This week, American astronauts returned to earth. Their trip to the space station was the first manned launch from the U.S. in 10 years.

By NASA? No. Of course, not.

This space flight happened because government was not in charge.

An Obama administration committee had concluded that launching such a vehicle would take 12 years and cost $36 billion.

But this rocket was finished in half that time—for less than $1 billion (1/36th the predicted cost).

That’s because it was built by Elon Musk’s private company, Space X. He does things faster and cheaper because he spends his own money.

“This is the potential of free enterprise!” explains aerospace engineer Robert Zubrin in my newest video.

Of course, years ago, NASA did manage to send astronauts to the moon.

That succeeded, says Zubrin, “because it was purpose-driven. (America) wanted to astonish the world what free people could do.”

But in the 50 years since then, as transportation improved and computers got smaller and cheaper, NASA made little progress.

Fortunately, President Obama gave private companies permission to compete in space, saying, “We can’t keep doing the same old things as before.”

Competition then cut the cost of space travel to a fraction of what it was.

Why couldn’t NASA have done that?

Because after the moon landing, it became a typical government agency—overbudget and behind schedule. Zubrin says NASA’s purpose seemed to be to “supply money to various suppliers.”

Suppliers were happy to go along.

Zubrin once worked at Lockheed Martin, where he once discovered a way for a rocket to carry twice as much weight. “We went to management, the engineers, and said, ‘Look, we could double the payload capability for 10 percent extra cost.’ They said, ‘Look, if the Air Force wants us to improve the Titan, they’ll pay us to do it!'”

NASA was paying contractor’s development costs and then adding 10 percent profit. The more things cost, the bigger the contractor’s profit. So contractors had little incentive to innovate.

Even NASA now admits this is a problem. During its 2020 budget request, Administrator Jim Bridenstine confessed, “We have not been good at maintaining schedule and…at maintaining costs.”

Nor is NASA good at innovating. Their technology was so out of date, says Zubrin, that “astronauts brought their laptops with them into space—because shuttle computers were obsolete.”

I asked, “When (NASA) saw that the astronauts brought their own computers, why didn’t they upgrade?”

“Because they had an entire philosophy that various components had to be space rated,” he explains. “Space rating was very bureaucratic and costly.”

NASA was OK with high costs as long as spaceships were assembled in many congressmen’s districts.

“NASA is a very large job program,” says Aerospace lawyer James Dunstan. “By spreading its centers across the country, NASA gets more support from more different congressmen.”

Congressmen even laugh about it. Rep. Randy Weber (R–Texas) joked, “We’ll welcome (NASA) back to Texas to spend lots of money any time.”

Private companies do more with less money. One of Musk’s cost-saving innovations is reusable rocket boosters.

For years, NASA dropped its boosters into the ocean.

“Why would they throw it away?” I ask Dunstan.

“Because that’s the way it’s always been done!” he replies.

Twenty years ago, at Lockheed Martin, Zubrin had proposed reusable boosters. His bosses told him: “Cute idea. But if we sell one of these, we’re out of business.”

Zubrin explains, “They wanted to keep the cost of space launch high.”

Thankfully, now that self-interested entrepreneurs compete, space travel will get cheaper. Musk can’t waste a dollar. Space X must compete with Jeff Bezos’ Blue Origin, Richard Branson’s Virgin Galactic, Boeing, Lockheed Martin, and others.

The private sector always comes up with ways to do things that politicians cannot imagine.

Government didn’t invent affordable cars, airplanes, iPhones, etc. It took competing entrepreneurs, pursuing profit, to nurture them into the good things we have now.

Get rid of government monopolies.

For-profit competition brings us the best things in life.

COPYRIGHT 2020 BY JFS PRODUCTIONS INC. DISTRIBUTED BY CREATORS.COM

from Latest – Reason.com https://ift.tt/3g4cBy1

via IFTTT

Yesterday, the Trump Administration commenced its third effort to wind down DACA. DACA Rescission 1.0 began in 2017. Attorney General Sessions wrote a letter to Acting DHS Secretary Duke. Sessions concluded that DACA was unlawful. And Duke, bound by that determination, issued a memorandum to rescind DACA on the sole ground that it was unlawful. She did not rely on any policy rationales. The district courts quickly enjoined the 2017 Duke Memorandum. Judge Bates (DDC) gave the administration another shot to rescind DACA. In 2018, DHS Secretary Nielsen issued a new memorandum. Call this document DACA Rescission 2.0. On appeal, the Supreme Court found that the 2017 Duke Memorandum was arbitrary and capricious. The majority declined to consider the 2018 Nielsen memorandum. (Justice Kavanaugh would have considered it). The Supreme Court’s decision affirmed the lower-court rulings, thus lifting the stays. As a result, the 2017 Duke Memorandum was now fully enjoined by several courts. The original 2012 DHS Secretary Napolitano Memorandum remained in full force.

On July 28, 2020, Acting DHS Secretary Wolf official withdrew the 2017 Duke Memorandum and the 2018 Nielsen Memorandum. By doing so, he has now mooted all the challenges to the 2017 Duke Memorandum and the 2018 Nielsen Memorandum. The district courts that entered the injunctions against those two documents no longer have a live case or controversy. Instead, we are left with the original 2012 Napolitano Memorandum. That document created DACA. And there are no court orders requiring DHS to implement the 2012 Memorandum in any fashion. Recall, all the challenges concerned the 2017 Duke Memorandum and the 2018 Nielsen Memorandum. Therefore, there is no injunction requiring DHS to grant new DACA authorizations.

For the foreseeable future (probably till November), Secretary Wolf has announced that DHS will “reject all pending and initial requests for DACA.” Doing so does not violate any court order. Again, there is no court order requiring DHS to grant DACA requests pursuant to the 2012 Napolitano Memorandum. The court orders only enjoined the 2017 Duke and 2018 Nielsen Memorandum. Here, the scope of the judgment becomes very important. A future court could order DHS to follow the terms of the 2012 Napolitano Memorandum. But that order has not yet been issued. As of today, DHS is in full compliance with all relevant court orders. (Press reports that the Trump administration has ignored the courts are simply wrong.)

But wait, there’s more. Attorney General Barr sent Secretary Wolf a letter on June 30–twelve days after Regents was decided. Barr withdrew the 2017 Sessions letter. He also withdrew the 2014 Obama Administration’s opinion that expressly authorized DAPA, and in a footnote, suggested DACA was lawful. (As of this evening, the opinion is still listed on OLC’s site.) This withdrawal is huge. OLC does not often yank opinions. I’m glad Barr finally took this step. DOJ was arguing out of both sides of its mouth in court about DACA’s legality, and was constrained by this opinion. Barr took these actions “to wipe the slate clean to make clear beyond doubt that you [Wolf] are free to exercise your own independent judgment in considering the full range of legal and policy issues implicated by a potential rescission or modification of DACA, as contemplated by the Supreme Court.”

In short, the Trump Administration has completely mooted the pending challenges to the DACA rescission. This challenge will need to start on a blank slate. For sure, the plaintiffs will argue that this new front is merely pretextual. But we will need new amended complaints, and a fresh round of litigation.

Now, what happens in November? If President Trump wins re-election, then Secretary Wolf will likely make his interim policy permanent. People who have DACA can continue to renew it, but new applications will not be granted. And that policy will be litigated up to the Supreme Court. I think Trump wins for reasons I’ll discuss below.

But what if Biden wins. Then his DHS Secretary will try to rescind the Wolf memorandum. But to do so, the Secretary would have to consider an infinitely-wide range of options under the Chief’s opinion. The failure to dot every “i” and cross every “t” could result in an arbitrary and capricious finding several years down the road. Who knows?

I think this policy is a manifestation of the John Yoo strategy. I was skeptical of this general strategy in Politifact. But I didn’t realize how it would be implemented. I simply assumed that a district court would enjoin whatever Trump does. I don’t think a district court can order the Trump Administration to exercise its prosecutorial discretion with respect to granting new DACA authorizations. The Supreme Court explained this was a substantive policy, subject to prosecutorial discretion. And there is no legal entitlement to DACA.

You see, rather than rescinding DACA, this new approach merely leaves the current memorandum in place, but declines to exercise discretion for the time being. For sure, a lower court somewhere will find this decision arbitrary and capricious. But I think the Chief Justice votes to stay those rulings. Why? Jon Adler explained well, Roberts likes to maintain the status quo.

Now what is the status quo? You may think the status quo is granting DACA applications. After all, DACA applications have been granted for nearly eight years. Well, not exactly. The status quo is that those grants were issued pursuant to discretion; not based on a court order. And now DHS is declining to exercise that discretion. The status quo, from the perspective of the 2012 memorandum, is maintained. The Wolf memorandum states this point expressly:

Consistent with the Court’s express remand for the agency’s reconsideration and the Napolitano Memorandum’s clear statement that it conferred no substantive rights, DHS did not expand beyond the status quo of the past several years for a few weeks while it was determining next steps. I now conclude that all pending and future requests should be treated in the same manner, rather than be subject to differential treatment depending on the fortuity of when DHS received the request within a short period of uncertainty. Nothing in the Napolitano Memo purports to preclude me from exercising my enforcement discretion to make these changes on an interim basis while I consider whether to make more substantial changes on a permanent basis. Even under the Napolitano Memo, no aliens had a legal entitlement to receive DACA—much less a legal entitlement to a particular renewal period. Nor can aliens with pending requests assert any meaningfully greater reliance interests in their initial or continued enjoyment of the policy and the attendant benefits than aliens who submit such requests after the issuance of this memorandum.

This paragraph can be copy-and-pasted in a stay application addressed to John G. Roberts. And I suspect it will be granted. The Trump Administration accurately understood, and desribed the status quo.

And once the Supreme Court stays the lower-court rulings, allowing this memorandum to remain in place, a Biden Administration would have to litigate for nearly two years to get out from under it. And if the Biden administration tries to grant new DACA authorizations, it will be acting in an arbitrary and capricious fashion, for failing to properly rescind the Wolf Memo. Cue an injunction from the Fifth Circuit. For years, Trump was stuck with Obama’s policies. Now, Biden would be stuck with Trump’s policies. What’s sauce for the goose is sauce for the gander.

DACA Rescission 1.0 and 2.0 were bungled, badly. Version 3.0 may actually stick for a few years until the Supreme Court decides the case. And even then, the Chief may send Biden back to square one. I have to admit, this approach is very clever, and takes the Chief on his own terms.

from Latest – Reason.com https://ift.tt/3gmuOqV

via IFTTT

Last Saturday in Louisville, Kentucky, about 300 armed members of the NFAC (Not Fucking Around Coalition), a self-described “black militia” based in Atlanta, had what the Louisville Courier-Journalcalled “a tense standoff” with about 50 armed Three Percenters, which the paper described as a “far-right…militia.” While the incident, which ended without violence, could be seen as yet another sign that the country is descending into 1968-style chaos, it was also a striking illustration of the Second Amendment’s enduring practical and symbolic importance that scrambled conventional stereotypes about the right to armed self-defense.

Since Kentucky allows open (or concealed) carrying of firearms without a permit, the two groups, both of which disavow aggression, were acting lawfully. And while their motives may look different, both are drawing on a long American tradition of wide gun ownership as a safeguard against tyranny.

NFAC members came to Louisville in support of protests provoked by the shooting of Breonna Taylor, an unarmed 26-year-old African-American woman who was killed by white police officers during a fruitless drug raid on March 13. The circumstances of Taylor’s death gave the guns carried by those militia members added significance.

Plainclothes police officers broke into Taylor’s apartment in the middle of the night based on meager evidence that a detective used to obtain a no-knock search warrant. Mistaking the armed invaders for robbers, Taylor’s boyfriend, Kenneth Walker, grabbed a gun and fired a single shot that struck one officer in the leg.

The cops responded with a hail of bullets, at least eight of which struck Taylor and several of which entered a neighboring apartment. Prosecutors initially charged Walker with attempted murder of a police officer but dropped that charge in May.

As Rep. Tom McClintock (R–Calif.) observed last month, “the invasion of a person’s home is one of the most terrifying powers government possesses,” and “every person in a free society has the right to take arms against an intruder in their homes.” While McClintock was emphasizing the dangers posed by no-knock warrants, his comments also raised the question of how Americans, no matter their skin color, can defend themselves against police officers who behave like criminals.

NFAC has one answer. By parading with military-style rifles of the sort that Joe Biden, the presumptive Democratic presidential nominee, wants to ban, the militia’s members show they are prepared to exercise the Second Amendment rights that gun control supporters typically portray as a fetish of white conservatives.

The assertion of those rights resonates historically, since modern gun control laws have their roots in the efforts of Southern states to disarm freedmen, depriving them of a constitutional right that Chief Justice Roger Taney, author of the Supreme Court’s infamous 1857 decision in Dred Scott v. Sandford, warned black people would enjoy if they were recognized as citizens. Under Jim Crow and during the civil rights movement, the right to armed self-defense was vitally important to African Americans resisting government-imposed white supremacy.

The Three Percenters, by contrast, were responding to NFAC’s presence in Louisville, aiming to “aid police” (as the Courier-Journal put it) in maintaining order. Yet the group, which rejects the “militia” label and disavows racism, also describes itself as defending civil liberties and resisting the illegitimate exercise of government power.

You need not endorse the tactics or ideologies of these organizations to recognize that both are relying on a legal legacy that makes mainstream Democrats like Biden uncomfortable. As the Supreme Court recognized in its landmark 2008 decision overturning the District of Columbia’s handgun ban, the Second Amendment was based partly on the premise that “when the able-bodied men of a nation are trained in arms and organized, they are better able to resist tyranny.”

The fact that two opposing groups are dedicated to defending the right of armed self-defense should not be surprising. The Second Amendment, like the First, is of value to people with divergent backgrounds and political views. Gun controllers should stop pretending otherwise.

This week, American astronauts returned to earth. Their trip to the space station was the first manned launch from the U.S. in 10 years.

By NASA? No. Of course, not.

This space flight happened because government was not in charge.

An Obama administration committee had concluded that launching such a vehicle would take 12 years and cost $36 billion.

But this rocket was finished in half that time—for less than $1 billion (1/36th the predicted cost).

That’s because it was built by Elon Musk’s private company, Space X. He does things faster and cheaper because he spends his own money.

“This is the potential of free enterprise!” explains aerospace engineer Robert Zubrin in my newest video.

Of course, years ago, NASA did manage to send astronauts to the moon.

That succeeded, says Zubrin, “because it was purpose-driven. (America) wanted to astonish the world what free people could do.”

But in the 50 years since then, as transportation improved and computers got smaller and cheaper, NASA made little progress.

Fortunately, President Obama gave private companies permission to compete in space, saying, “We can’t keep doing the same old things as before.”

Competition then cut the cost of space travel to a fraction of what it was.

Why couldn’t NASA have done that?

Because after the moon landing, it became a typical government agency—overbudget and behind schedule. Zubrin says NASA’s purpose seemed to be to “supply money to various suppliers.”

Suppliers were happy to go along.

Zubrin once worked at Lockheed Martin, where he once discovered a way for a rocket to carry twice as much weight. “We went to management, the engineers, and said, ‘Look, we could double the payload capability for 10 percent extra cost.’ They said, ‘Look, if the Air Force wants us to improve the Titan, they’ll pay us to do it!'”

NASA was paying contractor’s development costs and then adding 10 percent profit. The more things cost, the bigger the contractor’s profit. So contractors had little incentive to innovate.

Even NASA now admits this is a problem. During its 2020 budget request, Administrator Jim Bridenstine confessed, “We have not been good at maintaining schedule and…at maintaining costs.”

Nor is NASA good at innovating. Their technology was so out of date, says Zubrin, that “astronauts brought their laptops with them into space—because shuttle computers were obsolete.”

I asked, “When (NASA) saw that the astronauts brought their own computers, why didn’t they upgrade?”

“Because they had an entire philosophy that various components had to be space rated,” he explains. “Space rating was very bureaucratic and costly.”

NASA was OK with high costs as long as spaceships were assembled in many congressmen’s districts.

“NASA is a very large job program,” says Aerospace lawyer James Dunstan. “By spreading its centers across the country, NASA gets more support from more different congressmen.”

Congressmen even laugh about it. Rep. Randy Weber (R–Texas) joked, “We’ll welcome (NASA) back to Texas to spend lots of money any time.”

Private companies do more with less money. One of Musk’s cost-saving innovations is reusable rocket boosters.

For years, NASA dropped its boosters into the ocean.

“Why would they throw it away?” I ask Dunstan.

“Because that’s the way it’s always been done!” he replies.

Twenty years ago, at Lockheed Martin, Zubrin had proposed reusable boosters. His bosses told him: “Cute idea. But if we sell one of these, we’re out of business.”

Zubrin explains, “They wanted to keep the cost of space launch high.”

Thankfully, now that self-interested entrepreneurs compete, space travel will get cheaper. Musk can’t waste a dollar. Space X must compete with Jeff Bezos’ Blue Origin, Richard Branson’s Virgin Galactic, Boeing, Lockheed Martin, and others.

The private sector always comes up with ways to do things that politicians cannot imagine.

Government didn’t invent affordable cars, airplanes, iPhones, etc. It took competing entrepreneurs, pursuing profit, to nurture them into the good things we have now.

Get rid of government monopolies.

For-profit competition brings us the best things in life.

COPYRIGHT 2020 BY JFS PRODUCTIONS INC. DISTRIBUTED BY CREATORS.COM

from Latest – Reason.com https://ift.tt/3g4cBy1

via IFTTT

Last Saturday in Louisville, Kentucky, about 300 armed members of the NFAC (Not Fucking Around Coalition), a self-described “black militia” based in Atlanta, had what the Louisville Courier-Journalcalled “a tense standoff” with about 50 armed Three Percenters, which the paper described as a “far-right…militia.” While the incident, which ended without violence, could be seen as yet another sign that the country is descending into 1968-style chaos, it was also a striking illustration of the Second Amendment’s enduring practical and symbolic importance that scrambled conventional stereotypes about the right to armed self-defense.

Since Kentucky allows open (or concealed) carrying of firearms without a permit, the two groups, both of which disavow aggression, were acting lawfully. And while their motives may look different, both are drawing on a long American tradition of wide gun ownership as a safeguard against tyranny.

NFAC members came to Louisville in support of protests provoked by the shooting of Breonna Taylor, an unarmed 26-year-old African-American woman who was killed by white police officers during a fruitless drug raid on March 13. The circumstances of Taylor’s death gave the guns carried by those militia members added significance.

Plainclothes police officers broke into Taylor’s apartment in the middle of the night based on meager evidence that a detective used to obtain a no-knock search warrant. Mistaking the armed invaders for robbers, Taylor’s boyfriend, Kenneth Walker, grabbed a gun and fired a single shot that struck one officer in the leg.

The cops responded with a hail of bullets, at least eight of which struck Taylor and several of which entered a neighboring apartment. Prosecutors initially charged Walker with attempted murder of a police officer but dropped that charge in May.

As Rep. Tom McClintock (R–Calif.) observed last month, “the invasion of a person’s home is one of the most terrifying powers government possesses,” and “every person in a free society has the right to take arms against an intruder in their homes.” While McClintock was emphasizing the dangers posed by no-knock warrants, his comments also raised the question of how Americans, no matter their skin color, can defend themselves against police officers who behave like criminals.

NFAC has one answer. By parading with military-style rifles of the sort that Joe Biden, the presumptive Democratic presidential nominee, wants to ban, the militia’s members show they are prepared to exercise the Second Amendment rights that gun control supporters typically portray as a fetish of white conservatives.

The assertion of those rights resonates historically, since modern gun control laws have their roots in the efforts of Southern states to disarm freedmen, depriving them of a constitutional right that Chief Justice Roger Taney, author of the Supreme Court’s infamous 1857 decision in Dred Scott v. Sandford, warned black people would enjoy if they were recognized as citizens. Under Jim Crow and during the civil rights movement, the right to armed self-defense was vitally important to African Americans resisting government-imposed white supremacy.

The Three Percenters, by contrast, were responding to NFAC’s presence in Louisville, aiming to “aid police” (as the Courier-Journal put it) in maintaining order. Yet the group, which rejects the “militia” label and disavows racism, also describes itself as defending civil liberties and resisting the illegitimate exercise of government power.

You need not endorse the tactics or ideologies of these organizations to recognize that both are relying on a legal legacy that makes mainstream Democrats like Biden uncomfortable. As the Supreme Court recognized in its landmark 2008 decision overturning the District of Columbia’s handgun ban, the Second Amendment was based partly on the premise that “when the able-bodied men of a nation are trained in arms and organized, they are better able to resist tyranny.”

The fact that two opposing groups are dedicated to defending the right of armed self-defense should not be surprising. The Second Amendment, like the First, is of value to people with divergent backgrounds and political views. Gun controllers should stop pretending otherwise.

FOMC Preview: The Fed Must Find Ways To “Out Dove” Market Expectations Tyler Durden

Tue, 07/28/2020 – 23:18

While nobody expects any fireworks from the Fed tomorrow or any major market-moving announcement, the FOMC meeting will likely involve a debate over the toolkit with a discussion of how to pivot from “stabilization” to “accommodation” policies according to BofA strategists, who notes that while there likely is an agreement that the next steps should accomplish the goal of “enhancing forward guidance,” they do not think Fed officials have settled on the strategy.

Amid growing fears of covid chaos and renewed economic shutdowns, Powell will likely be grilled on, and will discuss some of the Fed’s options while the minutes released in three weeks will provide more clarity. That said, the statement is likely to provide little new insight, with only a few edits to the current conditions paragraph to highlight improvement thus far, but also express caution over recent signs of slowing in some of the high-frequency indicators.

More importantly, the rates and FX markets expect no new policy action to be taken at the July FOMC meeting, which should lead to a muted reaction across markets (it also sets up markets for a surprise). Instead, according to BofA, market participants will be much more focused on the guidance and “stage setting” that Chair Powell provides on what the next easing steps might look like. On net, a discussion of additional easing measures in the Powell press conference – such as forward guidance, asset purchase duration, and YCC/YCT – risks lower real rates, flatter curve, and weaker USD (and, in the worst case, a very adverse reaction across risk assets).

Economics: a policy discussion

As BofA frames it, there seems to be an agreement among Fed officials on the “what” but not the “how.” The consensus appears to be to send a strong signal that the Fed will be committed to accommodative policy, remaining at the ZLB, well into the recovery and perhaps even until full employment has been reached and inflation is able to run at/above the 2% target. This would be a more dovish strategy than following the 2008-09 recession when the Fed pursued a “normalization” policy, pushing up interest rates prior to achieving trend 2% inflation or closing the output gap. Back then the Fed discussed the balancing act between increasing rates earlier but slower, or waiting and having to hike more quickly. Looking back, it seems many Fed officials believe that waiting longer might have been prudent given that 2% inflation was not achieved and the Fed ended up reversing some of the hikes later in the recovery.

There are several options for the Fed to enhance forward guidance, which are not mutually exclusive:

the primary focus is on language, potentially using both outcome and calendar-based language. Fed officials seem particularly focused on making sure 2% inflation is reached, which means likely explicitly supporting an overshoot of the inflation target (something which the record surge in gold is clearly sniffing out). This could be done through a commitment to keep rates at zero until 2% is reached on a trend basis but also, perhaps, by reinforcing this language with calendar guidance.

The secondary focus is on balance-sheet policies such as yield curve caps or targets (YCT) or a change in the composition of the balance sheet (QE). While YCT on the short to medium end of the curve seems like an attractive option, it is still novel and Fed officials appear to want more time to study such a program. Recent language from Fed officials suggests our expectation for YCT to be introduced at the September meeting might end up being too early.

The Fed can choose to employ one or all of these strategies at the same time or phased in, depending on the state of the economy and markets (as a reminder, the worse the economy and the lower the S&P500, the greater the flexibility Powell will have to unleash the next phase, whatever it may be). Certainly, if facing a weaker economy with low realized and expected inflation, the Fed would likely need to be more aggressive. Another scenario would be if the market prematurely prices in hikes thereby tightening financial conditions. The Fed might look to fight this market pricing and push out hike expectations, which could be done through calendar guidance or YCT, most directly (unless of course the Fed wants to push the market lower so it has more degrees of freedom).

Meanwhile, the Fed is also engaging in a prolonged framework review that will likely guide the policy decision. The annual Jackson Hole conference will also take place virtually at the end of August. It has historically been a good forum for central bankers to debate policy and will likely be focused on the best way to achieve enhanced forward guidance.

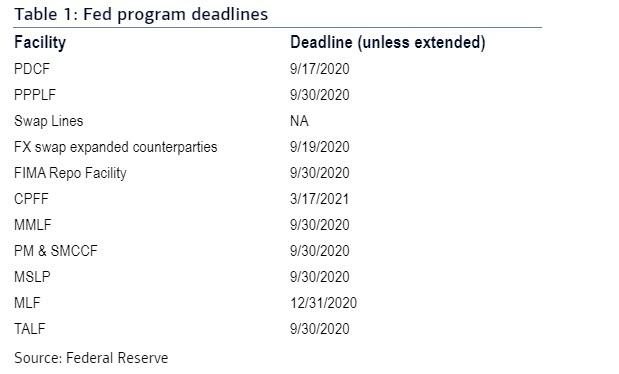

Fed markets programs: extension likely

The July FOMC meeting will likely see some communication around an extension of Fed and Treasury markets programs. Most markets programs are slated to expire in September as shown in the table below.

However, it is virtually assured that these will all be extended as the Fed will want to keep these programs indefinitely in place to guard against the risk of a more material economic slowdown and potential tightening of financial conditions (and also because any of the “temporary” aspects of the covid crisis are really permanent). BofA anticipates that most programs will be extended until March 2021 (in reality they will never expire). This would reduce the risk of a material tightening of financial conditions in 2H and smooth volatility stemming from year-end dealer balance-sheet constrains.

Most of the programs require Treasury approval for extension, and it is safe to assume that both the Fed and Treasury will be supportive of pushing out their deadline.

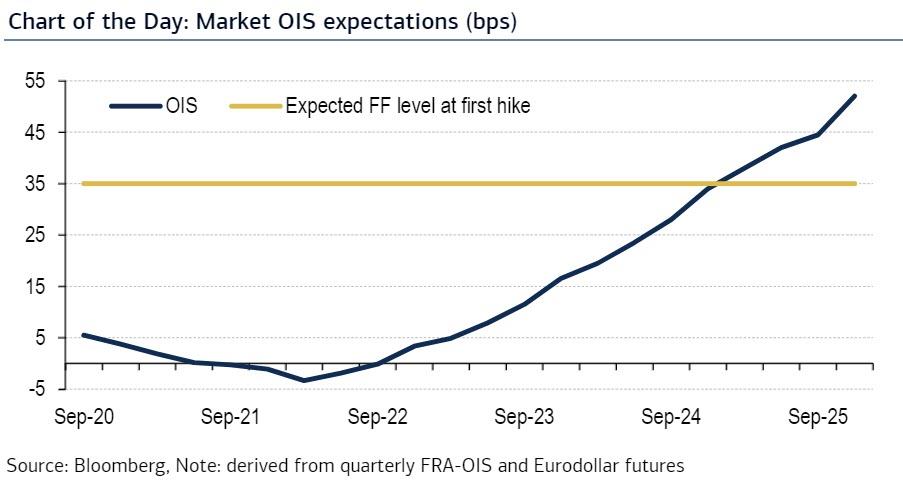

Rates: September stage setting and twist potential

According to BofA STIR strategists, the US rates market expects no new policy action to be taken at the July FOMC meeting. Instead, market participants will be much more focused on the guidance and “stage setting” that Chair Powell provides on the next steps to ease policy, including enhanced forward guidance, asset purchase adjustments, and yield curve control (YCC)/yield curve targeting (YCT).

While no change is expected to the Fed’s settings for administered rates (IOER, ON RRP) at this meeting, the rates market is already expecting a very dovish message from the Fed with the timing of the first rate hike not until late 2024 or early 2025 (if ever).

The main challenge for the Fed will be to find ways to “out dove” market expectations in their next easing round likely through:

the establishment of an inflation framework that ensures a “durable” increase in core PCE at or above 2% for 6 or 12 months before the first rate increase and

a potential reallocation of Treasury purchases to remove additional duration risk from the market.

BofA discusses the potential for a Fed UST twist and likely market reaction below:

Why twist? Recent media reports have suggested the Fed is considering changing the composition of their UST and MBS toward longer-dated securities to further ease financial conditions. This theme was furthered on last week by headlines from William Dudley, former NY Fed head, who noted that the Fed could extend its purchase duration. Both sets of comments come in the context of a Fed that is seeking to “pivot” from market stabilization to monetary easing via some combination of forward guidance, asset purchases, and potential YCC / YCT.

How to twist? The Fed has clear logic to twist upon implementation of enhanced forward guidance or YCC. The argument to twist would be most impactful if the Fed incorporated any calendar dimension to its guidance. For example, a credible Fed commitment not to raise rates or implement YCC until at least end ’22 / end ’24 would reduce the need to purchase securities at this part of the curve. The slated purchases could then be reallocated to longer-dated maturities to extract more duration risk from the market while keeping total purchase quantity the same or lower.

The Fed is currently purchasing $80bn/month of USTs (in proportion to USTs outstanding). BofA shows hypothetical Fed purchase scenarios below (Table 2) where the Fed could cease buying the 0-2.25Y or 0-4.5Y part of the curve, leave TIPS purchases unchanged, and distribute the remaining purchases in proportion to debt outstanding. The Fed could also remove more 10Y duration equivalent risk from the market while maintaining the current monthly purchase pace or lowering it to $65bn/m.

Twist effectiveness? Recall the 2011 twist and relevance of a similar policy today.

2011 twist: The Fed announced its most recent twist in September 2011 (a combination of short-term UST sales and longer-dated UST purchases) in reaction to the sharp risk off and economic slowdown following the US downgrade. This policy was mentioned in the August meeting minutes and was implemented the following meeting. The weighted average maturity of purchases increased substantially while keeping the total amount of UST holdings the same, on average (Chart 1, Table 2). Long-end rates declined materially the day the twist was announced and the curve aggressively bull flattened (Chart 2, Table 3). The month after the twist, rates sold off but the curve remained flatter.

Effectiveness today: Today is very different from 2011 and the Fed knows it. Comparing today vs September 2011: 10 and 30Y rates are 135-200bp lower, curves are significantly flatter, 10Y term premium measures have fallen 80-200bp, the real neutral rate (real 5y5y) has dropped 160bp, and the Chicago Fed fin conditions index is easier (Table 4).

The June FOMC meeting minutes reflect that the Committee is well aware of these dynamics: “declines in the neutral rate of interest, term premiums, and low levels of longer-term yields would likely act as constraints on the effectiveness of asset purchases in the current environment“. However, Treasury WAM and longer-dated issuance is higher, which a Fed twist would offset.

Twist impact: Fed twist would likely result in (1) 30Y UST rally and curve bull flattening, likely on par with 2011, and (2) spread curve steepening. The spread curve move would be driven by a modest cheapening of short-dated USTs vs OIS (less Fed buying) and a richening of longer-dated USTs vs OIS (more Fed buying). Bank front-end policing would likely limit the potential for a material UST-OIS cheapening.

Bottom line: there is rising likelihood for a “twist” operation, especially since the Fed seemingly wants to ease more. This risks wider 30Y spreads and reinforces even lower longer-dated real rate view (currently 10Y TIPS is at a record low -0.93%). Guidance on the likelihood of a Fed twist from Powell’s press conference or July FOMC minutes release (29 August) will be of keen interest to the rates market and the outlook for the long end of the curve. That said, not even BofA expects the Fed to commit to such a policy at this meeting, but likely start the stage-setting process this week.

* * *

Impact on the dollar

With an uneventful FOMC meeting widely anticipated, there is only moderate risk to FX and USD specifically. Still, potential discussion of the Fed’s toolkit (specifically options to ramp up monetary policy support in the event that downside risks are realized) seems a negative USD risk, in BofA’s view, as it is likely to reinforce the widespread belief among market participants in the Fed “put” that has driven up risk assets and undermined the greenback since end-March. For the same reason, extension of current programs may also weigh on USD. And while perception that a credible and effective set of additional Fed stimulus options exists, it would serve to further undermine USD per above, while as BofA ominously warns, “perception that the Fed is out of ammo could cause a reassessment of the Fed “put” and support USD via lower risk assets.”

Sharp USD weakness over in the second half of July has accelerated into this FOMC meeting. Over the last week, the DXY is about -3% lower, with EUR and SEK leading the pack of outperformers against USD. Much of the recent USD weakness is due to (1) buoyancy in risky “reflation”-sensitive assets, which continue to decouple from challenging economic conditions and recently worsening COVID-19 dynamics; as well as (2) the accelerating EUR rally driven by market participants concerned over missing out on bullish price action post-EU Recovery Fund approval (which however does not equate to broad dollar weakness as discussed previously).

Looking forward, BofA expects a reversal in USD weakness despite persistent over-valuation, and forecasts EUR/USD is 1.08 at end-2020 due to COVID-19-related risks to the global and US economies although it concedes that “persistently frothy risk appetite is a risk to this call.”

via ZeroHedge News https://ift.tt/3gaNwBs Tyler Durden

Environmental lawyer Robert F. Kennedy Jr. warned Americans on Thursday to be cautious about any new coronavirus vaccine, pointing out that key parts of testing are being skipped.

“The Moderna vaccine, which is the lead candidate, skipped the animal testing altogether,” Kennedy said during an online debate on mandatory vaccinations with renowned Harvard law professor Alan Dershowitz. The debate was aired by Valuetainment and moderated by Patrick Bet-David.

Kennedy is part of a political family, being the son of Senator Robert F. Kennedy and the nephew of President John F. Kennedy. Both were murdered in the 1960s.

Another aspect of testing was equally unsatisfying, Kennedy said. The Moderna vaccine was tested “on 45 people. They had a high-dose group of 15 people, a medium-dose group of 15 people, and a low growth group of 15 people.”

“In the low-dose group, one of the people was so sick from the vaccine they had to be hospitalized,” he explained.

“That’s six percent. In the high-dose group, three people got so sick they had to be hospitalized. That’s twenty percent.”

In spite of these significant problems,

“they’re going ahead, and making two billion doses of that vaccine.”

Another problem with the testing of the coronavirus vaccine is that it’s tested not on “typical Americans,” but a carefully selected group of people who don’t suffer from certain conditions.

“They use what they call exclusionary criteria,” Kennedy said.

“They are only giving these vaccines in these tests that they’re doing to the healthiest people.”

“If you look at their exclusionary idea criteria: You cannot be pregnant, you cannot be overweight, you must have never smoked a cigarette, you must have never vaped, you must have no respiratory problems in your family, you can’t suffer asthma, you can’t have diabetes, you can’t have rheumatoid arthritis or any autoimmune disease. There has to be no history of seizure in the family. These are the people they’re testing the vaccine on.”

He asked,

“What happens when they give them to the typical American? You know, Sally Six-Pack and Joe Bag of Donuts who’s 50 pounds overweight and has diabetes.”

Kennedy stressed several times that

“any other medicine … that had that kind of profile in its original phase-one study would be [dead on arrival].”

“No medical product in the world would be able to go forward with the profile that Moderna has,” he reiterated.

During the course of the debate, Kennedy also talked about the regular vaccines most people take, from Hepatitis B to the flu shot, emphasizing that no proper testing had ever been done, which is mandatory for any other medication. Vaccines “are the only medical product that does not have to be safety-tested against a placebo,” he explained.

In a study involving placebos, one group of people would be injected with the actual vaccine, while another group would be injected with saline solution, which would not have any effect in preventing a particular disease. The people who are part of the study would then be observed to see if there are any differences between the two groups, both regarding the disease vaccinated against, and side effects.

As these tests are never done on vaccines, “nobody knows the risk profile of any vaccine that is currently on the schedule. And that means nobody can say with any scientific certainty that that vaccine is averting more injuries and deaths than it’s causing.

In fact, it should be the opposite, Kennedy said, with vaccines being tested even more thoroughly than any other medication.

“It’s a medical intervention that is being given to perfectly healthy people to prevent somebody else from getting sick,” he pointed out.

“And it’s the only medicine that’s given to healthy people … and particularly to children who have a whole lifetime in front of them. So you would expect that we would want that particular intervention to have particularly rigorous guarantees that it’s safe.”

Kennedy said

“it’s not hypothetical that vaccines cause injury, and that injuries are not rare. The vaccine courts have paid out four billion dollars” over the past three decades, “and the threshold for getting back into a vaccine court and getting a judgment – [the Department of Health and Human Services] admits that fewer than one percent of people who are injured ever even get to court.”

He mentioned another reason not to trust blindly any company currently producing vaccines in the United States. Each one of the four vaccine producers “is a convicted serial felon: Glaxo, Sanofi, Pfizer, Merck.”

“In the past 10 years, just in the last decade, those companies have paid 35 billion dollars in criminal penalties, damages, fines, for lying to doctors, for defrauding science, for falsifying science, for killing hundreds of thousands of Americans knowingly.”

“It requires a cognitive dissonance,” Kennedy commented, “for people who understand the criminal corporate cultures of these four companies to believe that they’re doing this in every other product that they have, but they’re not doing it with vaccines.”

While Kennedy is often described as being against vaccines altogether, he stressed that he does not oppose vaccines, as such. He accused his critics of “marginalizing me and silencing me” by misrepresenting his actual position.

In May, Kennedy signed an appeal created by Archbishop Carlo Maria Viganò aimed at raising public awareness among people, governments, scientists, and the media about the serious dangers to individual freedom caused during the spread of Covid-19.

The appeal raised concern at one point about a COVID-19 vaccination in relation to human freedom.

“We also ask government leaders to ensure that forms of control over people, whether through tracking systems or any other form of location-finding, are rigorously avoided. The fight against Covid-19, however serious, must not be the pretext for supporting the hidden intentions of supranational bodies that have very strong commercial and political interests in this plan. In particular, citizens must be given the opportunity to refuse these restrictions on personal freedom, without any penalty whatsoever being imposed on those who do not wish to use vaccines, contact tracking or any other similar tool.”

The appeal made it clear that for Catholics it is “morally unacceptable to develop or use vaccines derived from material from aborted fetuses.”

Comments on the YouTube video of the debate between Kennedy and Dershowitz indicated, almost unanimously, that Kennedy had won the debate. Dershowitz conceded many points, arguing, however, that from the point of view of constitutional law, the coronavirus vaccine could be made mandatory.

Dershowitz, who has provided legal counsel to and defended people like Donald Trump, Jeffrey Epstein, and Julian Assange, cited a 1905 Supreme Court ruling as precedent. Jacobson v. Massachusetts upheld the authority of states to enforce compulsory vaccination laws.

Kennedy clarified that the state government at the time had offered people to either be vaccinated or pay a five dollar fine. Dershowitz’s argument, however, was that based on constitutional law, including this precedent, “the state has the power to literally take you to a doctor’s office and plunge a needle into your arm.”

Kennedy said,

“I think there’s a big constitutional chasm between, you know, that remedy, which is paying a fine, and actually going in and holding somebody down and forcibly injecting them.”

President Trump has already said that the new coronavirus vaccine would not be mandatory, but available for those “who want to get it. Not everyone is going to want to get it.” A LifeSiteNews petition saying no to mandatory vaccinations has garnered more than 650,000 signatures and can still be signed here.

The ethical issue of many vaccines being derived from cell lines of aborted babies was not discussed during the debate.

via ZeroHedge News https://ift.tt/39DBJZT Tyler Durden

Florida Man Used PPP Loans To Buy Lamborghini Huracan, Goes On Spending Spree Tyler Durden

Tue, 07/28/2020 – 22:55

For months, we’ve warned loans granted under the Paycheck Protection Program (PPP) for businesses seeking coronavirus relief funds were susceptible to fraud.

A Florida man was charged Monday after using PPP loans to buy a 2020 Lamborghini Huracan, according to the U.S. Department of Justice (DoJ).

2020 Lamborghini Huracan. h/t Fox News, DoJ

David T. Hines of Miami, Florida, fraudulently obtained $3.9 million in PPP loans and used those funds to buy the Huracan, shop at luxury stores, and splurge on fancy Miami resorts.

The DoJ charged Hines,29, with one count of bank fraud, one count of making false statements to a bank and one count of engaging in transactions in unlawful proceeds.

The DoJ complaint claims the man requested $13.5 million in PPP loans for four companies with dozens of employees.

“In the days and weeks following the disbursement of PPP funds, the complaint alleges that Hines did not make payroll payments that he claimed on his loan applications,” according to the complaint. “He did, however, make purchases at luxury retailers and resorts in Miami Beach.”

In early July, we reported a Texas man received almost $1 million in PPP loans to support 51 employees at his “Texas Barbecue” company, though the company never existed. The man used the loans to trade cryptocurrency on Coinbase.

Not too long ago, Treasury Secretary Steven Mnuchin said that he is considering “forgiving all small loans, but would need fraud protection,” for businesses. The government has so far approved about $518.1 billion spread over 4.9 million PPP loans since the pandemic began.

The LA Times notes there are at least a dozen PPP fraud cases filed in 11 states in July. Many of these cases are blatant fraud, such as falsifying tax or business records, lying on applications, and misusing the money.

While safeguards to prevent PPP fraud appear to be lacking, Senate Republicans have unveiled even more PPP loans for business, which has really upset the Tea Party. “Republicans are now no different than socialist Democrats when it comes to debt,” Senator Rand Paul said.

via ZeroHedge News https://ift.tt/2CNGXXm Tyler Durden

With ‘Liability Shield’ Red-Line Looming Over Stimulus Bill, Schumer Claims Dems “Have A Lot Of Leverage & Aren’t Afraid To Use It” Tyler Durden

Tue, 07/28/2020 – 22:35

While the to-ing and fro-ing over whether $200 is too little and $600 is too much plays out, the bigger issue separating the two sides of the aisle over the next US aid package is unlikely to find a goldilocks ‘just right’ outcome anytime soon.

As a reminder the Senate GOP plan includes:

$1,200 direct payments, CARES redux

PPP sequel “to help prevent more layoffs”

Federal UI bonus, hints at $200/week

Money for schools

$ for testing, treatment, vaccines

Liability shield for biz/hospitals/entities

Senate Majority Leader Mitch McConnell reaffirmed that his proposed changes to liability law must be included wholesale in the aid package during an interview on CNBC, saying…

…the legislation “will have liability protection in it, so we’re not negotiating with the Democrats over that.”

On the other side, as Bloomberg reports, Senator Dick Durbin, the chamber’s No. 2 Democrat, said he doesn’t see any reason his party would support the plan to shield businesses, schools and other organizations from lawsuits over Covid-19 infections from employees or customers.

“This is an effort by the Republicans to seize the moment and to push through changes in tort law that they have been longing for for decades that have nothing to do with Covid-19.”

House Speaker Nancy Pelosi said that the first day of negotiations did not go well:

“It wasn’t a good way for us to begin the discussion.”

Schumer was less pessimistic, and more bombastic, proclaiming that Democrats have the power and Republicans are desperate:

“I think Republicans are reading the polls. The president is slumping, their Republican Senate candidates are slumping in the polls. They have to show something,”

Adding that:

“We don’t have a majority in the Senate and we can’t pass it alone, but we have a lot of leverage and we’re going to use it,”

But on the bright side, we did not get leaked photos of her standing and pointing across the cabinet desk at members of the Trump admin.

Finally, Trump weighed in, giving himself an out by saying that there are some things in the Republican package that he doesn’t support.

The Senate Republicans’ more modest $1 trillion stimulus package unveiled yesterday remains a far cry from the blockbuster $3.5 trillion proposal that Democrats have proposed and thus, by the end of the farcical theater pretending to be a negotiation, the final sum will likely be closer to the latter than the former…

McConnell is somewhat cornered by pressure from more fiscally responsible conservatives (of course that is all relative). As Senator Kevin Cramer, a North Dakota Republican warned:

“The bigger the price tag gets, the fewer Republicans that will support it.”

And if they do, one wonders what that will do the price of gold?

via ZeroHedge News https://ift.tt/334UELW Tyler Durden

China Has Quietly Cut Dollar Usage In Cross-Border Trade By 20% Tyler Durden

Tue, 07/28/2020 – 22:15

The chorus calling for a weaker dollar is getting louder, and now includes none other than a stark warning from Goldman Sachs, which in a stunning shot across the bow of the modern monetary system warned overnight that U.S. monetary and fiscal policy (i.e., helicopter money a/k/a MMT) is triggering currency “debasement fears” and that for the first time “real concerns are emerging” about the future of the dollar as a reserve currency.

And while the DXY Index got a rare reprieve from the selling on Tuesday – despite Goldman’s ominous warning – gold continued marching higher, even as technical indicators show signs of near-record overextension.

As Bloomberg’s Ye Xie summarizes, “it seems like a perfect storm for the U.S. currency: the relentless decline of real yields, the U.S.’s inability to control the virus, the overhang of the twin deficits and the dear valuation.” Adding to reserve currency concerns, Bridgewater’s Ray Dalio – who is clearly talking either his or Beijing’s book although these days the two appear interchangeable – warned a Sino-U.S. “capital war” could harm the dollar.

Meanwhile, as Rabobank’s Michael Every has been discussing for the past few months, with the U.S. now using the privileged role of the dollar for political gains, such as penalizing banks over issues in Hong Kong and Xinjiang for instance, it will naturally alarm politicians in other countries, Xie adds.

Indeed, as Xie adds, China is already is quietly reducing its reliance on the dollar in cross-border trade and services. The percentage of the payments and receipts denominated in yuan in total FX transactions by banks for their clients increased to 37% in June, from 19% two years ago, according to data compiled by the State Administration of Foreign Exchange, with the Bloomberg strategist also calculating that the usage of the dollar has declined to 56% from 70% – a decline of ~20%.

While this shift partly reflects local companies’ desire to limit their exposure to FX volatility, it may also mirror an intentional nudge from the authorities… and it’s not just trade.

Picking up on his recent observation that Jack Ma’s decision to list his giant Ant Group in Shanghai and Hong Kong (where it is seeking a $200BN valuation) instead of the US, coupled with the exodus of U.S.-listed Chinese companies from America, Xie writes that this underscores the shift in capital markets, and adds that “by extension, one has to wonder what Beijing might to do with its $1.1 trillion Treasury holdings.”

Guo Shuqing, the party secretary of the PBOC, delivered a stern warning on the U.S. currency last month: “Some people say, ‘Domestic debt is not debt, but external debt is debt. For the United States, even external debt is not debt.’ This seems to have been the case for quite some time in the past, but can it really last for a long time in the future?”

As Xie concludes referring to the chart above, “apparently China isn’t waiting to find out the answer.”

via ZeroHedge News https://ift.tt/3jPlxcP Tyler Durden

{kind=link}