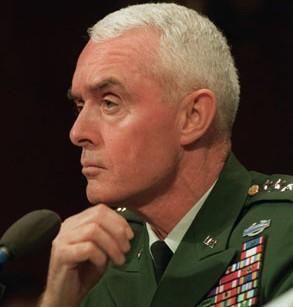

Retired General: Trump’s Syria Oil Plan Turns US Troops Into “Pirates”

After President Trump suggested on Sunday that he would like to make a deal with Exxon Mobil or “one of our great companies” to go into occupied Syria and take the oil, one of the few former top defense officials to explicitly condemn the plan which clearly smacks of naked US imperialism was retired General Barry McCaffrey.

Referencing Trump’s comments, an outraged McCaffrey posed the question on Twitter, “WHAT ARE WE BECOMING… PIRATES?”

He further stressed that the oil “belongs to Syria” and that ultimately “we lack Congressional authority to stay” in the country at all.

US convoy this week in northeast Syria. Image source: AP

The former US Army four star and MSNBC regular was one the few mainstream pundits this week to critique Washington’s Syria policy by questioning the entirety of America’s presence there in the first place, essentially calling it ‘illegal’.

Most establishment commentators have thus far ignored the imperialist aggression aspect of what appears a big oil grab on yet another US-occupied piece of the Middle East, and opted to argue the Pentagon should be “doing more” for the Syrian Kurds —meaning more of the same endless US occupation.

On Monday Defense Secretary Mark Esper spelled out that a deployment of some few hundred US troops will deny Syrian government access to oilfields in the northeast, instead ensuring they stay in Kurdish-led SDF hands.

The immediate justification given by the Pentagon chief was the usual ‘defeat ISIS’ mantra (despite, ironically, their leader Baghdadi being taken out in Saturday’s US raid into Idlib).

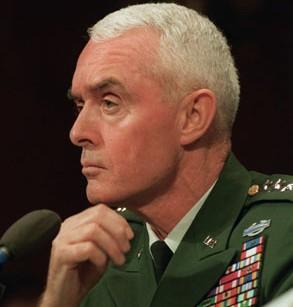

4-Star General Barry McCaffrey

“We want to make sure that SDF does have access to the resources in order to guard the [IS] prisons, in order to arm their own troops, in order to assist us with the ‘defeat ISIS’ mission,” Esper said.

One international legal expert, Anthony Cordesman, told The Guardian of the Pentagon plan that, “In international law, you can’t take civilian goods or seize them. That would amount to a war crime.”

Of course, it’s not as if Washington ever stopped to think twice about such abstract concepts as ‘international law’ — especially when in comes to military action and adventurism in the Middle East.

Oct. 27, 1962, is the date on which we humans were spared extinction thanks to Soviet Navy submarine Captain Vasili Alexandrovich Arkhipov.

Arkhipov insisted on following the book on using nuclear weapons. He overruled his colleagues on Soviet submarine B-59, who were readying a 10-kiloton nuclear torpedo to fire at the USS Randolph task force near Cuba without the required authorization from Moscow.

Communications links with naval headquarters were down, and Arkhipov’s colleagues were convinced WWIII had already begun. After hours of battering by depth charges from US warships, the captain of B-59, Valentin Grigorievich Savitsky, screamed, “We’re going to blast them now! We will die, but we will sink them all — we will not disgrace our Navy!” But Captain Arkipov’s permission was also required. He countermanded Savitsky and B-59 came to the surface.

Much of this account of what happened on submarine B-59 is drawn from Daniel Ellsberg’s masterful book, “The Doomsday Machine” — one of the most gripping and important books I have ever read. Dan explains, inter alia, on pages 216-217 the curious circumstance whereby the approval of Arkhipov, chief of staff of the submarine brigade at the time, was also required.

Ellsberg adds that had Arkhipov been stationed on one of the other submarines (for example, B-4, which was never located by the Americans), there is every reason to believe that the carrier USS Randolph and several, perhaps all, of its accompanying destroyers would have been destroyed by a nuclear explosion.

Equally chilling, says Dan:

The source of this explosion would have been mysterious to other commanders in the Navy and officials on the ExComm, since no submarines known to be in the region were believed to carry nuclear warheads. The clear implication on the cause of the nuclear destruction of this antisubmarine hunter-killer group would have been a medium-range missile from Cuba whose launch had not been detected. That is the event that President Kennedy had announced on October 22 would lead to a full-scale nuclear attack on the Soviet Union.

‘The Most Dangerous Moment in Human History’

Historian Arthur Schlesinger Jr., a close adviser to President John F. Kennedy, later described Oct. 27, 1962, as Black Saturday, calling it “the most dangerous moment in human history.” On that same day, the Joint Chiefs of Staff recommended an all-out invasion of Cuba to destroy the newly emplaced Soviet missile bases there. Kennedy, who insisted that former US Ambassador to Russia Llewelyn Thompson attend the meetings of the crisis planning group, rejected the advice of the military and, with the help of his brother Robert, Ambassador Thompson, and other sane minds, was able to work out a compromise with Soviet leader Nikita Khrushchev.

As for the Joint Chiefs of Staff, the president had already concluded that the top military were unhinged Russophobes, and that they deserved the kind of sobriquet used by Under Secretary of State George Ball applied to them — a “sewer of deceit.” As Ellsberg writes (in his Prologue, p. 3):

“The total death toll as calculated by the Joint Chiefs, from a US first strike aimed at the Soviet Union, its Warsaw Pact satellites, and China, would be roughly six hundred million dead. A hundred Holocausts.” And yet the fools pressed on, as in trying to cross “The Big Muddy.”

Intelligence Not So Good

The pre-Cuban-missile crisis performance of the intelligence community, including Pentagon intelligence, turned out to hugely inept. The US military, for example, was blissfully unaware that the Soviet submarines loitering in the Caribbean were equipped with nuclear-armed torpedoes. Nor did US intelligence know that the Russians had already mounted nuclear warheads on some of the missiles installed in Cuba and aimed at the US (The US assumption on Oct. 27 was that the warheads had not been mounted.)

It was not until 40 years later, at a Cuban crisis “anniversary” conference in Havana, that former US officials like Defense Secretary Robert McNamara and National Security Advisor McGeorge Bundy learned that some of their key assumptions were dead and dangerously wrong. (Ellsberg p. 215ff)

Today the Establishment media has inculcated into American brains that it is a calumny to criticize the “intelligence community.” This is despite the relatively recent example of the concocting of outright fraudulent “intelligence” to “justify” the attack on Iraq in 2003, followed even more recently, sans evidence, falsely accusing Putin himself of ordering Russian intelligence to “hack” the computers of the Democratic National Committee. True, the US intelligence performance on Russia and Cuba in 1962 came close to getting us all killed in 1962, but back then in my view it was more a case of ineptitude and arrogance than outright dishonesty.

As for Cuba, one of the most consequential CIA failures was the formal Special National Intelligence Estimate (SNIE) of Sept. 19, 1962, which advised President Kennedy that Russia would not risk trying to put nuclear-armed missiles in Cuba. To a large extent this judgment was a consequence of one of the cardinal sins of intelligence analysis — “mirror imaging.” That is, we had warned the Russians strongly against putting missiles in Cuba; they knew the US, in those years would not take that kind of risk; ergo, they would take us at our word and avoid blowing up the world over Cuba. Or so the esteemed NIE estimators thought.

The Russians, too, were mirror imaging. Khrushchev and his advisers regarded US nuclear war planners as rational actors acutely aware of the risks of escalation, who would shy away from ending life immediately for hundreds of millions of human beings. Their intelligence was not very good on the degree of Russophobia infecting Air Force General Curtis LeMay and others on the Joint Chiefs of Staff, who were prepared to countenance hundreds of millions of deaths in order “to end the Soviet threat.” (Ellsberg was there; he provides a first-hand account of the craziness in “The Doomsday Machine.”)

Where Did the Grenade Launchers Go?

I reported for active duty at Infantry Officers School at Fort Benning, Georgia, on Nov. 3, 1962, six days after the incident. Most of us new lieutenants had heard about a new weapon, the grenade launcher, and were eager to try it out. There were none to be found. Lots of other weapons normally used for training were also missing.

After we made numerous inquiries, the brass admitted that virtually all the grenade launchers and much of the other missing arms and vehicles had been swept up and carried south by a division coming through Georgia a week or so before. All of it was still down in the Key West area, we were told. Tangible signs as to how ready the JCS and Army brass were to attack Cuba, were President Kennedy to have acceded to their wishes.

Had that happened, it is likely that neither you nor I would be reading this. Yet, down at Benning, there were moans and groans complaining that we let the Commies off too easy.

* * *

Ray McGovern works with Tell the Word, a publishing arm of the ecumenical Church of the Saviour in inner-city Washington. He was an Army infantry/intelligence officer from 1962-64 and later served as Chief of CIA’s Soviet Foreign Policy Branch and morning briefer of the President’s Daily Brief. He is co-founder of Veteran Intelligence Professionals for Sanity (VIPS).

Saudi Sheikh Made Illegal Political Contribution To Obama’s 2012 Inaugural Through Prolific Straw Donor

A Saudi Sheikh and air conditioning magnate made a massive, illegal political contribution to Barack Obama’s inaugural committee in 2012, which was funneled through a prolific (and recently busted) DC straw donor who has operated on both sides of the aisle for years.

Sheikh Mohammed Al Rahbani

According to court documents and an analysis of campaign finance records by The Associated Press, Sheikh Mohammed Al Rahbani attempted to send $850,000 to Obama’s committee – which included a picture with Obama. Of that, straw donor Imaad Zuberi recently pleaded guilty to stealing $752,000. He also admitted to concealing his work as a foreign agent.

Imaad Zuberi, far left, arrives at Trump Tower in New York on Dec. 12, 2016

Zuberi – a top fundraiser for both Obama and Hillary Clinton during their presidential campaigns, marks “the latest in a string of cases that highlight the prevalence of banned foreign money in American politics and the often lax approach campaigns take in vetting contributions,” writes AP.

The criminal case against Zuberi doesn’t explain why Rahbani would have wanted to contribute to American political campaigns.

His company SAFID — a manufacturer of air conditioning-related products — is active throughout the Middle East and says on its website that it has worked on projects financed by the Saudi government.

Rahbani, in a few past interviews, has talked about his support of Obama. He posted pictures on his website of himself and his wife standing with Obama, former Vice President Joe Biden and their spouses at a 2013 inaugural event. The website was taken down shortly after Zuberi’s plea was made public. –The Associated Press

Donations funneled through Zuberi include those to Sen. Lindsey Graham, President Trump’s 2016 inaugural committee, and Democratic Rep. Eliot Engel, chairman of the House Foreign Affairs Committee. Graham gave some of those donations in 2017.

After President Trump’s 2016 victory, Zuberi immediately put on a MAGA hat, pumping “nearly $1 million” into Trump’s inaugural committee from unknown sources.

Zuberi has also been under scrutiny by federal prosecutors in New York after he donated $900,000 to Trump’s inaugural committee and $100,000 to a Republican campaign committee. Those donations occurred around the time Zuberi accompanied Qatar’s foreign minister to a meeting at Trump Tower.

Trump’s inaugural committee has not been accused of wrongdoing in connection with the money it received from Zuberi. It says it has cooperated with the federal inquiry. –The Associated Press

According to FEC records, Zuberi and his family made hundreds of donations to Republicans and Democrats across the political spectrum – often going to influential or outspoken lawmakers, such as Graham and Engel.

One campaign, not identified by name, accepted donations made in the name of one of Zuberi’s dead relatives, prosecutors said. Another political committee took donations from a person Zuberi invented.

Some donations reported by political campaigns were made in Rahbani’s and others’ names but were paid for with credit cards belonging to Zuberi or his wife, prosecutors said.

…

Zuberi has also been under scrutiny by federal prosecutors in New York after he donated $900,000 to Trump’s inaugural committee and $100,000 to a Republican campaign committee. Those donations occurred around the time Zuberi accompanied Qatar’s foreign minister to a meeting at Trump Tower. –The Associated Press

AP draws a parallel between the Zuberi case and two associates of Rudy Giuliani, Lev Parnas and Igor Fruman, who have been charged with making unlawful campaign contributions to US candidates and committees – including a $325,000 contribution to a group which supports Trump’s reelection, at a time when they were lobbying US lawmakers for the ouster of the US ambassador to Ukraine.

And in April, “a Washington political consultant was sentenced to three years of probation after admitting he made a $50,000 straw donation on behalf of a wealthy Ukrainian client who wanted tickets to Trump’s inauguration,” according to the report.

“I’m deeply concerned about foreigners trying to intervene in our elections, and I don’t think we’re doing enough to try to stop it,” said FEC chairwomn Ellen Weintraub. “They don’t get a say in who we elect — or at least they’re not supposed to.“

“The modern central bank business model is being disrupted” claims Saifedean Ammous, economics professor and author ofThe Bitcoin Standard: The Dcentralized Alternative to Central Banking. Ammous’ well-written exposition of an Austrian-School understanding of the nature of money – in a free market and not – concludes with several chapters directed toward the technology and economics of Bitcoin, the original blockchain crypto-currency. He answers the key questions regarding Digital Money (Chapter 8), What is Bitcoin Good For? (Chapter 9), and Bitcoin Questions (Chapter 10).

Professor Ammous sees Bitcoin as another, and very powerful, “disrupter” technology that provides the first real challenge to the global fiat money system run by nation states in a century. That is, it’s the first real challenge since the modern state retreated from the classical gold standard.

Reviewing the work of Austrian-School scholars, including Menger, Mises, and Rothbard, Ammous shows that the three classical attributes of valid market money – scalability, salability and stability – are being met by the digital currency.

He further shows, through a clear technical analysis, that Bitcoin is a superior form of value-conserving money, since it is, unlike all other goods (except human time) “strictly” scarce and not just relatively scarce.

Ammous tackles the toughest issue yet: the relationship between Bitcoin and the fiat central banking system, with its use of the Dollar and Special Drawing Rights to settle accounts between banks. (Gold is hidden somewhere in the background in various vaults.) In the process, he convincingly suggests the transaction costs of using Bitcoin as a non-governmental medium to settle accounts are quite low while the transaction or counterparty risks are virtually zero.

He then argues that, as Bitcoin continues to appreciate against both Gold and Fiat, central banks will find it impossible to continue to ignore Bitcoin as a Reserve against deposits. But then he goes further, in the Austrian tradition of applying general principals to the real world, as Hayek did in his “Denationalization of Money.” Ammous imagines how a nongovernmental (a “Decentralized Autonomous Organization,” as he terms it) banking system based on Bitcoin and on blockchain tokens could be convertible into Bitcoin through third party intermediaries (“banks”) providing affordable, non-fiat, currency transfers.

Ammous’s vision for a freer future leaps from his assertions of how powerfully Bitcoin disrupts the globalists’ fiat central banking system.

Sound money, the professor teaches us, leads to peace and prosperity while unsound money leads to devastation:

“If the modern world is ancient Rome, suffering the economic consequences of monetary collapse … then Satoshi Nakamoto is our Constantine, Bitcoin is our solidus, and the Internet is our Constantinople. For Ammous, Bitcoin serves as a monetary lifeboat for people forced to transact and save in monetary media constantly debased by governments… the real advantage of Bitcoin lies in it being a reliable long-term store of value, and a sovereign form of money that allows individuals to conduct permissionless transactions…”

Ammous’ concludes by arguing that Bitcoin is positioned to be the Global Unit of Account that disrupts the fiat central banking system which has allowed the modern state to engage in levels of tyranny and destruction rarely possible in previous human history:

“Monetary status is a spontaneously emergent product of human action, not a rational product of human design.”

The value of Bitcoin to our liberty and our culture remains to be tested against the realities of our world. But it’s not hard to embrace the hope that Ammous is right.

Masturbating Australians May Soon Have To Use Facial Recognition To Access Online Porn

Australian lawmakers looking to limit kids’ access to online pornography have come up with one possible solution; facial recognition.

“Home Affairs is developing a Face Verification Service which matches a person’s photo against images used on one of their evidence of identity documents to help verify their identity,” reads a recent regulatory filing. “This could assist in age verification, for example by preventing a minor from using their parent’s driver license to circumvent age verification controls.”

Home Affairs has acknowledged that the Face Verification Service was nonoperational, as it required the passage of biometric legislation through Parliament – while last week, the Parliamentary Joint Committee on Intelligence and Security said that new bills do not have sufficient privacy safeguards and needed to be redrafted, according to ZDnet.

In 2016, the first phase of Australian’s biometric Face Verification Service (FVS) was launched, “giving a number of government departments and the Australian Federal Police the ability to share and match digital photos of faces.” Needless to say, the program has expanded beyond its original scope.

Initially, the system was fairly limited. It only included photos of people who had applied to become Australian citizens. And use of the database was supposed to be limited to a handful of government agencies with a compelling need for it.

But since then, the government has steadily expanded the system. Photos from other sources were added to the database. And Australia has been trying to develop a more sophisticated Face Identification Service that can identify unknown persons.-Ars Technica

On Thursday, Committee Chair Andrew Hastie said that the committee heard concerns over privacy and the need to ensure that appropriate oversight was in place to protect individuals’ rights.

“The committee acknowledges these concerns and believes that while the Bill’s explanatory memorandum sets out governance arrangements, such as existing and contemplated agreements and access policies, they are not adequately set out in the current Bill,” he said.

“In the committee’s view, robust safeguards and appropriate oversight mechanisms should be explained clearly in the legislation.”

In other news, brick-and-mortar porn shops and trenchcoat sales may have a bright future in the land down under.

A lot of big names will report third quarter earnings this week, and the results are expected to be worse than the same period in 2018.

The timing comes as the shale sector is facing somewhat of a reckoning. After years of price volatility – with more downs than ups – oil prices have failed to return even remotely close to pre-2014 levels. For several years, shale E&Ps took on debt and issued new equity, promising investors that they would profit both from a rebound in prices and from rapid production growth.

They delivered on gains to output, but not on profits. At some point in the last year, investors really began to lose faith. Oil stocks have been the worst performers in the S&P 500 this year.

The latest release of earnings will probably do little to quell unease from big investors. Oil and natural gas prices have dropped this year, by about 17 percent and 31 percent, respectively. Job cuts have returned and bankruptcies are on the rise again.

The oil majors are pressing forward with their aggressive shale development plans. That may prevent a noticeable decline in production. But their earnings – many of the majors report this week – are expected to be down roughly 40 percent from a year ago, which will raise some tough questions.

Some of the largest banks have slashed their credit lines to smaller shale E&Ps. According to Reuters, JPMorgan Chase, Wells Fargo and the Royal Bank of Canada are among some of the lenders that have reduced the amount of credit they are offering to drillers.

The so-called credit redetermination period happens twice a year, and banks tend to offer financing based on a company’s reserves. Lower prices lower that assessment because some reserves become uneconomic to produce. As a result, the ability to access financing becomes more restricted.

Closing off the ability to borrow money could force more companies into bankruptcy. There have been roughly 199 bankruptcies from North American oil and gas companies since 2015, according to Haynes and Boone, LLP. Through September, there have been 33 bankruptcies in 2019, the highest number since 2016. There were 7 bankruptcies in September alone.

As Reuters notes, the backup plans for stressed shale companies are limited. Asset sales may not be a viable path – M&A activity has fallen sharply as buyers spurn troubled projects. In fact, activity in M&A is so weak that investment banks are slashing positions on their energy desks.

Likewise, returning to equity markets for a cash injection is essentially a non-starter. And as mentioned, banks are loath to agree to lend more. The only option is to cut spending.

Last week, the U.S. rig count fell by 21, the largest decline in six months. In fact, the rig count has declined for 11 consecutive months as drillers pull back.

“As yet, the decline in drilling activity is not reflected in lower production growth, but this is probably only a question of time,” Commerzbank said in a note on Monday.

“It is already the case that shale oil production is rising noticeably only in the Permian Basin, and only slightly at Bakken. It is already falling in other shale plays such as Eagle Ford and Anadarko.”

There is also growing scrutiny on the amount of oil and gas produced relative to what companies have promised. Bloomberg profiled a former hedge fund manager who has paid particular attention to Apache Corp., a company that “shale doubters” believe is overestimating the ratio of oil to gas that some its assets can produce.

This has led some analysts to cut their forecasts for production growth.

“The downgrade reflects lower oil prices, lower rig counts, capital constraints, pipeline bottlenecks and a negative trend in well-productivity,” Rob West, Research Associate at the Oxford Institute for Energy Studies, wrote in a commentary.

“After all, 2019 has been a punishing environment for any company to lower its production guidance, raise its capex or report an operational mishap.”

After Concho Resources revealed disappointing results from its 23-well “Dominator” project a few months ago, which set off a steep slide in its share price, there will probably be intensified scrutiny on any production misses this time around.

However, Rob West of OIES adds that concerns about productivity may be “premature,” and that drillers still have plenty of ways to keep logging productivity gains. The mishaps this year need not be the end of the story, West said.

Still, for now, investors are losing interest, and that may not change until and unless there is a major change in the industry’s outlook. The third quarter results probably won’t provide that catalyst. “People are ignoring shale names now and they’re sort of disgusted with them almost,” Rohan Murphy, an analyst with Allianz Global Investors in London, told Reuters in an interview.

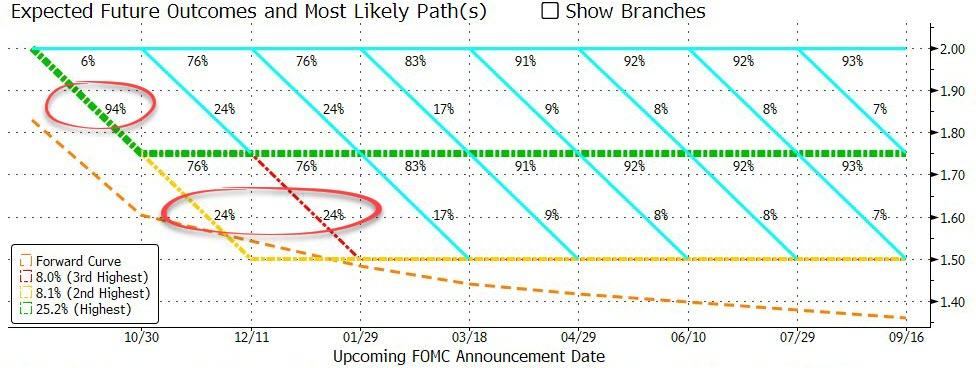

FOMC Preview: If The Fed Doesn’t Cut, Brace For Impact; If The Fed Cuts… Then What?

Press for time? Then the following excerpt from Curvative Securities’ Scott Skyrm is all you need to know what to expect tomorrow:

Given the Fed is in easing mode and dumping liquidity into the market, it is unlikely they will NOT ease tomorrow. With over $200 billion in RP operations and $60 billion a month of QE Lite, it would throw the markets in turmoil if the Fed did not ease. For tomorrow, look for guidance about future rate cuts.

The market is pricing about a 40% chance of another cut within the next five months, though I believe the Fed will pause easing after tomorrow and any future rate cuts will be “data dependent.”

Have a little more free time? Then read on the following FOMC preview, courtesy of RanSquawk:

The Fed is expected to lower rates by 25bps to 1.50-1.75%; key will be whether the Committee signals that it is now on pause, or whether the door to further cuts remains open. While market pricing and the analyst consensus are looking for a rate cut, some – such as Jefferies – have warned that there may be enough for the Fed to pause at this meeting. The FOMC will publish its rate decision on 31st October 2019 at 2:00pm EDT. Post-meeting press conference with Fed Chair Powell scheduled for 2:30pm EDT.

RATES:

The Street expects the Fed to cut rates for the third straight meeting, lowering the federal funds rate target by 25bps to 1.50-1.75%; money markets price the cut with over 90% certainty.

Another two rate cuts are priced in by the end of 2020.

The Fed’s September economic projections envisaged the FFR target at 1.75-2.00% at end of both 2019 and 2020 (rates are currently within this bracket), rising to 2.00-2.25% by end-2021. Any decision to cut rates will likely face dissent from Eric Rosengren and Esther George, both of whom have dissented previously.

IS A CUT A DEAD CERT?

Given the two cuts already implemented, some question whether the FOMC needs to lower rates further. After all, consider that as BofA’s David Woo said earlier this week, “Over the past 30 years the Fed has never cut more than 75bp at a stretch without the US economy going into a recession.“

Diminishing the case for a cut: data has generally held up well (payroll growth close to trend, jobless rate falling to 50-year lows; consumer spending has been stable, and confidence remains firm; CPI has been rising, though this is yet to be seen in PCE; however, internationally, downside surprises in China GDP growth and the subdued outlook in the Eurozone could add to the Fed’s caution, although US/China trade talks have been progressing well, as has Brexit, likely mitigating some of the Fed’s global concerns); meanwhile, equities are lingering near record highs, and financial conditions continue to loosen since September. Fed communications have also been generally constructive, with little signs that policymakers judge the outlook to have materially deteriorated since its last meeting.

However, on the other side of the coin, analysts have noted that the Fed has historically not tended to lean against aggressive market pricing, supporting the case for a cut.

FUTURE SIGNALS:

Looking ahead, markets are expecting just over one cut through the end of the year (including this week’s potential cut), suggesting there is be a feeling that the so-called ‘insurance cuts’/’mid-cycle adjustment’ are done; and looking to next year, markets price one to two rate cuts in 2020.

The notion that if the FOMC cuts, it will be on hold in December is given further credence by the Fed’s ‘insurance cut’ playbook in the 1990s, where on two occasions it cut by a cumulative 75bps before holding rates. How it frames such a ‘pause’ will be crucial; will it explicitly state that rate cuts are over? Will it retain a more data-dependent outlook? Within its statement, attention will be on the line that the Fed will “will act as appropriate to sustain the expansion” which in recent months the market has taken as a sign that additional cuts were on the horizon. The prevailing wisdom appears to be that the Fed will pause, whether or not it explicitly states it, and any further rate cuts may push accommodation to levels that implies it is more than a ‘mid-cycle adjustment’. It is worth keeping an eye on the vote of James Bullard, who last month argued for a deeper 50bps rate cut, which could show the appetite among the doves for further lowering of the FFR target (note: Bullard will vote in October and December, and then will next vote on policy in 2021).

REPO OPERATIONS:

Intra-meeting, the Fed announced that it would purchase T-Bills at a rate of USD 60bln per month. The intra-meeting nature of the announcement is understood to be significant as a signal that the Fed considers these operations as only part of the technical aspects of monetary policy implementation, rather than the sort of balance sheet expansion seen during the crisis, which was designed to crowd investors out of safer assets to help stoke economic activity. Since the Fed began overnight repo operations, its balance sheet has grown by USD 200bln as the central bank offers ample liquidity to prevent any jam-up in repo markets. The Fed has and will continue to emphasize that these operations ‘are not QE’. According to a recent newswire survey, 56% of economists surveyed think the Fed will find enough T-bills for its monthly purchases; 22% believe that the US Treasury will raise its bill issuance to accommodate the Fed; some economists also believe that the Fed will need to boost its bill-buying to include coupon-bearing Treasuries with up to three years in maturities (NOTE: The Treasury’s quarterly refunding announcement is due ahead of the FOMC meeting on Wednesday).

SRF ANNOUNCEMENT:

The Fed is expected to announce a more permanent operation in 2020, with the launch of a standing repo facility. There are many facets that still need to be worked-out, according to reports, like access to the SRF as well as the rates used to enable counterparties to engage with the market without any negative perceptions around the health of the banks; the Fed must also ensure that any SRF does not kill the private sector repo market. Accordingly, Chair Powell may allude to the background work being carried out, but may be light on specifics.

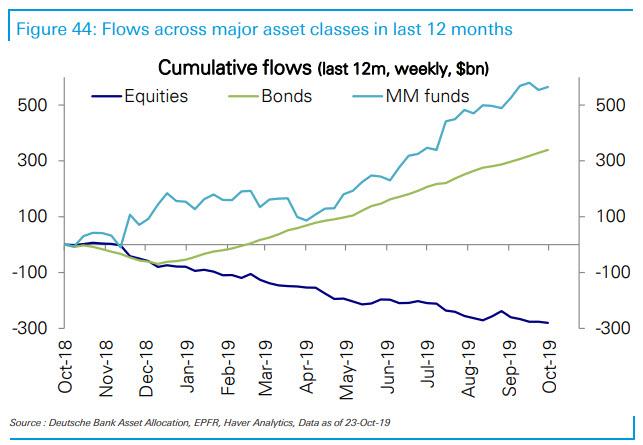

Not Even The Algos Have Any Idea What’s Going On Any More

With the S&P hitting an all time high just as the Fed is set to cut rates for the 3rd time in four months due to the “slowing economy” amid an earnings season that will show the first earnings recession in three years, not to mention near record outflows from stocks (and inflows to bonds)…

… which somehow has resulted in a surge in stocks, even as CEO sentiment crashes to financial crisis lows…

… it is safe to conclude that no human really has a clue what is going on.

But did you know that algos also no longer have any idea what to make of this market?

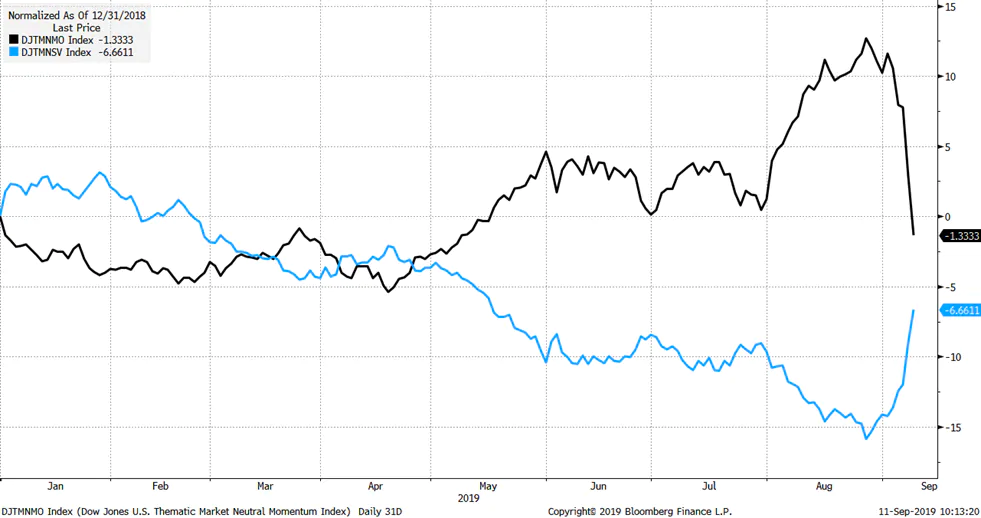

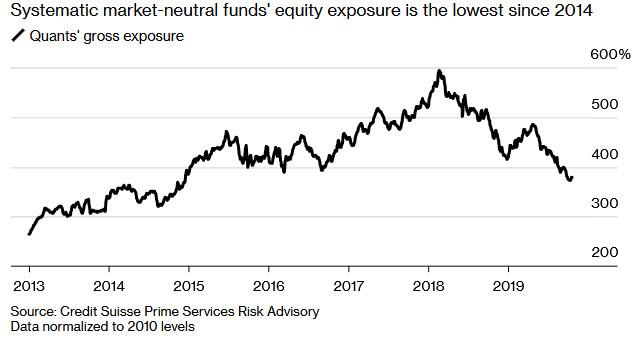

According to Credit Suisse prime brokerage data, market-neutral quants, the ones who got crushed hardest during the September quantastrophe that sent growth stocks tumbling and value stocks surging…

… have cut their gross stock allocations to the lowest in nearly five years, as the following Bloomberg chart shows.

The main reason for the deleveraging – or degrossing – is that quants no longer have a sense of what the market may do at any moment; meanwhile the violent whiplash that market neutral quants suffered during the early-September growth scare, has forced them to take down gross exposure further amid rising factor volatility as the anxiety-ridden rally of 2019 rolls on.

“It looks nice – the market’s up 20%, but it’s been a wild ride underneath the covers,” Mark Connors, global head of risk advisory at Credit Suisse told Bloomberg. “The factor path has been unpredictable.”

And sure enough, after it was left for dead following a decade of underperformance, last week the “value” strategy revived once more as hopes for a U.S.-China trade deal buoyed economic prospects, just weeks after a rotation in the opposite direction driven in part by recession fears.

As Bloomberg notes, while the initial take on such violent, unexplained moves is that they are due to late-cycle fragility as investors turn on every economic and political headline on a dime, Bloomberg also notes that some suspect the choppy rotations have been exacerbated by deleveraging among systematic funds, who find market’s bizarre moves to be too volatile for their current risk profile.

“Quants sometimes can be a canary in the coal mine,” said Melissa Brown, managing director of applied research at Qontigo. “Maybe we are going to see going forward more volatility in style factors as funds need to deleverage or people pull their money.”

Maybe. And if we do, we will see another circular loop emerge, as deleveraging funds force other funds to deleverage, resulting in even less liquidity, more volatility, and even more deleveraging, until some “bottom” is finally reached.

Meanwhile, some factors are becoming even more sensitive to shifts in positioning. The strength of the recent rally – short squeeze if you will – in cheap cyclical shares, for instance, caught many by surprise given the lack of a fundamental catalyst, Bank of America strategists wrote.

Pointing out the blatantly obvious, Los Angeles Capital Management’s Hal Reynolds said that “we are in a choppier environment,” noting that “compression in returns and pick-up in risk have both occurred this year, leading to the reduction in risk budgets.”

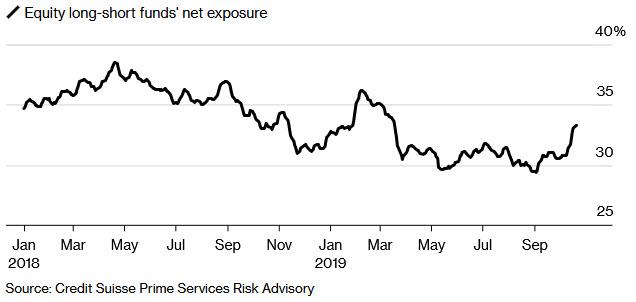

Meanwhile, as quants turned tail, some other – more-carbon driven – hedge funds turned more bullish. For example, macro funds and commodity trading advisors, which mostly trade index futures rather than individual stocks, have expanded their long bets this month, according to Credit Suisse data. Meanwhile, conventional long-short stock pickers boosted their net exposure to the highest since March as they covered shorts amid the surprise resurgence this month of “economic recovery” trades betting on higher inflation and growth.

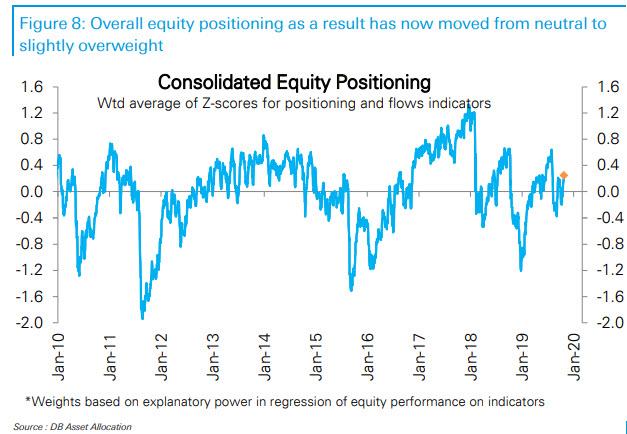

Financial stocks have outperformed, while defensive sectors from consumer staples to utilities have lost money — a reversal of market trends seen earlier this year. Meanwhile, Deutsche Bank’s consolidated equity positioning index shows that overall equity positioning has now moved from neutral to slightly overweight.

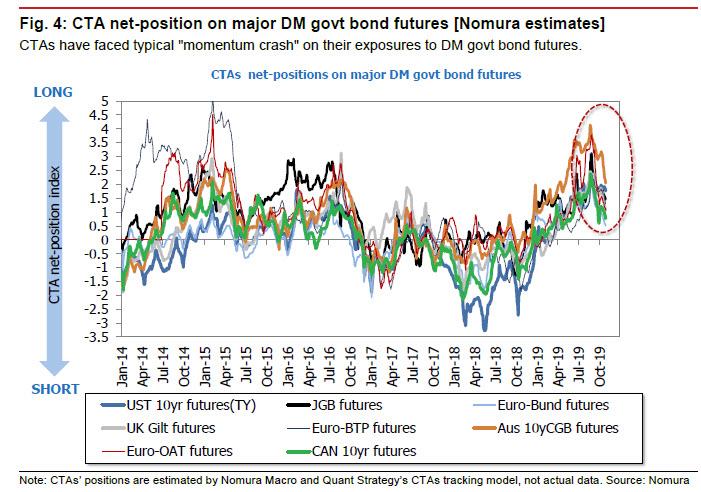

Ironically, the deciding factor whether equity quants return to the market and boost their equity allocation, may be in the hands of bond CTAs, whose performance has been critical to explain not just the recent plunge in bond yields and surge in negative yielding debt to a record notional of $17 trillion, but also to understand the performance of defensive, “bond-like” stocks in recent months.

Commenting on the risk of a potential positioning reversal by bond CTAs, Nomura’s Masanari Takada writes that “the rise in yields thus far accompanying the recovery in sentiment can, of course, be interpreted positively as part of the general move toward healthier markets. But we see something troubling in recent movements by systematic trend-following players. Trend-following algo traders, as typified by CTAs, have built up substantial long bond futures positions over the past year. While developments differ by region, CTAs have now reduced these long positions by only around 40-50% from their peak in summer 2019. Considering the collapse in upward momentum for bond prices, we see a risk that trend-followers could cut their longs further in the interest of avoiding losses. While the figures we give below are merely estimates of the room for a further rise in yields based on CTAs’ positions, we hope they will be of use when looking for near-term inflection points and thinking about a risk scenario in which CTAs completely close out these positions.”

Looking at the potential liquidation risk, Nomura’s quants note that CTAs have unwound their long positions by roughly 45% from the peak (28 August 2019), and point out that potential triggers at 10yr UST yields of

around 1.76% (the average cost of CTAs’ net buying since June),

around 1.90% (average cost since April), and

around 2.05% (average cost since March).

In the near term, the threshold to pay attention to is the second of these, 1.90%. In the extreme case in which yields were to break above 2.05% (the third trigger line), Nomura would expect an across-the-board collapse in CTAs’ long UST futures positions, which could cause yields to shoot up to around 2.5%.

In the end, however, as Nomura correctly notes, “whether CTAs close out their long bond futures positions and make a clear shift to long equity futures positions tends to be determined by the state of the global economy.” And considering the lack of upward economic momentum at present, the risk of an extreme mechanistic sell-off of bond futures that ignores the economic facts on the ground is unlikely to materialize.

Turkey ‘Double Whammy’: US House Recognizes Armenian Genocide, Approves Sanctions Over Syria Incursion

Late in the day Tuesday the US House of Representatives voted overwhelmingly in favor of adopting a historic resolution recognizing the Armenian Genocide. This, it should be noted, on the 96th anniversary of the founding of Turkey as a republic no less.

And in another major simultaneous “gift” to Turkey’s Erdogan — what headlines are already calling a “double whammy”— the House also voted overwhelmingly to approve a biting sanctions bill that if signed into law would crush Turkey’s economy and target Erdogan’s financial assets personally over his controversial military incursion into northern Syria.

Armenian Genocide vote in the House

Ankara has for years successfully lobbied against any such Congressional resolution on the 1915 Armenian genocide, treating it as an embarrassing and grievous wound to its reputation, also given the severe censorship within the country over this chapter in modern Turkey’s history.

It’s de facto illegal in Turkey to even acknowledge it, and over the past years multiple journalists, Armenians among them, have gone to jail for writing about the historic mass killings.

Turkey’s Ministry of Foreign Affairs was quick to condemn the resolution, H.R.296, dismissing it asa “delusion” of the “Armenian lobby and anti-Turkey groups” and further that it will only serve to damage future US-Turkey relations.

The measure recognizes the systematic killing of 1.5 million Armenians by Turkish military forces of the Ottoman Empire from 1915 to 1923. It also recognizes other Christian groups exterminated by Turkish Muslim forces, including “Greeks, Assyrians, Chaldeans, Syriacs, Arameans, Maronites, and other Christians,” according to the resolution’s text.

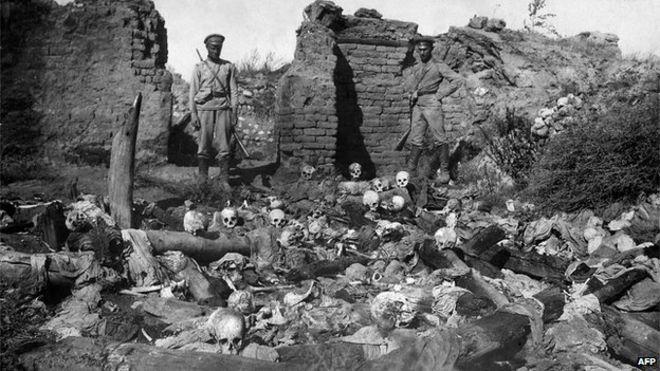

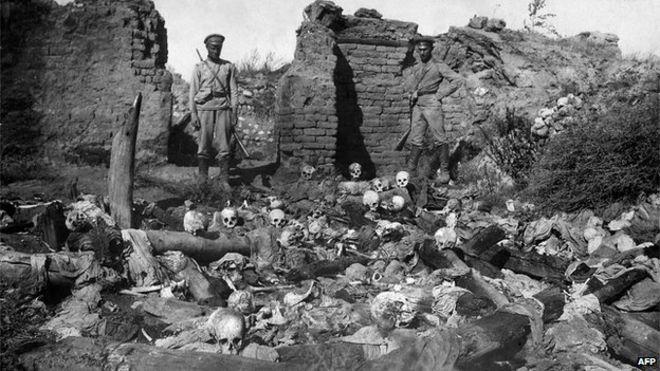

Historical photo of the Armenian Genocide, via AFP/BBC: “Skulls lie in the ruined Armenian village of Sheyxalan in 1915” (pic: Armenian Genocide Museum-Institute)

The Congressional text is scathing in its condemnation, beginning with:

Affirming the United States record on the Armenian Genocide.

Whereas the United States has a proud history of recognizing and condemning the Armenian Genocide, the killing of 1.5 million Armenians by the Ottoman Empire from 1915 to 1923, and providing relief to the survivors of the campaign of genocide against Armenians, Greeks, Assyrians, Chaldeans, Syriacs, Arameans, Maronites, and other Christians;

Whereas the Honorable Henry Morgenthau, United States Ambassador to the Ottoman Empire from 1913 to 1916, organized and led protests by officials of many countries against what he described as the empire’s “campaign of race extermination”, and was instructed on July 16, 1915, by United States Secretary of State Robert Lansing that the “Department approves your procedure … to stop Armenian persecution”;…

And ending with:

Resolved, That it is the sense of the House of Representatives that it is the policy of the United States to—

(1) commemorate the Armenian Genocide through official recognition and remembrance;

(2) reject efforts to enlist, engage, or otherwise associate the United States Government with denial of the Armenian Genocide or any other genocide; and

(3) encourage education and public understanding of the facts of the Armenian Genocide, including the United States role in the humanitarian relief effort, and the relevance of the Armenian Genocide to modern-day crimes against humanity.

Concerning Syria, the successful sanctions vote in the House was also meant as a rebuke not only to Erdogan for his ordered attacks on Kurds, but to Trump, after the recent Pence-brokered ceasefire deal and US draw down from border areas, touted by Trump as a great achievement toward peace.

The president is not expected to sign into effect any new sanctions related to ‘Operation Peace Spring,’ barring a major development or egregious and significant Turkish breach of terms of the US-brokered ceasefire.

George Papadopoulos Wants To Fill Rep. Katie Hill’s Seat

Former Trump campaign adviser George Papadopoulos wants former Rep. Katie Hill’s seat in Congress. Hill, a California Democrat, resigned on Sunday amid a House Ethics Committee probe into allegations that she had inappropriate sexual relations with a staffer.

Papadopoulos – who the FBI under James Comey sent a portly, well-paid spy and his honeypot assistant “Azra Turk” to befriend – filed his statement of candidacy with the Federal Election Commission on Tuesday for California’s 25th district, according toAxios.

Of note, Hill flipped a red seat blue during the last election cycle, which suggests Papadopoulos may actually have a shot of becoming a United States lawmaker.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}