The sun shines brightest across the North American continent as we enter summer’s dog days. Cold sweet lemonade is the refreshment of choice at ballparks and swimming holes alike. Many people drink it after cutting the grass, or whenever else a respite from the heat and some thirst quenching satisfaction is needed.

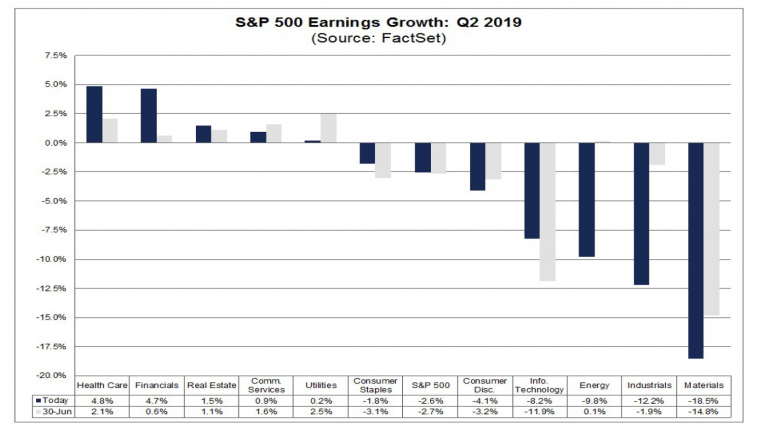

The economy, after 10 years of growth, appears to be heading for a respite too. Second quarter earnings, currently being reported by S&P 500 companies, have been a mixed bag thus far. But in sectors that actually make stuff, like materials and industrials, earnings are suffering double digit declines.

Regardless of whether companies were able to “beat estimates” (which as often happens, were revised lower just before the reporting season started), their actual Q2 results didn’t look very encouraging so far. The manufacturing sector in particular looks a bit frayed around the edges as the saying goes. [PT]

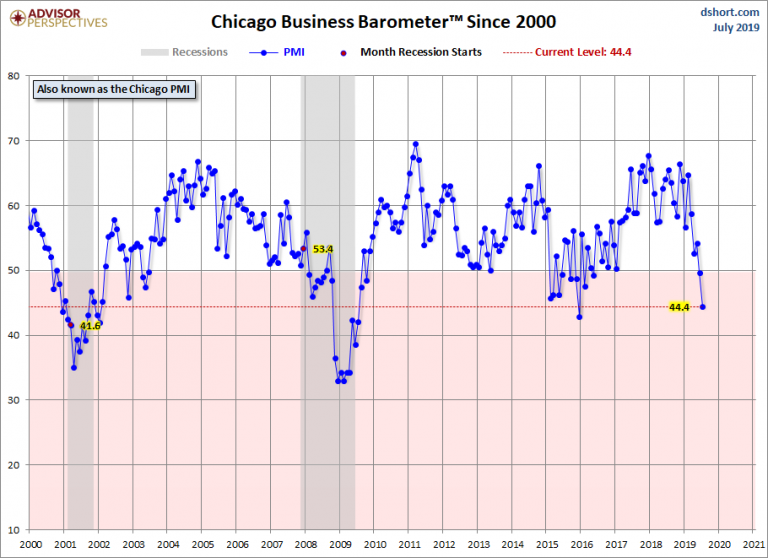

From a practical standpoint, earnings are declining in these sectors because manufacturing is contracting. For example, this week it was reported that the Chicago Purchasing Mangers’ Index (PMI) collapsed in July to 44.4. That is the second weakest Chicago PMI reading since the Great Financial Crisis.

For context, a Chicago PMI reading below 50 indicates a contraction of the manufacturing sector in the Chicago region. So far this year, the Chicago PMI has been down five out of seven months. On top of that, weaker demand and production pushed the employment indicator into contraction for the first time since October 2017.

Chicago PMI – based on this indicator it looks as though the economy either has already entered a recession or is very close to doing so. Occasionally dips in the Chicago PMI do not presage a recession – as for example in late 2015/ early 2016. It remains to be seen if the signal is more meaningful this time, but it definitely constitutes a warning sign. [PT]

Unfortunately, the weakness in manufacturing extends beyond the Chicago region. On Thursday it was reported that the U.S. Manufacturing PMI dropped in July to its lowest level since September 2009. Employment also fell for the first time since June 2013. What is going on?

US manufacturing PMI by Markit and the ISM manufacturing survey. These still indicate expansion, but are on the cusp of moving into contraction territory. Note: in terms of gross output, manufacturing remains the largest sector of the economy. [PT]

Economic Lemons

One place to look for edification is the auto industry. Namely, car dealers are reporting fewer buyers. They are in turn ordering fewer vehicles from manufacturers. The dealers don’t have room for the cars they have. Automakers, parts manufacturers and dealers directly employ more than two million people. As demand for cars declines, the jobs associated with the auto industry also decline.

Having too many cars with too few buyers is something an economist would call a supply glut. Of course, the easiest way to clear excess supply is to reduce prices. This may work up to a point. But if prices must be reduced beyond the cost of labor and materials inputs, there is a problem.

Making lemonade from these economic lemons is generally impossible. Still, that doesn’t mean companies don’t try by taking on greater and greater levels of debt. And the big banks, which are backstopped by the Fed, continue extending credit to keep the sham going.

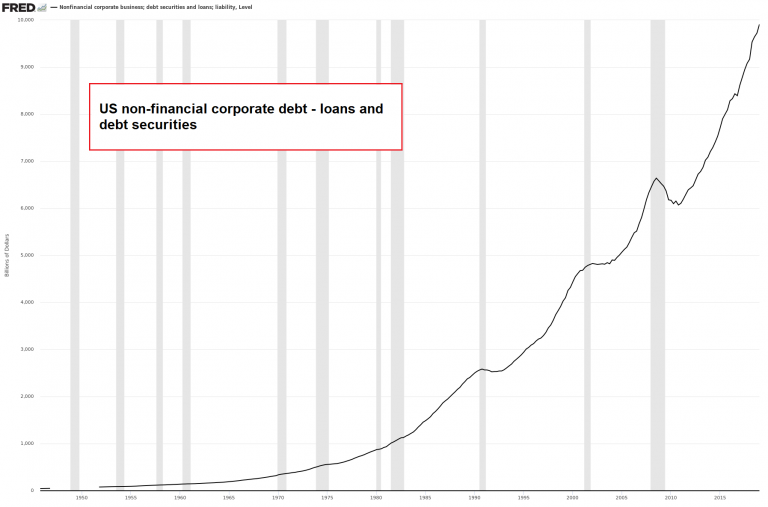

U.S. non-financial corporate debt is about $10 trillion, or roughly 48 percent of gross domestic product (GDP). That is up about 52 percent from its last peak in the third quarter of 2008, when corporate debt was about $6.6 trillion, roughly 44 percent of 2008 GDP. In short, corporate debt is at record levels and is rising much faster than economic output.

US non-financial corporate debt is approaching USD 10 trillion. The corporate sector is not exactly prepared for an economic downturn. [PT]

At this point in the business cycle, corporations have loaded themselves up with so much debt that they are extremely fragile. Should the economy slow ever so slightly, it will be game over for countless over-leveraged companies. Defaults will pile up like old furniture and tires along the dry LA River bed.

Do You Hear a Bell Ringing?

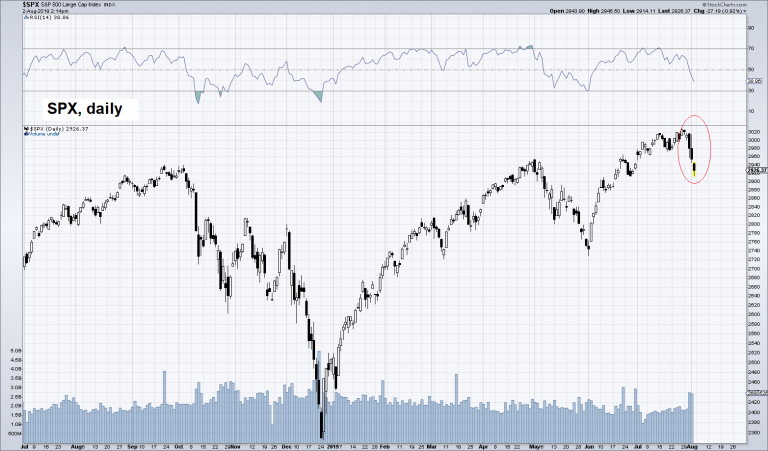

But while Main Street has been cooling off, Wall Street has been running hot. Promises of more cheap credit from the Fed have propelled stocks to record highs. Year-to-date, stocks, as measured by the S&P 500, are up over 17 percent.

On Wednesday, however, some uncertainty was added to the market. At the conclusion of the July Federal Open Market Committee (FOMC) meeting, Fed Chair Powell cut the federal funds rate 25 basis points. But instead of telegraphing that additional rate cuts would follow like Wall Street expected, Powell said it was merely a mid-cycle adjustment. In other words, he’s winging it.

S&P 500 Index, daily: a minor disturbance in the farce. This was the first time since 1987 that the index actually decline on the very day the first rate cut was announced. [PT]

Will the Fed cut rates further this year? Will they hold? These were the questions Wall Street was asking on Wednesday afternoon as the S&P 500 closed down 36 points.

Yesterday, after sleeping on the Fed’s ambivalence, traders showed up to work with focus and intent. They bought the dip with confidence. And everything was great until about mid-day. The S&P 500 was up 33 points – and then something unexpected happened.

President Trump, via Twitter, dropped a turd in a crowded swimming pool:

“…the U.S. will start, on September 1st, putting a small additional tariff of 10% on the remaining 300 billion dollars of goods and products coming from China into our country. This does not include the 250 billion dollars already tariffed at 25%.”

The market gets whacked by the God Emperor… [PT]

Following Trump’s tweet, Wall Street freaked out. The S&P 500 dropped 68 points, ending the day at 2,953.

“No one rings a bell at the top of the market,” says the old Wall Street adage. Make of this week’s manifestations what you will. We hear a bell ringing. Do you?

via ZeroHedge News https://ift.tt/2Kr5v8l Tyler Durden

The sun shines brightest across the North American continent as we enter summer’s dog days. Cold sweet lemonade is the refreshment of choice at ballparks and swimming holes alike. Many people drink it after cutting the grass, or whenever else a respite from the heat and some thirst quenching satisfaction is needed.

The economy, after 10 years of growth, appears to be heading for a respite too. Second quarter earnings, currently being reported by S&P 500 companies, have been a mixed bag thus far. But in sectors that actually make stuff, like materials and industrials, earnings are suffering double digit declines.

Regardless of whether companies were able to “beat estimates” (which as often happens, were revised lower just before the reporting season started), their actual Q2 results didn’t look very encouraging so far. The manufacturing sector in particular looks a bit frayed around the edges as the saying goes. [PT]

From a practical standpoint, earnings are declining in these sectors because manufacturing is contracting. For example, this week it was reported that the Chicago Purchasing Mangers’ Index (PMI) collapsed in July to 44.4. That is the second weakest Chicago PMI reading since the Great Financial Crisis.

For context, a Chicago PMI reading below 50 indicates a contraction of the manufacturing sector in the Chicago region. So far this year, the Chicago PMI has been down five out of seven months. On top of that, weaker demand and production pushed the employment indicator into contraction for the first time since October 2017.

Chicago PMI – based on this indicator it looks as though the economy either has already entered a recession or is very close to doing so. Occasionally dips in the Chicago PMI do not presage a recession – as for example in late 2015/ early 2016. It remains to be seen if the signal is more meaningful this time, but it definitely constitutes a warning sign. [PT]

Unfortunately, the weakness in manufacturing extends beyond the Chicago region. On Thursday it was reported that the U.S. Manufacturing PMI dropped in July to its lowest level since September 2009. Employment also fell for the first time since June 2013. What is going on?

US manufacturing PMI by Markit and the ISM manufacturing survey. These still indicate expansion, but are on the cusp of moving into contraction territory. Note: in terms of gross output, manufacturing remains the largest sector of the economy. [PT]

Economic Lemons

One place to look for edification is the auto industry. Namely, car dealers are reporting fewer buyers. They are in turn ordering fewer vehicles from manufacturers. The dealers don’t have room for the cars they have. Automakers, parts manufacturers and dealers directly employ more than two million people. As demand for cars declines, the jobs associated with the auto industry also decline.

Having too many cars with too few buyers is something an economist would call a supply glut. Of course, the easiest way to clear excess supply is to reduce prices. This may work up to a point. But if prices must be reduced beyond the cost of labor and materials inputs, there is a problem.

Making lemonade from these economic lemons is generally impossible. Still, that doesn’t mean companies don’t try by taking on greater and greater levels of debt. And the big banks, which are backstopped by the Fed, continue extending credit to keep the sham going.

U.S. non-financial corporate debt is about $10 trillion, or roughly 48 percent of gross domestic product (GDP). That is up about 52 percent from its last peak in the third quarter of 2008, when corporate debt was about $6.6 trillion, roughly 44 percent of 2008 GDP. In short, corporate debt is at record levels and is rising much faster than economic output.

US non-financial corporate debt is approaching USD 10 trillion. The corporate sector is not exactly prepared for an economic downturn. [PT]

At this point in the business cycle, corporations have loaded themselves up with so much debt that they are extremely fragile. Should the economy slow ever so slightly, it will be game over for countless over-leveraged companies. Defaults will pile up like old furniture and tires along the dry LA River bed.

Do You Hear a Bell Ringing?

But while Main Street has been cooling off, Wall Street has been running hot. Promises of more cheap credit from the Fed have propelled stocks to record highs. Year-to-date, stocks, as measured by the S&P 500, are up over 17 percent.

On Wednesday, however, some uncertainty was added to the market. At the conclusion of the July Federal Open Market Committee (FOMC) meeting, Fed Chair Powell cut the federal funds rate 25 basis points. But instead of telegraphing that additional rate cuts would follow like Wall Street expected, Powell said it was merely a mid-cycle adjustment. In other words, he’s winging it.

S&P 500 Index, daily: a minor disturbance in the farce. This was the first time since 1987 that the index actually decline on the very day the first rate cut was announced. [PT]

Will the Fed cut rates further this year? Will they hold? These were the questions Wall Street was asking on Wednesday afternoon as the S&P 500 closed down 36 points.

Yesterday, after sleeping on the Fed’s ambivalence, traders showed up to work with focus and intent. They bought the dip with confidence. And everything was great until about mid-day. The S&P 500 was up 33 points – and then something unexpected happened.

President Trump, via Twitter, dropped a turd in a crowded swimming pool:

“…the U.S. will start, on September 1st, putting a small additional tariff of 10% on the remaining 300 billion dollars of goods and products coming from China into our country. This does not include the 250 billion dollars already tariffed at 25%.”

The market gets whacked by the God Emperor… [PT]

Following Trump’s tweet, Wall Street freaked out. The S&P 500 dropped 68 points, ending the day at 2,953.

“No one rings a bell at the top of the market,” says the old Wall Street adage. Make of this week’s manifestations what you will. We hear a bell ringing. Do you?

via ZeroHedge News https://ift.tt/2rZDc6c Tyler Durden

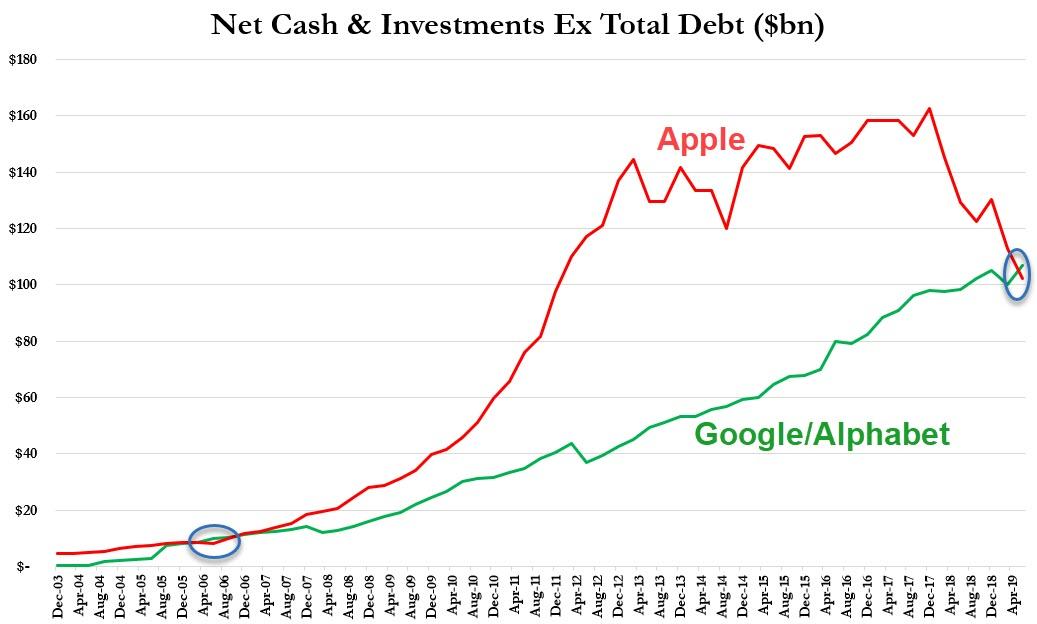

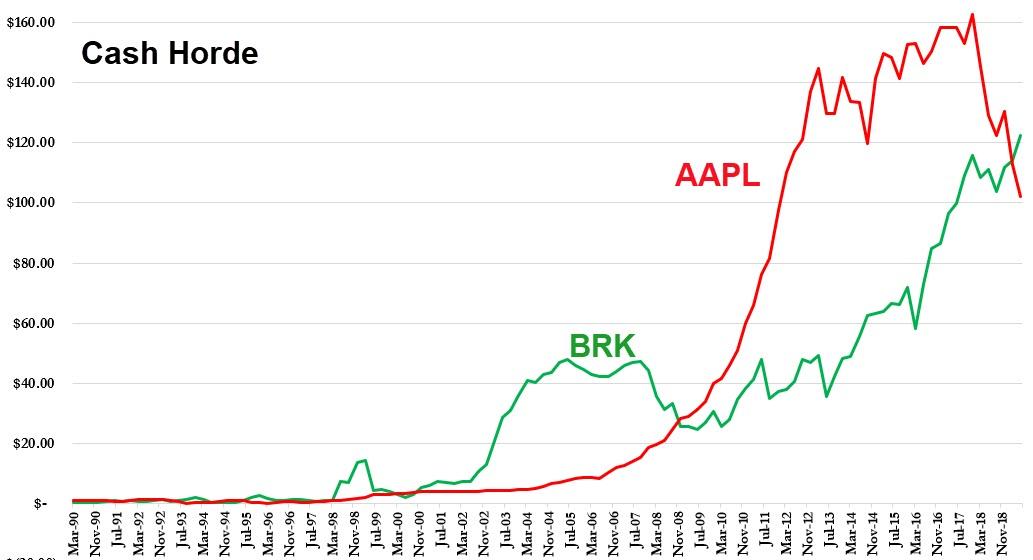

Just a few days after we reported that Apple’s once gargantuan cash hoard (net of debt) has tumbled from a record high of $163BN at the end of 2017 to just $102 billion at Q2, after aggressively funding tens of billions in buybacks and dividends, so much so that in the second quarter Google’s net cash of $107 billion surpassed AAPL for the first time ever…

… it is now Berkshire’s turn to also upstage the former cash giant, with Buffett’s sprawling conglomerate reporting a record $122.4 billion in cash at the end of the second quarter, rising above its prior cash record of $116 billion in 2017.

reflecting Buffett’s nearly 4-year drought in finding major acquisition opportunities since buying Precision Castparts. As Bloomberg notes, Buffett has been struggling to find enough well-priced opportunities to keep up the growth that allowed him to beat broader markets for decades.

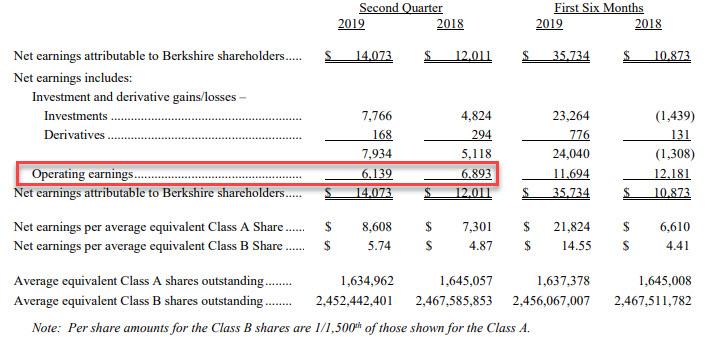

And speaking of Berkshire’s lack of growth which has resulted in its Class B stock declining 0.7% this year , significantly underperforming the market and 10% below their peak last October, it was on full display in the just completed second quarter, in which Berkshire’s operating profit fell more than expected, declining 11% to $6.14 billion, or roughly $3,757 per Class A share, from $6.89 billion, or roughly $4,190 per Class A share, a year earlier. Analysts were expecting an operating profit of $3,851.28 per share.

Operating earnings declined as Berkshire’s auto insurer Geico suffered a larger number of accident claims, while competition from foreign producers, lower imports and “trade policy” dampened cargo volumes for consumer and agricultural products at its BNSF railroad, Reuters noted. Earnings also barely budged at Berkshire’s manufacturing businesses, where U.S. tariffs hurt sales of gas turbine and pipe products at its Precision Castparts unit, and its service and retailing businesses.

Some more details:

Buffett’s railroad generated a modest profit in the quarter, bolstered by shipments of industrial products. BNSF’s profit rose 2% to $1.34 billion, while revenue was essentially unchanged. Profit was also flat in Berkshire’s manufacturing, services and retailing businesses, totaling $2.49 billion. That could help bat down concerns about its ability to weather a slowdown in the sector.

On the flip side, underwriting income at Berkshire’s insurers fell by almost 63% to $353 million. The life and health business at Berkshire’s namesake reinsurance group changed a contract with a major U.S. reinsurer, which reduced the earned premiums it raked in. Geico’s pre-tax underwriting gain fell 42%, as a higher ratio of loss claims to premiums earned more than offset growth in policies written, while expenses rose, partly due to advertising and employee costs. Underwriting at Berkshire’s reinsurance, property/casualty and commercial insurance units also weakened, reflecting higher claims payouts, changes in the expected timing of future payouts, and currency fluctuations, among other factors.

While Berkshire said more people flew NetJets corporate jets – indicating that the 0.1% are doing just great – “soft consumer demand” weighed on sales at home furnishings businesses, indicating that the less than 0.1% are not doing just great. Berkshire Hathaway Energy saw profit rise 4%.

Meanwhile, as Bloomberg notes, Kraft Heinz was once again missing from Berkshire’s results. Kraft Heinz, which is set to report results on Aug. 8, appointed a new CEO and finally issued its delayed 10-K filing in June as it worked to clean up from a $15.4 billion writedown. The restatements in June caused a $34 million hit for Berkshire, it said Saturday.

It wasn’t all bad news: Berkshire said quarterly net income rose 17% to $14.07 billion, or $8,608 per Class A share, from $12.01 billion, or $7,301 per Class A share, a year earlier, however that increase was entirely due to the rise in the stock market i.e., the higher unrealized gains on Berkshire’s investments. The company reported a whopping $7.9 billion in investment gains, up 55% from a year earlier. In other words, more than half, or 55%, of Berkshire’s net earnings came from the ongoing levitation in the S&P, which came with an abrupt halt in the past week (as a reminder, a recent accounting rule forced Berkshire to report such gains with earnings. That rule adds volatility to Berkshire’s net results, and Buffett says it can mislead investors, although when the market is rising – as it did in Q2 – nobody complains).

Meanwhile, in lieu of pursuing full-blown acquisitions in companies with “sky high valuations”, Berkshire has had to make do with equity purchases in public companies: he has built a $50.5 billion stake in Apple and controversially committed $10 billion in April to help Occidental buy rival Anardako. However, even when it comes to what upside is left in stocks Buffett appears to be having second thoughts as he was a net seller of stocks in the quarter. Nowhere was the billionaire’s market skepticism more visible than in the company’s buybacks of its own stock: Berkshire repurchased only $400 million in shares, down sharply from $1.7 billion in the first three months of the year.

via ZeroHedge News https://ift.tt/2T0FQqS Tyler Durden

A new patent filing suggests that United States retail giant Walmart may be developing its own U.S. dollar-backed digital currency similar to Facebook’s Libra cryptocurrency.

Walmart filed patent for “Digital Currency via Blockchain”

Patent filing number 20190236564, “System and Method for Digital Currency via Blockchain,” was published by the U.S. Patent and Trademark Office (USPTO) on Aug. 1. The document outlines a method for:

“Generating one digital currency unit by tying the one digital currency unit to a regular currency; storing information of the one digital currency unit into a block of a blockchain; buying or paying the one digital currency unit.”

Walmart continues to outline that the proposed digital currency project can provide a zero- or low-fee place for users to store wealth; one that can easily be redeemed and converted to store cash at selected retailers or partners. Such accounts could even be interest-bearing, the filing adds.

The digital currency could alternatively be developed so that it can be spent anywhere, the filing states, with prospective USD backing ensuring greater ease of deposits and withdrawals. It could, in another scenario, be tied to other digital currencies, rather than fiat ones.

Corporations becoming alternative banks

Early on in the filing, Walmart proposes that the launch of its digital currency could provide low-income households, for whom banking is costly, with “an alternative way to handle wealth at an institution that can supply the majority of their day-to-day financial and product needs.”

The “blockchain-protected digital currency” — as Walmart dubs it — could further challenge incumbent banks by removing the need for credit and debit cards:

“The digital currency may act as a pre-approved biometric […] credit. A person is the ‘credit card’ to their own digital value bank.”

The retailer further imagines that the scope of its digital currency could extend to form part of wider, blockchain-powered service ecosystem, envisioning the creation of an “open-platform value exchange for purchases and for crowdsource work.”

This would allow customers to buy products or services for themselves and for others — using the platform to hire a technician for repairs, an associate or a designated shopper for a given amount of time.

While it currently faces a robust regulatory pushback, Facebook’s Libra stablecoin project has a similar ambition to provide low-cost, borderless value transfer and build out a digital currency-powered network.

A new report from TASS News shows that Sukhoi Aircraft Company, part of Russia’s United Aircraft Corporation, has started series production of Su-57 fifth-generation fighter jets and will soon be delivering these planes to the country’s Aerospace Force.

Deputy Prime Minister Yuri Borisov, told TASS earlier this week that production of the stealth jets has started, with expected production ramps through the 2020s.

“A state contract was signed at the Army 2019 international arms exhibition between the Defense Ministry of Russia and the Sukhoi Company for the delivery of a batch of Su-57 fifth-generation fighter jets. The Sukhoi has started to fulfill its contractual obligations,” the vice-premier’s office reported.

The state contract requests the delivery of 76 Su-57s to Russia’s Aerospace Force by 2028.

Russia’s Defense Ministry said the Su-57s are “the most advanced fifth-generation multirole fighter jet, which will boost the domestic Aerospace Force’s combat capabilities.”

The vice-premier’s office released a statement that confirmed the first two Su-57s would be delivered to the Aerospace Force by year-end. “The first plane will be delivered to the customer before the end of 2019.”

The Su-57 is a multirole stealth fighter that is capable of maintaining supersonic cruising speed and is equipped with advanced onboard radio-electronic equipment, including a powerful onboard computer, advanced radar system, and armament placed inside its fuselage. The plane can track 60 targets and open fire at 16 of them concurrently.

The fifth-generation fighter jet has been battle-tested in combat conditions in Syria.

— Yuri Lyamin (@imp_navigator) November 19, 2018

According to Russia’s Tactical Missiles Corporation, Su-57s will have the capability of air launching hypersonic missiles in the early 2020s.

With US-Russia relations deteriorating in the aftermath of the collapse of the INF nuclear arms treaty, which prompted Russia’s Vladimir Putin to slam the US for “demolishing” global security, Russian state television listed U.S. military facilities that Moscow would target in the event of a nuclear strike, in a report which Reuters said “was unusual even by its own bellicose standards” and said that a hypersonic missile Russia is developing would be able to hit them in less than five minutes.

It’s entirely possible that Su-57s could evade US radar systems and launch hypersonic missile attacks at asset-heavy areas across Alaska, West Coast, and on the East Coast. The next world war will be fought with fifth-generation fighters and hypersonic weapons.

via ZeroHedge News https://ift.tt/2YD8WxH Tyler Durden

If new institutional reform is to come to the Eurozone, it will entail a major paradigmatic shift…

We now know that there will be a changing of the guard at the European Central Bank (ECB) in October. The current head of the International Monetary Fund (IMF), Christine Lagarde, will succeed current ECB President Mario Draghi at that time.

A known quantity among the political and investor class of Europe, Lagarde seems like a safe choice: she is a lawyer by training, not an economist. Hence, she is unlikely to usher in any dramatic changes, in contrast to current European Central Bank president Mario Draghi, who significantly expanded the ECB’s remit in the aftermath of his pledge to do “whatever it takes” to save the single currency union (Draghi did this by underwriting the solvency of the Eurozone member states through substantially expanded sovereign bond-buying operations). Instead, Lagarde will likely stick to her brief, as any good lawyer does. There’s no doubt that her years of operating as head of the IMF will also reinforce her inclination not to disrupt the prevailing austerity-based ECB ideology.

Unfortunately, the Eurozone needs something more now, especially given the increasingly frail state of the European economies. The Eurozone still doesn’t have a treasury of its own, and there’s no comprehensively insured banking union. Those limitations are likely to become far more glaring in any larger kind of recession, especially if accompanied by a banking crisis. That is why the mooted candidacy of Jens Weidmann may have been the riskier bet for the top job at the ECB, but ultimately a choice with more political upside. An old-line German central banker might have been able to lay the groundwork for the requisite paradigmatic shift more successfully than a French lawyer, especially now that Germany itself is in the eye of the mounting economic storm.

It’s summertime, but the living is certainly not easy in the Eurozone. The Mediterranean economies — notably Greece and Italy — have never really achieved sustainable growth over the last decade, and to the extent that either country ran deficits, or received bailout assistance, it was largely used to pay off debts to a range of bank creditors, rather than generate higher employment. However, the Eurozone’s weakness is now rapidly spreading to the North, notably in Germany, where the Ifo Institute’s manufacturing business climate index is “in freefall,” reports the Financial Times. The Ifo indicator — a good coincident gauge of overall economic health in the Eurozone’s main manufacturing hub — registered its worst reading in nine years, precipitously declining to minus 4.3 in July vs. a gain of plus 1.3 in June. Furthermore, Germany’s Purchasing Managers Index (PMI) has plunged to the mid-40sover the last few months. Fifty is the demarcation separating expansion from contraction, suggesting an imminent recession.

On top of that, Germany’s leading bank, Deutsche Bank (DB), is steadily being revealed to be the greatest repository of corporate corruption since BCCI. Whether it be money laundering for Russian oligarchs (or, allegedly, the Trump family); involvement in interest rate scams such as LIBOR manipulation; violations of U.S. economic sanctions on Iran, Syria, Libya and Sudan (among others); or the sale of toxic securities in the run-up to the 2008 financial crisis, DB has played a leading role, and is now paying the price. Berlin has repeatedly sought to find a buyer for the bank, but both Commerzbank and UniCredit have had a closer look under the hood and ran for the hills accordingly. The share price performance suggests that Deutsche Bank is an imminent candidate for a bailout, if not outright nationalization.

This comes during a historically unprecedented situation in global bond markets, particularly in the Eurozone where negative yields are now pervasive — in other words, investors are now willing to pay certain governments to safeguard their money, whether this be Germany, Denmark, Switzerland, or the Netherlands. This is a foolhardy risk to incur, given that all Eurozone governments are currency users, not issuers (only the ECB creates euros), and therefore carry the same kind of theoretical solvency risk as, say, an American state or municipality.

As the economist Frances Coppola notes, “Every Danish government bond currently circulating in the market is trading at a negative yield. And the inverted curve tells us that markets are pricing in further interest rate cuts, most likely to hold the ERM II peg when the ECB cuts rates and re-starts QE.” Which means yields can become even more negative. Such is the desperation for perceived “safe assets” that Austria, Belgium and Ireland have all sold 100-year securities (the yield on Austria’s 2117 bond has dropped nearly 100 basis points since it was launched two years ago with what was then considered a derisory 2.1 percent coupon, and recall that Ireland’s banking crisis placed the country close to national insolvency 11 years ago). It’s virtually impossible to make sensible economic forecasts a few months out, let alone a century, so this does suggest a certain kind of collective madness (or desperation) now taking over the bond markets.

All of which tells us that something is indeed rotten in the state of Denmark (and elsewhere), as Lagarde takes over as president of the ECB. The constellation of soft economic data in Europe has investors clamoring for the ECB to act, but negative yields suggest that there is little more that interest rate manipulation can do to generate an economic upturn. Indeed, economists Markus Brunnermeier and Yann Koby have persuasively argued that negative yields represent the juncture “at which accommodative monetary policy ‘reverses’ its effect and becomes contractionary for output.” In other words, monetary policy has reached the point where further attempts to cut rates might actually hinder economic growth, rather than promote it.

As Rob Burnett, a fund manager at Lightman Investment Management, has suggested, “What is required is demand-based stimulus and spending must be directed into the real economy” — in other words, fiscal expansion, which unfortunately is not the purview of the ECB. Furthermore, the central bank’s “quantitative easing” purchases of sovereign bonds have hitherto been conditionally predicated on the national finance ministries’ continuing to practice fiscal austerity, which in turn produces the exact opposite economic outcome that Burnett has proposed. The unfinished architecture of the Eurozone makes this problem particularly awkward, given that there is no “United States of Europe” treasury equivalent — a gaping institutional lacuna in the Maastricht Treaty — which in itself creates unstable dynamics that constrain national policy fiscal space. Politically, the ECB represents the awkward focal point in regard to increasing global market integration on the one hand with growing demands for reclaiming national political sovereignty on the other. Such challenges become more acute in the context of a global economy that, outside of the United States, is teetering toward recession (or worse).

It’s also a terrible environment for banking in particular, especially as any attempts to reduce deposit rates below zero (in effect charging depositors for the privilege of having banks store their money) would almost certainly trigger bank runs. Nor are the banks inclined to generate profits via lending activity when there is a steadily decreasing supply of creditworthy borrowers on the other side.

The other problem also relates to the Eurozone’s faulty half-finished architecture: free intra-Eurozone capital flows are promoted within the Eurozone (via the Trans-European Automated Real-time Gross Settlement Express Transfer system, aka the “TARGET2 system”), despite the absence of a unified supranational banking system or common, Eurozone-wide deposit insurance (such as the American FDIC). This creates ample scope for bank runs from one country to another (as the economist Peter Garber predicted back in 1998), and which were occurring in earnest back in 2012, as investor George Soros observed, and specifically tied to TARGET2.

Across the Eurozone, bank assets generally exceed GDP. They also do in non-Eurozone countries, such as Norway, Switzerland, and the UK. But the difference in the non-Eurozone countries is that they are all sovereign currency issuing countries, which means that all have unlimited capacity to provide deposit insurance in the event of a bank run. Paradoxically, it is precisely because of this unlimited currency issuing power that such bank runs seldom go very far in these countries. The public intuitively understands that the insurance can be made good.

This is why the United Kingdom and Switzerland were able to handle their respective banking crises in 2008 without threatening national insolvency. Retaining sterling as the national currency, the UK had unlimited fiscal capacity to offer credible deposit insurance instantaneously during its crisis. To cite one example, in 2007 a regional bank, Northern Rock, applied to the Bank of England (BOE) for emergency support to help it through a liquidity crisis triggered by the subprime mortgage slump in the U.S. and temporarily incurred substantial deposit runs as a result. The BOE’s prompt actions (made easier by the fact that they did not need to secure the collective approval of 27 other countries, as occurs in the single currency union) put a halt to the withdrawals. Likewise, Switzerland was able to recapitalize its own major banks relatively quickly after the 2008 crisis began in earnest and avoided the prolonged banking crises that characterized the Eurozone countries.

Ireland is a good example of the latter. An economy structurally similar to the UK, Ireland experienced a banking crisis with far more longstanding deleterious effects (including an unemployment rate almost double that of the UK at its peak). The crisis was far more serious than in non-Eurozone countries because the markets intuitively understood that the country did not have the fiscal capacity to adequately safeguard the banks’ deposit base (despite pledges to do so on the part of Dublin’s policymakers).

Within the Eurozone, the Emerald Isle’s problems were by no means unique. As is now well appreciated, all Eurozone member states operate under the same constraints with no national currency. In regard to coping with a potential banking crisis, however, the currency issuer, the ECB, does not have the regulatory or political authority to close a bank, regardless of what country the bank claims as its home (in the same way that, say, the American FDIC can operate to shut down a bank, no matter which state, and credibly restart it quickly, by virtue of the backstop of the U.S. Treasury). So far the member states within the single currency union have managed to dodge this particular bullet, but given the mounting strains now intensifying in the Eurozone, a credible banking union of some sort must ultimately be on the table. Wolfgang Münchau, columnist for the Financial Times, outlined the four key “centralised components” required to make such a union workable and durable: “a resolution and recapitalisation fund; a fund for joint deposit insurance; a central regulator; and a central supervising power.”

Even a central banker as powerful as Mario Draghi has yet been unable to persuade the major Eurozone powers, especially Germany, to accede to such a proposal, which Berlin still regards as a covert means of putting German taxpayers on the hook for billions of euros’ worth of other countries’ banking liabilities. In light of the current travails of Deutsche Bank (and the longstanding financial difficulties of Germany’s regional lenders, the so-called “Landesbanken”), however, attitudes might change in Berlin.

In any case, this represents one of the more formidable challenges Christine Lagarde is likely to face in her new job going forward. Given the existing institutional limitations of a monetary union without a supranational treasury backstop, no Eurozone FDIC can be credibly established absent institutional ties to the ECB. National banking interests cannot interfere with the deposit insurance fund because this would immediately destroy the credibility of the banking union. But absent broad multinational consensus, no such supranational FDIC can come into being.

The glue holding the Eurozone’s institutionally fragile structure together has always been the European Central Bank. As the sole issuer of the euro, the ECB is operationally free to provide as many euros as needed to keep the funding system in place. It cannot go broke. But politically, it is an orphan. The problem is that calls for international cooperation to improve its supranational governance structures to address these cross-country dynamics reinforces the impression of eroding national control, which in turn heightens populist backlash across the continent. Mario Draghi’s monetary gymnastics helped preserve the Eurozone, but the battle is not yet won.

One wonders whether someone with Christine Lagarde’s comparatively limited economic and financial expertise has the ability to confront these challenges with the same aplomb her predecessor. We shall find out soon enough.

via ZeroHedge News https://ift.tt/2KmjRqv Tyler Durden

As WWII came to an end, American Troops discovered Nazi files in a cave in Southern Germany… These documents revealed a project to discover the lost Aryan civilisation from which the Nazis believed they had descended.

This documentary uses rare footage as well as unseen photographs to help tell the story of three missions: a global search for the lost island of Atlantis, an expedition to find traces of the master race in the Himalayas, and an astonishing Nazi-sponsored quest for the mythical Holy Grail.

According to the Turkish National Defense Ministry, receipt of the first batch of Russian S-400 missile defense systems was completed on July 25th. Besides making headlines all around the world and causing a harsh response from the US, the delivery demonstrated Turkey’s readiness to provide independent defense and foreign policies in its own interests despite all the difficulties that it may face on this path.

The Russian S-400 missile defense system, according to Stratfor, is the “best all-around.” It is approximately 30 years in the making, as development began in the late 1980s, and it was officially announced in 1993.

The first successful tests of the system were conducted in 1999 at Kapustin Yar in Astrakhan and the S-400 was scheduled for deployment by the Russian army in 2001. By 2003, the system was yet to be deployed to Russia. Following various setbacks it was finally cleared for service in 2007.

The S-400 Triumph package consists of a 30K6E battle management system, six 98ZH6E SAM systems, 48N6E3 and (or) 48N6E2 surface-to-air missiles (SAMs) ammunition load and 30TsE maintenance facilities. Use of the 48N6E SAM is possible.

An S-400 Transporter Erector Launcher has four missile containers. Each container can house one 48N6E or four 9M96 surface-to-air missiles.

The S-400 can be used with a semi-mobile package of towed trailer-mounted radars and missiles. Typically, it is towed by the Russian 6×6 truck BAZ-6402-015.

It takes 5-10 minutes to set system assets from traveling position and about 3 more minutes to set it to ready from the deployed position.

The S-400 has a target detection range of approximately 600 km, while being able to simultaneously track around 300 targets. The maximum speed of the target may be up to 4,800 m/s, approximately Mach 14.

It can simultaneously engage approximately 36 targets, or 72 guided missiles. It can engage an aerodynamic target at a range of between 3 and 250 kilometers, while a ballistic target can be engaged at 60 kilometers.

The Russian armed forces have several S-400, located at various positions, as well as plans to equip the Kirov-class battlecruiser Admiral Nakhimov with the 48N6DMK anti-aircraft missile derived from the land-based S-400. By 2020 Russia plans to have 28 S-400 regiments, each comprising of two or three battalions. In turn, each battalion consists of at least eight launchers with 32 missiles and a mobile command post.

Two S-400 systems are deployed in Syria for use in protection of Russian personnel.

Since 2016, Belarus has two S-400 missile systems, both provided by Russia free of charge, as per a 2011 agreement.

China received its first S-400 regiment in May 2018 and carried out successful tests in August 2018. There was an issue where Russia had to send dozens of replacement missiles in early 2019 since a Russian cargo ship, reportedly carrying an export variant of the S-400’s most advanced interceptor, the 40N6E, was forced to return home as a result of damages sustained during a storm in the English Channel. On July 25th, 2019, Russia began the delivery of China’s second S-400 missile defense system regiment;.

In October 2017, Saudi Arabia announced that it had finalized an agreement for the delivery of the S-400 missile defense system. Unsurprisingly, the US’ key ally in the Middle East wasn’t subject to sanctions and constant warnings over purchasing the S-400. In February 2019, the Kingdom and Russia held consultations on the S-400.

The S-400 missile defense system is expected to enter into service in India in October 2020. The United States threatened India with sanctions over India’s decision to buy the S-400 missile defense system from Russia. So far, it’s proving as effective as the threats towards Turkey.

As of January 2018, Qatar has allegedly been in advanced talks for the purchase of S-400, but no additional information has been provided since.

There are various rumors and confirmations by officials from Pakistan, Iraq, Iran and Egypt for interest towards the S-400.

The US strongly opposes the purchase of S-400 by its allies, but mainly by Turkey, since Turkey was a key partner in the F-35 Joint Strike Fighter program. According to US officials, there were constant fears that it could be used to steal the fighter jet’s secrets. Turkey has, for over a year now, maintained that the deal was done and there was nothing the US could do to dissuade it from purchasing despite threats of sanctions and other aggressive actions.

In a last ditch and quite absurd effort US Republican Senator Lindsey Graham, allegedly on behalf of US President Donald Trump, suggested that the Turkish side may choose to “simply not turn on” their $2 billion system to avoid difficulties in the Turkish-US relations. This absurd proposal was later repeated by US Secretary of State Mike Pompeo.

US media claim that negotiations on an offer by the US for Turkey to purchase a Raytheon Patriot missile system are still on-going despite the S-400 delivery. How that makes sense is unclear, but the new US Defense Secretary Mark Esper was, after all, a Raytheon lobbyist. Regardless, the cost of the proposed Patriot is $3.5 billion, compared to the $2 billion Russian system.

Another factor why the US military political leadership opposes deliveries of Russian state-of-the-art air defense missile systems to other states is that such deals contribute to the Russian development programmes in this field. Right now, the Russian military is developing and testing interceptors of the A-235 Nudol anti-ballistic missile system and anti-satellite weapon. The system is set to replace the current one defending Moscow and the surrounding region from nuclear attacks, the A-135 Amur.

According to reports, the Nudol will operate in three stages:

Long-range, based on the 51T6 interceptor and capable of destroying targets at distances up to 1500 km and altitudes up to 800 km

Medium-range, an update of the 58R6 interceptor, designed to hit targets at distances up to 1000 km, at altitudes up to 120 km

Short-range (the 53T6M or 45T6 interceptor (based on the 53T6)), with an operating range of 350 km and a flight ceiling of 40-50 km

The main contractor for the project is Almaz-Antey, who created the S-300, S-400 and is working on the S-500. According to military experts, the future of the missile defense systems A-235 and S-500 will form the basis for the comprehensive, integrated aerospace defense system of Russia, which will include a variety of modern ground-based detection tools.

The additional experience and funds obtained by Almaz-Antey and Russian military experts during implementation of S-300 and S-400 deals around the world and their usage in the conflict zones such Syria will allow Russia to make its aerospace defense systems even more sophisticated and effective.

via ZeroHedge News https://ift.tt/337HnzZ Tyler Durden

A series of heatwaves across Central Europe this summer has brought record-breaking temperatures to Germany that sparked dangerously low water levels on the Rhine river, one of the continents most important shipping routes, which could decrease manufacturing and disrupt supply chains that might tip Germany into recession.

Water levels on the Rhine last summer made some parts of it unnavigable. This disrupted supply chains in Germany’s industrial heartland that use the river for shipping.

Reuters recently reported that the shortage of rainfall this summer and scorching hot temperatures across Germany and France had made some parts of the Rhine impassable for fully loaded cargo ships.

“Approximately 80% of all goods that are transported via domestic water transport go along the River Rhine. Thus, it is Germany’s most important waterway,” Robert Lehmann, an economist at Germany’s influential Ifo Institute research center, told CNBC Tuesday.

“Coal, oil, and gas or chemical products are transported with a much higher intensity: 10% to 30%. These are the main goods at the beginning of important value-added chains, thus, low water levels at the River Rhine can immediately lead to restrictions in industrial production.”

Low water levels on the river could have severe economic consequences for Germany’s economy that is already dealing with an industrial recession.

New economic data on Thursday showed Germany’s manufacturing sector plunged in July with factories producing goods at the slowest rate in seven years and export orders crashed to the lowest in more than a decade.

Germany’s automobile industry has been the most significant factor in the industrial slowdown, low water levels on the Rhine have also been seen as a factor.

Holger Schmieding, the chief economist at Berenberg Bank, told CNBC Tuesday that shipping on the river was halted last fall, this caused the production of German chemicals and pharmaceuticals to plummet by 10% from September to November and damaged the overall economy

“While some of this reflected an emerging softness in demand, the impaired shipping was the major cause. Chemicals and pharmaceuticals account for 8.3% of German industrial output and 2% of overall German value-added. So, a 10% fall in output of that sector maintained for a full quarter would reduce GDP (gross domestic product) for that quarter by 0.2 percentage points.”

The Rhine flows 760 miles starting in Switzerland and goes through Germany into the Netherlands, draining into the North Sea. It’s the top shipping route for intercontinental transportation of agricultural and petrochemical products.

Germany’s WSV rivers authority said they’re powerless in preventing the river from drying out. “The Rhine is a natural river,” said Hans-Heinrich Witte, president of WSV. “There are limits to what we can do to keep it open as an industrial waterway.”

Carsten Brzeski, the chief economist at ING Germany, noted last week that the German economy is at “the most dangerous crossroads since 2009” amid a broad base industrial slowdown. The sweltering temperatures just made the situation worse.

Traders told Reuters on Friday morning that water levels on some parts of the Rhine are increasing but from ultra-low levels after wet weather was seen in Germany this week.

“The northern sections of the Rhine, especially around Cologne, are still hovering around the minimum level for full loads but overall we are not facing the sort of serious problems we had last year,” one trader said.

“But I think we will see the river moving in and out of shallow water in the coming weeks.”

Unusually low water levels on the Rhine, an industrial recession in Germany, and economic stagnation across Europe, it seems like the European Central Bank will have their hands full this fall in trying to revive the Germany economy.

Does anyone know if the ECB can print water yet?

via ZeroHedge News https://ift.tt/33j8qIO Tyler Durden

In this article, we look at the implications of the new Johnson government: its strategy, the likely outcome of EU negotiations, and the golden opportunities to reform trade, tax and monetary policies to secure a better future based on free trade.

Introduction

It should have been no surprise that Boris Johnson is now Prime Minister. It should also be no surprise he will implement Brexit on 31 October, the last date agreed between Mrs May’s government and the EU. Johnson was elected by Conservative constituency members to do just that. His cabinet appointees are fully supportive, including ex-Remainers (that’s politics!) and he has appointed an aggressive rottweiler, Dominic Cummings, as his Brexit enforcer. Already, his influence over Brexit strategy can be detected. There are no compromises to be had, a point which slower minds in the commentariat find difficult to comprehend and accept.

It is likely there will be an agreement on the way forward after Brexit, which could involve a transition period, but nothing like that agreed with Mrs May. If, as seems unlikely, the EU digs its heels in, the UK will walk away. That is the message being given by the new administration.

The establishment media are still wrong-footed on Brexit. The BBC, and others, have been too idle to analyse properly, taking their information from biased pro-remain sources and politicians who are out of the loop. They are still doing it. Disinformation is substituted for truth.

The EU, disinformed by Remainers including a chorus of past ministers and prime ministers, has relied on the divisions within Parliament to put Britain into a political and economic stasis. Their repeated utterances (there will be no new negotiation, the withdrawal agreement stands etc.) reflect the continuation of the EU’s established position. That is likely to change, because the EU will find it is forced to accept the dangers to its own position.

There is a crucial difference between the new cabinet and its predecessor. In Johnson, as well as ministers such as Rees-Mogg, Raab, Javid and Gove there appears to be an understanding of and commitment to free markets, unlike anything we have seen since Margaret Thatcher. Obviously, the strength of that commitment is yet to be tested.

The new reality and the dismissal of the old socialising compromisers should swing Parliament behind the instructions given to it by the electorate in the Brexit referendum. An advertising campaign to prepare everyone for Brexit without a deal starts now. The strategy is not to go to Brussels (UK-US is being negotiated first) but only when Brussels comes to its senses will a dialog commence. Facing a lost cause, Remainers are likely to melt like midsummer hailstones, and the euro-nuts, like Dominic Grieve, will sink into obscurity.

The electoral consequences are appalling for the Labour Party. By changing from its conditional support for implementing the Brexit referendum to demanding a second one with the intention of overturning the first, they have almost guaranteed that in a general election they will face a wipe-out. This is important, because it means that they have no incentive to table a vote of no confidence in Johnson’s government. They have already gambled and lost.

Because of Labour’s bad call it looks like Boris’s government will get its way and is here to stay, not only through Brexit, but beyond. The EU will have to get used to it. The Europeans have lost control over the negotiations and seem unlikely to get more than a pittance of the £39bn settlement agreed with Mrs May. When Boris refers to our friends in Europe, he actually means our adversaries. When he refers to his preference for a deal against no deal, he means a deal only on his government’s terms. Already, trade negotiations are commencing with America, existing EU trade agreements with other significant nations will be simply novated, and the whole of the Commonwealth, including populous India are ready to sign up.

This is the new reality and Dominic Cummings’s task is to ensure all government departments are firmly on message. There is bound to be a little drift from this black and white, but the process of political destruction now moves from London to Brussels. Having made such a fuss of it, the Irish border is a non-issue. The UK has no need to put in a border. With lower UK tariffs, ownership of the problem is fully transferred to the EU and the Irish government.

Assuming the Treasury has already made provisions for it, Boris needs the £39bn promised by Mrs May to the EU to be reallocated to a mixture of the health service, education, law enforcement and tax cuts. Then there’s that infamous £350m per week, which was on the side of the Brexit bus. That was gross of the Thatcher rebate, so the actual figure is closer to £275m per week, and there was an amount within that spent in the UK under the EU’s sole direction. That left £181m in 2016, sent to Brussels for the privilege of EU membership, or £9.4bn per annum. How much of that can be diverted for funding government spending depends on the new government’s tariff policies. There is no doubt that from a purely economic point of view they should be removed in their entirety.

By not paying the planned £39bn divorce settlement and gaining the £9.4bn net annual payments to the EU, Johnson has some wriggle room when it comes to funding his spending plans and tax cuts. Without it, he will have to rely on inflationary financing, and hopefully there are enough wise heads in the cabinet to dissuade him from going down that road. Therefore, if only because of the money, the odds strongly favour a hardball approach on Brexit negotiations instead of compromise.

The EU’s problems are mounting

There is likely to be an important consequence, and that is a Johnson Brexit could trigger a mounting financial and ultimately political crisis in the European Union.

A study last year by Germany’s Halle Institute estimated a no-deal Brexit would cost 12,000 jobs in the UK, and 422,000 jobs in the other 27 EU members, of which 100,000 are in Germany and 50,000 in France. Yesterday, Ireland’s central bank forecast a loss of up to 100,000 jobs in the medium term in Ireland alone, on a no-deal. Clearly, the EU’s negotiators risk losing the wholehearted support of its two largest post-Brexit paymasters and others. But for Brussels, giving in on Brexit encourages rebellion from disaffected populations in other member states. Rather like the Soviets ruling Eastern Europe in the late eighties, the Brussels establishment finds itself struggling to keep its non-democratic political model intact.

It is increasingly likely Brussels will find events are spinning out of its control. For the UK, this introduces collateral damage, necessitating even more urgent separation from the EU. In a paper published at end-June, Bob Lyddon points out that a Eurozone financial crisis (which is becoming increasingly likely, as argued below) could cause the UK’s contingent liability as an EU member to be as much as €441bn. “This derives from the near-criminal irresponsibility by the UK’s negotiators”.

Whatever the numbers, there can be no doubt that this is an extremely serious issue. Furthermore, in the event of a financial and systemic crisis in the Eurozone, the UK will face its own crisis, if only because of cross-liabilities through the two banking systems. And the cyclical economic downturn that always follows the failure of a period of credit expansion is coming up on the inside rail very rapidly.

The EU economy is left badly unbalanced, with Germany dominating production and exports. Other populous member states, notably in the Club Med and France, are in a financial mess. They have relied on Germany’s production to provide for their unproductive profligacy. Her production output is now contracting.

Germany has been hit by three adverse developments at the same time. There is President Trump’s tariff war against China, which has undermined Germany’s largest growing markets at the eastern end of the Silk Road, and the threat he will deploy similar tactics against Germany. There is EU environmental legislation, which is making Germany’s motor production obsolete and forcing manufacturers to put a time-limit on existing production while investing enormous sums in electric technology. The damage this has done extends down the whole production chain, undermining the Mittelstand.

Then there is the crisis in Germany’s major banks, most publicly seen in Deutsche Bank because of longtail liabilities from its investment banking division. But all German banks, as well as those throughout the EU, face a lethal combination of margin compression from negative interest rates and a legacy of an expensive branch network when customers are migrating to online banking. The slump in German production now provides an additional threat to their loan books.

In the background, there is the turn in the global credit cycle from its expansionary phase into a periodic contraction, usually resulting in a credit crisis. To understand the transition from credit expansion to a tendency for it to contract is to recognise that the expansion of credit as a means of stimulating an economy depends on tricking economic actors into believing prospects are improving. When the evidence mounts that they are not, monetary stimulation fails, and credit begins to contract. Despite the ECB maintaining negative interest rates, despite the ability of highly-rated companies to raise finance at zero or even negative rates, and despite the ECB’s offer to pay companies to borrow (which is what deeper negative rates amount to) economic actors are now aware that it is all deception.

This is why Germany now has all the appearances of being in the early stages of a deepening economic slump, and there is nothing monetary policy can do about it. Brexit will simply add to these problems, not just for manufacturers, but for their bankers as well, as the Halle Institute report implies.

It is increasingly difficult to see how with escalating budget deficits in member governments Brussels can afford to continue with its head-in-the-sand approach to trade negotiations with Britain. The eurocrats naturally retreat into more protectionism when they see the system threatened. But asking Germany, France, the Netherlands, Austria, Finland, Sweden and Denmark for more money when their tax revenues are slumping is unlikely to cut much ice.

The new Johnson team will know some of this. There may be a temptation to make a portion of the £39bn, promised by Mrs May, available to Brussels to alleviate their pain in return for a quick deal. This goes against the new hard attitude of the Johnson government, exemplified by the presence of Dominic Cummings. But we shall see how this one pans out.

The UK economy Post-Brexit

Meanwhile, as economist Patrick Minford recently pointed out, a US-UK trade deal could lower prices of goods in the UK by as much as 20%, being the effect of EU tariff protection against global competition, raising prices above the world price level by that amount. Minford estimates a UK-US trade deal would lead to an overall gain to UK GDP of between four and eight per cent, a markedly different outcome from the project fear propaganda of the old establishment. And in the event of No Deal with the EU, the UK Treasury will receive up to £13bn in tariffs from EU importers, assuming no reduction in EU imports. Obviously, there will be substitution of EU goods for goods from the US and elsewhere, once trade agreements are in place, so this will be a maximum revenue figure.

The point is No Deal is not the disaster promised by the May establishment and its business lobbyists. It is a disaster for the remaining EU. Exiting the EU offers the Johnson government a good start, a clean sheet. Any compromise with the EU on trade and money detracts from this benefit.

It is an opportunity for Britain to reset the approach to political economy, which is our next topic. For attention-deficit politicians, there are two important factors to understand that are central to formulating post-Brexit policy: the reason why trade imbalances arise, and therefore how trade and economic policies should be constructed, and the destructive effects of inflationary financing.

How trade imbalances arise

It is vital to understand the source of trade imbalances, so that the mistake made by President Trump, which is driving the world into a Smoot-Hawley-style 1930s slump, is not repeated by Britain. The common error is to believe that the exchange rate sets trade surpluses and deficits. It therefore follows, the argument goes, that artificially raising the price of imported goods by imposing tariffs achieves the same effect.

The simplest explanation to understand why this is wrong is to start with a theoretical sound money example before progressing to the current fiat money environment. When gold was money and if unbacked currency and credit were not available, imports could only be paid for in gold or fully-backed gold substitutes. The same is true of exports. An individual borrowing to buy an imported good has to source gold or a fully-backed gold substitute, so the provider of money has to defer consumption, which includes that of imported goods. And unless the people in a nation collectively adjust the amount of gold in circulation, imports will always balance exports.

Compare this with nations trading with each other using unbacked state-issued currencies. These are issued at will by central banks as new money and by commercial banks in the form of bank credit. Therefore, anyone can buy an imported good without having to have the money, so long as a bank advances the credit.

Money and Credit expanded out of thin air replaces the need for imports to be paid for by exports. Now that all countries work their currencies the same way, the trade balance becomes a relative matter. Other things being equal, the country which expands its money and credit the greatest ends up with the largest trade deficit, and the one that expands the least the largest trade surplus.

But national statistics are designed to reflect money spent on consumption (GDP) separating out money spent on capital items. A nation whose population has a savings habit will spend less on imported consumer goods than a nation with a lower tendency to save. This is why Japan’s monetary expansion has not fuelled a trade deficit in consumer goods. In other nations, such as the US and UK, where personal savings are now minimal, credit expansion leads to chronic trade deficits.

The expansion of fiat money to bridge the gap between tax revenue and government spending similarly leads to a rise in imports, because the expansion of money and credit, when they are not saved by the consumers who ultimately benefit, always ends up fuelling consumer imports, often as a second or third order event. This gives rise to the twin deficit phenomenon commonly observed in both the UK and US, where consumer savings are virtually non-existent.

The destruction arising from inflationary financing

The Keynesian policy of stimulating an economy through a temporary budget deficit relied on deceiving economic actors into thinking there was more demand in the economy than existed. Like all confidence tricks, it eventually fails. Governments end up with perpetual budget deficits, which trend larger with every unresolved credit cycle.

Expanding money and credit as a means of funding government spending through the creation of debt has now become central to state finances everywhere, including the UK. The advantage for governments is very few people understand that this form of finance transfers wealth from the producers in an economy to the state. But the government is eating its own seed-corn by impoverishing its tax base, which if continued leads inexorably towards the destruction of its currency.

Any politician who claims to be a free-marketeer is not one unless sound money, devoid of inflationary financing, is embraced. Taking into account the importance of sound money and the reasons trade imbalances arise, a Johnson government that understands these issues will be equipped to fashion economic and monetary policy for the future. It is not enough to merely pay lip service to the necessary objectives, but to grasp the economic theory behind them, so that socialist and neo-Keynesian claptrap can be fully exposed in reasoned debate.

These are two objectives to strive towards, and will necessarily take time, because changes in government policy must steer the electorate along with it. They should be pinned up as mission statements on the notice boards in Downing Street. That being accepted, the following supporting policies must be implemented to re-orientate the ship of state towards economic success:

Tax policy. Tax cuts should be broadly financed by reductions in government spending, not through increasing the budget deficit in the hope that the economic stimulus will generate higher taxes. Welfare must only support people in genuine need, not those with just a sense of entitlement.

Government spending. Means must be found to reduce the proportion of government spending in the economy as a whole, to reduce the burden on the productive private sector. A financial and economic crisis requires departmental spending to be slashed, not just future planned increases cut, as was the case under Gordon Brown in 2009.

Encouragement to save. Taxes should be removed from savings and capital gains. Inheritance tax must be abolished. This is to allow people to accumulate personal wealth and to reduce the need for the state to provide.

Trade. Trade agreements with other nations should be viewed as a first step towards wholly free trade. By exploiting the comparative advantage of allowing people to buy what they want from providers of goods and services irrespective of location, capital resources will naturally be redeployed towards their more efficient use. This is why understanding that trade imbalances do not arise from currency differentials is so important.

Monetary policy. Steps must be taken to restrict the Bank of England from manipulating the economy through monetary policy. Targeting inflation and employment must be abandoned, and markets allowed to set interest rates. Credit expansion should be curtailed by ensuring that UK banks and branches of foreign banks operate to stricter capital rules. Goal-seeking stress-testing must end. In the longer-term, banks should lose the protection of limited liability, which has allowed bankers to make rash lending decisions without bearing the ultimate cost.

Gold. The Treasury must replenish the nation’s gold reserves. The risk of a global currency crisis is increasing by the day, and foreign currency reserves will need to be reallocated at least in line with those of other major nations.

Conclusion

Brexit is an opportunity to reset economic, monetary and trade policies. The implications of getting rid of the EU millstone go far beyond the leaving date of 31 October. Assuming a Johnson government has a good grasp of why free trade benefits the economy and why trade imbalances exist, combined with the courage to steer Britain towards the long-term prosperity offered by free markets, it will derive its future power from a strong economy instead of merely claiming it based on the past.

via ZeroHedge News https://ift.tt/2yw8gQ7 Tyler Durden