Distraction? Trump Sends Warships To Venezuela For “Counter-Narcotics Operation”

In late February we detailed how President Trump is not giving up on pursuing military options for Venezuelan socialist strongman Nicolas Maduro’s ouster — even as Washington was forced to increasingly turn its attention to the growing coronavirus threat in its midst — now a full-blown pandemic radically altering the fabric of American society and the economy.

And Bloomberg had also confirmed at the time :”President Donald Trump is frustrated that pressure is building too slowly on Venezuelan President Nicolas Maduro and is still considering military options in the country, including a naval blockade, a senior administration official said.” It’s long been reported that Trump favors the naval blockade idea even as his generals have pushed against it on grounds of practical execution of such a bold plan.

Amazingly, considering the timing, the president announced Wednesday that he’s ordered Navy ships to move toward Venezuela as part of broader counter-narcotics operations in the Caribbean.

AFP via Getty

This follows the White House last week issuing a $15 million bounty on Maduro and his inner circle over drug trafficking charges, amid sweeping indictments against what Washington dubbed a vast narco-state criminal enterprise orchestrated by the regime.

Considering all of this is being executed at a moment the United States now leads the world in numbers of confirmed coronavirus cases, which threatens to decimate an economy still on “pause” and extreme uncertainty still on the horizon, it must be asked: is this move on Venezuela (and it should be added – recent moves against ‘Iranian proxies’ in Iraq) all but a big attempt at coronavirus and record unemployment distraction?

* * *

Ron Paul certainly thinks so: President Trump and his advisors announced that the US military would begin conducting a “counter-narcotics operation” in the eastern Pacific and Caribbean.

Perhaps not coincidentally, Trump’s Justice Department indicted Venezuelan president Maduro on drug trafficking charges. Is the US about to “do a Noriega” on Maduro based on half-baked charged that the Venezuelan leader is some kind of drug kingpin?

Have the president’s war-braying neocons convinced him that the best thing to get our minds off of coronavirus is a “nice little war”? Today on the Ron Paul Liberty Report:

Goldman Sachs Buys 2 Luxury Private Jets As Main Street On Verge Of Collapse

This is definitely not a good look.

At a time when the federal government is struggling to manage its $2 trillion bailouts for main street and SMEs, a handful of Goldman Sachs insiders (probably high-ranking executives) have apparently decided to sandbag CEO David Solomon, who is already reeling from the blowback to his latest raise, the highest among his peers despite $GS’s lagging performance.

BBG reported Friday that Solomon recently OK’d the purchase of two private jets, breaking with a longstanding corporate tradition.

For years, there was an allergy inside Goldman Sachs to owning a private corporate jet. Top bankers had access to rides on planes shared with others, but didn’t want to erode their less-than-stellar image on Main Street with the unnecessary extravagance of having their own.

Until David Solomon took over.

The CEO has ordered up a pair of top-of-the-line Gulfstreams for the firm, according to people with knowledge of the matter. The firm chose a G700 model that sells for about $75 million each, is powered by Rolls-Royce engines and offers cabins so long and wide they contain a master suite with shower.

Understanding why Solomon’s decision might have rankled so many within Goldman requires some knowledge of the firm’s recent history. The bank has long used the fact that it didn’t own a private jet for its executives to travel in as a PR bulwark against liberal Democrats and other critics. Instead of owning a jet outright, Goldman allowed its executives access to chartered planes via an arrangement with NetJets, the Berkshire subsidiary that brokers part ownerships in business aircraft.

Of course, as BBG points out, at the highest levels of Wall Street power, private jets are an expected perk. Goldman is an outlier for not owning one, or even several, and rivals like JPM and MS have had theirs for years. Looking forward, it’s also possible that the use of private jets becomes more accepted in the age of coronavirus as flights become vectors for spreading disease.

Not only did Solomon buy two jets, but he and the firm chose a G700 model that sells for about $75 million each, is powered by Rolls-Royce engines and offers cabins so long and wide they contain a master suite with shower. According to BBG, marketing material for the G700 advertises a speakerless surround sound and “the industry’s only ultra-high-definition circadian lighting system.”

It’s exactly the kind of unwanted attention that might draw public scrutiny or outrage, or even possibly prompt the Feds to reconsider certain legal agreements struck between the bank and the DoJ over its handling of 1MDB.

As Bloomberg reminds us, when Congress dragged the CEOs of the big Wall Street banks to Capitol Hill in the aftermath of the crisis, they were asked which of them arrived in a private, company-owned aircraft.

All raised their hands – except Goldman’s then-CEO, Lloyd Blankfein.

“Let the record show,” said LA’s Democratic Congressman Brad Sherman, that “all the hands went up except for the gentleman from Goldman Sachs.”

It was a rare PR win for the firm, and a moment that actually resonated with the public. Though as we’ve learned, Goldman’s lack of a private jet is merely a ruse, and nothing more. It is in no way indicative of the culture at the firm, which was recently described by a former banker who turned against the bank to cooperate with the Justice Department in the 1MDB investigation, as “a culture of secrecy” where bankers were encouraged to bring in big deals and ignore compliance’s misgivings.

At least when GE had its private jet scandal, John Flannery was able to at least blame it all on his predecessor. This is one of the first Goldman scandals where Solomon distinctly does not have that luxury.

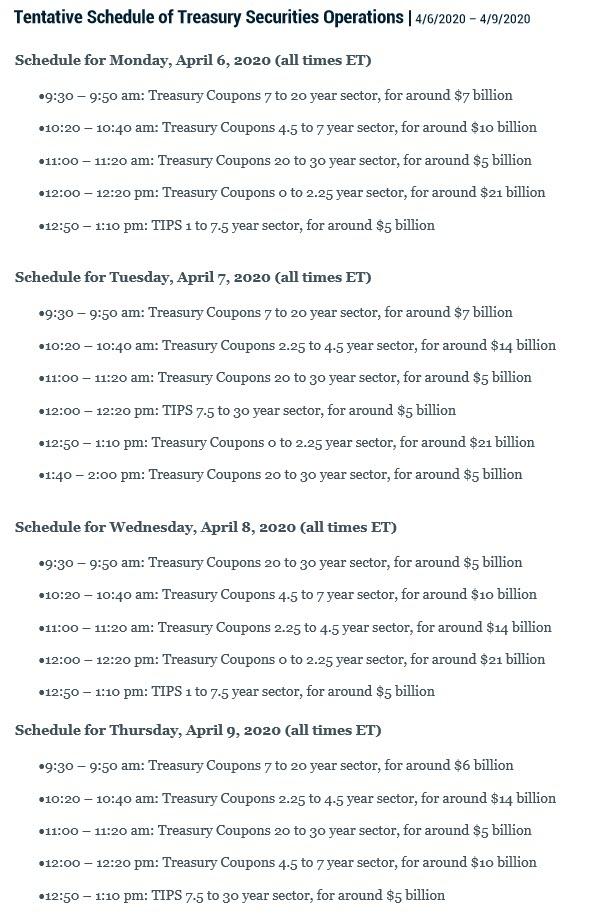

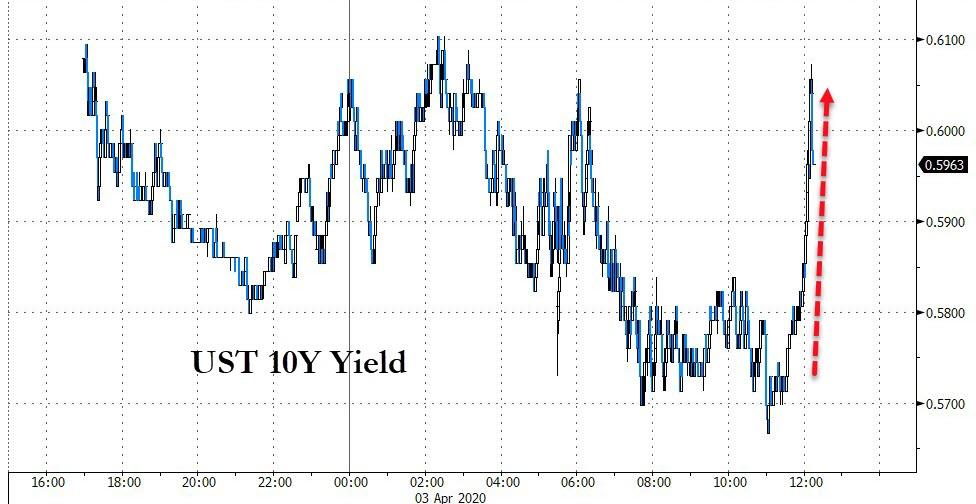

Bonds & Stocks Sold After Fed Announces Another Taper In Bond-Buying

From an initial $75 billion per day, to $60 billion per day last week, The Fed had just announced another ‘taper’ in its bond-buying program to $50 billion per day for next week…

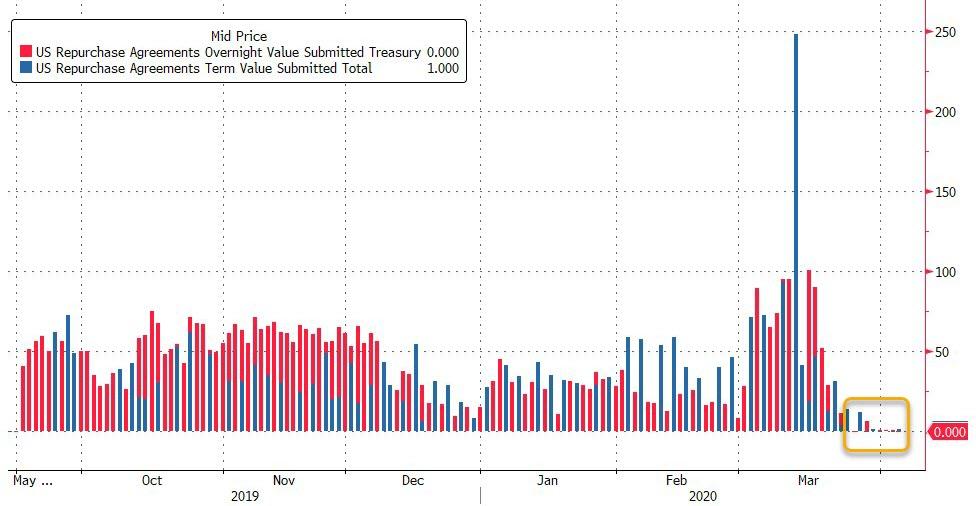

Having implicitly confirmed there is now a shortage of bonds as demonstrated by the recent repo ops that saw zero submissions as instead of using repo to park bonds with the Fed Dealers merely sell them back to the Fed, the NYFed has announced it will continue cutting back, or tapering, its “unlimited QE” bond-buying next week.

This makes some sense as The Fed’s intervention’s purpose – “to support the smooth functioning of markets” that had become impaired – has been at least partially achieved, with key metrics such as off-the-run spreads and the cash-futures basis moving back toward normal levels.

The headline stalled the late-Friday ramp in stocks…

“Unanticipated Shock” – Under Armour Lays Off 6,700 Workers, Stores Shuttered “Indefinitely”

Just days after Under Armor jumped into the mask-making game as it realized its core business of selling sports leisure apparel in overseas and domestic markets collapsed because the virus pandemic has led to global quarantines and shuttering of non-essential businesses. The Baltimore-based sportswear maker announced Friday that its retail stores would remain closed indefinitely and lay off 6,700 employees, reported The Baltimore Sun.

“This unanticipated shock to our business has been acute, forcing us to make difficult decisions to ensure that Under Armour is positioned to participate in the eventual recovery of demand,” Patrik Frisk, CEO and president, said in Friday’s announcement.

“We do not take these decisions lightly and are doing all we can to minimize the impact on our teammates during this time,” Frisk said.

Under Armour pulled its previous financial guidance for 2020 and initiated its restructuring plan that will cost $475 to $525 million for this fiscal year. The fate of its 188 North America stores is unknown at the moment, have been closed since March, and will remain closed “until further notice.”

Frisk said the company is seeing a “significant decline in revenue” while its stores remain closed. With lockdowns expected across the country to last through late April, the financial blow to the company could be devastating.

Under Armour, likely so many other companies, have drawn on their credit lines to survive the virus crisis crashing the US economy into a depression for the second quarter. The company said it has taken out $700 million on a revolving credit facility “to increase its cash position and preserve liquidity.”

We noted in February that Under Armour “estimated negative impact of the coronavirus outbreak in China of approximately $50 million to $60 million in sales related to the first quarter of 2020.”

Under Armour’s top executives have taken a 25% salary cut, along with the board of directors have had their compensation reduced by 25% during the crisis.

“There’s not much else that Under Armour can do now since there’s no way to know when the stores will reopen,” said David Swartz, an analyst for Morningstar.

“Unfortunately, unlike Nike and Adidas, Under Armour is not an established brand in Asia, where a lot of stores have reopened. The restructuring and the abandonment of the flagship in NYC is reflective of the company’s inability to turnaround its business even before the crisis,” Swartz said.

“Because of the strength of our brand and the steps we have taken, we will weather this storm,” Frisk said.

We guess the ‘Under Armour bros’ won’t be having wild parties at Kevin Plank’s Sagamore Farm this year – as it appears the company is on life support.

Goodbye V-Shaped Recovery: Morgan Stanley No Longer Expects Return To Normalcy Before End Of 2021

Two weeks ago, when the first dire Q2 GDP forecasts emerged which were however followed by hilarious V-shaped recovery assumptions for Q3 and onward, we said it’s only a matter of time before the banks throw in the towel on a V-shaped recovery as the full devastation of the Covid depression emerges.

We didn’t have long to wait.

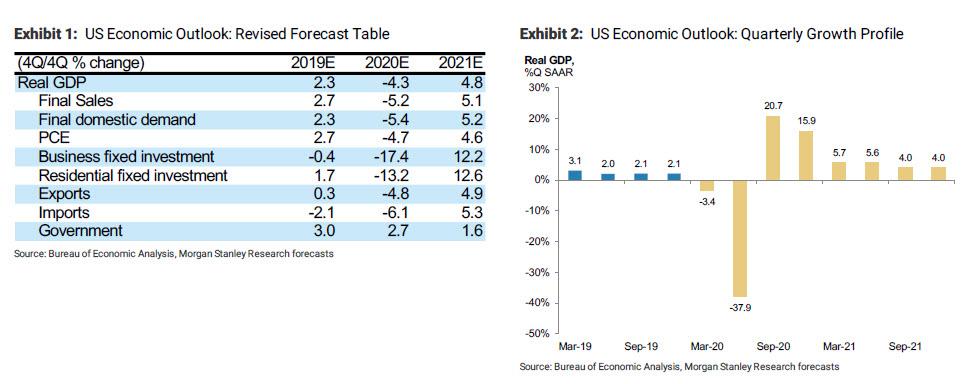

In a report from Morgan Stanley’s chief economist Ellen Zentner, the bank has not only surpassed both Goldman and JPMorgan in sellside gloom for how bad the Q2 depression will be, now expecting a massive 38% collapse in GDP, but more troubling for all those who believe the economy will recover overnight with a snap of the fingers, Morgan Stanley now sees “a shallower rebound in 3Q, and we do not see activity returning to its pre-virus level until the end of 2021.”

The reason: “The evolution of economic activity will be a function of how quickly the number of coronavirus cases peaks as well as how quickly social distancing measures are rolled back and how quickly consumer and business sentiment recovers such that at least somewhat normal economic behavior can resume.”

In other words, as we said nearly two months ago, the longer the shutdown lasts the greater the economic, social and – in Trump’s case – political toll.

Here are some more details from the MS report:

Disruptions to economic activity have become increasingly pervasive as social distancing measures and closures of nonessential businesses have spread across the country. This will lead to a sharp drop off in activity in 2Q that is reflected in the now 38% annualized decline in GDP that we expect for the second quarter (previously -30%). That follows what we expect will be a 3.4% annualized contraction in first quarter, for a cumulative decline in the level of real GDP through 2Q20 of 12%.

The evolution of economic activity thereafter will be a function of how quickly the number of coronavirus cases peaks as well as how quickly social distancing measures are rolled back and how quickly consumer and business sentiment recovers such that at least somewhat normal economic behavior can resume.

Our base case economic outlook is conditioned on our biotechnology team’s COVID-19 outbreak dynamic model, which was recently revised to show a high expected number of cumulative infections (~570,000), with daily new infection growth expected to slow in late April. Moreover, the team sees the largest risk for the US as a second wave of infections emanating from the central region of the country after the coasts have peaked in mid-April (see Biotechnology: COVID-19: Updating US Forecast For Greater Spread, Potentially Worse Trajectory Than Italy (30 Mar 2020)).

Zentner’s revised quarterly growth projections put full year GDP on course for a 4.3% contraction on a 4Q/4Q basis (Exhibit 1), the steepest four-quarter drop in activity on record in the post-war period. On an annual average basis, real GDP is expected to contract 5.5% in 2020, the steepest annual drop in growth since 1946 when real GDP contracted more than 11%

With this dynamic in place, MS now expects the US economic recovery will be more drawn out than previously anticipated, marked by a deeper drop into recession and slower climb out. The bank has revised down its expectation for 3Q GDP growth accordingly, and now look for a 20.7% annualized bounce in GDP in 3Q (Exhibit 2). Although that looks like an elevated quarterly growth number, off of such a low base our forecast implies that the level of real GDP in 3Q will recover back only 35% of the lost output in the first half of the year.

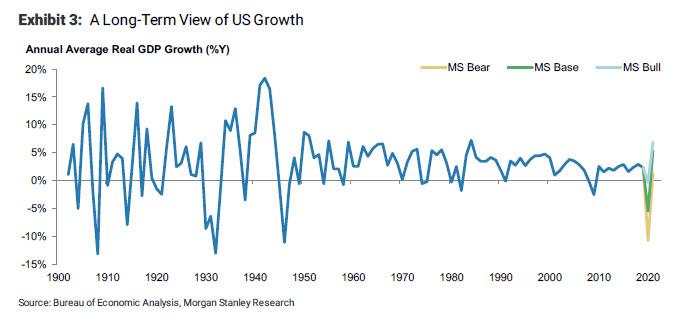

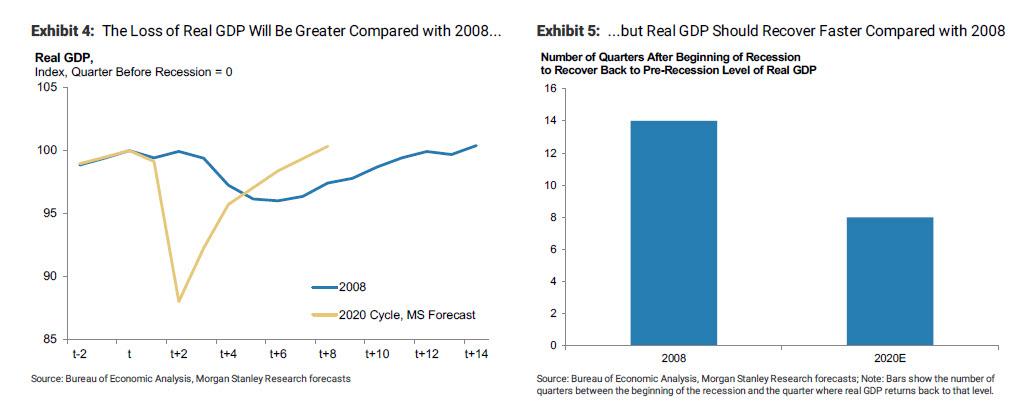

Reflecting Morgan Stanley’s loss of hope in a V-shaped recovery, the level of real activity in its forecasts remains below its 4Q19 level until the end of 2021: a sharper loss of real GDP compared with the 2008 recession (Exhibit 4). Still, the bank isn’t completely apocalyptic and expects that the rebound in economic activity should be quicker this cycle compared with 2008 when activity did not return to its 4Q 2007 level until the second quarter of 2011. We give the bank another week before it gives up on this particular optimistic view.

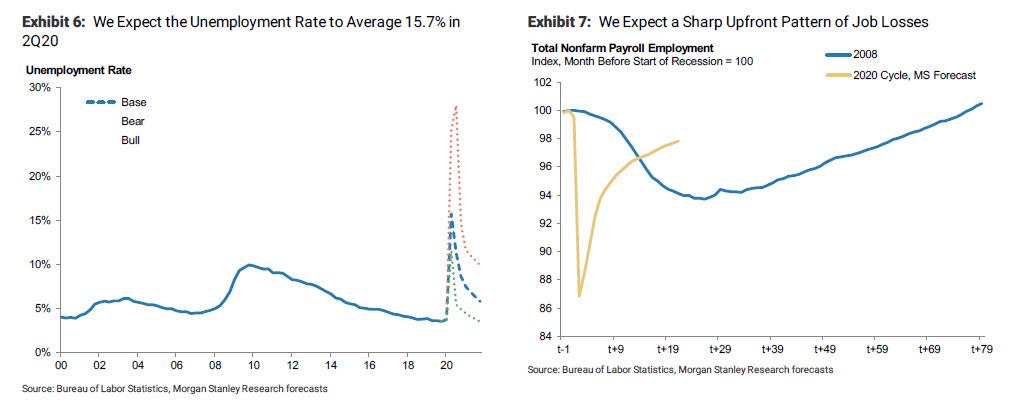

Finally, there is unemployment, which Morgan Stanley expects will peak at a ghastly 28% in late 2020.

Disruptions to economic activity and closures of nonessential businesses have increasingly weighed on the labor market. In the past two weeks alone we have seen nearly 10 million workers file for unemployment benefits, indicating that upcoming employment data on payroll growth in April and through the second quarter is likely to be deeply negative.

For the second quarter as a whole, we expect this will lead to a sharp rise in the unemployment rate to an average of 15.7% (Exhibit 6), the highest among records dating back to the 1940s. That builds in an assumption of cumulative job losses of 21 million in the second quarter, with a peak in the unemployment rate at 16.4% in May. In our bear case scenario, job losses amount to almost 40 million in 2Q, driving the unemployment rate up to 25%, and further economic weakness in 3Q20 leads the unemployment rate to drift up further to a peak of 28%, and the unemployment rate remains persistently higher over the forecast horizon in this scenario.

The pattern of job losses will largely follow the GDP pattern, although we do foresee some long-term job losses persisting over our forecast horizon. That may be particularly the case among small businesses (<100 employees), which BLS data indicate comprise more than 55% of total employment. We expect that payroll employment will begin to expand in June 2020, but will remain 2.7% below its pre-recession peak at the end of 2021. Nevertheless, that would feel like a stronger recovery compared to the persistent labor market weakness seen in the 2008 cycle (Exhibit 7).

And that’s what the second great depression looks like.

Pelosi Backpedals On Infrastructure Spending In Fourth Coronavirus Stimulus

House Speaker Nancy Pelosi has walked back ambitious plans for infrastructure spending in the next coronavirus stimulus package – and is instead focusing on boosting direct payments to individuals as well as loans to businesses, according to Bloomberg, which notes that the shift will leave an estimated $800 billion infrastructure plan in limbo.

“While I’m very much in favor of doing what we need to do to meet the needs of clean water, more broadband and the rest of that, that may have to be for a bill beyond this,” Pelosi told CNBC in a Friday appearance. “I think right now we need a fourth bipartisan bill — and I think the bill could be very much like the bill we just passed.”

“So I’d like to go right back and say let’s look at that bill let’s update it for some other things that we need, and again put money in the pockets of the American people,” she said – promoting the much easier sell, which Bloomberg notes would probably have an easier time getting through Congress.

Pelosi said the $350 billion included the last stimulus for small business to maintain payrolls for two months won’t be sufficient. She said the nation also will need an extension of the expanded unemployment benefits and additional direct payments to middle income individuals. –Bloomberg

Pelosi and other Congressional Democrats pitched approximately $800 billion in new infrastructure spending, which would be allocated towards boosting broadband, access to clean water, and funding for community health centers.

Congressional Republicans have pushed back against the idea – suggesting that we should wait and see what the impact of the first three packages have had, despite President Trump’s call for a $2 trillion infrastructure package.

Meanwhile, nobody has said how the infrastructure plan will be paid for, as nobody has come forward with an actual proposal.

The following article was originally published in “What I Learned This Week” on March 26, 2020. To learn more about 13D’s investment research, please visit their website.

Corporate debt is the timebomb everyone saw ticking, but no one was able to defuse. Ratings agencies warned about it: Moody’s, S&P. Central banks and international financial institutions did too: the Fed, the Bank of England, the Bank for International Settlements, the IMF. Financial luminaries expressed concern: Jamie Dimon, Seth Klarman, Jes Staley, Jeffrey Gundlach, Henry McVey. Even a presidential candidate brought the issue on the campaign trail: Elizabeth Warren. Yet, as we’ve documented in these pages for more than two years, corporations have only piled on more debt as their balance sheet health has deteriorated.

Total U.S. non-financial corporate debt sits at just under $10 trillion, a record 47% of GDP. One in six U.S. companies is now a zombie, meaning their interest expenses exceed their earnings before interest and taxes. As of year-end 2019, the percentage of listed companies in the U.S. losing money over 12 months sat close to 40%. In the 12 months to November, non-financial S&P 500 cash balances had declined by 11%, the largest percentage decline since at least 1980.

For too long, record-low interest rates inspired complacency, from companies to lenders to regulators and investors. As we warned in WILTW August 8, 2019, corporate fundamentals will eventually matter. Now, with COVID-19 grinding the global economy to a halt, that time has come.

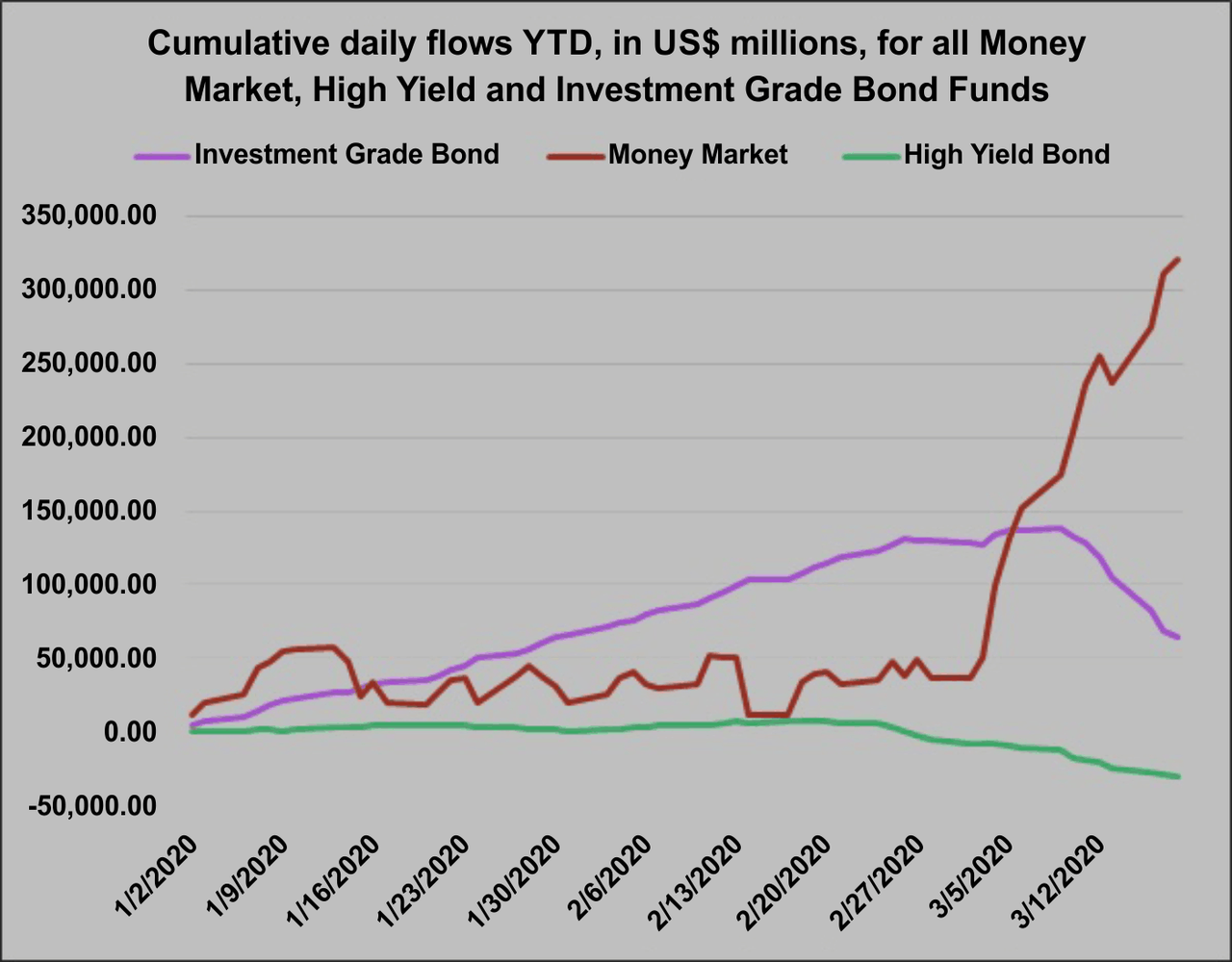

Systemic threats are littered throughout the corporate debt ecosystem. Greater than 50% of outstanding debt is rated BBB, one rung above junk. As downgrades come, asset managers will be forced to flood the market with supply at a time demand has dried up. Meanwhile, leveraged loans — which have swelled by 50% since 2015 to over $1.2 trillion — threaten unprecedented losses given covenant deterioration. And bond ETFs could face a liquidity crisis as a flood of redemptions force offloading of all-too-illiquid bonds (see WILTW January 31, 2019).

Red lights are now flashing. Distressed debt in the U.S. has quadrupled in less than a week to nearly $1 trillion. Last week, bond fund outflows quadrupled the previous record, which was set the previous week (chart below). Moody’s and S&P have already declared a significant portion of outstanding debt under review for potential downgrade. Leveraged loan spreads have ballooned to the point that the market for new loan issuance is effectively closed. Bond ETFs have been trading at historic discounts versus the NAV of their underlying bonds. And CLOs are facing the prospect of an existential crisis as Libor plunges and threatens to dip below zero.

Source: Financial Times

Markets rebounded this week as the government passed a stimulus bill and the Fed announced it will dedicate $200 billion to buying corporate debt. Given the size and fragility of the corporate debt bubble, it will prove far too little to stem the reckoning to come.

The implications are seismic. Buybacks and dividends will dry up. Layoffs will spike and consumer spending will plummet. Suffering gig and hourly workers will revolt against reappropriating taxpayer dollars to save corporate powers (WILTWMarch 19, 2019). And the bailout decisions made by the Fed and politicians now will define the presidential election in November.

“Fallen Angels Are Coming and the Fed Can’t Save Them,” read a Bloomberg heading on Tuesday. Moody’s has already dropped the ratings of dozens of companies. Lufthansa has been dropped from Baa3 to Ba1. Occidental Petroleum has faced the same downgrade. On Wednesday, Ford was downgraded by both S&P and Moody’s, becoming the largest fallen angel so far with its $35.8 billion debt pile. This week, JP Morgan analysts estimated that “fallen angels” — companies dropping from investment grade to high yield — will total $215 billion this year, more than double 2005’s record of roughly $100 billion.

Notorious ratings-agency corruption during the GFC has put extraordinary pressure on Moody’s, S&P, and Fitch to stay objective and vigilant today. Over the past year, they have been too complacent. As we documented in WILTW October 24, 2019, corporate balance sheets have deteriorated, yet well-deserved junk downgrades have not come. The ratings agencies now appear hellbent on reversing course regardless of the economic consequences. Their credibility is at stake.

Fallen angels present a two-fold threat. First, many asset managers can only hold so much junk debt. Downgrades will force selling, likely at steep losses. The inevitability of this is already spiking BBB yields (chart below). Second, the Fed’s announced bailout plans will only allow it to support the credit of investment-grade companies. In turn, a downgrade to junk could prove a death sentence for many companies crippled by the COVID-19 lockdown.

Source: Bloomberg

Many companies must borrow to survive, especially small firms. According to Arbor Data Science, 28% of U.S. companies with market caps less than $1 billion are zombies. Yet, it’s not just small businesses. Thirteen companies in the S&P 500 have debt-to-EBITDA ratios greater than eight:

Source: Investor’s Business Daily

With economic uncertainty at an extreme and yields spiking, who is going to lend to zombies right now? Exacerbating that problem, we are now at the start of the debt-maturity wall we’ve warned about for years. Roughly $840 billion of bonds rated BBB or below in the U.S. are set to come due this year.

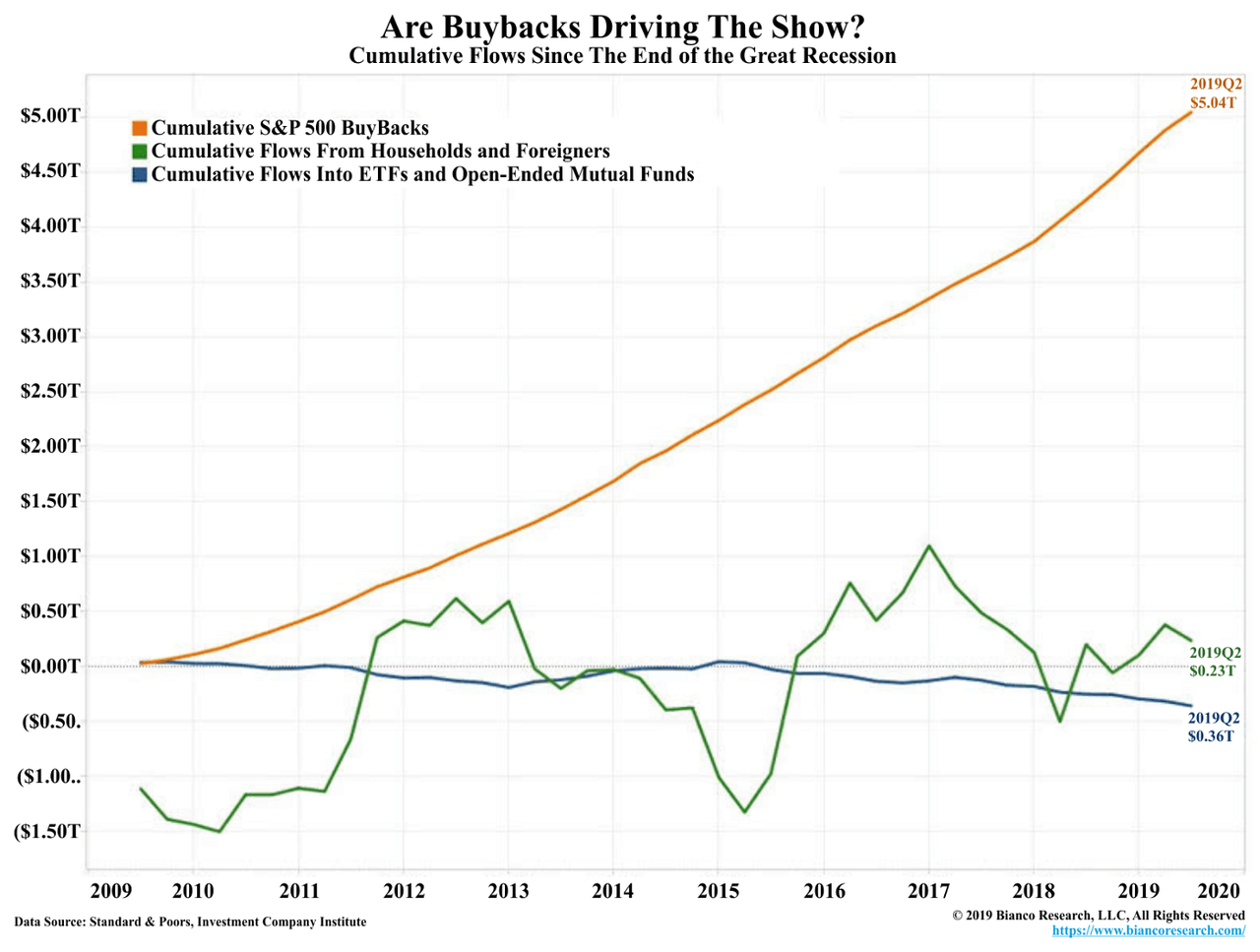

Companies are now racing to tap existing lines of credit, including Macy’s, Best Buy, AT&T, and GE. More are slashing dividends and buyback plans to conserve cash, including Ford, Royal Dutch Shell, Airbus, Freeport-McMoRan, Boeing, and Occidental Petroleum. The past decade’s bull run was built on buybacks (chart below). Now, that pillar is disappearing and regardless of bond buying, the Fed can’t stop it.

Source: Bianco Research

Yet, these are just the known challenges. As in all economic crises, the unforeseen is often the most devastating. Over the past decade, euphoric demand for debt in a yield-starved world has encouraged extreme financial engineering. The question now: How does that machinery react to an extreme shock?

A multitude of insidious risks are likely hidden in the system, as CLOs are now demonstrating. CLOs are tied to Libor. This month, Libor has plunged well below one. The possibility exists that it could dip below zero. This would cause panic in the CLO market. As Wells Fargo CLO analyst Dave Preston told Bloomberg last week: “If Libor falls to a level that produces a negative all-in coupon, it is not clear what would happen.” Roughly one in five CLO tranches have no Libor floor. Meaning, if Libor breaks zero, CLO debt holders would owe money back to the issuer. The problem is: “CLOs are simply not legally or operationally equipped to handle a reversal in cash flow.”

As the IMF warned last year, 40% of total corporate debt is at risk with a shock only half as severe as the GFC. From Goldman Sachs to Morgan Stanley to the St. Louis Fed to Dave Rosenberg, estimates now suggest the COVID-19 shock will likely be far more severe than the GFC.

Corporate debt was the defining excess of the past decade’s bull run. Buybacks were funded by debt — over the past half decade, S&P 500 companies have issued $2.5 trillion in debt to afford $2.7 trillion in buybacks. Debt has subsidized the skyrocketing salaries of CEOs. Cheap debt has enabled private equity to take over and financialize Main Street.

How severe the consequences will be obviously depends on how long COVID-19 keeps the world locked down. However, a reckoning with debt-fueled corporate greed is coming, regardless of Fed bond buying or government stimulus.

“Tiger King” Joe Exotic Moved To Prison Hospital After Being Placed In ‘Coronavirus Isolation’

For the past week or so, people across the US have only been talking about two things: COVID-19, and the “Tiger King”.

Netflix’s latest true-crime docu-series, “Tiger King”, chronicles the exploits of “Joe Exotic”, a former private zoo owner and big cat breeder who became enmeshed in a yearslong feud with an animal-rights activist named Carole Baskin who is widely suspected of murdering her husband (and, in some of the nastier versions of that rumor, of feeding his remains to her tigers).

Exotic, who declared himself the “Tiger King” of the US, ended up in prison after being caught up in a federal murder-for-hire plot that appeared to be an elaborate trap put in place by two of Exotic’s erstwhile business associates, and the FBI.

The documentary has already prompted authorities in Florida to reopen the investigation into the disappearance of Baskin’s husband, and given new life into a possible appeal for Exotic, who was convicted on most of the charges he was facing, and could spend decades in prison. Exotic has also asked for a pardon for President Trump, which we suspect could happen if things keep getting worse and the president needs another ace distraction to occupy the media.

Now, according to Excotic’s fourth husband (in addition to being a gay, gun-toting big cat fanatic, Exotic is also a polygamist who has married several much-younger “husbands”), Exotic has reportedly been transferred from a coronavirus isolation ward to the medical center at his new prison.

Inmate records show that Joseph “Exotic” Maldonado-Passage was recently transferred to the Federal Bureau of Prisons-operated Federal Medical Center Forth Worth in Texas. Exotic had previously been isolated at the Grady County Jail in Chickasha, Okla.

The facility “put him on COVID-19 isolation” because “the previous jail he was at, there were cases,” said Dillon Passage, Exotic’s fourth husband, during an appearance on Andy Cohen’s SiriusXM series “Andy Cohen Live.”

Exotic is currently seeking a combined $94 million from the US Fish and Wildlife Service, his former business partner Jeff Lowe and several former colleagues say. The polygamist announced his lawsuit and issued a call for a pardon from Trump on March 19 on his Facebook page.

The massive 2.2 trillion dollar bill that was signed into law fails most small businesses but the devil is well hidden in the details.

There is so much disinformation and bullshit floating around about this program that it is difficult to get the details. As a landlord and small business owner, I can tell you that as of Thursday morning the way the program is structured it will be of little help to most small businesses. While the government continues to slam expensive legislation through it seems they have no idea of the damage they are doing and how it is causing hundreds of thousands of businesses to close their doors forever. Washington has become so attuned to dealing with lobbyist from mega-companies it has lost sight of the fact small is small, and when this comes to business, this means usually under twenty employees, not hundreds.

90% Of Businesses Are Small

It now looks like this bill will allow for a rapid maximum loan amount of two and a half times a company’s average monthly payroll expense over the past 12 months. This loan would turn into a grant and be forgiven if they keep their employees on. This fails to take into consideration that not all small businesses are labor or payroll intense. Some businesses with large or expensive showrooms are getting hammered by rent, others by inventory, or things like taxes, utilities, or even by having to toss products due to spoilage.

This bill also fails to address the issue of what are these employees going to do while the company has no customers because their cities are going into semi if not complete lock-down measures due to quarantine efforts. They also ignore the fact that by keeping these employees on the payroll a generous employer is left open to the harsh mandates laid out in the previous bill passed just weeks ago. And last but not least, many small business owners take little in the way of a paycheck and pump most of their earnings back into their company so it will grow faster. It appears little is being done for these companies and they are set to remain in dire straights.

With so many tenants looking at foregoing rent, small landlords that don’t have deep pockets also face huge problems. We have our heads in the sand if we think companies that exist on events where people gather will overnight regain their luster. It is not like someone can simply flick a switch and things will return to normal. Reality undercuts the idea of the “V-shaped recovery” theory and the idea after the economy has come to a dead stop it can quickly reboot and be back at full speed in a few months. Washington also seems oblivious to how much it can cost a community when a business fails. This extension of crony capitalism throws just enough to the masses to silence their outrage. Large businesses with access to cheap capital will again be the winners and the big losers are the middle-class, small businesses, and social mobility.

Even with governments pouring money into their economies and central banks adding massive liquidity animal spirits have taken a beating. Much of this can be blamed on the hastily drawn up 110-page federal covid-19 economic rescue package, which Trump fully supported. It dealt a hard blow to small business. The two major reasons existed for strongly objecting to the bill, first, we had no idea what it would cost and second, it totally missed its target while dealing a crushing blow to small businesses across America. Still, the measure sailed through the House with an overwhelming 363-40 vote in less than an hour after the text was released.

Prior to its approval, the National Federation of Independent Business (NFIB) pointed out many struggling businesses with two to twenty workers don’t have the resources to weather the storm that it creates.The NFIB said in their letter of opposition,“The bill would impose potentially unsustainable mandates on small businesses’ hurting not helping the backbone of our local economies.” At the time they are experiencing increasingly slower sales is not the time to hit small businesses with a new mandate. Unlike government agencies, small business owners cannot turn to taxpayers when they can’t pay their bills. For a small business this is a disaster, the bill requires;

Employers with fewer than 500 employees and government employers offer two weeks of paid sick leave through 2020.

Those same employers must now provide up to 3 months of paid family and medical leave for people forced to quarantine due to the virus or care for family because of the outbreak

As expected, this measure, named “Families First Coronavirus Response Act.”resulted in millions of workers to suddenly lose their jobs. Ironically, it was held before the voters as proof lawmakers could work together during a crisis. By framing the poorly crafted pork-packed bill this way promoters positioned themselves to demonize those unwilling to support it. Remember, this bill is was in addition to the $8.3 billion emergency spending bill already approved to curb the spread of covid-19.

As for the President, many political pundits see Trump’s declaration of a national emergency 15 minutes before the market closed on Friday a contrived stunt to rally stocks. In addition, his endorsement of this package is seen as an effort to mitigate damage from his administration’s initially weak response to the crisis. Still, while we are told his job approval is rising many of us view what is flowing out of Washington as ill-conceived. Why will anyone want to work, especially government workers when they can get paid to stay home? How do you staff healthcare facilities when nobody comes to work?

President Trump may not understand at what point a small business becomes a medium or large business or simply doesn’t care. Ironically, the members of the NFIB, mostly small business owners of privately-owned companies with fewer than 20 employees, strongly supported this same President that is throwing them under the bus.

By framing these pork-packed bills as bipartisan their promoters imply they are fair and balanced. This is not true, small business is the big loser and hundreds of thousands will soon have to close.

The Covid-19 Rescue plan crucified our small businesses and the 2,2 trillion dollar bill that followed is a costly boondoggle mainly for the rich.

Let me be clear, this is not about wanting more money for small business, it is about government not being able to clean up the mess it creates by simply throwing money at it. Please just stop!

CNN anchor Brooke Baldwin just confirmed on Instagram that she has tested positive for COVID-19, joining her colleague, Chris Cuomo, among the more than 1 million people around the world who have been infected.

Baldwin, a star reporter on America’s most trusted Fake News organization, said on Instagram that she is “OKAY” and has “chills, aches, fever.”

During one recent news report shared on Baldwin’s twitter account, she can be heard acknowledging that some small studies have shown the malaria and lupus drugs hydroxychloroquine and chloroquine (which can purportedly be used, sometimes together with azythromycin, to alleviate sometimes deadly symptoms) promoted by President Trump – which CNN had earlier bashed – actually have been shown to help COVID-19 patients.

Early data from China has linked hydroxychloroquine, a drug used to treat malaria, with helping patients relieve coronavirus symptoms.

“We always want to have guarded optimism… It’s a study that needs to be repeated,” says infectious disease specialist Dr. Wilbur Chen. pic.twitter.com/DFbPf00seC

Hopefully, Baldwin won’t need those – or any – prescription medication to deal with the virus as her body fights it off. We also hope she doesn’t have crazy nightmares and chip a tooth like her colleague, Chris Cuomo. Before people start accusing Cuomo of passing it to his colleague, CNN hasn’t said anything about how the virus spread.

{kind=link}