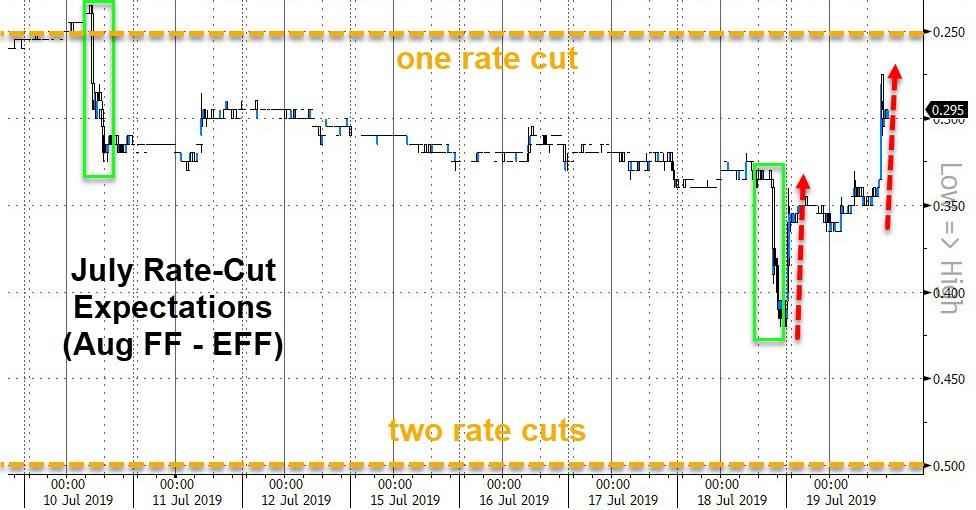

0, 25, or 50bps next week? Will Draghi leave Lagarde a rate-cut gift (or start buying stocks)? Those are the questions the market is asking and judging by the markets’ response, it’s moar of whatever hasn’t worked til now…

And the short-end is implying a 20% chance of 50bps next week (down from over 71% just after Williams spoke)…

But, despite the desperate jawboning last last week, to rescue market expectations back from Williams’ “academic” warnings, former fund manager and FX trader Richard Breslow notes that now that rate cuts and dovish talk are firmly on the agenda, it’s hard to think of anything, at this point, that might derail the ECB or the Fed. And we certainly know the mindset of the PBOC and the BOJ.

Which raises the question of whether economic data releases mean anything or not? With momentum having stalled in several major asset prices, it’s easy to conclude that they don’t. But they do.

Via Bloomberg,

Is the Fed cutting rates based on U.S. economy trends or because of the ubiquitous global headwinds? Are these forces anything monetary policy can do something about? Foreign-exchange traders certainly want to know the answer. And, given the dispersion of economist forecasts for this week’s numbers, a lot of other people are curious and confused as well.

Whether it’s one-and-done or the start of the march back toward zero will obviously affect what investors do for the rest of the year. Quite a few assets are at crossroads and where they go from here will depend on the answer. Oddly enough, there seems to be far more debate about what the Fed will do rather than how much the ECB will cut. And yet we know Europe unambiguously can use some additional stimulus.

Unfortunately, they’re going to provide the dubious kind in the form of more deeply negative rates, rather than the fiscal boost they need. Yet, for reasons that escape me, there seems to be more optimism about the efficacy of what the Europeans will do than the “insurance cut” from the FOMC. Despite some of last week’s comments, the Fed should do as little cutting as they can. Twenty-years of academic research or not. And the ECB will be wasting everyone’s time by not erring on the aggressive side.

Analysts, by and large, hate the dollar. They’ve been remarkably consistent in holding that view, even though the Dollar Index has done nothing all year but range back and forth. Such is the staging of currency-war wrangling more than a demonstration of the relative attractiveness of the dollar versus the rest of the G-10.

Equity markets have also lost their upward momentum. Given the waning technical picture and the geopolitical backdrop, it’s tempting to get intrigued about testing the downside. But markets aren’t here because of a fantastic global economy, rather courtesy of share buybacks and quantitative easing. Which we are getting more, not less, of. The market can certainly go down, but, at this point, there is nothing to suggest it shouldn’t be treated as a correction rather than a sea change. Keep a weathered eye on consumer spending. Not to mention all of the support levels below.

Business investment won’t pick up without trade talk progress. But even at these lofty prices, any constructive news will still be market positive. With central banks once again very much on the case, it’s worth remembering the many examples of traders feeling able to ignore geopolitical news courtesy of monetary-policy generosity.

As far as bonds are concerned, they continue to act like every setback is a buying opportunity. Gold’s good to have. Lots of people feel safer with yen or francs on the books. But bonds remain the ultimate haven to be parted with begrudgingly. Fixed-income traders can be happy with any economic number that’s an outlier. Rightly or wrongly, they’re happy to enjoy what has been a heads-they-win, tails-they-win environment.

via ZeroHedge News https://ift.tt/2Lz7EBJ Tyler Durden

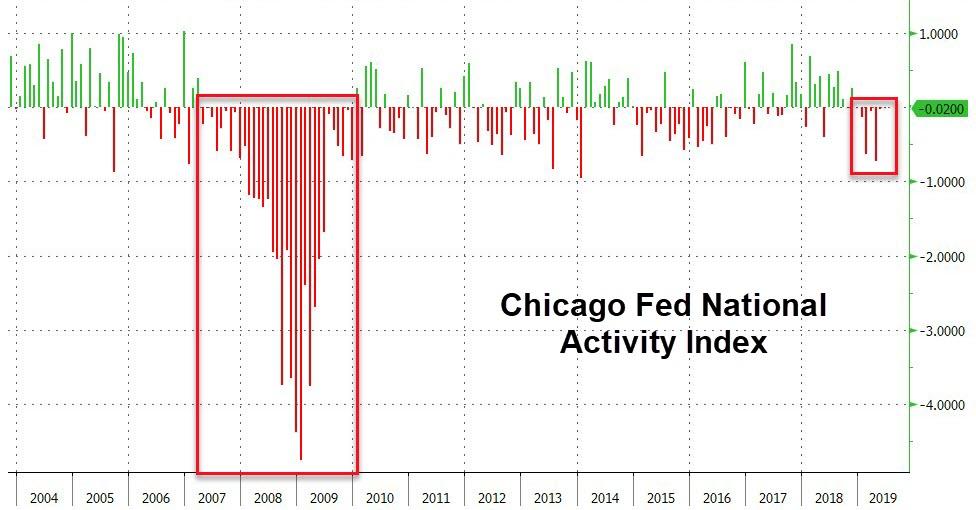

Against hope-filled expectations of 0.08 print, Chicago Fed’s National Activity Index disappointed once again, down 0.02 in June. This is the seventh month of declines in a row – the longest streak of contraction since the financial crisis.

36 indicators improved from May to June, while 49 indicators deteriorated (but of the indicators that improved, nine made negative contributions).

40 of the 85 monthly individual indicators made positive contributions, while 45 indicators affected the index negatively.

Only the ’employment’-related indicators suggested growth in June…

And this is all happening with stocks at record highs?

via ZeroHedge News https://ift.tt/2Z3TFqA Tyler Durden

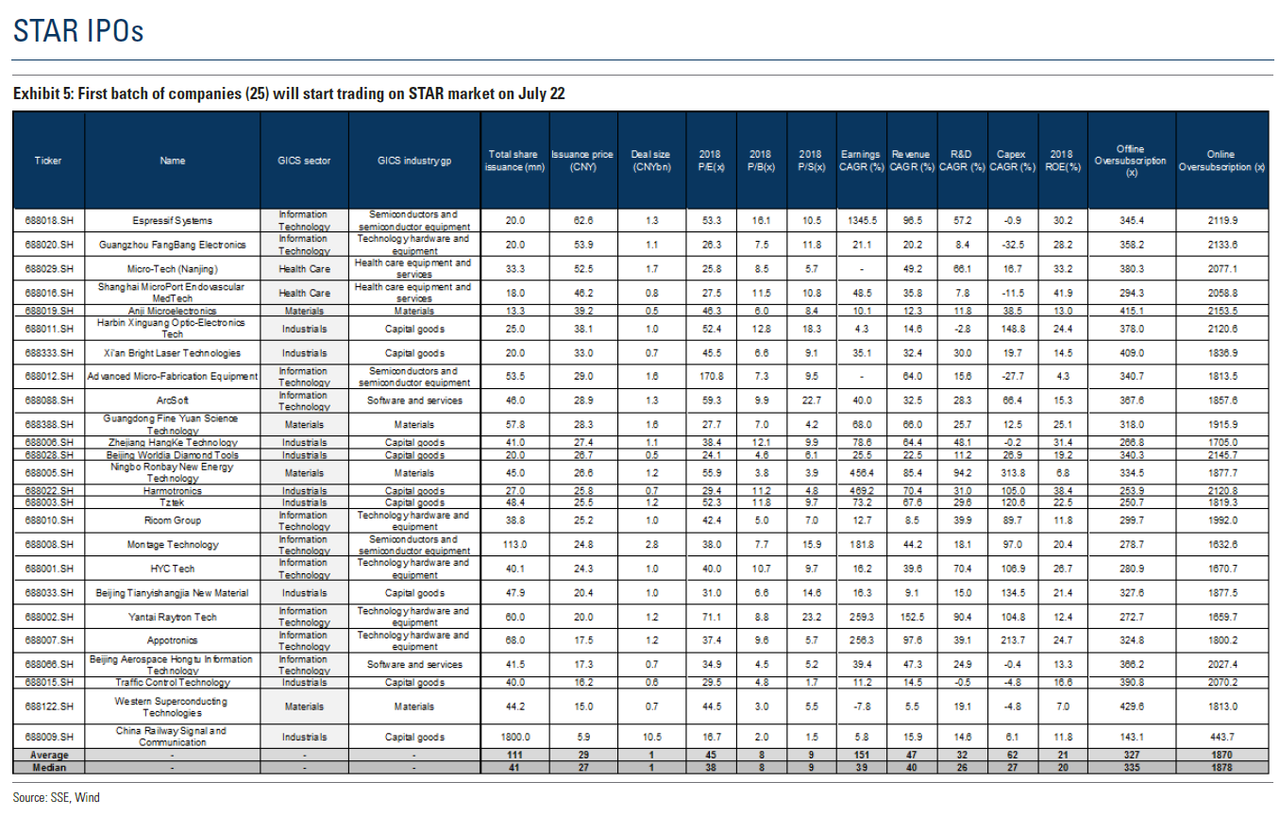

China’s long-awaited Star market started trading on Monday, and oh what a session it was. Chinese investors rushed to trade the 25 companies listed on the exchange, and the explosion of activity caused prices to climb an average of 140% intraday, producing a distinct echo of Chinese equity bubbles past.

Beijing hopes the Star Market, billed as Shanghai’s answer to the Nasdaq, will ideally inspire more science and technology-focused companies to list at home, rather than seeking an offering in Hong Kong or, worse, New York.

The launch is happening at a curious time. The trade war between Washington and Beijing has forced the Communist Party to contemplate what life would be like following a complete break with the US.

More than 140 technology and science companies have signed up to list on the new facility, which is run by the Shanghai Stock Exchange. In the beginning, the exchange aims to raise Rmb128.8 billion or $18.7 billion for its listed companies.

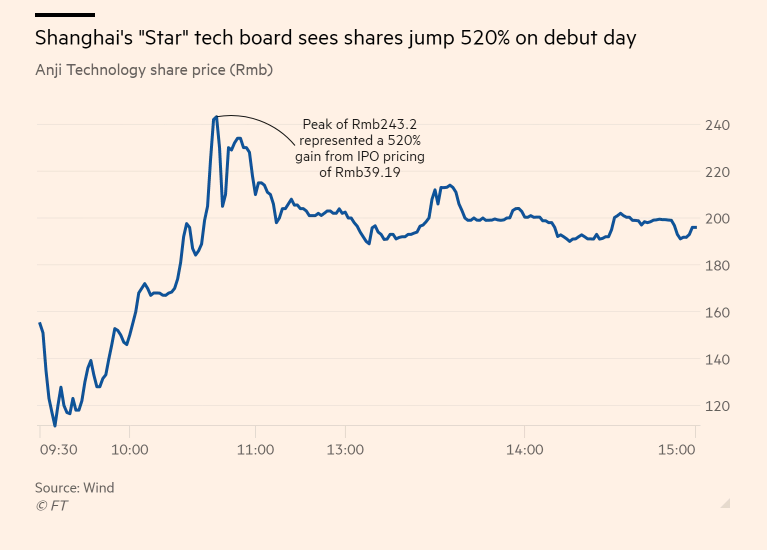

The frenzied trading during the market’s first session inspired some truly baffling moves: Anji Technology climbed as much as 520% during the first session (see below), and shares of Montage Technology climbed 285%. Four of the 25 listed stocks were up more than 200%. More than 16 stocks were up 100%.

Even the weakest performer leapt 84.22%.

The Shanghai Composite weakened as investors were drawn to the new exchange, which created an additional $44 billion of market cap for Chinese markets, Reuters reports, beating the expectations of even veteran investors.

Institutional market participants admitted that the price fluctuations were more violent than they had anticipated.

“The price gains are crazier than we expected,” said Stephen Huang, vice president of Shanghai See Truth Investment Management. “These are good companies, but valuations are too high. Buying them now makes no sense.”

Rapid moves like these are rare in China since Beijing has a habit of shutting down trading when things get volatile.

The Shanghai and Shenzhen exchanges permit prices of new issues to move 44% during their first day of trade, then 10% every day after that. By comparison, on the Star Market, there are no limits during a stock’s first five days of trading. And after that, stocks will be allowed to move up to 20% a day in either direction.

Though it might sound counterintuitive, allowing shares to register such exaggerated moves helped boost the market’s credibility, as the government declined to intervene.

China tries again to boost the credibility of its volatile stock market https://t.co/Il7jX5GCjX

To try and limit the influence of retail investors, Star Market only allows those with at least 500,000 yuan ($72,700) in their brokerage accounts to trade.

Investors see the government’s backing of the new market as a key attraction.

“The government is backing it and investors are speculating that the government will support it,” said Margaret Yang, market analyst with CMC Markets Singapore.

However, Ms Yang warned that this may not be enough to guarantee the market’s long-term prospects. “This game can keep going for at least a few days but in the long run it’s hard to say,” she said.

The new market is unique in China, and offers unique enticements to attract tech companies to list, including allowing dual-class shares that preserve founders’ control. Investors are also permitted to short sell individual stocks, a practice that has at times been forbidden in China’s extant markets.

Trinh Nguyen, a senior economist at Natixis, said Beijing wanted to convince domestic tech companies that domestic markets could handle their IPOs.

Whether they were successful remains to be seen. But soon, the NYSE and Nasdaq might lose out on the steady stream of Chinese listings that had become a dependable source of income until recently.

via ZeroHedge News https://ift.tt/2GoRbM8 Tyler Durden

The Etrade commercial aired during Super Bowl XLI in 2007. The following year, the financial crisis set in, markets plunged, and investors lost 50%, or more, of their wealth.

However, this wasn’t the first time it happened.

The same thing happened in late 1999. This commercial was aired 2-months shy of the beginning of the “Dot.com” bust as investors once again believed “investing was as easy as 1-2-3.”

Why this trip down memory lane? (Other than the fact the commercials are hilarious to watch.)

Because this is typical of the mindset seen at the end of extremely long “cyclical” bull market cycles.

Investing is simple. Just throw you money in the market and it goes up. Its so easy a “baby can do it.”

Here is something else you see at the end of bull market cycles:

How did they make this happen? Shen and Leung, who was also a computer engineer, are part of the FIRE movement — which stands for Financial Independence, Retire Early — where the goal is to save a lot so you can retire early. The couple retired at 31 with roughly $1 million in the bank. They’re currently withdrawing 3.5% a year from that nest egg, and say they can easily travel the world on that money — as they’ve got lots of practice being frugal.”

First, I want to give the couple a “fanatical thumbs up” for saving $1 million by their 30’s. That is an amazing feat which deserves respect and acknowledgment.

Secondly, they are very budget conscious and willing to sacrifice the luxuries most people long for to live their dream.

Another “thumbs up.”

However, the rise of the “F.I.R.E.” movement is symptomatic of a late stage bull market advance. More importantly, we can also predict how things will turn out for Shen and Leung.

For this discussion I want to use the data provided by Shen and Leung to build our examples.

Invested asset value: $1 million

Annualized withdrawal rate: 3.5%

Annualized return rate: 6% (Not specified but a reasonable estimate)

Living needs: $35,000 annually.

Life expectency: 85-years of age.

With these assumptions in place we can begin to do some forecasting about how things eventually turn out. However, we also have to assume:

The couple never has children

Never requires serious medical care (hopefully)

Never considers buying a house

Has no major life events, etc.

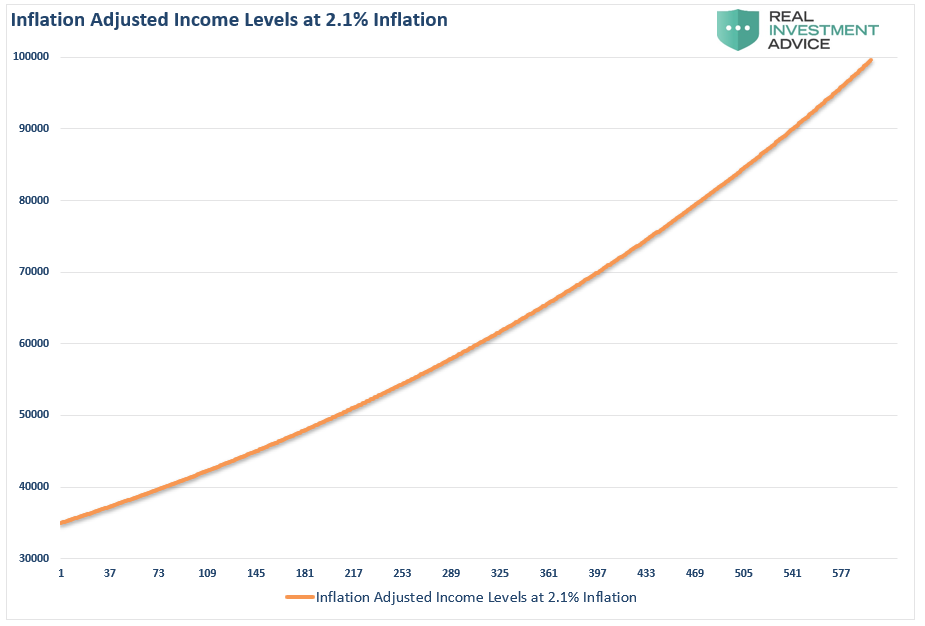

First, we need to start with the cost of living. As I showed recently in Part 1 of “Everything You’ve Been Told About Savings & Investing Is Wrong” is that the cost of living rises over time due to inflation. However, for most the increase in living costs rises dramatically more as needs for housing, children, education, travel, insurance, and health care occur through stages of life.

For this exercise, we will assume our example couple never changes their lifestyle so only inflation is a factor. We will use the historical average of 2.1% and project it out for 50-years.

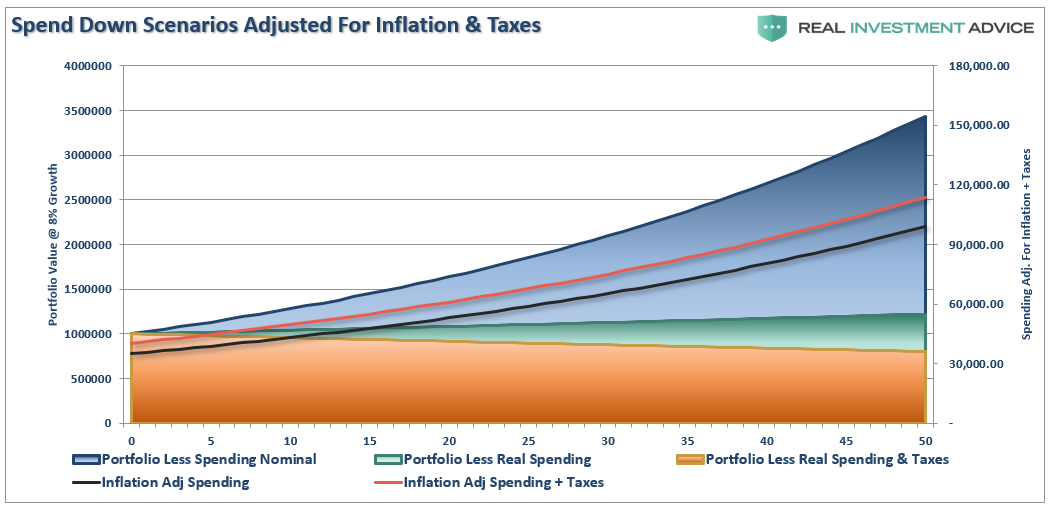

Understanding this, we can now take their $1 million, compound it at 6% annually (the preferred mainstream method), and deduct 3.5% annually adjusted for inflation over their 50-year time horizon.

We need to assume that since our couple is in their 30’s, the investable assets are in taxable accounts. Also, if this is the case, and they are not touching the principal, then we need to adjust the annual withdrawals for capital gains tax. The bottom two area charts adjust for 2.1% annual inflation and inflation plus a 15% tax on withdrawals.(Tax is paid on the gains taken to fund the withdrawal and the dividends paid in on an annual basis)

Not surprisingly, if our couple can indeed live on $35,000 a year, even when adjusting for inflation and taxation, a $1 million portfolio growing at 6% annually can indeed support them for their entire lifespan.

Reality Is Different

In Part 3 of our recent series on “saving and investing,”we laid out the issue, and importance, of variable rates of return. To wit:

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what happened to their money is substantial over long-term time frames.”

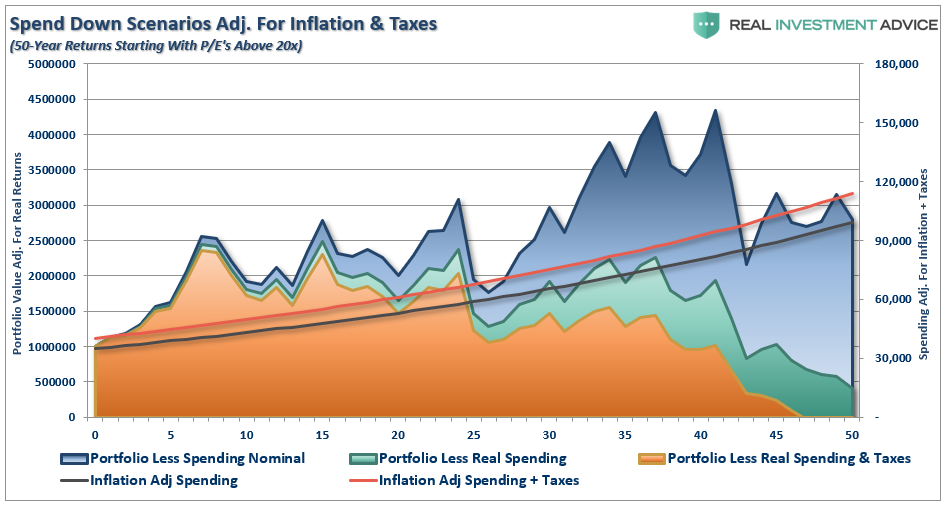

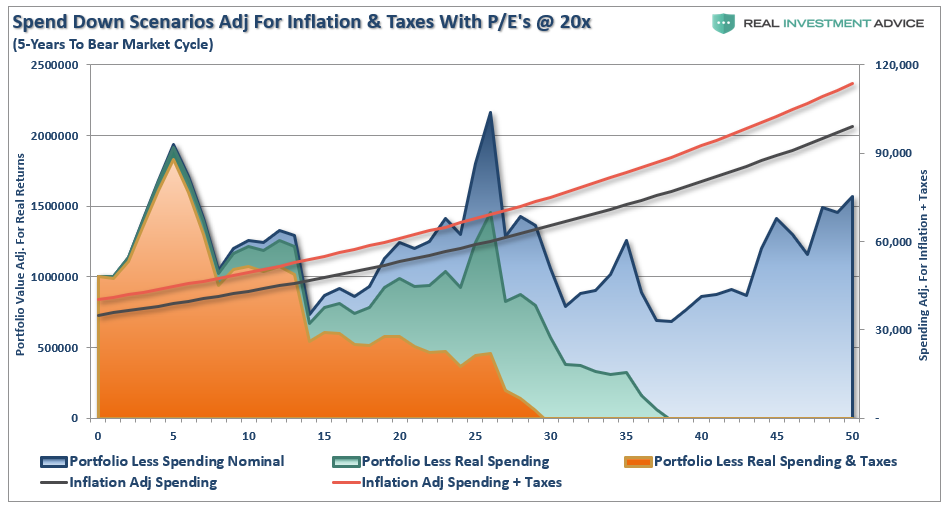

The chart below is exactly the same as above, however, this time we have used the average annual 50-year returns from previous periods in history where starting valuations were greater than 20x earnings as they are today. (High starting valuations beget lower future returns historically speaking.)

Over a 50-years, our couple will get the benefit of complete valuation and market cycles. In this case, since they are starting with high valuations at the outset, the first 30-years contains a long-period of lower returns, but that last 20-years receives the benefit of higher returns due to valuation reversion.

Due to market volatility and periods of negative growth, the original $1 million portfolio only grows to $3 million when including nominal spending. However, when accounting for volatility, inflation, and taxes, the survival rate of the portfolio diminishes sharply due to two reasons:

Down years reduce the growth rate of the portfolio over the given time frame.

Withdrawals in down years exacerbate the decline in the portfolio. (i.e. Portfolio declines by $65,000 plus the $35,000 annual withdrawal increases the 6.5% decline to 10%.)

Obviously, not accounting for volatility when planning to retire early can have severe future consequences. In this case they will run out of money in year 47.

The Big Bad Bear

As I said at the beginning of this missive, the “F.I.R.E.” movement is the result of a decade-long bull market cycle.

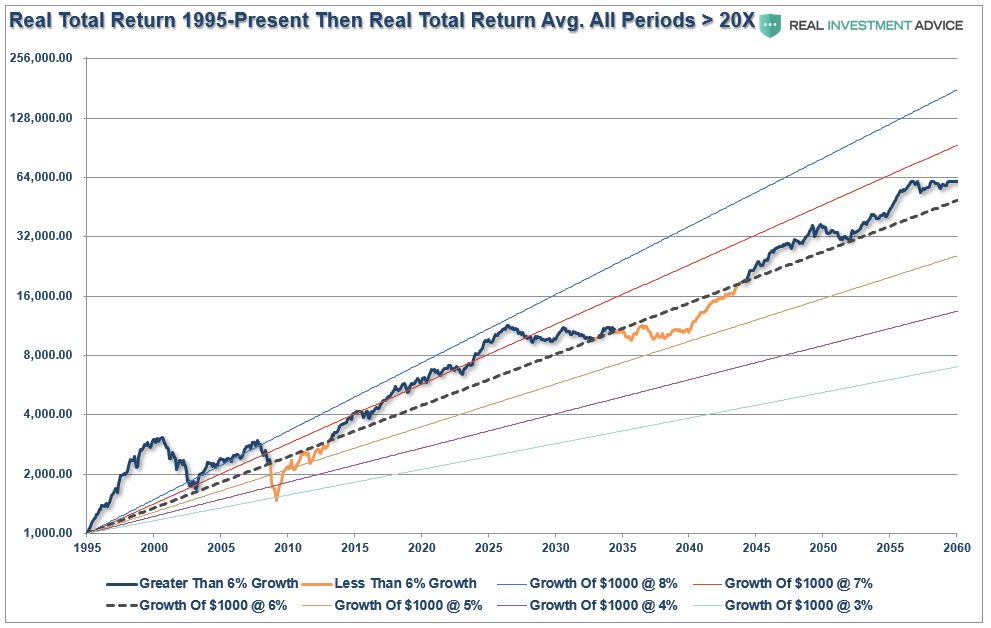

Most likely, our young couple will be met with a “bear market” sooner, rather than later, in their early retirement. If we use the return model from our recent article on “investors and pension funds,” we see a rather dramatic shift in life-expectancy of the portfolio.

“The chart below is the S&P 500 TOTAL REAL return from 1995 to present. I have projected an average return of every period in history where the market peaked following P/E’s exceeding 20x earnings. This provides for variable rates of market returns with cycling bull and bear markets out to 2060. I have also projected ‘average’ returns from 3% to 8% from 1995 to 2060. (The average real total return for the entire period is 6.56% which is likely higher than what current valuation and demographic trends suggest it should be.)”

The benefit of this model is that it shows the impact to portfolio returns when bear markets are “front-loaded,” as will likely be the case for most the “F.I.R.E.” followers.(Note, in the return model above the “bear market” is 5-years into the future)

The reason for the dramatic short-fall is that a major, “rip your face off,” bear market will cut asset values by 50% very early on. All of a sudden, the annual withdrawal rate of 3.5% becomes 7%, which outpaces the ability of the portfolio to grow fast enough to catch up with the withdrawal rate and the loss of principal. In this more realistic example, our couple will run out of money in 30 years.

This is the exact problem “pension funds” face currently.

The Other Problems From “Playing With F.I.R.E.”

While we have mainly addressed the issues surrounding assumptions being used by the ‘F.I.R.E.”movement in having enough assets to retire, there are some other important issues which should be considered.

Loss of your skill set. In retirement it is probable your skill set erodes and becomes outdated over time. New technologies, trends, innovations, etc. are running at a faster pace than ever.

Becoming unemployable. One of the things seen following the financial crisis was employers preferring to hire individuals who were already employed rather than hiring those out of work. The reasoning was that if you were good enough to keep your job during the recession, you obviously have a valuable skill set. Once you are out of the “labor force” for a while, it becomes more difficult to regain employment as employers tend to prefer those with a very steady work history, a growing career, and relevant skill sets.

Life. Besides simply running out of money sooner than you planned because of a bear market, a rising cost of living more than you counted on, or higher taxes (all of which are very likely in the near future) there is also just “life.” It doesn’t matter how carefully you plan; “S*** Happens!” More importantly, it always happens when you least expect it and at the worst possible time. These things cost money and impact our best laid spending and saving plans. The problem with “retiring early,” is that it leaves plenty of time for things to go wrong.

Unplanned Accident/Medical Problem.Young people suffer from an “invincibility syndrome.” They tend to not carry insurance, due to the cost, because they “never get sick.” While we certainly hope it never happens, a major accident or health issue can extract tens to hundreds of thousands of dollars of capital critically impairing retirement plans.

Too Old To Do Anything About It. The biggest problem for “F.I.R.E.” practitioners is that running out of money late in life leaves VERY few options for the rest of your retirement years. If our math above is even close to correct, which history suggests it is, then our young couple will be faced with going back to work in the 70’s. That is not exactly the retirement most are hoping for.

As I stated in our previous series, retiring early is far more expensive than most realize. Furthermore, not accounting for variable rates of returns, lower forward returns due to high valuations, and not adjusting for inflation and taxes will leave most far short of their goals.

While it sounds like I am bashing the “F.I.R.E. Movement,” I am not. I am for ANY program or system that gets young people to save more, stay out of debt, and invest cautiously. The movement is a good thing and it should be embraced.

But, it is also a symptom of a decade-long period of making “easy money” in the financial markets.

These periods ALWAYS end badly and the next “bear market” will quickly “extinguish the F.I.R.E.” as losses mount and dreams have to be put on hold.

It will happen. It always appears easiest at the top.

And, given one of E*Trade’s latest commercials, the next bear market may be coming sooner than we expect.

via ZeroHedge News https://ift.tt/2Och1cF Tyler Durden

Iran has handed down the death penalty to alleged members of a CIA-spy ring inside Iran’s military, which authorities said they uncovered earlier this year. And now for the first time, state media is circulating photos purporting to show some among the alleged CIA-linked operatives.

“The identified spies were employed in sensitive and vital private sector centers in the economic, nuclear, infrastructure, military and cyber areas… where they collected classified information,” Iran’s Ministry of Intelligence said on state television. They had been working “contractors or consultants,” the statement said.

Iranian judiciary spokesman Gholamhossein Esmaili had first announced in June that a number among seventeen total alleged spies rounded up were facing execution because of the “severity of their crimes,” as reported by NBC. The unnamed defendants were reportedly associated with the Iranian military and also followed a similar announcement madelast August the arrest of “tens of spies” uncovered within the government.

The agencies “successfully dismantled a (CIA) spy network,” an official only identified as head of counter-intelligence at the Iranian intelligence ministry, told reporters in Tehran. Arrests reportedly began in March

“Those who deliberately betrayed the country were handed to the judiciary… some were sentenced to death and some to long-term imprisonment,” he said, as cited by the AFP. However, the photos published – which appear to show Americans – only claim these are officers which had been “handling” the spites supposedly caught inside Iran.

None of the initial photos released showed those pictured in any kind of detention or interrogation, but instead most appeared to be personal or family photos. As Reuters reports:

Iranian state television published images it said showed the CIA officers who were in touch with the suspected spies.

There was no immediate comment on the Iranian allegations by the CIA or U.S. officials.

Additionally, in another stunning development, an Iranian television documentary aired Monday which claimed to show footage of an alleged CIA officer attempting to recruit an unidentified Iranian man. The footage was presented as taking place inside the United Arab Emirates.

Documents alleging to “prove” the allegations were also posted online by Iranian media channels.

“Because there are so many intelligence officers in Dubai. It is very dangerous… Iranian intelligence,” a blond-haired woman was shown telling the man. According to Reuters:

The woman spoke Persian with an accent which appeared to be American.

State media outlets had touted the documentary as dealing a heavy blow “to a CIA spy network in the region and beyond.

⚡️⚡️⚡️ Coming soon on @PressTV: The Mole Hunt ⚡️⚡️⚡️#Iran has dealt a heavy to a @CIA spy network in the region and beyond. The upcoming documentary will shed more light on Iran’s counter-intelligence operations. pic.twitter.com/mlQ3e8aqft

The photos and video purporting to show CIA assets and operatives have yet to be confirmed or denied by US political or intelligence officials and come amid already soaring tensions have put the region on edge, and as Britain has demanded the release of the UK-flagged tanker Stena Impero, captured in the Strait of Hormuz Friday.

via ZeroHedge News https://ift.tt/2JI5NIK Tyler Durden

As the midsummer sun rises, those traders who are not on vacation brace for an extremely busy week that includes the first of two big central bank meetings in the remainder of this month with the ECB meeting, as well as a barrage of US corporate earnings. The latest flash PMIs around the world and Q2 GDP in the US are the data highlights while earnings season really starts to ramp up in the US. In the UK we’ll also get official confirmation of who the next Prime Minister is. But the highlight of this week will be the much anticipated ECB meeting on Thursday.

At Sintra last month Draghi laid the foundations to make further policy easing feel less conditional, although Wall Street is split on when Draghi will actually make a formal announcement with Deutsche Bank believing that September is the natural occasion for the big decisions and details however some preparation is anticipated at the meeting next week. They expect the “or lower” easing bias to be reintroduced into rates guidance and that this will be the prelude to a 10bp deposit rate cut and tiering in September. They also expect a further 10bp cut in December. They also believe we will see upgraded forward guidance used to underline the ECB’s “absolute commitment” to the price stability mandate.

If the Council is unable to strengthen forward guidance sufficiently, a new wave of QE may be required. If so, analysts would not be surprised by new QE of €30bn per month for a minimum 9-12 months split equally between public and private assets and with a commitment to relax the limits if necessary.

Politics will also play a key role this week with Theresa May’s successor to be announced on Tuesday (spoiler alert: Boris Johnson) and the formal handover to take place on Wednesday.

One day prior to the ECB on Wednesday we’ll get the flash July PMIs in Europe. The last few months have seen some stabilisation in the data with the manufacturing PMI for the Euro Area hitting 47.6 in June (vs. 47.7, 47.9 and 47.5 in the three months prior). The consensus expects a 47.8 reading for July. As for the services reading the consensus expects a 53.5 print which compares to 53.6 last month. We’ll also get country level PMI data for Germany, France and also the Japan and the US.

Meanwhile, earnings season ramps up this week with 145 S&P 500 companies due to report and 10 of the Dow 30. The highlights include Harley Davidson, Coca-Cola, United Technologies and Visa on Tuesday, Boeing, Caterpillar, Ford, Facebook and AT&T on Wednesday, Amazon, Google and Intel on Thursday, and McDonalds and Twitter on Friday. At the time of writing we’ve had earnings reports from 69 of the S&P 500 companies so far with 78% beating on earnings and 64% on sales.

As for the rest of the data, the advance Q2 GDP reading in the US on Friday will be in the spotlight with the consensus expecting a +1.8% reading following +3.1% in Q1. We’ll also get June existing home sales on Tuesday, June new home sales on Wednesday, the preliminary June durable and capital goods orders data on Thursday along with the June advance goods trade balance. In Europe the only other data worth noting is the July IFO survey in Germany on Thursday and CBI survey data for July in the UK on Monday and Thursday.

Finally, other things worth keeping an eye on include Pakistan PM Imran Kahn making his first trip to the White House to meet with President Trump on Monday, the UK Lib Dem Party choosing their new leader on Monday, the IMF’s latest World

Economic Outlook update on Tuesday, and former Special Counsel Mueller testifying before the House Judiciary and Intelligence committees on Russian election interference on Wednesday.

Summary of key events in the week ahead, courtesy of Deutsche Bank’s Craig Nicol:

Monday: A very quiet day for data with only the June Chicago Fed national activity index in the US due for release. Halliburton will report earnings.

Tuesday: Data releases include final June machine tool orders in Japan, July CBI survey data in the UK, July consumer confidence for the Euro Area and the May FHFA house price index, July Richmond Fed survey and June existing home sales data all in the US. Companies reporting earnings include Harley Davidson, CocaCola, United Technologies and Visa. The next UK PM is expected to be announced while the IMF will release the latest World Economic Outlook.

Wednesday: The July flash PMIs in Japan, Europe and the US will be the main data focus. Away from that July confidence indicators are due in France, June M3 money supply data due for the Euro Area and June new home sales data due in the US. Earnings highlights include Boeing, Caterpillar, Ford, Facebook and AT&T. Former Special Counsel Mueller will testify before the House Judiciary and Intelligence committees on Russian election interference.

Thursday: The ECB monetary policy meeting will likely be the focal point of the day. As for data, in Europe we get the July IFO survey in Germany and CBI survey data in the UK. In the US the preliminary June durable and capital goods orders data is due in the US along with June wholesale inventories, July Kansas Fed survey and latest jobless claims data. As for earnings, Amazon, Google and Intel will report.

Friday: The focus of the data will be the advanced Q2 GDP revisions in the US. Prior to this the only data due in Europe is the July consumer confidence print in France. Earnings releases are also due from McDonald’s and Twitter.

Finally, looking at just the US, Goldman notes that the key economic data release this week is the Q2 advance GDP report on Friday. There are no scheduled speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, July 22

There are no major economic data releases scheduled.

Tuesday, July 23

09:00 AM FHFA house price index, May (consensus +0.3%, last +0.4%)

10:00 AM Richmond Fed manufacturing index, July (consensus +5, last +3)

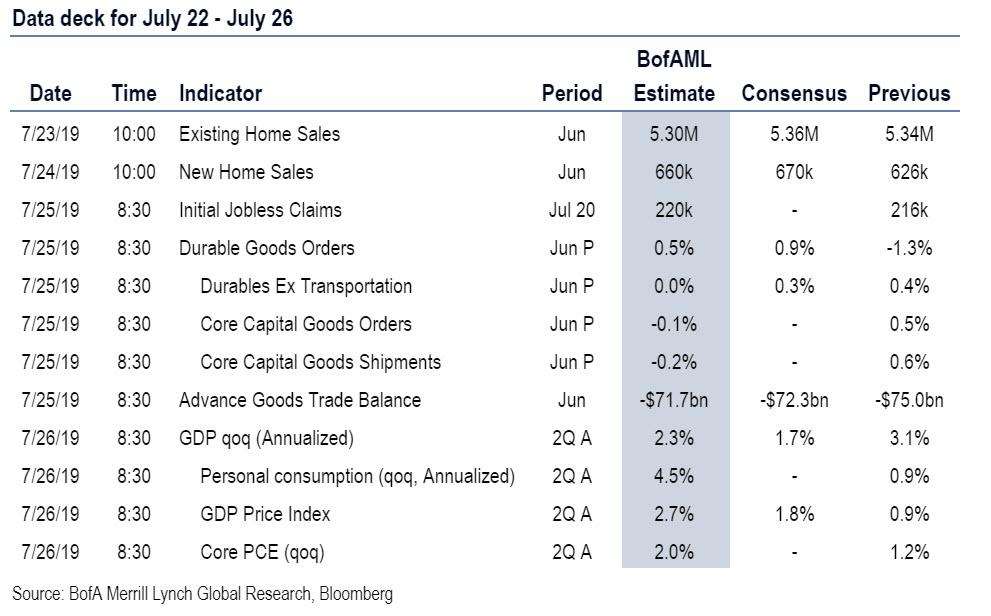

10:00 AM Existing home sales, June (GS flat, consensus -0.2%, last +2.5%): After rising 2.5% in May, we estimate that existing home sales were flat in June. Existing home sales are an input into the brokers’ commissions component of residential investment in the GDP report.

Wednesday, July 24

09:45 AM Markit Flash US manufacturing PMI, July preliminary (consensus 51.0, last 50.6)

09:45 AM Markit Flash US services PMI, July preliminary (consensus 51.8, last 51.5)

10:00 AM New home sales, June (GS +4.0%, consensus +5.4%, last -7.8%): We estimate that June new home sales rebounded 4.0% in June following a 7.8% decline in May, reflecting mean-reversion and a pick-up in mortgage applications.

Thursday, July 25

8:30 AM Durable goods orders, June preliminary (GS -0.3%, consensus +0.7%, last -1.3%); Durable goods orders ex-transportation, June preliminary (GS -0.1%, consensus +0.2%, last +0.4%); Core capital goods orders, June preliminary (GS -0.1%, consensus +0.2%, last +0.5%); Core capital goods shipments, June preliminary (GS -0.2%, consensus -0.2%, last +0.6%): We expect durable goods orders declined by 0.3% further in June, partly reflecting a further decline in commercial aircraft orders. We estimate core capital goods orders decreased by 0.1% and core capital goods shipments pulled back by 0.2%, as global manufacturing trends remain soft.

08:30 AM Advance goods trade balance, June (GS -$73.9bn, consensus -$72.4bn, last -$74.5bn): We estimate that the goods trade declined slightly to $73.9bn in June, following a rise in outbound container traffic.

08:30 AM Wholesale inventories, June preliminary (consensus +0.4%, last +0.4%): Retail inventories, June preliminary (consensus +0.2%, last +0.5%)

08:30 AM Initial jobless claims, week ended July 20 (GS 220k, consensus 219k, last 216k): Continuing jobless claims, week ended July 13 (consensus 1,693k, last 1,686k): We estimate jobless claims increased by 4k to 220k in the week ended July 20 after increasing by 7k in the prior week.

Friday, July 26

08:30 AM GDP, Q2 advance (GS +1.4%, consensus +1.8%, last +3.1%); Personal consumption, Q2 advance (GS +3.8%, consensus +4.0%, last +0.9%): We estimate a 1.4% increase in the initial release of Q2 GDP (qoq ar). We expect strength in personal consumption (+3.8%), but soft business fixed investment (-0.7%) and a 1.8pp drag from inventories.

Source: Deutsche Bank, Goldman, Bank of America

via ZeroHedge News https://ift.tt/30PdHpu Tyler Durden

Members of the FOMC might be in their “quiet period” ahead of the July Fed meeting, where the board is expected to cut interest rates by at least 25 bp, but President Trump’s attacks on the central bank continue.

In a series of tweets, Trump combines his criticisms of the central bank’s “misguided” policy with accusations that other countries are manipulating their currencies and Trump warned that it would be “Far more costly” for the Fed to wait to cut interest rates should a downturn take place, than to cut now and prevent a downturn by being proactive.

With almost no inflation, our Country is needlessly being forced to pay a MUCH higher interest rate than other countries only because of a very misguided Federal Reserve. In addition, Quantitative Tightening is continuing, making it harder for our Country to compete. As good…..

….as we have done, it could have been soooo much better. Interest rate costs should have been much lower, & GDP & our Country’s wealth accumulation much higher. Such a waste of time & money. Also, very unfair that other countries manipulate their currencies and pump money in!

It is far more costly for the Federal Reserve to cut deeper if the economy actually does, in the future, turn down! Very inexpensive, in fact productive, to move now. The Fed raised & tightened far too much & too fast. In other words, they missed it (Big!). Don’t miss it again!

In other words, Trump has basically strung together all of his prior criticisms of the Fed to remind policy makers with just over a week to go before their next policy meeting that he’s expecting a cut.

via ZeroHedge News https://ift.tt/2Yo2zC6 Tyler Durden

Following a massive fire at a Philadelphia refinery that sent gas prices higher across the Northeast, Philadelphia Energy Solutions LLC has filed for bankruptcy protection as the fuel-making company grapples with the aftermath of a June explosion and fire at its oil refinery that forced it to shut operations.

Now, for the second time in two years, the company has filed a Chapter 11 petition at the US Bankruptcy Court for the District of Delaware, BBG reports. It only just emerged from Chapter 11 in August 2018. But this time, its estimated liabilities are as high as $10 billion, according to the filings.

Last month, a leak at an alkylation unit, which is used to make high-octane gasoline, triggered an explosion that started a massive fire at the refinery, which forced the halt of activity at the refinery’s Girard Point section. The Point Breeze section, which had been running at a reduced rate, has likely run out of crude.

The East Coast’s largest oil refiner said in June that it was dismissing more than 1,000 workers and shutting its plant, which could process 335,000 barrels of crude oil a day.

The company had also been been putting the finishing touches on $150 million of DIP financing from owners and existing lenders, a person with knowledge of the matter said earlier this month.

The loan will allow the refinery to shut down safely, while pursuing $1.25 billion of insurance claims, the individual said.

Watch footage of the fire below:

A unit of Dallas-based Trinity Industries Inc. holds the largest unsecured claim, of almost $4.1 million, the court filings show. Other claims are held by CSX Transportation Inc. and BNSF Railway.

via ZeroHedge News https://ift.tt/2y1kwrk Tyler Durden

Thanks goodness for all the happy pictures of Prince George’s Birthday across the papers this morning. Not much else to celebrate here in Blighty. We’re about see a screed of cabinet ministers resign before they are pushed, while other Tories are threatening to decamp to the Liberals.. (which is likely to prove a career call ranking alongside joining Deutsche’s equity trading team..). The prospect of Boris? The Scots are going to demand immediate independence. What could possibly make the mood worse? All we really need now to complete the misery would be something scandalous from up in the Turnip growing regions.. and the country will tip into utter despair and despondency…

There is plenty of noise out there – tankers being seized in the Gulf, more demonstrations in Hong Kong and Trump digging his hole even deeper. Much talk over the weekend about how the US news about Trump’s racism is covering up the real story of the summer – who has Jeffrey Epstein been pimping for? More will no doubt be revealed. In terms of investments – passive stock funds do best, alpha funds trying to beat the market lost. The market can stay irrational longer than you can stay solvent has never been more true.

In terms of markets the coming two weeks are likely to be dominated by Central Banks. What addictive crack of lower rates and QE infinity will the ECB foist on Europe? After last week’s spat about Fed members giving poorly coordinated academic speeches to market audiences suggesting a double cut was on the way, what will Fed do at the end of the month? (The answers: i) wait, and kick the can down road, ii) 25 bp ease.)

This really is not a good time to be a central banker. For a start, the last 10 years of stunning economic growth and shared wealth expansion across the global economy, the last 10 years of stuttering faltering growth, monetary experimentation, rising social and wealth inequality and pointlessly low interest rates is being squarely blamed on their policy responses. Their solution? More of the same… It’s not a confidence building agenda.

The dangers are about credibility – what does the increasing politicisation of Central Banking mean for markets as their credentials are increasingly strained? The theme central bankers have screwed up and governments can’t be trusted is being exploited by crypto-currency snake oil salesman, and by big business that understands the attractions of non-government fiat money – unregulated – which is why banks are flirting with crypto and Facebook dipped its Libra idea to test the waters. Others are trying to crypo-ize gold – one scheme I’ve seen is a gold crypto coin backed by a fortress-vault hidden in the Swiss alps guarded by former Mossad agents! The consequences of a fiat breakdown could be horrible.

Central banks being independent is a comparatively recent notion. Giving them tightly defined objectives was designed to stop them simply juicing Government policy – but given the last 10-years of economic mayhem its hardly surprising they “tried to help”. Just a shame it’s gone so badly.

There are variations on the problems of Central Banking. The ECB is about politics – rebuilding Europe’s moribund economy needs a political figurehead to move on from the Mario Draghi age and pull Europe towards agreement on fiscal policy. However, do the German’s get that? It really worries me when I read an in-depth report by a German bank on domestic politics, and it doesn’t mention Europe once! Without German participation and agreement on fiscal union, then Europe and the Euro remains an ongoing crisis.

The Fed is a very different matter – Trump behaves like it’s his own personal piggy bank, at his beck and call to support the illusion he’s selling to his part of the electorate: “hey look, I’ve made the stock market strong, therefore I’ve Made America Great!”. For the Fed to capitulate would be a very bad thing indeed.

Why? Oh, would you really like the last 10-years of monetary distortion on financial assets to continue, ultra-low rates, corporate leverage, income inequality and financial asset inflation? Well, lots of short-term market professionals say yes – what’s not to like about rising bond and equity prices… Oh, nothing, except the higher they go, the more distorted they become..

The result is bad financial allocations – money chasing over-expensive financial assets and pushing investors to buy impossibly tighter, less liquid and more risky junk bonds and dimly understood equity models. Paying more for lower returns and lower liquidity is not a smart investment policy. And it’s just as bad in stock markets – last week I got pages of abuse for not understanding the value of Netflix. What’s not to understand? They charge too much for a lacklustre product while customers are leaving/not signing up and going elsewhere to binge-watch, while markets will be increasingly sensitive to funding them. But people buy it on the dips because they believe?

Being a central banker today has become a matter of patronage. The IMF job – which is traditionally run by a European – will be decided by the EU Brussels Blundership, largely on the basis that since Europe’s socialists didn’t get much of a share of the Brussels Jobs for the Boys, then they will get the IMF sinecure as a consolidation prize. Which one? Doesn’t much matter… But, no offense to unoffensive Dutch Finance Minister, Jerome Dijsselbloem, whomever Europe nominates is likely a bad compromise.

The best known technocratic central banker without a seat at the new table looks to be Mark Carney. He hasn’t been everyone’s cup of tea while head of the Bank of England, but he is a proper banker, rather than a second-career politician. He’s got the technical credentials and head for detail that’s needed to build credibility – a critical role for central bankers in today’s fervid markets. If confidence in the IMF and other global institutions wanes because its seen as European sideshow (which it became under Legarde), then the next move is not a compelling one.

Back to the UK…

Rumours and counter rumours about the soon to be upon us “First 100 Days of Boris” – which will incidentally be November 1st, the day after Boris promises we leave Europe with or without a deal. Without being harsh, opinionated or balanced – I give him ZERO chance of success. But I’ll be delighted if he can pull it off.

How will his rumoured European charm offensive work? Is Europe preparing a coordinated and enticing new deal for him? Is there a solution? Does Boris think an easier Irish backstop and more open dialog with Europe will pass muster with the No-Deal Brexit hard wing? Oh what fun we have to look forward to. Still selling sterling…

My immediate bet remains an Early Election as it becomes clear i) he can’t command a majority, ii) he can’t close any deal, and then line up another Tory Leader as the UK fragments.

via ZeroHedge News https://ift.tt/2SwvAGp Tyler Durden

It was the biggest hack of private data in modern history, and now, two years later, Equihacks Equifax has agreed to pay up to $700 million to resolve U.S. federal and state investigations into the 2017 hack that compromised the most sensitive information of 147 million people.

The resolution with the Federal Trade Commission, Consumer Financial Protection Bureau and 50 state attorneys-general draws a line under the hack, the largest-ever breach of consumer data. The credit scoring company has also settled with claimants in a class-action lawsuit.

“Equifax failed to take basic steps that may have prevented the breach that affected approximately 147 million consumers,” said Joe Simons, FTC chairman, in a statement on Monday morning.

“This settlement requires that the company take steps to improve its data security going forward, and will ensure that consumers harmed by this breach can receive help protecting themselves from identity theft and fraud,” he added.

Equifax will also pay as much as $425 million to compensate consumers – which works out to about $3 per affected individual so don’t spend it all at once – and will provide credit monitoring to those whose information was exposed. Equifax will separately pay $175 million to 48 states, the District of Columbia, and Puerto Rico, and an additional $100 million to the U.S. Consumer Financial Protection Bureau.

The agreement which is the largest data-security settlement by the agency, resolves a nearly two-year investigation by all 50 states and the FTC into the massive breach that compromised sensitive information like Social Security numbers and dates of birth, Bloomberg reported.

While the incident sparked outcries in Washington and among consumer advocates for more oversight of the three big consumer credit-rating companies: Equifax, TransUnion and Experian, culminating with a February hearing in which Democrats and Republicans on the House Financial Services Committee slammed the companies as Chairwoman Maxine Waters promised to tighten regulation of the industry, lawmakers have so far failed to act since the hack was disclosed.

In May 2017, hackers gained access to the Equifax network and attacked the company for 76 days, without the company being aware it was infiltrated. Equifax noticed “red flags” in late July, and then in early August contacted the Federal Bureau of Investigation, outside counsel and cybersecurity firm Mandiant. The company waited until September to inform the public of the breach.

As part of the hack, at least 147 million names and dates of birth, nearly 146 million Social Security numbers, and 209,000 payment card numbers and expiration dates were stolen, the FTC said, adding that Equifax failed to patch its network after being alerted in March 2017 to a critical security vulnerability affecting a database that handles inquiries from consumers about their personal credit data. Equifax’s security team ordered that vulnerable systems be patched, there was no follow-up to ensure the order was carried out, the FTC said.

Under the FTC settlement, Equifax will pay up to $425 million into a fund that will provide affected consumers with credit monitoring. The fund will also compensate consumers who bought credit- or identity-monitoring services from Equifax and paid other expenses as a result of the breach, the FTC said. The company also will implement an information-security program that will require annual assessments of security risks, obtaining annual certifications from the board of directors that the company has complied with the settlement, and testing security safeguards.

via ZeroHedge News https://ift.tt/2O8Y4rf Tyler Durden