Writers in the Washington Postand the New York Timesnow agree with many other sources that masks may be useful in combatting COVID-19, perhaps because masks reduce the probability that the wearer will infect others or, at least by discouraging touching of the face, the probability that someone else will infect the wearer.

Meanwhile, writers in the Washington Post and the New York Timesare beginning to describe how the economy might restart in the not-so-distant future. Neither mentions the word “mask.”

At this point, we don’t know for sure how well masks work, and there is a danger that masks could provide a false sense of security. If masks in fact greatly reduce transmission, however, then mask mandates will likely be part of the solution. A mask mandate is a much lesser intrusion on liberty than stay-at-home orders.

Surgical masks are not yet widely available, but apparently even DIY masks have some utility, allegedly helping to explain why the Czech Republic has modestly flattened the curve. The CDC could help at this point by encouraging everyone who must be in public or at work to wear at least a DIY mask, while still warning that the measure is not a replacement for social distancing. That might help people get used to the idea. More broadly, the government could help by focusing on mask production. For example, the federal government could promise to buy billions of surgical masks in the event manufacturers are unable to find buyers; the worst case scenario is that the national stockpile is replenished for the next pandemic.

In the longer term, more analysis would be helpful. Perhaps we’ll learn more as some countries, states, and municipalities adopt mask mandates, or as masks become more popular in some areas than other. Some form of random experimentation would be especially helpful. For example, once health care providers have enough surgical masks for themselves, the government could distribute masks in randomly selected municipalities and compare growth of COVID-19 infection rates.

from Latest – Reason.com https://ift.tt/2QSmkgr

via IFTTT

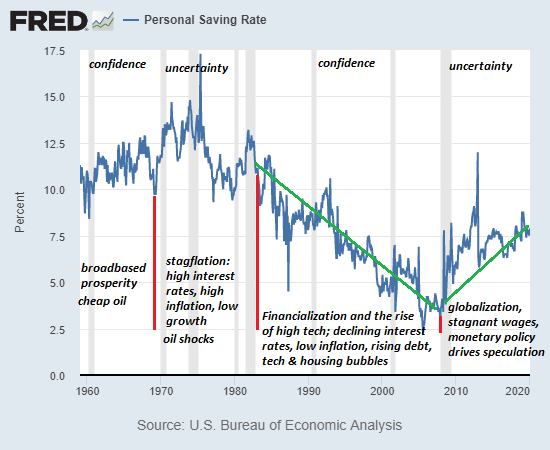

There are only two ways to survive a decline in income and net worth: slash expenses or default on debt.

In post-World War II America, the cultural zeitgeist viewed frugality as a choice: permanent economic growth and federal anti-poverty programs steadily reduced the number of people in deep economic hardship (i.e. forced frugality) and raised the living standards of those in hardship to the point that the majority of households could choose to be frugal or live large by borrowing money to enable additional spending. Either way, rising income and net worth would raise all ships, frugal and free-spending alike.

For everyone above the bottom 20%, frugality was viewed as a sliding scale of choice: if you couldn’t increase your income fast enough, then borrow whatever money you needed. If you chose to be frugal, in moderation (i.e. clipping coupons and shopping for the cheapest airline seats, etc.) this was viewed as admirable fiscal prudence; if pushed beyond moderation then it was dismissed as counter to the American spirit of everlasting expansion: tightwad is not an endearment.

Thus none of us immoderately frugal folks ever fit in. Our frugality raised eyebrows and drew derogatory exhortations from indebted free-spenders to “get out there and live a little,” i.e. blow hard-earned money on aspirational gewgaws or status-enhancing fripperies, including the oh-so-precious “experiences” that have now replaced gauche physical markers of status-climbing.

We are now entering a new era of forced frugality in which incomes and net worth stagnate or decline while the cost of living rises and borrowing is no longer frictionless.

To say that these changes will shock the system is putting it mildly. Here’s the key dynamic in forced frugality: income can drop precipitously without any ratcheting to slow the decline, but costs only ratchet higher, or decline by nearly imperceptible degrees; that is, costs are “sticky” and refuse to slide down as easily as income.

The second key dynamic in forced frugality is the tightening of lending and the rising cost of borrowed money. When lenders could assume that almost every household’s income would increase as a byproduct of ceaseless economic expansion, and assets such as stocks, bonds and houses would always increase in value (any spots of bother are temporary), then the odds of a nasty default (in which the borrower stiffs the lender–no monthly payments to you, Bucko)–were low.

But once incomes and asset valuations are more likely to fall than rise, the door to lending slams shut. Why would lenders extend loans to households and enterprises that are practically guaranteed to default? Any lender that self-destructive would soon be stripped of their capital and solvency.

The general assumption is that since central banks are buying bonds, interest rates for borrowers can only go down. This assumption is misguided. The base assumption of all lenders is that a very thin layer of borrowers will default. Once this layer thickens, it makes no sense to lend to everyone who can fog a mirror.

Unwary lenders are about to learn a very painful lesson about the creditworthiness of supposedly solvent middle-class households: since income isn’t “sticky,” households that had high credit scores for years can quite suddenly default on their loans once their incomes plummet.

As for the borrower’s assets, those too can plummet in value, leaving the lender with zero collateral or an asset for which there is no buyer, regardless of the appraised value.

The income/assets slope is greased while the cost slope is on a resistant ratchet. Income can slide down effortlessly while costs stubbornly refuse to fall.

The net result of this dynamic is forced frugality. For the first time in decades, households and enterprises cannot count on a resumption of growth in a few months and higher incomes and asset valuations.

To the dismay of living-large-on-debt households and enterprises, the only way to get more than you have now will be to save, save, save cash. Earning more from one’s labor will be difficult, as will reaping easy speculative gains from simply owning assets.

The debt-free frugal may be forgiven for indulging in a bit of schadenfreude toward those who scorned frugality in favor of living large in the moment. Now who’s living large? Not the extremely frugal, because squandering money gives them no pleasure, and they prefer the anti-status “status” of old cars and trucks, tools that have lasted decades and assets that look like everyone else’s except they’re debt-free.

As for income–those who control and invest their own capital and labor, the class I’ve long called mobile creatives–will have far more opportunities than those chained to the monoculture plantations of corporate cartels and government agencies squeezed by collapsing tax revenues.

A great many people who reckoned moderate frugality was more than enough will discover it no longer suffices. A great many other people who reckoned they were rich enough to spurn frugality will discover their income no longer covers their expenses and so expenses will have to be slashed and burned to the ground.

And many frugal people who did the best they could with limited income will find that even extreme frugality can’t fix a decline in income.

An economy-wide reckoning of what’s essential is just starting. Netflix subscription? Gym membership? Fast food takeout a couple times a week? No, no and no. A thousand no’s as there are only two ways to survive a decline in income and net worth: slash expenses or default on debt. Both are toxic to “growth” in spending and debt.

Dr. Fauci: “We’re Going To Have Millions Of Cases” And “Between 100K & 200K Deaths”

The last time Dr. Anthony Fauci did the Sunday Shows a few weeks back, he achieved a vaunted Washington milestone by doing all five network and cable Sunday shows – NBC, ABC, CBS, Fox News & CNN – in one day. That was back when President Trump’s approval rating was soaring, and the good doctor was indisputably the lead ‘subject matter expert’ guiding the White House’s response.

That was less than a month ago. But in that time, so much has changed.

President Trump and the good doctor are said to be at odds over some vaguely critical statements made by Fauci. Of course, that didn’t stop the administration and that task force’s media team from sending him out to do more Sunday Show appearances as officials hope futures will open higher after Friday’s selloff following the first three-day rebound since February.

Still, as the death toll in the US crept above 2,000, Dr. Fauci, officially the director of the National Institute of Allergy and Infectious Diseases and a member of the White House coronavirus task force told CNN’s “State of the Union” that models suggest the coronavirus will infect millions of Americans and could kill between 100,000 to 200,000.

However, he stressed that these projections are really a “moving target”, and that it’s possible the numbers could be much lower – or much higher – depending on how the US handles the response. So far, the disorganized response at the federal level has left a hodge podge of states to deal with their own problems, which is why Louisiana Gov. John Bel Edwards – a Democrat – is begging the Feds for help before the outbreak completely overruns his state’s capacity to handle it.

Video of Dr. Fauci telling @jaketapper that “Looking at what we’re seeing now, I would say between 100,000 and 200,000 cases… excuse me, deaths. I mean, we’re going to have millions of cases.” #CNNSOTU

Back to the interview, Dr. Fauci told Jake Tapper that “Looking at what we are seeing now, I would say between 100,000-200,000” deaths from the coronavirus. “We’re going to have millions of cases,” he added.

“But it’s such a moving target and you could so easily be wrong…what we do know is we have a serious problem in New York, we have a serious problem in New Orleans and we’re going to be developing serious problems in other areas. Although people like to model it, let’s just look at the data that we have, and not worry about these worst case and best case scenarios.”

Dr. Fauci also cautioned the public about how to interpret models:

“There are things called models, and when someone creates a model, they put in various assumptions. And the model is only as good and as accurate as your assumptions.”

“And whenever the modelers come in, they give a worst case scenario and a best case scenario. Generally, the reality is somewhere in the middle. I’ve never seen a model of the diseases that I’ve dealt with where the worst case scenario actually came out. They always overshoot.”

Dr. Fauci stressed that Trump’s hope to reopen the country by Easter will greatly depend on whether the public complies with the ‘shelter in place’ recommendations, though he said he greatly doubts that the US will be able to reopen by next week (Easter is April 12, still a couple of weeks away). And notably, when Tapper pressed Dr. Fauci about rumors the administration was ignoring Democratic governors pleas for more federal assistance simply because they were Democrats, Dr. Fauci assured CNN that anybody asking for assistance would get it.

#CNNSOTU Watch Tapper tried to trap Dr. Fauci to smear President Trump😂😂😂

Dr. shut him down quickly again and again throughout the whole interview. pic.twitter.com/wlcFa0VTg1

That last clip is really something: but the takeaway from the interview is this: prepare for the worst, but hope for the best. The result is going to depend on whether millions of Americans do their part not to spread the virus. So, instead of focusing on the projections, focus on reacting to the situation at hand.

The economy is the heart of the social body. If we shut down the heart of an organism to safeguard the hands and brain, the body dies.

The data on deaths and infected from the Covid-19 coronavirus epidemic is alarming. Let us remember the deceased, the infected and their families, and applaud the response of civil society, businesses, and citizens.

A pandemic crisis is addressed by providing safety protocols and sanitary equipment for businesses to continue to run and keep employment, not shutting down everything, which may create a larger social and health problem in the long term regardless of the massive liquidity and fiscal policies. Why? Because demand-side policies never work in a forced shutdown of all sectors. There is no demand to “incentivize” when the government orders the closing of all activities. And there is no supply to follow when the economic crisis creates a collapse in employment and consumption.

Many commentators are saying that shutting down the economy is an essential measure to gain time to control the virus. This analysis comes from people who simply do not understand the ripple effects and massive ramifications of a complete shutdown. They perceive that it is small collateral damage because they also believe that everything can go back to normal in one month. They are wrong. The impact is severe, widespread and exponential.

The decision to shut down the economy may cause long-lasting damages to job creation and businesses that cannot be unwound in a few months. Yes, it is essential to contain the virus spread and drastic measures are warranted, but we cannot forget that each month means millions of unemployed and thousands of business closures.

Each month of lockdown means more than millions of unemployed. It means thousands of businesses that go bankrupt and have to close forever. This debunks the V-shaped recovery theory (even with Congress package, which does not address the working capital nightmare unraveling). The best course of action to tackle the health crisis, as well as the economic collapse risk, is to follow the South Korea and Singapore strategy. This is not a spending crisis, but a test and prevention crisis.

The healthcare crisis has to be tackled from three angles: prevention, testing and ensuring that treatment and vaccines will be widely available when ready. If governments fall prey to panic and destroy the economic fabric of the country they will add poverty, misery, and bankruptcy to the fatalities of the epidemic, thus creating a larger, longer-lasting social and health depression.

The debate in the media has tried to focus on the issue of austerity and government spending as if this had been solved by having massive budgets.

This is not a crisis due to a lack of health spending but from the lack of foresight, prevention, and management of some countries.

South Korea is, with 51 million inhabitants, is one of the countries with a higher ranking in economic freedom (ranked 25 globally), public spending to GDP is much lower than most leading economies, at 30%, and per-capita health expenditure is much lower than in the EU or US. South Korea is also a world example in managing the pandemic, with 139 deaths and 9,332 cases at the end of this article. The same can be said of Singapore, also a leader in economic freedom and with much lower spending to GDP (18%).

On the opposite side, Spain or Italy, with large government spending (above 40% of GDP) and vast public healthcare systems, stand unfortunately at the top of the list in deaths. There may be many factors involved, but one is clear. More spending is not the magic solution to a crisis generated by poor prevention and mismanagement.

What has been the success of the leading countries? Little bureaucratic administration and a fast, effective and efficiently managed prevention, analysis and containment system.

Any Spanish or Italian citizen can understand that the accumulation of inefficiencies they have experienced in managing the pandemic would have been the same if in the past they had spent much more because resources would have been allocated to other things, not to an epidemic that the governments failed to recognize. It is a management problem, not necessarily of funding, and much less of funds managed by the government.

This leads us to another fallacy which is the concept of “public health” when what most politicians want to impose is “political health”. An efficient public service health system not only does not have to be a single-payer but much less a single manager and less so a political one.

Recall that in July last year that same government called on the autonomous communities to reduce spending on Health (“urgent plan for adjustments in pharmaceutical and health spending”, demanding measures “in the outpatient and hospital pharmaceutical provision, as well as in health products” ).

Public services and the private sector are giving everything and more in this crisis. This is the evidence of social capitalism that I comment on in my book, Freedom or Equality (PostHill Press).

The crisis has shown that the only solution to future challenges comes precisely from greater collaboration, with a solid and powerful private sector. There is no public sector without the private sector. There is no public health without the technology, innovation, research, products, and drugs of the private sector. No leading state in the world faces the challenges of health in the future by imposing political management as the only option.

Everyone knows that we will need all-important competition, freedom of choice, and technological leadership to serve many more people while maximizing the use of resources. Anyone who thinks that by destroying the private sector they are going to guarantee greater and better access to goods and services has a problem with history and statistics. No leading healthcare system is only state-managed. And none works only with state-owned resources.

Health professionals do not belong to the Government. They are free individuals, many of them working in the private and public sector at the same time, and they are part of civil society that provides a service with their magnificent work, which we taxpayers pay for.

This crisis has demonstrated the reality of capitalism as the most efficient and social system. Companies and self-employed workers have responded in an exemplary way. The number of businesses, entrepreneurs, and organizations that have acted quickly and efficiently to support countries like Spain or Italy in difficult times is enormous. Unfortunately, these days the examples of solidarity and contribution shown by anti-capitalist agitators are almost non-existent.

It is curious that those “anti-capitalists” who previously encouraged debt defaults and anti-business slogans today demand the most capitalist instruments in the world, support from the balance sheet of multinationals, multibillion-dollar bond issuances that they will have to sell to the investment funds they hate, and massive debt that will be financed by the investors they abhorred, with investments that will be made by the companies they condemn and giant loans from the banks they wanted to destroy. I have never seen more capitalist anti-capitalists.

Thanks to capitalism, we are going to get out of this crisis of poor prevention and worse management in a record period, if there are no more obstacles for economic recovery. In socialism, we would be forced to choose between misery and more misery, added with repression once the citizens began to show their discontent with the Government.

When the Government stands as the only power without checks and balances, the door is opened to incompetence, authoritarianism, and misery. Competition is essential for progress. The moment competition and freedom are curtailed, progress is destroyed.

That is the great advantage of a free economy. Progress in competition and freedom. The government is at the service of civil society and taxpayers, and not the other way around.

This crisis is going to destroy millions of jobs, but these can recover quickly and heal the economy if governments don’t make the mistake of addressing a pandemic crisis by creating an economic depression. Spain and Italy show why this is a grave mistake. The vast majority of small and medium companies are sent en masse to collapse, leading to years of economic stagnation, poverty, and massive unemployment. Destroying the economy is not a social policy.

Governments need to provide citizens and businesses with the tools to ensure safety, not kill the social fabric of the nation.

Instead of protecting the productive fabric to create more jobs when the pandemic is controlled, some countries are going to lead hundreds of thousands of small businesses to bankruptcy. Businesses that will not come back when, thanks to science, the crisis passes.

The health pandemic will be overcome thanks to human ingenuity, science, technology, and business. The interventionist pandemic will cost a lot more, in lives, in employment, in growth, and in opportunities.

The Unthinkable Is Happening: Oil Storage Space Is About To Run Out

In the past three weeks, oil plunged and has continued to plunge even more in the aftermath of the oil price war declared between Saudi Arabia and Russia, and where US shale (and its junk bonds) has been caught in the crossfire. However, as we reported last week, we may get to the absurd point when the price of a barrel of oil not only hits $0 but goes negative.

The reason: according to Mizuho’s Paul Sankey, at a whopping 15MM b/d in oversupply, crude prices could go negative as Saudi and Russian barrels enter the market. According to Sankey, much of the US 4MM bpd in crude exports will be curtailed as prices fall and tanker rates soar. And with US storage roughly 50% full, and able to take another 135MM bbl more, assuming a build rate of 2MM b/d, the US can add 14MM bbl/week for 10 weeks until full.

As a result, there is a now race between filling storage and negative pricing “unless U.S. decline rates can outpace inventory builds, which we very much doubt.” Said otherwise, absent dramatic changes, in roughly 3 months, energy merchants will be paying you if you generously take a couple million barrels of crude off their hands.

It went from bad to an outright disaster earlier this week when Goldman, Vitol, and the IEA all raised their estimate for daily oil oversupply to an unthinkable 20 million barrels per day, as a result of the collapse in oil demand as the global economy grinds to a halt coupled with Saudi Arabia’s determination to put all of its higher-cost OPEC peers out of business.

This means that for the oil market to rebalance, both Saudi Arabia and Russia would have to halt all output. Needless to say that is not happening, in fact Saudi Arabia is now pumping between 2 and 3 million barrels more than it did last month, which is why the negative oil price scenario envisioned by Sankey is looking more real by the day.

So real, in fact, that the US energy industry is starting to contemplate the all too real possibility of running out of storage and as Bloomberg reports American pipeline operators have begun asking oil producers to voluntarily ratchet back their output in the clearest sign yet that a growing glut of crude is overwhelming storage capacity.

As Bloomberg details, Plains All American Pipeline, one of the biggest shippers of crude in the U.S., sent a letter this week asking its suppliers to scale back production. The notice came from the company’s marketing unit that buys and sells oil to customers. At the same time, a Texas oil regulator said Saturday that drillers were getting similar notices from pipeline operators.

“We are sending this proactive request to our suppliers to ask that you take steps to reduce oil production in response to the pandemic,” Plains said in the letter obtained by Bloomberg. Good luck with that: in an industry geared to always producing, that’s similar to asking the Nile to reverse course.

The company sent a separate letter requiring customers to prove they have a buyer or place to offload the crude they’re shipping, according to people familiar with the matter. Enterprise Products Partners LP put out a similar call, one person said. The firm didn’t immediately have comment. The idea is to prevent anyone from parking oil in pipelines, an unprecedented step which suggests pipeline are now convinced US commercial storage will soon be full, at which point oil producers will have no choice but to pay customers to take the oil or wreck unprecedented havoc on the US oil infrastructure.

If there is any confusion, Bloomberg explains the situation succinctly: “the messages signal the oil market is fast approaching the moment traders have been warning about – when crude supplies overflow storage tanks and pipelines as the coronavirus pandemic drags down oil demand by the most in history.“

* * *

Also on Saturday, Ryan Sitton, a member of the Texas Railroad Commission that regulates the state’s oil industry, said he’d heard that “some Texas producers are starting to get letters from shippers (pipelines) asking for oil production cuts because they are out of storage.”

There were already signs that North America’s storage system was nearing its limit. On Friday, prices for physical delivery of several key crude grades in North America plunged to the lowest levels in decades. West Texas Intermediate crude in the heart of the Permian shale region plunged to $13.01 a barrel, the lowest since 1999. Meanwhile, West Canada oil is just $5 away from turning negative.

It gets crazier: trading giant Mercuria Energy Group bid just 95 cents for Wyoming Asphalt Sour, a dense oil used mostly to produce paving bitumen, and said the same barrel was bid at below zero earlier this month.

Surprisingly this plunge in oil prices has yet to really hit the gas pump, perhaps because US oil refiners have been steadily cutting back on the amount of crude they buy and process as lockdowns across the nation keep cars off the road, sending gasoline demand plummeting.

Meanwhile, a new wave of defaults is coming as US shale producers have begun to anticipate the day their product will be rejected by intermediaries, and are throttling back drilling even if it means they are staring a bond default squarely in the face. That said, it could take weeks if not months before that translates into a meaningful decline in oil production. Meanwhile, America’s largest oil-storage hub at Cushing, Oklahoma is already more than half full, and filling up at a furious pace.

Sitton has been pushing a plan that would have Texas imposing limits on its crude production as part of a deal with the Organization of Petroleum Exporting Countries. “We need to get in front of this,” he said on Twitter Saturday.

Ok, so ground storage is almost full but what about filling up all those tankers that are floating around aimlessly now that global demand has collapsed? After all it wouldn’t be the first time the US commercial storage was nearly exhausted forcing tankers to be deployed as temporary warehouses of physical product?

Well, that’s precisely what is going on. With the oil market falling into a so-called super contango, which means it is now profitable for traders to buy oil today, store it, and reap the profits by selling it at a higher price months or even years down the line, traders are scrambling to dump oil in portable storage. Firms including Vitol Group and Gunvor Group, two of the world’s largest oil traders, say there’s intense demand to keep barrels at sea.

Traders typically look to use the largest ships for oil storage as they are the most cost-effective. In recent days though, shipowners have also been receiving inquiries about smaller vessels that can hold a million barrels or fewer and for periods of time longer than 12 months, said International Seaways Chief Executive Officer Lois Zabrocky.

“This is a once-in-a-generation type of event,” she said Thursday, quoted by OilandGas360.

As Bloomberg reported separately, citing Robert Hvide Macleod, CEO of tanker owner Frontline Management, “oil is going on ships at a speed never seen before,” as a result of the market’s glut; he added that vessels are being filled at five times the pace of 2015, when oil market was last heavily oversupplied. International Seaways, another owner, said on Thursday that the total volume of oil in floating storage may top 100 million barrels during this glut.

Why? Because the bottom line bears repeating: “The world is producing 20 million barrels of oil too much every day”, or said otherwise there is no demand for roughly 20% of global output every single day. At this rate, how long before all the storage in Cushing, ARA and China is overflowing and every single tanker in the world is full?

And what happens to the oil price then? One thing is certain – there will be blood.

In a shocking and tragic development, the deadly Coronavirus has struck at the epicenter of Wall Street: moments ago, investment bank Jefferies announced that its CFO Peg Broadbent, has passed away from coronavirus complications, making him the first top financial executive to pass away from the deadly pandemic.

With Profound Sadness, Jefferies Announces Death of Jefferies Group LLC CFO, Peg Broadbent

Jefferies Financial Group Inc. (NYSE: JEF) today announced with profound sadness that Peg Broadbent, the CFO of Jefferies Group LLC, has passed away from coronavirus complications. The entire Jefferies family mourns Peg’s loss. On behalf of our Board of Directors, management team and all our global employees, we extend our deepest sympathies to Peg’s family.

Rich Handler, our CEO, and Brian Friedman, our President, expressed their most heartfelt condolences and stated: “We are heartbroken and grieve that our friend and colleague, Peg Broadbent, has passed away from coronavirus complications. Our thoughts, prayers and love go out to Peg’s dear wife, Hayley, and their young children, Sebastian and Peg, as well as Peg’s older children, Anna, Sophie and Charlie, and all of Peg’s extended family here and in the United Kingdom.

The loss of Peg is incredibly personal for us as he was a member of our own extended family. For over a dozen years, Peg has been our CFO and partner, and helped us build Jefferies from less than half its current size, and navigate through hard times and good times. He has also been a much-loved and respected leader to the incredible global team that provides the support, foundation and glue across our firm. But Peg was so much more. Part of what made Peg the great partner he was to all of us was his core humanity. No matter what the occasion, his decency, calmness and dry wit were always there, always making things better. We will miss him terribly.

We know Peg would want his passing to serve as a reminder to all of us of how much he cared for all of his friends at Jefferies and that our priority must be the health and happiness of our loved ones. May Peg’s memory be for a blessing for his family, for us and for all who loved him.”

Teri Gendron, CFO of Jefferies Financial Group, has been appointed as the interim CFO and Chief Accounting Officer of Jefferies Group LLC.

Governors Order Police To Stop & Interrogate New Yorkers As COVID-19 Cases Top 660K Globally: Live Updates

Late last night, President Trump said he wasn’t planning on quarantining New York, New Jersey and Connecticut, but that the governors of other states like Florida had complained about the number of travelers from out-of-state bringing disease and pestilence with them from the big city.

So, instead of a quarantine, governors are taking measures into their own hands, and authroizing the police and the national guard to interrogate anybody with an out-of-state license plate, or a rental vehicle or an out-of-state driver’s license about the steps they’re taking to quarantine themselves, and issue fines if necessary.

Spain on Sunday reported yet another record rise in the death toll – another 838 fatalities – bringing the total to about 6,500 deaths and almost 79,000 registered coronavirus cases, the fourth highest in the world. It’s at least the second day in a row that Spain has reported a ‘record-breaking’ jump in its death toll.

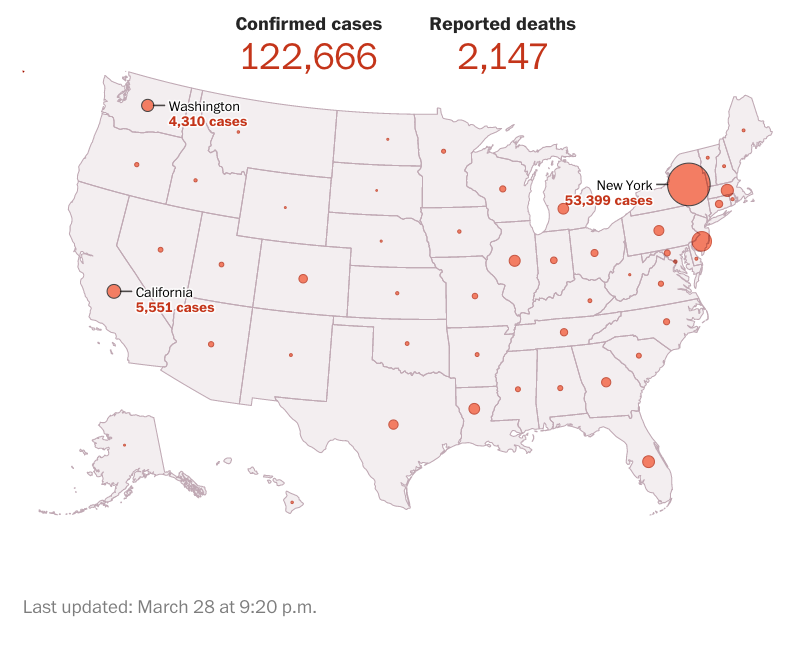

But the US, with its total number of cases climbing at the fastest pace on record anywhere – even as large swaths of the country still have trouble accessing tests – is really starting to panic. The number of confirmed cases globally is nearing 682k, and in the US, 124,866 have been confirmed as of Sunday morning, Johns Hopkins said. Another 2,191 deaths had been recorded, with nearly 200 of those having occurred since late Saturday.

Last night, Jim Dolan, the owner of NBA team New York Knicks, has tested positive for the coronavirus, the basketball team said in a Twitter post.

The Madison Square Garden Company Executive Chairman and Chief Executive Officer Jim Dolan has tested positive for coronavirus. He has been in self-isolation and is experiencing little to no symptoms. He continues to oversee business operations.

In other news, Peg Broadbent, the CFO of investment bank Jeffries, has passed away due to “complications” related to contracting COVID-19.

Texas, Florida, Maryland and South Carolina are among the other states that have ordered people arriving from New York to self-quarantine. In Texas, the authorities said on Friday that Department of Public Safety agents would make surprise visits to see whether travelers were adhering to the state’s mandate, and they warned that violators could be fined $1,000 and jailed for 180 days. Conn. Gov. Ned Lamont last week urged all travelers from New York City to self-quarantine for two weeks upon entering the state, but he stopped short of issuing an order requiring it.

Just like in the US, where national guard troops in multiple states are now stopping anybody with a New York license plate to ask them, kindly, what in the hell they are doing driving around in a different state, European police are struggling to stop wealthier Europeans from fleeing to their cottages by the lake and/or mountains, which purportedly ‘lessen the difficulty of confinement’.

Even political leaders have faced criticism. In Spain, José María Aznar, the former prime minister, departed for his holiday villa in Marbella, a celebrity resort on the Mediterranean, leaving Madrid on the day that schools were shuttered. News of his move prompted an angry backlash as the public demanded he shut himself inside his villa.

Meanwhile, after a hospital system in Michigan revealed new protocols that would prioritize life-saving equipment for younger patients with fewer co-morbidities, the US civil rights office released a new bulletin arguing that protocols to ration lifesaving medical care adopted by Alabama, Washington State and elsewhere were discriminatory and impermissible. This comes as more hospitals develop plans to ration care that sometimes involves making uncomfortable choices. This is “war”, right?

Many plans would prioritize patients who were most likely to survive their immediate illness, and who also had a better chance of long-term survival. Some assign patients a score based on calculations of their level of illness, with decisions on patients with similar scores being made by chance. Some plans instruct hospitals not to offer mechanical ventilators to people above a certain age, or with a certain combination of high-risk conditions.

In Louisiana, where Gov. Jon Bel Edwards is begging for more federal aid as the outbreak ramps up, an inmate at a federal prison also died from the coronavirus, according to an employee at the facility. The death is the first involving an inmate in the Federal Bureau of Prisons system. Yesterday, we reported that an infant had died in Chicago, possibly the first in the US. Authorities have apparently confirmed this is, unfortunately, the truth.

Newborns and babies have seemed to be largely unaffected by the coronavirus, but three new studies suggest that the virus may reach the fetus in utero.

“There has never before been a death associated with Covid-19 in an infant,” said Dr. Ngozi Ezike, the director of the Illinois Department of Public Health. “A full investigation is underway to determine the cause of death.” Older adults, especially those in their 80s and 90s, have been viewed as the most vulnerable in the outbreak, but younger people have also died despite having no co-occurring conditions, as we’ve pointed out.

The BoP website presently lists five inmates and no staff members at the Oakdale prison as having tested positive, and across the federal system, at least 27 inmates and prison workers have tested positive for the virus.

Along the border, a judge concerned that thousands of migrant children in federal detention facilities could be in danger of contracting the coronavirus ruled late Saturday that the government must “make continuous efforts” to release the migrant children from custody, which would seem to violate the spirit of the whole ‘shelter in place’ idea.

The order, from Judge Dolly M. Gee of the United States District Court, came after plaintiffs in a long-running case over the detention of migrant children cited reports that four children being held at a federally licensed shelter in New York had tested positive for the virus.

In New York City, still the center of the outbreak across the US, the number of infections has overwhelmed city systems in a matter of days. The city’s 911 system has been overwhelmed by calls for mostly virus-related medical problems. Typically, the system sees about 4,000 Emergency Medical Services calls a day.On Thursday, dispatchers received nearly double that number. They haven’t seen this many calls since 9/11.

Yesterday, we shared a video made by Taiwanese journalists involving a senior WHO official who steadfastly refused to say anything about China’s response or the WHO’s dismissive treatment of Taiwan.

Now, the NYT reports that the WHO official “ducked questions about Taiwan’s response to the coronavirus pandemic,” reviving suspicions about China and the “undue influence” that Beijing has over the WHO.

Thank god New Yorkers have Andrew Cuomo to lead them through this crisis, because it seems like despite all of the government’s efforts, the outbreak is still accelerating faster than most models had projected.

“While the president has said he’d like to open the country up in weeks not months, we’re going to be bringing that data forward to him,” Pence said in an interview with Fox News. “Ultimately, the president will make a decision that he believes is in the best interest of all of the American people”

Over in Italy, where the pace of new cases is finally starting to slow, a top Italian health official said Sunday that he believes the country is at the “peak” of the coronavirus outbreak and that within a week to 10 days the number of cases will start dropping. Deputy Health Minister Pierpaolo Sileri told the BBC that Italy’s lockdown is starting to work. The country is the world’s worst-hit by the pandemic, having overtaken the official Chinese death toll 10 days ago. “I believe we are living in the peak of this epidemic,” Sileri said. “In one week time, 10 days maximum, we will see a drop, a significant drop in positive cases.”

Let’s hope, for the Italians sake, and for the Americans’ sake, that he’s right.

The “2020 SOCIALLY DISTANT INVESTMENT SUMMIT” is coming on Thursday, April 2nd.

Click the link below to receive an email with a special “invitation only” link when the summit goes “live.” (Current newsletter subscribers are already registered.)

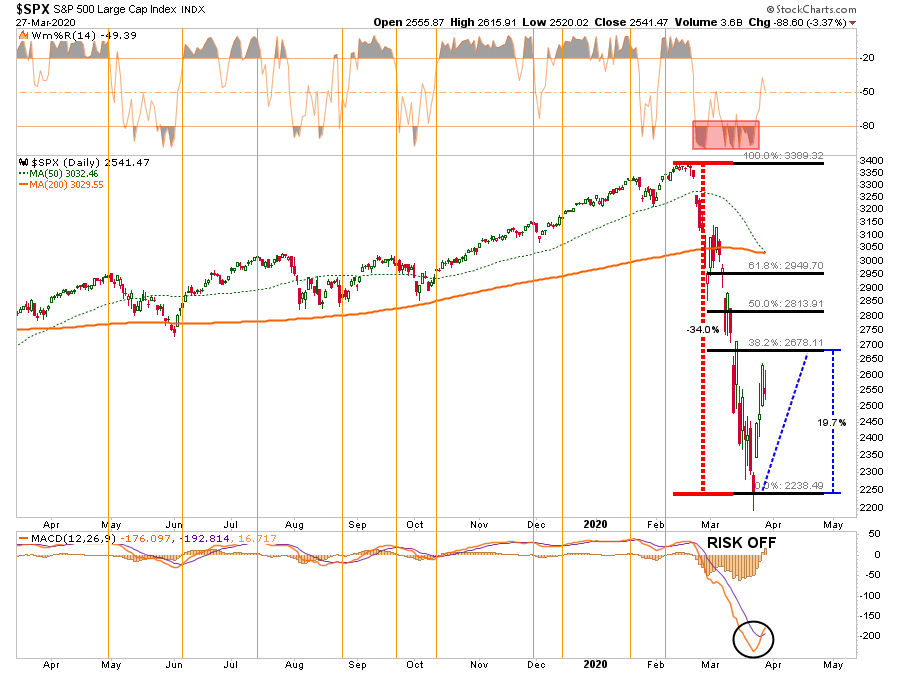

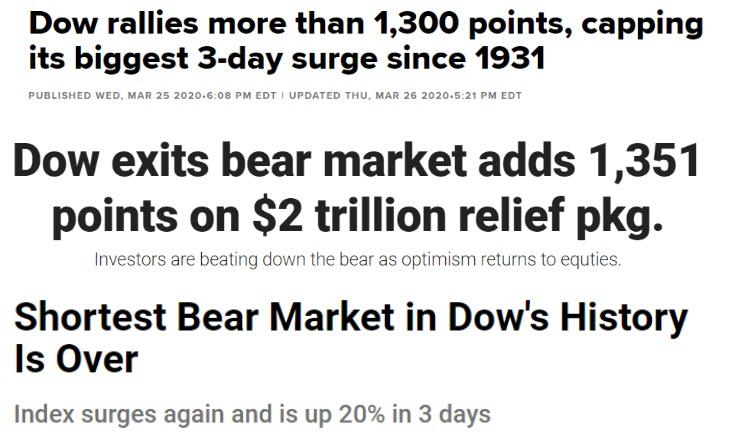

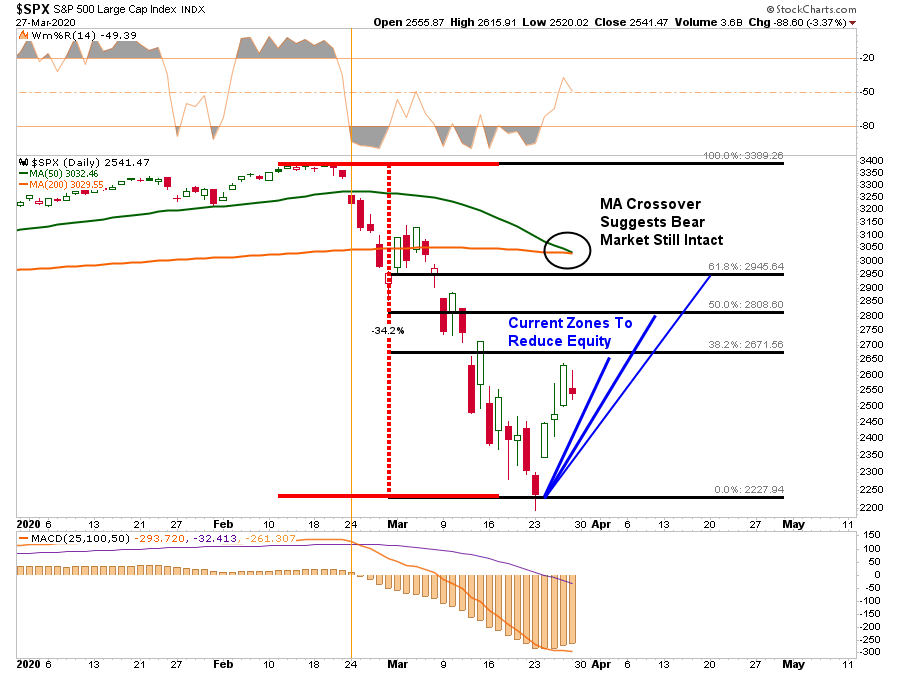

“From a purely technical basis, the extreme downside extension, and potential selling exhaustion, has set the markets up for a fairly strong reflexive bounce. This is where fun with math comes in.

As shown in the chart below, after a 35% decline in the markets from the previous highs, a rally to the 38.2% Fibonacci retracement would encompass a 20% advance.

Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.”

Chart Updated Through Friday

Not surprisingly, here were the headlines, almost exactly as we wrote them:

Well, you get the idea.

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. More importantly, “bear markets” only end when “NO ONE wants to buy it.”

Fed Can’t Fix It

As noted above, the “bear market” will NOT be over until the credit market is fixed. We are a long way from that being done, given the blowout in yields currently occurring.

The Fed has cut rates by 150 basis points to near zero and run through its entire 2008 crisis handbook.

That wasn’t enough to calm markets, though — so the central bank also announced $1 trillion a day in repurchase agreements and unlimited quantitative easing, which includes a hard-to-understand $625 billion of bond-buying a week going forward. At this rate, the Fed will own two-thirds of the Treasury market in a year.

But it’s the alphabet soup of new programs that deserve special consideration, as they could have profound long-term consequences for the functioning of the Fed and the allocation of capital in financial markets. Specifically, these are:

CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-sized businesses, complementing efforts by the Small Business Association.

To put it bluntly, the Fed isn’t allowed to do any of this.”

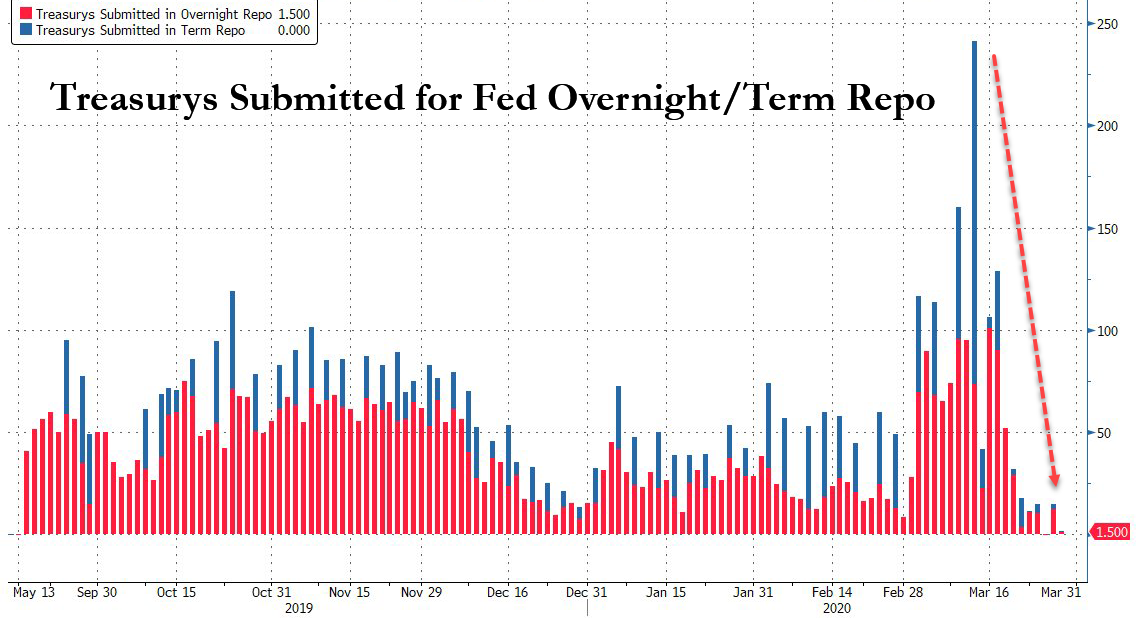

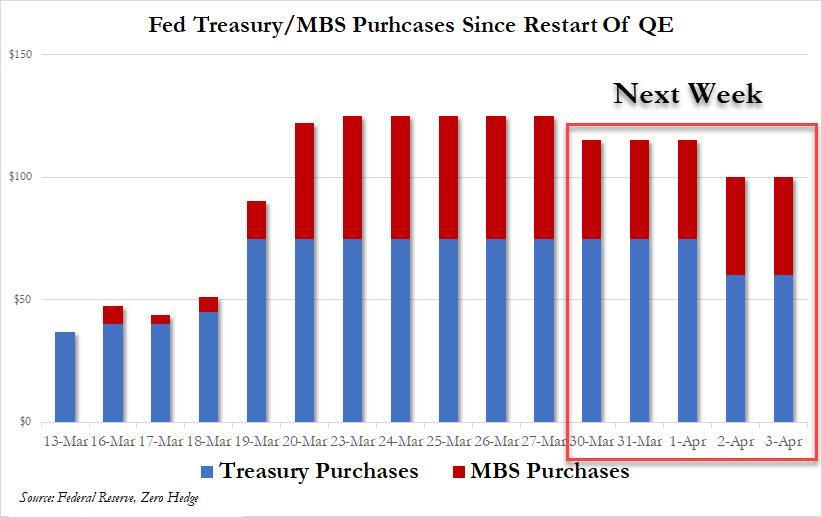

However, on Friday, the Federal Reserve ran into a problem, which could poses a risk for the markets going forward. As Jim noted, the mind-boggling pace of bond purchases quickly hit the limits of what was available to pledge for collateral.

Or rather, the Fed’s “unlimited QE,” may not be so “unlimited” after all.

The consequence is the Fed is already having to start cutting back on its QE program. That news fueled the late-day sell-off Friday afternoon. (Charts courtesy of Zerohedge)

While Congress did pass the “CARES” act on Friday, it will do little to backstop what is about to happen to the economy for two primary reasons:

The package will only support the economy for up to two months. Unfortunately, there is no framework for effective and timely deployment; firms are already struggling to pay rents, there are pockets of funding stress in credit markets as default risks build, and earnings guidance is abandoned.

The unprecedented uncertainty facing financial markets on the duration of social distancing, the depth of the economic shock and when the infection rate curve will flatten, and there are many unknowns which will further undermine confidence.

Both of these points are addressed in this week’s Macroview but here are the two salient points to support my statement:

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance, can be provided. This will lead to higher and longer-duration of, unemployment.”

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any type of disruption to their income going into the recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits leads to higher unemployment and lower asset prices until the cycle is complete.

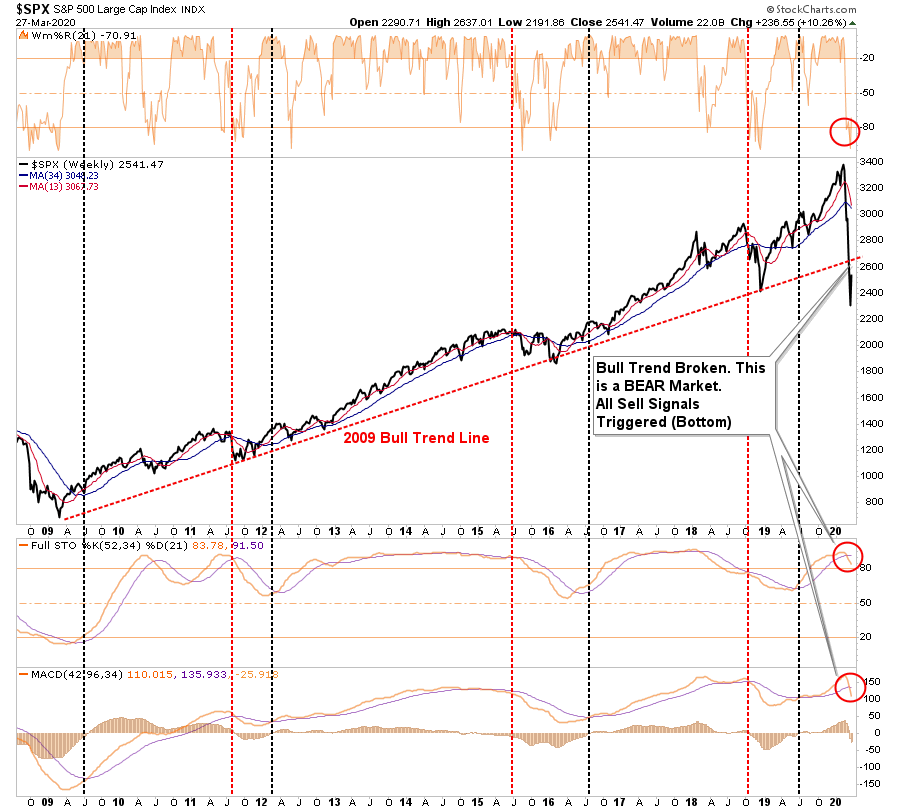

The long term bull pattern that existed since the 3/9/09 is over. That means the pattern of investors confidently buying every decline is over.

The market became historically oversold on 3/23 using many metrics, and that oversold condition coincided with the long term support area of S&P 500 2110-2180.

The short-covering and rebalancing had a lot to do with the size and speed of the 3-day rally. Also, we know the lack of ETF liquidity played a huge role as well as algorithmic trading.

Technically the market can still go up 6.9% higher from here to hit the 50% retracement level (3386 – 2237 = 1149/2 = 574 + 2237 = 2811….2811/2630 = +6.9%.) I would not bet on it.

The market only sustains a rally once there is light at the Coronavirus tunnel.

I do not think the S&P 500 will hit a new high this year. Maybe not in 2021, either.

His analysis agrees with our own, which we discussed with you last week.

“The good news is the markets are now more extremely oversold on a variety of measures than at just about any other point in history.

Warning: Any reversal will NOT BE the bear market bottom. It will be a ‘bear market’ rally you will want to ‘sell’ into. The reason is there are still many investors trapped in ‘buy and hold’ and ‘passive indexing’ strategies that are actively seeking an exit. Any rallies will be met with redemptions.

Most importantly, all of our long-term weekly ‘sell signals’ have now been triggered. Such would suggest that a rally back to the ‘bullish trend line’ from 2009 will likely be the best opportunity to ‘sell’ before the ‘bear market’ finds its final low.”

Last week’s chart updated through Friday’s close.

While the recent lows may indeed turn out to be “the bottom,” I highly suspect they won’t. Given the sell signals have been registered at such high levels, the time, and distance, needed to reverse the excesses will require a deeper market draw.

As Jeff Hirsch from Stocktrader’s Alamanc noted:

“While we are all rooting for the market to find support here so much damage has been done. A great deal of uncertainty remains for the economy and health crisis. This looks like a bear market bounce.

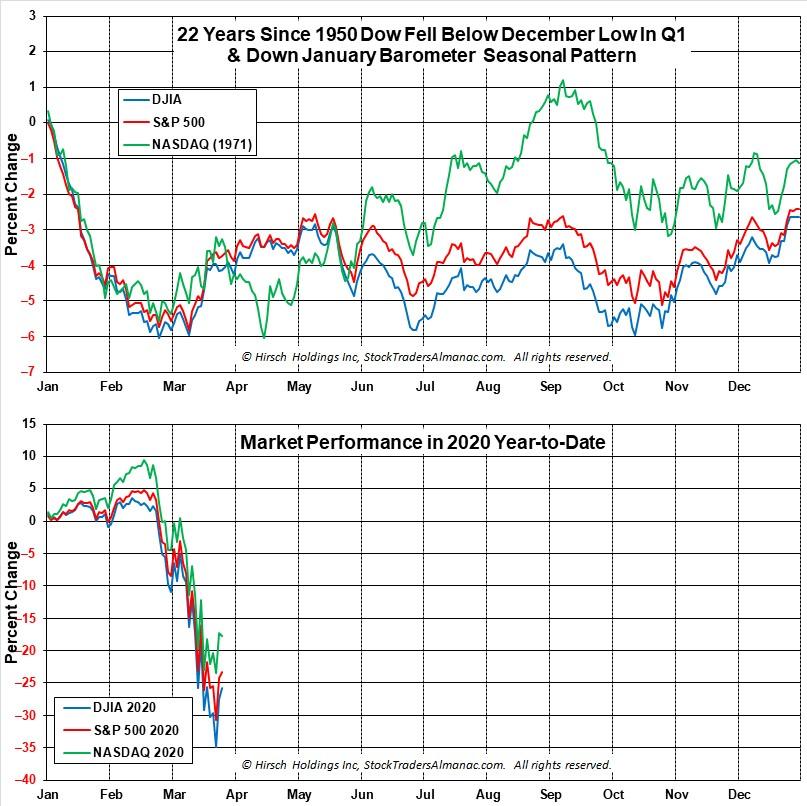

History suggests that we are in for some tough sledding in the market this year with quite a bit of chop. When the January Barometer came in with a negative reading, our outlook for 2020 began to diminish as every down January since 1950 has been followed by a new or continuing bear market, a 10% correction, or a flat year. Then another warning sign flashed when DJIA closed below its December closing low on February 26, 2020 as the impact of this novel coronavirus began to take its toll on Wall Street.

In the March Outlook, we presented this graph of the composite seasonal pattern for the 22 years since 1950 when both the January Barometer as measured by the S&P 500 were down, and the Dow closed below its previous December closing low in the first quarter. Below is a graph of DJIA, S&P 500 and NASDAQ Composite for 2020 year-to-date as of the close on March 25. Comparing 2020 market action to these 22 years, suggests a choppy year ahead with the potential for several tests of the recent low.”

“The depth of this waterfall decline may be too deep for the market to rebound quickly. This bear market also put this year’s Best Six Months (November-April) at risk of being negative. The record of down Best Six Months is not encouraging and it reminds us of a salient quote from the Almanac from an old market sage,

‘If the market does not rally, as it should during bullish seasonal periods, it is a sign that other forces are stronger and that when the seasonal period ends those forces will really have their say.’— Edson Gould (Stock market analyst, Findings & Forecasts, 1902-1987)’”

On a short-term basis, the market is also suggesting some risk. The daily chart below shows the market rallied to, and failed at, the first level of the Fibonacci retracement we outlined last week, suggesting profits be taken at this level. While there are two remaining targets for the bear market rally, the probabilities weigh heavily against them. (This doesn’t mean they can’t be achieved, it is “possible,” just not “probable.”)

Furthermore, with the “Death Cross” triggering on Friday (the 50-dma crossing below the 200-dma), this will put further downside pressure on any “bear market” advance from current levels.

Given the magnitude, and multiple confirmations, of these signals, it is far too soon to assume the “bear market” is over. This is particularly the case, given the sell-off is less than one-month-old.

Bear markets, and recessions, tend to last 18-months on average.

The current bear market and recession are not the results of just the “coronavirus” shock. It is the result of many simultaneous shocks from:

Economic disruption

Surging unemployment

Oil price shock

Collapsing consumer confidence, and

Most importantly, a “credit event.”

We likely have more to go before we can safely assume we have turned the corner.

In the meantime, use rallies to raise cash. Don’t worry about trying to “buy the bottom.”There will be plenty of time to see “THE” bottom is in, and having cash will allow you to “buy stocks” from the last of the “weak hands.”

Three percent of restaurants have already permanently closed due to the coronavirus crisis, according to research from the National Restaurant Association. Forty-four percent of operators have temporarily closed their restaurants, and 11% anticipate they will permanently close within 30 days.

Restaurant sales dropped 47% across the U.S. from March 1 to March 22, and 54% of operators now offer off-premise services only, according to an NRA survey of more than 4,000 restaurant operators.

Seventy percent of restaurants surveyed have had to lay off employees and reduce workers’ hours, and about half of restaurants expect further layoffs and hourly reductions in the next 30 days. More than 60% of restaurants have had to reduce their operating hours.

The association’s research spotlights just how gutting the coronavirus crisis has been for the restaurant industry — and many market experts worry the damage done so far is just the tip of the iceberg.

“This is uncharted territory,” Hudson Riehle, NRA SVP of research, said in a statement. “The industry has never experienced anything like this before.”

Eighty-eight percent of restaurant operators also reported that total sales volumes between March 1 and March 22 this year was lower than it was during the year-ago period, per NRA research.

The NRA requested more than $400 billion in financial relief, loans and insurance options for the industry from the government. On Wednesday, the Senate passed a $2 trillion stimulus package that included $350 billion in small business loans, $500 billion in loans for distressed companies and $250 billion in unemployment insurance benefits.

This safety net could help some restaurant operators keep their heads above water, but the question is, for how long?

And even though these loans will also offer forgivable debt if small- and medium-sized businesses continue to pay their employees, the stimulus package doesn’t address the NRA’s request of $100 billion in business interruption insurance.

Major restaurant chains have already suffered fatal blows to their businesses in just a few weeks time. Punch Bowl Social, the growing eatertainment chain looking to expand into hotels and cruises, now faces foreclosure. The Cheesecake Factory has furloughed 41,000 employees, CraftWorks has closed all of its restaurants and Union Square Hospitality Group has laid of 80% of its employees. If deep-pocketed brands with strong operations and decades of experience are folding under coronavirus pressure, the future is especially grim for independent restaurants — especially with Moody’s predicting restaurant sales could slip 20% over the next 12 months.

COVID-19 Outbreak Infects 66 At Maryland Nursing Home

While the nursing home in Kirkland, Washington, was the epicenter of the COVID-19 outbreak three weeks ago, the fast-spreading virus has turned its crosshairs onto the Northeast and Mid-Atlantic regions.

Virus cases and deaths are erupting in New York, New Jersey, Massachusetts, Pennsylvania, and Maryland.

The hardest-hit area is New York state, which has 53,399 confirmed cases and 827 deaths as of Saturday night (March 28). Reports are pouring in that hospital systems in the region are beyond capacity, and that is the point where the mortality rate could surge unless extra capacity is brought online to alleviate the lack of hospital beds and ICU-level treatment.

At the moment, New Jersey is the second hardest-hit area with 11,124 cases and 140 deaths, next is Massachusetts with 4,257 cases and 44 deaths, then Pennsylvania with 2,845 cases and 34 deaths, and last is Maryland with 995 cases and 10 deaths.

It appears the epicenter of the virus has shifted from West Coast to East Coast. Parts of the Northeast and Mid-Atlantic have densely packed metro areas with large senior populations, a dangerous combination that could lead to a further rise in cases and deaths.

With March coming to a close, the virus spread is shifting down East Coast. A new report, released by Maryland Gov. Larry Hogan on Saturday night revealed how a nursing home in the state has just confirmed 66 cases, resulting in 11 hospitalizations, reported CBS Baltimore.

.@GovLarryHogan confirmed a #CoronavirusOutbreak at the Pleasant View Nursing facility in Mt. Airy, Carroll County, MD. Hogan says 66 residents tested positive AND 11 are being hospitalized. We’re learning the facility has 104 beds/staff is being monitored. @fox5dcpic.twitter.com/wZifn6hAvL

Hogan said state and local officials are at the Pleasant View Nursing Home in Mount Airy, Maryland, located in Carroll County.

“Tonight, Maryland has experienced a tragic coronavirus outbreak at Pleasant View Nursing Home in Mount Airy. Multiple state agencies are on the scene and working closely with the local health department and the facility as they take urgent steps to protect additional residents and staff who may have been exposed.”

“As we have been warning for weeks, older Marylanders and those with underlying health conditions are more vulnerable and at a significantly higher risk of contracting this disease,” Hogan added.

The Carroll County Health Department published this memo to the public:

“Pleasant View Nursing Home continues to cooperate with and follow the guidance of the Maryland Department of Health and the Carroll County Health Department. We’re maintaining constant communication and will continue to provide resources and support to the patients, their families and facility staff during this difficult time.”

Elsewhere in the state, a fire station in Baltimore had to suspend operations after firefighters came in contact with an emergency medical services provider who tested positive for the virus.

The Maryland National Guard and Federal Emergency Management Agency (FEMA) have been setting up a large field hospital at the Baltimore Convention Center.

Here are a few photos of the medical surge site that Maryland is establishing at the Baltimore Convention Center as supplies arrive from @fema. Lots of partners from across state agencies; Feds; and private sector healthcare involved. pic.twitter.com/MSOTt3jZHq

Maryland National Guard is assembling a field hospital today including 250 beds at the Baltimore Convention Center. This is part of the effort to add thousands of hospital beds for #Covid_19pic.twitter.com/Hg4NX7H69A

MD National Guard humvees were seen in Baltimore, but the Guard says “there is not a threat of martial law…If you see a @MDNG Humvee on your street, know we are helping someone in need!” https://t.co/IayE27tzucpic.twitter.com/TVgUrSqgd5