Among the criticisms of the deployment of Customs and Border Protection (CBP) officers to Portland is that CBP is one of the more problem-ridden federal law enforcement agencies.

CBP, the nation’s largest civilian law enforcement agency with roughly 60,000 employees, has higher termination rates than other federal law enforcement agencies, lower recruiting standards, longstanding corruption problems, and a well-documented toxic culture.

Here’s another small but notable data point:

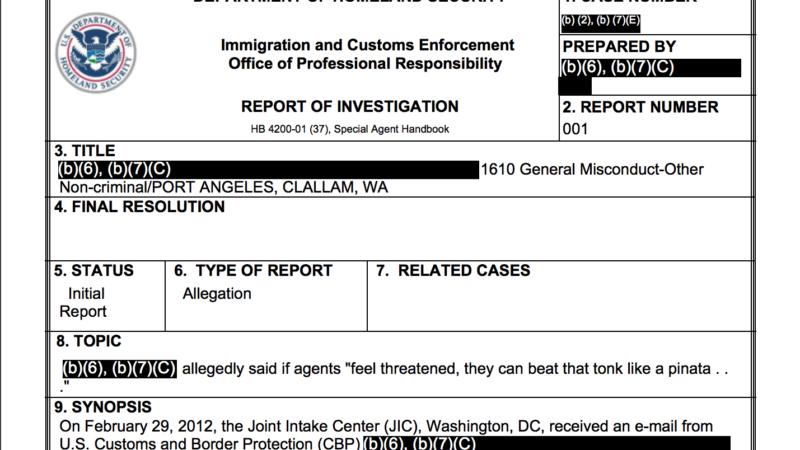

A CBP official was referred to internal affairs investigators for allegedly telling a room full of supervisors in 2012 that if Border Patrol agents feel threatened by a migrant, they should “beat that tonk like a piñata until candy comes out.”

A CBP use-of-force instructor emailed the Immigration and Customs Enforcement Office of Professional Responsibility (OPR), which handles internal affairs for CBP, on Feb. 29, 2012, to report the potential misconduct. The complaint generated an OPR investigation report, recently obtained by Reason through a Freedom of Information Act (FOIA) request.

The instructor wrote that at a supervisors meeting the official, whose name was redacted, said during a discussion on assaults against Border Patrol agents, “you tell all the guys that if they feel threatened, they can beat that tonk like a piñata until candy comes out.”

“Tonk” (sometimes spelled “tonc”) is a slang CBP term for a migrant. It allegedly refers to the sound of hitting someone on the head with a flashlight, although some Border Patrol defenders claim it is an acronym for “Territory of Origin Not Known.”

Last year, federal court records showed that a Border Patrol agent in Nogales, Texas, accused of hitting a Guatemalan migrant with his truck frequently used the word “tonk,” among other descriptors like “mindless murdering savages” and “disgusting subhuman shit unworthy of being kindling for a fire.” The agent, Matthew Bowen, was sentenced to probation for deprivation of rights under color of law.

Rolling Stone, in a story about the case against Bowen, described the history of the term:

A federal court case from 2004, which also centered on accusations of excessive force by the Border Patrol, includes an agent’s definition of “tonk” as “the sound heard when a ‘wetback’ is hit over the head with a flashlight.” Josiah Heyman is the chair of the anthropology department at the University of Texas, El Paso. In research on the border, he’s heard Border Patrol agents use the term “tonk” since the early 1990s. “That’s their position in the hierarchy,” he says of undocumented migrants in relation to Border Patrol agents. “They’re hittable people.”

The word also popped up in a secret Border Patrol Facebook group, unearthed by ProPublica, that was full of jokes about migrant deaths and vulgar, sexual memes about Rep. Alexandria Ocasio-Cortez (D–N.Y.). CBP announced earlier this month that four Border Patrol agents had been fired over their posts on the Facebook group.

A CBP spokesperson toldMother Jones last year that, “there is no clear answer on where the term originated or if it was once considered an acronym, but flatly, it is now considered a derogatory term and CBP does not condone its use.”

But the complaint against the CBP official wasn’t concerned with the word so much as his encouraging illegal and excessive force against migrants.

“I, being a use of force instructor, told him that I didn’t believe that that was within the use of force policy, and I cited the use of force continuum in an attempt to clarify the issue,” the instructor’s email to OPR said. “I told him that there are indicators that can help determine if someone will become assaultive, like the thousand yard stare, but that in itself does not meet the criteria for aggressive assaultive behavior. He told me that it did and, within the confines of the supervisor meeting taking place, I relented to keep the meeting moving.”

“I believe that his statement undermines the use of force policy,” the instructor continued, “and could lead our agents into possible litigation if it is his wish that we preach this philosophy to the agents.”

Reason filed the FOIA request to see if any CBP internal investigations had ever mentioned the term. (Silly me, I requested internal affairs records between 2012 and 2019, but CBP didn’t even have an internal affairs department until 2014—11 years after it was established.)

The OPR report does not say how the case was resolved, or whether the CBP official was disciplined. CBP’s public affairs office did not immediately respond to a request for comment.

from Latest – Reason.com https://ift.tt/39CpGfm

via IFTTT

Kris Kobach, the former Kansas secretary of state, is seeking the GOP nomination to replace retiring Republican Pat Roberts in this year’s race for Roberts’ U.S. Senate seat. And he has to thank for his campaign’s viability an $850,000 investment from controversial tech billionaire Peter Thiel.

“I think the money that that super PAC is putting into the race—primarily through this one rich guy—is absolutely the lifeblood of the pro-Kobach campaign at this moment,” Patrick Miller, a political scientist at the University of Kansas, told Recode. “You take that money away and Kobach doesn’t have a lot of campaign left.”

That Thiel—often identified, including by himself, as a libertarian—is dedicating himself to a candidate whose primary obsession is immigration restriction is a further sign of the tumultuous swirl of hypernationalism pushed by and surrounding Thiel (and discussed at length in a story in the August/September issue of Reason, now available online to subscribers).

Unnamed friends of Thiel tell Recode that Thiel “has a really strong preference for people who stick their middle finger up to the status quo and conventional wisdom. There is nobody who I think was more obviously sticking his middle finger up at conventional wisdom quite like Kris Kobach.”

Thiel’s interest in Kobach is likely rooted in the same reasons he was enthusiastic about Trump. Kobach was one of the minds behind Trump’s Muslim registry and his unrepentant anti-immigration views mark him as perhaps Trumpier than Trump. (Kobach believes COVID-19 death numbers are being manipulated up to harm the president, for one.) Trump endorsed Kobach in his failed attempt to become governor of Kansas in 2018, and Thiel began funding Kobach during that race. Fellow disillusioned Trump superfan and immigration-hater Ann Coulter co-hosted a Kobach fundraiser in Thiel’s New York apartment.

Recode reports that Thiel has “cut at least three successive checks to [a pro-Kobach PAC called Free Forever], the most recent for a half-million dollars last month.” The PAC has “spent more than four times what Kobach’s campaign itself has spent on television and radio ads…The heavy amount of mailers sent by the PAC have run the gamut of attacking [Republican challenger Roger] Marshall as ‘anti-American’ for being insufficiently tough on immigration, alleging that he voted to fund ‘Rosie O’Donnell summer camp,’ ‘global warming musicals,’ and ‘transgender plays,’ and promising that Kobach will ‘stop the next Ruth Bader Ginsburg.'”

Thiel’s other candidate donations this year are going to another super immigration hawk, and advocate of sending in federal troops to quell protesters, Arkansas Sen. Tom Cotton.

Kobach is also one of the leading voices claiming American elections are rife with fraud and had his attempt to fight it when he was Kansas’ secretary of state overturned in 2018 by a federal judge who questioned the reality of the problem Kobach was allegedly solving.

Among the criticisms of the deployment of Customs and Border Protection (CBP) officers to Portland is that CBP is one of the more problem-ridden federal law enforcement agencies.

CBP, the nation’s largest civilian law enforcement agency with roughly 60,000 employees, has higher termination rates than other federal law enforcement agencies, lower recruiting standards, longstanding corruption problems, and a well-documented toxic culture.

Here’s another small but notable data point:

A CBP official was referred to internal affairs investigators for allegedly telling a room full of supervisors in 2012 that if Border Patrol agents feel threatened by a migrant, they should “beat that tonk like a piñata until candy comes out.”

A CBP use-of-force instructor emailed the Immigration and Customs Enforcement Office of Professional Responsibility (OPR), which handles internal affairs for CBP, on Feb. 29, 2012, to report the potential misconduct. The complaint generated an OPR investigation report, recently obtained by Reason through a Freedom of Information Act (FOIA) request.

The instructor wrote that at a supervisors meeting the official, whose name was redacted, said during a discussion on assaults against Border Patrol agents, “you tell all the guys that if they feel threatened, they can beat that tonk like a piñata until candy comes out.”

“Tonk” (sometimes spelled “tonc”) is a slang CBP term for a migrant. It allegedly refers to the sound of hitting someone on the head with a flashlight, although some Border Patrol defenders claim it is an acronym for “Territory of Origin Not Known.”

Last year, federal court records showed that a Border Patrol agent in Nogales, Texas, accused of hitting a Guatemalan migrant with his truck frequently used the word “tonk,” among other descriptors like “mindless murdering savages” and “disgusting subhuman shit unworthy of being kindling for a fire.” The agent, Matthew Bowen, was sentenced to probation for deprivation of rights under color of law.

Rolling Stone, in a story about the case against Bowen, described the history of the term:

A federal court case from 2004, which also centered on accusations of excessive force by the Border Patrol, includes an agent’s definition of “tonk” as “the sound heard when a ‘wetback’ is hit over the head with a flashlight.” Josiah Heyman is the chair of the anthropology department at the University of Texas, El Paso. In research on the border, he’s heard Border Patrol agents use the term “tonk” since the early 1990s. “That’s their position in the hierarchy,” he says of undocumented migrants in relation to Border Patrol agents. “They’re hittable people.”

The word also popped up in a secret Border Patrol Facebook group, unearthed by ProPublica, that was full of jokes about migrant deaths and vulgar, sexual memes about Rep. Alexandria Ocasio-Cortez (D–N.Y.). CBP announced earlier this month that four Border Patrol agents had been fired over their posts on the Facebook group.

A CBP spokesperson toldMother Jones last year that, “there is no clear answer on where the term originated or if it was once considered an acronym, but flatly, it is now considered a derogatory term and CBP does not condone its use.”

But the complaint against the CBP official wasn’t concerned with the word so much as his encouraging illegal and excessive force against migrants.

“I, being a use of force instructor, told him that I didn’t believe that that was within the use of force policy, and I cited the use of force continuum in an attempt to clarify the issue,” the instructor’s email to OPR said. “I told him that there are indicators that can help determine if someone will become assaultive, like the thousand yard stare, but that in itself does not meet the criteria for aggressive assaultive behavior. He told me that it did and, within the confines of the supervisor meeting taking place, I relented to keep the meeting moving.”

“I believe that his statement undermines the use of force policy,” the instructor continued, “and could lead our agents into possible litigation if it is his wish that we preach this philosophy to the agents.”

Reason filed the FOIA request to see if any CBP internal investigations had ever mentioned the term. (Silly me, I requested internal affairs records between 2012 and 2019, but CBP didn’t even have an internal affairs department until 2014—11 years after it was established.)

The OPR report does not say how the case was resolved, or whether the CBP official was disciplined. CBP’s public affairs office did not immediately respond to a request for comment.

from Latest – Reason.com https://ift.tt/39CpGfm

via IFTTT

Kris Kobach, the former Kansas secretary of state, is seeking the GOP nomination to replace retiring Republican Pat Roberts in this year’s race for Roberts’ U.S. Senate seat. And he has to thank for his campaign’s viability an $850,000 investment from controversial tech billionaire Peter Thiel.

“I think the money that that super PAC is putting into the race—primarily through this one rich guy—is absolutely the lifeblood of the pro-Kobach campaign at this moment,” Patrick Miller, a political scientist at the University of Kansas, told Recode. “You take that money away and Kobach doesn’t have a lot of campaign left.”

That Thiel—often identified, including by himself, as a libertarian—is dedicating himself to a candidate whose primary obsession is immigration restriction is a further sign of the tumultuous swirl of hypernationalism pushed by and surrounding Thiel (and discussed at length in a story in the August/September issue of Reason, now available online to subscribers).

Unnamed friends of Thiel tell Recode that Thiel “has a really strong preference for people who stick their middle finger up to the status quo and conventional wisdom. There is nobody who I think was more obviously sticking his middle finger up at conventional wisdom quite like Kris Kobach.”

Thiel’s interest in Kobach is likely rooted in the same reasons he was enthusiastic about Trump. Kobach was one of the minds behind Trump’s Muslim registry and his unrepentant anti-immigration views mark him as perhaps Trumpier than Trump. (Kobach believes COVID-19 death numbers are being manipulated up to harm the president, for one.) Trump endorsed Kobach in his failed attempt to become governor of Kansas in 2018, and Thiel began funding Kobach during that race. Fellow disillusioned Trump superfan and immigration-hater Ann Coulter co-hosted a Kobach fundraiser in Thiel’s New York apartment.

Recode reports that Thiel has “cut at least three successive checks to [a pro-Kobach PAC called Free Forever], the most recent for a half-million dollars last month.” The PAC has “spent more than four times what Kobach’s campaign itself has spent on television and radio ads…The heavy amount of mailers sent by the PAC have run the gamut of attacking [Republican challenger Roger] Marshall as ‘anti-American’ for being insufficiently tough on immigration, alleging that he voted to fund ‘Rosie O’Donnell summer camp,’ ‘global warming musicals,’ and ‘transgender plays,’ and promising that Kobach will ‘stop the next Ruth Bader Ginsburg.'”

Thiel’s other candidate donations this year are going to another super immigration hawk, and advocate of sending in federal troops to quell protesters, Arkansas Sen. Tom Cotton.

Kobach is also one of the leading voices claiming American elections are rife with fraud and had his attempt to fight it when he was Kansas’ secretary of state overturned in 2018 by a federal judge who questioned the reality of the problem Kobach was allegedly solving.

Goldman Warns “Real Concerns Are Emerging” About The Dollar As Reserve Currency; Goes “All In” Gold Tyler Durden

Tue, 07/28/2020 – 11:28

In his morning critique of goldbugs’ resurgent optimism about the future of gold, which has exploded alongside the price of precious metals, which in turn have been tracking the real 10Y rate tick for tick…

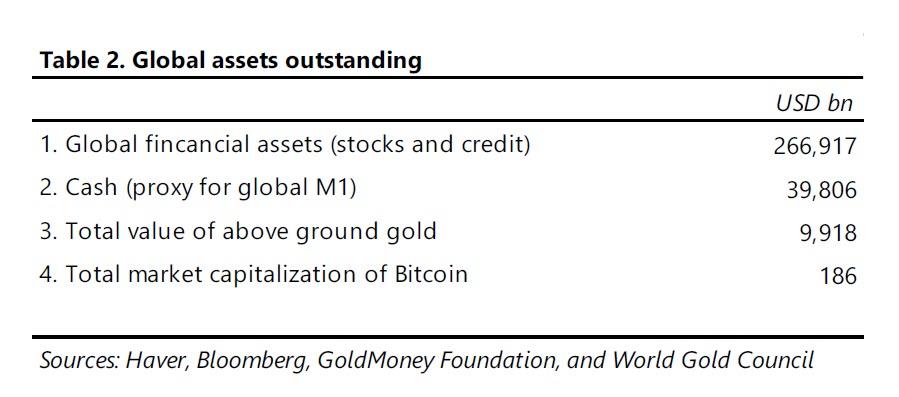

… Rabobank’s Michael Every argued from the familiar position of one who views the modern monetary system as immutable, and bounded by the “Venn Diagram” confines of the dollar as a reserve currency and financial assets as a bedrock of modern household wealth, of which as Paul Tudor Jones recently calculated, there is just over $300 trillion worth, compared to just $10 trillion in total gold value.

Indeed, according to Every, the surge in gold is meaningless because “if you buy gold, technically that is going to make you money. And yet that money is still going to be priced in US DOLLARS – and that gives the whole game away.”

Like fans of the England football team, gold fans can dream of the distant past when gold was the centre of the global monetary system; but they can keep dreaming if they think those days are ever going to return. Gold may be an appreciating asset, but all the evidence suggests that it won’t be one that is of any direct relevance to day-to-day life, finance, and business. Your currency won’t be tied to it. You won’t get paid in it. You won’t spend in it or save in it (other than to the switch back to US Dollars). You won’t be doing deals in it or importing in it.”

Yes but… what if your currency ends up getting tied to it? What if you do get paid in gold? What if you save in gold without any intention of switching back to dollars?

In short, what if the dollar is no longer the world’s reserve currency?

Impossible you say… well, we would disagree. After all, in a world where there is over $100 trillion in dollar-denominated debt which can not be defaulted on and thus must be inflated away, the “exorbitant privilege” of the dollar has become a handicap. But don’t take our word: here is Jared Bernstein, Obama’s former chief economist warning all the way back in 2014 in a NYT op-ed that the US Dollar must lose its reserve status:

There are few truisms about the world economy, but for decades, one has been the role of the United States dollar as the world’s reserve currency. It’s a core principle of American economic policy. After all, who wouldn’t want their currency to be the one that foreign banks and governments want to hold in reserve?

But new research reveals that what was once a privilege is now a burden, undermining job growth, pumping up budget and trade deficits and inflating financial bubbles. To get the American economy on track, the government needs to drop its commitment to maintaining the dollar’s reserve-currency status.

Agree or disagree with Bernstein’s ideology, never has his assessment about the state of the American economy been more accurate than it is now.

To be sure, since then there have been a handful of other “serious” economists suggesting that the only way the US economy can “reboot” itself and reset its economic engine is for the dollar to lose its currency status, but it is only in the past few days – when the dollar plunged and gold soared to new all time highs – that we have seen a barrage of Wall Street reports contemplating what until recently was viewed as impossible: a world where the dollar is not the reserve currency.

Meanwhile, after its explosive burst higher in March and April, the Bloomberg Dollar Spot Index is on course for its worst July in a decade. The drop comes amid renewed calls for the dollar’s demise following a game-changing rescue package from the European Union deal, which spurred the euro and will lead to jointly-issued debt.

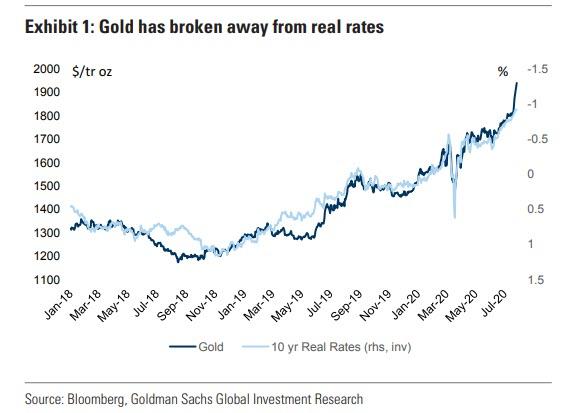

Which brings us to this morning, when none other than the world’s most influential investment bank Goldman Sachs, by way of its chief commodity strategist Jeffrey Currie, wrote that “real concerns around the longevity of the US dollar as a reserve currency have started to emerge.”

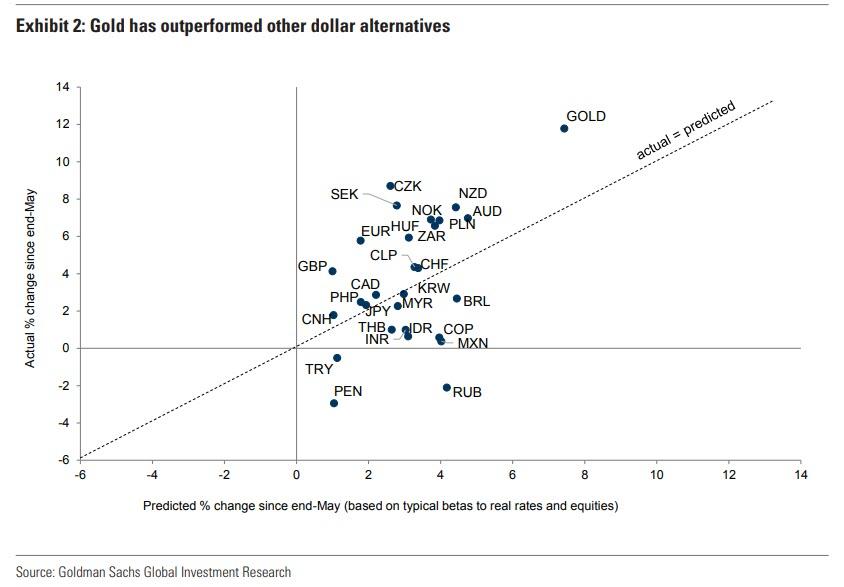

Specifically, Goldman looks at the recent surge in gold prices to new all-time highs which has “substantially outpaced both the rise in real rates…

… and other US dollar alternatives, like the Euro, Yen and Swiss Franc”…

… with Currie writing that he believes this disconnect “is being driven by a potential shift in the US Fed towards an inflationary bias against a backdrop of rising geopolitical tensions, elevated US domestic political and social uncertainty, and a growing second wave of covid-19 related infections.”

This, combined with the record level of debt accumulation by the US government, means that “real concerns around the longevity of the US dollar as a reserve currency have started to emerge.”

Then, Currie reminds his clients that he has “long maintained gold is the currency of last resort, particularly in an environment like the current one where governments are debasing their fiat currencies and pushing real interest rates to all-time lows, with the US 10-year TIPs at -92bp is 5bp below the 2012 lows,” and we indeed noted Currie’s reco to buy gold one day after the Fed went all-in on March 24.

Four months later, the urgency is even greater, and Currie writes that “with more downside expected in US real interest rates we are once again reiterating our long gold recommendation from March and are raising our 12-month gold and silver price forecasts to $2300/toz and $30/toz respectively from $2000/toz and $22/toz.”

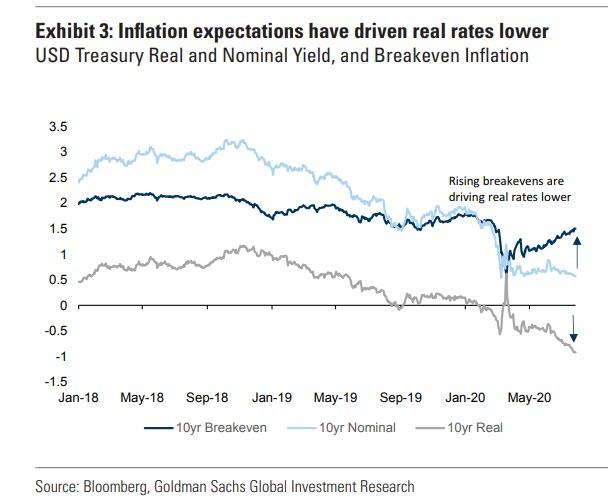

There are other reasons why Goldman believes that Gold’s surge is only just starting: “This relentless decline in real interest rates against nominal rates bounded by the US Fed has caused inflation breakevens to rise (see Exhibit 3) in an environment that would ordinarily be viewed as deflationary, i.e. a weakening US labor market as the country re-enters lockdown.”

This is bad, and is usually described by what may be the most loathed word in the banker lexicon: “stagflation.”

Which also explains the “irony” of the response: the greater the deflationary concerns that policymakers must fight today, the greater the debt build up and the higher the inflationary risks are in the future according to Currie, who expands further on this critical topic:

The deflationary shock caused by the pandemic drives the need to expand balance sheets to support demand today, as seen in the latest US $1.0 trillion Phase 4 stimulus and the €750 billion pan-EU recovery fund. The resulting expanded balance sheets and vast money creation spurs debasement fears which, in turn, create a greater likelihood that at some time in the future, after economic activity has normalized, there will be incentives for central banks and governments to allow inflation to drift higher to reduce the accumulated debt burden.

Indeed, this has already been seen in recent FOMC minutes, as discussions of explicit outcome-based forward guidance raises the prospect for Fed-sanctioned overheating of the economy.

And despite the longer-term nature of these risks, Goldman argues that “asset managers have real concerns today about persistent unanticipated shifts in inflation that can create large discrepancies between current expected real returns and actual realized returns” and this is manifesting itself in the continued faith in the dollar.

What about the gold price? Here is Currie’s explanation why gold will continue to surge:

The key point from a hedging perspective is that asset managers care about the level of inflation, not the changes in inflation, and from a level perspective, inflation hedges like commodities and equities are likely far cheaper today than in the future when inflation could arrive. When discussing the drivers of investment demand for gold and commodities, it is important to distinguish between debasement and inflation. The key is that the current debasement and debt accumulation sows the seeds for future inflationary risks despite inflationary risks remaining low today. While debasement in many cases leads to inflation, it is not always the case as witnessed over the past decade. Equally, the best debasement hedge (gold) is not always the best hedge against inflation (oil). Indeed, the word debasement comes from adding base metals like tin or copper to the precious metals that acted as hard currency; therefore, owning the pure precious metal is then the best hedge against debasement.

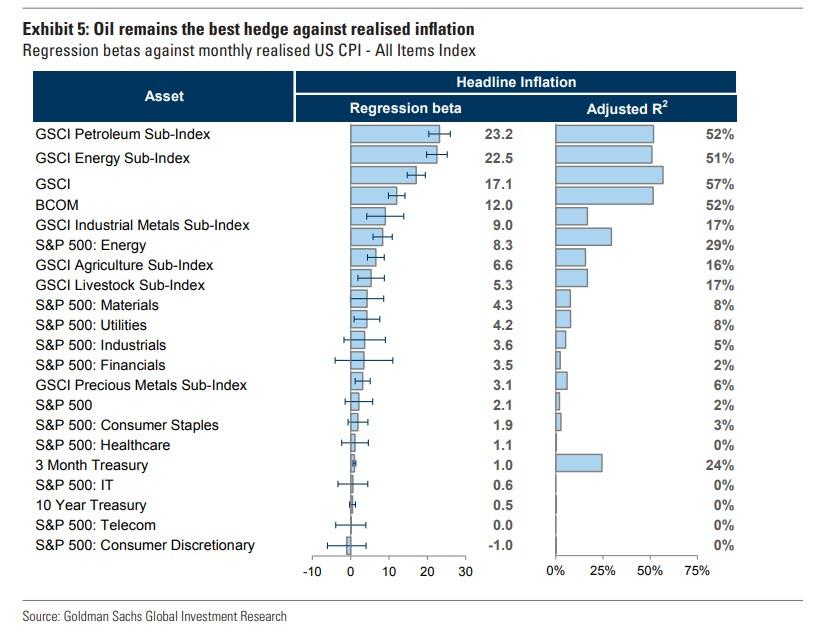

However, this does not mean gold is the best hedge against inflation — a common misconception of many investors. Gold doesn’t appear significantly in any CPI anywhere in the world. As a result, oil and other commodities that drive the items actually found in different CPIs are the best hedges against inflation. But

Next, Currie goes on to explain why oil may be the best pure play commodity hedge to inflation, “today the risk is from debasement of fiat currencies that sows the risk for inflation and gold is the best hedge against debasement. Further out as inflation risks rise, oil and equities hedge unexpected and expected inflation respectively better than gold (see Exhibit 5), and given the size of the bond portfolios built over the past decade that will need to be hedged against inflation risks, the sheer size of investment demand for commodities is likely to be massive, underscoring the need to act today. “

Hence, gold at $2,000 and soon… $3,000, $5,000 and much more. Indeed, even at $10,000/oz, the total value of gold would be just around $50 trillion, which is still orders of magnitude below the value of global financial assets that need to be hedged (and which according to Paul Tudor Jones is around $270 trillion).

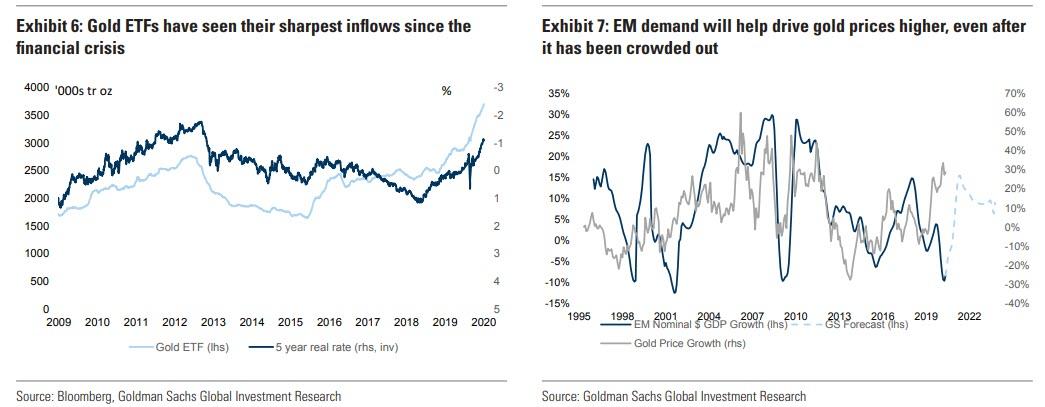

As Currie then notes, the result of this growing debasement risk is that “DM investment demand strength has continued with ETF additions in both Europe and US running high (see Exhibit 6). We see this trend persisting for some time as investment allocations into gold increase inline with allocations to inflation protected assets, similar to what happened after the financial crisis. Following the GFC, inflation fears peaked only at the end of 2011 as the bounce back in inflation ran out of steam, bringing the gold bull market to a halt. Similarly, we see inflationary concerns continuing to rise well into the economic recovery, sustaining hedging inflows into gold ETFs alongside the structural weakening of the dollar, we see gold being used as a dollar hedge by fund managers. Indeed, decomposing our gold forecast, with returns of 18% over the next 12 months, we estimate 9% of the growth is driven by 5yr real rates going to -2% over the next 12 month, (an est. elasticity of 0.1), while the second 9% comes from the 15% increase in the EM dollar GDP (an est. elasticity of 0.5) (see Exhibit 7).”

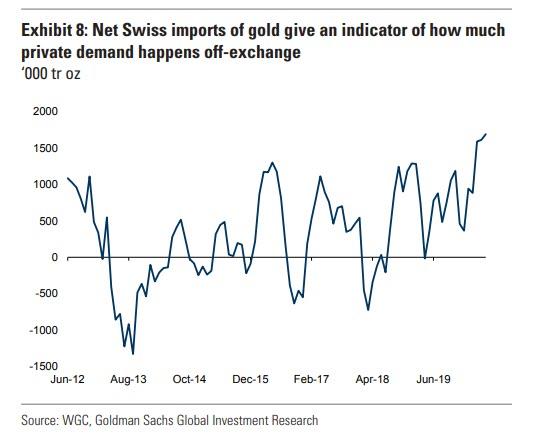

On top of these known flows, a large share of physical investment demand in gold is non-visible according to Goldman, in particular vaulted bar purchases by high net worth individuals. Looking at net Swiss imports one can see that gold stocks in Switzerland, where most of these private vaults are located, have been building at close to a record pace.

And in case that wasn’t enough, “the stretched valuations in equities, low real rates and high level of economic and political uncertainty all point toward continued inflows by high net worth individuals,” in Goldman’s view.

But wait there’s more, with Goldman singling out the potential of a fresh EM demand surge: Indian gold imports are still down 80% yoy in June and the Chinese gold premium is beginning to turn negative again (see Exhibit 9). More recently, however, the weakness in EM demand has been driven more by gold’s high price, as consumers cannot afford to buy gold products at those levels. However, EM currencies are no longer under pressure and India has begun to see the rupee strengthen over the past month. EM growth is also beginning to recover with EM activity entering positive YoY territory in June for the first time since January and our economists seeing the worst of

the EM outlook behind us (see Exhibit 10). EM retail investment demand is also boosted by easier monetary policy together with continued inflation driving EM real rates down. In India, policy rates fell below the YoY inflation rate for the first time since 2013.”

Taken together, and in light of the declining faith in the dollar as a reserve currency, Goldman believes that these factors create a perfect setup for a rebound in EM demand for gold similar to 2010-11:

We will likely see this demand materialize when price stabilizes somewhat and DM investment purchases slow down, creating more room for EM consumers. We feel that for now, investors should not be concerned by weak EM demand prints.

As a final point, Goldman also spared some love for silverbugs, raising its silver forecast to $30/toz on a 3/6/12 month horizon, “pulled upward by higher gold prices and better prospects for silver industrial demand, particularly in solar energy (c.15% of silver demand). Both the European Green Deal and Biden’s war on climate change plans imply a doubling every year of solar panel capacity installations in both the US and Europe. At the same time, silver demand in consumer electronics is benefiting from the transition to working from home as it is heavily used in consumer items such laptops, mobile phones and televisions. Even housing demand, where silver is used in light switches, looks to be better than expected with property sales in both US and China rebounding strongly. Silver has rallied almost 30% over the past few weeks but its ratio with gold is only back to its level at the beginning of this year of 80.”

Currie’s final point on silver:

Historically there has been a tight relationship between silver industrial demand and the gold-silver price ratio. If silver industrial demand next year is 5% higher versus its 2019 level, the gold-to-silver ratio would fall further to 77. Assuming this ratio, our $2300/toz gold target would imply a $30/toz silver price.

That sounds awfully familiar: oh yes, here’s why:

Average historical gold/silver ratio is 60. Means silver has to rise to $31 just to catch up to where it has been in the past. pic.twitter.com/3Lf5EQxFKy

As July comes to an end, should we be looking for a sellable rally to reduce risk? As addressed in “Fed Stimulus Has Created The Cobra Effect,” the failure of the market to “breakout” of the June highs raises our risk. To wit:

“With the late week sell-off, we have updated our risk/reward ranges below. Unfortunately, the market failed to hold its breakout, which keeps it within the defined trading range. The market did hold its rising bullish uptrend support trend line, which keeps the “bullish bias” to the market intact for now.

The ‘not-so-bullish’ aspect is that all four (4) of the primary buy/sell indicators have now tripped into “sell” territory. Such does not mean an imminent crash for the market. It does suggest upside is limited in the near term.”

A Rising Deviation

Yesterday, the markets rallied a bit on hopes for additional “stimulus” support from the Government as another $1 Trillion package is being bantered about. Given the broad differences between the Senate’s proposal and the House’s $3 Trillion packages, there is a substantial risk of failure of quick passage. Such could certainly roil markets near term.

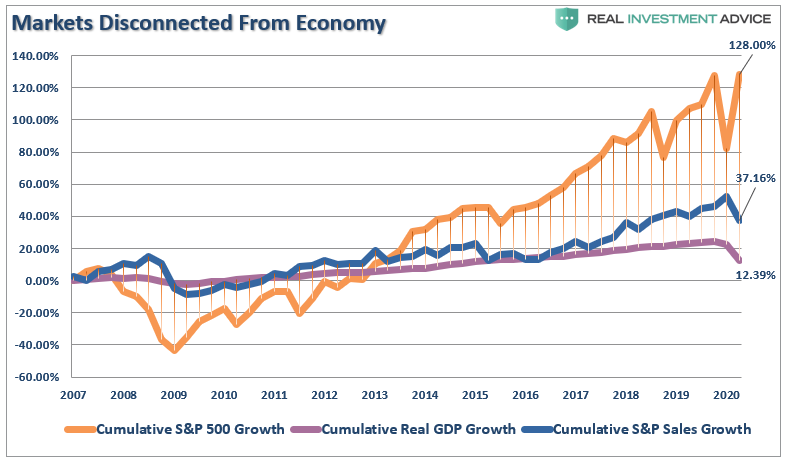

Furthermore, while the rally off the March lows has been substantial, there is still a vast disconnect between the markets and the underlying economic fundamentals. Given the divergence was driven by unprecedented monetary policy, the eventual reversion could be climatic.

Earlier this month, we discussed taking profits out of our most egregiously overbought technology stocks. As the end of July approaches, there are several reasons why we are looking for a “sellable rally” to reduce risk further.

Psychology:

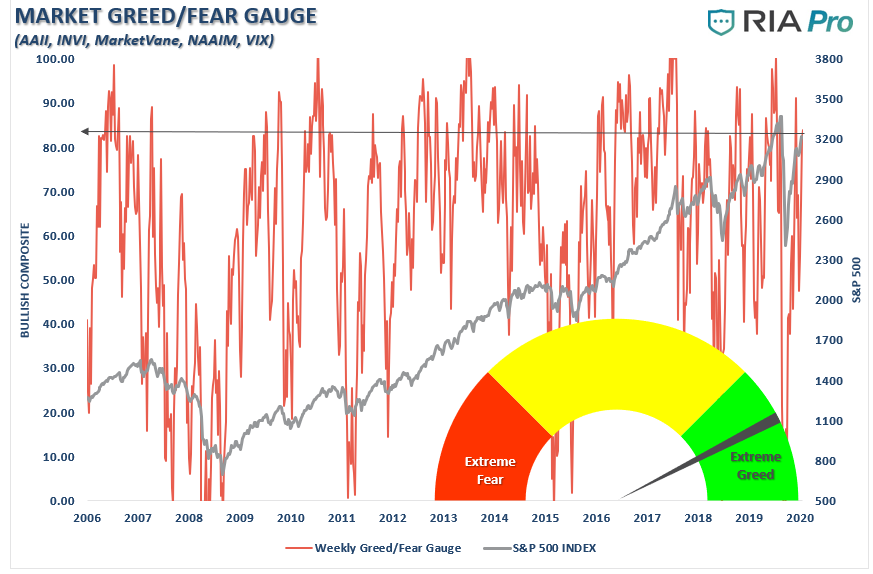

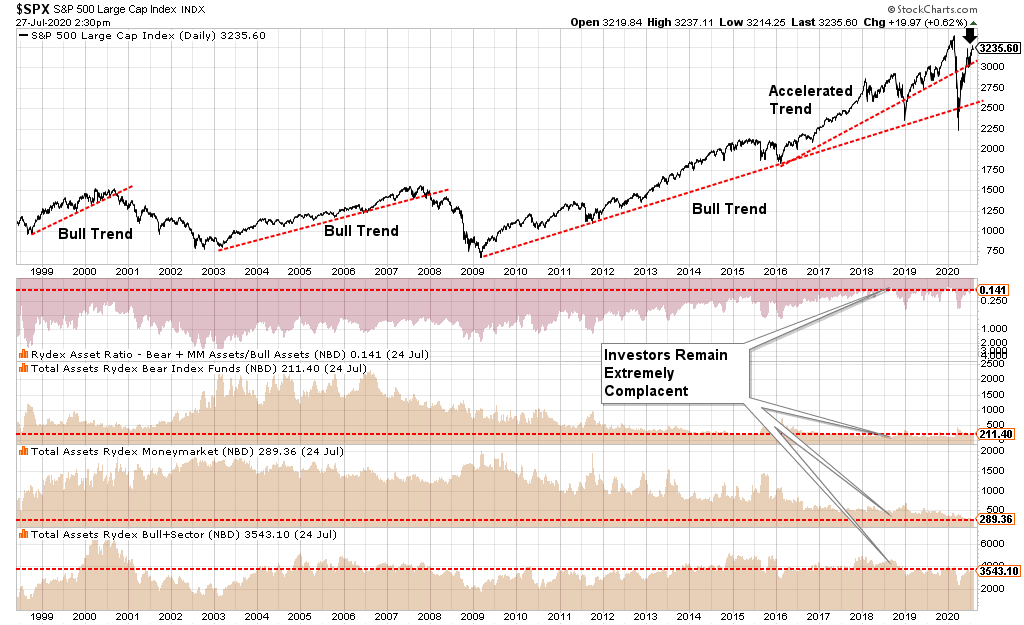

Despite the detachment of the market from the underlying fundamentals, investors have gotten much more “exuberant.” The RIAPro Greed/Fear Gauge (Subscribe for 30-days Risk-Free) is a function of how investors are “positioned” in the market. Currently, at 83.15, investors are very optimistic about future returns. Historically, levels of 80 and above have served as a “contrarian” indicator.

The same goes for positioning by looking at the Rydex bullish funds to bearish funds ratios. Despite the 35% plunge to March lows, investors remain bullishly biased in their positioning. Such suggests that investors remain aggressively positioned in equities, providing additional fuel for a market correction.

The current psychological conditions suggest a short-term top in the markets is likely. Importantly, none of the data suggests the next great “bear market” is upon us. However, in the short-term, it does suggest that downside risk may outweigh further upside reward currently.

Longer-term risks are more substantial.

Fundamental:

While “valuations” are a terrible market timing indicator and should not be used for such, they tell us just about future returns from investing. However, there are times, like now, where valuations can also tell us about the “rationalization” of investors to support an “overly bullish” bias.

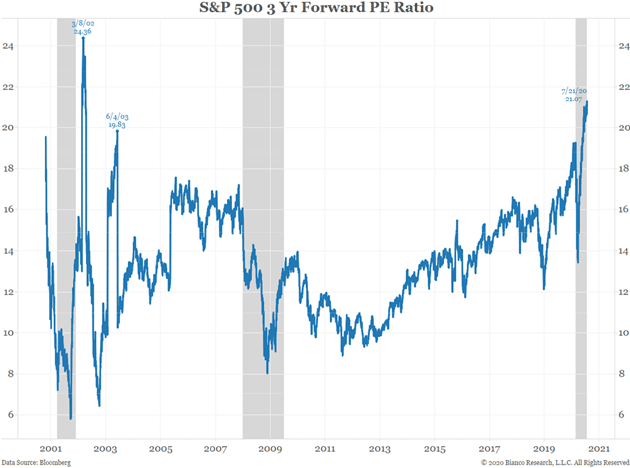

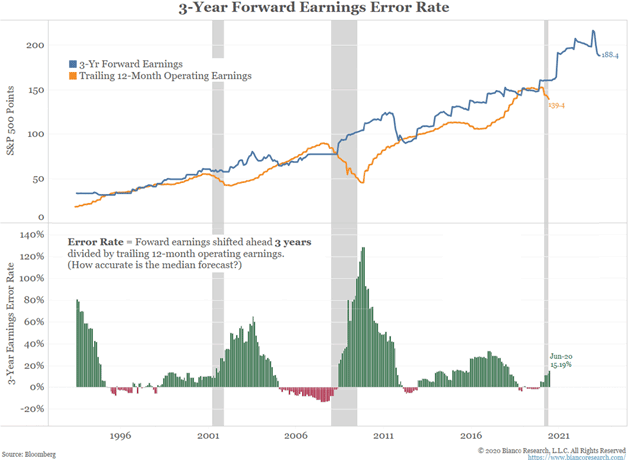

As Jim Bianco recently noted, investors are trying to rationalize paying excessive valuations for stocks today by using forward earnings estimates. The last time forward valuations were this expensive was at the peak of the “Dot.com” bubble.

Given that analysts are always overly optimistic about the future, we can assume that earnings will be worse than projected. Such means investors have vastly overpaid for ownership of equities, but to rationalize that ownership, they are now using estimates 3-years into the future.

Jim’s chart uses 3-year forward earnings estimates, which shows that stocks are not cheap regardless of the metric.

The problem, as I stated above, is that analysts are always overly optimistic. Such means that whatever rationalization you are using to buy stocks today thinking they are “cheap,” will wind up being very wrong tomorrow.

Valuations Matter A Lot

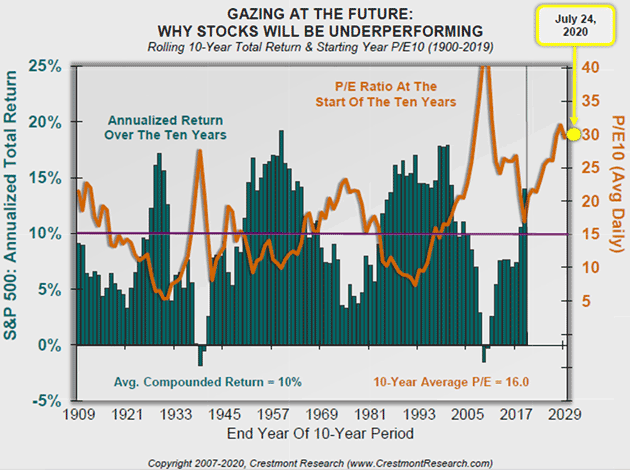

As John Mauldin noted recently:

“This chart overlays stock market performance and valuation. This chart (1) demonstrates the strong effect that valuation has on future returns, and (2) provides a gaze at the future for likely returns over the next 10-years!

The line in the chart is valuation, as measured by P/E. The bars in the chart reflect the 10-year total return for the S&P 500 Index. The line is shifted forward 10-years so the P/E aligns with each bar. That is the value for P/E at the start of the 10-years.

Peaks in the line correspond to troughs in 10-year returns. Similarly, dips in the line correspond with peaks in 10-year returns. Valuation matters!”

As stated above, while valuations are a terrible market timing indicator in the short-term, it tells you everything you need to know about returns long-term. Such is a lesson that young investors on “Robinhood” have yet to learn. Unfortunately, that lesson is taught always in the most brutal of fashions.

If history is a guide and always is, the valuation principles will remain true, and low single-digit returns will likely be the future.

Breadth

One of the big concerns we have had for some time has been the “lack of breadth” in the rally. As Bob Farrell once stated:

“Bull markets are strongest when broad and weakest when narrow.”

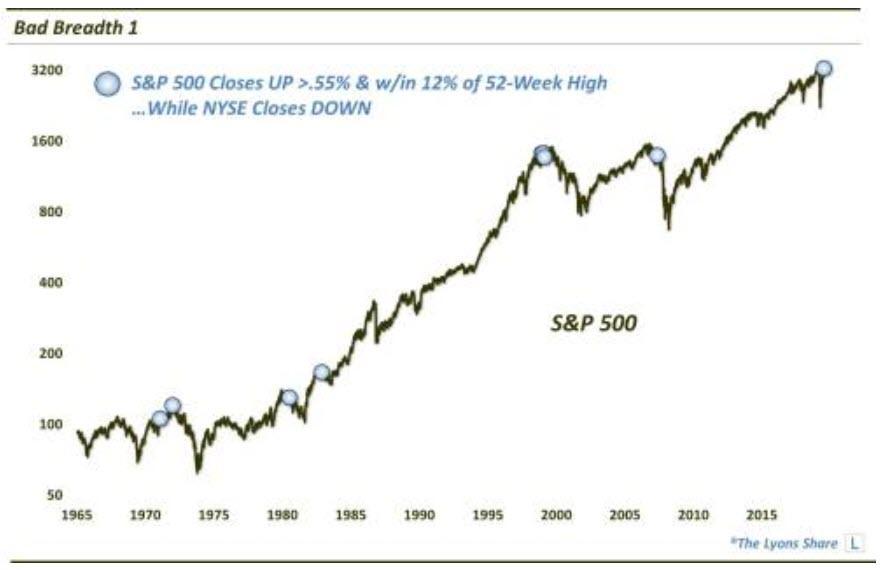

“Relaxing the parameters a bit, we dove a little deeper into the data and identified all days during that period that saw the SPX gain at least 0.55%, while within 12% of a 52-week high, when the NYSE closed down on the day. This chart shows all 9-such days in the past 55 years.”

Our friends at SentimenTrader also confirmed much the same yesterday:

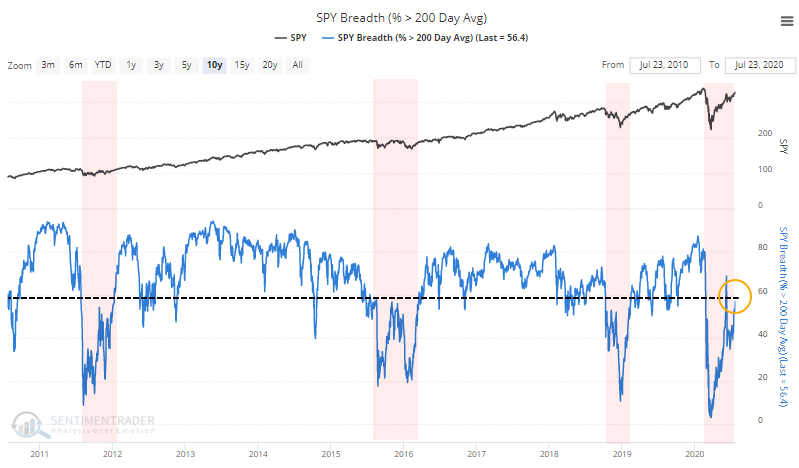

“Simply looking for prices above/below the 200-day moving average works just about as well as complex trend models, and it’s a good, clear-defined alternative. Combine that with a simple view of whether prices are making higher highs and higher lows (bull trend), lower highs and lower lows (bear trend), or both (neutral trend) and you can get an excellent sense for whether bulls or bears are in control. Those are mixed right now, with a slight edge to the bullish camp.

Healthy environments consistently see more than 60% of stocks, industries, sectors, and countries holding above their 200-day averages. Unhealthy environments consistently see fewer than 60% of these above their averages, and spikes above that level tend to get sold quickly.

That’s where we are now. In addition to a large number of stocks trailing the S&P by double-digits, fewer than 60% have held above their 200-day averages. When it spiked above 60% in June, selling pressure picked up immediately.”

Dumb Money Warning

Another clear warning has been that of retail investors.

“We’ve often noted that during times of unhealthy market environments, when fewer than 60% of stocks can hold above their 200-day averages, that periods of high optimism tend to lead to below-average forward returns.

We’re seeing that now, to a historic degree. Since we’ve been tracking this data, just over 20 years, there has never been a day when Dumb Money Confidence was at or above 80% while fewer than 60% of stocks in the S&P 500 were trading above their 200-day averages. Until now.” – SentimenTrader

When “bad breadth” collides with excessive “optimism,” you have all the ingredients for a short-term market reversal.

The only question is what will cause it?

Unfortunately, no one knows the answer. This is why we hedge risk to protect capital.

The Rules For A Sellable Rally

As SentimTrader went on to state:

“Helping to push this higher was recent record-setting option speculation. Even though some of the market’s leaders stumbled last week, the Options Speculation Index remains near a 20-year high. Plus, we have the added headwind of being in the most seasonally unfavorable period for stocks.”

I have spoken about the risk to markets over the next couple of months not only from seasonality, but also declining economic data, and a potential “s***-show” of a Presidential election.

With the market currently overbought, and on a short-term sell signal, it is likely a time to reduce risk somewhat until a better “setup” emerges.

Therefore, use rallies to:

Re-evaluate overall portfolio exposures. We will look to initially reduce overall equity allocations.

Use rallies to raise cash as needed. (Cash is a risk-free portfolio hedge)

Review all positions (Sell losers/trim winners)

Look for opportunities in other markets (The dollar is extremely oversold.)

Add hedges to portfolios

Trade opportunistically (There are always rotations which can be taken advantage of)

Drastically tighten up stop losses. (We had previously given stop losses a bit of leeway as long as the bull market trend was intact. Such is no longer the case.)

The Risk Of Ignoring Risk

There remains an ongoing bullish bias that continues to support the market near-term. Bull markets built on “momentum” are very hard to kill. Warning signs can last longer than logic would predict. The risk comes when investors begin to “discount” the warnings and assume they are wrong.

It is usually just about then the inevitable correction occurs. Such is the inherent risk of ignoring risk.

In reality, there is little to lose by paying attention to “risk.”

If the warning signs do prove incorrect, it is a simple process to remove hedges, and reallocate back to equity risk accordingly.

However, if these warning signs do come to fruition, then a more conservative stance in portfolios will protect capital in the short-term. A reduction in volatility allows for a logical approach to making further adjustments as the correction becomes more apparent. (The goal is not to be forced into a “panic selling” situation.)

It also allows you the opportunity to follow the “Golden Investment Rule:”

“Buy low and sell high.”

So, now you know why we are looking for a “sellable rally.

via ZeroHedge News https://ift.tt/32YVPwB Tyler Durden

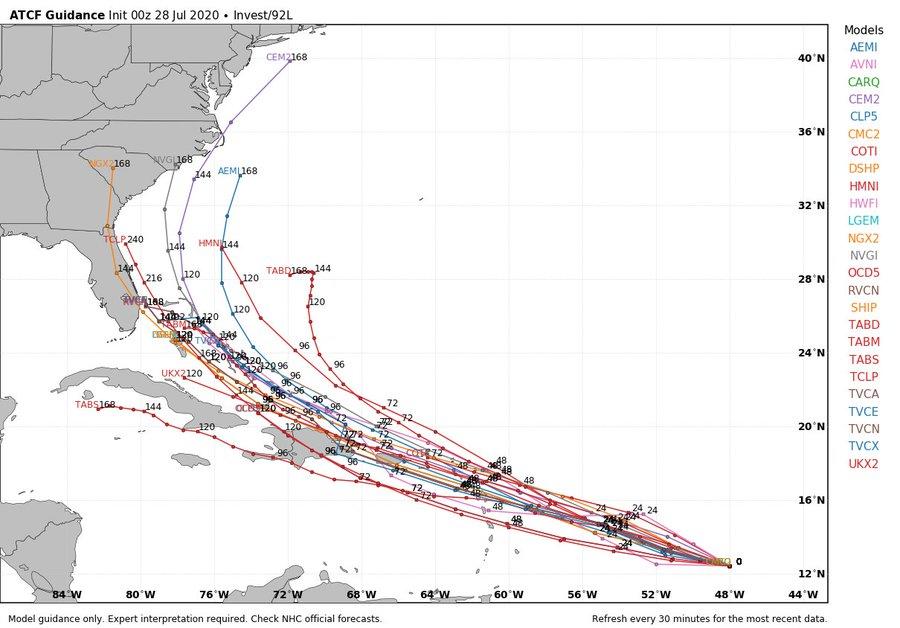

Another Tropical System Could Be Named Wednesday Tyler Durden

Tue, 07/28/2020 – 10:50

Another system swirling in the tropics could become the next Atlantic tropical storm, it would be named Isaias, and naming could happen as soon as late Wednesday or Thursday.

The disturbance is an area of low pressure located approximately 750 miles east of the Windward Islands, reported NBC Miami. The system is expected to organize in the next 24-48 hours.

Dubbed 92L, the system is moving west 15-20 mph, which suggest it will arrive in warm Caribbean waters by Wednesday afternoon.

The National Hurricane Center (NHC) said the system has a high probability of forming into a tropical depression or tropical storm in the next few days.

The intensity and how the storm will develop is still in question, though spaghetti models suggest if the storm strengthens, it could track near the Bahamas.

While track forecasts via computer models are preliminary – this is a weather disturbance to watch this week.

via ZeroHedge News https://ift.tt/306x6Vd Tyler Durden

Mainstream media is continually wrong about the relationship between gold and the dollar.

Another example came up today in the as the Wall Street Journal discusses the “traditional relationship” between gold and the dollar in Gold Prices Hit Record as Dollar Drops.

The number of errors in the article is staggering.

“You’re seeing money slipping out of the stock market or out of other assets and just eking into gold,” said David Govett, head of precious metals at commodities brokerage Marex Spectron.

“Gold’s traditional inverse relationship with the dollar had frayed this year, as both assets benefited from haven buying during the pandemic,” said WSJ author Joe Wallace.

“So far, a burst of buying by investors has more than offset the dearth of jewelry demand.”

Myth 1: Money Slipping Away

Money does not “slip away”. It is impossible for money to flow out of stocks into gold or bonds or from bonds to stocks or any other combination.

An individual can choose to dump stocks for gold but in aggregate, for every buyer there is a seller so there is no net flow. Rather there are repricing events.

Here’s another example. A “For Sale” sign on one house in a neighborhood can impact the price of every home, even before a sale is made. There is no flow, but the houses were all repriced.

Myth 2: Inverse Relationship

Gold does not have a traditional inverse relationship with the dollar. This subject came up today in a pair of Tweets.

These MSM idiots attributing gold’s move to the dollar’s decline are either stupid or have their head in the sand. Since late 2018 gold has run from $1200 to $1927 – in late 2018 the USD index was at 95, now it’s at 93. The MSM dollar narrative is bullshit…here:

“With the US dollar right where it is now, gold has been at $450, $380, $1080, and $1480.”

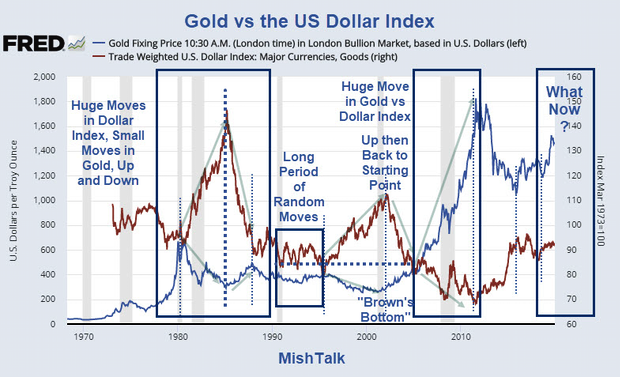

Gold vs US Dollar Index July 27, 2020

The lead chart reflects the price of gold vs the US dollar index on July 27.

The horizontal dashed line is the US dollar index at 93.7, When the solid blue line touches the dashed blue line the dollar index at that time is 93.7.

Price of Gold vs Dollar Index at 93.7

July 27, 2020: $1931

Mid 2016: $750

Mid 2003: $370

Repeat after me: The US dollar has little to do with the price of gold.

Myth 3: Jewelry Demand is Important

That comment shows huge ignorance about the true demand for gold as well as the price driver for gold.

What About Jewelry?

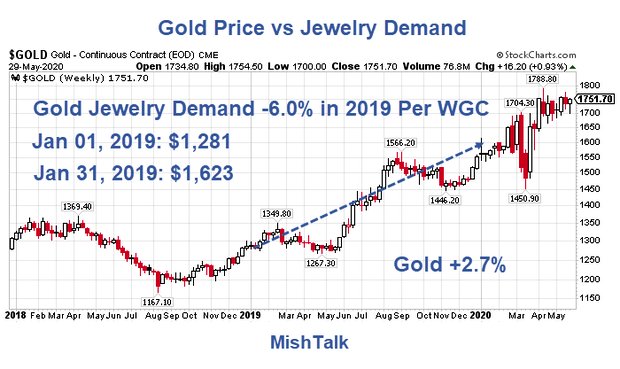

According to the World Gold Council, demand for Gold jewelry in 2019 fell 6 percent overall to 2,107 tons. How did the price of gold react?

Gold vs Jewelry Demand

Marginal Utility?

The subject of marginal utility of gold and jewelry came up in a Twitter discussion on May 30.

Jewelry is totally irrelevant to the price of gold.

The supply of gold is nearly every ounce ever mined. Curiously, similar to Bitcoin.

People confuse jewelry buying with the demand for gold and bitcoin mining with supply of Bitcoin.

Contrary to popular myth, the supply Bitcoin goes up every day. This is why halving the mining rate of Bitcoin did nothing for the price.

Similarly, people confuse demand for new gold jewelry as the demand for gold.

Misconceptions About Gold

The best explantionation of the demand for gold comes from Pater Tenebrarum at the Acting Man blog. He was my teacher in Austrian economics.

Tenebrarum wrote Misconceptions about Gold as a guest post on my blog in June of 2007 under the pseudonym Trotsky, a name he regrets. Gold was $650 at the time.

One can further illustrate gold’s unique nature as money with a study of gold prices vs. jewelry demand. If record fabrication demand for gold (jewelry) must be good for the price of gold, then a historic high in jewelry demand should in theory coincide with a high gold price.

However, record high jewelry demand in 1999 – 2000 in actual fact coincided with a 20 year bear market low in the gold price – the exact opposite of what traditional commodity supply/demand analysis would suggest.

We can therefore conclude that there must be a source of gold demand that is of far greater importance than the jewelry and industrial demand components, and that demand constitutes the true driver of the price of gold in terms of fiat money.

Indeed, there is. This demand component is called ‘monetary demand’. Monetary demand and the supply of gold is actually best described as the ‘degree of reluctance of the current owners of gold to part with their gold at current prices’ since, as mentioned above, some 160,000 tons are owned by somebody already.

Monetary Demand is the True Price Driver

Someone must hold every ounce of gold ever mined. Similarly, someone most hold every Bitcoin ever mined.

Diminishing new supply is meaningless in both. Demand for the total supply is what matters.

Gold rises and falls based on monetary demand. If one views Bitcoin as a competing currency, the same claim can be made but speculation clearly plays a larger role for Bitcoin and it has additional problems with potential central bank or government regulation.

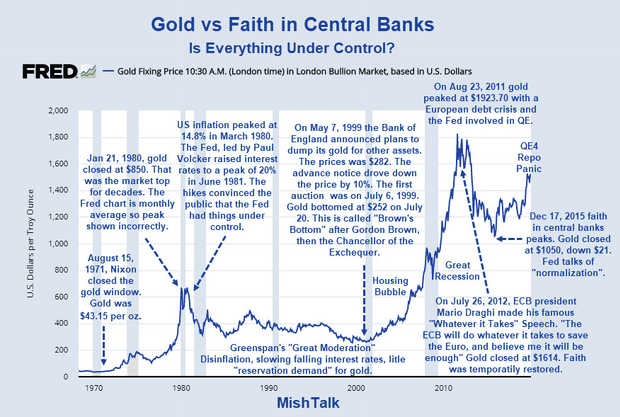

Gold vs Faith in Central Banks

I need to update that chart but it tells the right story.

Gold’s monetary demand is a function of faith in central banks. When ECB president Mario Draghi promised to do “Whatever it Takes” to save the Euro faith in central banks was temporarily restored.

That faith continued until the Fed’s talk of “normalization” dies on the vine. And now?

If you think the Fed has things under control you left your thinking cap on Mars.

via ZeroHedge News https://ift.tt/2X5nQyO Tyler Durden

The event will run from 12:30 to 1:45 PM Eastern time, and is free and open to the public. Registration and additional information is available here.

In June, I did a series of posts about Free to Move. The last post in the series, which has links to the earlier ones, is available here. In the first post in the series, I summarized what the book is about, and why I wrote it. The Introduction to Free to Move, which provides an overview of the rest of the book, is available for free download on the SSRN website here.

As previously indicated, I have promised to donate 50% of the royalties from Free to Move to charities benefiting refugees.

from Latest – Reason.com https://ift.tt/305VdDj

via IFTTT

Just days before boosted unemployment benefits for millions of American workers who have lost jobs due to the coronavirus pandemic are set to expire, Senate Republicans have unveiled a new stimulus package that would prevent those payments from vanishing entirely.

The proposal outlined on Monday afternoon by Senate Majority Leader Mitch McConnell (R–Ky.) would give unemployed workers an additional $200 per week on top of whatever benefits they receive through state-level unemployment insurance programs. That’s one-third of the current $600 unemployment benefits boost that the federal government has been paying since the passage of the Coronavirus Aid, Recovery, and Economic Security Act (CARES Act) in late March.

“The American people need more help,” McConnell said on the Senate floor as he announced the Health, Economic Assistance, Liability Protection and Schools (HEALS) Act.

The continued-but-reduced payments are on one hand an acknowledgment of the depth of the economic recession triggered by COVID-19 and associated lockdowns—more than 30 million Americans have filed for unemployment benefits since the start of the pandemic. On the other, they reflect a growing concern among Republicans about the status of the country’s finances after more than $3.6 trillion in emergency spending in recent months, as well as concern that the $600 per week payments might hamper the post-coronavirus recovery.

Though unemployment benefits vary from state to state, the federal “bonus” meant the average worker could qualify for as much as $900 per week—well over $20 an hour, if you assume a standard 40-hour workweek. Last month, the Congressional Budget Office estimated that nearly five out of every six beneficiaries would be earning more money by not working if the $600 unemployment benefits boost was extended through the end of the year.

Senate Democrats have proposed keeping the boosted benefits in place through March 2021 of the economy does not improve, and Senate Minority Leader Chuck Schumer (D–N.Y.) trashed the Republican plan in remarks delivered on the Senate floor shortly after McConnell announced the bill.

Some Republicans may also oppose the effort. Sen. Rand Paul (R–Ky.) stormed out of a Senate GOP luncheon last week and slammed his colleagues for proposing more deficit spending. The Club For Growth, a conservative grassroots organization that agreed to look the other way when Congress voted on the deficit-hiking CARES Act in March, called on lawmakers to reject the new stimulus plan. David McIntosh, the organization’s president, said in a statement that “the legislation irresponsibly spends on an amended extension of the expanded unemployment insurance benefit and another round of stimulus checks” and criticized McConnell for not including language that would expand educational choice for parents of students in public schools that may not reopen in the fall.

The HEALS Act, if passed, would be the fourth major stimulus package intended to address the COVID-19 pandemic, and it is in many ways a direct sequel to the CARES Act.

Like the CARES Act did in April, the HEALS Act calls for sending $1,200 direct payments to American households, and it would provide another infusion of federal cash to provide loans to small businesses that keep employees on payroll during the crisis. As was the case previously, those $1,200 checks will be phased out for individuals who earned higher levels of income last year. CNBC reported that the phase-outs will start around $75,000 and up. The payments will include an additional $500 per dependent.

When it comes to the small business loans, Sen. Susan Collins (R–Maine) said Monday they would be targeted specifically toward businesses with fewer than 300 employees—a narrower focus that would address one of the major complaints about the Paycheck Protection Program (PPP) established by the CARES Act.

McConnell said the bill would also include legal liability protection for businesses and hospitals to protect them from lawsuits if customers or patients contract the coronavirus—unless the business is guilty of “gross misconduct” or “willful ignorance.” And Sen. Tim Scott (R–S.C.) told HuffPost that the bill will include an amped-up tax break intended to encourage Americans to eat out at restaurants.

Tim Scott says he included the 100% business meal deduction in the GOP bill, up from 50%.

He says that with "limited indoor dining, we can keep folks safe…it will lead to more orders, translate to more take home pay…and more revenues for millions of small businesses."

The bill also includes $105 billion to help schools safely reopen, but it is unclear whether the payments will be made available only to schools that decide to reopen fully—something the president has suggested.

There is no official price tag for the HEALS Act yet—but, as Reason‘s Elizabeth Nolan Brown reported yesterday morning, the best estimates are coming in at around $1 trillion.

from Latest – Reason.com https://ift.tt/39ybWlS

via IFTTT