In May 2019, Justice Stephen Breyer chastised his five Republican-appointed colleagues for overruling one of the Supreme Court’s own precedents. “I understand that judges, including Justices of this Court, may decide cases wrongly,” Breyer wrote. “And I understand that, because opportunities to correct old errors are rare, judges may be tempted to seize every opportunity to overrule cases they believe to have been wrongly decided. But,” Breyer insisted, “the law can retain the necessary stability only if this Court resists that temptation, overruling prior precedent only when the circumstances demand it.”

It was an impassioned defense of the legal principle known as stare decisis, which is a Latin phrase meaning, “to stand by things decided.” Alas, Breyer’s own record somewhat undermined his lofty words. Breyer, after all, certainly knew a thing or two about overruling precedent, having voted to do that very thing himself in Lawrence v. Texas (2003), the landmark gay rights decision that overturned Bowers v. Hardwick (1986), which had upheld the power of state governments to prohibit “homosexual conduct.” Bowers “was not correct when it was decided,” the Court ruled in Lawrence, “and it is not correct today.”

Precedent matters at the Supreme Court—until it doesn’t.

Which brings us to abortion. Earlier this month, 207 members of Congress—39 senators and 168 representatives—filed a friend of the court brief urging the Supreme Court to take a second look at one of the most famous precedents in American law, the abortion rights-affirming decision Roe v. Wade (1973). “Stare decisis is not an ‘inexorable command,’ much less a constitutional principle,” the congressional brief argues. “The Court has exercised [its] judgement to overrule precedent in over 230 cases throughout its history…. It is time for the Court to take [the abortion issue] up again.”

The brief was filed as part of a case known as June Medical Services v. Gee, which the Court will hear later this term. At issue is a Louisiana law which requires physicians who perform abortions to have admitting privileges at nearby hospitals. In Whole Woman’s Health v. Hellerstadt (2016), the Court struck down a nearly identical regulation from Texas on the grounds that it placed an “undue burden” on a woman’s right to have an abortion.

But that was then. The Court’s membership has changed in the intervening years and there is now perhaps a new appetite on the bench to rule in support of such abortion restrictions.

The 207 members of Congress are hoping for more than that. They hope that the Court will not only distinguish June Medical from Whole Woman’s Health, but that the Court will take the present opportunity to revisit and overrule Roe itself.

That probably won’t happen. As I’ve previously argued, “even those conservative justices who might want to see [Roe and related rulings] overturned might still prefer to see the precedents gradually weakened and narrowed over time, via a series of cases, rather than simply obliterated in one fell swoop.”

At least for now, the Court’s abortion rights precedents are likely to remain on the books.

from Latest – Reason.com https://ift.tt/2u3zv5u

via IFTTT

In May 2019, Justice Stephen Breyer chastised his five Republican-appointed colleagues for overruling one of the Supreme Court’s own precedents. “I understand that judges, including Justices of this Court, may decide cases wrongly,” Breyer wrote. “And I understand that, because opportunities to correct old errors are rare, judges may be tempted to seize every opportunity to overrule cases they believe to have been wrongly decided. But,” Breyer insisted, “the law can retain the necessary stability only if this Court resists that temptation, overruling prior precedent only when the circumstances demand it.”

It was an impassioned defense of the legal principle known as stare decisis, which is a Latin phrase meaning, “to stand by things decided.” Alas, Breyer’s own record somewhat undermined his lofty words. Breyer, after all, certainly knew a thing or two about overruling precedent, having voted to do that very thing himself in Lawrence v. Texas (2003), the landmark gay rights decision that overturned Bowers v. Hardwick (1986), which had upheld the power of state governments to prohibit “homosexual conduct.” Bowers “was not correct when it was decided,” the Court ruled in Lawrence, “and it is not correct today.”

Precedent matters at the Supreme Court—until it doesn’t.

Which brings us to abortion. Earlier this month, 207 members of Congress—39 senators and 168 representatives—filed a friend of the court brief urging the Supreme Court to take a second look at one of the most famous precedents in American law, the abortion rights-affirming decision Roe v. Wade (1973). “Stare decisis is not an ‘inexorable command,’ much less a constitutional principle,” the congressional brief argues. “The Court has exercised [its] judgement to overrule precedent in over 230 cases throughout its history…. It is time for the Court to take [the abortion issue] up again.”

The brief was filed as part of a case known as June Medical Services v. Gee, which the Court will hear later this term. At issue is a Louisiana law which requires physicians who perform abortions to have admitting privileges at nearby hospitals. In Whole Woman’s Health v. Hellerstadt (2016), the Court struck down a nearly identical regulation from Texas on the grounds that it placed an “undue burden” on a woman’s right to have an abortion.

But that was then. The Court’s membership has changed in the intervening years and there is now perhaps a new appetite on the bench to rule in support of such abortion restrictions.

The 207 members of Congress are hoping for more than that. They hope that the Court will not only distinguish June Medical from Whole Woman’s Health, but that the Court will take the present opportunity to revisit and overrule Roe itself.

That probably won’t happen. As I’ve previously argued, “even those conservative justices who might want to see [Roe and related rulings] overturned might still prefer to see the precedents gradually weakened and narrowed over time, via a series of cases, rather than simply obliterated in one fell swoop.”

At least for now, the Court’s abortion rights precedents are likely to remain on the books.

from Latest – Reason.com https://ift.tt/2u3zv5u

via IFTTT

The FBI’s newly released plans to avoid mistakes when seeking permission to wiretap and surveil American citizens is insufficient, according to an expert brought in to advise the Foreign Intelligence Surveillance Court (FISC).

In December, the Office of the Inspector General (OIG) for the Department of Justice released a report showing significant problems with the warrants that the FBI submitted to FISC in order to secretly wiretap Carter Page, a former foreign policy adviser to Donald Trump’s 2016 presidential campaign. While the OIG’s report concluded that the agency was justified in investigating whether Page was unduly influenced by his connections with the Russian government, it also determined that the FBI withheld important details from the FISC that might have influenced its decision to grant these warrants. These omissions were not in Page’s favor, and ultimately the OIG found 17 different errors or omissions in the warrant requests, some of which were not corrected in subsequent applications.

The FISC’s judges were extremely unhappy to discover information had been withheld from them, and then-presiding Judge Rosemary M. Collyer (who has since retired) ordered FBI Director Christopher Wray to send a plan to the court by January 10 explaining how the FBI would avoid making similar mistakes in the future.

Wray submitted his plan last week. It’s a dense and technical response that is mostly inscrutable to anybody who does not have a history of involvement with the court’s surveillance processes. Wray provides a list of 12 actions the FBI has taken or will take to make sure future applications for Foreign Intelligence Surveillance Act (FISA) warrants include all the information judges should’ve had when the FBI sought permission to surveil Page. Wray’s plans revolve primarily around adding most steps to verify and re-verify information contained in the warrant requests to make sure that FBI agents and supervisors are not omitting information that might undermine or compromise their case for a surveillance warrant. Wray also says the agency will improve training by creating a case study program to teach FBI agents about historical precedents (I’m guessing the Page warrants will play a starring role).

While the FBI was hammering out this plan, the FISC appointed David Kris, a former Justice Department attorney during President Barack Obama’s administration, to advise the court. His appointment caused some partisan-tinged outrage. Kris had previously defended the FBI’s surveillance of Page and had been critical of claims by Rep. Devin Nunes (D–Calif.) that the warrants against Page had problems. Trump even attacked Kris in a tweet.

But Kris has also been skeptical of how the federal government uses surveillance against American citizens and has criticized the National Security Agency’s position that laws passed to fight the war on terror and to investigate Al Qaeda permitted the agency to secretly snoop on American citizens. And he voiced these criticisms while working on national security issues at the Justice Department under President George W. Bush.

It appears that version of Kris analyzed the FBI’s plans. On Wednesday, he responded that Wray’s proposals were ultimately insufficient. Part of the larger problem, which Wray has acknowledged, is that it’s hard to check the accuracy of information that’s not included or deliberately omitted. In the Page case, much of the erroneous intel that might have dissuaded the judges from granting a warrant was not included in the warrant application, and therefore its accuracy was not assessed.

Kris does not defend the FBI’s actions surveilling Page in his response, saying bluntly that nobody is disputing that “basic, fundamental, and serious errors” were found in the Page warrant requests. Kris worries that Wray’s plan doesn’t really account for what procedures will be used with surveillance requests that intersect with political campaigns. And while Kris does support the improvements that Wray has listed, he says the FBI needs to go further. He is calling for better communication between the FBI and Justice Department attorneys, which in this case partly contributed to the information gaps in the warrant applications. Kris also suggests the possibility of having field agents, not just agents working at FBI headquarters, signing onto warrant applications or at least requiring them to attest to the court to the facts that are in the warrant application. Field agents might be more likely to notice an important omission.

Kris also says the court should require that the FBI regularly submit reports on training participation rates and test scores. The court could, in turn, prohibit FBI agents who haven’t successfully completed FISA warrant from signing on as declarants; at the very least, the court would know to bring an extra level of skepticism.

After providing a number of similar suggestions, Kris concludes: “The FBI must restore—and the Court should insist it restore—a strong organizational culture of accuracy and completeness.” Students of FBI history, meanwhile, can debate whether “accuracy and completeness” have ever been part of its organizational culture.

We still don’t know whether the omissions in the Page warrant were an anomaly or something that happens regularly with FISA warrants, partly because the American public has never been this privy to the process. The Justice Department OIG is launching a new audit to investigate whether the errors with the Page warrant were unique. If so, that would suggest that the FBI did indeed play fast and loose with the rules when investigating the Trump campaign, perhaps because of a bias against him.

If it turns out that what happened to Page was not unique, it would mean that the FBI has been withholding information in order to engage in an undetermined amount of secret surveillance of American citizens—which would also be bad.

Either way, there’s likely more bad news to come.

from Latest – Reason.com https://ift.tt/2RlqHzS

via IFTTT

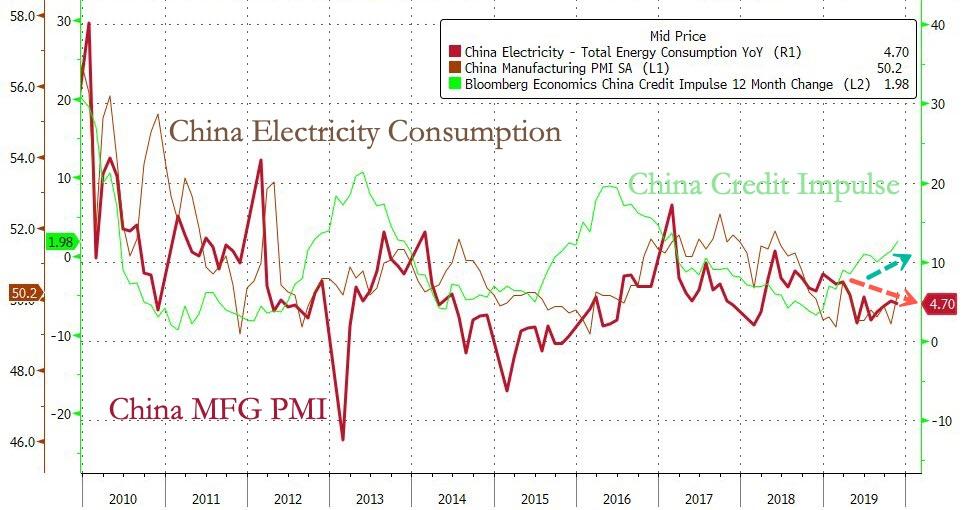

China’s Largest Utility Company Warns “Growth To Decelerate Sharply Through 2024”

Ahead of tonight’s key China data dump, State Grid, China’s largest utility company, has warned the rate of economic growth in the country could plunge to 4% within the next four years, according to internal forecasts, first seen by the Financial Times.

The state-owned utility has turned bearish on the Chinese economy. It forecasts a rapid slowdown that has already dented energy demand across all 23 provinces and could last until 2024.

Already, ten of the company’s 25 regional operations reported a loss in 2019, according to company insiders, resulting in decreased capital expenditures.

One official from the utility company, who asked not to be identified, said the economy was booming, and generally, that meant internal estimates about the economy were overly bullish. But now, it appears the exact opposite, and internal estimates show China’s economy is decelerating while official GDP estimates are up.

“We used to be more bullish than the market consensus,” the official said. “Now, we are doing the opposite.”

The Times notes that State Grid’s infrastructure spending has been a reasonably good barometer of China’s investment-driven economy. That is because infrastructure investment, in State Grid’s case, has been driven by the government. With the decreased investment, this suggests a slowdown in the economy is expected to persist through 2020.

Last month, the People’s Bank of China (PBoC) said the economy is expected to remain in a slump for the next five years, essentially confirming State Grid’s bearish economic outlook.

Liu Shijin, a policy adviser to the PBoC, said the country’s GDP will decelerate through 2025 and could print in a range of 5 to 6%.

Shijin warned that excessive monetary policy is failing to stimulate the economy and could cause it to rapidly decelerate.

China’s economic growth has already crashed to a three-decade low. State Grid’s worst-case scenario is a 4% GDP print by 2024.

“We were upbeat about China’s power demand five years ago because the economy was still robust and 7 or 8 percent GDP growth was the bottom line,” the official said. “No one expected growth to decelerate so sharply.” He warned that 4% growth by 2024 was the utility’s worst-case scenario.

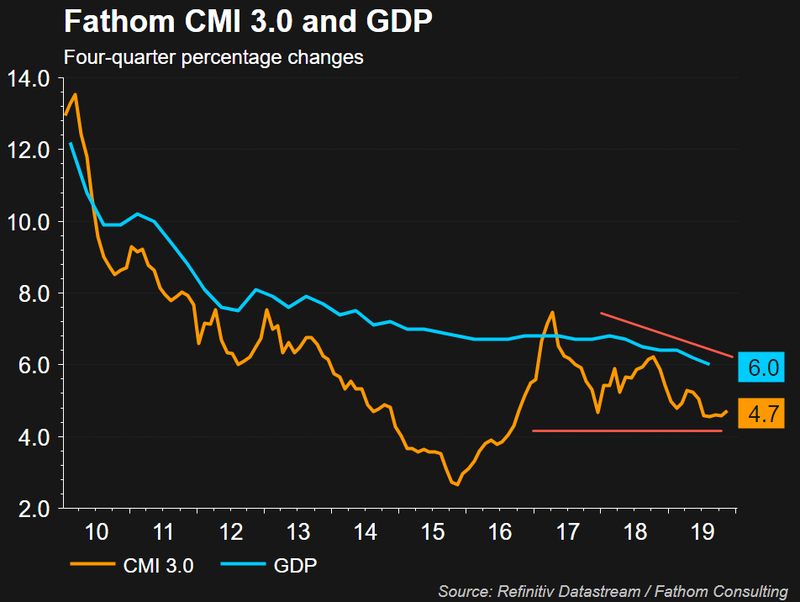

To gain more color on China’s slowdown, Fathom Consulting’s China Momentum Indicator 3.0 (CMI 3.0), which provides a more in-depth view of China’s economic activity than the official Chinese GDP statistics.

CMI 3.0 is based on ten alternative indicators for economic activity; some of those indicators include railway freight, electricity consumption, and the issuance of bank loans.

State Grid’s bearish outlook on the economy is some of the first internal data from a state-owned company confirming our thoughts that China’s massive money printing, as of early 2020, isn’t working and the country is headed for a prolonged slowdown.

And this is more bad news for global stocks at all-time highs expecting a massive rebound in China/global economy.

The FBI’s newly released plans to avoid mistakes when seeking permission to wiretap and surveil American citizens is insufficient, according to an expert brought in to advise the Foreign Intelligence Surveillance Court (FISC).

In December, the Office of the Inspector General (OIG) for the Department of Justice released a report showing significant problems with the warrants that the FBI submitted to FISC in order to secretly wiretap Carter Page, a former foreign policy adviser to Donald Trump’s 2016 presidential campaign. While the OIG’s report concluded that the agency was justified in investigating whether Page was unduly influenced by his connections with the Russian government, it also determined that the FBI withheld important details from the FISC that might have influenced its decision to grant these warrants. These omissions were not in Page’s favor, and ultimately the OIG found 17 different errors or omissions in the warrant requests, some of which were not corrected in subsequent applications.

The FISC’s judges were extremely unhappy to discover information had been withheld from them, and then-presiding Judge Rosemary M. Collyer (who has since retired) ordered FBI Director Christopher Wray to send a plan to the court by January 10 explaining how the FBI would avoid making similar mistakes in the future.

Wray submitted his plan last week. It’s a dense and technical response that is mostly inscrutable to anybody who does not have a history of involvement with the court’s surveillance processes. Wray provides a list of 12 actions the FBI has taken or will take to make sure future applications for Foreign Intelligence Surveillance Act (FISA) warrants include all the information judges should’ve had when the FBI sought permission to surveil Page. Wray’s plans revolve primarily around adding most steps to verify and re-verify information contained in the warrant requests to make sure that FBI agents and supervisors are not omitting information that might undermine or compromise their case for a surveillance warrant. Wray also says the agency will improve training by creating a case study program to teach FBI agents about historical precedents (I’m guessing the Page warrants will play a starring role).

While the FBI was hammering out this plan, the FISC appointed David Kris, a former Justice Department attorney during President Barack Obama’s administration, to advise the court. His appointment caused some partisan-tinged outrage. Kris had previously defended the FBI’s surveillance of Page and had been critical of claims by Rep. Devin Nunes (D–Calif.) that the warrants against Page had problems. Trump even attacked Kris in a tweet.

But Kris has also been skeptical of how the federal government uses surveillance against American citizens and has criticized the National Security Agency’s position that laws passed to fight the war on terror and to investigate Al Qaeda permitted the agency to secretly snoop on American citizens. And he voiced these criticisms while working on national security issues at the Justice Department under President George W. Bush.

It appears that version of Kris analyzed the FBI’s plans. On Wednesday, he responded that Wray’s proposals were ultimately insufficient. Part of the larger problem, which Wray has acknowledged, is that it’s hard to check the accuracy of information that’s not included or deliberately omitted. In the Page case, much of the erroneous intel that might have dissuaded the judges from granting a warrant was not included in the warrant application, and therefore its accuracy was not assessed.

Kris does not defend the FBI’s actions surveilling Page in his response, saying bluntly that nobody is disputing that “basic, fundamental, and serious errors” were found in the Page warrant requests. Kris worries that Wray’s plan doesn’t really account for what procedures will be used with surveillance requests that intersect with political campaigns. And while Kris does support the improvements that Wray has listed, he says the FBI needs to go further. He is calling for better communication between the FBI and Justice Department attorneys, which in this case partly contributed to the information gaps in the warrant applications. Kris also suggests the possibility of having field agents, not just agents working at FBI headquarters, signing onto warrant applications or at least requiring them to attest to the court to the facts that are in the warrant application. Field agents might be more likely to notice an important omission.

Kris also says the court should require that the FBI regularly submit reports on training participation rates and test scores. The court could, in turn, prohibit FBI agents who haven’t successfully completed FISA warrant from signing on as declarants; at the very least, the court would know to bring an extra level of skepticism.

After providing a number of similar suggestions, Kris concludes: “The FBI must restore—and the Court should insist it restore—a strong organizational culture of accuracy and completeness.” Students of FBI history, meanwhile, can debate whether “accuracy and completeness” have ever been part of its organizational culture.

We still don’t know whether the omissions in the Page warrant were an anomaly or something that happens regularly with FISA warrants, partly because the American public has never been this privy to the process. The Justice Department OIG is launching a new audit to investigate whether the errors with the Page warrant were unique. If so, that would suggest that the FBI did indeed play fast and loose with the rules when investigating the Trump campaign, perhaps because of a bias against him.

If it turns out that what happened to Page was not unique, it would mean that the FBI has been withholding information in order to engage in an undetermined amount of secret surveillance of American citizens—which would also be bad.

Either way, there’s likely more bad news to come.

from Latest – Reason.com https://ift.tt/2RlqHzS

via IFTTT

A Japanese woman was surprised when Hong Kong Express Airways required her to take a pregnancy test before boarding her flight.

They made the poor woman sign a form indicating her body type was observed by staff to appear pregnant. The test proved she wasn’t.

The woman was travelling to Saipan, the largest island among the Northern Mariana islands, a US territory.

Having a baby on the island gives the child automatic US citizenship. And in 2018, more tourists than residents gave birth on the Northern Mariana Islands.

That is perfectly legal. But immigration officials can turn you away if they determine you lied about your reasons for travel, or plan to have a medical procedure which you cannot afford.

And when that happens, the airline that brought you there has to fly you back, free of charge.

The birth tourism demand on Saipan comes mostly from Chinese nationals who want to give their child the gift of US citizenship.

That’s a major gift, since a US passport allows you visa-free access to more than double the number of countries a Chinese passport grants you, including most of Europe and North America.

But it’s not just Chinese parents who should be thinking about the advantages they can bestow on their children from day one of life.

First off, giving your child the opportunity to learn a second language from an early age should be on everyone’s list.

Jim Rogers, the legendary investor, moved to Singapore so his daughters could grow up in a Chinese speaking environment. The girls were taught Mandarin from their Chinese governess, and now speak it fluently.

Learning a second language as a child makes it that much easier to pick up when the brain is still nice and elastic. And choosing Mandarin is a nod to the fact that emerging markets in Asia are full of opportunity, and will be for the foreseeable future.

The other gift you can grant your child from birth, is a second citizenship.

A second citizenship and passport gives them the ultimate insurance policy. At any point in their lives, they will always have an alternative place to live, work, and invest outside of their home country. It opens all sorts of doors, opportunities, and Plan Bs.

Certain countries let you give the gift of citizenship to your children for free, simply by giving birth in that country. This is a gift they can pass down from generation to generation.

For example, Brazil grants birthright citizenship to any baby born on its soil. But it also gives the parents and siblings the right to immediately apply for permanent residency.

After a year of residency, parents can apply for naturalization to become a Brazillian citizen. For siblings under ten, they could become citizens in as little as six months after getting permanent residency. For siblings over ten, they become eligible for citizenship after their parents become citizens.

So your newborn could actually return the gift to the whole family.

Brazil’s passport is pretty good, ranked 55 worldwide on Sovereign Man’s Global Passport Ranking, with visa-free access to 149 countries. So it’s a solid Plan B in case your home country ever becomes undesirable.

At first having a baby in Brazil might sound radical. But it’s really not if you have a little flexibility. And aside from Brazil, there are dozens of places in the world where you can do this.

There’s no reason birthright citizenship shouldn’t be among the topics of family planning when having a baby. It’s truly a rare opportunity to have a generational impact on your family.

It’s at least worth considering, as long as your doctor signs off on travel during pregnancy.

John Mauldin recently penned an interesting piece:

“Ignoring problems rarely solves them. You need to deal with them—not just the effects, but the underlying causes, or else they usually get worse. In the developed world, and especially the US, and even in China, our economic challenges are rapidly approaching that point. Things that would have been easily fixed a decade ago, or even five years ago, will soon be unsolvable by conventional means.

Yes, we did indeed need the Federal Reserve to provide liquidity during the initial crisis. But after that, the Fed kept rates too low for too long, reinforcing the wealth and income disparities and creating new bubbles we will have to deal with in the not-too-distant future.

This wasn’t a ‘beautiful deleveraging’ as you call it. It was the ugly creation of bubbles and misallocation of capital. The Fed shouldn’t have blown these bubbles in the first place.”

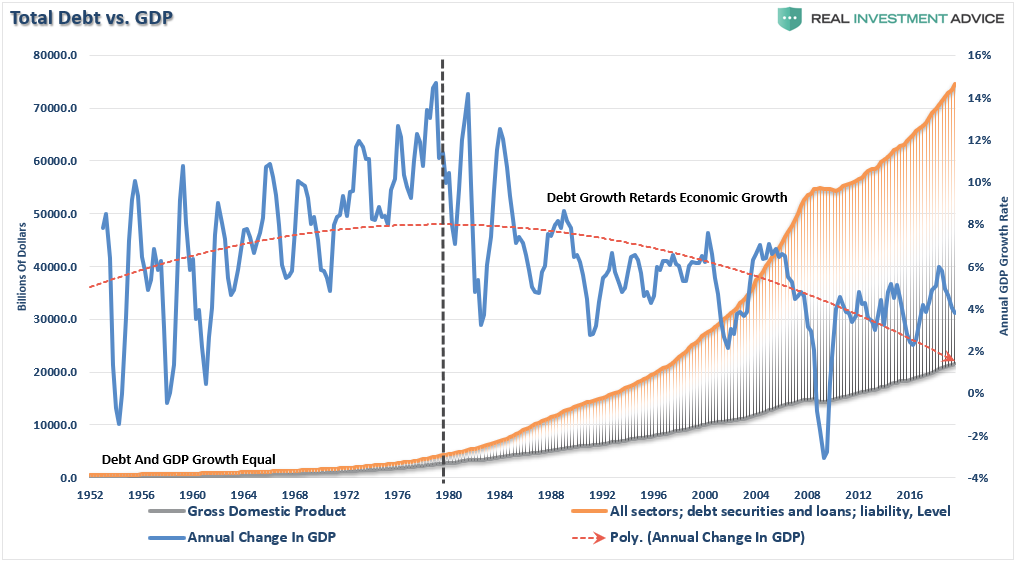

John is correct. The problem with low interest rates for so long is they have encouraged the misallocation of capital. We see it everywhere throughout the entirety of the financial system from consumer debt, to subprime auto-loans, to corporate leverage, and speculative greed.

“Since the bulk of the debt issued by the U.S. has been squandered on increases in social welfare programs and debt service, there is a negative return on investment.Therefore, the larger the balance of debt becomes, the more economically destructive it is bydiverting an ever-growing amount of dollars away from productive investments to service payments.”

Currently, throughout the entire monetary ecosystem, there is a rising consensus that “debt doesn’t matter” as long as interest rates and inflation remain low. Of course, the ultra-low interest rate policy administered by the Federal Reserve is responsible for the “yield chase,” and the massive surge in debt since the “financial crisis.”

Yes, current economic growth is good, but not great. Inflation, and interest rates, remain low, which creates an “illusion” that using debt remains opportunistic. However, as stated, rising levels of non-productive debt has negative long-term economic consequences.

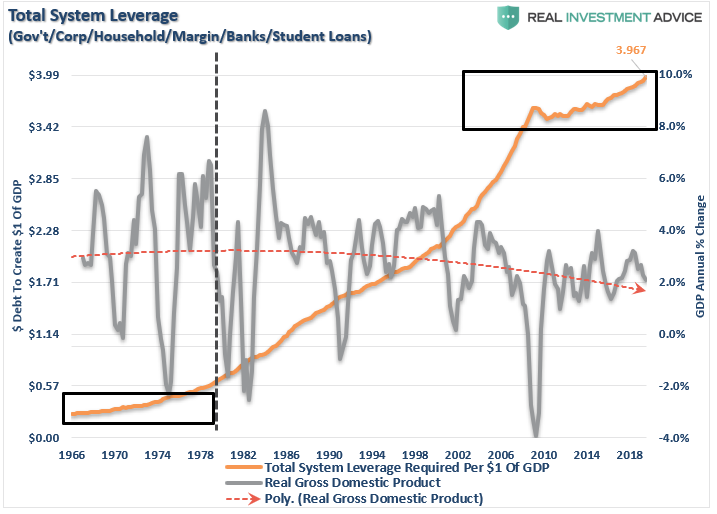

Before the deregulation of the financial industry under President Reagan, which led to an explosion in consumer credit issuance, it required just $1.00 of total system-wide debt to create $1.00 of economic growth. Today, it requires $3.97 to create the same $1 of economic growth. This shouldn’t be surprising, given that “debt” detracts from economic growth as the “debt service” diverts income from productive investments and leads to a “diminishing rate of return” for each new dollar of debt.

The irony is that while it appears the economy is growing, akin to the analogy of “boiling a frog,” we accept 2% economic growth as “strong,” whereas such growth rates were previously considered near recessionary.

Another conundrum is that corporations, and financial institutions, appear to be healthier, not to mention wealthier than ever. If such is indeed the case, then why is the Federal Reserve still needing to engage in “emergency monetary measures” to support the financial markets and economy after more than a decade?

As John stated above, the Fed’s actions are only “ignoring the problems” which, combined, is a problem too large for the Federal Reserve to fix.

The Dark Side Of Stock Buybacks

While many argue that “share buybacks” are just a method by which corporations can return cash to shareholders, there is a dark side. In moderation, repurchases can be a beneficial method for a company to deploy capital when no better options are available. (It’s the least best use of cash.)

But, as with everything in life, when taken to “excess” the beneficial effects, can become detrimental.

“The rules now reward management, not for generating revenue, but to drive up the price of the share price, thus making their options and stock grants more valuable.” – John Mauldin

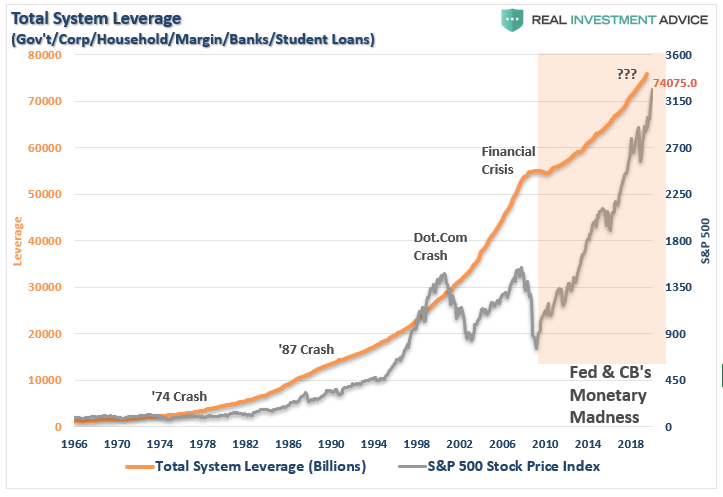

The problem for the Fed was, despite the best of intentions, lowering interest rates to zero did not spark a “bank lending spree” throughout the economy. Instead, the excess liquidity flowed directly back into the financial system, creating a global wealth gap, rather than supporting stronger economic growth.

The most vivid example of this “closed loop” was in corporate share repurchases. Corporations, able to borrow cheaply due to low rates, used debt and cash to repurchase shares to increase earnings per share. This was the easiest route to create “executive wealth,” rather than deploying capital in more risky endeavors. As the Financial Times penned:

“Corporate executives give several reasons for stock buybacks but none of them has close to the explanatory power of this simple truth: Stock-based instruments make up the majority of their pay and in the short-term buybacks drive up stock prices.”

Importantly, as noted by the Securities & Exchange Commission:

“SEC research found that many corporate executives sell significant amounts of their own shares after their companies announce stock buybacks.”

Again, buybacks may not be an issue, but when taken to excess such can have the negative side effects of inflating asset bubbles. As John Authers pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

“Stock buybacks” are only a short-term benefit. With liquid cash, or worse debt, used for a one-time benefit, there is a long-term negative return on uses of capital for non-productive investments.

All Levered Up

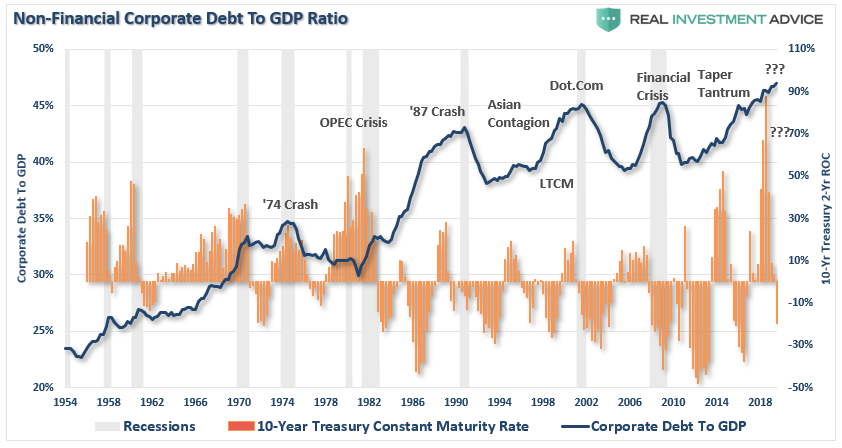

Currently, total corporate debt has surged to $10.1 trillion – its highest level relative to U.S. GDP (47%) since the financial crisis. In just the last two years, corporations have issued another $1.2 trillion of new debt NOT for expansion, but primarily used for share buybacks.

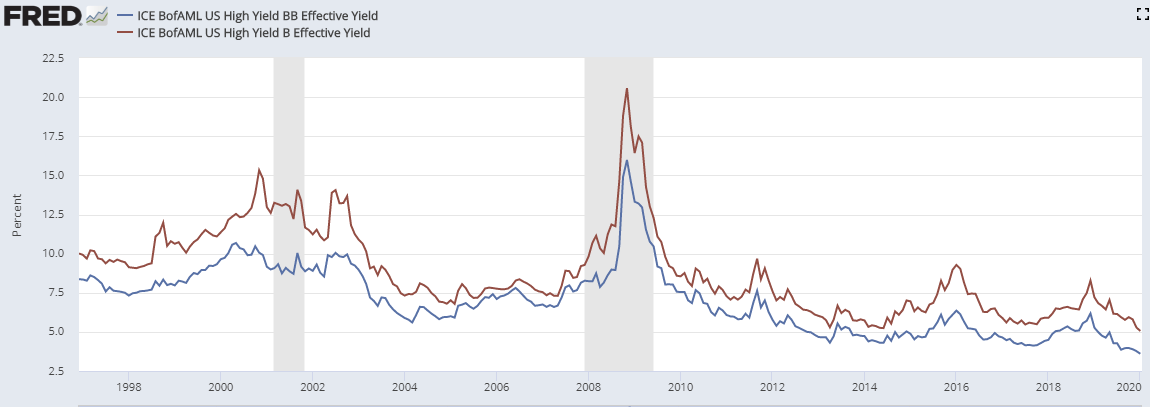

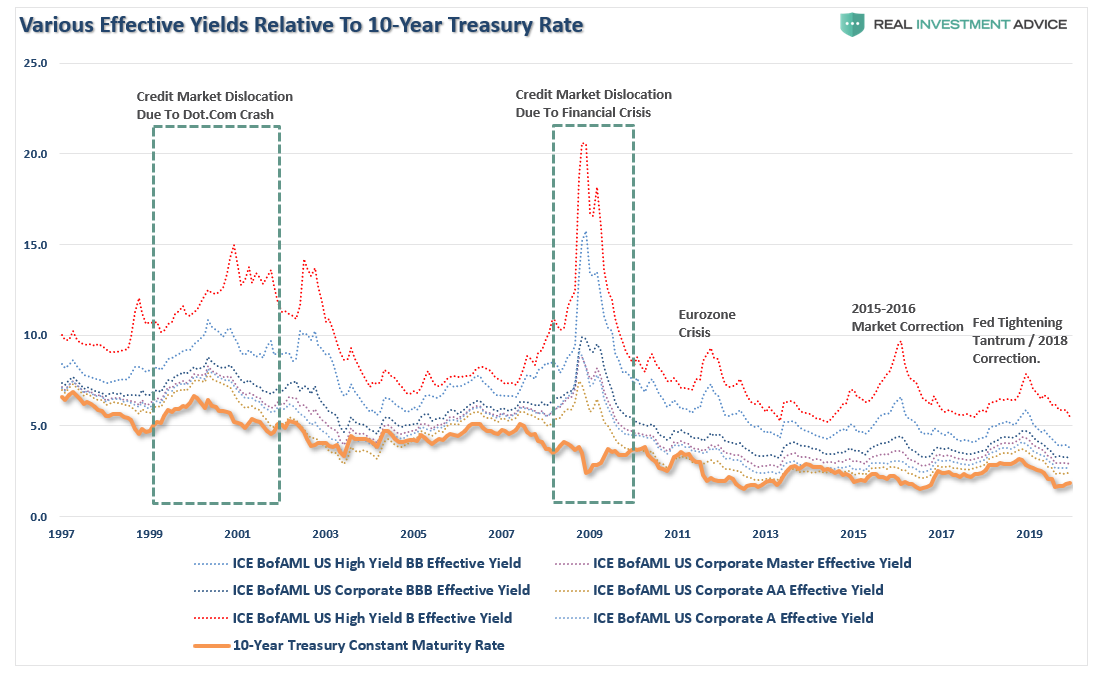

For the last 10-years, the Fed’s “zero interest rate policy” has left investors chasing yield, and corporations were glad to oblige. The end result is the risk premium for owning corporate bonds over U.S. Treasuries is at historic lows, and debt has allowed many “zombie companies” to remain alive.

During the next market reversion,the 10-year rate will fall towards “zero” as money seeks the stability and safety of the U.S Treasury bond. However, corporate bonds will be decimated. When “high yield,” or “junk bonds,” begin to default in large numbers, as they always do in a recession, which is why they are called “junk bonds,” investors will face sharp losses on the one side of their portfolio they “thought” was safe.

As the credit market falls into crisis, the Fed will have to ramp up additional stimulus to bail out the financial institutions caught long with an exceeding amount of poor-quality debt. As shown below, Treasuries will gain a bid as yields fall to zero, while corporate bonds lose value.

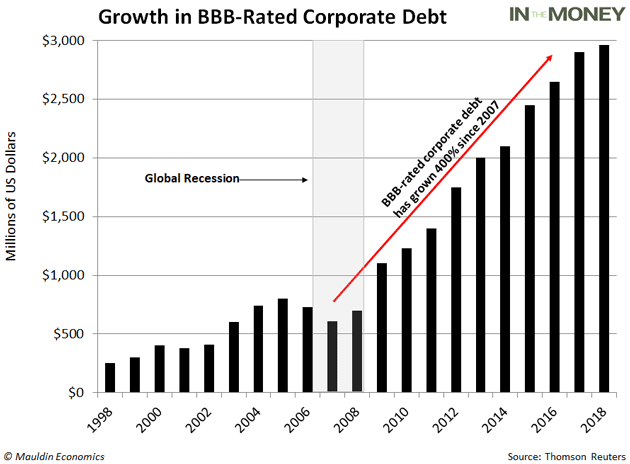

“In just the last 10 years, the triple-B bond market has exploded from $686 billion to $2.5 trillion—an all-time high. To put that in perspective, 50% of the investment-grade bond market now sits on the lowest rung of the quality ladder.

And there’s a reason BBB-rated debt is so plentiful. Ultra-low interest rates have seduced companies to pile into the bond market and corporate debt has surged to heights not seen since the global financial crisis.” – John Mauldin:

As noted previously,there is a large tranche of BBB bonds on the verge of being downgraded to “junk.” When this occurs, there will be an avalanche of selling as pension, mutual, and hedge fund managers dump bonds simultaneously into what will be an illiquid market.

Pensions Are Broke

But it is NOT just “share buybacks” and debt, which are problems hiding in plain sight.

“Moody’s Investor Service estimated last year that the total pension funding gap in the U.S. is $4.4 trillion. A few months ago, the American Legislative Exchange Council estimated it at nearly $6 trillion.”

With pension funds already wrestling with largely underfunded liabilities, the aging demographics are further complicating funding problems.

“The real crisis comes when there is a ‘run on pensions.’ With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the ‘fear’ that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are declining, will cause a debacle of mass proportions. It will require a massive government bailout to resolve it.”

This $6 trillion hit is going to come at a time where the Federal Reserve will already be at “full tilt” monetizing debt to stabilize declining financial markets to keep a “debt crisis” from spreading.

Strike Three, You’re Out

While investors have become extremely complacent over the last decade that Central Banks have gained control of the financial markets, this is likely an illusion. There are numerous catalysts which could pressure a downturn in the equity markets:

An exogenous geopolitical event

A credit-related event

Failure of a major financial institution

Recession

Falling profits and earnings

A loss of confidence by corporations which contacts share buybacks

Whatever the event is, which is currently unexpected and unanticipated, the decline in asset prices will initiate a “chain reaction.”

Investors will begin to panic as asset prices drop, curtailing economic activity, and further pressuring economic growth.

The pressure on asset prices and weaker economic growth, which impairs corporate earnings, shifts corporate views from “share repurchases” to “liquidity preservation.” This removes a major support of asset prices.

As asset prices decline further, and economic growth deteriorates, credit defaults begin triggering a near $5 Trillion corporate bond market problem.

The bond market decline will pressure asset prices lower, which triggers an aging demographic who fears the loss of pension benefits, sparks the $6 trillion pension problem.

As the market continues to cascade lower at this point, the Fed is monetizing nearly 100% of all debt issuance, and has to resort to even more drastic measures to stem selling and defaults.

Those actions lead to a further loss of confidence and pressures markets even further.

The Federal Reserve can not fix this problem, and the next “bear market” will NOT be like that last.

It will be worse.

As John concluded:

Coordinated monetary policy is the problem, not the solution. And while I have little hope for change in that regard, I have no hope that monetary policy will rescue us from the next crisis.

Let me amplify that last line: Not only is there no hope monetary policy will save us from the next crisis, it will help cause the next crisis. The process has already begun.” – John Mauldin

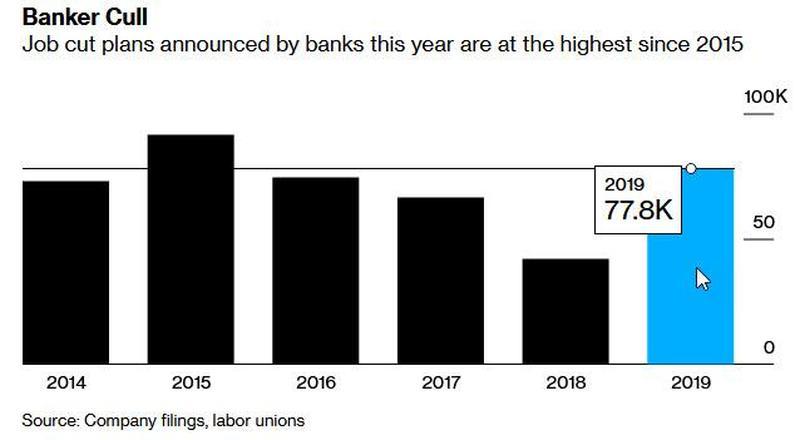

Barclays To Eliminate 100 Senior Investment Bankers

As the real economy continues to decelerate and the Federal Reserve’s ‘Not QE’ catapults growth stocks to record highs, thousands of bankers are being fired every month.

Bloomberg reports Barclays Plc is the latest big bank to layoff 100 senior staff at its investment bank unit.

The job cuts are expected throughout Europe and the US and will be mostly managing directors and director-level staff.

The restructuring was spurred by Barclays’s investment bank chief, Tim Throsby, who warned staff that he’d reduce bonuses. He also said pay for top performers would increase while pay cuts will be seen for non-performers.

With layoffs nearing, CEO Jes Staley is attempting to recapture the lost market share of its investment bank segment after years of dwindling profitability.

Banks across the world – the ones who should be benefitting from the trillion dollars global central banks printed in the last four months and 80 rate cuts in the previous 12 months – have unveiled the biggest round of job cuts in four years as they reduce costs to weather the global trade recession.

In 2019, 50 major banks announced plans to cut at least 77,800 jobs, the most since 91,500 in 2015.

Morgan Stanley, one of the most bearish banks on the global economy, fired 2% of its workforce last month, “due to an uncertain global economic outlook,” CNBC reported.

Banks in Europe have been crushed by the ECB’s catastrophic NIRP policy and face the added burden of negative interest rates that is crushing profitability and led to the most job losses last year.

Even as stocks continue to new highs on ‘Not QE,’ the banking industry is increasing cost-cutting measures as the real economy continues to stagnate, squeezing bank profitability.

One argument that President Donald Trump’s supporters have employed in the impeachment debate is that it was merely a “policy dispute.” Yes, Trump held up aid to Ukraine last summer, this line goes, but he did so in pursuit of his agenda in the region.

There are several problems with this argument. One is that it has become increasingly clear that the president was pursuing a personal political agenda through his personal lawyer, not a national agenda through the formal diplomatic process. Another problem, arguably more serious, is that even if Trump was pursuing some less blatantly corrupt goal, what he did was still illegal.

That is the conclusion reached by the Government Accountability Office (GAO) in a sharply worded letterreleased this morning. The letter raises serious questions about whether the Trump administration violated the constitutional separation of powers.

By withholding aid to Ukraine, the letter says, the Trump administration violated the Impoundment Control Act of 1974, which governs the modern budget process and which specifically prohibits the executive branch from declining to spend money that Congress has authorized.

“The Constitution,” the GAO letter says, “specifically vests Congress with the power of the purse, providing that ‘No Money shall be drawn from the Treasury, but in Consequence of Appropriations made by Law.'”

In addition, the Constitution gives Congress—and only Congress—the power to make laws. So when Congress makes a law that governs the budget process, and then passes a law laying out what money is to be spent and how, the president is constitutionally obliged to spend that money in the ways that Congress has authorized.

In certain circumstances, the executive can delay such spending, but this typically requires a letter to Congress offering a justification for the proposed delay. The Trump administration provided no such notification or justification. Instead, the delays were buried in Office of Management and Budget (OMB) footnotes.

Asked to explain the funding delay, OMB, which handles spending for the executive branch, told GAO that Trump was making sure the money was not spent “in a manner that could conflict with the President’s foreign policy.”

The money was withheld, in other words, to pursue executive branch policy objectives. This is not a permissible reason to delay such spending under the relevant law. As the GAO letter states, “Faithful execution of the law does not permit the President to substitute his own policy priorities for those that Congress has enacted into law.”

If this was a policy dispute, as Trump’s defenders have argued, and if it was a matter of pursuing “the President’s foreign policy,” as the executive branch has claimed, it was illegal. So even if you buy the Trump administration’s own explanation for the delay, the decision, which reports say was made shortly after the president finished a phone call with the Ukrainian president, was nevertheless against the law.

This is not some minor stretching of presidential power to be shrugged off. The notion that Congress and only Congress has the power of the pursue is a core constitutional concept, a fundamental aspect of the separation of powers. The president’s job is to execute the law, not make it.

Nor is this a matter in which the legal particulars are in dispute. As Ilya Somin of George Mason Law School wrote last year in a prescient discussion of the constitutional questions raised by the delay, “If there is one thing that constitutional law scholars agree on, it is that the spending power is supposed to be controlled by Congress, not the president. Even most of those who otherwise favor very broad presidential power concur.”

Federal officials were aware that they were likely breaking the law at the time. Emails made public by the Center for Public Integrity last year show that OMB and Defense Department employees were concerned that without a clear rationale for delaying the funds, the move would be illegal under the Impoundment Control Act. One OMB lawyer quit the job, not wanting to participate in a potentially illegal act.

Trump’s political appointees dismissed these concerns both privately and publicly. In October 2019, OMB Director Mick Mulvaney noted that a report had suggested “that if we didn’t pay out the money it would be illegal.” This, he argued, was “one of those things that has a little shred of truth in it, that makes it look a lot worse than it really is.” It’s just a little presidential lawbreaking. How bad could it really be?

Mulvaney’s casual attitude towards presidential lawbreaking offers more than a little insight into how the Trump administration thinks about its legal and constitutional obligations. And the GAO has now confirmed that OMB staffers were right to worry that the maneuver was illegal, even under the administration’s after-the-fact rationale that it was intended to pursue a legitimate presidential policy agenda. The Trump administration broke the law, it and violated a core constitutional principle in the process. It’s as bad as it looks.

from Latest – Reason.com https://ift.tt/2Nx6w0R

via IFTTT

The view that more money can revive an economy is based on the belief that money transmits its stimulatory effect through aggregate expenditure. With more money in their pockets, people will be able to spend more and the rest will follow suit. Money, in this way of thinking, is a means of payment and funding.

Money, however, is not a means of payment but a medium of exchange. It only enables one producer to exchange his produce with another producer. The means of payment are always real goods and services, which pay for other goods and services. All that money does is facilitate these payments. It makes the payments for goods and services possible.

For instance, a baker exchanges his bread for money and then uses the money to buy shoes. He pays for shoes not with money, but with the bread he produced. Money just allows him to make this payment. (The baker’s production of bread also gives rise to his demand for money.)

When we talk about demand for money, what we really mean here is the demand for money’s purchasing power. After all, people do not want a greater amount of money in their pockets but greater purchasing power.

On this Mises wrote in Human Action,

The services money renders are conditioned by the height of its purchasing power. Nobody wants to have in his cash holding a definite number of pieces of money or a definite weight of money; he wants to keep a cash holding of a definite amount of purchasing power.

In a free market, the price of money is determined by supply and demand, similar to the way the prices of other goods are. If there is less money, its exchange value will increase. Conversely, the exchange value will fall when there is more money. Within the framework of a free market, there cannot be such thing as “too little” or “too much” money. As long as the market is allowed to clear, no shortage of money can emerge.

Once the market has chosen a particular commodity as money, the given stock of this commodity will always be sufficient to secure the services that money provides. Hence, in a free market, the whole idea of the optimum growth rate of money is absurd. According to Mises:

As the operation of the market tends to determine the final state of money’s purchasing power at a height at which the supply of and the demand for money coincide, there can never be an excess or deficiency of money. Each individual and all individuals together always enjoy fully the advantages which they can derive from indirect exchange and the use of money, no matter whether the total quantity of money is great, or small. … the services which money renders can be neither improved nor repaired by changing the supply of money. … The quantity of money available in the whole economy is always sufficient to secure for everybody all that money does and can do.

In a market economy, the purpose of production is ultimately consumption. People produce and exchange goods and services in order to improve their lives and well-being — their ultimate purpose. This means that consumption cannot arise without production, while production without consumption would be a meaningless venture. Hence, in a free market economy consumption and production are in harmony. In a free market economy, consumption is fully backed by production.

What permits the baker to consume bread and shoes is his production of bread. A portion of his bread production is allocated to his direct consumption while the other portion is used to pay for shoes. His consumption is fully backed, i.e., paid by his production. Any attempt, then, to elevate consumption without the corresponding production leads to unbacked consumption, which must come at somebody else’s expense.

This is precisely what monetary pumping does. It generates demand, which is not supported by any production. Once exercised, this type of demand undermines the flow of real savings and in turn weakens the formation of real capital, stifing rather than boosting economic growth.

It is real savings, not money, that fund and make possible the production of better tools and machinery. With better tools and machinery, it becomes possible to lift the production of final goods and services — this is what economic growth is all about.

The Real Source of Wealth

Contrary to the popular way of thinking, setting in motion an unbacked consumption through monetary pumping will only stifle, and not promote, economic growth. This is because unbacked consumption weakens the flow of real savings and thus drains the source that funds real economic growth. If it were otherwise, poverty in the world would have been eliminated a long time ago. After all, everybody knows how to demand and consume.

The only reason loose monetary policies may appear to grow the economy is because the pace of real savings generation is strong enough to absorb the increases in unbacked consumption.

Once the pace of unbacked consumption reaches a stage where the flow of real savings disappears altogether, however, the economy falls into an economic slump. Any attempt by the central bank to pull the economy out of the slump by means of more monetary pumping makes things much worse, for it only strengthens unbacked, or unproductive, consumption, destroying whatever is left of real savings.

The collapse in the sources of real economic growth exposes commercial banks’ fractional reserve lending and raises the risk of a run on banks. To protect themselves, banks curtail their creation of credit out of “thin air.” Under these conditions, further monetary pumping cannot lift banks’ lending. On the contrary, more pumping destroys more real savings and destroys more businesses, which in turn makes banks reluctant to expand lending.

In these conditions, banks would likely agree to lend only to creditworthy businesses. However, as an economic slump deepens, it becomes much harder to find creditworthy businesses. Furthermore, because of loose monetary policy, the lower interest environment against the background of growing risk further diminishes banks’ willingness to extend credit. All this puts downward pressure on the stock of money.

Hence, the central bank may find that despite its attempt to inflate the economy, the money supply will start to fall. Obviously, the central bank could offset this fall through aggressive monetary pumping. The central bank could also monetize the government budget deficit. It could mail checks to every citizen. All this, however, would only further undermine real savings and devastate the real economy.