Former FDA Commissioner Warns Waiting For “Optimal” Testing Capacity Before Reopening Simply “Not Possible”

There’s no question that countries across the world are going to need to make hard choices and difficult judgment calls in the coming weeks and months as they confront the unavoidable fact that staying on lockdown until mass testing and even in many cases (such as in the US) mass contact tracing becomes possible simply isn’t realistic.

While AOC, Bernie and their democratic socialist followers would love it if the Treasury printed $20 trillion in paper, money to be immediately monetized by the Fed, to allow every American to stay home and stay eating – and, ideally, stay safe from the virus – until September.

What they don’t realizes is that such an unprecedented experiment in MMT would leave the country’s fate up to the whims of the financial markets. A simple spike in interest rates could transform the US into Venezuela faster than 99% of Americans probably think possible. These types of frictions also raise the risk of sudden, massive food-price inflation, the return of even more breadlines, and general unrest and chaos that could lead to far more generalized harm and loss of life than the virus would cause by itself.

Watch @ScottGottliebMD’s full interview with @savannahguthrie about some states soon easing up on stay-at-home guidelines, why he thinks some states should reopen even though he doesn’t think we’ll have proper testing until the fall and more. pic.twitter.com/Ex3Pkh7nf1

Given the current state of global affairs, it’s not difficult to game out how things could get apocalyptic pretty quickly, especially in developed countries like the US which, ironically, are less equipped because their citizens have absolutely no survival skills (though this of course doesn’t apply to everybody: there are large swaths of the US, in the farm belt and hunter-friendly red states, where surviving off the land might be a feasible option). If that truck doesn’t arrive with the next day’s goods, people in most towns will go hungry. Full stop.

This is why, as former FDA head Scott Gottlieb warned Monday that the US likely won’t have the capability to carryout mass testing until September (despite the fact Gov. Cuomo has promised to start rolling out random antibody testing this week).

“We’re not going to be there. We’re not going to be there in May, we’re not going to be there in June, hopefully we’ll be there by September,” Gottlieb said during an appearance on NBC’s “The Today Show”.

As more Democratic governors join the chorus of critics accusing the Trump Administration of failing to provide enough tests to safely reopen their economies, Gottlieb’s comments are the latest from a former ‘impartial’ government scientist suggesting that mass testing isn’t a requirement for reopening.

Dr. Fauci has already made this point during White House press briefings.

While many Americans remain anxious about reopening the economy too early, Gottlieb said that many states that haven’t seen high rates of penetration by the virus are probably ready to start rolling back some of the closures and stay at home orders.

“It’s a risk. … If we wait until we have sort of the optimal framework for testing, we’ll be waiting until the fall, and that’s just not going to be possible from an economic, social or public health standpoint.” @ScottGottliebMD on reopening despite not having proper testing. pic.twitter.com/l7df9BH21C

The US may not have the optimal amount of tests and capacity for contact tracing, but waiting until later this year for a train that might never come simply isn’t realistic, Gottlieb said. However, the lockdown has probably been adequate at this point to greatly reduce unnecessary deaths and infections – in other words, as we noted last night, developed economies have at least made progress toward “flattening the curve.”

Setting the question of testing aside, Gottlieb said that the US likely won’t be able “to do the work of tracking down everyone who is sick, or who might have been in contact with people who [are] sick.” But even Singapore and South Korea didn’t succeed in tracking down every one.

“It’s a risk, there’s no question it’s a risk,” he said. “I mean, we won’t have the testing that we want until September, I think, in terms of kind of broad coverage. You’re still going to see high positivity rates heading into May.”

But waiting until the fall just won’t be possible “from an economic, social or public health standpoint.”

“If we wait until we have sort of the optimal framework for testing, we’ll be waiting until the fall and that’s just not going to be possible from an economic, social or public health standpoint,” he said.

Gottlieb’s comments come as some states take steps to reopen their economies this week following a three-phase plan from the White House recommending that governors should do so in stages.

However, this doesn’t mean the US should just give up on expanding its testing capacity. Gottlieb says he hopes the US will be able to manage testing roughly 1% of the population on a weekly basis come September,

“I think a good rule of thumb would be (to test) about 1% of the population on a weekly basis – so the ability to test about 3 million people. We’re not going to be there. … Hopefully, we’ll be there by September.” –@ScottGottliebMDpic.twitter.com/N2gUfzjw68

As most viewers who have watched Gottlieb’s near-daily spots on CNBC and other cable news shows over the past few months, the fact that he left his job months before this outbreak is one of the lowkey worst Trump Administration personnel decisions made in the runup to the crisis – even as he insists he quit because of the strain of commuting from Westport, Conn. to Washington, DC. They should have begged him to stay.

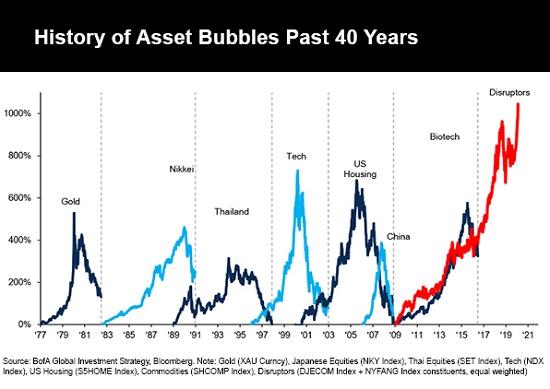

Bubbles always burst, and the confidence that “this isn’t a bubble” and “the Fed has our back” are counter-indicators.

Here we go again: stocks have once again reached nosebleed valuations completely disconnected from reality–in other words a repeat of the speculative-frenzy bubble that reached its peak on February 19. Once again, stocks are sporting delusional GDP-to-valuation and P-E (price-earnings) ratios, all based (again) on the belief that nothing–certainly not revenues, profits, debt levels, etc.–matters; the only thing that matters is the Fed pimping stocks.

What might observant punters have learned from the February 19 bubble popping? For one thing, the complacent belief that every technician’s target is guaranteed is suspect: at this writing, the vast majority of technical-analysis targets are much higher.

What’s the basis for these higher targets? Nothing but the implicit quasi-religious faith in the Fed.

For another, the belief that the market will give every punter an ample opportunity to sell once those targets are reached is equally suspect. Wouldn’t it be nice if every punter that sees a target for the 61.8% Fibonacci level, etc. can wait for that target and then cash out, as if nobody else (or ten thousand trading bots) aren’t planning to sell at the same target?

One often overlooked characteristic of stock market bubbles is the extremely small exit for sellers trying to avoid becoming impoverished bagholders. Bubbles always present small exits because once sentiment turns, buyers vanish and so price goes over the waterfall and crashes on the rocks below (accompanied by the screams of all the punters who reckoned they’d exit at the top).

For an example, please review a chart of stock market action between March 1 and March 23.

But modern markets have characteristics which have further diminished the exit to a tiny pinhole. These include (but are not limited to):

1. The dominance of index funds. When shares of the index are sold, every constituent stock gets sold. This triggers cascades of selling that overwhelm “buy the dip” buying.

2. Computers do most of the trading, and the algorithms are set to follow trends with extreme ferocity. Once the trend is “sell,” the program selling will self-reinforce the cascade.

3. Central banks have generated a mesmerizing moral-hazard propaganda field that implicitly suggests “we’ll never stocks go down again, ever!” Yet the only way central banks can causally intervene is to buy stocks directly in size, i.e. in the trillions of dollars. (Recall U.S. stocks are around $30 trillion, global stock markets about $80 trillion. Yes, buying futures contracts through proxies works in stable markets, but not so much in panic cascades of selling.)

Beneath the illusory stability, modern markets are extremely illiquid, meaning that when the bubble pops and punters/money managers try to sell, there are no buyers at any price.

Liquidity in a crash depends on “buy the dip” bagholders. Once they’ve been destroyed, there are no more buyers at any price. The “buy the dip” crowd will be wiped out after the first spike higher fails, and then nobody will be left who’s willing to catch the falling knife.

It’s illuminating to go back to to former Federal Reserve chairman Alan Greenspan’s 2014 belated bleatings in Foreign Affairs, Why I Didn’t See the Crisis Coming. Greenspan presented one primary reason: the Fed’s models failed to accurately account for “tail risk,” (otherwise known as things that supposedly happen only rarely but when they do happen, they’re a doozy), because guess what–they happen more often than statistical models predict.

“Tail risk” is a fancy way of saying that bagholders willing to buy the dip and be destroyed as the crash gathers momentum are too scarce to stop the waterfall of selling. That leaves everyone with a long position in stocks with a binary choice: either grasp the fleeting advantage of selling out in the first wave of selling–and by the way, there’s no advantage unless every single share is sold–or become a hapless bagholder.

Bubbles always burst, and the confidence that “this isn’t a bubble” and “the Fed has our back” are counter-indicators of just how crushing the pop will be: the greater the confidence/euphoria, the greater the crash.

Sober up, people. All bubbles pop, and the higher the extreme, the greater the crash. Only the first sellers will escape; everyone who hesitates or “buys the dip” will be crushed at the bottom of the waterfall.

If you want to sell your shares to bagholders, issue technical targets way above current levels and year-end targets at nonsensically lofty levels, then sell, sell, sell as the over-confident bagholders buy, buy, buy. (“But Mr. Pundit said the S&P 500 was gonna go higher, he promised!”)

Who goes into the market planning to buy at technical levels where everybody else is selling? How many “dumb money bagholders” does everyone reckon will be anxious to buy their shares at the top of the craziest overvalued bubble ever?

Here we go again: only two months after “buy the dip” and “the Fed has our backs” failed, the pundits and money managers are falling over themselves to declare “the bottom is in,” “there’s now light at the end of the tunnel,” and all the other reasons to complacently hold on and become a bagholder so the smart money can sell to you before the anointed TA targets are reached.

Key Events In This Extremely Chaotic, Action-Packed Week

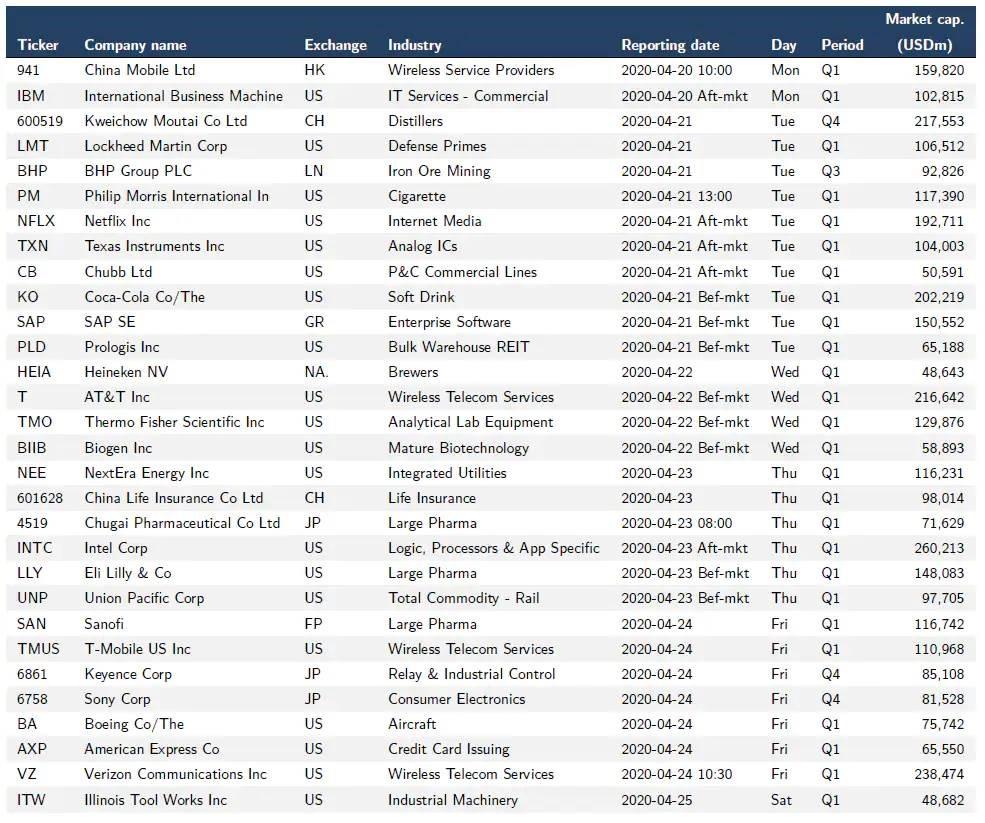

In what is sure to be a fast-moving, chaotic week, in which attention will focus on every marginal development in the war against Coronavirus (and Chinese exports thereof), Q1 earnings will step up a notch with 88 S&P 500 companies reporting this week and Europe joining the fray with 64 companies. In terms of the highlights to look out for, proceedings kick off today with IBM. Then tomorrow we’ll hear from The Coca-Cola Company, Netflix, SAP, Philip Morris International, Lockheed Martin, Texas Instruments and BHP. On Wednesday, we’ll then get AT&T and Thermo Fisher Scientific. Thursday sees releases from Intel, Eli Lilly and Company, NextEra Energy, Union Pacific, Credit Suisse and Hyundai. And finally on Friday we’ll hear from Verizon Communications, Sanofi, T-Mobile and American Express.

Going back to the virus epidemic and ongoing responses to the current economic depression, Thursday is the key day this week with the EU leaders summit a potentially big event for the future of Europe as they discuss how close the region can get to joint issuance in the near future. As Deutsche Bank’s Jim Reid writes, “expect creative ambiguity to rule as it normally does on the continent. Nevertheless you would expect more explicit details to be outlined as to how Europe will help Italy.” Will this be enough to keep Italian spreads (and domestic politics) in check though? To add to the story, S&P are expected to finalize the review of their BBB rating on Friday. The implications of Italy is junked will be dire. Staying with European discussions, the FT broke a story yesterday saying the supervisory wing of the ECB is pushing for an EU wide bad bank. It’s not clear whether this story will have legs but it’s clearly something that the weaker members will welcome much more than the stronger ones. Whether it’s NPLs or peripheral debt, can this crisis be the catalyst for more European financial solidarity or will it be one to expose the cracks of an imperfect union.

On the issuance of joint Eurogroup debt, Italian PM Conte said in an interview to Germany’s Sueddeutsche Zeitung yesterday reiterating the need for joint debt issuance highlighting the risk of market contagion if European leaders fail to act on pressure from Italy and Spain. He also added that the ESM rescue fund, Germany’s preferred tool to address the economic impact, “has a bad reputation in Italy.” Meanwhile, Klaus Regling, the ESM’s director-general, said in a separate interview with Italy’s Corriere Della Sera that concerns that the fund’s lending will have two parts — one to specifically deal with the outbreak, the other to reduce budget deficits — was misplaced. He added, “The conditions agreed at first will change during the period of which the line of credit is available. The Eurogroup will clarify it, saying that the only requirement for obtaining the loan is the way in which they spend the money.”

Looking at Thursday, we will not only will we see the latest jobless claims but also the flash PMIs from around the world for April – the first reading covering nothing but lockdowns. If you want a potential worst case scenario Italy was the only Western country to be on full lockdown in the survey period for March and they saw their services PMI fell to an astonishingly low 17.4. In all truth though the market has rightly or wrongly moved on from how bad data could get in the near-term to absorbing up the extra liquidity and also whether economies can open progressively through May.

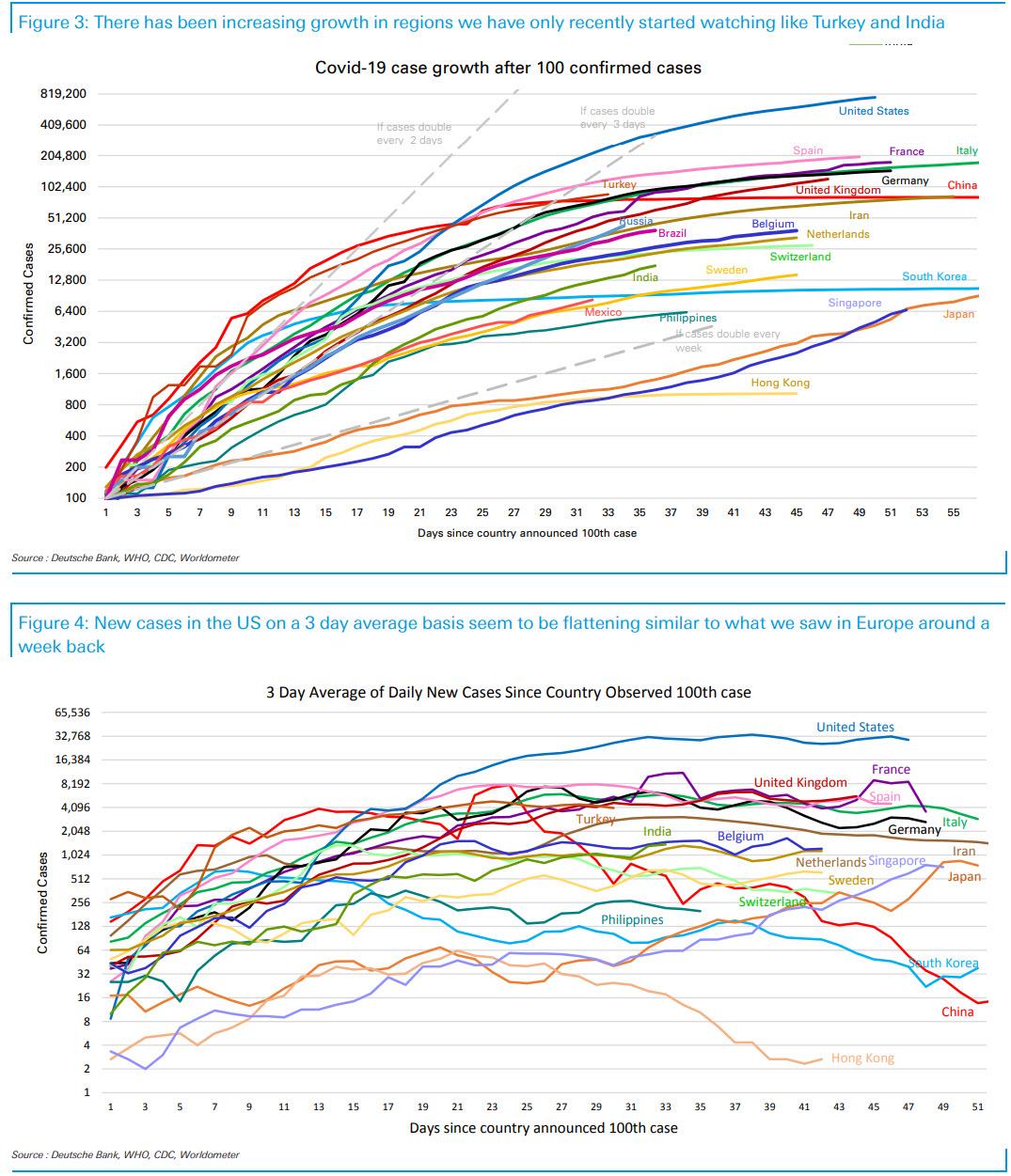

On this the latest on new cases and fatalities generally continue to show steady improvements as you’ll see in our Corona Crisis Daily. However this improvement is being used by many countries to encourage debate on what exit strategies will look like and the lifting of restrictions at potentially an earlier stage than China did. A risky balancing act.

Back to earnings, Saxo’s Peter Garnry writes that this week will be the first real litmus test on sentiment vs earnings reality and the outlooks from companies. Many interesting companies such as Netflix, Intel, Biogen, Delta Airlines, American Express and Boeing will report earnings this week. Maybe bad earnings are what finally get investors to realize that they are buying equities at very expensive levels here. No matter whether we use the dividend futures market or expected GDP growth numbers and how they have translated into EPS growth in the past we get to the same conclusion. The equity market is very expensive here and the risk-reward ratio is not attractive.

Among this week’s earnings Saxo highlights IBM (today) as the 350,000 employees company has a big footprint on corporate spending on technology infrastructure and thus is a good litmus test on corporate spending in the US. Tomorrow the big one is Netflix which is enjoying investors appetite for entertainment stocks – key here is the US segment because rising unemployment could be a risk to their subscriber base in the US unless streaming TV is now like the utility bill. Tomorrow we also get earnings from the first P&C insurer (Chubb) which will give insights into whether the sell-off among insurance stocks has been too much. Wednesday we get the first biotechnology earnings from Biogen which is a key risk to the health care sector which has been one of the best performing sectors during COVID-19. Delta Airlines also report on Wednesday which will undoubtedly be sad reading but hopefully there is some light at the end of the tunnel. Key focus for Delta Airliners is the balance sheet damage as that feeds directly into default risks etc. On Thursday we have Intel which will give the first glimpse of end-user demand in the computing industry and Credit Suisse will also report providing the first and most likely shocker to European investors. Friday we have earnings from American Express which could be very bad given the consumer credit card provisions delivered by banks last week. Boeing is also reporting on Friday and could be the positive surprise despite the negative backdrop from airliners as the company is restarting 737 Max production in May. Finally we have many Swedish earnings this week so we expect volatility in OMX this week and we believe Swedish earnings could be the first full picture disappointment for investors as Sweden’s procyclical companies must be hurting big time during these lockdowns.

Below is a day by day summary of the key events, courtesy of Deutsche Bank

Monday

Data: Germany March PPI, Italy February current account balance, Euro Area February current account balance, Canada February wholesale trade sales, US March Chicago Fed national activity index

Central Banks: BoE’s Haldane and Broadbent speak

Earnings: IBM

Other: Second UK-EU future relationship negotiating round begins

Tuesday

Data: UK March claimant count, February employment change, unemployment rate, average weekly earnings, Japan final March machine tools orders, Germany April ZEW survey, Canada February retail sales, US March existing home sales

Central Banks: Reserve Bank of Australia release minutes of April policy meeting, ECB’s Stournaras speaks

Earnings: The Coca-Cola Company, Netflix, SAP, Philip Morris International, Lockheed Martin, Texas Instruments, BHP

Wednesday

Data: UK March CPI, RPI, PPI, France April business confidence, Italy February industrial orders, industrial sales, US weekly MBA mortgage applications, February FHFA house price index, Canada March CPI, Euro Area advance April consumer confidence

Central Banks: Central Bank of Turkey policy decision

Earnings: AT&T, Thermo Fisher Scientific

Thursday

Data: Preliminary manufacturing, services and composite PMIs from Australia, Japan, France, Germany, Euro Area, UK and US, South Korea preliminary Q1 GDP, Japan final February leading index, Germany May GfK consumer confidence, UK March retail sales, public sector net borrowing, UK April CBI quarterly industrial trends survey, US weekly initial jobless claims, March new home sales, April Kansas City Fed manufacturing activity index

Earnings: Intel, Eli Lilly and Company, NextEra Energy, Union Pacific, Credit Suisse, Hyundai

Other: EU leaders hold video conference

Friday

Data: UK preliminary April GfK consumer confidence, Japan March nationwide CPI, February all industry activity index, Germany April Ifo business climate indicator, US preliminary March durable goods orders, nondefence capital goods orders ex air, final April University of Michigan sentiment

Central Banks: Russian central bank policy decision

Earnings: Verizon Communications, Sanofi, T-Mobile, American Express

Finally, here is a focus just on US events, coutesy of Goldman Sachs, which notes that the key economic data releases this week are the jobless claims report on Thursday and the durable goods report on Friday. There are no scheduled speaking engagements from Fed officials this week, reflecting the FOMC blackout period.

Monday, April 20

There are no major economic data releases scheduled today.

Tuesday, April 21

10:00 AM Existing home sales, March (GS -10.0%, consensus -8.2%, last +6.5%); After surging by 6.5% in February, we estimate that existing home sales fell by 10.0% in March. Existing home sales are an input into the brokers’ commissions component of residential investment in the GDP report.

Wednesday, April 22

09:00 AM FHFA house price index, February (consensus +0.3%, last +0.3%)

Thursday, April 23

08:30 AM Initial jobless claims, week ended April 18 (GS 4,300k, consensus 4,500k, last 5,245k); Continuing jobless claims, week ended April 11 (consensus 17,271k, last 11,976k); We estimate jobless claims remain elevated at 4,300k in the week ended April 18.

09:45 AM Markit Flash US manufacturing PMI, April preliminary (consensus 38.0, last 48.5)

09:45 AM Markit Flash US services PMI, April preliminary (consensus 31.3, last 39.8)

10:00 AM New home sales, March (GS -15.0%, consensus -15.8%, last -4.4%); We estimate that new home sales fell by 15.0% further in March after declining by 4.4% in the previous month.

11:00 AM Kansas City Fed manufacturing index, April (consensus -34, last -17)

Friday, April 24

08:30 AM Durable goods orders, March preliminary (GS -19.0%, consensus -12.0%, last +1.2%); Durable goods orders ex-transportation, March preliminary (GS -12.0%, consensus -6.0%, last -0.6%); Core capital goods orders, March preliminary (GS -10.0%, consensus -6.2%, last -0.9%); Core capital goods shipments, March preliminary (GS -7.0%, consensus -7.0%, last -0.8%); We expect durable goods orders to fall 19% in the preliminary March report, reflecting a jump in Boeing cancellations, sharp declines in rail freight, and reduced domestic and foreign demand related to the coronavirus. We estimate a 10% drop in core capital goods orders and a 7% decline in core capital goods shipments.

10:00 AM University of Michigan consumer sentiment, April final (GS 67.5, consensus 68.0, last 71.0); We expect the University of Michigan consumer sentiment index to decline by 3.5pt to 67.5 in the final estimate for April, reflecting further jobless claims and declines in the GS Twitter Sentiment Index. The report’s measure of 5- to 10-year inflation expectations increased by two tenths to 2.5% in the preliminary report for April.

Shake Shack To Return $10 Million PPP Loan After Large Businesses, Hedge Funds Criticized For Tapping

Shake Shack plans to return the $10 million support loan it tapped from the Paycheck Protection Program (PPP) amid brewing outrage over large businesses accessing government funds that were intended to save small businesses during the coronavirus pandemic.

According to Bloomberg, over a dozen publicly traded companies with revenue topping $100 million participated in the stimulus before the $349 billion rescue package ran out of money within two weeks of being launched.

“While the program was touted as relief for small businesses, we also learned it stipulated that any restaurant business — including restaurant chains — with no more than 500 employees per location would be eligible,” said Shake Shack CEO Randy Garutti in a joint statement with founder Danny Meyer.

“Shake Shack was fortunate last Friday to be able to access the additional capital we needed to ensure our long term stability through an equity transaction in the public markets,” the statement continues. “We’re thankful for that and we’ve decided to immediately return the entire $10 million PPP loan we received last week … so that those restaurants who need it most can get it now.“

The pair also lobbed criticism at the PPP, which ‘came with no user manual and was extremely confusing.’

“Late last week, when it was announced that funding for the PPP had been exhausted, businesses across the country were understandably up in arms,” Garutti and Meyer said. “If this act were written for small businesses, how is it possible that so many independent restaurants whose employees needed just as much help were unable to receive funding? We now know that the first phase of the PPP was underfunded, and many who need it most, haven’t gotten any assistance.” -Bloomberg

According to an SEC filing, the US-based burger chain which employs approximately 45 employees at each of its 275 locations, received the $10 million on April 10 through JPMorgan. The company is facing operating losses of more than $1.5 million per week, according to the statement.

Shake Shack made an operating profit of $128 million on revenues of $595 million in 2019, according to the Financial Times, while Bloomberg notes that it’s one of the fastest-growing restaurant companies in America.

According to the National Restaurant Association, 417,000 restaurant employees lost their jobs in March – a 6x increase in the record monthly decline set in October 2000. The sector employs approximately 15.6 million people in the US.

The sight of big companies getting aid while mom-and-pops complained they’d been frozen out of funding has sparked criticism of who was rescued by taxpayer dollars and who wasn’t. Asked whether such large, publicly-traded companies should be eligible for PPP funds, President Donald Trump on Sunday spoke about the role of franchisees as small businesses.

“I don’t know much about any of those companies. But a lot of times they’re owned by franchisees, where they own one or two places,” Trump said at a White House press briefing. “So a lot of that would depend on what the formula is.” -Bloomberg

According to Shake Shack’s website, they do not franchise – unlike some Ruths Chris steak houses and Potbelly sandwich stores, which accessed PPP funds. Potbelly defended their loan in a statement to Yahoo! Finance, saying that their workers are “vital to our economy.”

Ruths Chris is another story altogether worth checking out.

.@RuthsChris had $42.2 million in profits last year, spent $5.2M buying its own stock, and pays its CEO $6.1M

It has $86M in cash reserves

It just received $20M in taxpayer money from a fund meant to keep “small businesses” afloat

The Small Business Association approved $342.3 billion in loans just 13 days after the PPP was launched – with the rest of the $349 billion going towards fees and processing.

The SBA said in a statement with the Treasury Department that the “vast majority of these loans — 74% of them — were for under $150,000,” however an SBA report revealed that 2% of applications for the program accounted for nearly 30% of the funding.

Nine percent of the pot went to companies, such as Fiesta Restaurant Group Inc. that got loans of at least $5 million. Fiesta, which owns and franchises Pollo Tropical and Taco Cabana restaurants, said in a regulatory filing that it got $10 million. The company’s annual sales totaled $661 million and it had about 10,500 employees at the end of last year.

Sandwich chain Potbelly Corp., which had sales last year of $410 million and employed 6,000 people, also received $10 million.

Other companies that reported getting small-business funding are Zagg Inc., which makes protective coverings for smart phones and had $522 million in sales last year; Hallador Energy Co., a coal-mining company with $323 million in 2019 revenue; adventure-travel and cruise company Lindblad Expeditions Holdings Inc., which reported $343 million in sales last year; and data storage company Quantum Corp., with $403 million in sales. –Yahoo Finance

Last week we reported that hedge funds had also come under fire for participating in the program, which again, was designed for small businesses to cover payroll, rent and utilities for up to eight weeks.

“Most of the money has gone to much larger entities and the very small entities for the most part have been left behind,” said John Arensmeyer of the Small Business Majority – an advocacy group for small companies. “We’re dealing with finite dollars,” he added. “Even if more money is put into the system, we really need to prioritize very small businesses over publicly traded companies.”

Over the weekend, Congress was in negotiations for an $310 billion extension to the PPP which has been held up by House Speaker Nancy Pelosi (D-CA), who rejected the idea of a “clean” which would only help small businesses – and has instead insisted that Democratic interests be included in the next package. The upcoming legislation will reserve no less than $200 billion for firms which have 20 or fewer employees.

Markets are currently on fast-forward as politicians are also on fast-forward on when we will remove economic lockdowns and go “back to normal” – as if the virus isn’t the one in the driving seat in all this. In that regard let’s reconsider some of the projections we made in a report published on 13 March titled “28 Weeks Later”, which tried to guess what the world might look like once the immediate threat from COVID-19 has faded. We are just over 28 days on from that report and yet we seem to have already reached many of its conclusions – history on fast-forward along with markets, it seems. Specifically, we argued we would see:

Massive fiscal stimulus;

Fiscal and monetary policy joined at the hip via MMT;

A stronger role for the state;

Talk of a structural shift in market paradigms as globalisation breaks down;

Discussions over supply-chains shifting based not just on price, but on national security – on which note Japan’s latest fiscal stimulus has USD2.2bn set aside to help encourage Japanese firms to leave China, and even China dove White House Economic Advisor Larry Kudlow has stated he’s like to incentivise US firms to do the same; and

A stronger USD, most so vs. EM FX.

Moreover, we argued “we can expect a further significant deterioration in US-China relations.” This looks to be arriving – and yet it is not an area where the market seems willing to play fast-forward…for the moment.

For example, from the US side President Trump openly says he is “not happy” with China and is threatening unspecified “consequences” if evidence emerges that Beijing was complicit in allowing COVID-19 to spread internationally. Even meeker voices such as the UK and Australia are demanding transparency on this front – and bolder ones, like the Henry Jackson Society, have posited that China could be liable for USD trillions in damages. Indeed, as we enter the 2020 US election run-up we also have Trump dubbing his likely Democratic challenger as “Beijing Biden”, while Biden is attacking Trump as having been duped by China’s leaders in allowing COVID-19 to spread. None of this bodes well for future US-China relations – or what parts of the “Phase One Trade Deal” will remain once the dust settles.

Meanwhile, from the Chinese side we have seen aggressive “Wolf Warrior” rhetoric from Chinese diplomats, which has ruffled feathers globally. There have been widespread reports of discriminatory actions targeting foreigners in China, who are now seen as potential virus carriers: this has led to official protests from some African states, for example. Moreover, last week saw a slew of actions in Hong Kong, which has obviously slipped from global focus this year compared to last.

First, China’s liaison office (the de facto embassy) accused opposition law-makers of “malicious filibustering”, suggesting they should be dismissed from office for breach of oath; Reuters reported three anonymous senior judges had told them that judicial independence and rule of law are under threat from Beijing interference – a claim rebutted by Hong Kong and Chinese officials; the liaison office then openly lobbied for the rapid passage of new national security legislation to “prevent foreign interference” and prohibit “treason, secession, sedition, and subversion” against Beijing, which Hong Kong CEO Carrie Lam partly echoed; the same office then announced it is not bound by Article 22 of the Basic Law, which states mainland agencies cannot interfere with Hong Kong’s autonomy – again Lam demurred; and this weekend saw the arrest of 15 high-profile pro-democracy politicians, advocates, and activists in Hong Kong for partaking in illegal protests last year. This last step has drawn international condemnation and recent developments have worrying potential implications for the annual review the US undertakes on Hong Kong’s autonomous status. (And, again, Biden is attacking Trump for being too soft on China in this area.)

One other recent action in China also speaks volumes. Taiwanese media reports that China is to ban online gamers from interacting with foreigners. (Note this is a massive industry where China is the world’s largest single market). What is a vast informal channel of communication between China and the outside world is apparently to be severed. Moreover, the report also claims that online games will be monitored at all times and can no longer contain plagues, zombies, map-editing, role-playing, or any in-game group organizations, clans, or unions. Does this all speak to far larger Great Game playing out?

Of course, one can easily be distracted when China slashes its benchmark lending rate 20bp from 4.05% to 3.85% (for 1-year loans), which underlines that it is not recovering as well as it wishes to project, and yet is still far, far less stimulus than we are seeing elsewhere. Equally, one can be dragged aside by reports that the ECB is pushing for the establishment of a ‘bad bank’ in the Eurozone to suck up non-performing loans – which Brussels apparently does not want to see. Let’s also not forget chatter that the US might have to start using yield curve control policies to keep T-bill yields where they want them to be as issuance soars – which would be a further nail in the coffin for capital markets as actual markets rather than political liquidity channels, something we have long suggested would be logically congruent to MMT. Naturally we should also not overlook that West Texas Intermediate oil dipped below USD15 per barrel on Monday morning, a 21-year low.

However, if we really are seeing ‘game over‘ for US-China relations post-COVID then at some point markets are going to go into fast-forward again….and this time they can’t bully the Fed into cutting rates to zero because we are already there.

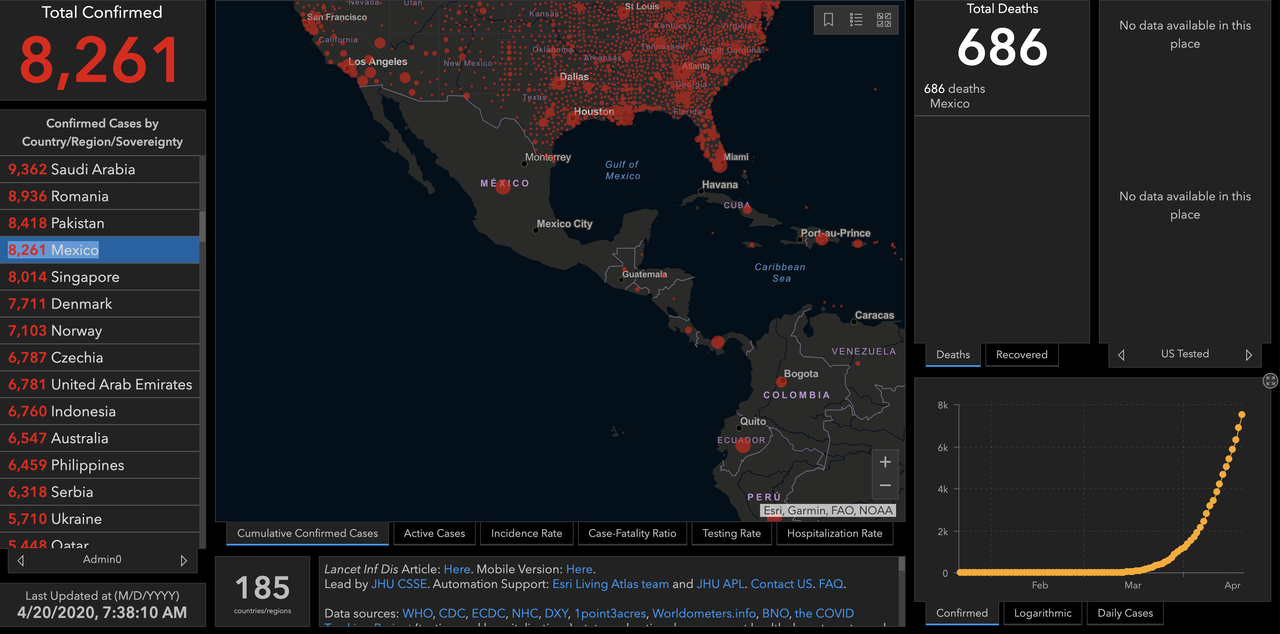

Brazil and Peru are grappling with the two largest outbreaks in Latin America, but Mexico is increasingly finding that the virus is more widespread in Mexican society than AMLO – who dismissed the threat from the virus in even more strident tones than Trump – and the government had expected.

Mexico has confirmed 8,261 cases and 686 deaths, according to Johns Hopkins.

Unlike in the US, most Mexicans receive their health care via the government. However, a streak of under-investment in recent years has left Mexico’s public-health care system in a much more fragile state than the systems of other ‘hot spots’ like in Italy and Spain, which also have mostly government-funded health care.

Since Mexico doesn’t have nearly as much funding, or as many doctors and nurses per capita as countries like the US and the rest of the developed world, outbreaks at hospitals have raised particular alarm. Last night, the Washington Post published a story about outbreaks at several government-run hospitals that have left several doctors and nurses dead from COVID-19. Many of these hospitals didn’t implement strict protocols needed to handle these patients without allowing the virus to spread. One reason they felt inclined not to exercise precaution was the messaging coming from the Mexican government, and its left-wing populist leader, AMLO.

The coronavirus outbreak in Mexico’s steel capital started at the very place that was supposed to help stop it.

Social Security Hospital No. 7, a towering 240-bed facility, is the main public medical center in the northern city of Monclova. But when a 42-year-old truck driver arrived with pneumonia-like symptoms last month, the hospital didn’t isolate him. Within two weeks, he was dead of covid-19.

Soon, a doctor and an administrator had also perished. Ultimately, 41 employees of the hospital wound up testing positive for the virus.

It was the first in a series of outbreaks at hospitals that have rattled Mexicans and raised questions about the Social Security Institute, the country’s biggest public health network. Nurses and doctors have held protests around the country. The governor of Baja California, Jaime Bonilla, lashed out at federal authorities for the lack of protective gear in his border state, saying doctors were “dropping like flies.”

Separately, local press has reported that hospitals in Mexico City – the largest, and most densely-populated metropolis in North America – are “nearing saturation point” according to a BBG summary of their reporting. Per BBG, hospitals in Mexico City have also started “turning away” some patients, just like certain hospitals in Tokyo.

Hospitals in Mexico City are nearing saturation point after they received 100 more Covid-19 patients requiring intubation in just two days, newspaper El Norte reported, citing Mayor Claudia Sheinbaum.

Of the city’s 16 municipalities, the most affected is Iztapalapa. The General Hospital there is at capacity and is turning away patients, Sheinbaum said. As more people are redirected to the two other hospitals in the same neighborhood, they’re also now full. The city, which is home to 8.8 million people, had 2,299 cases as of yesterday and 178 deaths. The country reported 650 deaths and 7,497 confirmed cases.

Fortunately, President Trump has promised to send Mexico 1,000 ventilators by the end of the month, which is critical as the number of patients requiring intubation soars. Mexico’s ratio of deaths to confirmed cases is the highest in Latin America, an obvious sign that the outbreak is very likely far more widespread than official numbers reflect.

The Coronavirus first wave is ebbing across Northern Europe and New York. Nations are now contemplating limited economic reopening. Government bailouts, support packages and central bank QE infinity have handed markets an extraordinary boost – it’s one of the biggest bull rallies on record!

Let joy be unconfined…

What’s not to like?

Well… don’t get me started. One of the big issues for markets is separating the news that actually matters from the stuff that is just news noise.

Real news is how effective the C-19 mitigation, QE-infinity and unlimited spending packages are likely to prove in the real world.

They are certainly working well for markets – which have arbitraged them to the max. The question is consequences – how much money will actually reach the real economy, how will it be spent, against how much will simply continue to fuel financial asset price inflation? All that money in financial markets keeps pushing up prices – just like tulips push out the ground. As long as central banks are willing to give a free put – does it matter for markets that economies are in free-fall? (I suspect.., at some point it will.) Mind the Gap.

Real news is that Oil prices didn’t actually need a spat between Saud and Russia to tumble – it’s the absolute dearth of demand for the black black oil that’s killing prices. What does that tell us about the real prospects for the global economy? Oil prices plunge to 20-year low as virus hits demand.

Real news will be about what markets are not telling us. As banks around the globe find credit lines being fully drawn down by corporate customers, they are being forced to lend even more. Virus Forces Deutsche Bank to Confront Fears. It’s the old adage – if you owe the bank a $1000, you are in trouble. If you owe the bank $10 billion, then the bank is in trouble. Yet, lending more and more to already over-levered companies to see them through the C-19 Shutdown, is apparently not a problem. It’s a curious sort of doublethink… but heck, markets buy it.

Real news is Ford demonstrating how it’s now perfectly possible to believe 6 impossible things at once. It tumbled into Fallen Angel status last month when it lost its investment grade rating. (How careless..) But, backstopped by the Fed declaration that, in their eyes, anyone who was investment grade on March 22nd, remains investment grade, it was able to issue a $10 bln bond issue at sub 10% yields which is eligible for QE Infinity. The institutional investors who posted over $20 bln of bids are keen to lock in yields today, secure in the knowledge the Fed will bail them if it gets worse, and the next similar deal will probably flip the 9% coupon to a 6%! I wonder how many more cars Ford sold as a result of the bond issue, and how many car buyers will still have incomes when Ford has to start paying it back? Just asking.. ?

Real news will be how monetary bailouts on the market and fiscal handouts to the real economy actually work. In the UK we have painfully slow delivery of policy promises. The second US SME bailout package is held up because the Democrats are trying to ensure the money actually goes to the small companies unlikely to survive the month is real news – the bulk of the first $350 bln rescue package was scooped up by big firms with the legal and financial resources to do so. The big pigs got to the trough first. Shake Shack, Potbelly Among Chains Tapping Small-Biz Funds.

Real News will be what companies say through this earning season about long-term plans and expectations. If you strip out the distortions of unlimited free money and QE infinity, markets are ignoring record P/E levels, and anticipate swift recovery. If companies are telling us about plans to mitigate for slowing business conditions, to cut costs and rationalise jobs in the wake of anticipated slowdown.. then we have a disconnect. Goldman Sees Record US Corporate Cash Spending Cuts This Year.

Real News will be just how deep the business pain goes across sectors. The pain in some, like aerospace and tourism, is already understood. How coronavirus brought aerospace down to earth. How others will react to slowing demand, lower discretionary consumer spending, and continuing uncertainty will be critical. Again, we’ll be listening for clues in what companies say.

Real news will be what the Europeans decide on Thursday re debt support for Italy (and by extension the rest of enfeebled Europe). It’s a big decision – do they tinker with the Euro’s creaking mechanisms to fudge more support, or do they come up with something that’s long term effective and transformational for Europe. Italy PM Calls for EU Solidarity.

Europe needs to solve for long-term growth, structural and youth unemployment, and increased unification to move the European economy forward and make it relevant. Or they can “kick the can” down the European goat track a little longer. Solving Europe is a real event with real market implications in terms of how the looming European Sovereign Debt crisis evolves and plays out.

Real news is working out how the future global economy is going to shape up – especially in terms of China and the Rest of the World. It feels like lines are being drawn. The papers are full of conspiracy theory. It’s easy to believe the Chinese have massively fudged the numbers of infections and deaths to avoid the worst possible outcome – making the Party Government look incompetent, and President Xi look complicit.

The distrust looks likely to deepen the divides between the Occident and Orient – with a host of implications for protectionism, tech eco-systems, and global supply chains. China arrested a host of Hong Kong Pro-democracy protestors at the close of last week. Under the cover of a pandemic, China is dismantling Hong Hong’s last freedoms. They’d been betting the world would not notice – too concerned with the rising daily C-19 numbers.

I am amused at some of the threads I’ve been following on business social media. Chinese Linked-in and Twitter users are either extremely naïve or are propaganda bots – responding to new ECB officials are concerned about Chinese takeovers while European countries were struggling, chat bot accounts showing pictures of pretty Chinese girls were writing about how beneficent Chinese capital is prepared to step in and rescue failing western firms – even throwing in sops like setting up R&D facilities in newly acquired Occidental companies. It would make me giggle – if it wasn’t so serious..

But when it comes to what is really important News, and what isn’t these days.. then I am beginning to wonder if markets actually matter any more?

When central banks make sure all companies are special by ensuring all survive, then none are special. The discipline of financial rectitude and the fear of default count for naught.

The sanction of bankruptcy is meaningless.

If you want to make successful investment choices now, work out which companies will get the biggest bang from the government buck, not just those most likely to survive the 2nd quarter pretty much earnings free, devoid of income and shuttered.

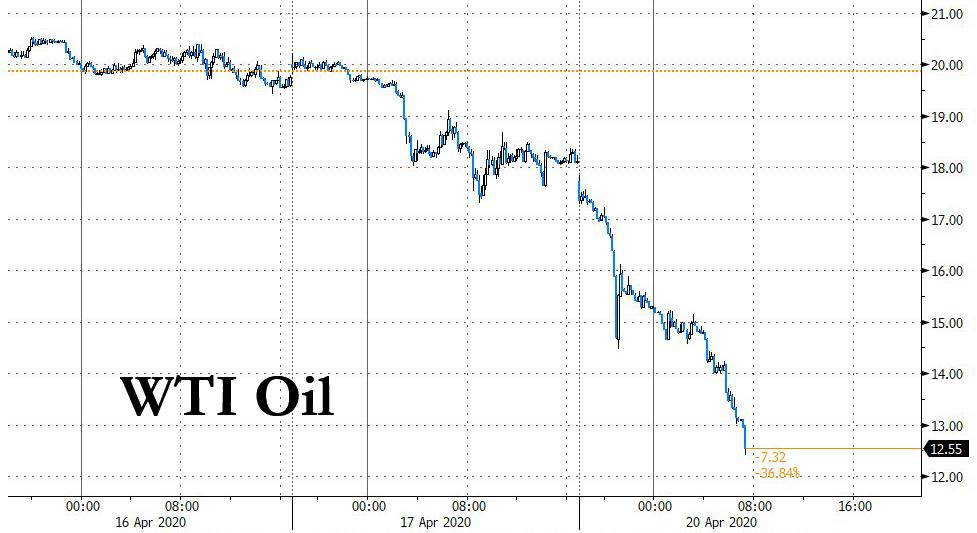

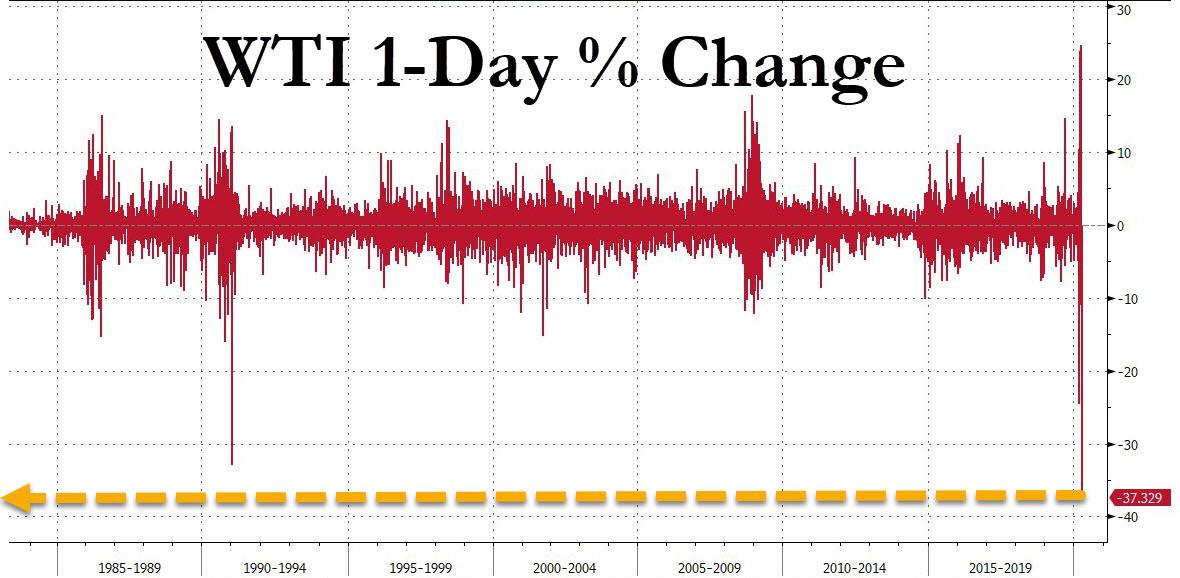

Futures Plunge As WTI Crashes By Most On Record, Tumbling To $11 Per Barrel

Oil prices crashed the most on record with the May WTI futures contract hitting its lowest level since 1999, plunging as low as $11 or down 38%, as nobody wants to take actual physical storage amid widespread fears crude storage will soon be full; meanwhile companies prepare to report the worst quarterly earnings since the financial crisis, while tens of thousands of people continue to get sick every day with the coronavirus.

While Brent was only down $1.12, or 4%, at $26.96 a barrel on Monday morning, the carnage took place in the landlocked WTI, whose May contract fell $5.70 to its lowest since March 1998 though the sell-off was exaggerated by the contract’s Tuesday expiry because no one wants to be left long to take delivery as there is nowhere to put the physical product. In any case, the 37% drop was the biggest one-day drop on record!

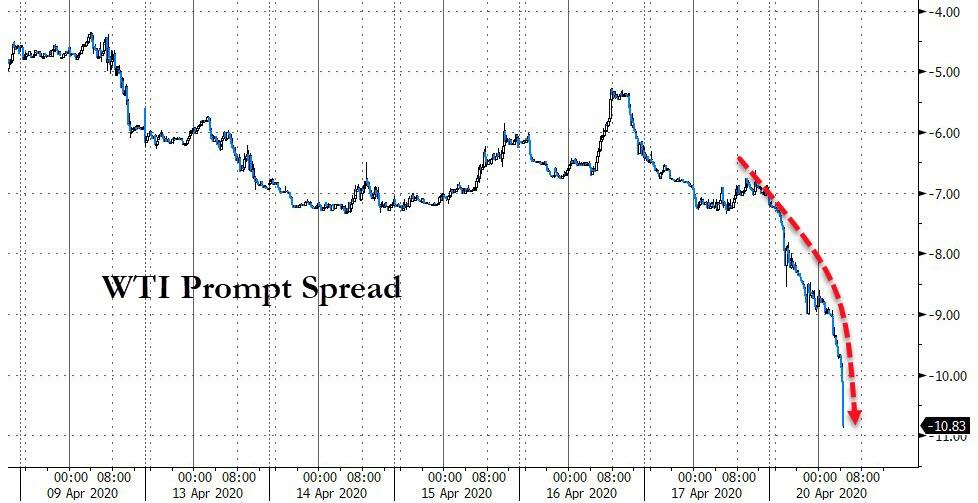

“The May contract is set to expire tomorrow and the bulk of the open interest and volume is already in the June contract,” said ING’s head of commodities strategy, Warren Patterson. To be sure, the June contract, which is more actively traded, fell only $2.18, or 8.7%, to $22.85 a barrel, sending the prompt spread to a record $11/barrel.

Not helping oil was an interfax report that Russia increased oil output by almost 1% in the last 3-days. While the OPEC+ deal comes into effect on May 1st, Russia is not bound by the pact to reduce its output until then; and – it appears – Moscow is looking to make the most of the next 10 days, even if it means sending the front-end to zero.

While some may dismiss the plunge in the front contract, the reality is that the world most popular oil ETF, the USO which, is driven mostly off the front end of the curve has crashed to just $3.73 despite registering a record one-day inflow of $552.5MM on Friday, and steamrolling countless retail traders who went long USO after the OPEC+ deal only to see their “profits” turn into catastrophic losses.

Commenting on the oil price move, Bloomberg points out that

the first of these spikes, in December 2008, came as the S&P 500 was putting in a nice rally of some 27.5% on a trough to peak basis from mid-November to early January. Perhaps it’s a coincidence that the index is once again ripping higher as crude exhibits this type of behavior. But maybe the oil market is offering a warning of just how significant the economic damage will be — damage that you could argue is no longer reflected in the price of equities.

Meanwhile, with a record 198MMb/d now stored offshore, the volume of oil held in U.S. storage, especially at Cushing is rising as refiners throttle back activity in the face of weak demand. “As production continues relatively unscathed, storage is filling up by the day. The world is using less and less oil and producers now feel how this translates in prices,” said Rystad’s head of oil markets, Bjornar Tonhaugen.

The mood in other markets was also gloomy as the first-quarter earnings season gets underway. Analysts expect STOXX 600 companies to post a 22% plunge in earnings, which would represent the steepest decline since the 2008 global financial meltdown, IBES data from Refinitiv showed.

After starting off higher, U.S. equity futures fell alongside European and Asian stocks on Monday as investors grappled with everything from the spread of the coronavirus to oil’s collapse and the next raft of corporate earnings. Contracts on the S&P 500 extended their decline through the European morning as the price of West Texas oil cratered.

The Stoxx Europe 600 Index fluctuated before turning lower, with energy companies slumping. Shares retreated across much of Asia, though the benchmark in Shanghai rose. The euro, pound and yen all weakened. European bonds mostly dropped. The German economy is in severe recession and recovery is unlikely to be quick, given that many coronavirus-related restrictions could stay in place for an extended period, the Bundesbank said on Monday.

Earlier in the session, Asian stocks also fell, led by health care and materials, after rising in the last session. Markets in the region were mixed, with Australia’s S&P/ASX 200 and Jakarta Composite falling, and Thailand’s SET and Shanghai Composite rising. The Topix declined 0.7%, with Takakita and Fuji PS falling the most. The Shanghai Composite Index rose 0.5%, with Sichuan Xichang Electric Power and Shanghai Sanmao Enterprise Group posting the biggest advances. Japanese exports declined the most in nearly four years in March as U.S.-bound shipments, including cars, fell at their fastest rate since 2011.

It was not all bad news with coronavirus infection rates clearly slowing in several major economies, while investors were bracing for the pace of earnings season to pick up.

IBM, Coca-Cola Co. and Netflix Inc. are among companies due to report in the coming days. Meanwhile, governments and policy makers are continuing attempts to limit the economic damage of the outbreak. U.S. lawmakers are moving closer to a deal to top up funds for small businesses, China pledged more stimulus as banks lowered borrowing costs and European officials are discussing creating a bad bank for the region, according to the Financial Times.

In rates, 10Y TSY yields were slightly lower, trading at 0.6273% with bunds trading through Friday’s best levels and peripheral debt widens to core as regional sensitivities around jointly issued debt come to the fore. Moves are modest, save for Italy as short-dated yields rise 14bps. Cash USTs drift higher, outperforming Bunds by ~1bp at the long end. Gilts close their opening gap, brushing off comments from BOE officials. The Bund curve bull-steepened, yet underperformed Treasuries; Italian debt extended its decline, underperforming euro-area peers amid speculation the nation’s Treasury may announce a bond syndication this week. Japan’s government bond yield curve bull flattened as the government was seen boosting issuance of short-tenor bonds to fund its extra budget, which was boosted by 8.9 trillion yen to fund cash handouts

In FX, the Bloomberg Dollar Spot Index firmed along with Treasuries as risk sentiment was fragile, with European stocks mainly mildly positive and U.S. equity futures slipping as earnings season intensifies. Oil-linked currencies tanked as crude prices plunged further. The Dollar initially gave back most of Asia’s gains, before surging higher again and back to session highs. Australian and New Zealand dollars led Group-of-10 gains; the kiwi gained after the government said it will partially ease lockdown restrictions next week. The greenback’s overall advance came in the wake of the Fed’s slowing QE purchases and with the earlier rally in equity markets loosing momentum. The Norwegian krone and the Canadian dollar led losses following a deepening slump in oil prices to the lowest level in more than two decades.

Elsewhere in commodities, spot gold spiked to session highs in early US trading, rising to $1,690. Base metals are mixed, LME Nickel rallies over 2.5%, aluminum drops 1.2%.

Expected data include Chicago Fed National Activity Index. Halliburton, Equifax, and IBM are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.9% to 2,844.75

STOXX Europe 600 down 0.02% to 333.41

MXAP down 0.8% to 143.94

MXAPJ down 0.6% to 465.88

Nikkei down 1.2% to 19,669.12

Topix down 0.7% to 1,432.41

Hang Seng Index down 0.2% to 24,330.02

Shanghai Composite up 0.5% to 2,852.55

Sensex up 0.3% to 31,679.98

Australia S&P/ASX 200 down 2.5% to 5,353.01

Kospi down 0.8% to 1,898.36

German 10Y yield fell 1.7 bps to -0.489%

Euro down 0.1% to $1.0864

Italian 10Y yield fell 4.0 bps to 1.619%

Spanish 10Y yield rose 1.6 bps to 0.832%

Brent futures down 3.7% to $27.04/bbl

Gold spot little changed at $1,682.21

U.S. Dollar Index down 0.1% to 99.67

Top Overnight News

Signs emerged that the global pandemic is easing in some hot spots, as regions from Spain to New York saw a slowdown in fatalities, though some Asian countries wrestled with worsening conditions

Chinese banks lowered borrowing costs and the government promised to sell another 1 trillion yuan ($141.3 billion) in bonds to pay for stimulus spending after the economy had its first contraction in decades due to the coronavirus outbreak

Spain will propose a rescue fund for Europe of as much as 1.5 trillion euros at an April 23 summit, according to newspaper El Pais

Britain and the EU will restart talks on Monday over their future relationship, with time running out to get an agreement after a six-week interruption caused by coronavirus

ECB officials have held early talks with the European Commission’s department for financial stability and capital markets on setting up a eurozone bad bank that would take billions of euros in debt off lenders’ balance sheets, the Financial Times reported, citing people briefed on the discussions

President Donald Trump raised the prospect that China deliberately caused the Covid-19 outbreak that’s killed over 39,000 Americans and said there should be consequences if the country is found to be “knowingly responsible”

Democrats and the Trump administration are near an agreement for Congress to act this week on a deal as large as $500 billion putting more funding into a tapped-out small business aid program and providing money for coronavirus testing and overwhelmed hospitals

Markets are pricing for the spread between Libor and overnight index swaps — a proxy for the risk-free rate — to compress sharply into June as funding conditions improve. Huge activity in both Eurodollar options and futures — used to bet on the path of Libor — suggest divisions on the pace of the easing

Asian equity markets traded mixed amid the ongoing fallout from the coronavirus pandemic and extended rout in oil prices which briefly saw the WTI May contract drop below USD 15/bbl for the first time since 1999 and the June contract briefly slip below USD 23/bbl with the sell-off due to a collapse in demand, concerns of declining storage capacity and ahead of Tuesday’s contract settlement. ASX 200 (-2.5%) and Nikkei 225 (-1.2%) were negative with the energy sector front-running the broad declines in Australia alongside the oil market woes and as Caltex also suffered from Couche-Tard abandoning its pursuit of the Co., while Tokyo risk appetite was sapped after mostly weaker than expected trade data including the largest decline in exports since 2016. Hang Seng (-0.2%) and Shanghai Comp. (+0.5%) were somewhat indecisive although outperformed their regional peers after the PBoC cut the 1-year and 5-year Loan Prime Rates by 20bps and 10bps respectively as expected, while the state planning agency noted that China will roll out more forceful and targeted fiscal, financial and employment policies. Finally, 10yr JGBs lacked demand following recent comments from the Japan Securities Dealers Association that global funds sold record levels of 10yr JGBs last month and with Japan’s government planning to issue more than JPY 25.69tln to fund supplementary budget, although losses were stemmed by support at 152.00 and amid weakness in Japanese stocks.

Top Asian News

China Pledges More Stimulus as Banks Cut Lending Rates

India’s Ban on Flying to Stay Until Virus No Longer a Danger

Singapore’s Daily Virus Infections Top 1,000 For First Time

European equities have given up gains since the open and trade mostly lower (Euro Stoxx 50 -0.4%), as the cautious tone from APAC trade reverberated across the continent. US equity futures see more pronounced losses in comparison following the State-side gains posted on Friday. European sectors remain mixed with no clear indication of the risk-tone, whilst Energy and Materials reside at the bottom of the bunch. Looking at the breakdown, the downside sees Basic Resources alongside Oil & Gas, whilst Healthcare resides at the other end of the spectrum; Travel & Leisure remains relatively flat. In terms of movers, miners see pressure in European trade after giant Vale reported Q1 iron ore sales -6.8% YY and iron ore production -18% YY. Co. cut its FY20 iron ore production to 310-330mln tons vs. Prev. 340-355mln tons amid delays to the resumption of operations at certain mines. FY nickel production guidance cut to 180-195k tons vs. Prev. 200-210k tons. Thus, Glenore (-1.6%), Rio Tinto (-1.8%), Anglo American (-2.8%), Fresnillo (-2.5%), BHP (-1.3%) all see losses. European bank also see downside after reports downplayed ideas that the a EZ bad-bank will be formed to deal with debt from the 2008 crisis. Elsewhere, Phillips (+6.4%) extends on opening gains despite overall downbeat earnings as the Co. aims to return to growth and improved profitability in H2 2020. Sanofi’s (+1.1%) Head of French business said the Co. will pay out a dividend this year, with the overall value modestly higher YY, albeit shares are moving in tandem with the European Healthcare sector.

Top European News

Riksbank Governor Lashes Out at Efforts to Strip Bank of Powers

CEO of Norway’s Wealth Fund Faces Probe After Luxury Jet Use

Nordic M&A Lawyers Say Clients Want to Exit Deals Already Struck

German Virus Cases Rise the Least Since March as Curbs Ease

In FX, the Kiwi only got a fleeting fillip from firmer than forecast NZ inflation overnight, but is outperforming fellow majors on PM Arden’s acknowledgement of the progress made in containing the spread of nCoV to the point that plans are afoot to re-open businesses end lockdown this time next week. Nzd/Usd is firmly back over 0.6000 in response and eyeing resistance ahead of 0.6100, while the Aud/Nzd cross has retreated markedly to test 1.0500 as the Aussie lags below 0.6400 vs its US peer amidst weak oil and other commodity prices, albeit with the DXY unable to retain a grasp of the 100.000 handle.

CAD/NOK/RUB/MXN – The Loonie, Norwegian Krona, Russian Rouble and Mexican Peso are all suffering alongside crude that is extending losses to deeper multi-year lows ahead of the looming May WTI futures expiry, with Usd/Cad hovering around 1.4050, Eur/Nok above 11.3000, Usd/Rub circa 74.5900 and Usd/Mxn back over 24.0000.

GBP/JPY/CHF/EUR – Pragmatic rather than poignant in terms of policy remarks from the BoE via Broadbent and Haldane have not really impacted the Pound, but Cable has pulled back from 1.2500 and Eur/Gbp is edging up towards the 200 DMA (0.8739) despite the draw of a particularly large option expiry at the 0.8700 strike (2.8 bn). Instead, Sterling seems to be suffering from general coronavirus fallout highlighted by IHS reporting the biggest fall in household income since it began publishing data. Similarly, but to a lesser extent due to fading risk sentiment after a mild boost from PBoC rate cuts, the Yen on a softer footing across the board, as Usd/Jpy meanders from 108.00 to 107.00 and Eur/Jpy pivots 117.00. Conversely, the Franc is rebounding from around 0.9700 and still close to 1.0500 against the Euro even though the single currency is forging gains vs the Greenback towards 1.0900 and latest Swiss bank sight deposits reveal even heftier intervention to curb Chf strength.

In commodities, WTI and Brent futures kick the week off on the back foot, with the former’s front-month future (May) -18% but disregarded given its expiry tomorrow and with open interest and volumes minuscule in comparison to the following month (June). There is little by way of fresh fundamental developments to sway the markets, although traders continue to attempt to gauge the supply/demand imbalance against the backdrop of COVID-19. WTI June dipped sub-23/bbl to a low of around USD 22.70/bbl (high USD 24.92/bbl), whilst the Brent June future losses further ground below USD 28/bbl, having printed a fresh intraday base at 27.06/bbl. Meanwhile, the Arb between the two June contracts has widened to almost USD 4/bbl vs. sub-3/bbl on Friday. Elsewhere, spot gold continues to be subdued below USD 1700/oz, with a firmer Buck providing further pressure to the yellow metal. Copper prices largely tracked lower with APAC sentiment, whilst action in the USD provides no relief to the red metal. Elsewhere, iron ore futures and nickel prices were supported overnight after mining giant Vale cut its production figures for the metals.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. -3, prior 0.2

DB’s Jim Reid concludes the overnight wrap

Talking of working from home I must say it suits the hours I work far better so I’m a fan. However when something goes wrong at home being able to escape to the office has always been a piece of salvation. Today I could have done with it as yesterday we had a small leak that I discovered in our garage. I came back into the house and told my wife I was going to go back and try to find the stopcock and turn it off. She rapidly replied that she didn’t want me to mess with it and she’d ring the builders that re-plumbed our house after she’d prepared lunch. I went back to lock the garage feeling like my masculinity had been taken away from me and couldn’t resist trying to turn off what I suspected was the stopcock just by the leak. As I turned it the valve blew and a small leak turned into a replica of the Las Vegas Bellagio fountains. Water was gushing out powerfully and spraying everywhere. To cut a long story my wife was furious at me for meddling and given that the stopcock had failed we had to find where the water supply came into the house. Half an hour and a lot of damage later we uprooted a manhole cover at the top of the drive and turned off the whole water supply to the house. That’s where we are still left this morning. Hopefully a plumber will be out this morning to give us water back. I think that classes as a job you can’t do working from home.

Talking of gushes of liquidity, the confusing thing for markets at the moments is the huge dichotomy between what will possibly be one of the worst synchronised global economic slumps in history against what is undoubtedly the largest ever intervention. On the second point DB’s Alan Ruskin showed at the end of last week ( link here ) that global central bank balance sheet expansion has already spiked c.$2.7 trillion since early March which now comfortably eclipses the full peak 12-month increase seen during the GFC (under $2.5tn). On our calculations this is the same amount as the annual total output of either the U.K. or French economies. Two thirds of this increase has come from the Fed so far.

Again using our back of the envelope calculations, given that the global economy is worth around $80 trillion dollars annually and that the IMF last week said it would fall -3% in 2020 (in real terms under the base case) that’s potentially ‘only’ $2.4 trillion of lost activity (less if you add inflation). Relative to the pre-covid trend they forecast $9 trillion of global GDP losses by the end of 2021. Even if you think these numbers are a bit low, when central banks have so far pumped in an annualised $23.4 trillion into the financial system you can see how it’s hard to get a feel for where markets can go. Clearly they won’t keep up that pace of liquidity injections unless economies fall even further but could you really have a situation in 1-2 months’ time where economies are still struggling to fully open and yet equity markets are back at record highs? I don’t think so but you couldn’t rule it out given the ginormous liquidity injections. Crazy times and we haven’t even mentioned the government injections.

In this liquidity rush one crucial part of the financial system that hasn’t managed to suck it up yet is Italian debt where 10yr spreads to bunds have widened around 100bps from the pre-covid tights to 226bps now. They’ve also widened nearly 70bps since the 26th March. For prospective the S&P 500 is up +9.30% since then.

On this hot topic and for other things in the market, Thursday is the key day this week with the EU leaders summit a potentially big event for the future of Europe as they discuss how close the region can get to joint issuance in the near future. Expect creative ambiguity to rule as it normally does on the continent. Nevertheless you would expect more explicit details to be outlined as to how Europe will help Italy. Will this be enough to keep Italian spreads (and domestic politics) in check though? To add to the story, S&P are expected to finalise the review of their BBB rating on Friday. Our colleagues did a piece last week on what the implications are if they are junked. See more here. Staying with European discussions, the FT broke a story yesterday saying the supervisory wing of the ECB is pushing for an EU wide bad bank. It’s not clear whether this story will have legs but it’s clearly something that the weaker members will welcome much more than the stronger ones. Whether it’s NPLs or peripheral debt, can this crisis be the catalyst for more European financial solidarity or will it be one to expose the cracks of an imperfect union.

On the issuance of joint Eurogroup debt, Italian PM Conte said in an interview to Germany’s Sueddeutsche Zeitung yesterday reiterating the need for joint debt issuance highlighting the risk of market contagion if European leaders fail to act on pressure from Italy and Spain. He also added that the ESM rescue fund, Germany’s preferred tool to address the economic impact, “has a bad reputation in Italy.” Meanwhile, Klaus Regling, the ESM’s director-general, said in a separate interview with Italy’s Corriere Della Sera that concerns that the fund’s lending will have two parts — one to specifically deal with the outbreak, the other to reduce budget deficits — was misplaced. He added, “The conditions agreed at first will change during the period of which the line of credit is available. The Eurogroup will clarify it, saying that the only requirement for obtaining the loan is the way in which they spend the money.”

Back to Thursday and not only will we see the latest jobless claims but also the flash PMIs from around the world for April – the first reading covering nothing but lockdowns. If you want a potential worst case scenario Italy was the only Western country to be on full lockdown in the survey period for March and they saw their services PMI fell to an astonishingly low 17.4. In all truth though the market has rightly or wrongly moved on from how bad data could get in the near-term to absorbing up the extra liquidity and also whether economies can open progressively through May.

On this the latest on new cases and fatalities generally continue to show steady improvements as you’ll see in our Corona Crisis Daily. However this improvement is being used by many countries to encourage debate on what exit strategies will look like and the lifting of restrictions at potentially an earlier stage than China did. A risky balancing act.

To markets now where the big mover overnight has been WTI oil which has slumped -16.31% to $15.29/bbl and the lowest in over 20 years. It should be noted however that near-term WTI prices are trading at massive discounts to later-dated contracts – primarily due to concerns about the storage hub in Cushing filling to capacity – with the more active June contract falling by around a third as much (currently trading at $23.73/bbl). Currencies for oil exporting nations are leading the declines this morning with the Norwegian krone down -0.81% while the Canadian dollar is down -0.52%. However, equity markets are more mixed. The Nikkei (-0.95%) and ASX (-1.25%) both down while the Hang Seng (+0.16%), Shanghai Comp (+0.30%) and Kospi (+0.33%) have all posted modest gains. The increase in confirmed virus cases over the weekend appears to be weighing on the markets in Japan as is the latest trade data. Elsewhere, futures on the S&P 500 are little changed.

In other overnight news, President Trump said that the talks between the White House and Democrats in Congress are near an agreement that would add cash to a program aimed at helping small businesses. He suggested that an announcement towards this might come today. Meanwhile, Bloomberg has also reported overnight that the US will allow importers and manufacturers to defer payments on many imported goods for 90 days, a move aimed at freeing up cash for pandemic-hit businesses. The deferral doesn’t apply to anti-dumping or countervailing duties, or so-called Section 201, Section 232 or Section 301 duties. As such, it won’t ease Trump’s duties on China, steel and aluminum, or enforcement actions he took including against Airbus. Elsewhere, China’s finance ministry said overnight that the country will issue an extra CNY 1tn ($141.3bn) in special-purpose bonds “in the near term,” for infrastructure spending. The moves comes after China’s top leaders in politburo meeting on Friday said that the nation is facing “unprecedented” economic difficulties and signaled that more stimulus was in the works.

Elsewhere this week, Q1 earnings will also step up a notch with 88 S&P 500 companies reporting this week and Europe joining the fray with 64 companies. In terms of the highlights to look out for, proceedings kick off today with IBM. Then tomorrow we’ll hear from The Coca-Cola Company, Netflix, SAP, Philip Morris International, Lockheed Martin, Texas Instruments and BHP. On Wednesday, we’ll then get AT&T and Thermo Fisher Scientific. Thursday sees releases from Intel, Eli Lilly and Company, NextEra Energy, Union Pacific, Credit Suisse and Hyundai. And finally on Friday we’ll hear from Verizon Communications, Sanofi, T-Mobile and American Express.

In the background, all this week we’ll see the UK and the EU holding their second negotiating round via videoconference on their future partnership following Brexit. This had originally been scheduled to take place in mid-March but was postponed as a result of the coronavirus pandemic. Although speculation has risen that the transition would be extended given the coronavirus, the UK reiterated last week that they would refuse to extend the transition period, which is due to conclude at the end of this year, even if it were the EU who requested the extension. Should either side seek an extension, under the Withdrawal Agreement they have until the end of June to agree on one. Before that deadline, a “High Level meeting” is planned in June where the two sides will be taking stock of the progress made. A high stakes game but maybe the U.K. are seeing the internal EU divisions over Italy as a chance to take some leverage at the negotiating table.

Reviewing last week now before the day-by-day week ahead listings. Equity markets continued their rally as investors weighed the expectations of economies reopening against the start of 2020 first quarter US earnings and deteriorating economic data. The S&P 500 rose +3.04% on the week (+2.68% Friday), after rising over +12% the week before. This is the first back-to-back weekly gains since the second week of February, before the index hit its highs. Technology stocks outperformed over the week and in general during the downturn, with the NASDAQ rising +6.09% (+1.38% Friday) on the week and is only just under 12% from its highs, versus the S&P 500 14.8% from highs. Bank (-7.64%) and Energy (+0.21%, but +10.4% Friday) sectors were key laggards as investors fretted about loan loss provisions in the former’s earnings and the further slump in oil for the latter. On the more positive side, European equities also rose for a second week in a row for the first time since February, with a strong Friday rally (+2.63%) pushing the Stoxx 600 to finish up +0.50% on the week. Equity performance was more mixed across Europe with correlations falling as different countries and regions roll out different reopening guidelines. The EU summit this week also cast a shadow on peripheral markets. The DAX rose +0.58% (+3.15% Friday), while the Italian FTSE MIB fell -3.21% (+1.71% Friday). The bank and oil heavy FTSE fell -0.95% (+2.82% Friday). Many Asian equities indices also rallied for a second week in a row, with Japanese stocks doing so for the first time since January. The Nikkei rose +2.05% (+3.15% Friday), while the CSI 300 gained 1.87% (+0.98% Friday) and the Kospi rallied +2.89% (+3.09% Friday) on the week. It was the fourth week in a row that Chinese stocks rose, with the CSI 300 roughly -8.7% down from both January highs and the more recent March 5 highs, before the virus outbreaks in the West.

The VIX fell -3.5pts over the course of the week to finish at 38.15, the lowest closing weekly level since February. Credit spreads continued to tighten even as oil again fell on the week. US HY cash spreads were -65bps tighter on the week (-27bps Friday), while IG tightened -27bps on the week (-2bps Friday). In Europe, HY cash spreads were -27bps tighter over the 5days (-3bps tighter Friday), while IG was -9bps tighter on the week (-1bps Friday). Oil was not able to benefit from the Easter weekend OPEC+ cut as investors did not think they went far enough and the gloomy demand forecasts grew more dire. Brent fell -10.80% (+0.93% Friday) while WTI fell -19.73% (-8.05% Friday) though this is partly due to the pressure on first month futures in US crude currently. WTI May futures, expiring next week, are trading at nearly a $7/barrel discount to June futures, close to the biggest spread between 1st/2nd month contracts in 11 years. This is due to concerns that some storage hubs could run into capacity problems.

Even as equity prices improved globally, core sovereign bond yields fell on the week in both Europe and the US, partly driven by increased central bank purchases. US 10yr Treasury yields fell -7.7bps (+1.5bps Friday) to finish at 0.64%, just 10bps from all-time lows. 10yr Bund yields fell -12.5bps (+0.2bps Friday) to -0.47% but peripherals spreads widened out on concerns about how coordinated the European recovery plan will be. French 10yr yields were -5.0bps tighter on the week against bunds (-0.6bps Friday), while Italian yields widened +32.7bps over the 5 days (-4.2bps Friday). Spanish 10yr bonds widened +15.9bps (-1.6bps Friday).

Fears Of Nationwide 9MM Ammo Shortage Sparks Panic Hoarding

The evolution of Americans panic hoarding during the COVID-19 pandemic has ultimately led to the stocking up on guns and ammo.

Gun shop owners report while there are no weapon shortages yet, a run on ammo has undoubtedly been seen across the country.

We first documented the run on guns and ammo in mid-March, identifying shops across many states with long lines of patrons, waiting to get their hands on AR-15s, shotguns, and handguns, along with the ammo for each respective weapon.

Rockland County NY 15 miles north of NYC . Nicknamed “Copland” because 2k NYPD officers reside. Line out the door of the local gun shop today. Hey Rick these are the people you and your colleagues were mocking on @CNN. Big mistake laughing at those u will depend on for safety pic.twitter.com/LsXdJYuNxD

Then we noted in early April how social unrest was developing in several states, as Americans were panic searching “buy ammo” to a degree never before seen on the internet.

In this piece, we’re going to focus on 9mm ammo specifically, and judging by internet search trends, Americans in every state are panic searching “9mm ammo” because local gun stores have limited supplies. Notice the interest over time, hitting a record high last month.

But why focus on 9mm? Well, because gun experts will say, besides a shotgun, a handgun chambering a 9mm round is an excellent self-defense round to defend your family and or yourself in emergencies.

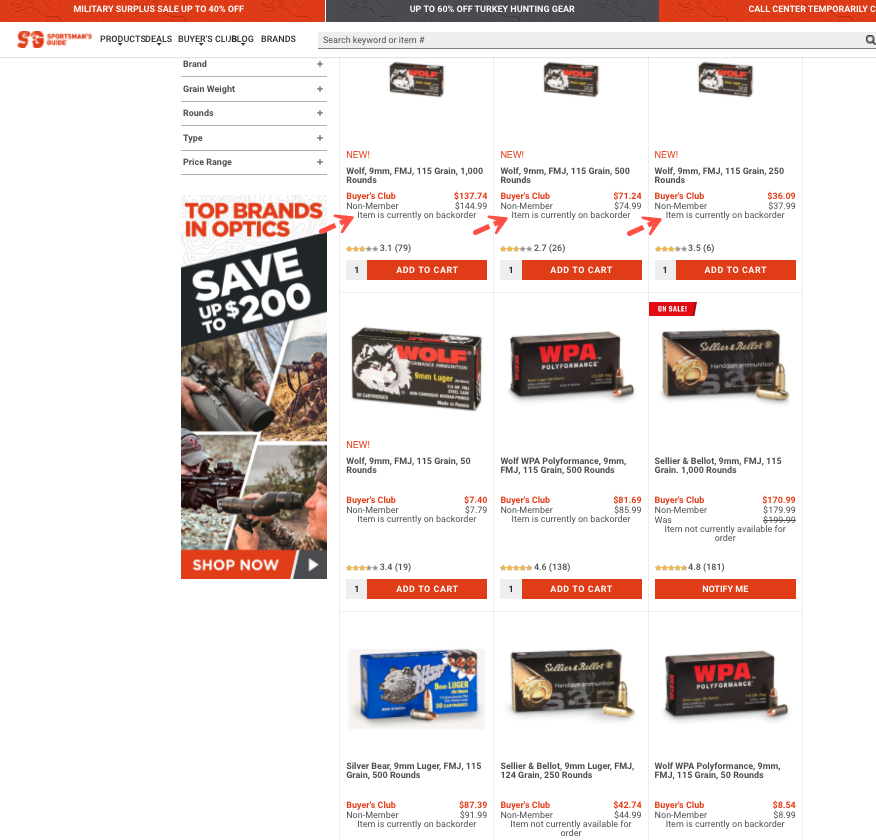

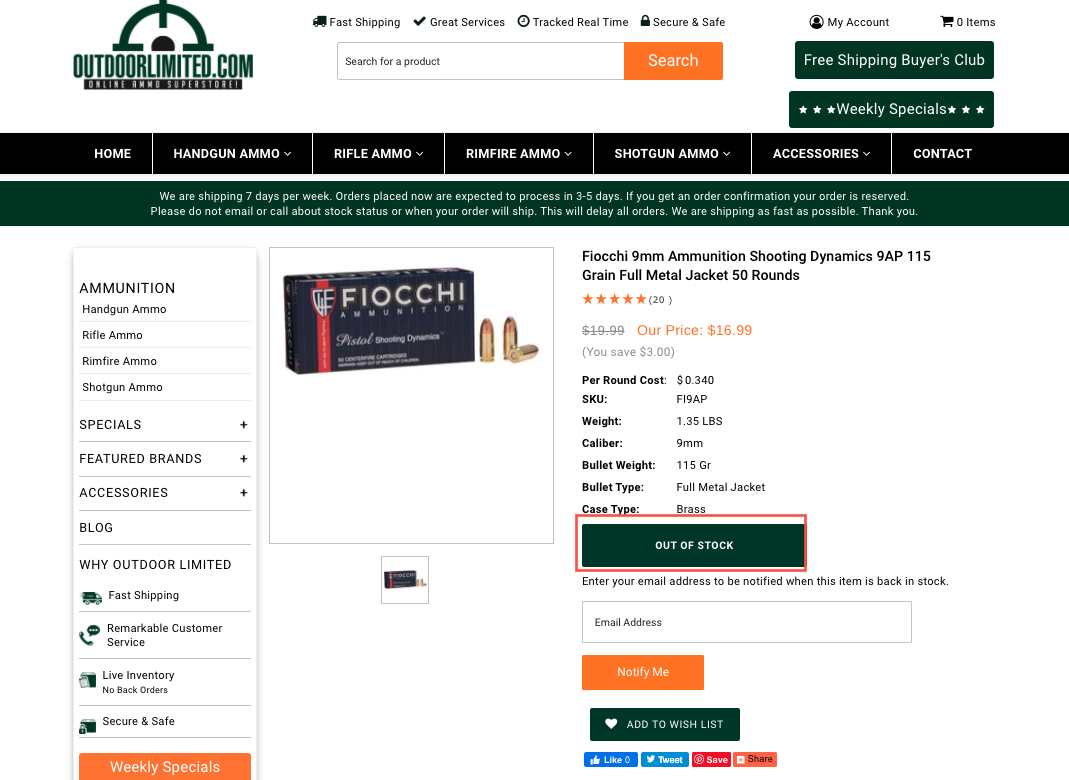

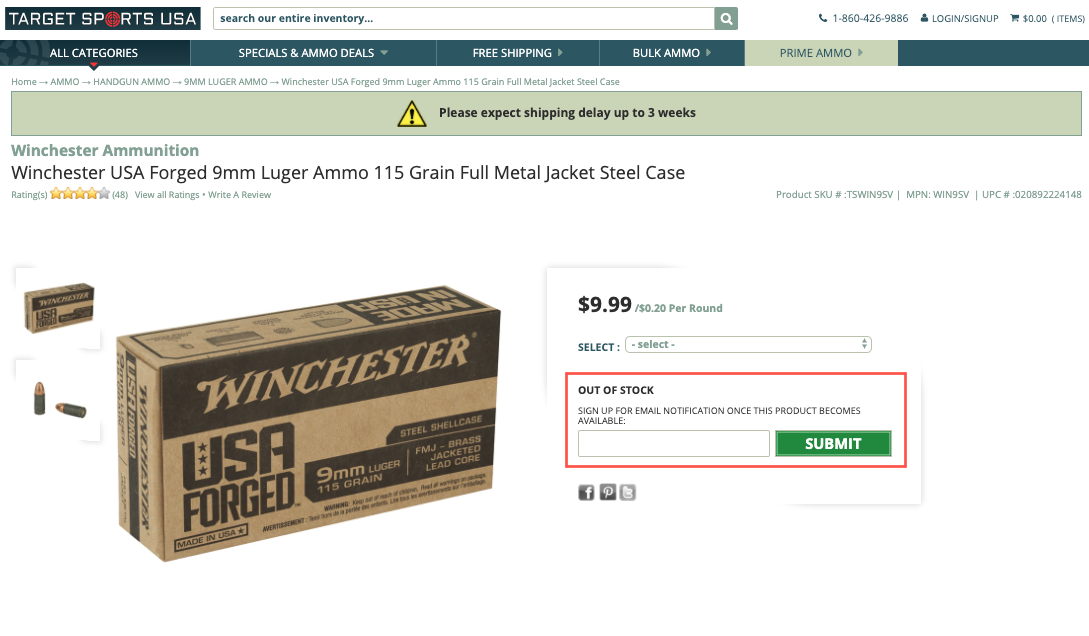

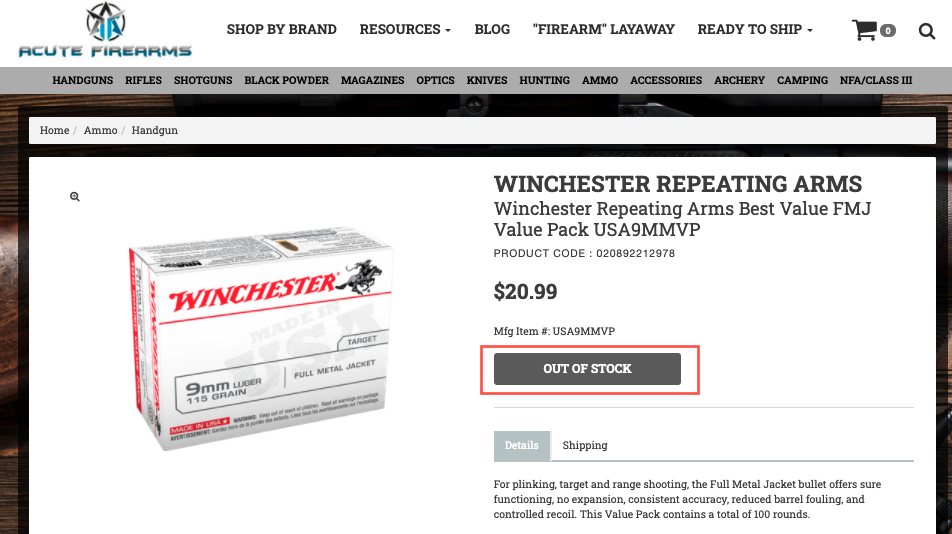

This leads us to several ammo websites that are showing specific types of 9mm rounds are “sold out” or “on backorder:”

Sportsman’s Guide

Foundry Outdoors

Outdoor Limited

Ammo Board

Target Sport USA

White Birch Armory

Acute Firarms

Freedom Munitions

A crashed economy, tens of millions of Americans out of work, quarantines still in effect, massive food bank lines, health care systems overwhelmed, and social unrest unfolding across the country – many people are loading up on weapons and ammo because the country is descending into chaos.

This was just announced by the Stanton Foundation (which generously funded my Free Speech Rules videos, but also has other interests beyond free speech):

In early April, the American Historical Association issued a call for historians to apply their skills to help illuminate the challenge COVID-19 poses to our nation and the world. As the AHA Council wrote: “Historians can … play an important role by providing context, in this case shedding light on the history of pandemics and the utility of that history to policy formation and public culture.”

To reinforce and support this call to action, the Stanton Foundation has launched a weekly contest to identify and reward what we judge the best new Applied History article or op-ed that illuminates the current coronavirus crisis. An advisory panel from the Applied History Project at Harvard Kennedy School’s Belfer Center will assist in the screening process. These articles should illuminate current challenges and policy choices by analyzing the historical record, especially precedents and analogues.

[I’m told that the contest is open to all applied history articles, whether or not written by professional historians. -EV]

Eligibility

To be eligible for the contest, entries must be: