This week, Air Force Gen. John “Jay” Raymond was sworn in as the chief of Space Operations for the new United States Space Force. While it was initially reported as somewhat of a joke when Donald Trump first announced it, the U.S. Space Force is a very real thing and is now the seventh military branch of the Pentagon.

On Tuesday, Raymond was sworn in by Vice President Pence at his ceremonial office.

“It is President Trump’s belief that the United States must remain as dominant in space as we are on land and sea and the air. And your charge is to see to that mission with the United States Space Force,” Pence said during the ceremony.

Raymond responded by saying, “Mr. Vice President, we have our marching orders and we are moving out. We do not want a conflict to begin or extend into space, we want to deter that conflict from happening. The best way I know how to do that is to do so from a position of strength.”

The Space Force will be comprised of roughly 16,000 officers and other personnel from the U.S. Air Force and U.S. Space Command. In fact Raymond is himself a commander of both the Air Force Space Command and the U.S. Space Command, possibly signaling that these agencies will be working very closely and consisting of many of the same members.

In addition to the personnel from other agencies the Space Force was granted $40 million through the 2020 National Defense Authorization Act (NDAA).

Trump is expected to hold a meeting with Pentagon officials this week to discuss uniform and logo details for the new agency. The meeting will include Defense Secretary Mark T. Esper, Air Force Secretary Barbara Barrett, and the new chief of Space Operations Jay Raymond.

The Trump administration is also planning on sending a legislative proposal to Congress for the fiscal year of 2021 which would create National Guard and Reserve units for the Space Force. The proposal also seeks to consolidate other space-related organizations in the government under the Space Force banner including the Space Development Agency.

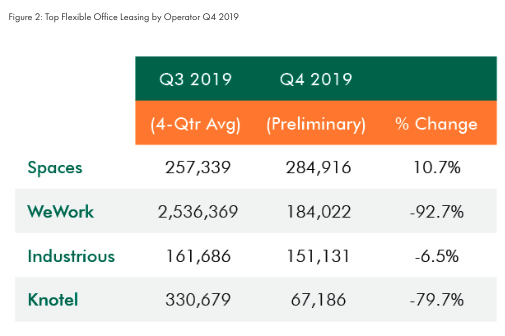

WeWork’s Lease Activity Crashed 93% In 4Q After Failed IPO

Several months after WeWork’s failed IPO — resulting in a bailout from SoftBank, the money-losing office-sharing company leased just four new sites for a combined 184,00 sq. Ft. of space in 4Q19, marking a 93% plunge from its quarterly average rate of 2.54 million sq. Ft. over the last four quarters, according to data from real estate firm CBRE shared with CNBC.

The abrupt slowdown in leasing activity comes as the WeWork’s valuation imploded last August after it shelved its IPO and ran out of cash a month later, forcing its largest investor, SoftBank, to conduct an emergency bailout to rescue the company.

With a questionable business model and no plans on turning a profit, WeWork’s valuation plunged from $47 billion in late 2018 to $8 to $10 billion by 4Q19.

In 4Q19, WeWork had to cut costs, lay off workers, and scale back operations across the world to avoid going bankrupt. In return, the company lost the top spot in the flexible office leasing space to Regus, which in 4Q19, increased lease footprint by 11% to 284,916 sq. Ft.

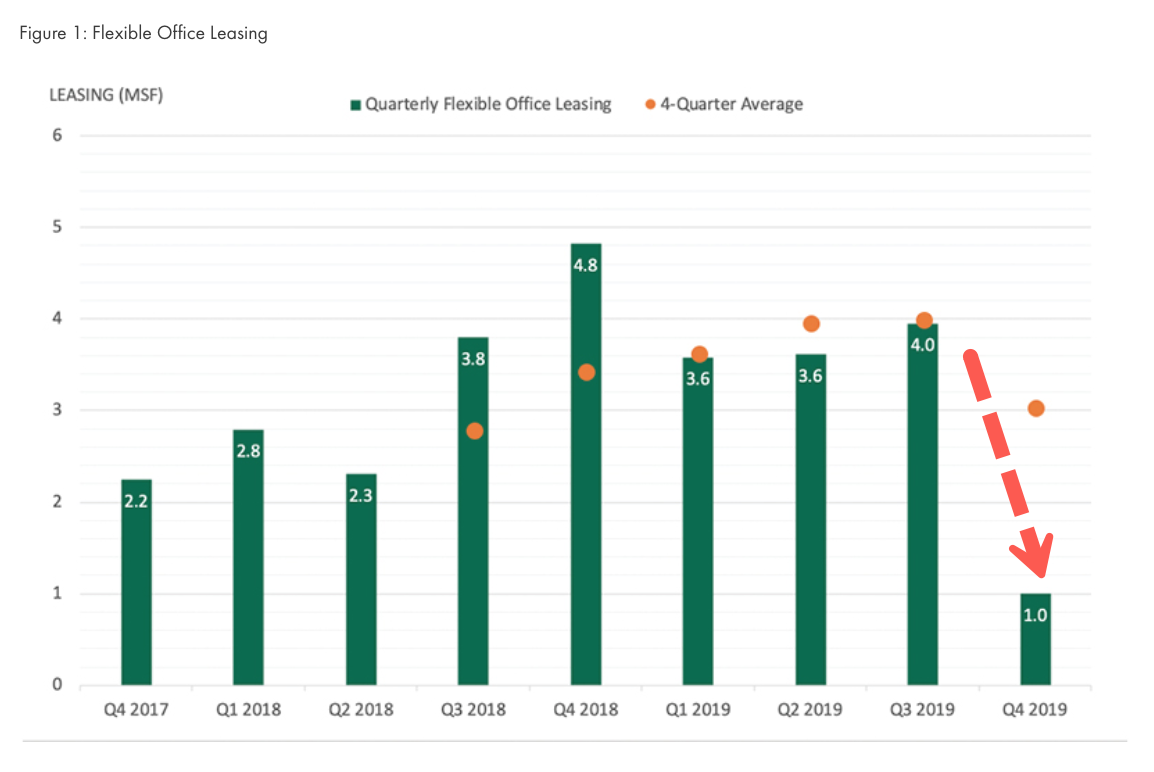

CBRE showed that industrywide, there was a significant pullback in office space leasing, mainly due to WeWork’s implosion.

Data shows office sharing operators declined to 1 million sq. Ft. in 4Q19 from 4 million sq. ft. in 3Q19.

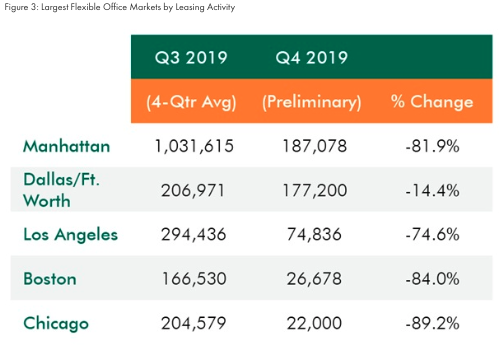

Manhattan was the top city for office sharing space, even though new space leased dropped 82% to 187,078 sq. Ft., on average, the prior four quarters. Activity in Chicago, Boston, and Los Angeles also saw notable declines over the period.

“We had seen this coming right after the IPO news,” said Julie Whelan, senior director of research at CBRE, who warned it could be a bumpy ride for WeWork and other office space sharing companies in 2020.

While I have reflected on the corrosive effects that fake and distorted media are having on our society’s well-being for the past few years, I am now more concerned about it than ever.

To me media distortions + great polarity + the upcoming elections = a significant risk to quality democracy.

It is no longer controversial to say that media distortions are a serious problem. Even most of the media folks I speak with share my concern. As Martin Baron, the Washington Post’s Executive Editor, said in reflecting on the problem, “If you have a society where people can’t agree on the basic facts, how do you have a functioning democracy?”

This is not just a fringe media problem; it is a mainstream media problem. A 2019 Gallup study said that only 13 percent of Americans surveyed have “a great deal” of trust in the media. Only 41 percent of those surveyed said that they have either a “fair” or “great deal” of trust in media. That compares with 55 percent having such confidence in 1999 and 72 percent in 1976. The dramatically decreased trustworthiness has even plagued icons of journalistic trust such as The Wall Street Journal and The New York Times, as sensationalism and commercialism have superseded accuracy and journalistic integrity as primary objectives.

A number of media writers have in private told me that their editors have specifically hired them to write negative, sensationalistic stories because they sell best. They explained that the financial decline of print media and the public’s short attention span have required them to produce such attention-grabbing headlines and stories or face financial decline.

I also see this problem becoming a greater issue —perhaps the greatest issue—of the presidential election. One very senior political strategist explained that in the upcoming presidential election only about 500,000 people—i.e., the swing voters in the swing states—will determine the election and the way these voters will be won is with critical sensationalistic headlines. As a result, this strategist works with those in the media to bring that about. To me that is a clear threat to democracy.

To be clear, I am not saying that distorted media is coming from all people in the news media or in all publications. In fact there are a number of true journalists and publications that seek to convey accurate information and there are newer outlets in new formats such as podcasts that produce excellent media. Also, social media platforms like the platform we are now communicating on allow large groups of people to communicate directly whereas in the past traditional media controlled all large-scale communications. Still, the problem remains.

What can be done to fix this problem? While I’m no expert on this, I will throw out a few thoughts.

The news media is unique in being the only industry that operates without quality controls or checks on its power. It has so much unchecked power that even the most powerful people and companies are afraid to speak out against it for fear of recrimination. At the same time we all treasure our free press. I think it would be terrible for our government to regulate it.

Perhaps because the loss of credibility is a threat to the media, prominent media organizations might explore ways of self-regulating the quality of what they are producing, or create ratings in the way the Motion Picture Association of America provides its movie ratings. If the industry created a self-regulatory organization that set standards and conveyed assessments of quality as is done in a number of other industries, perhaps that would work. Or perhaps private organizations—perhaps NGOs—would come forth to rate the quality of major media outlets accuracy.

Sen. Rand Paul is quoted on the front page of the Washington Post [here] this morning:

“Look, no Republicans were for the inquiry to begin with so why would be under any sort of obligation to feel like we need to complete the work that we never even agreed should’ve been begun in the first place?”

What a weird principle he’s working with! “I didn’t agree that you should have undertaken that inquiry, so regardless of what you turned up I have no obligation to see that it reaches a fair result”?

How about this for an answer: Because the country will be well-served (what a concept!) if and when we all know, whichever way it turns out, whether our president used the power of his office to exchange financial aid for assistance in an upcoming political campaign? Or: Because whether or not you agreed that the inquiry should have been begun in the first place, it has turned up evidence that is at the very least consistent with a very troubling narrative involving presidential misconduct, and some of us, at least, want to find out if that is actually what happened? Or: Because this is not a game of “Who’s Better: The House or the Senate,” and “Nyah, nyah nyah nyah nyah” is not an appropriate reaction to a serious constitutional crisis.

from Latest – Reason.com https://ift.tt/361LH45

via IFTTT

Sen. Rand Paul is quoted on the front page of the Washington Post [here] this morning:

“Look, no Republicans were for the inquiry to begin with so why would be under any sort of obligation to feel like we need to complete the work that we never even agreed should’ve been begun in the first place?”

What a weird principle he’s working with! “I didn’t agree that you should have undertaken that inquiry, so regardless of what you turned up I have no obligation to see that it reaches a fair result”?

How about this for an answer: Because the country will be well-served (what a concept!) if and when we all know, whichever way it turns out, whether our president used the power of his office to exchange financial aid for assistance in an upcoming political campaign? Or: Because whether or not you agreed that the inquiry should have been begun in the first place, it has turned up evidence that is at the very least consistent with a very troubling narrative involving presidential misconduct, and some of us, at least, want to find out if that is actually what happened? Or: Because this is not a game of “Who’s Better: The House or the Senate,” and “Nyah, nyah nyah nyah nyah” is not an appropriate reaction to a serious constitutional crisis.

from Latest – Reason.com https://ift.tt/361LH45

via IFTTT

Are you ready for this week’s absurdity? Here’s our Friday roll-up of the most ridiculous stories from around the world that are threats to your liberty, your finances, and your prosperity.

Feds steal $80,000 life savings from a confused elderly man

79 year old Terry Rolin kept his entire life savings in cash at his home in Pittsburgh. Inside a tupperware food container, he had saved $82,373 over his life working as a railroad engineer.

When he started to become confused at times, he realized his mental health was in decline. So he gave the cash to his daughter Rebecca and asked her to open a joint bank account with him, to keep his money safe.

Rebecca had an early morning flight to catch with no time to visit a bank, so she took the cash with her after checking online and confirming that it is perfectly legal to carry large amounts of cash on an airplane.

But the TSA became suspicious after seeing the cash at a security checkpoint. They alerted the Drug Enforcement Agency (DEA).

The DEA agent intimidated Rebecca into calling her father to confirm the story. Awakened from sleep, he sounded confused–the whole reason for the joint account in the first place.

So the DEA agent told Rebecca their stories didn’t match, and he seized every penny of the old man’s life savings.

Terry and Rebecca were never charged with a crime– they were victims of Civil Asset Forfeiture.

And unfortunately, horror stories like these are not isolated incidents. Now Terry and Rebecca are part of a class action lawsuit for innocent airline passengers who have never been convicted or even charged with a crime to have their stolen cash returned.

Woman arrested in India for concealing 1.2kg of gold in her rectum

People don’t trust their government in India, a country legendary for graft and corruption. This is especially true when it comes to money.

A few years ago, for example, India’s government announced that certain cash notes would be cancelled and no longer considered valid currency with IMMEDIATE effect.

This was debilitating for tens of millions of people across India’s poverty-stricken villages who have no access to bank accounts and rely on cash transactions.

It’s one of the many reasons why GOLD is so popular in India. But the government has plenty of restrictions for precious metals as well… prompting a surge in illegal gold smuggling into the country (according to India’s Director of Revenue Intelligence).

Just last week a woman was arrested in New Delhi’s Indira Gandhi Airport for smuggling an unbelievable 1.2 kilograms (2.65 pounds) of gold in her rectum, worth about USD $60,000.

It’s a pretty sad state of affairs when people are forced to do something so drastic just to make sure they have an honest currency that can’t be manipulated by bureaucrats.

India’s government is finally starting to wake up to this reality and is reportedly ‘considering’ loosening some of the restrictions.

City officials shut down restaurant because it got shot at

Rita Johnson owns a restaurant in Saginaw, Michigan.

One night when the eatery was rented out to a private party, it became the victim of a random shooting. Suspects shot at the building and ran away.

Luckily, no one was hurt.

The owner and the guests had no idea why they were targeted, nor by whom. But rather than find the criminals, the city revoked Rita’s permit and shut down the restaurant.

Wait a minute– wasn’t Rita the victim?

Yes. But the city’s excuse was that the restaurant was the site of criminal activity. The town also cited “Failure to maintain adequate security. . .”

This is pretty ironic coming from a city government that charges taxpayers a bunch of money for basic services, like, oh I don’t know, police??? Seems like it would have been the Saginaw Police Department’s job to maintain adequate security for taxpaying business owners.

US Supreme Court declines to hear “Free the Nipple Case”

A New Hampshire woman was arrested after performing yoga topless on the shores of Lake Winnipesaukee.

This occurred in the city of Laconia in May of 2016 (presumably on one of the handful of days each year that it’s warm enough to go topless in New Hampshire).

Two other women were subsequently arrested for a bare-chested “Free the Nipple” protest after the first arrest.

The town’s ordinance bans women from going topless, but allows men the freedom. Yet the New Hampshire Supreme Court ruled that the ordinance was not a violation of the 14th amendment’s requirement that laws be applied evenly.

Now the US Supreme Court has refused to hear the case, leaving the ban in place.

Neel Kashkari Appeals To “QE Conspiracists”: Show Me How The Fed Is Moving Stock Prices… So Here It Is

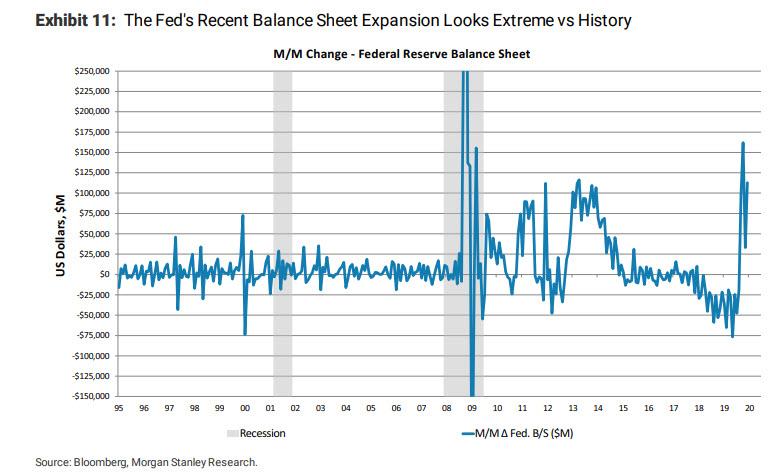

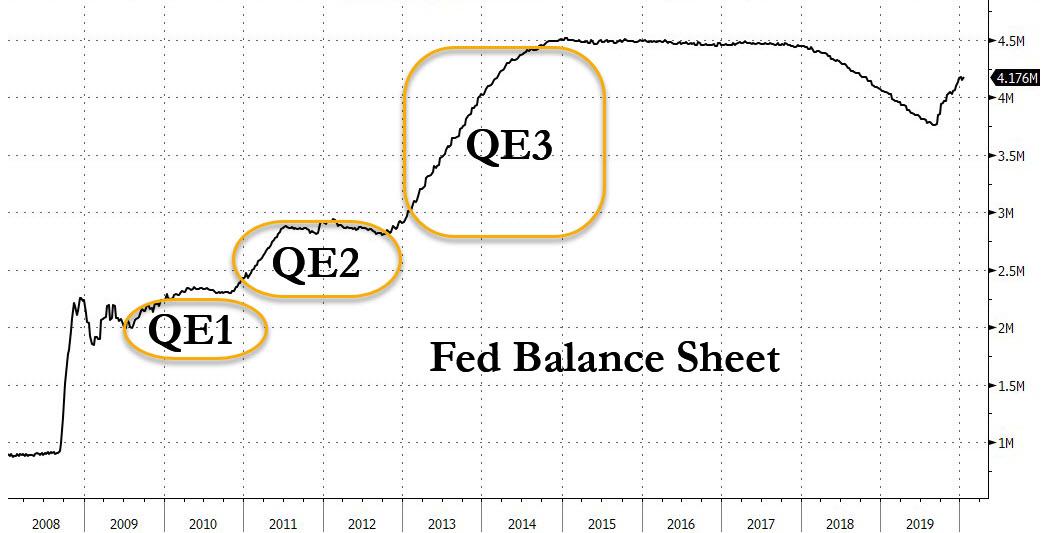

Things are starting to get surprisingly heated at the Fed, now that not only Wall Street strategists, and traders but also Fed presidents are starting to tell the truth about how the Fed’s “NOT QE”, which sorry but we will call it by its real name QE 4, is pushing stocks to ridiculous nosebleed record levels (as one can see by the relentless meltup in the S&P over the past four months), at valuations that are now higher the dot com days.

It all started when, in a moment of bizarre honesty, Dallas Fed president and former Goldmanite Robert Kaplan admitted in a Bloomberg interview that the expansion of its balance sheet was helping to lift asset prices. Commenting on the Fed’s massive liquidity response to the JPMorgan-precipitated repo-market crisis (it’s not just our view that Jamie Dimon caused the repo crisis), which triggered not only the first Fed use of repos since the financial crisis, but also $60 billion in monthly T-Bill QE, Kaplan said that “my own view is it’s having some effect on risk assets”, adding that “It’s a derivative of QE when we buy bills and we inject more liquidity; it affects risk assets. This is why I say growth in the balance sheet is not free. There is a cost to it.“

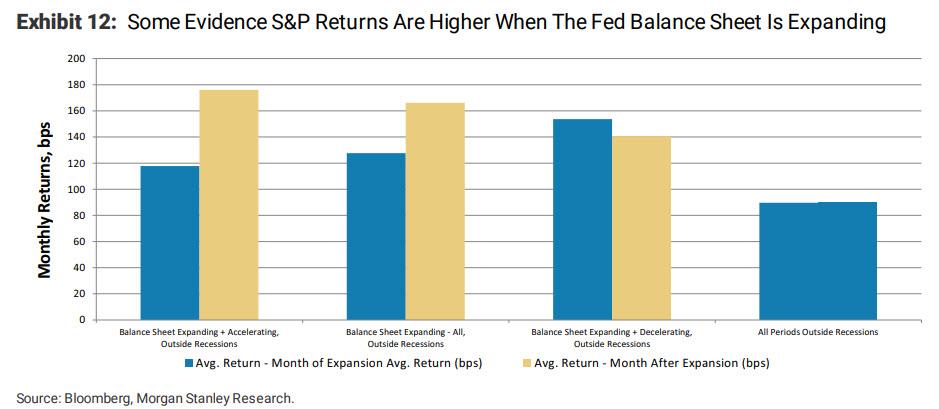

This interview followed just days after one of Wall Street’s most closely followed strategists, Morgan Stanley’s Michael Wilson wrote a report in which he said that “as the Fed has expanded the size of its balance sheet, we have been of the view that the resultant excess liquidity has been beneficial for stock prices and multiples. The potential impact of the Fed on equities has been a central feature of almost all our client conversations the last few months. Most clients suspect that there is some positive impact, though the transmission mechanism and quantification of that impact are hard to pin down, limiting confidence in its durability now that asset prices appear ahead of the fundamentals (Exhibit 1). Since the Fed has rarely expanded its balance sheet at the pace it has been on since October there is limited history to analyze, but we found some evidence that periods of balance sheet expansion have lined up with above average equity returns.”

Wilson then noted that “an expanding balance sheet outside of recessions has coincided with above-average monthly returns for the S&P”, something we have been pointing out since October.

Kaplan’s long-overdue admission, which confirmed everything we have said since 2009, prompted an avalanche of cathartic hot-takes from traders who, until now, had kept silent out of fear of being ostracized by their colleagues for espousing such a “tinfoil” conspiracy theory, first and foremost Bloomberg’s Richard Breslow who yesterday published a furious screed slamming the Fed for, well, everything we have been accused it of doing since 2009. Here, again, are the highlights:

Well the cat’s out of the bag. The worst kept secret in the financial world is now not only accepted orthodoxy, but finally being discussed openly by, at least some, authorities. Central bank policies are directly driving asset prices and the bubbles therein. It’s what they do. It has been so stunningly obvious that, at this point, it makes a mockery of things to deny it as an ongoing, and essential, part of how their strategy is implemented. Oddly enough, however, it’s a revelation that is, apparently, coming late to many people with a lot of savings and nothing to show for it. And it is an undeniable factor in this January’s price action.

Alan Greenspan knew it to be the case. Ben Bernanke had no problem with it. His strategy required it. Jerome Powell, was probably initially not enamored about it but saw no way around it. It fell on ardent loyalists to take his insistence that it was “not QE” with any seriousness. Otherwise, they would have had to admit to knowing little about financial markets

In some ways it was refreshing that Dallas Fed President Robert Kaplan openly talked about it in an interview Wednesday. Although he did couch it in terms that implied it was a matter of some concern to him. But, of course, he went on to say, “we’ve done what what we need to do up until now.” He doth protest, just not so much. Their ability to drive investor behavior is so well established that what is going on in the markets can’t remotely be seen as an unintended, or even unwanted, consequence

At this point, is it a bad thing to admit something that is so patently evident to everyone? The answer is probably yes. They have always been responsive to financial conditions. In many ways they’ve been transfixed by them. Now they are openly acknowledging that they own them. And once you do so, it becomes harder than ever, if even at all possible, to give them back. Kaplan said they need to “come up with a plan and communicate a plan for winding this (balance sheet) down.” That would be nice. And good luck with that.

Never mind that Chairman Jerome Powell tells everyone his efforts to shore up funding markets are “in no sense” QE. Try as policy makers may, they’ve lost the ability to convince people that Treasury purchases aren’t at least partially why the Dow Jones Industrial Average is up almost 4,000 points since late August.

Sure, it’s all labels. If you want to call it QE, you can. Or not. If you want to ascribe the rally to Powell, that’s up to you. Certainly the Fed thinks it’s on solid ground. Rather than trying to drive down long-term interest rates to stimulate the economy, a la QE, it’s simply buying T-bills to keep the financial system’s plumbing in order.

“Whether the Fed’s liquidity injection impacted directly the economy or the pricing of assets or not, it’s certainly true that a lot of people think it did,” said Jim Paulsen, Leuthold Group Inc.’s chief investment strategist. “Whether anything is going to change if the Fed takes it away doesn’t matter. If enough people feel it will, then it’s going to impact markets.”

It’s a tad ironic that for all his attempts to convince the market that QE4 is “not QE”, Powell who in October said that “Growth of our balance sheet for reserve management purposes should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis”, has less influence on the market’s interpretation of his own actions than, say, fringe, conspiracy blogs.

But we digress.

Fast forward to this morning, when in the latest attempt to preserve the last ounce of Fed credibility with strategists, traders, news services and even its own members are calling the Fed out on its stock market pumping, Minneapolis Fed president, and another former Goldmanite, Neel Kashkari issued a derogatory appeal to “QE conspiracists”, which now includes his Fed peers (and Goldman alumni) such as Robert Kaplan, in which he says that:

“QE conspiracists can say this is all about balance sheet growth. Someone explain how swapping one short term risk free instrument (reserves) for another short term risk free instrument (t-bills) leads to equity repricing. I don’t see it. /end “

QE conspiracists can say this is all about balance sheet growth. Someone explain how swapping one short term risk free instrument (reserves) for another short term risk free instrument (t-bills) leads to equity repricing. I don’t see it. /end

Something tells us that when Goldman was giving the lesson on how the Fed creates endogenous liquidity, Kaplan was present and Kashkari was out drafting his TARP bailout vision on a napkin, for the simple reason that the uberdovish Fed president who continues to push for lower rates, appears unable to grasp that both T-Bill monetizations and repo injections create incremental liquidity for financial institutions, something which the 10% rate that overnight G/C repo hit on Sept 16 2019 showed, had suddenly evaporated and prompted the Fed to scramble and inject hundreds of billions in liquidity in the next 4 months.

It was this massive liquidity injection, and not the “asset swap” aspect of QE that has lead the market – and Robert Kaplan – to correctly conclude that the Fed “affects risk assets.“

That said, we can commiserate with Kashkari for not being able to grasp how the Fed’s excess liquidity, which is supposed to assist dealer banks which ended up with insufficient liquidity during the repo crisis, is transformed into a higher risk asset prices. After all, Fed presidents certainly are not expected to understand the nuanced monetary plumbing dynamics of the markets they oversee (what’s that, they are, oh nevermind then…).

And in case Neel would rather get his information from other third party sources, we point him to a December BIS report titled “September stress in dollar repo markets: passing or structural?”, which explains clearly and concisely what the transmission channel is for excess Fed liquidity to result in higher asset prices. To save both Neel and readers the pain of reading the full report (although we certainly feel that Mr Kashkari should finally understand how the plumbing of the US financial system works, especially since this year he is a voting FOMC member and his dovish votes will only make the world’s asset bubble even bigger), we present the following except from the media briefing that was associated with the BIS report, in which Claudio Borio, head of the monetary and economic department at the BIS, laid out everything one needs to know:

high demand for secured (repo) funding from non-bank financial institutions, such as hedge funds heavily engaged in leveraging up relative value trades

This explains the demand side behind the September repo crisis, one which the Fed, Kashkari and virtually everyone else ignores, and instead focuses on the supply, or lack thereof, of liquidity, i.e.:

… the big four banks’ unwillingness to supply the funding, as their liquidity buffers, notably in the form of excess reserves with the Fed, were running low.

And while the Fed did everything in its power to boost the supply side by first opening up the repo taps and then launching QE4, it remained ignorant about the demand side, namely the hedge funds that were using repos to massively lever up on tiny arb pair trades which as we explained in December, consisted of buying US Treasuries while selling equivalent derivatives contracts, such as interest rate futures, and pocketing the arb, or difference in price between the two.

Does this remind readers of a trade popularized by another hedge funds in the 1990s? If you said LTCM give yourself a pat on the back. And it was the fear that the repo crisis would transform into an LTCM-like contagion that sparked the Fed’s massive liquidity injection, and also the resultant surge in risk prices once concerns about the viability of hedge funds dissipated.

And here, once again for the benefit of Kashkari, this is how the BIS explains how the financial system came close to the verge of collapse on September 16, poetically enough the 11 year anniversary of Lehman’s bankruptcy:

Shifts in repo borrowing and lending by non-bank participants may have also played a role in the repo rate spike. Market commentary suggests that, in preceding quarters, leveraged players (eg hedge funds) were increasing their demand for Treasury repos to fund arbitrage trades between cash bonds and derivatives. Since 2017, MMFs have been lending to a broader range of repo counterparties, including hedge funds, potentially obtaining higher returns. These transactions are cleared by the Fixed Income Clearing Corporation (FICC), with a dealer sponsor (usually a bank or broker-dealer) taking on the credit risk. The resulting remarkable rise in FICC-cleared repos indirectly connected these players. During September, however, quantities dropped and rates rose, suggesting a reluctance, also on the part of MMFs, to lend into these markets (Graph A.2, right-hand panel).Market intelligence suggests MMFs were concerned by potential large redemptions given strong prior inflows. Counterparty exposure limits may have contributed to the drop in quantities, as these repos now account for almost 20% of the total provided by MMFs.

So where does that leave us? Well, as the BIS concludes, since 17 September, “the Federal Reserve has taken various measures to supply more reserves and alleviate repo market pressures. These operations were expanded in scope to term repos (of two to six weeks) and increased in size and time horizon (at least through January 2020). The Federal Reserve further announced on 11 October the purchase of Treasury bills at an initial pace of $60 billion per month to offset the increase in non-reserve liabilities (eg the TGA). These ongoing operations have calmed markets.”

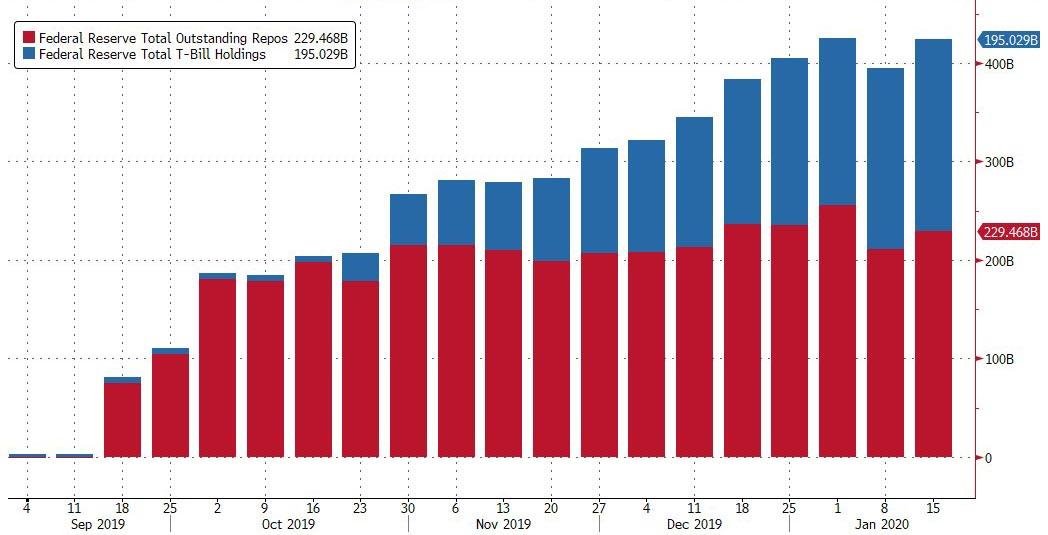

We have covered all these mitigating events, and the problem is that even though the Fed has now injected $230BN in liquidity via overnight and term repos, and $195BN via permanent T-Bill purchases, or POMO (i.e. “QE 4”), expanding the Fed’s balance sheet by $322 billion, the repo market still remains broken.

Worse, in order to keep banks well supplied with liquidity and hedge funds content and preventing them from closing out of these massively levered pair trades, last week repo expert Scott Skyrm said that the problem with the broken repo market and the Fed’s respective Repo operations, similar to the problem observed with QE and the Fed’s balance sheet in general over the past decade, is that the market is now addicted to the easy Fed liquidity.

As Skyrm wrote, “it’s easy to see how the Repo market can get addicted to easy cash from the Fed when the stop-out rates for the RP operations are 1.55% – behind the offered side of the market.” But, as the repo strategist adds, as the Fed keeps injecting cash, the market gets used to it.

Which is great in the short-term as it sends risk assets soaring as hedge funds put on even more risk-chasing trades via repo, but becomes a major issue over the long-term: “The long-term problem is that the some investor cash (real money cash) that was once going into the Repo market is now going elsewhere”, Skyrm explains. Indeed, the problem is that repo rates are trading in the lower end of the fed funds target range. When GC rates were higher in the range, Repo general collateral, as an investment, was more competitive than other overnight rates. But now that cash has gone to other markets, meaning the Fed is trapped in providing liquidity in perpetuity unless it hikes rates which in turn will cause a market crash.

In short, just as the market got addicted to QE and the result was a 20% drop in the S&P in late 2018 when markets freaked out about Quantitative Tightening, the Fed’s shrinking balance sheet, and declining liquidity, Skyrm cautions that “it will take pain to wean the Repo market off of cheap Fed cash” since “it‘s a circle” which can be described as follows:

For the Fed to end daily RP ops, they need outside cash to come back into the Repo market. For the Repo market to attract cash, Repo rates need to move higher. For rates to move higher, the Fed needs to stop RP ops.

The problem is that stopping RP ops could spark another repo market crisis, especially with $230BN in liquidity still being pumped currently via Repo. It also means that the Fed is now unilaterally blowing a market bubble with its repo and “NOT QE” injections, and yet the longer it does so the more impossible it becomes for the Fed to extricate itself from the liquidity pathway without causing a crash.

Or stated simply, the longer the Fed avoids pulling the repo liquidity band-aid, the bigger the market fall when (if) it finally does. The question then becomes whether Powell can keep pushing on the repo string until the November election, because a market crash in the months preceding it, especially since it will be of the Fed’s own doing, will result in a very angry president.

Krishna Memani, former vice chairman of investments at Invesco, agrees: “Powell went out of his way to explain that it wasn’t QE, but it doesn’t really matter. The Fed is in a bind. Effectively with policy initiatives they have, they have to increase reserves, and investors are aware of that. They will be in that mode for the foreseeable future.”

Angry 17-Year-Old Girl Threatens World Leaders In Davos: “You Haven’t Seen Anything Yet”

Never one to miss an opportunity to grab some attention and tell grown-ups how mean they are, Great Thunberg – the 17-year-old figurehead of environmentalism – addressed a large crowd (organizers claimed 15,000) in Switzerland, warning world leaders ahead of next week’s Davos meetings that “you haven’t seen anything yet.”

The so-called eco-warrior repeated her oft-heard comments that:

” So far during this decade we are seeing no sign whatsoever that real climate action is coming.

That has to change. This is just the beginning. You haven’t seen anything yet. We assure you of that.“

Her fearmongering appears to be working as the young people in the crowd held up terrified-sounding signs including:

“Fear for our glaciers”

“HELP the Koalas”

“One, two, three degrees! It’s a crime against humanity!”

“Let’s Change The System, Not the Climate”

“There Is No Planet B”

“I Have a Green Dream”

“We Want A Cooler Planet”

Thunberg is due to address the summit in the Swiss Alpine resort of Davos next week with a call on governments and financial institutions to stop investing in fossil fuels.

She will reportedly tell her corporate audience that it is ‘madness’ to continue investing in fossil fuels as disasters such as the wave of wildfires in Australia focus new attention on the baleful effects of rising temperatures

Does anyone else look at the image below and think of Monty Python’s Life Of Brian: “she’s not the messiah, she’s a very naughty girl”?

My new book Free to Move: Foot Voting, Migration, and Political Freedom will be published by Oxford University Press in April. It is now available for preorder on Amazon (where if you order now, you can get the benefit of any price reductions Amazon does between now and the release date), at the Oxford UP website, and elsewhere. If you contact me, I can send you a code that will entitle you to a 30% discount at Oxford UP site. A Kindle/e-book version should be available for preorder within the next 2-3 months.

Here is the publisher’s summary:

Ballot box voting is often considered the essence of political freedom. But it has two major shortcomings: individual voters have little chance of making a difference, and they also face strong incentives to remain ignorant about the issues at stake. “Voting with your feet,” however, avoids both of these pitfalls and offers a wider range of choices. In Free to Move, Ilya Somin explains how broadening opportunities for foot voting can greatly enhance political liberty for millions of people around the world.

People can vote with their feet through international migration, by choosing where to live within a federal system, and by making decisions in the private sector. These three types of foot voting are rarely considered together, but Somin explains how they have major common virtues and can be mutually reinforcing. He contends that all forms of foot voting should be expanded and shows how both domestic constitutions and international law can be structured to increase opportunities for foot voting while mitigating possible downsides.

Somin addresses a variety of common objections to expanded migration rights, including claims that the “self-determination” of natives requires giving them the power to exclude migrants, and arguments that migration is likely to have harmful side effects, such as undermining political institutions, overburdening the welfare state, increasing crime and terrorism, and spreading undesirable cultural values. While these objections are usually directed at international migration, Somin shows how a consistent commitment to such theories would also justify severe restrictions on domestic freedom of movement. That implication is an additional reason to be skeptical of these rationales for exclusion. By making a systematic case for a more open world, Free to Move challenges conventional wisdom on both the left and the right.

“In this excellent book, Somin makes a compelling case that migration –or foot voting—provides far more political power than voting. Any one voter has a trivially small chance of altering an election, but any household can choose a new state and local government by simply moving.This insight implies that devolving power to local governments will generate far more political voice than any conceivable reform to national elections. Freer international migration would empower even more people to choose their own government. Somin’s case is strong, his thinking is clear, and his writing is eloquent.”—Edward Glaeser, Fred and Eleanor Glimp Professor of Economics, Harvard University, and author of The Triumph of the City

“Ilya Somin shows that mobility-the freedom to move from here to there-might be the most underrated underpinning of a free society. It is especially important in America, where states can compete with one another to have social policies welcoming to enterprise and liberty.Voting is important; so is what Somin calls ‘foot voting.'”– George F. Will, columnist, Washington Post, and author of The Conservative Sensibility

“This eminently readable, tightly-argued, and compelling book is a model for how empirically-informed democratic theory ought to proceed. Somin shows us that in modern democracies, even when everyone has equal voice, that voice is usually close to worthless. Taking political freedom seriously requires a serious solution: foot voting. We need to ensure everyone has the right and power to move and work where they please. Exit beats voice almost every time, and the competition isn’t even close. Somin deftly considers and rebuts every major objection to his view. In the end, the conclusion is inescapable: the arguments for democracy don’t so much justify participatory democracy; they instead justify real freedom of movement.”– Jason Brennan, Robert J. and Elizabeth Flanagan Family Term Professor of Strategy, Economics, Ethics, and Public Policy, McDonough School of Business, Georgetown University; author of The Ethics of Voting

“Ilya Somin has done it again, producing a compelling new book, rich with insights about democratic theory, law, and economics. Free to Move takes a familiar idea-that people should be allowed and encouraged to choose the entities that govern them by moving between jurisdictions-and shows why it is valuable and how taking it seriously as a form of political choice provides a clear set of answers to some of our most pressing social problems. Those who share Somin’s belief in the value of ‘voting with your feet,’ will see the scope of their commitment pushed by his consistency and range, and those who do not will find themselves challenged and perhaps even convinced.”– David Schleicher, Professor, Yale Law School

For universities and other organizations that might be interested, I am available for speaking engagements related to the book. If you are an academic and assign the book to your class, I will speak to the class remotely by Skype for free, if you are interested.

By now you are probably thinking that this post is shameless self-promotion by a book author. I plead guilty to that charge! But, for what it is worth, I also intend to donate 50% of all royalties generated by Free to Move to charities benefiting refugees.

I will write more about the book closer to the publication date.

from Latest – Reason.com https://ift.tt/2sylV9Q

via IFTTT

My new book Free to Move: Foot Voting, Migration, and Political Freedom will be published by Oxford University Press in April. It is now available for preorder on Amazon (where if you order now, you can get the benefit of any price reductions Amazon does between now and the release date), at the Oxford UP website, and elsewhere. If you contact me, I can send you a code that will entitle you to a 30% discount at Oxford UP site. A Kindle/e-book version should be available for preorder within the next 2-3 months.

Here is the publisher’s summary:

Ballot box voting is often considered the essence of political freedom. But it has two major shortcomings: individual voters have little chance of making a difference, and they also face strong incentives to remain ignorant about the issues at stake. “Voting with your feet,” however, avoids both of these pitfalls and offers a wider range of choices. In Free to Move, Ilya Somin explains how broadening opportunities for foot voting can greatly enhance political liberty for millions of people around the world.

People can vote with their feet through international migration, by choosing where to live within a federal system, and by making decisions in the private sector. These three types of foot voting are rarely considered together, but Somin explains how they have major common virtues and can be mutually reinforcing. He contends that all forms of foot voting should be expanded and shows how both domestic constitutions and international law can be structured to increase opportunities for foot voting while mitigating possible downsides.

Somin addresses a variety of common objections to expanded migration rights, including claims that the “self-determination” of natives requires giving them the power to exclude migrants, and arguments that migration is likely to have harmful side effects, such as undermining political institutions, overburdening the welfare state, increasing crime and terrorism, and spreading undesirable cultural values. While these objections are usually directed at international migration, Somin shows how a consistent commitment to such theories would also justify severe restrictions on domestic freedom of movement. That implication is an additional reason to be skeptical of these rationales for exclusion. By making a systematic case for a more open world, Free to Move challenges conventional wisdom on both the left and the right.

“In this excellent book, Somin makes a compelling case that migration –or foot voting—provides far more political power than voting. Any one voter has a trivially small chance of altering an election, but any household can choose a new state and local government by simply moving.This insight implies that devolving power to local governments will generate far more political voice than any conceivable reform to national elections. Freer international migration would empower even more people to choose their own government. Somin’s case is strong, his thinking is clear, and his writing is eloquent.”—Edward Glaeser, Fred and Eleanor Glimp Professor of Economics, Harvard University, and author of The Triumph of the City

“Ilya Somin shows that mobility-the freedom to move from here to there-might be the most underrated underpinning of a free society. It is especially important in America, where states can compete with one another to have social policies welcoming to enterprise and liberty.Voting is important; so is what Somin calls ‘foot voting.'”– George F. Will, columnist, Washington Post, and author of The Conservative Sensibility

“This eminently readable, tightly-argued, and compelling book is a model for how empirically-informed democratic theory ought to proceed. Somin shows us that in modern democracies, even when everyone has equal voice, that voice is usually close to worthless. Taking political freedom seriously requires a serious solution: foot voting. We need to ensure everyone has the right and power to move and work where they please. Exit beats voice almost every time, and the competition isn’t even close. Somin deftly considers and rebuts every major objection to his view. In the end, the conclusion is inescapable: the arguments for democracy don’t so much justify participatory democracy; they instead justify real freedom of movement.”– Jason Brennan, Robert J. and Elizabeth Flanagan Family Term Professor of Strategy, Economics, Ethics, and Public Policy, McDonough School of Business, Georgetown University; author of The Ethics of Voting

“Ilya Somin has done it again, producing a compelling new book, rich with insights about democratic theory, law, and economics. Free to Move takes a familiar idea-that people should be allowed and encouraged to choose the entities that govern them by moving between jurisdictions-and shows why it is valuable and how taking it seriously as a form of political choice provides a clear set of answers to some of our most pressing social problems. Those who share Somin’s belief in the value of ‘voting with your feet,’ will see the scope of their commitment pushed by his consistency and range, and those who do not will find themselves challenged and perhaps even convinced.”– David Schleicher, Professor, Yale Law School

For universities and other organizations that might be interested, I am available for speaking engagements related to the book. If you are an academic and assign the book to your class, I will speak to the class remotely by Skype for free, if you are interested.

By now you are probably thinking that this post is shameless self-promotion by a book author. I plead guilty to that charge! But, for what it is worth, I also intend to donate 50% of all royalties generated by Free to Move to charities benefiting refugees.

I will write more about the book closer to the publication date.

from Latest – Reason.com https://ift.tt/2sylV9Q

via IFTTT