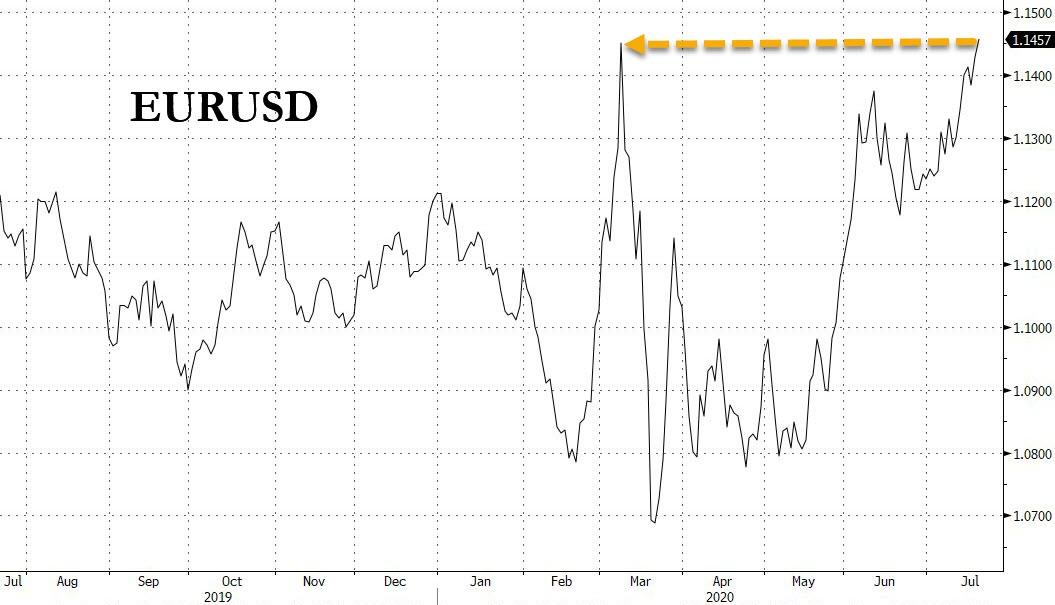

Futures Reverse Losses, Euro Jumps To 4 Month High On Hopes Of EU Rescue Package Deal

Tyler Durden

Mon, 07/20/2020 – 07:52

S&P500 futures pared earlier losses, as European stocks gained and European bond spreads narrowed while the euro strengthened to a four-month high as leaders reportedly made progress in negotiating a historic stimulus package which was still missing after three days of tense, deadlocked weekend negotiations.

US equity futures traded -0.1% lower after dropping -0.6% earlier. In Merger Monday news, Chevron agreed to buy Noble Energy for about $5 billion in shares, the first major deal since the coronavirus triggered a severe oil slump. “Our strong balance sheet and financial discipline gives us the flexibility to be a buyer of quality assets during these challenging times,” Chevron Chief Executive Officer Michael Wirth said in a statement on Monday. “This is a cost-effective opportunity for Chevron to acquire additional proved reserves and resources.“ The deal values Noble at $10.38 a share, or 0.1191 of a Chevron share, equivalent to a 7.5% premium over Friday’s closing price. The total enterprise value, including debt, is $13 billion.

The single currency hit its highest levels against the dollar since March 9, at $1.1467 after early Monday reports of progress following three days of negotiations towards the proposed 750 billion-euro fund. The four governments that have been holding up negotiations are ready to agree on a key plank of the deal, two officials said. The Netherlands, Austria, Denmark and Sweden, also known as the “Frugal Four” are satisfied with €390 billion of the fund being made available as grants with the rest coming as low-interest loans. Still, that number is about €110BN below the €500BN that was originally expected to be made available in the form of grants. A deal envisaging €400 billion in grants – down from a proposed €500 billion – was also rejected by the north, which said it saw €350 billion as the maximum.

Talks on the fund were adjourned on Monday until 1600 CET (1400 GMT). After the adjournment was announced, both the Austrian Chancellor Sebestian Kurz and Dutch Prime Minister Mark Rutte said progress was being made.

“The euro has gained on the likelihood that they do come up with some solution at this meeting,” said Marshall Gittler, head of investment research at BDSwiss Group. “I had expected them to fail, or at best to come to only a partial agreement, but the fact that they’ve kept at it for this long shows that they really are determined to succeed,” Gittler said. A successful agreement would probably give the euro a further boost, he added.

“The chances of a deal appear higher now than before the weekend, with the Frugal Four winning concessions while also acknowledging grants must be part of the deal,” strategists at UBS Global Wealth Management said in a note to clients. “While it remains to be seen if a deal can be done today, we continue to expect an eventual agreement, which would act as a catalyst for the euro and support Eurozone equities and bonds.”

Bond markets also cheered the progress, with Italy’s 10-year bond yield spread over Germany, a key gauge of risk in the region, falling to 161 bps, the lowest level since March.

Stock markets were more reserved in their optimism, however. The pan-European Stoxx 600 index 0.2% higher by mid-morning trade in London, reversing an earlier loss of -0.8% with a risk-off tone expressed in sectoral gainers and losers. Shares of chemical and construction companies led the gains, while the region’s travel and leisure stocks retreated on continued worries over the coronavirus pandemic. AstraZeneca Plc gained ahead of highly anticipated results from early vaccine studies.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan gained 0.26%, reversing loses earlier in the day, led by materials and IT, after rising in the last session. Most markets in the region were down, with Jakarta Composite dropping 0.6% and Australia’s S&P/ASX 200 falling 0.5%, while Shanghai Composite resumed its bubbly ways, closing at session highs, up 3.1% after regulators raised the equity investment cap for insurers and encouraged mergers and acquisitions among brokerages and mutual fund houses. China’s Chalco and Changjiang & Jinggong posting the biggest advances. Japan’s Topix gained 0.2%, with Japan Communications and Takara & Co Ltd rising the most. Australia’s S&P/ASX 200 index dropped 0.5% after authorities warned that a surge in COVID-19 cases in the country’s second most populous state could take weeks to tame.

More than 14 million people have been infected by the novel coronavirus globally and nearly 602,000 have died, according to a Reuters tally.

South Korea’s KOSPI pared gains to fall 0.1%. Japan’s Nikkei was also down 0.1% after data showed the country’s exports suffered a double-digit decline for the fourth month in a row in June.

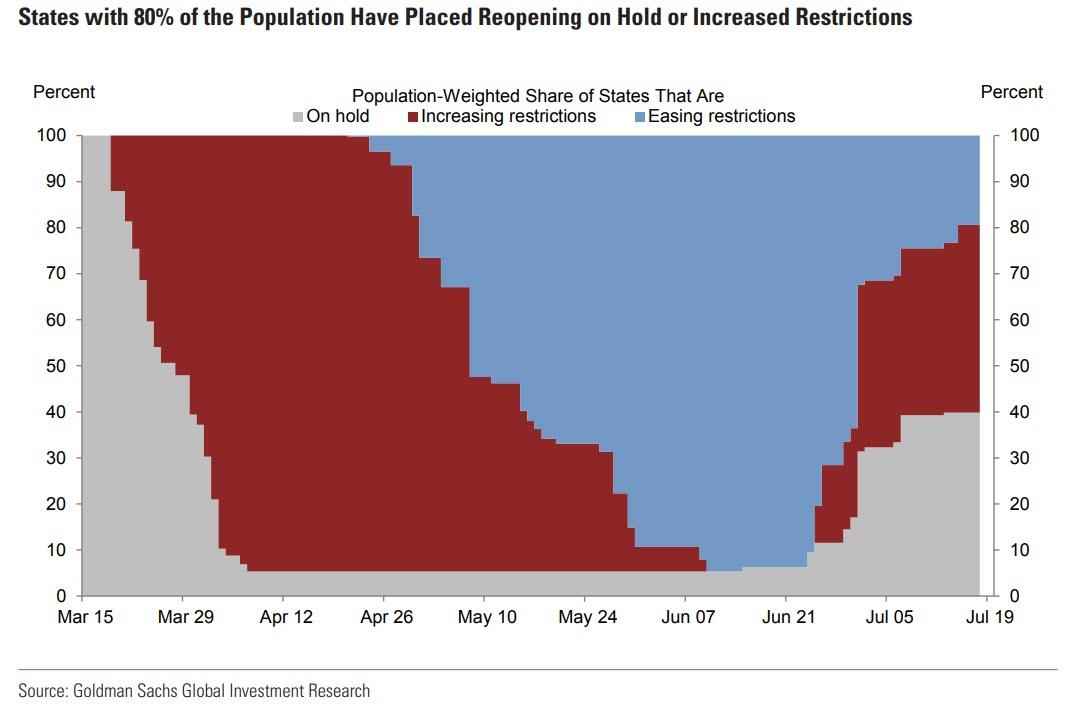

Meanwhile, in the US talks on a new stimulus package will start on Monday with with Mitch McConnell, Steven Mnuchin and others as several states in the country’s South and West imposed new lockdowns to curb the virus and 80% of states now stopping or reversing reopening according to Goldman.

With the virus spreading rapidly in parts of the U.S., there are still plenty of worries about the health of the global economy. Los Angeles Mayor Eric Garcetti has warned that the city is on the brink of another stay-at-home order. Hong Kong added a record 108 infections, will require civil servants to work from home and plans to mandate wearing of masks in all shared indoor areas.

”The economic dislocation of Covid-19 triggered a tremendous response by fiscal and monetary policy makers as well as central banks,” said Gene Tannuzzo, a portfolio manager at Columbia Threadneedle. “These measures helped to stabilise markets, yet we still find ourselves in an environment of continuous low growth.”

While stock markets have inched higher in recent weeks, there are still plenty of worries about the health of the global economy, especially with the virus spreading unabated in parts of the U.S. In the euro area, unemployment could hit almost 10% by the end of the year as the economy slumps, according to a Bloomberg survey.

In rates, Treasury yields were slightly richer across the curve, outperforming bunds following report that EU leaders are set to resume deadlocked recovery-fund talks. Treasury yields were lower by 0.5bp to 1.1bp across the curve with 2s10s, 5s30s flatter by 0.6bp and 0.2bp; 10-year yields around 0.618%, richer by less than 1bp vs Friday’s close. Bunds cheaper by 2.2bp, gilts by 1.2bp vs Treasuries.

In currencies, the Bloomberg Dollar Spot Index shrugged off early gains to slip as the euro rallied to 4 month highs. Italian bonds climbed and U.S. equity futures pared losses as European stocks gained. Meanwhile, the Japanese yen rose to 107.22. while Sterling gained 0.4% to trade as high as $1.2618. The risk-sensitive Australian dollar was down 0.1% at $0.6989.

In commodities, spot gold traded flat at $1,809.58 an ounce, still near a nine-year top. Oil extended losses toward $40 a barrel, unnerved by the prospect of rising coronavirus cases halting a recovery in fuel demand. WTI and Brent were both down 1% each to $40.14 per barrel and $42.71 per barrel, respectively. Prices for copper, a barometer of economic growth, fell on Monday after data showed rising inventories in Chinese warehouses and on concern the climbing coronavirus cases threatened a sustainable global recovery.

Halliburton and IBM are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.2% to 3,207.75

- STOXX Europe 600 down 0.5% to 370.93

- MXAP up 0.2% to 164.86

- MXAPJ up 0.2% to 542.42

- Nikkei up 0.09% to 22,717.48

- Topix up 0.2% to 1,577.03

- Hang Seng Index down 0.1% to 25,057.99

- Shanghai Composite up 3.1% to 3,314.15

- Sensex up 1% to 37,387.70

- Australia S&P/ASX 200 down 0.5% to 6,001.57

- Kospi down 0.1% to 2,198.20

- German 10Y yield rose 0.2 bps to -0.445%

- Euro up 0.4% to $1.1468

- Italian 10Y yield fell 1.7 bps to 1.043%

- Spanish 10Y yield fell 1.4 bps to 0.396%

- Brent futures down 0.6% to $42.90/bbl

- Gold spot up 0.1% to $1,812.34

- U.S. Dollar Index down 0.2% to 95.80

Top Overnight News

- The four EU governments holding up negotiations over 390Bn stimulus package to reboot the bloc’s economy are ready to agree on a key plank of the deal, officials said

- Informal Brexit meetings between the U.K. and EU’s chief negotiators in recent weeks have failed to make progress

- U.K. is set to halt its extradition pact with Hong Kong, marking a further diplomatic escalation with China

- Saudi Arabian King Salman bin Abdulaziz of has beenadmitted to a hospital in Riyadh early Monday for medical tests, the second elderly ruler of an oil-rich Gulf Arab nation to be hospitalized in less than a week

APAC stocks traded choppy after the region initially took its cue from Wall Street’s mixed close on Friday as the decline in Netflix shares kept other large tech stocks at bay ahead of another earnings-abundant week, with 92 S&P 500 companies alongside eight Dow 30 constituents bracing to report their numbers – including the likes of Tesla, Microsoft, Twitter, IBM and some major US airlines. ASX 200 (-0.5%) lost steam after the open as Australia remained subdued by the outbreak in its second largest state of Victoria– which prompted authorities to announce a mandatory mask-wearing rule over the weekend. Nikkei 225 (+0.1%) swung between gains and losses after seeing initial pressure as Japan’s June trade balance printed a significantly wider-than-expected deficit in JPY terms, but with losses somewhat cushioned on currency dynamics. Meanwhile, Hang Seng (-0.1%) conformed to the downside across the region at the open and as Hong Kong is set to tighten restrictions following a spike in COVID-19 cases, but later erased losses, whilst Shanghai Comp (+3.1%) outperformed as reports noted that Beijing is to lower its COVID-19 alert level as cases are back under control, whilst the PBoC also injected a net CNY 50bln via 7-day reverse repos. Finally, JGB futures traded lower in early Tokyo trade, whilst most of the curve saw some cheapening, but the longer-end held despite 20yr supply tomorrow.

Top Asian News

- Hong Kong Growth to Halve as City Loses Distinctiveness: S&P

- China Condemns U.K.’s ‘Wrong Words and Actions’ on Hong Kong

- BP Singapore Oil Traders Placed on Leave Amid Disputed Deals

European equities (Eurostoxx 50 +0.3%) kicked the session off on the backfoot before paring losses as market participants eye events in Brussels and the COVID situation in the US. Despite some of the harsh words spoken between EU leaders over the weekend, the latest state of play indicates that some form of agreement on the recovery fund could be on the cards as the so-called “frugal four” appear to have settled on a figure of EUR 390bln for the grants component of the fund (subject to pushing for additional rebates from the EU budget). As such, it is now on EU members external to the frugals to meet the group “halfway”. Talks have currently taken a pause and will resume once again later today at 1500BST. Despite a potential agreement being on the horizon and upside for the EUR currency (suggesting the market is taking a favourable view of the situation), stocks took a little while to recover off lows with indices now broadly flat/marginally firmer. Stateside, COVID concerns remain at the forefront with the US reporting +67k cases yesterday and as according to Fulcrum economists, the r-rate is above 1 in 45 of the 50 US states, which between them account for 95% of U.S. GDP. From a sectoral standpoint, sectors trade mixed with some of the more cyclical names such as travel & leisure and autos faring worse than peers. For the former, it is worth noting that reports suggest Barcelona could have to return to lockdown within the next two weeks, such a development would be troubling given it is such a tourist hotspot for Europe and a potential sign of things to come for other such destinations. Elsewhere, losses for health care names are shallower than most with AstraZeneca (+3.2%) lending some support after signing an in-principal agreement with Britain’s business ministry for 1mln doses of a treatment containing COVID-19 neutralising antibodies for those who cannot receive a vaccine. Note, markets also await data from the Co.’s early-stage human trials due to be published in The Lancet later today (timing TBC). Other notable movers include Natixis (-7.3%) after BPCE pushed back on FT speculation that it was looking to purchase the remaining 30% shares of Natixis they do not already control. To the upside, UBI Banca (+12.4%) sit at the top of the Stoxx 600 after reports noted that Intesa Sanpaolo increased its bid for UBI, offering EUR 0.57/shr in addition to 1.7 shares for each UBI share.

Top European News

- Glaxo to Invest Up to $1 Billion in CureVac Vaccine Pact

- U.K. Orders 90 Million Vaccine Doses from Pfizer, Valneva

- Europe’s Climate Laggard Plans Green Revolution With Oil Company

In FX, the Dollar is mixed vs major rivals and seems to be settling into relatively narrow ranges that often mark the start of a new week, albeit after some volatility in certain Usd/G10 pairings overnight and in early EU trade. The index is rotating around 96.000 within a 95.792-96.183 band and maintaining an underlying bid on broad risk aversion to counter losses against a few counterparts and the latest more specific US COVID-19 developments that include record rises of confirmed cases in some states again.

- EUR – Renewed hope of a deal on the EU Recovery Fund at the next meeting of leaders is keeping the Euro elevated amidst stops on a break of last week’s peak vs the Greenback that pushed the pair up to circa 1.1467 at one stage. However, an agreement is far from certain as the so called ‘frugals’ continue to contest the total size of the crisis package and composition between grants and loans – for a more in depth look at the current state of play and latest proposals check out the headline feed at 9.03BST. In terms of technical factors, Eur/Usd resistance is seen at the 1.1495 ytd high from March 9 ahead of 1+ bn expiries at 1.1500, while even heftier option expiry interest at the 1.1400 strike (2.6 bn) should add to psychological support and underlying bids.

- CHF/JPY – Both weaker vs the Buck, with the Franc back below 0.9400 and Yen under 107.00, albeit off worst levels through 107.50 on the back of worse than forecast Japanese trade data, while the former will have taken note of a Chf 5 bn or so jump in Swiss domestic bank sight deposits. Indeed, Eur/Chf is also higher alongside Eur/Jpy, eyeing 1.0775 and 123.00 ahead of CPI and trade respectively on Tuesday.

- GBP/NZD/CAD/AUD – All essentially flat relative to the US Dollar, with Sterling gleaning some traction from the single currency’s advance as Eur/Gbp fails to extend beyond last Friday’s high and drifts back down towards 0.9100, while the Kiwi rotates around 0.6550 on marginally favourable Aud/Nzd cross flows in the run up to RBA minutes and a speech from Governor Lowe that are keeping the Aussie contained/capped at 1.0675 and near 0.7000. Elsewhere, the Loonie is meandering between 1.3600 and 1.3570 awaiting Canadian housing data, retail sales and CPI over the next 48 hours for some independent impetus following the BoC and July MPR that was bereft of economic estimates.

- EM – Another strong rally in Chinese equities, a firmer PBoC Usd/Cny midpoint fix and net injection of 7-day liquidity all keeping the Yuan afloat above 7.0000 and close to resistance near 6.9800 that has been tested twice so far in July, but the Lira remains rigid between 6.8500-8600 ahead of Thursday’s CBRT policy meeting even though the Turkish CB jacked up the FX RRR by 300 bp to raise reserves by some Usd 9 bn.

In commodities, WTI and Brent have begun the week on the backfoot, as sentiment in general has been subdued for much of the session after a choppy APAC handover following a mixed US close and a number of updates from the EU Council meeting. For the crude complex itself newsflow has been slow, attention was grabbed by reports that the Saudi King Abdulaziz was admitted to hospital; but, ultimately did not cause a price reaction as the reason was testing for an infection. For the week itself there isn’t anything scheduled on the crude front of note, aside from the usual weekly private inventories, DoE’s & Baker Hughes updates. As such, the complex may well itself more at the whim of broader sentiment/USD action – barring any unscheduled updates of course. Most recently, Sinopec are cutting refining rates for July due to demand being impacted by severe flooding, according to sources. Moving to metals where spot gold is currently little changed on the day and is comfortably above USD 1800/oz handle and withing proximity to the high of circa USD 1812/oz. Citi, on the precious metal, writes that a rally to record prices is only a matter of time and ascribes a 30% chance to USD 2000/oz by Christmas; given, record ETF inflows, increased gold asset allocations & low real yields among other factors.

US Event Calendar

- Nothing major scheduled

DB’s Jim Reid concludes the overnight wrap

After 3 days and long nights of the extended EU recovery fund summit, the diplomatic lake in Brussels remains frozen over even if there does seem to be signs that we’ll see a thaw today.

The very latest reports this morning (although this could be out of date by the time you read) are pointing towards a possible compromise for €390bn in grants in the recovery fund. It seems much depends on whether Macron believes this to be ambitious enough. The wires have just quoted a French official as saying “France now see a path to a recovery fund deal”. It seems we may be on hold until this afternoon though but the fact that we are still going well into a fourth day suggests a desire to get something done.

The Euro is largely unchanged this morning against the greenback at 1.1424 even as the US dollar index is up +0.20%. Meanwhile, Asian markets are trading mixed with the Shanghai Comp (+2.62%) and Hang Seng (+0.35%) up while the Nikkei (+0.05%) and Kospi (-0.05%) are flat and the Asx (-0.48%) is down. Chinese markets have danced to a different beat over the last couple of weeks so not much read through for other global markets here. Elsewhere, futures on the S&P 500 are trading down -0.32%.

Moving onto the coronavirus, globally reported cases crossed the 14 million mark over the weekend with fatalities above 605k. Sao Paulo crossed New York to become the most infected state globally with 415,049 confirmed cases. In the US, cases rose at an average of +1.72% per day this weekend above the +1.53% rise per day registered in the previous 5 weekends while fatalities rose at +0.47% vs. previous 5 weekend average of 0.34%. In terms of state level data new case growth slowed in Texas, Florida and Arizona over the weekend compared to previous weekends indicating that renewed lockdown measures are helping. However, in California new case growth was at an average of +2.47% vs. the previous 5 weekend average of +2.20%. Meanwhile, fatalities picked up with Texas registering an average per day growth of +2.21% as against +1.07% per day over the previous 5 weekends. Likewise, Florida (at +1.83% vs. +0.99%), California (at +1.26% vs. +0.74%) and Arizona (at +3.41% vs. +1.77%) all registered rises.

In Asia, Hong Kong is planning to extend mandatory wearing of masks to more public spaces after registering a record 108 new infections yesterday and has extended restaurant restrictions and gym closures for another week. Melbourne has also mandated its residents to wear masks as Victoria state added another 275 cases. China’s Xinjiang province is also seeing a small spike in new cases (17) leading to concerns around a second wave.

In other overnight news, talks on a new coronavirus stimulus package will start at the White House today with Senate Majority Leader Mitch McConnell, Treasury Secretary Steven Mnuchin and others. Bloomberg reported that priorities for the talks include funding to expedite development of therapeutics and vaccines for the coronavirus, “protections for the American worker and those that employ individuals” and the manufacturing sector, particularly bringing jobs back to the US from abroad. President Donald Trump’s chief of staff said that “It looks like that new package will be in the trillion-dollar range, as we have started to look at it, whether it’s a payroll tax deduction, whether it’s making sure that unemployment benefits continue without a disincentive to return to work.”

The data highlight this week will be the flash PMIs for July on Friday (Japan Wednesday). Elsewhere earnings season picks up a bit more, with 88 releases from S&P 500 companies and another 76 from the STOXX 600.

For the flash PMIs for July, the highlight will be whether US progress has stalled given the increased spread of the virus over the last few weeks. In terms of expectations the US numbers are expected to tick up from the high 40s to the 51-52 range. In Europe there is more of a spread but the composite is expected to be at 51. It will be interesting to see if the European numbers can edge ahead of the US given the clearer run of reopenings. However Europe did see lower troughs and could have more scarring as a result. We will see over the months ahead as to whether the US – that didn’t ever totally lockdown – will see that offset by not fully controlling the virus.

Speaking of the US, another data highlight of note will be the weekly initial jobless claims for the week through July 18. Last week it fell by a smaller-than-expected -10k to 1.3m, which is the smallest weekly decline since they reached their peak back in late March, raising concerns over the speed of the labour market recovery. Over in Europe, another release will be the European Commission’s advance consumer confidence indicator for July (Thursday). The last couple of months have seen a rebound from its April low, but it still remains well below its levels at the start of the year, so it’ll be interesting to see if this upward momentum is sustained.

Earnings season moves into full flow this week, with 88 releases from S&P 500 companies and another 76 from the STOXX 600. In terms of the highlights to look out for, today we have IBM. Then tomorrow, that’s followed by Novartis, The Coca-Cola Company, Texas Instruments, Philip Morris, Lockheed Martin and UBS. Then on Wednesday, we have Microsoft, Thermo Fisher Scientific and Tesla. Thursday sees Roche, Intel, AT&T, Unilever, Union Pacific, Daimler, Twitter and Hyundai release earnings. Finally on Friday, we’ll hear from Verizon, NextEra Energy, T-Mobile and American Express.

It’s a quieter week on the central bank front, with Fed speakers now in their blackout period ahead of next week’s meeting. However, we will get decisions from some EM central banks, including Turkey and South Africa on Thursday and Russia on Friday. Otherwise, the Bank of Japan will be releasing the minutes of their June meeting today, and we’ll also hear from the BoE’s Haldane, Tenreyro and Haskel this week.

Looking back at last week now and markets were generally constructive even though the outlook for the virus in the U.S. has caused a great deal of uncertainty after more states paused and rolled back reopening plans. The S&P 500 gained +1.25% (+0.28% Friday) on the week, and finished at the highest end-of-week close of the pandemic. The tech-focused Nasdaq underperformed this week as earnings season got underway, falling -1.08% (+0.28% Friday) as the mega-cap growth NYSE FANG index saw its worst week (-4.91%) since the height of the market turmoil in March. European equities slightly outperformed the S&P with the Stoxx 600 gaining +1.60% (+0.16% Friday) over the five days. It was the third straight weekly advance, tied for the longest streak since November 2019. Major European bourses were all strongly higher on the week with the DAX (+2.26%), CAC (+1.99%), FTSE (+3.20%) and FTSE MIB (+3.30%) gaining ground. Asian indices were fairly mixed as Chinese stocks saw a large pullback after the over +7.5% rally the prior week with the CSI 300 down -4.29%, while the Nikkei (+1.82%) and Kospi (+2.37%) were higher over the week.

Core sovereign bonds were mixed even as risk assets generally rose. US 10yr Treasury yields fell -1.8bps (+1.0bps Friday) to finish at 0.627%, while 10yr Bund yields gained +1.8bps (+1.8bps Friday) to -0.45%. In other fixed income, HY cash spreads continued tightening both in Europe and the U.S. as sentiment improves and more stimulus seems on the way. US HY cash spreads tightened -39bps (-3bps Friday) and Europeans ones tightened -14bps (-4bps) Friday. The dollar fell -0.73% on the week to its lowest weekly close since February 2019, while the Euro gained +1.13% to the highest point early March.

via ZeroHedge News https://ift.tt/3jtBeXd Tyler Durden