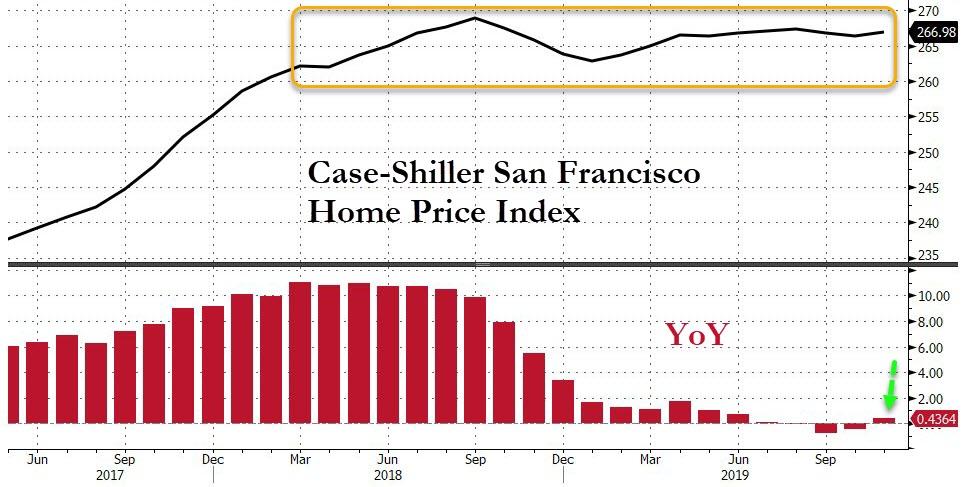

US Home Prices Accelerate At Fastest Pace In 9 Months

Case-Shiller home price gains have re-accelerated over the last 3 months and analysts expected another acceleration in November (the latest data set) and were right as the 20-City Composite surge 2.55% YoY (better than the +2.40% YoY expectation).

This is the biggest YoY rise since Feb 2019…

Source: Bloomberg

Home prices climbed 0.5% from the previous month – also topping forecasts – matching the October increase for the best back-to-back gains since early 2018.

All 20 cities in the index showed year-over-year home-price gains, led by Phoenix; Charlotte, North Carolina; and Tampa, Florida.

After dropping YoY in September and October, the mecca of all things socially just and tech-savvy – San Francisco – saw prices adjust higher and back into the green YoY…

Source: Bloomberg

Finally, a broader national index of home prices was up 3.5% from a year earlier, the most since April.

Rabobank: “What If We Are On The Brink Of An Exponential Increase In Coronavirus Cases?”

Submitted by Rabobank’s Michael Every

The beginning of 2020 starts to look alarmingly similar to 2018. Back then the US stocks extended their impressive 2017 gains in the first few weeks of trading only to plunge at the end of January and sustain heavy losses in the first half of February. In that period the S&P 500 Index plunged almost 12% from the peak to trough on the back of rising concerns that inflation may rise much faster than initially anticipated forcing the Fed to accelerate the pace of monetary policy tightening. It was just a taste of what was to come as 2018 proved to be a tumultuous year for the US equities which set record highs in September only to end the year deep in the red.

Back to 2020, global stocks are in a risk off mode amid escalating concerns about the coronavirus. The S&P 500 Index plunged 1.57% on Monday trimming its year-to-date gains to just 0.40%. One could argue that this is just a correction from seriously stretched levels that will ultimately prove as an opportunity to buy stocks on the back of an assumption that the Chinese officials will, eventually, get on top of the coronavirus.

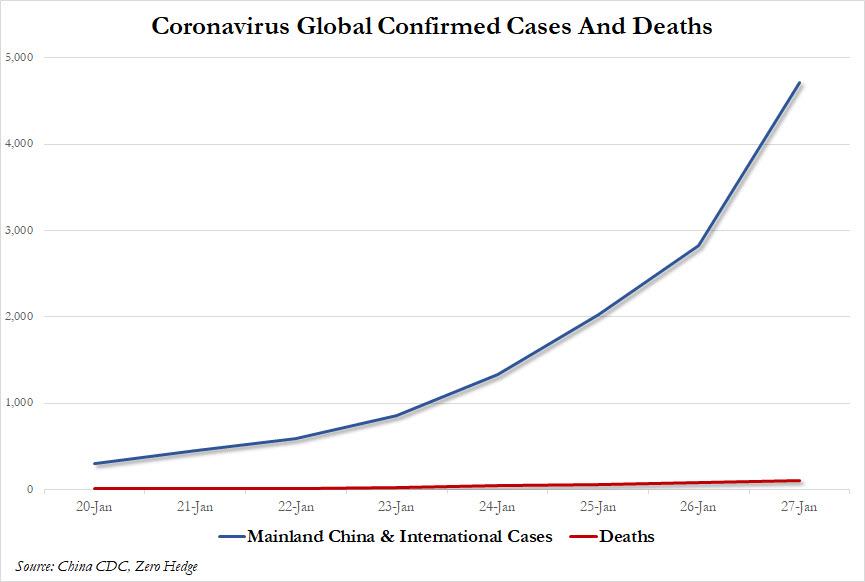

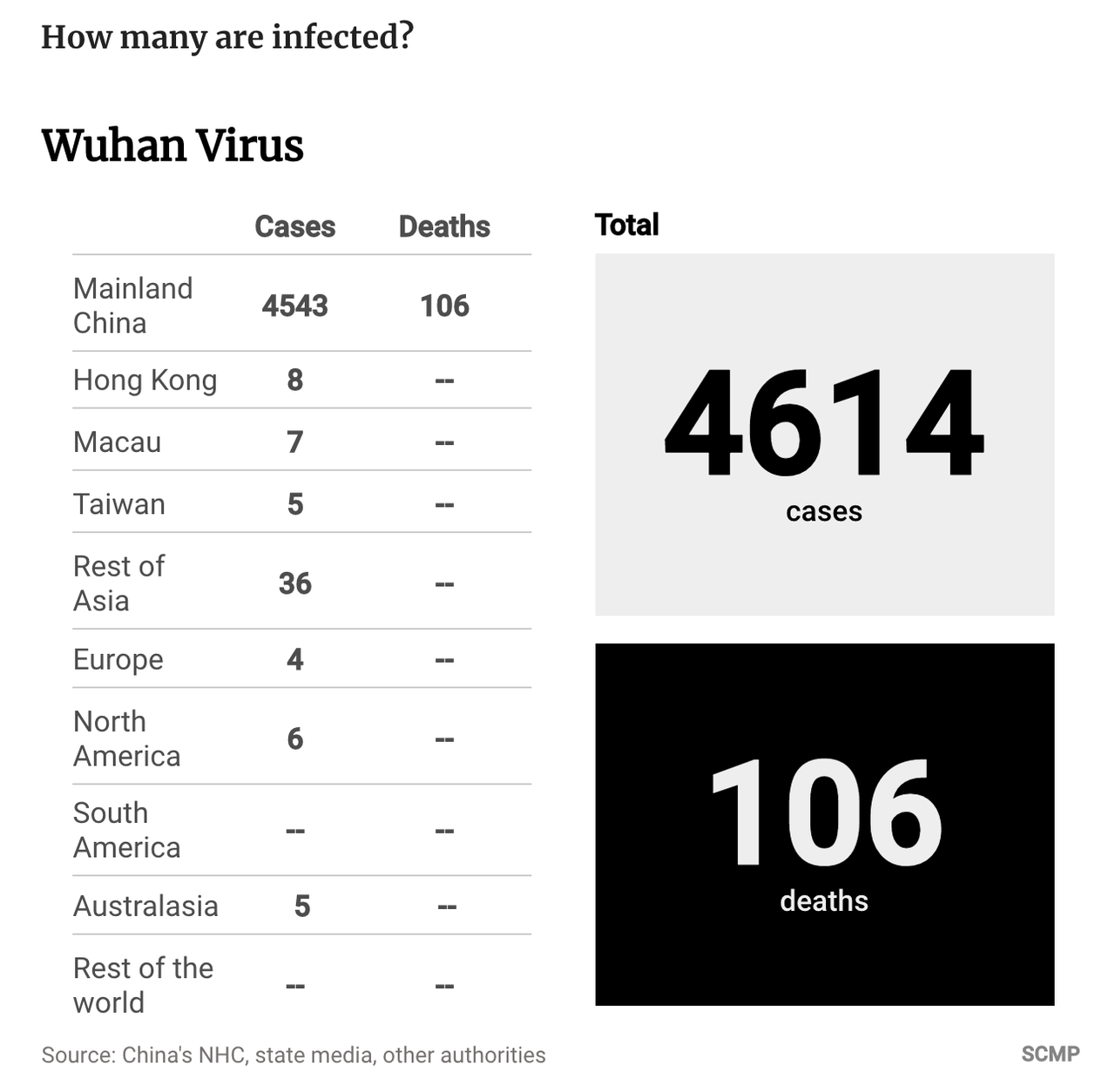

However, it is extremely difficult to estimate the negative impact on the Chinese economy at a time when the death toll is rising sharply (106 so far) and the number of confirmed cases is soaring (4,515 as of today). More than 50 million people in China are now in a lockdown.

It is also worth considering the following: what if we are on the brink of an exponential increase in the number of people affected by the deadly virus? One could argue that we have already reached this stage given that confirmed cases reportedly increased by 65% over the past few days.

There is more evidence that the coronavirus has an incubation period of about two weeks before those infected start to show signs of the illness in a country where half a billion people travel at this time of the year. While travel restrictions have been put in place, it could be too late. The worst may yet to come despite the best efforts by the Chinese authorities to contain the virus.

Market concerns about severe impact on China and the global economy are reflected in rising demand for safe haven assets. The yield on the 10-year US Treasury plunged below the trendline support from the September low. The October low at 1.5051% is the next level to watch ahead of 1.4272% (2019 low).

The US dollar is the beneficiary of growing demand for Treasuries. The Bloomberg Dollar Index is on the cusp of breaking above the trendline resistance at 1200. A bullish breakout in the USD Index would provide USD/EM crosses with even strong upside momentum. Commodity currencies have been the most impacted so far. The plunge in oil prices to the lowest level so far this year provided USD/RUB with sufficient upside traction to revisit the December 23 high at 63.1057. USD/RUB was leaning lower this morning, but the upside bias is likely to prevail in the coming days with 64.49 as the next potential target for USD/RUB.

Looking more broadly at the EM space, the pace of capital inflows into risky assets slowed down last week when concerns about the coronavirus increased. Exchange-traded funds focused on emerging markets attracted USD 311.7mn in the week ending January 14 – this was significantly lower than USD 3.16bn in the previous week, Bloomberg reported. The impressive run of 16 consecutive weeks of inflows may come to an end if risk aversion continues to rise.

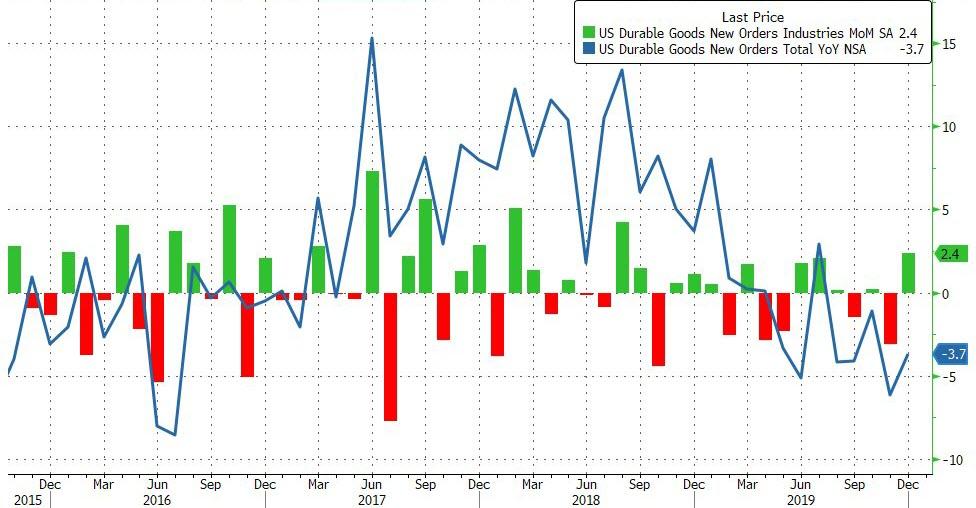

Boeing Implosion Leads To Worst Aircraft Orders In 11 Years, With GDP Collapse On Deck

After November’s big downside surprise in Durable Goods Orders, analysts hoped for a modest rebound in December but preliminary data showed a huge rebound (up 2.4% MoM vs +0.3% MoM expected).

Additionally the 2.1% drop in November was revised even further down to -3.1% MoM.

Source: Bloomberg

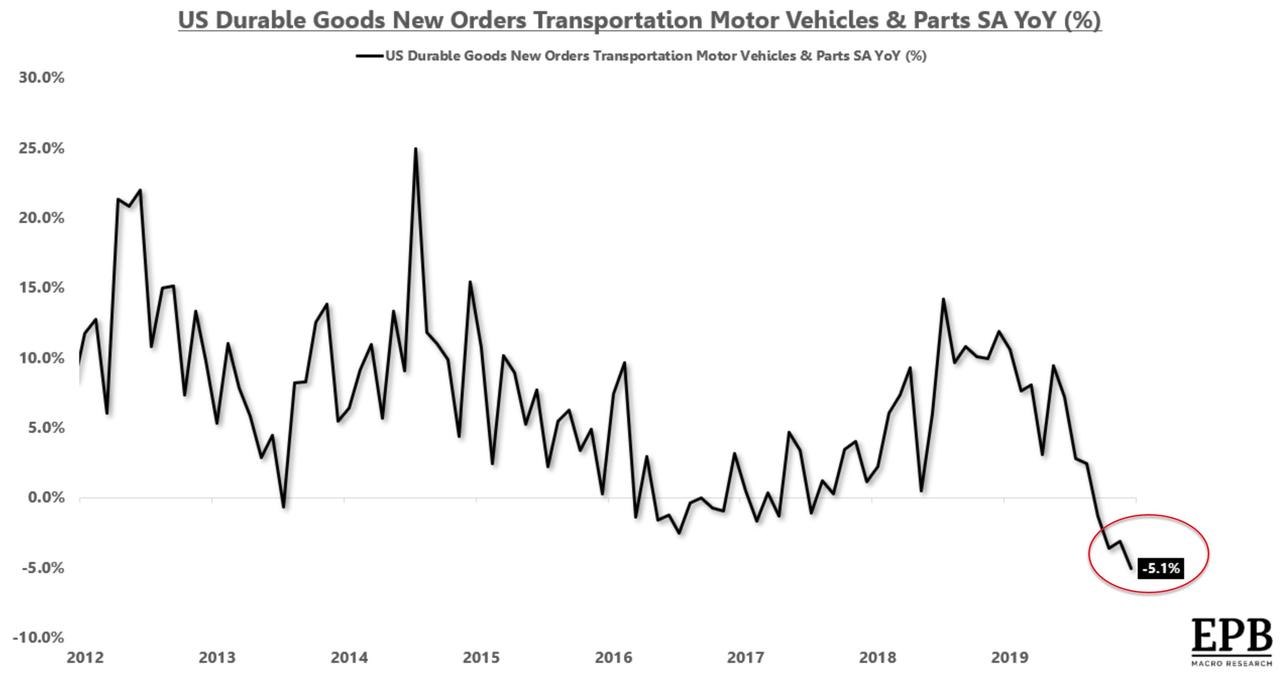

Motor Vehicles and Parts orders plunged YoY..

However, if we remove Defense spending (a 168.3% surge in Defense Aircraft New Orders), durable goods orders remain ugly…

Source: Bloomberg

Thanks to a 75% collapse in Non-Defense Aircraft New Orders…its lowest level since 2009 as Boeing implodes.

Source: Bloomberg

There goes GDP!

None of which should be a surprise, as we noted previously, Boeing’s production cuts will cut Q1 GDP growth by a third.

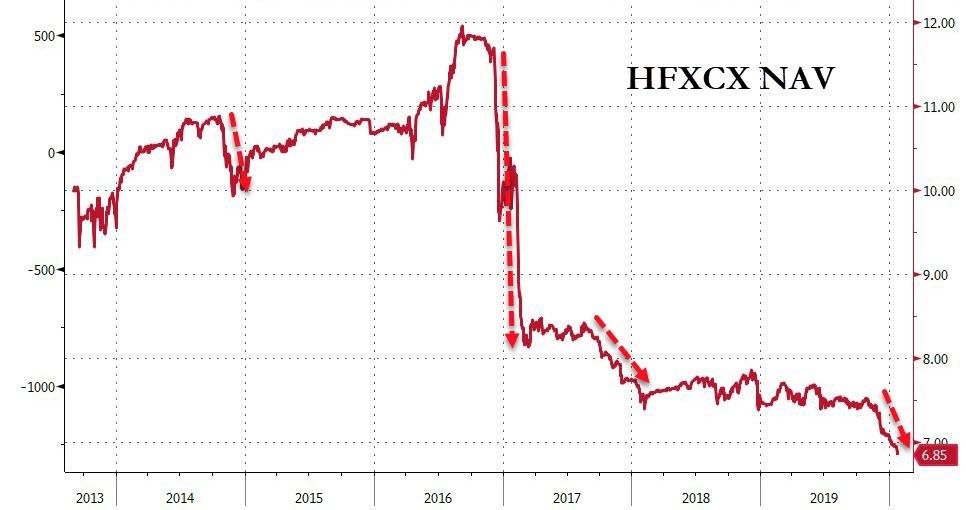

Multi-Billion Levered Options Strategy Fund Finally Faces The Music For Fraud

Three years ago, we first introduced the world to Catalyst Capital, and its Hedged Futures Strategy Fund, which wasn’t a managed futures fund after all…

“It was miscategorized,” said Morningstar (MORN) analyst Jason Kephart, noting that Morningstar analysts don’t cover the fund. The Catalyst fund uses put and call options on Standard & Poor’s 500 stock futures, with the aim of reducing volatilty and overall correlation to the blue-chip index.

Morningstar moved the fund into the options writing category Feb. 1, Mr. Kephart said.

Catalyst Capital CEO Jerry Szilagyi told Bloomberg in Feb 2017:

“It’s just people looking to sensationalize things and make headlines,” adding that “our exposure was greatly exaggerated, and our impact on themarket was greatly exaggerated.“

Which rang a bell to more than a few…

Bear Stearns CEO Alan Schwartz goes on CNBC in March 2008 and assures viewers that the firm has ample liquidity. “Part of the problem is that when speculation starts in a market that has a lot of emotion in it,” Schwartz says he has numbers to back up his insistence that the bank’s position is solid.

As we mocked at the time, the first rule of crisis management… “blame the speculators”

Catalyst Capital Advisors LLC (CCA) and its President and Chief Executive Officer, Jerry Szilagyi, agreed to pay a combined $10.5 million to settle the charges…

…although CCA told investors that it abided by a strict set of risk parameters for the Catalyst Hedged Futures Strategy Fund, it breached those parameters and failed to take the required corrective action during a majority of the trading days between December 2016 and February 2017.

As alleged, the fund lost hundreds of millions of dollars – approximately 20% of its value – from December 2016 through February 2017 as markets moved against it. The SEC’s complaint against Walczak alleges that he told investors that the fund employed a risk management strategy involving safeguards to prevent losses of more than 8%, when in fact no such safeguards limited losses and Walczak did not otherwise consistently manage the fund to an 8% loss threshold.

“CCA’s misrepresentations, and Walczak’s alleged departure from his stated approach to managing risk, deprived investors of accurate information about an important aspect of the fund’s management.”

In parallel action, the Commodity Futures Trading Commission (CFTC) today announced settled charges against CCA and Szilagyi, and a district court action against Walczak.”

Finally, we note that Feb 2017’s unprecedented decoupling between fundamentals, flows, bond yields, and in fact anything else that was in any way rationally discounting risk mimics the recent few months of farce that has been evident in the so-called markets as gamma built up and the virtuous cycle escalated stock prices to record high valuations.

The funny thing is – just like in Feb 2017 – Catalyst Capital was seeing a massive liquidation as the collapse in its assets under management suddenly accelerated once again…

Source: Bloomberg

The fund’s net asset value tumbled…

Source: Bloomberg

And its NAV’s decline perfectly synced with the surge in the stock market – as once again – the fund’s strategy forced them to buy more and more as prices rose, sustaining the rally…

Source: Bloomberg

And as is clear from the chart above, the decoupling in the last couple of days suggests things are about to get a little hectic for this strategy.

So, was Catalyst’s fund once again the driver of irrational buying panics as it liquidated its positions with forced buying into ever-rising index prices? We will see…

2000 vs. 2020: The Role Of Monetary And Fiscal Policies In Stock Market Cycles

Submitted by Joe Carson, former Chief Economist & Director of Global Economic Research for Alliance Bernstein

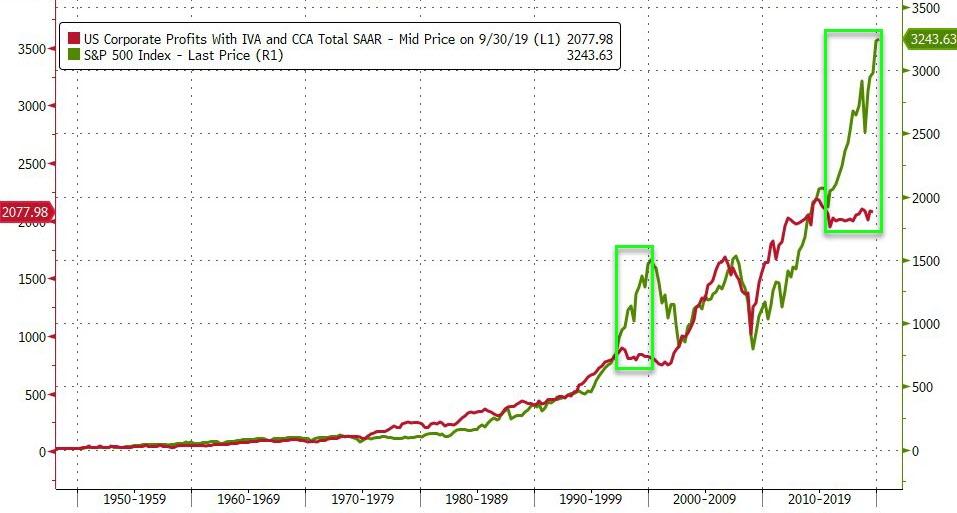

The equity market of 2020 has some of the lofty valuation features that showed up at the peak of 2000 cycle. Yet, a key difference is the accommodative stance of monetary and fiscal policies nowadays versus the restrictive stance of 2000. So, the key question for investors is how does the monetary and fiscal policy backdrop influence the investment outlook? Do friendly policies create the potential for even more elevated valuations, to last longer, or is it merely a mirage shifting the focus of investors attentions to the upfront benefits and away from the longer term fundamentals of earnings and portfolio risks?

Equity Markets 2020 vs. 2000

There are a number of macro measures that are often used to assess how expensive or cheap the equity markets are at any point in time. None of these are hard barriers that can’t be exceeded – as all records in finance (like in sports) tend to get broken eventually – but they do offer a perspective on the market valuation relative to past cycles.

For example, the S&P 500 price to sales ratio hit a record high of 2.16 at the beginning of 2000 and has now been exceeded for the first time by the current reading of 2.25X.

Similarly, the market valuation of domestic companies to Nominal GDP – a metric that compares equity prices to overall economic growth – stood at a record 1.85X in 2000 and at the start of 2020 it is estimated that this metric has matched or slightly exceeded the highs of 2000.

Both of these measures suggest that the equity market is expensive. But, critics would argue that favorable monetary and fiscal backdrop makes these measures less excessive than they appear at first glance.

To be fair, there is evidence to support their case. In 2000, for example, monetary and fiscal policies were draining liquidity, the lifeblood of all equity cycles. At the start of 2000, the fed funds rate stood at 5.5%, well above the underlying inflation rate suggesting a restrictive policy, and policy became even more restrictive as policymakers raised official rates three times, by a total of 100 basis points to 6.5% by the end of Q2.

The fiscal stance in 2000 was also restrictive as the federal budget was in surplus, an indication that the federal government was taking more money away from the economy than it was adding.

In 2020, monetary and fiscal policies are stimulative, evident by very low interest rates and a trillion dollar budget deficit. Moreover, these policies directly and indirectly spurred a demand and supply imbalance in finance, favoring equities relative to cash and fixed income assets.

For example, the 2017 tax cut for corporations triggered a windfall in cash flow enabling a number of companies to fund a large share buyback reducing the supply of equities. At the same time, the policy of low official rates along with the promise of low rates for the foreseeable future directly increased the demand for equities by the increasing the value of the future stream of potential earnings and at the same time diminished the current and expected returns on fixed income assets.

So it is fair to say that monetary and fiscal policies nowadays have created a more favorable environment, at least temporarily, for the equity markets. But has these policies fundamentally altered the long-term investment outlook and eliminated valuation and portfolio risks? The answer is no.

First, the operating profits of companies have not improved. The GDP measure of operating profits (before tax) has not increased for the past 5 consecutive years, and that’s one more than the 4 years of flat profit growth before the run-up of the equity markets in 2000.

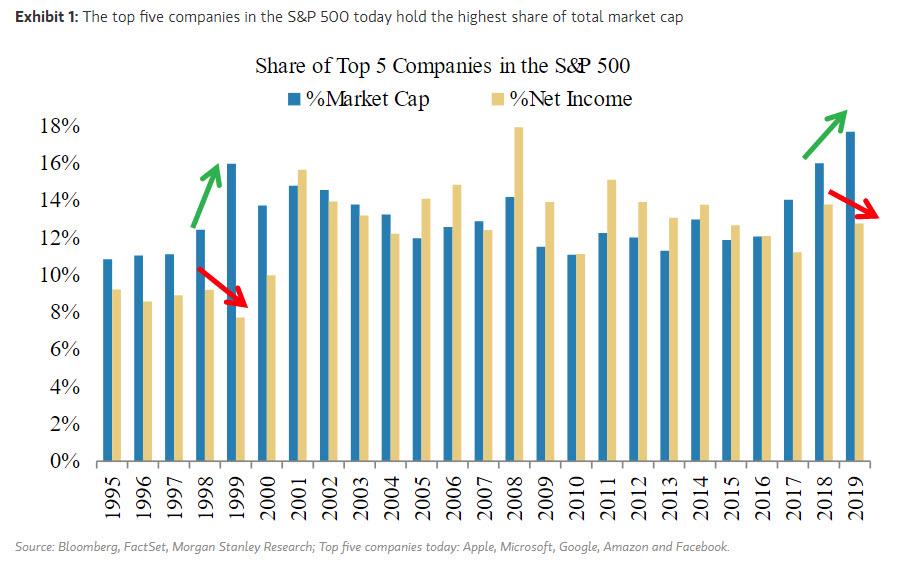

Second, the equity markets nowadays shows a more concentrated form of excessive valuation. For example, there are four trillion dollar companies, Apple, Google, Microsoft and Amazon, and when combined these companies market valuation account for roughly 13% of all domestic companies (the top five companies account for a record 18% of the S&P’s market cap). Moreover, the combined price to sales ratio of these 4 companies is over 5 – more than double than the overall market.

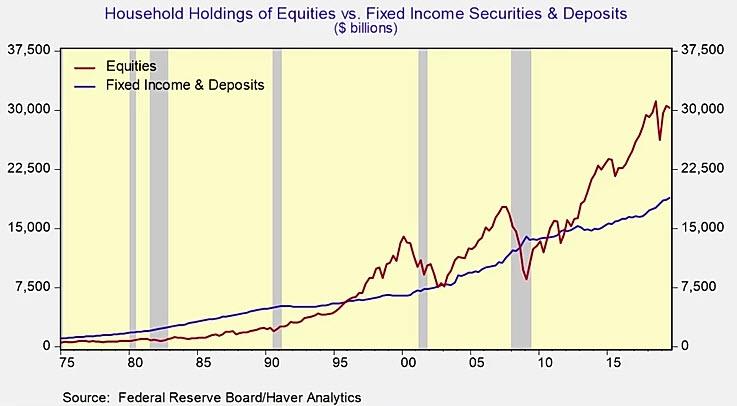

Third, the direct and indirect effects of these policies have greatly increased household portfolio risks by elevating the share of equities. In each of the last two finance/asset driven recessions households holdings of equities dropped below the levels of cash deposits and fixed assets – and if that happened again the wealth loss would be greater than equity declines of the tech and housing bubbles combined.

The final script of the role of monetary and fiscal policies in the current equity market cycle has not been written. The upfront benefits of these policies are clearly visible in equity market valuations, but the concentrated form of excessive valuations and its direct link towards household large exposure of equities does create new risks in the outlook.

In 2000, the draining of liquidity sank the equity markets.

In 2020, it could well be that the inflow of liquidity from policies became too concentrated that the equity market fell under its own excess weight triggering negative ripple effects through all segments of finance and the economy.

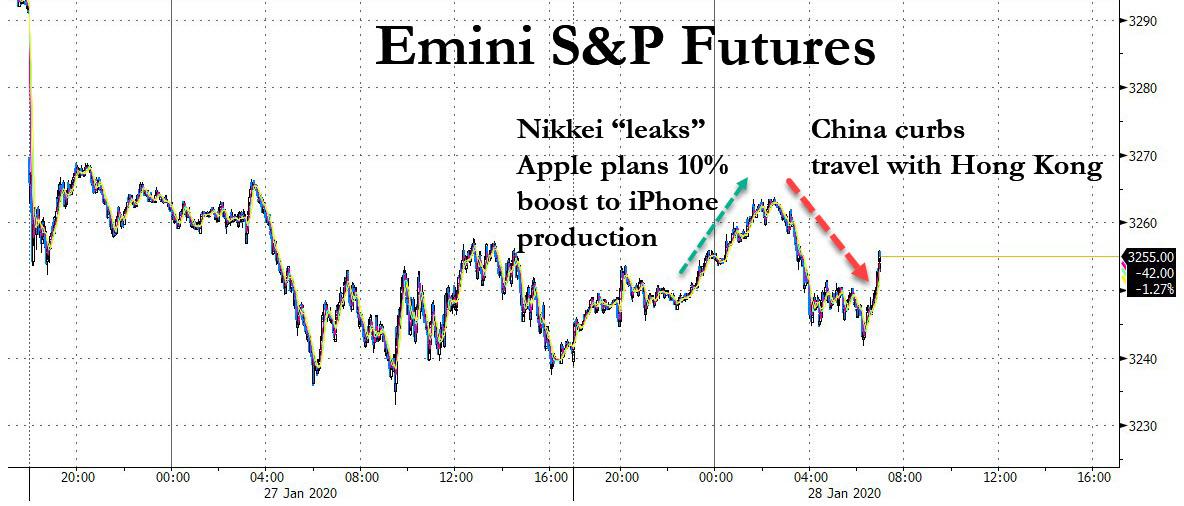

Futures Rebound On Apple Hail Mary Leak Despite Mounting Coronavirus Fears

After yesterday’s global stock selloff, the worst since early October, US index futures and European stocks staged a comeback and edged higher as investors digested the latest international efforts to contain the Coronavirus like virus from spreading, including curbs on travel between China and Hong Kong.

With all eyes on Apple today ahead of its earnings report, the world’s biggest company which single-handedly carried the weight of the S&P ascent for the past 5 months, leaked a report via the Nikkei that it had asked its suppliers to make up to 80 million iPhones over the first half of this year, a 10% increase over on last year’s production schedule that, as the Nikkei tactically added “could boost the company’s near-record share price.”

Sure enough, the news helped send AAPL stock rebound over 1% from yesterday’s rout and pushed both S&P and Nikkei future after the report hit, just before midnight.

However, much of the gains were promptly lost after Hong Kong Chief Executive Carrie Lam said the city will close some border checkpoints and restrict flights and train services from the mainland. The outbreak has shattered a calm in markets that hadn’t seen a 1% up-or-down move in the S&P 500 since early October. The latest surge in demand for havens also sent bond yields tumbling, with the global supply of notes with negative rates surpassing $13 trillion, to the highest since November according to Bloomberg.

After rising as much as 0.5% in early trading on the Apple news following a Monday pullback that wiped out around 180 billion euros of market capitalization from the European companies index, the European Stoxx 600 index gave up the as miners extend a decline and travel-and-leisure shares turn negative after news that China will stop individual travelers to Hong Kong to curb the spread of coronavirus.

Airbus was the biggest boost to the benchmark index, after the planemaker agreed to reach a settlement with French, British and U.S. authorities regarding a probe into allegations of bribery and corruption. “It’s just a rebound as markets await further information on what’s happening with the virus situation in China,” said Russ Mould, investment director at broker AJ Bell. “We’re moving into the results season with some European heavyweights slated for today, central bank meetings this week and Brexit on Friday. There is lots to keep people occupied.”

Shares of Europe’s most valuable technology company SAP dropped 2.5% as the software provider’s in-line results failed to impress investors. Some analysts also pointed to the company’s slowing cloud revenue growth. Dutch firm Philips slipped 1.3% after the health technology company’s quarterly sales fell short of estimates. The company is also said it was looking to sell its domestic appliances division. Among lenders, Swedish bank Swedbank gained 3.3% after a better-than-expected fourth quarter profit while Spain’s state-owned lender Bankia slipped 3.3% after a wider-than-expected quarterly loss.

Earlier in the session, Asian stocks declined, led by materials and energy, as investors weighed the fallout from the spread of the deadly coronavirus. The MSCI Asia Pacific Index fell for the fourth-straight day, its longest run of losses since September. Japanese shares fell for a second day and South Korean stocks sank as that market reopened after holidays. Most markets in the region were down, with South Korea’s Kospi Index plunging the most since October 2018, led by tourism-related stocks. Singapore’s Straits Times Index had its biggest drop since August. Investors who took holidays yesterday returned to a further increase in the coronavirus death toll, infections and geographic spread. Trading is set to resume in Hong Kong Wednesday; the latest guidance from China, where the outbreak is still concentrated, is for markets to reopen Monday.

“Risk appetite is unlikely to improve until we start getting news that the virus is under control,” DBS Group Holdings Ltd. strategists Philip Wee and Eugene Leow wrote in a note. “For now, the lack of positive news flow is likely to keep investors on the defensive.”

In FX, the Bloomberg Dollar Spot Index steadied and haven currencies reversed losses after China restricted travel to Hong Kong. The pound slipped with commodity-related currencies while currency volatility extended gains for near-term options. The offshore yuan fluctuated after a sharp slide the previous day while the yen nudged higher for a sixth session.

In rates, Treasuries first gained, with the yield on the 10Y sliding as low as 1.57% before reversing, and the 10Y was trading at 1.62% last.

In commodities, crude oil declined.

In addition to keeping a close watch on Coronavirus headlines – because even as containment efforts intensify, the likelihood of the virus disrupting global businesses and the world’s second-largest economy appears to be growing – investors are keeping an eye out for a slew of earnings due this week including from Apple, Pfizer, United Technologies and Lockheed on Tuesday. Durable goods orders and consumer confidence are among economic data due.

Market Snapshot

S&P 500 futures up 0.3% to 3,249.00

STOXX Europe 600 up 0.01% to 414.11

MXAP down 0.9% to 169.09

MXAPJ down 1% to 549.15

Nikkei down 0.6% to 23,215.71

Topix down 0.6% to 1,692.28

Hang Seng Index up 0.2% to 27,949.64

Shanghai Composite down 2.8% to 2,976.53

Sensex down 0.5% to 40,939.43

Australia S&P/ASX 200 down 1.4% to 6,994.46

Kospi down 3.1% to 2,176.72

German 10Y yield fell 1.6 bps to -0.401%

Euro down 0.04% to $1.1015

Brent Futures down 1% to $58.74/bbl

Italian 10Y yield fell 19.3 bps to 0.871%

Spanish 10Y yield fell 1.5 bps to 0.266%

Brent futures down 0.6% to $58.69/bbl

Gold spot down 0.2% to $1,579.52

U.S. Dollar Index up 0.04% to 98.00

Top Overnight News from Bloomberg

The outbreak of the deadly coronavirus threatens to derail a fragile stabilization in the world economy, which had appeared poised to benefit from the phase one U.S.-China trade deal, and signs of a tech turnaround.

The director-general of the World Health Organization is visiting Beijing to assess China’s response to the coronavirus as the death toll climbs to at least 100. Global efforts to curb the spread of the disease have intensified. Companies including Honda Motor Co. are evacuating workers from areas of China hardest hit by the outbreak. The U.S. said citizens should reconsider travel to China, while Hong Kong announced the temporary closing of all sports and cultural facilities starting Wednesday

President Donald Trump’s lawyers avoided the explosive allegation in former National Security AdvisorJohn Bolton’s book that the president tied aid to Ukraine to an investigation of a political rival as they sought to undermine the House impeachment case. Sen. Mitt Romney says four GOP senators may back Bolton testimony, according to Reuters

Oil extended declines after closing at the lowest level since mid-October as the coronavirus hits China’s economy and threatens to crimp worldwide energy demand. Libya says oil output may almost fully halt within days

The Taliban claimed responsibility for the downing of a “special American aircraft” flying over Afghanistan on what it described as an intelligence mission, while the U.S. military said there was no indication the plane was hit by hostile fire

Prime Minister Shinzo Abe nominated economist Seiji Adachi to the Bank of Japan policy board amid growing attention over his stance on monetary easing

America’s longest-serving secretary of state, Cordell Hull, is best known for winning the Nobel Peace Prize for his role in establishing the United Nations at the end of World War II. Today, 75 years later, another important piece of his legacy, the World Trade Organization, looks increasingly at risk as President Donald Trump realigns the U.S.’s relationships.

One way the rich get richer is through inheritance, and they’re barely paying taxes on it. Americans are projected to inherit $764 billion this year and will pay an average tax of just 2.1% on that income, New York University law professor Lily Batchelder estimates in a paper published Tuesday by the Brookings Institution.

Hefty losses were suffered across Asia-Pac bourses as virus-induced fears caught up to several indices on their return from the extended weekend and which followed Wall St’s worst performance in nearly 4 months. ASX 200 (-1.4%) traded subdued as the energy and mining related sectors led the declines due to concerns of the impact to demand and growth from the virus epidemic, although gold stocks bucked the trend after the recent safe-haven bid for the precious metal and defensives were also resilient in the downturn. Nikkei 225 (-0.5%) was pressured by the outbreak jitters as the number of confirmed cases in China rose to 4515 and total deaths at 106, considering that the Chinese account for around 30% of foreign tourists to Japan. KOSPI (-3.1%) and Singapore Straits (-2.5%) slumped in their first trading session after the Lunar New Year in reaction to the increased number of virus cases confirmed in China and their individual countries, while India’s NIFTY Index (Unch.) was indecisive with earnings the main driver for domestic stocks. Finally, 10yr JGBs were flat amid slight fatigue from the recent extended rally and after mixed results at today’s 40yr JGB auction, although downside was also restricted due to the sell-off across regional stocks.

Top Asian News

Abe Taps Seiji Adachi to Replace BOJ Board Member Harada

Afghan Troops Clash With Taliban to Access U.S. Plane Crash Site

Carrie Lam Says China to Stop Individual Travelers to Hong Kong

Japan Finds Coronavirus in Person With No Wuhan Contact: Jiji

Overall a mixed session thus far in the European equity space [Eurostoxx 50 +0.1] following on from a predominantly downbeat APAC handover as coronavirus jitters hit multiple bourses on their return from holidays. For reference, Hong Kong confirmed that its stock markets will trade as normal on January 29th, whilst Shanghai and Shenzen return on February 3rd. Back to Europe, FTSE MIB (+0.5%) outperforms its peers amid further tailwinds from the weekend’s regional election which diminished the chance of a snap election in the country. Meanwhile, Netherland’s AEX (-0.2%) modestly lags following earnings from Philips (-2.7%) after reporting sub-par earnings, albeit the company noted that it is reviewing options for its domestic appliances’ business. Philips holds a 6.2% weighting in the Dutch bourse. Sectors are mixed with no clear reflection of the overall risk-tone, although the IT sector (-0.9%) underperforms on account of earnings from SAP (-2.7%), despite what seemed to be positive on the surface. The DAX-giant (accounts for 10.5% of the index) raised profit revenue guidance but narrowed its all-important 2020 cloud sales to the range of EUR 8.7-9.0bln from the prior EUR 8.6-9.1bln. In terms of stock specifics – Airbus (+1.2%) rose in excess of 2% at the open the Co. reached a deal to settle corruption probes. Meanwhile, Bayer (+0.6%) shares remain supported amid a positive broker move at MainFirst Bank. As a reminder, 14 DJIA companies will be reporting this week, with today’s slate including 3M (4.17% weighting), Pfizer (0.95% weighting) and United Technologies (3.59% weighting) before market open followed by Apple (7.3% weighting) after the bell.

Top European News

Swedbank Promises Dividends Won’t Fall as Compliance Costs Swell

Greece to Issue 15-Year Debt for First Time in More Than Decade

Johnson Walks Huawei Tightrope as U.K. Sets Up Clash With Trump

Turkey Stocks Reverse Gains as Risk-Off Sentiment Halts Recovery

In FX, The traditional safe havens are back in vogue following a transitory and tame recovery in risk sentiment, as the Chinese coronavirus continues to unnerve markets amidst reports of the outbreak reaching further beyond the region. The Dollar is in demand almost across the board as a result, with the DXY pivoting 98.000 and briefly crossing Fib resistance just above the big figure at 98.011 before topping out at 98.035 in part due to fractional outperformance in the Franc and Yen that are holding above 0.9700 and 109.00 respectively. Conversely, Gold has handed back some of yesterday’s gains, but remains relatively well bid within a tight Usd1577-1583/oz range and technically bullish around 20 Bucks over last Friday’s circa Usd1566.62 low.

AUD/NZD/GBP – The major losers on a combination of contagion from China and cross flows for month end as the Aussie teeters around 0.6750 and not far from deeper troughs posted last October ahead of 0.6700, Kiwi hovers close to the base of 0.6550-22 parameters and Sterling skirts 1.3000. Aud/Usd and Nzd/Usd are still inversely correlated to moves in Usd/Cnh-Cny on breaking virus updates in the absence of official daily PBoC settings during the Lunar New Year break, with the Yuan inching nearer the 7.0000 mark again having reached peaks beyond 6.8500 only 8 days ago on the crest of the Phase 1 trade deal signing. Meanwhile, Cable is trading cautiously into Thursday’s BoE/MPC rate announcement and Brexit the day after, as market contacts note RHS interest in Eur/Gbp for month end that has lifted cross through 0.8450.

EUR/CAD/SEK/NOK – The Euro has survived another test of bids/support into the 1.1000 level, partly on the purported orders for January 31 noted above, but perhaps also benefiting from the common currency’s semi-safe haven status, while the Loonie has extended losses alongside the Norwegian Krona amidst yet another decline in crude prices. Usd/Cad has absorbed more offers at 1.3200, though not all and supply is said to be stacked up to 1.3210, while Eur/Nok has been up to 10.1155 and higher than Eur/Sek in percentage terms after mixed Swedish data in the form of retail sales, trade and ppi saw the latter briefly breach a Fib (10.6121), but not really threaten the 200 DMA (circa 10.6400).

In commodities, another subdued European session for WTI and Brent font-month futures, as the benchmarks pare overnight gains amid the overhang of the coronavirus outbreak. WTI Mar’20 futures have given up their 53/bbl+ status (vs. overnight high of 53.25/bbl) and drifts towards mild support at 52.70/bbl. Meanwhile, its Brent counterpart hovers around 58.75/bbl (vs. overnight high of 59.35/bbl) ahead of yesterday’s low of ~58.50/bbl. OPEC sources noted that Russia has been keen to exit from the agreed upon OPEC+ cuts, but they would be prepared to stay on-board in the event that prices drop below USD 60/bbl. Heading into tonight’s weekly API private crude inventory release, desks note that the complex will likely focus more on the virus developments. Nonetheless, the release is expected to show a build of 300k barrels in crude stocks, gasoline a build of 1.5mln and distillates a draw of 1mln – according to some data vendors. For reference, Barclays note that the further virus woes could see a USD 2/bbl impact on oil process on the potential economic fallout, meanwhile, UBS retains its positive outlook on oil prices in H2 2020, with Brent recovering to USD 64/bbl – recommends investors with high-risk tolerance to sell downside in Brent from USD 50/bbl. Elsewhere, spot gold trades relatively lacklustre around the 1580/oz mark ahead of mild support ~1577/oz – ABN AMRO warn investors of a possible price correction in the coming weeks, while remaining bullish on the lustrous metal in the longer-term. Copper prices have continued bleeding amid the global-growth implications of the virus outbreak – as prices remain sub 2.60/lb (vs. Jan high of 2.87/lb) and around levels seen last October.

US Event Calendar

8:30am: Durable Goods Orders, est. 0.35%, prior -2.1%; Durables Ex Transportation, est. 0.3%, prior -0.1%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.15%, prior 0.2%; Cap Goods Ship Nondef Ex Air, est. 0.2%, prior -0.3%

9am: S&P CoreLogic CS US HPI YoY NSA, prior 3.34%; CS 20-City YoY NSA, est. 2.4%, prior 2.23%

9am: S&P CoreLogic CS 20-City MoM SA, est. 0.4%, prior 0.43%; 20-City NSA Index, prior 218.4

10am: Richmond Fed Manufact. Index, est. -3, prior -5

DB’s Jim Reid concludes the overnight wrap

Morning from Brussels, after a day in Luxembourg yesterday. If you’re meeting me today, I apologise for my appearance as I stupidly left my luggage on the train yesterday. I decided to get the train and tube to City Airport from home rather than a taxi. This meant I was getting my normal commuting train. The big difference is that I had a suitcase and rucksack whereas I’d normally only have my rucksack. Rather cleverly I worked out as I got on the train that I’m a man of routine and as such if I just put my suitcase in the rack above the seats I wouldn’t remember it. I therefore put my rucksack there as well. Normally my rucksack stays at my feet and I would never forget it. I patted myself on the back and got on with emails. It wasn’t until I got to security at the airport an hour later that I realised that I’d left my suitcase on the train and just took my rucksack down and ignored my suitcase. Muscle memory and routine took over. So if you see me shopping for smalls in Brussels this morning you’ll know why. As soon as it happened I texted my wife to tell her and she texted back and said “well that’s a bit annoying but can’t talk as the twins have just taken my car keys from the armrest console and locked themselves in the car and are giggling at me trying to get in”. As usual my problems were trumped by our two little identical terrors.

Yesterday was the day that most major equity markets from around the world dipped into negative territory YTD – a far cry from the melt-up thesis of two weeks ago. The notable exception is the US where the S&P 500 remains +0.40% YTD even after yesterday’s -1.57% fall – the worst day since October 2nd last year and the first 1% or more daily move in either direction over the same period. The NASDAQ remains +1.86% YTD (-1.89% yesterday) and faces the start of a big week for tech earnings today with Apple leading the charge. S&P futures are up +0.48% this morning, partly on news ahead of earnings that 10% more phones are being produced than last year.

So can the micro help offset the bigger picture challenges? The Coronavirus is of course the main short-term driver of markets but as we’ve discussed of late, we think markets have been priced for perfection whereas the reality is that positioning and valuations are stretched and the data still has a lot to prove. Also the market risk of a Bernie Sanders Presidential victory has been completely underplayed (more later).

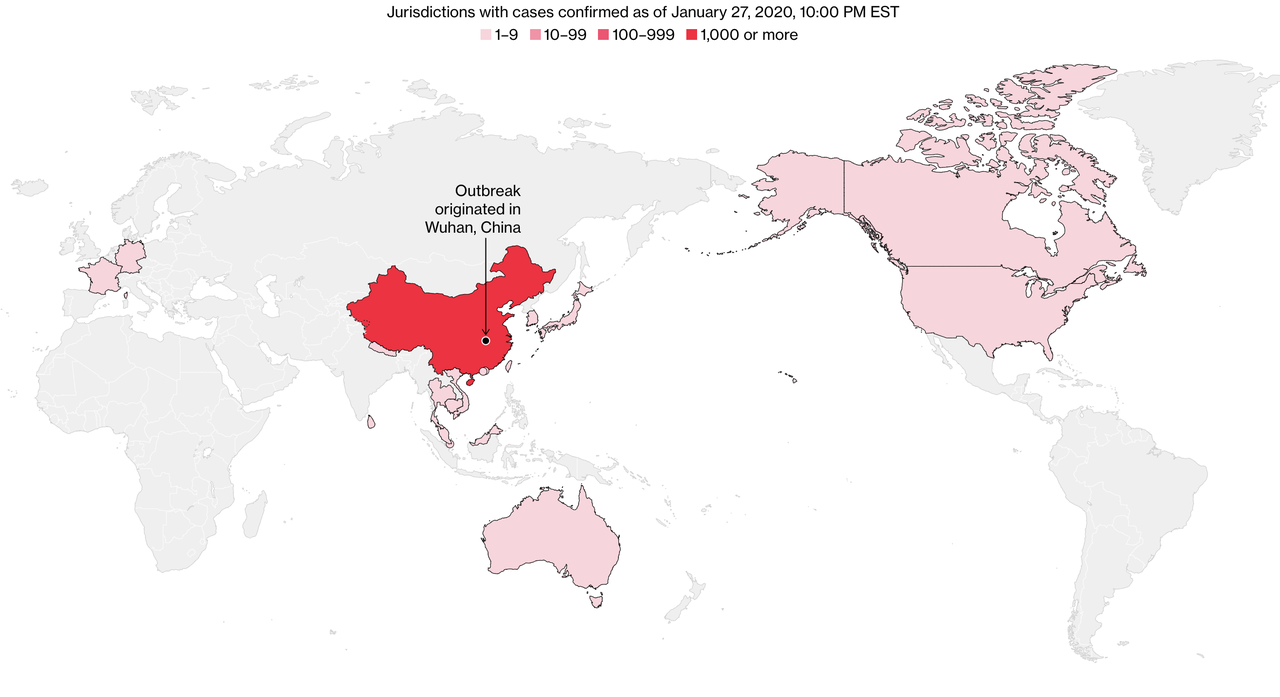

Before we discuss markets in more detail, in terms of the latest on the virus, total number of confirmed cases now stand at 4,515 (up from 2,774 yesterday) with around 47,833 (up from 30,000) people under observation. Globally, Thailand and Hong Kong have reported 8 cases each, 7 in Macau, 5 in the US, Australia, Taiwan and Singapore, 4 in South Korea, Japan and Malaysia, 3 in France, and 2 in Vietnam and Canada while, Germany, Sri Lanka and Nepal all have 1 confirmed case. However, there have been no fatalities outside of China. Meanwhile, Starbucks and WeWork have decided to shut locations in China while most other companies are enacting measures to shield employees in the areas hardest hit. Elsewhere, the US has issued a level 3 warning for China saying the citizens should avoid all nonessential travel to China. Futures on China’s stock market are down -0.72% this morning after declining by -5.64% yesterday. Also, the Dow Jones reported that as per current guidance Chinese stock markets are slated to re-open on February 3rd.

Something we’ve been thinking about on my team is how much should we be worrying about this from a macro standpoint. Without downplaying the very tragic human effects, a confirmed death toll of 106 so far (vs. 80 yesterday) is but a fraction of the hundreds of thousands of people who die each year globally from seasonal flu. On the other hand of course, this is a new virus that’s seen the number of confirmed cases double every 2 days (nearly doubled overnight) and at this rate is on the brink of passing the number of recorded cases of SARS back in 2003 in China and HK which eventually killed 774 people globally. Many experts suggest that by far the biggest issue in this episode is the long contagious period where there are no symptoms which makes the virus much harder to isolate and different from SARS. SARS had a higher mortality rate of 9.6% though against c.2.8% for Coronavirus so far. For reference the famous 1918 flu outbreak had a fatality rate of 2.5% with normal flu often no more than 0.1%. China’s reaction has been a lot more rapid than for SARS so a different template and this makes analysing it hard. In doing the research the thing that stood out for me was how many people die of flu globally in normal years even if the fatality rate is low. Anyway as a minimum Chinese data is going to take a notable hit for many weeks and getting a true read of underlying momentum is going to be hard.

Asia markets are continuing to trade lower this morning with the Kospi, which opened after the NY holiday, leading the declines at -3.22%. The Nikkei (-0.84%) and Australia’s ASX (-1.35%) are also down. The Nikkei is on track to make worst consecutive losses since the peak of trade war in August. Chinese and Hong Kong markets continue to remain close on account of holidays. As we discussed earlier US futures are up suggesting some break to the selling for now. As for overnight data releases, Japan’s December services PPI came in line with expectations at +2.1% yoy.

Amidst the virus’ spread, and as already mentioned, yesterday saw equity markets suffer on both sides of the Atlantic. The trade-sensitive Philadelphia semiconductor index had its worst day since August 23rd last year, down -3.91% (-0.04% YTD), while the losses were pretty severe in Europe too, with the STOXX 600 down -2.26% (-0.43% YTD) and the DAX down -2.74% (-0.33% YTD). Oil continued its decline on fears of plummeting economic demand, and Brent crude fell for a 5th consecutive session, down -2.95% to close below $59 a barrel for the first time since October and close to 13-month lows. Gold was the beneficiary as investors fled from risk, ending the session up +0.75% at its highest level since April 2013.

Investors also moved into sovereign debt, with 10yr Treasury yields down -8.6bps to 1.598%, their lowest level since October and only 25bps from all time lows, while the 2s10s curve flattened by c.-3bps to 15.5bps – its flattest level since November. Notably the Fed’s preferred yield curve measure (18m3m-3m) when assessing recession risks has returned back to being inverted.

Over in Europe, bunds (-5.0bps and -20bps YTD now), OATs (-4.8bps) and gilts (-5.5bps) also made gains. The real outperformances came in the periphery though, which had an incredibly strong day. Firstly in Italy, the spread of 10yr BTPs over bunds fell by -14.5bps, which is its biggest daily decline since September, and brings the spread to its lowest level in over two months. The outsized move follows the weaker-than-expected performance for Matteo Salvini’s right-wing Lega party in regional elections at the weekend, which is expected to strengthen the national government in the near term. DB’s Clemente De Lucia put out a note on the issue yesterday (link here) where he writes that the results from the regional elections push back the risks of an early election. The other big move came from Greek debt, which also rallied strongly with 10yr yields down -13.1bps, though pulling back from their intraday lows in which they looked on track to close at a record low. The moves there come after Fitch upgraded the country’s credit rating to BB with a positive outlook.

Speaking of politics, as we highlighted yesterday, something the market should definitely keep an eye on over the coming days is the Democratic primary in the US, where the first voting takes place this coming Monday in Iowa. This will be a key risk event for markets as the polling is tightly bunched there, and whoever comes out ahead is likely to take that momentum into the states ahead. Going into the caucuses, the national race seems to be settling around the two polling frontrunners of Joe Biden and Bernie Sanders, and right now Bernie Sanders has actually edged ahead of Biden on both Betfair and PredictIt. However, when we asked who was most likely to be the Democratic nominee in our EMR survey a couple of weeks ago, Biden was the most popular choice, with 49% of respondents, while Sanders was selected by just 10%, which suggests that many market participants (or at least the ones who answered our survey) could be completely underestimating the chances that Sanders might be selected as the nominee especially as 90% said his Presidential victory would be a negative for markets.

Adding to the downbeat mood yesterday, the Ifo survey from Germany surprised on the downside, with the business climate indicator falling to 95.9 in January (vs. 97.0 expected), the first decline for the reading since August. The expectations reading also fell to 92.9 (vs. 94.8 expected), though the current assessment did see a modest increase to 99.1, in line with expectations.

Over in the US, December’s new home sales also came in below expectations at a seasonally-adjusted annual rate of 694k in December (vs. 730k expected), with the previous month’s figure revised down by -22k. However, the Dallas Fed manufacturing activity did rise to -0.2 in January (vs. -2.0 expected), with the new orders indicator rising to 17.6, the highest since October 2018.

Turning to the day ahead now, and there are a number of US data releases, including December’s preliminary reading for durable goods orders, January’s consumer confidence reading from the Conference Board, and the Richmond Fed manufacturing index. Earlier in the UK, we’ll also get the CBI’s distributive trades survey for January. From central banks, we’ll hear from the ECB’s Villeroy, Lane and Hernandez de Cos, while earnings releases out today include Apple, LVMH, Pfizer and SAP. Finally the U.K. will today decide whether to allow Huawei a role in building its 5G network. This decision and those for other countries in a similar situation will have major geo-political consequences for years to come.

China Curbs Travel To Hong Kong As Projections Show 300,000 Might Already Be Infected

On Tuesday morning, China’s top health officials shared some grim statistics essentially confirming that the novel coronavirus believed to have emerged from a shady food market in Wuhan is on track to confirm some of the more dire projections shared by epidemiologists.

As we reported late yesterday, the death toll in China has soared past 100 while the number of confirmed cases doubled overnight. Health officials around the world have confirmed more than 4,500 cases, more than triple the number from Friday. All but a few of the deaths recorded so far have been in Wuhan or the surrounding Hubei province, per the SCMP.

Panic has swept across the region as border closures appear to be the overarching theme of Tuesday’s sessions. Even North Korea, which relies on China for 90% of its foreign trade, has closed the border with its patron. More than 50 million remain on lockdown in Hubei, and transit restrictions have been imposed by cities and regions around the country. An ‘extension’ of the Lunar New Year holiday is threatening GDP growth, as economists try to size up the knock-on potential impact on the global economy. The virus has now spread across China and another 17 countries/autonomous territories globally, according to BBG.

But the most important announcement made overnight – at least as far as global markets are concerned – was Hong Kong Chief Executive Carrie Lam’s decision to suspend high-speed rail and ferry service, while halving the number of flights between HK and the mainland. This news helped send US stock futures higher in early trade, after health experts yesterday urged Lam to use ‘draconian’ measures to curb the spread, for fear of a repeat of the SARS epidemic, which killed some 300 people, according to the BBC.

“The flow of people between the two places needs to be drastically reduced” amid the outbreak, Ms Lam told the South China Morning Post.

China, meanwhile, said it would stop individuals from traveling to Hong Kong to try and curb the virus.

Jiao Yahui, deputy head of the NHC’s medical administration bureau, said during a press conference Tuesday that shortages of medical supplies in Wuhan were still a serious problem.

CDC has issued new travel recommendations urging people to avoid all non-essential trips. But officials remained reluctant to declare a global emergency, instead insisting that this is merely an emergency “in China”. Of course, after yesterday’s brutal pullback, that’s to be expected.

The big piece of evidence that the WHO is purportedly looking for is human-to-human transmission outside China. Zhong Nanshan, a leading expert on SARS and other communicable diseases in China, confirmed human-to-human transmission in at least one case in Wuhan and two cases in Guangdong Province. Meanwhile, as we noted yesterday, one case of possible human-to-human transmission is being investigated in Canada, while Vietnam and Japan have now each confirmed one cases. Japan revealed on Tuesday that a bus driver in his 60s, who recently carried passengers from Wuhan, has been found to have the virus.

During a meeting in Beijing, President Xi told World Health Organization Director-General Tedros Adhanom Ghebreyesus that the safety of the people is his government’s first priority, and that he recognizes the situation is “very serious.”

“This was supposed to be a time for rest, but because of the pneumonia outbreak caused by the novel coronavirus, the Chinese people right now are faced with a very serious battle,” Xi said. “This is something we take very seriously because in our view nothing matters more than people’s safety and health. That is why I myself have been personally deploying, planning, and guiding all the efforts related to containment and mitigation of the outbreak.”

That’s ironic, considering Beijing’s sluggish response after the first cases were discovered in December. After all, Wuhan Mayor Zhou Xianwang on Tuesday spoke out against the deluge of criticism he has faced to accuse Beijing of tying his hands. This comes after President Xi and the party tried to scapegoat him and other local party officials for the crisis.

This was supposed to be a time for rest, but because of the pneumonia outbreak caused by the novel coronavirus, the Chinese people right now are faced with a very serious battle,” Chinese President Xi Jinping tells in Beijing.

Speaking at a press briefing in Beijing on Tuesday, Jiao Yahui, deputy head of the NHC’s medical administration bureau, said shortage of medical supplies was a major constraint in China’s efforts to contain the outbreak and treat infected people.

Tens of thousands of patients are under observation in China after displaying one or more symptoms of the virus. In the US, roughly 100 people are in isolation. But former FDA Commissioner Scott Gottlieb told CNBC that China is obscuring the true number of cases – a suspicion that’s widely held among American infectous-disease experts.

According to some projections, there might be up to 300,000 cases in China, and there are likely dozens of people who have died of pneumonia who in reality died from nCoV – but those deaths will never be recorded. Although China is “behaving better” than it did during the SARS outbreak, they’re still concealing information from the international community.

“They’re still not behaving well. They’re concealing information, including the spread to health care workers, which we didn’t know until last week” Gottlieb said.

China is already in a “full-blown epidemic.” The US will likely face some limited outbreaks, but Gottlieb said we have the tools to suppress the virus and prevent the same thing from happening in the US.

Jiao said China was sending about 6,000 medical personnel to Hubei from around the country – with more than 4,000 already there and 1,800 more due to arrive by Tuesday evening – to work in Wuhan and seven other cities in the province. In Wuhan, more than 10,000 hospital beds have been made available for patients, he said, while another 100,000 are being prepared.

In Beijing, CNBC’s Eunice Yoon reported that the local government is strongly encouraging the wearing of facemasks in public. Police guarding Beijing’s public transit are wearing full hazmat suits, and anybody hoping to board a train must be wearing a mask, and must submit to a temperature check via infrared thermometer. If an individual is found to have a fever, they’re sent to a hospital to be quarantined.

As Beijing tries to telegraph to the world that it has the situation under control, health experts have raised new questions about the government’s response. One infectious disease specialist told the NYT that they were skeptical about the Wuhan quarantine’s ability contain the virus (unsurprising considering that 5 million left the city before the lockdown began). Beijing and Guangzhou, a port city northwest of Hong Kong, have broken ground on new hospitals, mimicking the speedy construction of not one but two new hospitals in Wuhan to treat patients infected with the virus. Beijing is also reopening a hospital used to fight the SARS outbreak in 2003, while 6,000 medical staff have been sent to Hubei.

“At this stage of the outbreak, the things that make the most difference are finding people, diagnosing people, and getting them isolated,” said Dr. Tom Inglesby, an infectious diseases specialist and director of the Johns Hopkins Center for Health Security. “If you isolate the city, then my question and my concern is that you’re making it harder in a number of ways to do those things you need to do,” including ferrying critical supplies and ensuring that infected victims receive adequate treatment.

One of the greatest moral dilemmas that has been creeping into the everyday activities of specialists working with coal, oil and in some cases even gas (despite its being perceived a natural bridge to a low-carbon future) could be phrased in the following way: how do you stop producing fossil fuels when you still have cheap ample reserves?

In this context coal stands out – its relative inferiority in terms of environmental pollution prompted governments in developed economies to ban its future usage. Yet whenever its production is not curtailed by government-mandated cuts, producers simply continue to extract as much coal as possible. Straight in the middle of the so-called European approach to coal lies Germany, an erstwhile bulwark of the coal industry. Can it eventually survive without coal?

In stark contrast to oil and gas – of which Germany has traditionally been a major net importer and in both cases looking back to a more than 50-year history of depending on primarily Russian hydrocarbon riches – Europe’s leading economy has substantial reserves of coal, lignite in particular. In fact, Germany remains the world’s largest producer of lignite and burns most of it for power generation, accounting for some 22 percent of the nation’s gross electricity output. Ironically, lignite production is more CO2 intensive than hard coal as it is done by extracting coal from open-cast pits, nevertheless, its mid-term future looks a lot better than that of hard coal mining in Germany.

Whilst lignite remains economically competitive, Germany’s hard coal production went downhill after the government ended its subsidy schemes. The last hard coal mine closed its gates in December 2018, ending a 200-year history of the Ruhr Region and potentially starting a new development phase of Westphalia, a geographical phenomenon inextricably intertwined with coal.

Yet even though Germany ceased to extract hard coal itself, it continues to use it. Around 12 percent of power generation is coming from hard coal, imported primarily from Russia, Canada and the United States. Once Germany’s flagship industry, the steel sector consumes almost 40 percent of the nation’s hard coal.

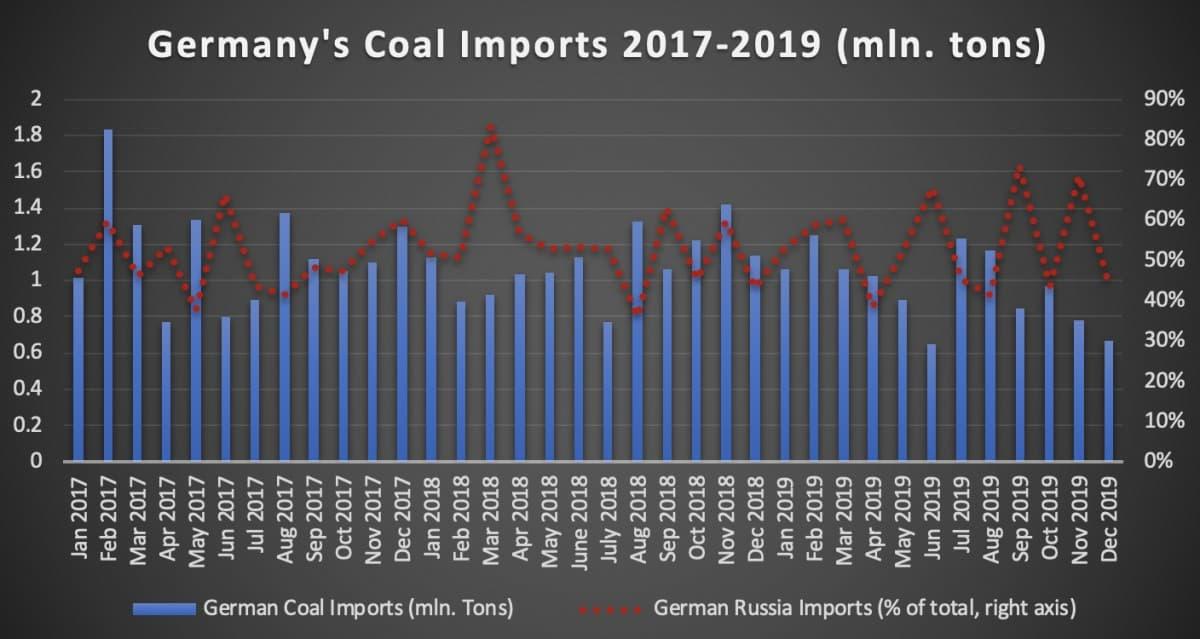

If Germany is to remain an industrial powerhouse, it would need to keep on importing hard coal as it remains an indispensable element of steel-making. This would in turn compel it to rely on imports from Russia (Murmansk and Ust-Luga, to be precise), thereby creating a triple dependence on Russian hydrocarbons. If one is to take monthly statistics in the past 3 years they would find that 53 percent of all imported coal came from Russia, a dependence which has palpably deepened in the past 24 months thanks to the vicinity of large coal-handling ports in the Russian Baltics. Oil, gas and coal – in all three instances Germany imports more than a third of its needs from Russia; in the case of gas it will be significantly higher very soon with NordStream-2 being slated for a mid-2020 commissioning and Groningen going to a government-mandated halt.

(Click to enlarge)

Graph 1. Germany’s Coal Imports in 2017-2019 / German Dependence on Russia (in million tons).

Source: Thomson Reuters.

It would be also interesting to see how the German government will resolve the issue of compensated closures, especially for lignite mines. Hard coal is an easier nut to crack – economically unviable, operationally underutilized (only some 6GW of the existing 20GW hard coal capacity was used in 2019) and widely unpopular due to a lack of serious lobbying effort. For hard coal, the 8GW set as target for 2030 does seem fairly manageable. Yet the government’s efforts to fix the first lignite closures by 2022 are still subject to discussion with mine operators, not to speak of its flaunted intention to launch enforced closures from 2027 which currently seems to be a task too complex to effectuate this quickly.

Interestingly, running somewhat counter to the general narrative as heard from advocates of wider renewables usage, the drop in German coal consumption is not fully supplanted by the mix of gas and renewables. Let’s look at 2019 a bit closer. Both lignite and hard coal usage dropped a whopping 20 percent year-on-year, coming from debilitating (and mandatory) carbon emissions prices and renewables being prioritized in terms of grid access, whilst renewables grew by 3 percent in 2019. In absolute terms the situation is even clearer – coal usage dropped by 20.5 million tons of coal equivalent, whilst renewables only rose by 3 million tons of coal equivalent (natural gas increased by almost 4 mtce).

The ramifications of Germany’s coal exit are truly manifold – on the one hand, Berlin is one of the few coal-producing nations to take its CO2 emission commitments seriously and has managed to decrease its carbon dioxide emissions by some 7 percent y-o-y in 2019 alone. It has spearheaded the European Union drive to decrease the continent’s emissions regardless of the platform. The 2038 phase out of German coal seems like a fairly feasible objective, buttressed by a draft bill which will seemingly soon be signed into law. Replacing lignite will be a tough call as it is cheap and located next to massive urban conglomerations – burning imported gas which also carries in it additional transportation costs might not be always the best option.

On the other hand, the decline of coal is happening concurrently with an unprecedented drop in Germany’s primary energy usage (the 2019 level plummeted to levels unseen since the early 1970s) and the nation’s industrial output might suffer as a result. Moreover, the general view on the coal exit presupposes that Germany’s States will compensate for the end of coal mining by creating new business opportunities and reshaping people’s skills to better suit the needs of the 21st century. However, that is happening only in a fragmented fashion – unemployment rates in major coal-producing hubs like Gelsenkirchen or Dortmund still amount to roughly double of the German average.

Turkey Behind Major ‘State-Backed Cyber-Espionage’ Targeting Europe & Middle East

After prior widespread state cyber-espionage operations were revealed connected to both Iran and Saudi Arabia in the past months, a new bombshell Reutersinvestigation has exposed a new alleged Turkish government-linked hacking operation which has targeted organizations across Europe and the Middle East for the past two years.

Citing multiple senior Western defense and security officials as well as public internet records the new report concludes at least 30 organizations ranging from government ministries to embassies to international companies have been targeted by hackers who appear to be doing the bidding of Turkey. Notably the Greek and Cypriot governments and their state email services have topped the list of targets.

File image via Arab Weekly news.

The Cypriot government confirmed it was targeted as part of the operation but did not give details. Iraq’s government, specifically national security offices, were also identified in the report as a prime target.

Security officials said that infrastructure registered in Turkey was used in the hacks, but did not reveal further details related to confidential intelligence assessments.

But interestingly, at least one entity inside Turkey itself was allegedly hacked – a Turkish chapter of the Freemasons said to have ties to US-based Turkish opposition cleric Fethullah Gulen.

The DNS-hijacking campaign is said to be similar in methodology detailed in separate prior reporting related to Iran known as DNSpionage. Reuters explains and summarizes the alleged Turkish hackers’ methods as follows:

The hackers used a technique known as DNS hijacking, according to the Western officials and private cybersecurity experts. This involves tampering with the effective address book of the internet, called the Domain Name System (DNS), which enables computers to match website addresses with the correct server.

By reconfiguring parts of this system, hackers were able to redirect visitors to imposter websites, such as a fake email service, and capture passwords and other text entered there.

Reuters reviewed public DNS records, which showed when website traffic was redirected to servers identified by private cybersecurity firms as being controlled by the hackers. All of the victims identified by Reuters had traffic to their websites hijacked – often traffic visiting login portals for email services, cloud storage servers and online networks — according to the records and cybersecurity experts who have studied the attacks.

The new hacking revelations also come as tensions between Turkey and its longtime enemies Greece and Cyprus are soaring over Turkey oil and gas exploration and drilling in the eastern Mediterranean, which the EU says has illegally cut into both countries’ Exclusive Economic Zones (EEZ).

Investigators took particular note of the victims and targets — all who appeared to be geopolitical enemies of Turkey, and in the case of Turkish-related groups targeted, they happened to be linked to the exiled Fethullah Gulen and/or his supporters.

Gulen has remained an official enemy of the Turkish state under President Erdogan, who has consistently put pressure on Washington to arrest and transfer the opposition cleric back to Turkey.

There was real fear in Europe over what could have happened this weekend in Italy. Regional elections in Emilia-Romagna and Calabria could have been terrible for the tenuous ruling coalition between PD and Five Star Movement.

But the center-left held serve against the insurgent campaign of Matteo Salvini and his Lega-led coalition.

Emilia-Romagna is the birthplace of Italian Communism and has been a stronghold for the political left for decades. Even though Salvini et.al. failed to win the day this is a clear case of failing falling forward.

It’s a massive improvement for the center-right in Italy and will effect how the region is governed. But the big story here is Five Star.

It is also clear that Five Star is now in complete collapse as an opposition party, garnering only 3.5% in E-M and just 7.3% in Calabria.

Nationally, Five Star is now polling between 15-17%, flirting with political irrelevance if the numbers drop much lower than this. But, where will those voters go?

Five Star was born as an opposition party to entrenched and corrupt Italian political elites. It was decidedly Euroskeptic and it’s not handled the transition from outsider gadfly channeling voter frustration into an effective governing force at all.

Five Star originally emerged (and remained until 2018) as an anti-system party that rejected cooperation with the other parties in the system and presented itself as a separate pole in opposition to both the centre-right and centre-left. At that time, it declared that it would only cooperate with the other parties on a strict issue-by-issue (and law-by-law) basis. The M5S rejected the legitimacy of the other parties in the strongest terms and fully-fledged cooperation was out of the question.

However, anti-system parties often eventually integrate into the system they previously opposed. This is especially true for populist parties as they are the ‘new normal‘ in European party systems and governments today. The integration and legitimation of populist parties can be a long or short process, according to the various incentives of the political system and electoral results, and is usually accompanied by a series of programmatic and organisational reforms.

The zenith of the integration of populist parties is represented by their eventual entry into national office. In many cases, populist parties are indeed able to survive office, and even to gain votes in subsequent elections. Italy’s Lega is a case in point. After a first disastrous experience in office (1994), the Lega, over time, benefited from a ‘learning process’. It now has a long record of government participation and dominates the Italian agenda. According to all the polls, the party led by Matteo Salvini is by far the strongest in the country today (estimated at 32%).

This is why Lega’s support in E-M has steadily risen over the course of the last three elections there and was nearly capable, in just a three-year time horizon to unseat the establishment there. Only a bitter fight driving massive turnout, nearly 59%, kept E-M from turning “blue.”

Previous elections saw turnout drop as low as 30%. Who turns up to vote when the outcome is predetermined?

Look at the results closely and you’ll see the thing disquieting the Italian plutocrats. Five Star and PD’s support dropped a combined twenty points. Not only is Five Star in freefall but it looks like PD may be as well. The next government in E-M will not take the voters for granted like they have been.

Lega and the Brothers of Italy scooped up the 7 seats in the government lost by PD, who no longer rule with a massive majority.

The results for Calabria were even worse. The Center-Left coalition lost more than thirty-two points over the 2014 election. And while that outcome wasn’t in doubt beforehand it shouldn’t be discounted either. Like Umbria’s election last fall, these results are telling everyone that big change is on Italy’s horizon.

The markets today are breathing a sigh of relief. Salvini has been beaten back for a bit. But for how long? Yes, the ruling coalition survives another day. Yes, it’s a little stronger than it was yesterday. But, Five Star as a party is in the early stages of collapse and the infighting among its high-ranking members will continue until such time as the coalition breaks.

Salvini was right back in August to dissolve the coalition. As Italy sinks economically and politically he is in the position to rally the populists, secure their support and gain support while the government takes all the blame.

And, as Zulianello suggests, since Lega is a properly constituted and functional organization, when it returns to government it will do so with a clear mandate and clearly-defined goals.

These are two things Five Star could never deliver on.

{kind=link}