The US Constitution never granted the federal government authority to create a central bank. The Founders, having lived through hyperinflation themselves, understood that government should never have a printing press at its disposal. But from the very beginning of America’s founding, the desire for a crony central bank was strong.

In fact, two attempts were made at creating a permanent central bank in America prior to the creation of the Fed. Fortunately, the charter for The First Bank was allowed to expire in 1811, and President Andrew Jackson closed down the Second Bank in 1833.

But, unfortunately, a third attempt was successful and the Federal Reserve was unconstitutionally created by Congress in 1913. Americans have been living under a corrupt and immoral monetary system ever since. The Federal Reserve is the printing press that has financed the creation of the largest government to ever exist. Endless welfare and endless military spending are both made possible by the Federal Reserve. The Fed can just print the money for whatever the US establishment wants, so those of us who long for a Constitutional and limited government have few tools at our disposal.

Despite all the propaganda claiming “independence,” the Fed has always been a deeply political institution. Because the Fed is a government-created monopoly with key government-appointed employees, its so-called “independence” is a mere fiction. However, the US Congress created the Fed with legislation; it can also abolish the Fed with legislation.

Last week, the facade of Federal Reserve “independence” was dealt a severe blow. Ironically, the person who broadcast to the world that the Fed is anything but “independent” was ex-New York Fed President Bill Dudley. Dudley wrote that, “Trump’s re-election arguably presents a threat to the United States’ and global economy, and if the goal of monetary policy is to achieve the best long-term economic outcome, the Fed’s officials should consider how their decisions would affect the political outcome of 2020.”

The timing of Dudley’s threats to use Fed monetary policy to affect the outcome of a US election couldn’t come at a more striking time. After all, for more than two solid years Americans have been bombarded with fabricated stories about Russians rigging our elections. And yet here is a Federal Reserve official threatening to do the same exact thing – but this time for real!

Whether it’s the mainstream media, the CIA, the FBI, or now the Federal Reserve, more and more Americans are waking up to the fact that there is a Deep State in America and its interests have nothing to do with American liberty. In fact, our liberty is what the Deep State wants to abolish.

When it comes to the Federal Reserve, I stand firmly by my conviction that it needs to be audited and then ended as soon as possible.

America’s Founders were not perfect. They were human beings just as capable of error as we are. But they had a remarkable understanding of the ideas of liberty. They understood that liberty cannot exist with a government that has access to a printing press. Sound money and liberty go hand-in-hand. If we want to enjoy the blessings of Liberty, we must audit and then end the Federal Reserve!

via ZeroHedge News https://ift.tt/2ZODkWu Tyler Durden

Markets have only just opened in the US, and already Wednesday is shaping up to be a difficult day for Alphabet, the parent company of Google and YouTube.

First, the FT published a report based on leaks from the Irish data regulator, which has jurisdiction over Google’s European operations since the company’s European headquarters is based in Dublin. Google has allegedly been using ‘hidden’ web pages to feed personal data gleaned from its users to paying advertisers, circumventing the EU’s GDPR privacy regulations in the process.

Google rival Brave said it submitted evidence of this arrangement to the company’s regulators. Google collects sensitive user data, like the race, health status and political leanings of its users, then secretly harvests this data for use in targeting ads, something that’s illegal in Europe.

Johnny Ryan, Brave’s chief policy officer, told the FT that he discovered the secret web pages as he tried to monitor how his data were being accessed and used on Google’s advertising exchange, which is the largest marketplace for ad sales space across the web.

Ryan said he discovered that Google had labelled him with an identifying tracker that it fed to third-party companies, which logged on to a hidden web page. The page showed no content, but it tracked Ryan’s browsing activity.

This appears to violate Google’s own rules prohibiting ad buyers from matching different social media profiles for the same user, in addition to EU laws and regulations.

A spokesperson for Google said the company hadn’t seen the details of Ryan’s independent “investigation”, but added that it was cooperating with any and all investigations carried out by European regulators.

In other news, YouTube agreed to pay $170 million to the FTC and the AG of New York State to settle allegations that it illegally collected data from children younger than 13 who watched children’s content on the platform, according to the Washington Post.

Regulators alleged that certain YouTube knew certain channels were popular among younger viewers, and that it touted this fact to brands and advertisers. To gather more data, YouTube tracked kids’ viewing histories for the purpose of serving them targeted advertisements, ultimately raking in “millions of dollars” despite obviously violating children’s privacy laws.

YouTube also agreed to change its business practices by ending the collection of data on YouTube of videos that are clearly created with younger audiences in mind. The settlement echoed concerns raised by nearly two dozen consumer privacy groups, who alleged that YouTube was side-stepping COPPA – or the Children’s Online Privacy Protection Act – the only federal law explicitly governing what tech firms are allowed to do regarding user data collection.

Still, the settlement, which didn’t require the company to admit guilt, stopped short of what advocates were hoping for.

YouTube CEO Susan Wojcicki said in a blog post Wednesday that the settlement would “better protect kids and families on YouTube,” adding:“We’ll continue working with lawmakers around the world in this area.”

via ZeroHedge News https://ift.tt/2NVsCeB Tyler Durden

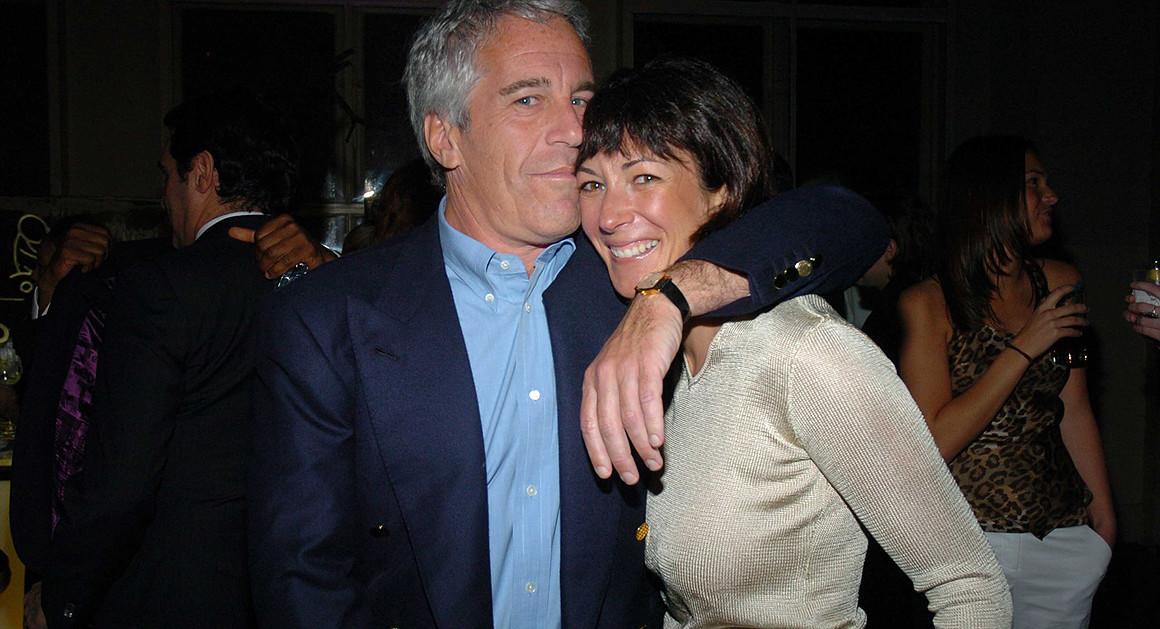

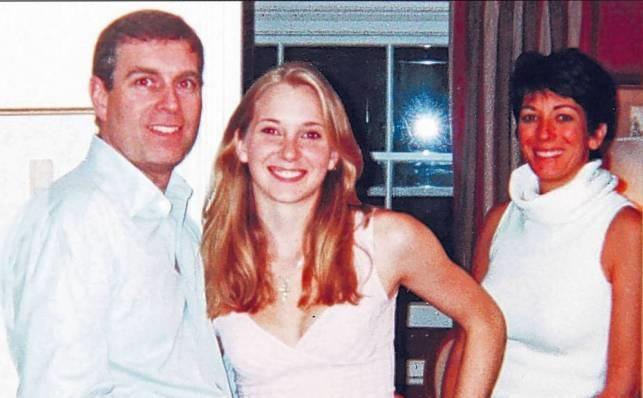

An attorney for Jeffrey Epstein confidant (and alleged groomer) Ghislaine Maxwell told a judge on Wednesday that there are “hundreds” of people named in what is expected to be approximately 2,000 pages of documents ordered unsealed by the federal appeals court in New York, according to Bloomberg.

The lawyer, Jeffrey Pagliuca, told U.S. District Judge Loretta Preska Wednesday that the materials also include an address book with about 1,000 names. Preska is considering how to carry out a ruling by the federal appeals court in New York that she must consider unsealing some of the documents. There was no detail at the hearing as to the identity of the people are named in the documents, and they may include women who say they are victims of Epstein, his friends and others. –Bloomberg

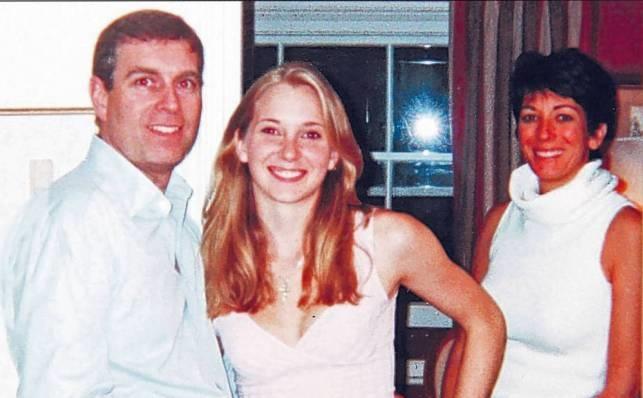

Prince Andrew, Virginia Roberts (Giuffre) and Ghislaine Maxwell

According to court filings, Maxwell was said to have hired, supervised and fired household staff, while directing the visits of dozens of “massage therapists” to Epstein’s residence, according to the Journal.

In depositions taken in 2009 and 2010 as part of civil lawsuits against Mr. Epstein, household employees said Ms. Maxwell was a central figure in Mr. Epstein’s private life. Several said Ms. Maxwell hired, supervised, and fired household staff, while directing the visits of dozens of “massage therapists”—typically young women.

Juan Alessi, who said in one of the depositions that he served as the Palm Beach house manager from around 1992 through 2002, described a basket of sex toys in Ms. Maxwell’s bathroom closet. He said he would find them around when he cleaned up after visits from the young women. –WSJ

The document release stems from a 2015 defamation lawsuit in New York brought by Epstein accuser Virginia Roberts Giuffre against Maxwell. Giuffre says Maxwell helped Epstein traffic herself and other underage girls to sex parties at the billionaire pedophile’s many residences. Maxwell has denied any wrongdoing and called Giuffre a liar.

The case was settled in 2017 and the records were sealed – however appeals by the Miami Herald, Harvard Law professor (and former Epstein pal) Alan Dershowitz and right-wing blogger Mike Cernovich were successful.

In August, the US Court of Appeals for the Second Circuit has ordered the partial releaseof Epstein documents, which revealed that Giuffre said that President Trump was a “good friend of Jeffrey’s,” but that Trump ‘didn’t partake in any sex with any of us,” adding “Donald Trump never flirted with me.”

Epstein was found dead in federal lockup last month after his arrest on child sex-trafficking charges. While the case was dismissed against Epstein, Judge Preska must now consider how to release the sealed records – and from the looks of it, the possibility remains that they may not be released at all.

via ZeroHedge News https://ift.tt/30TQJ0E Tyler Durden

Our swanky lifts blare out constant BBC News Opinion. Overheard this morning: “Switch it off.… we’re bored..”

There is other stuff going on. Trade continues to dominate the flows – when will we get the next meeting between the US and China? Not that we have particularly high expectations anything will happen, especially when Donald was tweeting about a deal now will be tough, but if the Chinese drag it into his second term it will be even more painful!

Signals of a slowing US economy in terms of the Manufacturing ISM below 50 (which is a bad sign confirming trade wars bite and is causing a contraction of production) drove a bond frenzy y’day. (Bad for stocks.) A record $30 bln day in terms of new US corporate issuance scream the headlines. Despite the volume, corporate bond spreads remain tight to treasuries. Meanwhile, we’re expecting over €20 bln of new bonds issued in Europe this week. More junk bonds into negative yield territory!

How long will it last? Friday’s US employment data isn’t half-as-important as folk think, but it’s still a critical barometer that could upset expectations short-term. The ECB has been sending mixed signals about what to expect at next week’s meeting. The market expects a new asset purchase plan – and we’ve had ECB board members speculating maybe not. Gosh! The toddler that is the market will have an almighty tantrum if it doesn’t get new toys!

Away from markets, Italy looks calmer (better not say anything lest I get accused of the pot calling the kettle dirty). It also looks like Hong Kong’s leader Carrie Lam is set to withdraw the extradition bill that triggered the current discontent. We’ve seen this kind of thing before – you can’t push tear gas back into the bottle once its been opened! However, it might be a short term buy-signal, or to exit names like HSBC.

But let us blather about the Pachyderm in the room…

I reckon you can pretty much forget about Brexit this year, maybe next. After yesterday’s masterclass in parliamentary chaos, the UK now faces an election and whoever wins will either have to overturn legislation forbidding a “No-deal” before dealing yet again with Brussels, or the victors will lead the country into a divisive second referendum which will probably result in decades of bitterness. It feels the UK is going nowhere – but it’s what now passes as political process.

The Tories should have been well placed to win an election: able to do a constituency by constituency deal with the Brexit Party, ridding themselves of their Remoaners, and with a clear policy platform to Brexit. But they did themselves no electoral favours yesterday. They made dreadful, but avoidable political mistakes. What the electorate will remember is a poor performance from Boris, but, critically, Rees-Mogg’s contemptuous sneering posture.

He may be a constitutional genius, but that’s now what voters want. Like so many of the current runt crop of politicians, Mogg has absolutely no sympatico for the common people – and that’s the nub of who will win. Who can best express and seize the imagination of the UK electorate is critical. The Brits are sick of petty politics and looking for change. Boris was on course, but I wonder if he’s blown it?

In short, lots more still to go wrong here in the UK. Anything is pure speculation. It could go something like this:

No Deal Legislation passes this week or early next

Election called for November

Europe agrees extension to Jan 2021

New Tories win Majority in election.. overturn no-deal legislation

New negotiation with Brussels goes nowhere – despite Boris’ new mandate.

No Deal Exit Jan.

Or it might be more like this:

Labour loses election with small minority – but forms govt supported by Lib Dems and SNP

Lib Dems promised a New Referendum on the deal proposed by Brussels – accept exit deal or stay

SNP promised a new Independence referendum

Labour govt fractures between Brexiteers and Remainers.

No Brexit

Brexit remains focus of UK politics till next election.

Who knows… who cares anymore?

via ZeroHedge News https://ift.tt/2HLvVRD Tyler Durden

Iran’s Fars News Agency has cited a top Iranian official who said that Tehran would return to its nuclear deal commitments only if it receives $15 billion for oil sales by the end of the year.

It appears President Macron’s last ditch effort to create conditions to eventually bring Tehran and Washington back to the nuclear negotiating table by offering Iran a $15 billion credit line as an incentive to come back into compliance with the nuclear deal is making headway. However, the US would have to soften on its harsh 100% Iran oil sanctions to meet Tehran’s conditions for the credit line.

“Iran… will return to full implementation of the JCPOA only if it is able to sell its oil and to fully benefit from the income from these sales,”said Deputy Foreign Minister Abbas Araghchi on Wednesday. “The French proposal goes in that direction.”

Iranian President Hassan Rouhani at the Bushehr nuclear power plant in Bushehr, Iran. Image source: Iranian Presidency office/EPA-EFE

However, massive and significant obstacles remain – not the least of which is that Iran’s President Hassan Rouhani just issued new ultimatums to European signatories to the 2015 nuclear deal. The European powers have another two months to save the JCPOA, Rouhani said in a speech Wednesday.

Meanwhile as details of the $15BN credit line are hammered out, Iran said it’s prepared to take further measures to walk away from its terms under the nuclear deal, likely in the form of another uranium enrichment cap breach, which would mark the third such purposeful violation designed to pressure Europe and Washington.

Rouhani had threatened to take the extra step by Thursday unless France and others act quick: “I think it is unlikely that we will reach a result with Europe by today or tomorrow … Europe will have another two months to fulfill its commitments,”Rouhani said according to state sources.

“The talks between Iran and European countries are moving forward … but we have yet to reach a conclusion,” he added. “Iran’s third step is of an extraordinarily significant nature,” he warned of plans to further remove Iran from conformity to the nuclear deal.

The International Atomic Energy Agency issued a report last week stating Iran is still enriching uranium up to 4.5 percent, which is above the 3.67% stipulated by the JCPOA but still significantly below weapons-grade levels of 90%.

As for France’s $15BN credit line plan, for it to actually work it’s crucial that the Trump administration would have to buy in – which is the main obstacle. A US decision is expected by the end of the week as a French delegation is in Washington to discuss the proposal.

via ZeroHedge News https://ift.tt/2PHWKMX Tyler Durden

Former Federal Reserve Chairman Alan Greenspan recently said he wouldn’t be surprised if yields on U.S. bonds turned negative and if they do, it wouldn’t be “that big a of a deal.”

That seems to be a sentiment widely held in central banking circles these days, but it’s wrong. Negative interest rates represent a threat to the financial system.

To understand why, let’s start with the existing fractional reserve banking system, which is more than a century old. For every dollar that goes into a bank, some set amount (usually about 10%) must go into a reserve account to be overseen by the central bank. The rest is either lent out or used to buy securities.

In other words, the fractional reserve banking system is leveraged to interest rates. This works when rates are positive. Loans are made and securities bought because they will generate income for the bank. In a negative rate environment, the bank must pay to hold loans and securities. In other words, banks would be punished for providing credit, which is the lifeblood of an economy. As German bankers recently explained to the European Central Bank:

We already have a devastating interest rate situation today, the end of which is unforeseeable,” Peter Schneider, who represents public-sector savings banks in the southern German state of Baden-Wuerttemberg, said on Wednesday. “If the ECB aggravates this course, that would hit not only the entire financial sector hard, but especially savers.

And to make matters worse, the German government is considering outlawing negative deposit rates. In a negative rate world, forcing rates on short-dated debt to zero would keep the yield curve permanently inverted. The fractional reserve banking system cannot operate properly in this environment.

Valuation models are another area of finance that need to be tweaked in a negative rate environment. Nobel prizes have been awarded to economists that developed concepts such as the efficient frontier, the Capital Asset Pricing Model and the Black-Scholes option pricing model. But when a negative value is assumed for the risk-free rate in these types of models, fair value results shoot off toward infinity. With trillions of securities and derivatives dependent on these models, valuation is critical.

In a similar vein, pensions use a discount interest rate to determine if they are properly funded. If one plugs in a negative interest rate as the discount rate, all pensions would technically be underfunded. The only pensions that would be properly funded would be those with assets exceeding expected liabilities. No pension is set up this way. Negative rates on fixed-income securities also means there is no way pension funds can ever generate enough income to meet their obligations.

When repurchase, or repo, rates go negative, lenders of securities must pay rather than receive income. Why would anyone lend out their securities if they also must pay for the privilege of doing so? Repos are the basic plumbing of the financial system, enabling the trade and settlement of securities transactions. If this market becomes dysfunctional, it is akin to the pipes in your walls leaking.

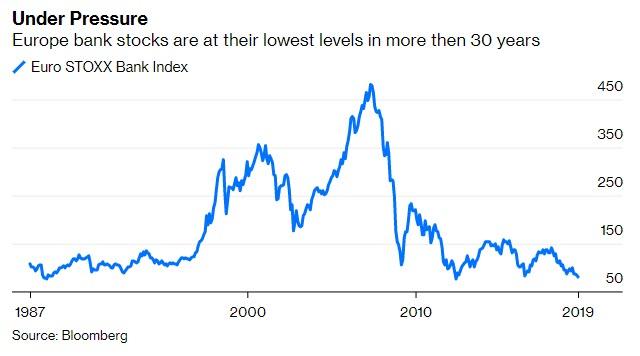

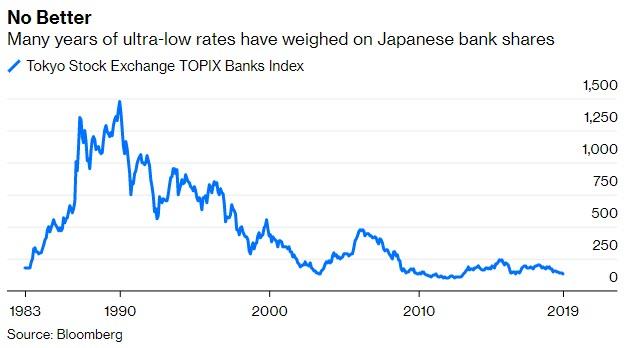

To see the results of low or negative rate environments, look no further than the euro zone and Japan. They account for 87% of the negative rates worldwide. Europe is essentially in recession with negative GDP in Italy, Germany and elsewhere. Its banking system is a mess, thanks to negative rates. As the chart below shows, European banks are trading at the lowest levels in more than 30 years.

Japan is not doing much better. Economists are projecting negative GDP in the fourth quarter and the Japanese banking system is even worse than Europe’s, trading at some of the lowest since the early 1980s.

These are not isolated occurrences. The first instances of modern negative interest rates arrived in Switzerland in the 1970s. As Bloomberg Opinion Columnist Stephen Mihm recently detailed, the results were not pretty.

The U.S., UK, Canada, Australia and New Zealand are the only developed bond markets that do not have negative rates anywhere on their yield curves. Should these countries join the rest of the developed world in moving to negative rates, the financial system will be under much more stress. If negative rates become more widespread across the globe, then the financial system needs to be rebuilt on a new set of assumptions. The problem is we do not yet know what those should be or how they would work.

via ZeroHedge News https://ift.tt/2HIhT2U Tyler Durden

After years of radio silence, Dr. Michael Burry – the small-time stockpicker who rose to fame for his bets against subprime mortgage bonds featured in the book (and later film) “the Big Short” – is once again doing the media rounds, talking about his latest equity plays and sharing his thoughts about the next big market blowups.

And in an interview with Bloomberg, Burry doesn’t disappoint. At one point, he shares his skepticism about passive investing, and the flood of money that has poured into index funds since the financial crisis. Burry sees similarities between these funds and the CDOs that nearly brought down the financial system in the run-up to the crisis.

Burry, who made a fortune betting against the CDOs, argued that these passive flows are distorting prices for stocks and bonds in much the same way that CDOs did for subprime mortgages. Eventually, the flows will reverse at some point, and when they do, “it will be ugly.”

“Like most bubbles, the longer it goes on, the worse the crash will be,” Burry, who oversees about $340 million AUM at Scion Asset Management in Cupertino, said.

That’s one reason he likes small-cap value stocks: they tend to be underrepresented in index funds, or left out entirely.

Here’s what Burry had to say on a number of topics:

Index funds and price discovery:

Central banks and Basel III have more or less removed price discovery from the credit markets, meaning risk does not have an accurate pricing mechanism in interest rates anymore. And now passive investing has removed price discovery from the equity markets.

The simple theses and the models that get people into sectors, factors, indexes, or ETFs and mutual funds mimicking those strategies – these do not require the security- level analysis that is required for true price discovery.

“This is very much like the bubble in synthetic asset- backed CDOs before the Great Financial Crisis in that price-setting in that market was not done by fundamental security-level analysis, but by massive capital flows based on Nobel-approved models of risk that proved to be untrue.”

Liquidity Risk

“The dirty secret of passive index funds – whether open- end, closed-end, or ETF – is the distribution of daily dollar value traded among the securities within the indexes they mimic. In the Russell 2000 Index, for instance, the vast majority of stocks are lower volume, lower value-traded stocks. Today I counted 1,049 stocks that traded less than $5 million in value during the day. That is over half, and almost half of those – 456 stocks – traded less than $1 million during the day. Yet through indexation and passive investing, hundreds of billions are linked to stocks like this. The S&P 500 is no different – the index contains the world’s largest stocks, but still, 266 stocks – over half – traded under $150 million today.”

“That sounds like a lot, but trillions of dollars in assets globally are indexed to these stocks. The theater keeps getting more crowded, but the exit door is the same as it always was. All this gets worse as you get into even less liquid equity and bond markets globally.”

It Won’t End Well

“This structured asset play is the same story again and again – so easy to sell, such a self-fulfilling prophecy as the technical machinery kicks in. All those money managers market lower fees for indexed, passive products, but they are not fools – they make up for it in scale.”

“Potentially making it worse will be the impossibility of unwinding the derivatives and naked buy/sell strategies used to help so many of these funds pseudo-match flows and prices each and every day. This fundamental concept is the same one that resulted in the market meltdowns in 2008. However, I just don’t know what the timeline will be. Like most bubbles, the longer it goes on, the worse the crash will be.”

BoJ Cushion

“Ironically, the Japanese central bank owning so much of the largest ETFs in Japan means that during a global panic that revokes existing dogma, the largest stocks in those indexes might be relatively protected versus the U.S., Europe and other parts of Asia that do not have any similar stabilizing force inside their ETFs and passively managed funds.”

Undervalued Japan Small-Caps

“It is not hard in Japan to find simple extreme undervaluation – low earnings multiple, or low free cash flow multiple. In many cases, the company might have significant cash or stock holdings that make up a lot of the stock price.”

“There is a lot of value in the small-cap space within technology and technology components. I’m a big believer in the continued growth of remote and virtual technologies. The global retracement in semiconductor, display, and related industries has hurt the shares of related smaller Japanese companies tremendously. I expect companies like Tazmo and Nippon Pillar Packing, another holding of mine, to rebound with a high beta to the sector as the inventory of tech components is finished off and growth resumes.”

Cash Hoarding in Japan

“The government would surely like to see these companies mobilize their zombie cash and other caches of trapped capital. About half of all Japanese companies under $1 billion in market cap trade at less than tangible book value, and the median enterprise value to sales ratio for these companies is less than 50%. There is tremendous opportunity here for re-rating if companies would take governance more seriously.” “Far too many companies are sitting on massive piles of cash and shareholdings. And these holdings are higher, relative to market cap, than any other market on Earth.”

Shareholder Activism

“I would rather not be active, and in fact, I am only getting active again in response to the widespread deep value that has arisen with the sell-off in Asian equities the last couple of years. My intention is always to improve the share rating by helping management see the benefits of improved capital allocation. I am not attempting to influence the operations of the business.”

Betting on a Water Shortage

“I sold out of those investments a few years back. There is a lot of demand for those assets these days. I am 100% focused on stock-picking.”

Late last month, Burry sat for an interview with Barron’s, where he explained his reasoning for his latest long position in GameStop. The embattled video-game retailer was undervalued, Burry argued, because the next generation of video game consoles from Sony and Microsoft were likely to feature physical optical disk drives, meaning gamers would have to buy the games from a brick-and-mortar retailer if they wanted to play them that day. He added that the “streaming narrative” had led GameStop’s shares to be extremely undervalued, and that 90% of the chain’s 5,700 stores were FCF positive.

via ZeroHedge News https://ift.tt/2PKcX4j Tyler Durden

Unfortunately for former Goldman managing director and NY Fed president, Bill “let them eat iPads” Dudley, that is a saying he is not familiar with, and one week after his stunning Bloomberg op-ed in which he advocated the Fed to prevent Trump’s 2020 re-election by sending the economy in a recession, resulting in a brutal response from virtually everyone who slammed Dudley’s musings as the final proof that the Fed was in fact a political animal, one which is more powerful than the executive branch in its ability to pick and choose presidents, Dudley is out with an “explainer”, seeking to “answer” some of the main questions posed by his “provocative” piece.

After reading “What I Meant When I Said ‘Don’t Enable Trump“, let’s just say that Dudley fails in explaining why he said is not what he said, and if anything he has successfully doubled down, giving Trump even more ammunition to throw the book at the political Fed for not cutting rates fast enough as the president has been demanding for months, and for eventually taking the blame for the coming economic and market crash.

Dudley’s letter, written in rhetorical Q&A format, begins by asking himself what motivated him to write this article. His answer is two fold:

First, President Trump’s trade war with China was increasing uncertainty about how global trading rules would evolve, what tariffs would be imposed, what changes firms might need to make to their global supply chains, and what the downside risks might be for the U.S. economy. Just a few days before the article was published, the president ordered U.S. firms to pull out of China.

Second, the president continued to attack the Federal Reserve and push it to ease monetary policy further. He emphasized that the Fed, not the White House or its trade war with China, should be blamed if the economy faltered. His attacks on the Fed included characterizing Chairman Jerome Powell as an “enemy” — on par, in his view, with President Xi Jinping of China.

As Dudley “saw it”, the combination of the trade war and the president’s attacks on the Fed “threatened to put the central bank in an untenable position”, one where Trump was shifting responsibility for the downside risks from his trade war onto the Fed. “I thought this was an important issue worth exploring.”

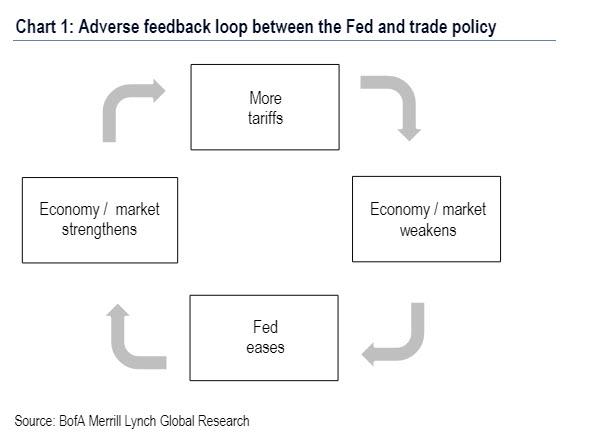

What Dudley means here is that whereas traditionally the Fed has been commended for bailing out banks the world by throwing trillions of dollars at a problem and hoping it goes away, even though some time in 2016 it became clear that this approach was doomed to failure and so it would be great to have a hapless scapegoat in the White House – i.e., someone such as president Donald Trump – to take the blame for decades of disastrous monetary policy which has resulted int he world’s biggest asset bubble in history, what happened next was not part of the program, namely Trump flipping the table on the Fed and making it the key catalyst for the upcoming US recession.

Indeed, one can say that Trump – painted daily as a bumbling buffoon by his enemies, and sometimes, friends – has in fact played his cards perfectly, demanding the Fed cut rates well into late 2018, something which the Fed eventually did, and giving Trump all the leverage in claiming that he was, in fact right, and the Fed was wrong. Certainly, with the market now expecting 4 or more rate cuts by the end of 2020 and tying the fate of the S&P to this expectation being fulfilled, one can argue that Trump will be even more right, and that the Fed – who can forget Powell’s famous statement that we are “a long way” from neutral less than a year ago when the Fed chair was still hawkish – was not only wrong, but clueless.

As such, one can counter Dudley’s rambling, defensive op-ed part 2 published today in Bloomberg, by simply pointing out that the reason for the former Goldman banker’s anger is not so much Trump’s trade war with China – which increasingly more Americans agree with and even Trump’s enemies concede was long overdue – nor Trump’s “attacks” on Fed independence, of course the Fed was never actually independent as anyone who remembers how LBJ literally attacked a Fed chairman in 1965, demanding more money, knows very well, but because Trump managed to quickly and effectively outsmart the Fed, and box the Fed chairman so that the Fed is now forced to underwriter Trump’s trade war, as we explained first one month ago.

So, apparently unable to express what he meant the first time around and sparking a firestorm of criticism, what was Dudley’s oh so complicated message that was lost in translation:

First, the Fed needs to be cautious that it does not inadvertently enable the president’s trade war with China.

As I wrote: “what if the Fed’s accommodation encourages the president to escalate the trade war further, increasing the risk of recession? The central bank’s efforts to cushion the blow might not be merely ineffectual. They might actually make things worse.”

In my judgment, there is a risk that the Fed, by easing, might encourage the president to take even more aggressive actions on trade and in raising tariffs. This might create even greater downside risks for the economy that monetary policy might prove ill-suited to address.

One can argue that this is a credible complaint. The only problem is Dudley should be addressing his anger not at Trump, but at Powell, who certified before the world that any further escalations in Trump’s trade war are effectively a justification for more rate cuts, for one simple reason: the US economy was doing well enough not to need a rate cut, yet the Fed – having become the world’s central bank – desperately needed a pretext to cut, and found one in Trump’s trade war. Whether this was Powell’s intention is unclear, although as we said at the time, “it certainly means that Trump is now de facto in charge of the Fed’s monetary policy by way of US foreign policy, and it also means that as BofA wrote, “the Fed is unintentionally underwriting the trade war.”

Of course, what Dudley is concerned about is not the trade war itself, but how it could implicate the Fed as the global economy continues to grind to a halt, and as he says, “the Fed’s problems might not end there. Not only might the Fed be unable to rescue the economy, but it also might be blamed for the economy’s poor performance. This risk is higher because of the president’s ongoing attacks on the Fed.” This is a point he echoes toward the end of the article as well, writing that “I don’t think the Fed should be attacked for the economy’s performance when the president’s own actions are creating the downside risks.”

Bingo: that’s it right there – the “risk” that the Fed may be blamed for not just the “economy’s poor performance” but that the great unwashed masses may one day wake up and realize that the reason why the global financial system is facing a crisis of monumental proportions has nothing to do with Trump – who is merely a vessel and a symptom of a broken system – and everything to do with a central bank which ever since its creation in 1913 has had one purpose, to make the rich richer and perpetuate a broken monetary system (even Mark Carney is saying the days of the dollar as a reserve currency are now over), is why Dudley is so very much on edge. After all, those same great unwashed masses, following the moment of epiphany may pay Dudley a visit in his mansion and demand an explanation of their own why everything has gone to hell, as it almost certainly will after the next recession.

Once one realizes that this is the true motive behind not just today’s Dudley article, but also his prior op-ed, then everything falls into place, including Dudley’s hint that the Fed’s actions will affect the “political outcome in 2020.”

Addressing what was arguably the most sensitive aspect of his original oped, namely the conclusion which suggested that the Fed should throw the economy into recession just to prevent Trump’s re-election, to wit:

“There’s even an argument that the election itself falls within the Fed’s purview. After all, Trump’s reelection arguably presents a threat to the U.S. and global economy, to the Fed’s independence and its ability to achieve its employment and inflation objectives. If the goal of monetary policy is to achieve the best long-term economic outcome, then Fed officials should consider how their decisions will affect the political outcome in 2020.”

… Dudley says that his “intention was to be provocative.” So what was his intention, if not to bring attention to the fact that contrary to countless lies, the Fed was never independent? He explains:

I was exploring where logic might take you if you started with two premises: 1) President Trump’s trade war was likely to be bad for the U.S. economy, and 2) the Fed’s goal is to achieve the best long-term economic outcome with respect to employment and inflation. In such circumstances, how should the Fed behave and what should it consider?

I was suggesting that if the Fed pushed backed that it might be able to achieve a better economic outcome. I was not suggesting that the Fed should do so regardless of the consequences for the economy or that it should stand by and allow a recession. And I was not trying to suggest that the Fed should take sides in the upcoming election.

So… Dudley’s point is that the Fed is not political, and yet it should push back on the president’s decisions to “achieve a better economic outcome”? A quick question here: Better for who? The banks, which were the only beneficiaries of Fed policies for the past decade? The 0.01% who got richer and richer since the financial crisis as the US middle class disappeared? And then there is the question of what mandate does the Fed have, in Dudley’s eyes, to one up the president when it comes to the best economic outcome.

Actually, an even simpler question: who “elected” the Fed? And just whose interests does the Fed represent? Maybe for the third part of his increasingly surreal op-ed series, Bill Dudley can start with a discussion of just how the Fed – an entity which as Bernanke’s former advisor once said: “people would be stunned to know the extent to which the Fed is privately owned” – represents the interests of the majority of Americans.

Then again, we doubt there will be a part 3 as by this point the backpedaling in Dudley’s “explainer” was so furious, not even he had any idea what it was he was trying to say, as the following “Q & A” confirms:

Q. Do you think the Fed should conduct monetary policy with an eye on influencing the outcome of the 2020 presidential election?

A. I do not. Doing so would be far outside the scope of the Fed’s authority and clearly inappropriate. Moreover, the Fed would be perceived as partisan and such a perception would likely compromise the Fed’s independence. Behaving in such a manner not only would be wrong, but it also would not be in the Fed’s interests.

So, it’s not within the scope of the Fed’s authority to influence the outcome of a presidential election as that would “compromise the Fed’s independence”, but it is the scope to “achieve a better economic outcome” than that pursued by the president? Interesting, please tell us more.

And so he does, when in the very next rhetorical answer, Dudley tries to reconcile what he wrote in: “Fed officials should consider how their decisions will affect the political outcome in 2020.”

I think central bankers should be aware of all the factors that affect the economic outlook. What the Fed does or doesn’t do can influence electoral outcomes, which in turn can have consequences for the economy and for monetary policy. But the Fed should never be motivated by political considerations or deliberately set monetary policy with the goal of influencing an election.

In other words, be aware of how your actions could sink Trump’s reelection chances, but… don’t follow through on them, especially since that would confirm the issue raised above, namely that the Fed was never independent and apolitical, and would culminate with the end of the US Federal Reserve, And yes, it is ironic that Dudley’s letter has done more damage to the perception of Fed “independence” than hundreds of Trump tweets slamming Powell.

In parting, and having “resolved” any speculation that he was calling for a monetary coup against the president – at least in his own mind – Dudley touches on the two most important points address in his letter, Fed independence, and what on earth prompted Dudley to write the original “hornets nest” op-ed in the first place.

So, on the first topic, whether “the Fed has been politicized”, Dudley answers:

In my view, President Trump’s persistent attacks on the Fed have politicized the central bank. People now wonder whether the president’s attacks are influencing the Fed’s decisions. For example, if the Fed eases monetary policy further at its upcoming September policy-making meeting, people are likely to wonder about the motivation. Is it concern about the economic outlook, or the president’s attacks on the Fed? In contrast, I don’t believe the Fed is politicized in the sense that it would consider trying to influence election outcomes.

Once again, the Fed was always politicized (see LBJ vs William McChesney Martin, and countless other examples of presidents bossing Fed Chairs around), but it desperately tried to deflect attention from this to avoid being called into Congress any time the leading political party needed lower rates to pursue a voter-friendly agenda, as will be the case with Helicopter money, aka MMT, in a few years, when the Fed will no longer be an independent entity in any capacity, and will be tasked with monetizing all the debt the US issues to pursue its Green New Stupidity.

However, where Dudley made a catastrophic fuck up is by himself suggesting that the Fed should not only try but succeed in influencing an election outcomes. It is this potentiality that sparked the outcry from both Democrats and Republicans, both Austrians and Keynesians alike, as that level of truth only emerges during periods of tremendous shock.

And, if nothing else, the second Dudley op-ed confirms that Dudley was in indeed in “shock” when he wrote his first Bloomberg column. And just in case there was any doubt, we leave readers with Dudley’s conclusion, one in which the former NY Fed president says that while there may be a “deep state” or a conspiracy, he is part of neither:

The article is mine and mine alone. Fed officials were not involved in any way. There is no “deep state” or conspiracy that I am part of. Fed officials are not using me as a vehicle to signal their unhappiness with the president’s attacks on the central bank and on Chairman Powell.

And the absolute punchline: “I wrote the article to express my concern that the president had placed the negative economic consequences of his trade war at the feet of the Fed, and that Fed officials had not pushed back against this more forcibly.” Which is amusing, because after all those often contradictory words, Dudley leaves his readers where they started: asking him how the Fed should “push back more forcibly” against the president,one which the Fed can prevent from getting re-elected – as Dudley himself admitted last week – if it only chooses, but it would never choose to do so as it is so apolitical, it should push to “achieve a better economic outcome” than the one sought by the president.

In short: if Dudley had dug the hole 6 feet deep with his original op-ed, he added a good 6 more feet with the sequel. We can’t wait what “Deep State Dudley” does for part 3…

via ZeroHedge News https://ift.tt/32pmeQD Tyler Durden

It appears that ‘the squad’ isn’t doing so well these days. Between Rep. Alexandria Ocasio-Cortez’s (D-NY) chief-of-staff suddenly quitting while under federal investigation for potential financial crimes, to Rep. Tlaib’s (D-MI) recent temper tantrum over her Israel’s visit – the latest progressive ‘firebrand’ to shit the bed is none other than freshman Rep. Ilhan Omar (D-MN).

Omar’s soap opera has been popcorn-worthy to say the least.

After allegedly committing perjury, immigration fraud, marriage fraud, state and federal tax fraud, and federal student loan fraud – and potentially marrying her own brother, it gets better.

The 37-year-old Minnesota Congresswoman’s husband, Ahmed Hirsi, wants a divorce following reports that Ilhan had an affair with DC political consultant, Tim Mynett – whom she paid $230,000 through her campaign since 2018 for fundraising consulting, digital communications, internet advertising and travel expenses.

Dr. Beth Mynett says in divorce filings that her cheating spouse admitted to the affair in April, and that he had even made a “shocking declaration of love” for the congresswoman before leaving his wife.

Tim and Beth Mynett

Talk about family separation!

The Minnesota congresswoman and her husband allegedly separated in March, and Omar asked Hirsi to divorce her around that time because she didn’t want to file the papers — but Hirsi refused, telling her if she wanted a divorce she should do it herself, said the source, who has known both parties for 20 years.

The husband allegedly changed his mind after Tim Mynett’s wife last week filed bombshell divorce papers claiming her spouse was having an affair with the Somali-born US representative — with Hirsi said to be angry he had been made to look the fool by the allegations of an extramarital affair. –New York Post

“I’m surprised he hasn’t filed already,” a source told The Post, adding that Hirsi was “very confused” after the cheating came to light.

Omar denied that she was dating Mynett in an August 27 interview with CBS affiliate WCCO. So either Mynett’s wife is lying – and decided to blow up her marriage by fabricating a story about her husband’s affair with Omar, or Omar is a total liar.

Omar was spotted enjoying time with Tim Mynett at a California restaurant in March.

Beth Mynett is seeking primary physical custody of her and her husband’s son in part because of Tim Mynett’s “extensive travel” with Omar — which isn’t exactly part of his job description, the document says.

“Defendant’s more recent travel and long work hours now appear to be more related to his affair with Rep. Omar than with his actual work commitments,” the court papers state. –New York Post

Omar’s husband Ahmed Hirsi, meanwhile, “is reportedly bouncing between friends’ houses and stays at the luxury condo when Omar isn’t in town, with the kids also spending time with a grandfather,” per the Post‘s source. Hirsi was apparently upset by Omar’s membership in “the Squad,” which left him with stay-at-home-dad duty for their two children, aged 7 and 16.

via ZeroHedge News https://ift.tt/2zNEzKK Tyler Durden

Proponents of Modern Monetary Theory emphasize that a country that controls its own currency and borrows in its own currency, like the United States, cannot default on its debt. This is because the central bank can, if necessary, “print” the money needed to pay the government’s creditors… – Econofact

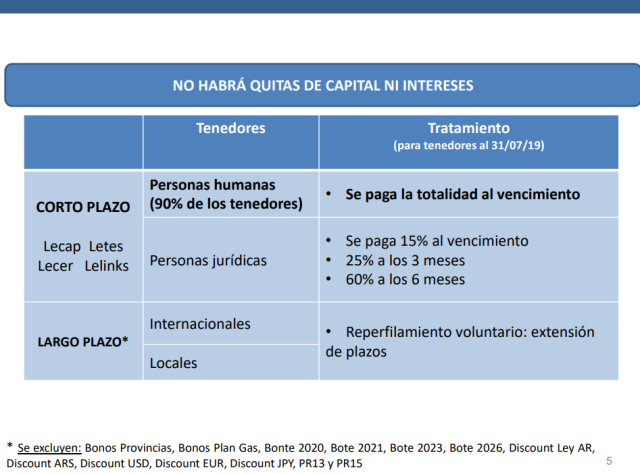

The MMT crowd has some ‘splaining to do after Argentina’s default on local currency Treasury Bills (Lecaps) last week.

We have argued for years with our MMT friends about the dubious assumptions and logic that Modern Monetary Theory is built, most importantly, that a sovereign borrower with an independent central bank and currency, by definition, cannot default. Though the debate has evolved over the years to now what is the true definition of “full monetary sovereignty,” a free floating exchange rate is a big assumption, for example, it would always come down to the case of the 1998 Russian default on ruble Treasury bills known as GKOs. to which the MMT crowd would retort, “special case.” Ironically, the Russians paid their hard currency Eurobonds and defaulted on local currency debt, the complete opposite of what MMT concludes.

Argentina could have monetized the Lecaps last week and let the peso float and collapse as the maturing peso debt would have immediately been converted to dollars. The government chose not to.

We would try to explain to our friends that when a sovereign borrower gets into trouble and experiences “rollover risk” and cannot refinance maturing debt due to a sudden stop of market financing, a policy choice must be made. Either monetize the maturing debt and send the country into hyperinflation as Bulgaria did in late 1996, or default and restructure as Russia did in 1998. We suspect Russia chose the latter because much of their debt was held by foreigners, including hedge funds, such as David Tepper, who said the GKO trade was the worst of his career.

We detect, and we are open to be corrected, from our debates over the years that the MMT crowd believes a reserve currency country, such as the United States, cannot and will never experience rollover risk. We wholeheartedly disagree.

If interest rates significantly increase in the highly indebted DM countries, such as the U.S and even Japan, but especially DMs dependent on foreign financing, public sector finances could enter a doom loop leading them down the road to potential rollover risk.

We saw how the markets fell apart in Q4 when long-term interest rates broke higher in the U.S. to even just above 3 1/4 percent in late September. That is not a very robust debt profile, folks, signaling, at least to us, the interest rate complex cannot normalize because debt is too high. The Fed had to ride to the rescue even as the effective Fed Funds rate was barely positive.

Furthermore, at the end of the day, as the only Joe other than the Yankee Clipper sums it best when it comes to fiat currencies,

As some point, any fiat currency, yes, even reserve currencies, can reach a tipping point into monetary inflation if confidence in its ability to maintain purchasing power is lost and money demand collapses. Even the previous levels of “appropriate” or “normal” levels of money supply then become almost meaningless.

Negative Yielding Debt

Enter the bizarro world of negative yielding debt we now find ourselves, driven by a QE induced structural shortage of long-dated risk-free fixed income instruments, trend following, negative convexity chasing algos with no context that negative rates are a no-no, and traders front running a new round of expected new QE, wrapped in a narrative of a coming deflationary collapse. More market nonsense, in our opinion, but we have trade the hand the market has dealt us. Even if the end game could be a disaster, in our opinion.

Long-term credit risk-free bonds, originally intended to be held to maturity, have been transformed by negative yields into radioactive short-term hot potato trading vehicles that decay your portfolio and P&L the longer they are held. Unless the ECB and BoJ are there to take out the traders at these negative yields, there is going to be a big problem. That is always the case when “the greater fool theory” is the main driver of markets.

We have been writing and debating MMT for years and have been consistent in the solid economic assumption there is no free lunch but MMT keeps evolving, as it should,

We still have ongoing debates with our good friends from the modern monetary theory (MMT) about whether a major sovereign government can default if they have an independent central bank. Yes, they can!

We had the same debate with our Argentine friends several years ago as to whether their government would or could devalue their currency when it was on an effective currency board. Yes, they did! And defaulted to boot.

Just as Russia chose to default on its GKOs (short-term ruble denominated treasury bills) in 1998 with an independent central bank, the same can happen to a G5 country as we approach the upper bound of debt limits and the lower for longer interest rate meme seems to be sunseting in a post-Trump world.

When a highly indebted sovereign crosses the tipping point — and nobody knows where the tipping point is — when the markets lose confidence in its ability to repay or rollover debt coming due and the window shuts on refinancing, they face three choices:

1) bailout – easy for a small country, such as Greece, but Italy or Japan are too big to bail; 2) hyperinflate – print money to pay maturing debt obligations and finance budget deficits. An aside: the Bulgarian central bank did this in 1996 resulting in hyperinflation, which peaked at a monthly inflation rate of 242% in February 1997. I was in the Bulgarian central bank in the fall of 1996, when a senior official looked me in the eye and said, [Gregor], we will not let the government default on its treasury securities.” I knew what was to come; and 3) default and restructure.

Like the Russians, the decision to hyperinflate, default, or go begging to the IMF, is a political one. Russia saw that a high percentage of holders of its local currency debt was held by foreigners, hedge funds such as David Tepper.

Tepper says that losing 29% ($80 million) on Russia when Russia defaulted after an IMF deal “the biggest screw-up in his career”. – Ivanhoff Capital

The Russians made a political choice to default and inflict the pain on foreigners rather their domestic population through hyperinflation. What was interesting is Russia continued to pay their dollar-denominated euro bonds, which had a relatively low debt service burden compared to the maturing GKOs. The Russian government effectively carved out and gave implicit seniority to a specific component of their debt structure. Totally contrary to what MMT predicts will happen, i.e., print money to pay the local debt and default on the hard currency external debt. – GMM, January 2017

So the ball is in your court, MMT friends.

Please explain how Argentina just defaulted on its local currency debt with an independent central bank and currency, which they chose not to float? No special case arguments, no circular logic of defining “monetary sovereignty,” and, yes, it was default and not a “reprofiling” as the government claims,

Just as the law of gravity does not stop at the borders of emerging markets neither should robust economic theories, if they are truly robust. We are more open to kind of a “bounded” MMT under special circumstances and a given timeframe. Universal? NFW.

Upshot?

Deficits do matter.

It is hard to imagine how an MMT advocate would explain away the experience of Argentina. Perhaps the requirement that a country can issue its own currency is, in fact, a requirement that a country can issue debt in its own currency. That would explain why Argentinian outcomes differ from those predicted by MMT. However, it is hard to imagine that a country would be able to issue debt in its own currency for long if it were engaged in deficit spending to the extent MMT advocates propose. In other words, that explanation — while preserving the integrity of the original argument — undermines its practical application.

Alternatively, MMT advocates might fall back on the inflation constraint, which they acknowledge when pressed. If inflation picks up, they say, then countermeasures will be adopted. Again, we have an explanation that undermines the practical application of MMT. But it is even worse than that. Argentina did not adopt countermeasures. In suggesting that countries could just adopt countermeasures when inflation picks up, MMT fails to account for political incentives. Its advocates confuse the possible with the probable.

Argentina’s experience gives us reason to doubt the practical relevance of MMT. In downplaying the costs of deficit spending and monetizing deficits, advocates of MMT enable political actors — even those with the best of intentions — to pursue policies that will ultimately reduce the living standards of the least well off. — AIER, March 2019

Debating these issues are healthy.

As always, we reserve the right to wrong and to be corrected by our MMT friends, who still seem to be developing their theory.

Special thanks to our good friend, Leonardo in Buenos Aires for providing us with the background for this post. Godspeed, our brother, to you and the good people of Argentina, especially the most vulnerable, during these difficult days.

* * *

Appendix

What Should Modern Monetary Theory Learn From Argentina? – AIER

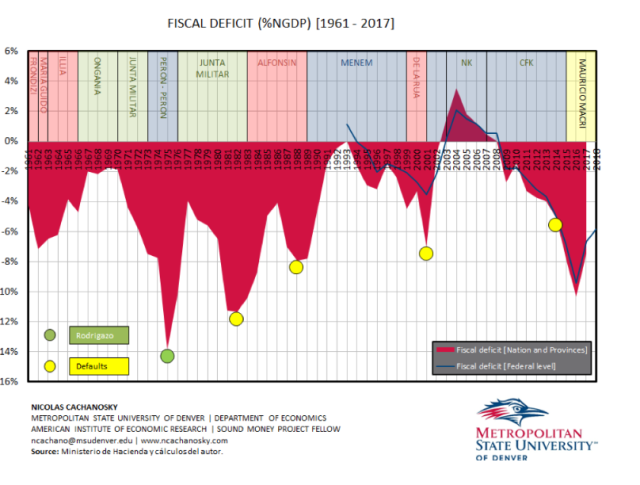

Good background piece on Argentina’s debt and monetary problems

[T]he monetary and fiscal history of Argentina for the period 1960–2017, a time during which the country suffered several balance of payments crises, three periods of hyperinflation, two defaults on government debt, and three banking crises. All told, between 1969 and 1991, after several monetary reforms, thirteen zeros had been removed from its currency. We argue that all these events are the symptom of a recurrent problem: Argentina’s unsuccessful attempts to tame the fiscal deficit. An implication of our analysis is that the future economic evolution of Argentina depends greatly on its ability to develop institutions thatguarantee that the government does not spend more than its genuine tax revenues over reasonable periods of time. – FRB of Minneapolis

Great Twitter thread by Brad Setser

There will be much written on the errors made by Macri (and likely the IMF). But the most obvious one was a simple error of debt management. Borrowing too much in foreign currency early on ….

External bonded debt doubled in a very short period of time.

…Fifteen months later, the giant bailout has become a millstone around Mr Macri’s neck. Voters angry at the continuing recession delivered a stinging rebuke on August 11, handing a big victory to his Peronist rival Alberto Fernández in a primary vote. The contest is regarded as a reliable barometer for the election in October and its result panicked investors because it spelt disaster for Mr Macri’s chances.

Following days of market chaos in the wake of the vote, Mr Macri’s government bowed to the inevitable last week and asked creditors for more time to pay back Argentina’s $101bn of foreign debt, including the IMF money, as Buenos Aires struggled to avoid the country’s ninth sovereign default — and the third this century. Currency controls were imposed on businesses on Sunday after it lost an estimated $3bn in reserves in just two days last week. – FT, Sept 1

via ZeroHedge News https://ift.tt/2Zxt5ud Tyler Durden

{kind=link}

{kind=link}

{kind=link}