Pandemic, Economic Crash, Social Unrest, And Now Four Asteroids? Tyler Durden

Tue, 06/02/2020 – 21:45

This year has been nothing short of astonishing. In the last five months, the US has been inundated with a virus pandemic, triggering an economic crash and 40 million unemployed, and now worsening social unrest in major metros. But what’s happening on the ground might be the least of our worries on Tuesday, as four asteroids are about to pass the planet.

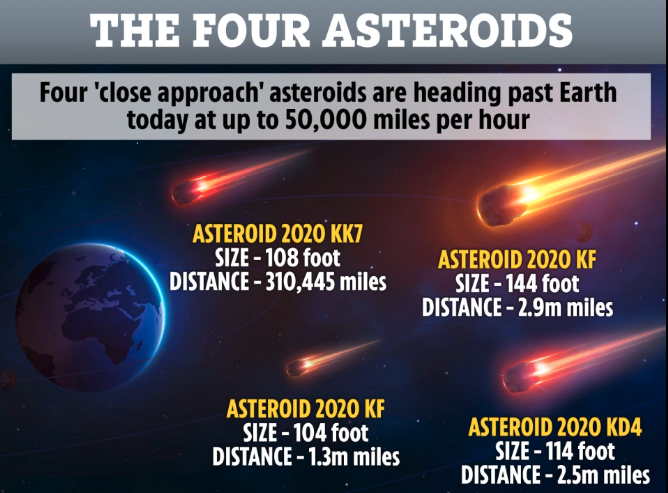

NASA’s Center for Near-Earth Object Studies (CNEOS) has detected “four near-Earth objects that will fly past” the planet on Tuesday, reported International Business Times.

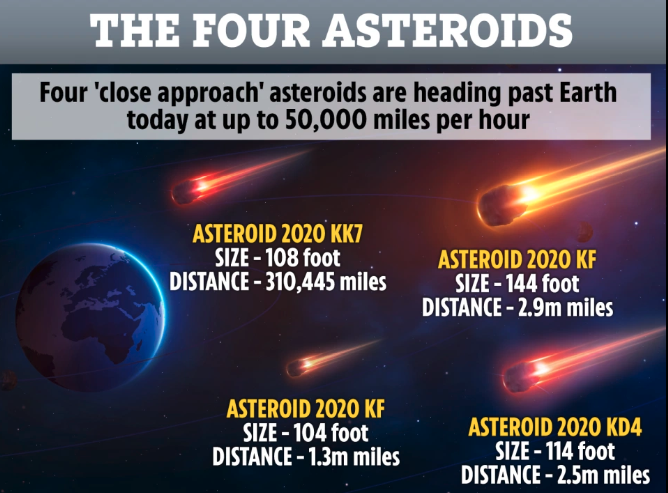

CNEOS’ data showed the first asteroid, identified as 2020 KK7, measures about 108 feet wide and traveling at 34,000 mph, will pass the planet on Tuesday at a distance of 0.00343 astronomical units or approximately 319,000 miles. To put this in perspective, this means the giant space rock will pass Earth at a distance that is about from here to the Moon.

The second asteroid to pass Earth is called 2020 KD4. The rock measures about 115 feet wide and is traveling at 12,000 mph, will pass the planet at a distance of about 0.02680 astronomical units or around 2.5 million miles away.

The third asteroid to pass Earth is called 2020 KF, which has an estimated diameter of 144 feet, is the largest asteroid to approach the planet, and is traveling at about 24,000 mph. It’s expected to pass the planet at a distance of about 0.03102 astronomical units or 2.9 million miles.

And the fourth asteroid to pass Earth on Tuesday is called 2020 KJ1, has an estimated diameter of about 105 feet, and is moving at 11,000 mph, will pass the planet at about 0.01403 astronomical units or 1.3 million miles.

Amid the social-economic collapse of America, political commentator Katie Hopkins’ prayers could be answered…

Former Antifa member Gabriel Nadales praised President Donald Trump for his tweet saying that he intends to designate Antifa a domestic terror organization after several nights of violent riots and looting in dozens of major American cities.

Nadales, who is an employee of Campus Reform‘s parent organization, the Leadership Institute, joined Stuart Varney on Fox Business Network on Monday to discuss the recent riots that arose out of protests to the killing of George Floyd, an unarmed black man killed while in Minneapolis police custody.

Nadales was among the first to call for Antifa to be labeled a terror organization in 2019. Trump said at the time he was considering labeling the group a terror organization. Now, it appears the president has made up his mind.

“The United States of America will be designating ANTIFA as a Terrorist Organization,” Trump tweeted Sunday.

Nadales reacted to the news Monday, telling Varney, “Antifa’s acts are the very definition of domestic terrorism.”

“If you look at some of the violence, it’s being instigated by anarchists and Antifa activists,” Nadales, the former Antifa member said, “not by the peaceful protesters who are rightfully angered by what happened.”

WATCH:

via ZeroHedge News https://ift.tt/2XTpYcC Tyler Durden

77-Year-Old Retired Police Captain Murdered By Looters Tyler Durden

Tue, 06/02/2020 – 21:05

A retired St. Louis City police captain was shot and killed overnight trying to stop looters outside a North City pawn shop, according to KMOV4.

77-year-old David Dorn was found at approximately 2:30 a.m. Tuesday on the 4100 block of Martin Luther King Dr.

“He was murdered by looters at a pawnshop. He was the type of brother that would’ve given his life to save them if he had to. Violence is not the answer, whether it’s a citizen or officer,” wrote the St. Louis Ethical Society of Police of Dorn, whose wife is a sergeant with the St. Louis Metropolitan Police Department.

St. Louis Police Chief John Hayden said Dorn was murdered during a looting while “exercising law enforcement training.”

“David Dorn was a fine captain, many of us young officers looked up to him,” Chief Hayden said.

Chief Hayden said officers will wear their mourning badges in response to Dorn’s death. –KMOV4

Graphic:

“All over some TVs.” 77-year-old St. Louis retired Police Captain David Dorn was shot dead by looters when he tried to get them to stop looting a local pawn shop. pic.twitter.com/Xtvii4HoB1

According to the report, Dorn was with the St. Louis Metropolitan Police Department for 38 years before becoming the police chief in Moline Acres. He joined the police academy in November 1969, graduating in May 1970. After his retirement he joined Patrol Support in October 2007.

Due to his history in law enforcement, Dorn helped out the owners of Lee’s Pawn and Jewelry – checking on it when the alarm would go off, which is what he was doing Tuesday when he was shot and killed.

CrimeStoppers is offering a $10,000 reward for any information leading to an arrest in the case (866-371-8477).

Meanwhile, about the only mainstream coverage given to Dorn’s death has come from Fox News’ Tucker Carlson.

Tucker Carlson On The Violence Against Cops By The Mob

“For 38 years David Dorn was a police officer in the city of St. Louis. No one ever accused Dorn of racism, he was black. He’s dead now, he was murdered last night by the mob.” pic.twitter.com/hszxwYSn7h

— The Columbia Bugle 🇺🇸 (@ColumbiaBugle) June 3, 2020

Federal Reserve Chairman Jerome Powell and Treasury Secretary Steven Mnuchin have become the public faces of the $3 trillion federal coronavirus bailout. Behind the scenes, however, the Treasury’s responsibilities have fallen largely to the 42-year-old deputy secretary, Justin Muzinich.

A major beneficiary of that bailout so far: Muzinich & Co., the asset manager founded by his father where Justin served as president before joining the administration. He reported owning a stake worth at least $60 million when he entered government in 2017.

Today, Muzinich retains financial ties to the firm through an opaque transaction in which he transferred his shares in the privately held company to his father. Ethics experts say the arrangement is troubling because his father received the shares for no money up front, and it appears possible that Muzinich can simply get his stake back after leaving government.

Justin Muzinich, deputy Treasury secretary, in 2019. (Wolfgang Kumm/Picture Alliance via Getty Images)

When lockdowns crippled the economy in March, the Treasury and the Fed launched an unprecedented effort to buy up corporate debt to avert a freeze in lending at the exact moment businesses needed to borrow to keep running. That effort has succeeded, at least temporarily, with credit continuing to flow to companies over the last several weeks. This policy also allowed those who were heavily invested in corporate loans to recoup huge losses.

Muzinich & Co. has long specialized in precisely this market, managing approximately $38 billion of clients’ money, including in riskier instruments known as junk, or high-yield, bonds. Since the Fed and the Treasury’s actions in late March, the bond market has roared back. Muzinich & Co. has reversed billions in losses, according to a review of its holdings, with 28 of the 29 funds tracked by the investor research service Morningstar Direct rising in that period. The firm doesn’t publicly detail all of its holdings, so a precise figure can’t be calculated.

The Treasury is understaffed, and Muzinich was overseeing two-thirds of the department before the crisis hit. He spent his first year as the Trump administration’s point man on its only major legislative achievement, the landmark $1.9 trillion tax cut that mainly benefited the wealthy and corporations.

As the markets panicked about the economic impact of the coronavirus, Muzinich’s responsibilities expanded. The Treasury worked with the Fed on the emergency lending programs, and the agency has ultimate power to sign off. Muzinich was personally involved in crafting the programs, including the effort to bail out the junk bond market, The Wall Street Journal reported in April. He communicates with Fed officials daily by phone, email or text, the paper said.

That effort has manyskeptics. The Fed has never bought corporate debt in its more than 100 years of existence, much less that of the indebted and fragile companies that raise money through the sale of junk bonds. Private equity firms, hedge funds and specialty investment firms like Muzinich & Co. dominate the market for junk-rated debt. In effect, the Fed has swooped in to protect the most sophisticated investors from losses on some of their riskiest bets.

Muzinich & Co. Profited From the Government’s Actions

Muzinich & Co.’s largest fund, with over $10 billion in assets, jumped in value when the Treasury and the Federal Reserve announced plans to buy bonds

Data from Morningstar Direct for the Muzinich Enhanced Yield Short-Term Fund

Justin Muzinich’s ongoing ties to the family firm present a thicket of potential conflicts of interest, ethics lawyers said. Instead of immediately divesting his stake in the firm when he joined the Trump administration in early 2017, Muzinich retained it until the end of that year. But even then, he did not sell his stake and use the proceeds to buy broad-based securities such as index funds, as is common practice. Instead, he transferred his piece of the company to his father, who owns Muzinich & Co. In exchange, he received what amounts to an IOU — a written agreement in which his father agreed to pay him for the shares, with interest, but with no principal due for nine years.

“This is something akin to a fake divestiture,” said Kathleen Clark, a law professor and ethics specialist at Washington University in St. Louis.

“It sure looks like he is simply parking this asset with a relative, and he will likely get it back after he leaves the government.”

A Treasury spokeswoman declined to say whether Muzinich has pledged not to take back the stake in the family firm once his public service ends. Muzinich “takes his ethics obligations very seriously” and “any suggestion to the contrary is completely baseless,” she said.

She added the arrangement with his family firm was approved by the Office of Government Ethics and agency ethics lawyers, who recently reexamined the setup given Muzinich’s role in the economic crisis response. They concluded that there is no currently envisaged scenario in which Muzinich would make decisions as a government official that would affect his father’s ability to repay the money he owes under the IOU.

“Treasury’s career Designated Agency Ethics Official has determined that there is no such conflict of interest, as there are no current or reasonably anticipated matters in which Deputy Secretary Muzinich would participate that would affect the note obligor’s ability or willingness to satisfy its financial obligations under the note,” she said in a statement. (The note obligor is Muzinich’s father.)

Muzinich & Co. did not respond to multiple requests for comment.

Muzinich’s relationship with the family firm also creates potential conflicts related to Muzinich & Co.’s clients. The firm makes money by charging investment management fees to several dozen wealthy individuals, insurance companies, pension funds, as well as what filings describe as a “quasi foreign government corporation.” The client list is not public and it’s unclear whether Muzinich would know about clients that came on board since he left. But any large investor has much to gain, or lose, from decisions being made by the Treasury about the bailout policies.

“The clients of this firm, I imagine, must be thrilled that Muzinich has this vitally important, powerful position with a huge amount of discretion and authority,” Clark said.

The Treasury spokeswoman declined to answer a question about the firm’s clients.

Even as Justin Muzinich has presided over bailout policies criticized by some observers, Muzinich & Co. executives have praised the government’s actions in recent briefings for investors. One described the interventions “as providing somewhat of a floor underneath the high yield market.”

Another Muzinich executive, David Bowen, who manages one of the firm’s high-yield bond portfolios, said during a May 20 webinar, “The Fed has been about as supportive, helpful, accommodative — whatever word you want to use — as anyone could imagine.”

Untangling the Financial Relationship

When Treasury Secretary Steven Mnuchin hired Justin Muzinich as counselor in early 2017, in many ways he was selecting a younger version of himself.

Justin Muzinich, center left, then a top adviser to Treasury Secretary Steven Mnuchin, center, on Capitol Hill on Sept. 12, 2017. (Al Drago/The New York Times/Redux)

Like Mnuchin, Muzinich grew up in New York City, the son of a wealthy finance executive. Also like his boss, Muzinich spent years collecting a series of elite credentials: He attended Groton and holds degrees from Harvard College, the London School of Economics, Yale Law School and Harvard Business School. He worked at Morgan Stanley and spent a few months at a hedge fund associated with billionaire Steven A. Cohen, followed by a few years at EMS Capital, which invests the money of the wealthy Safra family.

Colleagues praise Muzinich as hardworking and serious, and Democrats have expressed relief that he isn’t as inflammatory as many other Trump appointees. Powell, the Fed chair, called Muzinich “creative and extremely capable” in a statement to The Wall Street Journal in April.

In 2010, he joined the family firm and became its president. His father, George, founded the company in 1988, specializing in handling portfolios of American high-yield bonds for European pension funds. The company expanded to offer funds to other institutional investors and wealthy individuals, but it stuck to its focus on corporate credit — particularly the riskier type that pays higher interest rates. Headquartered in New York and London, the firm has eight offices across Europe and one in Singapore.

“Talking about credit all the time might sound boring, I’m sure it does,” Justin Muzinich said in a 2014 interview, “but that is what makes you good.”

As he rose in the family business, Muzinich also launched himself into GOP policy circles, advising the presidential campaigns of Mitt Romney in 2012 and Jeb Bush in 2016. He owns a $20 million ultramodern beachfront house in the Hamptons and a $4.5 million Park Avenue apartment and commutes from New York City to work in Washington.

When Muzinich entered the Trump administration, he reported owning stock and stock options in the family firm collectively worth at least $60 million. The true value could be much higher, but disclosure rules don’t require officials to give a specific figure for any asset worth more than $50 million.

The Treasury’s ethics officers are frequently called on to rule on complex questions, given that the department tends to attract people from careers on Wall Street who have large, complicated financial holdings — from ex-Goldman Sachs Chairman Hank Paulson to banker and Hollywood financier Mnuchin.

Stakes in individual companies can create conflicts of interest. So incoming Treasury officials typically sell those stocks and invest in broad-based options like mutual funds. Ownership in private investment funds can be particularly thorny because ethics rules treat each of the fund’s investments in specific companies as sources of potential conflicts. Sarah Bloom Raskin, who preceded Muzinich as deputy secretary in the Obama administration, reported holding only a collection of index and mutual funds that either track the whole stock market or a large basket of companies.

But government ethics officials did not require Muzinich to sell his stake in the family firm through his first year in office as counselor to Mnuchin.

According to ethics filings, Muzinich said that he did not divest it until December 2017, the month the tax law was signed. (Several months later, in April 2018, Trump nominated him to be deputy secretary.)

Muzinich did not receive cash for most of his stake in the family firm. Instead, his more recent financial disclosures show that the stake, held in a family trust, was replaced with an opaque asset described as a “receivable from family,” valued at over $50 million.

Muzinich’s disclosure filings don’t reveal much about this asset at all. They don’t say who the family member is or explain the arrangement. They don’t say how the terms were negotiated, or even if the valuation of the deal was vetted by an independent third party.

It turns out that Muzinich transferred his stake to his father. But his father didn’t have to pay him right away. According to a Senate Finance Committee memo obtained by ProPublica, Justin received two promissory notes from his father in return for the shares. The notes pay Justin between $1 million and $5 million in interest over a year, at a rate of 2.11%. Moreover, his father does not have to pay any principal on the loan for nine years.

Neither the financial disclosure forms nor the Senate memo say how long the agreement is supposed to last. Neither addresses the possibility of his getting the shares back after he leaves the government. The Treasury says the transaction is “not reversible” but did not elaborate.

In other words, Justin still has an ongoing long-term stake in the financial well-being of Muzinich & Co., since his father now owes him more than $50 million. If the company were to plummet in value or even go under, it could cost Justin. Actions the Treasury and the Fed take can either enhance the chances he gets his money back or lower them.

The Treasury defended the IOU transaction as an appropriate remedy for any conflicts of interest. The agency provided a statement from Elizabeth Horton, an ethics attorney who left the agency in 2019 and who worked with Muzinich on the divestiture from his family business. Horton said that when Muzinich first joined the agency, “the Treasury ethics office correctly advised him that he did not need to divest his holdings in his family business because of the generalized nature of his work on tax reform legislation.” She said that when his duties changed, “I advised Mr. Muzinich that an exchange for a fixed value note was an appropriate way to divest.”

Horton said that advice was “consistent with practice in previous administrations” — though the Treasury declined to cite similar cases. “Muzinich worked very closely with the ethics office and was extremely attentive to his ethics obligations,” Horton said.

ProPublica reached out to four ethics officials, including two former Treasury ethics lawyers. None could recall a similar divestment transaction. Three of the four disagreed that it resolved Muzinich’s conflicts, while one said that turning it into an asset with a value that doesn’t fluctuate with future developments should shield him from any allegations of impropriety.

The deal does not look like an arms-length transaction, said Virginia Canter, who served as a career ethics attorney at Treasury during the George W. Bush administration and is now at the watchdog group Citizens for Responsibility and Ethics in Washington.

“The terms of the loan suggest something less than a bona fide transaction,” she said. “Once he leaves office, nothing in the arrangement appears to preclude Muzinich from forgiving the debt owed to him by his father so they can amicably agree on returning to Muzinich the interest in the Muzinich family business.”

As ranking member of the Finance Committee, Sen. Ron Wyden opposed Muzinich’s nomination as deputy secretary because of his role in crafting the tax bill. Although he would have preferred a cash sale of the Muzinich & Co. stock, Wyden said in a statement that in July 2018 Muzinich had agreed to “strengthen his recusal commitments to include matters where his family’s company is a party.”

That satisfied Wyden at the time, but it is a very narrow restriction. A vast range of issues before the Treasury could affect Muzinich & Co. regardless of whether the firm was directly a party to any of them.

How Justin Muzinich treated the transaction for tax purposes could reveal whether it was a true and final sale or not.

Ordinarily, a sale of an asset such as equity in a company would trigger a capital gains tax bill. In Muzinich’s case, that could run into the tens of millions of dollars, even though his father paid him no cash upfront. But there is an exception if the asset in question is merely transferred with a commitment to have it returned, said Steve Rosenthal, a tax law expert at the Urban-Brookings Tax Policy Center.

“If you are merely parking or pledging securities, and you are going to get them back, that’s not viewed as a taxable transaction,” he said.

It is not clear how he reported the transaction to the IRS, and whether he was left with a huge tax bill. The Treasury declined to comment on the tax issues.

Tax Reform — for Friends and Family

Through his first year in the administration, even as Muzinich continued to own his stake in the family firm, he met with a wide range of business executives to hash out major tax provisions that would affect them, according to his 2017 calendars that ProPublica obtained after suing the Treasury last year under the Freedom of Information Act. Others were obtained by the watchdog group American Oversight. The Treasury redacted large sections of the calendars, saying that they required consultation with the White House before they could be released.

One of the most important principles in the federal government ethics rules covers whether an official is dealing with a “particular matter” that would affect a discrete group of people with specific interests or a “general matter” that affects a larger and more diverse group.

The Treasury spokeswoman said the tax reform bill was to affect a very large and diverse group, so ethics rules did not prevent Muzinich from working on it. He was allowed to keep his equity in the company while working on the tax bill because his “duties did not include particular matters that required divestiture of certain assets.”

But many industries had specific interests in the tax bill that they lobbied on — industries that may include clients of Muzinich & Co. Insurance companies, for example, featured prominently. Muzinich met with trade groups representing insurers as well as Liberty Mutual, The Hartford, Zurich and Blue Cross Blue Shield. In the final tax bill, property and casualty insurers fared particularly well by dodging new limitations on deductions that applied to other companies.

Insurance companies invest their premiums in order to increase their profits. In its regulatory filings, Muzinich & Co. reports that 17 of its 89 clients are insurance companies, which have given the firm more than $1.4 billion to invest. Muzinich & Co. did not provide a list of its clients.

Some of the companies Muzinich & Co. has stakes in also have been lobbying the Treasury on their own behalf. For example, Muzinich & Co. helps its clients invest in business development companies, a type of investment fund that enjoys lower taxes in exchange for providing capital to medium-sized companies. The firm itself owns stock in BDCs, many of them run by private equity companies such as Ares Capital Corporation, which has paid millions of dollars to lobby for looser rules governing the BDC industry.

Even beyond any overlap with the family firm’s interests, Muzinich’s calendars, which cover the period from February to September of 2017, reflect the administration’s priorities in negotiating the tax deal. Muzinich spent long days in meetings with private equity titans, energy company CEOs and heavy-hitting interest groups like the Business Roundtable and the anti-tax group Americans for Prosperity. His calendar shows no meetings with labor unions or progressive groups.

Muzinich did meet often with the Treasury’s in-house tax experts but frequently didn’t follow their recommendations. Richard Prisinzano, who served in the agency’s tax analysis office until August 2017, recalled trying to tell Mnuchin and Muzinich that drastically lowering corporate tax rates would likely prompt businesses to transform into C corporations, which often pay lower rates under the new law.

He argued that such a change would further reduce tax revenues. Muzinich disagreed, Prisinzano said, protesting that businesses wouldn’t change their corporate form just to lower their taxes. “He really pushed back,” Prisinzano recalled. “He said to me, ‘The secretary is a numbers person, and the numbers don’t make sense to him.’”

“‘I’m a numbers person, and they make perfect sense to me,’” Prisinzano said he responded. “That was not an answer that they liked.”

In the following two years, many large businesses did indeed convert into C corporations, including private equity giants Ares, Blackstone and KKR. The government hasn’t produced an estimate of how big a hit taxpayers took from these conversions.

During his confirmation hearing as deputy secretary in July 2018, Democratic senators pressed Muzinich on whether he agreed with the White House that the tax bill would “pay for itself,” despite the dire projections of independent forecasters such as the nonpartisan Congressional Budget Office. “Yes,” Muzinich responded.

It has not come close, as corporate tax collections plunged and left the national debt at historic levels on the eve of the pandemic.

Muzinich Takes on the COVID-19 Crisis

As the economic response to the novel coronavirus consumed Washington in March, Mnuchin turned again to Muzinich to negotiate with Congress over the shape of a bailout intended to sustain companies as they weathered the worst part of the crisis.

Ultimately, Trump administration officials and lawmakers settled on a package worth more than $2 trillion, divided into aid regimens for different sectors of the economy. While setting general parameters, the Coronavirus Aid, Relief and Economic Security Act gives the Treasury wide latitude over how the money is to be distributed. It calls for $50 billion in grants and loans for the airline industry, for example, with few rules on who should get what. (In another potential intersection with Muzinich’s Treasury work, Muzinich & Co. started a new business line to loan money to airlines to buy planes in February.)

Perhaps the greatest power the Treasury now has is the authority to sign off on Fed loan programs funded with CARES Act money. The Fed has said it will leverage that money to lend up to several trillion dollars.

Among their biggest decisions: Which firms to include in the $600 billion Main Street Lending Program, which will lend directly to mid-sized businesses, and how to structure two programs that will purchase up to $750 billion in corporate bonds.

The Main Street program, which has yet to launch, changed substantially after it was first announced to sweep in bigger companies and those with heavier debt loads. Offering a glimpse into how the Treasury directly shaped the Fed programs, Energy Secretary Dan Brouillette told Bloomberg the change was made in part to make sure beleaguered oil companies had access to the program’s favorable terms. Muzinich & Co.’s U.S.-based funds include dozens of energy companies.

Mnuchin also deputized Muzinich to fix problems that arose during the first round of funding for the Paycheck Protection Program, which offers forgivable loans to small businesses. The government hasn’t said who got money through the program, but Muzinich & Co.’s portfolio includes many companies that are small enough to be eligible.

The Fed’s bond purchasing programs will go even further to help companies with poorly rated credit.

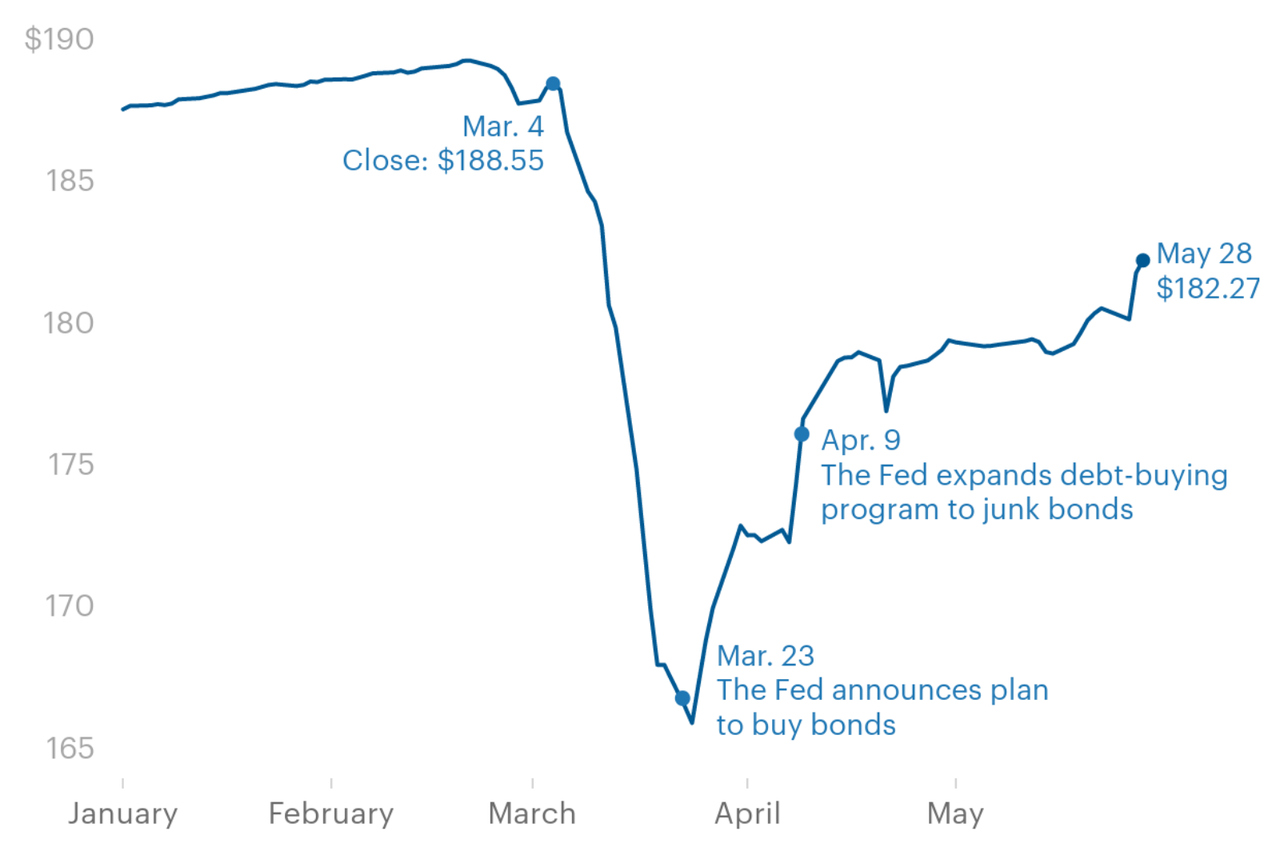

On March 23, the Fed and the Treasury announced a sweeping stimulus program that would involve buying hundreds of billions of dollars of investment-grade bonds. Selling bonds is a way for large companies like Boeing or PepsiCo to raise money for new investments, to fund day-to-day operations or to pay back older loans. Companies that are strong and profitable are expected to be able to pay back the borrowed money. Their bonds are deemed “investment grade” and come with lower interest rates. The news of the Fed program on its own heralded a dramatic recovery in the bond market, which in three weeks recovered nearly all of the 13.6% it had lost since the plunge began on March 6, according to one index.

Then, on April 9, the Fed announced, with the Treasury’s approval, that it would expand its efforts to buy some junk bonds. These carry higher interest rates because the borrowing companies are viewed as riskier and may already be heavily in debt. One index tracking that market segment surged nearly 8% on the news, the most in a decade. This risker category of bonds has expanded dramatically in recent years as companies took on higher debt burdens to do things like acquire competitors and buy back stock. These are the bonds in which Muzinich & Co. has long specialized.

At the end of 2019, Muzinich & Co. reported it had $2.8 billion of assets under management in its U.S. high-yield bond strategy. A Muzinich fund that focuses specifically on those bonds took significant losses in March, as companies like oilfield services provider Targa Resources and Caesars Entertainment saw the price of their bonds fall 30% and 35% respectively.

The government’s announcement buoyed Muzinich & Co.’s high-yield holdings along with everyone else’s. The portfolio manager for the firm’s U.S. high-yield offering also praised CARES Act’s tax provisions that would “help high yield companies.”

In a separate development in May, the Fed expanded another Treasury-backed lending program in a way that could help Muzinich & Co.’s portfolio. The central bank said May 12 it would support “syndicated loans,” another form of corporate debt often in which riskier firms borrow money from multiple lenders. Muzinich & Co. had more than $3 billion in assets under management in U.S. and European syndicated loans at the end of last year.

The good news for Muzinich & Co. keeps coming. As the firm’s head of investment strategy, Erick Muller, told investors in a May 13 webcast about the junk bond market: “The recovery is pretty spectacular.”

via ZeroHedge News https://ift.tt/2MqAh2y Tyler Durden

Unprecedented Surge In New CMBS Delinquencies Heralds Commercial Real Estate Disaster Tyler Durden

Tue, 06/02/2020 – 20:25

One month ago, we thought that the unprecedented implosion in US commercial real estate in the month of April following the near-uniform economic shutdown following the coronavius pandemic, manifesting in the surge in newly delinquent CMBS loans would be one for the ages, even though as we predicted May would likely be worse as a result of the spike in specially services loans.

And indeed while April was catastrophic, May was even worse.

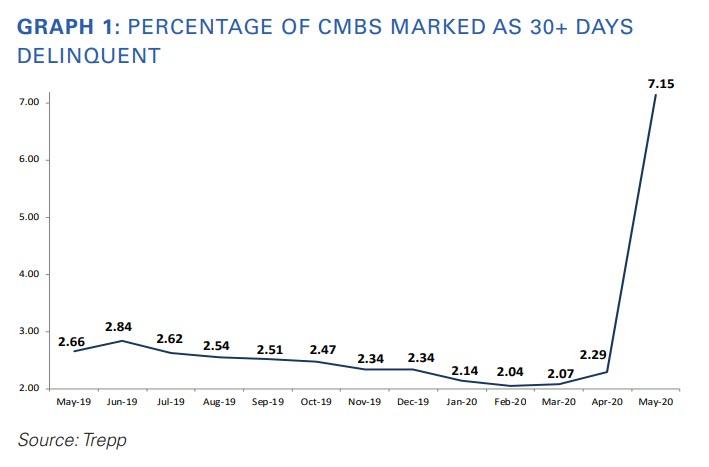

According to the latest remittance data by Trepp, the surge in CMBS delinquencies that most industry watchers were anticipating came through in May. After Trepp’s CMBS Delinquency Rate registered at 2.29% in April, in May the Delinquency Rate logged its largest increase in the history of this metric since 2009. The May reading was 7.15%, a jump of 481 basis points over the April number. Almost 5% of that number is represented by loans in the 30-day delinquent bucket.

There was some good news: given that about 8% of loans had missed payments for the April remittance cycle (in the grace period), the fact that delinquencies went up less than 5% has to be viewed as a small “win.” That, or simply the backlog of delinquencies has prevented the proper accounting of all deals.

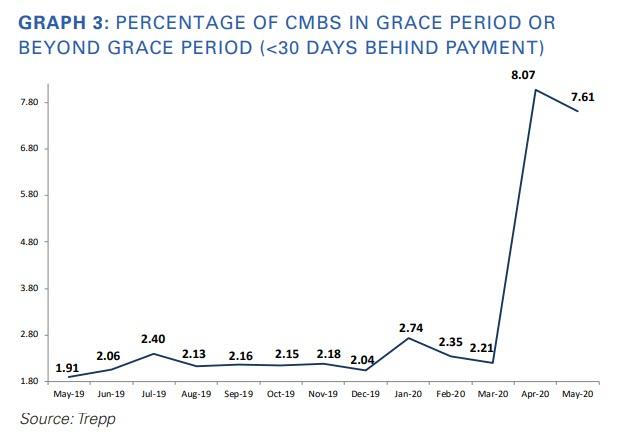

Alas, that “win” won’t last, and will be reversed next month, when the delinquency rate will hits double digits as about 7.61% of loans by balance missed the May payment but remained less than 30 days delinquent (i.e., within the grace period).

On the other hand, as more forbearances receive approval, some delinquent loans could revert to current status based on expectations of how loan statuses will be reported in servicer data going forward, if reported correctly. For instance, if a loan’s last payment was made in March, it would not show up as 60 days delinquent in June if a forbearance had been granted. Of course, this step merely delayed the inevitable, and once forbearances are exhausted, all those loans which are classified as current will all slide right into the default bucket without passing go.

Some other overall statistics:

The percentage of loans in special servicing rose from 4.39% in April to 6.07% in May. According to May servicer data, 16.2% of all lodging loans were in special servicing, up from 11.4% in April. In addition, 9.3% of retail loans are with the special servicer, up from about 6% the month prior. The percentage of loans on servicer watchlist in May was 19.9%.

The Overall Numbers

The overall US CMBS delinquency rate climbed 481 basis points in May to 7.15%. The all-time high on this basis was 10.34% registered in July 2012. We expect this number will be surpassed in the June update.

The percentage of A/B loans (i.e. loans in “grace period” or “beyond grace” period) was 7.61% in May.

Year-to-date, the overall US CMBS delinquency rate is up 449 basis points.

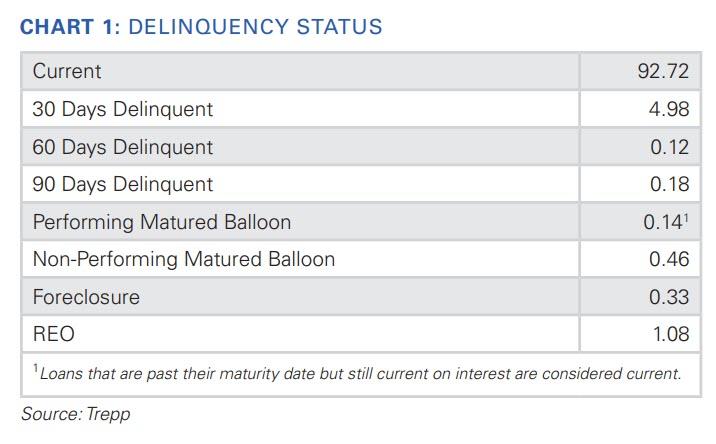

The percentage of loans that are seriously delinquent (60+ days delinquent, in foreclosure, REO, or nonperforming balloons) is now 2.17%, up six basis points for the month. (As noted above, the largest increase this month was seen in the 30-day delinquency category; expect the percentages for 60+ day delinquencies to move higher in June.)

If defeased loans were taken out of the equation, the overall 30-day delinquency rate would be 7.56%, up 515 basis points from April.

One year ago, the US CMBS delinquency rate was 2.66%.

Six months ago, the US CMBS delinquency rate was 2.34%

The CMBS 2.0+ Numbers

The CMBS 2.0+ delinquency rate jumped 503 basis points to 6.19% in May. The rate is up 545 basis points year over year.

The percentage of CMBS 2.0+ loans that are seriously delinquent is now 1.10%, which is up 12 basis points from April.

If defeased loans were taken out of the equation, the overall CMBS 2.0+ delinquency rate would be 6.54%, up 531 basis points for the month.

The CMBS 1.0 Numbers

Note: With CMBS 1.0 loans outstanding dwindling, we plan to retire this statistic beginning in Q3 2020.

The CMBS 1.0 delinquency rate rose 110 basis points to 41.74 % in May.

The percentage of CMBS 1.0 debt that is seriously delinquent rose 24 basis points to 40.89% last month.

If defeased loans were taken out of the equation, the overall CMBS 1.0 delinquency rate would be 47.04%

Overall Property Type Analysis (CMBS 1.0 and 2.0+)

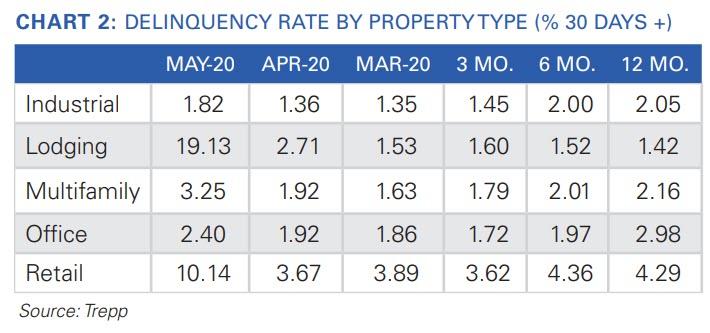

The industrial delinquency rate climbed 46 basis points to 1.82%

The amount of industrial loans categorized as A/B: 2.41% in May

The lodging delinquency rate jumped 1642 basis points to 19.13%.

The amount of lodging loans categorized as A/B: 14.08% in May

The multifamily delinquency rate rose 133 basis points to 3.25%.

The amount of multifamily loans categorized as A/B: 2.78% in May

The office delinquency rate moved up 48 basis points to 2.40%.

The amount of office loans categorized as A/B: 2.72% in May

The retail delinquency rate spiked 647 basis points to 10.14%.

The amount of retail loans categorized as A/B: 12.53% in May

via ZeroHedge News https://ift.tt/3gQmtMs Tyler Durden

Crime has been down for decades, but incarceration is still sky-high and brutality cases keep tearing the country apart. Does policing in America need a fundamental re-think?

Watching all the terrible news in the wake of the police killing of George Floyd, it’s been hard not to think about Eric Garner. The cases have so many similarities. Once again, an unarmed African-American man in his forties has been asphyxiated in broad daylight by a police officer with a history of abuse complaints. He and his fellow officers ignore cries of “I can’t breathe,” and keep subduing their target even after he stops moving, unconcerned that he’s being filmed.

Five years ago, while sketching the outline for a book about the Garner case called I Can’t Breathe, my editor suggested I take on a larger question.

Why, he asked, do we even have police? After all, the history of policing in our country, especially as it pertains to minority neighborhoods, has always rested upon dubious justifications. The early American police forces evolved out of slave patrols in the South, and “progressed” to enforce the Black Codes from the Civil War period and beyond, on to Jim Crow through the late sixties if not longer.

In an explicit way, American policing has almost always been concerned on some level with enforcing racial separatism. Because Jim Crow police were upholding a way of life, the actual laws they were given to enforce were deliberately vague, designed to be easily used as pretexts for controlling the movements of black people. They were charged with punishing “idleness” or “impudence,” and encouraged to enforce a range of vagrancy laws, including such offenses as “rambling without a job” and “leading an idle, profligate, or immoral course of life.”

I ended up not taking on that question, focusing on the hard-enough question of what had led two young, amped-up policemen to choke the life out of a harmless father and street character like Garner. I was more interested in those police than all police, and part of me – the white part, probably – thought the answer to the question of why we need police at all was at least somewhat self-evident.

But the Garner story ended up graphically revealing the way modern “Broken Windows” policing had evolved to fit the tactics of those centuries of racial enforcement. I learned that “vagrancy” laws had been replaced in cities like New York with essentially identical offenses like “obstructing pedestrian traffic” and “obstructing government administration.”

In Staten Island, a borough that to this day remains very segregated – white and black residents alike refer to the Staten Island Expressway that bisects black neighborhoods to the north and white neighborhoods to the south as the “Mason-Dixon line” – the young black men who lived in and around the Tompkinsville area where Garner was killed told stories of being stopped and ticketed whenever they crossed into the wrong neighborhoods.

The new strategies rely upon extremely high numbers of contacts between police and subject populations, who are stopped for every conceivable minor offense – public intoxication, public urination, riding bicycles the wrong way down a sidewalk, refusing to obey police orders, jumping subway turnstiles, and, in Garner’s case, selling loose cigarettes.

This idea of high-engagement policing was born in the mind of a Midwestern academic/corrections official named George Kelling. Kelling conducted a number of studies for think tanks like the Police Foundation and eventually co-authored a hugely influential 1982 article in the Atlantic called Broken Windows.

Kelling in his research found that while people may not actually be safer, they feel safer when there is less visible “disorder” in their neighborhoods, e.g. panhandling, litter, graffiti, etc. Also, research suggested such disorder was incentive to further disorder: as Stanford researcher Philip Zimbardo put it, “If a window in a building is broken and left unrepaired, all of the rest of the windows will soon be broken.”

“Broken Windows” revolutionized policing, changing it from a business of fighting crime to doing what Kelling described as “order maintenance.” If earlier police theorists like Orlando “O.W.” Wilson hoped to defeat crime by putting officers in squad cars and giving them advanced tools to react more quickly to offenses, the new strategy stressed stopping crime before it got started, by building and maintaining something not defined in law books – “order.”

Once again, police were charged with enforcing not rules but a way of life, and were asked again to view the law as more of a tool than an end in itself. The famous “Broken Windows” article spoke approvingly of officers in Chicago who read between the lines of the law to chase gang members out of a project: “In the words of one officer, ‘We kick ass.’”

The Kelling revolution was credited with early successes, like the cleaning up of the New York City subway. Soon the “Broken Windows” strategy (sometimes euphemistically called “community policing”) was the norm in big cities. Mass stops and arrests led to amazing numbers, like Baltimore under Mayor Martin O’Malley arresting 100,000 people in 2004 alone, or the city of Chicago stopping 250,000 people in 2014, a stop rate four times higher than New York in the peak years of “stop-and-frisk.”

When such policing became hot in the nineties, as advocates like Bill Bratton became national celebrities (here he is on the cover of Time in 1996 under the headline, “Finally, we’re winning the war against crime. Here’s why”), police departments became infected by a corporate-like mania for “goal-setting” and “deliverables.” There was no numerical way to impress politicians if police just worked cases as they came: to show progress, Bratton believed, one had to order police to produce concrete quantities of stops, searches, arrests.

Commissioners demanded captains deliver numbers and captains began browbeating lesser officers, who in turn pushed quotas on patrol cops, for reasons that often had nothing to do with crime. As depicted in the The Wire, in the stats revolution, “shit always rolls downhill.” The point was to get lieutenants promoted to captain, to get mayors re-elected, and help provide the rationale for the prison jobs state legislators were bringing home to suburban districts. All of this was greased by the lobbying money of construction firms, prison vendors, even private prison corporations – a great business for all, and all that was needed to keep it going was an endless stream of jailable people.

This is why, even as rates of both violent crime and property crime have been decreasing steadily since the early nineties, rates of incarceration have been exploding in the other direction. For most of the 20th century the rate of incarceration in America was roughly 110 per 100,000 people. As of last year, the number was 655 per 100,000. Although the numbers have dipped slightly in recent years, down from a high of about 760 per 100,000 in 2013, the quantity of prisoners in America remains absurdly high.

Such aggressive, military-style policing would be not be tolerated by voters if it were taking place everywhere. It’s popular, and continues to be embraced by politicians in both parties, because it’s only happening in “those” neighborhoods (or, as Mike Bloomberg once put it, “where the crime is”). Even during the Covid-19 crisis, 80% of the summonses for social distancing violations are given out to blacks and Hispanics. Does anyone really think that minorities account for that massive a percentage of those violations? Do they think black people really commit 3.73 times as many marijuana offenses as white people?

Basically we have two systems of enforcement in America, a minimalist one for people with political clout, and an intrusive one for everyone else. In the same way our army in Vietnam got in trouble when it started searching for ways to quantify the success of its occupation, choosing sociopathic metrics like “body counts” and “truck kills,” modern big-city policing has been corrupted by its lust for summonses, stops, and arrests. It’s made monsters where none needed to exist.

Because they’re constantly throwing those people against walls, writing them nuisance tickets, and violating their space with humiliating searches (New York in 2010 paid $33 million to a staggering 100,000 people strip-searched after misdemeanor charges), modern cops correctly perceive that they’re hated. As a result, many embrace a “warrior” ethos that teaches them to view themselves as under constant threat.

Police are trained to behave like occupiers, which is why they increasingly dress like they’ve been sent to clear houses in Mosul and treat random motorists like potential car-bombers – think of poor Philando Castile, shot seven times by a police officer who leaped back firing in panic like he was being attacked by Freddy Krueger, instead of a calm, compliant, educated young man. Officers with histories of abuse complaints like Daniel Pantaleo and Derek Chauvin are kept on the force because senior officers value police who make numbers more than they fear outrage from residents in their districts. The incentives in this system are wrong in every direction.

The current protests are likely to inspire politicians to think the other way, but it’s probably time to reconsider what we’re trying to accomplish with this kind of policing. In upscale white America drug use is effectively decriminalized, and Terry stops, strip searches, and “quality of life” arrests are unknowns. The country isn’t going to heal as long as everyone else gets a knee in the neck.

via ZeroHedge News https://ift.tt/3eIE6fp Tyler Durden

Lancet Issues Major Disclaimer On Anti-HCQ Study, As Manufactured Disinformation Foments Hysterics Tyler Durden

Tue, 06/02/2020 – 19:45

The Lancet has issued a major disclaimer regarding a study which prompted the World Health Organization to halt global trials of hydroxychloroquine (HCQ), an anti-Malaria drug currently being used around the world to treat COVID-19.

As we noted last week, major data discrepancies have called the entire study into question – though the lead author says it does not change the study’s findings that patients who received HCQ died at higher rates and experienced more cardiac complications than without.

Until the data has been audited, The Lancet issued the following “expression of concern” regarding the study.

“Important scientific questions have been raised about data reported in the paper by Mandeep Mehra et al,” reads the “expression of concern” from The Lancet.

“Although an independent audit of the provenance and validity of the data has been commissioned by the authors not affiliated with Surgisphere and is ongoing, with results expected very shortly, we are issuing an Expression of Concern to alert readers to the fact that serious scientific questions have been brought to our attention. We will update this notice as soon as we have further information.”

I took hydroxychloroquine for two years. A long time ago as a visiting cancer surgeon in Asia, in Thailand, Nepal, India, and Bangladesh. From 1987 to 1990. Malaria is rife there. I took it for prophylaxis, 400 milligrams once a week for two years. Never had any trouble. It was inexpensive and effective.

I started it two weeks before and was supposed to continue it through my stay and four weeks after returning. But I stopped it after two years. I was worried about potential side effects of which there are many, as with all drugs right down to Tylenol and aspirin. These, however, are rare. At a certain point, I was prepared to take my chances with mosquitoes and plasmodium, and so I stopped.

Chloroquine, the precursor of HCQ, was invented by Bayer in 1934. Hydroxychloroquine was developed during World War II as a safer, synthetic alternative and approved for medical use in the U.S. in 1955.

The World Health Organization considers it an essential medicine, among the safest and most effective medicines, a staple of any healthcare system. In 2017, US doctors prescribed it 5 million times, the 128th most commonly prescribed drug in the country. There have been hundreds of millions of prescriptions worldwide since its inception. It is one of the cheapest and best drugs in the world and has saved millions of lives. Doctors also prescribe it for Lupus and Rheumatoidarthritis patients who may consume it for their lifetimes with few or no ill effects.

Then something happened to this wonder drug.

From savior of the multitudes, redeemer and benefactor of hundreds of millions, it transformed into something else: a purveyor of doom, despair, and unspeakable carnage.

It began when President Trump discussed it as a possible treatment for COVID-19 on March 19, 2020.The gates of hell burst forth on May 18 when Trump casually announced that he was taking it, prescribed by his physician.

Attacks on Trump and this otherwise harmless little molecule poured in. The heretofore respected, commonly used, and highly effective medicinal became a major threat to life, a nefarious and wicked chemical that could alter critical heart rhythms, resulting in sudden cataclysmic death for unsuspecting innocents. Trump, more than irresponsible, was evil incarnate for daring to even mention it. While at it, the salivating media trotted out the canard about Trump’s nonrecommendation for injecting Clorox and Lysol or drinking fish-tank cleaner to combat COVID. It was Charlottesville all over again.

Before a nation of non-cardiologists, the mediaagonizedover, of all things, the prolongation of the now infamous “QT interval,” and the risk of sudden cardiac death. The FDA and NIH piled on, piously demanding randomized, controlled, double-blind studies before physicians prescribed HCQ. No one mentioned that the risk of cardiac arrest was far higher from watching the Superbowl. Nor did the media declare that HCQ and chloroquine have been used throughout the world for half a century, making them among the most widely prescribed drugs in history with not a single reported case of “arrhythmic death” according to the sainted WHO and the American College of Cardiology. Or that physicians in the field, on the frontlines, so to speak, based on empirical evidence, have found benefit in treating patients with a variety of agents including HCQ, Zinc, Azithromycin, Quercetin, Elderberry supplements, Vitamins D and C with few if any complications. Or that while such regimens may not cure, they may help and carry little or no risk.

And so, the world was aflame once again with a nonstory driven by the COVID media. The HCQ divide within the nation is only a continuation of innumerable divides that have surfaced since the pandemic began — and before. One will know the politics of an individual based on his position on any number of pandemic issues: lockdowns, sheltering in place, face masks, social distancing, “elective surgery,” and “essential businesses.” The closing of schools and colleges. Blue states and Red states. Governor Cuomo or Governor DeSantis. Nationwide injunctions or federalism. The WHO and Red China. Or, pre-pandemic, Brexit, open borders, DACA, and amnesty. CBD oil, turmeric, and legalizing marijuana. Russia Collusion, Trump’s taxes, the 25th amendment, Stormy Daniels, the Ukraine non-scandal, and impeachment. Or Obamagate. And now HCQ.

HCQ is only another bellwether. It represents the latest nonevent in a long string of fabricated media nonscandals. If a nation can be divided over HCQ it can be divided over anything. It shows neatly, as many of the other non-issues did, whether one embraces the U.S., our history, culture, and constitutional system, or rejects it. Whether one believes in Americanism or despises it. It is part of the ongoing civil war, thus far cold, but who knows? The passions today are no less jarring than they were in 1860. One would have thought that a man taking a medicine prescribed by his physician, even a President, would be a private matter. But no. Not today.

We swim in an ocean of manufactured disinformation created by a radical COVID media, our fifth column. They inflame the nation one way or another based on political whims. The propaganda arm of the Left, they seek victory at all costs including dismantling the economy, culture, and our governing system. Is there a curative for the COVID media and their Democrat allies who would destroy a nation to destroy Trump? He is all that stands between us and them. Is there an antiviral for this, the communist virus that has infected the nation, metastasized throughout its corpus, and now threatens the republic?

* * *

Dr. Moss is a practicing Ear Nose and Throat Surgeon, author, and columnist, residing in Jasper, IN. He has written A Surgeon’s Odyssey and Matilda’s Triumph available onamazon.com. Find more of his essays atrichardmossmd.com.

via ZeroHedge News https://ift.tt/3dtV4xY Tyler Durden

Tonight, I spoke with the Little Rock, Arkansas chapter about Corona and the Constitution. I addressed the Supreme Court’s recent decision involving the California church.

I also chatted with ReasonTV about some broader issues.

I travel a lot, but have not been on a plane since March. During the spring semester, I had to cancel about 20 speaking engagements due to the Coronavirus. Slowly, but surely, groups have started to schedule events by Zoom. This development is healthy. I worry that campus organizations will be severely constrained in their ability to hold events in the fall. There will not be enough space, and people will not want to pack into a room to watch a guest speaker. Also, the traditional model of serving food at events (buffet style!) is no longer permissible.

Zoom is a helpful replacement during these tough times. If your group is interested in hosting me for a talk on Zoom and the Constitution, please let me know. I already received an invitation from one student chapter in D.C., and am happy to help out.

from Latest – Reason.com https://ift.tt/3durqse

via IFTTT

On June 11 & 12, the Federalist Society for Law & Public Policy Studies will be hosting a virtual conference on “Covid-19 & the Law.” The various panels, each of which will be presented as a stand-alone webinar, cover a range of topics, including federalism, civil liberties, executive powers, public vs. private decisionmaking, and the 2020 elections. There is a keynote speech by Ajit Pai, Chairman of the Federal Communications Commission. Speakers include Ian Ayres, Susan Dudley, Nadine Strossen, Daniel Farber, Cass Sunstein, Jack Goldsmith, Mila Versteeg, and our own Eugene Volokh, among others. (I’ll be speaking as well.) Registration information is here.

from Latest – Reason.com https://ift.tt/2U2sGLN

via IFTTT

Tonight, I spoke with the Little Rock, Arkansas chapter about Corona and the Constitution. I addressed the Supreme Court’s recent decision involving the California church.

I also chatted with ReasonTV about some broader issues.

I travel a lot, but have not been on a plane since March. During the spring semester, I had to cancel about 20 speaking engagements due to the Coronavirus. Slowly, but surely, groups have started to schedule events by Zoom. This development is healthy. I worry that campus organizations will be severely constrained in their ability to hold events in the fall. There will not be enough space, and people will not want to pack into a room to watch a guest speaker. Also, the traditional model of serving food at events (buffet style!) is no longer permissible.

Zoom is a helpful replacement during these tough times. If your group is interested in hosting me for a talk on Zoom and the Constitution, please let me know. I already received an invitation from one student chapter in D.C., and am happy to help out.

from Latest – Reason.com https://ift.tt/3durqse

via IFTTT

{kind=link}

.jpg){kind=link}