What’s the Italian word for ‘hubris’? Somebody should ask League leader Matteo Salvini.

In a report published Friday, Bloomberg examines the circumstances surrounding Salvini’s failed political gambit, which the Interior Minister and Deputy PM had hoped would install him as prime minister of Italy, but instead resulted in his political rivals joining forces to outmaneuver him.

Less than a month ago, Salvini was out partying at Papeete Beach. At one point, he stepped up to the decks during a music festival, where the man who was until very recently the most powerful politician in Italy was surrounded by dancing bikini-clad women.

El viceprimer de Italia, Matteo Salvini, fue invitado a la cabina de DJ en un festival celebrado en la playa de Papeete en la ciudad turística italiana de Milano Marittima, cerca de Rávena. pic.twitter.com/6f90XLSnYW

This was Salvini at the height of his power. But little did he realize that, while he was partying, his rivals were busy plotting his downfall, and within weeks, his hopes of taking over as prime minister would be crushed.

At the time, Salvini had reason to celebrate.

The public didn’t know yet, but he had finally acquiesced to his party’s demands to withdraw his support for the coalition government that had seen his League govern with the Five Star Movement (M5S) for more than a year. Salvini believed that by forcing an election, he could capitalize on his popularity and return with a new conservative coalition that would more readily support his party’s platform of anti-immigrant measures combined with tax cuts that antagonized Brussels. And instead of serving as co-deputy PM, he would be prime minister.

Per BBG, Salvini was keeping his fellow Deputy PM, M5S leader Luigi Di Maio, in the dark about his plans, repeatedly swearing in public that he had no intentions of abandoning the coalition.

Days later, on Aug. 7, Salvini informed Prime Minister Giuseppe Conte, who had been brought on in a compromise between the two parties to rule as a neutral technocrat, that he planned to walk away from the government. Next, he informed Di Maio, who accused him of treachery.

The next day, Salvini told the public. In comments to the press, Salvini asked whether the public would trust him with the “full powers” of the premiership.

But he badly miscalculated. Soon, former PM Matteo Renzi of the Democratic Party exhorted his party to seek a coalition with M5S, despite their well-documented history of antagonism. Democratic Party leader Nicola Zingaretti, who had been against an alliance with Five Star, was soon facing pressure to put his misgivings aside.

Soon, the two parties approached Conte, who had resigned as PM roughly two weeks ago, about potentially returning to his post. He readily agreed. This past week, Italian President Sergio Mattarella gave Conte his blessing to form a new government. Now, all Conte needs is to fill out his cabinet and create a platform (one that’s likely to be centrist and technocratic) and he’s likely to take power officially next week.

But Salvini wasn’t ready to simply walk away. According to BBG, behind closed doors, Salvini made a last-minute offer to Di Maio in an attempt to salvage their alliance. If Di Maio would be willing to return as his coalition partner, Di Maio could have the premiership. But Di Maio turned him down.

Financial markets also gave the new government their blessing, as Italian stocks and bonds rallied on the belief that Conte would be more likely to play nice with Brussels.

To be sure, this isn’t the end of Salvini. He’s still the leader of his party, and senior officials told BBG that they expect him to make a political comeback.

In comments shortly after the formation of the new coalition, Salvini insisted that plotting at the G-7 summit earlier this month had helped cement his overthrow.

The marriage between M5S and the Democrats hasn’t even officially begun, and there are already reports of infighting within the coalition. And Salvini – or “the Captain”, as his admirers have labeled him – has untrammeled power over the League, a formerly regional party that Salvini built into a national powerhouse with approval ratings around 40% (up from 4% when he took over in 2013).

via ZeroHedge News https://ift.tt/30Ok9gB Tyler Durden

“Do Americans Need Air-Conditioning?” a New York Times piece asked in July. Air conditioning, it argued, is bad for the environment and makes us less human. It ran quotes suggesting that, “first world discomfort is a learned behavior”, and urging “a certain degree of self-imposed suffering”.

If environmentalists ruled the world, air conditioning wouldn’t exist. And there’s a place like that.

90% of American households have air conditioning. As do 86% of South Koreans, 82% of Australians, 60% of Chinese, 16% of Brazilians and Mexicans, 9% of Indonesians and less than 5% of Europeans.

A higher percentage of Indian households have air conditioning than their former British colonial rulers.

Temperatures in Paris hit 108.6 degrees. Desperate Frenchmen dived into the fountains of the City of Lights with their clothes on. Parisian authorities announced that they were deploying heat wave management plan orange, level three, which meant setting up foggers in public parks and distributing heat wave kits. The kits consist of leaflets telling people to go to libraries which have air conditioning.

France24, the country’s state-owned television network, advised people suffering from temperatures rising as high as 110 degrees to take cold showers and stick their feet in saucepans of cold water.

A 2003 heat wave killed 15,000 people in France. And, in response, the authorities have deployed Chalex, a database of vulnerable people who will get a call offering them cooling advice.

The advice consists of taking cold showers and sticking their feet in saucepans of cold water.

Desperate Frenchmen trying to get into any body of water they can have led to a 30% rise in drownings. The dozens of people dead are casualties of the environmentalist hatred of air conditioners.

Only 5% of French households have air conditioning. Even in response to the crisis, the authorities are only deploying temporary air conditioning to kindergartens.

The 2003 heat wave killed 7,000 people in Germany. And, today, only 3% of German households have air conditioning. Germany’s Ministry of the Environment refused to back air conditioning as a response to global warming.

Temperatures in Dusseldorf hit 105 degrees. Officials in Dusseldorf had recently rejected proposals to install air conditioning systems because they’re bad for the environment.

The climate action head at Germany’s Institute for Applied Ecology explained that air conditioning wouldn’t work because there’s not much wind during heat waves, and the country can’t end reliance on coal and run air conditioners at the same time. You can have air conditioners or save the planet.

But not both.

The issue isn’t poverty. in Greece, one of the poorest countries in Europe, 99% of households have air conditioning. What it comes down to is a willingness to choose comfort over environmental dogma.

In Europe, people are dying because they’ve been told that their sacrifices will save the planet.

The 2003 heat wave killed 70,000 people in Europe. That’s more than Islamic terrorists have.

When environmentalists claim that global warming is a greater threat than Islamic terrorism, they’re half-right. Global warming isn’t real, but the measures taken to fight it are killing thousands of people.

And it doesn’t have to be this way.

In 2007, only 2% of Indian households had air conditioning. Those numbers have more than doubled. India is expected to field a billion air conditioning units by 2050.

“I am not rich,” an Indian laundryman earning $225 a month, who had just put in air conditioning, told a disapproving Agence France-Presse, but we all aspire to a comfortable life.”

Some of us do.

The 2003 heat wave killed 2,000 Brits. The current heat wave has led to London being placed on a Level 3 health watch. But air conditioning in the UK still hovers at 3% of households. And every summer, the local media lectures Brits on the evils of air conditioning.

Every heat wave is treated as a compelling argument for reducing power to save the planet. The heat and its accompanying misery are treated as heralds of a global warming apocalypse. Soon, we are told, it’ll be hot all the time, the waters will rise, the icebergs will melt, and life will perish from the earth.

When a heat wave consumed Europe in 1540, leading to the hottest temperatures on record and the deaths of thousands, the people blamed a higher power. In England, where the River Trent dried up, the megadrought was blamed on Henry VIII’s sacrilegious crackdown on monasteries. Modern Europeans have a simple, rational explanation. Mother Earth is angry because we’re using air conditioners.

Or other people are.

China has 569 million installed air conditioners. More than any other country in the world. South Korea has 59 million air conditioners. That’s more than France, Germany and the UK combined.

Europe’s sacrifice is not only senseless, it’s also meaningless.

Vietnam has become a booming market for air conditioners. 17% of Vietnamese households now have one. Indonesia is leading its own boom in air conditioning. As is much of Asia and the Middle East.

Europe can go on letting its people die for the environment, but it won’t make any difference.

Air conditioning isn’t some American fetish, as European elitists sneer. It’s a worldwide movement. Every country that can manage it is getting air conditioners. Meanwhile people are dying in France.

While the rest of the world is cooling off, Europe is in thrall to a pagan pseudoscientific cult.

Its tenets insist that the planet is a living entity, but fail to understand its true implications. The climate is part of a living entity which changes on a timescale that challenges human understanding. For a thousand years of recorded history, Europe has undergone alternate warming and cooling periods. The Medieval Climate Anomaly was an example of how complicated those cyclical changes could be.

A heat wave isn’t proof that we’ve sinned against Mother Earth by heating and cooling our homes. It’s a reminder that the environment operates on an inescapable scale that is vaster than human beings.

We can cut down forests and build dams. But so can beavers. We cannot change the climate.

The bones of hippos have been found under Trafalgar Square. The Chauvet Cave in France includes pictures of rhinos. The Little Ice Age killed off England’s vineyards in the 14th century. The Thames began to freeze over in the 17th century. The Viking colonization of America collapsed under the wave of cold.

Air conditioning and heating are not how we change the climate. They’re how we cope with it.

Environmentalism has so hopelessly tangled human civilization and the environment that we are no longer able to understand the planet on its own terms, instead of as a luddite eschatology in which the climate is a deity punishing us for our civilizational ingenuity with hot weather and natural disasters.

And that makes it extremely difficult to adapt to the changes in a healthy way.

A century ago, Americans beat the heat by wading in fountains, sleeping on roofs and fire escapes, and escaping the city. Air conditioning has made it possible for us to live and work across the entire country.

In 1896, a heat wave killed thousands of Americans. New York City authorities resorted to the same measures as their modern Parisian counterparts, turning on fire hydrants and handing out ice.

Those temperatures amounted to a mere 90 degrees.

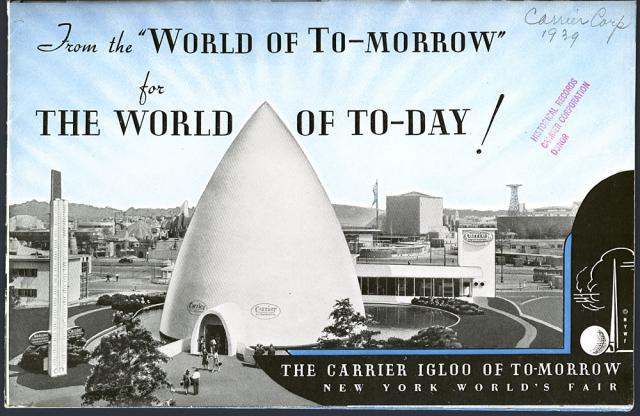

In 1902, Willis Carrier invented the air conditioner in Brooklyn. He imagined a world in which, “The average businessman will rise, pleasantly refreshed, having slept in an air-conditioned room. He will travel in an air-conditioned train, and toil in an air-conditioned office.” We live in that world now.

At the New York World’s Fair, while temperatures outside hit 90 degrees, Carrier debuted an Igloo display. Two giant thermometers contrasted “Nature’s temperature” with “air conditioning”.

It sold itself.

Air conditioning allows New Yorkers to shrug off 90-degree weather and go on living and working.

Today, New York is the home of the Green New Deal which believes in following Europe’s trends. If New York adopts Europe’s environmentalism, it will discover what living in 1896 really felt like.

Environmentalists have killed thousands of Europeans. They can kill thousands of Americans too.

via ZeroHedge News https://ift.tt/34goiMv Tyler Durden

Last week was full of portentous events. Only somebody who has not been awake for the last few years will fail to realize how these at first sight unconnected events are part of the same matrix. There was the ever louder talk in mainstream media about an approaching global recession, inverted yield curves and the negative yields, which tell us that the Western financial system is basically in coma and kept alive only by generous IV injections of central bank liquidity. By now it has dawned on people that the central bankers acting as central planners in a command economy and printing money (aka quantitative easing) to fuel asset bubbles are about to wipe off the last vestiges of what used to be a market economy.

Then we saw Trump taking new twitter swipes at China in his on-and-off “great trade deal” and the stock markets moving like a roller coaster in reaction to each new twitter salvo. Also, we had both Trump and Macron sweet talking about getting Russia back and again renaming their club G8. Last Tuesday at a G7 presser in Biarritz, the Rothschild groomed Macron took it one step further opening up about the reasons why they all of a sudden longed for friendship with Russia: “We are living the end of Western hegemony.” In the same series, Britain’s new government under Boris Johnson was telling his colleagues in Biarritz that he is now decisively going for a no-deal Brexit, after which he went back to London and staged a coup d’état by suspending parliament to ensure no elected opposition interfered with it.

Perhaps the weirdest news to crown it all, came from Jackson Hole, Wyoming, where the Western central bankers were holed up for their annual retreat. The president of Bank of England Mark Carney shocked everybody (at least those not present) by announcing that the US dollar was past its best-before and should be replaced with something the central bankers have up their sleeves.

The New World Order is in its death throes

What these events have in common is that they amount to an admission that the globalist New World Order project in its present form is dead, or at least in its death throes. It has bumped its head against an impenetrable Sino-Russian wall of resistance. The heated totalitarian propaganda against Russia since 2001 (when the NWO realized that Putin wasn’t their man); regime change and color revolutions in neighboring countries; attempts at Maidan style coups in Moscow; and finally the sanctions since 2014 were key to the Anglo-Zionist empires strategy. They needed to take over either China or Russia to gain absolute world hegemony. Taking over either one, they would have checkmated the remaining one, and after that the entire world. They rightly deemed Russia as the weaker piece and went all out in that direction. The NWO wanted to take advantage of Russia’s weakness in form of its Western minded comprador class and a shell-shocked liberal intelligentsia (dominating media, culture and business, just like in Hong Kong, BTW), which is constitutional uncapable of thinking with their own brains to liberate themselves from Soviet era stereotypes (“Soviet Union/Russia bad, West good”).

They then figured that economic and cultural sanctions (e.g. Olympic ban) coupled with doubling down on the propaganda would break the country. Luckily, the Russian narod, the common people saw through it all and would not play along with the enemy. At the same time, Russia paraded its resurrected military in Crimea and Syria as well as its formidable new hypersonic doomsday weapons. The military option to take over Russia was not in the cards any longer.

Russian economy from strength to strength

Believing their own propaganda, they had got that totally wrong. Endlessly repeating their own self-serving talking points they must have truly fancied that Russia’s economy amounted to nothing else than export of fossil fuels, that “Russia’s economy is the size of Holland’s,” that “Russia does not produce anything,” and that Russia was “nothing but a gas station with nukes” (somehow managing to ignore the significance of the nukes part). I seriously believe, that the propaganda had become so complete that the Western leaders and the intelligence people actually had come to adapt their own propaganda as the truth. What is for sure, is that all Western media, including what should be the most respected business journals and all those think tanks, had not published one honest appraisal of the Russian economy in 15 years. Every single piece I read over the years had clearly been written with the aim to denigrate Russia’s achievements and economic development. Nowhere to be found were reports on how Putin by 2013 had totally overhauled the economy transforming Russia into the most self-sufficient diversified major country in the world with all the capabilities of the foremost industrial powers. In fact, I tend to think that even the US presidents from Bush to Obama were fed in their intelligence briefings cooked up fake reports about the Russian economy and the whole nation. Actually, I would go one step further. I bet that the CIA itself in the end believed the propaganda it had given birth to. (It has been said that at some point the genuine Russia analysts had all been dismissed or demoted and replaced with a team specializing in anti-Russian propaganda).

But actually all the data was there in plain view. I myself took the trouble to compile a report on the real conditions of Russia’s economy fresh at the onset of the 2014 crisis. In the report, I set out to show that Russia indeed had modernized and diversified its economy; that it had a vibrant manufacturing industry in addition to its energy and minerals sector; and that its budget revenues and economy at large were not at all as dependent on oil and gas as it was claimed. Among other things, we pointed out that Russia’s industrial production had by then grown more than 50% (between 2000 and 2013) while having undergone a total modernization at the same time. In the same period, production of food had surged by 100% and exports had skyrocketed by almost 400%, outdoing all major Western countries. Even the growth of exports of other than oil and gas products had been 250%.

“The crisis-torn economy battered by years of robber capitalism and anarchy of the 1990’s, which Putin inherited in 2000, has now reached sufficient maturity to justify a belief that Russia can make the industrial breakthrough that the President has announced.”

Events have borne out this insight. And it is therefore that Russia won the sanctions battle.

The report represented an appeal to the Western leaders to give up on their vain hope of destroying Russia through their sanctions and risking nuclear war at it. Russia was invincible even in this respect. For that purpose I expressly added this missive in the introduction to the report:

“We strongly believe that everyone benefits from knowing the true state of Russia’s economy, its real track record over the past decade, and its true potential. Having knowledge of the actual state of affairs is equally useful for the friends and foes of Russia, for investors, for the Russian population – and indeed for its government, which has not been very vocal in telling about the real progress. I think there is a great need for accurate data on Russia, especially among the leaders of its geopolitical foes. Correct data will help investors to make a profit. And correct data will help political leaders to maintain peace. Knowing that Russia is not the economic basket case that it is portrayed to be would help to stave off the foes from the collision course with Russia they have embarked on.”

A follow-up report of June 2017 covering the sanctions years 2014 – 2016, showed how Russia went from strength to strength never mind the Western attempts at isolation. This report stressed that Russia’s economy had now become the most diversified in the world making Russia the most self-sufficient country on this earth.

In this report we exposed the single biggest error of the propaganda driven Russia analysis. This was the ridiculous belief that Russia supposedly was totally dependent on oil and gas just because those commodities made up the bulk of the country’s exports. Confusing exports with the total economy, they had foolishly confused the share of oil and gas in total exports – which was and remains at the level of 60% – with the share of these commodities of the total economy. In 2013 the share of oil and gas of Russia’s GDP was 12% (today 10%). Had the “experts” cared to take a closer look they would have realized that on the other side of the equation Russia’s imports were by far the lowest (as a share of GDP) of all major countries. The difference here is that while Russia does not export a great deal of manufactured goods, it produces by far a bigger share of those for the domestic market than any other country in the whole world. Taking the 60% of exports to stand for the whole economy was how the “Russia produces nothing” meme was created.

Finally in a November 2018 report, I could declare that Russia had won hands down the sanctions war having emerged from it as a quadruple superpower: industrial superpower, agricultural superpower, military superpower and geopolitical superpower.

Macron et co. realizes that Russia actually is a superpower

These facts have now finally dawned on certain key stakeholders of the globalist regime can be discerned from the fact that they have tasked their handpicked puppet president Macron to make up with Russia. Trump has got the same assignment, which is evident from the siren calls of the two leaders in Putin’s address. Both want to invite Putin to their future G7-8 get-togethers.

As it was said, Macron went as far as unilaterally capitulating and declaring the decline of the West. He went on to spell out that the reason for this spectacular geopolitical about-face was the rise of the Beijing – Moscow (de facto) alliance that has caused a terminal shift on the world scene. Curiously, he also openly blamed the errors of the United States for the dire state of affairs pointing out that “not just the current administration” were to be blamed. No doubt, the foremost of these errors, Macron had in mind, was the alienation of Russia and pushing the country into the warm embrace of China. It is quite clear, that this is what they want to remedy, snatch the bear back from the dragon. Fortunately, that won’t happen. Good if there will be rapprochement and good if the West will try, but after all what Russia has learnt by now it will not sell out on China under any circumstances. I think Putin and the Russian powers that be have clearly opted for a multipolar world order. That is definitely not what Macron’s and Trump’s employers have in mind but let them try.

Until Trump took office, the strategy of the US regime had been to pursue only Russia in its geopolitical ambitions, but by then it had dawned on them that Russia was invincible especially in the de facto alliance with China. In a sign of desperation, the empire then opened big time another front with China. Essentially going from bad to worse.

The world order is being shaken like never before

“The world order is being shaken like never before…”, that’s another quote from Macron. Obviously, it refers to the military and geopolitical strengths of the Sino-Russian alliance, but certainly also to the economic shifts as the West has lost – and will keep losing – its economic domination. This brings us back to Mark Carney of Bank of England and his unprecedented attack on the US dollar arguing that it was time to end its global reserve currency status. As one option Carney brought up that the major Western central banks would instead issue a digital cryptocurrency. That is to say, a NWO currency controlled by the central banks. That would effectively mean the replacement of the Federal Reserve cartel with a cartel of the Western central banks (the Fed obviously being a part of it). That’s yet one step further north from any kind of democratic control and a giant step towards world government.

What could possibly have prompted such a radical US hegemony puncturing idea to be put forward? One reason obviously is that the Western economies really are in that extreme critical condition that more and more analysts caution about. (We shall look at the economic facts further down). There’s a very real possibility that we will be hit by a doomsday recession. What’s sure is that Carney’s bizarre speech could possibly not have occurred in a normal economic environment (any more than Macron’s admission that the Western hegemony is done with). According to Zerohedge, The Financial Times, the party organ of the globalist elite, admitted as much in its report on the Jackson Hole meeting. The central bankers “acknowledged they had reached a turning point in the way they viewed the global system. They cannot rely on the tools they used before the financial crisis to shape the economic environment, and the US can no longer be considered a predictable actor in economic or trade policy — even though there is no imminent replacement for the US dollar in sight.”

There was an effective admission that the central bankers had run out of tricks to pull the economies out of the everything-bubble mess, not to mention the looming doomsday recession. According to FT, Carney went as far as flashing the war card saying: “past instances of very low rates have tended to coincide with high risk events such as wars, financial crises, and breaks in the monetary regime.” On the one hand this can be seen as an admission on how deeply tormented they are about the financial situation and what could happen when it comes crashing down. On the other hand, it can be seen as a sales pitch, “only we can fix it, trust us, give us a carte blanche.” Or more probably, both.

Note from above Carney saying: “the US can no longer be considered a predictable actor in economic or trade policy.” Bank of England President here directly attacking President Trump.

And just a couple of days later William Dudley an ex-president of New York Federal Reserve Bank (the most influential of the 12 federal reserve banks that comprise the Federal Reserve System) followed up on a direct attack on Trump. But as they say about spies, there are no ex-spies, and I would think the same applies for the global financial elite. And yes indeed, Dudley is a card carrying member of the Council of Foreign Relations. Dudley had penned an op-ed for Bloomberg titled “The Fed Shouldn’t Enable Donald Trump,” where he openly lobbies for the Fed to deliberately damage the economy in order to neutralize the policies (namely trade wars) of the sitting president and prevent his reelection chances by willfully ruining the economy.

One thing is for sure, the elite is desperate and in serious disarray. Very probable that the elite is split, too. It seems as if there were two globalist factions competing with each other and wanting to follow vastly different strategies. One faction supports Trump and the other is against him. Possibly, one that wants to do things with force and another that wants to gain by stealth. That could be Pentagon and the military-industrial complex vs. the financial elite, who also owns the media. My argument does not hinge on the veracity of those division lines, but that some rupture exists among the elites must be taken for granted, otherwise Trump would have been ousted by now with all that pressure on him.

To summarize this introduction.

The Western world is in turmoil: the previous overwhelming geopolitical domination is gone and over with; military solutions against the main adversaries – China and Russia – are off the books; hybrid wars against them have failed; China and Russia are economically stronger than ever, too strong for the adversary; and to boot the domestic Western economies are in extraordinary bad shape, risking a depression of epic proportions.

* * *

Further down in this report, I will look at the one aspect of the question I am best equipped to handle, namely the economy. I will outline just in how bad shape the Western debt-fueled casino economies are. Having that as the background, I will then show how surprisingly strong the Russian economy is, at least in comparison with the Western gambling nations. Most importantly, Russia is virtually debtless, and that’s really the clue to survival in this extraordinary economic environment. In addition to the solid finances, Russia has other things going for it, too, as we will see below. I will not provide comparative data on China. One reason for that is, that China is not an economic risk. China does not have the debt problem that it is frequently touted in Western press to have. China, as the world’s number one export country, would of course take a hit in a serious global crisis, but that would not kill the economy. Although, China is the biggest exporter, there has been a shift from export-led growth towards domestic investment and consumption. The share of exports of goods and services in the country’s GDP was by 2018 down to 19.5%, half of the 2006 peak of 36%. On the contrary, the Chinese economy would stay vivid and therefore also help to sustain Russia’s exports.

I may add as one more piece of background, that it is my firm belief that the approaching economic disaster has long been evident to the central bankers and the globalist elite decision makers. Most likely the game plan was to establish the absolute world hegemony – which they not long ago thought was within early reach – and then after that deal with the debts as they saw fit as democratic dissent would not matter a bit anymore by then. That’s why they felt confident in building up the asset bubbles to carry them over to the final solution. Reminds me about a story told about Moscow’s so-called Khrushchyovka tenement buildings. These are low-cost three- to five-storied houses built quickly and cheap during the Khrushchev era to address the dire housing shortages of the 1960s. According to the story, the planners knew they would serve only for a few decades, but that would not matter all that much because by that time there would be Communism and everything would be perfect anyway. No Communism materialized, but presently the Moscow government under Mayor Sobyanin has initiated a program to tear them all down and erect new buildings where flats with title will be given for free to house the 1.5 million present residents of those buildings slated for replacement. – Well, that’s sort of Communism, isn’t it? – This kind of wishful thinking must have kept the globalist elite going, too. Unfortunately for the dreamers, though, their plans hit a snag in form of Russia and China.

Central bank fueled asset bubbles

Russia is low in debt, but you can’t say the same about the US and other Western nations. And that debt really is what got the world in the present mess and brought it teetering on the brink of financial collapse. Since the late 80s, the US central bank, the Federal Reserve under Alan Greenspan developed an addiction to cure any downward tick on Wall Street with easy credit, eventually requiring after every downturn ever bigger central bank liquidity injections to keep the stock indices on a growth curve. Greenspan was experimenting with a policy aimed at creating a “wealth effect” aka “trickle-down.” The idea being that Wall Street bankers and big corporations be stuffed with all the free money they can swallow for the purpose of keeping stock and bond prices high. The theoretical frame told that doing so something would eventually trickle down to the real economy, and everybody would live happily ever after. After stocks and bonds, Greenspan’s wealth effect policy was addressed to inflate home prices and all real estate with that. That was the road that eventually led to the 2008 subprime loan crisis, which took down Lehman Brothers and then all of Wall Street and the whole global economy.

But Wall Street recovered soon, because Greenspan’s successor Ben Bernanke had set forth to blow up an even bigger asset bubble. And the Europeans followed suit. The Fed fueled the market frenzy with creating money out of thin air (aka quantitative easing) in favor of governments, banks and corporations to the tune of $3.5 trillion in the decade following the 2008 collapse.

The European Central Bank has done the same for Europe in volumes more than 2.5 trillion euro to date. All the other Western central banks joined the gambling by flooding the markets with fiat money at same levels relatively speaking.

But anyway this astronomic leverage and the humongous budget deficits of the Western countries didn’t get the real economy anywhere. They have blown up asset bubbles of phantasmagorical proportions with preciously little trickle-down. Since the pre-crash peak in October 2007, the broadest US stock index (Wilshire 5000) has gained 95% (on top of covering the nearly 60% crash from in between). In the same 12-year period industrial production (manufacturing, mining, energy, utilities) has grown only 5% combined over all those years. Deduct – the in itself lossmaking – shale oil and gas and there is barely no growth left in the 12 years. In fact, the US manufacturing sector was in June still 1.6% below the pre-crisis peak in December 2007. So we have a 5% gain in the most important part of the real economy vs. 95% in stock market gambling. The absurdity of the stock market growth is further evidenced by the gap between growth of real final sales and stock valuations since 2007 peak. Since then, the former has grown on an average 1.6% per year, while the stock market has delivered annualized growth at levels of 15%. Total industrial production share of the GDP in the US has sunk to 18%. (For comparison, the figure for Russia was 32% and growing.)

Trickle-down, anyone?

It would be false to claim there has not been any trickle-down at all. Millions of people have kept their jobs because of it. But at the same time they have had their real wages squeezed and the overwhelming majority have seen their standards of living drop. Only massive loads of consumer credits and ultra-cheap mortgages have kept up an illusion of superficial prosperity among the middle classes. This debt-fueled prosperity and it’s cursory result, the artificial real estate asset bubble will prove a wolf in sheep’s clothing when the everything-bubble bursts.

There’s been another form of trickle-down, too, a much more real and actually beneficial one. By creating the debt-fueled illusion of prosperity, the Western central banks have actually subsidized China, Russia and all of the emerging world as they have flushed their export goods on the global markets where the Western nations have picked it all up on borrowed money. Thanks for that, though. At the same time, that has driven production costs up in the West with the consequence that their own industries have been priced out.

The humongous borrowings fail to produce GDP growth

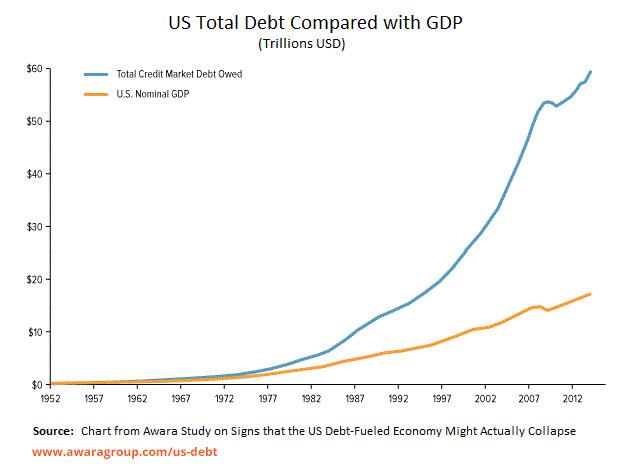

Every year since the last bout of the crisis in 2008, growth of debt in the national economies of each Western country has far exceeded the growth of economic output measured as GDP. Below chart shows just how bad it has been in the US.

The debt and GDP growth curves started to diverge in the late 70s, but from 2000 debt has spiraled out of control delivering preciously little incremental GDP. Deduct the wasteful debt and wasteful spending and there would be no growth whatsoever.

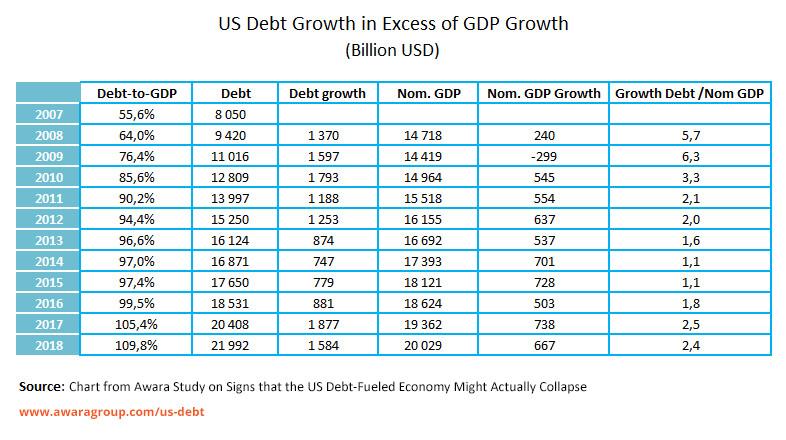

Not only has there been no real GDP growth but even the nominal growth has to a crucial extent been provided for by means of the enormous government borrowings. We see from below table that that in each year from 2008 to 2017 even the nominal GDP growth has been less than the growth of government debt, with 2015 and 2015 as the only exceptions when they were on par.

In the peak crisis years 2008 and 2009, debt growth was a staggering 5.7 and 6.3 times that of GDP growth.

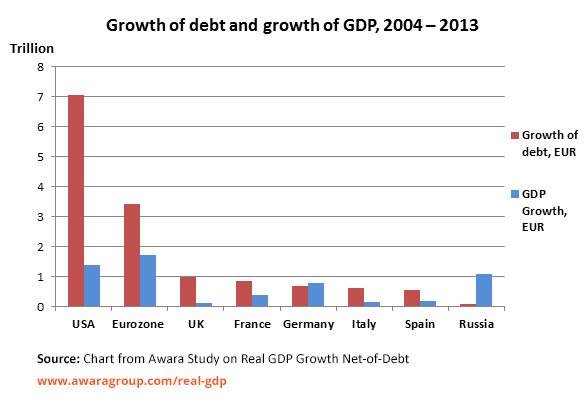

The debt game has been equally miserable all over the West, perhaps with the only exception of Germany, who has wisely refrained from participating, even when egged on by liberal economists calling Germany’s more prudent policy unfair to the gambling nations. Below chart shows how much more the Western governments have borrowed than produced economic growth. The chart covers years 2004 to 2013, but the trend has been the same ever since. GDP growth has been vastly less than the growth of the colossal debtberg.

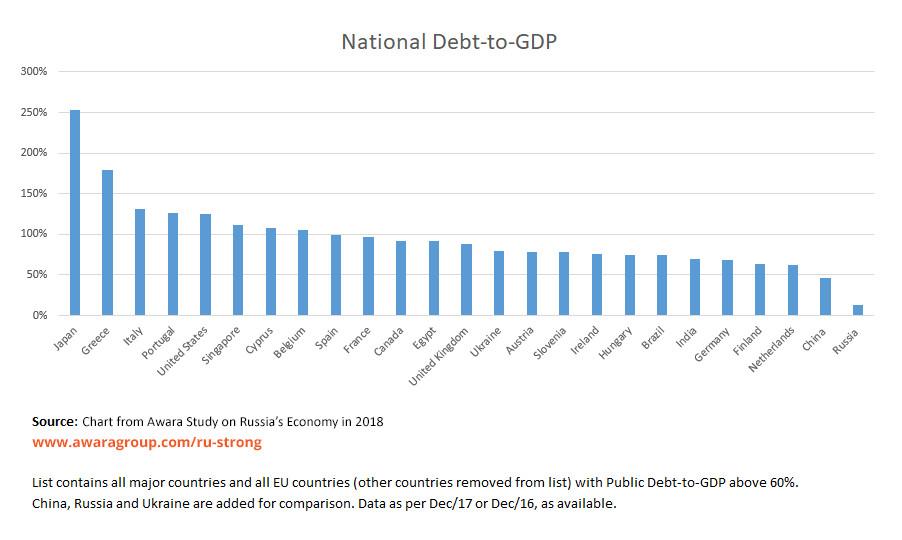

Note Russia there as the shining exception.

Below chart ranks countries according to their debt burden relative to GDP. And again you see how debtless Russia is compared with the squandering nations.

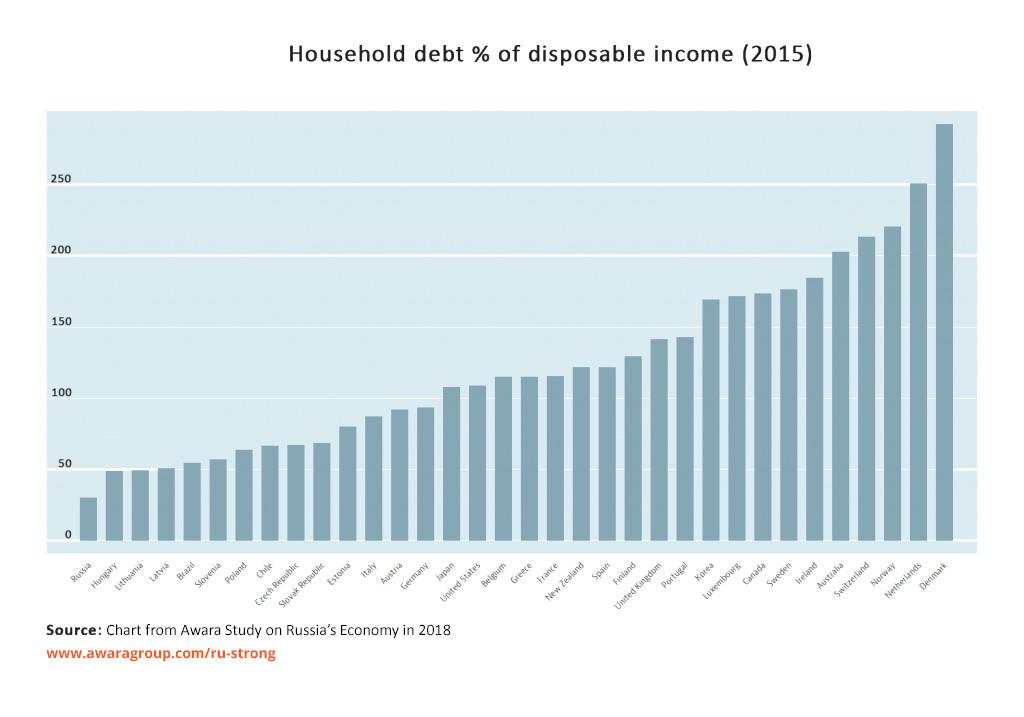

These charts concerned only government debt, when we add private debt to it, the picture is doubly worse. From the point of view of a national economy it really doesn’t matter in which form the excess debt expands, public or private. In fact, on an average in the West the situation with household debt is equally dire. Below chart tells you just how bad. And again note Russia as the one shining exception.

And it’s no better with corporations, which have throughout the last decade been enjoying mindboggling levels of central bank largesse in form of virtually unlimited interest-free financing. For example, compared to earnings, US bond issuers are about 50% more leveraged now than in 2007.

First no real interest, then on to negative yields

One of the many deadly side effects of the central bankers’ practice on gambling with the national economies is that they first eliminated real interest rates (pushed rates below inflation) and then doubled down on the destruction of sound economic principles by cooking up a system with negative yielding bonds (bonds which yield below zero). By now $30 trillion of the $60 trillion US bond market yield below inflation (no real interest) and nearly $17 trillion worth of bonds are in negative yield territory. That’s mostly made up by sovereign debt of Japan and European governments (12 at the moment) but recently the mass of negative yielding corporate bonds has also doubled to $1.2 trillion. Half of the $5 trillion worth of European government bonds sport a negative yield as well as 20% of European investment grade corporate bonds.

Secondly, the asset price bubbles in real estate and financial markets in fact represent inflation, it’s just not officially recorded as such. As it is only the 10% (and increasingly, the 1%) who get the money, they spend it on the stuff that counts for them, stocks and real estate. Keeping their loot offshore also helps to dampen inflation at home. The squeeze on the middle classes and stagnating wages, is sadly an important factor in keeping inflation down. Ordinary people just can’t afford to buy.

One should also note, that resulting from the illusionary debt-fueled prosperity and its effect on keeping the local Western currencies artificially high, there has actually been an inflation in wages and production costs, but only in relative terms in comparison with the emerging world. This in turn has led to further offshoring of manufacturing jobs.

A crucial factor, which in the crazy money printing environment has kept consumer goods from hyperinflating has been imports from the emerging Asia and especially China. Huge growth of the Chinese manufacturing industry coupled with massive influx of cheap labor from the rural countryside into the cities enabled China for a couple of decades to constantly increase its exports to the US and Europe and these countries to keep prices down. (Including by domestic industries having to lower prices in competition). With the Trump trade wars and dramatically increasing protectionism, this will change. And it could get very ugly.

Finally, there is an important consideration that few if anyone seem to understand. That is the fact that the US and other Western countries have been able to print the stupendous amounts of money while keeping rates down and without the currency values crashing only because they enjoy local currency monopolies in their respective territories. The USD has of course been enjoying a global monopoly, but that is fast fading. All the other factors mentioned above (and several other ones), have enabled to prop up and prolong these currency monopolies, but there is a limit to everything. In the coming recession, I would expect some of the lesser currencies to lose their monopoly trust and that would shatter the position of the bigger currencies USD and Euro and force them to raise interest rates. I have earlier written more in detail about this in a report titled How the Dollar and Euro Monopolies Destroyed the Real Market Economy. https://www.awaragroup.com/blog/dollar-euro-monopolies-destroyed-market-economy/

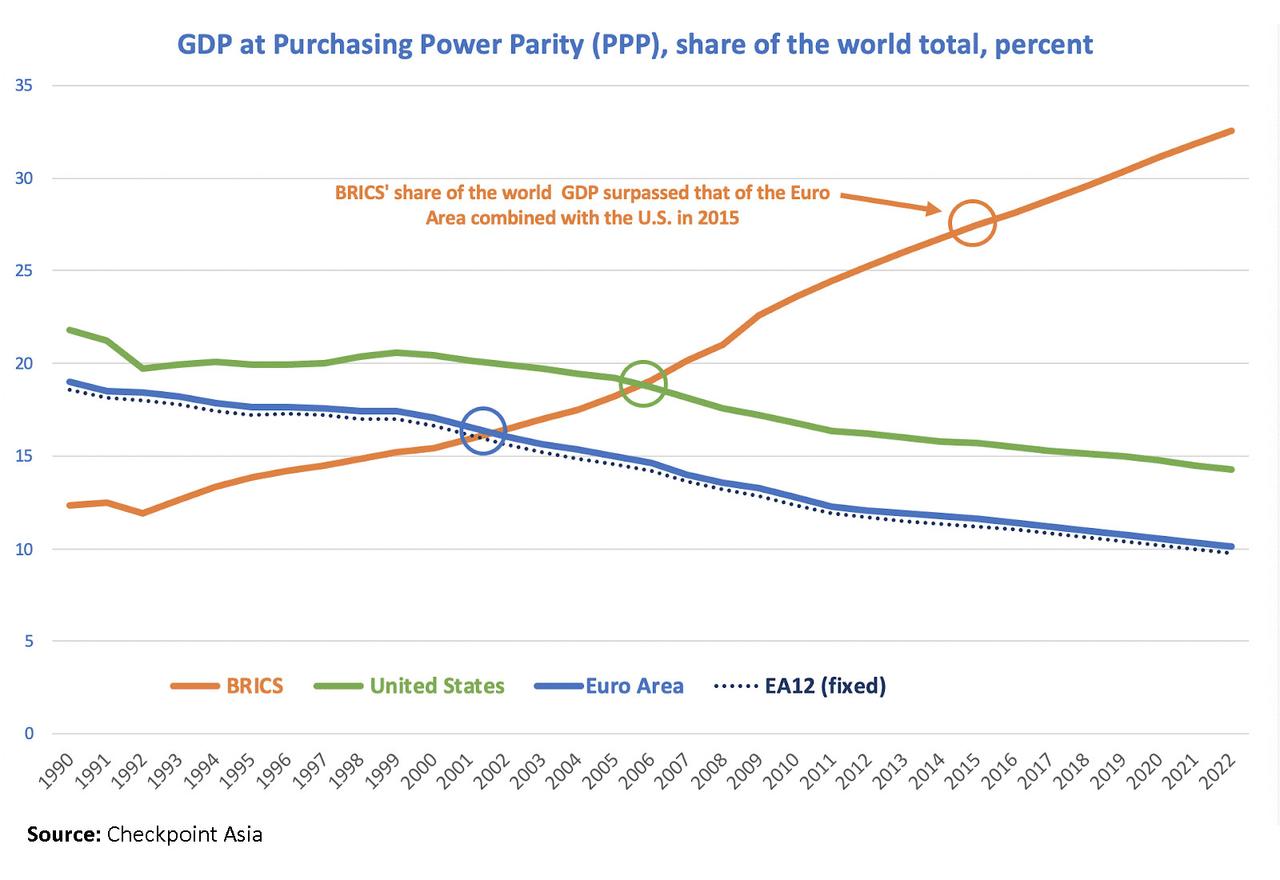

The below chart suggests that the Western countries are already on the way to lose their respective currency monopolies. The BRICS countries (Brazil, Russia, India, China, South Africa) now have a combined GDP (measured in PPP, which is the only correct way to measure the relative size of national economies) larger than not only the G7 countries, but the US and Eurozone economies combined.

At its foundation in 1973, the G7 countries had a combined GDP PPP of 50% of the world economy, by today it is down to 30%. In the same time the nominal GDP share of world economy has crashed from 80% to 40%. The currency monopolies came with the economic superiority, it is therefore only natural that with the economic domination goes the currency domination, too. If we haven’t reached the tipping point yet, then that will happen within 5 to 10 years.

In summary, everything else unchanged, the risk of inflation picking up with just a few percentage points could have the entire Western financial systems coming crashing down due to the pressure on interest rates growing. The Fed and the ECB are continuously speaking about their inflation targets and how they want to pump the markets with more liquidity to raise inflation. There could yet be a big surprise in store for them. Interest rates as such could also be the primary trigger (even without inflation first rising), as nations would have to protect their currencies and attract financing for their colossal debtbergs.

Must add as a P.S. that the incipient flight to gold might well be one of the trigger events for those currencies to lose their monopolies. (Gold price is up 20% since May).

Deleveraging will come

These massive borrowings have delivered nothing of tangible value. Now, when the party is nearly over all there is left are the debt bubbles that have hit the roof. The real values of all the assets below bear no relation to the money that went into inflating the balloons. What’s left is economic hardship for 80% of the people, a crumbling infrastructure and simmering social tensions.

The debt saturation point has been reached, therefore this time it will be different, the central bankers have lost their magic wand and won’t be able to renew the debt binge and extend it with one more decade. Instead, there will be a day of reckoning. Governments and corporations will have to put their act together and let the market weed out the failed entities. Those who cannot carry the debt, will have to shed it. There will be bloodbath with defaults, bankruptcies and massive unemployment. – Perhaps a revolution here and there. – There will be no choice, deleveraging must happen.

Now, whether this system will come crashing down or just slowly die as it trundles downhill will not matter all that much. It will eventually die either way. Most people would prefer the slow motion option, but only with the crash would a cure come. Whatever, it has become increasingly difficult to stave off the crash and this time around, the financial markets would take the real economy down with them big time.

The impressive figures on Russia

The question then is, who would be left standing? Naturally, those who are less leveraged. Now, scroll back to have a new look at the above charts on government and household debt. Find the position of Russia there? That’s right. Russia is the country with – by far – the least debt, both public and private. Having after 2014 following sanctions been cut off from the Western debt orgy, even Russian corporations are shielded against a possible Western debt apocalypse.

In a global recession, no country is safe, but Russia looks to have quite a lot going for it in terms of economic advantages. Russia’s national balance sheet is next to none with by far the lowest debt of all major countries. All economic actors, the government, corporations and households are economically solid and minimally leveraged. Not only is the government virtually debtless, but it has again replenished its spectacular forex and sovereign wealth fund reserves. On top of that comes a hefty budget surplus. – Yes, you heard that right, surplus. In a time when all Western countries are in a chronic fight against deficits, you rarely even hear the term budget surplus. And more, Russia runs the world’s third biggest trade surplus. Add to that the current account surplus, and there’s the hat trick in form of your classic triple surpluses. Russia has a lot more going for it, too, as we will see.

Let’s look at Russia’s present financial health report.

Thanks to import substitution (domestic production instead of imports to neutralize sanctions) Russia’s industrial production rose 2.6% year-on-year in June. (USA +1.1%, UK +0.8%, Japan -2.4%, Germany -5.9%). Above, we mentioned that US industrial production was up with as little as a cumulative 5% since 2008 to date. In the same period Russia’s industry grew 18% notwithstanding the hardships of sanctions and sharp drop in oil price. In fact, since 2014 when the sanctions were first imposed, Russia’s industry has grown 12%.

Russia’s merchandise trade surplus for the first half of 2019 was $93 billion, ranking third in the world after China and Germany and before South Korea. Imports were down by 3%, the other side of the coin of growing domestic manufacturing. Even when exports also were slightly down, lower imports will keep the surplus on track to reach levels near $200 billion for the full year, just under last year’s record $212 billion.

Q1 current account surplus clocked in at $33 billion, up 10% over the year.

In this connection, it might be helpful to remind that Russia’s economy is nowhere near as dependent on fossil fuel extraction as it is habitually believed in the West. In fact, oil and gas only account for 10% of Russia’s GDP according to World Bank statistics. (In 2017, total natural resources share of GDP was 10.7%, but that includes minerals and forest, too).

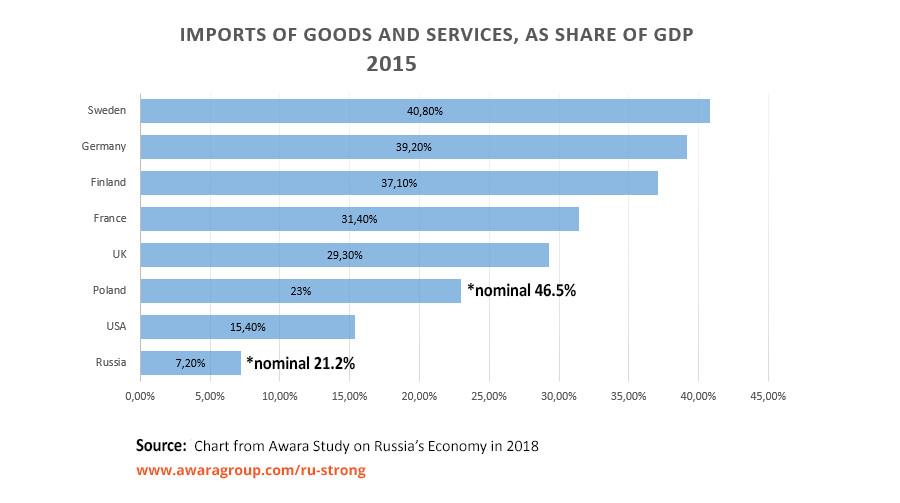

We also need to point out that Russia has an enormous strength by way of being the world’s most self-sufficient major country. Russia has the by far lowest level of imports relative to GDP of all countries, as evidenced by below table. It shows that Russia’s imports as a share of GDP was as low as 7.2%, while the corresponding level for Western European countries was between 30 to 40%. The extraordinary low levels of imports in a global comparison obviously signifies that Russia produces domestically a much higher share of all that it consumes (and invests), this in turn means that the economy is superbly diversified contrary to the claims of most so-called Russia experts.

Despite initial scares, inflation has remained low even when the VAT rate was from the new year raised from 18% to 20%. The rolling 12-month inflation runs at 4.6% but with the declining trend the full year inflation is expected to hit the central bank’s target 4%.

The job market continues strong with record low unemployment levels, while the job participation rate has not deteriorated (so no tricks here). The July reading of 4.6% translates to 3.4 million unemployed, which is low for a country with a population of 146 million. The strength of the labor market was underscored by an increase of real salaries by 3.5% by July. This while disposable income otherwise has remained subdued.

Whereas the US is combating persistent budget deficits (latest reading, a deficit of 4.5% of GDP) – likewise the EU countries – Russia mustered a huge budget surplus equal to 3.4% of the GDP by July this year.

Russia’s foreign exchange and gold reserves have also done a spectacular comeback reaching $520 billion.

The Russia sovereign wealth fund surged in July to reach a value equal to 7.2% of GDP.

Despite the wholesome macroeconomic environment and impressive figures, Russia’s GDP growth has been less than 1% so far this year (year-on-year 0.6% in Q1 and 0.9% in Q2). However, by the looks of it the fundamental economy seems to be growing and modernizing, while the drag on the growth comes from depressed household consumption. What’s more important, though, is that while Russia’s growth is hovering around the 1%, so is that of all of the Western world. (Accuse me of whataboutism if you will, but these things need to be put in perspective). Q2 growth in the Eurozone was 1.1%, with Germany even about to slide into recession. UK clocked in at 1.2% and Japan at 0.4%. (All figures, year-on-year). The US showed only 2% (revised down 28 August) even when fueled by a mountainous budget deficit set to reach $1 trillion for the fiscal year and despite all that easy money the Fed keeps pumping out. Only China remained firmly in growth territory with 6.2%.

But, the real conundrum is, how can Russia produce the same GDP as all the Western countries with their seemingly limitless injections of give-away money? How is it possible that all those trillions and trillions that the Western central bankers have thrown on the economy do not produce any real incremental economic output?

The big disadvantage Russia has compared with the Western countries is the exorbitant real interest rate that the central bank maintains. The steering rate is presently 7.25%, with inflation predicted to be 4%, that translates into a primary real interest of 3.25%. Compare that with the negative real interest – and even negative yields – of competitor countries. As, the Russian central bank has failed to create a real banking sector which would lend according to international standards to the country’s businesses, the ones that are lucky to get a loan at all would look to pay interest at the level of 15% of more (save the largest corporations). The Governor of the Russian Central Bank Elvira Nabiullina does not see this as a problem, though. She has said that instead she would pin her hopes on improving the countries investment climate (sic!). (She calls for improvement of corporate governance, development of human capital, and all kinds of nice things. That would sure do it.)

Just this week, Putin called a high profile meeting with Nabiullina, the minister for economic development Maxim Oreshkin, and the finance minister Anton Sulanov, to express his deep concern with the sluggish GDP growth and stagnating income. No doubt, that the depressed income is not only a drag on the economy but on the president’s popularity. There is only one quick fix for it. The government and the CBR must ditch their overzealous austerity programs. It’s good that Russia is not over leveraged with debt, but certainly some debt would be in order to finance the infrastructure and other national strategic development programs instead of ripping it off people’s backs. Free the funds for raising pensions and public service salaries instead. And most importantly, Nabiullina must lower the rates and not run real interests in excess of 3% when the rest of the developed world is in negative territory. There is no other quick remedy for raising people’s income. That’s Putin’s choice. Hope somebody tells that to him.

In conclusion, we are not saying that Russia would not be hurt by the coming recession, we merely express our confidence that Russia is among the world’s countries best placed to cope with it.

via ZeroHedge News https://ift.tt/2zEWNxY Tyler Durden

Walmart is unleashing their creepy robots throughout 350 stores this year – most of which will roam the aisles and look for items that are either out of stock or out of place, after which a human will be alerted to remedy the issue, according to Fast Company.

Another robot, the ‘Auto-C’ self-driving floor scrubber, will navigate the store to as it laughs in binary at the human job it just took.

“What we think is very valuable to us is we have a life-sized laboratory where hopefully millions of people will be seeing our robot,” said Sarjourn Skaff – CTO and cofounder of Bossa Nova, which makes the company’s new shelf scanners. “It’s a very valuable lab for researchers to experiment with human-robot interaction concepts. The scale allows you to get to the truth faster.”

The rest of the article details how Skaff and team experimented with various ideas in order to make robot-human interactions more smooth – such as trying out ‘turn signals’ and brake lights. They found that trying to replicate traffic signals and other road-related customs were a total dud.

“We expected the turn signals to just work,” said Skaff. “It was a big surprise that actually the answer is no. People had a hard time transcribing an experience from the road to one that’s indoors.”

However, it was an apt comparison to make in another way. The last time that humans had to readjust to having machines in their space was when the automobile infiltrated the roads at the turn of the century. And back when cars were first coexisting with humans, their designers hadn’t yet found a common interaction language. There were no turn signals or even brake lights. It’s a remarkable echo of what’s happening now with robots being introduced in public spaces.

Dan Albert, a car historian and author of the new book Are We There Yet?, points out that well into the 1950s, people still put their hands out the window to signal which direction they planned to turn. Other cars were equipped with a little flag called a “trafficator” that popped out from the side of the vehicle to indicate left or right. Brake lights weren’t always what we’re familiar with today, either; even the use of red, yellow, and green in traffic lights wasn’t a foregone conclusion. “All those things are very random,” Albert says. “Every engineer thinks, I’ll do it this way.”

Eventually, Bossa Nova settled on a ‘rotating ring of light’ – which Skaff says the company is still testing as an indication of direction.

via ZeroHedge News https://ift.tt/32k8V44 Tyler Durden

Civil liberties are in greater danger today from the intolerant hard-left than from the bigoted hard-right. This may seem counterintuitive: There has been far more violence — mass shootings in malls, synagogues and other soft targets — from extremists who identify more with the hard-right than with the hard-left. But the influence of the hard-left on our future leaders is far more pervasive, insidious and dangerous than the influence of the hard-right.

People on the “woke” hard-left seem so self-righteous about their monopoly over Truth (with a capital T) that many of them see no reason to allow dissenting, politically incorrect, views to be expressed. Such incorrect views, they claim, make them feel “unsafe.” They can feel safe only if views they share are allowed to be expressed. Feeling unsafe is the new trigger word for demanding censorship.

A “woke” rally in Washington. We must always remember that it is not only the road to hell that is paved with good intentions. It is also the road to tyranny. Photo: Wikipedia.

No university student has the right to be safe from uncomfortable ideas, only from physical threats, and any student who claims to be in physical fear of politically incorrect ideas does not belong at a university. The most extreme example of this distortion of the role of higher education took place at my own university when a distinguished dean of a Harvard residential college was fired from his deanship because some “woke” students claimed to feel unsafe in his presence because he was representing, as a defense lawyer, a man accused of rape.

We often forget that the concept of “political correctness” originated in the Stalinist Soviet Union, where Truth — political, artistic, religious — was determined by the central committee of the Communist Party and any deviation was regarded as unacceptable. To be sure, there is a vast difference between how Stalin treated political incorrectness and how the “woke” generation treats it. Stalin murdered those who deviated from his Truth, while “wokers” generally shun and discredit, though there has been occasional violence from elements of the hard-left toward those who deviate from their Truth. But both produce a similar result: less dissent, less reliance on the marketplace of ideas and more self-censorship.

For many “wokers,” freedom of speech is nothing more than a weapon of the privileged used to subjugate the unprivileged. It a bourgeois concept that emanates from an anachronistic white, male constitution that is irrelevant to the contemporary world. Free speech for me — the underprivileged — but not for thee — the privileged. That is what the “wokers” want. Affirmative action for speech!

The other dangerous similarity between the Stalinists and the “wokers” is that both disdain due process for those they deem guilty of political incorrectness or other crimes and sins. They reject any presumption of innocence or requirement that the accuser bear the burden of proof. These bourgeois concepts are based on the recognition of human fallibility and uncertainty. For Stalinist and “wokers,” there is no uncertainty or fallibility. If they believe someone is guilty, he must be. Why do we need a cumbersome process for determining guilt? The identities of the accuser and accused are enough. Privileged white men are guilty perpetrators. Intersectional minorities are innocent victims. Who needs to know more? Any process, regardless of its fairness, favors the privileged over the unprivileged.

When I was in college in the 1950s, it was the McCarthyite right that was censoring and denying due process. It was the liberal left that was defending free speech, dissent and due process. But for some on the left, this stance was self-serving, because it was people on the extreme left who were being denied these protections. Now that it is conservatives who are being censored and denied due process on campuses around the country, many on the left have remained silent. Civil liberties for me, but not for thee.

That is why I make the controversial claim that today the “woke” hard-left is more dangerous to civil liberties than the right. To be sure there are hard right extremists who would use — and have used — violence to silence those with whom they disagree. They are indeed dangerous. But they have far less influence on our future leaders than their counterparts on the hard-left. They are not teaching our college age children and grandchildren. They are marginalized academically, politically and in the media. The opposite is true of hard-left Stalinists. Many have no idea who Stalin even was, but they are emulating his disdain for free speech and due process in the interests of achieving the unrealizable utopia they both sought. They also have in common the attitude that noble ends justify ignoble means.

It is precisely because the ends sought by the “wokers” are often noble — racial and gender equality, a fairer distribution of wealth, protection of the environment, a women’s right to choose, gay marriage — that liberals find it harder to condemn them for their intolerance toward civil liberties. But we must always remember that it is not only the road to hell that is paved with good intentions. It is also the road to tyranny.

via ZeroHedge News https://ift.tt/30Ng1O9 Tyler Durden

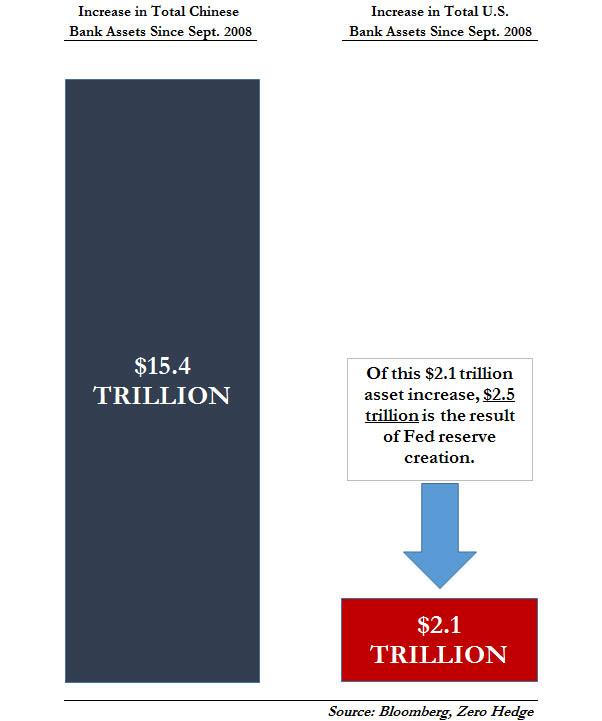

Back in the days of the Fed’s QE, much of thinking analyst world (the non-thinking segment would merely accept everything that the Fed did without question, after all their livelihood depended on it), was focused on how massive, and shocking, the Fed’s direct intervention in capital markets had become. And while that was certainly true, what we showed back in November 2013 in “Chart Of The Day: How China’s Stunning $15 Trillion In New Liquidity Blew Bernanke’s QE Out Of The Water” is that whereas the Fed had injected some $2.5 trillion in liquidity in the US banking system, China had blown the US central bank out of the water, with no less than $15 trillion in increases to Chinese bank assets, all at the behest of a juggernaut of new credit creation – be it new yuan loans, shadow debt, corporate bonds, or any other form of debt that makes up China’s broad Total Social Financing aggregate.

Now, almost six years later, others are starting to figure out what we meant, and in an Op-Ed in the FT, Arthur Budaghyan, chief EM strategist at BCA Research writes about this all important topic of China’s “helicopter” money – which far more than the Fed, ECB and BOJ – has kept the world from sliding into a depression, and yet is blowing the world’s biggest asset bubble.

Budaghyan picks up where we left off, and notes that over the past decade, Chinese banks have been on a credit and money creation binge, and have created RMB144Tn ($21Tn) of new money since 2009, more than twice the amount of money supply created in the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28 TRILLION. Why does this matter? Because Chine money’s supply is the size of broad money supply in the US and the eurozone put together, yet China’s nominal GDP is only two-thirds that of the US.

This, as the BCA analyst explains, is a major problem.

Below we repost his latest FT Op-Ed, which explains why – as we said in the 2019 year ahead post – we remain confident that the spark for the next global financial crisis will be in China.

* * *

China’s ‘helicopter money’ is blowing up a bubble, authored by Arthur Budaghyan is chief emerging market strategist at BCA Research, and first published in the FT.

The escalation of the trade conflict between the US and China has raised the likelihood of greater stimulus by Beijing to prop up the economy. While China’s excessive debt isn’t news, investors must wake up to the reality of “helicopter money” — enormous money creation by Chinese banks “out of thin air”.

While this sugar rush may provide short and medium-term cover for investors, the long-term effects will exacerbate China’s credit bubble. China, like any nation, faces constraints on frequent and large stimulus, and its vast and still rapidly expanding money supply will produce growing devaluation pressures on the renminbi.

When a bubble emerges we are often told that this bubble is different. Many economists justify China’s credit and money bubble and continuing stimulus by pointing to the nation’s high savings rate. But this narrative is false. At its root is the idea that banks are channelling or intermediating deposits into loans. This is not how banks operate.

When a bank expands its balance sheet, it simultaneously creates an asset (say, a loan) and a liability (a deposit, or money supply). No one needs to save for this loan and money to be originated. The bank does not transfer someone else’s deposits to the borrower; it creates a new deposit when it lends.

In all economies, neither the amount of deposits nor the money supply hinge on national or household savings. When households and companies save, they do not alter the money supply.

Banks also create deposits/money out of thin air when they buy securities from non-banks. As banks in China buy more than 80 per cent of government bonds, fiscal stimulus also leads to substantial money creation. In short, when banks engage in too much credit origination — as they have done in China — they generate a money bubble.

Over the past 10 years, Chinese banks have been on a credit and money creation binge. They have created Rmb144tn ($21tn) of new money since 2009, more than twice the amount of money supply created in the US, the eurozone and Japan combined over the same period. In total, China’s money supply stands at Rmb192tn, equivalent to $28tn. It equals the size of broad money supply in the US and the eurozone put together, yet China’s nominal GDP is only two-thirds that of the US.

In a market-based economy constraints are in place, such as the scrutiny of bank shareholders and regulators, which prevent this sort of excess. In a socialist system, such constraints do not exist. Apparently, the Chinese banking system still operates in the latter.

There are clear downsides. Helicopter money discourages innovation and breeds capital misallocation, which reduces productivity growth. Slowing productivity and strong money growth ultimately lead to rising inflation — the dynamics inherent to socialist systems.

Air show in Tianjin, China shows off China’s helicopters. Getty Images.

In the long run, more stimulus in China will entail more money creation and will heighten devaluation pressures on the renminbi. As we all know, when the supply of something surges, its price typically drops. In this case, the drop will take the form of currency devaluation.

As it stands, China’s money bubble is like a sword of Damocles over the nation’s exchange rate. Chinese households and businesses have become reluctant to hold this ballooning amount of local currency. Continuous helicopter money will increase their desire to diversify their renminbi deposits into foreign currencies and assets. Yet, there is no sufficient supply of foreign currency to accommodate this conversion. China’s current account surplus has almost vanished.

As to the central bank’s foreign exchange reserves, at $3tn they are less than a ninth of the amount of renminbi deposits and cash in circulation. It is inconceivable that China can open its capital account in the foreseeable future.

If China chooses the path of unrelenting stimulus, investors should recognise the long-term negative outlook for the renminbi. Continuous stimulus will beef up investment returns in local currency terms, but currency depreciation will substantially erode returns in US dollars or euros in the long run.

The investment implications go beyond Chinese markets. Market volatility over the past few months as the talk of stimulus picked up has given us a peek into the future. As the renminbi has depreciated by 12 per cent since early 2018, the pain has reverberated across Asian and other emerging markets. The MSCI Asia and MSCI EM equities indices have each fallen 24 per cent in dollar terms since their peak in January 2018. Long-term pressures could play out even more dramatically.

Fortunately, Chinese authorities recognise these issues. Yet they face an immense task of stabilising growth while containing credit and money expansion. This will be hard to achieve in an economy that has become addicted to credit creation.

via ZeroHedge News https://ift.tt/32figtC Tyler Durden

The Democratic Presidential candidates who have been the most backed by billionaires have not been doing well in the polling thus far, and this fact greatly disturbs the billionaires. They know that the Democratic nominee will be chosen in the final round of primaries, and they have always wanted Pete Buttigieg to be in that final round. Therefore, they have backed him more than any of the other candidates. But what worries them now is that his opponent in that round might turn out to be Bernie Sanders, whom they all consider to be their nemesis.

They want to avoid this outcome, at all costs. And they might have found a way to do it: Elizabeth Warren. Here is how, and why:

Among the top three in the polling — Joe Biden, Bernie Sanders, and Elizabeth Warren — only Biden is among the top five in the number of billionaires who have backed him, and each of the other four candidates scores higher than Biden does in the number of billionaire backers. Furthermore, Biden is sinking in the polls. Consequently, Democratic Party billionaires are increasingly worrying that their Party might end up nominating for the Presidency someone whom they won’t support. That person would be Sanders. And the Democratic National Committee — which relies heavily upon its billionaire backers in order to be able to win elections (just as the Republican National Committee relies upon Republican billionaire backers in order to win) — is terrified by this possibility (alienating its Party’s crucial moneybags).

The saving grace for these billionaires (and for the DNC) increasingly seems likely to be Senator Warren’s candidacy, which draws support away from Sanders, and therefore gives Buttigieg a chance ultimately to win the nomination.

As of August 30th, the most-comprehensive website reporting on the latest polling information and trendlines concerning the Democratic Party presidential primary contests, https://projects.economist.com/democratic-primaries-2020/, reports that more registered Democrats are considering whether to vote for Warren (50%) than for any of the other candidates, including #2 Biden (48%), and #3 Sanders (38%). The percentages shown there as currently intending to vote for each one of those are 27% Biden, 18% Warren, and 16% Sanders. Buttigieg is currently only at 5% who are intending. The “intending” trendlines are downward for all of the candidates except Warren, whose trendline is steadily upward ever since May and is trending to surpass Biden at around the time when the primaries actually start in February 2020. So: right now, Warren clearly seems to be the likeliest winner of the Democratic Party’s nomination. The likeliest possibility to block that would be for Sanders to reduce his loss of progressive voters to Warren, and for Warren to start trending downward while Sanders trends upward; so, that’s what the billionaires would want to prevent from happening.

On August 27th, the top website for Democratic Party activists, Political Wire, headlined “Warren Overtakes Biden as Most Favorable Candidate”, and reported that not only does Warren now edge out both Biden and Sanders in net favorability rating, and top the entire field of candidates in that extremely important measure, but Warren is overwhelmingly the most frequently mentioned second choice of Democratic Party primary voters, which means that not only would the voters who intend to vote for her in the primary be delighted if she were to become the Democratic nominee — this outcome would also likeliest produce the most-unified Party going into the general election. This, in turn, would mean that Democratic Party billionaires, instead of Republican Party billionaires, would almost certainly control the country after 2020 — the country would be controlled by people such as Thomas Steyer and Donald Sussman, instead of by people such as Sheldon Adelson and Paul Singer. It would be a different ‘democracy’, but not really much different; it would be like the difference between George W. Bush and Barack Obama — it would be different in rhetoric and bumper-stickers, but very similar in actual policies. (For examples: whereas Bush invaded and destroyed Afghanistan and Iraq, Obama invaded and destroyed Libya and Syria; and, all the while, both of them supported the Sauds and Israel; and, moreover, both of them supported Wall Street, though Obama tongue-lashed them, which Bush didn’t.) So: though the rhetoric is sometimes different, the basic policies aren’t. The policies of Republican billionaires and of Democratic billionaires are basically similar.

As of just a few weeks ago, the Democratic Party’s five top U.S. Presidential candidates, in terms of whom had been backed the most strongly by America’s billionaires, were, in order from the top: Pete Buttigieg, Cory Booker, Kamala Harris, Michael Bennett, and Joe Biden. Warren was 12th down from Buttigieg’s #1 position, in support from the billionaires. Sanders was at the very bottom — zero billionaires backing him (he was the only one of the 17 reporting candidates who had no billionaire backer).

The Democratic Party’s billionaires are just crazy about Buttigieg, but the question right now is whom will they choose to be running against him during the decisive final round of the primaries? Would they rather it be Sanders? Or instead Warren?

They definitely prefer Warren. Her recent soaring poll-numbers are raising her support, from them, so strongly that the neoconservative-neoliberal (i.e., pro-billionaire) David Bradley’s The Atlantic magazine headlined on August 26th, “Elizabeth Warren Manages to Woo the Democratic Establishment”. This magazine reported (to use my language, not theirs) that the rats from the sinking ship Joe Biden have begun to jump onboard the U.S.S. Elizabeth Warren’s rising ship, which might already be tied even-steven with the other two leading ships, of Biden and of Sanders. Since Sanders is the only American Presidential candidate whom no billionaire supports, there are strong indications that Warren is drawing some of them away from Biden. This could turn the nominating contest into, ultimately, Buttigieg versus Warren (both of whom are acceptable to billionaires), instead of into Buttigieg versus Sanders (which would pose the threat to them of producing a Sanders Presidency). There is little reason to think that Buttigieg will decline to the #2 position in billionaires’ support; but, if this contest turns into Sanders v. Buttigieg, instead of into Warren v. Buttigieg, then Democratic Party billionaires not only would pour even more money into Buttigieg’s campaign against Sanders, but they would likely end up donating to the Republican Presidential nominee in 2020 if Sanders ends up beating Buttigieg (as polls indicate he almost certainly would). By contrast, if this nominating contest ends up being between Warren v. Buttigieg, then the Party’s billionaires wouldn’t likely switch to supporting the Republican Presidential nominee — they’d continue donating to the Democratic Party, regardless of which of those two candidates wins the nomination, in order to defeat Trump (or whomever the Republican nominee turns out to be), and take the control of the country away from Republican billionaires (as it now is).

Therefore, David Bradley’s propaganda organs are turned on, really hot, by Lizzie. For some typical examples, at Bradley’s biggest-circulation one, The Atlantic, its recent stories gushing about her have been headlined: “Elizabeth Warren Had Charisma, and Then She Ran for President”, and “Elizabeth Warren’s Big Night”, and “The Activist Left Already Knows Who It Wants for President”. For example: the last-mentioned of those articles was about “Netroots Nation, a conference that’s been around since the early 2000s,” which “is run by the liberal political blog Daily Kos.” Here’s what it hides: Daily Kos was founded and owned by the CIA asset and El Salvadorian aristocrat Markos Moulitsas, a ‘former’ Republican far-right person, who set up his website in 2002 and suddenly specialized in fooling progressive Democrats to endorse whomever the billionaire-run Democratic National Committee wants them to support. Unlike David Bradley’s ‘moderate’-Democrat rags, Moulitsas’s ‘progressive’-Democrat rag, Daily Kos, targets to make suckers of Democrats who might vote in the primaries for people that the billionaires actually fear — and that’s now especially Sanders — in order to turn them instead toward favoring the ‘mainstream’, ‘more electable’, Democratic Party candidates (such as Biden, Buttigieg, and Harris — not David Bradley’s darling as Buttigieg’s stalking horse, Warren). In 2016, that ‘mainstream’ was Hillary Clinton (whom the DNC had rigged the primaries to ‘win’ against Sanders), but more recently it was Joe Biden and Pete Buttigieg; and, now, this ‘mainstream’ is starting to include (from the billionaires’ standpoint) Elizabeth Warren. That’s because Warren is vastly more preferred by billionaires than is Sanders, and so they want the Party’s progressives to choose her, instead of Sanders, so that the final Democratic Presidential contest will be between Warren versus the billionaires’ actual favorite, which is Buttigieg. If they can’t get him, at least they can get her, the Party’s billionaires clearly now are hoping.

“When Leah Daughtry, a former Democratic Party official, addressed a closed-door gathering of about 100 wealthy liberal donors in San Francisco last month, all it took was a review of the 2020 primary rules to throw a scare in them. … “I think I freaked them out,” Ms. Daughtry recalled with a chuckle, an assessment that was confirmed by three other attendees. They are hardly alone. … But stopping Mr. Sanders … could prove difficult for Democrats.

Martin went on to say:

His strength on the left gives him a real prospect of winning the Democratic nomination and could make him competitive for the presidency if his economic justice message resonates in the Midwest as much as Mr. Trump’s appeals to hard-edge nationalism did in 2016. And for many Sanders supporters, the anxieties of establishment Democrats are not a concern.

That prospect is spooking establishment-aligned Democrats. …

David Brock, the liberal organizer [founder of the Media Matters anti-progressive Democratic Party website against Republicans], … said he has had discussions with other operatives about an anti-Sanders campaign and believes it should commence “sooner rather than later.” …

Howard Wolfson [here’s the wiki on him], who spent months immersed in Democratic polling and focus groups on behalf of former Mayor Michael R. Bloomberg of New York, had a blunt message for Sanders skeptics: “People underestimate the possibility of him becoming the nominee at their own peril.” …