The decline and collapse of Kamala Harris’ presidential ambitions should serve as a lesson that Democratic presidential candidates shouldn’t try to paper over a history of harsh practices in the criminal justice arena.

But never mind, here’s former New York mayor and self-funding Democratic presidential candidate Michael Bloomberg trying to act as though criticism of his stop-and-frisk policy is a brand new thing that just came up because he’s running for president:

Former NYC Mayor @MikeBloomberg tells @GayleKing "nobody asked" him about stop & frisk until he started running for president.

"I'm sorry. I apologize. Let's go fight the NRA and find other ways to stop the murders and incarceration. Those are things that I'm committed to do." pic.twitter.com/ww1pJPraBt

In that clip from CBS This Morning, Gayle King notes that there’s some suspicion about how sincere Bloomberg really was when he apologized for his city’s stop-and-frisk searches, which heavily targeted minority citizens but rarely uncovered the contraband drugs or guns used to justify them. Bloomberg responds that “nobody asked me about it until I started running for president.”

This, of course, is utter nonsense. Bloomberg hasn’t just been criticized for New York’s stop-and-frisk policy; the ciy was sued over it. Even as he was doing some initial groundwork for his presidential run, he was still defending the policy. Just a year ago—in response to, yes, people asking him about it—he was still insisting that it helped lower crime rates in New York City, even though there’s little data to back up this claim, and even though crime continued to fall after the practice ended.

One federal judge ruled that these warrantless dragnet searches based on no probable cause were unconstitutional. Does Bloomberg want is to believe that no one at any point in that process “asked me about it”?

The reality is that Bloomberg himself only reversed his position right before announcing his run for president. That’s why his sincerity is being questioned. His entire history as mayor and everything he said on the subject up until last month made it clear that he believed his stop-and-frisk policy was a good idea—facts, criticism, and judicial rulings be damned.

He does indeed acknowledge now that crime has kept falling even after New York City ended these spot searches. He sees this as a “mark of an intelligent, competent person when they make a mistake, they have the guts to stand up and say ‘I made a mistake, I’m sorry.'” But he still doesn’t seem to acknowledge the deeper issues at play. The policy was intrusive, racist, and unconstitutional, but hey, the mayor meant well.

Nor has he learned the broader lesson here: that there are problems that cannot be solved by heavily policing the populace. The relentless nanny inside Bloomberg is still fully in charge. So he’ll be more than happy to go after gun owners (he immediately tries to deflect criticism by pivoting to an attack on the National Rifle Association), and he will doubtlessly keep wanting to use the government to control our private decisions. And if he keeps making the wrong choices on our behalf? He meant well, and maybe the next time he runs for office he’ll apologize about it.

from Latest – Reason.com https://ift.tt/2Yuom8X

via IFTTT

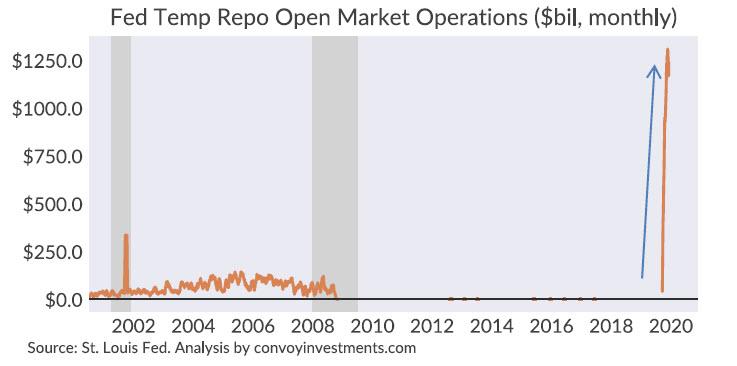

Has QE4 begun? The $1.2 trillion per month hole in the repo market.

In the two months since the repo market blow up, the Fed has been making repo open market operation purchases at a rate of $1.2 trillion per month.

Below is the monthly rate of Fed open market purchases since 2000. In the era of QE and ample reserves, the Fed has not touched open market operations for more than 10 years before 2019. Prior to that, the highest rate of open market operations we saw in history was roughly $300 billion/month briefly after the September 11 attacks, with long‐term averages of around $50 billion/month. To say the current rate of $1.2 trillion/month is unprecedented would be an understatement

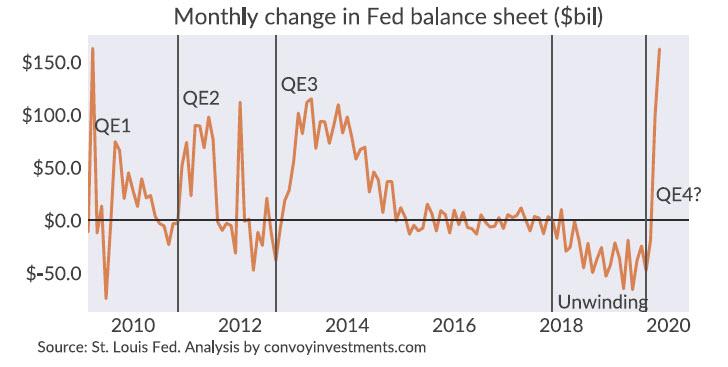

The planned QE unwinding has hit a brick wall and the Fed balance sheet is now expanding at a rate matched only briefly by QE1, and faster than QE2 or QE3.

Is this a temporary rescue of the repo market or the start of a sustained QE4? To answer that question, we must look at how monetary policy has evolved since the Financial Crisis.

1. Pre‐2008, scarce reserves regime:

Total reserves: small (<$50 billion)

Excess reserves: none

Interest on excess reserves: 0%

Managing interest rates: to increase rates, Fed sells securities on the open market and reduces supply of reserves, vice versa to decrease rates.

Banks: regulations are lax and risk tolerance is high

Treasury department: carefully manages its cash flows to not impact the total reserve levels.

2. 2008‐2019, ample reserves regime:

Total reserves: large ($trillions)

Excess reserves: large ($trillions)

Interest on excess reserves: positive at around Fed funds rate

Managing interest rates: Because there is more reserves than the banks could possibly need, Fed sets interest rates by paying a floor rate on reserves.

Banks: regulations are strict and risk tolerance is low

Treasury department: no longer actively manages its cash flows, its activities directly affect total reserve levels.

3. 2019 onwards, scarce reserves regime again?:

A combination of QE unwinding, strict banking regulations, and a concentration of reserves in a handful of banks have once again made reserves scarce, which means a rate floor is no longer effective at managing against rate rises. This was painfully obvious in December of 2018 and September of 2019. Thus far, the Fed has chosen their pre‐2008 strategy of temporary open market operations to manage rates in this new scarce reserves environment. But because the total pool of reserves is around 50 times larger now than pre‐2008, the size of the required open market operations is in the $trillions, not $billions, per month.

Going forward, the Fed must make a choice of staying in a regime of scarce reserves or going back to ample reserves. The Fed can lower interest on excess reserves and reduce bank incentives to hold excess reserves to some degree, but the new post‐2008 regulations will still necessitate a far larger base of reserves than pre‐2008. So managing a scarce reserves banking system on a large base of reserves will require continued massive open market operations. It will likely also require a change from the Treasury department’s cash flow management.

Alternatively, the Fed can recognize that they’ve found the floor for the total amount of reserves necessary in our new regulatory environment and add some reserves via another round of QE as cushion and grow the total reserves in line with our GDP. This would allow us to stay in the ample reserves regime.

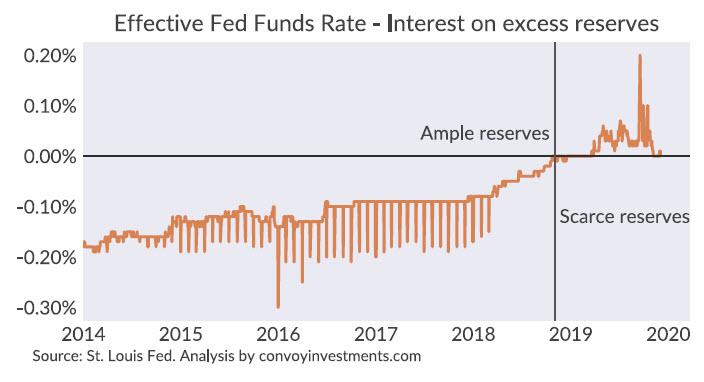

The key metric I’d keep an eye on is the difference between interest on excess reserves and the effective Fed Funds rate, which I show below. We made the switch from an ample reserves regime to a scarce reserves regime in December of 2018.

If the system has more than enough reserves, the effective Fed Funds rate would be below the interest on excess reserves because not every participant is eligible for interest on excess reserves, hence they’d push the average Fed Funds rate below interest on excess reserves. In the 2019 environment of scarce reserves, market participants are starved for reserves and bid the average Fed Funds rate at or above interest on excess reserves. At the moment, the Fed has done enough open market operations to meet reserve demand and drive Fed Funds rate exactly back to interest on excess reserves.

Going forward, whether the Fed pushes effective Fed Funds rate below interest on excess reserves will signal the next era of monetary policy. If the Fed chooses the scarce reserves route, Fed funds rate will stay at or above interest on excess reserves. The Fed will continue to buy short‐term securities as necessary to meet demand for reserves and push down the short end of the curve and I’d bet on the yield curve steepening again. If they choose the ample reserves route, Fed Funds rate will fall back below interest on excess reserves, the Fed will go back to buying 10 year bonds, and I’d expect to see further flattening of the yield curve.

Unless banking regulations change dramatically, my guess is that QE4 is coming. The Fed would rather have a cushion of ample reserves against unexpected repo market blow ups than react retroactively with $trillions/month of open market operation purchases.

This short essay does what the House Judiciary Committee’s panel of “expert witnesses” did not successfully do.

First, it explains the meaning of the Constitution’s “high Crimes and Misdemeanors” standard. Next, it discusses how that standard applies to President Donald Trump’s interactions with Ukrainian President Volodymyr Zelensky. Finally, it details the kind of evidence the House Judiciary Committee should gather to determine whether the president committed an impeachable offense.

Many phrases in the Constitution—such as “necessary and proper,” “Privileges and Immunities,” and “Convention for proposing Amendments”—carry specialized 18th century meanings not obvious to the modern reader. Recall that most of the leading Founders were lawyers and the Constitution is a legal document. Some of these phrases derive from 18th century law.

Therefore, to understand them you have to consult 18th century legal materials in addition to better-known sources such as the 1787 convention debates or the Federalist Papers.

Unfortunately, most of the scholars called by the House Judiciary Committee to address the meaning of “high Crimes and Misdemeanors” were not able to do so accurately.

According to the authoritative Westlaw database, two of the three Democratically appointed witnesses have published no scholarly work on impeachment: Their specialties are in other areas. None showed any familiarity with 18th century fiduciary standards—which (as explained below) are part of the law of impeachment. All of the witnesses voted against President Trump, and several have been involved in anti-Trump activity.

It’s not surprising, therefore, that, except for professor Jonathan Turley’s heavily footnoted 53-page written statement, the testimony was biased and superficial.

What Is the Standard?

Impeachment law is not for amateurs. It rests on English parliamentary history extending at least as far back as the 1300s. Furthermore, impeachment standards evolved over time. To understand the Constitution’s rules we must know what the standards were when the Constitution was adopted. We can do so by consulting 18th century parliamentary records and legal materials.

Here’s some of what they tell us:

The term “high Crimes” means, approximately, “felonies.”

The phrase “high … Misdemeanors” refers to what the founding generation called “breach of trust” and what modern lawyers call breach of fiduciary duty. Fiduciary duties are the legal obligations imposed upon those who manage the affairs of other people—bankers, corporate executives, accountants, guardians, and so forth. In broad outline, fiduciary law when the Constitution was adopted was similar to what it is today.

In the 14th and 15th centuries, an official could be impeached because Parliament disagreed with his policy decisions. However, as several American Founders recognized, by the 18th century this was no longer true. The official must have violated (in the words of several sources) “the known and established law.” This limited impeachment to serious crimes and fiduciary breaches.

The trial in the upper house of the legislature was a judicial proceeding, not primarily a political one. As the 1782 edition of the popular Jacob’s Law Dictionary noted, “the same evidence is required in an impeachment in Parliament, as in the ordinary courts of justice.” The hearsay and impressionist evidence gathered by the House Intelligence Committee is not admissible.

The core of the case against President Trump is that he used his political position to seek re-election assistance from a foreign government. Although there’s dark talk of crimes committed, the principal charge is fiduciary rather than criminal. In other words, a “high … Misdemeanor.”

House Democrats have struggled to define Trump’s alleged offense. Initially, they described it as “quid pro quo.” Then they employed the term “bribery.” The legally correct designation is “self-dealing.”

Self-dealing is betraying your employer’s interests to enrich yourself. It’s a violation of the fiduciary duty of loyalty.

We can assume the president might benefit from a Ukrainian investigation, but that doesn’t mean asking for an investigation was self-dealing as defined by fiduciary, and therefore by impeachment, law. There’s nothing unusual or improper about a president asking a recipient of U.S. foreign aid to address corruption. As for seeking political advantage: If we punished every politician who did that, they would all be swinging from the yardarm.

This is as true in foreign as in domestic affairs. When President Barack Obama told the Russian president he would have more flexibility after his re-election, he was saying (1) an agreement now would benefit both Russia and the United States, but (2) I’m going to sacrifice our mutual interests for the present because such an agreement might hurt my re-election campaign. Was this impeachable self-dealing? Almost certainly not.

So where is the divide between “normal” conduct and impeachable conduct? To answer this, we need to weigh at least three factors: impeachment precedent, the national interest, and the practice of other presidents.

Impeachable Conduct

For defining the Constitution’s phase “high … Misdemeanors,” the most important precedents (although not the only ones) lie in 18th century impeachment and fiduciary law.

An 18th century impeachment treatise outlines the specific facts by which several officials were impeached for what we now call self-dealing.

They include the following:

(1) the official enriched himself at the expense of the Crown by arranging for royal pardons,

(2) he stole funds from the Royal Navy,

(3) he confiscated ships and cargos without due process and appropriated the proceeds,

(4) he obtained “exorbitant grants of lands and money, to the great detriment of the revenue,”

(5) he seized forfeited land that should have gone to the Crown, and

(6) acting through a strawman, he took the proceeds from timber sales in the king’s forests.

All these cases boil down to stealing public property. They don’t look like the Trump–Zelensky dealings at all.

Another part of the answer lies in whether President Trump violated the national interest. As a general rule, self-dealing generally is not just enriching yourself. It’s enriching yourself at the expense of your employer. If Trump’s interests were aligned with those of the country, there was no fiduciary breach.

Despite Col. Alexander Vindman’s complaint that Trump violated “the consensus of the interagency,” the question of whether Trump acted contrary to the national interest is a difficult one to answer.

Perhaps we had a national interest in not asking President Zelensky to investigate. But we also had a national interest in asking, because it would be useful to know if Ukrainian officials were trying to meddle in our presidential elections. And it would be useful to know whether the family of a leading presidential candidate is engaged in corruption. Remember: the president asked only for an investigation, not for a pre-determined result.

Thus, you can argue the “national interest” issue both ways. It looks more a policy question than a clear case like theft of public funds.

Still another part of the answer lies in how similar officials act in similar circumstances. In absence of a crime, if you want to determine whether a banker handled funds properly, you should investigate how bankers usually handle funds. If you wish to determine whether an investment adviser gave reasonable advice, you should consult what other reputable advisers recommend in the same circumstances.

Similarly, to decide whether President Trump engaged in impermissible self-dealing, we need testimony about how other officials conduct themselves. We know, for example, that then-Vice President Biden explicitly made aid to Ukraine conditional on firing a Ukrainian prosecutor. If that conduct wasn’t impeachable (and I don’t believe it was) then Trump’s more tepid conduct certainly isn’t impeachable.

Thus, the Judiciary Committee should ask for testimony from officials of prior presidential administrations, and preferably from the former presidents themselves. Did they ever make foreign aid conditional? What were the conditions? Why? And so forth.

Another Panel

It was a good idea to empanel academic experts to provide guidance on the meaning of “high Crimes and Misdemeanors.” It should be done again, and this time correctly.

The next panel should include presidential historians, parliamentary historians, and experts on fiduciary law. It should not consist primarily of law professors, who are notorious for engaging more in advocacy than in true scholarship.

Every panelist should have published research on impeachment, fiduciary law, or related areas. No panelist should be enmeshed in pro-Trump or anti-Trump political activity. They should be limited to discussing constitutional impeachment standards without expostulating on evidentiary testimony. Weighing the evidence is the job of the committee members, not of academics with little judicial or “real life” experience.

Once the scholarly panel has testified, the committee should explore whether the president’s Ukrainian actions clearly violated the national interest and it should gather testimony on the conduct of former administrations in comparable situations.

And only if all those investigations support a “self-dealing” conclusion should the committee recommend articles of impeachment.

This week the Trump administration finalized new rules for the Supplemental Nutrition Assistance Program (SNAP), otherwise known as food stamps. The plan could potentially remove as many as 688,000 people from the rolls.

Rep. Alexandria Ocasio-Cortez (D–N.Y.) took to Twitter yesterday to talk about how the cuts could have affected a younger version of herself. When her father died in 2008, while Ocasio-Cortaz was still a student at Boston University, her family depended on food stamps to get by. If the new rules were in place then, she claimed, “we might’ve just starved.”

My family relied on food stamps (EBT) when my dad died at 48.

I was a student. If this happened then, we might’ve just starved.

Now, many people will.

It’s shameful how the GOP works overtime to create freebies for the rich while dissolving lifelines of those who need it most. https://t.co/WOrYvhfPj4

But when the new rules take effect on April 1 of next year, any college student whose family is facing the same hardships that AOC did will still have access to the food stamp program. The changes being enacted will only affect able-bodied adults with no dependents.

That’s not necessarily a defense of the Trump administration’s SNAP eligibility changes—more on that in a moment—but rather a commentary on the sad state of The Discourse whenever transfer programs are subject to public debate. When any attempt to curtail welfare spending is met with accusations that officials are literally out to starve poor people to death, there’s is no space for an actual, practical discussion about who should have access to the safety net.

It’s one thing to argue that the food stamp program (or any other part of the welfare state) should not be cut. But Ocasio-Cortez only makes that position look ridiculous by engaging in hyperbole over a relatively mundane change in eligibility. And, indeed, that’s what this is. Under current rules, able-bodied adults with no children can receive food stamps for up to three months once every three years, but states have the authority to waive that limitation and grant full access in counties where the unemployment rate is higher than a mere 2.5 percent. Under the new rules, states will be able to grant waivers only in counties with an unemployment rate over 6 percent or higher.

Yes, those changes are expected to eliminate SNAP benefits for about 688,000 people when they take effect. For context, there were more than 39 million people receiving SNAP benefits in 2018, a total that has fallen only slightly since the height of the last recession. And food stamps have always operated as a short-term benefit designed to ease the transition after a job loss, not a perpetual entitlement for adults who are fully capable of working and who live in areas with low unemployment.

A more rational debate over the status of SNAP benefits would recognize that no matter where you draw the arbitrary lines for eligibility, there will always be some people who don’t qualify. That doesn’t mean the government is trying to starve them to death.

But there can—or at least there should—be a legitimate debate over the costs and benefits of this proposed policy change. Cutting those 688,000 people off from SNAP benefits will save about $5.5 billion over five years, according to USDA officials. That’s a sizeable amount of money, but it pales in comparison to the $28 billion Trump has pledged to send to farmers—via a different USDA program—to make up for the losses caused by his trade war with China.

In other words, the administration might not be condemning Americans to starve in the streets, but it can’t really claim a strong commitment to fiscal conservatism, either.

Our inability to have a reasonable debate about just $5.5 billion has some sobering implications. The federal budget deficit is going to surpass $1 trillion this year. The national debt is heading towards $30 trillion by the end of the decade. And Social Security and Medicare will run a combined deficit of $100 trillion over the next 30 years.

Those are big problems that require serious solutions—solutions that will almost certainly require reductions to current transfer programs. But you can’t have a serious debate if every cut is seen as a death sentence.

from Latest – Reason.com https://ift.tt/2DV026S

via IFTTT

This week the Trump administration finalized new rules for the Supplemental Nutrition Assistance Program (SNAP), otherwise known as food stamps. The plan could potentially remove as many as 688,000 people from the rolls.

Rep. Alexandria Ocasio-Cortez (D–N.Y.) took to Twitter yesterday to talk about how the cuts could have affected a younger version of herself. When her father died in 2008, while Ocasio-Cortaz was still a student at Boston University, her family depended on food stamps to get by. If the new rules were in place then, she claimed, “we might’ve just starved.”

My family relied on food stamps (EBT) when my dad died at 48.

I was a student. If this happened then, we might’ve just starved.

Now, many people will.

It’s shameful how the GOP works overtime to create freebies for the rich while dissolving lifelines of those who need it most. https://t.co/WOrYvhfPj4

But when the new rules take effect on April 1 of next year, any college student whose family is facing the same hardships that AOC did will still have access to the food stamp program. The changes being enacted will only affect able-bodied adults with no dependents.

That’s not necessarily a defense of the Trump administration’s SNAP eligibility changes—more on that in a moment—but rather a commentary on the sad state of The Discourse whenever transfer programs are subject to public debate. When any attempt to curtail welfare spending is met with accusations that officials are literally out to starve poor people to death, there’s is no space for an actual, practical discussion about who should have access to the safety net.

It’s one thing to argue that the food stamp program (or any other part of the welfare state) should not be cut. But Ocasio-Cortez only makes that position look ridiculous by engaging in hyperbole over a relatively mundane change in eligibility. And, indeed, that’s what this is. Under current rules, able-bodied adults with no children can receive food stamps for up to three months once every three years, but states have the authority to waive that limitation and grant full access in counties where the unemployment rate is higher than a mere 2.5 percent. Under the new rules, states will be able to grant waivers only in counties with an unemployment rate over 6 percent or higher.

Yes, those changes are expected to eliminate SNAP benefits for about 688,000 people when they take effect. For context, there were more than 39 million people receiving SNAP benefits in 2018, a total that has fallen only slightly since the height of the last recession. And food stamps have always operated as a short-term benefit designed to ease the transition after a job loss, not a perpetual entitlement for adults who are fully capable of working and who live in areas with low unemployment.

A more rational debate over the status of SNAP benefits would recognize that no matter where you draw the arbitrary lines for eligibility, there will always be some people who don’t qualify. That doesn’t mean the government is trying to starve them to death.

But there can—or at least there should—be a legitimate debate over the costs and benefits of this proposed policy change. Cutting those 688,000 people off from SNAP benefits will save about $5.5 billion over five years, according to USDA officials. That’s a sizeable amount of money, but it pales in comparison to the $28 billion Trump has pledged to send to farmers—via a different USDA program—to make up for the losses caused by his trade war with China.

In other words, the administration might not be condemning Americans to starve in the streets, but it can’t really claim a strong commitment to fiscal conservatism, either.

Our inability to have a reasonable debate about just $5.5 billion has some sobering implications. The federal budget deficit is going to surpass $1 trillion this year. The national debt is heading towards $30 trillion by the end of the decade. And Social Security and Medicare will run a combined deficit of $100 trillion over the next 30 years.

Those are big problems that require serious solutions—solutions that will almost certainly require reductions to current transfer programs. But you can’t have a serious debate if every cut is seen as a death sentence.

from Latest – Reason.com https://ift.tt/2DV026S

via IFTTT

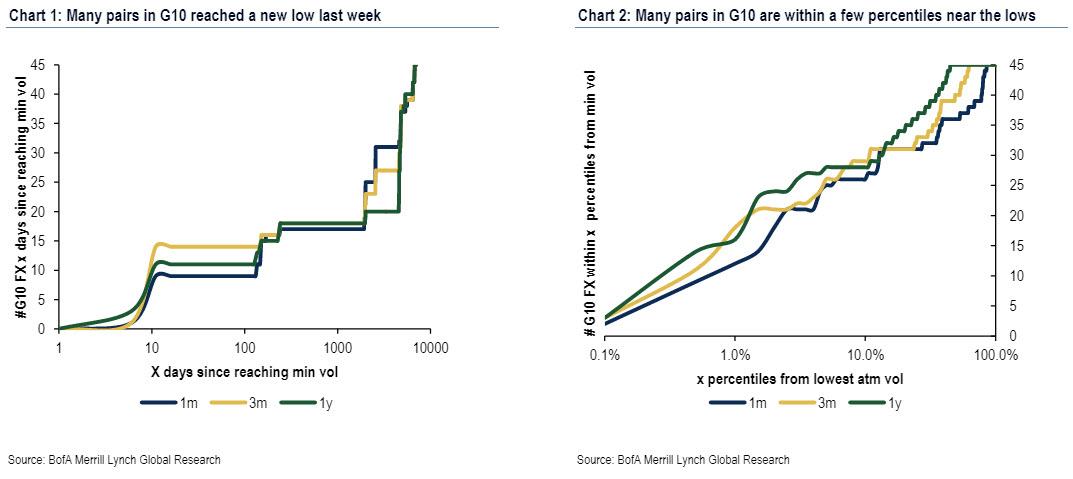

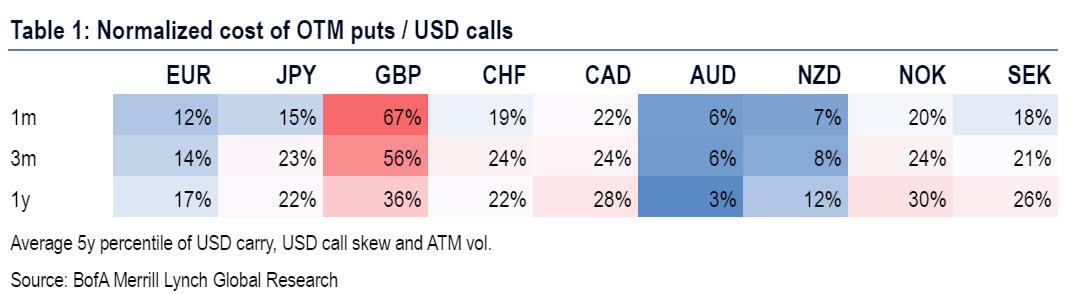

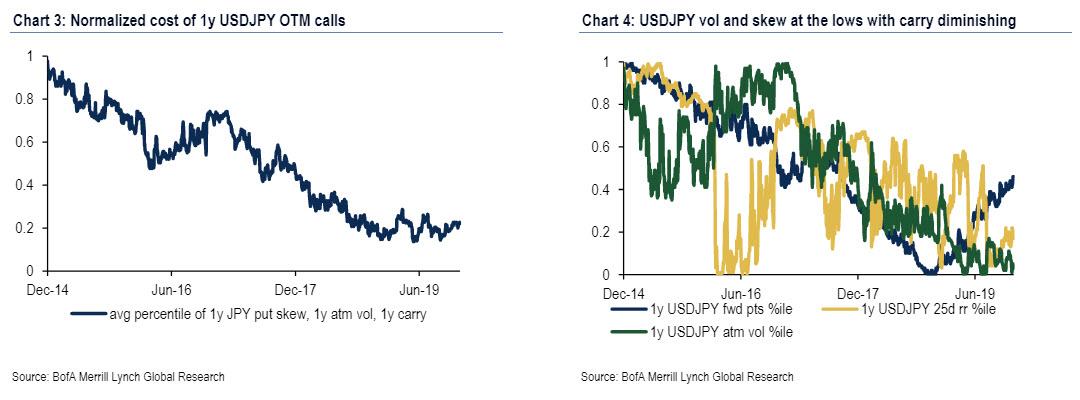

FX Volatility Nears All Time Low In “Perfect Storm Of Vol, Skew And Carry”

While the VIX still has a fair ways to go before it plumbs the all-time single-digits lows that defined the spectacularly serene equity markets in 2017, FX vol is already there: the JPMorgan Global FX volatility index has dropped to 6 year low levels, and is just shy of all time lows.

Of course, most of this stability in the FX realm is due to central banks depressing cross-asset vol; yet the more vol is pushed lower, the higher it will spring back once central banks lose control; as such it is only a matter of time before buying FX vol is a winning trade.

Commenting on this record low FX vol and currency-specific volatility, BofA’s Vadim Iaralov writes that a “dozen FX vols reached new lows last week and most remain close to their all-time lows” in what he calls a “perfect stormof vol, skew and carry.”

Some more details from the BofA FX strategist:

A number of G10 vols have already made new lows last week including nine pairs in G10 of one-month ATM vols, 14 pairs of three-month vol and 11pairs of one-year. Current vols remain low at 1st percentile or lower including 12 pairs of one-month vols, 18 pairs of three-month vols and 16 pairs of one-year vols.

His obvious conclusion: the low vol offers attractive hedging opportunities, especially for investors concerned about against USD gains.

Looking at the dollar alone, in addition to low ATM vols, Iaralov points out that USD call skew is also near historically flat and USD carry remains positive, if somewhat diminished after recent Fed cuts.

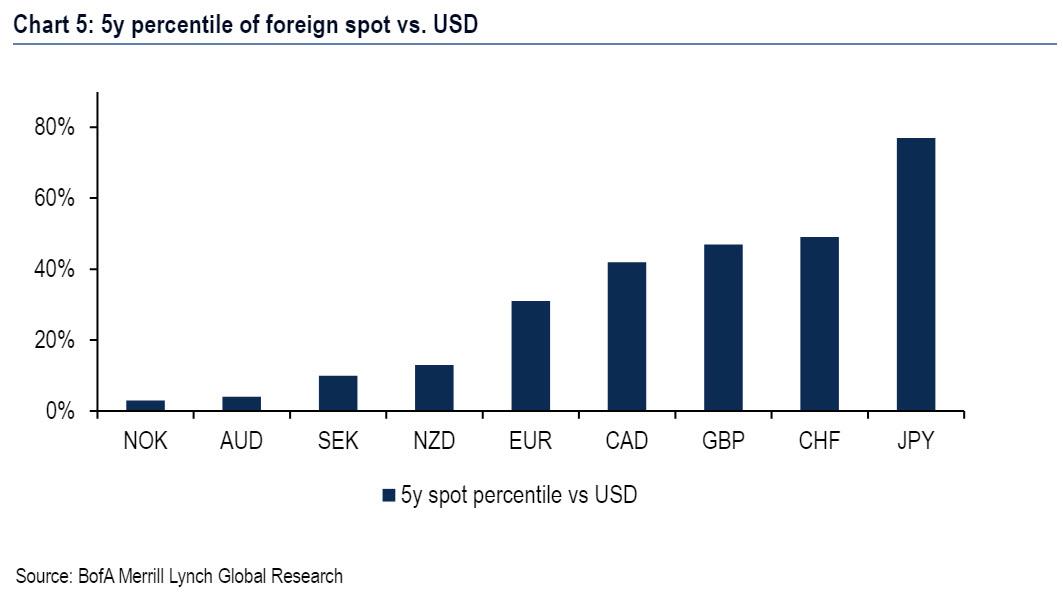

FX traders can combine these measures to normalize cost of out-of-the-money options; BofA has done so, and found that out-of-the-money puts on AUD, NZD and EUR are especially attractive, offering topside USD hedges at a historically low cost. By contrast, GBP, NOK and CAD hedges are less affordable. Given Brexit and the UK election ahead, 1m GBP hedges via OTM puts are especially pricey.

In addition, recent JPY gains have cheapened OTM USD/JPY calls of fixed strikes, for example for corporates restructuring existing hedges. As Iaralov adds, the front-end 1m USDJPY benefits from a confluence of attractive vols, skew and carry. However, at the 1y mark the carry has turned less beneficial, pricing in another Fed cut, even though the vols and USDJPY skew are near the lows.

Finally, when constructing low vol hedging trades, keep in mind that spot levels can be incorporated when considering the cost of options struck at specific, fixed strikes rather than in delta terms. OTM USD calls at fixed strikes are cheaper when USD/FX is weaker as it is for USD/JPY and more expensive for USD vs NOK and USD vs AUD.

Tech War Set To Deepen As China Stockpiles US Chips Amid ‘Silicon Curtain’ Threat

The US and China trade war continues to deepen this week with the increasing chance that a phase one trade deal has been delayed until 2020. In the meantime, we’ve been reporting on a Sino-U.S. technology war developing, something that has been heating up in recent months.

China understands the tech war with the US is about to erupt, that’s why the country has been pulling forward orders of US chips, reported Bloomberg. It’s an acknowledgment that China is preparing for the worse, and it’s likely the Trump administration could prevent Chinese companies from buying chips if the trade war deepens further.

We reported earlier this week that the Trump administration considered banning Huawei from using the US financial system as a nuclear option to crush the company.

If White House officials were proposing that, then they’ve also been preparing to ban Chinese companies from buying US chips altogether.

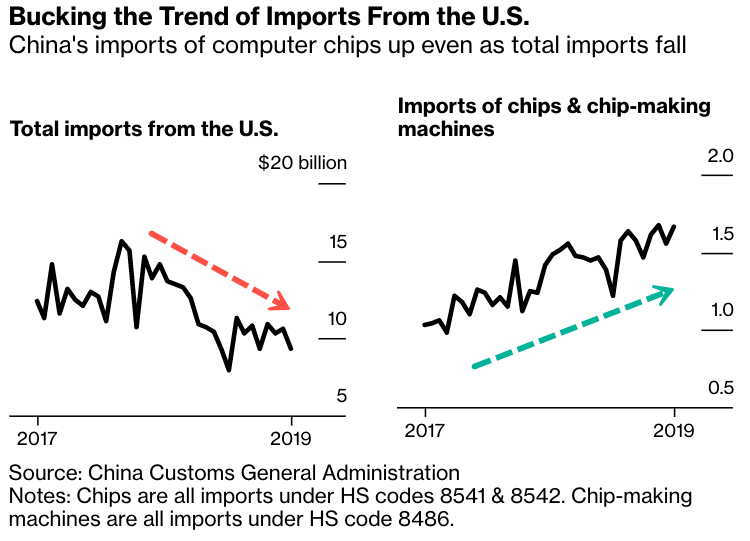

In the past three years, Chinese imports of US chips have jumped, despite ongoing trade war threats that have surged in the last 1.5 years.

As shown below, imports of chips and chip equipment were $1.7 billion in Aug., the most since 1Q17, and continued increasing through Oct.

Bloomberg notes that there’s a severe risk that the Trump administration could impose new measures that would establish a “silicon curtain” to halt all shipments of US chips to China.

“It’s politically intolerable to China that the US has an at-will ability to turn off major companies like ZTE and Fujian Jinhua, as well as being able to deal major operational blows to Huawei,” Dan Wang, a tech analyst at Gavekal Dragonomics in Beijing, told Bloomberg “So the government and the companies are trying to be more technologically independent.”

This past summer, the Trump administration blacklisted Chinese companies, including Huawei, from selling products to certain US firms unless the federal government granted special licenses. This forced Huawei to develop new domestic chips to reduce the dependence on the US.

Many Chinese firms, including Huawei, have been ramping up purchases of US chips since about 2018, in anticipation of being blacklisted.

Huawei understands what’s coming down the pipe and how the trade war is likely to deepen in 2020. The company has also moved its US research center to Canada to avoid having its US assets frozen.

Huawei, like many other Chinese firms, pulled forward chip sales to get ahead of new US economic sanctions. So what happens when Chinese firms stop frontloading chip purchases? Does that mean PHLX Semiconductor Sector is in a blowoff top if purchases pullback?

Seth Barrett Tillman and I published a new essay on Lawfare. We discuss a theory of “bribery” for the impeachment clause. Here is an excerpt:

Just as the executive branch should not investigate and prosecute horse-trading and log-rolling by members of Congress, Congress should not investigate and impeach horse-trading by the president. Where the president acts for mixed motives while engaging in log-rolling and horse-trading—entertaining related considerations of public policy, his party’s success and his chances of personal reelection—there is nothing to investigate.

Judge Frank Easterbrook stated this principle in even stronger terms regarding the conviction and sentencing of Illinois Governor Rod Blagojevich, who offered to appoint Valerie Jarrett, a close associate of President-elect Obama, to a vacant U.S. Senate seat, in exchange for Blagojevich’s receiving an appointment to the Obama cabinet. Blagojevich was convicted on multiple counts. On appeal, in U.S. v. Blagojevich (2015), the U.S. Court of Appeals for the Seventh Circuit found that particular counts of his conviction could not stand. Judge Easterbrook explained that “a proposal to trade one public act for another, a form of logrolling, is fundamentally unlike the swap of an official act for a private payment.” He added that “[g]overnance would hardly be possible without” political log-rolling, “which allow[s] each public official to achieve more of his principal objective while surrendering something about which he cares less, but the other politician cares more strongly.”

Thus, according to Easterbrook, in such circumstances, even mixed motives are irrelevant. Such acts are presumptively lawful, and should not be investigated, let alone be considered for indictment or impeachment. If there is any evidence that there was some sort of secret benefit (such as a suitcase full of cash), then the government can investigate and, if warranted, prosecute that additional act. The secretness of the benefit is evidence of corrupt intent. Where one public official act is traded for another public official act, there has not been any illegal conduct.

We can think of one high-profile and far more brazen effort by a president to improve his party’s prospects through the use of official communications. In 1864, during the height of the Civil War, President Lincoln encouraged Gen. William Tecumseh Sherman to allow soldiers in the field to return to Indiana to vote. What was his primary motivation? It was to make sure that the government of Indiana remained in the hands of Republican loyalists who wished to continue the war until victory. This action risked undercutting the military effort by depleting the ranks. Lincoln had dueling motives. Privately, he sought to secure a victory for his party. This personal interest should not impugn his public motive: win the war and secure the nation.

from Latest – Reason.com https://ift.tt/33Tsqk3

via IFTTT

Seth Barrett Tillman and I published a new essay on Lawfare. We discuss a theory of “bribery” for the impeachment clause. Here is an excerpt:

Just as the executive branch should not investigate and prosecute horse-trading and log-rolling by members of Congress, Congress should not investigate and impeach horse-trading by the president. Where the president acts for mixed motives while engaging in log-rolling and horse-trading—entertaining related considerations of public policy, his party’s success and his chances of personal reelection—there is nothing to investigate.

Judge Frank Easterbrook stated this principle in even stronger terms regarding the conviction and sentencing of Illinois Governor Rod Blagojevich, who offered to appoint Valerie Jarrett, a close associate of President-elect Obama, to a vacant U.S. Senate seat, in exchange for Blagojevich’s receiving an appointment to the Obama cabinet. Blagojevich was convicted on multiple counts. On appeal, in U.S. v. Blagojevich (2015), the U.S. Court of Appeals for the Seventh Circuit found that particular counts of his conviction could not stand. Judge Easterbrook explained that “a proposal to trade one public act for another, a form of logrolling, is fundamentally unlike the swap of an official act for a private payment.” He added that “[g]overnance would hardly be possible without” political log-rolling, “which allow[s] each public official to achieve more of his principal objective while surrendering something about which he cares less, but the other politician cares more strongly.”

Thus, according to Easterbrook, in such circumstances, even mixed motives are irrelevant. Such acts are presumptively lawful, and should not be investigated, let alone be considered for indictment or impeachment. If there is any evidence that there was some sort of secret benefit (such as a suitcase full of cash), then the government can investigate and, if warranted, prosecute that additional act. The secretness of the benefit is evidence of corrupt intent. Where one public official act is traded for another public official act, there has not been any illegal conduct.

We can think of one high-profile and far more brazen effort by a president to improve his party’s prospects through the use of official communications. In 1864, during the height of the Civil War, President Lincoln encouraged Gen. William Tecumseh Sherman to allow soldiers in the field to return to Indiana to vote. What was his primary motivation? It was to make sure that the government of Indiana remained in the hands of Republican loyalists who wished to continue the war until victory. This action risked undercutting the military effort by depleting the ranks. Lincoln had dueling motives. Privately, he sought to secure a victory for his party. This personal interest should not impugn his public motive: win the war and secure the nation.

from Latest – Reason.com https://ift.tt/33Tsqk3

via IFTTT

“Paper or plastic?” may soon be a superfluous question in New Jersey.

On Thursday, the state Senate’s Budget and Appropriations Committee advanced a bill that would ban grocery stores from giving customers either paper or plastic bags. Businesses would be required to give customers free reusable bags instead.

That last requirement will be in place for just the first two months after the ban takes effect. After that, customers will have to either bring their own bags or be prepared to carry loose groceries home in their arms.

A flat ban on single-use bags is radical, to say the least. New Jersey would be the first state to do it. New York and California have restricted themselves to banning only plastic bags.

The idea for New Jersey’s more far-reaching restrictions reportedly came to the bill’s sponsor, state Sen. Bob Smith (D–Middlesex), during his vacation to Aruba. There, plastic bags are banned and paper bags are slapped with heavy fees.

“Nobody’s grumbling,” Smith told NJ.com back in May. “Everybody in the line, they all do it.”

Thursday’s vote brings this aspect of island living a little closer to reality in the Garden State.

The bill would also give food service businesses two years to stop using Styrofoam. Plastic straws, a frequent target of anti-plastic activists and lawmakers, got off relatively easy: They won’t be banned—but restaurants would be allowed to provide them only on request.

Backers claim the bill will protect New Jersey’s natural environment. “This legislation is us fighting back to ensure we have clean oceans, clean ecosystems and to evolve our habits to include safe alternatives for our environment,” Smith said in a press release issued after the committee vote.

If this version of the bill becomes law, violators will get a warning on their first offense. A second transgression will land a $1,000 fine, and scofflaws will pay up to $5,000 for their third violation.

The bill makes exceptions for bags used to carry uncooked meat, pharmaceuticals, newspapers, live animals (particularly fish and insects from pet stores), and laundry. It also exempts prepackaged foods from its bans.

Garden State lawmakers have been toying with the idea of restricting plastic bags for some time now. In 2018 the legislature passed a tax on plastic bags, but Democratic Gov. Phil Murphy vetoed it—for being too lenient.

Smith and state Sen. Linda Greenstein (D–Mercer) introduced their own bag ban in June 2018. One committee approved it in September, but it stalled in the Budget Committee until yesterday. It now goes to the Senate floor for a second reading.

Not everyone is happy about the proposal.

Paper bag manufacturers argued at yesterday’s hearing that their product was a solution to plastic pollution, and that it should therefore be spared.

Michael Deloreto, a spokesperson for the New Jersey Food Council, pointed out that the free reusable bags required by the bill—ones with stitched handles, made of much thicker plastic or cloth, and designed for multiple uses—would cost a grocery store chain with 30 locations more than $20 million for the two months they’re required to give them away. In comparison, giving away plastic bags costs about $128,000 a month.

Deloreto argued for letting stores give away slightly cheaper reusable bags. The Food Council says it supports a ban on paper and plastic bags.

Other single-use plastic bag bans have had the unintended side effect of prompting people simply to switch to reusable plastic bags that use much more plastic. Studies of bag bans in California and the U.K. have found that they dramatically increase the consumption of these reusable bags, with many customers treating them the same as single-use plastic bags.

Overall plastic consumption still fell in both cases. But in both California and the U.K., reusable bags were not distributed for free. New Jersey shoppers would face no such deterrent during the first two months of the bag ban, making it possible that in the short term the bill will increase overall plastic consumption.

At yesterday’s hearing, ban supporters spoke of the tens of thousands of plastic and Styrofoam items they’d collected off the state’s shoreline during an annual beach clean-up. But the bill would leave the biggest sources of litter untouched. According to a 2018 survey published by a state-funded nonprofit, the New Jersey Clean Communities Council (NJCCC), neither plastic bags nor paper bags were among the state’s top 10 most littered items (which account for 43 percent of all litter). Styrofoam food containers didn’t make the top 10 either. It instead featured things like tire scraps, business papers, plastic water bottles, and tobacco packaging and accessories.

Bags of all kinds made up 4.9 percent of litter. Unbranded retail bags made up 1.7 percent.

The results from the Ocean Conversancy’s 2019 coastal cleanup were similar. Volunteers collected 37,440 items of trash off New Jersey’s beaches, including 5,928 cigarette butts, 5,981 candy wrappers, and 1,047 plastic grocery bags—about 3 percent of all items collected.

The NJCCC survey includes a number of policy recommendations that don’t involve banning items, including forging anti-litter partnerships with stores and other businesses that are litter hotspots, promoting more adopt-a-highway and adopt-a-beach programs, and better placement of public trash receptacles.

Such measures are both more voluntary and more effective. At best, all a bag ban can do is eliminate a tiny percentage of trash while inconveniencing customers and heaping more costs on business.

from Latest – Reason.com https://ift.tt/365Dz2I

via IFTTT