Big-Tech, Bonds, Bitcoin, & Bullion Bid As Dollar Dive Continues Tyler Durden

Thu, 08/20/2020 – 16:01

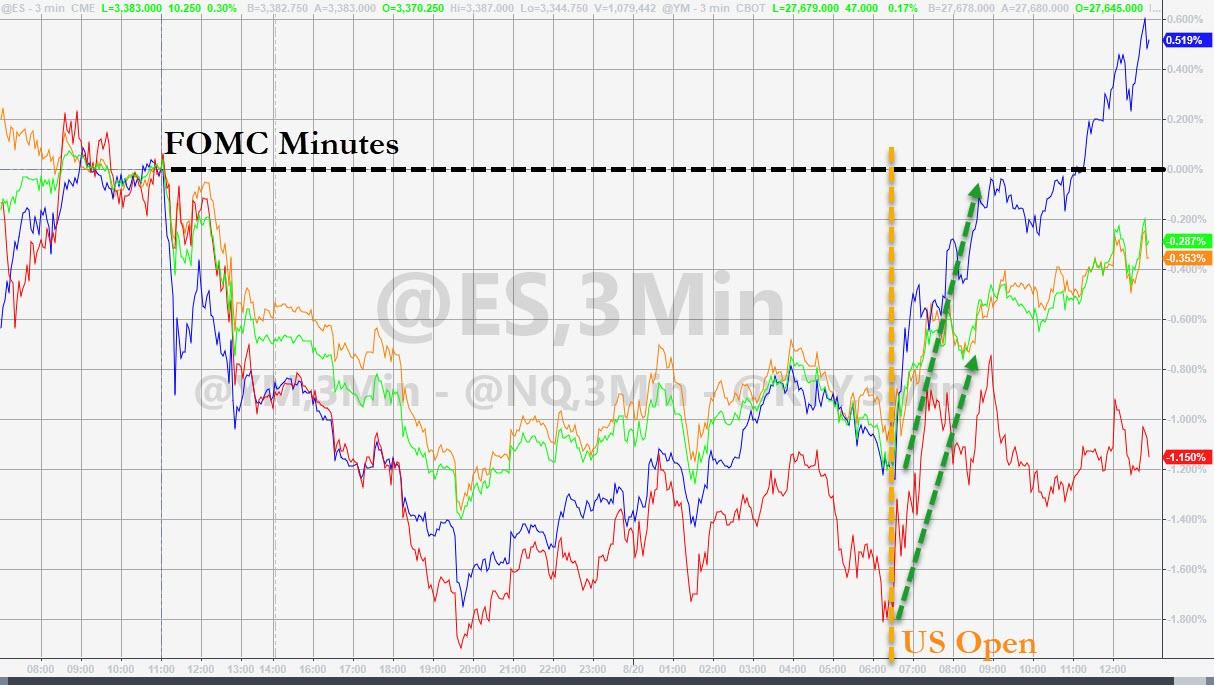

From the opening bell today, stocks – well, we should say mega-tech stocks – were utterly panic bid (catalyzed early by JNJ vaccine headlines), with the Nasdaq erasing all of the post-FOMC Minutes losses (NOTE that none of the other major indices managed to retrace the losses)…

On the day, it looked early on like The Dow may suffer its 4th losing day in a row – a terrible thing that has not been seen since February – but it, like everything else, was bid into the green and beyond. Small Caps closed red…

YTD, the Nasdaq is crushing Chinese stocks and Europe remains negative…

FANG stocks rallied back near its record intraday high and closed at a record closing high…

Source: Bloomberg

Bonds were also bid (after disappointing claims data showed an economy un-recovering), erasing all of the FOMC Minutes spike in yields…

Source: Bloomberg

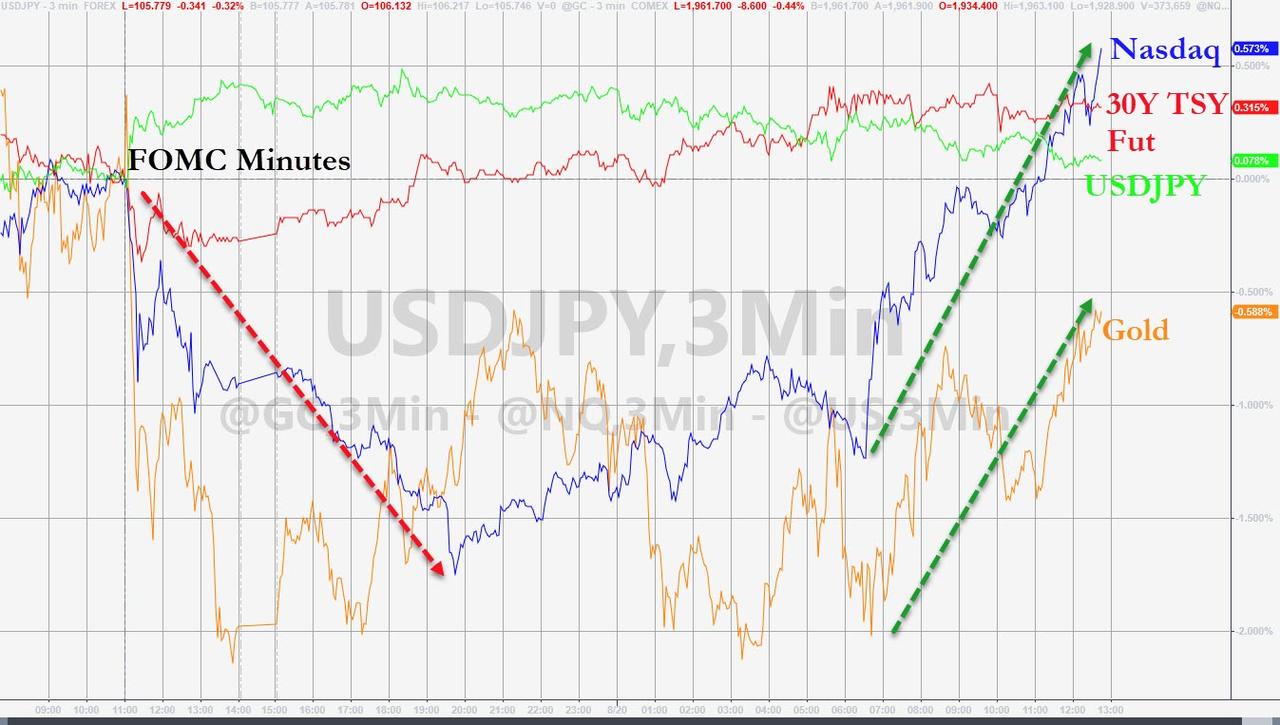

The dollar chopped around early on but tumbled after Europe closed…

Source: Bloomberg

And as the dollar slipped, gold rallied back from yesterday’s dive…

Source: Bloomberg

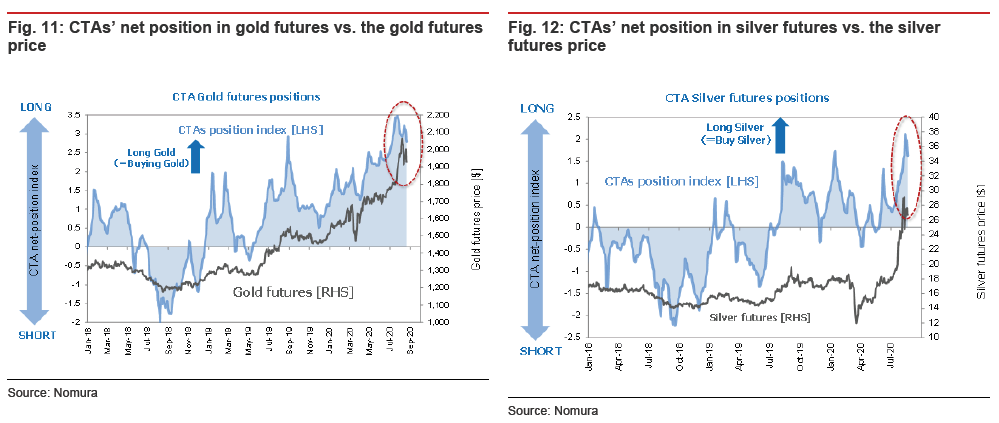

CTA positioning in gold fits with the price move but silver seems to suggest there is room for more as CTAs are squeezed in….

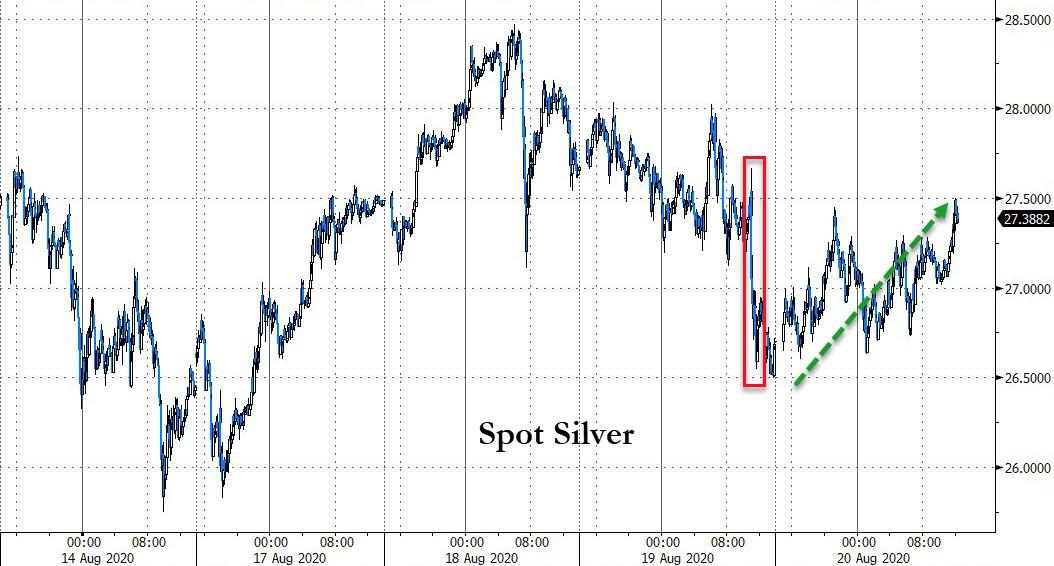

As did silver…

Source: Bloomberg

Since the FOMC Minutes suggested no YCC, only gold is still lower as Nasdaq ripped back to catch up and overtake the dollar and bonds…

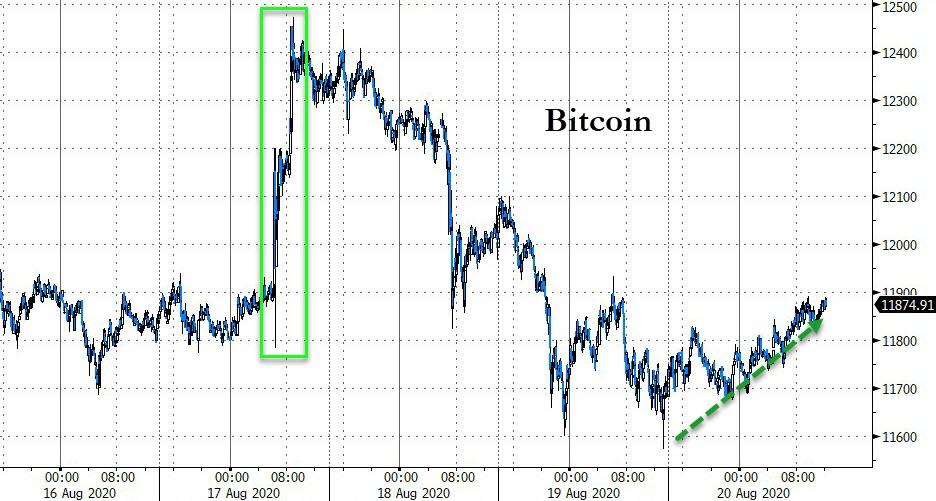

Bitcoin also rallied on the day…

Source: Bloomberg

Oil prices dumped and pumped today and ended lightly lower…

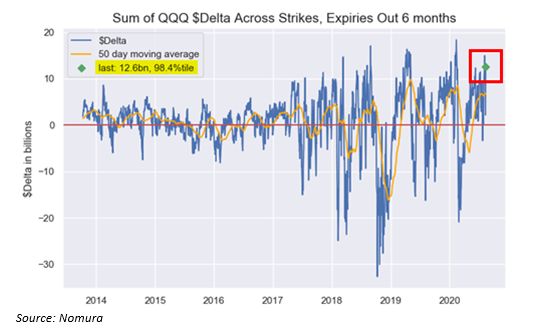

What is perhaps more notable is the potential for this to end… soon. Nomura’s Charlie McElligott writes today about the impact of tomorrow’s options expiration given the derivative market’s exposure goinb in. The $Gamma seen in QQQ (Nasdaq) options remains rather “extreme” at 87.3%ile (was 95th %ile into yday) as we have rallied violently to upper strikes.

This, McElligott warns, in conjunction with 99.3%ile $Delta and now an expected 58% of the Gamma rolling-off after this Friday’s expiration (!!!) makes the case for potentially “binary” price-action next week with a catalyst in either direction, as Dealer “long Gamma” hedging flows should collapse thereafter and allow for a much larger range of movement.

Additionally, the cross-asset strategy MD notes that he currently sees QQQ Gamma “flipping” below $272.06, ex tomorrow’s expiry.

And there is an increasingly ominous major (bearish) divergence between the ‘price’ of the index and the breadth of its underlying components (in this case, the % of names above their 50-day moving average) suggests trouble ahead…

Source: Bloomberg

It certainly did not end well in February as the index continued to rise in the face of growing virus headlines from around the world (but under the hood, a growing number of names were doubting the index’s apparent omnipotence).

via ZeroHedge News https://ift.tt/34hm81w Tyler Durden

‘Fight Club In The Skies’: Brawl Erupts On American Airlines Flight Over Mask Policy Tyler Durden

Thu, 08/20/2020 – 15:50

The past months of coronavirus lockdown and social distancing measures have produced some truly bizarre scenes, but perhaps none so strange and potentially dangerous as the brawl that broke out on an American Airlines flight this week.

The incident which happened Monday and was caught on video, reportedly started when a traveler on a Las Vegas to Charlotte flight refused to comply with the airline’s coronavirus protective face mask policy. After a flight attendant ordered the maskless woman to exit the flight, other angry passengers appeared to invervene while the airline called authorities to get a disruptive woman off, and that’s when punches started flying.

The passenger that uploaded the widely shared video said, “Nothing like a morning Fight Club as tempers flared on American Air LAS-CLT flight today.”

“So much for social distancing!” the eyewitness added. Onlookers could be seen getting increasingly frustrated that the belligerent woman in the pink shirt was causing a significant flight delay due to the incident.

Security was called in and escorted the women off the plane, but the latest in a series of ‘mask vs. maskless’ tense encounters over this bizarre summer of COVID-19 social distancing measures.

The full three-and-a-half minute video of the ordeal shows a woman standing in the aisle arguing another while airline personnel are nowhere in sight, followed by the moment fists go flying. A man in row behind also later joins in the melee.

An American Airlines official statement on the incident later said, “On Monday, a customer on American Airlines Flight 1665 with service from Las Vegas to Charlotte failed to comply with our mandatory face-covering policy after boarding the aircraft prior to departure.”

It continued: “In accordance with our policy, the customer was subsequently asked to leave the aircraft and became disruptive, resulting in an altercation with other passengers.”

via ZeroHedge News https://ift.tt/3ghnBrc Tyler Durden

Virtue Reversal: Goodyear Bends The Knee After Trump Sparks Boycott Tyler Durden

Thu, 08/20/2020 – 15:32

After a ham-handed attempt at damage control with a non-apology over biased “diversity” training sparked outrage from President Trump – which in turn sparked a boycott by conservatives, Goodyear CEO Rich Kramer issued a direct apology on Thursday.

“To be clear, Goodyear does not endorse any political organization, party or candidate,” reads Kramer’s statement, which adds that the company “strongly supports our law enforcement partners and deeply appreciates all they do to put their lives on the line each and every day for their communities.”

“We have clarified our policy to make it clear associates can express support for law enforcement through apparel at Goodyear facilities,” which means – no MAGA hats, but presumably means ‘Blue Lives Matter’ and ‘All Lives Matter’ attire is now acceptable.

(Cue BLM boycott)..

A message from Rich Kramer: By now, you are aware of a visual from our Topeka factory that has been circulating in the media. I want to personally clear the record on what you are seeing and hearing. pic.twitter.com/UqqFeFQn6t

On Wednesday, President Trump tweeted “Don’t buy GOODYEAR TIRES” after a leaked photo of an external firm’s ‘diversity training’ slide appeared to show that the company considers “Blue Lives Matter,” “All Lives Matter” and “MAGA” attire “unacceptable,” while at the same time encouraging “Black Lives Matter” and “Lesbian, Gay, Bisexual, Transgender Pride (LGBT)” attire.

Don’t buy GOODYEAR TIRES – They announced a BAN ON MAGA HATS. Get better tires for far less! (This is what the Radical Left Democrats do. Two can play the same game, and we have to start playing it now!).

Increasing the number of police in schools doesn’t make school safer and leads to harsher discipline for infractions, according to a new study in the journal Criminology & Public Policy.

The longitudinal study, published by researchers at the University of Maryland and the firm Westat, looked at disciplinary offenses at 33 public middle and high schools in California that increased their number of school resource officers (SROs) in 2013 or 2014, and then compared them over time with 72 similar schools that did not. The study found that increasing the number of SROs led to both immediate and persistent increases in the number of drug and weapon offenses and the number of exclusionary disciplinary actions against students.

While the initial bump in offenses could be explained simply as an effect of increased policing, the boost in recorded crimes and exclusionary responses persisted for 20 months in the schools studied. The researchers say this suggests that rather than deter crime in schools, increasing the number of SROs leads to more “formal responses to behaviors that otherwise would have been undetected or handled informally.”

“Our findings suggest that increasing SRO staffing in schools does not improve school safety and that increasing exclusionary responses to school discipline incidents increases the criminalization of school discipline,” Denise Gottfredson, professor emerita at the University of Maryland Department of Criminology and Criminal Justice, said in a statement.

The study’s findings come as school districts across the country are reconsidering the use of SROs in the wake of national demands for policing reforms. The number of police in schools has skyrocketed in schools over the past four decades, first in response to drugs and then mass shootings. Police departments and organizations like the National Association of School Resource Officers argue that well-trained SROs act as liaisons between the school and police department.

Earlier this month, Chicago Public Schools slashed its school police budget by more than half. So far, San Francisco is the largest school district to move toward defunding its SRO program. The Oakland school board also voted unanimously to eliminate the district’s police department and shift its $2.5 million budget to student support services. Minneapolis, Denver, Seattle, Charlottesville, and Portland, Oregon, have also ended or suspended relationships with local police.

Civil liberties groups and disability advocates have long argued that increases in school police and zero-tolerance policies for petty disturbances have fueled the “school-to-prison” pipeline and led to disproportionate enforcement against minorities and students with disabilities. (The study did not find a significant change in criminal referrals and exclusionary actions against special needs students.)

As with policing at large, viral videos of excessive force and small children being arrested have sparked national outrage.

Last week, body camera footage emerged showing police officers in Key West, Florida, trying and failing to handcuff an eight-year-old boy, whose wrists were too small for the cuffs. And an Orlando SRO made headlines last September when he arrested a six-year-old girl.

In February, a school resource officer at a high school in Camden, Arkansas, was relieved of duty after video showed him putting a student in a chokehold and lifting the student off the ground. Last December, a North Carolina SRO was fired after he brutally body-slammed a middle-schooler. In November, a Broward County sheriff’s deputy in Florida was arrested and charged with child abuse after a video showed him body-slamming a 15-year-old girl at a special needs school.

Chicago activists who want to defund the school system’s police program have cited a 2019 video in which Chicago police officers kick, punch, and tase a 16-year-old girl.

The study recommends that “educational decision-makers seeking to enhance school safety consider the many alternatives to programs that require regular police presence in schools.”

from Latest – Reason.com https://ift.tt/3l1c2b7

via IFTTT

Increasing the number of police in schools doesn’t make school safer and leads to harsher discipline for infractions, according to a new study in the journal Criminology & Public Policy.

The longitudinal study, published by researchers at the University of Maryland and the firm Westat, looked at disciplinary offenses at 33 public middle and high schools in California that increased their number of school resource officers (SROs) in 2013 or 2014, and then compared them over time with 72 similar schools that did not. The study found that increasing the number of SROs led to both immediate and persistent increases in the number of drug and weapon offenses and the number of exclusionary disciplinary actions against students.

While the initial bump in offenses could be explained simply as an effect of increased policing, the boost in recorded crimes and exclusionary responses persisted for 20 months in the schools studied. The researchers say this suggests that rather than deter crime in schools, increasing the number of SROs leads to more “formal responses to behaviors that otherwise would have been undetected or handled informally.”

“Our findings suggest that increasing SRO staffing in schools does not improve school safety and that increasing exclusionary responses to school discipline incidents increases the criminalization of school discipline,” Denise Gottfredson, professor emerita at the University of Maryland Department of Criminology and Criminal Justice, said in a statement.

The study’s findings come as school districts across the country are reconsidering the use of SROs in the wake of national demands for policing reforms. The number of police in schools has skyrocketed in schools over the past four decades, first in response to drugs and then mass shootings. Police departments and organizations like the National Association of School Resource Officers argue that well-trained SROs act as liaisons between the school and police department.

Earlier this month, Chicago Public Schools slashed its school police budget by more than half. So far, San Francisco is the largest school district to move toward defunding its SRO program. The Oakland school board also voted unanimously to eliminate the district’s police department and shift its $2.5 million budget to student support services. Minneapolis, Denver, Seattle, Charlottesville, and Portland, Oregon, have also ended or suspended relationships with local police.

Civil liberties groups and disability advocates have long argued that increases in school police and zero-tolerance policies for petty disturbances have fueled the “school-to-prison” pipeline and led to disproportionate enforcement against minorities and students with disabilities. (The study did not find a significant change in criminal referrals and exclusionary actions against special needs students.)

As with policing at large, viral videos of excessive force and small children being arrested have sparked national outrage.

Last week, body camera footage emerged showing police officers in Key West, Florida, trying and failing to handcuff an eight-year-old boy, whose wrists were too small for the cuffs. And an Orlando SRO made headlines last September when he arrested a six-year-old girl.

In February, a school resource officer at a high school in Camden, Arkansas, was relieved of duty after video showed him putting a student in a chokehold and lifting the student off the ground. Last December, a North Carolina SRO was fired after he brutally body-slammed a middle-schooler. In November, a Broward County sheriff’s deputy in Florida was arrested and charged with child abuse after a video showed him body-slamming a 15-year-old girl at a special needs school.

Chicago activists who want to defund the school system’s police program have cited a 2019 video in which Chicago police officers kick, punch, and tase a 16-year-old girl.

The study recommends that “educational decision-makers seeking to enhance school safety consider the many alternatives to programs that require regular police presence in schools.”

from Latest – Reason.com https://ift.tt/3l1c2b7

via IFTTT

Criticism of President Donald Trump’s response to the COVID-19 epidemic has figured prominently at the Democratic National Convention this week. But last night the party shifted its focus to a different sort of epidemic.

The actress Kerry Washington, the evening’s M.C., introduced the topic at the beginning of the program, saying “90 percent of Americans support common-sense gun laws, because we need to do more to address the epidemic of gun violence.” A convention video continued the theme. “Long before this pandemic, our country has been suffering from an epidemic of gun violence,” a Florida gun control supporter identified as “Maria W.” says, describing murder by firearm as a “public health crisis.”

Democratic presidential nominee Joe Biden uses similar rhetoric. “Joe Biden knows that gun violence is a public health epidemic,” his campaign website says, introducing “The Biden Plan to End Our Gun Violence Epidemic.” This year’s Democratic platform likewise talks about “ending the epidemic of gun violence.”

Leaving aside the question of whether the “common-sense gun laws” Biden favors would actually have a meaningful impact, is it accurate to describe gun violence in the United States as an “epidemic”? Obviously not in any literal sense, since gun violence is not caused by an infectious microorganism that spreads from person to person. Figuratively, however, the term epidemic implies a problem that is escalating and out of control, which is true of gun violence only if you focus on a narrow slice of the data.

According to the FBI’s numbers, total homicides in the United States fell from 24,700 in 1991 to a low of 14,164 in 2014—a 43 percent drop. The homicide rate fell even more dramatically, from 9.8 per 100,000 in 1991 to 4.4 per 100,000 in 2014—a 55 percent drop. Homicides rose in 2015 and 2016, then fell in 2017 and 2018, when the rate was 5 per 100,000, up 14 percent from 2014. The FBI has not published final data for 2019 yet, but preliminary numbers for the first half of the year indicate that homicides fell by 7.4 percent.

The trends for murders committed with firearms are slightly different because the type of weapon used varies over time. Gun homicides fell from a peak of 17,075 in 1993 to a low of 7,803 in 2014—a 54 percent drop. The number rose in 2015, 2016, and 2017, then fell in 2018, when it was 32 percent higher than in 2014 but still 40 percent lower than the 1993 total. The gun homicide rate in 2018 was about 3.1 per 100,000, half the 1993 rate.

As Philip Bump noted in The Washington Post last year, most Americans are not aware of this dramatic decline in gun homicides. In a 2019 Marist poll, 59 percent of respondents believed “the per capita gun murder rate in the U.S.” was higher than it was 25 years earlier, while 23 percent thought it was “about the same.” Just 12 percent knew that the rate had fallen, while 6 percent were not sure.

That misperception probably has a lot to do with news coverage of mass public shootings, which account for less than 1 percent of gun homicides. But all the talk about a gun violence “epidemic” reinforces the false impression that we are seeing historically high levels of murders committed with firearms.

The Democrats might argue that three consecutive years of rising gun homicides (followed by a drop) constitute an epidemic, even if the rate remains historically low. But they were already talking about an “epidemic” of gun violence in 2016, when the most recent FBI data indicated no trend that could justify that description even by the most generous definition.

Exaggerating a problem is a time-honored technique to build support for the policies you favor. It creates a sense of urgency that encourages voters to overlook those policies’ shortcomings, such as the irrelevance of “assault weapon” bans and the inability of “universal background checks” to affect the gun sources that criminals typically use.

At the same time, describing gun violence as an epidemic—the same framing that has generated myriad dubious studies of this criminological topic in medical and public health journals—applies a pseudoscientific veneer to proposals whose merits depend on value judgments as well as uncertain predictions about the practical consequences of “common-sense” gun controls. Such rhetoric also slants the debate by suggesting that deadly violence is a disease that can best be controlled by attacking the vectors of transmission—i.e., guns and bullets. It may not be accurate to talk about gun violence this way, but it is definitely useful.

from Latest – Reason.com https://ift.tt/34kfMi2

via IFTTT

Even those in the nonfinancial media have noticed the skyrocketing price of gold this year. Some partially identify, but don’t quite understand, some of the many (and more measurable) intermediary effects in the chain of causation such as a “weakened US dollar” and “low bond yields.” Those in the financial press add to these factors with ones like “central bank reserves” management, along with mining production and “jewelry and industrial demand.”

One mainstream headline surprisingly hit closest to the mark regarding the few (and less measurable) underlying causes: “Fear and Cheap Money Send Gold Price Soaring.”

But the chief cause for this and all major rises in gold prices is not “fear and” but fear of cheap money.

In a 2013 interview titled “What Is Key for the Price Formation of Gold?,” Robert Blumen makes the following seven key points, not only for then, but for today and the foreseeable (fiat money) future:

“There might be a statistical correlation between, for example, a net inflow into one sector and higher (or lower) prices. If someone has a statistical model that works, that is great. But it’s not causal. But it seems to me that even if someone has discovered correlations like that, they will be coincident with the price, rather than predictive. In order to forecast the price, you need an indicator that moves in advance of the price.”

“[There] is [a] vast amount of brainpower that goes into quantifying gold flows into market segments, such as industry, jewelry, coins, and funds. These quantities may be interesting for some purposes, but they’re not really that relevant if what you’re trying to do is understand the gold price, because there is not a connection between quantities and price in the way that most people think there is.”

“The gold market is not segregated into one market for the gold that was mined this year and another market for gold that was mined in past years. The buyer doesn’t care whether he’s buying a newly mined ounce of gold or buying from somebody who had purchased gold that was mined 100 years ago. All of the buyers are competing to buy and all of the sellers are competing to sell.”

“Gold is primarily an asset. It is true that a small amount of gold is produced and a very small amount of gold is destroyed in industrial uses. But the stock to annual production ratio is in the 50 to 100:1 range. Nearly all the gold in the world that has ever been produced since the beginning of time is held in some form.”

“In an asset market, consumption and production do not constrain the price. The bidding process is about who has the greatest economic motivation to hold each unit of the good. The pricing process is primarily an auction over the existing stocks of the asset. Whoever values the asset the most will end up owning it, and those who value it less will own something else instead. And that, in in my view, is the way to understand gold price formation.”

“Most of the market research about gold deals with exchange demand, which has the advantage that you can measure it. But reservation demand is far more relevant to the price. The profile of reservation demand among people who own gold is the main determinant of the gold price from the supply side….Reservation demand is where you demand something by holding onto it rather than selling it….I have reservation demand at the moment for an auto, a dining room table, a couch, a mobile phone, and so forth.”

Thus: “The gold price is set by investor preferences, which cannot be measured directly. But I think that we understand the main factors in the world that influence investor preferences in relation to gold. These factors are the growth rate of money supply, the volume and quality of debt, political uncertainty, confiscation risk, and the attractiveness (or lack thereof) of other possible assets.”

The 2015 book Austrian School for Investors: Austrian Investing between Inflation and Deflationserves as an important complement to Blumen’s work on gold price formation. The four authors are not just Austrians in an economic sense, but literal Austrians from the country of the same name. What follows are five key points from the “Precious Metals” section of chapter 9 on “Austrian Investment Practice”:

1. “The marginal utility of gold declines at a slower rate than that of other goods. It is owing to this superior characteristic that gold and silver enjoy their monetary status, and not their supposed scarcity. Their high marketability represents also their decisive advantage over other stores of value….For this reason, central banks hold gold as a currency reserve, and not real estate, artworks or commodities.”

2. “Most analysts assert that gold has the characteristics of an inflation hedge. There are, however, also critical voices. They opine that there is no statistical correlation between gold prices and price inflation rates, and conclude that the inflation hedge notion is thus a myth. We examined this question and drew the following conclusion: gold does not correlate with the rate of inflation as such, but with the rate of change of the inflation rate.

3. “If gold is already weakening in a period of disinflation, it must be even weaker in a period of deflation. This is however a fallacy. The trend of gold in a deflationary environment has barely been analyzed, not least because there exist only very few examples of deflationary periods….In a period of pronounced deflation, [not only do] government budgets become overstretched [but] trust in the financial system and paper currencies declines, while gold gains in importance due its top-notch credit quality.”

4. “Akin to an hourglass, liquidity in the financial system gradually flows downward as the willingness to take risks declines. At the very bottom is gold. Due to general skepticism, the circulation of gold declines as it is increasingly hoarded. The degree of hoarding is always proportional to the confidence in government and its currency.”

5. “Gold exhibits a very low correlation with most other asset classes, especially stocks and bonds.”

The answer to the question of why gold is skyrocketing is “follow the money printing.” US M0 money supply has been subject to a number of quantitative easing (QE) programs since 2008, pushing money supply growth ever higher.

All this suggests that “fear of cheap money” really is a primary factor in pushing up demand for gold. Such fear increases in times of economic turmoil. Such turmoil is almost always caused, and made worse, by government intervention. In 2020 that includes, not just more QE, but also the chaotic government responses to the coronavirus and civil unrest. But don’t expect economists or investors to agree on all this any time soon. I will end with a quote from an article by economist Bob Murphy:

There’s an old joke that the price of gold is understood by exactly two people in the entire world. They both work for the Bank of England and they disagree.

via ZeroHedge News https://ift.tt/32e4OrN Tyler Durden

Obama State Department Official Destroyed Records At Christopher Steele’s Request Tyler Durden

Thu, 08/20/2020 – 15:05

In January 2017, former State Department official Jonathan Winer destroyed several years worth of reports from former UK spy Christopher Steele, at Steele’s request, according to the Daily Caller, citing a report released Tuesday.

Winer, a former legislative assistant to former Sen. John Kerry who became the State Department’s Special Envoy for Libya when Kerry was Secretary of State – was Steele’s contact at the State Department, and received the now-debunked reports claiming that President Trump had been compromised by the Russians.

According to the Senate report, Winer disclosed that he destroyed reports that Steele had sent him over the years. The Senate report also says that Winer failed to reveal when asked in his first interview with the committee that he had arranged the meeting for Steele at the State Department months earlier. –Daily Caller

“After Steele’s memos were published in the press in January 2017, Steele asked Winer to make note of having them, then either destroy all the earlier reports Steele had sent the Department of State or return them to Steele, out of concern that someone would be able to reconstruct his source network,” reads the Senate report, which quote sWiner as saying “So I destroyed them, and I basically destroyed all the correspondence I had with him.“

In total, Winer had received over 100 intelligence reports from Steel between 2014 and 2016.

Emails that The Daily Caller News Foundation obtained through a Freedom of Information Act lawsuit show that Winer shared Steele’s reports with a small group of State Department officials. The Senate report says that the State Department was able to provide the committee with Steele’s reports from 2015 and 2016, though most from 2014 are missing. –Daily Caller

In March, Steele told a UK court that he had “wiped” all of his dossier-linked correspondence in December, 2016 and January, 2017, and had no records of communications with his primary dossier source, Igor Danchenko.

In addition to receiving reports from Steele, Winer gave Steele various anti-Trump memos from Clinton operative Sidney Blumenthal, which originated with Clinton “hatchet man” Cody Shearer. Winer claims he didn’t think Steele would share the Clinton-sourced information with anyone else in the government.

“But I learned later that Steele did share them — with the FBI, after the FBI asked him to provide everything he had on allegations relating to Trump, his campaign and Russian interference in U.S. elections,” Winer wrote in a 2018 Op-Ed.

Steele was paid $168,000 by opposition research firm Fusion GPS to produce his anti-Trump dossier, which was funded in part by Hillary Clinton and the DNC, who used law firm Perkins Coie as an intermediary.

Publishers Join Movement To Wrest More App-Store Subscription Money Away From Apple Tyler Durden

Thu, 08/20/2020 – 15:04

It looks like Epic Games decision to sue Google and Apple, alleging anti-competitive and punitive reprisals illegally undertaken by both tech giants against Epic when it tried to avoid pay what it says was an unjust “tax”. Both companies removed Fortnite, a popular game made by Epic, from their respective app stores when the company tried to install its own payment mechanism within the apps that wouldn’t go through Apple.

In its lawsuit against Apple, Epic Games alleged Apple had become “what it once railed against”, citing the company’s legendary “1984” ad where Apple accused IBM of trying to drive Apple out of business. Apple was doing the same thing by denying Fortnite and Epic Games access to offer their products on the app store.

Now, it looks like Epic’s gambit – ie that more companies, including publishers who have been grumbling over the raw “Apple News” deal that many ended up pulling out of – has paid off. Because on Thursday afternoon, news broke about how a coalition of publishers are seeking to retain 15% more in subscription fees siphoned off by Apple as an additional tax for being displayed in the app store.

The Wall Street Journal, which is also owned by one of the company’s backing the complaint, broke the story.

In a letter to Apple Chief Executive Tim Cook on Thursday, a trade body representing the New York Times, the Washington Post, The Wall Street Journal and other publishers said the outlets are looking to qualify for improved deal terms to keep more money from digital subscriptions sold through Apple’s app store.

News publishers currently pay Apple 30% of the revenue from first-time subscriptions made through iOS apps; that commission is reduced to 15% after the subscriber’s first year.

“The terms of Apple’s unique marketplace greatly impact the ability to continue to invest in high-quality, trusted news and entertainment particularly in competition with other larger firms,” said the letter, which is signed by Jason Kint, chief executive of the trade body, Digital Content Next.

We now wait to see whether more groups will join the battle against Apple, as well as Alphabet’s “Google Play” app store.

via ZeroHedge News https://ift.tt/34vDM1Z Tyler Durden

Is the establishment panicking at the nomination of someone that dclearly thinks for herslf and refuses to accept as writ the groupthink of The Federal Reserve?

Judging by the wording of the following open-letter to The Senate urging Shelton be rejected, because her “views are so extreme and ill-considered as to be an unnecessary distraction from the tasks at hand,” and of course, the fact that she has not publicly disavowed the President as #OrangeManBad:

” She has advocated for a return to the gold standard; she has questioned the need for federal deposit insurance; she has even questioned the need for a central bank at all. Now, she appears to have jettisoned all of these positions to argue for subordination of the Fed’s policies to the White House – at least as long as the White House is occupied by a president who agrees with her political views. “

President Trump has nominated Judy Shelton to one of the vacancies on the Board of Governors of the Federal Reserve System. The nomination recently cleared the Senate Banking Committee and will soon reach the Senate floor. We urge the Senate to reject this nomination.

The undersigned all served on the staffs of either the Board of Governors or the Federal Reserve Banks. We have served in various capacities as economists, lawyers, bank supervisors, and in other professional capacities. We know and appreciate the unique position of the Federal Reserve in our nation’s economy and the need to preserve its nonpartisan approach to its many responsibilities.

The Federal Reserve is a vital part of our government and has been particularly important during our current crisis. The COVID-19 pandemic has required the suspension of much of the nation’s and the world’s economic activity. The Fed’s quick action to provide the markets with the necessary liquidity was crucial to restoring order to those markets and ensuring that the economic crisis that we are enduring did not become much, much worse. However, like the pandemic, the economic challenges persist.

Ms. Shelton has a decades-long record of writings and statements that call into question her fitness for a spot on the Fed’s Board of Governors. She has advocated for a return to the gold standard; she has questioned the need for federal deposit insurance; she has even questioned the need for a central bank at all. Now, she appears to have jettisoned all of these positions to argue for subordination of the Fed’s policies to the White House — at least as long as the White House is occupied by a president who agrees with her political views.

The Fed has serious work ahead of it. While we applaud the Board having a diversity of viewpoints represented at its table, Ms. Shelton’s views are so extreme and ill-considered as to be an unnecessary distraction from the tasks at hand.

The late Chairman Paul Volcker was noted for advising new governors that “when you enter this building, you leave your politics at the door.” Sound advice that, from her record, Ms. Shelton is incapable of following.

We urge the Senate to reject her nomination.

The signatories are mostly lawyers…

In an attempt to provide some balance, here is The Mises Institute’s Robert Aro explaining the reason why the establishment hates Judy Shelton…

Imagine if a member of the Federal Reserve’s Board of Governors said the following :

“When governments manipulate exchange rates to affect currency markets, they undermine the honest efforts of countries that wish to compete fairly in the global marketplace. Supply and demand are distorted by artificial prices conveyed through contrived exchange rates.

Or something honest like:

“The Fed should focus on stable money as a key factor in economic performance. Given that central banks today are the world’s biggest currency manipulators, it’s imperative that the next chairman prioritize the integrity of the dollar.”

And what if they showed an understanding of both history and sound money principles with something intelligent:

“For all the talk of a “rules-based” system for international trade, there are no rules when it comes to ensuring a level monetary playing field. The classical gold standard established an international benchmark for currency values, consistent with free-trade principles.

While she’s not a governor yet, the quotes were from Trump’s appointee Judy Shelton, approved this week by the Senate banking committee on party line at a vote of 13-12. To be nominated to the board of directors, Ms. Shelton will now be put forward to be voted on by the full senate, 53 of the 100 being Republicans.

Yet below, we can see everything wrong with the Mainstream Media (MSM), mainstream economists, and American politics starting with theNew York Times article entitled, God Help Us if Judy Shelton Joins the Fed. Former counselor to the Treasury secretary during the Obama administration, Steven Rattner began with :

Trump’s latest unqualified nominee to the Federal Reserve Board must be rejected.

The defaming article shows Mr. Rattner has no care nor understanding of economics. According to him, Ms. Shelton is known for taking “long-discredited positions in the monetary system,” referring to the gold standard, as he claims it was the “culprit in deepening the Great Depression.” Clearly he is no fan of (or perhaps isn’t educated enough to have heard of) Mises or Rothbard.

In what some may described as laudable on Ms. Shelton’s behalf, Mr. Rattner, fueled by ignorance, continues:

Among other heretical stances, she has supported the abolition of the Federal Reserve itself, putting her in a position to undermine the very institution she is being nominated to serve.

A similar tone was found in the National Review, a magazine which defines itself using the highly nebulous and ill-defined “modern conservative movement.” Going back several months the “controversy” surrounding Judy Shelton was shared in an oxymoronic write-up called: The Wrong Kind of ‘Intellectual Diversity’ at the Fed. It is nothing more than a rant showing the senior editor also knows little about history or economics, but being in a position to publish, does so with a vociferous opinion. He begins with the usual appeal to popularity:

First, she has been a single-minded advocate of a policy that most economists rightly reject: the revival of the gold standard.

What is popular is not always true, especially regarding economics. The article cites quotes from 2009 to the Wall Street Journal in an attempt to discredit her by showing she has not always been consistent in her stances over the span of the past decade. By contrast, the rant implies all other members of the Fed and economists have.

Unfortunately, some people claim to like diversity, but not when it’s different from their own bias. The senior editor who wrote the hit piece can be found on twitter.

Unlike the New York Times and National Review, surprising as it may seem, CNBC’s position was more neutral when discussing the senate hearing, noting :

She faced persistent and at-times hostile questions about her support for the gold standard, her beliefs on whether bank deposits should be insured and whether the Fed should be independent of political influences.

Last but not least, the Wall Street Journal wrote it best , much to the chagrin of its rivals:

the news write-ups inevitably described her with adjectives like “controversial.” She should take it as a badge of honor, given how she would provide needed intellectual diversity at the Fed.

Only in a world this backwards where, in a supposed free country, socialism is considered good and capitalism bad that Shelton could receive so much scorn. To think, 1 out of 7 members of the board could have ideas other than inflationist dogma but they would be shunned for speaking up, says a lot of the society in which we are living. Perhaps the real reason is, if appointed, it could set Judy Shelton in line to the position of Federal Reserve Chair?

Ironically enough, as long Congress stays partisan, we may see her in one of the most powerful central banking positions in the world. It won’t “End the Fed” overnight, but maybe it’s one step closer!

And finally, as Mark Hendrickson concludes, Shelton is 100 percent correct when she questions why a dozen people (the Federal Reserve Board of Governors) should set the prices of capital (interest rates) any more than they should set the price of cars, houses, or bubble gum.

Markets can do that and do it better – as they did before there even was a Federal Reserve system. Shelton opposes policies that would be more at home in a centrally planned economy. That alone is reason enough to confirm her.

via ZeroHedge News https://ift.tt/2YjygLM Tyler Durden