With the Federal Reserve meeting this week, we got to thinking about what playwrights call “Second Act problems”. Act One introduces the characters, lays out the challenges they face, and makes the audience care about both. Act Three provides resolution, with comedies ending “happily ever after” and tragedies with death and despair.

Acts one and three are pretty straightforward in terms of the Fed’s current narrative: March – May’s COVID Crisis was Act One and Act Three will be the eventual normalization of monetary policy.

But Act Two is much harder to write, as Pulitzer Prize winner David Mamet once described: it is “not the beginning and not the end, (it is) the time in which the artist and the protagonist doubt themselves and wish the journey had never begun.” It is also filled with “quotidian, mechanical and ordinary drudgery”. Act Two, in other words, is real life.

A few examples of the real-world problems in the Fed’s Act Two:

#1: Wednesday will see the release of the latest Summary of Economic Projections (SEP), the FOMC’s estimates of future economic conditions:

June’s SEP showed a mean estimate of 9.3% unemployment and 1.0% core PCE inflation.

The average unemployment rate for 2020 YTD is 8.2% and recent months show a steady trendline lower from the April’s 14.7% peak.

Core PCE has been trending higher, with May-June-July at 1.0%, 1.1% and 1.2% respectively.

Takeaway: the new SEP will likely see an upgrade of the FOMC’s economic projections, forcing the Fed to defend its still highly accommodative policy stance. Separately, our personal opinion is that the Fed will stop issuing SEPs in December 2020. In the August 27th update to its “Statement on Longer-Run Goals and Monetary Policy Strategy”, the section which previously mentioned the SEP was deleted and there is no longer any reference to it (see links below).

#2: What is the current state of the US economy, exactly; is it still accelerating off the bottom or stalled?

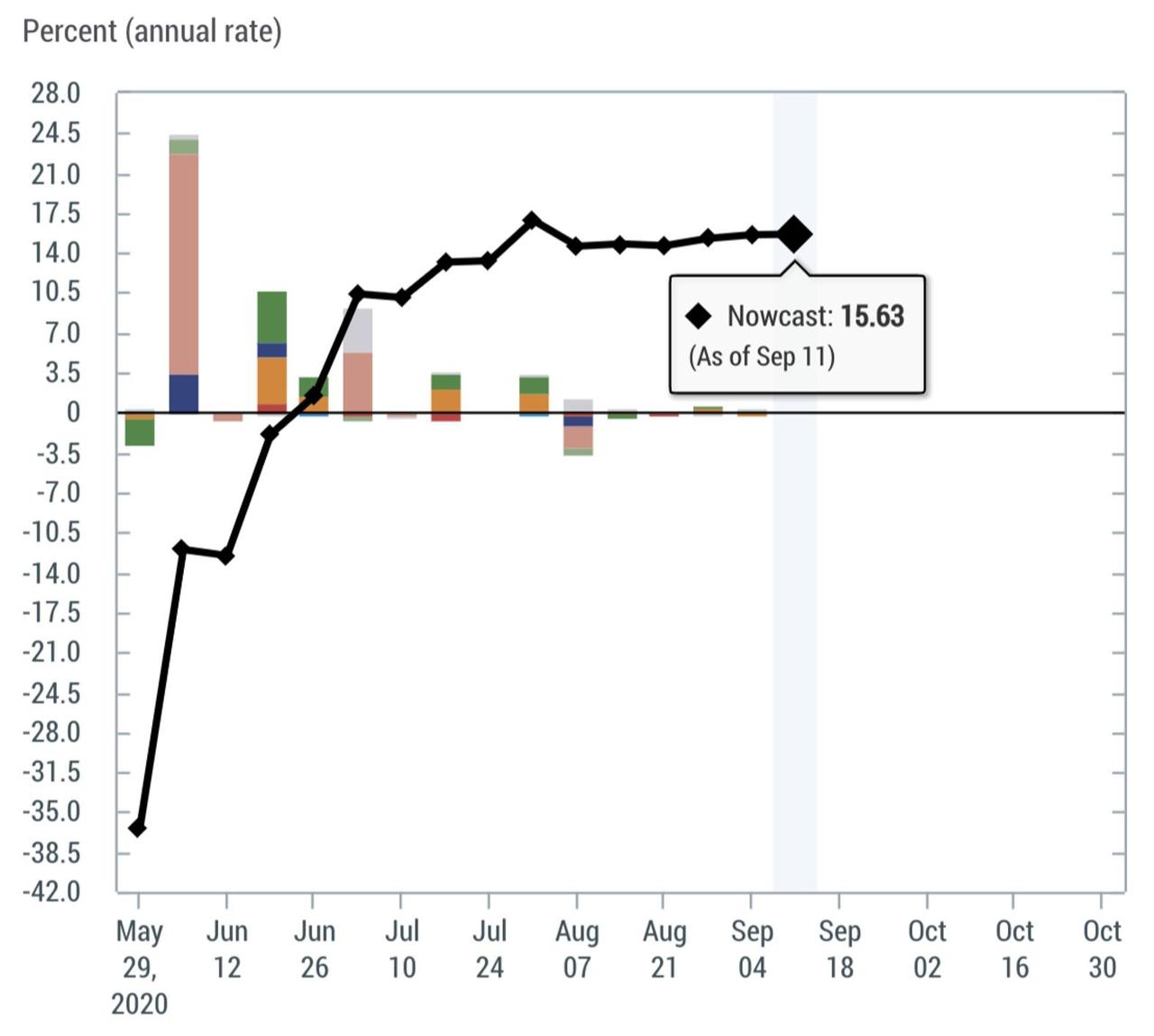

The New York Fed’s Nowcast model for Q3 says “stalled”, at 15.6% growth relative to Q2:

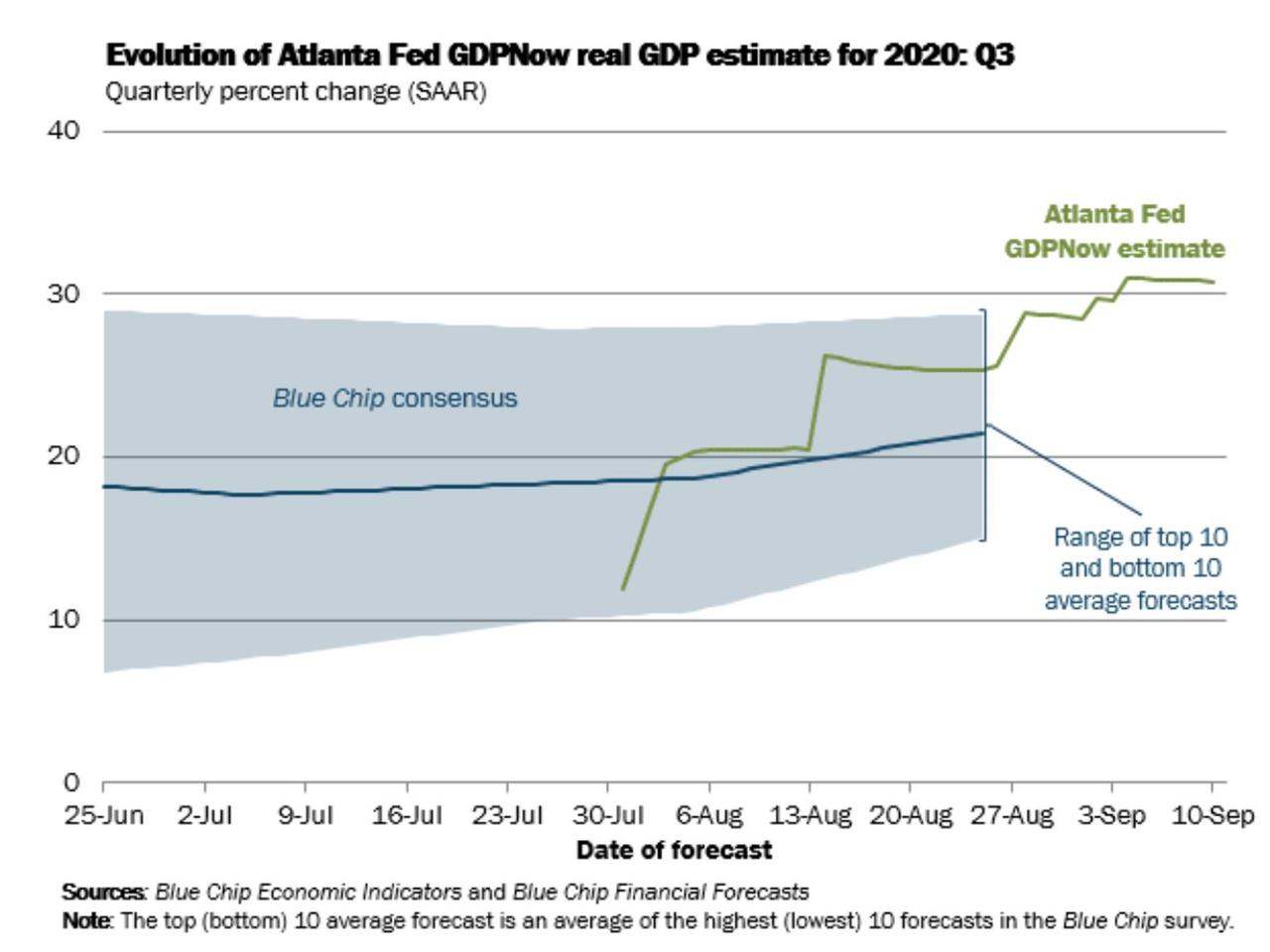

And the Atlanta Fed’s GDPNow model agrees (at least based on September’s data), but is looking for 30.8% GDP growth versus about 20% from blue chip economists:

Takeaway: this is a classic Act Two problem, dealing with the real-world issues of how ongoing COVID-related economic constraints limit future economic improvement. The NY Fed’s Weekly Economic Index is slightly more positive on recent economic trends (link at the end of this section) but is a relatively new indicator so we’ll take its more constructive message with a grain of salt for now.

#3: How FOMC decisions affect stock prices, the real-world problem that matters most to us. Since we’re 2 days away from an FOMC decision, it’s worth reviewing “The Pre-FOMC Announcement Drift”, aka the “Fed Drift”.

In a 2011 paper, New York Fed economists showed that from 1994 to 2011 almost all the S&P 500’s returns came in the 3 days around an FOMC decision. Over this period the index rose by 270%, and most of those gains happened the before, the day of, and the day after a Fed meeting.

Updating this analysis in 2018, the same researchers found that the Fed Drift now only applied to FOMC meetings where the Chair held a press conference and the FOMC issued a new SEP. (Link below for the full analysis)

Takeaway: first and most obviously, the revised Fed Drift says we should rally this week with Wednesday’s meeting conclusion and new SEP and today’s move higher may well be algorithmic front-running of that phenomenon. Second, if we are right that the Fed will retire the Summary of Economic Projections in 2021, then we will have a new chapter of the Fed Drift to consider.

Summing up the Fed’s “Second Act problem” with three investment takeaways:

#1: The pace of the current US economic recovery is too slow and uncertain for the Federal Reserve to meaningfully alter its policy stance any time soon. Yes, it has slowed its net asset purchases to zero since June (see chart link below) but these would certainly return if the US economy slowed and financial conditions began to deteriorate again. As for policy rates, those will be locked near zero for at least a year according to Fed Funds Futures and 2-year yields.

#2: Real (world) rates will continue to support high equity valuations. Ten-year TIPS, for example, currently yield -1.0% and the implied inflation breakeven is 1.6%, right where it was pre-COVID. Why own a 10-year Treasury at an all-time worst negative real return when the S&P 500 yields 1.5% and offers the chance of rising payouts over time?

#3: The Fed knows its Third Act (normalizing policy) has to wait until the Second Act comes to a natural conclusion.

Bottom line: with fiscal stimulus likely off the table through the November elections, the Fed knows it is alone in carrying the Act Two narrative forward for now. That should be a good backdrop for US equities through year end.

U.S equity futures and European stocks rose as investors awaited the decision of the Federal Reserve’s policy meeting later Wednesday and the August retail sales report which was expected to show a modest growth slowdown. Treasuries were steady and the dollar slipped.

After a modest dip early in the session following news that Facebook is facing an antitrust lawsuit by the FTC as early as late this year, S&P futures rebounded and hit a session high of 3,418.25 before paring gains to a 0.3% rise, as investors hoped for a renewed dovish pledge by the Federal Reserve to keep interest rates low for a prolonged period, with upbeat quarterly results from FedEx also boosting sentiment. After dropping for two weeks in a row, the S&P 500 has rebounded 1.8% in the past two sessions, with defensive sectors including real estate and utilities among the biggest gainers.

FedEx soared 10% in premarket trading after reporting a bigger-than-expected quarterly profit, helped in part by price hikes and lower fuel costs. Shares in peer UPS gained 4.6%, while Robinhood darling Kodak soared over 50% after an internal legal review cleared the company of option trade improprieties. Apple rose 0.7%, after ending the previous session just marginally higher, as it rolled out a new virtual fitness service and a bundle of all its subscriptions, Apple One. Other tech-related stocks including Alphabet, Amazon.com, Tesla and Microsoft all gained between 0.6% and 1.0%.

Investors have been looking for catalysts to take markets higher after an impressive global recovery sputtered in the first half of September, with some hoping that Powell will deliver more Kool-aid by boosting its dovish stance after adopting a more relaxed approach on inflation last month. That’s helping to shore up sentiment in the face of risks ranging from U.S. presidential elections and the prospect of a no-deal Brexit.

“Central banks are far from out of ammunition,” Mark Haefele, chief investment officer at UBS Global Wealth Management, wrote in a note to clients. “Investors should be positioned for the upside in equities.”

“The Fed may follow up by announcing some new easing steps in accordance with its new regime, though the general market consensus seems to be that it will adopt a wait and watch approach,” said Lee Hardman, a strategist at MUFG in London.

The Fed’s two-day meeting is its first under a newly adopted framework that promises to shoot for inflation above 2% to make up for periods where it is running below that target, in other words not to raise rates for a long, long time. The FOMC will release its policy statement and economic projections at 2 p.m. ET followed by Fed Chair Jerome Powell’s virtual news briefing half an hour later.

On the covid front, overnight President Trump said a vaccine shot for the coronavirus could be ready within four weeks. Separately, China’s top bio-safety scientist said one may be available for public use as early as November or December.

European stocks rose for a fourth day as Zara-owner Inditex posted a quarterly profit, although UK blue-chip stocks came under pressure after a surge in the previous session. The STOXX 600 index inched 0.3% higher, extending on its winning streak. Inditex said current trade showed a progressive return to normality with online sales growing sharply and store sales recovering, pushing its shares 6.3% higher, and helping lift the Stoxx retail sector 1.1%. Meanwhile, London’s FTSE100 was dragged lower by a weakness in the banking sector. A bright spot in the market was a 26.4% surge in shares of the Hut Group, the first major British initial public offering in seven years. Swiss plumbing materials company Geberit rose 1% after saying it would buy back shares worth up to 500 million Swiss francs ($551 million) over two years. Sweden’s Handelsbanken rose 2.6% after revealing plans to close almost half of its branches and cut about 1,000 jobs over the next two years.

Signs of compromise emerged on the Brexit front, with Reuters reporting that Britain offered tentative concessions on fisheries in trade talks with the European Union last week, just as London was threatening to breach the terms of its divorce deal with the bloc.

“The only catalyst that I can see for European equities is Brexit that could push markets one way or the other,” said Julien Lafargue, head of equity strategy at Barclays Private Bank. “Europe, in our mind, is a trading market. You want to buy Europe when everybody hates it, you want to sell it when everybody loves it. At this stage, we’re at a neutral.”

Earlier in the session, Asian stocks also gained, led by health care and communications. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Taiwan’s Taiex Index rising, and Jakarta Composite and Shanghai Composite falling. The Topix gained 0.2%, with Shin Nippon Bio and Marusan Securities rising the most. The Shanghai Composite Index retreated 0.4%, with Zhenjiang New Energy and Beijing Dahao Technology posting the biggest slides.

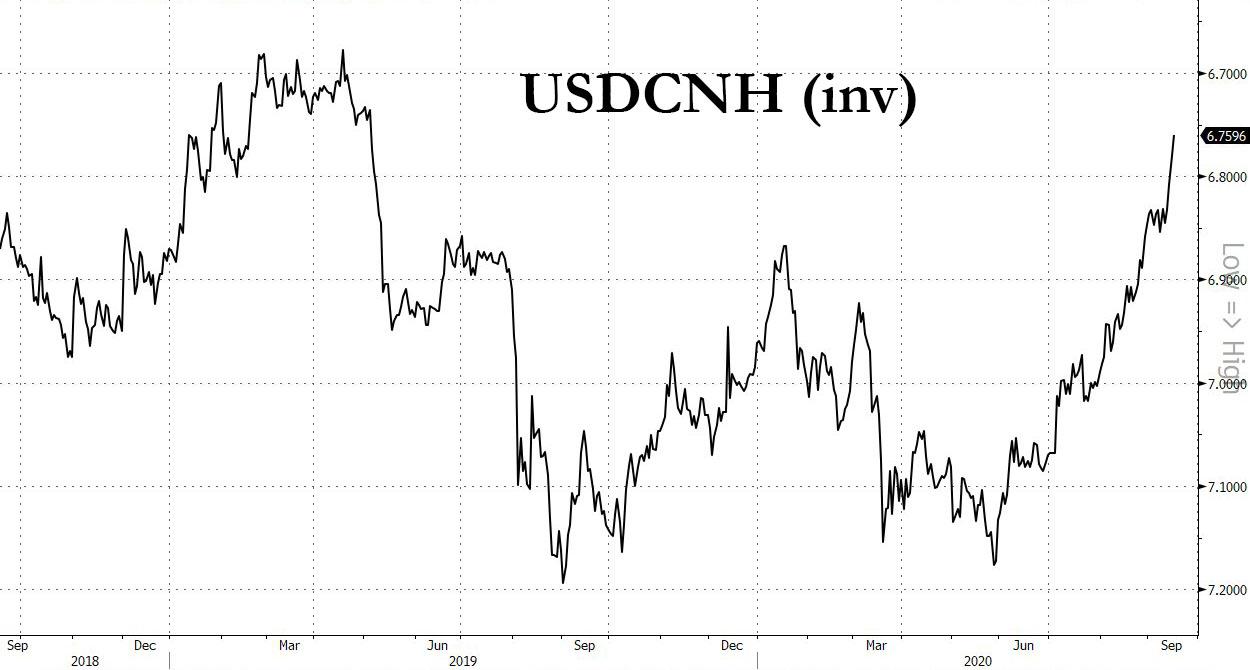

In FX, the U.S. dollar fell across the board on Wednesday as expectations grew that the U.S. central bank may hint at more policy action, while the Chinese yuan vaulted to its highest level since May 2019. The Bloomberg Dollar Index extended its longest losing streak in a month with a fourth consecutive day of declines after China’s central bank raised the daily reference rate for the nation’s currency and amid a continued rally in risk assets. Investors have turned bullish on China, with the prospects for the world’s No. 2 economy improving on the back of strong retail sales and industrial output data. In offshore trade, the Chinese currency, which is on track for four straight months of gains, notched a fresh 16-month high, hitting 6.7536 per dollar. “People are starting to embrace a new theme, which is that China is managing much, much better than anyone else,” said Davis Hall, head of capital markets in Asia at Indosuez Wealth Management.

“The dollar got sold on last 3 FOMC (Federal Open Market Committee) days so we continue with that pattern today”, noted Kenneth Broux, a strategist at Societe Generale. Trading could, however, easily and quickly shift soon after the statement, Commerzbank foreign exchange analyst Antje Praefcke warned via Reuters.

The Japanese yen also made significant gains during the session and touched levels not seen since the end of July, briefly going under 105 per dollar. The euro rose 0.27% to $1.1852. Sterling reversed earlier losses and rose 0.6% to $1.2995 in what would be its biggest daily rise in 2-1/2 weeks before a meeting of the Bank of England on Thursday, when policymakers may strike a downbeat assessment for the struggling economy.

In commodities, crude oil rose above $39 a barrel following a surprise drop in U.S. crude stockpiles. Gold continued trading in a narrow range, last seen at $1,963/oz.

In addition to the Fed’s decision, investors are also awaiting retail sales data for August, due at 8:30 a.m. ET, with expectations of a reading of 1.0% compared with July’s figures of 1.2%.

Market Snapshot

S&P 500 futures up 0.3% to 3,410

STOXX Europe 600 up 0.3% to 372.19

MXAP up 0.5% to 174.35

MXAPJ up 0.6% to 573.76

Nikkei up 0.09% to 23,475.53

Topix up 0.2% to 1,644.35

Hang Seng Index down 0.03% to 24,725.63

Shanghai Composite down 0.4% to 3,283.92

Sensex up 0.5% to 39,239.04

Australia S&P/ASX 200 up 1% to 5,956.13

Kospi down 0.3% to 2,435.92

Brent Futures up 2.6% to $41.57/bbl

Gold spot up 0.7% to $1,967.52

U.S. Dollar Index down 0.1% to 92.94

German 10Y yield fell 0.2 bps to -0.481%

Euro up 0.2% to $1.1867

Brent Futures up 2.6% to $41.57/bbl

Italian 10Y yield fell 2.2 bps to 0.793%

Spanish 10Y yield fell 1.0 bps to 0.261%

Top Overnight News from Bloomberg

Federal Reserve officials are expected to project rates staying near zero though 2023, reinforcing the message delivered by Powell in late August that they will delay tightening policy to achieve inflation that averages 2% over time

Coronavirus vaccines will be ready for public use as early as November or December in China, a top scientist said, which would make the country one of the first in the world with an inoculation

The U.K. inflation rate fell to the lowest since 2015 last month, driven by government tax cuts and other stimulus designed to dig the economy out of the depth of the coronavirus crisis

Bank of England officials are expected to lay the groundwork this week for yet more monetary stimulus as optimism over the U.K.’s economic rebound from the coronavirus pandemic fizzles out

The European Union’s executive proposed toughening the bloc’s emissions targets in a move that’ll force industry to face stricter pollution standards. The bloc willsell 225 billion euros ($267 billion) of green bonds as part of its landmark recovery fund, a watershed moment for an expanding market

Japan’s parliament formally elected ruling party stalwart Yoshihide Suga — the 71-year-old son of a strawberry farmer — to be the country’s first new prime minister in almost eight years

Boris Johnson has held talks with rebels in the U.K.’s ruling Conservative Party in an attempt to win their backing for his controversial law rewriting part of the Brexit deal he struck with the European Union last year

A quick look at world markets courtesy of NewsSquawk

Asian equity markets traded mixed and only partially benefitted from the tech-led gains in US, with the region tentative heading into the upcoming flurry of central bank announcements beginning with the FOMC later today. ASX 200 (+1.0%) and Nikkei 225 (+0.1%) were positive with Australia buoyed as the tech and telecoms sectors found inspiration from the outperformance of their counterparts stateside, while the advances in Japan have been tempered by a firmer currency and mixed data which showed a surprise Trade Surplus and narrower than expected contraction to Exports, although Exports were still at a substantial decline and Imports missed to suggest a weak consumer profile. In addition, participants await incoming PM Suga’s inauguration and the conclusion of the BoJ’s 2-day policy meeting which kicks off today. Conversely, Hang Seng (U/C) and Shanghai Comp. (-0.4%) lagged after a neutral PBoC liquidity operation and ongoing US-China tensions following the WTO ruling that US tariffs on China violated trade rules, as the US have spoken against the WTO announcement and President Trump suggested he may do something about the WTO following the ruling, while it was also reported the US is to announce charges related to Chinese hacking and blacklisted a Chinese developer in Cambodia, amid allegations they built facilities on land seized from locals which could be used to host military assets. Finally, 10yr JGBs were flat with price action stuck near the 152.00 resistance level and amid the indecisive risk tone, while participants were also tentative as the BoJ begins its 2-day policy meeting.

Top Asian News

Japan’s Parliament Elects Yoshihide Suga as New Prime Minister

Singapore to Pay Citizens for Keeping Healthy With Apple Watch

Digital Money Thefts Deal Setback to Japan’s Cashless Drive

Stocks Rally to Revive Indian IPOs in Worst Year Since 2016

European cash bourses eke mild gains (Euro Stoxx 50 +0.1%) alongside US equity futures (ES +0.4%, NQ +0.4%, YM +0.4%) amidst a relatively light session thus far in terms of news flow, and in the run up the FOMC policy decision later today. Cash bourses are mostly higher with the exception of the FTSEs (FTSE 100 -0.1%, FTSE MIB -0.2%) whilst broad-based gains are experienced throughout the rest of the region. UK’s FTSE sees a number of large-cap mining names consolidating after yesterday’s firm performance. Sectors across Europe are mostly higher with no real risk profile to be derived. The retail sector leads the charge, with the likes of Inditex (+7.5%) and Salvatore Ferragamo (+8.9%) propping up the sector post-earnings, whilst the IT sector coat-tails on the Wall Street sector performance yesterday. In terms of individual movers, Lufthansa (-1.6%) share remain pressured as sources said the group could cut its fleet by 130 planes and cut further jobs, altogether equating to around 28k vs. Prev. indicated 26k, while separate reports said the Co. has cut its year-end flights guidance. Meanwhile, the main shareholders of Caixabank (+0.3%) and Bankia (+2.3%) have given the green light for a merger, with a meeting reportedly called for tomorrow to approve to approve the terms, according to sources.

Top European News

THG Shares Soar After $2.4 Billion IPO to Ride Online Boom

Sweden’s Biggest Bank Says Cost Cuts to Hit 1,000 Employees

Hitachi Abandons U.K. Nuclear Power Project in Blow to Industry

VW Follows Daimler in Making Green-Bond Debut for Electric Cars

In FX, it is hardly a surprise to see the Dollar mostly rangebound and the index recoil to its confines around the 93.000 axis that has been pivotal for a while, as many if not most currency market participants keep positions light in the run up to the FOMC. However, US retail sales data looms before the big event and often possesses the potential to surprise given a wide spread of forecasts either side of consensus for the headline number and key control group GDP component. For now, the DXY is holding within a 92.852-93.189 band as major counterparts largely respect recent support, resistance and round number or psychological levels.

AUD/NZD/NOK – Marginal outperformers on a combination of factors, including strength in underlying commodities and crude, while the Aussie has piggy-backed yet another firm PBoC CNY fix and the Kiwi is underpinned by better than expected Q2 current account balances and the NZ Government upgrading its 2020 GDP and unemployment rate projections. Aud/Usd and Nzd/Usd are consolidating above 0.7300 and 0.6700 respectively, as Eur/Nok retreats from close to 10.7200 through 10.6500.

JPY/EUR – Also firmer vs the Greenback, but the Yen and Euro are still waning ahead of 105.00 and 1.1900 amidst more decent option expiry interest, between 105.25-15 in Usd/Jpy (1.4 bn) and 1.1835-25 in Eur/Usd (1.1 bn), with the latter also wary about ECB insinuations regarding the strength of the single currency. Back to the Yen, next up the BoJ and in the interim mixed Japanese trade metrics and Suga approved by the lower house as new PM.

GBP/CHF/CAD/SEK – The Pound appears top heavy again above 1.2900 against the Buck and 0.9200 in Euro cross terms as the Brexit implications of the IMB continue to hamper Sterling in addition to formidable technical hurdles in Cable from 1.2933 to 1.2935 (200 WMA/Fib and 55 DMA) and some pre-BoE caution. Elsewhere, the Franc remains stuck in a 0.9100-0.9050 rut, like the Loonie between 1.3200-1.3150 awaiting independent direction from Canadian CPI and the Swedish Krona within 10.4320-10.4035 vs the Euro in wake of Sweden’s ESV fiscal watchdog revising its GDP forecast for this year to show less contraction than envisaged in June, as per other state and private entities.

EM – Apart from the ongoing appreciation of the Yuan and gains fuelled by the depressed Dollar/oil price rebound, pretty mundane midweek session trade awaiting Fed policy pronouncements, guidance, the SEP and chair Powell’s press conference. However, the Lira is still struggling to pare declines from record lows under threat of EU sanctions following a warning from the EP that a resolution to that effect will be on Thursday’s agenda.

In commodities, WTI and Brent front month futures are continuing the grind higher seen during the APAC session as the complex is underpinned by the large surprise drawdown in Private crude inventories (-9.5mln bbls vs. Exp. +1.3mln bbls) alongside developments in the Gulf of Mexico. Hurricane Sally has been upgraded to a Category 2 hurricane as it makes landfall, with the latest update noting that historic and life-threatening flooding is likely through Wednesday along and just inland of the Florida Panhandle. The BSEE estimated Hurricane Sally cut 26.9% of US gulf offshore oil production (prev. 21.4%) and Nat Gas shut off in the region is seen at 28.0% (prev. 25.3%), whilst refining activity is also closely watched due to its vulnerability to flooding, and as just under 54% of US capacity sits in PADD III in the Gulf Coast. Meanwhile, the JMMC gears up to meet tomorrow, with eyes on any commentary regarding oil prices and market outlook. Sources last week said the recent price decline has caused concern in Riyadh, however, not enough to induce panic, and Saudi is planning to keep production steady. “We are likely to see the group once again put pressure on those who are still producing above their quota levels to comply”, ING predicts, with reports also noting that OPEC+ compliance in August stood at 101%. Looking ahead, the weekly EIA crude stocks will be released at the usual time, with the headline expected to show a build of 1.271mln bbls. Elsewhere, precious metals benefit from the softer USD, with spot gold extending gains above USD 1950/oz having had tested the level to the downside in overnight trade. Spot silver holds its head above USD 27.00/oz after printing a base at USD 27.02/oz – with eyes turning to the FOMC decision. In terms of base metals, LME copper erased earlier losses with the aid of a weaker Dollar, whilst Dalian iron ore futures fell overnight amid falling steel margins in China dampening the demand outlook for the base metal.

US Event Calendar

8:30am: Retail Sales Advance MoM, est. 1.0%, prior 1.2%

Retail Sales Ex Auto MoM, est. 1.0%, prior 1.9%

Retail Sales Control Group, est. 0.3%, prior 1.4%

10am: Business Inventories, est. 0.1%, prior -1.1%

10am: NAHB Housing Market Index, est. 78, prior 78

2pm: FOMC Rate Decision

4pm: Net Long-term TIC Flows, prior $113.0b; Total Net TIC Flows, prior $67.9b deficit

DB’s Jim Reid concludes the overnight wrap

Striking a chord today will be the Fed, who’ll be making their latest monetary policy announcement later. This is the FOMC’s first meeting since they released their revised Statement on Longer-Run Goals and Monetary Policy Strategy at Jackson Hole, in which they announced the move to a flexible average inflation target, thus allowing inflation to overshoot 2% following a period in which it’s been below target. There was also a change to the wording around their maximum employment objective, now saying that policy will be informed by its “assessments of the shortfalls of employment from its maximum level.” Though the change in the strategy opened the door to adjustments in forward guidance and asset purchases at this meeting, the communications from the Fed since then have signalled a lack of urgency on delivering meaningful changes to the policy stance. As a result, our US economists don’t think there’ll be any changes to the Fed’s forward guidance on interest rates, but do see the FOMC reframing their asset purchases as being focused on providing accommodation, rather than aiding market functioning. This meeting will also feature the release of the quarterly Summary of Economic Projections, which they think should reflect a meaningful upgrade to the near-term growth and inflation forecasts. On the dot plot, they think there’ll be continued unanimous support on holding the policy rate steady through 2021, with a firm majority still seeing the policy rate at the zero lower bound in 2023. See their full preview here.

Risk assets saw a solid overall performance yesterday ahead of the Fed’s decision, though US markets gave up about half their gains late in the session while remaining up on the day. The S&P 500 finished +0.52% higher for its 3rd consecutive daily advance, but was up as much as +1.1% midday. Tech stocks outperformed again, with the NASDAQ up +1.21%. The market dip from the peaks came around midday NY time, about the same time as a story reported a lack of consensus on US fiscal stimulus – more on that below.

Europe earlier saw solid gains, as the STOXX 600 closed up +0.66%. Banks underperformed on both sides of the Atlantic though and were the worst industries in their respective indices, with the STOXX Banks index down -1.49%, and the S&P 500 banks industry group down -2.48%. Meanwhile oil prices rebounded, with Brent Crude coming off its 3-month low thanks to a +2.32% advance – only the second daily gain in the last ten sessions.

Overnight one interesting story is that the US Federal Trade Commission, which has been investigating Facebook for more than a year over whether the social media giant has harmed competition, could file a case by the end of the year. The news report added however that no final decision has been made on this. Facebook is down -1.86% in overnight trading. Meanwhile, yesterday a Senate Judiciary panel laid out a case for how Google has used its dominance in search and digital advertising to benefit its products and harm competition. This comes ahead of preparations by the Justice Department to sue Google in coming weeks. This is all coming at a time when only 1 in 3 Americans are holding a positive view of Big Tech, as was highlighted by Apjit Walia from my team in a research piece earlier this month. He thinks they’ll come in for increased scrutiny post the election.

Asian markets are largely trading up outside of the Hang Seng (-0.24%) and Shanghai Comp (-0.24%) this morning. The Nikkei (+0.12%), Kospi (+0.27%) and Asx (+1.0%) are all higher along with S&P futures (+0.21%). In FX, the onshore Chinese yuan is up a further +0.15% to 6.7728. Brent crude oil prices are up +1.68% to $41.21. As we go to print, Yoshihide Suga has been elected Japan’s new prime minister by the lower house.

There hasn’t been a great deal of new news on the coronavirus over the last 24 hours, though we did hear from President Trump, who said in a Fox & Friends interview yesterday that “We’re going to have a vaccine in a matter of weeks”. He has doubled down overnight saying that the one would be ready within 3 to 4 weeks. This is going to be an interesting dynamic given there are just seven weeks to the election. The President’s interview came just prior to reports that researchers monitoring the Pfizer vaccine have reported no safety issues after 12,000 patients received a second of two doses. Staying on a vaccine, we also heard from the head of Germany’s vaccine regulator that the first approvals could be granted at the end of this year or early next year. Our latest Exit Strategy Tracker contains the latest on vaccine developments so please see it here.

In terms of case numbers, Western Europe remains a source of concern, with the entire Irish cabinet going into self-isolation yesterday after their Health Minister Donnelly had been tested. Dublin has closed all bars that do not serve food and has asked residents to not have visitors from more than one home come to their house. Elsewhere, both Spain and the UK’s case numbers remained above 3,000, and in Italy a further 1,229 were reported. Here in the UK, the government acknowledged the strain in the country’s testing ability with Health Secretary Hancock telling the House of Commons, “we have seen a sharp rise in the numbers coming forward for a test… we will be able to solve this problem in a matter of weeks.” In the US there were over 50,000 new cases yesterday compared to 26,000 new cases last Tuesday. Summer virus hot spots continue to cool off though, with California and the Houston-area of Texas posting their lowest positivity rates on data going back to April. Elsewhere, confirmed cases in India have reached the 5 million mark as the country is now topping 90k new cases almost on a daily basis. Furthermore, as per Bloomberg, the official counts of confirmed cases and deaths are marred by underreporting and inadequate testing.

While we will hear about any changes to the US monetary policy in a few hours, don’t hold your breath when it comes to fiscal. Congressional leaders met again yesterday to discuss. A follow on stimulus bill has been discussed since July with both parties remaining quite far apart. Yesterday, we heard from White house advisor and the President’s son-in-law Jared Kushner that an agreement may not come until after the election, while Speaker Pelosi threatened to keep the House in session until another fiscal deal is done. Lawmakers in the House are currently expected to recess on 2 October in order to campaign ahead of the 3 November elections. A bipartisan group of 50 lawmakers in the House put a $1.5 trillion bill on the floor that aimed at being a middle ground for both parties with elements of both parties’ original salvos, however leading members in both parties have already said it was both not enough and too much respectively. The concern continues to be that the proximity to the election is causing an apparent lack of political incentive of either side to act.

While this was going on, Sovereign bonds had a mixed performance yesterday ahead of the Fed, with 10yr Treasury yields up +0.7bps, having closed within a 4bps range over the last week. Bund yields were also up but just +0.1bps, though gilts underperformed once again, as 10yr yields rose +2.3bps. Over in commodities, platinum had another strong performance, rising +1.62% for a 5th straight session, while copper fell -0.11% as it came down from its 2-year high the previous day.

Looking at yesterday’s data, US industrial production rose by a below-consensus +0.4% in August (vs. +1.0% expected), though July’s reading was revised up half a percentage point to +3.5%. Meanwhile capacity utilisation rose to 71.4% in August, which is noticeably higher than the 64.1% in April, but still down from the 76.9% back in February. We also got the Empire State manufacturing survey, which rose to 17.0 (vs. 6.9 expected). Here in the UK, the unemployment rate in the 3 months to July rose to 4.1% as expected, which is the first time the jobless rate has been above 4% since October 2018. In addition, the more up-to-date estimates for August 2020 from Pay As You Earn Real Time Information showed the number of payroll employees was down by -695k (or -2.4%) compared with March 2020. Finally, the ZEW survey from Germany showed investor expectations rose to 77.4 in September (vs. 69.5 expected).

To the day ahead now, and the aforementioned Federal Reserve decision will be the highlight of the day for investors. This morning there’s also European Commission President Ursula von der Leyen’s State of the Union address. Otherwise, we’ll also hear from the ECB’s Hernandez de Cos and Holzmann, and can expect a monetary policy decision from the Brazilian central bank. Data releases from Europe include UK CPI for August and the Euro Area trade balance for July, while the US releases include August retail sales and the September NAHB housing market index.

via ZeroHedge News https://ift.tt/33Cfwcj Tyler Durden

Boeing Put Profits Before People’s Lives By Hiding 737 MAX Design Flaws, Congress Finds Tyler Durden

Wed, 09/16/2020 – 06:53

18 months after Ethiopian Airlines Flight 302 plummeted out of the sky just minutes after takeoff last March, Congressional investigators have finally released a comprehensive report outlining the many mistakes made both by Boeing and the FAA during the certification process.

In the months that have passed, investigators have kept the pressure on Boeing (and its share price) with a steady stream of leaks. We’ve already seen emails showing Boeing engineers criticizing the 737 MAX 8 design time in some of the harshest terms imaginable (at one point, one irate engineer complained that “the plane was designed by clowns, who were supervised by monkeys”.

Production pressures that jeopardized the safety of the flying public. There was tremendous financial pressure on Boeing and the 737 MAX program to compete with Airbus’ new A320neo aircraft. Among other things, this pressure resulted in extensive efforts to cut costs, maintain the 737 MAX program schedule, and avoid slowing the 737 MAX production line.

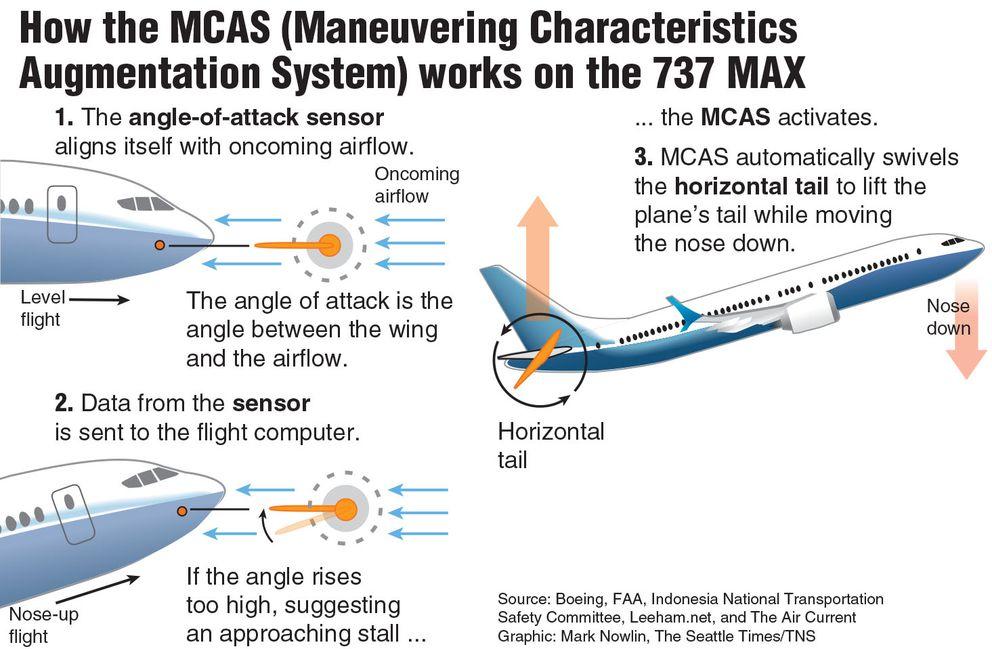

Faulty Design and Performance Assumptions. Boeing made fundamentally faulty assumptions about critical technologies on the 737 MAX, most notably with MCAS, the software designed to automatically push the airplane’s nose down in certain conditions. Boeing also expected that pilots, who were largely unaware that MCAS existed, would be able to mitigate any potential malfunction.

Culture of Concealment. Boeing withheld crucial information from the FAA, its customers, and 737 MAX pilots, including internal test data that revealed it took a Boeing test pilot more than 10 seconds to diagnose and respond to uncommanded MCAS activation in a flight simulator, a condition the pilot described as “catastrophic.” Federal guidelines assume pilots will respond to this condition within four seconds.

Conflicted Representation. The FAA’s current oversight structure with respect to Boeing creates inherent conflicts of interest that have jeopardized the safety of the flying public. The report documents multiple instances in which Boeing employees who have been authorized to perform work on behalf of the FAA failed to alert the FAA to potential safety and/or certification issues.

Boeing’s Influence Over the FAA’s Oversight Structure. Multiple career FAA officials have documented examples where FAA management overruled a determination of the FAA’s own technical experts at the behest of Boeing. These examples are consistent with results of a recent draft FAA employee “safety culture” survey that showed many FAA employees believed its senior leaders are more concerned with helping industry achieve its goals and are not held accountable for safety-related decisions.

All these flaws eventually led to the “preventable deaths” of 346 passengers. Boeing repeatedly dismissed warnings and complaints from employees related to MCAS, which was created to compensate for a redesign of the plane’s interior to create more space for passengers. One of the flaws was that MCAS relied on a single sensor, which was prone to feeding faulty information.

Why did Boeing need MCAS? Because, as the NYT explains, the engines on the Max are larger and placed higher than on its predecessor, so they could cause the jet’s nose to push upward in some circumstances. MCAS was designed to push the nose back down. In both crashes, the software was activated by faulty sensors, effectively forcing the plane’s nose down repeatedly, eventually forcing them into a fatal nosedive.

What’s more, Boeing successfully lobbied the FAA to avoid classifying the new software as “safety critical”, meaning that the company didn’t need to update pilots on how it worked. Some pilots reportedly weren’t even aware the software existed before the crashes. Boeing deliberately concealed test data showing that if a pilot took longer than 10 seconds to realize that MCAS had kicked in accidentally, the results would be “catastrophic”. Boeing knew all that before the twin crashes that shut down the program…and the company still did nothing. The company also deliberately concealed faulty alerts that would have warned pilots about problems with the sensor used to trigger MCAS.

In a statement, DeFazio blamed Boeing for kowtowing to Wall Street pressure, and putting profits before people’s lives.

“Our report lays out disturbing revelations about how Boeing—under pressure to compete with Airbus and deliver profits for Wall Street—escaped scrutiny from the FAA, withheld critical information from pilots, and ultimately put planes into service that killed 346 innocent people. What’s particularly infuriating is how Boeing and FAA both gambled with public safety in the critical time period between the two crashes,” Chair DeFazio said. “On behalf of the families of the victims of both crashes, as well as anyone who steps on a plane expecting to arrive at their destination safely, we are making this report public to put a spotlight not only on the broken safety culture at Boeing but also the gaps in the regulatory system at the FAA that allowed this fatally-flawed plane into service. Critically, our report gives Congress a roadmap on the steps we must take to reinforce aviation safety and regulatory transparency, increase Federal oversight, and improve corporate accountability to help ensure the story of the Boeing 737 MAX is never, ever repeated.”

Rep Rick Larson added that the report, combined with separate findings from regulators in Indonesia and Ethiopia, would help paint a more complete picture of what led to the crash.

One of the most egregious decisions made by Boeing was opposing a requirement that pilots receive simulator training to fly the plane. If pilots needed to be retrained, Boeing would have had to eat some of the cost out of its end of the deal, according to an NYT report. This focus on cost-cutting “drove a lot of really bad decisions,” DeFazio said.

The Democrats on the committee also accused Boeing of putting a priority on profits by strongly opposing a requirement that pilots receive simulator training to fly the plane. Under a 2011 contract with Southwest Airlines, for example, Boeing promised to discount each of the 200 planes in the airline’s order by $1 million if the F.A.A. ended up requiring simulator training for pilots moving from an earlier version of the aircraft, the 737NG, to the Max.

“That drove a whole lot of really bad decisions internally in Boeing, and the F.A.A. did not pick up on these things,” Mr. DeFazio said.

The report alleges that the ‘time pressure’ imposed on the 737 MAX project was unusually intense. Keith Leverkuhn, former Boeing VP and General Manager of the MAX program, allegedly kept “a countdown clock” in a conference room, which he allegedly described as an “excitement generator”.

“One of the mantras that we had was the value of a day,” he said, “and making sure that we were being prudent with our time, that we were being thorough, but yet, that there was a schedule that needed to be met…” one Boeing worker said.

Back in 2012, in order to lower development costs, Boeing reduced the work hours involved in the MAX’s avionics regression testing by 2,000 hours. It also examined other reductions to save costs, including a reduction to flight test support by 3,000 hours.

Boeing doesn’t shoulder the blame alone. According to the report, the FAA “failed to ensure the safety of the traveling public” as “excessive” outsourcing had “impaired [the FAA] from acting independently.”

The report comes as regulators are reportedly close to finally lifting the grounding order by approving the newly redesigned MAX; the expectation is that the plane might be back in service before the end of the year.

In addition to the report, Congress has introduced legislation that would toughen the agency’s certification process, in part by requiring that it carry out regular independent audits on company-employed representatives.

Responding to the allegations in the report, the FAA said it “is committed to continually advancing aviation safety and looks forward to working with the committee to implement improvements identified in its report.” Boeing, meanwhile, said it had learned lesson. “Boeing cooperated fully and extensively with the committee’s inquiry since it began in early 2019. We have been hard at work strengthening our safety culture and rebuilding trust with our customers, regulators and the flying public.”

But like we’ve learned from Sweden’s approach to the pandemic: Just because people have the option of doing something, doesn’t mean they will. The 737 MAX 8 has such negative associations, that President Trump suggested Boeing rename the plane, and the company has been quietly working on a rebranding effort.

After failing to ring up even a single order for the MAX in 2020, Boeing finally celebrated a small order from Enter Air, a Polish charter airline, a few weeks ago. However, recent reports about alleged design flaws with the aerospace giant’s 787 Dreamliner, and other Boeing planes, could create lingering problems for shares even after the 737 MAX is back in the skies.

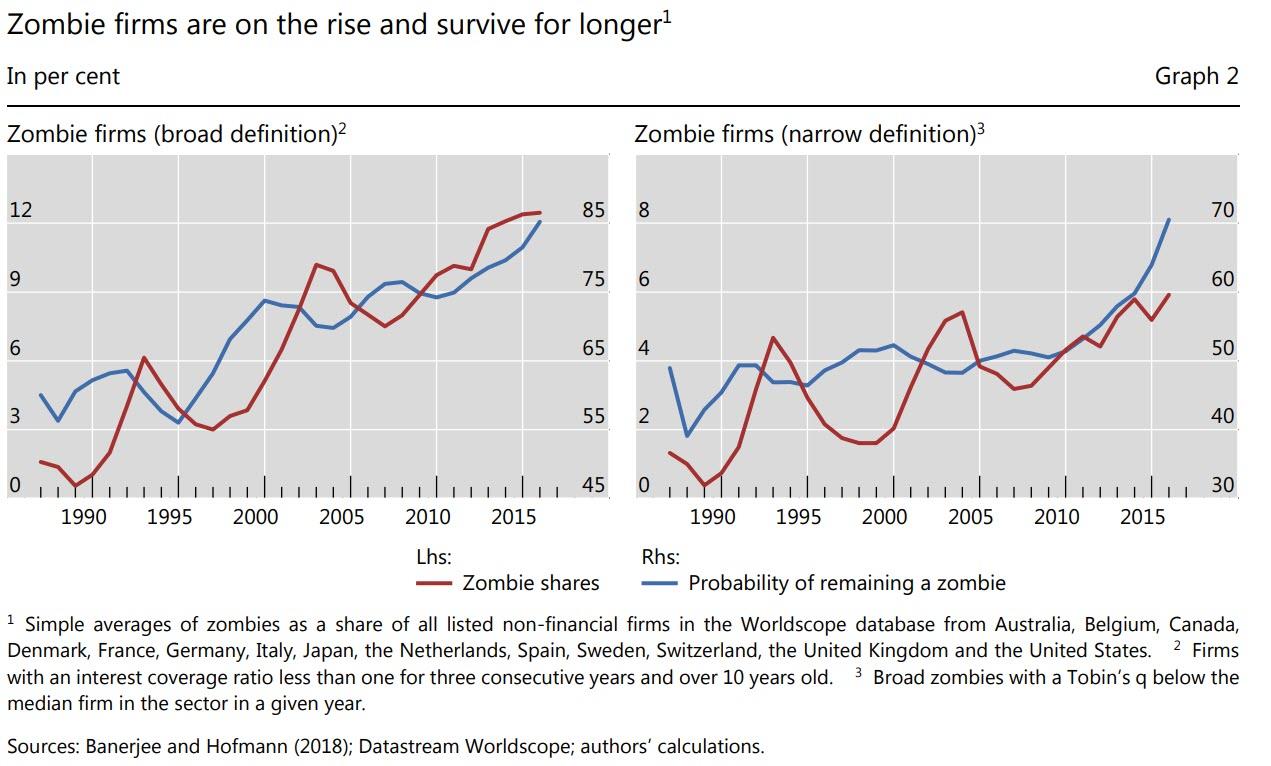

Europe’s zombie firms are multiplying like never before…

In Germany, one of the few European economies that has weathered the virus crisis reasonably well, an estimated 550,000 firms – roughly one-sixth of the total – could already be classified as “zombies”, according to research by the credit agency Creditreform. It’s a similar story in Switzerland.

Zombie firms are over-leveraged, high-risk companies with a business model that is not remotely self-sustaining, since they need to constantly raise fresh money from new creditors to pay off existing creditors. According to the Bank for International Settlements’ definition, they are unable to cover debt servicing costs with their EBIT (earnings before interest and taxes) over an extended period.

The number of zombie companies has been rising across Europe and the Anglosphere – due to of two main factors:

Central banks’ easy money forever policies, which brought interest rates down to such low levels that even firms with a reasonable chance of default have been able to continue issuing debt at serviceable rates. Many large zombie firms have also been bailed out, in some cases more than once. Spanish green energy giant Abengoa has been bailed out three times in five years.

The tendency of poorly capitalized banks to continually roll over or restructure bad loans. This is particularly prevalent in parts of the Eurozone where banks are especially weak, such as Italy.

A Bank of America report from July posits that the UK accounts for a staggering one third of all zombie companies in Europe. They represent 20% of all companies in the U.K, up four percentage points since March, according to a new paper by the conservative think tank Onward. In the two hardest-hit sectors — accommodation and food services, and arts, entertainment and recreation — the proportion of zombie firms has soared by 9 and 11 percentage points respectively, to 23% and 26%.

The number of zombie firms has shot up as companies have taken on huge volumes of fresh debt merely to weather the virus crisis while, in many cases, generating a lot less in revenues. Across the globe, non-investment grade companies issued $322 billion in the first eight months of this year — as much as in the whole of 2019, according to BIS data. At the same time, companies that were already zombies, instead of entering bankruptcy and having their debts restructured, have been bailed out by government and/or the central bank.

For their part, smaller companies have also taken on more bank loans, largely or completely backed by government. Many firms, particularly in the sectors most affected by the crisis, have lower revenues and weaker cash flow. As a result, the borrowed cash gets used up quickly but the debt remains. If they weren’t zombies before the Pandemic, they’ll be zombies going forward.

What is to be done with all these zombies? That’s the question many are now asking. The report by Onward proposes a cunning plan (in the Baldrick vein) — called New Start — that would convert any coronavirus debt that can’t be paid back into an income contingent loan collected as a share of trading profits. The debt would come due only when a company begins turning a profit.

“The New Start scheme gives the option to intelligently delay repayments only for those firms who need it,” says the study’s author Angus Groom. “This can be rolled out as a scheme managed by HM Treasury and implemented and controlled by banks — all the while maximizing taxpayer value for loans that the Government has already underwritten.”

The term “scheme” in British English in this context means “program,” but the USian meaning of “scheme” seems to be at least equally appropriate. And taxpayers will likely never see those funds again.

This is one of a number of proposals doing the rounds in Europe aimed at finding a way of keeping most, if not all, of Europe’s zombies upright, for as long as possible. They include a straight “state debt for equity” swap, which would essentially involve governments converting the emergency loans taken out by struggling companies into equity. This idea is particularly popular among senior bankers, such as Unicredit CEO Jean Paul Mustier, presumably because the unpayable coronavirus debt companies owe the banks would also be turned into equity.

“It is a win-win all around,” says City of London grandee Lord Leigh of Hurley: “Taking equity stakes in borrower-SMEs would provide those businesses with interest-free liquidity, leaving their growth potential unimpeded, whilst correspondingly giving banks the opportunity to recoup more of the money they have committed in the medium to long term.”

Former UK Chancellor George Osborne has proposed another solution: just forgive all small business coronavirus debt. As with most of the proposals, the plan is couched in terms of exclusively saving small companies. If past is prologue, it’s the larger ones — the ones that owe the banks millions or billions — they’re most interested in saving.

“None of these options are ‘uncontroversial’ and each involves varying degrees of moral hazard, taxpayer loss and engineering complexity,”says Groom. “However our solemn conclusion is that some form of action is unavoidable.”

Up to now, many — though not all — of the short-term rescue interventions by governments or central banks can be justified in some way or another, particularly if they support the unemployed and unlock credit that had frozen up even for healthy companies. But it’s quite another thing when the short-term rescue efforts become a long-term reality that helps to engender more and more new zombies as well as make preexisting zombies even bigger.

There are plenty of reasons why filling the economy with ever larger numbers of zombie firms is not a good idea. For a start, zombie firms are less productive and crowd out investment in more productive firms. Researchers at the BIS found that each one percentage point increase in the prevalence of zombie firms means 0.25 percentage points slower employment growth and a 17% decline in the capital investment rate.

Allowing zombie firms to proliferate in order to protect banks from the consequences of their bad lending practices and investors from the consequences of their bad investment choices doesn’t just reward — and by extension, incentivize — bad actions and decisions; it stores up bigger problems for the future.

Eight People In Indonesia Caught Not Wearing Masks Punished By Having To Dig Graves Of COVID Victims Tyler Durden

Wed, 09/16/2020 – 04:15

In a headline that could soon wind up coming out of the U.S. if Joe Biden is elected President, eight people in Indonesia were forced to dig the graves of coronavirus victims as penance for not wearing their masks when leaving their homes.

The punishment is supposed to act as a “deterrent” for others to not violate Covid-19 guidelines, according to the Evening Standard.

The persons suspected of breaking the rules were caught leaving their homes without masks and, as a result, were ordered to dig graves at a public cemetery in Ngabetan village, according to the report. The offenders were asked to dig the graves in groups of two, but weren’t asked to attend the ensuing funeral services.

“There are only three available grave diggers at the moment, so I thought I might as well put these people to work for them. Hopefully this can create a deterrent effect against violations,” Cerme district head Suyono said.

This follows Anies Baswedan, Governor of Jakarta, issuing new restrictions that don’t expire until September 27 to combat the capital’s outbreak. Crowds on main streets have thinned out since the implementation of the new rules, which were put in place because medical facilities were once again reaching “unsafe levels”.

Seven of the 67 Covid referral facilities in Jakarta are 100% occupied and 46 of them are more than 60% occupied.

More than 54,000 of Indonesia’s 218,000 Covid cases are in Jakarta.

via ZeroHedge News https://ift.tt/33AoB5g Tyler Durden

British citizens made their feelings known after the Policing Minister suggested that people should spy on their friends and neighbours and report them to the authorities if they see them breaking Covid rules.

Minister Kit Malthouse’s idea was compared to the East German Stasi by many, after he encouraged reporting neighbours gathering in more than groups of six, saying it was a viable option.

“There is obviously the non-emergency number that people can ring to report issues, if they wish to,” the minister told the BBC Radio 4’s ‘Today’ show. “If people are concerned, if they do think there’s a contravention, then that option is open to them.”

Encouraging people to snoop on neighbours and report each other to the authorities is like communist East Germany. It’s un-British. https://t.co/a19qkmIByM

Britain moves a step closer to being a surveillance state. This goes beyond Britain’s traditional curtain twitchers. Echoes of East Germany’s Stasi? #coronavirushttps://t.co/j52GVg5IO0

Probably not enough discussion about what‘a happening to our national psychology re Covid and certainly potential effects of being asked to police each other.

The beginning of the week saw the so called ‘rule of six’ brought into force overnight and with little fanfare in England. It literally bans social gatherings of more than six people if they’re not from the same household.

Those who are found to be contravening the law face fines of between £100 and £3,200, while anyone found to be hosting a house party faces a £10,000 punishment.

Former British Supreme Court Justice Lord Jonathan Sumption denounced the new regulations as “unenforceable,” noting that the only way the plan would work is if a “Stasi-style” network of “snoopers and informers” is formed.

Metropolitan Police Federation chair Ken Marsh was critical of Malthouse, suggesting that the minister must think “we have an endless supply of officers who can just go out to these things.”

“It will be hundreds and hundreds of calls coming in from curtain-twitchers,” Marsh stressed.

Former Conservative party leader Iain Duncan Smith also noted that “calling on people to spy on each other is not a particularly good situation to be in”.

Earlier in the year, police forces in parts of the UK set up hotlines to allow people to snitch on those who were not abiding by social distancing rules.

In European countries such as Spain and Italy, the government has also encouraged people to snitch on social distancing rule breakers.

Pompeo Vows US Will Never Let Iran Acquire Russian & Chinese Weapons Tyler Durden

Wed, 09/16/2020 – 02:45

Weeks ago the United States lost its bid to get the UN Security Council to extend the international arms embargo on Iran, which is set to expire October 18.

And now on Tuesday Secretary of State Mike Pompeo is vowing tonever let Iran acquire Chinese and Russian weapons, but it remains unclear precisely how he hopes to make this happen.

Pompeo said during an interview with European radio broadcaster “France Inter” on Tuesday that “Nothing has been done so far to enable the extension of this ban, and therefore the United States assumed its responsibilities.” He’s of course referencing the fact that the Europeans have by and large sought to uphold the terms of the 2015 nuclear deal, or JCPOA.

Russian anti-air defense systems, file image via Tehran Times.

“We will act in this manner. We will prevent Iran from acquiring Chinese tanks and Russian air defense systems, and after that, selling weapons to Hezbollah undermines the efforts of French President Emmanuel Macron in Lebanon.”

Washington has stood isolated over its decision to enact so-called “snapback” sanctions on the Islamic Republic in late August.

Ironically the snapback option is available to participants in the JCPOA, which the US formally withdrew from in May 2018.

#Видео Расчеты С-400 Западного военного округа провели боевые пуски зенитных управляемых ракет по учебным воздушным целям на полигоне Ашулук в Астраханской области.

Meanwhile, over the past year there’s been talk of Moscow actually supplying Iran with its advanced S-400 anti-air defense system, something which the Trump administration might almost treat as an act of war.

Interestingly, on the very day Pompeo made is new statements vowing to never let Russian weapons come into Iran’s hands, the Kremlin was busy show off the S-400’s capabilities.

…caused over so many years. Any attack by Iran, in any form, against the United States will be met with an attack on Iran that will be 1,000 times greater in magnitude!

Iran has also come back into headlines this week after it was alleged leaders in Tehran are plotting to assassinate the US ambassador to South Africa in revenge for the January US drone strike on Gen. Qasem Soleimani.

In response, Trump vowed that any such aggression out of Iran would be met with an American response “1,000 times greater in magnitude!” However, Trump did not exactly confirm the alleged plot, instead he merely cited “press reports” suggesting that it may be true.

via ZeroHedge News https://ift.tt/32x5r0Y Tyler Durden

The Government has no legal right to impose the severe and miserable restrictions on our lives with which it has wrecked the economy, brought needless grief to the bereaved and the lonely and destroyed our personal liberty.

This is the verdict of one of the most distinguished lawyers in the country, the retired Supreme Court Judge Lord Sumption.

He said last week in a podcast interview: ‘I don’t myself believe that the Act confers on the Government the powers that it has purported to exercise.’

Lord Sumption’s intervention is, of course, so huge and important that the media of this country have somehow not noticed it. So, as has been the case from the start, you have to get it from me.

He was referring to the Public Health Act of 1984, the basis for almost all the sheaves of increasingly hysterical decrees against normal life which the Health Secretary Matt Hancock has issued since March. I promise you that it is not usual for a retired senior judge to use such language in public.

This 1984 Act was drawn up mainly to give local magistrates the power to quarantine the sick.

Nothing in it remotely justifies these astonishing moves – house arrest, travel restrictions, harsh limits on visiting family members, interference with funerals and weddings, closure of churches, compulsory muzzles, bans on assembly and protest.

English law just does not allow an Act of Parliament to be stretched so far.

Lord Sumption was referring to the Public Health Act of 1984, the basis for almost all the sheaves of increasingly hysterical decrees against normal life which the Health Secretary Matt Hancock (above) has issued since March. I promise you that it is not usual for a retired senior judge to use such language in public.

Magistrates are never given such powers. It is a principle of our law that fundamental freedoms cannot be invaded or overruled unless the law specifically allows it.

As he is one of the most distinguished legal minds of our time, Jonathan Sumption’s opinions on this matter are surely important.

Let us hope that the Courts of England, which have so far been content to let the Government do what it likes, will listen to what he says when they look at the matter again later this month, in the case brought by Simon Dolan, a businessman who is seeking a judicial review of the Government’s policy on Covid-19.

It is extraordinary for such a person as Lord Sumption to go public in this fashion. And he went on to say another astonishing thing.

He pointed out that powers do exist – in the shape of the formidable Civil Contingencies Act – under which the Prime Minister could do all the things he has done. But the CCA requires regular parliamentary scrutiny and renewal.

The Government’s team of lawyers must know this. So why wasn’t the CCA used? We can only guess that the Prime Minister and his Health Secretary feared that if they had to keep coming back to Parliament, even the dim, slumbering and gullible MPs we have nowadays would eventually have spotted, and halted, the immense power grab now under way.

Lord Sumption’s intervention is, of course, so huge and important that the media of this country have somehow not noticed it.

So, as has been the case from the start, you have to get it from me. But believe me, it is an indication of just how deep into the swamp of despotism this Government has already waded.

Let us escape soon, before we are so far in we can never get out again.

Bare-faced state bullies

The most terrible warning of what lies ahead of us – if we cannot smash the Government’s lies – is in Melbourne, Australia, where a vain little despot called Daniel Andrews has locked his subjects in their homes, banned demonstrations against this policy, and unleashed heavy-handed police against protesters and dissenters.

At this rate, Melbourne will soon be twinned with Minsk, capital of Belarus. The treatment of protesters on the streets of both cities is remarkably similar. I was most struck by what happened to a young woman demonstrator at the hands of Melbourne police, after they had grabbed and restrained her, so that she was powerless.

An officer actually put a covering over her mouth. It was not the only such incident that day and it explains, to those who object, why I call these things muzzles.

They are there to humiliate, to cancel individuality and to indicate assent – forced or otherwise – to the crazy policy of trying to treat a virus with naked state power.

If US police forced handcuffed Left-wing protesters to wear Trumpoid ‘Make America Great Again’ baseball caps it would be about the same.

Humiliation: Police officers in Melbourne, Australia, restrain a protester and force her to wear a face mask

Now hiking’s a crime, but dope is fine

One of my rules is that the more political the police become, the more useless they are against actual crime. Here is a good example. Police who have over the past few months pursued sunbathers, hikers, people going into their own front gardens or showing their naked faces on trains, now plan a new extra-soft line on marijuana.

Even though this terrible drug is increasingly linked with lifelong mental illness and violence, liberal police chiefs are still lost in a Sixties-style haze of dope, believing dubious claims that it is a medicine.

Legalisers have long privately admitted these claims are a red herring to give pot a good name. How can something which makes many of its users mentally ill be a medicine?

But lo, police chiefs are backing a new ‘cannabis card’ that will provide de-facto decriminalisation of the drug for millions of people with health conditions. Officers, who have already almost given up arresting people for possession, say it will give them a new excuse for failing to enforce the law.

Too busy on granny patrol, making sure children can’t see their grandmothers, I expect.

Schoolboy Johnson’s lies keep getting bigger

Imagine a naughty schoolboy afraid to admit what started as a minor misdeed. Such a schoolboy, having broken the headmaster’s window with his catapult, and trying to evade punishment, might invent a story about a gang of yobs bursting into the school grounds.

So the police are called and he deepens the falsehood. The longer it goes on, the more embarrassing it will be to confess. Innocent people are rounded up, arrested and charged on the basis of his claims.

He gives false evidence against them. They lose their freedom, perhaps have their lives ruined.

Rather than admit he hugely overestimated the danger of Covid, he continues to insist it is a deadly plague and that it will be back soon in a terrible second wave

The lie is now even worse. He must either confess or elaborate the false story of the gang, for ever. And the worse it gets, the harder it is to own up. So he lies and keeps lying.

So it is with our Prime Minister. He panicked in March, on the basis of poor advice. He did immense damage and knows it.

But rather than admit he hugely overestimated the danger of Covid, he continues to insist it is a deadly plague and that it will be back soon in a terrible second wave.

The official Covid death and hospitalisation figures, declining ever since April 8, are now bumping along the bottom of the graph, close to zero.

Hence the false epidemic of so-called Covid ‘cases’, which the Government is trying to pretend exists. How simple-minded do you need to be not to see the great flaw in this?

On Monday, the media reported new coronavirus cases in the UK had risen to 2,988 on Sunday, the highest daily total since May. Panic! Or perhaps not.

I searched the Government’s own spreadsheets and what did I find? More than 1.1 million tests each week but fewer than 10,000 positive results. Judging by the state of the hospitals and the death rates, I think we may assume most were just fine, as most who catch this disease are.

So, for this, we propose to stop people gathering in groups of more than six? I sense even those who have, up till now, put up with this rubbish are beginning to tire of it.

Good, for until you do and demand truthful explanations of why your children’s education has been ruined, why legions of people will lose their jobs, why daily life is an intensifying misery of jobsworths and bureaucracy, and why hundreds of businesses built up with years of sweat and risk are now dying, you will just get more lies.

via ZeroHedge News https://ift.tt/3iNRTnD Tyler Durden

If you say “September 11” most people automatically think of the attacks on the World Trade Center buildings and the Pentagon on September 11, 2001. What they probably don’t even remember happened on September 11, were the attacks on the United States Consulate in Benghazi, Libya, in 2012.

Once the Libyan Revolution began in February 2011, the CIA began placing assets in the region, attempting to make contacts within the region. Ambassador J. Christopher Stevens, whose name and image would soon become synonymous with the Benghazi attacks, was the first liaison between the United States and the rebels. The task before the American intelligence community at that time was securing arms in the country, most notably shoulder-fired missiles, taken from the Libyan military.

Eastern Libya and Benghazi were the primary focal points of intelligence-gathering in the country. But there was something else at work here: The CIA was using the country as a base to funnel weapons to anti-Assad forces in Syria, as well as their alleged diplomatic mission.

Early Rumblings of Disorder in Benghazi

Trouble started in April 2012. This was when two former security guards of the consulate threw an IED over the fence. No casualties were reported, but another bomb was thrown at a convoy just four days later. Soon after, in May, the office of the International Red Cross in Benghazi was attacked and the local al-Qaeda affiliate claimed responsibility. On August 6, the Red Cross suspended operations in Libya.

This was all part of a troubling escalation of violence in the region. The British Ambassador Dominic Asquith was the victim of an assassination attempt on June 10, 2012. As a result of this and of rocket attacks on convoys, the British withdrew their entire consular staff from Libya in late June of that year.

American military and consular personnel on the scene were increasingly troubled by the situation and communicated their concerns to top brass through official channels. Two security guards in the consulate noticed a Libyan police officer (or at least someone dressed as one) taking pictures of the building, which raised alarms. Indeed, consular officials had been requesting additional security as far back as March.

On June 6, 2012, a large hole was blown in the wall of the consulate gate. It was estimated that 40 men could go through the hole in the wall. In July, the State Department informed officials on the ground that the existing security contract would not be renewed. On August 2, Ambassador Stephens requested additional security detail. The State Department responded by completely removing his security detail three days later. Three days after this, his security detail had left Libya entirely. On August 16, the regional security officer warned then-Secretary of State Hillary Clinton that the security situation in Libya was “dire.”

The Day of the Attack on Benghazi: The Cover-Up Begins

The September 11, 2012 attack was actually two attacks by two separate militias. The first was the attack on the diplomatic mission, the second was a mortar attack on the CIA annex. But the attacks themselves were effectively watched in real time by the White House, thanks to security drones in the region. By 5:10pm ET, President Barack Obama, Vice President Joe Biden and Secretary of Defense Leon Panetta were watching real-time footage via a drone deployed to the area.

Half an hour later, the State Department officially refused to deploy the Foreign Emergency Support Team (FEST). FEST exists specifically for rapid response to terrorist attacks around the world and have special training with regard to defending American embassies. Within three hours, an Islamic group in the region had claimed responsibility for the attack. Approximately six hours after the first shots were fired, two former Navy SEALs who constituted the only serious defense forces for the consulate were killed by enemy fire. The surveillance drone had been watching them fight on their own for over two hours.

At 10:30 that night, Hillary Clinton nebulously blamed “inflammatory material on the Internet” for the attack. The notion that the attack was motivated by Innocence of Muslims was absurd: On the day before the attack, the leader of al-Qaeda in the region called for vengeance due to the death of his secretary. Three days after the attack, Stephens’ personal diary was found unsecured, along with all the other sensitive intelligence information in the compound.

For days, the film was blamed despite the White House having full knowledge that it was a terrorist attack. Indeed, on September 14, Barack Obama promised the father of one of the slain Navy SEALs not that he would bring to justice those who planned the attack, but the man who made the movie.

On September 20, 2012, the White House spent $70,000 on apology videos for the film. One day later, ten days after the attack, Clinton admitted to the public what she had known for over a week: That this was a coordinated terrorist attack. However, on the 25th, President Barack Obama addressed the United Nations once again blaming the video, giving what is perhaps one of the more memorable quotes of his presidency: “The future must not belong to those who slander the Prophet of Islam.”

On September 27, 2012, Nakoula Basseley Nakoula was arrested in Los Angeles for parole violations, all of which were related to his production of the film and served a year in jail. He was later sentenced to death in absentia by the Egyptian government.

Barack Obama did not attend his daily intelligence briefing for six consecutive days prior to the attacks, instead campaigning for re-election against Mitt Romney.

Susan Rice, then acting as the United States Ambassador to the United Nations, made the rounds on no fewer than five major Sunday morning talk shows, a process known as “the Full Ginsburg.” On these shows, she was armed with a set of talking points from the CIA. These talking points included the false assertion that these were spontaneous protests inspired by similar protests against the American Embassy in Cairo, with no connection to institutional terrorism.

The Rice appearances and the talking points she was provided with further confirm a general pattern: The Obama Administration was fundamentally incapable of acknowledging who the real enemy was. And when things went wrong, the focus was not on setting them right to protect Americans in the future, but on protecting the image of the Obama Administration – most notably the President and the Secretary of State. Hence the blame was shifted from Islamic terrorist groups onto a YouTube video.

The (Seemingly Endless) Benghazi Investigations

There were no fewer than 10 investigations of the attack on Benghazi, none of which found evidence of wrongdoing, despite several of them having been run by Republicans.

However, the American public did get some valuable information out of these hearings, not least of all that Hillary Clinton doesn’t value the lives of American servicemen. For example, the attention of Hillary Clinton’s deleted emails first came to the State Department and the United States Congress thanks to these investigations. Indeed, approximately 30 of the “gone with the wind” emails from her private, home-brewed server related to the non-response to the attack on Benghazi. This is according to the State Department itself.

But still the question remains: Why let these men die? And why lie about it for days after the fact?

The answer lies in two political concerns: First, the re-election of Barack Obama, second the planned candidacy of Hillary Clinton.

The date of the attack is very important: This was the final weeks of a presidential election campaign. And while Obama won handily (in no small part due to the aloof, patrician image of Bain Capital principal Mitt Romney), he is nothing if not a savvy politician. An attack on the United States Consulate in Libya was not something he wanted in public consciousness during an election season, not least of all if it were the result of a terrorist attack from what had formerly been a stable nation, slowly coming into the fold of what is euphemistically called “the International Community.”

For Clinton, the situation was even more dire. She effectively “owned” the situation in Libya, as the remaking (and ultimately destruction) of North Africa was one of the signature projects of her tenure at State. What’s more, she certainly owned the security situation on the ground, which likely was never secure.

The building was given the designation of “temporary,” largely to get around a number of regulations that apply to permanent State Department buildings. The request for more security from Ambassador Stephens might have been ill advised not because it was impossible to secure the location in any kind of long-term and sustainable way. The right move might very well have been to remove American personnel entirely, but this would have gone against the official narrative that everything was going swimmingly in Libya.

Other countries and organizations (such as the Red Cross) were leaving because they could not protect their people. The Clinton State Department saw this as unthinkable, because it would represent a failure and contradict the narrative.

And while Republican-led committees did not find any wrongdoing, it’s important to note that they also complained of being stonewalled by the administration at every turn. It’s hard to uncover evidence of wrongdoing when there is an institutional campaign to prevent you from getting any evidence at all.

A number of whistleblowers and other sources show that there were additional forces ready to go in the region to defend the consulate. So why were none of them deployed? Why were four American lives lost due to inaction at the highest levels of government?

Why no one was deployed is perhaps down more to incompetence and bad policy than any kind of a conspiracy. Our article on 9/11 is instructive on this matter: sometimes the cover-up is a conspiracy to conceal idiocy and failure of the actual event. In the case of Benghazi, while there is evidence to point toward a politically motivated cover-up, the actual event, like the 9/11 attacks, seems mostly to be a result of bad policy and incompetence rather than malice.

In this case, the bad policy was the Obama Administration’s desire to avoid even the appearance of “boots on the ground” and hand wringing about getting the permission of Libya (and about 12 other countries) to deploy assistance to the consulate. This was part of the general political philosophy of appeasement of Islamic terrorists that marked the Obama Administration.

This explains the stand-down orders which official sources have denied, but which have been confirmed by a number of whistleblowers and leaked documents since the attacks.

Both the President and the Secretary of Defense issued orders to deploy forces, but none were deployed. Once the Ambassador was confirmed as missing, a two-hour meeting ensued where top men within the Obama Administration came up with a number of action items, mostly revolving around the YouTube video (fully five of ten action items were related to the video) and hand wringing regarding a lack of permission from the Libyan government to protect our own forces.

The Americans in the CIA Annex were eventually evacuated to the airport by members of a militia comprised of former Qadaffi regime loyalists, not the opposition militias that were nominally allied with the United States. Meanwhile, actual American forces spent a bunch of time putting on and taking off their uniforms and tactical gear because the instructions from Washington changed by the minute.

It was a total paralysis of action on the ground by the top brass in D.C., because they were afraid of it looking like ground forces were being deployed, both from the perspective of the political response at home and the political response in Libya. As a result, four Americans died and a massive cover-up was rolled out to protect those responsible for grossly negligent inaction.

After the fact, emails were sent out, the purpose of which was less about finding out what went wrong to prevent it from happening again and to assign responsibility, than it was about making sure everyone was on the same page with regard to talking points.

The attack on Benghazi, the deaths of four Americans and the ensuing cover-up are an insightful view into the reality lurking behind many so-called “conspiracy theories.” What began as bureaucratic bungling and ideologically driven hamfistedness became a cover-up and, in a sense, a conspiracy after the fact. None of this is meant to let Obama-Clinton off the hook. Indeed, none of the criticisms of Obama-Clinton become any less sharp when they are considered as incompetence and butt-covering.

via ZeroHedge News https://ift.tt/2H6o5EH Tyler Durden

Trump Confesses He Wanted To Assassinate Syria’s Assad But Mattis Stopped Him Tyler Durden

Tue, 09/15/2020 – 23:25

In an extremely rare, if not absolutely unprecedented confession from a sitting American president, Trump stunned a news panel on Tuesday morning in saying he wanted to assassinate President Bashar al-Assad of Syria.

“I would’ve rather taken [Assad] out. I had it all set. Mattis didn’t want to do it,” Trump said in a wide-ranging interview with Fox & Friends.

“I would have rather taken him out” — Trump says he wanted to assassinate Bashar al-Assad, but Mattis stopped him pic.twitter.com/pUcFTSW2w9

The question has persisted over the past years of war in Syria after Bob Woodward first reported in 2018 that Trump was pursuing it.

At the time Trump had vehemently denied it: “No, that was never even contemplated, nor would it be contemplated and it should not have been written about in the book,” he had previously stated.

But Trump casually described Tuesday that in fact he was seriously considering it, only to be stopped by his Secretary of Defense at the time, Marine general Jim Mattis, which Trump added “was a highly overrated general”.

The Fox hosts quickly followed by asking whether Trump “regretted” not taking out Assad. Trump responded:

“No, I don’t regret that. I could have lived either way with that. I considered [Assad] certainly not a good person. But I had a shot to take him out if I wanted but Mattis was against it.”

The real quote from Woodward’s book regarding #Syria ‘s Assad is that @realDonaldTrump told Mattis:

However, considering the Russian military has been deeply entrenched in Syria since 2015, and as Putin vowed not to allow the West to complete its push for regime change, we wonder how exactly Trump “had a shot to take him out”.

Recall that Trump has bombed Syria on two occasions after allegations Assad used chemical weapons, with the 2018 attack involving over 100 tomahawk cruise missiles on Damascus. During the first instance, in April 2017, his daughter Ivanka reportedly influenced the decision.

NBC reported in April 2017: Donald Trump’s decision to bomb Syria was influenced by his daughter, Ivanka, being “heartbroken and outraged” at the country’s alleged chemical weapons attack, one of the president’s sons told a British newspaper.

Interesting that Trump wanted to assassinate Assad only to be advised against it and then reach out directly to Assad a few years later to discuss Austin Tice only to be rebuffed by the Syrian leader, crazy politics.

She reportedly showed her father pictures of suffering children while making the plea. Trump’s Syria policy has since then been all over the map – on the one hand he’s consistently voiced a desire to “bring the troops home” while more recently touting that “we’re securing the oil”.

via ZeroHedge News https://ift.tt/33vpjRf Tyler Durden

{kind=link}