More Evidence China Is Lying; Number Of Urns More Than Double Reported Coronavirus Deaths

China has been caught lying once again about coronavirus figures – with the latest evidence coming from ground-zero in Wuhan, where according to official CCP data just 50,006 people were infected with COVID-19, and 2,535 dying of the virus.

Yet, Chinese investigative outlet Caixin revealed that when mortuaries opened back up this week, photos revealed a far greater number of urns than reported deaths. In one, a truck loaded with 2,500 urns can be seen arriving to the Hankou Mortuary. According to the report, the driver said he had delivered the same amount the previous day.

In another photo, seven 500-urn stacks can be seen inside the mortuary, adding up to 3,500 deaths.

This adds up to more than double the amount of reported deaths in the region – for which grievingfamily members waited in line for as long as five hours to collect, according to Shanghaiist.

Urns are reportedly being distributed at a rate of 500 a day at the mortuary until the Tomb Sweeping Day holiday, which falls on April 4 this year.

Wuhan has seven other mortuaries. If they are all sticking to the same schedule, this adds up to more than 40,000 urns being distributed in the city over the next 10 days.

When reporters at Bloomberg made calls to the funeral homes to check on the number of urns waiting to be collected, the mortuaries said that they either did not have that data or were not authorized to disclose it. –Shanghaiist

Given the constant, provable lies, does anyone believe that China has actually contained COVID-19?

And of course, as former White House press secretary Sean Spicer pointed out implicitly, don’t expect the mainstream media to question anything…

Reminder to all of the journalists that took China at face value when they claimed they had no more cases https://t.co/mlS0t9HvRo

As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.

Amusingly, a few days ago yet another article appeared explaining how the Money Multiplier works. The example goes like this: Someone deposits $10,000 and a bank lends out $9,000 and then the $9,000 gets redeposited and 90% of the gets lent out and so an and so forth.

The notion was potty. That is not remotely close to how loans get made. Deposits and reserves never played into lending decisions.

What’s Changed Regarding Lending?

Essentially, nothing.

The announcement just officially admitted the denominator on reserves for lending is zero.

There are no reserve lending constraints (but practically speaking, there never were).

The flashback is amusing as I reference a number of people worried about hyperinflation.

Here are the facts of the matter as I explained in 2009.

Money Multiplier Theory Is Wrong

Lending comes first and what little reserves there are (if any) come later.

There really are no excess reserves.

Not only are there no excess reserves, there are essentially no reserves to speak of at all.

The rationale behind the last bullet point pertains to banks hiding losses. Regulators suspended mark-to-market accounting.

When Do Banks Make Loans?

They meet capital requirements

They believe they have a creditworthy borrower

Creditworthy borrowers want to borrow

All three requirements must be met.

Banks generally do not lend if they are capital impaired.

Clearly someone must want to borrow.

Point two is worthy of discussion.

Banks may not have a creditworthy borrower, they just have to believe it, or they have an alternate belief that applies. In 2007 banks knew full well they were making mortgage liar loans.

So Why Did They?

Because banks bought into the idea home prices would not go down so they did not give a rat’s ass if someone was out on the street. All they cared about was the quality of the loan. If Home prices appreciated, they were covered.

From a bank lending aspect, nothing has changed. Neither reserves nor deposits never entered into the picture.

Denominator Officially Zero

The denominator on lending is now officially zero. But nothing really changed. The Fed was always ready, willing, and able to supply unlimited reserves.

The only thing that’s new is the official announcement that reserves are fictional.

Capital Concerns in 2009

There are capital concerns, but note that in March of 2009 the Fed suspended mark-to-mark accounting.

That was the key announcement that launched the bull market.

Capital Concerns Now

There are still capital concerns, but the Fed stepped up to the plate and is willing to buy corporate bonds.

Guess who is going to unload as much questionable junk as possible and guess who will buy it.

Banks know they have losses but hey will not admit them.

All it takes to mask them is a clever swap takes the assets off the balance sheet of the banks and temporarily hides them on the balance sheet of the Fed.

What About New Lending?

Hiding junk is not new lending. It is not new production. And it is not new hiring.

To achieve real growth we need new production, not hiding of losses.

Losses and Zombies

Once again, the Fed has chosen to hide losses and shelter zombie corporations.

This will be a drag on any recovery.

All Excess Now

Hey, look on the bright side.

By definition, all reserves are now excess reserves. Banks can collect on all reserves.

The rate may not be much, but Interest on Excess Reserves = Interest on Reserves

See here, which lists “[w]orkers supporting the operation of firearm or ammunition product manufacturers, retailers, importers, distributors, and shooting ranges,” but prefaces all the categories (not just the gun-related ones) with:

This list is advisory in nature. It is not, nor should it be considered, a federal directive or standard. Additionally, this advisory list is not intended to be the exclusive list of critical infrastructure sectors, workers, and functions that should continue during the COVID-19 response across all jurisdictions. Individual jurisdictions should add or subtract essential workforce categories based on their own requirements and discretion.

The Free Beacon (Stephen Gutowski) notes that, several days ago, N.J. Attorney General Gurbir Grewal defended including gun stores in the N.J. lockdown by saying,

[T]he Governor’s executive order tracks every other executive order that has a stay at home provision and none of those—none of those—contain an exemption for firearm stores, nor does the federal guidance from Homeland Security contain that type of exemption when it comes to essential facilities and nonessential facilities. So, we’re consistent with every other executive order that calls for stay at home. We’re consistent with federal guidelines and we’ll defend the Governor’s executive order in court.

from Latest – Reason.com https://ift.tt/2UIHT3V

via IFTTT

Rosneft Abruptly Exits Venezuela, Sells Assets To Russian State, Amid US Squeeze On Maduro

In the past weeks the Kremlin has shown it’s willing to punch back as well as take drastic necessary defensive action in the face of Washington sanctions at a moment America is preoccupied and made more vulnerable by the coronavirus threat — first by dumping OPEC+ and MbS, effectively declaring war on US shale— and now by taking aggressive measures to insulate Russia’s state-controlled Rosneft.

On Saturday Rosneft announced it has sold off all its Venezuelan oil assets to an unnamed Russian state entity. “The government of the Russian Federation has acquired assets in Venezuela from Rosneft. A company 100% owned by the Russian Federation has become the owner,” Russia’s TASS said.

A company statement framed the move as key to protecting shareholders’ interests at a moment the Trump administration ramps up pressure on Maduro and external entities still doing business with Caracas. It’s been widely reported that Rosneft has explored exit options since early 2019 when Venezuelan assets continued rapidly losing money, leading to worsened current operating conditions.

Venezuelan President Nicolas Maduro holds a sword given as gift by Russian oil company Rosneft’s CEO, Igor Sechin. File image: AFP via Getty

“As a result of the concluded agreement all assets and trading operations of Rosneft in Venezuela and/or connected with Venezuela will be disposed of, terminated or liquidated,” Rosneft said. “We took this decision in the interests of our shareholders, as a publicly traded international company,” Rosneft spokesman Mikhail Leontyev further told TASS. “And we have a right to expect, indeed, that the US regulators fulfill their public promises.”

On Thursday the White House went so far as to issue a $15 million bounty on Maduro and his inner circle over drug trafficking charges, amid sweeping indictments against what Washington dubbed a vast narco-state criminal enterprise orchestrated by the regime. It appears Rosneft took note of Trump’s willingness to press his economic war on Venezuela further even as the United States now leads the world in numbers of confirmed coronavirus cases, which threatens to decimate an economy still on “pause” and extreme uncertainty still on the horizon.

All of this follows in mid-February the US slapping new sanctions on Rosneft Trading SA, a unit of Rosneft, and the company’s executive Didier Casimiro, accusing it of being the “primary culprit” of a campaign to evade Washington’s pressure campaign on the Maduro government. But the sanctions stopped just short of naming parent company Rosneft, though the Trump administration long accused it of“actively evading sanctions — engaging in ruses, engaging in deception.”

Via AFP/Getty

Bloomberg observed that “The fight over Venezuela fits into a much larger geopolitical battle between Trump and Vladimir Putin, with both turning to oil as the weapon of choice.” And the report further cited Russia’s ambassador to Venezuela, Sergey Melik-Magdasarov, as saying:

“Don’t worry! This is about Rosneft’s assets being transferred to Russia’s government directly. We keep moving forward together!,” he [Amb. Melik-Magdasarov] said, in a message that also posted on the embassy website.

The assets include Rosneft’s stakes in local upstream companies Petromonagas, Petroperija, Boqueron, Petromiranda and Petrovictoria, as well as oil-service, commercial and trading units.

The Russian Federation controls Rosneft with just over 50% of its shares, while BP Plc is the second-largest shareholder with 19.75%, and Qatar’s QH Oil Investments owns 18.93%.

Rosneft’s position has long been that US sanctions are illegal and that its own operations in Venezuela are commercial in nature, not political, after in prior months the company’s cooperation with state-run PDVSA became an “open secret”.

The ultimate strategy behind Saturday’s dramatic announcement is as yet uncertain, it should be noted:

But Russ Dallen, head of Caracas Capital Markets brokerage, cautioned that it’s too early to know for sure whether the move is intended to bolster Maduro.

“We don’t know whether the new state entity is a cemetery corporation, where companies go to die, or whether the Russians are simply doing it to take Rosneft — which is their crown jewel and provides a large portion of Russia’s income — out of the way of sanctions and Putin will use the new company to continue to help Maduro,” he said.

Rosneft has emerged as one of PDVSA’s closest joint venture partners, being crucial as a heavy lifter keeping Venezuelan oil afloat at a moment Washington tries to strangle and blockade the socialist state’s industry.

What spectacular timing. Like a shot ricocheting at Heaven’s Door as a virus pandemic rages and Planet Lockdown is the new normal, Bob Dylan has produced a stunning 17-minute masterpiece dissecting the November 22, 1963, assassination of JFK – releasing it at midnight US Eastern Standard Time on Thursday.

For baby boomers, not to mention obsessive Dylanologists, this is the ultimate sucker punch. Countless eyes will be plunged into swimming pools revisiting all the memories swirling around “the day they blew out the brains of the king / Thousands were watching, no one saw a thing.” But that’s not all: the Dylanmobile takes us on a magical mystery tour of the 60s and 70s, complete with the Beatles, the Age of Aquarius and the Who’s “Tommy.”

If there’s any cultural artifact capable of sending a powerful jolt across a discombobulated America trying to come to grips with a dystopic Desolation Row, this is it, the work of America’s undisputed, true Exceptionalist. The times, they are-a-changin’. Oh, yes, they are.

There are so many nuggets in Dylan’s lyrics they would be worthy of a treatise, tracking the vortex of music, literature, film references and interlocking Americana.

This is essentially an incantatory mantra set to piano, sparse percussion and violin. We have two narrators: a dying Kennedy (“Ridin’ in the backseat next to my wife / Headin’ straight on in to the afterlife / I’m leanin’ to the left, got my head in her lap / Oh Lord, I’ve been led into some kind of a trap”) and Dylan himself.

Or this can be read as Dylan playing Kennedy’s doppelganger, plus occasional interventions, such as Kennedy’s would-be killers

(“Then they blew off his head while he was still in the car / Shot down like a dog in broad daylight / Was a matter of timin’ and the timin’ was right / You got unpaid debts we’ve come to collect / We gonna kill you with hatred, without any respect / We’ll mock you and shock you and we’ll grin in your face / We’ve already got someone here to take your place”).

The pearl at the heart of the mantra is nothing sort of apocalyptic:

“They killed him once and they killed him twice / Killed him like a human sacrifice / The day that they killed him someone said to me, / ‘Son, The Age of the Antichrist has just only begun.’”

Extra words to define it would be idle. Wherever you are in Planet Lockdown, sit back in stay at home social distancing mode, turn on, tune in and time travel. There will be blood on the tracks.

Joe Biden: “Believe All Women” (Except The One Accusing Me Of Sexual Assault)

In September, 2018 – former Vice President Joe Biden weighed in on allegations of sexual assault against Justice Brett Kavanaugh by insisting that any woman’s public claims of sexual assault should be presumed to be true.

Except for Biden’s former Senate staffer, Tara Reade, who says Biden penetrated her with his fingers in 1993 when she was in her mid-20s, making her life “hell.”

Biden’s deputy campaign manager magically transformed “believe all women” into “all women have a right to tell their story” on Friday, saying in a statement to Fox News: “Women have a right to tell their story, and reporters have an obligation to rigorously vet those claims. We encourage them to do so, because these accusations are false.“

If you believed Kavanaugh’s accuser, why in the world would you not believe Biden’s? Believing women doesn’t end when it starts to impact your politics.

— The Gravel Institute (@GravelInstitute) March 27, 2020

Remember when Benjamin Wittes said, “Kavanaugh himself bears the burden of proof.” Does the same apply for Biden? https://t.co/Qb53NAJI3g

As we noted last week, Reade said in an interview with Rolling Stone‘s Katie Halper that Biden sexually assaulted her after she was asked to run a gym bag over to him.

Biden’s “hands were on me and underneath my clothes,” she said, after he “had me up against the wall.”

“I remember him saying first, like as he was doing it, ‘Do you want to go somewhere else,'” she said, adding “And then him saying to me when I pulled away, he got finished doing what he was doing, and I kind of just pulled back and he said, ‘Come on man, I heard you liked me.’ And that phrase stayed with me because I kept thinking what I might’ve said and I can’t remember exactly if he said ‘i thought’ or ‘I heard’ but he implied that I had done this.”

Reade then went on to say that “everything shattered in that moment” because she knew that there were no witnesses and she looked up to him. “He was like my father’s age,” she said. “He was like this champion of women’s rights in my eyes and I couldn’t believe it was happening. It seemed surreal.”

Reade then said Biden grabbed her by the shoulders and said, “You’re okay. You’re fine” and proceeded to walk away.

Reade said that Biden also told her something after the alleged assault that she initially didn’t want to share because “it’s the thing that stays in my head over and over.” But after some pressing from Halper, Reade decided to share:

“He took his finger. He just like pointed at me and said you’re nothing to me.”

Halper said she spoke with Reade’s brother and close friend, and both of them recall Reade telling them about the alleged assault at the time. –NewsOne

Reade says that after she revealed some of Biden’s inappropriate behavior, she was accused of doing the bidding of Vladimir Putin, according to The Intercept.

Early this week, we were among the first to report on the “break down” in precious metals markets.

While the demand for gold has been soaring as a safe haven asset amid the multiple global crises we are currently facing, forced paper gold liquidation (as leveraged funds scramble to cover margin calls) and unprecedented logistical disruptions created a frantic hunt for actual bars of gold.

Specifically, as Bloomberg details, at the center of it all are a small band of traders who for years had cashed in on what had always been a sure-fire bet: shorting gold futures in New York against being long physical gold in London. Usually, they’d ride the trade out till the end of the contract when they’d have a couple of options to get out without marking much, if any, loss.

But the virus, and the global economic collapse that it’s sparking, have created such extreme price distortions that those easy-exit options disappeared on them. Which means that they suddenly faced the threat of having to deliver actual gold bars to the buyers of the contract upon maturity.

It’s at this point that things get really bad for the short-sellers.

To make good on maturing contracts, they’d have to move actual gold from various locations. But with the virus shutting down air travel across the globe, procuring a flight to transport the metal became nearly impossible.

If they somehow managed to get a flight, there was another major problem. Futures contracts in New York are based on 100-ounce bullion bars. The gold that’s rushed in from abroad is almost always a different size.

The short-seller needs to pay a refiner to re-melt the gold and re-pour it into the required bar shape in order for it to be delivered to the contract buyer. But once again, the virus intervenes: Several refiners, including three of the world’s biggest in Switzerland, have shut down operations.

“I realized it was going to be an extremely volatile day,” Tai Wong, the head of metals derivatives trading at BMO Capital Markets in New York, said of Tuesday. “We watched this panic develop literally over the course of 12 hours. Having seen enough market dislocations, you recognize that the frenzy wasn’t likely to last, but at the same time you also don’t know how long it would extend.”

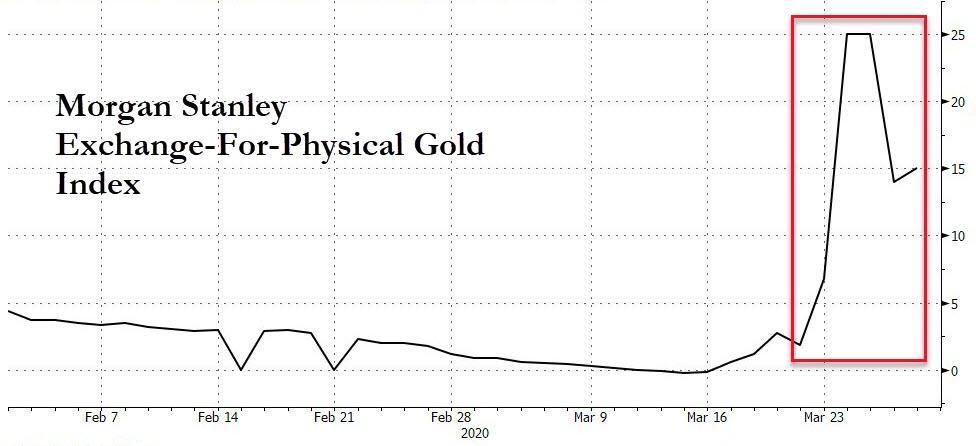

By the end of the week, the shorts had sourced the metal and chartered flights, reverting the spot-futures spread…

But Morgan Stanley’s Exchange-For-Physical Index shows a large physical premium remains…

“There’s no gold,” says Josh Strauss, partner at money manager Pekin Hardy Strauss in Chicago (and a bullion fan).

“There’s no gold. There’s roughly a 10% premium to purchase physical gold for delivery. Usually it’s like 2%. I can buy a one ounce American Eagle for $1,800,” said Josh Strauss. “$1,800!”

“The case for gold is simple,” says Strauss.

“You want to own gold in times of financial dislocation and or inflation. And that’s been the case since time immemorial. And gold behaves well in those cases. In those cases stocks behave poorly. It’s a great portfolio hedge. Gold does poorly when you’ve got strong economic growth and low inflation. Tell me when that’s going to happen. Gold held its value during 2008 and after all that money printing it tripled over the next three years.”

And in case you doubted this, the cost of an American Eagle one ounce coin at the US Mint is now $2,175…

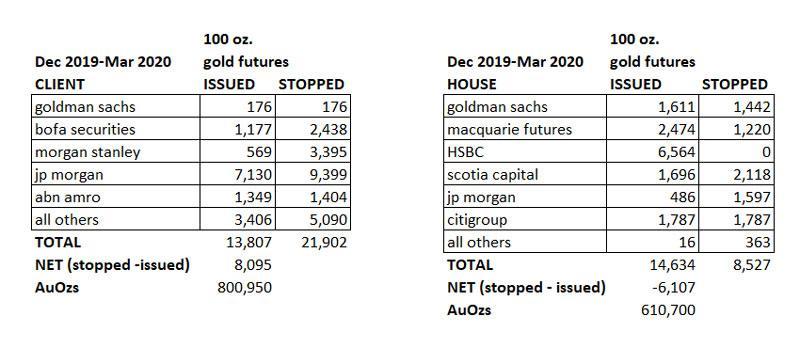

But now we can see more details of what is behind this ‘shortage’ as SKWealthAcamdemy’s J.Kim details, the latest COMEX Issues and Stops reports expose conditions behind the COMEX physical gold supply problems. Though I have written about the various reasons why physical gold supply problems manifest many times in the past, this topic still remains one rarely discussed by financial journalists, and never discussed by the mass financial media.

For client accounts, when bullion banks stop more notices than issued, they, will lose physical inventory.

For house accounts, the opposite is true.

When bullion banks issue more notices than stops, then they will lose physical inventory as well. Normally, when bullion banks manufacture waterfall declines in paper gold and silver prices, as they did earlier this month, with the complicity of the CME’s largely unreported rampage in raising initial and maintenance margins on futures contracts many times within a 2-month period in the midst of a stock market crash, they load up on physical gold and silver for their house accounts while ensuring that their clients take almost zero delivery of physical gold and silver ounces. However, if they are unable to execute this clever strategy, this is when physical gold supply problems can manifest.

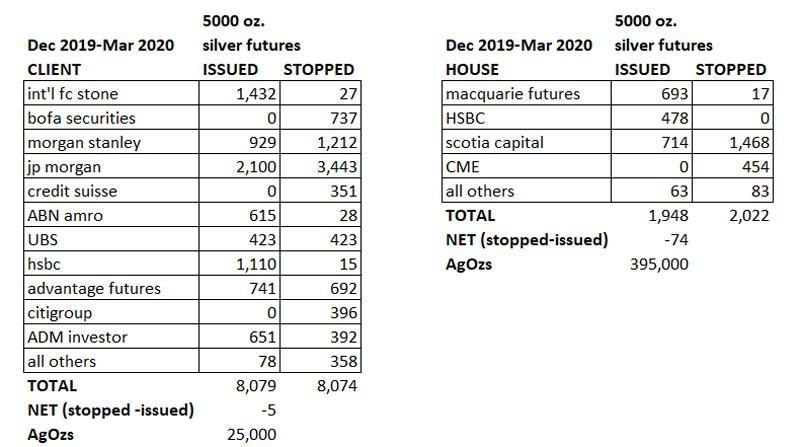

In fact, I have not seen a single news site in the entire world, except for my own, mention the relentless increase in initial and maintenance margins in gold and silver futures contracts (the 100-oz gold futures contract and the 5000-oz silver futures contract) for the past two months, in a desperate attempt to knock long positions out of the game and thereby prevent an increasing amount of physical delivery requests.

Just recently, the CME raised margins yet again for 100-oz gold futures contracts to $9,185/$8,350 for initial/maintenance margins, representing a massive 86% increase in margins, and for 5000-oz silver futures contracts to $9.900/$9,000 for initial/maintenance margins, representing a gigantic 73% increase in margins, in just a couple months’ time. Normally, such relentless increases in initial/maintenance margins in gold futures markets is sufficient to prevent physical gold supply problems from afflicting futures markets, but the fact that even this reliable manipulation mechanism failed recently is a sign of additional tectonic earthquakes to come in the global financial system.

However, as you can see for the data I have compiled for the behavior of issues and stops for client and house accounts for bullion banks in gold and silver from December 2019 to March 2020, this pattern of normal behavior, in which bullion banks take advantage of their own artificially manufactured paper gold and silver price plunges to load up on physical metals at the expense of their clients, has strongly reversed during this four-month time span. I have only included data for the major gold (100-oz) and silver (5000-oz) futures contracts below and not for the mini gold (10-oz) and mini silver (1000-oz) silver futures contracts.

Furthermore, I only separated out the bullion banks by name that had several hundred to a few thousand contracts stopped or issued, and compiled all other data under the category of “all others”. For those of you that don’t understand the terminology “stopped” and “issued”, the categories refer to the number of delivery notices that were “issued” (short positions issuing notification that underlying gold/silver would be delivered) and “stopped” (long positions receiving a delivery notice).

Therefore, when delivery notices are “issued” in house accounts, the issuing bank is on the hook for delivering the physical ounces associated with the underlying contracts. On the contrary, when notices are “stopped”, then the stopping bank would receive notification of the future delivery of the physical ounces associated with the underlying contracts. The same holds true for client accounts. Thus, all bullion banks desire more stopped than issued notices for their house accounts, and desire more issued versus stopped notices for their client accounts. This way they accumulate more physical inventory during artificially engineered paper price crashes.

As you can see, the massive engineered drop in paper silver prices versus the massively higher physical silver prices for the past month backfired on the bullion banks, as it led to a frenzy of clients asking for physical delivery, whereas in the past, bankers had been able to chase client long positions out of the market without ever being on the hook for physical delivery. Thus the amount of contracts stopped versus issued for clients was nearly break even for silver futures contracts, a pattern I have not witnessed in a long time during a banker raid on paper silver prices. And in regard to house accounts, under past similar circumstances, I had always observed JP Morgan bankers taking a tremendous amount of physical silver delivery during engineered collapses in paper silver prices. However, during the last four months, this situation did not materialize, perhaps due to the stress on physical stores of silver created by so many clients asking for physical delivery. As you can see in the data I complied above, this time around, JP Morgan bankers were nearly absent in taking physical silver delivery for their house account. In fact, for the bullion bank house accounts, the amount of stopped versus issued contracts, net, was only 74 contracts, or a mere 395,000 AgOzs for their House accounts. As a basis of comparison, during similarly engineered collapses in paper silver prices in the past, JP Morgan alone was able to accumulate and take delivery of many millions of physical silver ounces.

In regard to real physical gold delivery, the situation was even worse for bullion bankers than their situation with real physical silver delivery, which likely has given rise to physical gold supply problems at the current time. In their client accounts, physical delivery requests exploded, with the net (stopped minus issued) totaling 8,095 contracts representing 800,950 AgOzs of real physical gold requested for delivery. In their house accounts, the bullion banks were unable to yield a positive net situation either, with issued contracts exceeding stopped contracts by 6,107 contracts, representing 610,700 AgOzs. Thus, when adding these two figures together, the bullion banks are on the hook for delivering more than 1.4M AgOzs.

This unexpected demand on bullion bank physical gold reserves has undoubtedly led to a disruption of physical gold delivery associated with the gold futures markets, though various COMEX spokespeople have claimed there is no shortage of physical gold whatsoever, and that the disruption of delivery is simply due to a disruption in the supply chain caused by the coronavirus pandemic, i.e., when in doubt, blame the coronavirus pandemic for all manifested stresses revealed in the global financial system. Earlier, here, on 24 February, I speculated, well before US stock markets started to crash, that the coronavirus pandemic would be scapegoated for the market crash, and I was 100% right. Is it possible that the coronavirus pandemic is now being scapegoated for shortages of physical gold as well?

Oddly, a gold analyst, Ole Hanson stated in response to the shortages of gold physical supply in the futures markets: “There is plenty of gold in the market, but it’s not in the right places. Nobody can deliver the gold because we are forced to stay home.” The explicit function of COMEX warehouses is to store the physical gold that backs gold delivery associated with gold futures contracts. Consequently, why is the physical gold “not in the right places” and in these warehouses, as if it is stored where it is supposed to be stored, and the data is accurate (1.76M registered AuOzs and an additional 6.98M eligible AuOzs in COMEX warehouses as of 26 March 2020), there should be no physical gold shortages to meet physical demand right now? Did Mr. Hanson, in his statement that gold is “not in the right places” unwittingly reveal that the reported COMEX warehouse data is fraudulent?

Secondly, some would suggest that ever since the COMEX mandate that paper gold could be used to close out physical delivery requests through EFP (Exchange For Physical) transactions by Exchange Rule 104.36 enacted on February 18, 2005, which allowed for the substitution of gold ETFs for physical gold, that no physical shortage of gold could ever result.

Since paper was allowed to replace physical, could not bullion banks just literally “paper over” any physical supply deficit? And if the answer to this question is yes, then why is the COMEX experiencing physical shortages of gold right now? Well, as I explained in an article that I published on my news site in June 2011, in which I explained how EFP transactions operate (which you can read here), “the Related Position [Physical] must have a high degree of price correlation to the underlying of the Futures transaction so that the Futures transaction would serve as an appropriate hedge for the Related Position [Physical].” Consequently, since there has been a massive price decoupling between physical and paper gold prices, perhaps this price decoupling has enabled the underlying holder of longs in gold that asked for physical delivery to reject any EFP transaction, since there is no longer a “high degree of price correlation” between paper and physical gold, and to insist on physical gold delivery with no substitution for this request. And this rejection of EFPs and EFS (exchange for swaps) as acceptable behavior is perhaps what is causing the physical gold supply problems in the futures markets right now.

See here, which lists “[w]orkers supporting the operation of firearm or ammunition product manufacturers, retailers, importers, distributors, and shooting ranges,” but prefaces all the categories (not just the gun-related ones) with:

This list is advisory in nature. It is not, nor should it be considered, a federal directive or standard. Additionally, this advisory list is not intended to be the exclusive list of critical infrastructure sectors, workers, and functions that should continue during the COVID-19 response across all jurisdictions. Individual jurisdictions should add or subtract essential workforce categories based on their own requirements and discretion.

[T]he Governor’s executive order tracks every other executive order that has a stay at home provision and none of those—none of those—contain an exemption for firearm stores, nor does the federal guidance from Homeland Security contain that type of exemption when it comes to essential facilities and nonessential facilities. So, we’re consistent with every other executive order that calls for stay at home. We’re consistent with federal guidelines and we’ll defend the Governor’s executive order in court.

from Latest – Reason.com https://ift.tt/2UIHT3V

via IFTTT

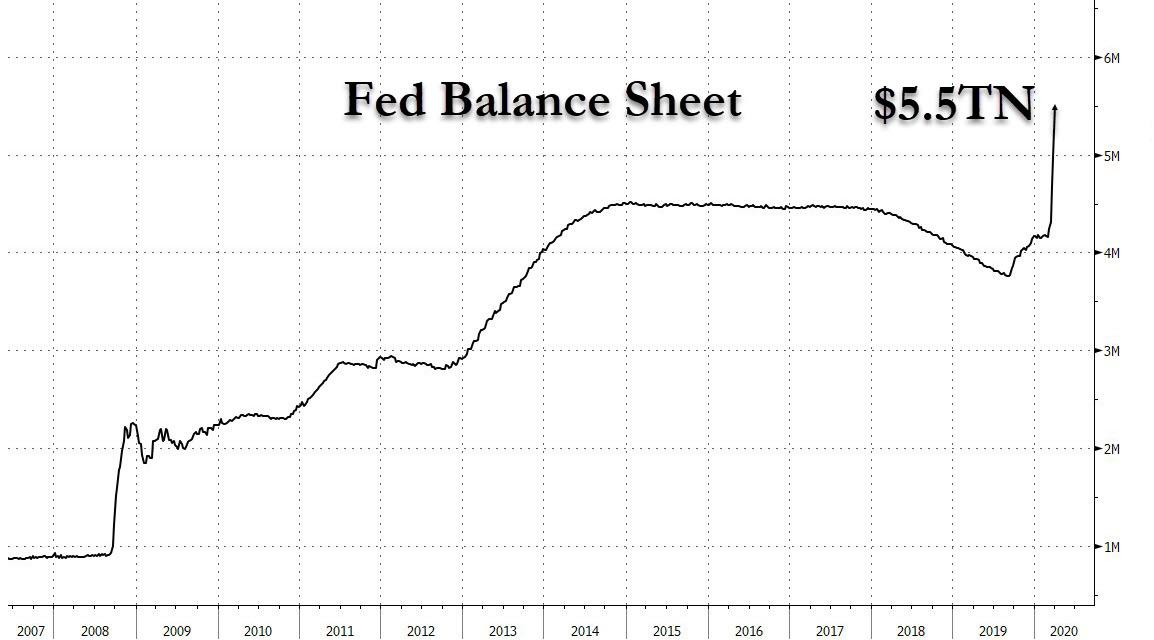

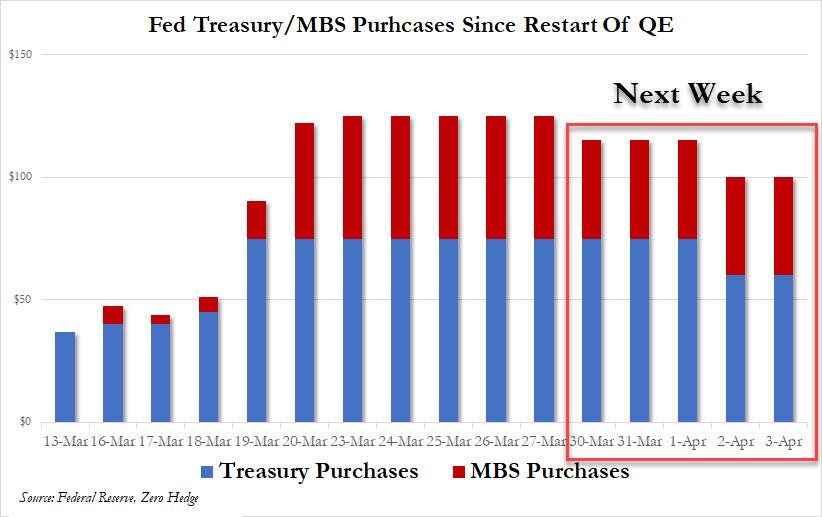

$9,000,000,000,000: Former Fed Strategist Now Expects Fed’s Balance Sheet To Double This Year

Late on Thursday, we calculated that as of the end of this turbulent week, the Fed will have added a record $625 billion to its balance sheet, bringing the total to $5.5 trillion, an increase of $1.3 trillion in two weeks (6% of GDP), which was the amount the Fed monetized during all of QE1 in response to the financial crisis, but which took place over a period of almost 2 years.

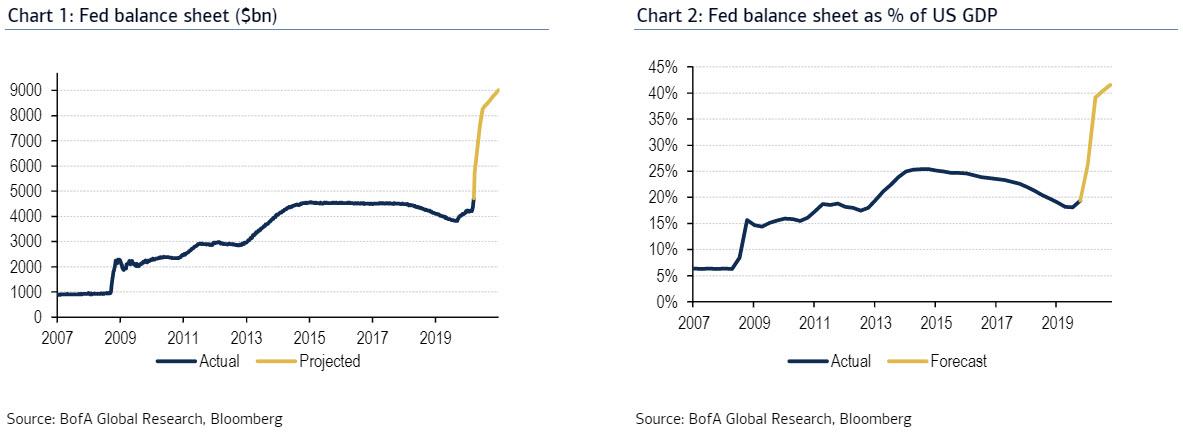

That’s just the start of what will soon become the most aggressive expansion in Fed balance sheet history because according to BofA’s Fed guru Mark Cabana, who was a former officer in the New York Fed’s Markets Group, the Fed’s balance sheet is now set to double to $9 trillion by the end of the year, to wit:

We acknowledge there is elevated uncertainty around the outlook for the balance sheet, but anticipate it will approximately double in size from end ’19 to end ’20.

The estimates for the Fed’s balance sheet “after unlimited QE and new programs” currently imply that between end ’19 & end ’20:

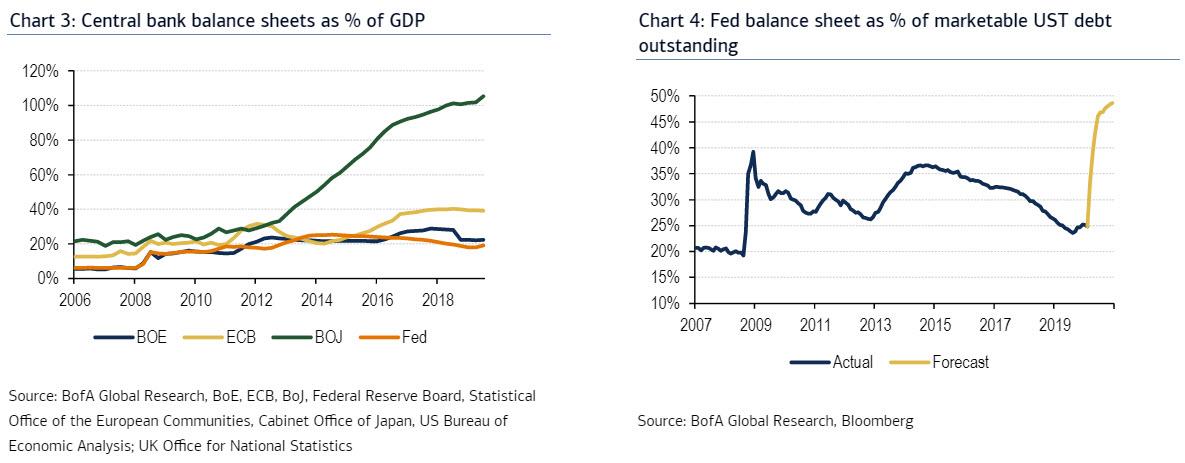

Fed balance sheet to US GDP will rise from 20% to 40%, in the process unleashing an unprecedented liquidity tsunami that will send asset prices soaring once the pandemic is over yet the Fed refuses to shrink its balance sheet (Chart 2)

Fed UST as percentage of marketable debt will rise from 20% to 50%, in other words the Fed will now monetize all US Treasury issuance and then some (Chart 4)

Fed UST holdings will increase by $1.8tn and agency MBS by $700+bn

Reserves will increase three- to four-fold

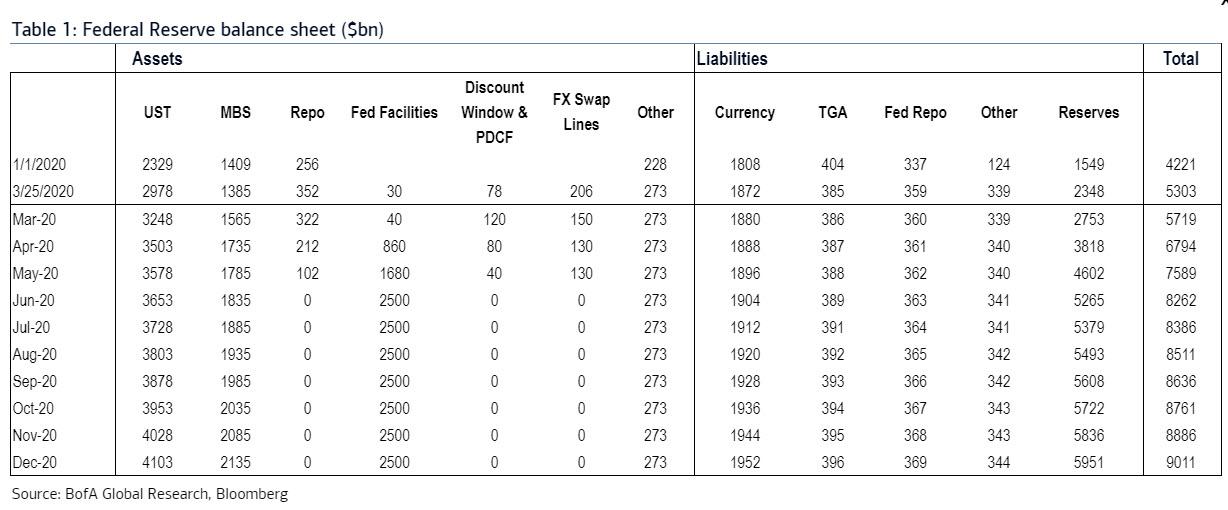

All of the above in table format:

To arrive at these estimates, Cabana make the following assumptions about Fed purchases and use of the Fed’s facilities:

UST and MBS purchases: expect two phases:

(1) initial bazooka to support market functioning. The Fed has purchased $75bn/day of USTs and $50bn/day of MBS. Through next week Cabana anticipates an average of $60bn/day of USTs and $40bn/day of MBS, which is fascinating because Cabana published this report in the early morning hours of Friday, and just a few hours later the Fed announced that it would follow precisely this schedule, tapering TSY QE from $75BN to $60BN and MBS from $50BN to $40, which announcement sent stocks sharply lower in the last 30 minutes of trading on Friday.

(2) standard QE from April through December with $75bn/month of USTs and $50bn/month of MBS; this would help with the glut of upcoming UST supply.

Fed facilities – The Fed has announced five facilities: CPFF, MMLF, PMCCF, SMCCF and TALF. Treasury made an initial investment of $10bn in these facilities, which can be 10x levered. Congress is set to allocate another $454bn to the Fed facilities, which can be 10x levered. This implies the max size of these facilities is roughly $5tn, and BofA anticipates 50% takeup spread across three months. In ’08, TALF saw 35% takeup, so assume about 1.5x takeup of facilities now vs ’08 levels.

Discount window and PDFC – Assume discount window and PDCF use peaks at around $120bn in the near term then gradually declines.

FX swap lines – Assume FX swap line use peaks around $200bn, and current 84 day operations roll off in June.

While the former NY Fed staffer acknowledges that there is an elevated uncertainty around these estimates, he sees the risks to his estimates “as skewed to the high side.”

In short, once you start helicopter money you never stop.

* * *

Finally, what are the market implications from the Fed going full BOJ. There are three, as the Fed’s launch of helicopter money in conjunction with the treasury should support:

liquidity – the sharp reserve increase will allow for funding markets to operate in state of abundant liquidity

low long-term US rates – As even Cabana admits, “the Fed’s large holdings of US Treasuries will amount to COVID-19 stimulus debt monetization and support low longer-term UST yields”, in short after 11 years of debate whether the Fed is or isn’t monetizing debt, we finally have a clear answer and guess what, the tinfoil conspiracy blog won.

Corporate bonds (i.e. LQD) will benefit from Fed credit programs.

One final point: buy physical gold, lots of it (pay whatever premium over spot is asked), because the real purpose behind the Fed’s helicopter money which miraculously came at the “right” time – just as the economy was about to tailspin into a recession even without covid-19- courtesy of a virus which prompted a coordinated global reset and the launch of helicopter money, will allow the Fed to commence the endgame of fiat currencies. In the process, the Fed will inject $4.5 trillion into capital markets which will eventually trickle down to the economy.

The endgame is simple: an initial deflationary bust followed by hyperinflation, first in asset markets and soon after, as the Fed triples down on helicopter money until it eventually buys gold outright in the final dollar devaluation, everywhere else.

Being an analyst of Credit and Bubbles over the past few decades has come with its share of challenges. Greater challenges await. I expect to dedicate the rest of my life to defending Capitalism. One of the great tragedies from the failure of this multi-decade monetary experiment will be the loss of faith in free market Capitalism – along with our institutions more generally.

Somehow, we must convince younger generations that the culprit was unsound finance.

And it’s absolutely fixable.

Deeply flawed, experimental central banking was fundamental to dysfunctional markets and resulting deep financial and economic structural impairment. The Scourge of Inflationism. If we just start learning from mistakes, we can get this ship headed in the right direction.

Over the years, I’ve argued for “rules-based” central banking that would sharply limit the Federal Reserve’s role both in the markets and real economy. The flaw in “discretionary” central banking was identified generations ago: One mistake leads invariably to only bigger blunders.

What commenced with Alan Greenspan’s market-supporting assurances of liquidity and asymmetric rate policy this week took a dreadful turn for the worse: Open-end QE, PMCCF, SMCCF, MMLF, CPFF, MSBLP, TALF… They’re going to run short of acronyms. Our central bank has taken the plunge into buying corporate bond ETFs, with equities ETFs surely not far behind. The Fed’s balance sheet expanded $586 billion – in a single week ($1.1 TN in four weeks!) – to a record $5.25 TN. Talk has the Fed’s new “Main Street Business Lending Program” leveraging $400 billion of (this week’s $2.2 TN) fiscal stimulus into a $4.0 TN lending operation. Having years back unwaveringly set forth, the ride down the slippery slope of inflationism has reached warp speed careening blindly toward a brick wall.

…

The Fed “very alert about financial risk”? What exactly has the Fed been “looking at at much more detail”? Financial excess? Speculative leveraging? Mounting vulnerabilities in the derivatives complex, the ETF universe, corporate leverage? Global hedge fund leverage? Highly levered mortgage companies? We’ve now witnessed two historic bouts of market illiquidity and dislocation – exposing massive speculative leveraging – and Dr. Bernanke sticks resolutely with his “global savings glut” thesis. Central banks have during this cycle created more than $16 TN of new “money,” for heaven’s sake. Of course it’s been “a monetary policy thing.”

I’ve always viewed Bernanke as a decent man. But as a central banker – as the mastermind for the terminal phase of a runaway global monetary experiment – he’s been a disaster. His analytical framework is so flawed it’s difficult to comprehend the amount of power and discretion placed in his hands. It was Bernanke that invoked the government printing press to resolve whatever might ail the markets or economy. His crackpot theories that the Fed’s failure to print sufficient money supply after the ’29 stock market crash caused the Great Depression should have been sternly rebuked years ago. Worst of all, Dr. Bernanke specifically used the risk markets (stocks, corporate Credit, derivatives and such) as the primary mechanism for post-Bubble system reflation. The former Fed chief is the father of “QE,” “helicopter money,” and the ETF complex that took the world by storm.

Documenting for posterity the ever-lengthening list of lending facilities, this week from the Federal Reserve:

“The Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.”

“The SMCCF will purchase in the secondary market corporate bonds issued by investment grade U.S. companies and U.S.-listed exchange-traded funds whose investment objective is to provide broad exposure to the market for U.S. investment grade corporate bonds.”

“The Money Market Mutual Fund Liquidity Facility (MMLF) to include a wider range of securities, including municipal variable rate demand notes (VRDNs) and bank certificates of deposit.”

“Facilitating the flow of credit to municipalities by expanding the Commercial Paper Funding Facility (CPFF) to include high-quality, tax-exempt commercial paper as eligible securities.”

“…A Main Street Business Lending Program to support lending to eligible small-and-medium sized businesses, complementing efforts by the SBA.”

“The TALF is a credit facility authorized under section 13(3) of the Federal Reserve Act intended to help meet the credit needs of consumers and small businesses by facilitating the issuance of asset-backed securities (“ABS”) and improving the market conditions for ABS more generally… The TALF SPV initially will make up to $100 billion of loans available.”

The Fed was to expand its assets by at least $625 billion this week. In concert with global central bankers, unprecedented liquidity operations coupled with a massive U.S. fiscal program was sufficient to reverse collapsing global markets. Once reversed, there was more than ample fodder from the reversal of short positions and market hedges to power a historic market spike (“biggest three-day surge since 1931”).

Chairman Jay Powell, appearing Thursday on the Today Show: “There’s nothing fundamentally wrong with our economy. Quite the contrary. The economy performed very well right through February. We’ve got a fifty-year low in unemployment for the last couple years. So, we start in a very strong position. This isn’t that something is wrong with the economy.”

Powell’s optimism was echoed by regional Fed presidents: Dallas’s Robert Kaplan: “We were strong before we went into this, and we believe that we’ve got a great chance to come out of this very strong.” Atlanta Fed President Raphael Bostic: “The economy started at a great place.”

The Fed believes it has “temporarily stepped in to provide loans” – for a system considered fundamentally sound and robust. I am an analyst and not a pessimist. But, most unfortunately, the opposite holds true. U.S. and global economies were unstable “Bubble Economies” fueled by Credit and financial excess, most notably by unprecedented asset market speculative leverage. Fed assets surpassed $5 TN this week, and I’ll be stunned if they ever again fall below this level. I am reminded of Fed officials having actually expected in 2011 that its “exit strategy” would return the Federal Reserve balance sheet to near pre-crisis levels – only to double assets again in about three years to $4.5 TN.

The Austrian “Bubble Economy” concept will be invaluable as we analyze dynamics going forward. From the economic perspective, a decade of ultra-loose financial conditions incentivized businesses to over-borrow – from multinational corporations, to mid- and small business to sole proprietorships. Tens of thousands of unprofitable (and negative cashflow generating) enterprises proliferated throughout the economy – from Silicon Valley “tech Bubble 2.0,” to shale, alternative energy, biotech, media, entertainment and leisure, and so on. Ultra-loose financial conditions stoked over- and malinvestment, while generally distorting business spending patterns.

Confounding post-Bubble financial and economic landscapes will create investment decision mayhem.

U.S. and global economies are severely maladjusted – and ravenous Credit gluttons. Importantly, this ensures Trillions of monetary stimulus along with Trillions of fiscal spending will be absorbed as if dumping buckets of water onto the scorching desert sand.

Stimulus will for a time sustain scores of uneconomic enterprises, at the cost of prolonging the workout process. Nonetheless, with Bubbles popping in shale, technology, leisure and entertainment and elsewhere, millions of job losses will prove permanent.

Negative wealth effects will also wreak havoc on consumer spending patterns. From the Fed’s Z.1 report, Household Net Worth (Assets less Liabilities) ended 2019 at a record $118.4 TN, having ballooned $23 TN, or 21%, over the past three years. Household Net Worth ended 2019 at a record 545% of GDP, up from previous cycle peaks 492% (Q1 2007) and 446% (Q1 2000). Household holdings of Equities (Z1: Equities and Mutual Funds) ended Q4 at $30.8 TN, a record 142% of GDP (up from 2007’s 102% and 2000’s 117%).

Now comes the downside.

Easy gains from asset inflation are spent more freely than incomes.

Changing spending patterns will expose the fragile underbelly of the “services” and consumption-based U.S. economy.

Meanwhile, some of the most expensive real estate markets in the country will suffer collapsing demand, with major effects on construction, spending and confidence (not to mention loan losses).

One of the many lasting pandemic consequences will be a reassessment of living in New York City, San Francisco, Los Angeles and other densely-populated urban centers. Beyond negative asset market wealth effects, I expect a prolonged impact on high-income earners (i.e. Wall Street compensation, executive pay, company stock rewards, Silicon Valley, entertainment and media, real estate-related, etc.). Expect some upper-end real estate Bubbles – having persevered even through the last crisis – to finally succumb. The bursting of an unprecedented nationwide commercial real estate Bubble will have major impacts on construction and the finances of owners of real estate, as well as on the underlying loans, securitizations and derivatives.

Every segment of the economy will be impacted – many deeply. Expectations for a quick recovery are wishful thinking. And I doubt it will be possible for the Fed and global central bankers to step back from market liquidity support operations. We should not be surprised by ongoing weekly Fed balance sheet growth of several hundred billion. Household, business and market confidence have been shaken – and will be slow to recover. Markets have been conditioned over recent decades to anticipate rapid recovery. Confidence was bolstered this week by incredible “whatever it takes” measures. I’m just not convinced the necessity for ongoing rapid central bank expansion will prove as confidence inspiring.

New York state reported its first coronavirus infection on March 1st. In less than four weeks, cases multiplied to 45,000. From the February 22nd CBB: “Cases tripled to nine Friday in Italy, with the first death reported.” Italy reported 919 deaths Friday, with total deaths of 9,134 and cases of 86,498.

Governments have made very unfortunate missteps managing this pandemic. Many now look to the trajectory of China’s outbreak for hope that cases elsewhere will begin declining soon – with economic normalization commencing in earnest. Yet Western democracies have a major disadvantage in managing a pandemic. Societies would not tolerate health authorities going door to door checking for symptoms and removing those with fevers (sometimes kicking and screaming) for immediate transport to isolation facilities.

One has only to view photos of a bustling Central Park or videos of crowded NYC subways to realize that “lock down” means something quite different in the U.S. than it does in Wuhan and Hubei Province. And only China has 170 million cameras and a sophisticated surveillance system – that in one case provided the ability to track an infected individual “down to the minute” as he traveled between provinces and along public transit in Nanjing.

Bill Gates’ comments (CNN Coronavirus Townhall, March 26th) resonated. Having warned of pandemic risk in a 2015 TED talk, and after years of being fully immersed with the Bill and Melinda Gates Foundation’s efforts in infectious disease control, vaccines and other global health initiatives, Gates possesses deep understanding of the subject matter. His view is that nationwide shutdowns and social distancing efforts must be strictly maintained until the number of active coronavirus cases declines to a low and manageable level. A cursory glance at one of the nationwide outbreak maps is sufficient to appreciate that the outbreak is currently out of control throughout the country.

We’ll learn more next week, but it appears the White House is moving forward with a plan to gauge the outbreak across the country in a county by county effort to get the economy moving back toward capacity as soon as possible. It’s difficult for me to see governors, mayors, local government officials and vulnerable healthcare systems around the country supporting any relaxation of pandemic management efforts.

Unfortunately, there will be no speedy economic recovery. Let’s hope the change of season offers some relief. But then there’s the loaming prospect for a second wave next fall and winter. Various experts, including Bill Gates, say a vaccine is a year to 18 months out. There’s going to be a hell of a battle in deciding how best to move the economy forward from here.

As for the markets: markets will do what markets do. And global market dynamics are incredibly unsound. Count me skeptical that the biggest three-day rally (in the DJIA) since 1931 is a sign of health. I fully appreciate that “buy the dip, don’t be one” has been richly rewarding for a long time now. “There couldn’t be a better time to start investing [than] right now… Fortunes are going to be made out of this time… I can guarantee you that if you stay in and you just stick with it, three years from now you will be very, very happy that you did.” I’d be especially cautious with guarantees. Suze Orman (and most) have little appreciation for what is now unfolding. The younger generation has yet to experience a grueling protracted bear market. “Buy the dip” and “buy and hold” are poised to dishearten.

Incredible central bank liquidity operations yanked global markets back from the precipice.

In the three sessions, Tuesday to Thursday, the Dow surged 21.3% (ending the week up 12.8%). The week saw the S&P500 rally 10.3%, lagging the Japanese Nikkei’s 17.1% surge. Brazil’s Bovespa recovered 9.5%, as emerging equities bounced back. Mexico’s peso rallied 4.6%, leading an EM currency recovery. In “developed” currencies, the Norwegian krone rallied 11.6%, in another week of acute market instability.

After spiking 44 bps the previous week, investment-grade Credit default swaps (CDS) this week sank 40 to 112 bps. The iShares investment-grade corporate bond ETF (LQD) surged 14.7%, more than reversing the previous week’s extraordinary 13.3% decline.

The Fed’s move to open-ended QE coupled with corporate bond and bond ETF purchases was instrumental in arresting market collapse and sparking upside dislocation. This, along with expanded central bank swap arrangements, reversed global market illiquidity and panic.

If I believed global markets were chiefly facing liquidity issues, I would be more hopeful.

Illiquidity was pressing, and global central bankers responded with “whatever it takes” (and it took a lot). Believing the global Bubble has burst, I see the overarching issue more in terms of a developing Solvency Problem. Burning the midnight oil in homes around the globe, rating agency employees enjoy enviable job security. And that would be Credit analysts for corporations, financial institutions, municipalities, investment-grade bonds, junk debt, structured products and nations. Credit and Solvency issues will turn systemic.

It’s a different world now. And while “whatever it takes” can accommodate speculative deleveraging and generally support market liquidity, The Solvency Problem will prove a historic challenge. The global economy has commenced a major downturn, hitting an already impaired global financial system. While markets enjoyed a recovery this week, EM debt is turning toxic. Energy-related debt is already toxic. Risk of general business and real estate debt turning toxic is growing rapidly.

As I posited last week, I see an environment hostile to speculative leverage. This ensures a fundamental tightening of financial conditions and attendant downward pressure on global asset markets – securities and real estate, in particular. And with Bernanke’s 40-year bond yield “ski slope” at the end of a historic run, central banks have today little capacity for using rate cuts to reflate asset prices.

The U.S. economy is in trouble. Europe is in greater trouble. EM economies face a disastrous combination of financial and economic hardship. And just as China moves to restart its economy, the massive Chinese export sector is confronting collapsing global demand. How long Beijing can hold things together is a critical issue. In the theme of bursting Bubble economies and unfolding Solvency Problems, no country faces greater challenges than China (with its deeply maladjusted economy and gargantuan financial sector).

{kind=link}

{kind=link}