Thank God for the tech scene. When our established institutions fail in the face of existential threats, at least we have the quick thinking and resourcefulness of America’s computer jockeys to help us muddle through.

People acted like they were crazy. One infamous Recode article chortled at the tech industry’s early and prudent substitution of virus-transmitting handshakes for other less-germy forms of greeting. There go the nutty techies, trying to stem the tide of pestilence! If only more people had followed those California weirdos’ leads. Of course, outlets that had been spreading COVID-19 denialism and shaming preppers in February are now demanding indefinite shutdowns without skipping a beat.

The problem with an exponential trend is that by the time it’s obvious that we should change our behavior, it’s already too late. This is why it was so easy to mock the early adapters to the developing pandemic scenario. But they weren’t insane; they were prescient. Their whole job is to study and get ahead of emerging trends in business and technology. More people should have taken them seriously.

Either way, after being among the first to identify and communicate the problem, the tech community is now forging ahead with targeted COVID-19 responses.

There is no master plan. A global grab-bag of coders, designers, DIYers, tinkerers, makers, and bioengineers have simply decided to turn their talents to where they think they’re most needed. And they’re not asking for permission, either. There’s no time to pretend like our many dumb regulations are worth worrying about right now. The technologically-inclined are just doing what they feel they have to do, whether Uncle Sam likes it or not—although in this case, the feds seem relieved that someone is taking up the slack.

Examples abound. Consider the debacle with the CDC-created tests. Infectious disease experts in the early hotspot of Seattle grew impatient with federal dithering. Rather than waiting for the CDC to get its diagnostic act together, a group of doctors with the Seattle Flu Study developed and started running their own test without CDC approval. Their act of civil disobedience resulted in a major, but tragic, breakthrough in public health surveillance: they learned through their testing that the virus had already been circulating in Seattle for several weeks. Might they have learned earlier and been able to prepare if not for such public incompetence?

The CDC and Food and Drug Administration (FDA) eventually started relaxing testing regulations as the human cost of these blunders became clearer. There’s still room for improvement. Startups like Everylywell, Carbon Health, and Nurx developed tests that people can take at home so they don’t have to risk getting infected at a test site. Awesome! But the FDA said “nein!” and made these startups stop their tests and destroy their samples. Well, maybe there’s a DIY solution: researchers are crowdsourcing an accessible open source test that more people can use on their own.

The maker scene has also been quick to hack together low cost alternatives to badly needed medical supplies. Volunteers in six continents enlist in a public Google doc extolling their talents, locations, and how they’d like to help. A couple in New York is printing face shields for testing clinics. Italian hospitals received cheap new ventilator valves that would otherwise cost $11,000. Teams of tinkerers brainstorm together on low cost ventilator schematics so that more healthcare workers can assemble functioning equipment with whatever supplies they’ve got around them.

Many of these endeavors are on shaky regulatory grounds. Surgical masks, for example, are usually subject to FDA regulation. The modern day Betsey Rosses weaving CAD files for personal protective equipment can follow regulatory best practices, but they’re probably not asking permission first.

The official response to the COVID-19 pandemic has been profoundly disappointing, if not entirely unexpected. But a nation with such a wealth of technical talent should be able to coordinate an early and effective public-private response to existential threats. The U.S. failure to prepare for COVID-19 reveals a deep lack of state capacity.

Imagine how much more effective this outpouring of American inventiveness would have been with a competent state partner from the start. After heeding early analyses of a troubling trend, planners could quickly look to identify what we need and how to get it. Sources of regulatory friction could be pruned at the outset. And public health experts could provide counsel on the trade-offs between experimentation and safety, providing some ground rules for the rapid innovation that would come.

It’s too late for that now. Thankfully, after unfortunate weeks of dithering, the U.S. establishment has finally started leveraging our strategic corporate and technological resources to better address the COVID-19 pandemic. Some official organs are still spreading misinformation about the effectiveness of mass mask-wearing, but it’s a start.

This kind of primal national crisis is precisely when official institutions should shine. It is revealing that our odds of success have hinged mostly on an ad hoc collective of virushackers being able to ignore or override the institutions founded explicitly for this kind of crisis. For now, they work together to tamp down an invisible enemy. But once that is vanquished, many will have lost even more faith in the establishment. When such an appealing alternative presents itself, why bother with the outdated, overpriced, and ineffective model?

from Latest – Reason.com https://ift.tt/342Wwnc

via IFTTT

EU Leaders Aghast As Hungary’s Orban Given Sweeping ‘Emergency Powers’ To Fight Coronavirus

A coronavirus political bombshell went off in the heart of Europe, grabbing world headlines early this week, after Hungary’s parliament voted to allow Prime Minister Viktor Orban sweeping emergency powers deemed necessary to fighting the pandemic.

The bill approved by the nationalist government givens Orban the right to rule by decree, without having to consult lawmakers or other branches of government. It overwhelmingly passed 138 votes in favor with 53 against — easily pastthe required two-thirds majority.

It predictably evoked immediate backlash from leaders across Europe and the West, given he’s already long been under scrutiny for allegedly weakening Hungary’s judicial and parliamentary systems in what critics have long complained is a bid for greater ‘authoritarian’ control. From the start, it should be remembered, he was loathed by EU technocrats for rejecting the so-called open door response to migrants and refugees in 2015.

Hungarian Prime Minister Viktor Orban, MTI via AP/FOX

The new emergency powers legislation is now in effect as of Tuesday. Crucially, Orban alone has the ability to decide when the emergency powers end. The prime minister sought to assure parliament and the public during Monday’s vote: “When this emergency ends, we will give back all powers, without exception.”

He said the unprecedented legislation was necessary as “Changing our lives is now unavoidable,” according to prior statements. “Everyone has to leave their comfort zone. This law gives the government the power and means to defend Hungary.”

Though Hungary has significantly fewer cases than most other European states at over 440, including 15 deaths, it reportedly has lagged behind in testing, with fears its health care system is too weak to handle a serious outbreak.

Critics of Orban and his Fidesz party, though hugely popular within the country, have slammed the new emergency powers’ legislation as an egregious betrayal of free speech among citizens, given authorities can hand out up to five year prison sentences for “spreading false information”.

The suspension of parliament, punishments for journalists if the government believes their coronavirus reporting is not accurate, and heavier penalties for violating quarantine regulations are all made possible by the order. No elections or referendums can be held while it is in place.

The law says specifically that “a person who, during the period of a special legal order and in front of a large audience, states or disseminates any untrue fact or any misrepresented true fact that is capable of hindering or preventing the efficiency of protection is guilty of a felony and shall be punished by imprisonment for one to five years.”

Orban shot back, however, telling critics in a national radio broadcast this week: “We cannot react quickly if there are debates and lengthy legislative and lawmaking procedures. And in times of crisis and epidemic, the ability to respond rapidly can save lives.”

“The Government is not asking for anything extraordinary,” he added. “It is asking for the ability to rapidly enact certain measures. We don’t want to enact measures that the Government has no general right to enact —we simply want to do so swiftly.”

Despite other European countries in some cases enacting similar drastic and draconian coronavirus measures involving the curtailing of individual rights and movement, EU officials and pundits dramatically declared it essentially the ‘death of democracy’ in central Europe.

Fed Launches Repo Facility To Provide Dollars To Foreign Central Bank

With US dealers no longer using the Fed’s repo facilities (this morning we had another “no bid” overnight repo with just $250MM in MBS submitted for a $500 billion op) as the Fed soaks up all securities via its aggressive QE which is still buying $75BN in paper each day, perhaps Powell felt a bit unloved and at 830am this morning the Fed unveiled yet another “temporary” emergency liquidity providing facility, this time to foreign central banks, in the form of a repo facility targeting “foreign and international monetary authorities”, i.e. foreign central banks which will be allowed to exchange Treasuries held in custody at the Fed for US dollars.

In other words, just a week after the Fed “enhanced” its swap lines with central banks and included a bunch of non G-5 central banks to the list of counterparties, it has found that this is not working – perhaps due to the prohibitive rates on the facility – and is now handing out dollars outright against US denominated securities. We wonder if the central bank uptake will be any higher than the repo facility aimed at US dealers and which is now redundant. Of course, when that fails the Fed can just offer to buy all central bank securities in what even reputable FX strategists now joke is a Fed on full tilt, and intent on buying out all foreign central banks.

And so, just as the financial situation was starting to stabilize, the Fed reminds everyone just how broken everything still is.

Fed launches ANOTHER temporary facility to provide $USD liquidity to foreign central banks (this time foreign central bank holdings of US Treasury’s can be exchanged for dollars).

At this rate, Fed is on course to buy out foreign central banks… and call it an M&A facility pic.twitter.com/iAXRCVoZS9

Federal Reserve announces establishment of a temporary FIMA Repo Facility to help support the smooth functioning of financial markets

The Federal Reserve on Tuesday announced the establishment of a temporary repurchase agreement facility for foreign and international monetary authorities (FIMA Repo Facility) to help support the smooth functioning of financial markets, including the U.S. Treasury market, and thus maintain the supply of credit to U.S. households and businesses. The FIMA Repo Facility will allow FIMA account holders, which consist of central banks and other international monetary authorities with accounts at the Federal Reserve Bank of New York, to enter into repurchase agreements with the Federal Reserve. In these transactions, FIMA account holders temporarily exchange their U.S. Treasury securities held with the Federal Reserve for U.S. dollars, which can then be made available to institutions in their jurisdictions. This facility should help support the smooth functioning of the U.S. Treasury market by providing an alternative temporary source of U.S. dollars other than sales of securities in the open market. It should also serve, along with the U.S. dollar liquidity swap lines the Federal Reserve has established with other central banks, to help ease strains in global U.S. dollar funding markets.

The Federal Reserve provides U.S. dollar-denominated banking services to FIMA account holders in support of Federal Reserve objectives and in recognition of the U.S. dollar’s predominant role as an international currency. The FIMA Repo Facility, which adds to the range of services the Federal Reserve provides, will be available beginning April 6 and will continue for at least 6 months.

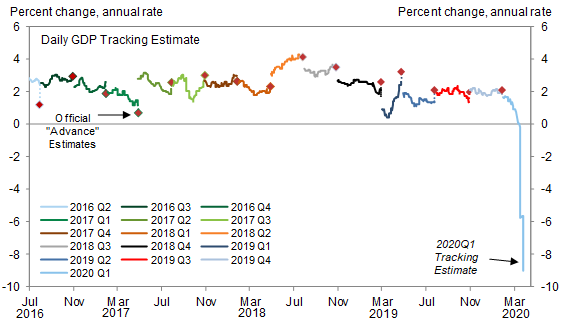

“The Biggest Decline Ever”: Goldman Now Sees US GDP Crashing 34% In Q2

Just over a week ago, when we reported on the ongoing feud between Goldman and JPM to come up with the most terrifying GDP forecast for the US, and when we asked if a Second Great Depression has begun after Goldman’s chief economist Jan Hatzius slashed his Q2 GDP forecast from -5% to -24%, we said “we expect Goldman to take the machete to this analysis as well in the coming days, because if the US economy is indeed paralyzed for at least one quarter, then all of GDP could be lost.”

We were right, because early on Monday morning Goldman’s Haztius did just that, and in a report titled “The Sudden Stop: A Deeper Trough, A Bigger Rebound”, he writes that he is “making further significant adjustments to our GDP and employment estimates. We now forecast real GDP growth of -9% in Q1 and -34% in Q2 in qoq annualized terms (vs. -6% and -24% previously) and see the unemployment rate rising to 15% by midyear (vs. 9% previously).”

Yes, the Q1 GDP drop is stunning…

… but it is the Q2 collapse which wipes out more than a third of the US economy that is truly jawdropping because as Hatzius admits, “it would represent a decline that is more than three times larger than the previous low in the history of the modern US GDP statistics.”

Detailing the assumptions behind his latest revision, Hatzius explains that he has increased his estimates of the peak hit to services consumption, manufacturing activity, and construction, “in light of new evidence on the severity of the hit across the different sectors” and now expects the level of GDP in April to be 13% below the January/February trend, as shown in Exhibit 1. “We assume that this drag then fades gradually by 10% each month in the services industry and by 12.5% in the manufacturing and construction industries.”

Behind the core of the drop Goldman sees a 19% annualized drag from services consumption on Q2 growth, on top of a 3pp drag on Q1 growth. as shown in the next chart.

Ok but why do the reputable epidemiologists at Goldman believe the pandemic will fade in coming weeks? Here’s why (and yes, warm weather makes an appearance):

While the exact timing of the medical and economic recovery is highly uncertain and relapses are plausible, our assumption is that stronger lockdown and social distancing measures and perhaps some weather effects reduce new infections sharply over the next month. Combined with potential medical breakthroughs or adaptation by firms and consumers, this slowdown in new infections is likely to lead to a gradual economic recovery. The slow pace of recovery in our forecast even in 2021 allows for longer-lasting scarring effects on businesses and workers

And at the risk of repeating ourselves too, we will say that within a week, Goldman will cut its forecast again this time to -50% as we approach the moment when even banks admit the entire US economy has ground to a halt.

In any case, as Goldman explains further, its latest apocalyptic forecast reflects the net effect of two directionally offsetting changes:

On the one hand, the anecdotal evidence and the sky-high jobless claims numbers show an even bigger output and (especially) labor market collapse than it had anticipated. This not only means deeper negatives in the very near term but also raises the specter of more adverse second-round effects on income and spending a bit further down the road.

On the other hand, both monetary and fiscal policy are easing dramatically further, which will tend to contain these second-round effects and add to growth down the road. The Phase 3 fiscal package was much bigger than we had expected, we now anticipate a Phase 4 package focused on state fiscal aid, and the Fed is likely to use the $454bn addition to the Treasury’s Exchange Stabilization Fund aggressively to sustain the flow of credit to private-sector and municipal borrowers.

The chart below translates the monthly path of the level of GDP shown in Exhibit 1 into a quarterly path of GDP growth, adding the impact of what Goldman believes will be second round effects and the fiscal impulse. For the first half of 2020, the bank now look for real GDP growth of -9% in Q1 and -34% in Q2, versus -6.3% and -24% previously. As Hatzius admits, the “Q2 forecast would represent a decline that is more than three times larger than the previous low in the history of the modern US GDP statistics (-10% in 1958 Q1).” Subsequently, the bank’s assumptions about the gradual fading of the virus drag imply a growth pace of just over 15% in the second half of 2020. In conclusion, Goldman’s forecast of full-year 2020 growth is now -6.2% on an annual average basis and -5.4% on a Q4/Q4 basis.

In other words, to preserve its traditional cheerful aura – even as it now forecasts a depression in the second quarter, Goldman has offset its future forecast with an even more vicious V-shaped recovery, and has upgraded its expectations for the recovery after midyear, now expecting a hilarious 19% annualized GDP gain in Q3 (vs. 12% previously), with the bank’s estimates implying that a bit more than half of the near-term output decline is made up by year-end and that real GDP falls 6.2% in 2020 on an annual-average basis (vs. 3.7% in our previous forecast).

Good luck with that.

Finally, turning away from GDP, Goldman’s unemployment outlook is just as dire, admitting that the surge in layoffs has “already outpaced our expectations.” Jobless claims rose about twelve-fold over the week of March 15-21 to 3.28mn, nearly five times the previous historical high for a single week, with Goldman noting that jobless claims are likely to rise further during the week of March 22-28.

Press reports citing state officials indicate that claims rose dramatically from March 15-21 to 22-28 in California and Texas. Our analysis of anecdotal press reports for the 15 most populated states suggests a significant increase in total claims during March 22-28, in part because many states experienced application bottlenecks in the first week and in part because stay-at-home orders likely had a greater effect in the second week.

As a result, Goldman now estimates that the level of jobless claims rose by more than 2mn to about 5.5mn during March 22-28. A less conservative extrapolation of the estimated ratio of week 2 to week 1 claims in these states would imply an even higher national total. It then expects even higher numbers in the coming weeks:

We expect claims to remain very elevated—likely over 2mn—for at least another week (March 29-April 4) and somewhat elevated after that. Widespread reports of application bottlenecks suggest that many laid off workers have yet to file. Some employers, especially in the retail sector, are taking a staggered approach to layoffs. And many business owners and workers are just beginning to learn about the more generous unemployment insurance benefits—which will exceed normal wages for many workers—and the expansion of coverage included in the Phase 3 legislation. In total, we expect over 11mn claims to be filed in the first three weeks of the coronacrisis and at least a couple million more in the rest of April.

What do soaring claims mean for the unemployment rate?In short, Goldman now sproject a nearly 12% increase in the unemployment rate to a peak rate of 15%.

Finally, just like JPM, Goldman admits it really has neither the visibility nor the proper models to predict what happens next as the US economy slides into a depression:

Using the labor market data in this fashion requires an estimate of “Okun’s law”, the relationship between the change in the unemployment rate and the change in real GDP (relative to trend). Normally, the coefficient for Okun’s law is thought to be about 2, meaning that a 1pp rise in the unemployment corresponds to a 2% hit to real GDP. During this crisis, however, a more appropriate Okun’s law coefficient is likely to be closer to 1.

Our current estimate of a roughly 12pp increase in the unemployment rate implies a roughly 12% peak decline in the level of GDP, which is broadly consistent with the estimates in Exhibits 1 and 2. Going forward, we plan to use this relationship and its industry-level counterparts aggressively to keep our GDP estimates up to date in coming months as more timely labor market data become available. This could well imply further substantial revisions to our real GDP estimates—in either direction—as the scale of the labor market downturn comes into fuller view in coming weeks and months.

This means that as we enter the cruelest month in the history of the US economy, when GDP may plunge double digits in April alone, brace for even more cuts from Goldman which will forecast a -50% GDP print before it’s all said and done.

Rally Fizzles, Futures Slide As Dollar Surge Returns

The torrid quarter-end rally which many attributed to a flood of forced pension fund buying as part of aggressive rebalancing, reversed overnight as US index futures reversed all overnight gains even as European stocks headed for a fifth increase in six sessions amid ongoing debate whether the market meltdown has ended despite the accelerating spread of the coronavirus (spoiler alert: no), while treasury yields dipped below 0.7% while the disconcerting dollar rally is back front and center.

S&P 500 futures rose as high as 2,640 before sliding back under 2,600 as politicians were said to contemplate a fourth round of stimulus, but they struggled to stay in the green as speculation the pension fund bid had faded. Oil producers Exxon Mobil Corp. and Occidental Petroleum Corp. jumped in the premarket thanks to a rebound in oil prices from 18-year lows after the United States and Russia agreed to discuss stabilizing energy markets.

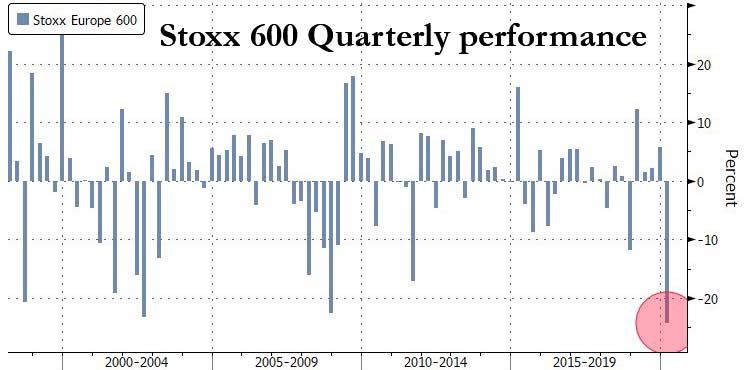

In Europe, energy shares led gains in the Stoxx 600 Index after the World Health Organization said signs emerged of some stabilization in the region’s outbreak. A measure of European corporate-credit stress eased further. Even with today’s modest rebound Europe is still set for its worst quarter on record.

The US was no better, and despite the recent rally the slump from the mid February record highs has set the Dow Jones .on course for its worst first quarter ever, while the S&P 500 is on track for its worst since 1938.

Earlier in the session, Asian stocks were little changed, with energy rising and industrials falling despite China reported ridiculously strong manufacturing data, which saw the mfg PMI surge to three year highs, in what was a clear political message from Beijing that China’s economy had a V-shaped recovery and had put the coronavirus concerns behind it.

China’s official manufacturing purchasing managers’ index (PMI) bounced to 52.0 in March, up from a record-low 35.7 in February, but analysts cautioned that a durable near-term recovery is far from assured as the global coronavirus crisis knocks foreign demand.

As Bloomberg notes, signs of a recovery across equities worldwide have arrived at the end of their worst quarter since 2008, which has put investors in a quandary, questioning whether some $12 trillion in extraordinary monetary and fiscal stimulus by countries and central banks can counter further the global economy grinding to a halt as the outbreak spreads. New York City, which is emerging as the new epicenter of the pandemic, reported a 16% increase in deaths in six hours. Italy and the Netherlands are considering extending lockdowns, and Spain’s 849 deaths were the most in one day for the country.

“We just don’t know how long the lockdown or stasis of the world economy is going to be,” said Toby Lawson, head of global markets at Societe Generale Securities Australia, told Bloomberg TV. “It would be very premature to say that we’ve seen the bottom.”

In FX, the dollar rose at least 1% versus the euro and three other major peers. The yen sank as the end of Japan’s fiscal year brought positioning adjustments after suffering a mini flash crash at the Tokyo fixing. Japan’s ruling party proposed the country’s biggest-ever stimulus package worth 60 trillion yen ($554 billion). EUR/USD fell under 1.10 as the dollar extended gains for a second day, supported by month- and quarter-end flows; the Bloomberg Dollar Spot Index was set for its best quarter since 2016.

Elsewhere, Norway’s krone was the best performing currency of the day among Group-of-10 peers as oil prices rebound; the currency was still set for its worst quarter since 1992 against the greenback on the back of the worst quarter on record for oil. Yen declined on dollar demand from Japanese investors to re-balance their portfolios on the final day of the fiscal year. The Australian and New Zealand dollars gained with commodities after Chinese manufacturing activity rebounded strongly in March, boosting risk sentiment. The pound slumped and headed for its worst quarter since the 2016 Brexit referendum

Gilts fell after the U.K. Debt Management Office announced it will more than double its issuance to sell 45 billion pounds ($55 billion) of bonds in April, with four auctions being conducted per week. US Treasurys gained across the curve.

Expected data include Conference Board Consumer Confidence. Conagra, McCormick, and Blackberry are reporting earnings.

Market Snapshot

S&P 500 futures up 0.9% to 2,633.75

STOXX Europe 600 up 1.9% to 320.86

MXAP down 0.06% to 136.58

MXAPJ up 1.4% to 435.89

Nikkei down 0.9% to 18,917.01

Topix down 2.3% to 1,403.04

Hang Seng Index up 1.9% to 23,603.48

Shanghai Composite up 0.1% to 2,750.30

Sensex up 4% to 29,577.93

Australia S&P/ASX 200 down 2% to 5,076.83

Kospi up 2.2% to 1,754.64

German 10Y yield rose 1.3 bps to -0.477%

Euro down 0.5% to $1.0998

Italian 10Y yield rose 15.0 bps to 1.307%

Spanish 10Y yield fell 1.4 bps to 0.592%

Brent futures up 3% to $23.44/bbl

Gold spot down 0.9% to $1,607.97

U.S. Dollar Index up 0.3% to 99.45

Top Overnight News

Italy is discussing an extension of lockdown measures into May as European countries fight to contain the spread of the coronavirus, even as the outbreak shows signs of slowing

German unemployment rose by just 1,000 in March, significantly less than economists predicted, before far-reaching restrictions on business and movement sparked thousands of furloughs in Europe’s largest labor market

Stress is easing in dollar funding with key U.S. channels tentatively following overseas counterparts. The three-month dollar Libor fixing fell for the first time in over two weeks on Monday, while commercial paper rates — the yield on short-term notes issued by companies — also retreated

The worst quarter for credit markets since at least the global financial crisis is ending with some signs of improvement. Spreads on credit-default swaps and dollar bonds in Asia dropped Tuesday

Japan’s ruling party proposed the country’s biggest-ever stimulus package worth 60 trillion yen ($554 billion) as the spreading coronavirus locks the economy in a recession

A surge in hedging costs for Japanese investors has wiped out the attraction of a popular trade — French bonds. Yen investors had to pay as much as 0.7% to hedge their euro exposure for three months last week, surging from just above 0.2% last month, a Bloomberg gauge showed

Asia equity markets were mostly higher (before trimming some gains) as the region took its cue from the gains on Wall St following recent global stimulus efforts and with sentiment also underpinned by an improvement in the latest Chinese PMI figures. ASX 200 (-2%) and Nikkei 225 (-0.9%) were lifted from the open with early outperformance in Australia led by the largest weighted financials sector and with sentiment also boosted after yesterday’s record AUD 130bln stimulus announcement, while Japanese exporters initially benefitted from a weaker currency, although both indices then gave up the gains amid Q1-end rebalancing and amid some doubts regarding the Chinese data. Hang Seng (+1.3%) and Shanghai Comp. (+0.1%) conformed to the early constructive tone following encouraging Chinese PMI data in which headline Manufacturing and Non-Manufacturing PMI topped estimates and the Composite PMI also printed in expansion territory. However, gains in the mainland were somewhat limited as some downplayed the data given that it was a recovery from the prior month’s record low base and with China’s stats bureau warning the rebound does not mean the economy has returned to normal and that this month’s data alone cannot determine an improving trend. Finally, 10yr JGBs were pressured in a continuation of the pullback from the 153.00 level, with demand subdued by the early upbeat tone in risky assets and following weaker results at the 2yr JGB auction.

Top Asian News

Japan Plans Record 60 Trillion Yen Stimulus as Virus Spreads

Yunda Jumps After Report Alibaba Plans to Buy at Least 10% Stake

China Factory Rebound Hints Worst Is Over as Stimulus Lies Ahead

Hong Kong Retail Sales Plunge Record 44% in February on Virus

European equities trade on a firmer footing once again (Eurostoxx 50 +0.3%) as sentiment remains upbeat alongside quarter-end rebalancing flows and post-Chinese PMI metrics, albeit stocks have drifted off highs. On the data front, price garnered some support from the last survey data out of China in which headline Manufacturing and Non-Manufacturing PMI topped estimates and the Composite PMI also printed in expansion territory. However, it is worth noting that some desks have downplayed the data given that it was a recovery from the prior month’s record low base and with China’s stats bureau warning the rebound does not mean the economy has returned to normal and that this month’s data alone cannot determine an improving trend. In terms of sector specifics, energy names sit near the top of the pile in a bounce-back from some of the declines yesterday with WTI now back above USD 21/bbl and Shell (+4.0%) shares shrugging off expectations of a USD 400-800mln Q1 impairment charge and weak refining margins. Elsewhere, travel and leisure names have also seen support during today’s session as hopes continue to be pinned on government support measures, albeit, from a UK standpoint, Times’ Swinford noted comments from Transport Secretary Shapps that the “UK government is attempting to find the right solution for airlines”, something which Swinford inferred as meaning that it “doesn’t sound like a big bailout is coming”. The main theme in the pre-market was largely centered around the suspension of buybacks and dividends (details of which can be found in the European equity opening news) with particular focus on the UK banking sector with the latest reports via Sky News suggesting that the Prudential Regulation Authority will, on Tuesday or Wednesday, state that Barclays, HSBC, Lloyds and RBS will not be paying dividends as part of FY results. Notable individual movers include Imperial Brands (+12.4%) after signing a new revolving credit facility of EUR 3.5bln and noting no material impact on group performance, Bayer (+2.0%) has reached a settlement with US plaintiffs and WPP (+6.9%) are firmer despite suspending its buyback, dividend and outlook, whilst noting that it maintains a strong balance sheet.

Top European News

Euro-Area Inflation Slows More Than Forecast on Oil Slump

Nightmare Haunting Euro’s Founders May Now Be Reality With Italy

Smiths Delays Ventilator Unit Spinoff as Virus Roils Markets

Strong Start to Pandemic QE Raises Hopes of Credit Turnaround

In FX, the Buck has extended gains vs major counterparts, albeit to varying degrees as a sharp rebound in Chinese PMIs, some consolidation in crude and remaining asset rebalancing flows for the final trading session of March, Q1 and the current financial year help some rival currencies to resist the Greenback’s advances. However, the DXY looks more assured around 99.500 and certainly back on the 99.000 handle within a 99.694-99.100 range, and could continue its recovery towards resistance at 99.915 (prior 2020 high before the psychological 100.000 mark was breached precisely one month later on March 20 when the index hit 102.999).

NOK – The G10 outlier and outperformer, partly due to the aforementioned bounce in oil prices, but mainly as the Norges Bank plans to jack up foreign currency sales against the Norwegian Krona to the equivalent of Nok2 bn per day in April from Nok1.6 bn this month and only a quarter of the new daily total in February. Eur/Nok is hovering just above 11.5100, but has been under 11.5000 in contrast to Eur/Sek flat-lining between 11.1040-0610 parameters.

CAD/AUD/NZD/GBP/EUR/JPY/CHF – Firmer or more stable crude is also providing the Loonie with some underlying support around 1.4200 vs its US peer, while the Aussie and Kiwi are both holding off overnight pre-Chinese PMI flash crash lows of 0.6080 and 0.5948, though down from best levels reached (0.6200+ and 0.6037 respectively) when the headline prints exceeded consensus and regained 50+ growth rather than deep contraction levels. Elsewhere, the Pound has lost its grasp of 1.2400, but faring better against the Euro circa 0.8900 as the single currency retreats through 1.1000 vs the Buck on soft Eurozone inflation and the ongoing nCoV spread in Spain. Note, hefty Eur/Usd option expiries do not seem likely to impact at this stage, but for the record there are several ranging from 1 to 1.6 bn rolling off from 1.1000 to the 1.1100 strike and beyond. Meanwhile, the Yen and Franc are towards the bottom of 108.70-107.75 and 0.9649-0.9581 bands and hindered by safe-haven outflows, with the latter not deriving any support from considerably firmer than forecast Swiss retail sales.

EM – Some respite for the Rouble after a call between US President Trump and his Russian counterpart Putin aimed at stopping the dispute with Saudi Arabia over the price of oil and market share, but little joy for the Lira even though the CBRT has rolled out more liquidity provisions for Turkish banks.

In commodities, WTI and Brent front-month futures experience consolidation from the prior session’s hefty losses, in which prices tumbled to their lowest points in almost 20 years. The former outperforms on the prospect of potential US-Russia cooperation in the energy markets to stem the rotting prices. US President Trump conducted a phone call with his Russian counterpart yesterday with Kremlin noting that this was at the request of the US. The leaders agreed on the need for stability in the energy markets, albeit no further details were released. WTI front-month contracts have reclaimed USD 21/bbl to the upside having yesterday printed a base at around USD 19.30/bbl, whilst Brent touched a multi-year low at ~ USD 21.60/bbl, with prices now nearer to USD 23.50/bbl. Elsewhere, spot gold trades subdued amid a firmer USD and with portfolio rebalancing also in the fray. The yellow metal hovers just above the 1600/oz mark having hit an overnight peak at USD 1626/oz. Meanwhile, copper prices remain supported by the strong China NBS manufacturing PMIs which rose back into expansionary territory from last month’s detrimental print. Copper gains a firmer footing above USD 2/lb ahead of resistance at 2.5/lb from a technical standpoint.

US Event Calendar

9am: Case Shiller 20-City MoM SA, est. 0.4%, prior 0.43%

9am: Case Shiller 20-City YoY NSA, est. 3.23%, prior 2.85%

We’re straight to Asia this morning where the main story is the significant bounce back in China’s PMIs. The manufacturing PMI jumped to 52.0 for March which is relative to 44.8 expected and 35.7 last month, and is also the strongest print since September 2017. Meanwhile the services PMI printed at 52.3 versus 42.0 expected and 29.6 last month. That left the composite reading at 53.0 versus 28.9 in February. A sub-index of new manufacturing export orders also rose to 46.4 in March, up from 28.7 last month.

Despite the huge jump, the accompanying statement from the NBS said that “while manufacturing PMI rebounded rapidly in March, the survey showed companies still face relatively big operational pressures,” and added that more firms are reporting funding shortages and falling demand than in February. The statement also said that “the global virus spread will hit the world economy and trade seriously and bring new, severe challenges to the Chinese economy.” So the tone still remains understandably cautious but nonetheless the data does provide sliver of hope for expectations of a ‘V or U’ shaped recovery for markets in the aftermath of coronavirus induced lockdowns.

Chinese markets have posted small gains following the data with the Shanghai Comp and CSI 300 up +0.42% and +0.56%, while the Hang Seng has gained +1.09%. Elsewhere, it’s more mixed. The Kospi has risen +1.77% however the Nikkei (-0.48%) and ASX (-1.53%) are both down.

In other overnight news, Bloomberg has reported that the White House and congressional Democrats are preparing for a fourth round of economic stimulus to get the US through its coronavirus outbreak. The report added that the White House has already compiled lists of requests from government agencies totalling roughly $600bn towards this and the proposals include more state aid as well as financial assistance for mortgage markets and the travel industries. Futures on the S&P 500 are little changed.

Following on from this the main story in financial markets yesterday was the astonishing fall in oil prices – albeit one which has reversed this morning – where the combination of an impending global recession and the Saudi-Russia price war saw yet further declines. By the end of the session yesterday, WTI was down by -6.60% to just $20.09/barrel, which is its lowest level since 2002, and the 8th time this month alone that WTI has declined by more than 5% in a single day. With just one day left in the month to go, the price of WTI crude has now more than halved since the end of February (-54.69%), making this month for WTI even worse than the falls in October 2008 (-32.62%) and the biggest monthly decline in data going back to March 1983. Remember that in the first week of the year WTI hit $65.65 intra day after the US/Iranian military strike and escalation, so it’s down -69.11% since that peak.

The movements in the oil market have attracted the attention of global leaders, with President Trump telling Fox News yesterday that he planned to talk with Russian President Putin about oil, also saying that “I never thought I’d be saying that maybe we have to have an oil increase, because we do. The price is so low”.

Over in global equity markets it was a generally positive picture after Friday’s declines, with the S&P advancing +3.35%. The move continues the S&P’s run of having moved by at least 1% in either direction in 20 out of 21 sessions so far this month. In a further sign that some semblance of stability could be returning, the VIX index of volatility fell by -8.5pts yesterday to 57.08pts, which is its lowest level in over two weeks. In Europe, equities pared back losses to close higher, with the STOXX 600 recovering from an intraday low of -2.42% shortly after the open to close up +1.28%. Banks dragged on the index however, with the STOXX Banks index falling a further -5.69% yesterday as lower core rates in Europe have started to become a trend again.

Having said that 10yr Treasury yields were up +5.2bps yesterday to 0.73%, as large equity moves and general optimism saw long end rates rise, even as the short end yields went lower. In Europe, for a second session running there was a notable widening in peripheral spreads. The spread of Italian 10yr yields over bunds was up +16.7bps, bringing its 2-day rise to 37.8bps, while the spread of Spanish (+8.2bps), Portuguese (+8.7bps) and Greek (+6.3bps) yields over bunds also widened yesterday. Italian bonds may have been impacted by continuing concern at there not being any outline of assistance for the country at last week’s meeting of EU leaders and also Conte’s words over the weekend that anti-EU sentiment could increase in the country. Staying with fixed income, credit spreads broadly tightened in the US, with HY cash spreads -17bps tighter and IG tightening -9bps, while EUR spreads widened 11bps and IG widened 1bp.

It was a strong day for the US dollar yesterday, with the Bloomberg dollar index snapping a run of 4 successive declines to strengthen by +0.71%. However, the oil-producing currencies suffered, with both the Canadian dollar (-1.28% against USD) and the Norwegian Krone (-0.57%) struggling yesterday against other major currencies.

Before we look at yesterday’s data with all of the uncertainty around making point forecasts in this environment, Justin Weidner on our US Economics team has built a simple model based on only five parameters (e.g., the length of containment measures, initial decline in output, etc.) to trace out the potential impact of the Covid-19 on US GDP growth over the next two years. Here’s the link to the model: DB US Eco Covid-19 GDP model . The team describes the model in a report out yesterday (see Tracing the economic fallout ) and also detail simulations. They find that the median path has growth falling 37% in Q2 on an annualized basis and -1.1% in 2020 (Q4/Q4). The interquartile range has outcomes ranging from -22% to -51% for Q2 annualized growth and from -4.4% to +0.5% for 2020 Q4/Q4 growth. Their own forecast (-33% in Q2 and -3.2% for 2020) fits well within these ranges.

Now to those economic data releases, the European Commission’s monthly economic sentiment indicator for the Euro Area fell by -8.2 points in March from 103.4 to 94.5. This is the largest monthly decline since records began in 1985. However, the survey responses were collected between 26 February-23rd March, and for many countries the vast majority of responses were collected before lockdown measures began, so further deterioration is still likely ahead of us. Over in the US meanwhile, the Dallas Fed manufacturing outlook survey saw the general business activity index fall to -70.0 in March, well below the -10.0 reading expected and the lowest level since the survey began in June 2004. Finally, we got the German inflation reading for March, where the preliminary estimate of HICP came in at 1.3%, down from February’s 1.7%.

To the day ahead now, and data releases include the flash estimate of Euro Area CPI for March, as well as the preliminary readings for France and Italy. Meanwhile we’ll get the change in German unemployment for March, along with the final reading of Q4 GDP in the UK and January’s GDP in Canada. Finally in the US, we’ll get the Conference Board’s consumer confidence indicator for March, along with the MNI Chicago PMI and the S&P/Case-Shiller US National Home Price Index

Believe it or not, we’re still in the month of March. On March 1, New York City recorded its first positive case for the novel coronavirus. On March 2, Mayor Bill de Blasio—with future “Love Gov” Andrew Cuomo at his side—said “We have the capacity to keep this contained.” On March 10, de Blasio told MSNBC, with reckless inaccuracy, that “If you’re under 50 and you’re healthy, which is most New Yorkers, there’s very little threat here. This disease, even if you were to get it, basically acts like a common cold or flu. And transmission is not that easy.” By March 15, with great reluctance, Hizzoner finally joined the rest of big-city America in closing public schools. On March 16, he worked out at the Park Slope YMCA.

Now near the end of the month, New York City is the American epicenter of the deadly virus, with more than 36,000 positive tests and 750 deaths, and de Blasio has gone from reluctant institutions-shutterer to someone who has threatened churches and synagogues with “potentially closing the building permanently” if they don’t keep their doors closed during the upcoming holidays.

Plague-life comes at you fast, exposing some of the worst pathologies of governance and politics. An examination of such begins today’s Reason Roundtable podcast, featuring Nick Gillespie, Katherine Mangu-Ward, Peter Suderman, and Matt Welch. We discuss the catastrophe of slow testing, the mixed messaging on masks, the gargantuan bailout/stimulus package, and—of course!—what to watch and listen to during the long days of quarantine.

Thank God for the tech scene. When our established institutions fail in the face of existential threats, at least we have the quick thinking and resourcefulness of America’s computer jockeys to help us muddle through.

People acted like they were crazy. One infamous Recode article chortled at the tech industry’s early and prudent substitution of virus-transmitting handshakes for other less-germy forms of greeting. There go the nutty techies, trying to stem the tide of pestilence! If only more people had followed those California weirdos’ leads. Of course, outlets that had been spreading COVID-19 denialism and shaming preppers in February are now demanding indefinite shutdowns without skipping a beat.

The problem with an exponential trend is that by the time it’s obvious that we should change our behavior, it’s already too late. This is why it was so easy to mock the early adapters to the developing pandemic scenario. But they weren’t insane; they were prescient. Their whole job is to study and get ahead of emerging trends in business and technology. More people should have taken them seriously.

Either way, after being among the first to identify and communicate the problem, the tech community is now forging ahead with targeted COVID-19 responses.

There is no master plan. A global grab-bag of coders, designers, DIYers, tinkerers, makers, and bioengineers have simply decided to turn their talents to where they think they’re most needed. And they’re not asking for permission, either. There’s no time to pretend like our many dumb regulations are worth worrying about right now. The technologically-inclined are just doing what they feel they have to do, whether Uncle Sam likes it or not—although in this case, the feds seem relieved that someone is taking up the slack.

Examples abound. Consider the debacle with the CDC-created tests. Infectious disease experts in the early hotspot of Seattle grew impatient with federal dithering. Rather than waiting for the CDC to get its diagnostic act together, a group of doctors with the Seattle Flu Study developed and started running their own test without CDC approval. Their act of civil disobedience resulted in a major, but tragic, breakthrough in public health surveillance: they learned through their testing that the virus had already been circulating in Seattle for several weeks. Might they have learned earlier and been able to prepare if not for such public incompetence?

The CDC and Food and Drug Administration (FDA) eventually started relaxing testing regulations as the human cost of these blunders became clearer. There’s still room for improvement. Startups like Everylywell, Carbon Health, and Nurx developed tests that people can take at home so they don’t have to risk getting infected at a test site. Awesome! But the FDA said “nein!” and made these startups stop their tests and destroy their samples. Well, maybe there’s a DIY solution: researchers are crowdsourcing an accessible open source test that more people can use on their own.

The maker scene has also been quick to hack together low cost alternatives to badly needed medical supplies. Volunteers in six continents enlist in a public Google doc extolling their talents, locations, and how they’d like to help. A couple in New York is printing face shields for testing clinics. Italian hospitals received cheap new ventilator valves that would otherwise cost $11,000. Teams of tinkerers brainstorm together on low cost ventilator schematics so that more healthcare workers can assemble functioning equipment with whatever supplies they’ve got around them.

Many of these endeavors are on shaky regulatory grounds. Surgical masks, for example, are usually subject to FDA regulation. The modern day Betsey Rosses weaving CAD files for personal protective equipment can follow regulatory best practices, but they’re probably not asking permission first.

The official response to the COVID-19 pandemic has been profoundly disappointing, if not entirely unexpected. But a nation with such a wealth of technical talent should be able to coordinate an early and effective public-private response to existential threats. The U.S. failure to prepare for COVID-19 reveals a deep lack of state capacity.

Imagine how much more effective this outpouring of American inventiveness would have been with a competent state partner from the start. After heeding early analyses of a troubling trend, planners could quickly look to identify what we need and how to get it. Sources of regulatory friction could be pruned at the outset. And public health experts could provide counsel on the trade-offs between experimentation and safety, providing some ground rules for the rapid innovation that would come.

It’s too late for that now. Thankfully, after unfortunate weeks of dithering, the U.S. establishment has finally started leveraging our strategic corporate and technological resources to better address the COVID-19 pandemic. Some official organs are still spreading misinformation about the effectiveness of mass mask-wearing, but it’s a start.

This kind of primal national crisis is precisely when official institutions should shine. It is revealing that our odds of success have hinged mostly on an ad hoc collective of virushackers being able to ignore or override the institutions founded explicitly for this kind of crisis. For now, they work together to tamp down an invisible enemy. But once that is vanquished, many will have lost even more faith in the establishment. When such an appealing alternative presents itself, why bother with the outdated, overpriced, and ineffective model?

from Latest – Reason.com https://ift.tt/342Wwnc

via IFTTT

We would like to propose a challenge: tweet about each of the 100 cases in the library. We call it the #100Cases challenge. If you complete the challenge, please email me, and I will send you an autographed bookplate. The videos will be freely available till May 31, so there is no cost to play along.

Phil Miles, my law school classmate, took the challenge between October 2019 and February 2020. He tweeted about one case a day, with some short observations. It was a very impressive effort. Here are some of his tweets.

Day 1: #SCOTUS100 Chisolm v. Georgia – Allowing federal lawsuits against states turns out to be unpopular… among states. 11th Amendment incoming.

Day 21: #SCOTUS100 Gonzales v. Raich – Growing a plant in your house and consuming it is still covered by the Commerce Clause. The Court relied in part on the dictionary definition of "economic" – presumably did not consult a dictionary for the definition of "commerce."

Day 89: #SCOTUS100 New York Times Co v Sullivan – Defamation of public figures requires actual malice… thus protecting NYT’s long-standing tradition of negligently publishing false information.

Weird, nobody questioned this corporation’s right to 1A free speech protections ????

We would like to propose a challenge: tweet about each of the 100 cases in the library. We call it the #100Cases challenge. If you complete the challenge, please email me, and I will send you an autographed bookplate. The videos will be freely available till May 31, so there is no cost to play along.

Phil Miles, my law school classmate, took the challenge between October 2019 and February 2020. He tweeted about one case a day, with some short observations. It was a very impressive effort. Here are some of his tweets.

Day 1: #SCOTUS100 Chisolm v. Georgia – Allowing federal lawsuits against states turns out to be unpopular… among states. 11th Amendment incoming.

Day 21: #SCOTUS100 Gonzales v. Raich – Growing a plant in your house and consuming it is still covered by the Commerce Clause. The Court relied in part on the dictionary definition of "economic" – presumably did not consult a dictionary for the definition of "commerce."

Day 89: #SCOTUS100 New York Times Co v Sullivan – Defamation of public figures requires actual malice… thus protecting NYT’s long-standing tradition of negligently publishing false information.

Weird, nobody questioned this corporation’s right to 1A free speech protections ????

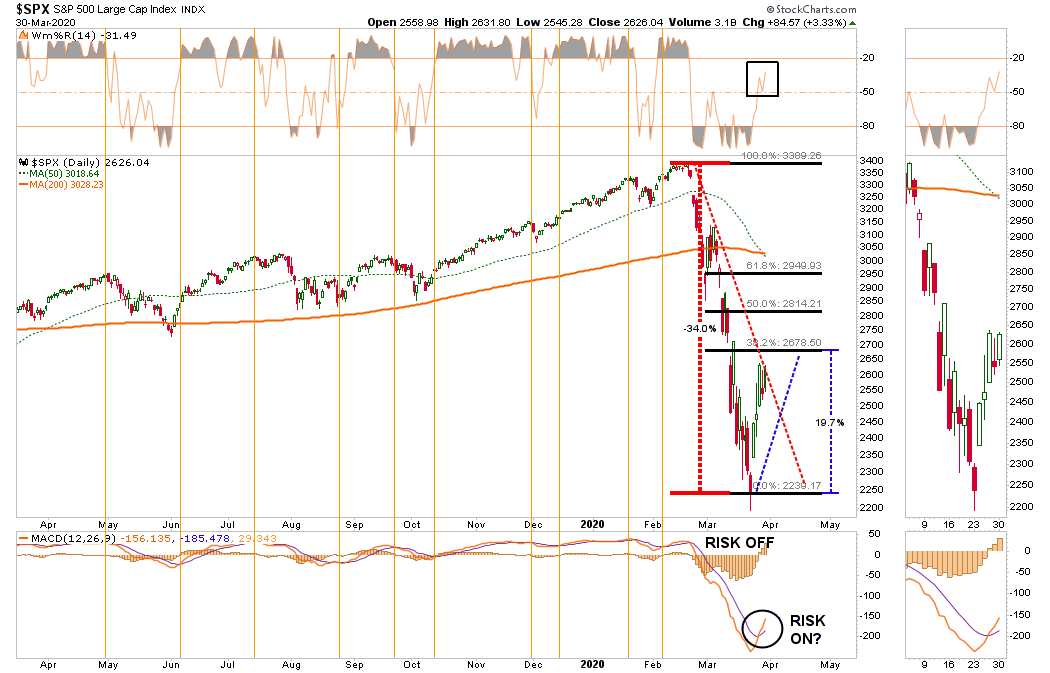

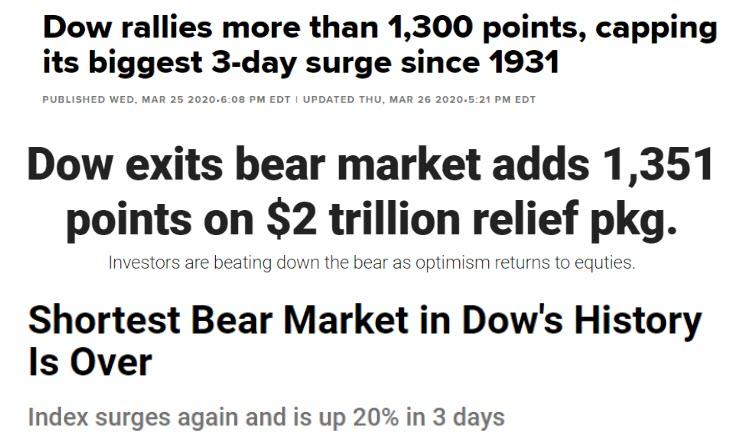

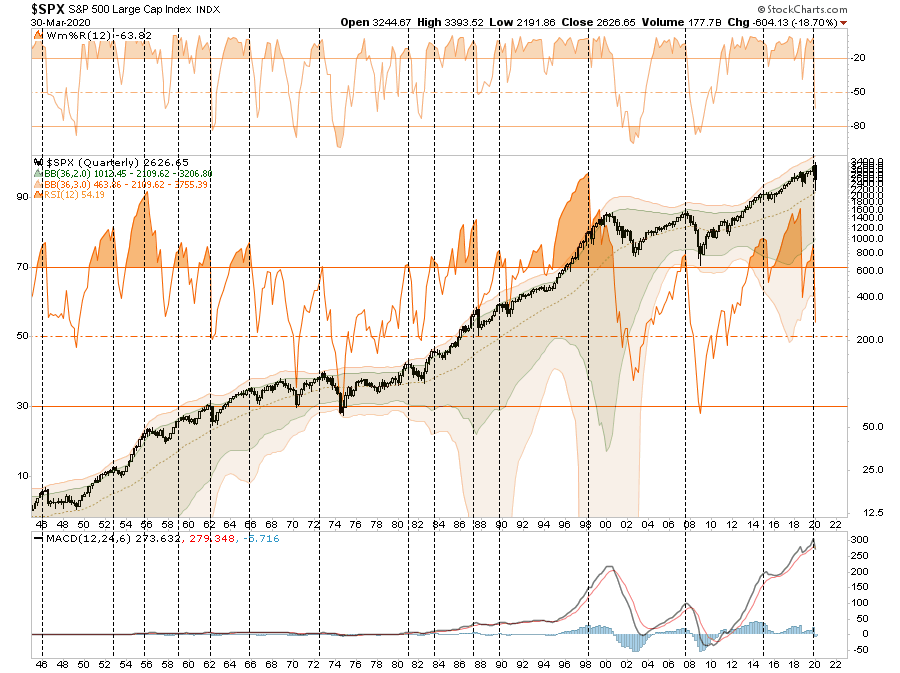

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Honestly, no one knows for certain. However, there are 5-questions that “Market Bulls” need to answer if the current rally is to be sustained.

These questions are not entirely technical, but since “technical analysis” is simply the visualization of market psychology, how you answer the questions will ultimately be reflected by the price dynamics of the market.

Let’s get to work.

1. Employment

Employment is the lifeblood of the economy. Individuals cannot consume goods and services if they do not have a job from which they can derive income. From that consumption comes corporate profits and earnings.

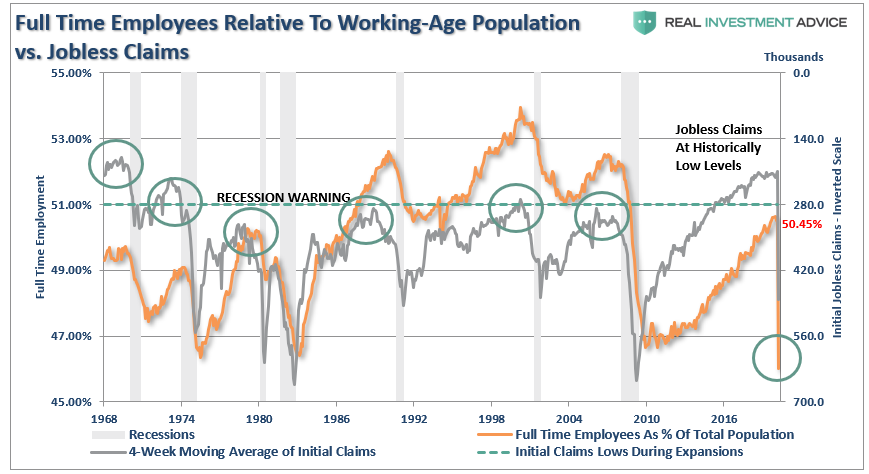

Therefore, for individuals to consume at a rate to provide for sustainable, organic (non-Fed supported), economic growth they must work at a level that provides a sustainable living wage above the poverty level. This means full-time employment that provides benefits, and a livable wage. The chart below shows the number of full-time employees relative to the population. I have also overlaid jobless claims (inverted scale), which shows that when claims fall to current levels, it has generally marked the end of the employment cycle and preceded the onset of a recession.

This erosion in jobless claims has only just begun. As jobless claims and continuing claims rise, it will lead to a sharp deceleration in economic confidence. Confidence is the primary factor of consumptive behaviors, which is why the Federal Reserve acted so quickly to inject liquidity into the financial markets. While the Fed’s actions may prop up financial markets in the short-term, it does little to affect the most significant factor weighing on consumers – their job.

Question: Given that employment is just starting to decline, does such support the assumption of a continued bull market?

* * *

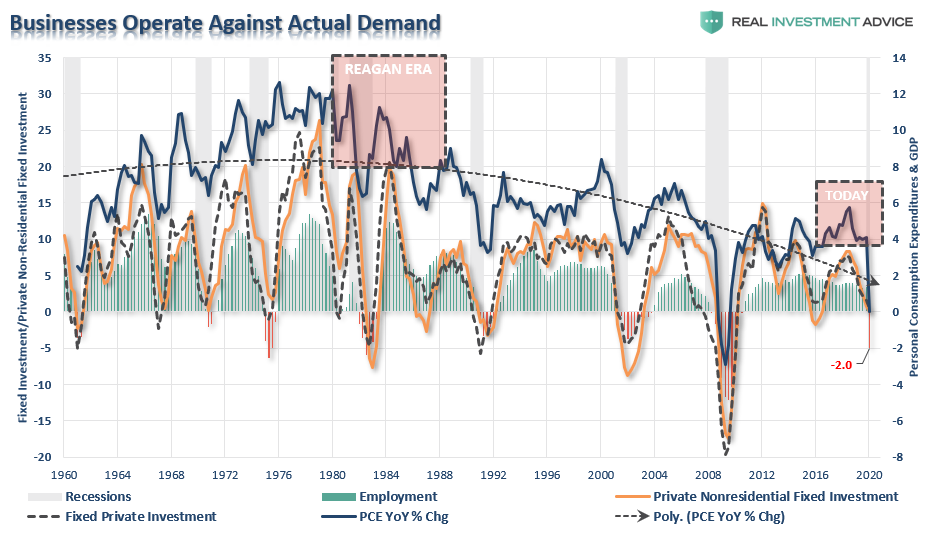

2. Personal Consumption Expenditures (PCE)

Following through from employment, once individuals receive their paycheck, they then consume goods and services in order to live.

This is a crucial economic concept to understand, which is the order in which the economy functions. Consumers must “produce” first, so they receive a paycheck, before they can “consume.” This is also the primary problem of Stephanie Kelton’s “Modern Monetary Theory,” which disincentivizes the productive capacity of the population.

Given that Personal Consumption Expenditures (PCE) is a measure of that consumption, and comprises roughly 70% of the GDP calculation, its relative strength has great bearing on the outcome of economic growth.

More importantly, PCE is the direct contributor to the sales of corporations, which generates their gross revenue. So goes personal consumption – so goes revenue. The lower the revenue that flows into company coffers, the more inclined businesses are to cut costs, including employment and stock buybacks, to maintain profit margins.

The chart below is a comparison of the annualized change in PCE to corporate fixed investment and employment. I have made some estimates for the first quarter based on recent data points.

Question:Does the current weakness in PCE and Fixed Investment support the expectations for a continued bull market from current price levels?

* * *

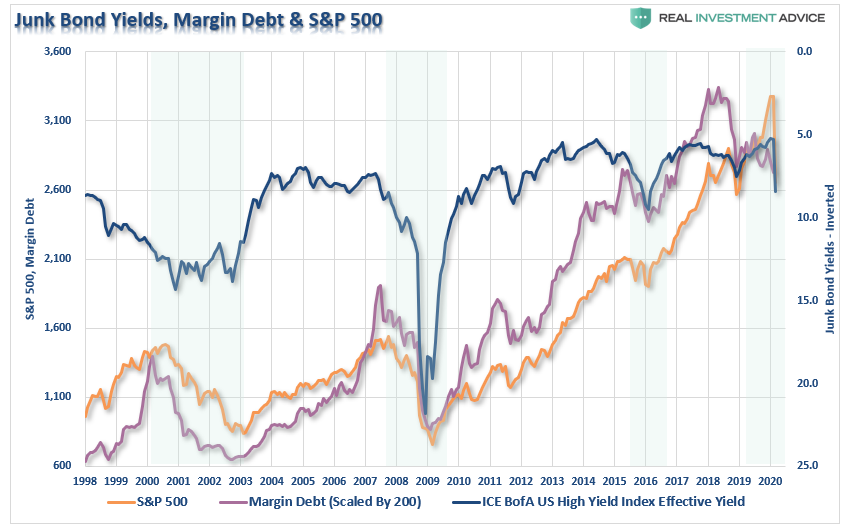

3. Junk Bonds & Margin Debt

While global Central Banks have lulled investors into an expanded sense of complacency through years of monetary support, it has led to willful blindness of underlying risk. As we discussed in “Investor’s Dilemma:”

“Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g. food) is paired with a previously neutral stimulus (e.g. a bell). What Pavlov discovered is that when the neutral stimulus was introduced, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.”

That “stimuli” over the last decade has been Central Bank interventions. During that period, the complete lack of “fear” in markets, combined with a “chase for yield,” drove “risk” assets to record levels along with leverage. The chart below shows the relationship between margin debt (leverage), stocks, and junk bond yields (which have been inverted for better relevance.)

While asset prices declined sharply in March, it has done little to significantly revert either junk bond yields or margin debt to levels normally consistent with the beginning of a new “bull market.”

With oil prices falling below $20/bbl, a tremendous amount of debt tied to the energy space, and the impact the energy sector has on the broader economy, it is likely too soon to suggest the markets have fully “priced in” the damage being done.

Question:What happens to asset prices if more bankruptcies and forced deleveraging occurs?

* * *

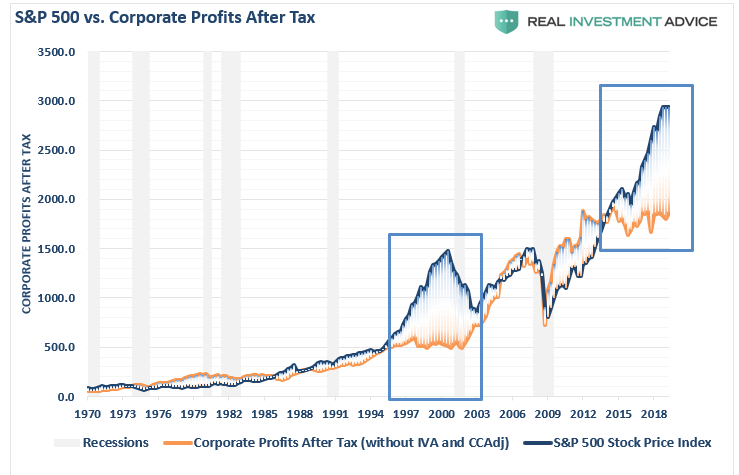

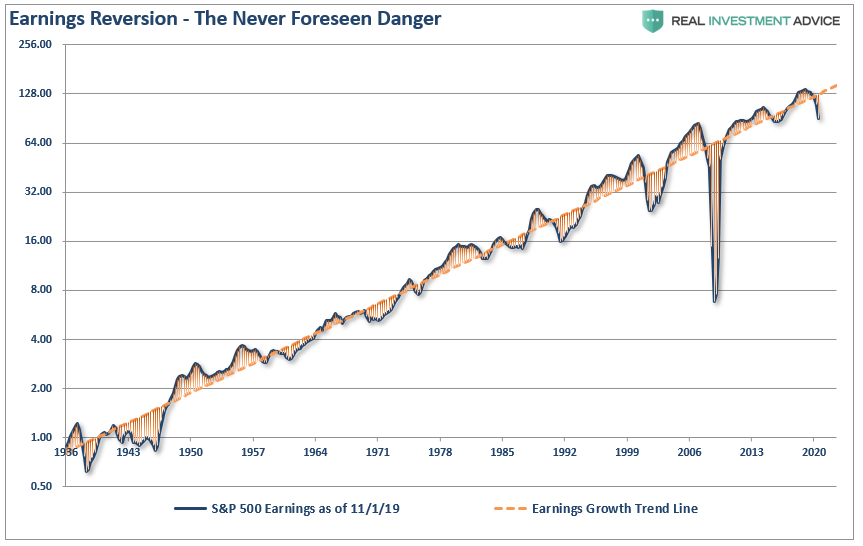

4. Corporate Profits/Earnings

As noted above, if the “bull market” is back, then stocks should be pricing in stronger earnings going forward. However, given the potential shakeout in employment, which will lower consumption, stronger earnings, and corporate profits, are not likely in the near term.

The risk to earnings is even higher than many suspect, given that over the last several years, companies have manufactured profitability through a variety of accounting gimmicks, but primarily through share buybacks from increased leverage. That cycle has now come to an end, but before it did it created a massive deviation of the stock market from corporate profitability.

“If the economy is slowing down, revenue and corporate profit growth will decline also. However, it is this point which the ‘bulls’ should be paying attention to. Many are dismissing currently high valuations under the guise of ‘low interest rates,’ however, the one thing you should not dismiss, and cannot make an excuse for, is the massive deviation between the market and corporate profits after tax. The only other time in history the difference was this great was in 1999.”

It isn’t just the deviation of asset prices from corporate profitability, which is skewed, but also reported earnings per share.

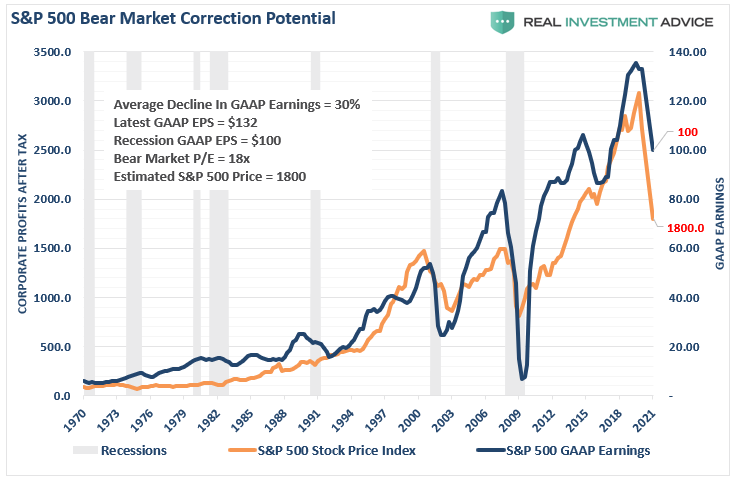

The impending recession, and consumption freeze, is going to start the mean-reversion process in both corporate profits, and earnings. I have projected the potential reversion in the chart below. The reversion in GAAP earnings is pretty calculable as swings from peaks to troughs have run on a fairly consistent trend.

Using that historical context, we can project a recession will reduce earnings to roughly $100/share. (Goldman Sachs currently estimates $110.) The resulting decline asset prices to revert valuations to a level of 18x (still high) trailing earnings would suggest a level of 1800 for the S&P 500 index. (Yesterday’s close of 2626 is still way to elevated.)

The decline in economic growth epitomizes the problem that corporations face today in trying to maintain profitability. The chart below shows corporate profits as a percentage of GDP relative to the annual change in GDP. The last time that corporate profits diverged from GDP, it was unable to sustain that divergence for long. As the economy declines, so will corporate profits and earnings.

Question: How long can asset prices remain divorced from falling corporate profits and weaker economic growth?

* * *

5. Technical Pressure

Given all of the issues discussed above, which must ultimately be reflected in market prices, the technical picture of the market also suggests the recent “bear market” rally will likely fade sooner than later. As noted above”

“Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Importantly, despite the sizable rally, participation has remained extraordinarily weak. If the market was seeing strong buying, as suggested by the media, then we should see sizable upticks in the percent measures of advancing issues, issues at new highs, and a rising number of stocks above their 200-dma.

However, on a longer-term basis, since this is the end of the month, and quarter, we can look at our quarterly buy/sell indication which has triggered a “sell” signal for the first time since 2015. While such a signal does not demand a major reversion, it does suggest there is likely more risk to the markets currently than many expect.

Question: Does the technical backdrop currently support the resumption of a bull market?

* * *

There are reasons to be optimistic on the markets in the very short-term. However, we are continuing to extend the amount of time the economy will be “shut down,” which will exacerbate the decline in the unemployment and personal consumption data. The feedback loop from that data into corporate profits and earnings is going to make valuations more problematic even with low interest rates currently.

While Central Banks have rushed into a “burning building with a fire hose” of liquidity, there is the risk that after a decade of excess debt, leverage, and misallocation of assets, the “fire” may be too hot for them to put out.

Assuming that the “bear market” is over already may be a bit premature, and chasing what seems like a “raging bull market” is likely going to disappoint you.

Bear markets have a way of “suckering” investors back into the market to inflict the most pain possible. This is why “bear markets” never end with optimism, but in despair.

{kind=link}