assets to be adversely impacted by the topping of the Chinese credit impulse. Australian house prices and US 5Y forward 5Y inflation will likely also be hit in this first group.

The mining and industrial sectors also have short lag times, but their correlation is slightly lower. The other highly correlated group of assets, including eurozone banks, also gets strongly affected by credit impulse, but the rather large lag time opens the door for other factors to influence the price action of these assets as well.

Low correlation with certain assets suggests that Chinese credit, while being one of the drivers, may not be the main driver of price performance for these assets (e.g. semis/software ratio, sovereign yields in the West and value/quality ratio).

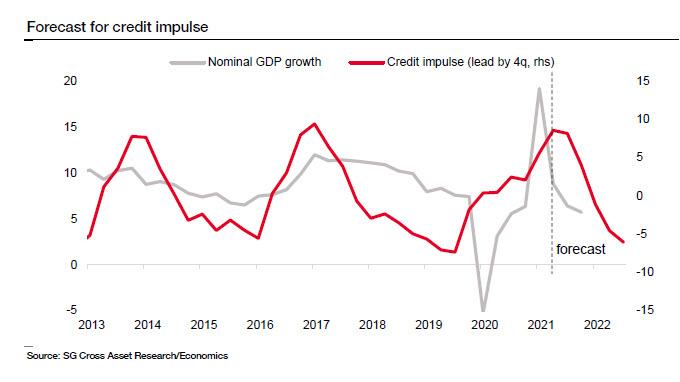

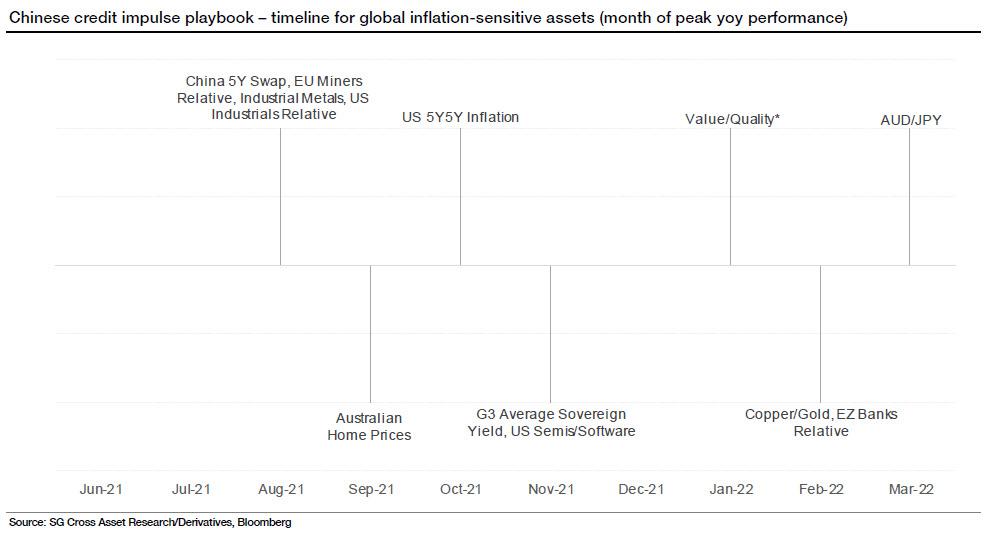

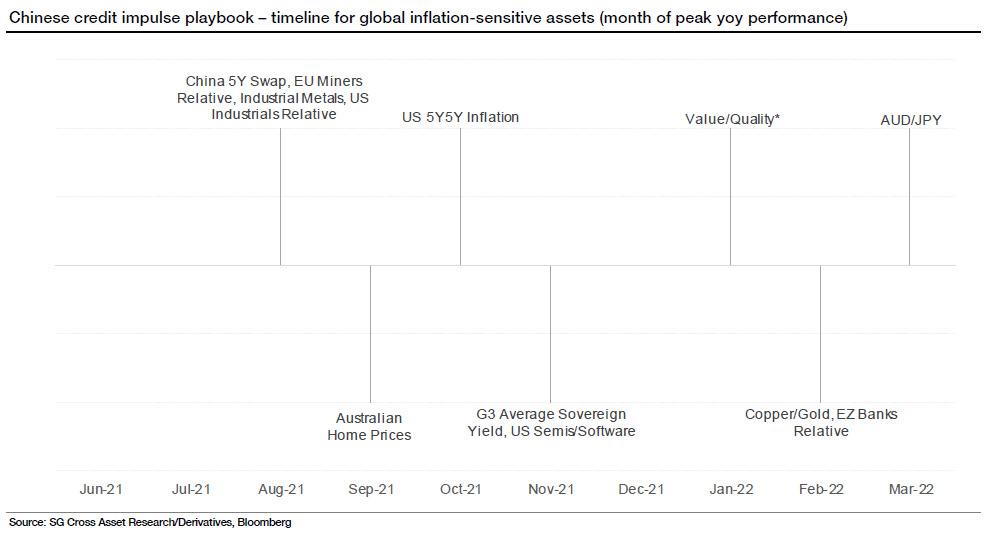

In the chart below, SocGen provides a critical estimated timeline of the peak Y/Y performance for each of the assets it sees as impacted by China’s credit impulse slowdown. While these assets are influenced by multiple factors and therefore could easily diverge from expectations, the chart below does present a neat output from a lagged regression analysis and is a useful guideline for the balance of this year and next.

Bottom line: if the world is hit by the double whammy of continued deleveraging in China which pushes the credit impulse into contraction, coupled with Fed “thinking about thinking about tapering” sometime in late 2021, then all bets are off.

The US House of Representatives has passed a bill called the Protecting the Right to Organize (PRO) Act. If the Senate passes the bill and the President signs it, this would usher in a union labor coup.

It would become illegal for employers to attempt, in any way, to influence employees to not join a labor union or participate in collective bargaining. The bill would overturn right to work laws in 27 states. These laws prohibit unions from requiring workers to join a union, and prohibit unions from forcing non-union members to pay dues.

The bill would also force employers to share employees’ private information with union organizers:

“a voter list to a labor organization… shall include the names of all employees in the bargaining unit and such employees’ home addresses, work locations, shifts, job classifications, and, if available to the employer, personal landline and mobile telephone numbers, and work and personal email addresses.”

And it would allow unions to do away with secret voting, leaving plenty of room for unions to intimidate workers who don’t fall in line.

What this means:

Unions are a big reason why American education has declined substantially against the rest of the world, why it is so hard to hold police accountable for crimes they commit on duty, and why the costs of American-made products are so high.

Labor regulations help unions form a protectionist racket which keeps certain people out of jobs, weakens competition for the best employees, and raises costs for both employers and consumers. It seems like most people realize this, since union membership has been declining for decades. According to the Bureau of Labor Statistics, union membership has declined by almost 3.5 million members since 1983, while the labor force has grown by about 50 million workers.

State laws, like the ones threatened by this legislation, protected workers against unions bullying them into joining and paying dues. So here comes the giant union bailout from the federal government— using the employees’ money.

Regulations like these are bad for the business owner, bad for the employees, bad for the consumers, and bad for the economy. Unions gain more power, but everyone else is left with less choice and less prosperity.

What you can do about it:

There are still some places in the world where the freedom to run a business still exists. Here are a couple jurisdictions which actually go out of their way to attract businesses, and position themselves as commerce and innovation-friendly environments.

Estonia

Since gaining independence from the Soviet Union in 1991, Estonia has positioned itself as a relatively free market jurisdiction. Over the past few years, Estonia has developed e-residency. It’s not actual residency— Estonia sells it as a “digital nation for global citizens.”

They have tailored the product to entrepreneurs, freelancers, digital nomads, and business owners who want remote exposure to European markets, funding, and services.

E-residency is open to anyone in the world, and allows the e-resident to register a business in Estonia. This has certain advantages, like the ability to open a business bank account in the European Union, which could allow non-EU residents to do business in the region more easily.

E-residents also have access to to an online marketplace where they can use services to launch and grow a business. For example, different companies which offer accounting, payment processing, legal advice, and insurance are all available through the e-residency portal. In a sense, Estonia is providing secure online infrastructure for online businesses.

United Arab Emirates

The UAE is home to dozens of free trade and special economic zones, which offer special tax rates and reduced regulation to various types of businesses. For example, Dubai Multi Commodities Centre (DMCC) is a free trade zone with 0% corporate and personal income tax rates, which allows 100% foreign ownership of companies established in the zone. Companies can be owned by a single or multiple owners, and the zone does not restrict the movement of capital out of DMCC.

You do need a physical presence in the zone, but the good news is an approved application to set up your business in the zone also comes with residency for the owner. Most zones operate in a similar way, but cater to specific industries, like e-commerce, media, or technology.

This isn’t to say that either of these options is necessarily right for everyone. The point is that while some governments are making it harder to do business, there are always other jurisdictions happy to attract productive people.

Of course the easiest place to start a business depends on what type of business you want to run.

Industrial manufacturing might lead you to choose a place with fewer labor restrictions (see: union slams Ford for moving production to Mexico), while services and consulting businesses might be able to locate anywhere, and hire contract workers (i.e. Puerto Rico’s 4% corporate tax on businesses exporting services).

If you are in the medical profession, for example, you may want to check out the January Alert (for Sovereign Man: Confidential subscribers) on Medical tourism destinations in Latin America. The reason most of these places can offer inexpensive, high-quality healthcare is because the lack of government restrictions, which translates to easier business start-up for medical professionals.

Although it can be sad to see the US become a less friendly place for businesses and productivity, it should be encouraging that more jurisdictions are positioning themselves to attract productive people and companies.

As long as competition exists, there should always be options— with any luck, more every year.

The Fed tipped its hand today, and unveiled its “viral reaction function” revealing the timetable according to which the Fed will start talking about QE tapering.

As discussed previously, James Bullard, president of the St. Louis Federal Reserve, said in an interview with Bloomberg Television that getting 75% of Americans vaccinated would be a signal that the pandemic was ending, which is a necessary condition for the central bank to consider tapering its bond-buying program. According to our calculations, extrapolating current vaccination rates would mean that – all else equal – we could see the Fed’s 75% bogey be hit in just two short months.

As we further said, one thing Powell did not want to do is give any calendar estimation as to when the Fed could start “thinking about thinking” about tapering. Well, thanks to Bullard, it may have no choice but to do so as soon as the summer. And what’s worse, now that the market is aware of the Fed’s “viral reaction function”, any sharp jump in the vaccination rate will provoke risk off moves as traders start pricing in the inevitable tapering of QE which they now know will be catalyzed by a “normalization” in the pandemic.

A subsequent calculation by Bloomberg came up with a slightly later D-day: as Bloomberg commentator Ye Xie wrote, “at the current rate of inoculation, that threshold could be met by early August, just before the Fed’s Jackson Hole Symposium, a venue known for major policy announcements.”

So assuming the Fed gives markets a couple of months to prepare for the move, the actual tapering could start early next year. That time frame is roughly in line with the median forecast in the Fed’s survey of primary dealers, even though market pricing suggests a more aggressive timetable.

Meanwhile, as we also laid out last week in “China Credit Impulse Set To Collapse As Beijing Orders Banks To Curtail Loan Growth For Rest Of 2021“, China’s stimulus tapering is already under way, with Bloomberg pointing out that “the year-on-year growth of total social financing fell to 12.3% in March, from 13.3% in February and a peak of 13.7% in October. At this rate, the credit impulse, or the change of new credit as a percentage of GDP, could start to shrink by July or August — just as the Fed may lay the groundwork for its own tapering.”

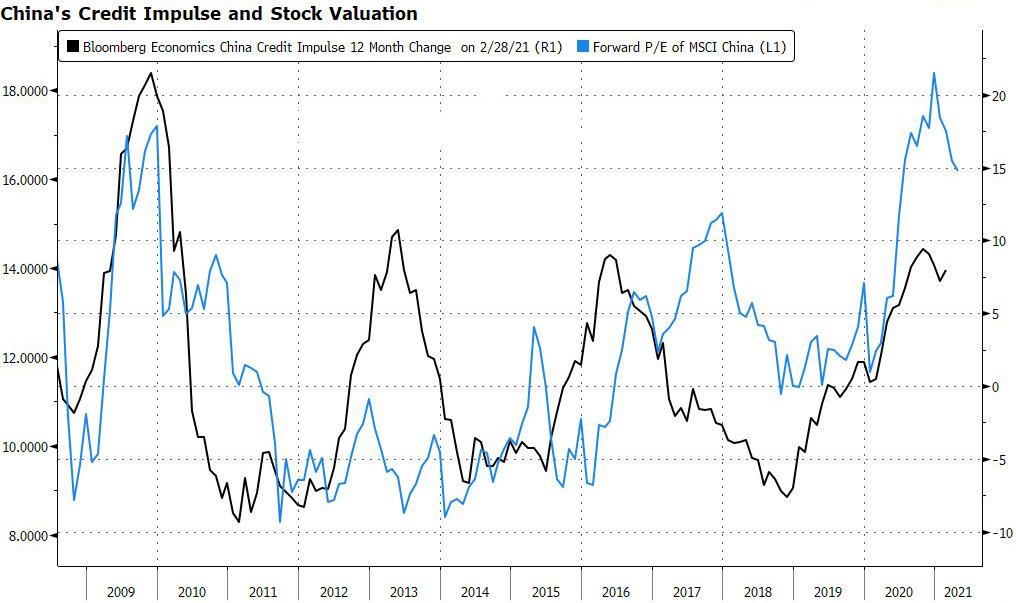

So, as Bloomberg’s Xie concludes, “from a liquidity perspective, the summer could be a challenging time for markets. In the past decade, the slowdown of China’s credit impulse has consistently been accompanied by investors cutting the valuation of the MSCI China Index.”

But it’s not just Chinese stocks that are subject to the monthly injections and drains of the all-important credit impulse: As a reminder, the credit impulse first reaches assets that are driven primarily by the Chinese economy (Chinese bond yields and industrial metals). Next to be impacted are inflation breakevens and sovereign yields in Western economies. The peak correlation for other growth-sensitive assets such as eurozone banks and AUD/JPY arrives with bigger lag of around 4-5 quarters. This result, while logical, is quite significant, as it gives us a playbook for the ebb and flow in Chinese credit impulse.

In the chart below, SocGen provides a critical estimated timeline of the peak Y/Y performance for each of the assets it sees as impacted by China’s credit impulse slowdown. While these assets are influenced by multiple factors and therefore could easily diverge from expectations, the chart below does present a neat output from a lagged regression analysis and is a useful guideline for the balance of this year and next.

House Minority Whip Steve Scalise (R-La.) posted video footage of numerous unaccompanied children being housed in a Donna, Texas, Border Patrol facility and said it’s tantamount to “child abuse.”

“I visited the Donna processing facility yesterday. … This is the devastating result of their disastrous left-wing immigration agenda. RT so everyone can see what they’re trying to hide. This is child abuse,” Scalise wrote on Twitter on April 10.

The video showed what appeared to be possibly hundreds of children covered in aluminum-style blankets, packed next to each other in transparent pens. The sound of people talking loudly in the background can be heard.

A day before releasing the video, Scalise, the No. 2 Republican in the House, posted a video of himself talking near a section of the U.S.–Mexico border.

“This is out of control. It’s the middle of the night. We’ve seen dozens of children flow freely across the border in just the past few minutes,” he said in a tweet as dozens of people who appear to be trying to cross the border illegally walk past him.

🚨 I visited the Donna processing facility yesterday.

These are the videos Joe Biden & Kamala Harris don’t want you to see.

This is the devastating result of their disastrous left-wing immigration agenda.

The Epoch Times has contacted the Department of Homeland Security for comment.

On April 12, the White House reached a deal with Mexico, Guatemala, and Honduras to potentially stem the flow of illegal immigration into the United States, a Biden administration official said.

Special assistant to the President for Immigration for the Domestic Policy Council Tyler Moran said in a TV interview that the administration “secured agreements” that would place “more troops on their” respective borders.

“Mexico, Honduras, and Guatemala have all agreed to do this,” Moran said. “That not only is going to prevent the traffickers and the smugglers and cartels that take advantage of the kids on their way here, but also to protect those children.”

The announcement comes as numerous illegal immigrants have attempted to cross the U.S.–Mexico border in recent months. In March, the U.S. Customs and Border Protection (CBP) encountered more than 171,000 illegal immigrants, including a significant number of unaccompanied children, according to data provided by the agency.

Authorities encountered 18,890 unaccompanied children in March, well above previous highs of 11,475 in May 2019 and 10,620 in June 2014 reported by the Border Patrol, which began publishing numbers in 2009.

More than 4,000 parents and children—mostly unaccompanied minors—have been crammed into a CBP tent complex designed for 250 in Donna, Texas. More than 600 children were packed into a room built for 32 last week, according to Reuters.

China Smartphone Sales Rise 67.7% Despite Semi Chip Shortage

It was just a day ago that we were writing how the automotive industry in China had returned back to its pre-pandemic levels. Now, it looks like, despite a semi chip shortage, the smartphone industry is also roaring back.

According to the China Academy of Information and Communications Technology, smartphone shipments were up 67.7% year over year for March. The huge comp was helped along by last March’s lockdowns across most of Asia due to the pandemic.

For March 2021, 5G mobile phone shipments came in at 27.5 million units, according to Bloomberg. They comprised of 76.2% of all total domestic shipments for the month.

Sales were up despite an ongoing semi chip shortage that has caused chaos not just in the electronics sector, but also in the automotive world, where it has forced numerous automakers to delay production.

Recall, the China Passenger Car Association released auto sales numbers last Friday, indicating that sales are back to levels they were at two years ago, despite still being far below the country’s record set in March 2018.

The demand for electric vehicles was “red hot”, according to The Wall Street Journal. The country sold 437,000 electric vehicle units during the quarter, marking about 8% of the country’s market share. EVs remain in high demand in large cities like Beijing and Shanghai.

SAIC-GM-Wuling Automobile Co., one of GM’s local joint ventures; Tesla; and BYD Co. combined to for 55% of the EV market in March. U.S.-listed Chinese EV startups Li Auto Inc., Nio Inc. and XPeng Inc. combined for sales of just 46,000 cars.

China is expected to head back toward its sales record by 2024, analysts note, as recent weak performance of the country’s stock market has zapped citizens’ purchasing power.

China Smartphone Sales Rise 67.7% Despite Semi Chip Shortage

It was just a day ago that we were writing how the automotive industry in China had returned back to its pre-pandemic levels. Now, it looks like, despite a semi chip shortage, the smartphone industry is also roaring back.

According to the China Academy of Information and Communications Technology, smartphone shipments were up 67.7% year over year for March. The huge comp was helped along by last March’s lockdowns across most of Asia due to the pandemic.

For March 2021, 5G mobile phone shipments came in at 27.5 million units, according to Bloomberg. They comprised of 76.2% of all total domestic shipments for the month.

Sales were up despite an ongoing semi chip shortage that has caused chaos not just in the electronics sector, but also in the automotive world, where it has forced numerous automakers to delay production.

Recall, the China Passenger Car Association released auto sales numbers last Friday, indicating that sales are back to levels they were at two years ago, despite still being far below the country’s record set in March 2018.

The demand for electric vehicles was “red hot”, according to The Wall Street Journal. The country sold 437,000 electric vehicle units during the quarter, marking about 8% of the country’s market share. EVs remain in high demand in large cities like Beijing and Shanghai.

SAIC-GM-Wuling Automobile Co., one of GM’s local joint ventures; Tesla; and BYD Co. combined to for 55% of the EV market in March. U.S.-listed Chinese EV startups Li Auto Inc., Nio Inc. and XPeng Inc. combined for sales of just 46,000 cars.

China is expected to head back toward its sales record by 2024, analysts note, as recent weak performance of the country’s stock market has zapped citizens’ purchasing power.