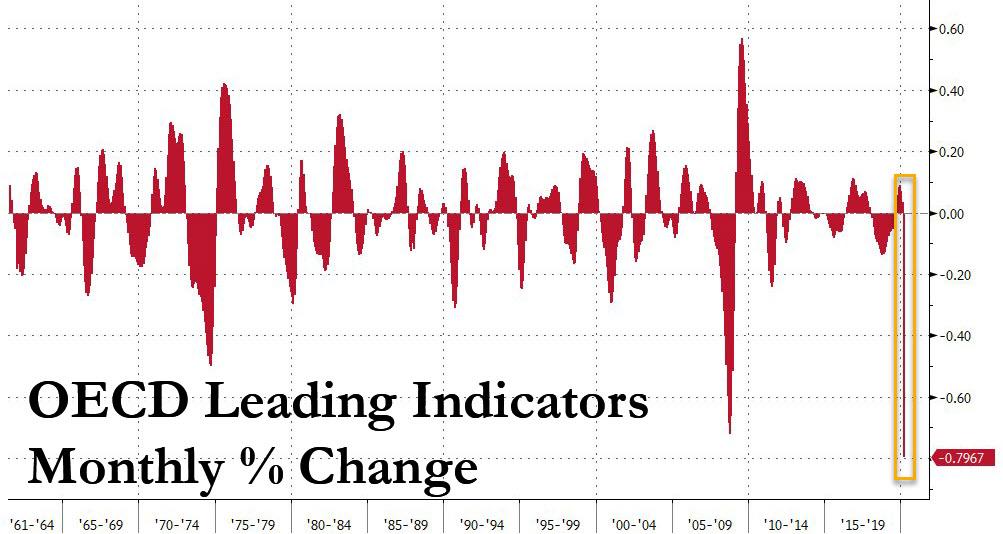

Global Economies Suffer “Largest Drop On Record”: OECD

In case anyone needed more proof that the entire world is sliding into recession, if not outright depression, on Wednesday morning the Organisation for Economic Cooperation and Development said that major economies are seeing the biggest monthly slump in activity ever amid the coronavirus crisis and no end is in sight without clarity about how long lockdowns will last.

The OECD said its leading indicators, which are designed to flag turning points in economic activity, suggested all major economies had plunged into a “sharp slowdown” with only India registering as being in a mere “slowdown”.

The indicators were flagging “the largest drop on record in most major economies”, the Paris-based OECD said in statement, adding that huge uncertainty over how long lockdowns would last severely muted their predictive value.

As a result, the OECD said the indicators “are not yet able to anticipate the end of the slowdown, especially as it is not yet clear how long, nor indeed severe, lockdown measures are likely to be”. Last month, the OECD estimated that each month major economies spend in lockdown knocked 2% off their annual growth.

Yet while the OECD has no idea what will happen, traders appears to be convinced that the worst is now behind us. As Rabobank wrote this morning, the stock market rallies of the past two days are despite the fact that neither economic nor earnings data have really begun to unveil the enormity of the economic crisis that the world has been plunging into in the past few weeks.

Even though investors have been appeased by the massive policy responses of governments and central banks around the world, this will not be cost free. The weakness at the long end of the US curve yesterday is likely related to the Treasury’s plans to resume sales of 20 year notes. The deteriorating position of public finances of governments can be expected to bring a reaction from credit rating agencies in various countries. S&P marked out Australia this morning with a reduction in its AAA credit rating outlook to negative. Unsurprisingly, the decision was based on the anticipated sharp rise in public debt and the fact that the country is facing its first recession in almost 30 years. On Tuesday, Fitch had already downgrading the credit ratings of the country’s big banks from AA+ to A- on the expected rise in bad debts as business fail. The news threw cold water on yesterday’s sharp recovery in AUD/USD.

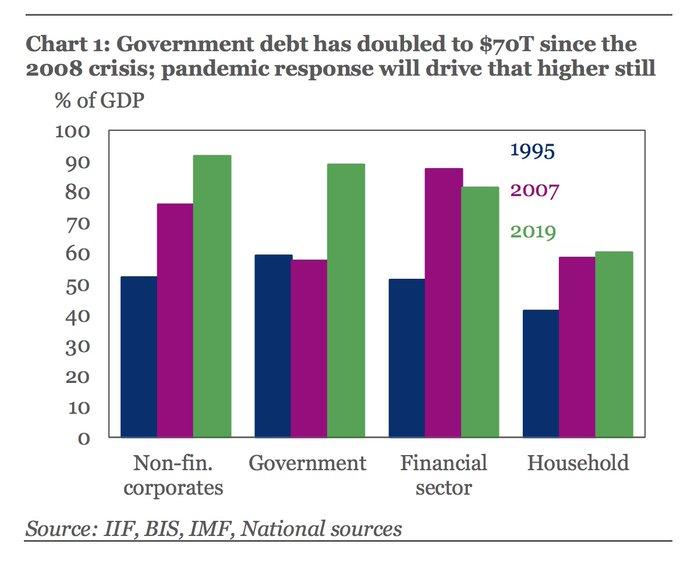

In other words, just to get back to even the world will have to incur tens of trillions in more debt which will make future growth even more scarce. Even before the global corona crisis, the IIF calculated that global debt rose by more than $10 trillion in 2019 when the global economy was humming, topping $255tn. At over 322% of GDP, global debt is now 40% or $87tn higher than at the onset of 2008 financial crisis, with the bulk of the increase in government debt (+$4.3tn) & non-financial corp sectors (+$2.8tn).

This ensuring that even the tiniest hint of inflation and jump in long rates will result in a global debt crisis, forcing even more central banks intervention, until eventually the Fed owns every risk asset to delay complete, systemic collapse.

Videoconferencing technology has been helping to keep people connected, employed, and semi-sane in these unprecedented times. Zoom has emerged as a crowd favorite since the COVID-19 pandemic’s start, quickly gaining ground on old-school competitors like Skype, Google Hangouts, and Apple’s FaceTime.

So, of course, tech-panicky politicians want to interfere. This time, the theatrics are coming courtesy of congressional Democrats and state attorneys general—two groups skilled at taking social ills and science problems and turning them into self-promotional opportunities.

“Virtual conferencing platform Zoom is facing the prospect of mounting legal threats in Washington after a slew of prominent Democratic lawmakers urged federal regulators Tuesday to investigate its privacy and security lapses,” reportsPolitico‘s Cristiano Lima.

Those calling for the Federal Trade Commission (FTC) to investigate Zoom include Democratic Sens. Amy Klobuchar (Minn.), Michael Bennet (Colo.), Sherrod Brown (Ohio), Richard Blumenthal (Conn.), Frank Pallone (N.J.), and Jan Schakowsky (Ill.).

In statements to Politico, spokespeople for Bennet and Klobuchar expressed vague concerns about Zoom user “privacy and security.” Brown put his thoughts in a letter last week.

Stories about lax data privacy practices, leaked videos, and hacked meetings have made the news recently, and these are certainly worth keeping a media and privacy watchdog spotlight on. But the political impulse we’re witnessing—broadly accuse first, find evidence later (maybe)—is a dangerous one.

In Washington, independent and supposedly neutral investigations by federal regulators have a way of turning into congressional witch hunts when bureaucrats bring back results legislators don’t like.

An FTC spokesperson told Politico the agency shares “concerns about the need to ensure the privacy and security of videoconferencing systems in light of their central importance during this crisis” but could not comment on specifics with regard to Zoom.

Attorneys general in Connecticut, Florida, and New York are also part of a group effort seeking information and company data from Zoom.

For its part, Zoom notes that it “was built primarily for enterprise customers—large institutions with full IT support,” and that “usage of Zoom has ballooned overnight,” from a maximum of 10 million daily meeting participants in December 2019 to more than 200 million per day in March. In the shift, “we recognize that we have fallen short of the community’s—and our own—privacy and security expectations,” wrote CEO Eric S. Yuan in a post laying out steps the company is taking to fix that.

Certainly, government officials and anyone conducting sensitive business should avoid free Zoom calls and other insecure communications platforms (which includes, of course, Skype, FaceTime, Google Hangouts, and their ilk, too). And if Zoom proves incapable of keeping its promises to do better, consumers can, should, and will move on.

But scaring up too much fear about Zoom privacy issues at the moment is silly. Those of us using the service for cross-country family hangouts, idle chats with old friends, exercise classes, virtual happy hours, and other mundane purposes face little significant threat, and certainly no more than we do on other mass-use social media and communications services.

The bottom line: Calls to investigate Zoom right now are being driven by a need for politicians to seem like they’re “doing something” (anything) in response to the COVID-19 outbreak. But while officials are right to be wary of using Zoom for government business, they’re probably just being melodramatic busybodies about the rest.

A federal court has upheld Texas’ temporary ban on surgical abortion:

Breaking: 5th Circuit rules for Texas in case over coronavirus abortion ban. Judge Kyle Duncan, a Trump appointee, cites "the escalating spread of COVID-19, and the state’s critical interest in protecting the public health."

Eight in 10 Americans support stay-at-home orders. From a HuffPost/YouGov survey conducted last weekend:

An 81% majority of the public says it’s currently the right decision for states to tell residents to stay at home unless they have an essential reason for going out. Just 8% say it’s the wrong decision. An even broader 89% say they are personally trying to stay home as much as possible, with only 6% saying they’re not making any such effort.

Doctors, not politicians, should decide whether hydroxychloroquine is appropriate for COVID-19 patients, writes Jeffrey A. Singer, who has been a practicing clinical physician for more than 35 years. Adds Singer:

What I’ve seen about hydroxychloroquine makes me cautiously optimistic. Doctors should not be prohibited from using their best clinical judgment and recommending it to patients—especially considering the fact that these drugs have been around for a long time, which means we are familiar with their risks and complications. The government should stay out of this and let clinicians practice medicine, provided they get their patients’ informed consent. Patients have a fundamental right to try drugs they think may save their lives. Doctors they consult must be free to give patients their best advice, unencumbered by government overseers.

In New York, “the state budget that leaders are now finalizing would allow judges to ban individuals convicted of some sex crimes in mass transit from using the system for up to three years,” Politicoreports.

An update from Sen. Rand Paul (R–Ky.), who was diagnosed with COVID-19 last month:

I appreciate all the best wishes I have received. I have been retested and I am negative. I have started volunteering at a local hospital to assist those in my community who are in need of medical help, including Coronavirus patients. Together we will overcome this! pic.twitter.com/9SeypT7rL6

I’ve been reading a lot of the contrarian (primarily from fellow righties) COVID19 opinions, and I wanted to work through them in good faith. I find most of them pretty unpersuasive. As they say, THREAD:

In the least surprising news of the year, the anti-smoking lobby thinks COVID-19 justifies the complete and permanent prohibition of cigarettes. https://t.co/gnkFpgtzak

Stocks Extend Overnight Gains On Slew Of Positive Fauci Comments

In what is a slightly different tack from his usual role as foil to President Trump’s optimism, Dr. Anthony Fauci has made a series of very optimistic statements this morning about the turning point of the pandemic and re-opening the economy sooner than many had feared…

*FAUCI: BEYOND THIS WEEK, SHOULD SEE BEGINNING OF TURNAROUND

*FAUCI: U.S. MUST KEEP PUSHING, MITIGATION EFFORT HAVING EFFECT

*FAUCI: RIGHT NOW EXPECTED DEATHS LOOK LESS THAN THOUGHT EARLIER

*FAUCI: WAS IN ROOSEVELT ROOM LAST NIGHT ON RE-ENTRY PLAN TALK

*FAUCI: MAKES SENSE TO AT LEAST PLAN HOW RE-ENTRY WOULD LOOK

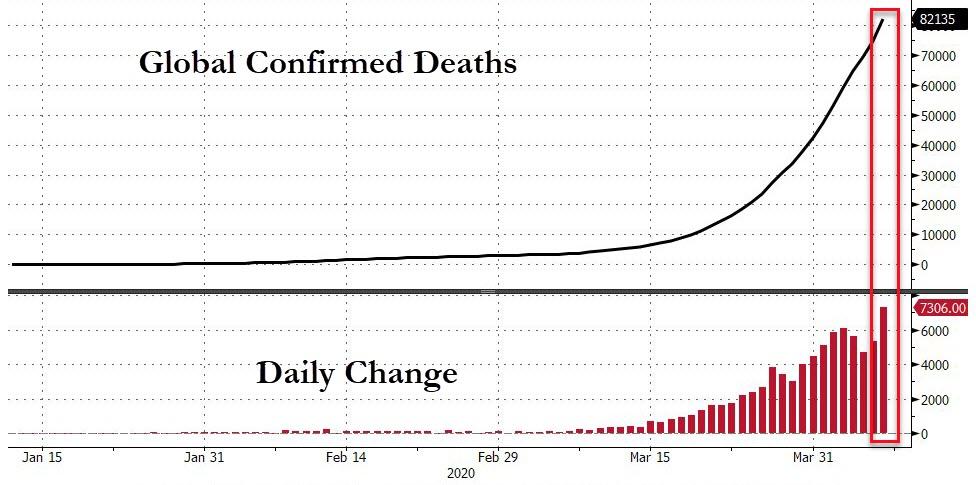

Admittedly, global deaths are growing at their fastest pace yet…

But still, US equity futures are rallying on these positive comments…

Rabobank: “If You Had A Button To Press To Eject Now, Would You?”

Submitted by Michael Every of Rabobank

Don’t count your chickens

YouTube and Twitter contain some of the best ways to waste time and rot one’s brain known to man. They also contain rare gems to stimulate and delight. Indeed, watching Nassim Taleb disembowel his intellectual opponents in real time is the closest one can get to experiencing the atmosphere of febrile 18th century London coffee houses, or perhaps even ancient Athens.

On a similar note, the other day I was watching on YouTube Eric Weinstein—whom I met with his brother Brett at a convention once briefly in Sydney—discuss everything from pro-wrestling to US elections to cultural preferences to the unfortunate anatomy of bed bugs, and he also came out with this timely gem.

Tonight, for those who know, is Passover, the ancient Jewish festival which celebrates liberation from slavery in Egypt and avoiding a deadly plague. This year it happens with Jewish communities around the world locked down or under curfew – in order to avoid a plague. Some irony! (“Why is this Seder night different from all other Seder nights?”)

As Eric pointed out, this tradition does one basic thing well: it reminds its celebrants every single year that sometimes one needs to get out while the getting is good, even if the bread hasn’t finished rising. Of course, this isn’t literally about bread. It’s about recognizing that sometimes one needs to accept that the overarching structures around us are wrong, unsustainable, or even dangerous even while they are comfortable: and then it’s time to “move” accordingly regardless of what can be seen as high costs.

One can interpret that as being brave in markets, as this is a markets Daily, or in life in general. Yet as Eric points out, we are currently surrounded by structures that are not fit for purpose. We have a British PM in intensive care after plugging herd immunity and boasting that he shook hand with Coronavirus patients. We have leading scientists telling us there will be zero, then 250,000, then 5,700 deaths; and Dr Fauci, who is lionized today, was telling us in January and February that COVID was nothing to worry about at all. We have economists arguing the economy needs to come first at some point – as if opening it up will not see the virus wreak havoc and just end up with it closing down again.

More broadly, we have socioeconomic systems that didn’t work pre-virus. Yet we seem eager to run back to where we were three months ago – when three months ago many were screaming that mankind was cutting its own throat via global warming; that inequality was building to dangerous levels; and that so were international tensions.

So what’s the point? First, “eat something, already!” Second, try to take a step back and look at the bigger picture. What really makes sense? What doesn’t? If you had a button to press to eject now, would you? And if you don’t, can you make one?

In markets terms, what will the world look like in 18 months? Do you know? Do you like what you foresee? If not – move!

For many market participants yesterday was an opportunity to express relief that in some countries the level of new coronavirus cases was levelling off allowing a few governments to consider loosening lockdowns. That said, shockingly the number of deaths is still rising and the stark reality of this appeared to halt the two day stock market rally in Asia overnight. Even though the S&P 500 had briefly re-entered a bull market in yesterday’s trading, it had already closed slightly lower yesterday, led by movements in the oil price. The IEA shook the market yesterday by slashing its price forecasts for WTI in 2020 by 20%. That said, already the oil market is this morning finding its feet on the hope that tomorrow’s virtual OPEC+ meeting will settle on production cuts.

Day ahead

The stock market rallies of the past two days are despite the fact that neither economic nor earnings data have really begun to unveil the enormity of the economic crisis that the world has been plunging into in the past few weeks. A glimpse of this has been provided by recent US labour data and huge claims for welfare in countries such as the UK and Canada last month. This morning the Bank of France issued a sobering forecast of a 6% decline in GDP in Q1 2020. Even though investors have been appeased by the massive policy responses of governments and central banks around the world, this will not be cost free. The weakness at the long end of the US curve yesterday is likely related to the Treasury’s plans to resume sales of 20 year notes. The deteriorating position of public finances of governments can be expected to bring a reaction from credit rating agencies in various countries. S&P marked out Australia this morning with a reduction in its AAA credit rating outlook to negative. Unsurprisingly, the decision was based on the anticipated sharp rise in public debt and the fact that the country is facing its first recession in almost 30 years. On Tuesday, Fitch had already downgrading the credit ratings of the country’s big banks from AA+ to A- on the expected rise in bad debts as business fail. The news threw cold water on yesterday’s sharp recovery in AUD/USD.

Inevitably, there has also been an increase in finger pointing from politicians this week as they take a step back from their initial panic reactions. President Trump has singled out the WHO for being late in warning about the virus outside of China. Trump, who will be keen to shift any blame away from himself ahead of the November election, has threatened to withhold funding for the WHO. The UK’s chief medical officer has admitted that the decision of PM Johnson’s government not to roll out mass testing was a mistake. Having little to no idea how far the virus has spread in the broader community will hamper any plans to allow the economy to normalise in the coming months.

After 76 days the lockdown in Wuhan has now been lifted. 50,000 people have reportedly already purchased train tickets to leave. The world will be watching with interest since reports are circulating that Singapore and in Hong Kong are now suffering a second wave of infections of COVID 19 which is potentially worse than the first. Hong Kong has extended indefinitely a two week closure of its airports to foreign arrivals that was due to end on Tuesday and is extending its relief package. This comes as Japan PM Abe declares a state of emergency for Tokyo, Osaka and five other virus hotspots in the country.

In Europe, yesterday’s meeting of EU finance ministers failed to settle on a compromise as to how to deal with the financial costs of the virus. Ahead of the meeting, which dragged into the early hours of this morning, Spain’s PM Sanchez had warned that nothing less than the future of the European project could be at stake. Talks will continue tomorrow.

For the most part, economic data releases continue to reflect a pre-crisis situation. That said, today’s release of the minutes of the Fed’s March meetings can be expected to display how panicked policy makers were last month. The minutes are expected to bring detail of the Fed’s decisions on March 3 and March 15 and the slate of measures that were taken then. This should be another sobering reminder of the enormity of the current crisis.

Graham Pledges To Cut WHO Funding After Trump Slams Coronavirus Response

Sen. Lindsey Graham (R-SC) is backing President Trump’s decision to reassess US funding to the World Health Organization (WHO) in the next coronavirus appropriations bill unless the organization makes top-down changes to leadership.

“I’m not going to support funding the WHO under its current leadership,” Graham told Fox News, adding “They’ve been deceptive, they’ve been slow, and they’ve been Chinese apologists. I don’t think they’re a good investment under the current leadership for the United States, and until they change their behavior and get new leadership, I think it’s in America’s best interest to withhold funding because they have failed miserably when it comes to the coronavirus.”

Lindsey Graham says he’s going to take the burden off the President and use his position on the appropriations subcommittee to eliminate any money for the WHO in the next appropriations bill pic.twitter.com/PnxLmcWaYG

Graham’s comments follow President Trump’s condemnation of the WHO on Tuesday – when he repeatedly threatened to cut funding to the UN-linked body for being “very biased towards China” as well as 0its terrible response to COVID-19.

“We’re going to put a very powerful hold on it, and we’re going to see. It’s a great thing if it works, but when they call every shot wrong, that’s not good,” said Trump – only to later soften his tone and say he’s still considering the move.

The U.S. is the biggest contributor to the WHO’s budget in the world. Trump’s fiscal 2021 budget request proposed cutting funding $122 million to about $58 million.

The WHO has continually voiced warnings about the dangers of the novel coronavirus since it first appeared in Wuhan, China, last December. The organization declared that the virus’s outbreak was a public emergency of international concern in January and then declared it was a pandemic in mid-March.

But the organization said in early February that widespread travel bans were not necessary to prevent the outbreak. Trump on Tuesday accused the WHO of disagreeing with his decision to enforce travel restrictions on incoming flights from China. –The Hill

Last week Sen. Martha McSally (R-AZ) demanded the resignation of WHO Director-General Tedros Adhanom Ghebreyesus for “helping Communist China cover up” the coronavirus outbreak which has blanketed the world.

“The greatest idiot is a man who thinks strong stock markets are an indication of economic health.“

Yesterday was a curious day in markets… The good news ran out of steam and the rally faded… Reality rears its head again? Was it just a bull phase in a bear market, or something more significant? Does the market realise just how deep the crisis has bit into the real economy?

I’ve been trying to think through what the increasing dis-connect between the financial reality of the looming deep and dark global recession – which is upon us – versus Euphoric Markets, means in terms of opportunities and likely outcomes. The perception gap is wide enough to drive a container ship thru.

Personally, I remain massively uncomfortable with current stock and bond prices, but can I afford to remain flat/short as Central Bank monetary policy will underpin and support prices? Some analysts are predicting record stock levels later this year. Banks are all saying buy corporate credit. It’s all on the back of market distortions created by policy.

After 35 years working in finance – when it comes to the real world, it sometimes feels like: FINANCIAL MARKETS HAVE BECOME TOTALLY IRRELEVENT.

Yet that would be a mistake. Financial assets – listed bonds and stocks – are cocooned in a bubble, but global commerce desperately requires liquidity and cash to survive. It’s happening – behind the illusion created by public markets.

What is actually happening out there in the real world?

According to a note I read this morning 80% of the global workforce has seen their workplaces closed or partly closed as a result of the crisis. A tiny portion of workers will be covered by government payroll schemes or other insurance, and they face long delays in receiving money. Over a billion workers have been affected. Many will be forced to take on crippling debt to get through the crisis. This will prove the biggest, most devastating, demand shock in history.

That is reality.

There is not a single corporate on the planet preparing itself for a global boom. All around the globe corporates are engaged in a mad-cash scramble. Smart Chief Financial Officers know long cash is going to be critical as the globe slides into depression in Q2 and a recession that will last far longer than Wall Street and the City perceive.

There are some fascinating trades being done – and they tell us lot about real condition, business, commerce and the developing crisis. I am working on secured asset deals with decent spreads, and full capital equity/debt financings in decent double digits. Email for details. Carnival’s secured 11.5% Senior bond last week was just one example of what is bubbling under in transport, consumer debt, property and receivables.

This morning we’ve seen details of AirBNB raising $1 bln from Silver Lake and Sixth Street in a debt/equity deal that slashes their last valuation of $31 bln to $18 bln. The two hedge funds will be getting a 11-12% Coupon. The company will raise further debt to cover the obvious short-falls in income the Virus lockdown has triggered. I’m told it’s looking to raise more debt.

After cutting 95% of its routes, Lufthansa is ditching 40 aircraft (including its’ A-380 superjumbos which I doubt will ever fly again), axing its low-cost carrier and warning about years of disruption. It’s talking to brokers about monetising part of its fleet by raising senior debt on unencumbered aircraft. Its eyeing up its $5 bln in bank lines for drawdown. Its CFO has resigned on health grounds.

The crisis for airlines will get worse as credit card companies hold back on paying immediately on any ticket sales because of their declining credit, and fuel suppliers demand upfront payments. I’m seeing Airlines around the globe engaged in a similar scramble. Easy Jet got £600 mm from the UK Treasury y’day, and took bids on financing part of its fleet. Name an airline and I can probably tell you what they are looking to sell, steal or suborn in order to raise cash.

Global Travel and Tourism accounts for about 10% of Global GDP, and its clearly the first hit sector. Tui got a massive bailout from Germany last month. Its back at the front door asking for more already.

If it’s bad in Travel, go factor what a sudden 30% unemployment shock does to demand for clothes, tech, cars, and property. Listen to the anecdotal evidence around you. Workers not yet furloughed having their salaries cut because of tumbling demand. Managers beginning to panic about whether government support, subsidy and payroll schemes will kick in before they go bankrupt.

And then widen your focus outside the developed world, and wonder how critically this is going to impact across Emerging Markets and the Developing World.

There may be a few bright spots – although Zoom is getting it in the neck about security.. There are jobs in supermarkets and healthcare.

However, all that glitters is not gold: former US FDA executives say the only reason Cholorquine treatments have been getting attention is not due to any scientific evidence,but purely down to Trump advocacy of the drugs. (Some might wonder if manufacturers of the drugs might feature in the President’s personal undisclosed portfolio – that definitely, absolutely, and categorically does not exist. (US Readers – Sarcasm Alert.))

Economic mayhem is the reality. Not the fact global markets briefly made it into a 20% recovery bull market yesterday.

This is going to be a long, hard, slog of a recovery.

Yoorp

I suppose I better say something about the big European meeting y’day If that was test of European Integration, then it was a F- Fail. Some kind of hash-up will be announced involving blah blah and some more blah with a bit of really, yeah-but, well, if and maybe. Not our problem – except it probably is.

S&P futures rebounded and European stocks fell as investors were conflicted by Tuesday’s late plunge – which saw stocks close red after the biggest surrender of gains since Oct 2008…

… and the latest data surrounding the coronavirus economic, as well as the ongoing political chaos in Europe. The dollar trimmed a gain and Treasuries slipped.

The three big US index futures swung between modest losses and gains before turning higher as air carriers including Delta Air Lines rose in the premarket. Overnight, the White House was again said to be developing plans to get the U.S. economy back in action even as Wuhan reopened to the world, starting a second wave of infections.

Despite strong early gains on Tuesday after health officials said the pandemic may kill fewer Americans than recent projections, the three major indexes ended lower as oil prices tumbled. New York, the U.S. epicenter of the pandemic, was one of several states to post their highest number of daily virus-related fatalities on Tuesday, with total infections in the country approaching 400,000. Also overnight, Tesla became the latest U.S. company to furlough staff and cut salaries during a shut down of its U.S. production facilities.

In Europe, most of the 19 sector groups on the Stoxx Europe 600 Index were in the red, after euro-area finance chiefs as usual failed to agree on a $540 billion economic package to respond to the pandemic. The euro dropped as much as 0.6% to $1.0830…

… while Italian 10-year bonds took a hit with yields jumping as much as 18 basis points to 1.80% as European officials struggled to reconcile visions for how to recover from the virus as a feud emerged between Italy and the Netherlands over mutualized bond issuance. Core debt in the region gained. France’s first-quarter output shrank the most since World War II, the latest indicator of the severity of the shock to the world’s biggest trading region.

Earlier in the session, Asian stocks were little changed, with energy falling and health care rising, after rising in the last session. Most markets in the region were down, with Jakarta Composite dropping 3.2% and Singapore’s Straits Times Index falling 1.3%, while Japan’s Topix Index gained 1.6%. The Topix gained 1.6%, with Kubotek and Intellex rising the most. The Shanghai Composite Index retreated 0.2%, with Ningbo Jifeng Auto Parts and Suzhou Chunqiu Electronic Technology posting the biggest slides.

As Bloomberg notes, investors remain reluctant to take big risks while forecasts are for the virus to grow rapidly in some of the biggest economies,the U.S., Japan, Germany, France and the U.K. They’re also concerned that fiscal stimulus measures will be too late or not enough to counter the effects of the pandemic as efforts to formulate a European response drag on.

“As the quarter progresses, investors start to understand that everything we’re seeing is in the form of assistance and aid to just tide the economy over,” Bob Michele, global chief investment officer at JPMorgan Asset Management, said on Bloomberg TV. “It’s not stimulus that gets the economy going at a much higher rate than where it is.”

In FX, the dollar advanced against all its G-10 peers and the euro slipped after European Union finance chiefs failed to agree measures to mitigate effects of the coronavirus. The Australian dollar slipped after S&P Global Ratings cut the country’s credit-rating outlook to negative from stable. The kiwi initially edged lower after New Zealand’s central bank said it is open to increasing the size and scope of its asset-purchase program, but since regained most losses. The pound steadied after slipping against a broadly stronger dollar; Prime Minister Boris Johnson’s deputy Dominic Raab sought to reassure Britain that the battle against coronavirus was under control even as the daily death toll rose to a record Tuesday. Norway’s krone, Sweden’s krona and the Australian dollar led G-10 declines.

In commodities, WTI crude rose after Tuesday’s sharp plunge. Investors are weighing whether the world’s biggest producers will be able to strike a deal that cuts enough output to offset an unprecedented demand loss from the coronavirus outbreak.

To the day ahead now, and data releases out today include the Bank of France’s industry sentiment indicator for March, weekly MBA mortgage applications from the US, and from Canada there’ll be February’s building permits and March’s housing starts. Later on, there’ll also be the minutes from the Federal Reserve’s emergency FOMC meeting on March 15 which will be an interesting snapshot of what went on the day the Fed cut rates 100bps to close to zero.

Market Snapshot

S&P 500 futures up 0.7% to 2,674.5

STOXX Europe 600 down 1.4% to 322.09

MXAP up 0.06% to 139.57

MXAPJ down 0.9% to 446.91

Nikkei up 2.1% to 19,353.24

Topix up 1.6% to 1,425.47

Hang Seng Index down 1.2% to 23,970.37

Shanghai Composite down 0.2% to 2,815.37

Sensex down 1.1% to 29,750.17

Australia S&P/ASX 200 down 0.9% to 5,206.94

Kospi down 0.9% to 1,807.14

German 10Y yield fell 3.6 bps to -0.345%

Euro down 0.3% to $1.0855

Brent Futures down 0.2% to $31.80/bbl

Italian 10Y yield rose 12.4 bps to 1.443%

Spanish 10Y yield fell 1.3 bps to 0.805%

Brent Futures down 0.2% to $31.80/bbl

Gold spot up 0.1% to $1,649.77

U.S. Dollar Index up 0.4% to 100.25

Top Overnight News from Bloomberg

The White House is developing plans to get the U.S. economy back in action that depend on testing far more Americans for the coronavirus than has been possible to date, according to people familiar with the matter

A pan-European approach for Covid-19 mobile apps should be drawn up by April 15, the EU said in proposals set to be rubber-stamped as soon as Wednesday

The French economy shrank the most since World War II in the first quarter, and the outlook for the rest of the year is souring significantly amid the confinement to limit the spread of the coronavirus, according to the Bank of France

Germany’s economy will likely shrink this quarter at more than twice the pace recorded at the height of the financial crisis, according to the country’s leading research institutes

The number of new coronavirus infections in Germany rose the most in three days, bringing the total to 107,663 in one of Europe’s worst-hit nations

A tentative tone was observed in Asia-Pac bourses following the lacklustre performance stateside where all major indices finished with marginal losses after the initial risk on tone eventually lost steam ahead of looming key risk events including the conclusion of the Eurogroup deliberations and tomorrow’s OPEC+ meeting. ASX 200 (-0.8%) traded choppy with the early heavy losses in Australia triggered by weakness across the top-weighted financials sector after the regulator issued guidance on banks and insurers in an effort to restrict dividends and with sentiment also dampened after S&P cut the outlook on the country’s AAA sovereign rating to negative from stable, although the index later shrugged off the losses as the sentiment improved in late trade, while the Nikkei 225 (+2.1%) was also indecisive for most the session after the cabinet approved a record JPY 108tln stimulus package and declared a month-long state of emergency as expected. Hang Seng (-1.1%) and Shanghai Comp. (-0.2%) conformed to the early cautious tone in the region amid PBoC liquidity inaction but with downside stemmed after the State Council continued to outline supportive measures and after outbound travel restrictions were lifted from Wuhan which was the former epicentre of the coronavirus outbreak. Finally, 10yr JGBs traded back above the 152.00 level but with price action rangebound amid the indecision in Japan and following a tepid Rinban announcement in which the BoJ are present in the market for a total of JPY 670bln of JGBs in 1-3yr and 5-10yr maturities with the amounts unchanged from prior operations.

Top Asian News

Morgan Stanley Among Biggest Lenders to Embattled Luckin Founder

Nintendo’s Animal Crossing Becomes New Hong Kong Protest Ground

Fuchs’s BFAM Hedge Fund Suffers 16% Loss Amid March Market Rout

Pakistan’s Fragile Health System Faces a Viral Catastrophe

The risk tone across Europe took a turn for the worse after Eurozone Finance Ministers yesterday failed to agree on the stimulus measures to deploy in light the coronavirus crisis. Italy noted that it will reject a final report sent to EU leaders unless debt mutualisation is mentioned as a tool whilst also demanding no conditional attachments to the ESM loans. Netherlands reiterated their objection Eurobonds and intimated a majority agree on this. Price action this morning saw futures sliding off following reports of the impasse in talks, and confirmation via Eurogroup President Centeno of the delay. European cash markets are subdued by circa 1.0-2.0% across the region (Euro Stoxx 50 -1.4%). Sectors are mostly in the red with underperformance seen in Energy amid yesterday’s losses in the complex, whilst Financials also bear the brunt of the Eurogroup deadlock and lower yield environment. Looking at the breakdown, Oil and Gas are the laggards whilst Travel & Leisure continue to feel some reprieve. In terms of individual movers, Tui (+3.5%) leads the early doors gains in the Stoxx 600 after the Co. confirmed the signing of EUR 1.8bln state aid bridge loan. Tesco (-5.0%) shares remain in negative territory after the Co. noted that COVID-19 is having a material impact on business and the group is incurring significant additional costs. The estimated impact is seen on retail cost lines seen between GBP 650-925mln. Commerzbank (-6.4%) remains near the bottom of the pan-European index after reports the sale of its Polish unit mBank could be delayed amid the virus crisis

Top European News

Hedge Fund Lansdowne’s Decline Deepens After Worst-Ever Loss

Tesco Plans $6 Billion Special Dividend as Stockpiling Eases

Goldman’s Oppenheimer Says Recovery Will Be Strong After Big Dip

In FX, the Aussie has reversed further from Tuesday’s post-RBA peaks in wake of S&P’s ratings review that came with a sting in the tail as the agency downgraded its outlook on the sovereign’s AAA standing. Aud/Usd is back below 0.6150 vs 0.6200+ when broad risk sentiment was still buoyant and its Antipodean peer was also outpacing the Usd on the 0.6000 handle compared to just under 0.5950 currently. In terms of Kiwi specifics, RBNZ Deputy Governor underlined the severity of the COVID-19 contagion overnight by stating that QE can be expanded to include other assets like linkers given that the pool of conventional bonds that can be purchased is limited. Elsewhere, the Loonie has lost 1.4000+ status after failing to test sub-1.3950 resistance ahead of Canadian housing data and against the backdrop of idling crude prices awaiting tomorrow’s OPEC+ showdown.

EUR/CHF/GBP – All on a weaker footing against the US Dollar as risk appetite wanes, but with the Euro also undermined by the Eurogroup’s failure to resolve differences on a coordinated fiscal response to the coronavirus even though dire economic predictions continue to unfurl, ie French Q1 GDP -6% per the BdF and Germany contracting almost 10% in the current quarter according to leading institutes. Eur/Usd holding between 1.0902-1.0831 parameters and perhaps propped by an array of decent option expiries stretching from 1.0800 to 1.0900 – full details available via the headline feed at 7.33BST. Meanwhile, the Franc is skirting 0.9700, but retaining an underlying safe-haven premium relative to the single currency as the cross hovers around 1.0550 and Sterling is also somewhat mixed awaiting more UK nCoV updates and progress reports from hospital where PM Johnson remains in intensive care. Cable is clinging to 1.2300 and Eur/Gbp is meandering in the low 0.8800 area, well above 1.5 bn expiry interest from 0.8700 to 0.8710.

JPY/DXY – The Yen and Buck are still jostling for position amidst fluctuating risk-on/off phases, with Usd/Jpy confined to narrow 109.00-108.50 extremes and the index not much more adventurous in advance of weekly US mortgage applications and FOMC minutes either side of 100.00, albeit with a firmer bias on balance up to 100.430 at best.

In commodities, choppy price action is seen in the energy complex in the run-up to arguably the most OPEC+ meeting to date. A delegate overnight noted that scenarios range from 10mln BPD of output curtailment to no cuts at all. The OPEC+ group’s monitoring committee is said to be preparing a draft for prospective output cuts. Several sources via Energy Intel note two scenarios will reportedly be presented: 1) The first scenario sees OPEC+ no longer being bound by production restrictions. This set-up would see a continuation of the current state of affairs – Saudi would stick to its current production quota in excess of 12mln BPD (vs. 9.7mln BPD in March) 2) In the second scenario, OPEC members alongside Russia and other producers would implement joint 10mln BPD reductions through to the end of the year, whilst TASS yesterday reported a time-frame of three months. Elsewhere, last night’s APIs proved to be another bearish release, with inventories building 11.9mln barrels vs. Exp. build of 9.3mln. Albeit, prices remained locked onto OPEC headlines. The release of the EIA STEO (ahead of next week’s OPEC and IEA Oil Market Reports) encapsulated the March impact of COVID-19, the agency cut 2020 world oil demand growth forecast by 5.6mln BPD to 5.23mln BPD and raised 2021 forecast by 4.68mln BPD to 6.41mln BPD. Nonetheless, WTI and Brent front-month futures are now mixed after sentiment was hit by news of a roadblock among EZ finance ministers on a stimulus package for the bloc. WTI outperforms its Brent counterpart with the former currently residing around USD 24.50/bbl, having had earlier topped its 21DMA (USD 24.98/bbl) to a high of USD 25.29/bbl in overnight trade. Brent meanwhile briefly dipped below USD 32.00/bbl having earlier tested resistance at USD 33/bbl (intraday high). Elsewhere, spot gold remains steady and within a relatively narrow USD 1640-57/oz intraday band. Copper prices meanwhile wiped out mild overnight gains as risk sentiment deteriorated after reports EZ finance ministers failed to reach a consensus on EU-wide stimulus to combat COVID-19. The red metal looks to retest its 21DMA to the downside at USD 2.25/lb.

US Event Calendar

7am: MBA Mortgage Applications, prior 15.3%

9:45am: Bloomberg Consumer Comfort, prior 56.3

2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Things are getting to a stage at home where my wife has started to give haircuts to the children. I didn’t watch her give the 2 year old twins their sheering yesterday but in seeing the results last night at bed time my strong guess is that they moved a lot in the process. I have numerous pictures from my childhood where my brother and I have spectacular bowl cuts as home haircuts in the more austere 1970s and early 1980s were all the rage. Parents literally used to put bowls on your head and cut around it – well mine did. Nowadays my children normally get pampered in a salon with an exotic fish tank. So we’re taking them back 40 years albeit without the bowl as a template. I look forward to the photographic memories of uneven hair in 40 years’ time. Thankfully this problem has passed my hair by long ago.

Talking of haircuts, the Eurogroup meetings yesterday were trying to find ways of ensuring bondholders don’t take one in the future. However talks have continued through the night and a press conference has been scheduled for 10am CET this morning. According to Bloomberg, France and the southern bloc have been pushing for a firm commitment for a recovery fund that would be financed by jointly issued bonds however this has caused a split with the likes of Germany and the Netherlands pushing back. The plan of a recovery fund has been put forward by the French government and aims to create a temporary reserve worth 3% of EU GDP with a lifetime of as long as 10 years, and would be funded by the joint issuance of debt to mutualize the cost of the crisis. This is in addition to the three main proposals which we had highlighted yesterday that are under discussion. As well as the recovery fund, the group is also believed to be struggling on the wording related to the ESM proposal. A preliminary draft agreement distributed to ministers yesterday night didn’t include a reference to joint debt or the time frame for a recovery fund to be arranged, and was rejected by supporters of these solutions. We should know more later this morning.

In addition to the Eurogroup, the ECB unveiled a set of temporary collateral easing measures yesterday, which included accepting Greek government bonds as collateral. Looking at the other measures, there was also a temporary increase in the Eurosystem’s risk tolerance with a “general reduction of collateral valuation haircuts by a fixed factor of 20%. However, the statement did say that the measures were temporary during the coronavirus and “linked to the duration of the PEPP”, with a reassessment coming before the end of the year. However it shows that rules are rules until events overtake them.

Over in the US meanwhile, Senate Majority leader McConnell said that he was working to provide further funds for the small-business loan programs, with a vote being held tomorrow. The initial numbers released are in the $250bn range, supplementing the $350bn that the government passed in the original $2.2 trillion stimulus package. Treasury Secretary Mnuchin said he excepts the votes in the Senate and House to take place by the end of the week, having spoken with leaders in both chambers. This plan is not in conjunction with Speaker Pelosi’s for another $1trillion aid package focused on small businesses that she floated at a call with Democrats on Monday, and it remains to be seen whether the two party leaders can merge the two bills or if there will be more political gridlock on this round of stimulus.

In terms of markets, it looked set to be another positive day for risk assets across the board yesterday, with a number of equity indices technically entering bull market territory intraday, having risen by at least 20% from their closing lows less than a month ago. However after Europe closed we saw a notable retracement. The S&P fell from a near 3.5% gain to close down slightly at -0.16%, the smallest absolute move the index has seen since a similar drop on February 13th and only the 3rd day out of the last 28 trading days where we saw a smaller than 1% move in either direction for the day. Interestingly twitter suggested this was the biggest intra-day gain for the S&P 500 where the index eventually fell and closed lower since 17th October 2008. The late market fall did seem to coincide with a fall in Oil which went from positive territory to close -3.57% in the last three hours of trading as nervousness mounts about whether the imminent OPEC+ talks (meeting tomorrow) will see enough progress, although the news appears to be more positive overnight (see below). There was also an increase in US weekly inventory levels which contributed to the late fall.

Over in Europe before the falls, Germany’s Dax did cross the so called bull market definition, with its +2.79% increase yesterday putting it up +22.68% since 18th March. The STOXX 600 was up +1.88% and is now +16.79% from the lows. Credit spreads reflected the change in risk sentiment, with US HY cash spreads -38bps tighter and IG -11bps tighter. While it was similar on this side of the Atlantic, where Europe HY cash spreads were -31bps tighter and IG -8bps tighter.

This morning Asian markets are a bit more mixed. The Hang Seng (-0.99%) and Shanghai Comp (-0.32%) are both down while the Nikkei (+0.57%) and Kospi (+0.08%) have posted modest gains. In FX, the Australian dollar is down -0.65% after S&P cut the country’s credit-rating outlook to negative from stable while the US dollar index is up +0.31% this morning after yesterday’s -0.78% decline. Elsewhere, futures on the S&P 500 are trading flat. In commodities, WTI and Brent crude oil prices are trading up +5.25% and +2.20% respectively with President Trump saying in an interview overnight that he has spoken to Russian President Vladimir Putin and Saudi Arabia’s Crown Prince Mohammed bin Salman about low oil prices and believes that “it’s all going to work out.” Base metal prices are also trading up with iron ore up as much as +2.82%.

In other news, the SCMP has reported that the Hong Kong government is set to announce a fresh round of more than HKD 30bn ($3.87 bn) in stimulus to support businesses devastated by the coronavirus pandemic. Meanwhile, Australian parliament is also expected to pass a record AUD 130bn ($80 bn) jobs-rescue plan today.

The positive sentiment earlier in the session yesterday came as the market narrative continues to shift towards the exit strategy from the shutdowns and social distancing measures. In the US, the Director of the National Economic Council, Larry Kudlow, said that the economy could re-open in the next 4-8 weeks. Remember in our “The exit strategy” note from last week (link here) we had the US easing restrictions at May 22nd so a choice price for you rather than a four week bid-offer. Over in Italy, Bloomberg reported that certain firms could open again in mid-April, earlier than our May 7th speculation but clearly baby steps still at the moment. Nevertheless, it should be pointed out that the news wasn’t entirely one-sided, with Prime Minister Abe declaring a state of emergency in 7 prefectures including Tokyo, while Paris banned outside sports (i.e. exercise) between 10am and 7pm.

In terms of new covid-19 cases our fears that Tuesday would bring a lagged weekend reporting catch up of new cases and deaths in the UK materialised as the UK saw 786 new deaths reported yesterday, the highest of the outbreak. However as you’ll see in the Corona Crisis Daily the 3-day average of growth in UK deaths at 12.6% is still substantially below the previous 3-day growth rate of 22.4%. A similar story emerged in NY as even while new case growth fell to 5.2%, the rate of new deaths rose yesterday even though it broadly remains in a down trend. Spain and Italy showed no “Tuesday effects” with both countries seeing the lowest percentage change so far in both new cases and fatalities.

Back to markets and the risk-on meant it was another bad day for safe haven assets, with yields on 10yr Treasuries and bunds up by +4.2bps and +11.6bps respectively, the biggest daily increase for both in nearly 3 weeks. The moves in southern Europe were also sizeable, with BTPs up +12.6bps (spreads only 1.0bps wider), though Greece was the outlier as yields fell by -6.6bps given the collateral news reported above. Other safe assets also suffered, with the dollar index falling by -0.78%, snapping a run of 4 successive increases, while gold’s 4-day winning run also came to an end with a -0.80% decline.

There wasn’t much in the way of data out yesterday, though the NFIB’s small business optimism index in the US fell to 96.4 in March, down from 104.5 in February. That’s the largest decline on record, and it’s the lowest level since October 2016, before President Trump’s election. We did get data on US job openings for February, which stood at a higher than expected 6.882m (vs. 6.500m expected), though the number has been rendered a snapshot of a previous age thanks to the impact of the coronavirus. Finally from Europe, we also got February’s industrial production numbers from Germany. They showed a year-on-year decline of -1.2% (vs. -3.0% expected). Largely old news.

To the day ahead now, and data releases out today include the Bank of France’s industry sentiment indicator for March, weekly MBA mortgage applications from the US, and from Canada there’ll be February’s building permits and March’s housing starts. Later on, there’ll also be the minutes from the Federal Reserve’s emergency FOMC meeting on March 15 which will be an interesting snapshot of what went on the day the Fed cut rates 100bps to close to zero.

Boris Johnson Said To Be “Stable”, But Remains In ICU

As promised, Downing Street has released its morning update on the condition of Prime Minister Boris Johnson. And according to Spokesman James Slack, who spoke with reporters on a conference call on Wednesday, Johnson is still in “stable” condition, but remains in intensive care after spending Tuesday night there.

Slack also said Johnson is “responding” to whatever treatment he is receiving.

“The prime minister remains clinically stable and is responding to treatment,” Slack said. He added that Johnson is in “good spirits”, but is unable to work right now.

“The PM is not working, he is in intensive care. He has the ability to contact those that he needs to. He is following the advice of his doctors at all times”

Slack affirmed that Foreign Secretary Dominic Raab has been deputized to stand in for Johnson.

News of the PM’s recovery, though still not guaranteed as he remains in the ICU, is still unquestionably good news for a country that has rallied around Boris Johnson, a politician whose popularity inside and outside Britain have made him a uniquely beloved figure in British politics.

One nationwide movement involved neighborhoods walking outside at the same time to ‘clap for Boris’.

Johnson, the consummate politician, will hopefully emerge from treatment strengthened and ready to deploy this new political capital to finish guiding the UK through the outbreak, and then through Brexit.

Tesla Furloughs Majority Of Workers, Cuts Employee Pay Through The End Of Q2

Despite somehow delivering 88,000 vehicles in Q1, Tesla came out on Tuesday and announced it was going to be furloughing all non-essential workers and implementing salary cuts due to the very same coronavirus outbreak that CEO Elon Musk once publicly labeled as “dumb”.

In true “carrot on a string” fashion, the company also disclosed at the same time that it expected to resume normal operations on May 4, “barring any significant changes”, according to Reuters.

Recall, Tesla had suspended production at Fremont and in New York on March 24. The Fremont suspension came after a spat with the Alameda County Sheriff’s department about whether or not Tesla was an “essential” business. It also came 8 days after Musk told his workers they were “more likely to die in a car crash” than from coronavirus.

Two days after Tesla’s delayed close, on March 26, it was reported that two Tesla employees had tested positive for coronavirus.

According to an email sent to U.S. employees by in-house counsel Valerie Capers Workman, workers pay is going to be cut 10%, directors will have their salaries cut by 20% and VP salaries will be cut by 30%, the company said.

Tesla said that pay for salaried employees would be reduced on April 13 and that cuts would remain in place until the end of the second quarter, despite the company’s plans to re-open in early May.

Any employee who cannot work from home and hasn’t been assigned to “critical work” onsite will be furloughed. Tesla said that workers will maintain their healthcare benefits until the company re-opens.

The Fremont factory employs (employed) more than 10,000 workers and was planning a ramp up in Model Y production.

We’re sure the pay cuts and employee furloughs are all due to the “dumb” coronavirus and wouldn’t be happening otherwise. Right? Or, who knows, maybe it’s time to introduce another model, do a presentation and take deposits again…

In ‘Major Shift,’ Dems Plan To Fight Trump Over Small Business Funding Expansion, ‘Pt. 4’ Stimulus Plan

For hundreds of thousands of small business owners, the early days of the ‘Paycheck Protection Program’ – the $350 billion pool of federal money that the big banks are doling out in low-interest (but not as low as it could have been), essentially risk-free, loans – were marked by frustration, exhaustion and dread, as loan applicants were denied, or told to apply at another bank (one where they had a “lending relationship…as if the Greek immigrant who owns your local diner has a revolving credit line with Goldman).

And even once applications were in, the system was instantly overwhelmed, and it quickly became clear that the amount of money that would be needed would be far more than Congress had allotted (applications received via Bank of America alone during the first couple of days amounts to more than $32 billion in liquidity, roughly 10% of the entire program total).

With both Republicans and Democrats sending signals about a fourth coronavirus relief bill, the administration is once again inexplicably producing what appear to be lowball numbers (the only reason we can see is that they’re once again being influenced by Mark Meadows and the Freedom Caucus types, even though Trump himself has said his reelection is reliant on how he handles this, and should be throwing money at this problem). Yesterday, reports claimed they were seeking a $200-$250 billion to top off the ‘PPP’.

Now, Politic reports that the Democrats have shifted gear, when in reality it looks like they’ve simply laid their cards on the table: For Pt. 4, Pelosi and Schumer want Trump to boost the small biz money to half a trillion, while committing more money to hospitals, states and SNAP benefits.

Per Politico, this is setting the country up for another battle over the contents of the bill.

NEW … PELOSI AND SCHUMER GO BIG … The dem ldrs say they want

— 100 bn for hospitals

— 150bn for state and locals

— 15% more in SNAP benefits

— of the 250bn, they want 125bn targeted for farmers, family, women, minority, vet-owned biz in rural, tribal, suburban and urban areas