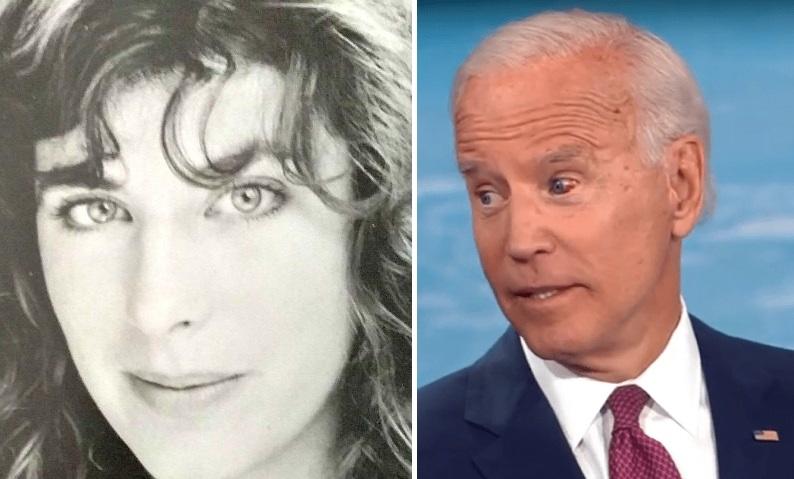

NYT Deletes Tweet, Stealth-Edits Article After Excusing Biden Sexual Misconduct

The New York Times, which tried to sabotage Supreme Court Justice Brett Kavanaugh’s career with months of baseless #MeToo allegations – not only downplayed Joe Biden’s well-documented history of unwanted physical contact with women on Sunday, they cast extreme doubt on a detailed sexual assault allegation by former Biden staffer Tara Reade.

The original article, which can be seen in the Wayback Machine reads: “No other allegation about sexual assault surfaced in the course of reporting, nor did any former Biden staff members corroborate any details of Ms. Reade’s allegation. The Times found no pattern of sexual misconduct by Mr. Biden, beyond the hugs, kisses and touching that women previously said made them uncomfortable.“

The current, stealth-edited version now reads: “No other allegation about sexual assault surfaced in the course of reporting, nor did any former Biden staff members corroborate any details of Ms. Reade’s allegation. The Times found no pattern of sexual misconduct by Mr. Biden.“

Reade filed a police report against Biden with the Washington D.C. police alleging that the former Vice President (and then Senator) forcibly penetrated her without consent in 1993. She does not reference Biden by name in the complaint, which the Biden campaign has strongly denied.

The Times, meanwhile, had the audacity to write: “Filing a false police report may be punishable by a fine and imprisonment.“

Remember the press spent a month essentially arguing that underage drinking was evidence that Kavanaugh committed sexual assault, but a long pattern of “hugs, kisses, and touching that women previously said made them uncomfortable” proves Biden’s innocence. pic.twitter.com/CPGr48o8nK

Look at how the Times framed Kavanaugh and his accuser, Christine Blasey Ford – whose allegations that Kavanaugh sexually assaulted her at a gathering in the mid 1980s were refuted by every single person at the party.

I think what is frustrating about kavanaugh is not only assumption of guilt is they were trying to paint him as this frat boy that did whatever he wanted pic.twitter.com/PSqqIglahu

The declaration for the state comes about three weeks after the first disaster order in New York, the epicenter of the virus.

Non-state territories including the U.S. Virgin Islands, the Northern Mariana Islands, Washington, Guam, and Puerto Rico are all under disaster declarations. The only one that isn’t under such a declaration is American Samoa.

“Public Assistance Federal funding is available to the state, tribal and eligible local governments and certain private nonprofit organizations on a cost-sharing basis for emergency protective measures, including direct federal assistance under Public Assistance, for all areas in the state of Wyoming affected by COVID-19 at a federal cost share of 75 percent,” Trump’s declaration on Wyoming read.

It’s the first time a president has ever declared a major disaster in all 50 states at the same time, said deputy press secretary Judd Deere.

🚨With @realDonaldTrump’s declaration for WY, the President has now declared for the 1st time in history that a major disaster exist within all 50 states at once. The President continues to respond to the needs of every Governor to protect the health of all Americans. 🇺🇸 #COVID19

“The President continues to respond to the needs of every Governor to protect the health of all Americans,” Deere wrote on Twitter on Saturday.

Wyoming Gov. Mark Gordon sought the declaration last week in a letter to Trump.

“Though Wyoming has not reached the dire situations of some states, this declaration will help us to prepare and mobilize resources when we need them,” Gordon said, according to news reports.

The United States, meanwhile, has surpassed Italy on Saturday as the country with the most deaths related to the CCP (Chinese Communist Party) virus pandemic, according to a running tally from Johns Hopkins University.

Despite the data, there have been indicators that the social distancing guidelines are working, said Trump on Friday.

“Nationwide, the number of new cases per day is flattening substantially, suggesting that we are near the peak and our comprehensive strategy is working,” he said during a White House briefing.

Trump added that he is now looking to create a taskforce that is comprised of doctors and business leaders aimed at reopening the U.S. economy.

Health authorities have urged Americans to avoid close contact with one another, use good hand-washing hygiene, and not leave their homes as much as possible. Symptoms of the potentially fatal disease include fever, cough, and shortness of breath, according to the Centers for Disease Control and Prevention.

Turkey’s Interior Minister Resigns Over Coronavirus Curfew Chaos, Erdogan Rejects Resignation

After cynically urging Syrian refugees toward coronavirus-hit Europe, Turkey’s Interior Minister Suleyman Soylu announced on Twitter on Sunday that he was resigning from his post over the chaotic implementation of a two-day curfew in major Turkish cities to tackle the coronavirus outbreak.

The resignation followed Turkey’s announcement, late on Friday, of a weekend lockdown but in the brief time before it went into effect many people rushed out to buy food and drink in the country’s commercial hub Istanbul, a city of 16 million people, and other cities.

“Although in a limited period of time, the incidents that occurred ahead of the implementation of the curfew was not befitting with the perfect management of the outbreak process,” Soylu said in his statement.

Soylu, who has held the post since August 2016, shortly after the failed staged coup against Erdogan, said the scenes that took place just following the declaration of the curfew on Friday night did not reflect a smooth implementation of policy. Soylu added that he had been proud to serve as interior minister and would remain loyal to Erdogan.

The lockdown decision was taken with good intention and aimed at slowing the spread of coronavirus, he said. The lockdown ended at 2100 GMT on Sunday, prompting questions why it was started in the first place, as a 48 hour lock down achieves absolutely nothing.

However, Soylu’s resignation was even shorter than Turkey’s curfew as just hours after the interior minister’s resignation announcement, President Erdogan rejected the resignation, sparking celebration among Turkey’s nationalists.

#Turkey’s Interior Min resigns, taking blame for botched curfew. Social media erupts with shock that a Turkish politician has actually taken responsibility. AKP rumour mill starts. Erdogan rejects resignation. Nationalists celebrate. As you were, Turkey. pic.twitter.com/PpRNB1EWju

If his resignation had been accepted by President Erdogan, Soylu would have been the second Turkish minister to leave his post since the coronavirus pandemic was declared. Transport Minister Mehmet Cahit Turhan was removed two weeks ago after the ministry drew criticism for holding a tender amid the outbreak to prepare to build a huge canal on the edge of Istanbul.

On Sunday, Turkey reported 97 more deaths related to the novel coronavirus, bringing the death toll to 1,198. The country also has nearly 57,000 confirmed cases since the first patient was diagnosed a little more than a month ago.

When The World Stopped – Stunning Scenes From A Global Lockdown

Deaths breached the 100,000 mark on Friday, another grim milestone for the world engulfed in a pandemic.

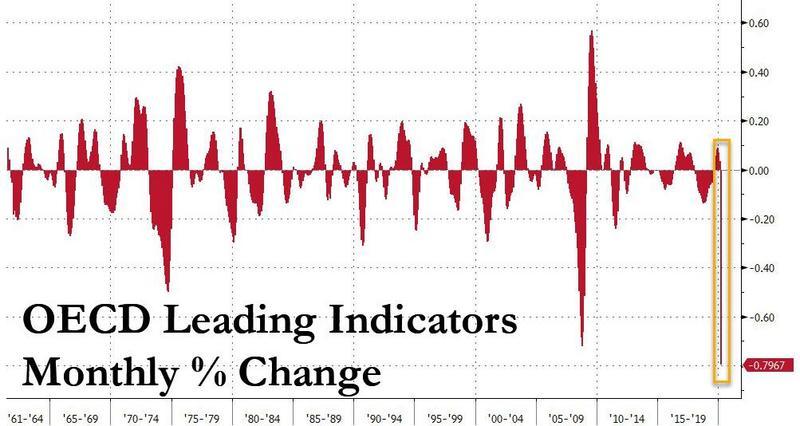

More than a billion people across the world remain in quarantine as the global economy crashes into a depression in the second quarter. The OECD and WTO on Wednesday published two separate reports that both outline global economic activity has collapsed.

The OECD Leading Indicators show the global economy experienced a sharp decline in the last month.

The WTO shows world trade has plunged well below 2008 levels. One word: unprecedented.

As a result of quarantines, unemployment claims have rocketed higher in nearly every major developed and emerging market economy. Tens of millions of people have been laid off as streets, highways, shopping districts, and manufacturing hubs have become lifeless.

While words can only describe so much of a world in lockdown, Bloomberg has published a handful of pictures illustrating what the world looks like after a month of pandemic:

New York City

A lone pedestrian walks inside the Oculus, a transportation and shopping hub in Manhattan’s financial district on March 30. H/T Photographer Gabby Jones/Bloomberg

Los Angeles

The usually busy 110 freeway on April 1. H/T Photographer Patrick T. Fallon/Bloomberg

Paris

The Arc de Triomphe looms over an empty Champs Elysees and its shuttered luxury retailers on April 4. H/T Photographer Cyril Marcilhacy/Bloomberg

Milan

Umbrellas outside closed cafes line a street leading to the Navigli canal system on April 8. Photographer H/T Francesca Volpi/Bloomberg

Sao Paulo

The Municipal Market on April 8. H/T Photographer: Rodrigo Capote/Bloomberg

Moscow

Police patrol a deserted Red Square on April 2. H/T Photographer: Andrey Rudakov/Bloomberg

Jerusalem

The Old City on March 29. H/T Photographer: Kobi Wolf/Bloomberg

Istanbul

An empty walkway inside the Grand Bazaar on March 25. H/T Photographer: Kerem Uzel/Bloomberg

London

Banners fly outside closed luxury boutiques on New Bond Street on April 9. H/T Photographer: Simon Dawson/Bloomberg

Toronto

Security guards are among the few people inside the Toronto Eaton Centre on March 25. H/T Photographer: Cole Burston/Bloomberg

Madrid

Shuttered bars and tapas restaurants line a deserted street on March 16. H/T Photographer: Angel Navarrete/Bloomberg

Mumbai

Men sit inside the closed Crawford Market on March 25. H/T Photographer: Dhiraj Singh/Bloomberg

Lisbon

A pedestrian crosses a deserted street of usually crowded shops and cafes on March 22. H/T Photographer: Jose Sarmento Matos/Bloomberg

It becomes evident that the world has ground to a halt in one of the fastest economic crashes ever. It remains to be seen if the recovery phase is V-shaped, U-shaped, or L-shaped.

More or less, we’re leaning towards an L-shaped recovery…

President Donald Trump has an expansive view of how much unchecked power the U.S. chief executive can wield. For example, in a speech back in July 2019, he asserted, “I have an Article II, where I have to the right to do whatever I want as president.” The Article II to which Trump was referring is the section of the U.S. constitution that outlines the powers given to the president. Among other things, that article requires that the president “shall take care that the laws be faithfully executed.” An ordinary language reading of that section does not prima facie suggest that it gives a president the right to whatever he or she wants to do.

More recently, during a March 12 White House press availability, Trump was asked if he was going to declare a national emergency in response to the coronavirus pandemic. “We have very strong emergency powers under the Stafford Act,” responded the president. He then added, “I have the right to do a lot of things that people don’t even know about.”

In a chilling op-ed in TheNew York Times, Brennan Center legal scholars Elizabeth Goitein and Andrew Boyle suggest that Trump’s statement could be referring to the secret powers that previous presidents have granted themselves in “presidential emergency action documents.” As Goitein and Boyle explain:

These documents consist of draft proclamations, executive orders and proposals for legislation that can be quickly deployed to assert broad presidential authority in a range of worst-case scenarios….These include suspension of habeas corpus by the president (not by Congress, as assigned in the Constitution), detention of United States citizens who are suspected of being “subversives,” warrantless searches and seizures and the imposition of martial law.

As the coronavirus pandemic worsens, it is not far-fetched to think that President Trump might seek to exercise the heretofore secret emergency powers delineated in the documents. “Even in the most dire of emergencies, the president of the United States should not be able to operate free from constitutional checks and balances,” they argue. “Presidential emergency action documents have managed to escape democratic oversight for nearly 70 years. Congress should move quickly to remedy that omission and assert its authority to review these documents, before we all learn just how far this administration believes the president’s powers reach.”

It is way past time for Congress to rein in unconstitutional assertions of executive power by exposing and incinerating these secret presidential emergency action documents. Meanwhile, President Trump needs to adhere to his Article II oath: “I do solemnly swear (or affirm) that I will faithfully execute the office of President of the United States, and will to the best of my ability, preserve, protect and defend the Constitution of the United States.”

from Latest – Reason.com https://ift.tt/2y7pshO

via IFTTT

There’s no doubt that the Coronavirus is a serious infection that can lead to severe illness or death. There’s also no doubt that ‘virus hysteria’ has been used for other purposes. Wall Street, for example, has used virus-panic to advance its own agenda and get another round of trillion dollar bailouts. In fact, it took less than a week to get the pushover congress to ram through a massive $2.2 trillion boondoggle without even one lousy congressman offering a peep of protest. That’s got to be some kind of record.

In 2008, at the peak of the financial crisis, Congress voted “No” to the $700 billion TARP bill. Some readers might recall how a number of GOP congressmen bravely banded together and flipped Wall Street “the bird”. That didn’t happen this time around. Even though the bill is three times bigger than the TARP ( $2.2 trillion), no one lifted a finger to stop it. Why?

Fear, that’s why. Everyone in congress was scared to death that if they didn’t rush this debt-turd through the House pronto, the economy would collapse while tens of thousands of corpses would be stacking up in cities across the country. Of course the reason they believed this nonsense was because the goofy infectious disease experts confidently assured everyone that the body-count would be “in the hundreds of thousands if not millions.” Remember that fiction? The most recent estimate is somewhere in the neighborhood of 60,000 total. I don’t need to tell you that the difference between 60,000 and “millions” is a little more than a rounding-error.

So we’ve had the wool pulled over our eyes, right? Not as bad as congress, but, all the same, we’ve been hoodwinked and we’ve been fleeced. And the people who have axes to grind have been very successful in taking advantage of the hysteria and promoting their own agendas. Maybe you’ve noticed the reemergence of creepy Bill Gates and the Vaccine Gestapo or NWO Henry Kissinger warning us that, “the world will never be the same after the coronavirus”.

What do these people know that we don’t know? Doesn’t it all make you a bit suspicious? And when you see nonstop commercials on TV telling you to “wash your hands”or “keep your distance” or “stay inside” and, oh yeah, “We’re all in this together”, doesn’t it leave you scratching your head and wondering who the hell is orchestrating this virus-charade and what do they really have in mind for us unwashed masses??

At least in the case of Wall Street, we know what they want. They want money and lots of it.

Have you looked over the $2.2 trillion CARES bill that Trump just signed into law a couple weeks ago? It’s pretty grim reading, so I’ll save you the effort. Here’s a rough breakdown:

$250 billion will go for the $1,200 checks that most of us will receive in a couple weeks.

And $250 billion will be provided for extended unemployment insurance benefits.

That’s $500 billion.

Working people will get $500 billion while Wall Street and Corporate America will get 3 times that amount. ($1.7 trillion)

And even that’s a mere fraction of the total sum because– hidden in the small print– is a section that allows the Fed to lever-up the base-capital by 10-to-1 ($450 billion to $4.5 trillion) which means the Fed can buy as many “toxic” bonds and garbage assets as it chooses.

The Fed is turning itself into a hedge fund in order to buy the sludge that has accumulated on the balance sheets of corporations and financial institutions for the last decade.

It’s another gigantic ripoff that’s being cleverly concealed behind the ridiculous coronavirus hype. It’s infuriating.

So here’s the question:

Do you think Congress knew that working people would only get a pittance while the bulk of the dough would go to Wall Street?

It’s hard to say, but they certainly knew that the economy was cratering and that $500 billion wasn’t going to put much of a dent in a $20 trillion economy. In other words, even if everyone goes out and blows their measly $1,200 checks on Day 1, we’re still going to experience the sharpest economic contraction on record, a second Great Depression.

Maybe they should have talked about that in congress before they voted for this trillion-dollar turkey? Maybe they should have thought a little more about how the money should be distributed: Should it go to the people who actually buy things, generate activity and produce growth, or to the parasite class that blows up the system every decade and drags the economy down a black hole? That seems like something you might want to know before you pass a multi-trillion dollar bill that’s supposed to fix the economy.

It’s also worth noting that the $5.8 trillion is not nearly the total amount that Wall Street will eventually get. The Fed has already spent $2 trillion via its QE program (to shore up the dysfunctional repo market) and Fed chair Jay Powell announced on Thursday that another $2.3 trillion in loans and purchases would be used to buy municipal bonds, corporate bonds and loans to small businesses. The allocation for small businesses, which falls under the, Main Street Lending Program, has been widely touted as a sign of how much the Fed really cares about struggling Mom and Pop businesses that employ the majority of working Americans. But, once again, it’s a sham and a boondoggle. The program is on-track to get $600 billion funding of which the US Treasury will provide the base-capital of $75 billion. The rest will be levered-up by 9-to-1 by the Fed, which means it’s just more smoke and mirrors.

What readers need to realize is that the Treasury has accepted the credit risk for all of the loans that default. In other words, the American people are now on the hook for 100% of all of the loans that go south, and there’s going to be alot of them because the banks have no reason to find creditworthy borrowers. They get a 5% cut off-the-top whether the loans blow up or not. And, that, my friend, is how you incentivize fraud which, as Bernie Sanders noted, “is Wall Street’s business model.”

It also helps to explain why Trump has repeatedly rejected congressional oversight of the various bailout programs. He’s smart enough to know a good swindle when he sees one, and this one is a corker. The government is essentially waving trillions of dollars right under the noses of the world’s most ravenous hyenas expecting them not to act in character. But of course they will act in character and hundreds of billions of dollars will be siphoned off by scheming sharpies who figure out how game the system and turn the whole fiasco into another Wall Street looting operation. You can bet on it.

So, what is the final tally?

Well, according to Trump’s chief economic advisor, Larry Kudlow, the first bailout installment is $6.2 trillion (after the Fed ramps up the Treasury’s contribution of $450 billion.). Then there’s the $2.3 trillion in additional programs the Fed announced on Thursday. Finally, the Fed’s QE program adds another $2 trillion in bond purchases since September 17, when the repo market went haywire.

Altogether, the total sum amounts to $10.5 trillion.

You know what they say, “A trillion here, a trillion there, pretty soon you’re talking real money.”

Of course, no one on Capitol Hill worries about trivialities like money because, “We’re the United States of America, and our dollar will always be King.” But there’s a fundamental flaw to this type of thinking. Yes, the dollar is the world’s reserve currency, but that’s a privilege that the US has greatly abused over the years, and it’s certainly not going to survive this latest wacky helicopter drop. No, I am not suggesting the US would ever default on its debt, that’s not going to happen. But, yes, I am suggesting that the US will have to repay its debts in a currency that has lost a significant amount of its value. You don’t have to be Einstein to figure out that you can’t willy-nilly print-up $10 or $20 trillion dollars without eroding the value of the currency. That’s a no-brainer. Central bankers around the world are now looking at their piles of USDs thinking, “Hmmm, maybe it’s time I traded some of these greenbacks in for a few yen, euros or even Swiss francs?”

So how does this end? Can the Fed continue to write trillion dollar checks on an account that is already $23 trillion overdrawn? Will Central banks around the world continue to stockpile dollars when the Fed is printing them up faster than anyone can count? And what about China? How long before China realizes that US Treasuries are grossly overvalued, that US equities markets are unreformable, that the dollar is backed by nothing but red ink, and that Wall Street is the biggest and most corrupt cesspit on earth?

Not long, I’d wager. So, how does this end? It ends in a flash of monetary debasement preceded by a violent and destabilizing currency crisis. It’s plain as the nose on your face. The Fed knows that when a nation’s sovereign debt exceeds 100% of GDP, “there’s almost no mathematical way to service that debt in real terms.” Well, the US passed that milestone way-back in 2019 before this latest drunken spending-spree even began. It’s safe to say, we’ve now entered the financial Twilight Zone, the Land of No Return. If we add the Fed’s bulging balance sheet to the final estimate, (after all, it’s just another shady Enron-type Special Purpose Vehicle) the national debt will be somewhere north of $33 trillion by year-end, which means that Uncle Sam will be the greatest credit risk on Planet Earth. Imagine how jaws will drop on the day that Moodys and Fitch slash the ratings on US Treasuries to Triple B “junk” status. That should turn a few heads.

So what can we expect in the months to come?

First, the economy is going to slip into a deflationary period as people get back to work and slowly resume their spending.

But once demand picks up and the Fed’s liquidity starts to kick in, the economy will rebound sharply followed by steadily rising prices.

That’s the red flag that will signal a weakening dollar.

Similar to 1933, when Roosevelt took the U.S. off the gold standard and printed money like crazy, economic activity picked up but the value of the dollar dropped by 40%.

A similar scenario seems likely here as well.

Economist Lyn Alden Schwartzer summed it up like this in an article at Seeking Alpha:

“One of the common debates is whether all of this debt, counteracted by a tremendous monetary expansion by the Federal Reserve in response, will cause a deflationary bust or an inflationary problem…..Fundamentally, evidence points to a period of deflation due to this global shutdown and demand destruction shock, likely followed in the coming years by rising inflation….

In the coming years, the United States will be effectively printing money to fund large fiscal deficits, while also having a large current account deficit and negative net international investment position. This is one of the main variables for my view that the dollar will likely decrease in value relative to a basket of foreign currencies in the coming years….” (“Why This Is Unlike The Great Depression”, Seeking Alpha)

So, after decades of lethal low interest rates, relentless meddling and gross regulatory malpractice, the Fed has led us to this final, fatal crossroads: Inflate or default.

From the looks of things, the choice has already been made. Wiemar America, here we come!

“The Cut Is Just 4.3MMbpd”- Goldman Throws Up Over OPEC+ Deal, Sees Oil Dropping Back To $20

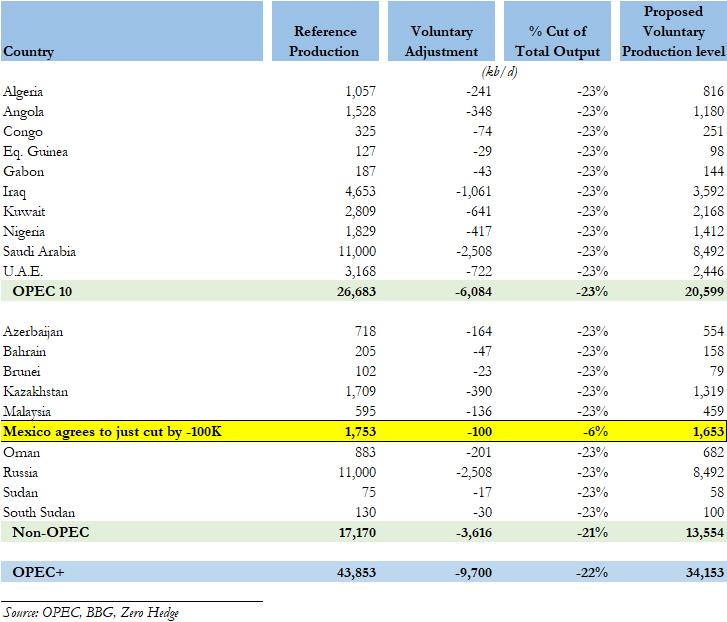

Earlier today, when summarizing the terms of the “historic” OPEC+ cut, which was presented theatrically as a 10MMb/d 9.7MMb/d by OPEC+ and all the oil bulls (including Citi’s Ed Morse who may have been acting in his capacity as OPEC advisor instead of Citi commodity analyst, when he immediately raised his oil price target) we said “OPEC Reaches “Historic” Deal To Cut Oil Production As Mexico Wins “Mexican Standoff” With Saudis… But It’s Not Enough” because “in a world where there is now up to 36MMb/d less oil demand, the world’s oil producers have agreed to cut production by… 9.7MMb/d” and added that “the real cuts when ignoring accounting gimmicks, amount to just over 7mmb/d, still a record amount, but hardly enough to put an even modest dent in today’s massively oversupplied market.”

As a reminder, this is what OPEC+ agreed on, with Mexico an outlier after winning the “Mexican standoff” with Saudi Arabia which would grant the country an exemption from the deal, in cutting just 6% of production, or 100Kb/d, instead of the 23% agreed by everyone else (whether they actually do cut production by 23% is an entirely different matter, now that everyone will feel slighted by the Mexican special treatment and look to cheat by maximizing their output, especially if the price of oil does not rebound).

With that in mind, moments ago Goldman’s commodity analyst Damien Couravalin published his latest OPEC+ deal post-mortem, in which he agreed with our take (and even title) and in a report titled “A historic yet insufficient cut”, he writes that “taking into account updated core-OPEC production guidance from April, this 9.7 mb/d “headline” deal represents a 12.4 mb/d cut from claimed April OPEC+ production (given the Saudi, UAE, Kuwait ongoing surge) but an only 7.2 mb/d cut from 1Q20 average production levels.“

Precisely as we said 4 hours earlier.

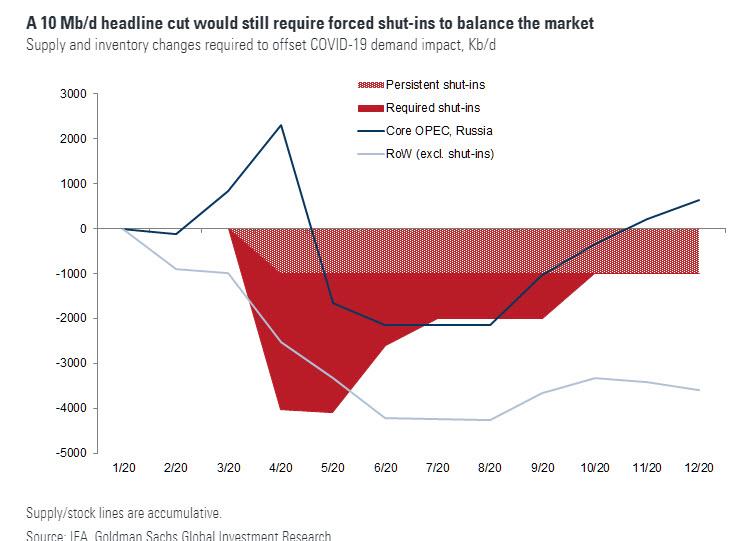

Doing the math, the Goldman analyst calculates that “the OPEC+ voluntary cut would only lead to an actual 4.3 mb/d reduction in production from 1Q20 levels” adding that “based on our updated oil balances, such OPEC+ voluntary cuts would still require an additional 4.1 mb/d cut in May production at the binding storage capacity constraint” which means that “at the 35% compliance level outside of core-OPEC, the necessary production cuts need would need to be 0.5 mb/d larger.”

Then, having been skeptical about the deal all along, Couravlin adds that “today’s agreement leaves the voluntary cuts as still too little and too late to avoid breaching storage capacity, ensuring that low oil prices force all producers to contribute to the market rebalancing” which prompts the Goldman analyst to reiterate his view that “inland crude prices will decline further in coming weeks as storage capacity becomes saturated and expect further weakness in WTI timespreads and crude prices in coming weeks, as already presaged on Friday, with downside risks to our short-term $20/bbl forecast.“

Judging by the swift and violent drop in oil once the market reopened at 600pm ET, following a very brief kneejerk move higher the market agrees.

His full note is below:

A historic yet insufficient cut

OPEC+ members have agreed to cut production by a record large 9.7 mb/d from May 1. The agreement came after settling over a smaller contribution from Mexico of only 0.1 mb/d instead of the 0.4 mb/d initially planned. Taking into account updated core-OPEC production guidance from April, this 9.7 mb/d “headline” deal represents a 12.4 mb/d cut from claimed April OPEC+ production (given the Saudi, UAE, Kuwait ongoing surge) but an only 7.2 mb/d cut from 1Q20 average production levels.

G20 ministers appear to have also committed to output reductions, with headlines today of potentially 3.7 mb/d output cuts by the US, Brazil and Canada or even 5 mb/d mentioned on Friday. These are very unlikely to be voluntary cuts but instead set to occur over time and due to market forces (ie. low prices) given the significant geological and regulatory hurdles in reducing production (well illustrated by Mexico’s refusal to cut by a reported 0.4 mb/d following its 50% increase in upstream capex since 2018), with the Iranian minister adding that they could take a year. We therefore do not count these as voluntary cuts in our oil balance.

Optimistically, assuming full compliance from core-OPEC and 50% compliance by all other participants already in May (vs. 35% achieved in Jan/Feb-19 despite the new cut being 8x larger), the OPEC+ voluntary cut would only lead to an actual 4.3 mb/d reduction in production from 1Q20 levels. Based on our updated oil balances, such OPEC+ voluntary cuts would still require an additional 4.1 mb/d cut in May production at the binding storage capacity constraint. At the 35% compliance level outside of core-OPEC, the necessary production cuts need would need to be 0.5 mb/d larger.

Given the difficulty for most producers outside of core-OPEC to implement large cuts, today’s agreement leaves the voluntary cuts as still too little and too late to avoid breaching storage capacity, ensuring that low oil prices force all producers to contribute to the market rebalancing. Ultimately, this simply reflects that no voluntary cuts could be large enough to offset the 19 mb/d average April-May demand loss due to the coronavirus. We therefore reiterate our view that inland crude prices will decline further in coming weeks as storage capacity becomes saturated and expect further weakness in WTI timespreads and crude prices in coming weeks, as already presaged on Friday, with downside risks to our short-term $20/bbl forecast.

The reduction in seaborne exports from OPEC+ producers will however likely lead Brent prices to outperform as the cut in seaborne exports (especially from the record April Saudi/UAE export program) will ease the pull on the global VLCC fleet, freeing vessels to be used for floating storage and capping freight rates. We therefore expect Brent prices to outperform WTI prices in coming weeks. The announcement of today’s cuts may also provide some support to long-dated prices as the expected price support later this year creates a disincentive for producers to add new hedges and instead likely incentivize them to monetize existing ones (a buying flow of forwards)

Finally, Reuters reported that the IEA is set to announce this week oil purchases into SPR that would contribute towards effective oil output cuts. For example, a 2.5 mb/d SPR purchase announcement would help square the “20 mb/d cut” stated in the OPEC+ draft statement (pegging OPEC+ at 12.5 mb/d cut and G20 at 5 mb/d). Importantly, we do not view such SPR purchases as changing our supply-demand balance since we estimate that combined commercial and government storage capacity would be reached by late April, with 4 mb/d of production shut-ins required even before the OPEC+ deal starts. Such a high SPR purchase pace would further likely be logistically difficult as strategic reserves are designed for fast drawdowns not fills, and typically operate at high utilization levels with low spare capacity.

Aerial View Of Manhattan In Lockdown, Now A Ghost Town!

The latest aerial view of Manhattan in lockdown is riveting. YouTube account Mingomaticflew a drone over the island on Sunday morning (April 12) and found a city straight out of I Am Legend.

The video starts with a broad view of Manhattan from the sky, then cuts to ground level scenes. The drone flies around some of the highest-trafficked areas, such as the Financial District, Grand Central Terminal, Rockefeller Center, Times Square, Radio City, and Chinatown, to only find just a couple of cars and less than a dozen people in the entire 5-minute video. The video ends with an impressive tilt shot of the New York Stock Exchange with no one on the street.

Lifeless Manhattan illustrated in ten images:

Charging Bull:

NYSE Exchange:

West 50th Street:

West 48th Street:

Grand Central Terminal:

Chinatown:

Globe Sculpture at Columbus Circle:

Rockefeller Center:

Rainbow Room NBC Studios:

Empire State Building:

Here are Mingomatic’s other impressive drone shots detailing how NYC and Jersey have transformed into ghost towns:

President Trump has an expansive view of how much unchecked power the U.S. chief executive can wield. For example, in a speech back in July, 2019, he asserted, “I have an Article II, where I have to the right to do whatever I want as president.” The Article II to which Trump was referring is the section of the U.S. constitution that outlines the powers given to the president. Among other things, that article requires that the president “shall take care that the laws be faithfully executed.” An ordinary language reading of that section does not prima facie suggest that it gives a president the right to whatever he or she wants to do.

More recently during a March 12 White House press availability Trump was asked if he was going to declare a national emergency in response to the coronavirus pandemic? “We have very strong emergency powers under the Stafford Act,” responded the president. He then added, “I have the right to do a lot of things that people don’t even know about.”

In a chilling op-ed in the New York Times, Brennan Center for Justice at New York University School of Law legal scholars Elizabeth Goitein and Andrew Boyle suggest that Trump’s statement could be referring to the secret powers that previous presidents have granted themselves in “presidential emergency action documents.” As Goitein and Boyle explain:

These documents consist of draft proclamations, executive orders and proposals for legislation that can be quickly deployed to assert broad presidential authority in a range of worst-case scenarios. …These include suspension of habeas corpus by the president (not by Congress, as assigned in the Constitution), detention of United States citizens who are suspected of being “subversives,” warrantless searches and seizures and the imposition of martial law.

As the coronavirus pandemic worsens, it is not far-fetched to think that President Trump might seek to exercise the heretofore secret emergency powers delineated in the documents. “Even in the most dire of emergencies, the president of the United States should not be able to operate free from constitutional checks and balances,” they argue. “Presidential emergency action documents have managed to escape democratic oversight for nearly 70 years. Congress should move quickly to remedy that omission and assert its authority to review these documents, before we all learn just how far this administration believes the president’s powers reach.”

It is way past time for Congress to rein in unconstitutional assertions of executive power by exposing and incinerating these secret presidential emergency action documents. Meanwhile President Trump needs to adhere to his Article II oath: “I do solemnly swear (or affirm) that I will faithfully execute the office of President of the United States, and will to the best of my ability, preserve, protect and defend the Constitution of the United States.”

from Latest – Reason.com https://ift.tt/2y7pshO

via IFTTT

Oil & Stocks Tumble Into Red After Big Opening Gains Evaporate

A mixture of good (European daily virus death count growth slowing) and bad (US virus death count growth not slowing) news mixed with an ‘odd’ deal with OPEC+ and G20 debt restructuring chatter has sparked an instant bid in stocks and oil prices but just as quickly those bids are disappearing…

Dow futures were up almost 300 points at the open but have given it all back and turned ugly red already…

Oil opened up over 8% after the OPEC+ deal…

But, as one major brokerage platform wrote to clients today:

Due to potential market volatility, OPEC meetings and the upcoming holiday weekend, Crude Oil (CL & QM) will require 150% of initial margin for today’s trading session.

At 3pm ET, initial margin will increase to 200%.

Any client wishing to hold a position after today’s close must have 200% of the maintenance margin requirement.

Which may help explain why WTI is now trading back below Thursday’s lows…

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}