More than 500 doctors have added their names to a letter to President Trump urging him to end the lockdown, warning that it will cause more death than the coronavirus itself.

In the letter, sent last week, doctors described the lockdown as a “mass casualty incident”.

“We are alarmed at what appears to be the lack of consideration for the future health of our patients. The downstream health effects of deteriorating a level are being massively under-estimated and under-reported. This is an order of magnitude error,” it states.

Written by Simone Gold, a California emergency medical specialist, and further signed by hundreds of doctors, the letter adds “The millions of casualties of a continued shutdown will be hiding in plain sight, but they will be called alcoholism, homelessness, suicide, heart attack, stroke, or kidney failure.”

“In youths it will be called financial instability, unemployment, despair, drug addiction, unplanned pregnancies, poverty, and abuse,” the letter further urges.

It notes that “Suicide hotline phone calls have increased 600%,” while sales of alcohol have increased 300% to 600%.

“Because the harm is diffuse, there are those that hold it does not exist. We, the undersigned, know otherwise,” the letter concludes.

While globalists have urged that lockdowns need to continue, medical and economic experts across the board in multiple countries are warning that the loss of life will be much greater than that caused directly by the virus itself, if lockdowns are not scrapped.

A Guardian analysis has found that there have been thousands of excess deaths of people at home in the UK due to the lockdown.

Professor Richard Sullivan also warned that there will be more excess cancer deaths in the UK than total coronavirus deaths due to people’s access to screenings and treatment being restricted as a result of the lockdown. Physicians in the US are issuing the same warnings over cancer screening.

Sullivan’s comments were echoed by Peter Nilsson, a professor of internal medicine and epidemiology at Lund University, who said, “It’s so important to understand that the deaths of COVID-19 will be far less than the deaths caused by societal lockdown when the economy is ruined.”

A data analyst consortium in South Africa asserts that the economic consequences of the country’s lockdown will lead to 29 times more people dying than the coronavirus itself.

Experts have also warned that there will be 1.4 million deaths from untreated TB infections due to the lockdown.

via ZeroHedge News https://ift.tt/2TBKfCb Tyler Durden

Clinton-Appointed Judge Lets Florida Felons Vote, Could Add ‘Hundreds Of Thousands’ To November Rolls Tyler Durden

Mon, 05/25/2020 – 20:00

A federal judge in Florida on Sunday declared key portions of the state’s felon voting law unconstitutional in a ruling that could allow hundreds of thousands of new voters being added to the rolls just in time for the 2020 presidential election.

In a 125-page ruling, US District Judge Robert Hinkle, a Clinton appointee, slammed the state’s “pay-to-vote” system which the GOP-controlled Florida Legislature passed nearly a year ago, which ended the state’s lifetime ban on voting for most ex-felons, but requires that they repay legal financial obligations first, according to Politico.

“This pay-to-vote system would be universally decried as unconstitutional but for one thing: each citizen at issue was convicted, at some point in the past, of a felony offense,” wrote Hinkle. “A state may disenfranchise felons and impose conditions on their reenfranchisement. But the conditions must pass constitutional scrutiny.”

“Whatever might be said of a rationally constructed system, this one falls short in substantial respects,” he added.

Hinkle’s ruling could lead to a major addition to the state’s voting rolls just months before the election in the battleground state. President Donald Trump, who narrowly won the state four years ago, has made winning Florida a key part of his reelection strategy.

One study done by Daniel Smith, a University of Florida political professor, found that nearly 775,000 people with felony convictions have some sort of outstanding legal financial obligation. –Politico

Hinkle claims that requiring people with felony convictions to pay legal fees – which are separate from restitution or fines ordered by the court – before being allowed to vote violated the US Constitution’s ban on poll taxes.

“[T]axation without representation led a group of patriots to throw lots of tea into a harbor when there were barely united colonies, let alone a United States,” wrote Hinkle. “Before Amendment 4, no state disenfranchised as large a portion of the electorate as Florida.”

Hinkle did, however, reject arguments by the groups and individuals who sued that the Florida’s law was discriminatory.

The ruling was immediately applauded by the long-line of groups that were part of the legal challenge, which spanned three different lawsuits.

“Today’s decision is a landmark victory for hundreds of thousands of voters who want their voices to be heard,” Paul Smith, vice president of the Campaign Legal Center, said in a statement. “This is a watershed moment in election law. States can no longer deny people access to the ballot box based on unpaid court costs and fees, nor can they condition rights restoration on restitution and fines that a person cannot afford to pay.” –Politico

And just like that, Trump lost Florida?

via ZeroHedge News https://ift.tt/3ejPH4t Tyler Durden

Donald Trump was impeached last winter for one technical violation of the law and a host of made-up ones. The technical violation was his move to block $391 million in Ukrainian military aid.

It was a violation because it because it interfered with Congress’s exclusive spending powers. But it was purely technical because presidents traditionally have wide latitude in determining how expenditures are made. Back in 1801, Thomas Jefferson’s treasury secretary, Albert Gallatin, argued that the executive branch should be allowed “a reasonable discretion” while, 160 years later, John F. Kennedy had no scruples about unilaterally moving more than $1 million – a lot of money in those days – from one budget account to another to pay for a pet project known as the Peace Corps. No one thought much of it at the time, so Trump’s decision to hold up an appropriation in 2019 doesn’t seem like a big deal.

And it wasn’t, as the December 18 articles of impeachment made clear. Rather than dwelling on the blockage itself, they quickly moved on to the real question at hand, which is why it occurred. The answer, of course, was to pressure newly-elected Ukrainian President Volodymyr Zelensky to launch an investigation into why a notorious oligarch named Mykola Zlochevsky had given Joe Biden’s son Hunter a lucrative no-show job and why the then-vice president had then pushed for the firing of a prosecutor looking into Zlochevsky’s company, Burisma Holdings.

Since any such investigation would have reflected poorly on Biden, the presumptive Democratic nominee, Democrats charged that Trump was seeking to “obtain an improper personal political benefit” by “enlist[ing] a foreign power in corrupting democratic elections.” After welcoming Russian interference in 2016, he was now angling for Ukrainian interference in 2020 – or so they maintained. But the charge never made sense for one all-important reason: however much Trump might benefit, the public had a legitimate interest in learning why Biden had allowed his son to enter into an obviously corrupt relationship at a time when he was supposedly serving as Obama’s point man in rooting out Ukrainian corruption.

It’s as if 1920s Chicago crime buster Eliot Ness had looked the other way while a close relative took a job with Al Capone. So while Democrats made a big show of moral indignation, Senate Republicans were unmoved with the partial exception of notorious featherbrain Mitt Romney, and Trump was acquitted.

But now let’s take a look at Schiff’s sins and see how they compare. Back in 2017, he was the ranking Democrat on the House Intelligence Committee and therefore the man Democrats counted on to lead the charge that Trump had colluded with the Kremlin in order to steal the election. He did so with gusto. Quoting from a dossier prepared by ex-British MI6 agent Christopher Steele, he regaled a March 2017 committee hearing with tales of how Russia bribed Trump adviser Carter Page by offering him a hefty slice of a Russian natural-gas company known as Rosneft and of how Russian agents boosted Trump’s political fortunes by hacking Hillary Clinton’s emails and passing them on to WikiLeaks. Conceivably, such acts could have been purely coincidental, Schiff acknowledged.

“But it is also possible,” he went on, “maybe more than possible, that they are not coincidental, not disconnected, and not unrelated, and that the Russians used the same techniques to corrupt U.S. persons that they have employed in Europe and elsewhere. We simply don’t know, not yet, and we owe it to the country to find out.”

Hours later, he assured MSNBC that the evidence of collusion was “more than circumstantial.” Nine months after that, he informed CNN’s Jake Tapper that the case was no longer in doubt: “The Russians offered help, the campaign accepted help, the Russians gave help, and the president made full use of that help.” In February 2018, he told reporters: “There is certainly an abundance of non-public information that we’ve gathered in the investigation. And I think some of that non-public evidence is evidence on the issue of collusion and some … on the issue of obstruction.”

The press lapped it up.

But now, thanks to the May 7 release of 57 transcripts of secret testimony – transcripts, by the way, that Schiff bottled up for months – we have a better idea of what such “non-public information” amounts to.

The answer: nothing.

A parade of high-level witnesses told the intelligence committee that either they didn’t know about collusion or lacked evidence even to venture an opinion. Not one offered the contrary view that collusion was true.

“I never saw any direct empirical evidence that the Trump campaign or someone in it was plotting [or] conspiring with the Russians to meddle with the election,” testified ex-Director of National Intelligence James Clapper. Obama Attorney General Loretta Lynch told the committee that no one in the FBI or CIA had informed her that collusion had taken place. Sally Yates, acting attorney general during the Obama-Trump transition, was similarly noncommittal. So were Obama speechwriter Ben Rhodes and former acting FBI Director Andrew McCabe. David Kramer, a prominent neocon who helped spread word of the Steele dossier in top intelligence circles, was downright apologetic: “I’m not in a position to really say one way or the other, sir. I’m sorry.”

But rather than admit that the investigation had turned up nothing, Schiff lied that it had – not once but repeatedly.

Let that sink in for a moment. Collusion dominated the headlines from the moment Buzzfeed published the Steele dossier on Jan. 10, 2017, to the release of the Muller report on Apr. 18, 2019. That’s more than two years, a period in which newspapers and TV were filled with Russia, Russia, Russia and little else. Thanks to the uproar, acting FBI Director Andrew McCabe and Deputy Attorney General Rod Rosenstein secretly discussed using the Twenty-fifth Amendment to force Trump out of office, while an endless parade of newscasters and commentators assured viewers that the president’s days were numbered because “the walls are closing in.”

Schiff’s only response was to egg it on to greater and greater heights. Even when Special Prosecutor Robert Mueller issued his no-collusion verdict – “the investigation did not establish that members of the Trump Campaign conspired or coordinated with the Russian government in its election interference activities,” his report said – Schiff insisted that there was still “ample evidence of collusion in plain sight.”

“I use that word very carefully,” he said, “because I also distinguish time and time again between collusion, that is acts of corruption that may or may not be criminal, and proof of a criminal conspiracy. And that is a distinction that Bob Mueller made within the first few pages of his report. In fact, every act that I’ve pointed to as evidence of collusion has now been borne out by the report.”

So Trump colluded with the Kremlin, but in a non-criminal way? Even if Mueller got Schiff in a headlock and screamed in his ear, “No collusion, no collusion,” the committee chairman would presumably reply: “See? He said it – collusion.”

The man is an unscrupulous liar, in other words, someone who will say anything to gain attention and fatten his war chest, which is why contributions flowing to his re-election campaign have risen from under $1 million a year to $10.5 million since the Russia furor began. The man talks endlessly about the Constitution, patriotism, his father’s heroic service in the military, and so on. But the only thing Adam Schiff really cares about is himself.

Trump’s sins are manifold. But with unerring accuracy, Schiff managed to zero in on the one sin that didn’t take place. Considering that the $391 million was destined for ultra-right military units whose members sport neo-Nazi regalia and SS symbols as they battle pro-Russian separatists in the eastern Ukraine, Schiff’s crimes are just as bad, if not worse. Ladies and gentlemen, we give you the next candidate for impeachment, the congressman from Hollywood – Adam Schiff!

via ZeroHedge News https://ift.tt/2TEaFTM Tyler Durden

JPMorgan: The Surge In Gold Is A Sign Of Eroding Confidence In Central Bank-Generated Money Tyler Durden

Mon, 05/25/2020 – 19:00

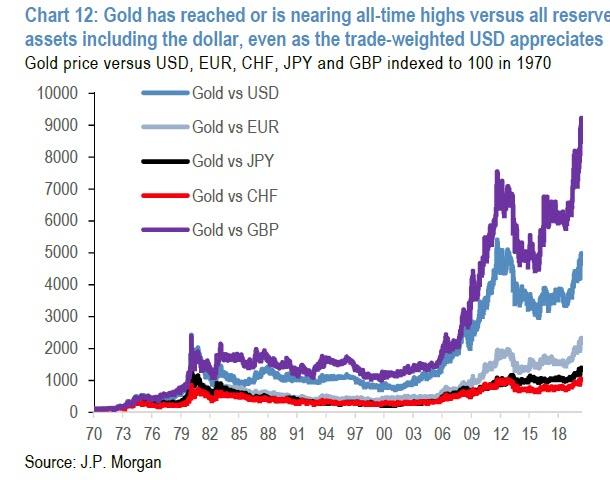

The past few months have been painful for many FX traders, as a result of a global economic crisis has left the major reserves currencies – USD, EUR, JPY, CHF, GBP – clustered at rate levels between roughly 0% to -0.5%, which doesn’t allow rate differentials to inspire much movement amongst them, and is also one reason a G10 currency index like DXY hasn’t moved much during this crisis.

But the lack of dispersion within this bloc shouldn’t be “misread as investor comfort with these reserve assets in an era of record budget deficits from high starting levels of indebtedness, in turn motivating long-term concerns about sovereign risk in Europe and inflation or fiscal irresponsibility elsewhere” as JPMorgan writes in its Weekly Asset View report authored by John Normand.

Indeed, as the bank ominously continues, these background concerns may partly explain why Gold, “which is the world’s legacy reserve asset”, has made or is nearing all-time highs versus the euro, yen, sterling, Swiss franc and the dollar (9% from an all-time high) even as the trade-weighted dollar creeps higher.

And while JPM takes a measured approach in qualifying what this move in gold means for the dollar, saying “this isn’t anything close to the dollar crisis that is foretold every few years in response to extreme loose Fed policy or rising twin deficits (fiscal and current account)” explaining that such an “outcome would deliver instead high-volatility USD depreciation versus all reserve currencies due to capital flight”, the bank’s conclusion is nonetheless disturbing for its brutal honesty:

… instead, take this Gold move as a sign of eroding confidence in central bank-generated money generally, a trend that will probably continue until enough growth returns to put fiscal policy on a more efficient path.

But what is enough growth does not return to put fiscal policy on a more efficient path? What if, instead, the entire world turns into China where the only economic growth comes from flooding the economy with debt, resulting in massive malinvestment and an avalanche of defaults just waiting to begin?

Indeed, what if the world is has crossed the Rubicon where the marginal utility of debt is collapsing and it takes exponentially more leverage to create even the smallest uptick in growth.

What happens to gold then?

via ZeroHedge News https://ift.tt/3c2GOuy Tyler Durden

“The US Is Bluffing”: China Claims Trump Too “Weakened” By Pandemic To Intervene In Hong Kong Tyler Durden

Mon, 05/25/2020 – 18:29

In his overnight market commentary, Rabobank’s Michael Every laid out an interesting hypothesis why markets continue to fade the risk of a serious escalation in tensions between the US and China: “Perhaps as within serious HK money circles there is absolute certainty that the US is now an EU-style paper tiger and has no stomach for a real fight, and that Trump is so beholden to Wall Street that he won’t dare act.”

And while Every himself disagrees with this sanguine assessment, saying this stance “captures the self-confidence in Beijing but utterly fails to capture the bipartisan anger in DC, or the fact that both sides are using Beijing as a stick to beat each other with in the 2020 presidential election, or that the US has financial weapons as fearsome as its military, or that the Fed is there to prop up the stock market anyway”, he appears to have a point regarding China’s “self-confidence.”

In an editorial published in China’s Global Times, the authors claim that Trump is indeed nothing but a paper tiger and that “US talk of Hong Kong a nothingburger” in response to Beijing’s formulation of a national security law. To be sure, the article is filled with the usual jingoist allegations, first claiming that “the US is again leading the Western camp in besieging China” a stance that is driven by the “compression of Western values”, resulting from “the rise of emerging markets and developing countries becoming increasingly independent.”

The editorial then makes a rather valid point that how China frames national security in the context of Hong Kong is entirely its own matter and not that of the US:

Fighting the national security law for Hong Kong is not a universal value and cannot withstand serious scrutiny. Isn’t national security the top priority for each and every country? Washington has always used national security as an excuse to suppress normal commercial activities. Saying that the national security law in Hong Kong hinders the city’s high degree of autonomy and ends its freedom will hardly fool all Westerners, let alone manipulate the whole international community.

China indeed has every right to pursue whatever it sees as its national interest; the real question is who will suffer more from the explicit return of Hong Kong under China rule. And while Trump has claimed that Hong Kong will be crippled as a financial gateway to China should it lose its special trade status with the US, China counters that the US is no longer a critical partners, read source of foreign funds (a curious position considering China’s capital account is about to turn negative and will, more than ever, rely on outside sources of capital). Instead, the Global Times argues that as Hong Kong’s relationship with the US fades, it will be replaced by a more powerful one with China:

The biggest pillar for Hong Kong’s status as an international financial center is its role as a window to the Chinese mainland as well as its special relationship with the mainland economy.

The special trade status given by the US is important, but is not a decisive factor to determine whether Hong Kong is a financial center or not. As long as the economy in the Chinese mainland keeps booming, Hong Kong will not decline. If the US changes its policy toward Hong Kong, that will result in a lose-lose situation. But Hong Kong will be able to adjust and maintain its prosperity with the support of the Chinese central government.

But what is most remarkable about the op-ed is the view that as a result of the US being “entangled” with the coronavirus epidemic, which has claimed 100,000 American lives, Trump will be unable to mobilize the “tools and resources” he needs to intervene externally:

As the US is entangled in the COVID-19 epidemic, its actual ability to intervene externally is weakening. The White House claimed it would impose sanctions on China, but the tools and resources at its disposal are fewer than those it could mobilize before the outbreak. It is only bluffing.

If this is indeed the fundamental position of China’s leadership re Covid-19 which just “slipped” through in an op-ed written by a state-owned newspaper – that the US’ own fight with the pandemic has left it too weak to respond to foreign policy challenges – it would provide China with a convenient motive to make sure the pandemic which started in Wuhan goes global and cripples any ability by the US to oppose China’s imminent intervention in Hong Kong.

The editorial concludes by claiming that while the Western world appears united, when it is faced with the risk of losing the “Huge Chinese market”, any opposition to Beijing would disappear:

The entire Western world will not follow the US. China is a huge market and the US is unable to provide enough compensation to offset the losses if Western countries become alienated from China. Values still have a strong appeal, but they cannot replace the fundamental interests of a country in pursuit of development. Besides, China has not intervened in the way of life of Western countries. Taking sides based on values at a disproportionate economic cost is not supposed to be the logic of international relations in the 21st century.

The author then writes that “as long as China acts based on facts, resolutely formulates the national security law for Hong Kong, strictly limits the law’s scope to ensure both national security and the city’s stability under the “one country, two systems” principle, while safeguarding the basic rights and interests of the Hong Kong people”, which of course is all just the propaganda strawman that Xi Jinping is using to justify a historic move in Hong Kong, “China will take the initiative in Hong Kong affairs” and “the US stirring of Western public opinion will lead to nothing.”

via ZeroHedge News https://ift.tt/2A5u9K0 Tyler Durden

California Church Asks US Supreme Court To Intervene In Lockdown Battle After Clinton, Obama Judges Strike Down Tyler Durden

Mon, 05/25/2020 – 18:00

A California church and its bishop have asked the US Supreme Court to step in after the 9th Circuit Court of Appeals struck down their emergency application to reopen amid the coronavirus pandemic, in defiance of executive orders issued by Gov. Gavin Newsom.

Lawyers for the South Bay United Pentecostal Church and Biship Arthur Hodges filed with the USSC after the 9th Circuit panel split 2-1, with Judges Barry Silverman and Jacqueline Nguyen – appointed by Clinton and Obama respectively – wrote in their Friday order “We’re dealing here with a highly contagious and often fatal disease for which there presently is no known cure,” adding “In the words of Justice Robert Jackson, if a ‘court does not temper its doctrinaire logic with a little practical wisdom, it will convert the constitutional Bill of Rights into a suicide pact.’”

Apparently a fatality rate below 0.3% counts as ‘often fatal,’ and it would be a ‘suicide pact’ to allow people to worship freely while accepting the well-established risks of contracting COVID-19.

The panel’s third judge, Trump appointee Daniel Collins, weighed in with an 18-page dissent arguing that Gov. Newsom’s orders intrude on religious freedom protected by the First Amendment, according to Politico.

“I do not doubt the importance of the public health objectives that the State puts forth, but the State can accomplish those objectives without resorting to its current inflexible and over-broad ban on religious services,” wrote Collins, who noted that the Governor’s orders allow many workplaces to open, while religious gatherings remain banned even if they can meet social distancing requirements imposed on other permitted activities.

“By explicitly and categorically assigning all in-person ‘religious services’ to a future Phase 3 — without any express regard to the number of attendees, the size of the space, or the safety protocols followed in such services8 — the State’s Reopening Plan undeniably ‘discriminate[s] on its face’ against ‘religious conduct,” Collins continued.

The legal dispute may turn on how much weight the justices choose to give to a 115-year-old Supreme Court precedent, Jacobson v. Massachusetts, which upheld a mandatory vaccination scheme for smallpox.

Lawyers for Newsom have argued that the decision gives states broad powers during a public health emergency and effectively supersedes typical protections for First Amendment activity, including religious practice.

While the 1905 high court ruling remains on the books with no case since where the justices have grappled with similar issues, in his dissent from the Friday 9th Circuit order, Collins sounded skeptical about the sweep of the century-old case.

“Even the most ardent proponent of a broad reading of Jacobson must pause at the astonishing breadth of this assertion of government power over the citizenry, which in terms of its scope, intrusiveness, and duration is without parallel in our constitutional tradition,” he said. –Politico

In other parts of the country, challenges to pandemic lockdowns have been met with mixed results in federal courts. For example, New Orleans’ Fifth Circuit and the Cincinnati Sixth Circuit have granted emergency relief to churches in defiance of state orders, while Chicago’s 7th Circuit joined the San Francisco-based 9tth circuit in declining to intervene.

Hedge Fund CIO: “We Have Reached The Point Where The Entirety Of Future Prosperity Has Been Pulled To The Present” Tyler Durden

Mon, 05/25/2020 – 17:40

By Eric Peters, CIO of One River Asset Management

The Fed presides over the world’s largest economy. Treasury claims otherwise, but the Fed is also guardian of the world’s reserve currency. From this position of power, global central banks were drawn by force of gravity to adopt Fed policies. Over the past decade, global central banks gravitated to the Fed’s policy mix, lowering rates, expanding liquidity, spurring a historic rise in global debt and leverage. Entering 2020, the world had the most homogeneous policy mix since Roman rule. And, as in all things living, lack of diversity reduces resiliency.

Fed policy dominance had complex, unintended consequences, some of which we can observe. For instance, it relieved politicians of the task of governing. Each crisis was easily solved with monetary magic, pulling future demand to the present. This allowed politicians to avoid making tough choices between spending for today versus investing for tomorrow. Without such vital debates, we borrowed from our youth to spend on our ageing. Student debt is one of the many such manifestations. Wildly inflated asset prices are another.

Monetary policy dominance taken to its logical conclusion leads to a world where the entirety of future prosperity has been pulled to the present. At that end point, no matter how many monetary magic wands are waved, the real economy is unresponsive, monetary policy is utterly impotent. As you approach this point, monetary policy gradually losses effectiveness. Somewhere close to the end, politicians are forced to start governing again, making choices. But unlike central bankers who are all the same, each politician is uniquely different, heterogeneous.

As politicians fill the vacuum left by impotent central bankers, they deploy different tools – fiscal, tax, trade, exchange rate, regulatory, immigration and military. They try to coordinate with central bankers, but this produces only illusory benefits because monetary policy once impotent remains so until the system reboots. Today, we are transitioning from a world led by homogeneous central bankers who used a few identical policies in similar ways to one led by heterogeneous politicians who will be using a wide range of policies in wildly different ways.

Global central bank homogeneity produced an era of policy predictability. This encouraged economic actors to leverage balance sheets and business strategies to a stable future. Their actions, like share buybacks and just-in-time manufacturing, were reflexive in that each incremental investment dampened market and economic volatility, reinforcing expectations for a stable future. Naturally, reflexive processes lead to extreme outcomes. Without quite realizing it, economic actors accepted increased systemic fragility in exchange for higher profitability.

Trends unfold when the world changes. Prices adjust as we recognize that the future is likely to look different from the past. Underlying change is often driven by natural cycles. They include cycles in weather, debt, leverage, capital investment, innovation, politics, population, international relations. In late stage, they are sometimes amplified by mass hysteria. Systematic trend-following strategies just finished their worst decade of performance in 120yrs. So did long volatility strategies. It was a decade of homogeneity, policy predictability. It’s over.

via ZeroHedge News https://ift.tt/36woqsE Tyler Durden

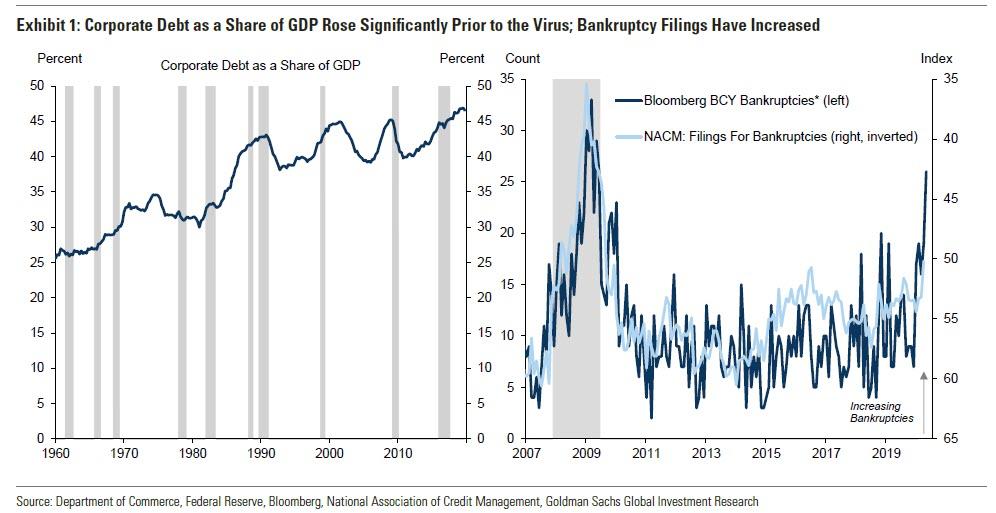

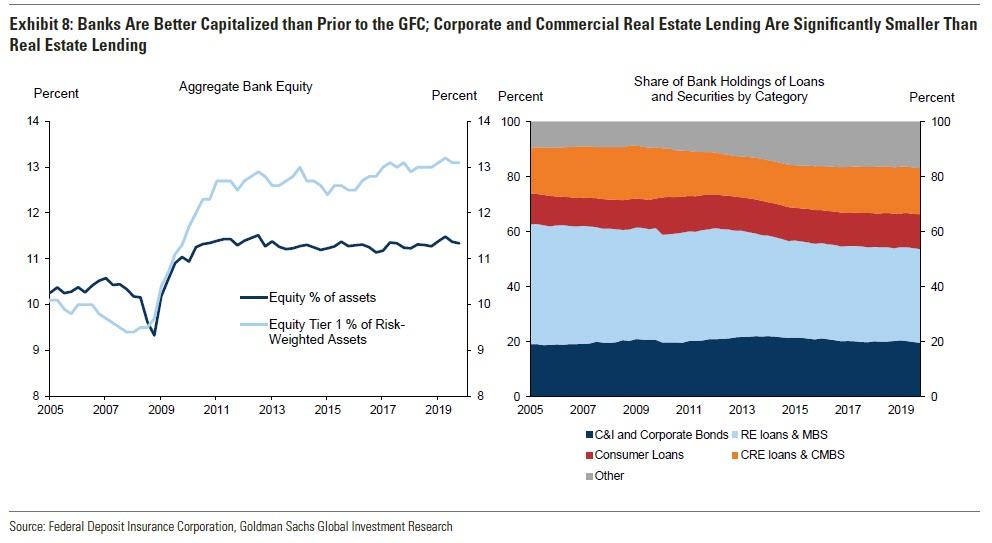

In response, Goldman “assesses the likely scale of economy-wide credit losses, the exposure of creditors to those losses, and the potential risks to financial stability and the banking sector” to conclude that “rising bankruptcies and delinquencies suggest the default cycle has started.”

How did Goldman get to that assessment?

Looking at corporate credit, the bank first looked at corporate debt, noting that nonfinancial corporate debt grew by over 60% since 2011 and recently rose to an all-time high as a share of GDP (Exhibit 1, left), leading to growing concern even prior to the virus that corporate defaults could rise dramatically in the next downturn. Meanwhile, the sharp decline in revenues across many industries has left a large share of companies with negative cash flow, and rising bankruptcy filings and cases suggest the corporate default cycle has started.

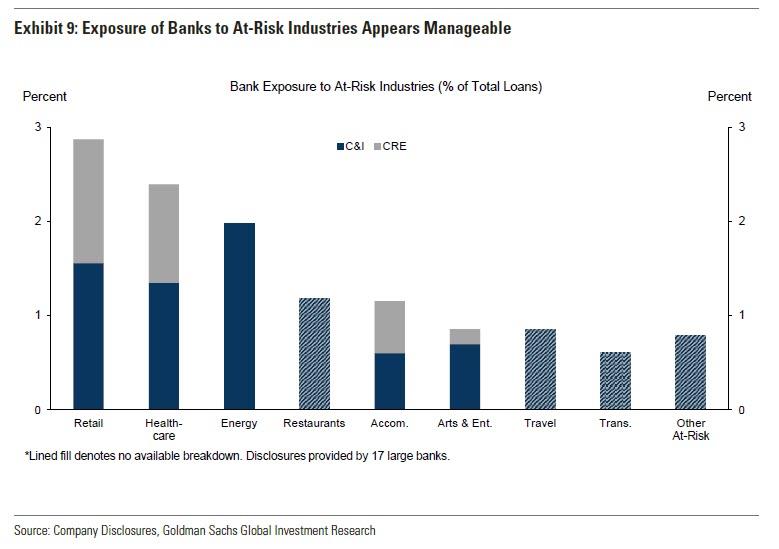

Unlike the financial crisis, the bank finds that a unique feature of this downturn “is the wide variation in industry exposure to the virus, with physical constraints on spending, occupational health risks, and geographical variation in the virus outbreak affecting industries differently.”

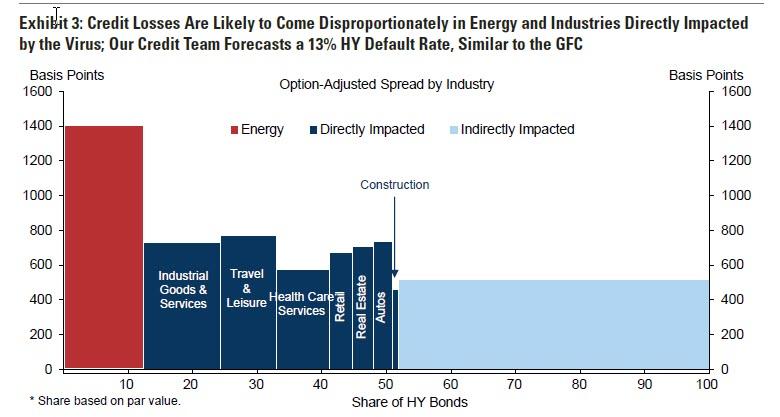

Goldman then performs an analysis of which industries are most impacted by credit losses due to the coronacrisis, and summarizes the findings in the next chart, which shows a coarser breakdown of virus-impacted industries, as well as their market share in the high-yield corporate bond space.

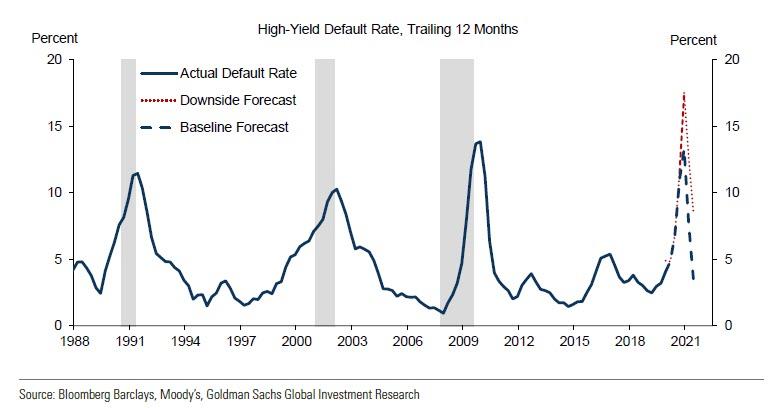

The energy sector stands out both in terms of its size and default risks, given the collapse in oil demand, its disproportionately large footprint in the corporate bond market relative to its GDP share, and the heavy amounts of leverage in the sector. Roughly half of high-yield corporate bonds are in the energy or virus-impacted industries, according to Goldman which adds that its credit strategists “estimate that the 12-month trailing high-yield default rate will increase to 13% by the end of 2020, similar to the peak rate reached during the Global Financial Crisis (Exhibit 3, bottom).”

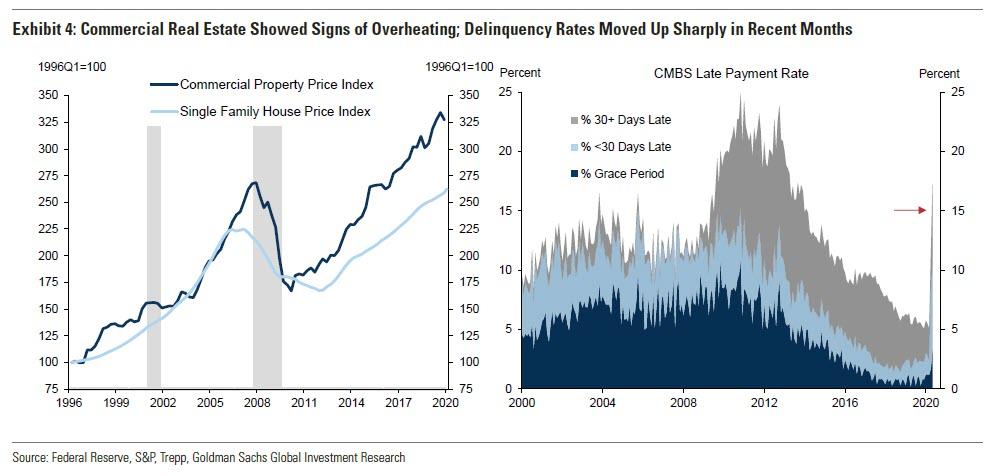

In addition to energy debt, another key area of concern – as we have repeatedly pounded the table in recent weeks – is commercial real estate (CRE), given signs of overheating and overstretched valuations prior to the virus, as well as the unprecedented declines in demand in industries such as lodging, healthcare, and retail.

Commercial real estate prices have outpaced single family house prices since the prior downturn (chart below, left), with CRE capitalization rates falling to historically low levels. Late payments on commercial mortgages have picked up sharply in recent months, suggesting mounting pressures (chart below, right).

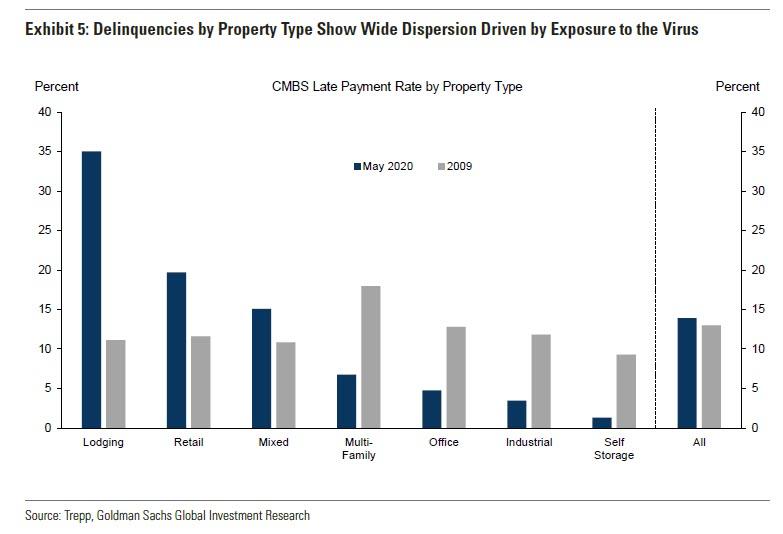

Tangentially, and as also discussed here extensively before, the unique nature of this downturn suggests that “variation in virus exposure will play a large role in determining the breadth and depth of credit losses in commercial real estate.” Delinquencies by property type already show wide dispersion, with virus-exposed property types such as lodging and retail showing much higher delinquency rates than less exposed property types such as self-storage. This contrasts with the prior real estate bust, when delinquencies were roughly evenly distributed across property types.

Overall, Goldman expects a deeper contraction of property incomes than during the financial crisis period, given the heavy stresses to rents and occupancy rates facing many properties, and overall losses on commercial mortgages similar to those observed during the financial crisis.

Meanwhile, even as consumers have been slow to telegraph stress, kept afloat thanks to hundreds of billions in transfer payments, significant downside risks to household debt also remain, particularly if unemployment insurance benefits are not extended, and if higher out-of-pocket medical expenses due to loss of employer-based health insurance push more households to default.

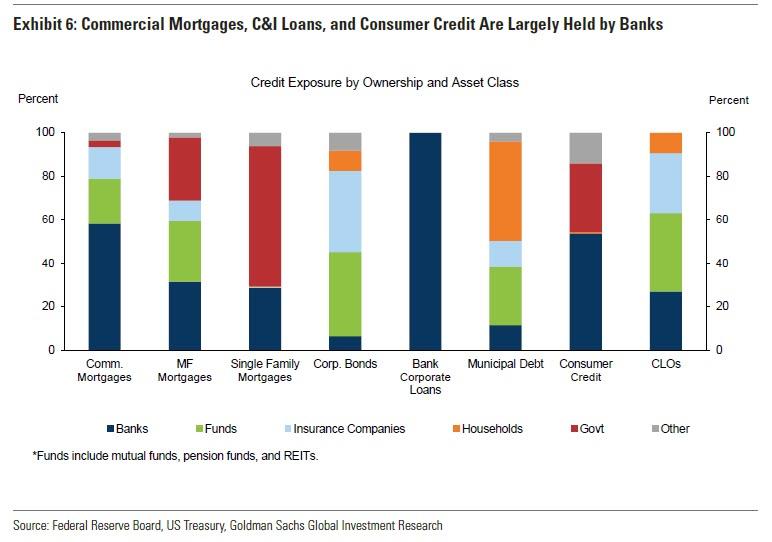

Who Will Bear The Losses

We next look to see where credit losses are most likely to be felt. The Fed’s Financial Accounts suggests that the banking system plays a large role in providing credit for commercial real estate and overall corporate borrowing, two areas of greater concern. Household debt is also largely held by banks, particularly residential mortgages, credit card loans, and auto loans, while student debt is largely held by the federal government.

Municipal debt, another area of concern, is largely held by households, mutual funds and pensions funds, and insurance companies, and thus likely poses a smaller threat to financial stability. Lastly, a growing share of corporate lending—especially in riskier categories, such as leveraged loans—is now done by nonbank financial institutions, including collateralized loan obligations (CLOs), asset managers, hedge funds, and private equity companies, and such lending is not well captured in the Fed’s Financial Accounts. TIC data provides some evidence that non-bank financial institutions and insurance companies own much of US CLO securities, a growing area of concern. Crucially, CLOs do not generally permit early redemptions and are thus less susceptible to runs, which is why Goldman strategists do not see CLOs posing a major risk to financial stability, “despite the likely significant pickup in defaults on leveraged loans.”

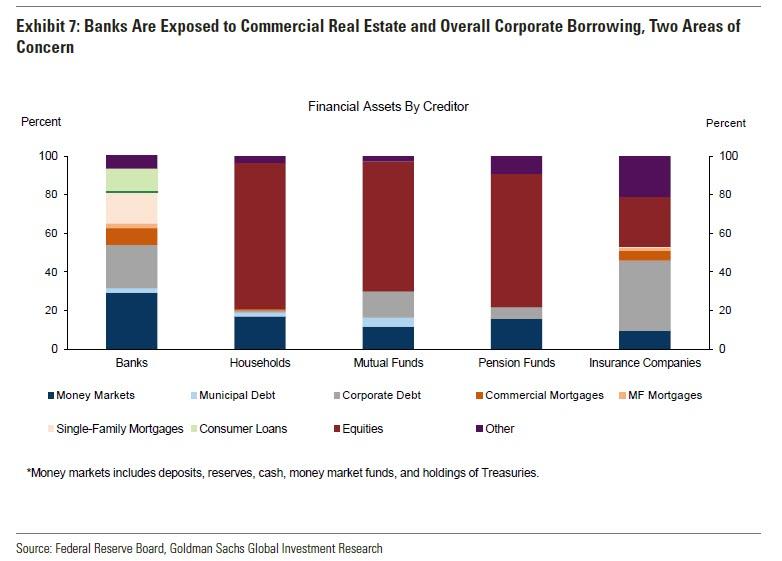

The next chart shows a breakdown of financial asset holdings by creditor, excluding financial institutions such as hedge funds and private equity companies where data is less readily available. Banks are highly exposed to many areas of credit, while households, mutual funds, and pensions are largely more exposed to equities. Insurance companies are somewhere in between, and hold a significant amount of exposure to corporate debt, including CLOs.

The bottom line is simple: contrary to conventional wisdom that banks are now far, far safer than they were during the financial crisis, they bear the broadest exposure to the coming default wave which will soon test just how safe they are.

Risks to the Banking System

As Goldman reminds us, the Fed’s Financial Stability Report warned that financial sector vulnerabilities including for the banking sector, are likely to be significant in the near term, while the April FOMC minutes indicated concern that banks could come under greater stress, particularly if more adverse economic scenarios were realized. The Fed’s Senior Loan Officer Opinion Survey (SLOOS) indicated that lending standards tightened significantly, particularly for commercial and industrial (C&I) and CRE loans, with most banks citing a less favorable or more uncertain economic outlook, as well as a reduced tolerance for risk, as reasons for tightening lending standards. Loan loss provisions across banks have increased significantly in preparation for the rise in defaults and delinquencies.

Curiously, only a modest percentage of banks cited a deterioration in their capital position as playing a role in tightening lending standards in the first quarter. In addition, residential real estate remains the largest category of lending in the banking system by a significant margin. And while Goldman believes that given that this downturn was not precipitated by a housing crisis, losses on this particularly large category will likely be smaller than during the GFC, the question of how quickly consumer cash flows return to normal will be critical in answering just how significant residential losses will be in a few months time.

That said, one clear worry is that certain industries are heavily exposed to the virus, which may lead to larger risks to the banking system if the lending of particular banks, or the banking system as a whole, is highly concentrated in these industries.

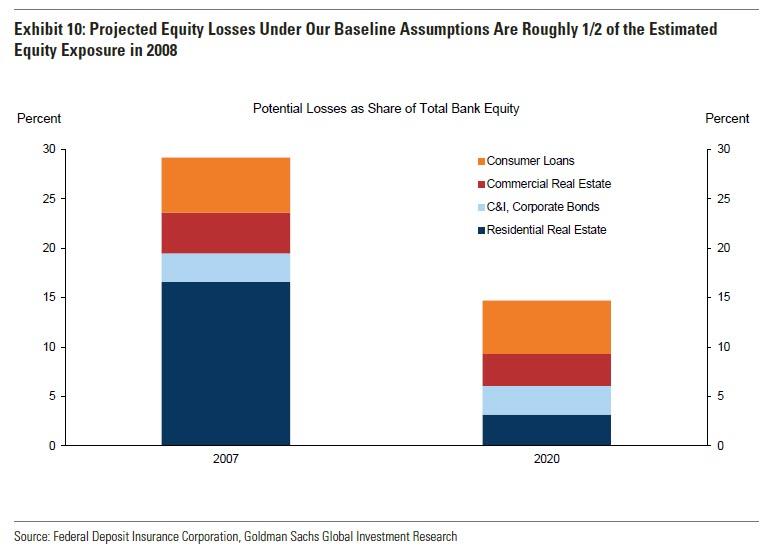

Next, Goldman assesses the vulnerability of bank balance sheets as of 2019 Q4, and estimates the losses on total bank equity from losses across asset categories. The bank assumes similar losses on C&I and CRE lending as in the 2008 crisis, but a smaller hit on residential mortgages and consumer loans (this may be a costly mistake). The bank then calculates the estimated losses as a percent of total bank equity capital, estimating that losses on C&I, CRE, consumer, and residential real estate loans would amount to roughly 15% of total bank equity, compared to around 30% of total bank equity at risk heading into the Global Financial Crisis, using ex-post realized losses across the same categories. Two main reasons account for this difference: first, losses on the large residential real estate category are likely to be smaller, and second, bank equity levels are higher today than before the crisis. Once again, these optimistic assumptions may end up having to be substantially revised higher.

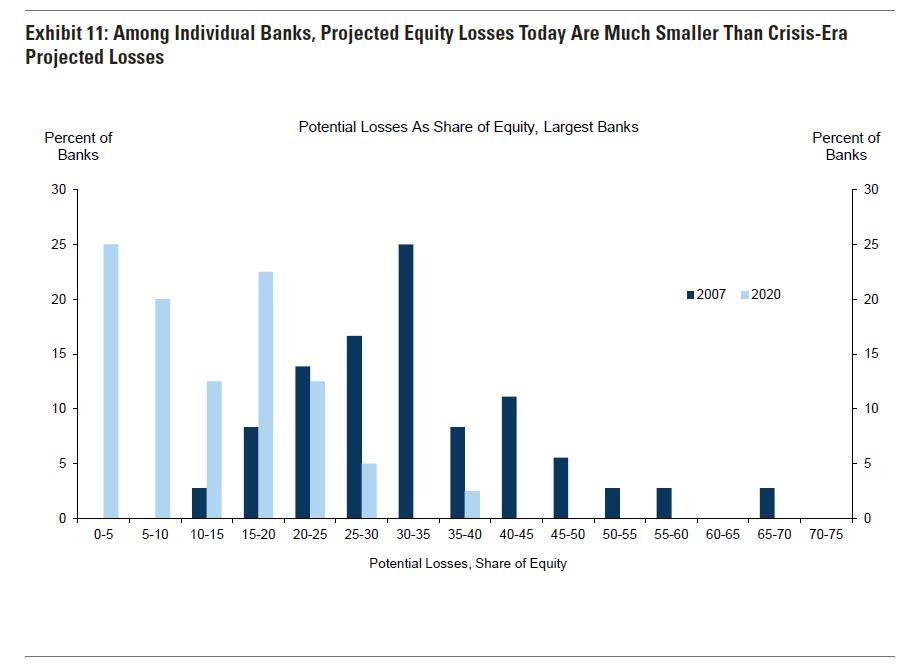

Finally, the bank looks at lending exposure of the largest banks individually: bank-level data can reveal differences across banks and highlight whether there are a significant number of banks with large exposures to at-risk categories. Naturally, using the optimistic assumptions profiled above, Goldman finds that while there is dispersion among the largest banks in their exposure to losses, almost all of the largest banks today are less vulnerable than the median large bank was prior to the financial crisis, thus invalidating the entire analysis for the simple reason that the current crisis may end up being far more dire to bank loans than 2008/2009 if an economic recovery isnt forthcoming in short notice.

In summary, Goldman finds that while financial stability concerns appear manageable, significant downside risks remain. A slower than expected recovery and a prolonged downturn would likely stress the banking system further, and a growing share of riskier lending is now done by less regulated nonbank financial institutions, where risks are harder to assess. Its conclusion: “Should a more adverse scenario arise, Fed officials have indicated the willingness to further help facilitate the provision of credit by the financial system.”

In other words, if the coming default crisis ends up being as bad as the GFC, the Fed will end up owning a whole lot more bankrupt bonds and loans than just Hertz.

via ZeroHedge News https://ift.tt/3ejlPFs Tyler Durden

The Bank of Japan Was The Biggest Buyer Of Japanese Corporate Bonds In April Tyler Durden

Mon, 05/25/2020 – 17:00

Our observation that as of this moment the Fed owns, via the HYG and JNK ETFs, bonds of bankrupt rental company Hertz sparked inexplicable outrage in the bullish camp. We find this confusing: how is the Fed owning bonds either a bullish or bearish case? It merely confirms that capitalism is now dead, that we have centrally-planned, “fake markets” as Bank of America put it, and which as Deutsche Bank further clarified, “these are administered markets and market outcomes will be dictated by the policy goals of the Fed and Treasury, and the tools they select to implement policy.”

That bulls are taking this fact as an affront, simply shows just how vested they too are in perpetuating a myth that markets still exist (as if it is somehow the imploding economy and not the Fed’s $4 trillion in liquidity injections since March that has boosted the stock market) while pretending they have some idea of what happens next based on “fundamentals” or “data” when in reality the only thing that matters is how much liquidity the Fed injects on any given day, making strategists, analysts and “paywalled pundits” irrelevant (an outcome which is devastating to their financial health).

In any case, shortly after our article, the Fed apologists scrambled to write articles such as this one whose sole counterarguments are outright obtuse: the amount of bankrupt bonds held by the Fed is so small so please don’t worry, and in any event, the ETFs will likely sell them.

First of all, anyone who claims to “know” what the ETFs will do with the defaulted bonds likely has a barrel of snake oil they need offloaded with immediate delivery, and their motives should be closely scrutinized from now on. As we explicitly said in our article, it is most certainly the case that the Fed will seek to offload its exposure – similar to what the ECB did when it ended up holding bonds of bankrupt Steinhoff but not before sparking a major scandal in financial cricles – after all the last thing Powell needs is another Congressional hearing inquiring how the Fed buying junk bonds – and junk bonds from massively levered, defaulted zombie corporations at that – is helping US workers. If anything, this merely cements our core argument that the process of rushing to buy corporate bonds was a panicked scramble meant to preserve confidence in a bursting asset bubble, one that was rushed from the beginning without almost any thought as to the consequences.

And since said “paywalled pundits” appears to have missed what we said, we will repeat it: the way the Fed’s purchases of corporate bonds are structured, especially as the US nears a default tsunami, it is only a matter of time before Powell ends up holding dozens if not hundreds of defaulted CUSIPs both directly and via ETFs. Will Powell then quietly dump all of them to pretend the Fed never intended to lose the Treasury’s funds by propping up insolvent companies? He will of course try. But if he fails, and if the ETFs do not offload their exposure to defaults, the Fed will most certainly be part of the bankruptcy process, courtesy of the debt-to-equity conversion of the underlying securities.

We also eagerly look to find just which independent, third-party entity buys the defaulted Hertz bonds held by HYG and JNK on behalf of the Fed to absolve Powell of his dismal decisionmaking.

The truth is that nobody knows what happens next, now that the Fed is an active intermediary in capital markets and is purchasing highly risky paper that defaulted just days after the Fed started buying ETFs. Anyone who claims otherwise is a complete hack.

As for that other “counterargument”, that “neither the Fed nor the Treasury has significant exposure to HTZ“, well- yes of course – the program has been in operation for just over a week: it better not have significant exposure to Hertz. What about in 3 months, or 6 months or one year from now when dozens of the companies that make up the JNK and HYG ETFs also file Chapter 11? Or what about the “fallen angel” companies that sell bonds directly to the Fed and end up having to file themselves. Will it be significant then?

Here is the answer: now that the Fed has gone the path of the BOJ and is directly intervening in capital markets, if not yet buying stocks (we can’t wait for the same bulls to explain how the Fed buying the SPY is great news for everyone), we can look to the Bank of Japan for examples of just how “insigificant” its exposure to the corporate bond market is.

WEll, according to SMBC Nikko Securities analyst Riyon Matsuyama, the Bank of Japan was the biggest buyer of Japanese corporate bonds in April compared with other categories for the first time since June last year, as Bloomberg reported overnight.

That sounds pretty significant to us: when the central bank is not only the buyer of last resort, but buyer of biggest resort, that would suggest that something is very, very wrong. It also suggests that there are virtually no other buyers (although we are confident the abovementioned bulls can “explain” how this too is “not one of the things to worry about”). In any case, it would also suggest that the BOJ owns a lot of corporate bonds.

And the Fed is hot on the BOJ’s footsteps.

According to Matusyuama – who calculated using data released by the Japan Securities Dealers Association this week and BOJ – the BOJ’s purchases as a proportion of all notes transacted in April rose to 30%, the highest level since June 2018.

This surge in holdings should not come as s surprise: after all, at the end of April, the BOJ decided to double its purchases of corporate bonds and sure enough, that’s what it is doing even if it means not only crowding out all other market players, but in the process destroying what little was left of price discovery. Why? Because the BOJ buys corporate bonds with money it creates out of thin air, and with no regard for fundamentals, resulting in a complete disconnect between fundamentals and asset prices.

Maybe this is why the abovementioned “paywalled pundits” are so angry: the fact that they are now relegated to merely frontrunning central bank purchases (something which even Blackrock embraced, admitting that’s the only way to make money now adding that it “will follow the Fed and other DM central banks by purchasing what they’re purchasing, and assets that rhyme with those”) means that any of their so-called insights are nothing more than Fed cheerleading garbage. Which is fine – after all that’s the centrally-planned world we live in, but just own up to it and stop pretending to have some deep, premium-pricing insight (which costs $29.95 per month) about the US or global economy which translates into an outlook on prices, investing, the universe and everything.

via ZeroHedge News https://ift.tt/2TChIMu Tyler Durden

Money printing by the Fed and Congress is off the charts. The Federal Reserve doubled its balance sheet in a matter of months, and Congress is pumping out trillions of dollars in spending bills to fight the economic crisis caused by the Covid 19 lockdown. The really scary thing is not the massive money printing, but the fact that absolutely nobody seems to care about the risk to the U.S. dollar.

Money manager Peter Schiff thinks he knows why, and explains:

“(Back in 2008-2009,) even Larry Kudlow was worried about what the Fed was doing, but nobody is worried about it now. The reason is they have been lulled into this false sense of complacency in that we got away with it the last time… and there was no negative consequence.

We didn’t have runaway inflation and did not have loss of confidence in the dollar. So, there was no price to be paid…

Since we got away with it before, they think they will get away with it again, and I think they are completely wrong…

All we did was inflate a bigger bubble, but now this bubble has popped, and it found the mother of all pins in the Coronavirus that put a gaping hole in it, so the air is coming out much faster. Now, they are trying to reflate this thing. We are going to suffer the consequences, not only what we are doing now, but what we did back then…

When is all this inflation going to move out of the stock market and into the supermarket? I am surprised this has not already happened, but I do think we are at the end of the line… Here’s what is going on. We are going to have this massive inflation tax. We are seeing price increases at the supermarkets.”

What has to break is the U.S. dollar, and that’s coming, according to Schiff, “We are going to overwhelm with dollar supply…”

“We are printing all this money. The Fed is buying all these bonds. . . . This is it. The Fed is going all in on QE. There is no limit. They are printing all this money, and, so, ultimately, the dollar is going to tank. It hasn’t happened yet, but it will. That’s when the party really ends. That’s when there is massive pressure on consumer prices. That’s when there is massive (upward) pressure on interest rates. . . . This could be an inflationary depression. We could have hyper-inflation. We didn’t have anything like that in the Great Depression. During the 1930’s, prices went down, and people got some relief with lower prices. That made the downturn not as bad. Imagine high unemployment with the cost of living skyrocketing. That’s what we are heading for. It’s going to be the 1970’s only on steroids because it’s going to be a much deeper economic contraction with a much bigger increase in consumer prices.”

Schiff says, “When we reopen, nothing will be the same because we will not be able to reflate this bubble.”

So what do you do? Precious metals are a no-brainer investment. Schiff says,

“It’s not that gold is gaining in value, it’s that fiat currencies are all losing value. Gold is the one stable factor. It’s the one thing governments can’t create out of thin air. Every currency in the world, except the dollar, are hitting new record lows against gold. You need more Euros, Rands or Aussie dollars to buy an ounce of gold. . . . The U.S. dollar is losing value more slowly, but this is going to change. We are going to win the race to the bottom…

People need to convert their dollars now into gold or silver. If you think the price of gold is going up now, wait til the dollar is the weakest of the currencies. . . . That’s going to accelerate the appreciation of gold . . . and that’s going to put gold in the spotlight as the replacement to the U.S. dollar as the main reserve asset for global central banks.”

Join Greg Hunter of USAWatchdog.com as he goes One-on-One with money manager and economic expert Peter Schiff, founder of Euro Pacific Capital and Schiff Gold.