Glenn Greenwald Shocks With Explanation On Why Mainstream Media Is Ignoring Assange Trial Tyler Durden

Sat, 09/19/2020 – 19:00

Well-known journalist Glenn Greenwald has once again sparked intense debate on the Left by refusing to conform to any level of group-think.

On Friday he mused about the ongoing Julian Assange extradition trial in London, offering an explanation as to why mainstream US media has seemingly dropped Assange from its radar, despite during the early years of the most bombshell WikiLeaks revelations working closely with Assange in terms of corroborating coverage.

It’s true that one reason that the Assange prosecution – despite its extreme dangers and consequences – is receiving so little media attention is that it doesn’t have a partisan angle.

But another is that many liberals believe their political adversaries deserve to be in prison. https://t.co/bViOmUAKDi

Greenwald started with a tweet acknowledging that Assange’s plight, which includes the possibility of being extradited to the United States where he faces certain life in prison, has received “little media attention” ultimately because it doesn’t have an easy partisan angle.

“But another is that many liberals believe their political adversaries deserve to be in prison,” Greenwald stated, going on the offensive.

And that’s where the most famous founding journalist at The Intercept began going off on liberals’ exaggeration of what Trump represents and how he came to power:

“If you start from the premise that Trump is a fascist dictator who has brought Nazi tyranny to the US, then it isn’t that irrational to believe that anyone who helped empower Trump (which is how they see Assange) deserves to be imprisoned, hence the lack of concern about it,” Greenwald said.

If you start from the premise that Trump is a fascist dictator who has brought Nazi tyranny to the US, then it isn’t that irrational to believe that anyone who helped empower Trump (which is how they see Assange) deserves to be imprisoned, hence the lack of concern about it.

Essentially Greenwald is saying, ‘no, Trump is not a Nazi’ — and this flawed belief will only compound errors when it comes to other pressing issues such as Assange’s fate.

Greenwald previously addressed the “authoritarian arguments” which claimed the WikiLeaks founder does not deserve journalistic protections.

One of the most dangerous and authoritarian arguments you’ll hear from those who support Trump DOJ’s attempt to imprison Assange is that it doesn’t endanger press freedoms because “Assange is not a journalist.” Leave side the huge stories he’s broken & journalism prizes he won… pic.twitter.com/J94n5E5tMO

Earlier this month President Trump shocked many national security state insiders by suggesting be might be open to pardoning Edward Snowden.

While the Assange case would no doubt be a much higher hurdle for Trump in terms of the ‘deep state’ fierce pushback that would be sure to follow any similar consideration, it remains a possibility, especially were to Trump take the White House again after November.

via ZeroHedge News https://ift.tt/3hFUZsk Tyler Durden

“I have given the deal my blessing, if they get it done that’s great, if they don’t that’s fine too,” President Trump told reporters at the White House on Saturday.

Of course, CFIUS still needs to technically sign off on the deal. But that’s not the only obstacle remaining in the way of a spinoff that company insiders say could lead to a US public offering roughly one year from now if everything works out.

Trump’s comments come after the Commerce Department on Friday issued regulations prohibiting American companies from providing downloads or updates for TikTok after 11:59 pm on Sunday. The order also applies to WeChat, another popular Chinese-owned messaging and payments app, that will be subjected to the ban – at least in the US market (the administration has promised that any restrictions won’t apply to American companies doing business in foreign markets like China).

In a statement, TikTok said its “proposal” to Washington included “unprecedented levels of transparency.”

During an earlier briefing on Friday, Trump called TikTok “a pretty incredible asset” and said that the companies appeared close to a deal that would ameliorate security concerns from a group of GOP senators.

If the deal is ultimately structured like a spinoff, regulators in Beijing will likely need to sign off as well, which could create problems. However, there’s been some talk about ByteDance selling TikTok without the content recommendation algorithm at its heart. Beijing has already confirmed, via a leak to the SCMP, that it won’t allow an American company to walk away with TikTok’s algorithm.

ByteDance has already sought help from American courts, arguing that President Trump’s ban was illegal under American law. Unfortunately for the company, invoking “national security” gives Trump broad latitude to act; the courts don’t have much latitude to restrain him, according to Bloomberg.

Following the Commerce Department’s latest order, the company filed another lawsuit late Friday seeking to stop the Commerce Department’s order forcing Apple and Alphabet to drop TikTok from their app stores. TikTok owner ByteDance said it dropped its lawsuit against the Trump Administration, which it filed in California, and filed a new lawsuit in Washington. The company argued that Trump’s ban is “political” in nature, and that Trump is only using national security as a ruse.

TikTok also claimed that the ban violates first amendment protections on free speech.

via ZeroHedge News https://ift.tt/3cdiNCN Tyler Durden

Nuclear Scenario For Markets Emerges In ‘Jaw-Dropping’ SCOTUS/Election Plot-Twist Tyler Durden

Sat, 09/19/2020 – 18:00

“If the script were being written, this would be the plot-twist that would drop jaws in the theater…”

That is the dramatic (and rightfully so) introduction to a tweet thread by Jake Sherman describing the potential playbook for the next few months as election campaigning and the SCOTUS-nomination-process mutate into what could potentially be a “nuclear option” for markets into year end… and the start of 2021.

Here are the highlights from Sherman’s view on the potentially cataclysmic events over the next few weeks:

45 DAYS before Election Day, the Notorious RBG — the left’s most-beloved and celebrated jurist — dies, and @senatemajldr, the left’s most-hated lawmaker who is also up for re-election, vows a floor vote on President DONALD TRUMP’S nominee to the Sup Court.

THE U.S. CAPITOL will be center stage over the next 15 weeks until the end of 2020, as the Congress considers this open Supreme Court seat.

THIS IS, QUITE LITERALLY, a mesh of MCCONNELL’S most animating interests: power and judicial nominees. The left frequently says that MCCONNELL is obsessed with power — and nothing but power. There is some truth to that — MCCONNELL is acutely aware of what is afforded to him by being the majority leader, and he says it quite frequently: He controls what comes up for a vote, and what doesn’t and when.

HE USES THAT POWER and that leverage with maximum impact. you should expect that here, w a chance to reshape the court for decades to come & a better than even chance of slipping into the minority, @senatemajldr will leverage every ounce of power afforded to him to fill this seat

MCCONNELL has made his promise plain:“President Trump’s nominee will receive a vote on the floor of the United States Senate.”

PAY ATTENTION TO WHAT MCCONNELL DOESN’T SAY: He doesn’t say when. Rushing the nomination could hurt some vulnerable senators. But it could also guarantee Republicans a Supreme Court seat. As WaPo’s put it:“[T]his is a rare moment where a congressional caucus leader’s short-term & long-term interests seriously diverge, his/her immediate interests vs legacy. Fascinating political power play ahead.”

HOW HE’S FRAMING IT TO HIS COLLEAGUES: MCCONNELL wrote GOP senators:“This is not the time to prematurely lock yourselves into a position you may later regret. … I urge you all to be cautious and keep your powder dry until we return to Washington.”

SO, EXPECT a nomination and hearings before the election, but not necessarily a vote.

IS IT POSSIBLE that he tries to squeeze a vote in before Election Day? Yes. Absolutely — especially if TRUMP demands it

IS IT POSSIBLE that he pushes the vote until after the election, both as a practical matter to help his vulnerable colleagues, and a motivating factor for his base? Yep. Absolutely.

IS IT POSSIBLE JOE BIDEN wins the presidency, Republicans lose the Senate and MCCONNELL jams through the nominee in the lame duck? Yes, you bet. Can Democrats do anything besides bellyache? No. They can’t.

Despite what you will hear from the left in the coming days, CHUCK SCHUMER’S power is exceedingly limited. Senate Dems have scheduled a 1 p.m. caucus call (h/t MARIANNE LEVINE) to discuss their options.

REMINDER:If MARK KELLY beats MARTHA MCSALLY in Arizona, he could be sworn in at the end of November, altering the tight majority that MCCONNELL has to work with. It would then be 52-48. This seems like a very live option.

YES, Lindsey Graham has said a number of times that Senate should not consider a nominee in the last year of a president’s term. He said it in 2016 during a Judiciary hearing. He said it to @JeffreyGoldberg in 2018 — if a nominee comes in TRUMP’S last term, he wanted to wait

DOES THAT MEAN, that GRAHAM – in a neck-in-neck race for re-election – will stay true to that? No. Absolutely not. In July, he appeared to walk back his 2018 comments in an interview with CNN’s Manu Raju:

Asked about his past opposition to moving a nominee in a presidential election year after the primary season, Graham said:

“After Kavanaugh, I have a different view of judges,” referencing the brutal 2018 confirmation process of Supreme Court Justice Brett Kavanaugh.

“I’d like to fill a vacancy. But we’d have to see. I don’t know how practical that would be,” Graham told CNN Monday. “Let’s see what the market would bear.”

YOU WILL HEAR A LOT OF REPUBLICANS say it’s dangerous to have a 4-4 court going into an election, but there was a 4-4 court going into the last election… There are a number of Republican senators to watch very closely in the coming days. They will get peppered with several questions: Should the SENATE wait until next year to confirm a nominee? And, would you vote no if MCCONNELL put it on the floor? Is a lame-duck vote appropriate?

While the script above is key, the punchline for markets is the all too real possibility of a deadlocked 4-4 SCOTUS vote deciding what may be the most contested election in US history should Republicans fail to gather the votes to fill the vacant supreme court seat before the election.

And sure enough, Republican Alaska Sen. Lisa Murkowski has already fired the proverbial first shot, confirming she would not vote to replace a Supreme Court justice until after the inauguration.

“When Republicans held off Merrick Garland because nine months prior to the election was too close, we needed to let the people decide,” Murkowski said in August, according to The Hill.

“And I agreed to do that. If we say now that months prior to the election is OK when nine months is not, that is a double standard and I don’t believe we should do it.”

Now where have we seen this before?

Murkowski’s statements echo that of Maine Sen. Susan Collins, a fellow moderate and the only other pro-choice Republican in the Senate.

“I think that’s too close, I really do,” Collins said when asked whether she would vote to confirm a Supreme Court justice in October. Collins also said that she would oppose seating a justice in the lame duck session of Congress if President Donald Trump loses the election in November.

Collins made her position official in a Saturday tweet saying the Senate should wait until after the election for the vote (although as some have noted, she doesn’t make any promises on how she would vote if/when a vote is called).

Add to this the outcome risk from the Mark Kelly vs Martha McSally special election in Arizona (where Kelly has a steady lead), and a 4-4 SCOTUS deciding the next president suddenly looks very real.

Simply put, the political quagmire unleashed by the passing of Ruth Bader Ginsburg leaves the market in an even more precarious position since if a contested election was a source of great uncertainty before, a 4-4 SCOTUS extends that uncertainty even further as we already know there will be no concessions for weeks, and the extensions of mail-in ballots will merely add fuel to the fire of what is shaping up as the most contested election in US history.

In short, this is the “worst case scenario” – that JPMorgan just warned about last week when envisioning a contested election’s impact on markets – on steroids, since The Fed has nothing new to offer and fiscal stimulus will definitely be off the table now until an election decision is made, a decision that may not comes for months without a SCOTUS tiebreaker vote.

Back in July, Goldman’s David Kostin wrote that one of the key concerns expressed by its clients is that a contested election could drag on, resulting in little clarity for weeks if not months, in a rerun of the contested 2000 election between Al Gore and George W. Bush, when it took a Supreme Court challenge and 34 days for the winner to be decided. This is what Goldman said then:

Health concerns and social distancing protocols suggest that more voters than ever will decide not to cast ballots at traditional polling stations on Election Day and instead vote by mail. In the case of a close election, it will take time to count – and invariably re-count – all the absentee and mail-in ballots. The deadline for each state to certify its result and finalize electors is December 8th (35 days after the election) or six days before the Electoral College convenes on December 14th (first Monday after the second Wednesday in December).

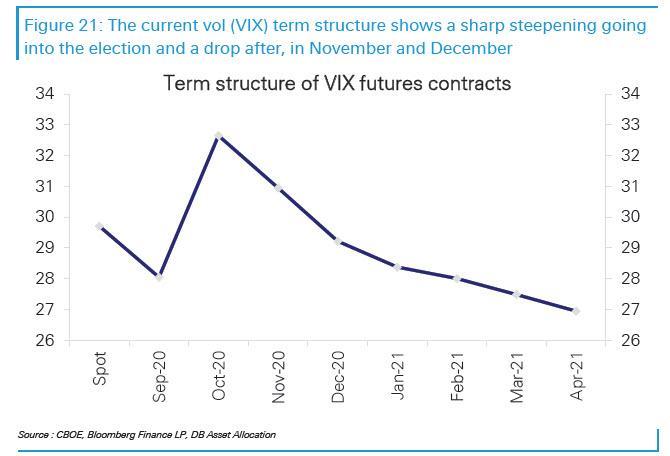

Echoing this, Deutsche Bank’s Parag Thatte wrote that the pricing of VIX futures with November and December expiries are likely too sanguine that there will be a quick and clear outcome of the elections.

Then last week, JPM’s chief equity strategist Misla Matejka joined this chorus of warnings about a contested election result, which he sees as the “worst-case scenario” for the market (Matejka also sees a contested election as the top risk for market performance into the year-end), adding that potential legislative paralysis could be “even more damaging” than Bush vs Gore for economy, as key stimulus measures to support economy could be delayed until well after the election:

The 2000 US presidential election between Bush and Gore provides a precedent for this. Equity markets struggled in the period following elections, with S&P500 dropping close to 12%.

Fast forward 20 years, when “in the current scenario,” JPM believes that “the potential legislative paralysis could be even more damaging for the economy, as key stimulus measures to support the economy might be delayed, and the partisanship is very elevated.”

Finally, the same point was underscored by Artemis Capital CIO who earlier today also wrote that “vol markets value the US election as a massive binary risk event that occurs at one point-in-time (like earnings in a stock)” However, “the real risk is a contested election and US constitutional crisis that occurs throughout time. If the latter comes to pass, forward vol is very mispriced.“

Vol markets value the US election as a massive binary risk event that occurs at one point-in-time (like earnings in a stock)

The real risk is a contested election and US constitutional crisis that occurs throughout time

If the latter comes to pass, forward vol is very mispriced

Putting all this into one chart, this is what the confusion and uncertainty heading into the election looked like before the death of RBG:

And now to all this add the potential “nuclear option” for markets of a contested election ANDa deadlocked 4-4 SCOTUS (as Roberts again makes a “surprise” flip) failing to declare a winner, unlike the Bush v Gore 2000 election. What happens then? For the presidency, for the economy, for geopolitics, and for the stock market?

* * *

The script – as bizarre at it appears – has now been written and stocks just have to start “weighing” the risks more efficiently; Sunday night futures open will be fun to watch.

via ZeroHedge News https://ift.tt/35RjErJ Tyler Durden

ActBlue Raises Record $50 Million Following Ginsburg Death Tyler Durden

Sat, 09/19/2020 – 17:30

Left-wing fundraising organization ActBlue raised a staggering $50 million by 4 p.m. ET on Saturday following the death of Supreme Court Justice Ruth Bader Ginsburg, according to the Associated Press.

Hey reporters wondering if this SCOTUS news is motivating Democrats. Here is a chart of donations to our fund to help elect Democrats to the Senate. Donate (or watch the number go up) here: https://t.co/KGWmpELi2Lpic.twitter.com/XCEk21Wnyh

According to their online web tracker, donations flew in at over $100,000 per minute just hours after Ginsburg’s death – accelerated after Sen. Majority Leader Mitch McConnell (R-KY) announced that the Senate would hold a vote on Ginsburg’s seat, according to Breitbart.

“President Trump’s nominee will receive a vote on the floor of the United States Senate,” said McConnell on Friday evening.

Joe Biden’s presidential campaign also appeared to use Ginsburg’s death to raise money ahead of the election in November via an email that vice presidential candidate Sen. Kamala Harris (D-CA) sent. The email also reiterated that “voters should pick a President, and that President should select a successor” for Ginsburg. –Breitbart

“We cannot let them win this fight. Millions of Americans are counting on us to stand up, right now, and fight like hell to protect the Supreme Court — not just for today, but for generations to come,” stated the email from Harris. “The work of holding Senate Republicans accountable to the standard they set in 2016 starts now. To Joe and me, it is clear: The voters should pick a President, and that President should select a successor to Justice Ginsburg.”

“But we know, like you do, that the most important thing we can do to protect that legacy is not just winning the White House, but electing a Senate majority that will confirm fair-minded Supreme Court appointees who believe in equal justice under the law … That’s why I’m asking you today to fight alongside me and to make sure that when the time comes, President Joe Biden can appoint a justice to Justice Ginsburg’s seat who will uphold the rule of law and fight for all of us “

ActBlue has come under fire in recent weeks after nearly half of the group’s 2019 donations were revealed to be from anonymous donors who listed themselves as unemployed.

“After downloading hundreds of millions of [dollars in] donations to the Take Back Action Fund servers, we were shocked to see that almost half of the donations to ActBlue in 2019 claimed to be unemployed individuals,” said John Pudner, president of conservative political group, Action Fund. “The name of employers must be disclosed when making political donations, but more than 4.7 million donations came from people who claimed they did not have an employer. Those 4.7 million donations totaled $346 million ActBlue raised and sent to liberal causes.“

“It is hard to believe that at a time when the U.S. unemployment rate was less than 4 percent, that unemployed people had $346 million dollars to send to ActBlue for liberal causes,” Pudner continued, adding that “4.7 million donations from people without a job … raised serious concerns.”

Notably, by mid-June, ActBlue had contributed $119,253,857 to Biden – a figure which remained unchanged until at least July. As of this writing, they have contributed $194 million – an increase of $75 million.

They’ve also been scrutinized for taking a boatload of anonymous gift card donations valued at $100 or less.

The recent surge in donations related to RBG, however, may just be from panicked Democrats who desperately want Joe Biden to win in November.

Amazon Keeps Spreading Across America, Plans 1000 Warehouses In Suburban Neighborhoods Tyler Durden

Sat, 09/19/2020 – 17:00

Amazon is doubling down on ultra-fast deliveries with plans to open 1,000 small delivery centers across U.S. metro areas and suburbs, according to Bloomberg. The expansion will allow the e-commerce giant to take on Target and Walmart.

“The facilities, which will eventually number about 1,500, will bring products closer to customers, making shopping online about as fast as a quick run to the store. It will also help the world’s largest e-commerce company take on a resurgent Walmart.”

The small warehouses would support Amazon’s efforts to provide customers with two-day and or one-day deliveries for specific items, even if a demand surge is seen. The primary strategy here is to compete with Walmart and Target’s same-day delivery schemes.

Bloomberg explains the strategy behind additional micro warehouses:

“Historically, Amazon gnawed away at brick-and-mortar rivals from warehouses on the exurban fringes, where it operated mostly out of sight and out of mind. That worked fine when the company was promising to get products to customers in two days. Now Walmart and Target Corp. are using their thousands of stores to beat Amazon at its own game by offering same-day delivery of online orders. Walmart also recently started is own Prime-style subscription service, upping the competitive ante.”

The new strategy is already working at a fulfillment center in Holyoke, Massachusetts, situated near a dead mall, and down the street from more than 600,000 people.

Amazon will open a distribution center in the city of Holyoke at 161 Lower Westfield Road this fall. (Hoang ‘Leon’ Nguyen / The Republican)

Amazon’s plan to add micro fulfillment centers is in response to its handling of the virus pandemic. The company had to suspend many non-essential items to deal with the increased demand following the coronavirus outbreak. This created a public backlash for slow shipping times. Customers started to abandon the e-commerce giant for quicker shipping options with Walmart and Target.

During March and April, Amazon announced 175,000 new hires to keep up with demand. Even after lockdowns eased, people continued to order online as the coronavirus cases surged in the summer. Amazon hired 100,000 additional workers in September ahead of the holiday season.

“In just a few years, Amazon has built its own UPS,” said Marc Wulfraat, president of the logistics consulting firm MWPVL International Inc., who estimates Amazon will deliver 67% of its own packages this year and increase that to 85%. “Amazon keeps spreading itself around the country, and as it does, its reliance on UPS will go away.”

Amazon has also been in talks with the largest mall owner in the U.S., Simon Property Group, where anchor department stores could be transformed into Amazon distribution hubs. Bloomberg noted:

“Department stores such as J.C. Penney are often two stories and lack sufficient loading capacity, they said, meaning they require extensive remodeling to accommodate an Amazon delivery hub. Moreover, mall leases with existing tenants often prohibit the owner from introducing a delivery hub that could spoil the shopping experience, and city officials might not quickly approve an industrial use in a retail area. It’s more likely that dead malls will be bulldozed to make way for an Amazon warehouse, as they have in the Midwest, than for an Amazon delivery station to sprout in a half-vacant mall to coexist with Kay Jewelers and Cinnabon.”

If Amazon does, in fact, sign a deal with Simon to transform some of America’s dead malls into micro fulfillment centers, this could be bad news for investors betting against CMBX 6.

Along with plans for micro fulfillment centers, Amazon was recently granted federal approval to operate fleets of delivery drones. This could mean, one day, Amazon Prime Air will make last-mile trips from small fulfillment centers to customers’ homes in 30 minutes to a few hours.

via ZeroHedge News https://ift.tt/2RJivde Tyler Durden

Tug Of War Across Markets Hides “Trade Of A Lifetime” Tyler Durden

Sat, 09/19/2020 – 16:00

Another day, another set of market takes, warning that the recent advent of helicopter money – which resulted in a mind-boggling $21 trillion in policy stimulus, roughly a quarter of global GDP, in just the past 6 months – will lead to a 1970’s style stagflation, runaway inflation and – perhaps for some – the trade of a lifetime.

In his latest Bear Trap Report, author Larry McDonald writes that “the trade of a lifetime is found in a growing tug of war across markets.” He is referring to the ongoing clash – and most important topic in finance today – between inflation and deflation. As he adds, investors are focused on obvious deflation risk, “but the side effects of the $15 Trillion of fiscal and monetary spending globally are underappreciated” (it’s really $21 trillion according to BofA but at that number of zeroes does it really matter).

And while everybody knows the COVID-19 tragedy poses a significant deflation risk – the signs are on every street corner, in McDonalds’ view, “the ‘unexpected’ we must be positioned for is Trillions in fiscal stimulus oozing into the economy after this virus has been snuffed out.” This is a topic we touched on last week in “Trump Agrees With Powell: “Much Higher” Fiscal Stimulus Is Needed… And Why That Could Crash Stocks“, in which we pointed out that Powell’s clear invocation of more fiscal stimulus during the FOMC presser is what catalyzed the break in the market’s upward momentum as tech names were furiously sold off.

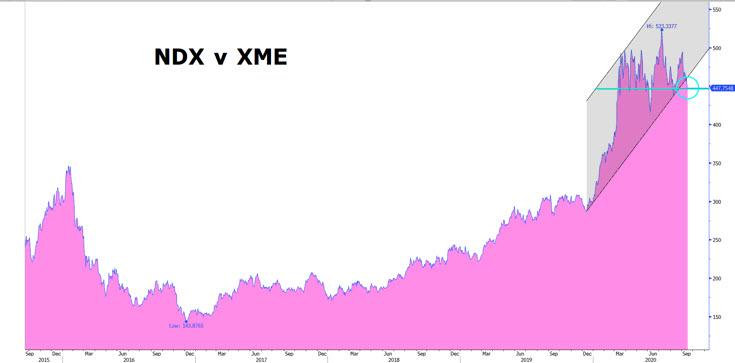

And while going into the FOMC reflation was largely “left for dead” as the sharp rebound in the QQQs following the early September swoon showed, McDonald now sees last week’s outperformance of the XME Metals & Materials ETF as the first heartbeat of a Phoenix coming back to life, “the GENESIS of a significant leg higher.”

Furthermore, he notes, “we don’t even need real inflation for commodities to shine looking forward. The consensus is so skewed to further deflation that even the slightest change in expectations will lead to meaningful outperformance from commodity-sensitive risk assets relative to the S&P 500.”

There’s more: Powell himself may be sending markets a message and not just in the Fed’s sudden halt of corporate bond and ETF purchases in August. This is what McDonald said about the key message from last week’s FOMC:

We believe the most important takeaway from this week’s FOMC meeting comes down to Chairman Powell feebly attempting to parse between QE and forward rates guidance. On Wednesday, the Fed gave “powerful forward guidance” of zero rate hikes for as far as the eye can see, but was unable to provide any forward guidance on asset purchases – Powell refused to answer the question twice in the press conference. With conviction, we believe this is significant and the probability of a Nasdaq crash has risen meaningfully.

In our view, Chair Powell is sending Congress and SoftBank a very clear message. The last thing the FOMC wants right now? To get back into a “2010-2016” like-situation where politicians keep piling all the heavy lifting on central banks. Now, that would be deflationary (Sequestration, Tea Party)! The second last thing the FOMC wants right now is excessive speculation in the Nasdaq – if it pops like the dot-com bubble, it would require even more help from the Fed. They want to let some air out of the balloon, without disrupting financial conditions on Main St.

And while the Fed also gave the ducks doves what they wanted by indefinitely extending QE (which remains at a tune of $120BN/monthly), the question that Powell refused to answer is what is the definition of indefinitely: 3 months? 12 months? 3 years?

Not only did the Fed NOT answer the question, but Powell left the door open for LESS balance sheet accommodation. This ladies and gentleman, is the sword thrusted into the side of the beast that is the Nasdaq. A ferocious bull is wounded.

To be sure the market is clearly starting to appreciate the growing double threat of a potential reflationary spillover from tens of trillions in stimulus and the Fed’s “not so dovish” twist Powell didn’t offer investors certainty on the balance sheet expansion policy path, which according to Bear Traps “was a shot across the bow” and “the bottom line, for big tech to command today’s lofty valuations, balance sheet expansion certainty is needed from the Fed.”

The result: the worst September for the Nasdaq since Q4 2018:

At this point, and likely true to its name, the Bear Traps report turns fatalistic warning that “A lot of pain has been inflected, the bulls will try and buy the dips into quarter-end, September 30th. We see a crash by October 10th, sell EVERY rally.”

That may be a bit extreme, because the muscle memory of traders is still buzzing with the expectation that a market crash will merely prompt the Fed to go back to its monetary stimulus roots, and as such instead of selling traders may well resume buying having already priced in the necessary step of Fed intervention (which however requires another market crash). So the sequence of events, especially with Trump desperate to demonstrate a strong stock market into the election, is not quite so clear to us.

However, one thing that is clear is that the market remains solidly in the deflation camp, which in turn reveals what the Bear Traps report contends is the story of the month, namely “the growth to value tremors have been revisiting with intensity, the ‘quake’ is coming.”

This can be seen in the chart of Russell growth to value below…

… and zoomed in, where said tremors have seen the ratio peak at an all time high in arly September, and then quickly reversing to three month lows in what may be the start of an epic mean reversion.

So is long Value/short Growth the trade of a lifetime?

According to McDonald as long as the RLG Russel Growth vs. RLV Russell Value ratio stays under 1.85, “the long value trade is a home-run” as more and more investing legends – Druckenmiller, Einhorn, Melkman, Greenspan, Sherman/Gundlach, and co – publicly talk-up inflation risk:

“The natives are restless, real money asset managers are listening. Capital is starting to exit growth, nearly $1T last 10 days.”

And the cherry on top: a Bridgewater implosion:

“In our view, the modern risk-parity model is about to collapse and is in store for a colossal face-lift (risk parity = long equities and extra-long bonds).”

Why? Because a “convexity climax” would mean that by the time we actually see inflation, it will be far too late to protect a bond portfolio.

Today, an extra $70T in fixed income globally sits with less than 1.0% in yield, this comes with a steep price. After a long decade of austerity, Brexit, trade wars, and Covid19; bond investors have fallen into a deep sleep. Every extra dollar placed in this ocean of risk changes the formula. The market’s reaction function will join us FAR before inflation actually appears. It’s already happening today. Hence, the latest commodity bid, you don’t see 35% one-month moves in Silver very often.

Without going into too much depth, there are countless underlying inflation drivers which both the Fed and Congress have already put in play.

A shift from just in time global supply chain to increased domestic manufacture as a counterpoise to China’s Belt and Road policy is a safe forecast. This will cause a huge demand for labor. The Phillips Curve won’t remain flat under that scenario. The younger generations as a rule are sensitized to environmental concerns. As the USA and Europe become more green, associated costs will cause extra price pressure. In sum, inflation is a quite complex phenomenon, and thus is unlikely to have a simple, obvious cause. This explains why academia has failed to arrive at a nice, neat simple explanatory model for inflation.

Right now we have massive money creation, massive fiscal stimulus, and strong social forces combining to create an inflation juggernaut. Stocks and bonds will both enter a secular bear market, debt as a percentage of GDP will continue to climb, nominal tax rates on the rich will increase, Central Banks will remain accommodative at least for the medium term, and money supply will continue to expand. Most important of all, wages will go higher. The risk-parity trade is dead. Over the next twelve months we will bury it and read its last rites.

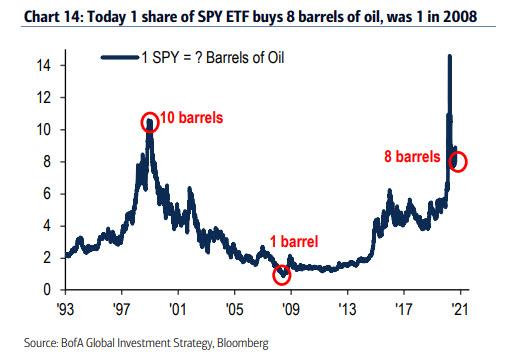

It’s not just McDonald: another inflationary prediction comes from BofA CIO Michael Hartnett who gives two reasons why inflation assets will outperform:

Gold vs Treasuries at critical US/EU debt crises highs of 2011/12 (Chart 2); new highs in gold & Chinese renminbi = US dollar debasement (Chart 13); lower gold & higher real yields (last trough was 2012) = Great Rotation; in both scenarios inflation assets would outperform.

Oil vs US stocks close to 90-year lows; today 1 share of SPY ETF buys 8 barrels of oil, was just 1 barrel in 2008.

Finally, in evaluating a near-term trigger, McDonald notes that “as Congress delivers the next fiscal care package, hand in hand with a vaccine cocktail coming to market in the months ahead, it will be a reflation investors delight. These two engines will be the trade’s rocket fuel, propelling the investment thesis from the early to “middle innings.” Months from now, Powell may look very wise in NOT offering up “certainty in balance sheet accommodation” ahead of Congress and Vaccines. He kept his powder dry.”

But what if Congress fails to deliver this year as the constant bickering between Pelosi and McConnell strongly suggests? Well, then the deflation camp has another party, potentially resulting in a 10-20% drawdown. However, it is precisely that market stress that will force the classic policy response out of Capital Hill. The conclusion: “This New Deal on roids will have one anchor tenant as large scale infrastructure spending will join us early next year – next, commodities and value crush growth stocks in 2021.”

via ZeroHedge News https://ift.tt/2EkeDfS Tyler Durden

Secret Service Intercepts ‘Highly Toxic’ Poison Ricin Mailed To White House Tyler Durden

Sat, 09/19/2020 – 15:45

Just as the presidential race has been upended by the death of Ruth Bader Ginsburg, the Secret Service has intercepted a piece of mail addressed to the White House containing the lethal poison ricin, according to media reports.

It’s not clear where or when the mail was intercepted, though authorites are saying the letter may have been sent from Canada, per the NYT.

Ricin is made from the by-products of producing castor oil, which is made from the castor oil plant, otherwise known as Ricinus communis. It’s a highly potent toxin, and it has no known antidote. The poison gained renewed notoriety after being featured in a notable plot arch from the TV show “Breaking Bad”.

The White House hasn’t yet commented on the news, which was first reported by the NYT and a handful of other media organizations citing unidentified sources who have reportedly been briefed on the matter.

Though the identity of whoever sent this substance has yet to be ascertained, some on the right couldn’t help but note the timing, coming so soon after the death of Justice Ginsburg, and amid an outpouring of hysteria accusing Trump of ‘destroying American Democracy.’

BREAKING:

The Secret Service just intercepted a package addressed to President Trump which contained Ricin

These are the lengths the left is willing to go to stop him from filling a Supreme Court seat.

Back in 2013, a Mississippi man sent ricin to the White House, and a Republican senator, in a bizarre attempt to frame a rival. The lurid story got plenty of play in the press, but the culprit, James Everett Dutscke, was later sentenced to 25 years in prison.

via ZeroHedge News https://ift.tt/3iLQUnV Tyler Durden

A new study by Princeton University’s US Crisis Monitor shows that the U.S. experienced 637 riots between May 26 and Sept. 12, and 91% of those riots were linked to the Black Lives Matter movement.

In other words, BLM was responsible for 9 out of 10 riots across the country.

Riots are defined by the project as “demonstrations in which any demonstrators engage in violently disruptive or destructive acts (e.g. violence, looting, vandalism, etc.), as well as mob violence in which violent mobs target other individuals, property, businesses, or other groups.”

“Forty-nine states, not counting Washington, D.C., experienced riots during that time period, the study found. California led the nation with 86 riots during that time, closely followed by Oregon with 79 riots during that time period, the data show,” reports the Daily Caller.

Mainstream media talking heads have repeatedly asserted that the riots were either not happening on any large scale or were “mostly peaceful.”

The statistics suggest otherwise.

Despite attempts to spin the riots as peaceful protests, more and more Americans aren’t buying it.

“A majority of U.S. adults (55%) now express at least some support for the movement, down from 67% in June amid nationwide demonstrations sparked by the death of George Floyd,” reported Pew.

“The share who say they strongly support the movement stands at 29%, down from 38% three months ago.”

When one considers the level of intimidation and bullying metered out to those who refuse to express support for BLM, the real figures are probably much lower in terms of support for Black Lives Matter.

It’s no surprise that Democrats like Nancy Pelosi are only now condemning riots, arson and looting after 4 months of mayhem.

After initially ignoring or justifying the violence, Democrats have seen the polls and performed a total 180.

* * *

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/33Yfzzt Tyler Durden

“I’m Speechless”: Police Chase Down Tesla On Autopilot Doing 90 MPH With Driver And Passenger Asleep Tyler Durden

Sat, 09/19/2020 – 15:00

Another day, another story of a horribly irresponsible Tesla owner “beta testing” the company’s Autopilot software while putting countless other lives at risk.

And likely, another day the NHTSA in the U.S. will do nothing about it.

Today’s story comes out of Canada, where a 20 year old man is facing charges for sleeping behind the wheel of a Tesla that was doing more than 90 mph.

The RCMP was called when witnesses saw “a speeding Tesla electric car heading south of Edmonton, and what appeared to be no one behind the wheel,” according to NBC.

Both front seats were fully reclined and both the driver and the passenger appeared to be asleep, according to the report. The car was doing about 87mph on a roadway with a posted speed limit of about 68mph.

Police say that when chasing the Tesla down, it accelerated to more than 90mph as other drivers on the roadway pulled over after seeing the patrol car’s lights.

RCMP Sgt. Darrin Turnbull said: “Nobody was looking out the windshield to see where the car was going. I’ve been in policing for over 23 years and the majority of that in traffic law enforcement, andI’m speechless. I’ve never, ever seen anything like this before, but of course the technology wasn’t there.”

The driver was charged with speeding and had a temporary hold put on his license.

Superintendent Gary Graham of Alberta RCMP Traffic Services concluded: “Although manufacturers of new vehicles have built in safeguards to prevent drivers from taking advantage of the new safety systems in vehicles, those systems are just that — supplemental safety systems. They are not self-driving systems, they still come with the responsibility of driving.”

We wonder if Gary could give the NHTSA a call…

via ZeroHedge News https://ift.tt/35QooO1 Tyler Durden

On Monday, I return to work from an extended vacation (I didn’t miss much it seems). I’m refreshed and ready for what will likely be one of the craziest periods for the markets since the COVID Crash.

I realize I’m the guy who has gone out there and said you have a free shot on goal ever since late March. I even called it “Project Zimbabwe,” as it was so obvious that you only had two acceptable exposure options, long and very long.

That said, now is a time for a bit of caution leading into the election.

Longer term, markets are going much, much higher because no matter who wins the Presidency, both parties are committed to the sort of fiscal and monetary expansion that only Banana Republics can countenance.

“Project Zimbabwe” is very much the playbook here.

That said, over the next few weeks leading up to the election, there will almost certainly be volatility.

The election itself may be undecided in the first day. Who knows what happens if one side does not accept the outcome? Markets abhor uncertainty.

With all of that in mind, this is your friendly reminder to de-gross a bit.

Increased liquidity equals free optionality. Besides, it’s not like I think I’ll miss much upside leading into election day.

In summary, I’ve been a seller over the past few weeks. I’m letting Event-Driven trades run off and I’m hesitant to add new ones unless they’re somehow hedged. I am also going to let my September paper roll off and will not re-load for November—not unless implied volatility spikes into election day.

This isn’t a call to panic sell or get short. It’s still “Project Zimbabwe” out there. Rather, much like going into the COVID Crash, this is a time to go through your book and ask if you’re confident in each of your positions, or if there are a few that ought to be jettisoned. Remember, most of the money is made buying the panic dips—do you have room to add on a violent pullback?

In summary, I want some extra room in case this election turns into a complete klusterfuk.

via ZeroHedge News https://ift.tt/3iKRcew Tyler Durden

{kind=link}