As cases exponentially spread, financial markets swoon, and various institutions shut down (despite the president’s insistence today that “Nothing is shut down”), Reason Roundtable podcasters Peter Suderman, Katherine Mangu-Ward, Nick Gillespie, and Matt Welch give a progress report on their own levels of PANIC and DOOM from inside the infectious zones known as New York City and the District of Columbia. Regular listeners will not be surprised to learn that there are vigorous levels of disagreement.

Also under discussion: the eternal return of Joe Biden, the looming knockout blow to the democratic socialist presidential candidate (if not quite to his policies), the problem of using statistics in conversation, and the dark right-wing past of the inventors of the Boysenberry.

As cases exponentially spread, financial markets swoon, and various institutions shut down (despite the president’s insistence today that “Nothing is shut down”), Reason Roundtable podcasters Peter Suderman, Katherine Mangu-Ward, Nick Gillespie, and Matt Welch give a progress report on their own levels of PANIC and DOOM from inside the infectious zones known as New York City and the District of Columbia. Regular listeners will not be surprised to learn that there are vigorous levels of disagreement.

Also under discussion: the eternal return of Joe Biden, the looming knockout blow to the democratic socialist presidential candidate (if not quite to his policies), the problem of using statistics in conversation, and the dark right-wing past of the inventors of the Boysenberry.

NY AG Orders Televangelist Jim Bakker To Halt Advertising Of Alleged Coronavirus Cure

New York’s Attorney General Letitia James sent a cease-and-desist order to televangelist Jim Bakker, ordering him to stop promoting an alleged cure for coronavirus, reported ABC News.

In early February, on the “The Jim Bakker Show,” guest Sherrill Sellman claimed that “Silver Solution” is a remedy for the deadly coronavirus, that at the time, was spreading across China. Here’s a snippet of the broadcast:

Jim Bakker is standing by the claims he has made about the silver solution he sells … and he’s willing to sell you a case of it for just $300. pic.twitter.com/sXKxC54kvM

When Sellman was asked if the coronavirus elixir would cure Covid-19, she replied, “Let’s say it hasn’t been tested on this strain of the coronavirus, but it’s been tested on other strains of the coronavirus, and it has been able to eliminate it within 12 hours.”

Since the broadcast, Bakker has been selling “Silver Solution” on his website for $300 for a pack of 12.

“Your show’s segment may mislead consumers as to the effectiveness of the Silver Solution product in protecting against the current outbreak,” the cease-and-desist order said. “Any representation on the Jim Bakker Show that its Silver Solution products are effective at combating and/or treating the 2019 novel coronavirus violates New York law.”

James’ office asked Bakker to add a disclaimer on all Silver Solution products of how the FDA has not evaluated the product’s effectiveness against the virus.

“In addition to being mindful about our health, we must also beware of unscrupulous actors who attempt to take advantage of this fear and anxiety to scam or deceive consumers,” James said in a statement.

Dr. Peter Lurie, president of the Center for Science in the Public Interest, told Inside Edition that Bakker’s Silver Solution is nothing more than snake oil.

“It’s an absolute outrage that they’re pushing this product. There’s no proof about its effectiveness,” Lurie said. “Stay away from the product. All you’re doing is wasting your money!”

Lurie has been petitioning the FDA and FTC to take action against Bakker “to halt this fraud on the public.”

Back in 2018, Bakker was pumping an imminent apocalypse, selling boatloads of doomsday prepper food kits.

Capitalizing on fear is big business for Bakker as it appears his followers now have a ‘magic coronavirus cure’ and doomsday prepper food kits for the virus crisis sweeping across America that could soon be labeled a pandemic.

In January, Guggenheim CIO Scott Minerd warned that ultimately, markets will need to reprice for this rising risk with increased bond spreads relative to Treasury securities. However, that day of reckoning when spreads rise is being held off by the flood of central bank liquidity and international investors fleeing negative yields overseas.

And let’s not forget downgrade risk of BBBs: today 50 percent of the investment-grade market is rated BBB, and in 2007 it was 35 percent. More specifically, about 8 percent of the investment-grade market was BBB- in 2007 and today it is 15 percent. It has more than quintupled in size outstanding, from $800 billion to $3.3 trillion. We expect 15–20 percent of BBBs to get downgraded to high yield in the next downgrade wave: This would equate to $500–660 billion and be the largest fallen angel volume on record—and would also swamp the high yield market.

Ultimately, we will reach a tipping point when investors will awaken to the rising tide of defaults and downgrades. The timing is hard to predict but this reminds me a lot of the lead-up to the 2001 and 2002 recession.

The prolonged period of tight credit spreads experienced in the late 1990s lulled investors into unwittingly increasing risk at a time they should have been upgrading their portfolios.

This brings to mind the famous observation by economist Hyman Minsky, who stated that stability is inherently destabilizing. That is to say that long periods of relative stability in risk assets causes investors to keep upping the risk during a long period of calm.

Ultimately, this leads to what he called a Ponzi Market where the only reason investors keep adding to risk is the fear that prices will be higher tomorrow (or in the case of bonds, yields will be lower tomorrow).

“I have never in my career seen anything as crazy as what’s going on right now,” adding “this will eventually end badly.“

Adding that…

“We are either moving into a completely new paradigm, or the speculative energy in the market is incredibly out of control. I think it is the latter. I have said before that we have entered the silly season, but I stand corrected,” Minerd said at the end of his recent letter.

“This is not a buy-the-dip market. It is a don’t-catch-a-falling-knife market. “

And now, today,in his latest letter to investors – the outspoken and literal – giant of the markets warns that the market is waking up to not just the viral contagion of coronavirus, but also to financial, economic, and geopolitical contagion.

If I had written a commentary on how 4,000 people dying from the flu would topple global financial markets, I think I would have been deemed insane. Yet today that is exactly the story.

After all, the World Health Organization estimates that influenza kills 290,000 to 650,000 people per year. How does this statistically small number of 4,000 versus a global population of 7 billion bring the market to its knees? I don’t think I have to explain that right now, but if anyone thinks I need to, feel free to reach out to me in a socially distant fashion once you have washed your hands for 20 seconds and then rinsed them in Purell.

Amazingly, the market is finally waking up to the prospects of not just viral contagion but also to financial contagion. The phenomenon of a relatively insignificant event cascading through an unpredictable series of circumstances resulting in a severe outcome has been referred to as the “butterfly effect.”

The concept is derived from how a seemingly insignificant phenomenon like a butterfly flapping its wings in Brazil leads to a hurricane on the other side of the globe.

Who could predict the exact chain of events set off by the coronavirus that leads us to the circumstances that we face today? Besides the public health and economic crisis, would anyone have considered that this would also turn into a geopolitical crisis? Russia is attempting to use this critical moment to its own advantage, and the collapse of the Russian-OPEC alliance—precipitated by Russia’s goal of killing off the U.S. shale industry—has turned into an all-out price war that is causing chaos in the energy markets.

Now the financial contagion is spreading rapidly into the credit markets where not only energy bonds are plunging but other sectors like airlines, lodging, and retail are sure to follow suit.

Then there is the knock-on effect to corporate earnings and cash flows across a broad swath of industries once the world enters a global recession which now appears to be inevitable.

We arrive at this moment with the overleveraged corporate sector about to face the prospect that new-issue bond markets may seize up, as they did last week, and that even seemingly sound companies will find credit expensive or difficult to obtain.

The prospect of a crisis at maturity—that a borrower with maturing debt finds it impossible to roll the debt over to pay it off—is a very real prospect even for companies that are solvent. It has happened before, and it will happen again.

All of this points to the fact that it is virtually impossible to identify the next domino to fall but one thing seems certain: They will continue to fall.

How did we get into such a precarious position? After a decade of profligate borrowing by corporations, it would seem that any reasonable investor would have realized the fragility of the financial system.

Rumors are circulating in the market hoping for a return of crisis era programs like TAF, TARP, TALF, TLGP, and TSLF. (Can anyone remember what all these alphabet programs stand for?) But resurrection of these programs may arrive in time for Easter.

For now, stocks are limit down, the entire yield curve for Treasury securities yields under 1 percent and credit spreads are exploding, especially in energy bonds.

What next?

I hate to admit this, but our proprietary models indicate that fair value on the 10-year Treasury note will reach -50 basis points before year end and the possibility that rates could overshoot to -2 percent.

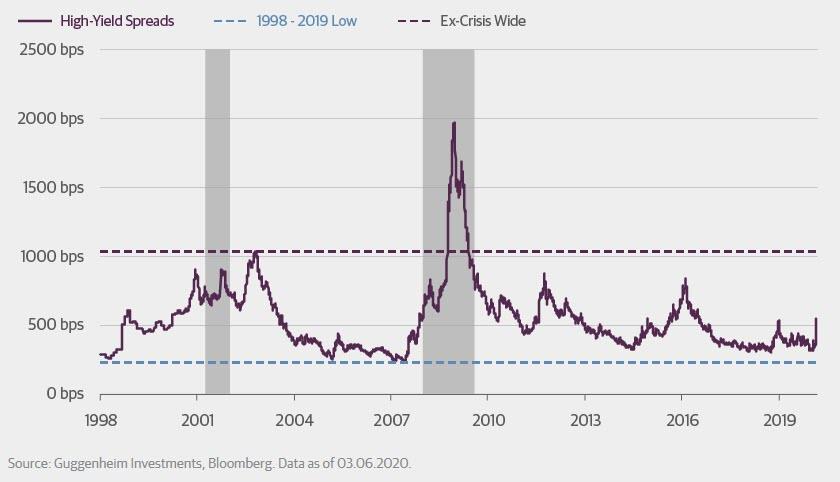

Credit spreads have a long way to expand. BBB bonds could easily reach a spread of 400 basis points over Treasurys while high yield would follow suit with BB bonds at 750 basis points over and single B bonds at 1100 basis points over. The risk is that it could be worse.

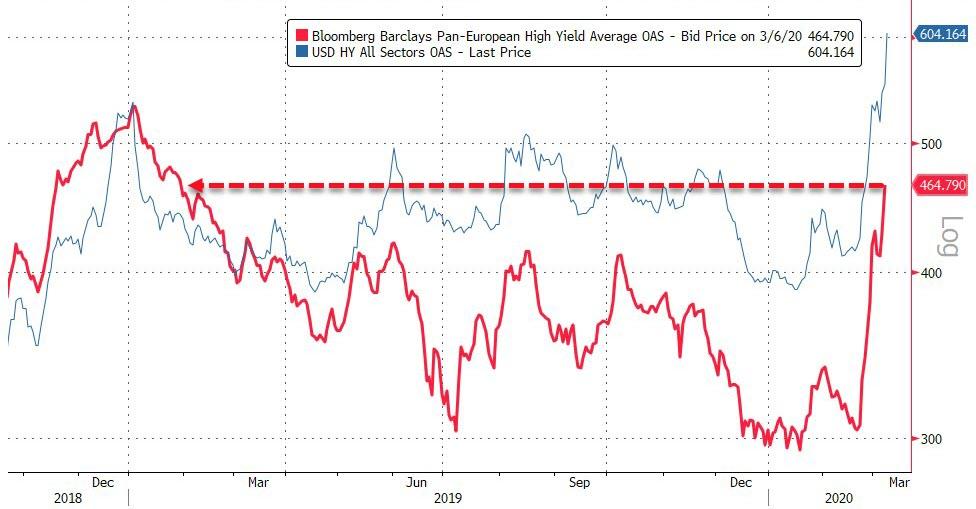

High-Yield Bond Spreads Have a Long Way to Expand

Source: Guggenheim Investments, Bloomberg. Data as of 03.06.2020.

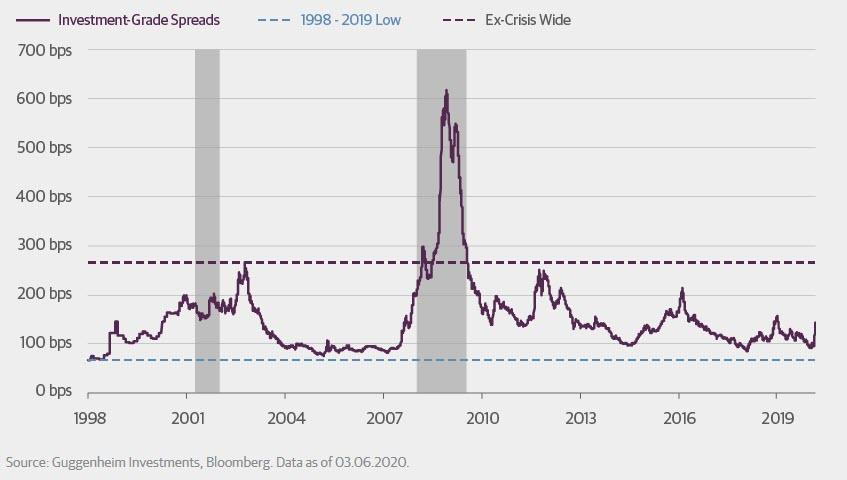

And don’t forget that a large number of investment grade bonds already have leverage ratios equivalent to high yield. As the market learned in the case of Kraft Heinz (KHC) last month, rating agency forbearance may soon dissipate, especially as earnings and free cash flow declines. KHC, a well-known household brand with a market cap of over $30 billion, saw its corporate bond rating slashed from BBB- to BB+ by both S&P and Fitch in one day. The downgrade made 19 KHC bonds totaling $22 billion in total outstanding ineligible for the most broadly-followed investment-grade corporate bond index benchmarks.

Investment-Grade Bond Spreads Are Poised to Widen

Source: Guggenheim Investments, Bloomberg. Data as of 03.06.2020.

And don’t forget that a large number of investment grade bonds already have leverage ratios equivalent to high yield. As the market learned in the case of Kraft Heinz (KHC) last month, rating agency forbearance may soon dissipate, especially as earnings and free cash flow declines. KHC, a well-known household brand with a market cap of over $30 billion, saw its corporate bond rating slashed from BBB- to BB+ by both S&P and Fitch in one day. The downgrade made 19 KHC bonds totaling $22 billion in total outstanding ineligible for the most broadly-followed investment-grade corporate bond index benchmarks.

Our estimate is that there is potentially as much as a trillion dollars of high-grade bonds heading to junk. That supply would swamp the high yield market as it would double the size of the below investment grade bond market. That alone would widen spreads even without the effect of increasing defaults.

As for stocks, technical analysis suggests that there should be support around 2600 on the S&P 500, but in a recession scenario a level closer to 2000 could be the ultimate outcome.

Many skeptics have challenged this idea, saying that the panic is close to an end. In this circumstance I recall the quote from Winston Churchill:

“This is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.”

California’s housing crisis has gotten so bad that state lawmakers are considering a little divine preemption.

Last Friday, state Sen. Scott Wiener (D–San Francisco) introduced Senate Bill (S.B.) 899, which would allow religious institutions—as well as nonprofit hospitals, rehabilitation centers, and nursing homes—to build affordable housing “by right” on land they own.

That means that local planners wouldn’t have the discretion to deny these housing projects, and third parties would lose the ability to hold them up with interminable environmental appeals and lawsuits.

“Churches and other religious and charitable institutions often have land to spare, and they should be able to use that land to build affordable housing and thus further their mission,” said Wiener in a press release. “SB 899 ensures that affordable housing can be built and removes local zoning and approval obstacles in order to do so.”

Wiener’s bill would let qualifying nonprofit institutions build housing projects containing at least 40 units on their own land. If that land is located in an area already zoned for commercial or residential use, these nonprofits could build up to 150 units.

Any organizations that take advantage of SB 899 would have to guarantee that the new housing they produce is 100 percent affordable (meaning it’s offered at below-market rates to low-income people). That affordability requirement would expire after 45 years for for-sale housing, and after 55 years for rental housing.

S.B. 899 comes on the heels of another piece of legislation—Assembly Bill (A.B.) 1851, sponsored by Assemblymember Buffy Wicks (D–Oakland)—which would eliminate parking requirements for housing projects being built on church land.

As Wiener notes, churches often have spare land in prime locations that would make excellent sites for new housing. Many are also already involved in providing temporary shelter to the homeless. But thanks to zoning restrictions, parking requirements, and lengthy approval processes, many religious institutions are kept out of the housing development business.

One prominent example is the Clairemont Lutheran Church in San Diego, which has been trying to include an affordable housing component to the redevelopment of a dilapidated fellowship hall on its property since 2015. Their plans required building over existing spaces in the church’s underutilized parking lot, and that ran afoul of a city code that ties parking requirements for churches to the square inches of pew space that they have.

“Two weeks of the year that parking lot is utilized to the full extent. 50 weeks of the year it’s not,” says Eddie McCoven, a spokesperson for the Clairemont Lutheran Church.

Thanks to lobbying by Clairemont and other faith-based nonprofits, the San Diego City Council voted in December 2019 to scrap the pew-space-to-parking-space formula and reduce church parking minimums overall.

These local efforts are now being mirrored at the state level with the legislation being introduced by Wiener and Wicks.

McCoven says his church is still in the development process, and he predicts that breaking ground for the housing component of their project is still a couple of years away. The plan, he says, is eventually to build somewhere between a dozen and 20 new affordable units.

McCoven says bills such as S.B. 899 and A.B. 1851 will help other congregations interested in developing affordable housing to spend less time and money on the planning process, and more on actually building homes.

“If this type of legislation was already in place when we were starting this project, we would be a lot further along than we are,” he tells Reason. “Any congregation that decides this is something they want to pursue, would probably make it a whole lot easier and a much more streamlined.”

from Latest – Reason.com https://ift.tt/39FbMIL

via IFTTT

California’s housing crisis has gotten so bad that state lawmakers are considering a little divine preemption.

Last Friday, state Sen. Scott Wiener (D–San Francisco) introduced Senate Bill (S.B.) 899, which would allow religious institutions—as well as nonprofit hospitals, rehabilitation centers, and nursing homes—to build affordable housing “by right” on land they own.

That means that local planners wouldn’t have the discretion to deny these housing projects, and third parties would lose the ability to hold them up with interminable environmental appeals and lawsuits.

“Churches and other religious and charitable institutions often have land to spare, and they should be able to use that land to build affordable housing and thus further their mission,” said Wiener in a press release. “SB 899 ensures that affordable housing can be built and removes local zoning and approval obstacles in order to do so.”

Wiener’s bill would let qualifying nonprofit institutions build housing projects containing at least 40 units on their own land. If that land is located in an area already zoned for commercial or residential use, these nonprofits could build up to 150 units.

Any organizations that take advantage of SB 899 would have to guarantee that the new housing they produce is 100 percent affordable (meaning it’s offered at below-market rates to low-income people). That affordability requirement would expire after 45 years for for-sale housing, and after 55 years for rental housing.

S.B. 899 comes on the heels of another piece of legislation—Assembly Bill (A.B.) 1851, sponsored by Assemblymember Buffy Wicks (D–Oakland)—which would eliminate parking requirements for housing projects being built on church land.

As Wiener notes, churches often have spare land in prime locations that would make excellent sites for new housing. Many are also already involved in providing temporary shelter to the homeless. But thanks to zoning restrictions, parking requirements, and lengthy approval processes, many religious institutions are kept out of the housing development business.

One prominent example is the Clairemont Lutheran Church in San Diego, which has been trying to include an affordable housing component to the redevelopment of a dilapidated fellowship hall on its property since 2015. Their plans required building over existing spaces in the church’s underutilized parking lot, and that ran afoul of a city code that ties parking requirements for churches to the square inches of pew space that they have.

“Two weeks of the year that parking lot is utilized to the full extent. 50 weeks of the year it’s not,” says Eddie McCoven, a spokesperson for the Clairemont Lutheran Church.

Thanks to lobbying by Clairemont and other faith-based nonprofits, the San Diego City Council voted in December 2019 to scrap the pew-space-to-parking-space formula and reduce church parking minimums overall.

These local efforts are now being mirrored at the state level with the legislation being introduced by Wiener and Wicks.

McCoven says his church is still in the development process, and he predicts that breaking ground for the housing component of their project is still a couple of years away. The plan, he says, is eventually to build somewhere between a dozen and 20 new affordable units.

McCoven says bills such as S.B. 899 and A.B. 1851 will help other congregations interested in developing affordable housing to spend less time and money on the planning process, and more on actually building homes.

“If this type of legislation was already in place when we were starting this project, we would be a lot further along than we are,” he tells Reason. “Any congregation that decides this is something they want to pursue, would probably make it a whole lot easier and a much more streamlined.”

from Latest – Reason.com https://ift.tt/39FbMIL

via IFTTT

A Joe Biden presidency would be a bonanza for plaintiff’s lawyers.

After his strong performance in the South Carolina Democratic primary and on Super Tuesday, Biden has been consolidating support among a wide range of key Democratic constituencies. But the trial lawyers have been backing him since before it became trendy.

Four Biden fundraising events tell the story.

On May 21, 2019, Biden had a fundraiser at a home of Orlando, Fla., lawyer John Morgan. Orlando magazine reported the event raised $1.7 million and reports that Morgan owns, with his wife, the plaintiff’s law firm Morgan & Morgan, and also “ClassAction.com; Abogados.com (the Spanish word for attorney is abogado); and Litify, a software management system for law firms.”

On June 18, 2019, Biden held a fundraiser at what a pool report described as “a tent on a balcony-like outside area adjacent to the law offices of Weitz and Luxenberg P.C. in Manhattan.”

My review of Federal Election Commission records discloses about 50 contributions to the Biden presidential campaign from Weitz & Luxenberg employees, totaling $97,400. Most of the contributions are from lawyers, but an accountant and the firm’s information technology director also kicked in. Many of the contributions are grouped around the date of the June 18 event.

Weitz & Luxenberg specializes in asbestos lawsuits. The firm paid former New York State assembly speaker Sheldon Silver millions of dollars to refer cases to it in a scheme that yielded federal criminal charges and a conviction of Silver that was eventually overturned by an appeals court. Weitz & Luxenberg was not charged in the case. The firm’s website boasts that the firm’s lawyers have obtained $8.5 billion in asbestos verdicts; they are also pursuing artificial hip-makers and Monsanto’s Roundup herbicide.

On Monday, December 2, 2019, Biden had another fundraiser with trial lawyers, this time about 70 of them at the Union League Club in Chicago. Among the hosts, according to a pool report, was lawyer John Simmons. Lawyers at his firm, Simmons Hanly Conroy, have donated $119,100 to Biden’s presidential campaign, according to Federal Election Commission records. That firm, too, specializes in asbestos litigation.

On February 24, 2020, Biden had a fundraiser at the Mount Pleasant, S.C., home of Lisa and Joe Rice. Joe Rice is a co-founder of the plaintiff’s law firm Motley Rice.

My review of Federal Election Commission records discloses about 30 contributions to the Biden presidential campaign from Motley Rice employees, totaling $59,850. Most of the donations are from lawyers, though a paralegal and a “law intern” also gave money to Biden. Motley Rice also is involved in Roundup litigation, as well as in cases about breast implants, hernia mesh, Takata airbags, Johnson & Johnson’s baby power, and prescription opioids.

OpenSecrets.org, a website that tracks campaign finance, lists the two plaintiff’s firms, Morgan & Morgan and Simmons Hanly Conroy, as Biden’s top two contributors for the period 1989 to 2020.

Biden’s relationship with the tort bar goes back decades. The Los Angeles Times reported in 2008 that Simmons Hanley Conroy, then known as SimmonsCooper, offered to invest $2 million to help Biden’s son Hunter and Biden’s brother James buy a hedge fund company.

Joe Biden, a lawyer himself, long served on the Senate Judiciary Committee, where he was in a position to craft legislation and to vote on judicial nominations that affected the profits of these law firms.

Presidential candidate Biden professes to be for “a constitutional amendment to entirely eliminate private dollars from our federal elections,” to “reduce the corrupting influence of money in politics.” I disagree with Biden’s stated position. I favor protecting the rights of trial lawyers—just like corporate lawyers and executives and any other American—to participate in the political process by making campaign contributions.

Voters considering Biden, though, will want to be clear-eyed about what all this means. What the trial-lawyer donors understand is that a President Biden would nominate judges who are favorably disposed, or at least not hostile. Biden would also pursue a policy and legislative agenda favorable to plaintiff-lawyer interests.

What might that look like?

There’s a contrarian conservative or libertarian case for privatizing some policy decisions into product liability law. Rather than officially banning guns or ammunition, this line of thought goes, make the manufacturers liable for civil damages in school shootings and other violent crimes. Rather than outright banning fossil fuels, make the oil companies or the automakers liable for the climate consequences of emissions. The trial lawyers and the courts will take care of the rest.

I’m not advocating this line of thought, just describing it. And venturing this prediction: if Biden does wind up in the White House, various other parts of the private economy may suffer in a variety of ways, but it sure will be good for the legal business.

from Latest – Reason.com https://ift.tt/38HJU5H

via IFTTT

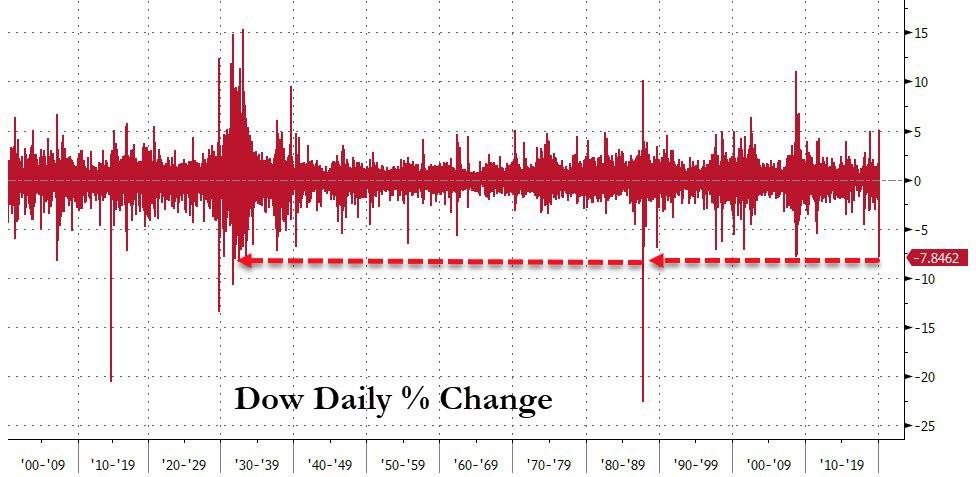

Breaking: Everything… In Biggest Stock-Selling Day In 20 Years

At its lows today, this was the market’s biggest down day since 1987 (by the close the biggest since Oct 2018!

Source: Bloomberg

Did the 11-year-long, almost unstoppable bull run that started on March 9, 2009, just end on March 9, 2009?

Source: Bloomberg

Thanks to the market perceiving President Trump’s response as remaining one of “denial” of the scale of the problem, and concerns that any fiscal stimulus will be underwhelming, things were already anxious as markets opened Sunday night. But the situation was worsened considerably as both Russia and Saudi Arabia stood poised to flood the market with cheap crude (supply) in an all-out price war just as the coronavirus is spurring the first contraction in demand since 2009.

“The situation we are witnessing today seems to have no equal in oil market history,” said IEA Executive Director Fatih Birol.

“A combination of a massive supply overhang and a significant demand shock at the same time.”

Oil futures fell by about one-third in New York and London on Monday, the biggest drop since the Gulf War in 1991, before pulling back to a 20% decline.

Source: Bloomberg

Crashing below $30!

US markets were a bloodbath from Sunday night future open (ETFs showed things were uglier than the 5% limit down in futs) and stocks were unable to show any real resilience…

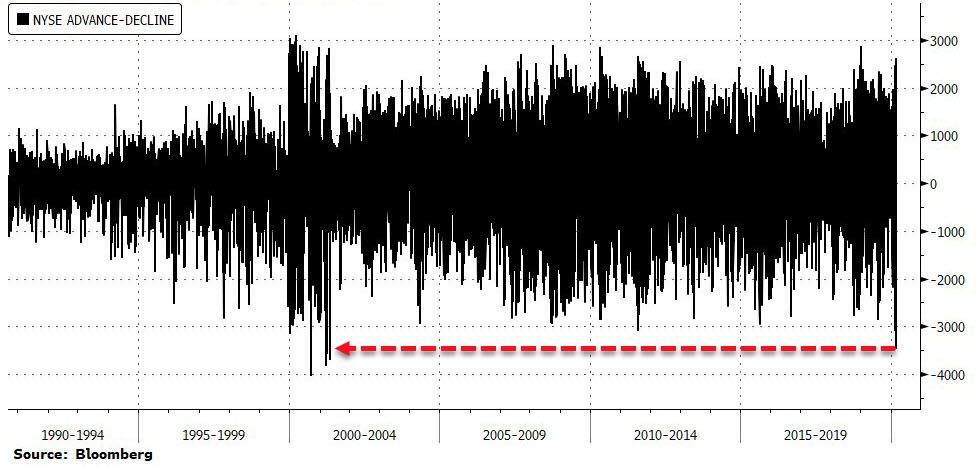

Early selling pressure today – judged by NYSE’s advance-decline line – was at its strongest since the DotCom collapse…

The shrill cry from the asset-gatherers and commission-rakers – “TURN THE BUY-THE-DIP MACHINES BACK ON!!!!”

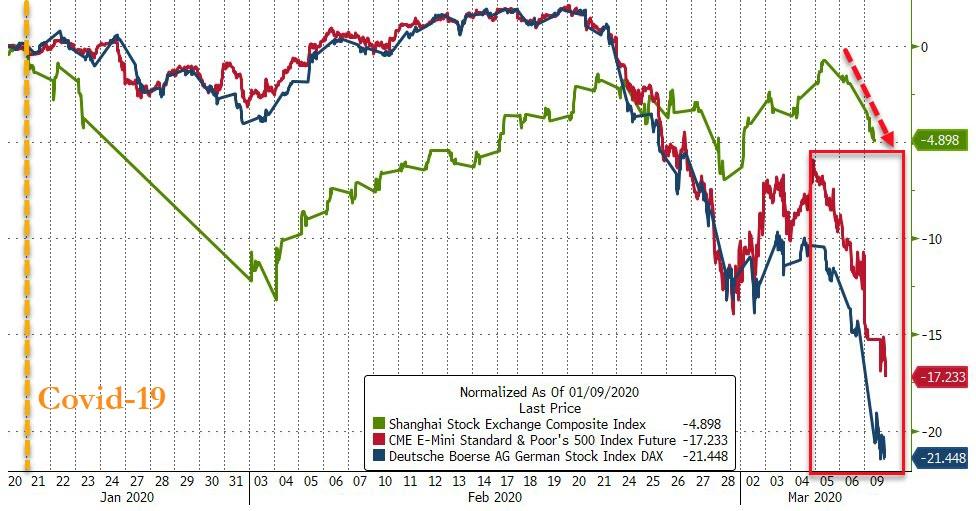

Chinese stocks – somewhat uncharacteristically – tumbled overnight… finally…

Source: Bloomberg

European stock markets just suffered their worst decline since Lehman… Oct 2008…

Europe is now down over 22.5% – a bear market – from highs just 3 weeks ago…

Source: Bloomberg

The selling was absolutely across the board…

Source: Bloomberg

European banks crashed to their lowest since March 2009… but judging by EU bank credit, there’s more to come…

Source: Bloomberg

And European credit is crashing…

Source: Bloomberg

Gilt yields fall below 0% in two- and five-year segments, with BOE’s buyback seeing the institution buy at a sub-zero rate

Source: Bloomberg

But, Italian yields surged, rising 30bps in 2-year to 10-year segments.

Source: Bloomberg

And US markets were an ever bigger bloodbath… The Dow dropped 2019 points!!! Worst day for stocks since Oct 2008

And while China began to drop, US and Europe lead the way since the start of the Covid-19 headlines…

Source: Bloomberg

Russell 2000 entered a bear market today (down 23.5% from January highs), dropping most since Lehman…

Source: Bloomberg

Dow Transports have erased all of the post-Trump election gains…

Source: Bloomberg

S&P broke key technical support…

Source: Bloomberg

All the major US equity indices have broken below their 200DMA…

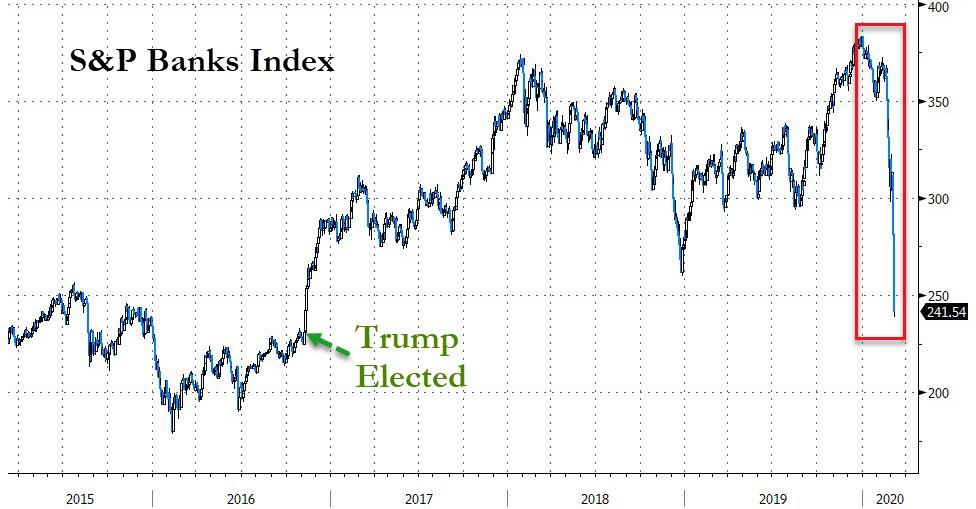

US Banks were crushed today…

Source: Bloomberg

The big banks are down a stunning 30-40% in the last 3 weeks…

Source: Bloomberg

The Energy sector suffered its biggest loss ever, crashing over 18% on the day…

Source: Bloomberg

Virus-related sectors have been destroyed…

Source: Bloomberg

VIX exploded above 60 today – the highest since Lehman…

Source: Bloomberg

And VIX’s term structure is the most inverted since Lehman…

Source: Bloomberg

Credit markets have completely collapsed (but are slightly under-pricing relative to VIX) – today was biggest jump in IG credit since Lehman…

Source: Bloomberg

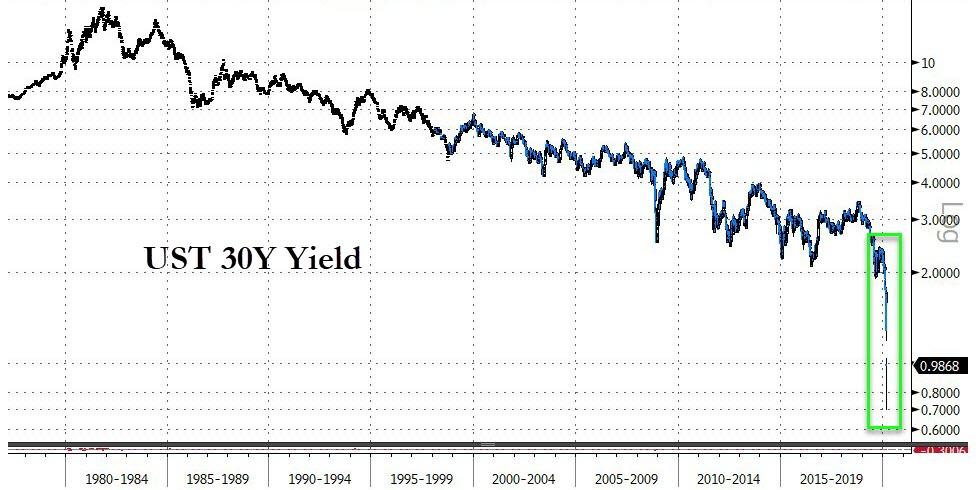

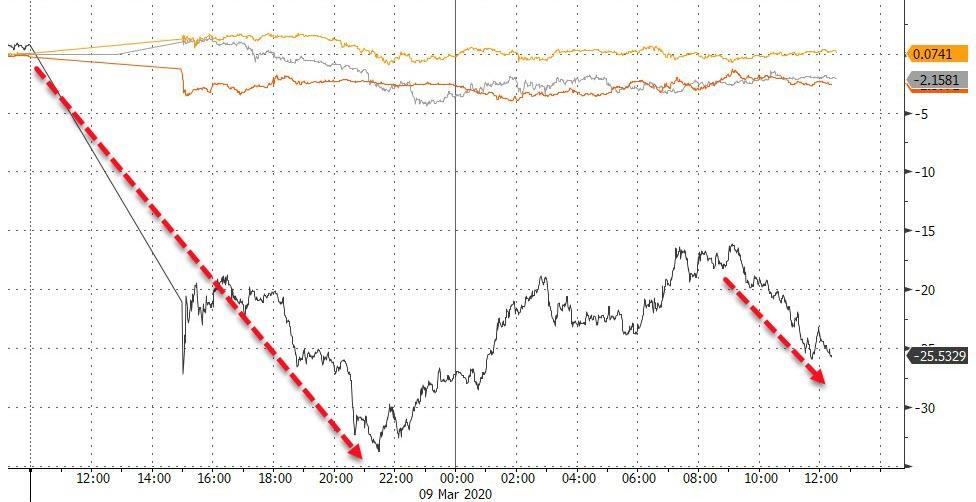

Today’s crash in Treasury yields was the biggest since Nov 2008

Source: Bloomberg

At its trough in yields overnight – it was the biggest yield drop in history…

Source: Bloomberg

10Y yields hit their lowest ever at 31.3bps…

Source: Bloomberg

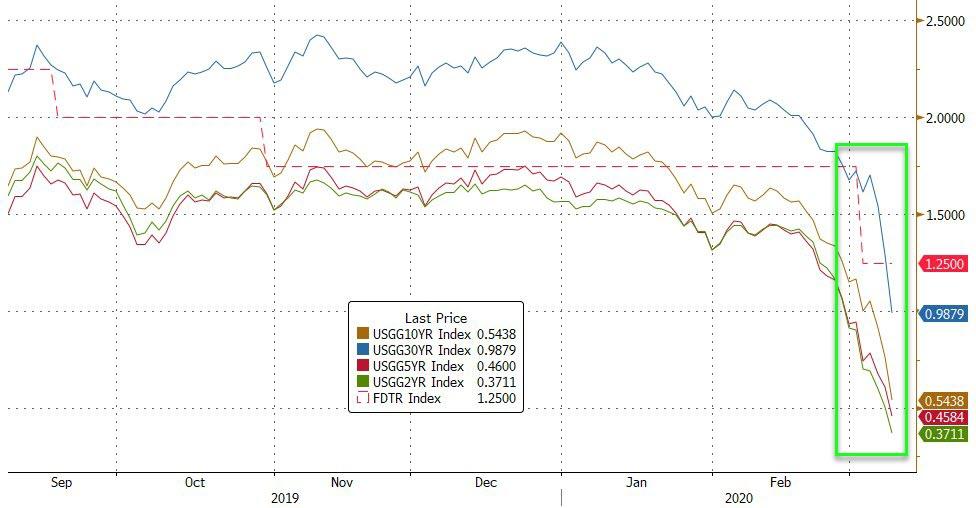

The entire Treasury curve is now below Fed Funds…

Source: Bloomberg

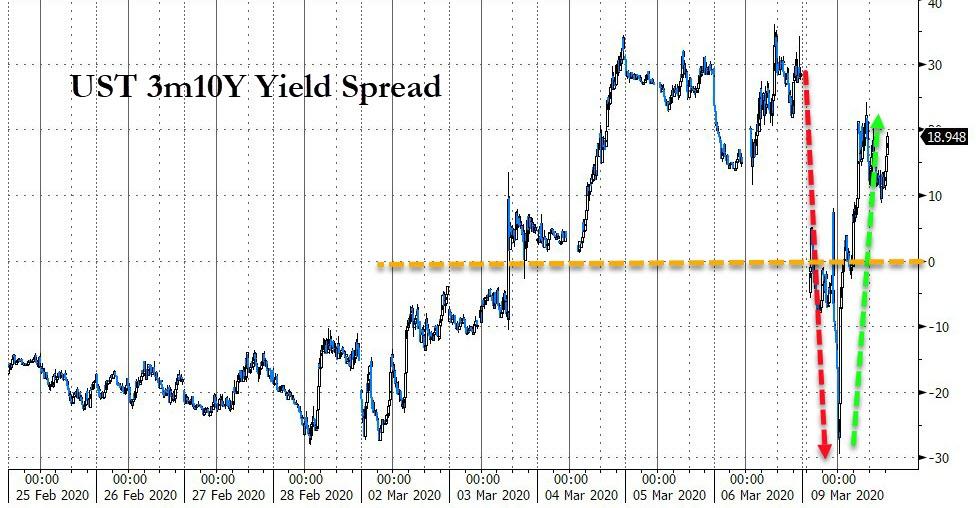

The Yield curve crashed into inversion as yields plunged overnight but stabilized later – still flatter on the day…

Source: Bloomberg

Amid all this carnage, the dollar ended only modestly lower…

Source: Bloomberg

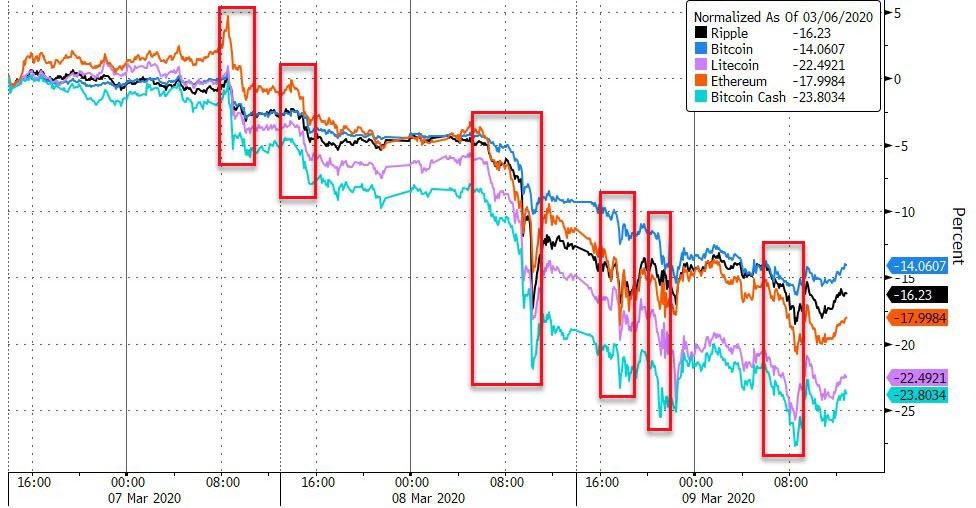

Cryptos were crushed along with almost everything else…

Source: Bloomberg

Gold managed very modest gains, copper and silver were down over 2% as crude collapsed…

Source: Bloomberg

Gold/Oil spiked to its second highest level ever today…

Source: Bloomberg

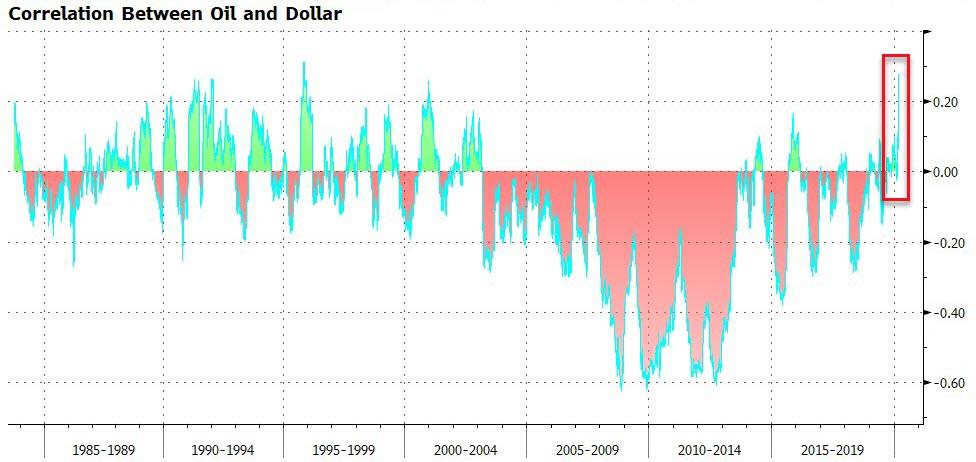

Once again oil’s drop today coincided with dollar weakness and in fact, as Bloomberg details, the relationship between oil and dollar has turned on its head: The lower the crude prices are, the weaker the U.S. currency.

Source: Bloomberg

Since the turn of the century, the two have typically had a negative correlation. A strong dollar has meant weak oil prices and vice versa, partly because oil is priced in dollars. Granted, the relationship hasn’t been stable in recent years, but a positive correlation has been rare.

There could be several explanations:

For one, lower oil prices add deflation pressure and lower the bar for the Fed to ease monetary policies.

Second, with the U.S. a net energy exporter now, weaker oil prices reduce investment in the shale industry.

Third, oil prices signal weak global demand, causing unwinding of carry-trade positions funded by the euro.

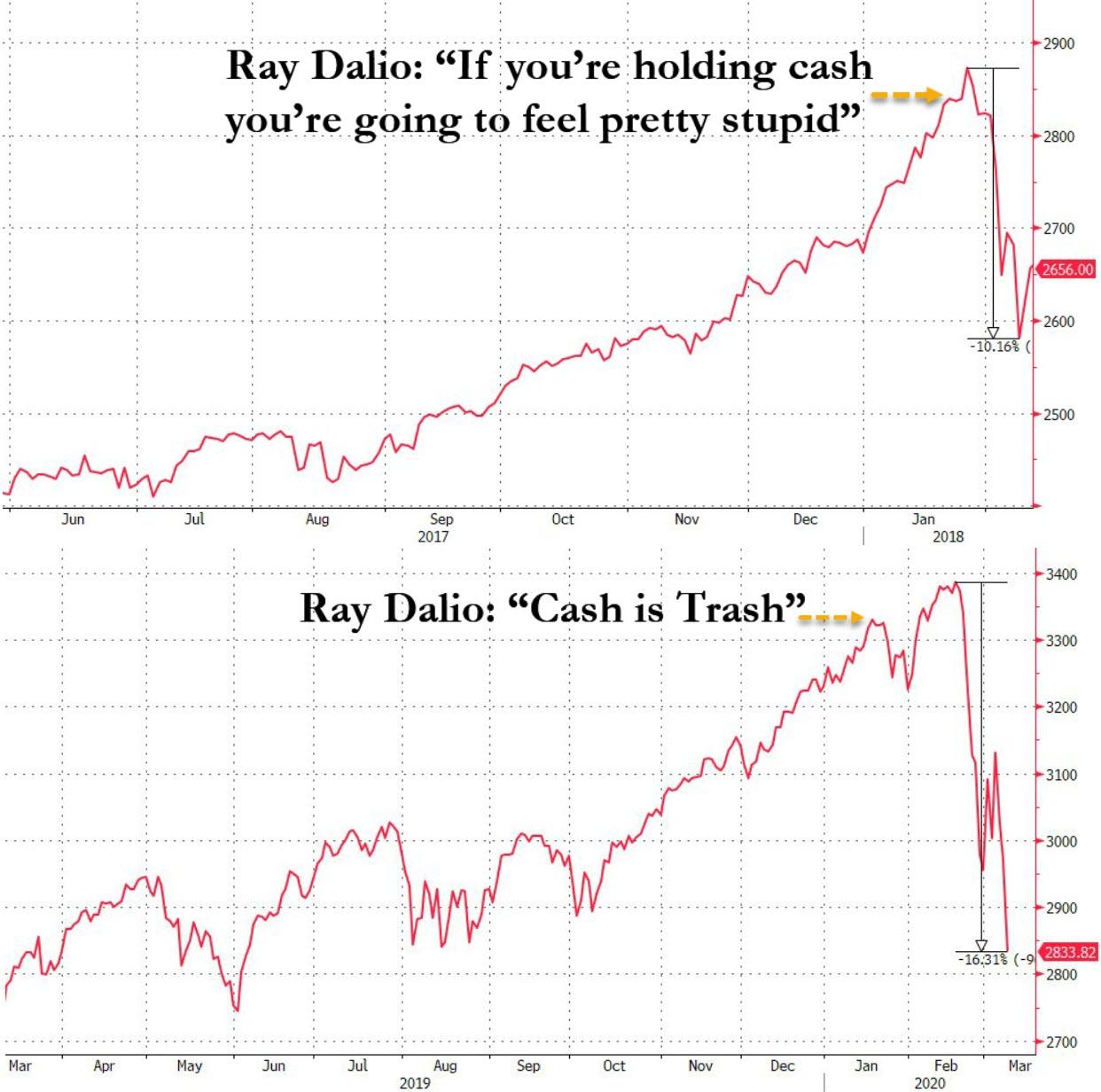

And finally, we wonder – has Ray Dalio lost his touch?

Source: Bloomberg

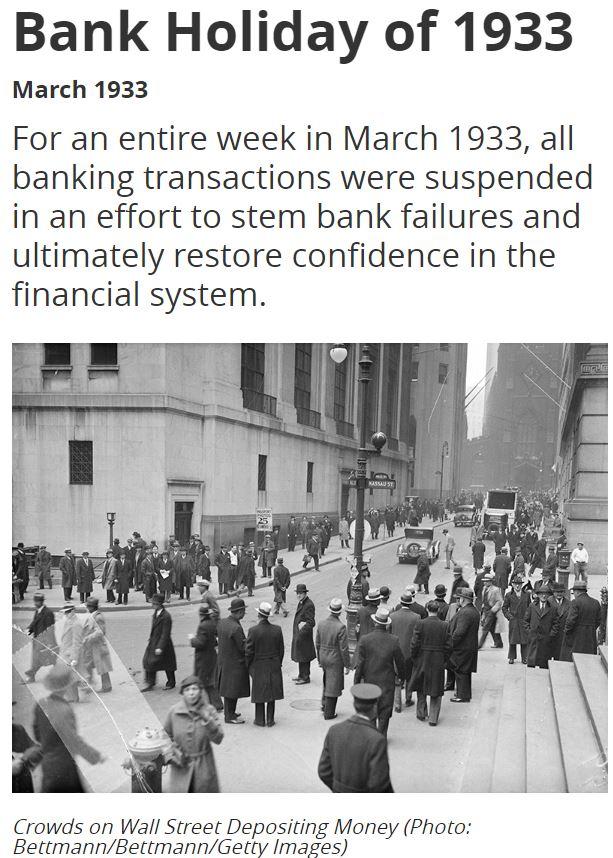

And don’t forget it’s also the anniversary of 1933’s Banking Crisis Holiday

And in case you’re wondering. The 2K analog is holding very well… implying we should get a decent bounce here before the finally catastrophic collapse…

Source: Bloomberg

The market is now demanding 3 rate-cuts at or before the next Fed meeting (on March 18th)…

Coronavirus-Infested Cruise Ship Docks In Oakland After Being Turned Away From San Francisco

After being turned away from a port call in San Francisco on Thursday, the ‘Grand Princess’ cruise ship has docked at the Port of Oakland early Monday afternoon.

Already, at least 21 passengers and crew (mostly crew) have tested positive for the virus. Passengers and crew from 54 countries are on the ship, according to the cruise line. Many others have reported feeling ill via social media, where many passengers have been posting.

Though most passengers won’t exit for at least a day or two as the cruise line and local health officials process passengers and scan them for signs of the virus, at least they will no longer be drifting listlessly at sea. Many passengers were already beginning to get a little antsy over the weekend.

We are being involuntarily held on Grand Princess currently cruising just outside San Francisco. We are confined to our cabins and given limited options for meals. Apart from the original 45 people tested Thurs (2 days ago), no one we know of has been tested. What is happening???

After the ‘Diamond Princess’ cruise ship was quarantined in Japan for two weeks, creating a diplomatic hot potato between Japan and the many countries, including the US, who pushed to evacuate their citizens from the ship.

Notably, scientists who submitted a sample of the virus found on the ship discovered similarities with the strain isolated in Washington State, which seems to support the company’s claim that the former passenger who succumbed to the virus in Cali – becoming the state’s first confirmed coronavirus death – might have caught the virus before boarding the cruise.

Hi all, we submitted the #COVIDー19 genome sequence from the viral strain linked to the #GrandPrincess cruise ship off coast of San Francisco to #GISAID. Phylogenetic analysis shows that it clusters with the outbreak clade circulating in Washington State. @UCSF#coronavirus

President Trump infamously said he would rather have kept the ship out at sea for fear of his ‘numbers’ (the number of confirmed coronavirus cases) doubling.

78 Public & Private Labs Approved To Test For Coronavirus On Monday, CDC Says

US stocks are heading back toward their lows of the session as President Trump’s response to the outbreak remains outright denial, blaming the “fake news” and pointing out that the flu killed more people last year…

So last year 37,000 Americans died from the common Flu. It averages between 27,000 and 70,000 per year. Nothing is shut down, life & the economy go on. At this moment there are 546 confirmed cases of CoronaVirus, with 22 deaths. Think about that!

…while rumors about fiscal stimulus haven’t been convincing enough (we assume we’ll hear something more concrete after Trump meets with his economic team, including Mnuchin, this afternoon).

But if you’re looking for some vaguely positive news, here it is – with one catch: The CDC has confirmed that 78 labs across the country have been certified to conduct as many as 75,000 coronavirus tests each. Dr. Nancy Messonnier, director of the US Centers for Disease Control and Prevention’s National Center for Immunization and Respiratory Diseases, said Monday during a briefing that the 78 public and commercial labs had been certified to carry out coronavirus tests.

Over the weekend, several experts and state governors, most visibly NY Gov. Andrew Cuomo, took the CDC and FDA to task for failing to authorize private laboratories to test for the novel coronavirus, and for failing to authorize automated testing. The FDA gave its approval for Northwell Health Laboratories in Lake Success – out on Long Island – to start testing, and it will now be testing 75 to 80 samples a day as the most advanced lab in the state.

“After days of advocating the FDA and the federal government to expand testing capacity for the novel coronavirus in New York State and working with Northwell and [the state lab at] Wadsworth to expedite the process, we just received word that Northwell Laboratories has been authorized to test under Wadsworth’s emergency use authorization,” Cuomo said Saturday. “Manual testing of 75 to 80 samples per day will begin at Northwell immediately, but we still need automated testing approved so we can perform thousands per day.”

The CDC’s refusal to publish data about the number of coronavirus tests carried out across the country angered millions of Americans earlier this month, and a report on Friday confirming that the US had run fewer than 2,000 tests since the beginning of the outbreak seemed to confirm fears that the administration had been caught flat-footed despite the lengthy lead time to prepare for the virus to hit.

According to an update to the CDC’s website, Washington, DC is also able to test for the virus, in addition to all 50 states. Meanwhile, the CDC said Guam, Puerto Rico and Virgin Islands are in the process of securing an approval.

And while VP Pence, who is leading the White House task force guiding the coronavirus response, promised during an appearance on Fox News in an interview that aired Saturday night that the US would have more tests available “soon” and that two major commercial labs would have testing online as soon as Monday, according to Fox News.

Pence explained the tests consist of a cotton swab of the nose for gathering samples that can be examined for the presence of the virus, and assured viewers the administration has focused on making tests available since the moment the outbreak hit the country.

“And I want your viewers to know that as we’ve been ramping up the tests, since the coronavirus first really came ashore in the United States, that we’ve been focusing tests at the point of the need where states have requested them,” Pence said. “State labs said they needed them, and particularly in the Seattle area and in parts of California that have seen multiple coronavirus cases and tragically, families that have seen the loss of life.”

Messonnier added on Monday that “commercially available” tests might soon outnumber the tests produced by the government.

“The number of commercially available tests is much larger than that and our expectation within the next couple weeks, as more and more commercial entities come on board, is that the majority of the available testing will actually be from the commercial sector,” Messonnier said.

Then again, pretty soon, Americans might be getting their coronavirus tests by Bill Gates.

Of course, the big question when it comes to US testing capabilities remains: Will increased testing instill confidence that the US is doing what it needs to contain the epidemic? Or will the new case numbers spook stocks even lower?