Trump Team Assures Big Tech Lobbyists That WeChat Ban Won’t Impact China Business Tyler Durden

Fri, 08/21/2020 – 18:20

A little over a week ago, we shared how President Trump’s decision to expand the scope of his crackdown on Chinese tech firms to include WeChat, Tencent’s ubiquitous platform for everything from payments, to messaging to e-commerce sent a wave of panic through American multinationals like Apple who depend on the Chinese market for growth, and feared being essentially shut out due to an oversight by the administration.

The backlash has been just as intense as could be expected. In a quintuple-byline story published Friday afternoon, Bloomberg reported that an army of corporate lobbyists are working with Team Trump to try and find a way to restrict WeChat’s use in the US without hamstringing every American company that depends on the app to connect with Chinese consumers.

According to sources from within the West Wing, the administration is still “working through the technicals” of how they’re going to restrict WeChat in the US while allowing American companies to liaise with it in foreign markets.

The Trump administration is signaling that U.S. companies can continue to use the WeChat messaging app in China, according to several people familiar with the matter, two weeks after President Donald Trump ordered a U.S. ban on the Chinese-owned service.

The administration is still working through the technical implications of how to enforce such a partial ban on the app, which is owned by Tencent Holdings Ltd., one of China’s biggest companies. A key question is whether the White House would allow Apple Inc. and Alphabet Inc.’s Google to carry the app in its global app stores outside of the U.S., according to the people, who spoke on condition of anonymity.

Over the past week, lobbyists went into “overdrive” and started harassing White House and Commerce Department staffers about Trump’s order, and the “logistics and intention of the WeChat executive order.” Now they’re pushing to “narrow” the scope of the looming ban.

“We are talking to everyone who will listen to us,” said Craig Allen, president of the US-China Business Council, whose group represents companies including Walmart Inc. and General Motors Co. “WeChat is a little like electricity. You use it everywhere” in China, Allen said.

Author Robert Kiyosaki, who wrote the book Rich Dad, Poor Dad says the United States is headed for totalitarianism and that he wants to flee the country with his gold. American is already fascist, regardless of opinions on the matter.

In an interview with Kitco, Kiyosaki explains that Americans have almost lost every smidge of liberty that their ancestors had.

“The freedom of speech is gone. Freedom of speech, freedom of assembly, and also the freedom of religion,” he said.

Kiyosaki has prepared for a time when he would have to leave the U.S., he said, by holding safe-haven assets like gold and silver.

“Way back when I started storing gold in Switzerland and in Singapore, so in case I had to run, plus I had different passports. Gold and silver are flight capital, and as you know, the only people making money today in America are moving vans,” he said.

Regardless of the price of gold, whether it’s $1000 or $15,000, Kiyosaki says he will continue to buy more because it’s one way to protect yourself from the central banks. Kiyosaki wants to remind people that he fought for capitalism, not socialism. But the U.S. is becoming Marxist quickly.

In a tweet on Aug. 21, the author of Rich Dad Poor Dad told followers that there was no time to “think about” investing in safe havens.

“Major banking crisis coming fast”

The reason, he said, was that Warren Buffett had chosen to dump bank stocks.

“WHY BUFFET is OUT OF BANKS . Banks bankrupt. MAJOR BANKING CRISIS COMING FAST,” he wrote.

“Fed & Treasury to take over banking system? Fed and Treasury ‘helicopter fake money’ direct to people to avoid mass rioting? Not a time to ‘Think about it.’ How much gold, silver, Bitcoin do you have?”

WHY BUFFET is OUT OF BANKS . Banks bankrupt. MAJOR BANKING CRISIS COMING FAST. Fed & Treasury to take over banking system? Fed and Treasury “helicopter fake money” direct to people to avoid mass rioting? Not a time to “Think about it.” How much gold, silver, Bitcoin do you have?

He added that bitcoin also qualifies as a safety asset because it’s “international currency; it operates outside the Fed and the Treasury. Kiyosaki says he holds gold because it’s “God’s money” and Bitcoin because its the “people’s money.” He seems to be attempting to remove himself from the system of enslavement set up by the Federal Reserve.

via ZeroHedge News https://ift.tt/2Eu9PE8 Tyler Durden

“It’s Just Absolutely Incredible”: What’s Going On In The Corporate Bond Market Is Stunning Tyler Durden

Fri, 08/21/2020 – 17:40

In a recent report from hedge fund giant Brevan Howard, the investor pointed out the biggest flaw in the policy response to the covid pandemic: “Many businesses face solvency risks that are not addressed by borrowing; a debt overhang cannot be cured by more borrowing no matter how cheap it may be.“

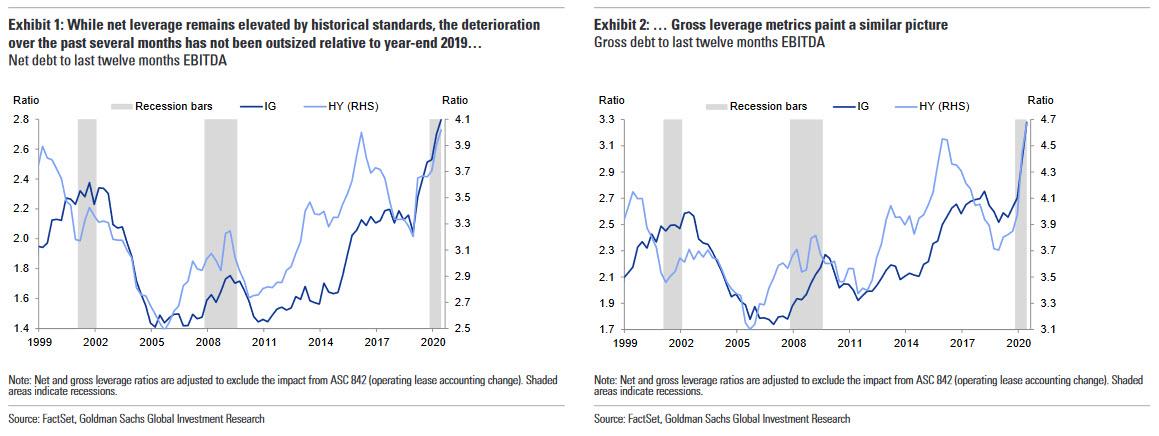

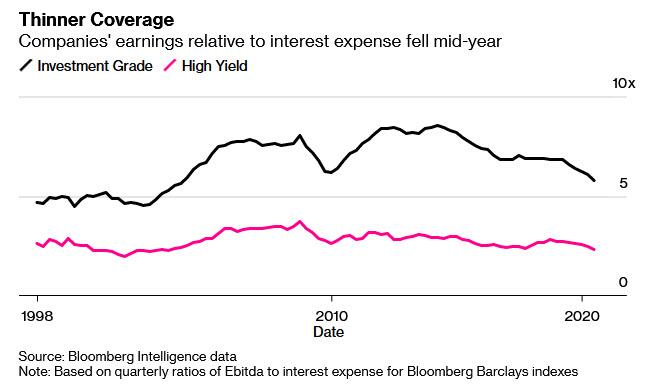

While that statement is absolutely true, and it applies not only to the aftermath of the covid shutdowns but everything that has happened in the past decade, it hasn’t stopped both government and corporations from going on a historic borrowing spree, in the former case thanks to “helicopter money” whereby central banks now directly monetize all the debt government treasurys have to sell, and in the latter as company CFOs take advantage of record low rates to borrow as much as possible before the window closes. This can be seen in the Goldman chart below which shows that both investment grade and high yield leverage is at all time high levels:

The numbers are staggering: on Friday, BofA Chief Investment Strategist Michael Hartnett calculated that US corporate bond issuance is currently annualizing a mindblowing $2.5 trillion this year, between $2.1TN for IG and $0.4TN for high yield. As Bloomberg writes today, while much of that fresh cash – more than $1.6 trillion in total – has helped scores of companies stay afloat during the pandemic lockdown, “it now threatens to curb an economic recovery that was already showing signs of sputtering” as many companies will have to divert even more cash to repaying these obligations at the same time that their profits sink, leaving them with less to spend on expanding payrolls or upgrading facilities in months ahead.

The paradox is that this is all by design: in doing everything in its power to prevent the corporate debt bubble – which was already at a record size before the covid pandemic – from bursting, the US central bank unleashed monetary policies that have terminally decoupled the bond market from all fundamentals, while also arresting default risks by taking over credit risk without punishing investors and moving into lower-rated debt than ever before, which started off the risk-on period as Nordea’s Andreas Steno Larsen writes today and shows in the following chart:

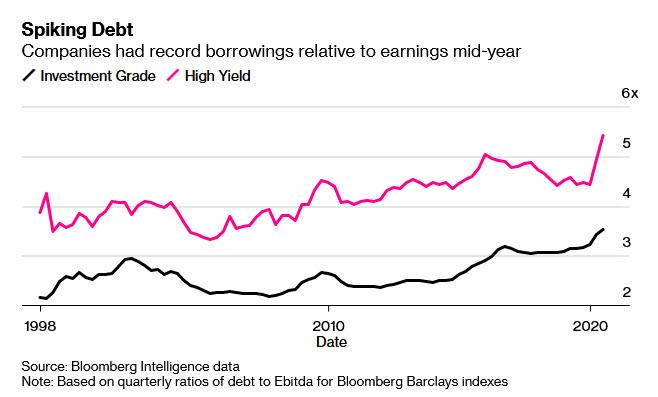

In a sign of just how pronounced the borrowing overhang has become, Bloomberg points out that the average junk-rated company had debt levels relative to earnings that were so high in the middle of the year, according to a new analysis by Bloomberg Intelligence, that they almost would have tripped do-not-touch alerts from banking regulators a few years ago. Those warnings back then only applied to a handful of borrowers. Had regulators not opted to drop these warnings, they could today apply to far more.

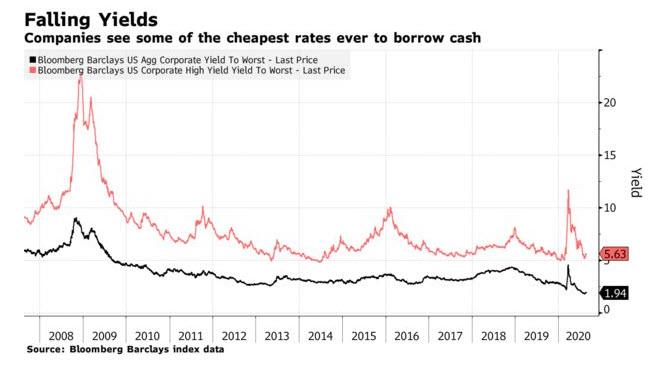

Corporations have also been borrowing heavily as the Fed has slashed short-term interest rates to near zero and supported credit markets through, for example, buying company bonds. Lower rates have spurred investors to buy higher-yielding, riskier securities, which has allowed even junk-rated firms to borrow more to tide them over during the crisis. High-grade issuers have already sold more bonds in 2020 than any other full year in history. Junk corporations have surpassed 2019’s total already.

Some specifics: leverage (i.e., the ratio of total debt to Ebitda) for investment-grade companies was 3.53x in the second quarter for the Bloomberg Barclays U.S. Corporate high-grade index. That’s the highest in data going back to 1998, and is up from 3.42 in the first three months of the year, when the impact of the pandemic was only just beginning to show up in earnings. It compares with a 20-year average of 2.65.

For high yield, leverage stood at a record 5.42 at the end of June, up from 4.93 at the end of March and 4.44 at the end of 2019. Avis Budget Group Inc., the car rental company, had debt equal to 27 times earnings as of June 30, up from five times at the end of March, as it burned cash in the second quarter, although that figure could improve later this year as its earnings start to rebound. In 2016, banking regulators pushed back against leveraged buyouts that left companies with ratios above six.

No matter how one slices the data the message is clear: “An overburdened corporate sector is likely to grow less rapidly and that could slow the whole recovery down,” said Kathy Jones, chief fixed-income strategist for Charles Schwab.

Of course, none of that matters now when rates are at all time lows, but fast forward a few years when inflation kicks in and suddenly corporate America is facing another unprecedented crisis as it has to not only rollover record amounts of debt but has to refi into ever higher rates.

Quoting Lale Topcuoglu, senior fund manager at JO Hambro Capital Management in New York, Bloomberg warns that a slower recovery could have wide-reaching implications in financial markets. Many securities prices reflect investors’ expectation that profits will normalize next year, when in fact it could take at least two or three years. Not surprisingly, she believes that many junk bonds as being overpriced.

“It just seems absolutely incredible how much people are closing their eyes and buying,” Topcuoglu said.

The good news is that unlike last year when much of the new debt issuance went to fund stock buybacks, much of the debt sold in recent months has refinanced maturing borrowings allowing companies to lock in even lower rates for the next 5 to 10 years; furthermore many of the companies are holding on to the money they raised as cash and may end up not spending it.

And while the fact that companies managed to stay afloat during the pandemic is “a good thing compared with the alternative of even more corporations having gone bankrupt” not all companies have been able to access that credit, with smaller borrowers often getting shut out as a DoubleLine Portlio Manager wrote WEdnesday in “Large Firms Reap Benefits From Central Bank Easing As Small Ones Suffer.”

To be sure, even the large companies face a day of reckoning or as Bloomberg puts it simply “a hangover” as many corporations were already groaning under their debt loads even before the Covid-19 pandemic, and now will have to work harder to cut borrowings as earnings remain depressed. Even if companies are hanging on to the money they borrowed, they must still pay interest on it, and could eventually use the cash if the pandemic drags on. Many will simply revert to using the debt proceeds to repurchasing their stock and make quick profits for management and shareholders as we pointed out earlier this week. Ultimately it is the economy, and the middle class workers who will suffer the most as chief JPM economist Michael Feroli wrote, warning that with corporations shunting more of their earnings toward paying interest and paying down debt, they will struggle to hire and invest as much as they would at the end of a more conventional recession.” That could translate to a relatively sluggish recovery instead of the fast, “V-shaped” one many investors hope for.

“The debt overhang is going to be a headwind for capital spending and for hiring, not just in the second half of the year but probably into next year as well,” Feroli said.

Another paradox is that as corporate leverage is rising to all time highs, rates continue to sink as investors have no choice but to buy their debt, which in turn forces even more debt issuance, even higher leverage and so on, until the Fed is tasked with yet another corporate debt bailout:

With short-term interest rates having fallen to near-zero levels, borrowing is cheaper for most companies than it was just a year ago. Average yields on U.S. investment-grade corporate bonds touched all time lows of 1.82% earlier this month, and are still hovering near those levels, according to Bloomberg Barclays index data.

As a result of record low rates, even as leverage soars, interest coverage, or EBITDA to total interest expense, has fallen to 5.8 in the second quarter for investment-grade companies, compared with a 20-year average closer to 7. The June 2020 level was the lowest since 2003. For junk-rated companies, the interest coverage ratio fell to 2.3 in June, also the lowest since 2003.

Unlike the 2008 bubble, ratings firms have taken note of the broad downward trend in credit quality, with S&P downgrading more high-yield debt in the second quarter, relative to upgrades, than any time in at least a decade, according to data compiled by Bloomberg. That too has not stopped investors from piling on: just recently junk-rated Ball Corporation sold debt for the lowest ever yield for a “high” yield bond at 2.875%.

Meanwhile, corporate earnings per share fell by about a third in the second quarter from the same period last year, and are likely to fall in the third and fourth quarters as well and may not recover their 2018 levels until the end of 2021. As a result, strategists expect leverage and interest coverage to erode further.

None of this fazes investors who have gone “balls to the wall” buying corporate debt with the Fed’s blessing now that the central bank is buying both investment grade and high yield ETFs and bonds in the open market. To justify the euphoria, investors have given companies a break for about a year and are looking ahead into mid-2021 or even later to evaluate where they will perform after, for example, the world finds and distributes a Covid-19 vaccine. That to Bloomberg explains why cruise companies that are burning cash, such as Royal Caribbean Cruises Ltd. and Carnival Corp., have been able to borrow repeatedly, and have seen most of their new bonds trade well above the price at which they were originally sold.

But even if bond prices are broadly rising, investors need to be cognizant of the risks they’re buying, said Schwab’s Jones.

“This cycle is very different because we’ve had so much support from central banks and we have so much liquidity in the market,” Jones said. “But the old saying ‘liquidity does not equate to solvency’ is something people need to keep in mind when they’re investing.”

Brevan Howard would most certainly agree.

We give the final word to GnS Economics’ founder Tuomas Malinen who today writes that “we have stock markets that have decoupled from real economic activity to an unprecedented degree and a moribund European banking sector practically doomed to collapse. The constant resuscitation and bailouts of the central banks since the last crisis in 2009 have pushed us to the brink of ‘Financial Armageddon’, initiated this time by the repo-market implosion and the coronavirus pandemic.”

His conclusion: “When it truly gets going, as it likely will, do not blame the virus. Blame the reckless central bankers.“

via ZeroHedge News https://ift.tt/329FuDc Tyler Durden

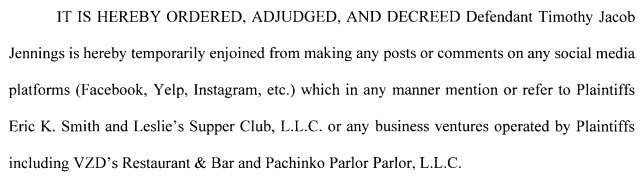

Smith is apparently involved with Jennings’ ex-wife, who is in a bitter custody battle with Jennings. Jennings, Smith alleged, had written posts falsely stating that Smith was a “pedophile” and a “known predator” (see the application for the TRO for more), so Smith sued Jennings for libel.

So far so good: Smith might have a valid libel claim. But instead of just getting damages, or even an injunctions against future libels, the court issued this pretrial restraining order (Smith v. Jennings(Okla. Dist. Ct.), dated Wednesday):

That can’t be constitutional, it seems to me.

But beyond that, Oklahoma is one of the several states that still forbids injunctions in libel cases, even narrow injunctions that ban repeating statements found to be libelous after a trial on the merits. See House of Sight & Sound, Inc. v. Faulkner, 912 P.2d 357, 361 (Okla. Civ. App. 1995); First Am. Bank & Trust Co. v. Sawyer, 865 P.2d 347, 352 (Okla. Civ. App. 1993). There is a narrow exception for “conspiracy, intimidation, or coercion,” but it is narrow indeed, and First Am. Bank & Trust Co. made clear that the “coercion” element is not satisfied simply by speech being aimed at pressuring a business to give the speaker a refund or similar benefit.

And I’ve seen plenty of other cases that issue such clearly unconstitutionally overbroad injunctions. Just a reminder, I think, that things happen in trial courts that are hard to reconcile with the appellate precedents—and if the losing party doesn’t have the money, energy, or time to fight the case on appeal, the trial judge’s decision stands.

from Latest – Reason.com https://ift.tt/2COg19P

via IFTTT

A coalition of New York City police, firefighter, and prison guard unions have lost their bid to block the city’s planned release of a huge trove of police misconduct records. The ruling clears the way, at least for the moment, for New York City’s Civilian Complaint Review Board (CCRB) to post officers’ complaint histories, and for the New York Police Department to release separate disciplinary records it holds.

All those records had been confidential for the past 40 years under Section 50-a, a notorious police secrecy law. But the New York legislature repealed the law in June—a stinging defeat for police unions, who are still bitterly fighting to claw back what records they can. Today U.S. District Judge Katherine Polk Failla declined to grant a preliminary injunction barring New York City from releasing unsubstantiated misconduct allegations.

“Whoa!” an unidentified person on an unmuted line shouted during the telephonic court hearing, as Failla announced she was almost totally rejecting the police unions’ request.

Last month, Failla temporarily blocked New York City from disclosing the records while she weighed the unions’ arguments that the release of unsubstantiated complaints would lead to retaliation against police officers and harm their reputations and future employment prospects.

But before the unions filed their lawsuit, the review board released misconduct records to the New York Civil Liberties Union (NYCLU) and ProPublica, the latter of which published its own database of more than 4,000 complaints. A court initially blocked the NYCLU from releasing its records, but yesterday the 2nd Circuit Court of Appeals lifted that stay as well.

The NYCLU immediately published a database of more than 320,000 complaints filed against the city’s police officers since 1985. The New York Timesreports that only 3 percent of those complaints were substantiated.

Today Failla ruled that the unions had failed to demonstrate the release would cause concrete harms or risks for officers.

“Plaintiffs have presented speculation only that these disclosures will increase risk of officer harm,” Failla said, noting that such records are public in a dozen other states.

Failla did, however, grant a narrow injunction blocking the city from releasing records on certain low-level disciplinary offenses that can be expunged under the officers’ collective bargaining agreement.

CCRB Chair Fred Davie said in a press release today that this outcome “is not only legally justified, but is the only logical path forward for preserving what New Yorkers and lawmakers intended through the repeal of 50-a. I applaud today’s decision—the fight for transparency has been delayed, but not deterred.”

The unions have until Monday afternoon to appeal Failla’s ruling to the 2nd Circuit Court of Appeals.

from Latest – Reason.com https://ift.tt/3l0CUYK

via IFTTT

Steve Bannon, former chief strategist to President Donald Trump, has been charged with defrauding donors to We Build the Wall, a private fundraising effort partially spearheaded by Bannon that collected donations in order to pay for portions of a U.S.-Mexico border barrier. Bannon built his public persona by amplifying anti-immigrant and pro-populist sentiments, first on Breitbart News, and then as Trump’s right-hand man during the 2016 campaign. Prosecutors now allege he fleeced his fellow America Firsters out of more than $1 million, which he then used to pay one of his co-conspirators and to cover his own personal expenses “unrelated to We Build the Wall.”

Bannon was indicted Thursday on one count of conspiracy to commit wire fraud and one count of conspiracy to commit money laundering.

As the executive chairman of Breitbart News following the death of site founder Andrew Breitbart, Bannon shaped the outfit’s nativist stance—with stories on things like “scary descriptions of refugees“—and called it “the platform for the alt-right” in a 2016 interview. He would go on to become one of the architects of Trump’s travel ban aimed at Muslim-majority countries. And though the Trump administration has said on various occasions that it supports a legal immigration program, Bannon calledlegal immigration “the real beating heart of [the] problem.”

In addition to encouraging nativist discontent, Bannon has branded himself as one of America’s most prominent populists, bucking the establishment, in theory, to assist the Little Guy. The indictment against Bannon calls into question his dedication to advancing his goals, considering he allegedly deceived his fellow patriots for the sake of financing a lavish personal life.

Bannon, who was found and arrested Thursday morning on a $35 million yacht belonging to a close associate, has already called the indictment a “political hit job.” A few figures on the right have followed suit, including Fox News host Lou Dobbs, who characterized it as a “deep state plot,” and Jenna Ellis, a Trump 2020 campaign adviser, who tweeted it was “yet another malicious political prosecution,” referring to the growing list of close Trump aides who have faced criminal charges.

Yet the indictment describes an ornate plot set in motion by Brian Kolfage, Andrew Badolato, Timothy Shea, and Bannon, who used the fundraising ruse to regularly siphon large sums of money from people who believed that 100 percent of their donations would go toward construction and that the campaign organizers indicted this week were volunteering their time and resources without payment. The project raised a total of $25 million and, according to the campaign’s website, 100 miles are “ready to be built.” Though under five miles of border fencing has actually been erected, the site reads “Promises Made, Promises Kept.”

Bannon claimed this week that the prosecution was motivated by politics. “This entire fiasco is to stop people who want to build the wall,” he said as he left the federal courthouse in Manhattan on Thursday, though Bannon himself was one of the primary obstacles standing in the way of his project’s success.

If convicted, Bannon faces up to 40 years in prison, but his actual sentence will likely not come close to that statutory maximum penalty. The average federal sentence for wire fraud in 2019 was around two years, a range that’s stayed relatively consistent over the last decade. For money laundering, the average sentence falls around 75 months or a little over six years.

from Latest – Reason.com https://ift.tt/2EhZThn

via IFTTT

Smith is apparently involved with Jennings’ ex-wife, who is in a bitter custody battle with Jennings. Jennings, Smith alleged, had written posts falsely stating that Smith was a “pedophile” and a “known predator” (see the application for the TRO for more), so Smith sued Jennings for libel.

So far so good: Smith might have a valid libel claim. But instead of just getting damages, or even an injunctions against future libels, the court issued this pretrial restraining order (Smith v. Jennings(Okla. Dist. Ct.), dated Wednesday):

That can’t be constitutional, it seems to me.

But beyond that, Oklahoma is one of the several states that still forbids injunctions in libel cases, even narrow injunctions that ban repeating statements found to be libelous after a trial on the merits. See House of Sight & Sound, Inc. v. Faulkner, 912 P.2d 357, 361 (Okla. Civ. App. 1995); First Am. Bank & Trust Co. v. Sawyer, 865 P.2d 347, 352 (Okla. Civ. App. 1993). There is a narrow exception for “conspiracy, intimidation, or coercion,” but it is narrow indeed, and First Am. Bank & Trust Co. made clear that the “coercion” element is not satisfied simply by speech being aimed at pressuring a business to give the speaker a refund or similar benefit.

And I’ve seen plenty of other cases that issue such clearly unconstitutionally overbroad injunctions. Just a reminder, I think, that things happen in trial courts that are hard to reconcile with the appellate precedents—and if the losing party doesn’t have the money, energy, or time to fight the case on appeal, the trial judge’s decision stands.

from Latest – Reason.com https://ift.tt/2COg19P

via IFTTT

A coalition of New York City police, firefighter, and prison guard unions have lost their bid to block the city’s planned release of a huge trove of police misconduct records. The ruling clears the way, at least for the moment, for New York City’s Civilian Complaint Review Board (CCRB) to post officers’ complaint histories, and for the New York Police Department to release separate disciplinary records it holds.

All those records had been confidential for the past 40 years under Section 50-a, a notorious police secrecy law. But the New York legislature repealed the law in June—a stinging defeat for police unions, who are still bitterly fighting to claw back what records they can. Today U.S. District Judge Katherine Polk Failla declined to grant a preliminary injunction barring New York City from releasing unsubstantiated misconduct allegations.

“Whoa!” an unidentified person on an unmuted line shouted during the telephonic court hearing, as Failla announced she was almost totally rejecting the police unions’ request.

Last month, Failla temporarily blocked New York City from disclosing the records while she weighed the unions’ arguments that the release of unsubstantiated complaints would lead to retaliation against police officers and harm their reputations and future employment prospects.

But before the unions filed their lawsuit, the review board released misconduct records to the New York Civil Liberties Union (NYCLU) and ProPublica, the latter of which published its own database of more than 4,000 complaints. A court initially blocked the NYCLU from releasing its records, but yesterday the 2nd Circuit Court of Appeals lifted that stay as well.

The NYCLU immediately published a database of more than 320,000 complaints filed against the city’s police officers since 1985. The New York Timesreports that only 3 percent of those complaints were substantiated.

Today Failla ruled that the unions had failed to demonstrate the release would cause concrete harms or risks for officers.

“Plaintiffs have presented speculation only that these disclosures will increase risk of officer harm,” Failla said, noting that such records are public in a dozen other states.

Failla did, however, grant a narrow injunction blocking the city from releasing records on certain low-level disciplinary offenses that can be expunged under the officers’ collective bargaining agreement.

CCRB Chair Fred Davie said in a press release today that this outcome “is not only legally justified, but is the only logical path forward for preserving what New Yorkers and lawmakers intended through the repeal of 50-a. I applaud today’s decision—the fight for transparency has been delayed, but not deterred.”

The unions have until Monday afternoon to appeal Failla’s ruling to the 2nd Circuit Court of Appeals.

from Latest – Reason.com https://ift.tt/3l0CUYK

via IFTTT

Steve Bannon, former chief strategist to President Donald Trump, has been charged with defrauding donors to We Build the Wall, a private fundraising effort partially spearheaded by Bannon that collected donations in order to pay for portions of a U.S.-Mexico border barrier. Bannon built his public persona by amplifying anti-immigrant and pro-populist sentiments, first on Breitbart News, and then as Trump’s right-hand man during the 2016 campaign. Prosecutors now allege he fleeced his fellow America Firsters out of more than $1 million, which he then used to pay one of his co-conspirators and to cover his own personal expenses “unrelated to We Build the Wall.”

Bannon was indicted Thursday on one count of conspiracy to commit wire fraud and one count of conspiracy to commit money laundering.

As the executive chairman of Breitbart News following the death of site founder Andrew Breitbart, Bannon shaped the outfit’s nativist stance—with stories on things like “scary descriptions of refugees“—and called it “the platform for the alt-right” in a 2016 interview. He would go on to become one of the architects of Trump’s travel ban aimed at Muslim-majority countries. And though the Trump administration has said on various occasions that it supports a legal immigration program, Bannon calledlegal immigration “the real beating heart of [the] problem.”

In addition to encouraging nativist discontent, Bannon has branded himself as one of America’s most prominent populists, bucking the establishment, in theory, to assist the Little Guy. The indictment against Bannon calls into question his dedication to advancing his goals, considering he allegedly deceived his fellow patriots for the sake of financing a lavish personal life.

Bannon, who was found and arrested Thursday morning on a $35 million yacht belonging to a close associate, has already called the indictment a “political hit job.” A few figures on the right have followed suit, including Fox News host Lou Dobbs, who characterized it as a “deep state plot,” and Jenna Ellis, a Trump 2020 campaign adviser, who tweeted it was “yet another malicious political prosecution,” referring to the growing list of close Trump aides who have faced criminal charges.

Yet the indictment describes an ornate plot set in motion by Brian Kolfage, Andrew Badolato, Timothy Shea, and Bannon, who used the fundraising ruse to regularly siphon large sums of money from people who believed that 100 percent of their donations would go toward construction and that the campaign organizers indicted this week were volunteering their time and resources without payment. The project raised a total of $25 million and, according to the campaign’s website, 100 miles are “ready to be built.” Though under five miles of border fencing has actually been erected, the site reads “Promises Made, Promises Kept.”

Bannon claimed this week that the prosecution was motivated by politics. “This entire fiasco is to stop people who want to build the wall,” he said as he left the federal courthouse in Manhattan on Thursday, though Bannon himself was one of the primary obstacles standing in the way of his project’s success.

If convicted, Bannon faces up to 40 years in prison, but his actual sentence will likely not come close to that statutory maximum penalty. The average federal sentence for wire fraud in 2019 was around two years, a range that’s stayed relatively consistent over the last decade. For money laundering, the average sentence falls around 75 months or a little over six years.

from Latest – Reason.com https://ift.tt/2EhZThn

via IFTTT

The Democratic Party just hosted its first-ever virtual national convention, where it nominated Joe Biden and Kamala Harris for president and vice president. The goal of the four-day event was to unify the party’s moderates and progressives by focusing on President Donald Trump’s moral and political failings.

But despite all the talk of change, it was clear that after four years of rising walls, spiraling debt, and rule by executive order, the Democrats are resolved to stay the course and continue expanding the size and scope of the federal government.

Biden blasted the Trump administration for its disastrous response to the coronavirus pandemic and pledged to institute a national mask mandate; the rest of his plan was short on specifics. New York Gov. Andrew Cuomo, whose decision to return elderly people infected with COVID-19 to nursing homes led to thousands of deaths, was summoned to provide the party’s vision for responsible leadership.

The Democrats sought to exploit the coronavirus to justify bigger government—what they call “bold” federal action. They pledged strong gun control measures to respond to an “epidemic of gun violence,” even though the gun homicide rate today is half what it was in the early ’90s.

They promised that a Biden-Harris administration would address systemic racial bias and reform a criminal justice system that, ironically, Biden played a lead role in creating. But the speeches were short on specifics about what a Democratic White House would actually do to reverse the impact of laws like the 1994 crime bill, which Biden defended all the way up until the beginning of his presidential campaign last year.

The party did offer numerous proposals for new government mandates and increased spending on social programs to fight racial and wealth inequality. It also tied social justice issues to Biden’s $2 trillion plan to address climate change, which he’s selling as a form of economic stimulus—even as the federal debt just climbed above 100 percent of gross domestic product.

Similar to Trump, Biden promises to move jobs back to the U.S. And though former President Bill Clinton attacked Trump’s tariffs on China, Biden hasn’t committed to repealing those tariffs if elected.

A major theme was Trump’s incompetence, divisiveness, and general inability to rise to the challenges he has confronted. Convention organizers sought to convince voters that Joe Biden would bring back decency and the pre-Trump normal.

Hawaii Rep. Tulsi Gabbard, the Democrats’ most visible critic of our endless wars, wasn’t invited, but former Secretary of State Colin Powell, who alongside Biden helped make the case for the Iraq War, delivered a speech. He argued that a Biden administration would bring back the glory days of America projecting its power around the globe.

Hillary Clinton called Trump’s concerns about vote-by-mail fraud a conspiracy theory, and then repeated one of her own, claiming that it wasn’t her fault she lost the election: Russia stole it away.

Even if you’re disaffected with 2-party politics-as-normal, even if you find the major candidates unacceptable election after election, the 2020 Democratic National Convention was designed to convince you that you can create change at the polls this time for real, and that voting is not just your right but your responsibility—just as long as you vote for Joe Biden and Kamala Harris.

Written and edited by Justin Monticello. Graphics by Isaac Reese and Meredith Bragg. Research by Regan Taylor. Audio production by Ian Keyser.

Photos: Democratic National Convention via CNP/SplashNews/Newscom; Democratic National Convention via CNP/SplashNews/Newscom; Caroline Brehman/CQ Roll Call/Newscom; CNP/AdMedia/Newscom; CNP/AdMedia; Anna Moneymaker—Pool via CNP/MEGA/Newscom; Anna Moneymaker—Pool via CNP/MEGA/Newscom; David Cliff/ZUMA Press/Newscom; Lev Radin/ZUMA Press/Newscom; John Lamparski/ZUMA Press/Newscom; Everett Collection/Newscom; Rod Lamkey—CNP/Sipa USA/Newscom; Ron Sachs/dpa/picture-alliance/Newscom; Richard Ellis/ZUMA Press/Newscom; Jeff Malet Photography/Newscom; Ron Sachs/picture alliance/Consolidated News Photos/Newscom; SMG/ZUMA Press/Newscom; MIKE THEILER/UPI/Newscom; CARLOS BARRIA/Reuters/Newscom; BRIAN SNYDER/UPI/Newscom; Anna Moneymaker—Pool via CNP/MEGA/Newscom; David Crane/ZUMA Press/Newscom; Dennis Brack/DanitaDelimont.com “Danita Delimont Photography”/Newscom; Democratic National Convention V/ZUMA Press/Newscom; CNP/AdMedia/SIPA; Democratic National Convention via CNP/picture alliance/Consolidated News Photos/Newscom; GARY I ROTHSTEIN/UPI/Newscom; Allison Ross/TNS/Newscom; Tia Dufour/White House/ZUMA Press/Newscom

from Latest – Reason.com https://ift.tt/2YpVEY1

via IFTTT