President Trump tweeted on Saturday that he is considering labeling the militant, black-clad, mask-wearing ‘anti-fascist’ group known as Antifa as a terrorist organization, just one week after GOP Senators introduced a bill to “properly” identify the group as domestic terrorists.

“Consideration is being given to declaring ANTIFA, the gutless Radical Left Wack Jobs who go around hitting (only non-fighters) people over the heads with baseball bats, a major Organization of Terror (along with MS-13 & others),” tweeted Trump, adding “Would make it easier for police to do their job!”

Consideration is being given to declaring ANTIFA, the gutless Radical Left Wack Jobs who go around hitting (only non-fighters) people over the heads with baseball bats, a major Organization of Terror (along with MS-13 & others). Would make it easier for police to do their job!

Antifa has gained notoriety since the 2016 election for instigating violent confrontations with conservatives – most recently journalist Andy Ngo, who was beaten and robbed by members of Portland’s Antifa cell, sending him to the hospital.

In July, 2018, the same Portland groupl, Rose City Antifa, planned a “direct confontation” with participants at a pro-Trump rally – “calling for militant antifascist resistance against Patriot Prayer,” according to a call to action on the leftist website, “It’s Going Down.“

The previous month, a clash between the groups ended up in a viral video of an Antifa member using an object to assault conservative Ethan Michael Nordean, also known as Rufio – who subsequently knocked out the ‘terrorist’ (or so he would be classified under the new declaration).

Last week, GOP Sens. Ted Cruz (R-TX) and Bill Cassidy (R-LA) introduced a bill to classify Antifa as domestic terrorists – defining it as “a movement that intentionally combines violence with the group’s alt-left positions,” and “represents opposition to the democratic ideals of peaceful assembly and free speech for all.”

As noted by The Blaze, however, labeling Antifa as “Domestic Terrorists” may also require an entirely new law.

federal law does not have the same clear-cut designation for domestic terrorism organizations that it does for foreign terror organizations (FTOs), explained Andy McCarthy in a 2017 column at National Review.

“There are federal-law processes for designating foreign and international terrorism because defending against foreign threats to national security is primarily a federal responsibility,” McCarthy explained, because foreign operatives have fewer civil rights protections than American citizens and that the best weapon against domestic terror is local law enforcement, not federal. –The Blaze

Well, here we are. All roads have led to here. The combustion case outlined in April, the technical target zone outlined in January of 2018. Trade wars, 20% correction in between, Fed capitulation in response, slowing growth data, inverted yield curves, political volatility, deficit and debt expansion, buybacks. All the big themes that have dominated the landscape in recent memory, they all have led us to here: Record market highs and high complacency into a historic Fed meeting where once again a new easing cycle begins.

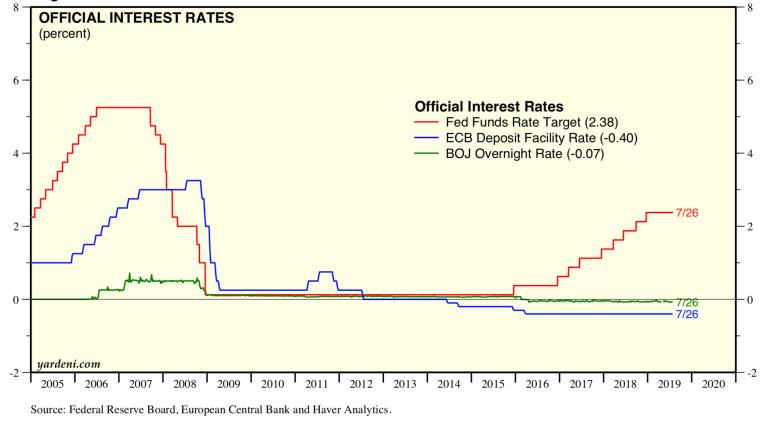

Like flies drawn to a light investors have ignored everything that may be construed as negative as the market’s primary price discovery mechanism, central banks, are once again embarking on a global easing cycle from the lowest bound tightening cycle ever. By far. Many central banks such as the BOJ and ECB have never normalized, the Fed barely raising rates before capitulating once again to macro and market reality:

What’s the end game here? I have to ask given the larger backdrop:

Central banks 2009-2018:

We will print $20 trillion & cut rates to nothing & that will reach our inflation goals.

Central banks 2019: Ok, none of that worked so let’s print more & cut rates again.

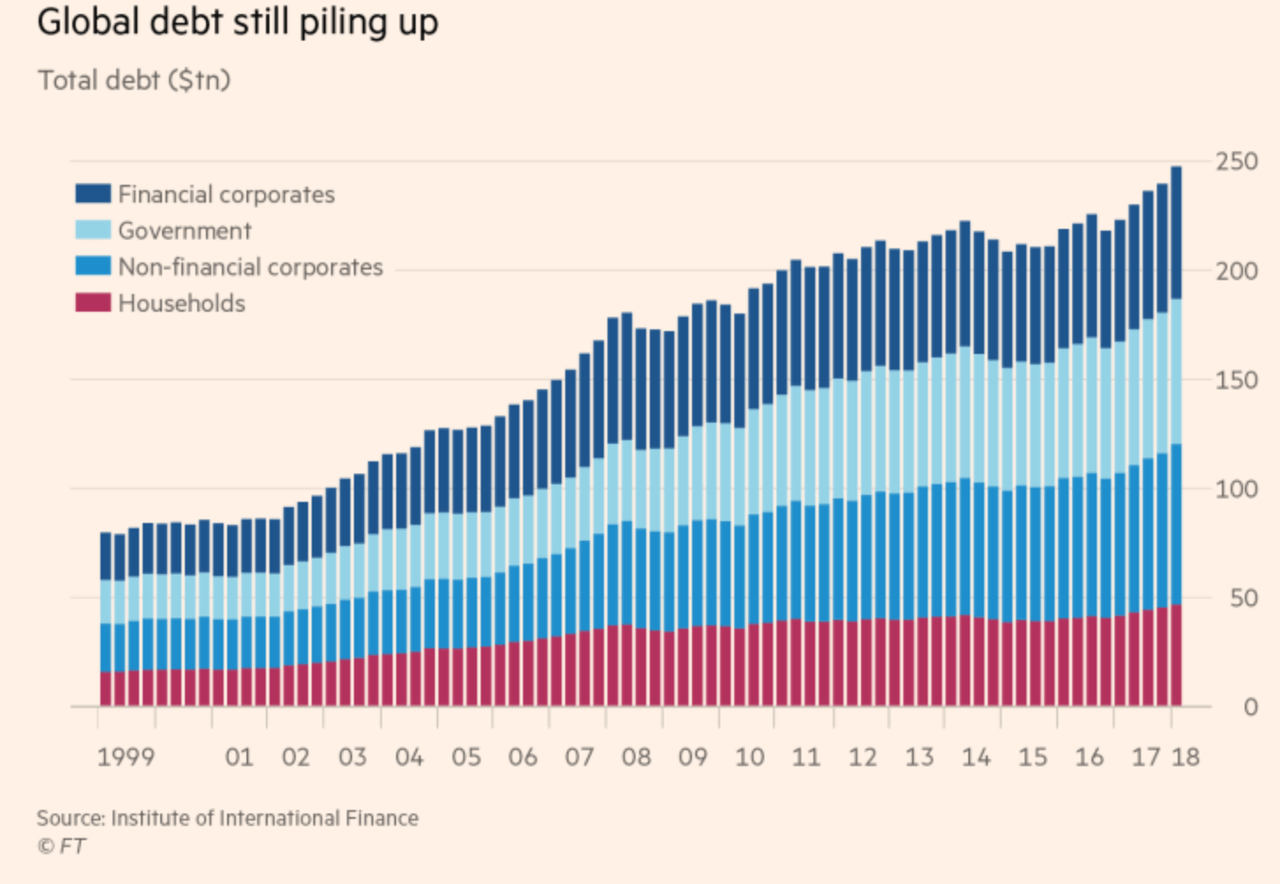

What has all this produced? For one the slowest recovery on record, but also the longest expansion. But this expansion has come at a very steep price as artificial low rates have led to massive record debt expansion, $250 trillion in global debt:

The world is sitting on over $13 trillion in negative yielding debt, corporate debt ballooned to all time highs is keeping zombie companies afloat, the desperate search for yield is forcing pension funds into riskier assets, 100 year bonds, BBB rated credit is the largest component of debt markets, everything is distorted and the desperate search for yield has produced another market bubble.

How to define a market bubble? Simple, take the valuation of stock markets over the underlying size of the economy and the size of this bubble is self apparent:

Perspective:

Current US Stock Market Capitalization: 144.8% of GDP

Peaked in 2017 at 154%

For reference: The previous 2 peaks came in at 146% in 2000 & 137% in 2007.

Asset prices remain historically disconnected from the size of the underlying economy.

Sustainability: Questionabl pic.twitter.com/EIypajbIu1

I don’t know what fair value is in this distorted world, but the historic mean is significantly lower and it’s only truthful to acknowledge that central banks have sizably contributed to an artificial excess in the ratio.

It’s not a central bank put, it’s a central bank bubble. In other words: To be buying stocks here based on the Fed put is to believe that central banks can maintain asset values above the underlying size of the economy at a historically unsustained level especially in a period of slowing growth.

Following the period of the largest global central bank intervention on record (2016-2017) US tax cuts were promised to deliver 4% growth:

“With the tax plan, we’re going to easily see 4 percent growth next year” – National Economic Council director Gary Cohn December 2017

Gary was of course not the only one, Kudlow, Trump, Ryan, all the pushers behind the big tax cut were promising the moon. None of that came to fruition.

Reality: We didn’t even get 3% growth. US GDP for 2018 was just revised down to 2.9%. Second quarter 2019 GDP has just slowed down to 2.1% and the entire globe is struggling with growth across the board. “Things are getting worse and worse” Mario Draghi head of the ECB said this week.

And it is:

So let’s acknowledge reality here: US tax cuts have done absolutely nothing to change the growth trend in GDP in this cycle:

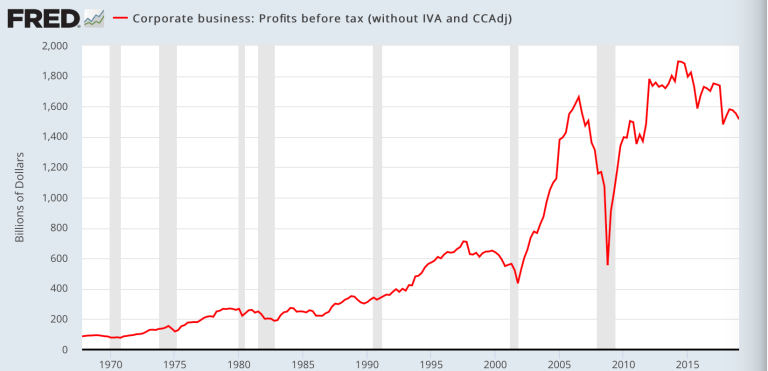

Has it translated into cast corporate profits? Not really.

Corporate profits before taxes in aggregate peaked in 2014:

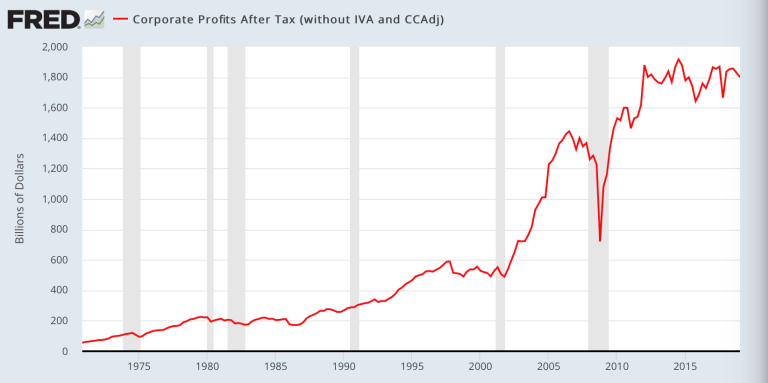

This is not an image of expanding profits. What tax cuts have done is minimize the fallout of the decline:

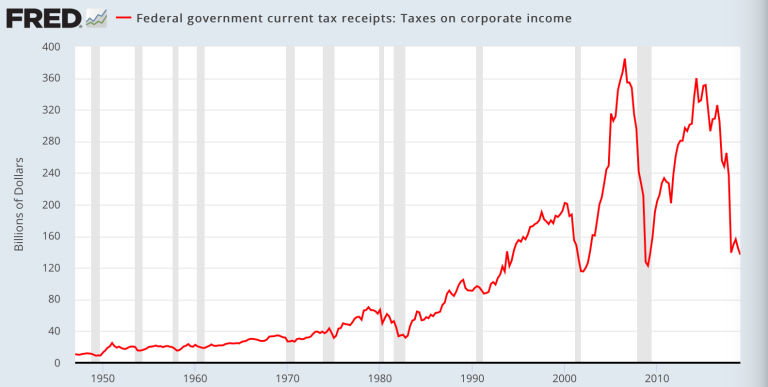

And this is what it took:

A total collapse in tax receipts on corporate income. Corporate tax receipts are now lower than in 1995 with an economy that is much larger.

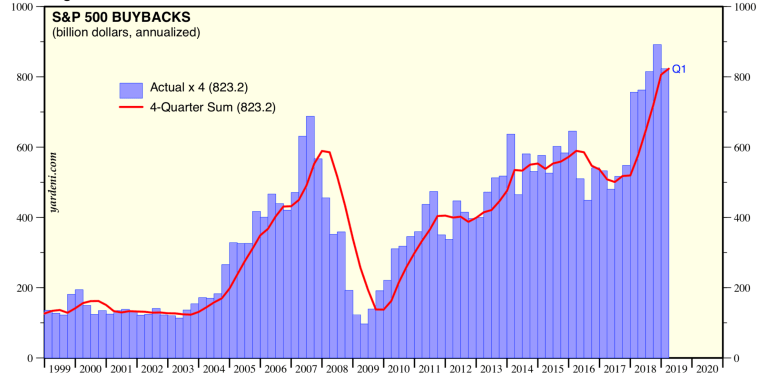

And we know what corporations are doing with the windfall. It’s not an increase in Capex, or business investment (both of which are declining), but it’s been a massive expansion into share buybacks. Via Yardeni research:

We can observe an accelerating trend similar to the one in the lead up to the 2007 market top when the Fed was also forced to cut rates. And forced the Fed is. It has boxed itself into a corner where it hardly can afford to disappoint markets. After accidentally setting expectations for a 50bp rate cut via ill communicated speeches just one a week ago, the Fed quickly corrected market expectations and consensus is now for a 25bp rate cut. An insurance cut it is advertised as.

Is it?

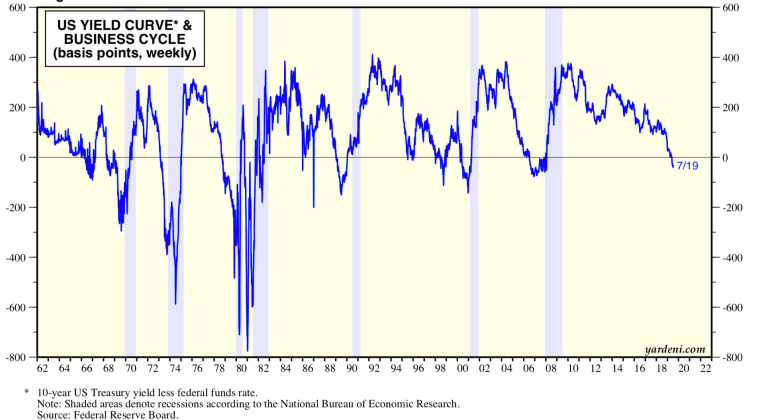

The yield curve picture is sending a message that suggests this is no insurance cut:

These yield curves is what has the Fed freaking out and cutting. The problem of course is this: In 2001 the Fed had to cut by 525 bp. In 2007 they had to cut by 500 bp. This cycle they’re starting from 225bp. Never before has stock market capitalization versus the economy been this high with the Fed having such little ammunition.

There are historical examples where “insurance” rate cuts helped delay the inevitable, notably 1998 and the 1980s. But the 1980s also had a market crash and the 1998 example resulted in the tech bubble and subsequent crash making both examples not exactly inspiring examples of success. Is this the end game, blow a massive market bubble?

With a stock market running at a capitalization of 145% of GDP with no history of being able to sustain above these levels, is this the end game here? Blow an even bigger bubble? And that’s the issue I see with talking about an insurance cut being successful here: Markets are already in historically extended valuation territory relative to the size of the economy. Buyers beware.

So what is the world doing to combat slowing growth? Nothing. Everybody is relying on central bankers to save us all again. Politicians have given up, if they ever really tried. There is zero discussion of structural solutions by anybody. Nobody is even trying to have a discussion. Economists are increasingly talking about MMT (money printing forever) and central banks are talking about people QE in light of rates going more negative in Europe.

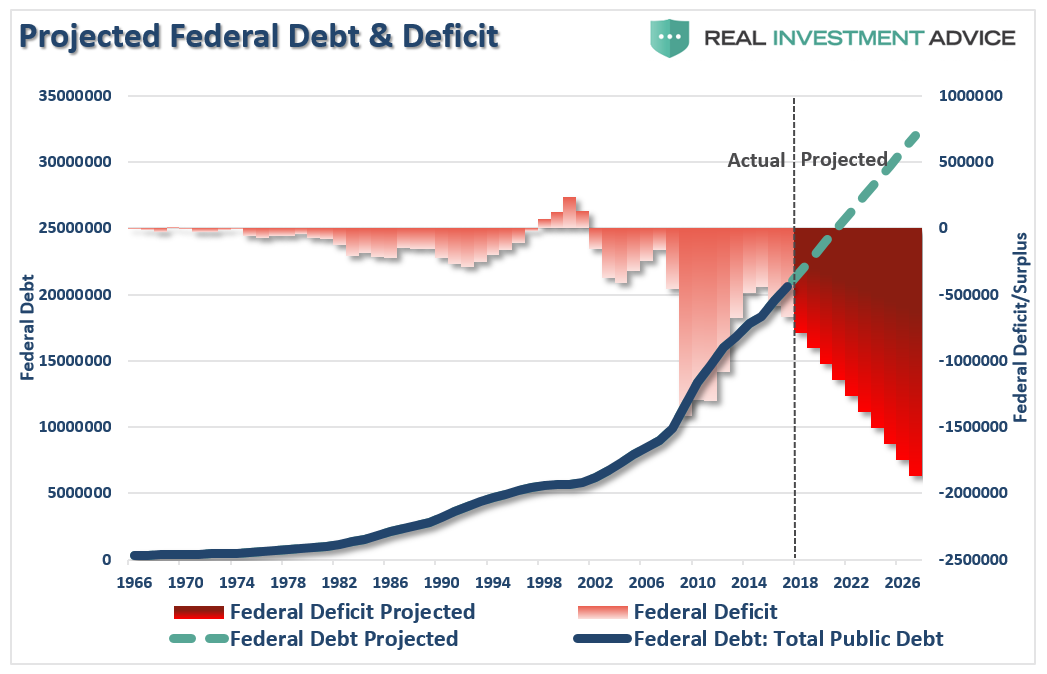

In the US deficits are hitting trillion dollars with no end in sight. As divided and distracted the country is by political inflammation, propaganda and hate both parties agree on one thing: Spend more money. A monstrosity of a budget was agreed to by the House this week further exacerbating deficits and raising the debt ceiling for another meaningless deadline. We’ll see if it passes the Senate, but here’s what we’re faced with:

“The deal suspends the debt limit through July 2021 and sets top-line levels for defense and nondefense spending for the next two fiscal years. It establishes a $1.37 trillion budget agreement in the first year, with $738 billion for defense spending and $632 billion in non-defense spending for fiscal year 2020.”

$738B for defense versus $632B non-defense spending. Now let’s cut food stamps to save.

I’m highlighting all this to make clear: There are no solutions on the horizon. There is no dedicated serious leadership on either side of the political isle to address any structural solutions. None. There is nothing but debt expansion and hope that the Fed can extend the business cycle by inflating stock prices to above 145% of GDP.

That’s it.

Businesses are not investing in growth while consumers are loading up on credit card debt. What do businesses know that consumers do not yet?

Are businesses simply waiting for a China deal? Well, then they may be waiting for a long time as Donald Trump dialed back expectations on Friday suggesting China may want to wait to make a deal until after the 2020 election.

Whether posturing or not fact is there is no China deal and absolutely nothing has changed on the structural growth front.

But here we are:

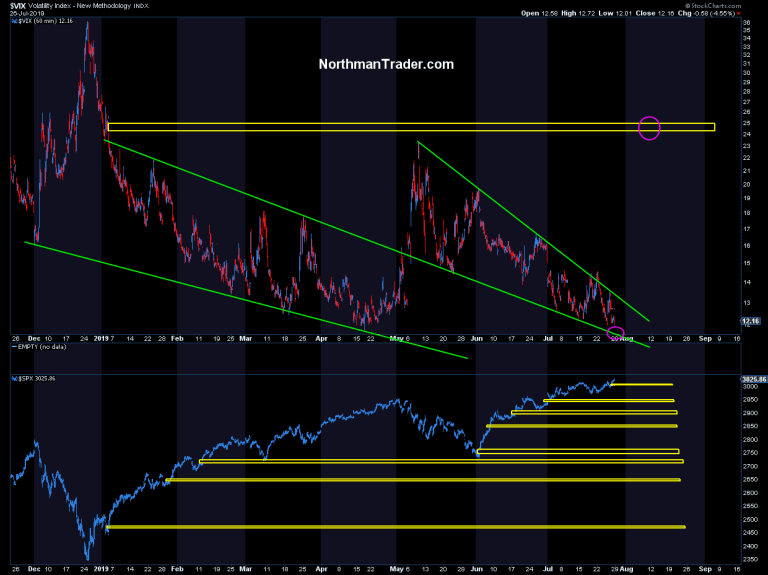

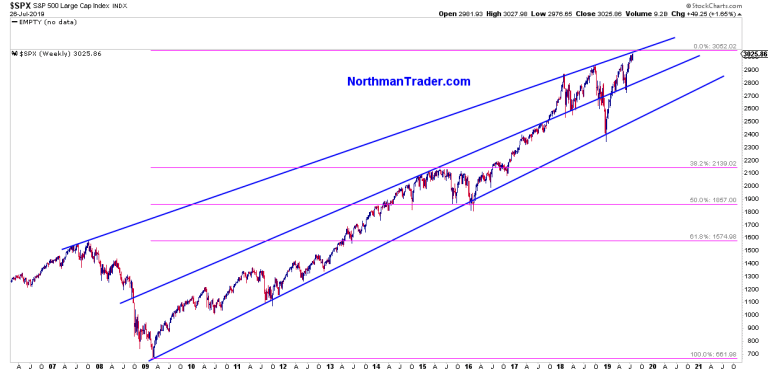

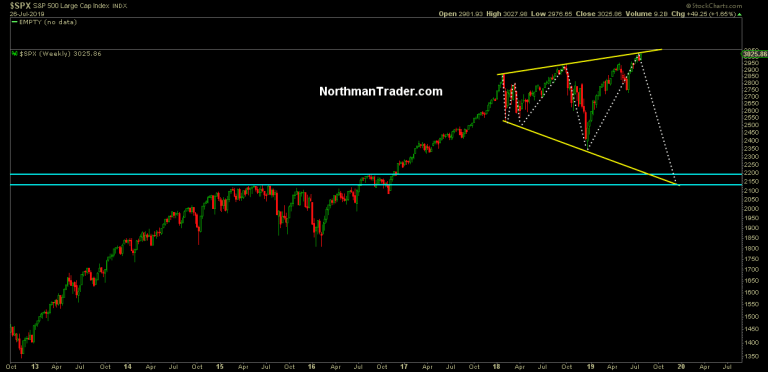

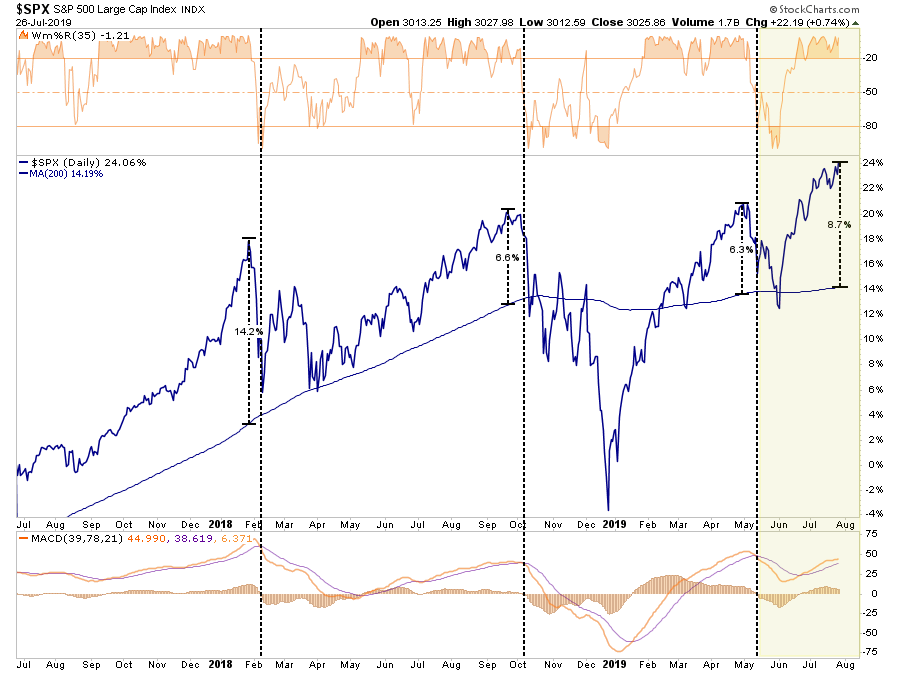

New highs $SPX on a negative divergence amid volatility compression, right into the upper trend line outlined in the megaphone structure we’ve been discussing.

I’ve repeatedly outlined the 3000-3050 $SPX area (see also recent Weekly Market Briefs , Distortion) to be a key technical resistance zone and markets have pushed into the middle of this zone right ahead of the Fed.

I’ve outlined several technical concerns about this rally (see also This Week on NT).

To highlight two: Open gaps and volatility compression:

A subject I discussed on Friday on CNBC:

What’s the risk profile into this important Fed meeting then?

On the $VIX its further compression into the lower trend line, but in context of a pattern that is looking to break out hard at some point.

In regards to markets 2 key charts from the previous risk profiles:

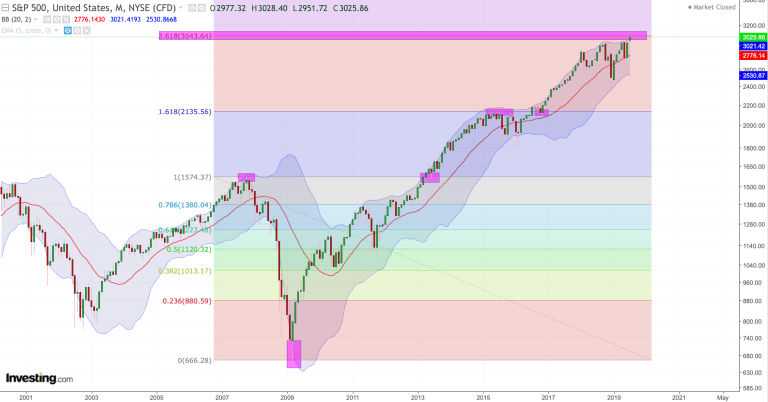

$SPX is a stone’s throw away from its 2.618 fib:

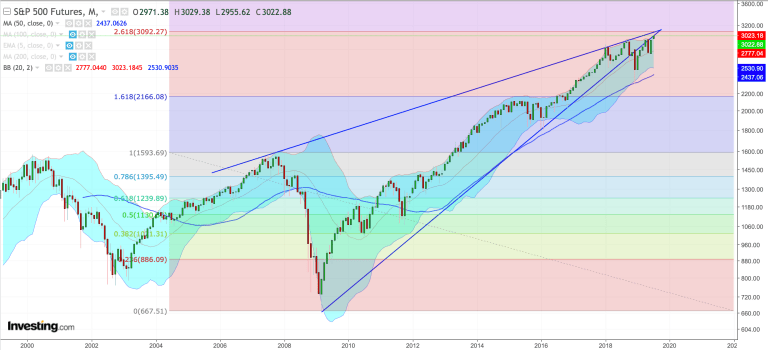

$ES has further theoretical room to go (Per Combustion):

On the larger trend profile there’s also room into 3052 or so:

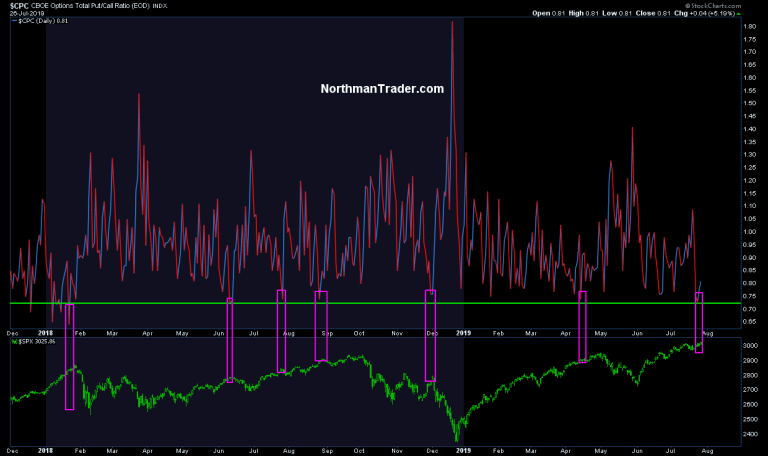

Off of the 2018 lows the Fed capitulation and policy turn has produced a massive rally into a key resistance zone. Markets are fully expecting a rate cut his week and have ignored all negatives in markets with the expectation that the Fed will spark another squeeze in equities. In 2007 the first cycle rate cut of 50bp led to a two week rally for the final top. This rally here has entered a key resistance zone we’ve outlined to be a potential massive sell zone in equities. This week and the one that follows may then be pivotal for this market. A breakout cannot be excluded as a possibility, neither can a fake breakout that reverses or an outright violent rejection of the risk zone. What the Fed can’t afford is disappoint markets or the political establishment that wants the Fed to cut rates aggressively. Investors are apparently unconcerned either way and are betting on a positive outcome as evidenced by a very low put/call ratio:

We are in a unique period in history. The end game is approaching. An extension of the market bubble above 145% stock market capitalization to GDP or a reversion back toward more of a historical mean which is what the current technical and macro environment suggests:

As suggested last week this is a big battle for control. Investors as of now are pursuing a 10 year standing motto:

In Fed we trust.

Best of luck.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2ZcsBpc Tyler Durden

Following Trump’s ambitious multi-billion dollar ‘space force’ coming closer to fruition, especially after last month the Democratic-controlled House Armed Services Committee voted to give Trump his expensive program, though they want it called the “Space Corps,” Russia has warned of a new space arms race which could endanger humanity.

Russian Foreign Minister Sergey Lavrov said Friday at the session of the Council of Foreign Ministers of BRICS (Brazil, Russia, India, China, South Africa) countries, “We are concerned over US plans to deploy weapons in space that are already being implemented. This will lead to another qualitative stage of an arms race,” according to TASS.

Russian FM Lavrov Image source: TASS

“As you know, Russia and China have already presented a draft proposal on preventing deployment of weapons in space at the disarmamanet conference in Geneva. We appreaciate it that BRICS countries support annual resolutions on this pressing issue at UN General Assembly sessions,” he added.

The growing concern comes amid the breakdown in key missile defense treaties, such as the Intermediate-Range Nuclear Forces (INF) which both countries have already pulled out of, and concern that the New START (Strategic Nuclear Reduction Treaty) could also be faltering.

Moscow has long blamed the United States for reigniting a global arms race not witnessed since the Cold War:

“Worrisome examples are US efforts to break down the missile defense treaty and . Uncertainty also persists around the INF [Intermediate-Range Nuclear Forces] Treaty. We have suggested to extend it but have not heard a response from Washington yet,” Lavrov concluded.

However, when Trump first unveiled plans for a US ‘space force’ last year he cited precisely China and Russia as getting a “head start” in militarizing space. Russian defense leaders as well as Russian media have long denied that the Kremlin is seeking to weaponize space.

“Russia has already started, China has already started. They’ve got a start, but we have the greatest people in the world, we make the greatest equipment in the world, we make the greatest rockets, and missiles, and tanks, and ships in the world.”

Image via OZY

When Trump first shocked the world by announcing the program in June of 2018, he expressly said at the beginning of his comments that “we must have American dominance in space.” And followed with: “Very importantly, I am hereby directing the Department of Defense and Pentagon to immediately begin the process necessary to establish a Space Force as the Sixth Branch of the Armed Forces.”

But there is evidence to suggest Trump’s words about a Russian leg up in military space capabilities are accurate. Per a prior report in Axios, “Russia has had sophisticated launch systems for decades, in addition to another that tracks objects more than 30,000 miles above the Earth, according to the CSIS 2018 Space Threat Assessment.”

And further a separate recent report from the Director of National Intelligence found that both China and Russia are working to develop anti-satellite weapons “that could blind or damage sensitive space-based optical sensors, such as those used for remote sensing or missile defense.”

The Pentagon and Air Force have put estimates for the new Space Force at $8 billion and $13 billion, respectively.

via ZeroHedge News https://ift.tt/2KefT3c Tyler Durden

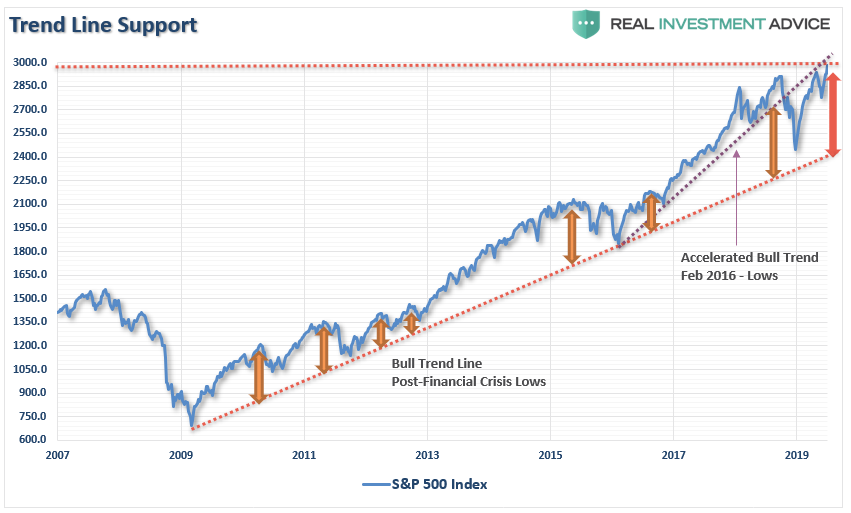

Last week, we discussed the setup for a near-term mean reversion because of the massive extension above the long-term mean. To wit:

“There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

This analysis is what led us to take action for our RIAPRO subscribers last week (30-Day Free Trial), as we added a 2x-short S&P 500 index fund to Equity Long-Short Account to hedge our longs (GOOG, CRM, NVDA, EMN, IVV, RSP) against a potential mean reversion.

“This morning, we are adding a small 2x S&P 500 short position to the trading portfolio to hedge our core long positions against a retracement over the next few weeks. We will remove the short if the market can regain its footing and move higher, or the market sells off and reaches oversold conditions.”

This is the purpose of hedging, as it reduces volatility over time, which inherently reduces the risk of emotionally based trading mistakes.

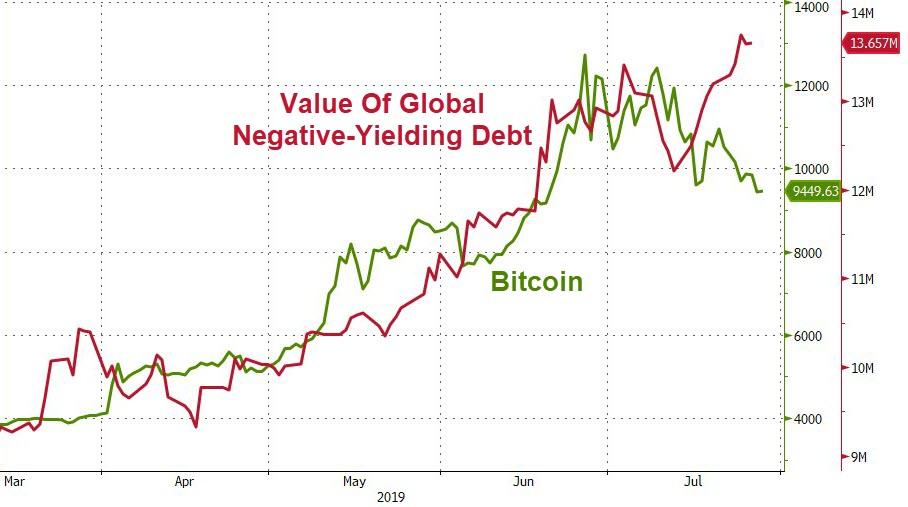

“The mean reversion trade: For the past few weeks I’ve been musing that the “irresistible force” that has moved all markets has been the aggressive repricing of future interest rate expectations since last November. We’ve had a HUGE rally in the bond market, MASSIVE flows into bond funds, record levels (>$13.7T) of negative yielding bonds, inverted yield curves, even Greek bonds trading through Treasuries…as markets anticipate a recession and much more Central Bank largess…which might just take us into MMT and/or never-never land where the Central Banks just buy all the bonds and that’s that. I’ve thought that this irresistible force may have gone too far too fast and was due for a “set-back” which would precipitate mean reversion trades across markets.

The core concepts of the mean reversion trades I’m considering are as simple as, 1) the public buys the most at the top (thank you, Bob Farrell,) and 2) when they’re yelling you should be selling, and 3) positioning risk leaves some markets especially vulnerable.”

They are exactly right.

While the market is rallying in anticipation of more Central Bank easing, especially following the recent announcement by the ECB of lower rates and more QE, the markets are momentarily detached from weaker earnings growth, weaker economic growth, and a variety of other market-related risks.

However, in the very short-term, the market is grossly extended and in need of some correction action to return the market to a more normal state. As shown below, while the market is on a near-term “buy signal”(lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.

As we have noted over the last few weeks, the very tight trading range combined with negative divergences also does not historically suggests continued bullish runs higher without some type of corrective action first.

All of this supports why we trimmed our long positions slightly last week and increased our cash holdings for the time being.

Our models still suggest a likely correction over the next two months as we move past the Fed. Such is particularly the case if the Fed signals their “rate cut” may be “one and done” for the time being.

But for now, we are going to opt to “wait and see” what happens.

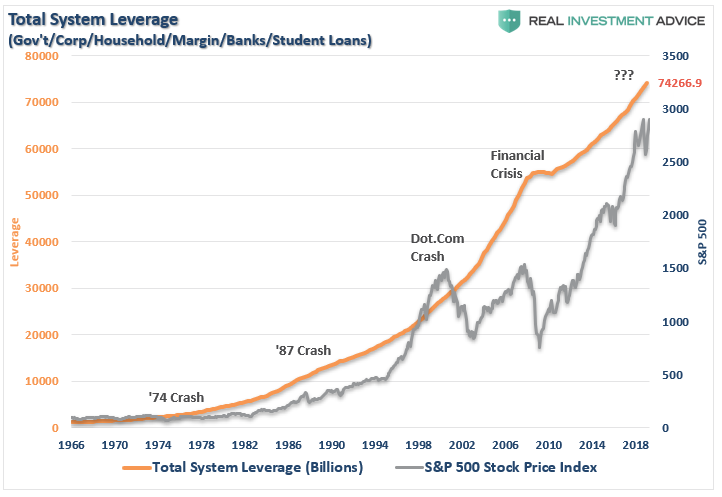

The $70 Trillion Dollar Graveyard

On Thursday, Congress passed the spending bill we discussed last week:

“A divided House on Thursday passed a two-year budget deal that would raise spending by hundreds of billions of dollars over existing caps and allow the Government to keep borrowing to cover its debts, amid grumbling from fiscal conservatives over the measure’s effect on the federal deficit.

65 Republicans joined the Democratic majority in the 284-149 vote, with 132 Republicans voting against the bill, despite President Trump’s endorsement and pressure from key outside groups, including the Chamber of Commerce, to avoid a potentially catastrophic default on the Government’s debt.”

I highlighted the last sentence in red because it is an outright “LIE” used to convince Americans that out of control spending must be done.

The reality is that “interest payments on the debt” are part of the MANDATORY spending in our budget along with social security, medicare, etc. Currently, about $0.75 of every dollar of tax revenue goes to mandatory spending. For the last few months the Government has been at its statutory debt limit, and “surprise” we didn’t default on our debt. Why? Because there is enough revenue currently coming in to cover the mandatory spending.

“In 2018, the Federal Government spent $4.48 Trillion, which was equivalent to 22% of the nation’s entire nominal GDP. Of that total spending, ONLY $3.5 Trillion was financed by Federal revenues, and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare and interest on the debt, those payments required $3.36 Trillion of the $3.5 Trillion (or 96%) of revenue coming in.”

Do some math here.

The U.S. spent $986 billion more than it received in revenue in 2018, which is the overall ‘deficit.’ If you just add the $320 billion to that number you are now running a $1.3 Trillion deficit.

The U.S. will not default on its debt.

This is particularly the case since we no longer have any budgetary controls.

Importantly, the spending increase of $320 billion is on top of the annual 8% automated budget increase and the preexisting deficit. My original projection above is too conservative by $500 billion, or more.

But that’s not the real story.

The crux of that article was focused on the roughly $6 Trillion of unfunded liabilities of U.S. pension funds which Congress is now drafting a piece of legislation for entitled the “Rehabilitation For Multi-employer Pensions Act.”

As noted in that article, while Congress is preparing a bailout for U.S. pension funds, there is a $70 Trillion pension problem globally which is not being addressed.

“According to an analysis by the World Economic Forum (WEF), there was a combined retirement savings gap in excess of $70 trillion in 2015, spread between eight major economies…

However, this isn’t the $70 Trillion graveyard we are addressing today. From CNN:

“America’s debt load is about to hit a record. The combination of cheap money and soaring debt helped fuel the decade-long economic expansion and bull market, but America’s gluttony of loans could work against it if its fragile economic balance shifts.

In the first quarter of 2019, the United States’ total public- and private-sector debt amounted to nearly $70 trillion, according to research by the Institute of International Finance. Federal government debt and liabilities of private corporations excluding banks both hit new highs.”

Oh…you are talking about THAT $70 Trillion.

The chart below is Total U.S. Credit Market Debt (including Student Loans) which is currently running just a smidgen over $74 Trillion.The last time there was even a hint of deleveraging was during the “Financial Crisis.”

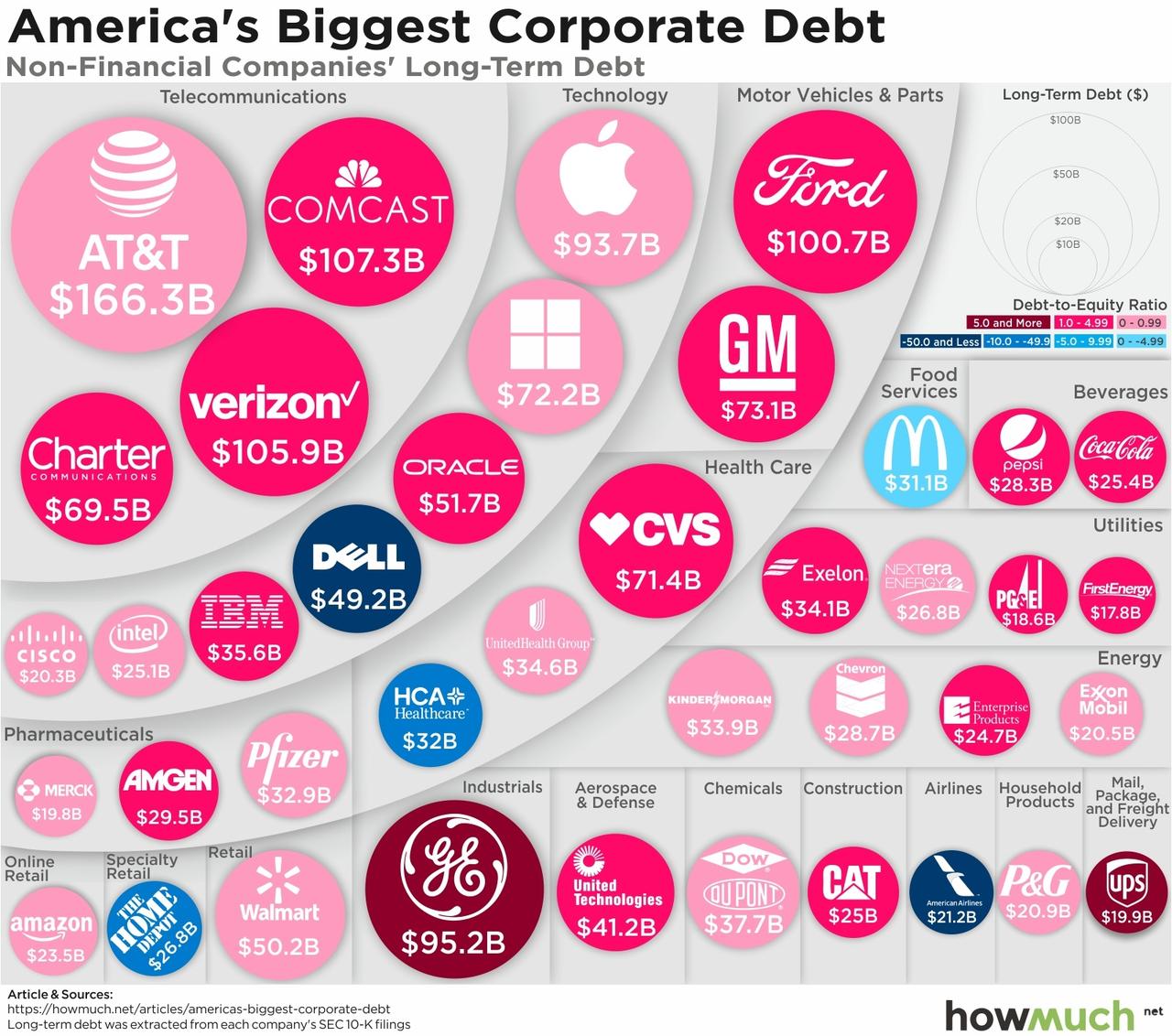

Corporate debt is a problem.

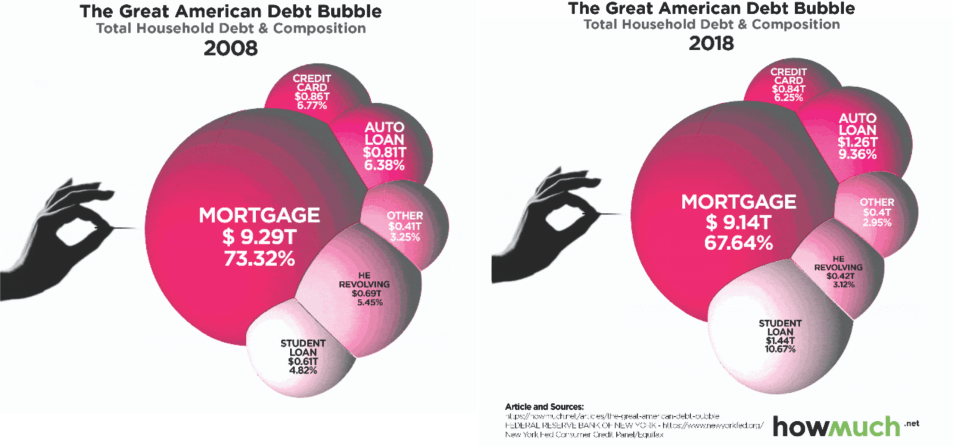

The wonderful website “HowMuch” put the corporate debt bubble into a graphic to help us visualize the potential for widespread defaults during the next economic and market downturn.

The problem with corporate debt is the amount of debt which is at risk of default during the next economic recession. (This isn’t an “IF,” it’s a “WHEN” statement.)

“The graph shows the implied ratings of all BBB companies based solely on the amount of leverage employed on their respective balance sheets. Bear in mind, the rating agencies use several metrics and not just leverage. The graph shows that 50% of BBB companies, based solely on leverage, are at levels typically associated with lower rated companies.”

“If 50% of BBB-rated bonds were to get downgraded, it would entail a shift of $1.30 trillion bonds to junk status. To put that into perspective, the entire junk market today is less than $1.25 trillion, and the subprime mortgage market that caused so many problems in 2008 peaked at $1.30 trillion.Keep in mind, the subprime mortgage crisis and the ensuing financial crisis was sparked by investor concerns about defaults and resulting losses.”

The reason BBB-rated debt is so plentiful is due to the Fed’s ultra-low interest rate policy over the last decade. Near zero rates, and easy credit terms, has seduced companies into taking on debt to fund operations, dividends, and stock buybacks. The consequence is we are now seeing corporate debt exceeding the levels of the global financial crisis.

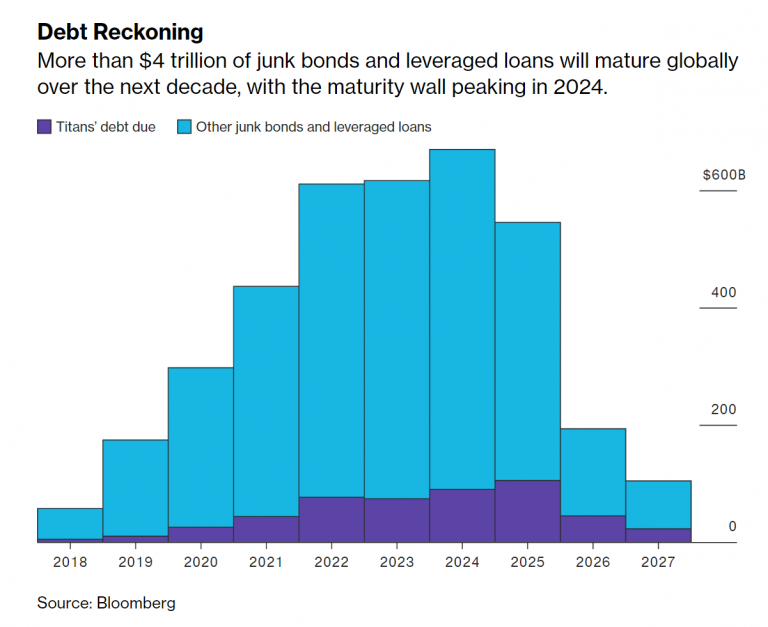

The real risk is that over the next 5-years more than 50% of the junk-bonds and leveraged-loans (which is sub-prime debt for corporations) is maturing and must be refinanced.

Let that sink in for a minute.

A weaker economy, recession risk, falling asset prices, or rising rates could well lock many corporations OUT of refinancing their share of this $4.88 trillion debt. Defaults will move significantly higher, and much of this debt will be downgraded to junk.

But it isn’t just corporate debt, that’s a problem.

Whistling Past The $246+ Trillion Graveyard

“According to the latest IIF Global Debt Monitor released today, debt around the globe hit $246 trillion in Q1 2019, rising by $3 trillion in the quarter, and outpacing the rate of growth of the global economy as total debt/GDP rose to 320%.

This was the second-highest dollar number on record after the first three months of 2018, though debt was higher in 2016 and 2017 as a share of world GDP. Total debt was broken down as follows:

Households: 60% of GDP

Non-financial corporates: 91% of GDP

Government 87% of GDP

Financial Corporations: 81% of GDP

And while the developed world has some more to go before regaining the prior all time leverage high, with borrowing led by the U.S. federal government and by global non-financial business, total debt in emerging markets hit a new all time high, thanks almost entirely to China.”

This is why Central Banks, from the ECB to the Federal Reserve, are terrified of an economic recession or downturn. As I said previously, “debt is the ‘weapon of mass destruction’”

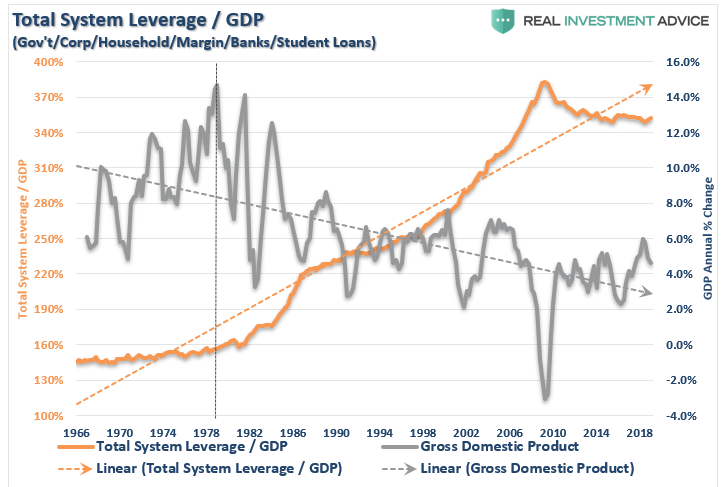

Given that global debt is 320% of global GDP, a deleveraging cycle will be too large for Central Banks to contain.

The deleveraging cycle WILL occur, all that Central Banks can do is hope to extend the current cycle long enough that “maybe” economic growth will catch up with the problem and lower the risk.

The irony is that it is the Central Banks on actions (lowering interest rates to zero and flooding the system with liquidity) which has inflated the debt bubble.

But that’s everyone else’s problem, right.

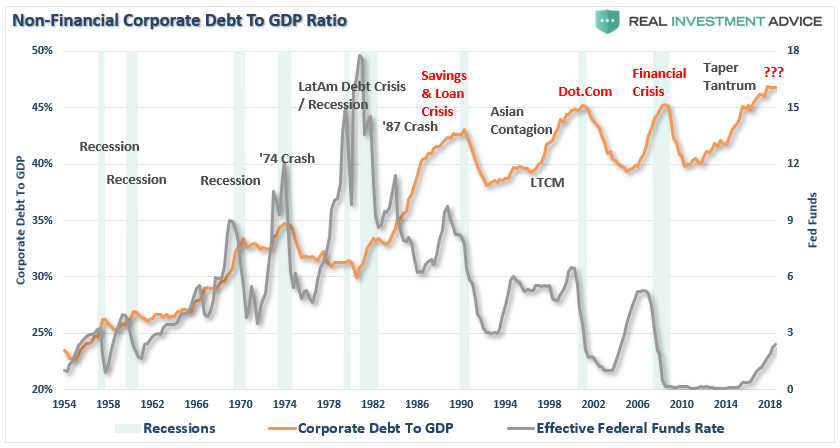

As noted above, the U.S. is currently running a debt-to-GDP ratio of roughly 350% so we are certainly not immune to the risk of a global “debt contagion.”

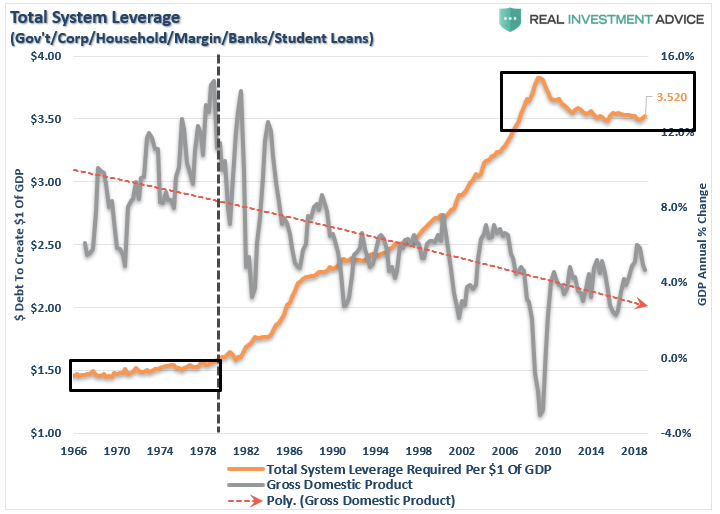

We can look at this a bit differently. The economy currently requires $3.50 of NEW debt just to generate $1 of new growth.

The problem with the exceedingly high debt levels is that since economic growth is a function of debt-supported spending, there is a finite limit to how much debt can be absorbed. As “HowMuch” showed, 10-years after the financial crisis, individuals are more levered today than they were then. (Notice the doubling of auto and student loan debt in particular.)

The Real Crisis Is Coming

As I noted this past week, the real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, and a near $6 trillion dollar funding gap, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely.

The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping, credit is collapsing, and shadow-banking freezes, the ensuing debacle will make 2008 look like mild recession.

It is unlikely Central Banks are prepared for, or have the monetary capacity, to substantially deal with the fallout.

As David Rosenberg previously noted:

“There is no way you ever emerge from eight years of free money without a debt bubble. If it’s not a LatAm cycle, then it’s energy the next, commercial real estate after that, a tech mania years after, and then the mother of all of them, housing over a decade ago. This time there is a huge bubble on corporate balance sheets and a price will be paid. It’s just a matter of when, not if.”

Never before in human history have we seen so much debt. Government debt, corporate debt, shadow-banking debt, and consumer debt are all at record levels. Not just in the U.S., but all over the world.

If you are thinking this is a “Goldilocks economy,” “there is no recession in sight,” “Central Banks have this under control,” and that “I am just being bearish,” you would be right.

But that is also what everyone thought in 2007.

via ZeroHedge News https://ift.tt/2SLyIi4 Tyler Durden

Faced with a declining birth rate and an unwilling to fill population shortfalls with immigrants like some of its European neighbors, Hungary has rolled out a seven-point “Family Protection Action Plan” which showers boatloads of cash, loan assistance and tax breaks to couples who agree to crank out lots of Hungarian children.

For starters, the state is offering $35,000 to couples who get married and have at least three children. Specifically, women under 40 who are getting married for the first time will receive an interest-free, general-purpose loan of $35,000. Upon the birth of the couple’s first and second children, loan payments will be suspended for three years each – with 1/3 of the principal paid off after the second child. After the third child is born, the debt will be wiped out.

Couples with two or more children can also use their loans for the purchase of an existing property – but it gets better.

“People living in villages should wait just a little bit longer,” said Prime Minister Viktor Orbán in February. “Within a few weeks, we would like to announce a scheme specifically customised to their needs. This means that today young married couples agreeing to have two children are eligible for grants worth 22 million forints ($75,000 US) for starting their lives and creating their first homes, while families agreeing to have three children are eligible for grants worth 35 million forints ($120,000 US),” said Orbán in his February announcement.

Hungary will also help out with mortgages – picking up the tab on roughly $13,500 US after the couple’s third child, with an additional $3,500 US of relief for each further child.

Moreover, women who have given birth to and raised four children will pay no income taxes for the rest of their lives, while grandparents who are still working are entitled to take leave to help take care of their new grandchildren.

There’s even a $9,000 subsidy for the purchase of a seven-passenger vehicle. “If you’ve ever tried to fit three children with car seats and everything else you need for children and probably the dog too in a car, you know how hard it is,” said Hungary’s minister of state for family, youth and international affairs, Katalin Novák. “Cars in Europe also tend to be smaller than American cars”

As The Federalist‘s Emma Elliott Freire notes, “An unusual feature of the subsidies is that they go into effect while a child is still in the womb. Parents can claim the relevant subsidy for their baby as soon as an expectant mother reaches her second trimester of pregnancy.”

“This is a philosophical aspect for us. We believe life begins at conception. We value unborn children, not only born children,” according to Novák, who added: “Hungarian young people are very family friendly. They want to get married and have at least two children. If that’s a fact, then we have to help them.”

Meanwhile, it looks like Orbán’s existing measures to boost fertility have been working since he took office.

She also argues the government’s policies are already proving successful. “Fertility has increased by more than 20 percent since 2010 [when Orbán took office]. It hit an all-time low of 1.25 in 2010 and now it is at 1.49,” she says. This still falls far short of the fertility replacement rate of 2.1, but Novák believes all signs point in the right direction for the long term, particularly the marriage rate.

“Between 2002 and 2010, under the Socialist government, the current opposition party, marriages decreased by 23 percent. Since 2010, marriages have increased by 43 percent,” says Novák. She believes if marriage rates go up, more children will inevitably follow. Novák also points out that since 2010, divorces have decreased by 29 percent and abortion in Hungary has fallen to an all-time low. –The Federalist

The catch?

In order to receive the benefits, women must remain married and employed.

“We link family support to work. You have to take part in the labor market. Unemployment is at 3.4 percent. We struggle more with a lack of labor force,” according to Novák.

“We don’t want to change people. We want to make it possible for them to raise a family if they wish to,” she added. “I have three children with my husband. I know that there comes a moment when you sit down and decide if you want to have another child. You discuss pros and cons. We want to put more arguments in the pros column. It’s up to you, but we want to make it easier to have a child or another child.”

via ZeroHedge News https://ift.tt/2Ytar5o Tyler Durden

The Democrats who were looking to cast Robert Mueller as the star in a TV special, “The Impeachment of Donald Trump,” can probably tear up the script. They’re gonna be needing a new one.

For six hours Wednesday, as three cable news networks and ABC, CBS and NBC all carried live the hearings of the House Judiciary and Intelligence Committees, the Mueller report was thoroughly trashed.

The special counsel stood by his findings. His investigation was not a “hoax” or “witch hunt,” he said. He admitted that he had found no Trump-Russia conspiracy. He denied he exonerated Trump of obstruction of justice.

All this we knew, and all of it we have heard for months.

What was new, what was dramatic, what was compelling was how the House Republicans arrived with their war paint on and ripped Mueller and his investigation to such shreds that viewers were feeling sorry for the special counsel at the end of his six hours of grilling.

The Republicans exposed him as only vaguely conversant with his own report. They revealed that he had probably not written his own statement challenging the depiction of his findings by Attorney General Bill Barr.

Mueller’s staff of lawyers, Republicans showed, reads like a donors list for Hillary Clinton. The FBI contingent that started the investigation was a cabal so hateful of Trump that some had to be fired.

Republicans raised questions about the origins of the investigation, tracing it back to early 2016 when Maltese intelligence agent Joseph Mifsud leaked to a staffer of the Trump campaign, George Papadopoulos, that Russia had Clinton’s emails. That and subsequent meetings have all the marks of an intel agency set-up.

Repeatedly, Republicans brought up the dossier written by British spy Christopher Steele, who fed Russian-sourced disinformation to Clinton campaign-financed intel firm, Fusion GPS, who passed it on to the FBI, which used it as evidence to justify warrants to spy on Trump’s campaign.

To many in the TV audience, this was fresh and startling stuff.

Yet Mueller’s response to all such allegations was that they were outside his purview and that other agencies were looking into them.

Wednesday’s hearings often proved painful to watch.

Mueller, a 74-year-old decorated Marine veteran of Vietnam and a former director of the FBI, sat mumbling his dissents as one charge after another was fired at him, his associates and his investigation.

For this disaster, the Democrats are alone to blame.

Mueller had wanted to file his report and leave it to the attorney general and Congress to act, or not act, on its contents. His job was done, and he did not want to testify publicly.

Democrats, desperate for impeachment hearings, wanted him to recite for the TV cameras every charge against the president.

What Democrats hoped would be a recital of Trump’s sins, Republicans turned into an adversarial proceeding that ended Mueller’s public career in a humiliating spectacle lasting a full day.

Where do Democrats go from here?

Their goal from the outset has been to persuade the nation that Trump colluded with Putin’s Russia to steal the 2016 election, and that the progressives are the true patriots in seeking to impeach and remove an illegitimate president and prosecute him for acts of treason.

The Republican position is that, for all his flaws and failings, Trump won the 2016 election fairly and squarely. He is our president, and the drive to impeach and remove him is an attempted constitutional coup d’etat by a “deep state” terrified that it cannot win against him in 2020.

The rival narratives are irreconcilable.

The Republican message of Wednesday: Proceed with hearings to impeach and there will be blood on the floor.

Democrats are in a hellish bind.

Should they proceed with hearings on impeachment, they will divide their party, force their presidential candidates to cease talking health care and start talking impeachment, and probably fail.

Impeachment hearings would fire up the Republican base and energize the GOP minority to prepare for combat in a Judiciary Committee where they are already celebrating having eviscerated the prosecution’s star witness.

If Democrats vote impeachment in committee, they will have to take it to the House floor, where their moderates, who won in swing districts, will be forced to vote on it, splitting their own bases in the run-up to the 2020 election.

If Democrats lose the impeachment vote on the House floor, it would be a huge setback. But if they vote impeachment in the House, the trial takes place in a Senate run by Mitch McConnell.

Trump would go into the 2020 battle against a Democratic Party that failed to overthrow the president in a radical coup that it attempted because it was afraid to fight it out with the president in a free and fair election.

via ZeroHedge News https://ift.tt/2LKkRHZ Tyler Durden

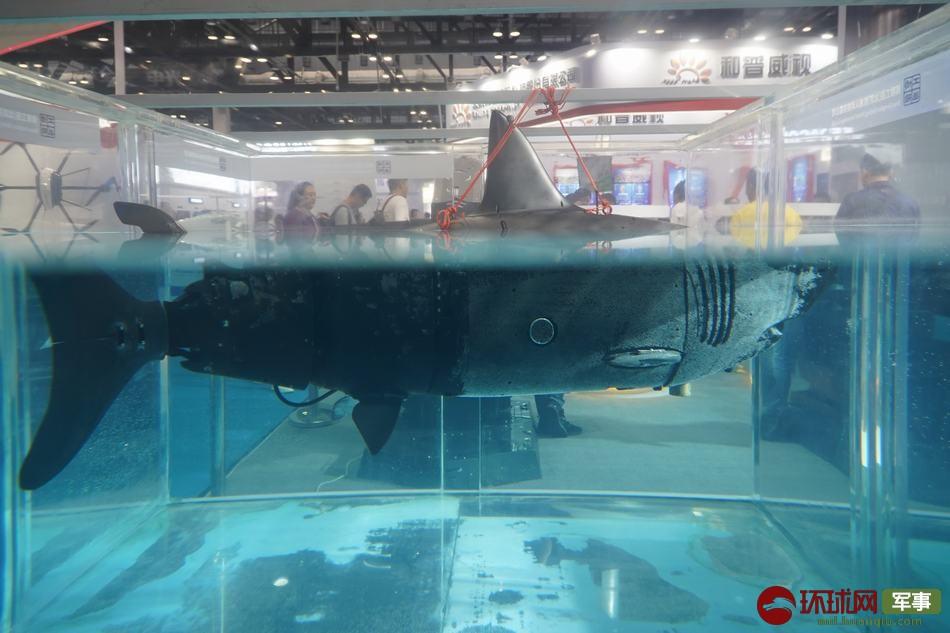

China is developing underwater drones that look exactly like sharks, the military analysis site South Front reports, based on new photos out of a Beijing military expo.

The shark-styled ‘Great White’ looking underwater drones are reportedly designed to conduct deep water reconnaissance missions, with a claimed operating depth of 150 meters.

Photos uploaded online from what was described as a major military expo at the “China National Convention Center” in Beijing this week, which featured dozens of domestic and foreign manufacturers, showcased a “high-speed, heavy-load, low-noise distant water drone for searching, tracking, monitoring, and reconnaissance tasks.”

The “bionic” machine resembles a massive Great White shark – which itself would be quite conspicuous if someone caught site of it actually cruising in the ocean.

However, it remains to be seen if it could be picked up on underwater sonar; presumably, the “shark drone” is designed to blend in with typical sea life.

Small underwater drones resembling fish were also showcased at the military expo.

Commentary alongside the published photos said they could be equipped with different external devices based on varying mission requirements.

It’s not the first time that Chinese media touted new developments in creepy looking bionic shark and fish devices for spying.

According to Chinese state media, AI “smart fish” have reportedly been under development by Chinese contractors for years, but ostensibly for environmental and engineering purposes, including for scientists to view hard to reach places under the sea or inside underwater pipes.

A team at Lanzhou Petrochemical Polytechnic has invented a smart “robot fish” that can explore underwater realms…

The robotic fish utilizes many advanced technologies, including mechanical electronics, sensors and artificial intelligence. It can be used for pipeline detection, hydrology, water quality monitoring, underwater rescue and more.

What’s up with China’s subsea drones. The shark is a high-speed, heavy-load, low-noise distant water drone for searching, tracking, monitoring, and reconnoitering tasks. Really curious if there’s any utility in these looking marginally fish-like https://t.co/GIEseWliOppic.twitter.com/jcZaSmLT8K

It remains to be seen what kind of practical real world or even military application a giant Great White-looking shark drone could have, considering its large size, other than perhaps sending enemies scrambling for fear there’s a real man-eater in the waters.

via ZeroHedge News https://ift.tt/2MkqyM5 Tyler Durden

Morgan Creek Digital Assets co-founder Anthony Pompliano says the European Central Bank (ECB)’s expected dovish turn will be “rocket fuel” for Bitcoin.

In a tweet posted on July 26, Pompliano commented on a fresh Bloomberg article investigating the ECB’s imminent policy moves — potentially including interest-rate cuts and renewed quantitative easing — designed to boost a faltering Eurozone economy. He said:

“ROCKET FUEL: They’re going to cut rates and print money right as we march towards the Bitcoin halving. Buckle up. This will be wild 🚀”

Pompliano had notably recently cited bitcoin’s halving – the reduction of mining rewards in half in May 2020 – as being one of the largest drivers of Bitcoin’s predicted price appreciation. His forecast is that the coin will hit $100,000 by the end of 2021.

Bloomberg’s article cited ECB President Mario Draghi’s recent comments indicating the institution’s intent to deliver another round of monetary stimulus this September. Notably, the ECB head stated that “on the inflation front, we don’t like what we are seeing […] That’s very important.”

Central bankers, Eurozone woes

The ECB president said he anticipates that contractions in Euro area manufacturing could contaminate the services sector, in part due to global trade tensions. While dismissing the prospect of a broad recession, he stated that consumer-price growth had fallen short of the ECB’s goal of just below 2% – justifying calls for significant support.

The ECB’s Governing Council has also added a crucial line to its “commitment to symmetry” statement, which Bloomberg notes reflects an openness to prolong stimulus to elevate price growth for some time:

“The Governing Council has tasked the relevant Eurosystem Committees with examining options, including ways to reinforce its forward guidance on policy rates, mitigating measures, such as the design of a tiered system for reserve remuneration, and options for the size and composition of potential new net asset purchases.”

One Danske Bank economist told Bloomberg he expects 20 basis points of rate cuts from the ECB and more QE, adding: “It’s a matter of when and how ECB will act, no longer if.”

The United States Federal Reserve is meanwhile expected to cut interest rates next week, while Turkey has just introduced the biggest interest-rate cut since at least 2002. Across the globe, Australia’s central bank has also signalled it is likely to further ease policy.

As recently reported, the head of global fundamental credit strategy at Deutsche Bank has remarked that central banks’ dovish policies are positively impacting “alternative” currencies such as bitcoin while hurting investment banks.

[ZH: And as central banks go more full-dovetard, sending global negative-yielding debt to record-er highs, so alternative stores of wealth – with zero or positive carry – become worth more]

via ZeroHedge News https://ift.tt/32URqs6 Tyler Durden

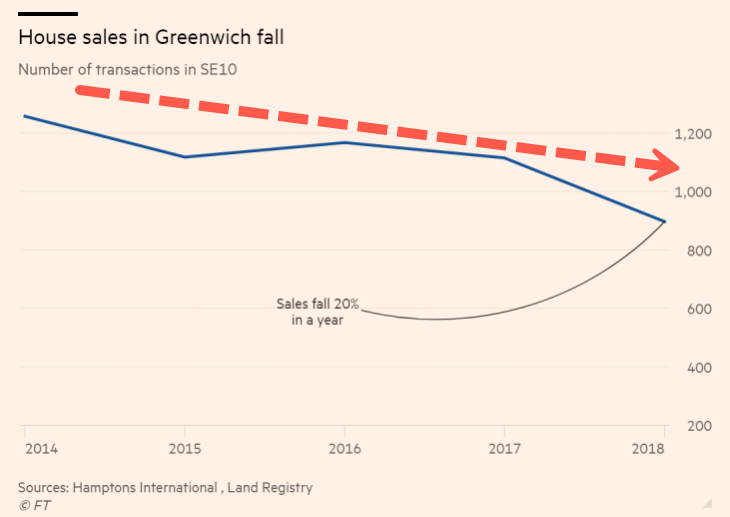

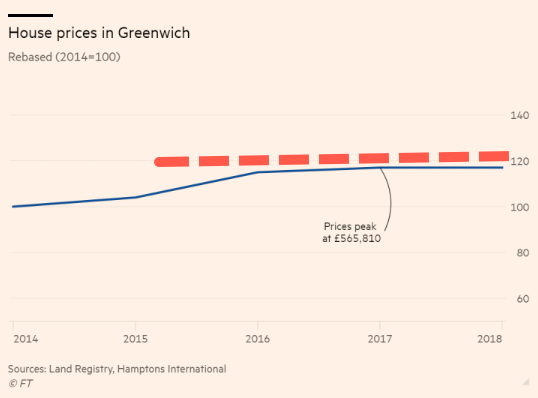

The London property bust continues to gain momentum.

Knight Dragon, a Hong Kong real estate developer, is building 15,000 homes across 150 acres on the riverside Greenwich Peninsula neighborhood near Canary Wharf over the next several decades, reported Financial Times.

According to Land Registry data compiled by Hamptons International, there were 897 sales in the SE10 postcode area covering Greenwich, Maze Hill, Greenwich Peninsula, down 20% from 2017, and 29% since 2014.

Graham Lawes, director of residential sales at JLL Greenwich, said the decline in sales doesn’t include sales of homes that are currently under construction, but said even those sales are stalling.

The risk of Brexit has triggered uncertainty, diminishing rental yields, and a London real estate property bust has discouraged any new foreign investors from entering the market.

In 2015, foreign investors accounted for 80% of new-build sales in London. Now Lawes indicates their share is less than 40%. A quarter of the transactions in Greenwich Peninsula development have been foreign investors, says Kerri Sibson, sales and marketing director at Knight Dragon.

Jonathan Benarr, director of APAC at Quintessentially Estates, said Knight Dragon is based in Hong Kong, indicating that a lot of Hongkongers and mainland Chinese investors would invest in its oversea projects. But now, “there is definitely a sense of caution.” First-time investors are being cautioned by “scary headlines” about London’s real estate downturn, says Benarr. “That has limited people’s willingness to go into ‘regeneration areas’ .”

“The only sales being done in developments at the moment, frankly, are the ones where they have got Help to Buy,” says Lawes, referring to the government-backed scheme that offers buyers of new homes worth up to £600,000 a 40% equity loan in London and a 20% loan elsewhere.

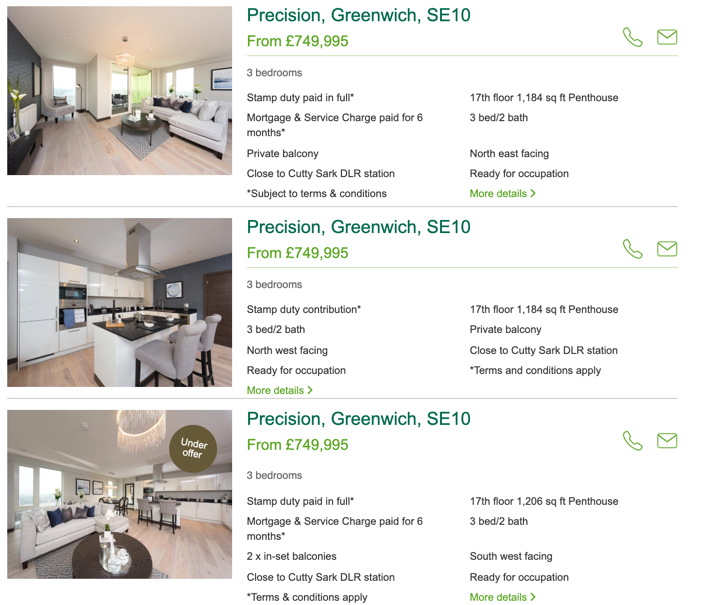

Knight Dragon’s development in focus is called Upper Riverside, has five towers totaling 900 homes, hasn’t seen condo price increases in three years.

The slowdown in property sales and a downturn in prices have led to increased incentives by developers. In Precision tower, which finished in March, developer Weston Homes has offered to cover buyers’ mortgages for six months.

U.K.’s Office for National Statistics (ONS) revealed earlier this month, that the overall property bust in London continues to gain momentum. Prices across the city dropped 4.4% over the year to May 2019, marking the most significant annual decline in almost a decade.

With foreign investors, mainly Chinese, running for the exit doors amid fears of Brexit, it seems that more pain is ahead for the London property market.

via ZeroHedge News https://ift.tt/2Yt4W6K Tyler Durden

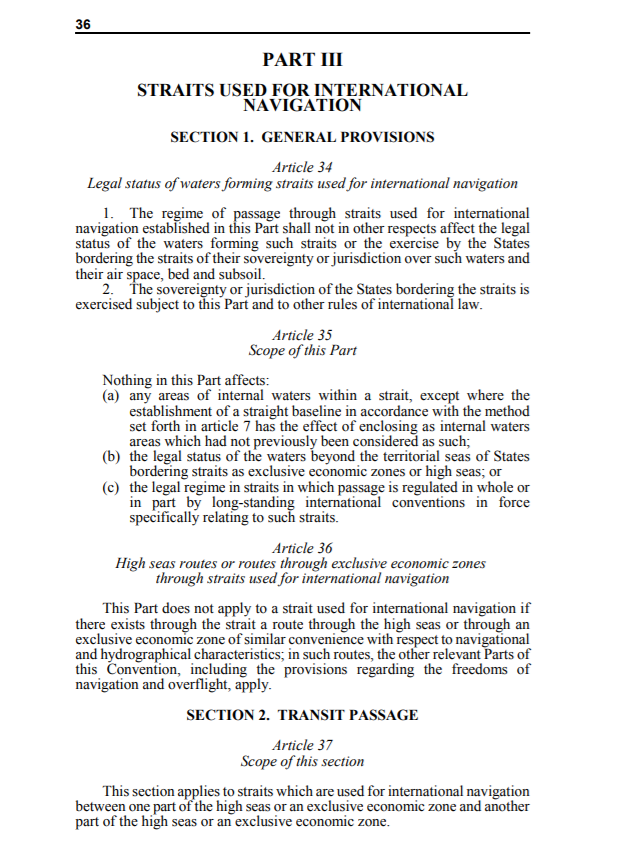

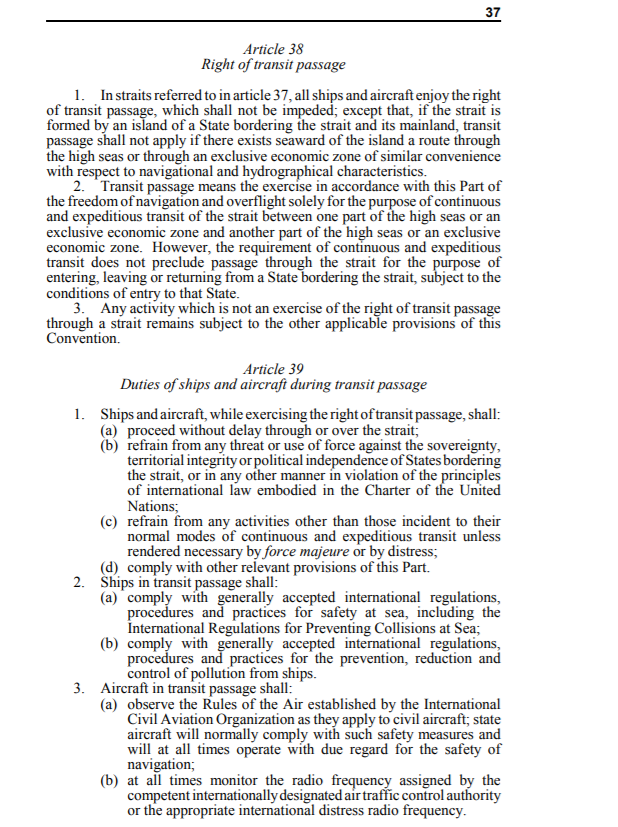

The British seizure of the Iranian tanker off Gibraltar was illegal. There is no doubt of that whatsoever. The Iranian response to the seizure of its tanker in the Strait of Gibraltar, by the seizure of a British Tanker in the Strait of Hormuz, was also illegal, though more understandable as a reaction. The implications for the global economy of the collapse of the crucial international law on passage through straits would be devastating.

It may seem improbable that the UK and or France would ever seek to close the Dover Strait, but in the current crazed climate it is no longer quite impossible to imagine the UK seeking to mess up access to Rotterdam and Hamburg. It is still easier to imagine them seeking to close the Dover Strait against the Russian Navy. Yet the essential freedom of navigation through the Kerch strait, respected by Russia which controls it, is necessary to the survival of Ukraine as a country. For Turkey to close the Bosphorus would be catastrophic and is a historically recurring possibility. Malaysia and Indonesia would cause severe dislocation to Australia and China by disrupting the strait of Malacca and the Suharto government certainly viewed that as an advantage from which it should have the right to seek to benefit, and was a continued nuisance in UN Law of the Sea discussions. These are just a few examples. The US Navy frequently sails through the Taiwan Strait to assert the right of passage though straits.

Keeping the Strait of Hormuz open is perhaps the most crucial of all to the world economy, but I hope that the above examples are sufficient to convince you that the right of passage through straits, irrespective of territorial waters, is an absolutely essential pillar of international maritime law and international order. The Strait of Gibraltar is vital and Britain has absolutely no right to close it to Iran or Syria. If the obligation on coastal states to keep maritime straits open were lost, it would lead to economic dislocation and even armed conflict worldwide.

Please note that the right of passage through straits is here absolute, in a UN Convention which is one of the base blocks of international law. It does not state that the right to transit through straits can be subject to any sanctions regime which the coastal state chooses to impose; indeed it is clearly worded to preclude such coastal state activity. Nor can it be overridden by any regional grouping of which the coastal state is a member.

Jeremy Hunt’s statement to parliament that the Iranian tanker had “freely navigated into UK territorial waters” was irrelevant in law and he must have known that. The whole point of passage through straits is that it is by definition through territorial waters, but the coastal state is not permitted to interfere with navigation.

It is therefore irrelevant whether, as claimed by the government of the UK and their puppets in Gibraltar, the tanker was intending to breach EU sanctions by delivering oil to Syria. There is a very strong argument that the EU sanctions are being wilfully misinterpreted by the UK, but ultimately that makes no difference.

Even if the EU does have sanctions seeking to preclude an Iranian ship from delivering Venezuelan oil to Syria, the EU or its member states have absolutely no right to impede the passage of an Iranian ship through the Strait of Gibraltar in enforcement of those sanctions. Anymore than Iran could declare sanctions against Saudi oil being delivered to Europe and close the Straits of Hormuz to such shipping, or Indonesia could declare sanctions on EU goods going to Australia and close the Malacca Strait, or Russia could declare sanctions on goods going to Ukraine and close the Strait of Kerch.

There are two circumstances in which the UK could intercept the Iranian ship in the Strait of Gibraltar legally.

One would be in pursuance of a resolution by the UN Security Council under Chapter VII of the UN Charter. There is no such resolution in force.

The second would be in the case of a war between the UK and Iran or Syria. No such state of war exists (and even then naval blockade must be limited by the humanitarian measures of the San Remo Convention).

What we are seeing from the UK is old fashioned Imperialism. The notion that Imperial powers can do what they want, and enforce their “sanctions” against Iran, Syria and Venezuela in defiance of international law, because they, the West, are a superior order of human being.

The hypocrisy of arresting the Iranian ship and then threatening war when Iran commits precisely the same illegal act in retaliation is absolutely sickening.

Finally, there will no doubt be the usual paid government trolls on social media linking to this article with claims that I am mad, a “conspiracy theorist”, alcoholic or pervert. It is therefore worth pointing out the following.

I was for three years the Head of the Maritime Section of the Foreign and Commonwealth Office. I was Alternate Head of the UK Delegation to the UN Preparatory Commission on the UN Convention on the Law of the Sea. I both negotiated, and drafted parts of, the Protocol that enabled the Convention to come into force. I was the Head of the FCO Section of the Embargo Surveillance Centre and responsible for giving real time political and legal clearance, 24 hours a day, for naval boarding operations in the Gulf to enforce a UN mandated embargo. There are very few people alive who combine both my practical experience and theoretical knowledge of precisely the subject here discussed.

* * *

Unlike our adversaries including the Integrity Initiative, the 77th Brigade, Bellingcat, the Atlantic Council and hundreds of other warmongering propaganda operations, this blog has no source of state, corporate or institutional finance whatsoever. It runs entirely on voluntary subscriptions from its readers – many of whom do not necessarily agree with the every article, but welcome the alternative voice, insider information and debate.

{kind=link}

{kind=link}