Convicted Killer Scott Peterson Spared Death Penalty By California Supreme Court Tyler Durden

Mon, 08/24/2020 – 13:55

Citing impermissible trial court errors made during the jury selection process, the California state Supreme Court has just thrown out the death sentence of Scott Peterson, one of the greatest tabloid villains of the 2000s.

Peterson was convicted and then sentenced to death in 2004 for the killing of his his eight-months-pregnant wife, Laci, 27, in their Modesto home on Christmas Eve 2002. He was also convicted of murdering their unborn son, Conner.

Their remains washed ashore in Richmond four months later near an area where Peterson said he had gone fishing. He has maintained his innocence.

According to Bloomberg, the trial court erroneously dismissed prospective jurors because of written questionnaire responses expressing opposition to the death penalty, “even though the jurors gave no indication that their views would prevent them from following the law—and, indeed, specifically attested in their questionnaire responses that they would have no such difficulty,” wrote Justice Leondra R. Kruger in the unanimous (7-0) decision to toss the sentence.

Under US Supreme Court precedent, the court said, the errors require reversing the death sentence. However, the state may choose to retry the penalty phase of the trial on remand if prosecutors so wish.

via ZeroHedge News https://ift.tt/3aQyFdA Tyler Durden

New Robinhood Traders Are Getting Their Stock Market Education From TikTok “Rattlesnakes” Tyler Durden

Mon, 08/24/2020 – 13:40

In what is undoubtedly an egregious case of “the blind leading the blind”, new Robinhood traders are now getting their investing education from TikTok influencers who are – needless to say – not investing professionals.

Not only are many TikTok influencers that talk market not investing professionals, some of them aren’t even out of college yet. But this hasn’t stopped new traders from flocking to these videos, aimed at rookie traders, a stunning new report from Bloomberg notes.

Like Errol Coleman, for instance – a TikTok influencer with 158,000 followers that can be found explaining thinks like support and resistance on his channel. “We already know this is a resistance, because it tried to push up and got rejected,” he says in one of his videos. Crafty advice, Errol. Thanks.

But the demand for these types of how-to videos is “off the charts”. Videos that use the hashtag #RobinHoodStocks have more than 3.1 million views and Coleman is the head of the pack. He is a senior at Adams State University studying business marketing.

The Robinhood crowd couldn’t be happier getting their answers from their “peers”, Bloomberg notes. Ben Pryor, a 22-year-old influencer, said it “makes other people feel like, ‘hey, I can do this stuff too.’”

Pryor has 109,000 followers on TikTok. Among them is Sam Masten, a first year student at NC State University, who said learning about the market has made him “way more involved in the news and what’s going on in the U.S. than I was before.”

Pryor has at least learning one valuable lesson: the less stocks you recommend, the less trouble you can get in. He told Bloomberg: “I tell them, I can’t predict the future — you’re entitled to make your own decisions.”

But it isn’t all fun and games for everybody – the influx of new traders is upsetting some who have been in the business for years. Brad Klontz, a psychologist and certified financial planner said: “What I saw was a bunch of people telling people what stocks to buy, and this was directed at young, impressionable, middle-class people who were just like me — desperate to try and improve their situation.”

John Stoltzfus, chief investment strategist at Oppenheimer & Co. is similarly worried, “especially for people who are novices and don’t understand the ramifications.”

He said of the TikTok influencers: “It’s like a rattlesnake in the garden. If there’s a rattlesnake in the garden, you better not go in there barefoot.”

But in addition to pumping their stock picks, there’s money to be made as an influencer. YouTube ads can provide income for some users and some influencers, like Pryor, chart $10 for an educational course.

Maybe the TikTok ban in the U.S. isn’t looking like such a bad idea after all.

4 requests this week for “hey I want to start trading, can you help me?” Just sending this to everyone. Also everyone should (re)read Panic by Michael Lewis pic.twitter.com/YxLBvY7No9

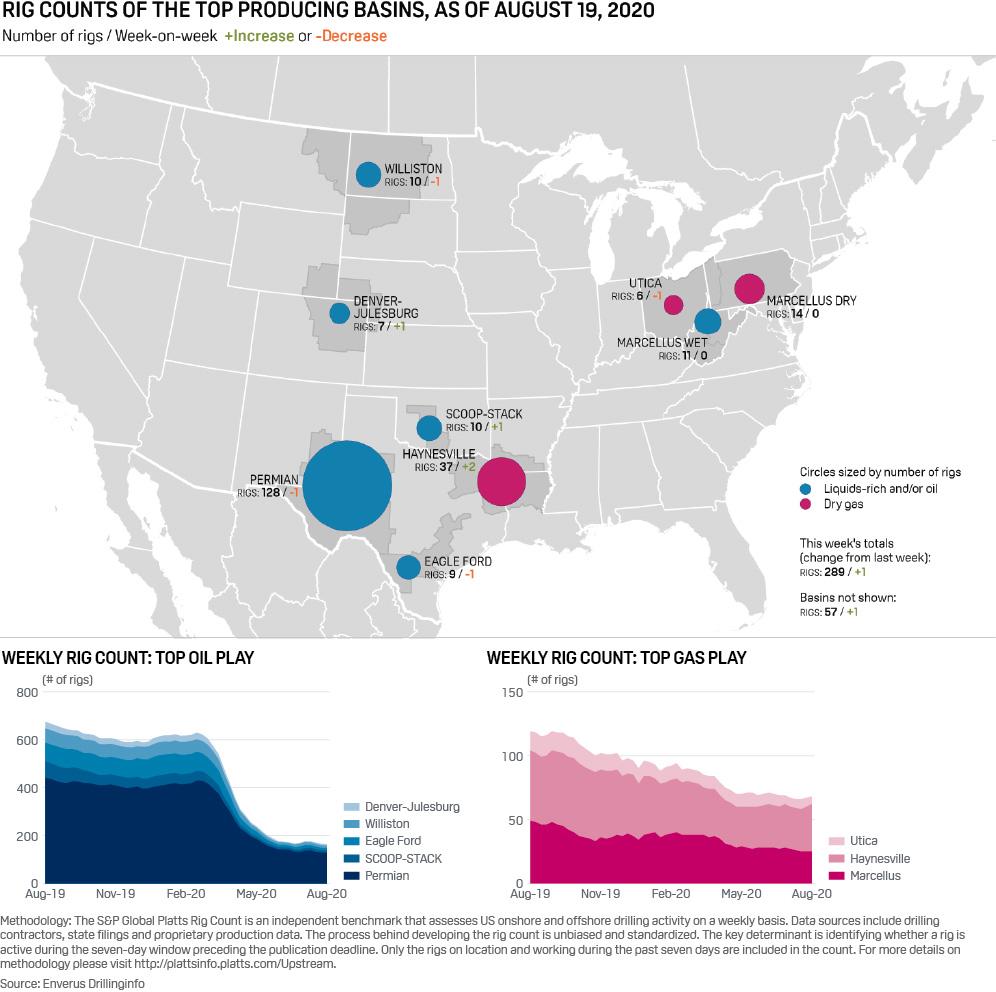

US drilling activity has top billing in S&P Global Platts editors’ pick of commodities trends this week. Plus, LNG netbacks, China-US energy trade, and EU carbon prices.

1. Permian oil rig count reaches 11-year low

What’s happening? Permian Basin oil rigs dropped by one to 128 rigs in the week ending August 19, marking an 11-year low, according to data from Enverus. Overall, the US oil and gas rig count was up one to 289 in the same week. The decline in the Permian rig count has slowed but has been dramatic: in the first week of March 428 rigs – 300 more than currently – were working in the basin. Although the Permian is the largest US oil producing basin and viewed as one of the most economic, upstream operators are being prudent amid low crude prices caused by the coronavirus pandemic, according to S&P Global Platts Analytics.

What’s next? Q2 earnings calls in early August brought some badly-needed confidence to an industry wracked by months of uncertainty from low oil demand in the wake of the coronavirus pandemic. Operators that had curtailed oil output as wells became uneconomic at prices not seen in 20 years, by early August had restored the bulk of their volumes and began, or planned, to restart some limited drilling and well completions. In short, visibility is improving and operators are starting to look forward to what they believe will be a more solid year in 2021.

2. Asian netbacks rally triggers increased US LNG activity

What’s happening? US Gulf Coast LNG netbacks from Northeast Asia are rallying, incentivizing a ramp-up in activity at liquefaction terminals. Feedgas deliveries to the six major US export terminals recently reached the highest level since early June but were still down by about 50% since a record volume in March.

What’s next? Considerable downside risk remains in the cards should early-winter Asian demand disappoint, which could see a wave of cargoes flow back to Europe mid-winter.

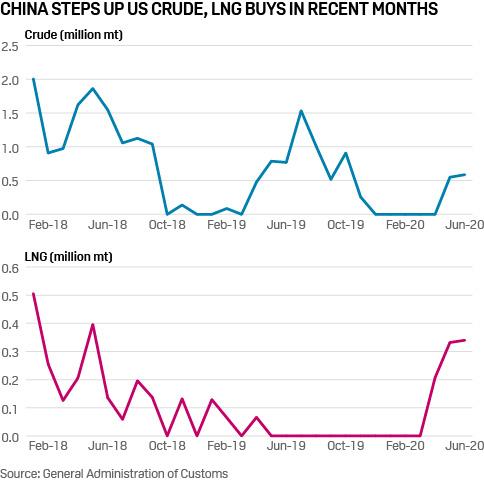

3. Low oil prices hamper China’s efforts to meet US trade deal target

What’s happening? China has stepped up purchases of US crude in recent trading cycles to try to comply with the Phase 1 trade deal struck with Washington in January. August is on track to have the largest amount of US crude delivered to China in a given month, expected to cross 30 million barrels. At least seven China-bound cargoes, carrying around 14 million barrels of crude, have been scheduled for September loading in the US Gulf Coast in recent days with China as their destination, S&P Global Platts fixtures data showed.

What next? Low oil prices may severely impede Beijing’s efforts to meet the purchase target for energy products in terms of dollar value. China’s crude imports from the US for the first three quarters of 2020 may reach around $3.42 billion based on the average Platts Dated Brent price of $40.87/b up to August 17 this year. If China imported 10 VLCCs (20 million barrels) of US crude per month in Q4, worth $100 million each at an oil price of $50/b, it would only amount to another $3 billion. This is far below the Phase 1 commitment, which calls for an additional $18.5 billion of US energy purchases in 2020, and $52.4 billion worth of purchases across the next two years, over 2017 levels.

4. EU carbon prices hold above Eur25/mt, but more supply coming

What’s happening? EU carbon dioxide allowance prices have held up at above Eur25.00/mt in August, after easing back from a 14-year high of over Eur30.00/mt in July. Dramatic gains since a March crash to Eur15.00/mt have taken prices back above their pre-COVID trading range, with support coming from an expected increase in the EU’s 2030 emissions target due in September, which will tighten supply after 2021.

What’s next? Recent price strength may face a test as September approaches, with monthly auction volumes set to rebound to over 86 million mt, compared with just 37.5 million mt in August. October and November will also provide similar volumes of fresh EUAs into the market, which may help to balance the more bullish impacts of upcoming regulatory reforms. Europe’s carbon market continues to be characterized by a tug-of-war between rather bearish short-term fundamentals pitted against expected future tightness as the EU beefs up the system to deliver the lion’s share of its rising climate ambition out to 2030 and beyond.

via ZeroHedge News https://ift.tt/31okzwR Tyler Durden

“F**K Danbury” – Connecticut Mayor Names Sewage Treatment Plant After Comedian John Oliver Tyler Durden

Mon, 08/24/2020 – 13:05

The Connecticut city formerly best known as “dirty Danbury” – perhaps previously best known for the name of the nearby women’s prison where “Orange is the New Black”‘s author served her sentence – is back in the headlines this week after announcing that it plans to name its new sewage treatment plant after HBO comedian John Oliver.

Why? Because Oliver lambasted the city in a bit from his popular weekly political humor show “Last Week Tonight”. During a segment about discrimination in jury selection affecting most of Connecticut’s small-ish cities (it’s a mostly suburban state), Oliver offered to “fight” anybody from Danbury, because “f**k Danbury,” he said.

During the unveiling, the mayor of the city said the name was appropriate because the plant is “full of crap, just like you, John”.

The comedian focused on the racial disparities in jury selection and reports that minority residents of the Connecticut cities of Hartford and New Britain were excluded from selection.

“If you’re going to forget a town in Connecticut, why not forget Danbury?” he said. “Because, and this is true, f— Danbury. From its charming railway museum to its historic Hearthstone Castle, Danbury, Conn., can eat my whole ass.”

“I know exactly three things about Danbury,” he said. “USA Today ranked it the second-best city to live in in 2015, it was once the center of the American hat industry and if you’re from there, you have a standing invite to come get a thrashing from John Oliver — children included — f— you.”

Danbury Mayor Mark Boughton is a former contender for statewide office and a known political entity in his corner of the state (the border between Conn.’s Fairfield and Litchfield Counties, which abuts New York State). He released a video responding to Oliver that quickly went viral in the local press.

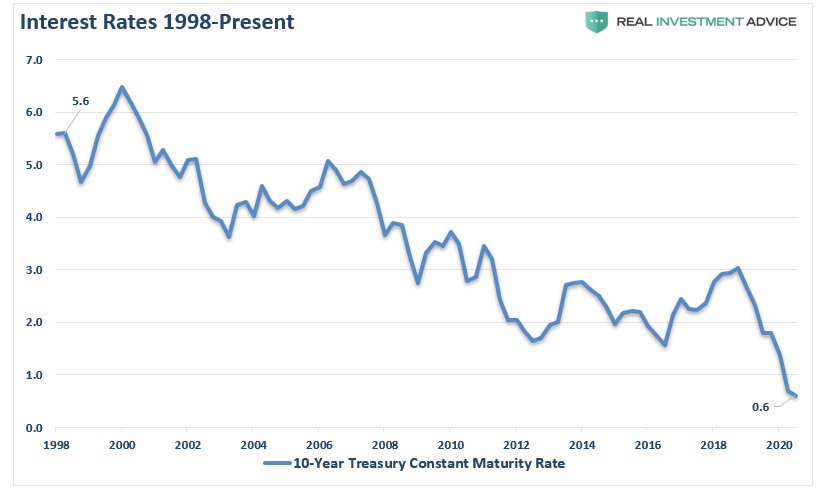

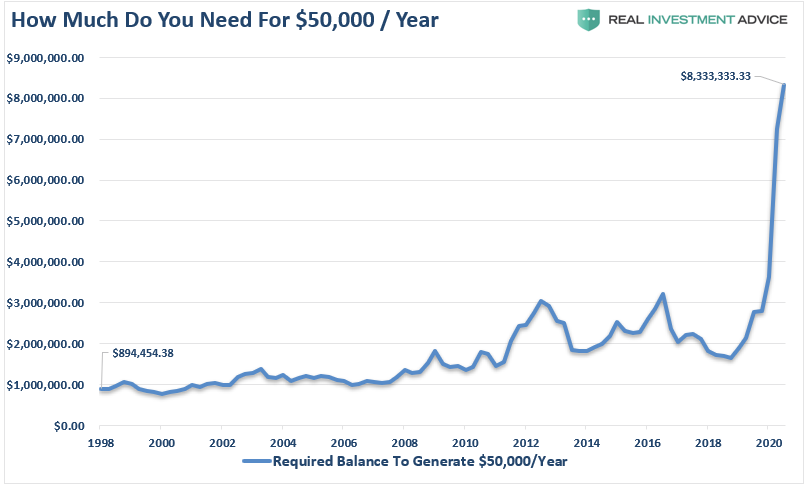

The 4% Rule Is Dead. A recent article by Shawn Langlois via MarketWatch pointed out this sobering fact but is one we have discussed previously. Retirees have long counted on being able to retire on their assets and take out 4% each year. However, a little more than 20-years later, the “death of the withdrawal rate” has arrived. What should retirees do now?

As noted by Shawn:

“The 4% Rule has long been used as a guideline for retirees in determining how much they should be able to withdraw from their retirement account while still maintaining a balance that will allow for the same income stream to flow through their golden years.”

The idea of the 4% rule originally suggested that once retired, the portfolio allocation is shifted to ultra-safe Treasury bonds. Such an allocation shift provided for the income required to live on, plus a Government guarantee of the principal.

Here’s the problem.

When the 4% rule was put into place, Treasury yields were 5%. Today, they are closing in on 0.5%.

This is a massive problem for retirees today. As shown, $1 million will no longer generate a $50,000 income for retirement. Today, it is just $6900/year.

Even more shocking has been the speed of the change. In 2016, it took roughly $5 million to generate $50,000/year. Just 4-years later, that number has skyrocketed to over $8 million.

For both young savers, and boomers approaching retirement, the challenges of planning for retirement today are daunting.

Problem #1: Very Few People Have $8 Million

While it is nice to think that throwing a few shekels into the market will magically turn into millions, the reality is far different. As discussed in “Why Are Boomers So Broke,”after two of the greatest bull markets in U.S. history during their lifetime, the savings statistics are depressing.

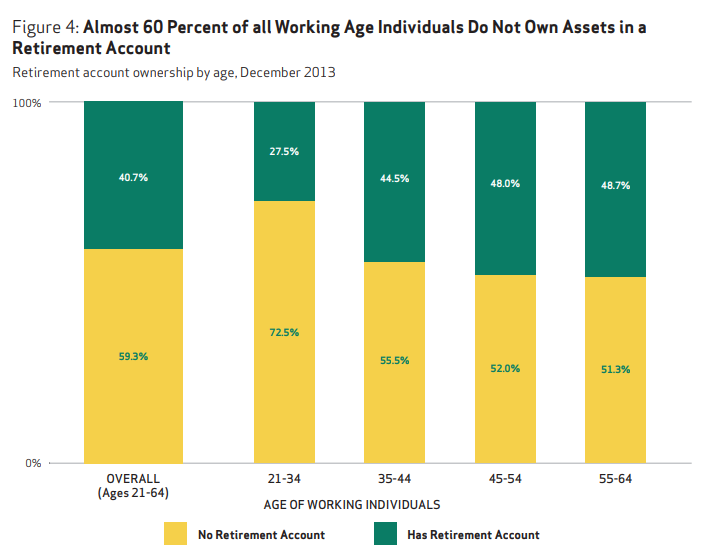

For many reasons, individuals simply don’t save money. Currently, almost 60% of ALL WORKING-AGE individuals DO NOT own assets in a retirement account.

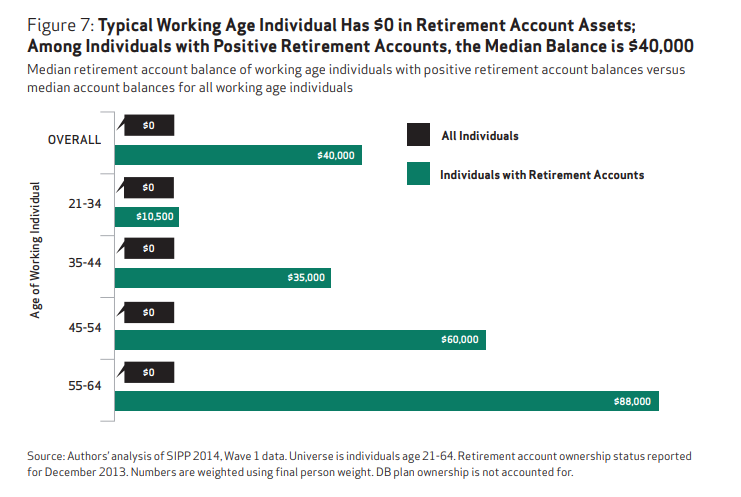

However, it’s actually more dismal than that. The typical working-age household has ZERO DOLLARS in retirement account assets. Importantly, “baby boomers” who are nearing retirement had an average of just $40,000 saved for their “golden years.”

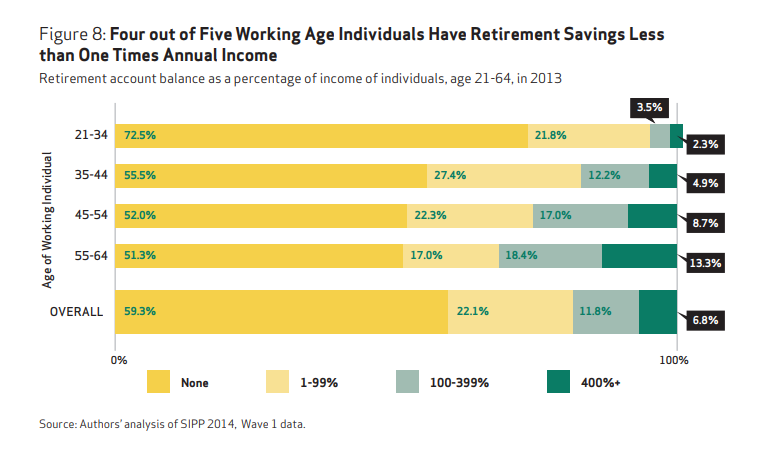

Lastly, only 4-0ut-of-5 working-age households have retirement savings of less than one times their annual income. This does not bode well for the sustainability of living standards in the “golden years.”

According to the study by MagnifyMoney:

“Although the average American household has saved roughly $175,000 in various types of savings accounts, only the top 10 percent to 20 percent of earners will likely have savings levels approaching or exceeding that amount. 29 percent of households have less than $1,000 in savings.”

You can’t get to $8 million if you can’t save to start with.

Problem #2: Can’t Save For Retirement

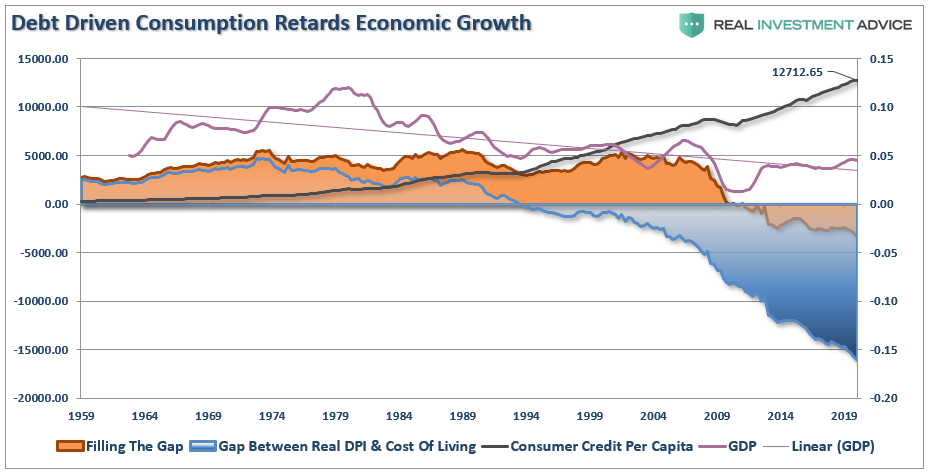

The ability of people to save money has become substantially more problematic. I showed the following chart recently, which illustrates the gap between income, savings, and the cost of living.

“The continued increases in debt, which was used to fill the gap between income and the cost of living, contributed to the retardation of economic growth.”

When viewing the “saving problem” from this perspective, it is easy to understand the survey responses from Kiplinger and Personal Capital. Americans said the biggest roadblocks to saving for retirement were:

The high cost of health insurance. “From 1999 to 2017, the cost of family health insurance coverage has more than doubled the amount of take-home pay it consumes.”

Disappointing investment performance.“Just under 30% of all respondents (29.4%) said that disappointing investment performance had stopped them from saving as much as they would have liked to for retirement.”

The amount of consumer debt they carried. “21.3% of Americans said that debt, not including student loans, kept them from saving for retirement combined with the increased costs of living.”

While the Fed keeps inflating stock markets, the “trickle-down” effect has yet to occur.

Problem #3: Don’t Forget The Inflation

In 1980, $1 million would generate between $100,000 and $120,000 per year while the cost of living for a family of four in the U.S. was approximately $20,000/year. Today, there is about a $50,000 shortfall between the income $1 million will generate and the cost of living.

This is just a rough calculation based on historical averages. However, the amount of money you need in retirement is based on what you think your income needs will be when you get there.

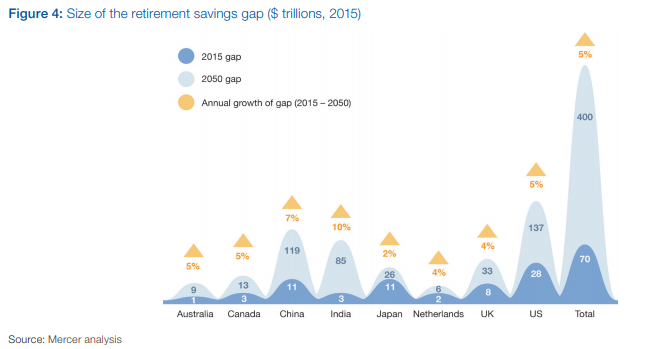

For most, there is a desire to live a similar, or better, lifestyle in retirement. However, over time our standard of living will increase with respect to our life-cycle stages. Children, bigger houses to accommodate those children, education, travel, etc. all require higher incomes. (Which is the reason the U.S. has the largest retirement savings gap in the world.)

If you are in the latter camp, like me, a “million dollars ain’t gonna cut it.”

Problem #4: Starting Your Plan With The Wrong Estimate

Let’s set up a simplistic example.

John is 23 years old and earns $40,000 a year.

He saves $14 a day

At 67 he will have $1 million saved up (assuming he actually gets that 6% annual rate of return)

He then withdraws 4% of the balance to live on matching his $40,000 annual income.

That pretty straightforward math.

IT’S ENTIRELY WRONG.

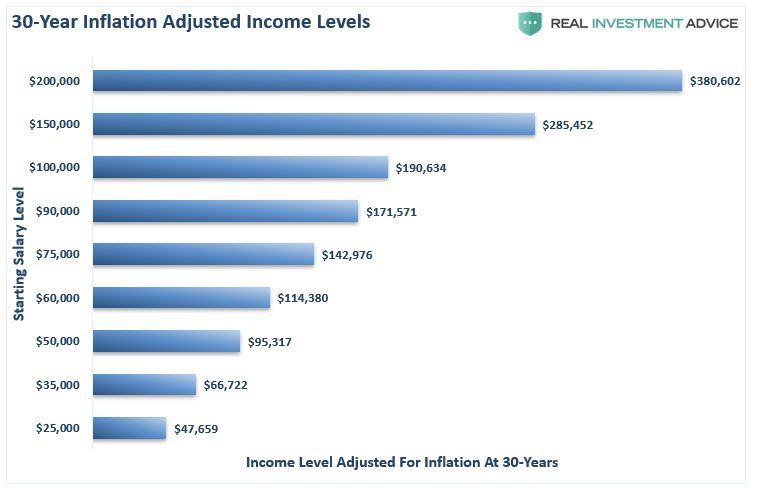

The living requirement in 44 years is based on today’s income level, not the future income level required to maintain the current living standard.

Look at the chart below and select your current level of income. The number on the left is your income level today and the number on the right is the amount of income you will need in 30-years to live the same lifestyle you are living today.

The Inflation-Equation

This is based on the average inflation rate over the last two decades of 2.1%. However, if inflation runs hotter in the future, these numbers become materially larger.

Here is the same chart lined out.

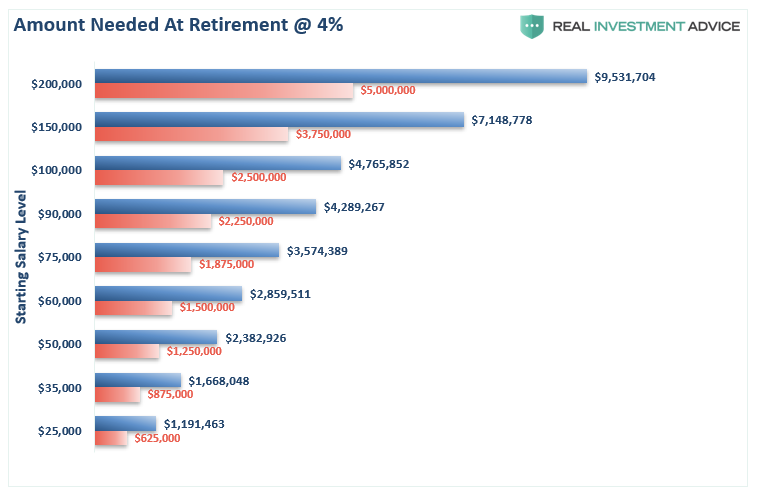

The chart above exposes two problems with the entire premise:

The required income is not adjusted for inflation over the savings time-frame, and;

The shortfall between the levels of current income and what is actually required at 4% to generate the income level needed.

The chart below takes the inflation-adjusted level of income for each bracket and calculates the asset level necessary to generate that income assuming a 4% withdrawal rate. This is compared to common recommendations of 25x current income.

So, if you need to fund a $50,000 lifestyle in 30 years, assuming a 4% withdrawal rate, it would require a future balance of more than $2 million. Unfortunately, this is no longer realistic.

Based on current valuations in the 95th percentile, and interest rates below 1%, the ability to get anywhere close to 4% is unlikely. Such is going to leave a majority of people working well into their retirement years.

Start Rethinking Your Plan

The analysis above reveals the important points individuals should consider in their financial planning process:

Expectations for future returns and withdrawal rates should be downwardly adjusted.

The potential for front-loaded returns going forward is unlikely.

The impact of taxation must be considered in the planned withdrawal rate.

Future inflation expectations must be carefully considered.

Drawdowns from portfolios during declining market environments accelerate the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

The yield chase over the last 11-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Investing for retirement, no matter what age you are should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

Things You Can Do Now

Save More And Spend Less: This is the only way to ensure you will be adequately prepared for retirement. It ain’t sexy, or fun, but it will absolutely work.

You, Will, Be WRONG. The markets go through cycles, just like the economy. Despite hopes for a never-ending bull market, the reality is “what goes up will eventually come down.”

RISK does NOT equal return. The further the markets rise, the bigger the correction will be. RISK = How much you will lose when you are wrong, and you will be wrong more often than you think.

Don’t Be House Rich. A paid-off house is great, but if you are going into retirement house rich and cash poor, you will be in trouble. You don’t pay off your house UNTIL your retirement savings are fully in place and secure.

Have A Huge Wad. Going into retirement have a large cash cushion. You do not want to be forced to draw OUT of a pool of investments during years where the market is declining. This compounds the losses in the portfolio and destroys capital which cannot be replaced.

Plan for the worst. You should want a happy and secure retirement – so plan for the worst. If you are banking solely on Social Security and pension plans, what would happen if the pension was cut? Corporate bankruptcies happen all the time and to companies that most never expected. By planning for the worst, anything other outcome means you are in great shape.

Most likely whatever retirement planning you have done is most likely overly optimistic.

Change your assumptions, ask questions, and plan for the worst.

The best thing about “planning for the worst” is that all other outcomes are a “win.”

via ZeroHedge News https://ift.tt/32pNQqi Tyler Durden

The pandemic- and lockdown-slammed economy is starting to show signs of life—but don’t get your hopes up too high just yet. Last week, Federal Reserve officials said the economy is recovering more slowly than anticipated and revealed their concerns that Americans have taken an unprecedented gut-punch from COVID-19 and from government reactions to it.

The dismal news came in the form of minutes from the Federal Reserve Open Market Committee’s (FOMC) end-of-July meeting. And the minutes serve as a reminder that, as dangerous as the novel coronavirus is, public health measures have the potential to do at least as much harm as viruses.

Understandably, the battered condition of jobs and businesses was the overriding concern. Despite some signs of improvement, “economic activity still appeared to have declined at a historically rapid rate in the second quarter,” the minutes revealed. “The projected rate of recovery in real GDP, and the pace of declines in the unemployment rate, over the second half of this year were expected to be somewhat less robust than in the previous forecast.”

“Indicators of business fixed investment suggested that investment had generally not begun to recover but that the pace of declines had moderated, on balance, in recent months,” they added.

The FOMC meeting came at the end of the second quarter, during which gross domestic product (GDP) dropped by an unprecedented 9.5 percent (an annual rate of 32.9 percent). July also saw COVID-19 cases spike in some states, and many government officials then re-imposed lockdowns that shuttered businesses and cut off paychecks.

“In June, we saw a significant increase in concerns related to reclosures due to rising levels of Coronavirus cases,” reports Alignable, a small business network, of a survey of its members. In July, 5 percent of the 5,738 business owners polled said it was their “top concern.”

Business owners have good reason to worry about lockdown orders, many of which arbitrarily distinguish between “essential” businesses allowed to function and “nonessential” businesses condemned to closure. At the end of July, Yelp, the crowd-sourced review company, noted that “even as total closures fall, permanent closures increase with 72,842 businesses permanently closed, out of the 132,580 total closed businesses.” Permanent closures made up 55 percent of all businesses that closed since March 1.

Numbers like that have a devastating human cost.

“As many as a third of the 230,000 small businesses that populate neighborhood commercial corridors may never reopen,” the Partnership for New York City reports of the carnage in that metropolis. Those closed businesses mean “as many as 520,000 jobs were lost from the small business sector.”

The loss of jobs is a national phenomenon.

“Through June, only about one-third of the roughly 22 million loss in jobs that occurred over March and April had been offset by subsequent gains,” say the FOMC minutes.

Since the July FOMC meeting, the national situation has changed somewhat. The July spike in U.S. COVID-19 cases has subsided, offering hope that people will regain confidence in moving about and engaging in some degree of normal activity. The decline in daily confirmed cases also may nudge government officials towards loosening restrictions so that people can exercise their own judgment about going about their lives, rather than depending on officials’ whims.

But initial unemployment claims jumped back above one million last week. Before 2020, the previous peak in claims was 695,000 in October of 1982. That’s an indicator that the economic hemorrhaging continues even if there are signs of life and we’re (hopefully) past the worst of the pain.

Future spikes in COVID-19 cases—predicted in some quarters—could mean another drop in economic activity. That could result from personal choices by people fearful of infection, and because of draconian restrictions imposed by officials on those who might choose otherwise if left to their own devices.

“Participants observed that uncertainty surrounding the economic outlook remained very elevated, with the path of the economy highly dependent on the course of the virus and the public sector’s response to it,” the FOMC warns. “The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.”

To offset the damage to people’s lives, the FOMC promises to use its own monetary policy tools—low interest rates, in other words—and assumes increased government spending. But it also warns that these policy tools are likely to be outweighed by the absence of actual economic activity and “the reactions of many states and localities in slowing or scaling back the reopening of their economies.”

Basically, cheap money and government checks aren’t a substitute for manufacturing, buying, selling, and employing. Nothing can stand in for productive human interactions.

None of this is to minimize the dangers posed by the pandemic. The virus has extracted a terrible toll in terms of deaths and suffering. People are justified in being wary of COVID-19, relative to their own vulnerability and their personal tolerances for risk.

But the pandemic can’t be considered in isolation. It must be balanced against other human needs, such as social interaction, education, and the economic activity that produces the prosperity that makes it possible to fight against health threats. If governments forcibly shut down their societies, they may strangle the virus, but they’re just as likely to kill off their own people—or, more likely, drive them to ignore the rules out of necessity.

We’re in for a continuing measure of pain from the pandemic no matter what happens. But government officials have the ability to get out of the way of people trying to improve their conditions—or they can make the situation much worse.

from Latest – Reason.com https://ift.tt/2Yul9ri

via IFTTT

Tennessee’s legislature and governor have heard the protests of people camped outside the Capitol for two months demanding policing reforms. They have responded by making existing laws harsher in a way that threatens the protesters’ voting rights and gun rights.

Last Thursday, Republican Gov. Bill Lee signed into law H.B. 8005. The highest-profile part of the bill turns the crime of illegal camping on state property from a misdemeanor to a Class E felony with a mandatory minimum sentence of 30 days in jail. Tennessee strips all felons of the right to vote and the right to own a gun, and the state makes it particularly difficult to get those rights restored. This part of the law is completely indifferent as to whether the camper is engaging in anything destructive or violent: Simply camping is enough. The law also grants qualified immunity for any state employees who seize property from those found illegally camping.

The legislation also prohibits the release of anybody arrested for a bunch of protest-related offenses (including the aforementioned illegal camping) for 12 hours after they’re arrested. TheTennesseannotes that such holds aren’t mandated by state law for most other crimes, including some that are much more serious than protest misconduct. This new authority makes it easy to shut down protests by broadly accusing protesters of crimes and then detaining them for 12 hours before dropping charges.

H.B. 8005 also adds mandatory minimums of 30- to 45-day jail sentences to some protest-related offenses, and it recategorizes some misdemeanors—such as disrupting a government meeting, obstructing a highway, and painting graffiti on a government building—so that they’re considered more serious misdemeanors and therefore have harsher penalties.

The harsher penalties were hammered out and passed in mid-August over the objection of Democratic lawmakers, and the Tennesseanreports that even some Republican legislators were concerned about repercussions of the broad bill. One Republican senator even filed an amendment to keep the camping offense a misdemeanor, but that didn’t make it into the final bill.

The two groups of protesters who have been protesting at the Capitol—Teens4Equality and the People’s Plaza—aren’t giving up on pushing for criminal justice reforms.

“What’s happening is an attempt to try to make us afraid to protest and so what we’re going to do is make sure that doesn’t happen,” Justin Jones of the People’s Plaza told News 4 Nashville. He said his organization will try to get the bill struck down as unconstitutional.

Hedy Weinburg, executive director of the American Civil Liberties Union’s Tennessee chapter, put out a statement criticizing Lee:

We are very disappointed in Governor Lee’s decision to sign this bill, which chills free speech, undermines criminal justice reform and fails to address the very issues of racial justice and police violence raised by the protesters who are being targeted. While the governor often speaks about sentencing reform, this bill contradicts those words and wastes valuable taxpayer funds to severely criminalize dissent. This law also robs individuals of their right to vote if they are convicted of these new felony charges. In a critical moment of reckoning that has led to policing reforms nationwide, Tennessee has chosen to turn a blind eye to the reasons the protests are happening and is instead choosing to shut down the right of the people to protest. We will be closely monitoring enforcement of this law and are urging Tennesseans to get out and vote like their rights depend on it.

from Latest – Reason.com https://ift.tt/3j6QUP1

via IFTTT

‘Definitely Not A Cult’: There Is Now A Dating App Exclusively For Tesla Owners In Development Tyler Durden

Mon, 08/24/2020 – 12:25

As Tesla eclipses $2000 per share and a nearly $400 billion fully diluted market cap, the obligatory jokes about the company being a “cult stock” will likely echo louder than they ever have.

Those trying to defend the company as not being a “cult” have their work cut out for them – especially with the unveiling of “Tesla Dating”, a dating app that’s exclusively for Tesla cultists owners.

The app is currently “in the works” and hasn’t launched yet, according to Business Insider. Its setup is similar to other dating apps, like Tinder, except that everyone on the app is a verified Tesla owner.

The app’s creator, Ajitpal Grewal, said he got the idea for it “after realizing Tesla owners only wanted to talk about one thing: how much they love their Teslas.”

He told Business Insider: “It became a big part of their identity, and they shared a lot of the same values, like wanting to reduce their impact on the environment, stanning Elon Musk, or appreciating high tech. Suddenly it hit me, these people would be perfect for each other.”

The verification process seems rock solid.Grewal said he will verify that people actually own Teslas by “asking users to submit a picture of themselves inside their Tesla.”

The app remains in “early stages” of development, but for those Tesla cultists already used to ordering products that don’t exist – and may never exist – there’s a website set up to take reservations.

“I believe your car tells a lot about you as a person,” Grewal concluded. It sure does, Ajitpal. It sure does.

via ZeroHedge News https://ift.tt/2EpoT6m Tyler Durden

The Democratic National Convention heavily promoted the conspiracy theory that President Trump is dismantling or undermining the postal service in an attempt to suppress the vote or undermine the presidential election in November. Democrats clearly don’t want in-person voting in November, despite the high risk of fraud with mail-in voting.

And Joe Biden says that, unlike Trump, he’d listen to the experts.

Well, Dr. Fauci has insisted that in-person voting can be done safely.

“I think if carefully done, according to the guidelines, there’s no reason that I can see why that would not be the case,” Dr. Fauci toldNational Geographic.

Fellow White House Coronavirus Task Force Member Dr. Deborah Birx also agrees.

“If you go into Starbucks in the middle of Texas and Alabama and Mississippi that have very high case rates, then I can’t say that it would be different waiting in line at the polls,” she said.

Even the notoriously liberal National Public Radio (NPR) seems to be admitting that in-person voting isn’t as risky as Democrats are suggesting, having reported this week that “new research suggests in-person voting may be less risky than many fear.”

The NPR report cites a new peer-reviewed study published in the American Journal of Public Health, which concluded that in-person voting in Wisconsin’s April 7 election did not cause a spike in coronavirus cases despite 400,000 people voting.

In that report, researchers from Stanford University’s Graduate School of Business and the University of Hong Kong’s School of Public Health call the Wisconsin election “a large natural experiment” for better understanding the coronavirus transmission risk.

The team found that hospitalizations in Wisconsin for COVID-19 cases “steadily declined throughout April,” dropping from a high of 101 on April 3 — four days before the election — to a low of 14 on April 18, according to data from the Wisconsin Department of Health Services.

There were 71 people, that agency reported in mid-May, who did test positive for the coronavirus who had either been poll workers or voted in person in Wisconsin’s balloting.

But the study noted that many of those cases involved people who had been exposed to the coronavirus in situations unrelated to voting.

“There is no evidence to date that there was a surge of infections attributable to the April 7, 2020, election in Wisconsin,” the study says.

“It appears that voting in Wisconsin on April 7 was a low-risk activity.”

If NPR of all places can report this, maybe Democrats should stop instilling fear in people about in-person voting.

For First Time, Iran’s Nuclear Agency Confirms Natanz Facility Blast Was “Sabotage Operations” Tyler Durden

Mon, 08/24/2020 – 11:55

For the first time, a top Iranian nuclear official has described the July 2nd fire at Natanz nuclear facility as sabotage, and not due to an accident.

“The explosion at Natanz nuclear facility was a result of sabotage operations,” Behrouz Kamalvandi, a spokesman for Iran’s Atomic Energy Organization announced Sunday. “Security authorities will reveal in due time the reason behind the blast,” he added.

Badly damaged Natanz facility, via the Atomic Energy Organization of Iran.

Recall that before and after the fire which caused severe damage, setting back the development of advanced uranium enrichment centrifuges, there was a series of ‘mystery’ explosions and fires at various military and industrial sites across Iran, raising suspicions of a major Israeli or even US-backed covert campaign to destabilize the country’s defense infrastructure.

But the Natanz incident stood out as the most likely to have been the result of covert sabotage operations, with even The New York Times citing intelligence sources to say it was the result of “a powerful bomb”:

“A Middle Eastern intelligence official with knowledge of the episode said Israel was responsible for the attack on the Natanz nuclear complex on Thursday, using a powerful bomb,”NYT wrote last month.

This satellite image from Planet Labs Inc. showing extent of damage at Natanz, which reportedly destroyed an advanced centrifuge assembly plant.

“A member of the Islamic Revolutionary Guards Corps who was briefed on the matter also said an explosive was used,” the report added.

Iranian media has at the same time suggested a cyber-attack by outside entities, but has stopped short of naming the US or Israel, while also quoting Iranian leaders as saying they would retaliate if proven.

Iranian authorities have until now kept mum on their suspicions in the midst of an investiation; however, they have assured Iran’s enemies on repeat occasions that retaliation is coming, possibly in the form of cyber-warfare or other sabotage against Israel or the US.

via ZeroHedge News https://ift.tt/3grnyZZ Tyler Durden

{kind=link}

{kind=link}