A Minnesota man named George Floyd died Monday after a bystander video showed him begging for air while a police officer held a knee to his neck.

According to a statement by the Minneapolis Police Department (MPD), officers responded to reports of a forgery and were advised that the suspect appeared to be under the influence. Floyd was sitting in his car when officers arrived on the scene and commanded him to exit his vehicle. The statement says that Floyd got out of his car, physically resisted the officers, and was handcuffed. It was then that officers noticed that Floyd “appeared to be suffering medical distress.” (The statement does not provide further detail.)

But a bystander captured 10 minutes of the interaction on video. When the video starts, an MPD officer is seen pressing his knee into the side of Floyd’s neck while he’s on the ground and handcuffed.

Floyd is heard pleading with the officer, repeatedly saying, “I can’t breathe,” “My neck hurts,” and “They gone kill me.” He continues to move his head, presumably in an attempt to breathe.

“You got him down, man! Let him breathe at least,” a bystander is heard saying in the background. Another comments that his nose is bleeding. Others ask how long the officers plan to keep him on the ground and question the decision to keep him pinned by the neck.

At one point, another officer on the scene responds to the criticisms, saying that they tried to put Floyd in the police vehicle “for 10 minutes.”

About four minutes in, Floyd stops moving. That’s when the officer whose knee is pressed to Floyd’s neck pulls out what bystanders identify as mace and the other officer on scene moves to get between the officer and the crowd.

The bystanders continue to tell the officers that Floyd isn’t responding and urge them to check his pulse. The officer continues to keep his knee pressed to Floyd’s neck until emergency medical services arrive, which was called by the officers.

— Benjamin Crump, Esq. (@AttorneyCrump) May 26, 2020

Floyd was transported to Hennepin County Medical Center. He died shortly after.

MPD confirmed that neither Floyd nor the officers used weapons in the incident, that the officers were not injured, and that the officers involved were wearing body cameras, which were activated at the time.

MPD has requested that the Minnesota Bureau of Criminal Apprehension investigate the incident. The FBI will also be part of the investigation.

“This abusive, excessive, and inhumane use of force cost the life of a man who was being detained by the police for questioning about a non-violent charge,” Crump said in a statement.

from Latest – Reason.com https://ift.tt/3edoRuO

via IFTTT

Kudlow Calls For “Back To Work Bonus” As Americans Prefer Sitting On Couch Rather Than Working Tyler Durden

Tue, 05/26/2020 – 13:25

White House economic adviser Larry Kudlow on Tuesday told Fox News that the Trump administration is examining another round of stimulus for unemployed workers that will get them back to work.

Kudlow calls it the “back to work bonus,” a move that will bring people from off the sidelines and back into the workplace as the economy restarts.

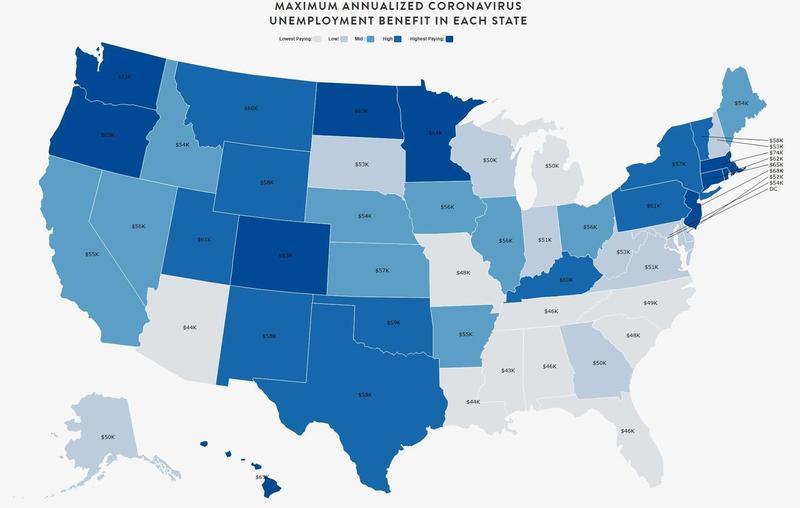

A significant problem for the Trump administration has developed during the economic crash, unemployment benefits for some workers are now paying more than their old jobs did, which is set to delay the employment recovery.

Thanks to the March CARES Act which boosted unemployment benefits by $600 per week, around half of all US workers stand to take in more money while laid off than they did before the pandemic – at least until that increase expires at the end of July.

We noted last week that the CARES Act, which included a $1,200 stimulus check and an additional $600 weekly payment for the unemployed, has led to a labor shortage at one Arizona restaurant.

Times Square Italian Restaurant owner Paullette Cano said with an “unemployment rate at almost 20%, you’d think we’d have a lot of applicants coming in, but we’re not.”

Cano said the CARES Act and unemployment checks have resulted in many of her furloughed employees staying home. They collectively told her their pay from the government is much better than working at her restaurant.

“They don’t want to come back to work,” she said. “It’s the unemployment. They’re receiving about $840 a week, which puts them about $22 an hour.”

Moving on to the subject of China, Kudlow said that Trump is so “miffed” with the Chinese over the virus, that the trade deal is not longer his No. 1 focus concerning China – echoing comments that Trump himself made recently.

Commenting on the market’s rally on Tuesday, Kudlow said Q3 could see one of the biggest jumps in US GDP growth in history, and that the market is rallying on signs that we’ve “hit bottom”, and that the worst of the economic disruption is behind us.

Kudlow also said the administration would extend some assistance to US companies seeking to move parts of their supply chain back to the US from China.

Circling back to Kudlow’s comment on the “back to work” bonus,” we recently penned “When Work Is Punished: Did The ‘Generous’ CARES Act Just Guarantee High Unemployment Is Here To Stay?“ — where it was noted the CARES Act has the potential to create an entirely new generation of welfare serfs, subsisting on significant welfare benefits with no incentive to ‘get back to work’, even after the lockdowns are lifted. This will lead to a labor market that won’t recover anytime soon, thwarting any hopes of a V-shaped recovery this year.

The virus, to its credit, has triggered a dangerous policy response by the government of helicopter money that will effectively delay the recovery. Kudlow announcing the prospects for more stimulus to get people back into the workforce suggests the administration could be in the wrong for paying people more money to stay at home rather than what their prior job was paying — basically disincentivizing people to look for jobs.

via ZeroHedge News https://ift.tt/3erPCvL Tyler Durden

Record Large 2Y Auction Prints At Record Low Yield As Bid To Cover Tumbles Tyler Durden

Tue, 05/26/2020 – 13:17

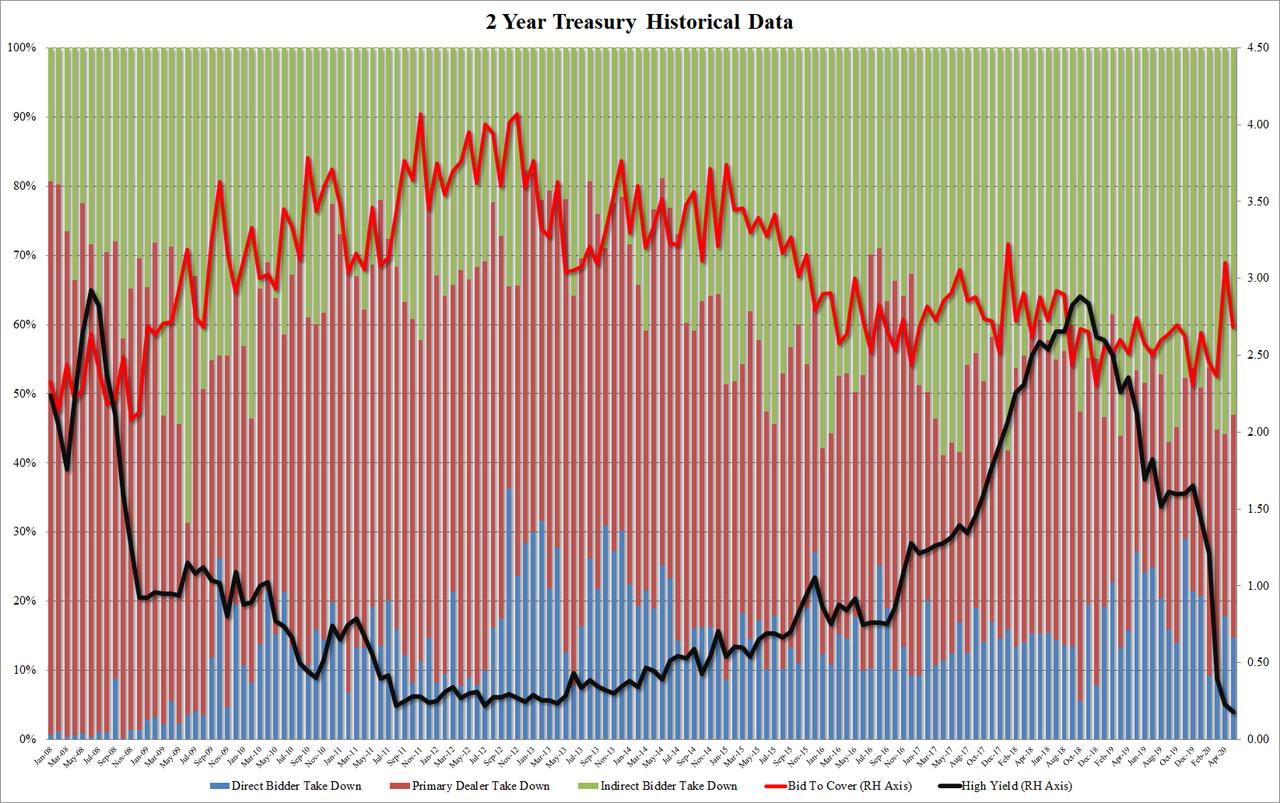

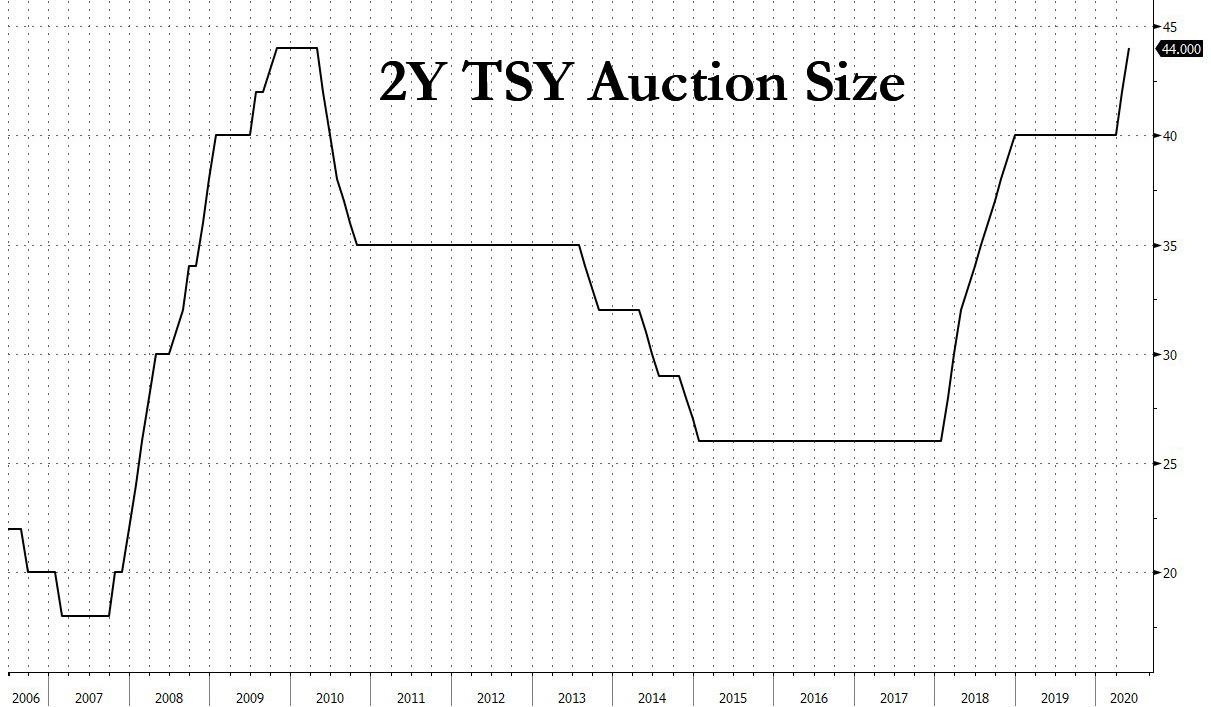

Following a sharp drop in short-end rates in May, when fed funds futures traded negative for the first time ever sending 2Y yields plunging, it was a given that today’s 2Y Treasury auction would price with a record low yield, the only question was by how much. We got the answer moments ago when $44BN in 2Y paper priced at a yield of 0.178%, down from 0.229% in April, and below the previous record low of 0.222% hit in August 2011 when the US was downgraded by S&P. Still, there were some hiccups with the high yield tailing the When Issued 0.176% by 0.2bps.

There were more hiccups in the bid to cover, which tumbled from last month’s 3.102% to 2.683%, which however was still well above the six-auction average of 2.58.

The internals were less exciting, with Indirects taking down 53.1%, down from last month’s stellar 55.81%, and with Directs allotted 14.8%, it left 32.10% to Dealers, right on top of the recent historical average.

Overall, a strong auction despite a few minor blemishes which may be attributable to the rapidly increase in the 2Y auction which is now tied for all time high at $44BN…

… yet with the Fed increasingly likely to cut rates to negative at the next sign of trouble (even though it won’t admit it), the question is how long before the 0.176% yield touches 0.000% and turns negative.

via ZeroHedge News https://ift.tt/3cbe4jv Tyler Durden

A White House petition was created last week after news broke that the Twitter accounts of Chinese dissidents started to disappear after a controversial Chinese-American artificial intelligence (AI) expert was hired to serve on the company’s board.

On May 11, Twitter announced in a press release that it was hiring Li Fei-Fei (李飛飛), an AI expert and former vice president of Google, to its board of directors as a “new independent director” with immediate effect. Li quit Google in 2018 after a trail of leaked internal emails revealed that she appeared to be more concerned about the public relations damage to Google’s image if news broke about the company’s work on Project Maven than the ethical issues raised by over 3,000 Google employees.

Project Maven is a U.S. Department of Defense AI project that seeks to use the technology to help military drones select targets from video footage.

During her tenure at Google, there is no public record of Li objecting to the controversial Project Dragonfly, which was meant to be a search engine that would suit China’s censorship rules, as she opened an AI research facility in Beijing.

When she took the helm of Google’s new AI center in Beijing, Li was quoted in Chinese media as using the CCP slogan “stay true to our founding mission” and said that “China has awakened.” In addition, Li allegedly has ties to a student association that is affiliated with the Chinese Communist Party’s (CCP’s) United Front, according to Radio Free Asia.

A week after Li joined Twitter, a Chinese writer who goes by the handle Caijinglengyan (財經冷眼), discovered that four of his accounts were simultaneously deleted on May 18. He did not receive an explanation until May 23, when he was told his accounts had been taken down for violating Twitter’s rules against posting identical content on duplicate accounts.

He countered that he had only posted content on one of the accounts and used the other to retweet the original post. He pointed out that Twitter does not have a policy precluding a person from having more than one account.

The writer stated that he believes the real reason for his account cancellations was that, on May 17, he tweeted that Twitter’s new board member has a “red background.” In the post, he alleged that she is a member of a student association affiliated with the CCP’s United Front and has close ties with “Second Generation” and “Third-Generation Reds.”

Caijinglengyan claimed that many other Twitter accounts used by Chinese dissidents were suddenly suspended without notice. After he contacted them, he found that they had also criticized Li or started commenting about Li just before their accounts were banned.

The writer listed @beacon__news (灯塔爆料社) and @kevinheaven9 (Calvin看美国) as other Twitter users who found their Twitter accounts suddenly shut down. He claimed that one Twitter user simply wrote “Li Fei-Fei is coming, I have to run,” and soon found that both his primary account and secondary account had been suspended.

French-based Chinese dissident Wang Longmeng (王龍蒙) wrote that Twitter’s ban on those who criticized Li and exposed her background “was undoubtedly related to Li Feifei’s appointment as a director, because criticism and negative information were banned, which is Beijing characteristic,” reported Liberty Times. He believes that Twitter was quickly “dyed red” after Li took charge.

On May 20, a petition was created on the White House website titled “Call for a thorough investigation on Twitter’s violation of freedom of speech.” The creator of the petition wrote that Twitter is suppressing criticism of the CCP and suspending dissident accounts while pro-Beijing accounts remain unscathed.

The petition listed May 18 as a date when many “anti-CCP” Twitter users found their accounts permanently suspended. The author of the document pointed out Li’s involvement with Project Maven and alleged that she was engaged in extensive military-technical programs while running Google’s AI center in Beijing.

The document then alleged that Li continues to have “close ties with top leaders of the CCP.” The petition closed by calling on the U.S. government to investigate “Twitter’s violation of freedom of speech, and on Dr. FeiFei Li’s collaborations with the CCP, a threat to national security.”

via ZeroHedge News https://ift.tt/3c5NrML Tyler Durden

Indian Media Reports Up To 10,000 Chinese Soldiers Have ‘Invaded’ Border Territory Tyler Durden

Tue, 05/26/2020 – 12:45

After over the weekend international reports said that multiple hundreds, or up to 1,000 Chinese troops have crossed into India following prior small-scale skirmishes weeks ago involving dozens of Indian and Chinese soldiers near a remote but strategically important mountain pass near Tibet, Indian media is now reporting that up to five to ten thousand PLA troops have now moved into Ladakh’s disputed Galwan river area.

Some Indian media reports have suggested multiple thousands, while a new Business Standard India reportnowclaims up to 10,000 Chinese soldiers inside India occupying the Galwan Valley while digging into fortified positions.

Though such figures remain unconfirmed and very likely inflated, it’s clear that Indian authorities are watching with growing alarm what they view as an ‘invasion’ of their sovereign territory.

India-China border at Nathula, via PTI/Indian Express

Per the reports, a larger conflict between the two nuclear armed powers is on the horizon:

“The most worrying situation is in the Galwan valley, where the PLA has crossed China’s own claim line (which Beijing had stated was the border with India) and breached 3-4 kilometers into Indian territory. PLA troops are digging defenses to equip themselves to face any Indian attack.”

Sporadic but fierce clashes have occurred going back to the 1960’s along the shared 2,100 mile border, which often involves literal fist-fights among opposing troops and border patrol guards.

A prior 2017 incident involving Indian soldiers crossing into Bhutan ostensibly to thwart a Chinese road construction project extending into the Galwan Valley resulted in a tense standoff and direct two-month long negotiations.

Indeed, given that Beijing sees New Delhi as the principal impediment to the realization of its ambitions to dominate Asia, a more violent clash along the volatile, poorly demarcated Sino-Indian border is highly likely. Unless China emerges as the dominant power in South Asia (and the Indian Ocean), China is likely to remain a regional power in East Asia. Put another way, China’s quest for pan-Asian dominance will intensify the ongoing Sino-Indian rivalry as India itself is seeking primacy—but not hegemony—in southern Asia.

Meanwhile, unconfirmed Indian media reports say large Indian patrol units have begun building up in opposition to the recent PLA movements and provocations.

* * *

A brief review of the escalating situation:

via ZeroHedge News https://ift.tt/3c0KpJH Tyler Durden

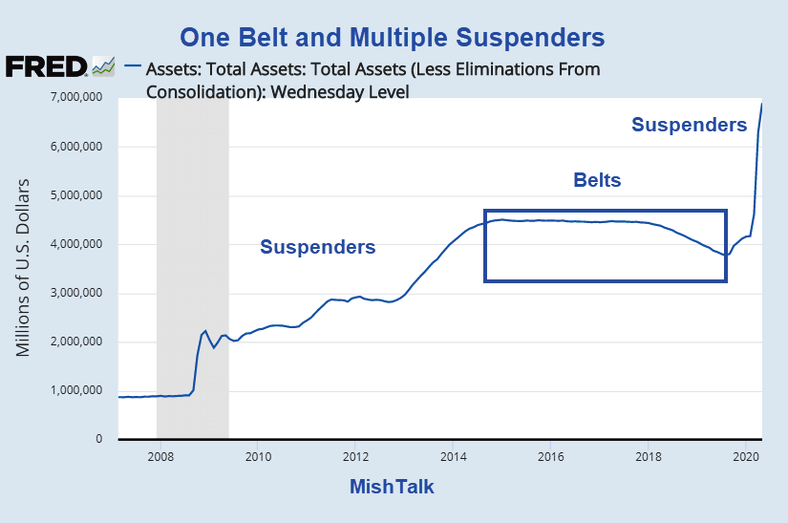

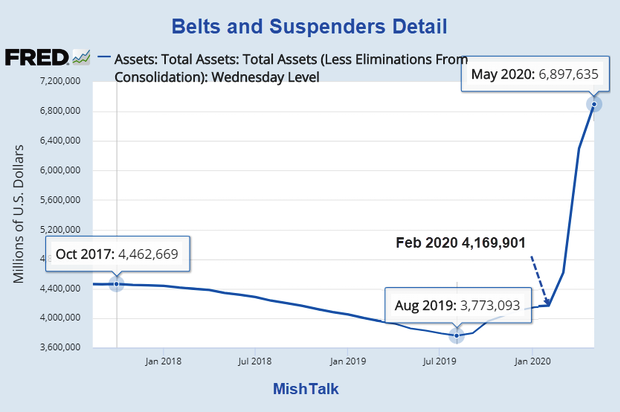

Bernanke’s vague answer to Sen. Richard Shelby, R-AL, when asked how the Fed will deleverage the balance sheet, was this: “In terms of exiting from our balance sheet… a couple of years ago we put out a plan; we have a set of tools. I think we have belts, suspenders – two pairs of suspenders. I think we have the technical means to unwind at the appropriate time; of course picking the exact moment to do, of course, is always difficult.”

Belts and Suspenders Detail

Belts and Suspenders Synopsis

Belt tightening took the Fed’s balance sheet from $4.46 trillion to $3.77 trillion.

Suspenders took the Fed’s balance sheet from $3.77 trillion to $6.90 Trillion in just 9 months.

“And we are going to be assessing the question when it will be appropriate to resume the organic growth of our balance sheet.”

More prophetic words have seldom been heard.

Some objected to my post because of the word “organic”. I commented.

The Fed may do a brief period of “organic” expansion (which by the way can mean anything the Fed wants), but I propose more QE is coming whether the Fed “intends” to do so or not.

Fed’s 2019 Interest Rate Expectations vs Market’s Expectations

Even without Covid-19, the Fed was not remotely close to its expectations.

My Dot Plot comment at the time: “I side with those who expect more rate cuts.”

Clueless Wizards

Some people have immense faith in proven clueless wizards. Others think the Fed does nothing but follow market expectations.

However, this creates what would appear at first glance to be a major paradox: If the Fed is simply following market expectations, can the Fed be to blame for the consequences?

More pointedly, why isn’t the market to blame if the Fed is simply following market expectations?This is a very interesting theoretical question.

Corollary number one stands for the for plot example above.

Corollary Number One

The Fed has no idea where interest rates should be. Only a free market does. The Fed will be disingenuous about what it knows (nothing of use) and doesn’t know (much more than it wants to admit), particularly in times of economic stress.

In case you missed the post, please give it a look. There’s lots more in play regarding what the Fed knows and doesn’t.

Message From Gold

Another pair of suspenders is on deck.

Gold has that message. Do you?

via ZeroHedge News https://ift.tt/3cZSX4J Tyler Durden

A Minnesota man named George Floyd died Monday after a bystander video showed him begging for air while a police officer held a knee to his neck.

According to a statement by the Minneapolis Police Department (MPD), officers responded to reports of a forgery and were advised that the suspect appeared to be under the influence. Floyd was sitting in his car when officers arrived on the scene and commanded him to exit his vehicle. The statement says that Floyd got out of his car, physically resisted the officers, and was handcuffed. It was then that officers noticed that Floyd “appeared to be suffering medical distress.” (The statement does not provide further detail.)

But a bystander captured 10 minutes of the interaction on video. When the video starts, an MPD officer is seen pressing his knee into the side of Floyd’s neck while he’s on the ground and handcuffed.

Floyd is heard pleading with the officer, repeatedly saying, “I can’t breathe,” “My neck hurts,” and “They gone kill me.” He continues to move his head, presumably in an attempt to breathe.

“You got him down, man! Let him breathe at least,” a bystander is heard saying in the background. Another comments that his nose is bleeding. Others ask how long the officers plan to keep him on the ground and question the decision to keep him pinned by the neck.

At one point, another officer on the scene responds to the criticisms, saying that they tried to put Floyd in the police vehicle “for 10 minutes.”

About four minutes in, Floyd stops moving. That’s when the officer whose knee is pressed to Floyd’s neck pulls out what bystanders identify as mace and the other officer on scene moves to get between the officer and the crowd.

The bystanders continue to tell the officers that Floyd isn’t responding and urge them to check his pulse. The officer continues to keep his knee pressed to Floyd’s neck until emergency medical services arrive, which was called by the officers.

— Benjamin Crump, Esq. (@AttorneyCrump) May 26, 2020

Floyd was transported to Hennepin County Medical Center. He died shortly after.

MPD confirmed that neither Floyd nor the officers used weapons in the incident, that the officers were not injured, and that the officers involved were wearing body cameras, which were activated at the time.

MPD has requested that the Minnesota Bureau of Criminal Apprehension investigate the incident. The FBI will also be part of the investigation.

“This abusive, excessive, and inhumane use of force cost the life of a man who was being detained by the police for questioning about a non-violent charge,” Crump said in a statement.

from Latest – Reason.com https://ift.tt/3edoRuO

via IFTTT

In Fulton v. City of Philadelphia, the Court is considering whether to reverse Employment Division v. Smith, the case holding that (generally speaking) religious objectors aren’t constitutionally entitled to exemptions from generally applicable laws. I have long been one of the few law professors who (1) thinks Smith is right, but (2) thinks that jurisdiction-by-jurisdiction Religious Freedom Restoration Acts are generally a good idea. I wrote an article about that in 1999 (A Common-Law Model for Religious Exemptions), and now an amicus brief in Fulton (with the help of my students Robert Bowen, Delaney Gold-Diamond, and Caleb Mathena).

The amicus brief is on my own behalf, so there are no reasons for me to keep it confidential before I file it (it’s due next Wednesday, June 3, but I’d like to file it a couple of days early), and every reason not to: If there are any errors, small, medium, or large, in my thinking on this, I would love to have a chance to fix them. So if any of you are interested in having a look and giving me your suggestions, I’d much appreciate it. (Note that the brief has not yet been cite-checked or fully proofread, though I’d be glad to know of proofreading glitches as well as about more serious ones.) I include the Summary of Argument below, but you can read the whole brief here.

[1.] Justice Scalia was right: Courts should not be constantly “in the business of determining whether the ‘severe impact’ of various laws on religious practice” suffices to justify a constitutionally mandated exemption from a generally applicable law. Employment Division v. Smith, 494 U.S. 872, 889 n.5 (1990). “[I]t is horrible to contemplate that federal judges will regularly balance against the importance of general laws the significance of religious practice.” Id.

Indeed, overruling Smith would revive all the flaws of a broad substantive due process regime: It would require courts to routinely second-guess legislative judgments about the normative foundations for a wide range of laws, and about the laws’ practical necessity.

For instance, should people have a right to assisted suicide? This Court in Washington v. Glucksberg, 521 U.S. 702 (1997), refused to recognize such a right under substantive due process, and upheld an assisted suicide ban under the rational basis test. But if Smith were overruled, any person who claims a religious obligation to assist in suicide would trigger the very sort of strict scrutiny inquiry that Glucksberg forecloses.

Likewise, this Court has rejected heightened scrutiny of economic regulations, such as minimum wage laws. But if Smith were overruled, a person who claims a religious obligation to hire people but for less than minimum wage would be entitled to an exemption, unless the regulation passes strict scrutiny. And the list could go on.

Of course, it is appealing to protect religiously motivated action (or inaction) that does not really hurt anyone. But what constitutes “hurting anyone” is a hotly contested issue, as this very case shows. It is contested normatively. (Should refusing to deal with a same-sex couple qualify as hurting them? Is paying people a supposedly “exploitative” wage, even with their consent, hurting them?) And it is contested practically. (Would allowing assisted suicide end up pressuring people into choosing death even if they would rather not?) This Court’s rejection of a general right to liberty under the rubric of substantive due process wisely recognizes that these questions should ultimately be left to the political process.

[2.] To be sure, normative and pragmatic judgments about which actions hurt others are familiar to courts. Much of the common law of tort, contract, and property reflects such judgments.

But such decisions are only tentative, because they can be overruled by legislatures. Judges have the first word on these matters, but not the last. That makes common-law decisionmaking legitimate even when aggressive use of substantive due process would not be.

Indeed, decisionmaking under RFRAs is in this respect similar to such common-law decisionmaking. Because RFRAs (state or federal) are mere statutes, they give judges authority to create exceptions but subject to possible revision by legislatures.

Thus, for instance, this Court concluded in Gonzales v. O Centro Espírita Beneficente União do Vegetal that, in effect, hoasca was not so harmful as to justify denying an exemption request, 546 U.S. 418 (2006)—but if Congress had disagreed, it could have exempted the hoasca ban from RFRA, and thus had the last word on the subject. But if Smith were overruled, this Court’s estimate of harm would have been final, unrevisable without an Article V constitutional amendment.

[3.] Some substantive constitutional rights, of course, do require courts to evaluate the normative and pragmatic justification for restrictions on those rights, and the test in those cases often is strict scrutiny. But Smith was correct in concluding that claims of those rights are quite different from claims of religious exemptions, 494 U.S. at 885-86. Those rights require second-guessing legislative judgments only for specific, well-defined zones of regulation (e.g., content-based speech restrictions), where such judicial decisionmaking is especially justified. Overruling Smith would require courts to consider overriding legislative decisions as to a vast range of generally applicable laws.

[4.] Nor should this Court limit Smith to laws that lack secular exceptions. A law can be generally applicable if it does not single out religious behavior for special burdens, even if it does include exceptions for certain kinds of secular behavior. Indeed, a vast range of important laws have many exceptions—trespass law, the duty to testify, antidiscrimination law, copyright law, contract law, and many others.

[5.] This brief takes no position on whether statements of government officials and the shifting legal basis for the government’s actions may indicate that the City of Philadelphia singled out Catholic Social Services for different treatment on the basis of religion. Pet. Br. __. The brief argues only that this Court should reaffirm the Smith principle that, absent such intentional discrimination, the Free Exercise Clause does not provide a presumptive constitutional right to religious exemptions from government actions.

[Footnote:] This brief also does not discuss the original meaning of the Free Exercise Clause, a matter treated in Justice Scalia’s and Justice O’Connor’s opinions in City of Boerne v. Flores, 521 U.S. 507 (1997), and likely in other forthcoming amicus briefs in this case.

from Latest – Reason.com https://ift.tt/2M1JSN2

via IFTTT

“A Moment Of Truth For The Euro”: ECB Preparing To Run QE Without Bundesbank Tyler Durden

Tue, 05/26/2020 – 12:05

The shape of Europe’s massive monetary injection may change dramatically in the coming months. According to Reuters, citing four sources, the ECB has drafted contingency plans to carry out its multi-trillion QE programme without the Bundesbank in case Germany’s top court forces the main participant in the scheme to quit.

Not only is the European central bank planning on how to continue QE without German – mostly by having other European central banks step in although it is unclear just how effective this would be – but, in a worst-case scenario, the ECB would also launch an “unprecedented legal action against the German central bank, its biggest shareholder, to bring it back into the program.”

According to Reuters, such a moves would mark “a moment of truth for the euro”, testing Germany’s commitment to a currency it played the biggest role in creating (for a simple reason: Germany was the primary beneficiary for years as eliminating the chronically strong Deutsche Mark allowed German exports to flourish), and forcing it to tackle some deep-seated reservations within the country about ECB policies.

As reported earlier this month, Germany’s constitutional court gave the ECB an ultimatum until early August to justify its massive buying of government bonds or continue the scheme without the Bundesbank, which carries out more than a quarter of the bond purchases. Without the Bundesbank, the ECB’s QE is effectively done.

While consensus remains optimistic, expecting the legal challenge from the court in Karlsruhe to be resolved by the Bundesbank itself by demonstrating that the policy was appropriate and addressing concerns about its side effects, staff at the ECB and the euro zone’s national central banks are preparing for what one source described as the “unbelievable”: a scenario in which the court bans the Bundesbank from taking part in the purchases.

In that case, the ECB, or less likely the other euro zone central banks, would take up the Bundesbank’s quota in the Public Sector Purchase Programme (PSPP) and buy German bonds, although with far fewer non-German bonds in private hands in Europe, the European QE program would have to be forcibly shrunk on very short notice.

There is one loophole: to allow other central banks to buy Bunds, Europe’s “no risk sharing” principle – one which the Bundesbank itself insisted upon when the programme was launched in 2015 – would have to be broken. Until now each national central bank bought its own government’s bonds and the risk is shared over the limited amount of debt bought by the ECB itself.

The ECB has slowed down German bond purchases since the start of the coronavirus pandemic to focus its firepower on Italy, which has come under pressure in the bond market as the outbreak has savaged its already shaky public finances. Indeed, according to Reuters, Bundesbank purchases of German sovereign debt, or Bunds, totaled just 628 million euros ($688 million) in April, or just 2.3% of the government bonds bought under the PSPP that month.

There is a bigger problem: even if the Bundesbank quits the scheme, leaving Germany’s Bunds out is “not an option” given that they serve as the de facto euro zone benchmark for private investors thanks to their top-notch credit rating and ample availability. Nobody would buy Italian debt just because German bonds were not available.

But the biggest risk should this plan be activated is that cutting off Germany from the ECB’s flagship stimulus program would invite speculation about a euro zone break up, which the ECB has been trying to quash since the euro crisis of 2010-12. In the meantime, the ECB would probably launch an infringement procedure against the German central bank for failing to fulfil its obligation as a member of the Eurosystem if it has to stop buying bonds, the sources said.

If the Bundesbank then failed to comply, the ECB could take the matter to European Court of Justice (ECJ), in what would be the first such case since the euro was created in 1999. The ECJ has already upheld the ECB’s QE but its ruling was disregarded by Germany’s constitutional court, opening a further conflict German and European Union institutions.

All of this is a worst case scenario: the German government has shown optimism that any such scenario can be avoided. Chancellor Angela Merkel told senior officials from her party earlier this month that the issue was “solvable” if the central bank explained the plan.

via ZeroHedge News https://ift.tt/36u4ua4 Tyler Durden

This past weekend, I asked if the decline in March was a bear market or just a big correction. The debate that ensued was polarizing, to say the least. However, defining the market using long-term analysis is essential in determining the current trend, potential outcomes, and portfolio assumptions.

“Such brings up an interesting question. After a decade-long bull market, which stretched prices to extremes above long-term trends, is the 20% measure still valid?

To answer that question, let’s clarify the premise.

A bull market is when the price of the market is trending higher over a long-term period.

A bear market is when the previous advance breaks, and prices begin to trend lower.

The chart below provides a visual of the distinction. When you look at price “trends,” the difference becomes both apparent and useful.”

“This distinction is important.

“Corrections” generally occur over very short time frames, do not break the prevailing trend in prices, and are quickly resolved by markets reversing to new highs.

“Bear Markets” tend to be long-term affairs where prices grind sideways or lower over several months as valuations are reverted.

Using monthly closing data, the ‘correction’ in March was unusually swift but did not break the long-term bullish trend. Such suggests the bull market that began in 2009 is still intact as long as the monthly trend line holds.

However, I have noted the market may be in the process of a topping pattern. The 2018 and 2020 peaks are currently forming the “left shoulder” and “head” of the topping process. Such would also suggest the “neckline” is the running bull trend from the 2009 lows. A market peak without setting a new high that violates the bull trend line would define a “bear market.”

Defining Long-Term Market Cycles

That analysis brings up an interesting question.

What if the secular bull market that began in 1980 is still in process?

Before you adamantly deny this possibility, we need to consider the context of both long-term investor psychology cycles and valuations.

Let’s start with the following chart of investor psychology.

This chart is not new, and there are many variations similar to it, but do not dismiss the importance. Throughout history, individuals have repeatedly responded to market dynamics in the same fashion. At each delusional peak, it was always uttered, in some form or variation, “this time is different.”

“Long-term investment success depends more on the WHEN you start investing. Such is shown in the chart of valuation cycles.”

“Here is the critical point. The MAJORITY of the returns from investing came in just 4 of the 8-major market cycles since 1871. Every other period yielded a return that lost out to inflation during that time frame.”

However, by looking at each full-cycle period as two parts, bull and bear, it obscures the importance of the “full cycle.” What if instead of there being 8-cycles, we look at themasonly three?

Note in the chart above that CAPE (cyclically adjusted P/E ratio) reverted well below the long-term trend in both prior full-market cycles. When viewed in this manner, we see the full-market cycle encompasses many bull and bear market cycles, but only completes when valuations are reset.

While valuations briefly dipped below the long-term trend in 2008-2009, they did not revert to previously low levels. Given valuations have remained elevated since 1982; it suggests the full-market cycle has yet to complete. Such a reversion would align the fundamental and psychological underpinnings seen at the beginning of the last two full-market cycles.

Long-Term Analysis – Is The 80’s Bull Still Running?

We can further examine the idea of long-term market cycles if we overly the psychological and time-frame analysis. The first full-market cycle lasted 63-years from 1871 through 1934. This period ended with the crash of 1929 and the beginning of the “Great Depression.”

The second full-market cycle lasted 45-years from 1935-1980. This cycle ended with the demise of the “Nifty-Fifty” stocks and the “Black Bear Market” of 1974. While not as economically devastating as the 1929-crash, it did greatly impair the investment psychology of those in the market.

The Running Bull Market

The current full-market cycle is only 38-years in the making. Here is a short-list of what prices are pushing up against:

Elevated valuations

Collapsing economic data

Declining earnings and corporate profitability

Weak economic growth

Surging debt levels

Deflationary economic pressures

Suppressed wage growth

Weakening demand from consumption

Even this short-list of headwinds makes it worth questioning whether the current full-market cycle has completed. Such is particularly the case when Central Banks are required to maintain ever-increasing levels of monetary interventions to keep financial markets functioning.

The idea of the “bull market,” which begin in 1980, is still intact is not a new one. As shown below, a chart of the market from 1980 to the present suggests the same.

The long-term bullish trend line remains, and the cycle-oscillator is only half-way through a long-term cycle. Furthermore, by the time the market resolves itself, a 61.8% retracement would reset markets back to the 1999 levels. Such is based only on the assumption that the long-term full market cycle has not yet completed.

I am NOT suggesting this is the case.

Instead, this is a thought-experiment about the potential outcome from the collision of weak economics, high levels of debt, valuations, and investor’s “irrational exuberance.”

Yes, this time could entirely be different.

It just never has been before.

Using Long-Term Analysis To Measure Potential Outcomes

Regardless of whether you agree with the premise, do not completely dismiss the importance of long-term price cycles. Currently, it is “in vogue” to believe it is only monetary policy driving markets now. Over the long-term, there have been many excuses for rising prices, which eventually gave way to “fundamental gravity.”

One of the most interesting emails I received in response to my monthly analysis above was from Jim Colquitt, President of Armor Index, Inc. To wit:

“If we draw the ‘Head & Shoulders’ pattern you described above, we find an interesting symmetry. The distance from the beginning of the left shoulder (September 2017) to the end of the left shoulder (December 2018), is the same distance (15 months) from the end of the left shoulder to the end of the head (March 2020).

If we assume this symmetry remains intact, it will allow us to complete the right shoulder of the head and shoulder pattern 15 months later in June 2021. Such would be somewhere in the price range of ~2,030 or roughly ~31% lower than current levels.”

Where Do We Go From Here

What does this analysis suggest if the market breaks below the neckline? Or, what if markets bounce off of the neckline as support?.

‘Head & Shoulder’ pattern theory suggests a move to the downside would put the target price at the equivalent of the distance from the head to the neckline as measured from the neckline. A break would equate to roughly ~840 on the index, or ~72% lower than current levels (see “Chart 2”).

Conversely, if the neckline is rejected, pattern theory suggests the distance above is used but is added to the top of the right shoulder. Such would equate to an index level of roughly ~4,160 or ~41% higher than current levels (see “Chart 2”). However, such a rise would likely come after testing the neckline (~2,030) and would equate to more than a 100% return from that point.

It is also interesting that current market levels are almost perfectly in line with the left shoulder peak in September 2018, the resistance/support levels from April through July 2019, and February through April 2020. Such could be the top for the right shoulder.

Should we test the lows of the worst case scenario, pattern theory puts the target range at levels, which are almost perfectly in line with the lows of the 2002 and 2008 recessions (see “Chart 3”).

Jim is correct in the analysis. We certainly hope markets don’t revisit the lows of the previous two bear-markets. For investors that is the worse possible outcome. However, such an outcome does have historical precedents within the context of completing a full-market cycle.

Conclusion

There is a sizable contingent of investors, and advisors, today who have never been through a real bear market. After a decade long bull-market cycle, fueled by Central Bank liquidity, it is understandable why mainstream analysis believe markets can only go higher.

Bear market cycles rarely end in a single month. There is much “hope” the Fed’s flood of liquidity can arrest the market decline. However, there is still a tremendous amount of economic damage to contend with over the months to come.

When analyzing the markets using monthly data, it certainly appears as if the long-term bull market that began in 1980 remains intact currently. However, we have roughly a decade of potentially hard times ahead of us if we are early in the process of completing the second half of the full-market cycle.

If you are a short-term market trader, this analysis likely has little importance to you. It also doesn’t mean market returns over the next decade are negative every single year. What it does suggest is that investors will face increased volatility and low average rates of return.

For most investors, a “buy and hold” investment strategy will likely leave you far short of your goals.

That is just what this particular set of analysis suggests. There is an unlimited number of potential outcomes that can occur over the next decade. Some of them good, some of them bad. Such is why it is important to measure the amount of risk being taken to achieve financial goals and manage that risk accordingly.

Or, you can disregard the analysis entirely and continue hoping for the best.

However, if investing worked as the media tells you, then why, after three major bull markets in the last 30-years, are 80% of Americans still broke?

via ZeroHedge News https://ift.tt/36uOjcF Tyler Durden

{kind=link}

{kind=link}