Media say yes, experts say no. Covid-19, known as the coronvirus, will wreak widespread changes on American society and usher in “the end of affluence politics,” suggests Matt Stoller in Wired. “Disruption to everyday life might be severe,” Nancy Messonnier of the Centers for Disease Control and Prevention (CDC) warned on Tuesday. On Wednesday, President Donald Trump announced that Vice President Mike Pence would be the coronavirus czar.

Cases continue to rise in China, South Korea, Japan, Italy, and Iran, with new cases cropping up in Austria, France, Germany, Greece, Switzerland, and elsewhere. And countries around the world are shutting down schools and travel in response.

So it it time to panic?

The number of U.S. cases remains low. The CDC has confirmed 60 cases, with only one (discovered yesterday) of unknown origin. Fourteen cases are in people who recently traveled to China or were in close contact with someone who had. “The rest were either repatriated individuals who fled the vicinity of the virus’s origin in China on State Department-chartered planes or else were rescued from the disastrous Diamond Princess cruise ship outbreak,” notes Olivia Messer at The Daily Beast.

And while experts are expecting more cases, many are not that worried. For instance, the UCLA epidemiologist Jeffrey Klausner told Messer:

It’s possible to say suddenly we’ll have 20 or 30 cases from one particular place. People should expect that, but people should not be overly concerned about that. If we were testing everyone for the common cold, we would find hundreds of thousands of cases.

Alessandro Vespignani, an infectious disease modeler at Northeastern University, toldScience:

This has a range of outcomes from the equivalent of a very bad flu season to something that is perhaps a little bit worse than that.

Worldwide, the average death rate for the disease remains unclear, confounded by both uneven reporting and a constantly shifting number of confirmed cases. Death rates may be also be inflated if less severe cases of the virus are going unconfirmed.

“In Italy, roughly 3% of the confirmed number of cases ended in death as of Monday,” notes Kenneth Rapoza at Forbes. “But the number of new cases jumped early Tuesday to 270,” bringing the death rate down to 2.6 percent.

In South Korea, the fatality rate so far has been 0.9 percent; in Iran, by contrast, it’s an astounding 14 percent. “Outside medical experts said reporting on the total number of cases of infection in Iran was possibly lagging behind reporting on deaths,” says NBC.

An analysis of coronavirus cases in China found a fatality rate of 2.3 percent, though rates varied wildly by age. “No deaths occurred in those aged 9 years and younger, but cases in those aged 70 to 79 years had an 8% fatality rate and those aged 80 years and older had a fatality rate of 14.8%,” reportsMarketWatch.

It’s hard to get a clear picture of how coronavirus compares to previous high-profile disease threats, since so many people benefit from either spreading or squelching fear and so many others seem intent on using it to push pet political issues (e.g., “Coronavirus makes the case for Medicare-for-all“).

“The World Health Organization (WHO) still avoided using the word ‘pandemic’ to describe the burgeoning crisis today, instead talking about ‘epidemics in different parts of the world,'” noteScience writers Jon Cohen and Kai Kupferschmidt. “But many scientists say that regardless of what it’s called, the window for containment is now almost certainly shut.”

Some think containment was never a realistic option to begin with:

many epidemiologists have claimed that travel bans buy little extra time, and WHO doesn’t endorse them. The received wisdom is that bans can backfire, for example, by hampering the flow of necessary medical supplies and eroding public trust. And as the list of affected countries grows, the bans will become harder to enforce and will make less sense: There is little point in spending huge amounts of resources to keep out the occasional infected person if you already have thousands in your own country.

In any event, “the fight now is to mitigate, keep the health care system working, and don’t panic,” Vespignani told Science.

FREE MINDS

No, YouTube isn’t the government, a federal court affirmed yesterday. The case stems from a lawsuit filed by Prager University, which objected to the restricted viewing conditions that YouTube placed on some of the organization’s videos. “PragerU runs headfirst into two insurmountable barriers—the First Amendment and Supreme Court precedent,” writes Ninth Circuit Judge M. Margaret McKeown. More here.

The Ninth Circuit, predictably, delivers a thorough beatdown to PragerU’s frivolous “YouTube is a government actor bound by the First Amendment” argument. It’s a good summary of state action doctrine and why private platforms are, you know, private. /1 https://t.co/S3g00481Kr

San Francisco startups are shedding employees rapidly. “More than 30 startups have slashed more than 8,000 jobs over the past four months,” The New York Timesreports. It’s particularly bad in the legal weed industry:

Perhaps the most drastic turn has happened among cannabis start-ups, which rode a wave of exuberance in recent years as countries like Canada and Uruguay and several U.S. states loosened laws that criminalized the drug. Last year, more than 300 cannabis companies raised $2.6 billion in venture capital, according to PitchBook.

Then in mid-2019, investors started doubting whether the industry could deliver on its lofty promises when some publicly traded cannabis companies were tarred by illegal growing scandals and regulatory crackdowns. Start-ups like Caliva, a cannabis producer; Eaze, a delivery service; and NorCal Cannabis Company, another producer, have together cut hundreds of members of their staffs in recent months.

“A lot of companies are not going to make it through this year,” said Brendan Kennedy, chief executive of Tilray, a cannabis producer that went public in 2018. Mr. Kennedy said he was stopping spending on new projects to survive the shakeout.

A.G. Barr advocating for ‘clean renewal’ of Patriot Act without any legislation to reform FISA is a disservice to @realDonaldTrump and should be roundly defeated.

The secret FISA court should be forbidden from allowing spying on political campaigns ever again — period!

Canadian fashion CEO Peter Nygard is being investigated for allegations of sex trafficking. His spokesperson told The Wall Street Journal that Nygard “welcomes the federal investigation and expects his name to be cleared. He has not been charged, is not in custody and is cooperating with the investigation.”

from Latest – Reason.com https://ift.tt/2HZje5h

via IFTTT

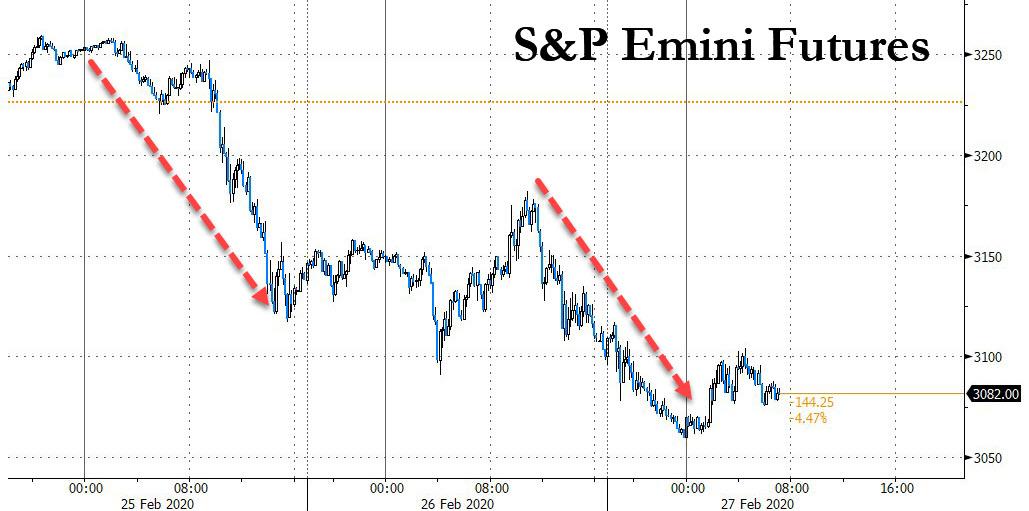

Dow Tumbles Into 10% Correction As Futures Crash, 10Y Yields Plunge To Record Lows On Pandemic Panic

After three days of tentative attempts to BTFD in the overnight session, on Thursday for the first time the puke in futures and global markets was so widespread that “pajama traders” did not pass go and proceeded to sell without prejudice…

… as S&P 500 futures dropped as much as 1.6% and threatened to slide below 3,000 today, while Dow Jones futs were down more than 375 points lower, sending the broad index into correction territory, down 3000 points from its last week highs.

The MSCI All-Country World Index fell for a sixth straight day, with Japan’s Topix and the Stoxx Europe 600 leading declines among major indexes.

The same risk aversion that was sparked in recent days by a growing pandemic panic, drove global stocks lower on Thursday, increasing their drop in value this week alone to more than $3 trillion…

… and U.S. Treasuries yields hit record lows just below 1.28% after the Centers for Disease Control and Prevention reported the first U.S. coronavirus case of unknown origin.

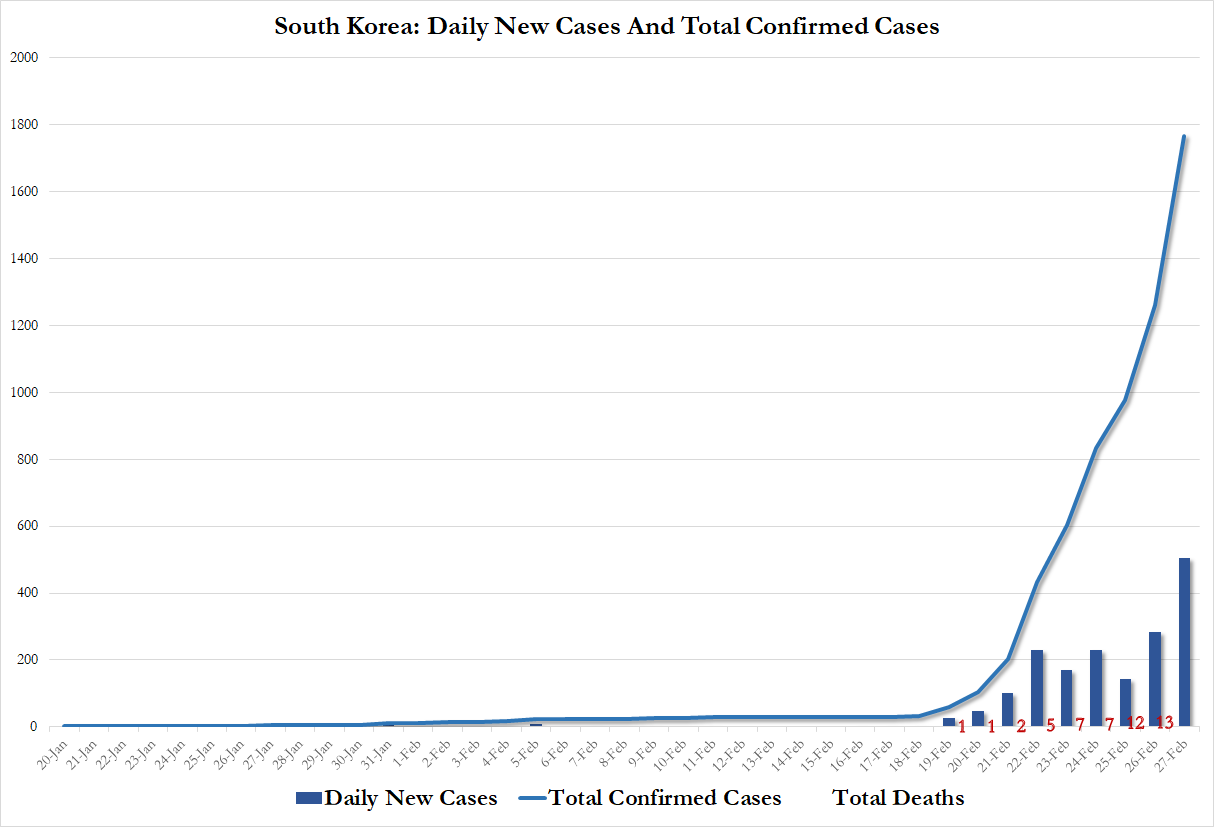

… as the coronavirus spread faster outside China than in, with South Korea reporting a whopping 505 new cases, nearly double the 284 on February 25, pushing total cases to 1766 and a 13th coronavirus-related death reported. Overnight President Trump named Vice President Mike Pence to lead the government’s preparations to tackle the virus outbreak and sought to reassure the public that the authorities are ready to handle the situation; at the same time California reported the first US coronavirus case which had been the result of “community transmision”, and whose origin was unknown.

“The fact that, not only is there no sign yet of the pathogen being contained, but rather we now also face the specter of it spreading through the U.S., will continue to weigh on the global macro outlook for the coming months,” Simon Ballard, chief economist at First Abu Dhabi Bank, wrote in a note. “Buckle up for continued high volatility and escalating risk aversion.”

Meanwhile, next door Japan’s ruling party is reportedly considering an extra budget to tackle the virus outbreak, according to Nikkei, as Germany reported 9 new cases of coronavirus so far on February 26, whilst Denmark reported its first case.

As traders scrambled for some clarity amid the panic, global equities have now fallen for six straight days, and Wall Street’s volatility gauge was near its late-2018 highs.

European stocks were pummeled from the open, with the STOXX 600 index falling 3%, the lowest level since Oct 22, 2019, and the blue-chip index in Italy – the worst-hit country in Europe – sinking as dozens of European companies issued warnings about potential damage to their profits. Travel stocks underperformed, down ~12% since the start of the week, with all sectors in the red. Anheuser-Busch InBev NV was among the worst performers in Europe after a dismal forecast. Several large companies on the benchmark, including HSBC Holdings Plc, are today trading without the right to dividends, potentially exacerbating declines.

In the United States, Microsoft became the second trillion-dollar company to warn about its results after Apple. Its Frankfurt-listed shares were down 3%.

Earlier in the session, Coronavirus fears sent Asian stocks toward their biggest six-day losing streak since August, with the IT and energy sectors falling the most. Markets in the region were mixed, with the Jakarta Composite Index and Japan’s Topix falling, while Thailand’s SET and Hong Kong’s Hang Seng Index climbed. The U.S. urged travelers to reconsider trips to South Korea as cases there rose above 1,500. While Bank of Korea left its key interest rate unchanged, it lowered its annual growth forecast on mounting evidence of an economic hit from the coronavirus. The Topix declined 2.4%, with PIA and Sanix falling the most. The Shanghai Composite Index rose 0.1%, with Tianjin Songjiang and Shanghai Shenhua posting the biggest advances.

Goldman Sachs said the equity market sell-off would create opportunities to add risk eventually and that it did not expect a deep bear market or U.S. recession. “However, near term we feel that positioning and valuations are not yet depressed enough and uncertainty on the global growth impact from the coronavirus is likely to remain high,” Goldman Sachs said in a note to clients.

“Safe-haven currencies are doing very well and gold is heading back higher, and unless we see a slowdown in the coronavirus cases outside China, risk sentiment will continue to be undermined,” said Peter Kinsella, global head of FX strategy at UBP in London

Yields on U.S. Treasuries, which fall when prices rise, dropped to a record low 1.28 for 10-year debt and the yield curve continued to send recession warnings. German 10-year debt fell to -0.5140%. Italian debt underperformed as the spread of the virus there raised fears of a recession. Australia’s 10-year yield dropped to a record low on accelerated demand for haven assets as the nation initiated an emergency pandemic plan.

Meanwhile, as the market begs for a Fed bailout, fed funds futures are now pricing a quarter-point rate cut by the end of April, while the benchmark three-month London interbank rate for dollars fell Thursday by the most since January. The May 2020 fed funds contract has an implied rate of 1.305%; that’s more than a quarter of a percentage point below the fed funds effective rate, currently 1.58%. The January 2021 fed funds future shows close to three quarters of a percentage point of easing by year end. The three- month U.S. dollar Libor rate fixed lower by 3.287bp on Thursday, ICE data show, the largest decline since Jan. 8.

In FX, the dollar fell against most major currencies as investors worried over the U.S.’s vulnerability to the spread of the coronavirus. The pound reversed gains to lead G-10 losses after the U.K. said it would prepare for a no-trade-deal exit if negotiations with the European Union did not proceed swiftly.

“The dollar is being broadly sold as risk-off sentiment heightens on the report of the infection in the U.S.,” said Takuya Kanda, general manager at Gaitame.com Research Institute Ltd. in Tokyo. “The currency is also under pressure because Trump’s speech may have disappointed the market.” The yen enjoyed support from purchases by local banks, rising nearly 2% on the week; it pared gains after Japanese Prime Minister Shinzo Abe reportedlycalled for all elementary, middle and high schools in the country to close from Monday through to the end of the spring holidays as part of measures to combat the virus spread. The safe-haven Swiss franc also gained on Thursday. Sweden’s krona advanced against all major peers, supported by flows from the Norwegian krone, and after retail sales data and an economic tendency survey surprised to the upside.

Predictably safe haven gold rose 0.8% to $1,652 per ounce, just shy of the seven-year high it hit on Monday, and silver gained 1% to $18.03 an ounce. Meanwhile oil – sensitive to global growth – fell more than 2% to its cheapest in 14 months

To the day ahead now, there’s an array of data in the US, including the second reading of Q4’s GDP, the preliminary January readings for durable goods orders and non-defence capital goods orders ex-air, weekly initial jobless claims, the Kansas City Fed’s manufacturing activity index for February, and January’s pending home sales. From central banks, we’ll hear from ECB President Lagarde, as well as the ECB’s Panetta, Schnabel, Lane, de Guindos and Lane. In addition, the Fed’s Evans and the BoE’s Cunliffe will also be speaking. Autodesk, Best Buy, Dell Technologies, and VMware are among companies reporting earnings.

Market Snapshot

S&P 500 futures down 0.6% to 3,092.50

STOXX Europe 600 down 1.5% to 398.54

MXAP down 0.7% to 159.60

MXAPJ up 0.01% to 524.89

Nikkei down 2.1% to 21,948.23

Topix down 2.4% to 1,568.06

Hang Seng Index up 0.3% to 26,778.62

Shanghai Composite up 0.1% to 2,991.33

Sensex down 0.3% to 39,760.00

Australia S&P/ASX 200 down 0.8% to 6,657.90

Kospi down 1.1% to 2,054.89

German 10Y yield fell 0.9 bps to -0.514%

Euro up 0.5% to $1.0934

Italian 10Y yield rose 0.5 bps to 0.827%

Spanish 10Y yield rose 1.3 bps to 0.263%

Brent futures down 1.9% to $52.44/bbl

Gold spot up 0.3% to $1,645.04

U.S. Dollar Index down 0.2% to 98.78

Top Overnight News

More coronavirus cases were reported in countries other than China for the first time, the World Health Organization said, a significant development as new cases spread around the globe

Vast swathes of the Lombardy and Veneto regions of Italy, stretching from Milan to Venice, remained in a virtual lockdown. Spain kept about 700 guests confined to a Canary Islands hotel as they undergo tests, while France announced four new confirmed cases, including a 60-year-old Frenchman who died in a Paris hospital overnight. Greece reported its first case

The ongoing coronavirus epidemic is causing a significant challenge to U.S. businesses in China due to travel disruptions and reduced staff productivity, according to the results of a survey by the the American Chamber of Commerce

The rapid spread of the coronavirus has prompted the Bank of Japan to ask major banks about their readiness for a worsening of the outbreak, people with knowledge of the matter said

U.K. Prime Minister Boris Johnson told the European Union he’ll walk away from the negotiating table in June if it’s not clear he’s going to get a Canada-style free trade agreement for Britain. The U.K. is setting a tough timetable for the negotiations, saying it wants the broad outline of an agreement by June, so the deal can be finalized by September

Saudi Aramco is starting early preparations for an international listing, just months after the oil giant turned its record initial public offering into a domestic affair and sidelined global banks, people with knowledge of the matter said

There’s a good chance that U.K. companies will unleash spending this year with a double boost from an expansionary budget and more clarity over Brexit, according to Bank of England Chief Economist Andy Haldane

Norway’s sovereign wealth fund boosted its South Korean government debt holdings in 2019 to $5.6 billion from $5.1 billion in the previous year, according to data published on its website

Spain’s vicious start-and-stop cycle of bad jobs has become one of Europe’s most chronic economic dilemmas, a problem unresolved by its post-crisis boom

Asian equity markets traded mostly lower following a mixed Wall Street handover, as major indices faded gains heading into the latter part of the US session before the Dow and S&P dipped into negative territory – with the former’s losses tallying over 2000 points this week thus far. Furthermore, US equity futures trickled lower since reopen amid the rising virus cases outside China and with the first “community spread” reported in the States. ASX 200 (-0.8%) is mostly weighed on by its banking and base-metal miners, while some earnings-related movers were scattered across the index. Nikkei 225 (-2.1%) underperformed with downside led by manufacturing, automakers, and financials, whilst Panasonic shares slid over 4% after ending its solar partnership with Tesla. KOSPI (-0.7%) hit levels last seen in October last year as the index continued to be weighed on by the surging number of coronavirus cases in the country, alongside the surprise hold on rates by the BoK. Elsewhere, Hang Seng (+0.3%) joined the regional stock rout as the energy and entertainment names added further to the losses seen this week, whilst Shanghai Comp (+0.1%) showed resilience and bucked the trend despite yet another PBoC inaction, as the rate of virus deaths in the country eased, the rate new cases steadied, and with further pledges from China to cushion the virus impact and stem the contagion.

Top Asian News

China May Cut Deposit Rates So Battered Banks Can Keep Lending

Hong Kong Property Tycoon Peter Woo to Take Wheelock Private

South Korea Reports 505 More Coronavirus Cases, 1 Death Feb. 27

Once again, it’s been a tough start to the session for European equities (Eurostoxx 50 -2.3%, FTSE 100 -1.9% and now in correction territory) as market sentiment is dictated by incremental newsflow surrounding COVID-19. Focus continues to reside on developments external to China with the further selling pressure being brought about by multiple updates including the potential first “community spread” case in the US, the mounting case count in South Korea and government’s across the globe lifting their threat levels over the virus. Despite comments from the WHO that the coronavirus case count might have been inflated in Italy by testing errors, markets have not been able to stage anything close to a meaningful recovery. From a sector standpoint, as has been the case throughout the week, selling has been relatively broad-based with only utility names holding up marginally better than their peers following earnings from Engie (+4%). Travel names continue to remain the ugly duckling in Europe with recent- cost-cutting measures across the sector unable to stop the rot; Tui -6.3%, easyJet -7.5%, Lufthansa -7.5%, RyanAir -7%, IAG -8%. Elsewhere, it’s been a busy morning of corporate updates with WPP (-14%) at the foot of the Stoxx 600 after a disappointing Q4 sales outturn, Belgian Heavyweight AB Inbev (-9.5%) are lower after warning on Q1 profits in the wake of COVID-19, whilst UK homebuilder Persimmon (-4.5%) lag peers after posting an annual decline in profits. To the upside, Carrefour (+3.5%) are firmer after announcing increased cost savings targets alongside earnings, Reckitt Benckiser (+2.5%) have reversed losses seen at the opening after taking a GBP 5bln impairment on Mead Johnson Nutrition and British American Tobacco (+1.5%) are showing mild gains after showing pretax profit and sales growth in its latest earnings update. Stateside, focus will be on Microsoft (-2.5% pre-market) after the Co. cut its Q3 personal computing segment revenue guidance due to coronavirus.

Top European News

Danske Bank Cuts Hundreds of Jobs in Effort to Rein In Costs

Reckitt Benckiser Takes $6.5 Billion Charge Over Formula Deal

Boris Johnson to Put U.K. on Collision Course With EU Over Trade

Norway’s Wealth Fund Returns Record $180 Billion in 2019

In FX, the Greenback has unwound all and more of its gains vs most G10 peers amidst ramped up Fed rate cut expectations on the ever-increasing spread of China’s COVID-19 epidemic to the point of pandemic proportions. The Buck’s retreat coincides with a marked rise in the number of suspected US cases and one confirmed in North Carolina from unknown origin that the CDC contends may constitute a community spread. In response, the DXY has reversed further below the 99.000 level to a 98.658 low and not far from Fib support at 98.550 that virtually coincides with another strong technical mark in the form of a late November 2019 high. Ahead, multiple US data releases and more Fed rhetoric, but for the time being it’s all about coronavirus and contagion.

EUR/NZD/CHF/AUD – The major beneficiaries of the aforementioned US Dollar demise, with the Euro embarking on a firmer recovery rally through 1.0900, 1.0926 resistance and a 1.0937 Fib before pulling up just ahead of 1.0950, a decent 1.0955 option expiry (1 bn) and another Fib at 1.0958. Meanwhile, the Kiwi and Aussie have both pared losses from sub-0.6300/0.6550 lows even though the RBNZ and NZ Finance Minister have warned of near term downside economic effects from the nCoV, with the former estimating a 0.3% point q/q hit to Q1 GDP, and Australia’s PM expressed concerns about a global pandemic that warrants action. In similar vein, the Franc has shrugged off latest dovish SNB commentary to a certain extent, as Usd/Chf slips closer to 0.9700 in contrast to Eur/Chf remaining above 1.0600 on the relative common currency strength noted above.

JPY – Volatile trade for the Yen around 110.00 vs the Greenback and within a 120.56-119.96 range against the Euro, as underlying safe-haven demand alongside dovish BoJ remarks propelled the Japanese unit to best levels before key chart support and psychological levels held. However, a raft of looming Japanese economic indicators should provide some fundamental direction, including CPI, jobs, IP and retail sales.

CAD/NOK/GBP/SEK – The Loonie is meandering either side of 1.3325 ahead of Canadian current account data and capped by another marked decline in crude, but showing a bit more resilience than the Norwegian Crown that has fallen below 10.2750 vs the Euro in wake of much weaker than forecast retail sales. Conversely, the Swedish Krona has been cushioned by encouraging sentiment indicators and wider trade surplus, with Eur/Sek retreating towards the bottom of 10.6125-5570 extremes. However, Sterling is back under pressure on a combination of bearish factors, as Cable reverses from around 1.2950 to 1.2870 or so and Eur/Gbp tests 0.8500 on heightened no deal Brexit prospects, more month end cross flows and elevated BoE easing expectations rather than actual MPC guidance via Cunliffe.

EM – Losses across the board on broad risk aversion, but with the Try also subject to further Syrian related angst as Russia refutes any meeting in early March and the Lira breaches a key mark (circa 6.1600 vs the Usd) that had been providing a buffer.

In commodities, WTI and Brent prices are, once again, subdued on virus demand concerns as cases continue to rise and spread globally; currently, front-month futures are lower by around USD 1.0/bbl and remain just below the USD 48/bbl and USD 52/bbl marks. WTI is currently on track to post a weekly loss in excess of 10%, a loss which would be the largest weekly decline since December 2018 on a percentage term. Crude specific newsflow, away from the virus has been light, with the only pertinent comments stemming from Russian Energy Minister Novak that he wishes to increase co-operation with both Saudi Arabia and OPEC+; further pushing back on the talk of a rift within the cartel. In terms of notably commentary Gazprom have remarked that, because of the lack of clarity over demand, OPEC+ should wait a while longer before making a decision around adding to or extending production; which comes ahead of next week’s OPEC+ gathering. Turning to metals where spot gold is little changed on the day and has seen a much less volatile session than has occurred over the last few weeks; interestingly, the precious metal is currently little moved from the unchanged mark on a weekly basis in-spite of a range just shy of USD 65/oz at present. Elsewhere, copper prices are modestly softer and continued to be afflicted alongside other base metals on demand-side fears.

US Event Calendar

8:30am: GDP Annualized QoQ, est. 2.1%, prior 2.1%

8:30am: GDP Price Index, est. 1.4%, prior 1.4%

8:30am: Core PCE QoQ, est. 1.3%, prior 1.3%

8:30am: Cap Goods Ship Nondef Ex Air, est. 0.0%, prior -0.3%

8:30am: Durable Goods Orders, est. -1.45%, prior 2.4%

8:30am: Durables Ex Transportation, est. 0.2%, prior -0.1%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.1%, prior -0.8%

8:30am: Personal Consumption, est. 1.7%, prior 1.8%

8:30am: Initial Jobless Claims, est. 212,000, prior 210,000

8:30am: Continuing Claims, est. 1.72m, prior 1.73m

9:45am: Bloomberg Consumer Comfort, prior 65.6

10am: Pending Home Sales MoM, est. 3.0%, prior -4.9%; Pending Home Sales NSA YoY, est. 2.05%, prior 6.8%

11am: Kansas City Fed Manf. Activity, est. -1, prior -1

DB’s Jim Reid concludes the overnight wrap

News-flow surrounding the COVID-19 Coronavirus continues to take on a fairly predictable path given all that our expert epidemiologist said earlier this week on the conference call (link here for replay details). It‘a been a 24 hour period where markets initially wanted to buy the dip but after a series of constant mini blows the S&P 500 fell -0.38% last night and futures are down a further -1.34% this morning.

The latest on the virus overnight is that a case has been confirmed in Northern California of unknown origin as the person hadn’t travelled to any foreign country recently or had contact with any of the confirmed cases. This could be a sign that the virus is spreading in a local area. The new case brings the total of known infections in the US to 15, not counting repatriated Americans. Meanwhile, South Korea reported another 334 cases (307 in Daegu) overnight bringing the total to 1,595 with fatalities at 13. Also, as the number of patients rise in Daegu, the city authorities are saying that they don’t have enough hospital beds to treat patients. The US State Department issued a level 3 advisory, the highest being level 4, for South Korea overnight asking Americans to “reconsider” travel to South Korea. In what could be termed as a surprising move, the BoK shied away from cutting rates at its meeting today against expectations of a 25bps cut. President Trump also addressed the US last night and tried to reassure the public that they face limited risk from the spread of the virus but it didn’t feel as bullish as some of his previous pronouncements on the virus.

Risk off is continuing to dominate Asian markets this morning with the exception of China where the bourses are up (CSI +0.81% and Shanghai Comp +0.53%). The Nikkei (-2.09%), Hang Seng (-0.82%) and Kospi (-0.85%) are all down alongside most other indices in the region. As for Fx, the Japanese yen is up +0.30% overnight. Elsewhere yields on 10y USTs are down another -3.4bps to 1.305%. The Australian 10y is also down by -6.4bps to a record low of +0.850%. In commodities, crude oil is extending declines after hitting 13 month lows with brent crude prices down -1.33% this morning while gold prices are up +0.53%.

In other overnight news, the IMF and World Bank said overnight that they may reconsider the meetings scheduled for mid-April in Washington amid the coronavirus’ spread. The meetings typically draw about 2,800 delegates from 189 member countries, plus hundreds of other observers and journalists.

The WHO are now reporting over 80,000 cases worldwide and an increasing number of countries confirming the presence of the virus. Indeed new cases are now higher outside of China than inside. Yesterday we saw the virus spread into new parts of Europe and the last untouched continent (if you exclude Antarctica). South America saw its first confirmed case in Brazil, where an older man who had just returned from a trip to Northern Italy tested positive. Greece and North Macedonia similarly saw their first cases yesterday following a pair of women returning to their respective homes from a recent trip to Italy. Staying with Italy many of the Serie A matches this weekend will be played behind closed doors with no fans and the Ireland vs. Italy Six Nations rugby game for next weekend was be called off. Italy now has 453 cases with 12 deaths. The ECDC said in its risk assessment report yesterday that “It is likely that Europe will see similar developments like in Italy, varying from country to country”. Germany’s Health Minister Jens Spahn said yesterday that Germany is at the beginning of a coronavirus epidemic after new cases sprung up in the country which can no longer be traced to the virus’s original source in China. Germany has 27 confirmed cases now vs. 16 the day before.

Against the backdrop of all this, the US has updated its travel advisory for Italy to “Exercise Increased Caution”. Later in the day Delta cut the number of flights to South Korea and Nestle SA, the world’s largest food company, has told employees to avoid traveling for business reasons until mid-March to keep from contracting or spreading the coronavirus. These actions are only likely to increase over the next few days. Meanwhile, Microsoft reduced its quarterly outlook yesterday due to the virus impact.

Elsewhere, Iran has imposed travel restrictions and suspended Friday prayers in areas hit by the virus after the country announced 19 Iranians have died due to the disease compared to 139 case, which is now the most deaths recorded outside of China though there are worries about the transparency and thereby accuracy of the reporting there. Overnight, Saudi Arabia has decided to temporarily halt religious visits that include stops in Mecca and Medina, which draw millions of people a year to Islam’s holiest cities, to prevent spread of virus in the country. The move comes amidst spread of virus in neighbouring countries including Kuwait, Bahrain, Iraq and the UAE. Saudi Arabia has not reported any cases so far. Meanwhile, Pakistan also reported its first two cases yesterday.

There initially looked like there would be some respite for risk markets yesterday, with the S&P 500 trading higher through the NY morning (+1.73% at the peak). Then markets headed lower later in the session as the reports of new cases built and after an unsubstantiated report that there may be an outbreak of the virus just outside of New York City. The MSCI All-Country World Index sank -0.6%, reaching 16 week lows on its fifth straight decline, and the S&P 500 index joined it ending down -0.38% lower, also the fifth day lower in a row, which is the longest such streak since August. The large intraday swings continue to support a high VIX index level, which was relatively steady above 27 points. The US 10yr Treasury continues to its slide into fresh record lows down -1.8bps, finishing at 1.333%. Oil joined equities in a move higher while Europe was open and then reverting lower in the US afternoon session as risk assets were hit across the board, Brent finished down -2.80%.

The 3M/10Y yield curve threatened to invert further throughout the day, before finishing unchanged near 5 month lows. Yesterday we highlighted that the WIRP Bloomberg page showed the chance that the Fed would cut rates again ahead of their April meeting was 66.5%, up from 24.5% a week earlier, but now the market is pricing in an 84.5% chance. In a report (link here) out yesterday, our US economists estimated that a cumulative equity decline of around 16% would exert a drag on US growth equivalent to nearly a 25bp rate hike. As such, they note that a continuation of the deterioration in risk sentiment could materially raise the risk of Fed rate cuts in the coming months. That is 16% from highs, which means we are nearly half way there already, with the S&P -7.96% off highs!

Before that European equities stabilised yesterday, with the Stoxx 600 paring back losses earlier in the session to close unchanged, just before headlines really started to turn around. European stocks did end their run of four successive moves lower for the index though. Italian assets outperformed, in spite of the country being at the centre of the coronavirus cases in Europe, with the FTSE MIB advancing 1.40%. 10 year yields were higher in Germany (+0.7 bps), France (+1.3bps), and Italy (+0.6bps). iTraxx Crossover index of credit-default swaps climbed by +4.45bps to 258bps, its highest level since 8th October. The Dollar strengthened through the day with the DXY dollar index now up for 14 of the last 18 sessions. With investors in search of havens in the second half of the day, gold resumed its march higher after the ‘big‘ -1.46% drop yesterday and is now up over +4.5% over the last 2 weeks

Elsewhere in the US, former Vice President Biden received a crucial endorsement from Jim Clyburn, South Carolina state representative and highest ranking African American in congress. Biden who was already leading with Black voters across the country, had not performed well in the first two primaries and finished a fairly distant second in Nevada. He needs to do well in South Carolina on Saturday in order to build momentum into Super Tuesday and have a path to the nomination. Clyburn said on Sunday political talkshows that he was worried about having a candidate with the title ‘socialist’ on the ticket and many party leaders have commented on what it could do to House and Senate races. Clyburn might be the first signal that party leaders are going to more forcefully back a moderate alternative.

In terms of data, US new home sales gave a rush of good news, even if slightly backward looking at this point. New home sales surged to its highest level since 2007 in January, reaching an annualized rate of 764k, significantly above consensus expectations of 718k. It was the best month-on-month change since last summer. This reflects on the record low levels of long term rates in the US coupled with strong consumer sentiment.

To the day ahead now, and economic data releases out include the Euro Area’s M3 money supply for January, along with consumer and economic confidence readings for February. Meanwhile there’s an array of data in the US, including the second reading of Q4’s GDP, the preliminary January readings for durable goods orders and non-defence capital goods orders ex-air, weekly initial jobless claims, the Kansas City Fed’s manufacturing activity index for February, and January’s pending home sales. From central banks, we’ll hear from ECB President Lagarde, as well as the ECB’s Panetta, Schnabel, Lane, de Guindos and Lane. In addition, the Fed’s Evans and the BoE’s Cunliffe will also be speaking.

It’s impossible to overstate just how much governments hate not being able to read your mail, listen to your phone calls, and peruse your text messages. When all that snoopy officials can pull up is scrambled gobbledygook, they just know they’re missing out on the good stuff, like little kids bristling at whispered adult conversations.

That explains the U.S. government’s decades-long war against private cryptography and its most recent manifestation in the crusade against “warrant-proof encryption.”

No matter how much government officials stamp their feet and hold their breath, it’d be a bad idea to give them the access they want to our data. And they do keep stamping their feet.

“By enabling dangerous criminals to cloak their communications and activities behind an essentially impenetrable digital shield, the deployment of warrant-proof encryption is already imposing huge costs on society,” Attorney General Bill Barr huffed last summer when he delivered the keynote address at the International Conference on Cyber Security in New York City. “It seriously degrades the ability of law enforcement to detect and prevent crime before it occurs. And, after crimes are committed, it thwarts law enforcement’s ability to identify those responsible or to successfully prosecute the guilty parties.”

If that sounds familiar, it’s because it’s essentially a rephrasing of former FBI Director James Comey’s 2014 argument that “those charged with protecting our people aren’t always able to access the evidence we need to prosecute crime and prevent terrorism even with lawful authority. We have the legal authority to intercept and access communications and information pursuant to court order, but we often lack the technical ability to do so.”

In turn, Comey barely rewarmed the Clinton White House’s overwrought 1994 warnings that “the same encryption technology that can help Americans protect business secrets and personal privacy can also be used by terrorists, drug dealers, and other criminals.”

The encryption technology that gets officials so hot and bothered year after year grows increasingly widespread for the simple reason that it satisfies a very real demand. Barr may worry about privacy-minded terrorists and drug sellers, but most people are more concerned about hackers, identity thieves, and nosy busybodies. In response, tech companies build end-to-end encryption into a host of products so that regular people can benefit without memorizing a user’s manual.

In response, Barr and company argue that all they want is a “back door” built into communications services so that they can gain access when necessary—and only after they jump through all the legal niceties, we’re assured.

But weakened, government-accessible encryption isn’t a magic solution that will be used only to catch bad guys. It will be weakened encryption, period.

“The problem with backdoors is known—any alternate channel devoted to access by one party will undoubtedly be discovered, accessed, and abused by another,” notes David Ruiz, a writer with the internet security firm Malwarebytes Labs. “Cybersecurity researchers have repeatedly argued for years that, when it comes to encryption technology, the risk of weakening the security of countless individuals is too high.”

“Encryption is one of the few security techniques that mostly works. We can’t afford to mess it up,” cautions Matt Blaze, a cybersecurity expert at the University of Pennsylvania. “As someone who’s been working on securing the ‘net for going on three decades now, having to repeatedly engage with this ‘why can’t you just weaken the one tool you have that actually works’ nonsense is utterly exhausting.”

How can we know that the critics are right? Because the U.S. government itself claims that a Chinese company has, for years, been misusing exactly such back doors.

“U.S. officials say Huawei Technologies Co. can covertly access mobile-phone networks around the world through ‘back doors’ designed for use by law enforcement, as Washington tries to persuade allies to exclude the Chinese company from their networks,” the Wall Street Journalreported on February 12.

Well, it’s only fair. For half a century, the CIA and German intelligence spied on international communications courtesy of back doors they built into the products of Crypto AG, a company the agencies co-owned.

The CIA and its German partner kept that arrangement secret for a long time, but mandated access to everybody’s messaging apps would be public knowledge and serious hacker-bait. It might even be a target for bad actors wielding the hacking tools that were stolen in 2017 from the National Security Agency—an exploit generally considered among the most significant events in cybersecurity.

Whoopsies. It’s almost like you really shouldn’t trust government types with the ability to peruse your communications and paw through your data.

Despite that history, Senators Lindsey Graham (R-S.C.) and Richard Blumenthal (D-Conn.) are floating a bill that would make tech companies “earn” Section 230 protection against liability for other people’s communications that pass through their platforms by adopting “best practices” that satisfy amorphous government standards.

“The AG could single-handedly rewrite the ‘best practices’ to state that any provider that offers end-to-end encryption is categorically excluded from taking advantage of this safe-harbor option,” writes Riana Pfefferkorn, associate director of surveillance and cybersecurity at Stanford Law School. “Or he could simply refuse to certify a set of best practices that aren’t sufficiently condemnatory of encryption. If the AG doesn’t finalize a set of best practices, then this entire safe-harbor option just vanishes.”

The whole thing is cloaked in the language of “child sex-abuse material” so that privacy advocates have to argue against a measure nominally aimed at kiddy porn in order to protect strong encryption protection for everybody’s communications. Yes, once again, government officials pretend that the terrible things they want to do are all about protecting the children.

Meanwhile, any back doors forced into our encrypted communications are likely to affect harmless people more than they inconvenience criminals and terrorists.

“Short of a form of government intervention in technology that appears contemplated by no one outside of the most despotic regimes, communication channels resistant to surveillance will always exist,” states a 2016 report from the Berkman Center for Internet and Society at Harvard University.

Unwilling to rely on commercial products that may or may not keep their secrets, criminals and terrorists develop their own encryption products—including secure phones. They’re very unlikely to comply with law enforcement demands for back doors.

“I think there’s no way we solve this entire problem,” the FBI’s Comey admitted to the U.S. Senate Judiciary Committee in 2015. “Encryption is always going to be available to the sophisticated user.”

But what about the rest of us? Despite all the evidence of the foolishness of their efforts, government officials keep trying to make us expose our data to them and the criminals who ride on their coattails.

from Latest – Reason.com https://ift.tt/2Pv3I5e

via IFTTT

It’s impossible to overstate just how much governments hate not being able to read your mail, listen to your phone calls, and peruse your text messages. When all that snoopy officials can pull up is scrambled gobbledygook, they just know they’re missing out on the good stuff, like little kids bristling at whispered adult conversations.

That explains the U.S. government’s decades-long war against private cryptography and its most recent manifestation in the crusade against “warrant-proof encryption.”

No matter how much government officials stamp their feet and hold their breath, it’d be a bad idea to give them the access they want to our data. And they do keep stamping their feet.

“By enabling dangerous criminals to cloak their communications and activities behind an essentially impenetrable digital shield, the deployment of warrant-proof encryption is already imposing huge costs on society,” Attorney General Bill Barr huffed last summer when he delivered the keynote address at the International Conference on Cyber Security in New York City. “It seriously degrades the ability of law enforcement to detect and prevent crime before it occurs. And, after crimes are committed, it thwarts law enforcement’s ability to identify those responsible or to successfully prosecute the guilty parties.”

If that sounds familiar, it’s because it’s essentially a rephrasing of former FBI Director James Comey’s 2014 argument that “those charged with protecting our people aren’t always able to access the evidence we need to prosecute crime and prevent terrorism even with lawful authority. We have the legal authority to intercept and access communications and information pursuant to court order, but we often lack the technical ability to do so.”

In turn, Comey barely rewarmed the Clinton White House’s overwrought 1994 warnings that “the same encryption technology that can help Americans protect business secrets and personal privacy can also be used by terrorists, drug dealers, and other criminals.”

The encryption technology that gets officials so hot and bothered year after year grows increasingly widespread for the simple reason that it satisfies a very real demand. Barr may worry about privacy-minded terrorists and drug sellers, but most people are more concerned about hackers, identity thieves, and nosy busybodies. In response, tech companies build end-to-end encryption into a host of products so that regular people can benefit without memorizing a user’s manual.

In response, Barr and company argue that all they want is a “back door” built into communications services so that they can gain access when necessary—and only after they jump through all the legal niceties, we’re assured.

But weakened, government-accessible encryption isn’t a magic solution that will be used only to catch bad guys. It will be weakened encryption, period.

“The problem with backdoors is known—any alternate channel devoted to access by one party will undoubtedly be discovered, accessed, and abused by another,” notes David Ruiz, a writer with the internet security firm Malwarebytes Labs. “Cybersecurity researchers have repeatedly argued for years that, when it comes to encryption technology, the risk of weakening the security of countless individuals is too high.”

“Encryption is one of the few security techniques that mostly works. We can’t afford to mess it up,” cautions Matt Blaze, a cybersecurity expert at the University of Pennsylvania. “As someone who’s been working on securing the ‘net for going on three decades now, having to repeatedly engage with this ‘why can’t you just weaken the one tool you have that actually works’ nonsense is utterly exhausting.”

How can we know that the critics are right? Because the U.S. government itself claims that a Chinese company has, for years, been misusing exactly such back doors.

“U.S. officials say Huawei Technologies Co. can covertly access mobile-phone networks around the world through ‘back doors’ designed for use by law enforcement, as Washington tries to persuade allies to exclude the Chinese company from their networks,” the Wall Street Journalreported on February 12.

Well, it’s only fair. For half a century, the CIA and German intelligence spied on international communications courtesy of back doors they built into the products of Crypto AG, a company the agencies co-owned.

The CIA and its German partner kept that arrangement secret for a long time, but mandated access to everybody’s messaging apps would be public knowledge and serious hacker-bait. It might even be a target for bad actors wielding the hacking tools that were stolen in 2017 from the National Security Agency—an exploit generally considered among the most significant events in cybersecurity.

Whoopsies. It’s almost like you really shouldn’t trust government types with the ability to peruse your communications and paw through your data.

Despite that history, Senators Lindsey Graham (R-S.C.) and Richard Blumenthal (D-Conn.) are floating a bill that would make tech companies “earn” Section 230 protection against liability for other people’s communications that pass through their platforms by adopting “best practices” that satisfy amorphous government standards.

“The AG could single-handedly rewrite the ‘best practices’ to state that any provider that offers end-to-end encryption is categorically excluded from taking advantage of this safe-harbor option,” writes Riana Pfefferkorn, associate director of surveillance and cybersecurity at Stanford Law School. “Or he could simply refuse to certify a set of best practices that aren’t sufficiently condemnatory of encryption. If the AG doesn’t finalize a set of best practices, then this entire safe-harbor option just vanishes.”

The whole thing is cloaked in the language of “child sex-abuse material” so that privacy advocates have to argue against a measure nominally aimed at kiddy porn in order to protect strong encryption protection for everybody’s communications. Yes, once again, government officials pretend that the terrible things they want to do are all about protecting the children.

Meanwhile, any back doors forced into our encrypted communications are likely to affect harmless people more than they inconvenience criminals and terrorists.

“Short of a form of government intervention in technology that appears contemplated by no one outside of the most despotic regimes, communication channels resistant to surveillance will always exist,” states a 2016 report from the Berkman Center for Internet and Society at Harvard University.

Unwilling to rely on commercial products that may or may not keep their secrets, criminals and terrorists develop their own encryption products—including secure phones. They’re very unlikely to comply with law enforcement demands for back doors.

“I think there’s no way we solve this entire problem,” the FBI’s Comey admitted to the U.S. Senate Judiciary Committee in 2015. “Encryption is always going to be available to the sophisticated user.”

But what about the rest of us? Despite all the evidence of the foolishness of their efforts, government officials keep trying to make us expose our data to them and the criminals who ride on their coattails.

from Latest – Reason.com https://ift.tt/2Pv3I5e

via IFTTT

Japan, China Close Schools Nationwide; South Korea Confirms 505 New Cases, Surpassing China For First TIme: Live Virus Updates

Update (0735ET): After yesterday’s rally fizzled, Germany is giving the ‘fiscal stimulus’ tape bomb one more go.

GERMAN GOVERNMENT CONSIDERING POSSIBLE STIMULUS PROGRAMME IN CASE CORONAVIRUS EPIDEMIC HITS GERMAN ECONOMY HARD – HANDELSBLATT

Yesterday, a German lawmaker poured cold water on reports that Germany might ditch its constitutional ‘debt break’ to boost spending in response to the economy-killing outbreak.

* * *

Update (0715ET): with the country’s third election in a year just days away, Israel is taking serious pains to avoid acknowledging the coronavirus cases that have been confirmed in the country by blaming them on Italy and South Korea (each case involved a traveler who had recently returned from one of those two countries).

The country said Thursday it would bar non-Israelis who had recently visited Italy after confirming that a man who had recently visited the country had tested positive for the virus, according to Reuters.

* * *

US equity futures are pointing to yet another lower open on Thursday morning after WaPo interrupted President Trump’s press conference last night to reports the first COVID-19 case “of unknown origin,” which the CDC later confirmed was in Sonoma County, and could be the epicenter of America’s first “community outbreak.” Shortly after, South Korea reported its largest number of new coronavirus cases in a single day, as the number of new cases reported outside China once again surpassed the number inside China. Brazil confirmed the first case in South America yesterday, bringing the virus to every continent except Antarctica.

A few hours later, and South Korea has reported another 171 cases, bringing the total cases confirmed on Thursday to 505 – surpassing China’s daily total (433) for the first time, as Bloomberg pointed out. So far, South Korea has confirmed 1,766 cases, along with 13 deaths, in the 38 days since the first case was reported on Jan. 20. The US and South Korea have cancelled planned military exercises after a US soldier caught the virus in Korea.

Over in Hawaii, Hawaiian Air has suspended service to South Korea starting March 2 through April 30, while Delta reduces flights as the outbreak in South Korea intensifies (Hawaii has already had one COVID-19 scare involving a Japanese tourist; we suspect the state wants to avoid a similar episode involving South Korea). Congresswoman and presidential candidate Tulsi Gabbard requesting a suspension of flights from South Korea and Japan as the outbreak in the US worsens.

Fearing the sudden breakout in the Middle East might spread inside its borders, Saudi Arabia has halted pilgrimages to Islam’s holy sites – known as the Hajj – that are a mandatory practice for Muslims. Across the Persian Gulf, Iran has now confirmed 26 deaths 245 cases. But given the virus’s rapid spread throughout the Islamic Republic, many suspect that the real number of cases is far higher (earlier in the week, a local lawmaker said 50 people had died in the city of Qom alone).

Iran Health Ministry spokesman Kianoush Jahanpour said the large number of new cases is due to more labs handling virus tests. He warned that the public should expect more cases in the future.

Yesterday, Greece was one of eight countries – Brazil, Pakistan, North Macedonia, of course Greece, Georgia, Algeria, Norway and Romania – to confirm their first cases. On Thursday, Greece confirmed two more cases, one of them in its capital city of Athens. The initial case was found in Thessaloniki, Greece’s second city.

At last count, coronavirus has infected more than 80,000 people around the world and caused more than 2,700 deaths since the outbreak began in Wuhan back in December.

Following Brazil’s confirmation overnight, its Latin American neighbors are taking steps to stop the virus from spreading across their borders. According to the AP, Peru is keeping a team of specialists working 24/7 at Jorge Chávez International Airport. Argentina has asked citizens to report any flu-like symptom. Puerto Rico has established a task force to prepare for an outbreak in Puerto Rico. And Chile has announced a health emergency and purchased millions of masks and protective outfits for health workers.

But perhaps the biggest story overnight came out of Japan, where the government swore yesterday that the Tokyo Games would take place as scheduled this summer, after an IOC member speculated that if the virus wasn’t cleared up by late May, Japan might be forced to cancel the Olympics.

PM Shinzo Abe asked all schools in Japan to remain closed until the spring holidays begin late next month to try and contain the virus. Abe’s decision follows a rash of new cases reported in the north of Japan, including the first cases in Hokkaido, with no discernible path of origin, Nikkei reports.

As of Thursday, 175 cases have been confirmed across 19 of Japan’s prefectures, including Hokkaido, Tokyo, Aichi, and Chiba. Earlier on Thursday, Hokkaido instituted a weeklong closure of all 1,600 public elementary and junior high schools. Abe made the announcement during a meeting of the government’s headquarters.

Schools must now decide whether to abide by the PM’s non-binding ask, though it’s expected that nearly all schools will comply.

Chinese Premier Li Keqiang, President Xi’s ‘point-man’ in charge of the coronavirus response, said that China will extend its school closures for another month because of the virus, according to CCTV.

In Australia, which confirmed a handful of cases during the early days of the outbreak, but has since gone quiet, PM Scott Morrison said Thursday in what some might describe as a ‘fearmongering’ speech that “there is every indication that the world will soon enter a pandemic phase of the coronavirus.”

“As a result, we have initiated the implementation of the coronavirus emergency response plan. While the WHO is yet to declare the nature of the coronavirus and its move toward a pandemic phase, we believe that the risk of a global pandemic is very much upon us and as a result, as a government, we need to take steps to prepare.”

WHO’s Dr. Tedros, who yesterday asked officials not to use the word ‘pandemic’, must have been thrilled to hear Morrison’s screed.

Morrison said Australians can still go “to the football match, or the concert” because Australia has “stayed ahead” of the virus. But now it’s time to move onto the next phase, which includes “preparation for the possibility of a much more significant event.”

‘There is every indication that the world will soon enter a pandemic phase of the coronavirus,’ Australian Prime Minister Scott Morrison said. Governments around the world are ramping up measures to battle a looming pandemic https://t.co/yHNaDgy54ypic.twitter.com/K9SXjTcq85

Over in France, French President Emmanuel Macron said “we have a crisis before us. An epidemic is on its way” during a visit to a Paris hospital where coronavirus patients are being treated. His statement followed reports that 2 have died in France, an elderly Christian tourist and a 60-year-old French national. The Frenchman died earlier this week in Paris at the hospital Macron visited Thursday. The total number of cases in France reached 18 on Wednesday, roughly the same number as neighboring Germany.

Spain detected two more cases on Thursday, bringing the total this week to 14. Neither was connected to Italy, health authorities said. Switzerland confirmed 3 more cases, bringing its total to 4, though Swiss authorities said they’re testing 66 others. In Italy, the number of confirmed cases climbed to 528. Of those, 278 are self-isolating at home, 159 recovered with symptoms in hospital and 37 are in intensive care.

As the AP reminds us, Germany’s health minister said Wednesday that the country was “at the beginning of an epidemic” as authorities in the west tested dozens of people. New cases on Thursday brought Germany’s total to 21.

Two new cases confirmed in the UK on Thursday raised the total to 15. A primary school in Buxton was forced to close for “a deep clean” after a parent of one of the students tested positive for the virus.

The EU Commission doubled-down on its anti-border-closure position, saying no EU country wants to close internal borders. Meanwhile, the FT reports that EU officials are weighing the risks of clusters of Italian-style outbreaks surface across the continent.

US Colleges Race To Cancel Study Abroad Programs, Especially In Italy, Amid Covid-19 Spread

With the confirmed number of coronavirus cases in Italy now nearing 400, including 12 deaths, and Germany, France and Spain now witnessing a growing caseload, a growing number of American universities are now canceling their study abroad programs due to Covid-19 fears.

Fox News reports that at least seven universities have suspended programs in Italy alone— with more schools expected to take the drastic action. In many cases it involves disrupting current ongoing programs, and undergoing the logistically difficult feat of getting hundreds of students home early to the US.

Image via Diablo Valley College

Schools especially with programs in southeast Asia are carefully eyeing restrictions and/or suspending their programs altogether, such as Florida International University, which announced Tuesday it is halting its expansive study abroad programs in Italy, Japan, and South Korea.

The school’s executive vice president, Kenneth G. Furton, said in a statement. “Education abroad spring programs to these countries are canceled. At the same time, any students or employees who are currently on university business in those countries must return to the U.S. immediately.”

The statement those who did recently travel to these places to “quarantine themselves at home and to stay away from campus.”

Universities are concerned their programs which allow students to spend weeks, months, or often whole semesters in Europe and Asia studying and exploring foreign countries could inadvertently see students and staff sent straight into impacted countries’ virus epicenters, such as northern Italy.

St. Peter’s Square at the Vatican, via AP.

“This was a difficult decision for the university to make, given that these students were already immersed in these important global experiences,” the dean of global education at Elon University, Woody Pelton, which just canceled its own programs, said in a news release.

“However, the health and safety of students is our top priority,” he added.

In one notable instance, Syracuse University actually currently has hundreds of students studying abroad in Italy. CNN reports that at least 342 Syracuse students are now organizing early returns from Italy.

Among American universities lately canceling programs abroad include Syracuse University, New York University, Fairfield University, Elon University, Stanford University, the University of Southern California, Sacred Heart and the University of New Haven – according to Fox.

Stanford called their study abroad students today to have them all return. “Get out while you can” was the call a friend’s student daughter was awakened to early this morning. #coronavirushttps://t.co/j82v6CGG1w

Students in current programs in many cases took to social media to vent their having to come home on short notice, with one noting Stanford informed program members to “get out while you still can”.

Gonzaga University in Washington state also announced late Wednesday it is suspending its Italy program, amid a fast growing trend of schools urging their students home this week.

The economic storm hasn’t passed; the false calm is only the eye of the financial hurricane.

To understand the economic cataclysm ahead, do the math. Those expecting the Covid-19 pandemic to leave the U.S. economy untouched are implicitly making these preposterously unlikely claims:

1. China will resume full pre-pandemic production and shipping within the next two weeks.

2. Chinese consumers will resume borrowing and spending at pre-pandemic rates in a few weeks.

3. Every factory and every worker in China will resume full pre-pandemic production without any permanent closures or disruptions.

4. Corporate America’s just-in-time inventories will magically expand to cover weeks or months of supply chain disruption.

5. Not a single one of the thousands of people who flew direct from Wuhan to the U.S. in January is an asymptomatic carrier of the coronavirus who escaped detection at the airport.

6. Not a single one of the thousands of people who flew from China to the U.S. in February is an asymptomatic carrier of the coronavirus.

7. Not a single one of the thousands of people who are in self-quarantine broke the quarantine to go to Safeway for milk and eggs.

8. Not a single person who came down with Covid-19 after arriving in the U.S. feared being deported so they did not go to a hospital and are therefore unknown to authorities.

9. Even though U.S. officials have only tested a relative handful of the thousands of people who came from Covid-19 hotspots in China, they caught every single asymptomatic carrier.

10. Not a single asymptomatic carrier caught a flight from China to Southeast Asia and then promptly boarded a flight for the U.S.

I could go on but you get the picture: an extremely contagious pathogen that is spread by carriers who don’t know they have the virus to people who then infect others in a rapidly expanding circle has been completely controlled by U.S. authorities who haven’t tested or even tracked tens of thousands of potential carriers in the U.S.

These same authorities are quick to claim the risk of Covid-19 spreading in the U.S. is low even as the 14 infected people they put on a plane ended up infecting 25 passengers on the flight. These same authorities tried to transfer quarantined people to a rundown facility in Costa Mesa CA that was not suitable for quarantine, forcing the city to file a lawsuit to stop the transfer.

Do these actions instill unwavering confidence in the official U.S. response? You must be joking.

Do the math, people. The coronavirus is already in the U.S. but authorities have no way to track it due to its spread by asymptomatic carriers. People who don’t even know they have the virus are flying to intermediate airports outside China and then catching flights to the U.S.

None of the known characteristics of the virus support the confidence being projected by authorities. The tests are not reliable, few are being tested, carriers can’t be detected because they don’t have any symptoms, the virus is highly contagious, thousands of potential carriers continue to arrive in the U.S., etc. etc. etc.

The network of global travel remains intact. Removing a few nodes (Wuhan, etc.) does not reduce the entire network’s connectedness that enables the rapid and invisible spread of the virus.

It doesn’t take thousands of cases to trigger a dramatic reduction in the willingness to mix with crowds of strangers. A relative handful of cases is enough to be consequential.

Many of the new jobs created in the U.S. economy over the past decade are in the food and beverage services sector, the sector that is immediately impacted when people decide to lower their risk by staying home rather than going out to crowded restaurants, theaters, bars, etc.

Many of these establishments are hanging on by a thread due to soaring rents, taxes, fees, healthcare and wages. Many of the employees are also hanging on by a thread, only making rent if they collect big tips.

Central banks can borrow money into existence but they can’t replace lost income. A significant percentage of America’s food and beverage establishments are financially precarious, and their exhausted owners are burned out by the stresses of keeping their business afloat as costs continue rising. The initial financial hit as people reduce their public exposure will be more than enough to cause many to close their doors forever.

As small businesses fold, local tax revenues crater, triggering fiscal crises in local government budgets dependent on ever-higher tax and fee revenues.

A significant percentage of America’s borrowers are financially precarious, one paycheck or unexpected expense away from defaulting on student loans, subprime auto loans, credit card payments, etc.

A significant percentage of America’s corporations are financially precarious, dependent on expanding debt and rising cash flow to service their expanding debt load. Any hit to their revenues will trigger defaults that will then unleash second-order effects in the global financial system.

The global economy is so dependent on speculative euphoria, leverage and debt that any external shock will tip it over the cliff. The U.S. economy is far more precarious than advertised as well.

The economic storm hasn’t passed; the false calm is only the eye of the financial hurricane.

Italy Investigating Price Gouging Into Coronavirus Masks And Hand Sanitzer

Italian regulators are beginning to investigate the free market price gouging online for items like hygienic masks and sanitizing gels as the novel coronavirus has started raging its way through the country.

The country has suffered the largest outbreak in Europe and has reported over 260 cases and 7 deaths, most of which are occurring in the North of the country, according to Reuters.

Milan deputy chief prosecutor Tiziana Siciliano said: “We have decided to open an investigation after media reports of the insane prices fetched up by these products (masks and gels) on online sales websites in the last two days.”

As the coronavirus continues to make its way through the country, many local shops and pharmacies have run out of masks and sanitizer gels, causing people to resort to buying the items online, where prices have (naturally) risen.

What a honeymoon in Rome looks like in 2020

“The price of masks online has risen from one cent to 10 euros each and a one-liter bottle of disinfectant that last week was on sale for 7 euros, was up to 39 euros yesterday,” Siciliano continued.

Sales of hand sanitizers are up 9x in Italy to 900,000 packs over the first six weeks of 2020. They’re expected to reach and eclipse the 1 million mark by the end of the month.

Nielsen Research Institute said on Tuesday:

“Sales of hygienic hand gels have gone through the roof. The shelves of big retailers (hypermarkets, supermarkets, cash and carry, specialist pharmacists and discounters) have been cleared out.”

Even more dystopian and frightening, police are also warning citizens that criminals may pose as health inspectors to gain access to peoples homes to steal money or other valuables.

{kind=link}

{kind=link}

{kind=link}