End Of An Era As Goldman Stops Reporting Prop Trading Results

It’s the end of an era for Goldman: after a decade of breaking out its prop trading results, which in the aftermath of the Volcker Rule was renamed “Investing and Lending” (because apparently all it took to confuse regulators was a name change), the bank once known as Government Sachs (and in its glory days better known for incubating virtually all central bankers and possessing the street’s most fearsome prop trading desk, but those days are now long gone) and is now better known for its co-branded Apple credit cards which target subprime consumers, has stopped reporting its prop results.

As first noted last week, Goldman revamped its quarterly reporting structure to “inject more visibility” into how the firm makes money, in response to growing investor concerns that report “clarity” could boost the stock price. And while the stock price was indeed boosted, Goldman decided to not only reclassify its revenues making any historical comparison impossible but add far more complexity and opacity into how it makes money, by deleting the investing & lending reporting line as well as any mention of this segment, often its most profitable in periods of rising markets – expect, paradoxically for the current “rising market” – but one that also drew complaints about transparency.

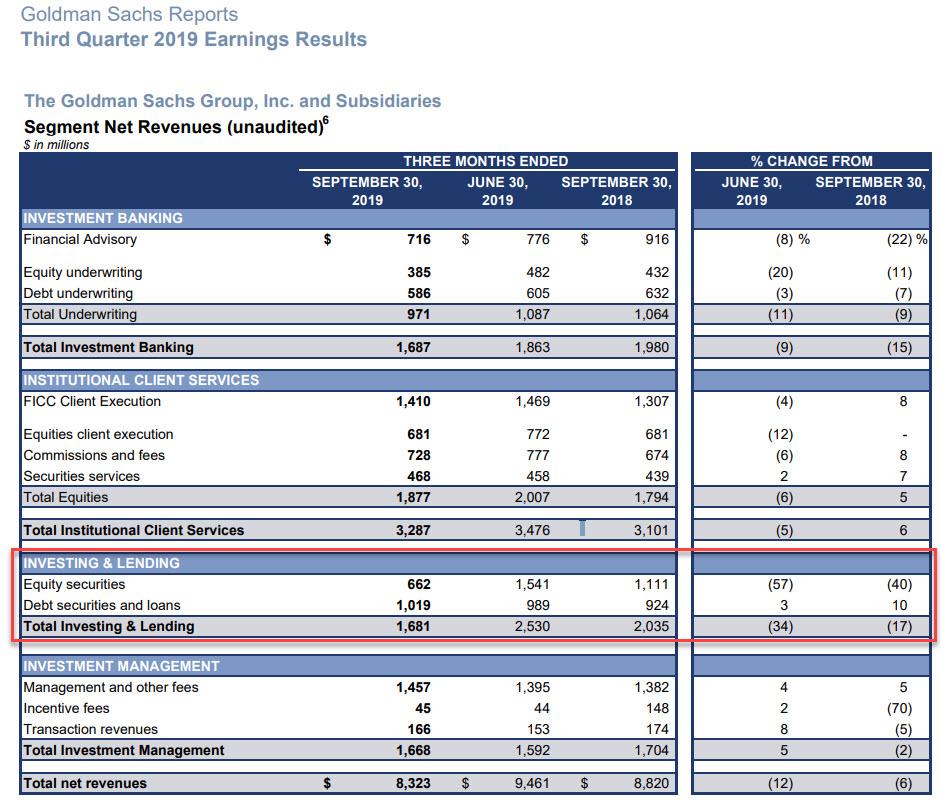

This is what Goldman’s Q3 Earnings summary page looked like: note the prominently featured Investing and Lending group.

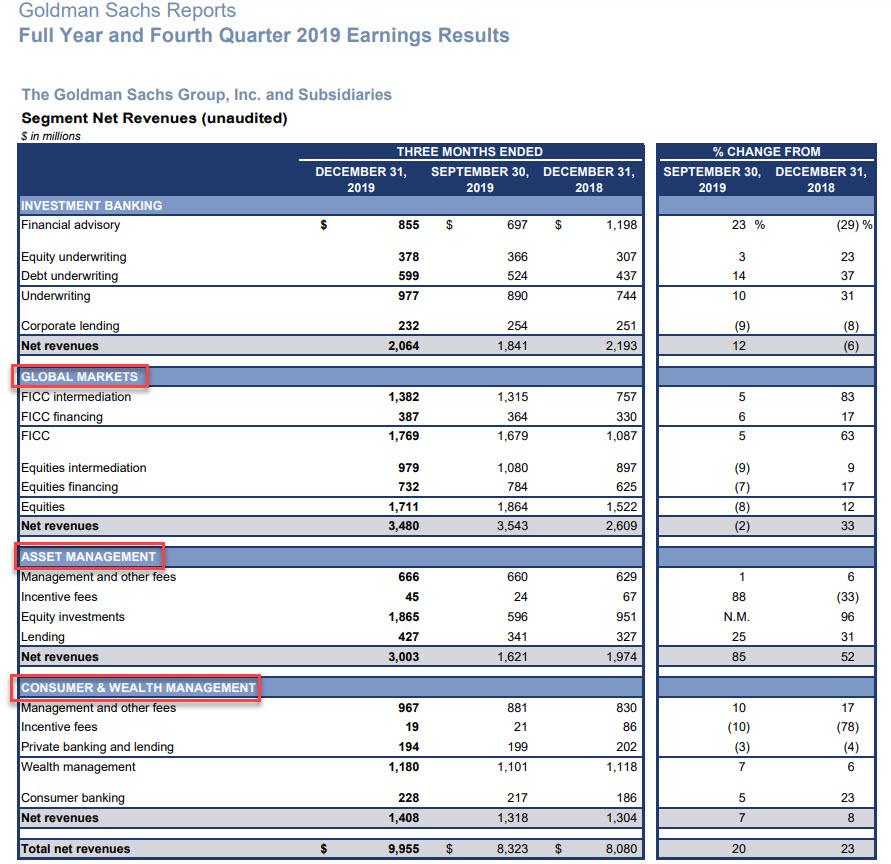

And this is what the Earnings Summary page looks like as of this morning: not only is Investing and Lending completely gone, but while Goldman has kept Investment Banking, it has renamed Institutional Client Services as Global Markets, while Investment Management has been split into i) Asset Management and ii) Consumer and Wealth Management.

So what do we know now? Well, sadly not much, since all the newly broken out data has to be backed into now missing historical income statement lines which Goldman has decided not to do… you know, because it is so concerned with transparency.

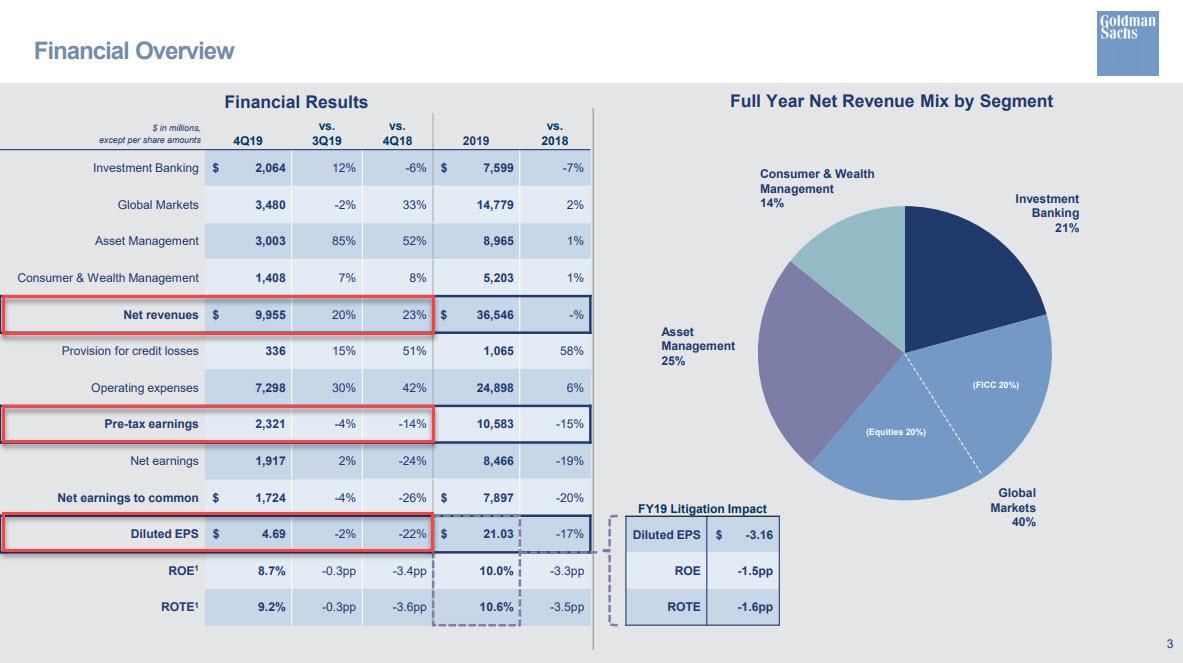

What we do know is what Goldman wants us to know, which is that in Q4, revenues increased by 23% to $9.955BN, stronger than the $8.5BN expected, although due to a 42% surge in operating expenses to $7.3 Billion, Net Income was down by 24% to $1.92 billion, resulting in EPS of $4.69, and missing expectations of $5.54.

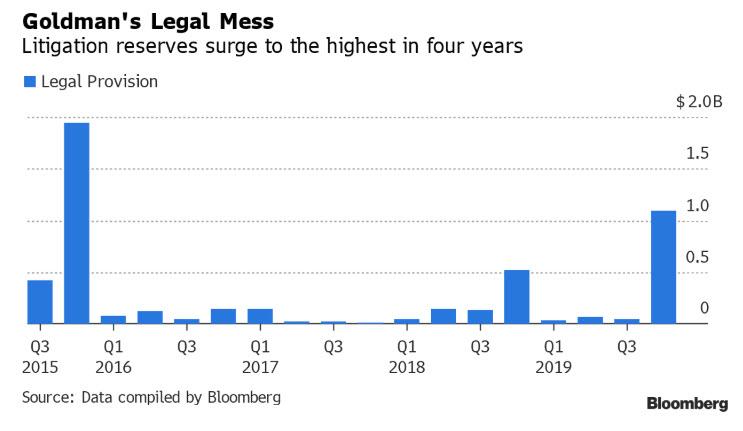

The reason for the expense surge was a $1.09BN legal charge taken as ahead of the bank’s settlement over its criminal activity involving 1MDB. As a reminder, the scandal involves claims of embezzlement and money laundering that triggered investigations in the U.S., Singapore, Switzerland and beyond. Goldman Sachs has been under scrutiny for years over its role in raising money for state-owned investment fund 1Malaysia Development Bhd and for the money it made on the deals, roughly $600 million.

As Goldman notes, while compensation and benefits were essentially unchanged, higher non-compensation expenses included:

Significantly higher net provisions for litigation and regulatory proceedings ($1.24 billion in 2019 vs. $844 million in 2018)

Higher expenses related to the firm’s credit card and transaction banking activities (primarily reflected in professional fees and other expenses) and expenses related to United Capital.

Higher expenses for consolidated investments and technology

Excluding the $1BN legal charge, Goldman’s earnings were not bad, with FICC leading the rebound as one would expect, surging 63% Y/Y from the woeful Q4 2019, to $1.769B, the bulk of which or $1.4BN came from Credit Intermediation. Commenting on this group, Goldman said that FICC intermediation net revenues were significantly higher, reflecting higher net revenues across most major businesses

2019 net revenues higher YoY, due to higher net revenues in FICC intermediation and FICC financing

4Q19 operating environment generally characterized by improved market conditions compared with 3Q19, while client activity levels were lower

And visually:

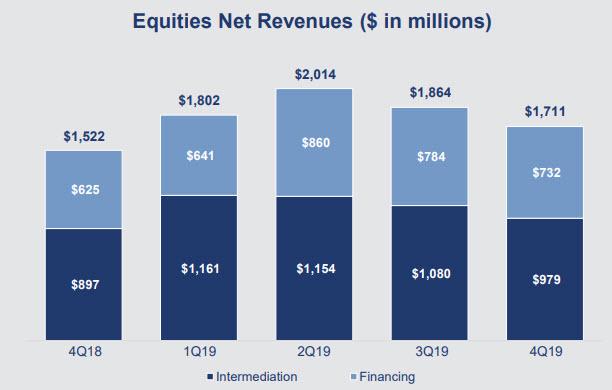

There was far less excitement in the bank’s equities group, where the increase was a far more modest 12% to $1.711BN “reflecting improved spreads and higher average customer balances” while “Equities intermediation net revenues were higher, driven by cash products.”

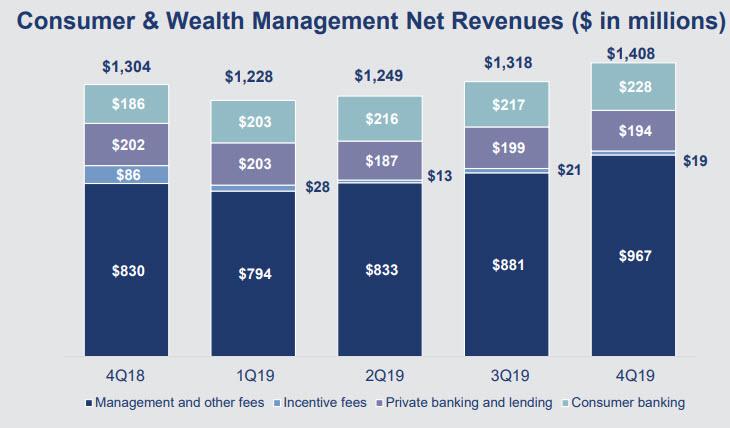

Unfortunately, as noted above, Goldman is no longer reporting its prop revenue, i.e., investing and lending, and instead has broken out its “Markus” attempt to become a plain vanilla retail banks, in the form of Consumer and Wealth Management, where revenue was modestly higher Y/Y, “driven by higher net interest income, primarily reflecting an increase in deposit balances.”

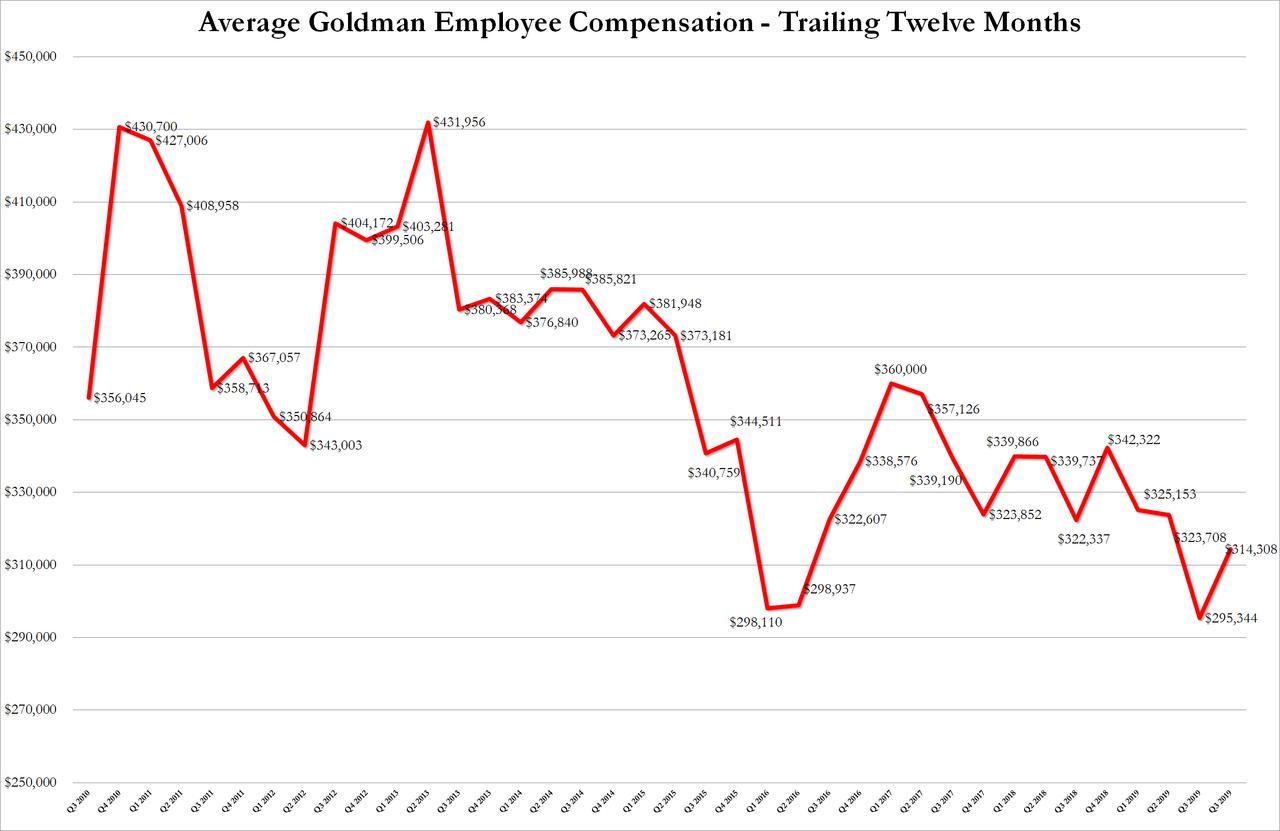

And since Goldman has now officially thrown in the towel on even pretending to be Wall Street’s goto prop desk, which once spawned thousands of hedge fund traders, the compensation was commensurate with the bank’s transformation to a retail bank, and in Q4, average bank comp was $314,308, modestly above the $295,344 report last quarter which was the lowest going back to the financial crisis.

Finally, maybe because algos were too lazy to inquire into why Goldman’s EPS missed so badly or because they were not too excited with the revised earnings, Goldman stocks was sharply lower this morning.

Giuliani Associate’s Ukraine Insider Thought Russia Was Protecting Fired US Ambassador: Texts

House Democrats on Tuesday released a cache of notes and text messages from former Rudy Giuliani associate Lev Parnas, shedding significant light on key aspects of ‘Ukrainegate‘ at the heart of impeachment proceedings against President Trump. This includes efforts to get the former US Ambassador to Ukraine recalled, as well as Rudy Giuliani laying out his mission and the situation in Ukraine at the time.

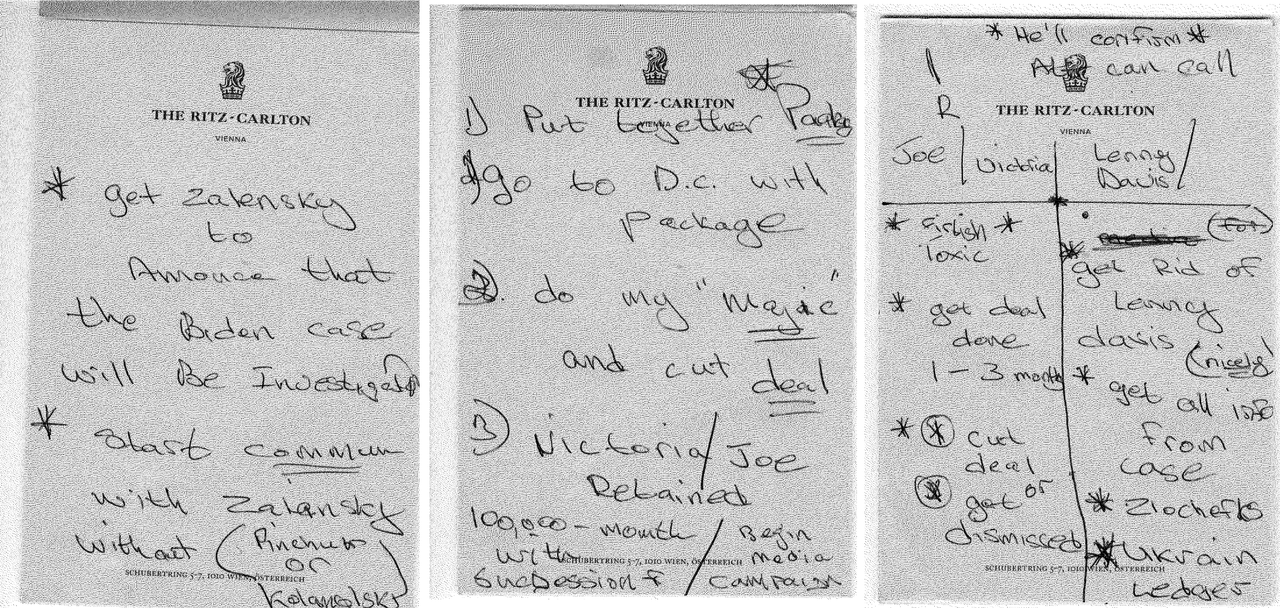

The first segment of the 38-page release contains several pages of undated, unverified, hand-written notes from the Ritz-Carlton Vienna, ostensibly penned by Parnas – which state “get zelensky to announce that the Biden case will be investigated,” and “Put together package,” followed by “Go to D.C. with package,” and “Do my ‘magic’ and cut deal.”

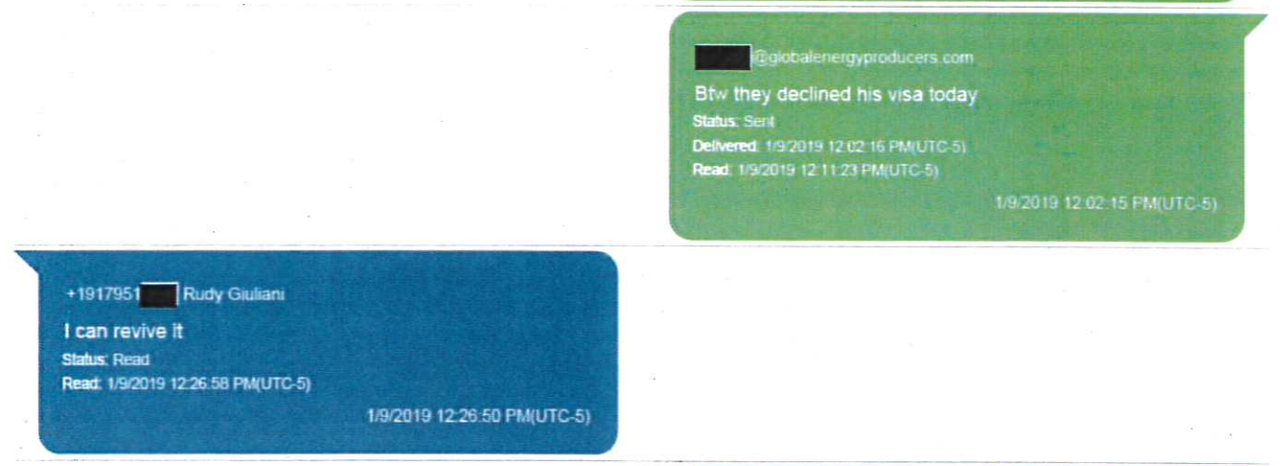

The second segment details January, 2019efforts by Parnas to have Rudy Giuliani secure a visa for Viktor Shokin – the former Ukrainian prosecutor who instead testified via a January, 2019 phone call that he was fired at the request of then-VP Joe Biden for investigating Burisma – a Ukrainian gas company which hired Biden’s son hunter for more than $50,000 per month to sit on its board.

“Btw they declined his visa today,” Parnas wrote Giuliani, referring to Shokin, to which Giuliani responds “I can revive it.”

Despite Giuliani involving “no 1” on it (possibly Trump), he was ultimately unable to secure the visa, leading to Shokin’s testimony via telephone.

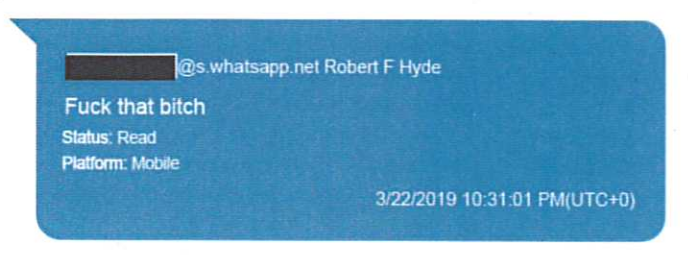

The third segment of the release involves discussions from March, 2019 between Parnas and an associate surrounding the effort to get former US ambassador Marie Yovanovitch fired. The associate, Congressional House GOP candidate Robert F. Hyde of Connecticut, appears to have ties within the incoming Zelensky administration – which wanted Yovanovitch fired.

Robert F. Hyde poses with President Donald Trump

“Fuck that bitch” Hyde texts Parnas – referring to fired US ambassador Marie Yovanovich, who ran the US embassy in Kiev at the time. “Wow. Can’t believe Trumo [sic] hasn’t fired this bitch. I’ll get right in that.”

Without instruction from Parnas, Hyde then texts Parnas to let him know that his associates on the ‘inside’ say she is “under heavy protection outside Kiev,” to which Parnas replies “I know crazy shit.”

Then, Hyde says ‘his guy’ (within the Zelensky administration) thinks Russia’s FSB may be protecting Yovanovitch.

Here is the entire exchange between Parnas and Hyde (emphasis ours, via /u/ihategelatine) – which is currently being used to suggest nefarious intentions against Yovanovitch.

Robert F. Hyde: Fuck that bitch

Parnas: [links multiple articles]

Robert F. Hyde: Wow. Can’t believe Trumo [sic] hasn’t fired this bitch. I’ll get right in that.

Robert F. Hyde: [Links multiple articles/pictures]

Robert F. Hyde: She under heavy protection outside Kiev

Robert F. Hyde: The guys over they asked what I would like to do and what is in it for them

Robert F. Hyde: Wake up Yankees man

Robert F. Hyde: She’s talked to three people. Her phone is off. Computer is off.

Robert F. Hyde: She’s next to the embassy

Robert F. Hyde: Not in the embassy

Robert F. Hyde: Private security. Been there since Thursday.

Parnas: Interesting

Robert F. Hyde: They know she’s a political puppet

Robert F. Hyde: They will let me know when she’s on the move

Robert F. Hyde: And they will let me know when she’s on the move

Parnas: Perfect

Robert F. Hyde: I mean where if they can find out.

Robert F. Hyde: That adress I sent you checks out

Robert F. Hyde: It’s next to the embassy

Robert F. Hyde: They are willing to help if we/you would like a price

Robert F. Hyde: Guess you can do anything in the Ukraine with money… what I was told

Parnas: Lol

Robert F. Hyde: Update she will not be moved special security unit upgraded force on the compound people are already aware of the situation my contacts are asking what is the next step because cannot keep going to check people will start to ask questions

Robert F. Hyde: If you want her out they need to make contact with security forces

Robert F. Hyde: From Ukranians

Robert F. Hyde: What’s the word bro

Robert F. Hyde: Any good stuff?

Parnas: Call you soon in studio

Robert F. Hyde: Let’s go Holmes

Robert F. Hyde: RG was good. But Ingraham had some hard questions

Robert F. Hyde: Nothing has changed she is still not moving they check today again

Robert F. Hyde: Hi buddy

Robert F. Hyde: It’s confirmed we have a person inside

Parnas: [Links youtube video]: “Trumps takedown of FBI (Winning montage!)”

Robert F. Hyde: Nice

Robert F. Hyde: Hey brother do we stand down??? Or you still need intel be safe

Robert F. Hyde: She had visitors

Robert F. Hyde: It’s confirmed we have a person inside

Robert F. Hyde: Hey broski tell me what we are doing what’s the next step

Weeks after the exchange between Hyde and Parnas, Yovanovitch was recalled as ambassador on April 25, 2019. Exactly three months later on July 25, Trump would tell Zelensky on a now-infamous phone call that Yovanovitch was “going through some things.”

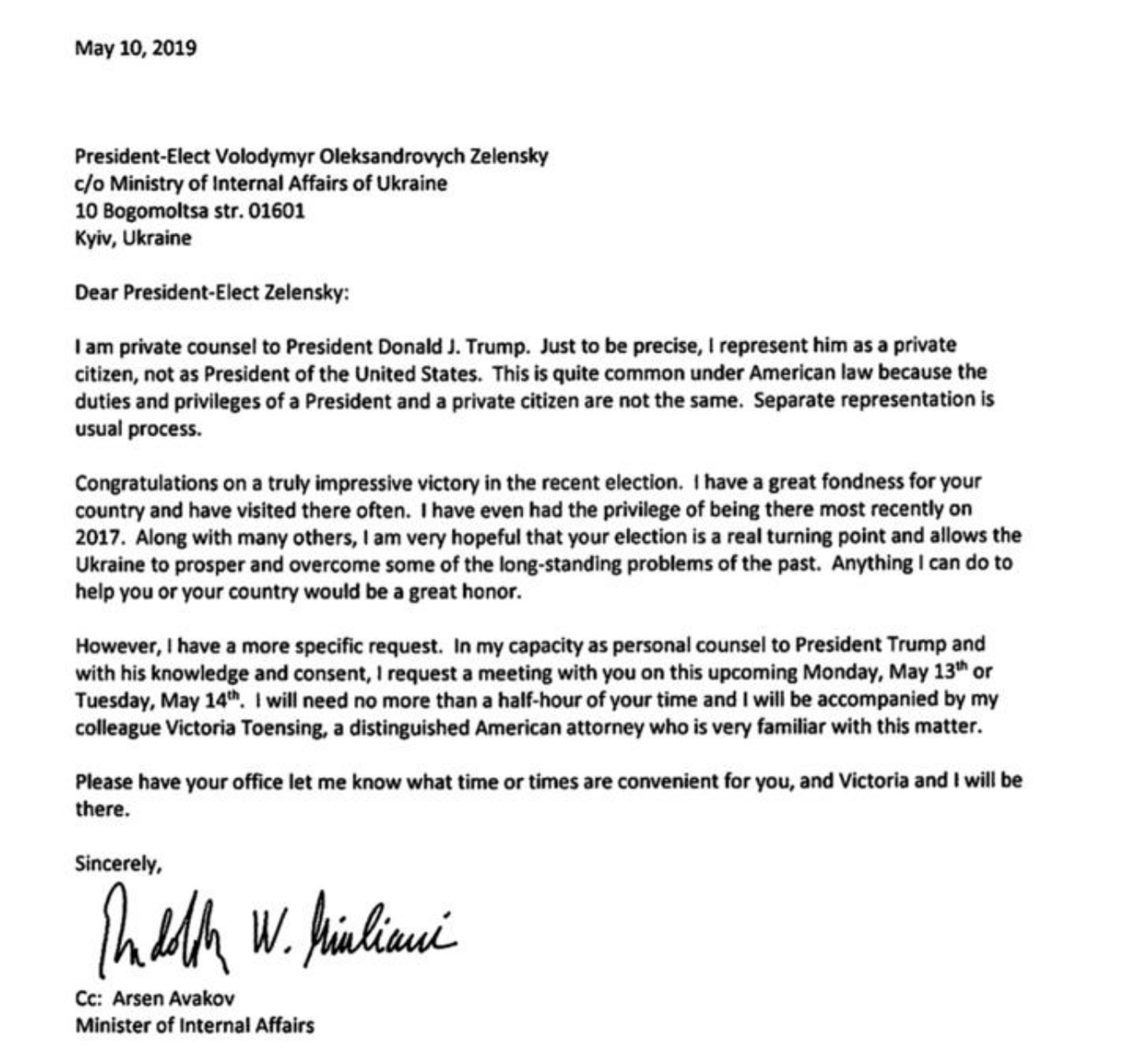

The fourth and fifth segments contain a May 10 letter from Giuliani to Zelensky asking for a 30-minute meeting, and unidentified text messages from May, 2019.

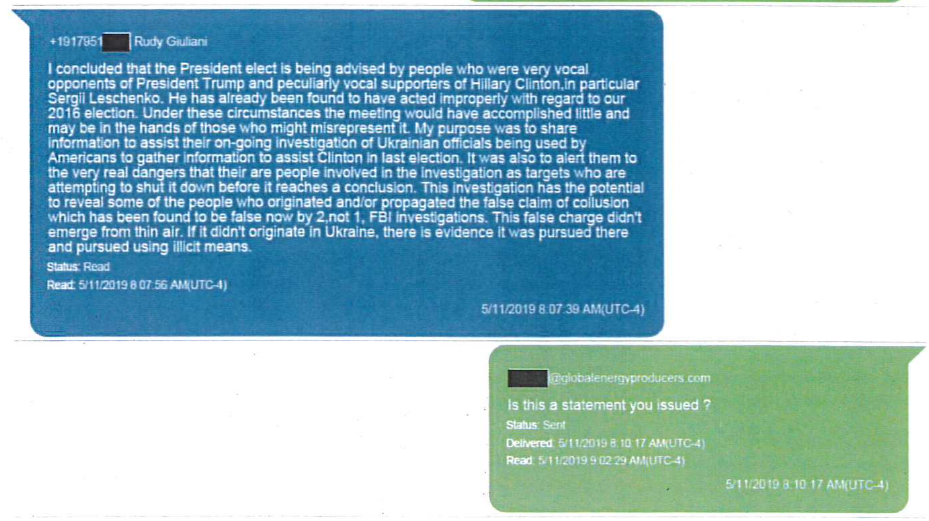

The sixth segmentcontains what appears to be Rudy spitballing his case to Parnas, writing in several texts on May 11:

“I am going to say I have been informed the people advising the PRES ELECT [Zelensky] are no friends of the President [Trump]. At least one was involved in delivering fraudulent evidence falsely accusing the campaign and made horrible statements about his desire to defeat him. Hopefully Pres elect will realize that tge [sic] operatives around him don’t have his best interests at heart.”

“I concluded that the President elect is being advised by people who were very vocal opponents of President Trump and peculiarly vocal supporters of Hillary Clinton, in particular Sergei Leschenko. He has already been found to have acted improperly with regard to our 2016 election. Under these circumstances the meeting would have accomplished little and may be in the hands of those who might misrepresent it. My purpose was to share information to assist their on-going investigation of Ukrainian officials being used by Americans to gather information to assist Clinton in last election. It was also to alert them to the very real dangers that their [sic] are people involved in the investigation as targets who are attempting to shut it down before it reaches a conclusion. This investigation has the potential to reveal some of the people who originated and/or propagated the false claim of collusion which has been found to be false now by 2, not 1, FBI investigations. The false charge didn’t emerge from thin air. If it didn’t originate in Ukraine, there is evidence it was pursued there and pursued using illicit means.”

Parnas seems to be confused by Giuliani’s text, writing back “Is this a statement you issued?”

In response to the released documents, Marie Yovanovitch told MSNBC that there should be an investigation into whether she was monitored in Ukraine.

Core Producer Price Inflation Tumbles To Weakest Since 2016

Following the surprise acceleration in consumer prices, producer prices were expected to re-accelerate after diverging for three months. While the MoM gain in headline PPI was a slight disappointment (+0.1% vs +0.2% MoM) but on a YoY basis it met expectations at +1.3% (still well below CPI)…

Source: Bloomberg

However, core producer price gains (ex-food and energy) were the weakest since August 2016 at just +1.1% YoY…

Source: Bloomberg

Certainly nothing here to spook The Fed into any hawkish action.

This is a collection of 32 tactics, instances, misnomers, immortal fake propaganda, and even wrong-doing cropping up ceaselessly on Wall Street, in the media, in press releases, in earnings reports, and in the broader nexus between Wall Street and the media.

All of them were pointed out by WOLF STREET commenters. I put them together and grouped some of them, and added some explanations in a few cases even when not needed. In no particular order:

#1: “The moronic statements regarding ‘money on the sidelines.’”

“That ‘money on the sidelines’ thing drives me nuts. I sit around wondering how captured financial commentators must be to even entertain such concepts on such a regular basis.”

“Money on the sidelines is immortal. It has been cited all my investing life, and it will still be cited long after I’m gone, to be passed proudly from generation to generation, no matter how often it gets debunked.”

“I found a coin on the sidewalk once. It must be the infamous sidelines money. Just a million coins more, and I will have enough to go on vacation.”

#2: “The claptrap surrounding earnings beats – after earnings targets have been quietly but drastically reduced.”

#3: “Forward earnings projections” to rationalize high stock prices. Everyone is doing it, even the Fed. Forward earnings projections are part of the great body of American fiction and get slashed as earnings-report dates get nearer so that the much-lowered projections can then be “beat” (see #2 above). This produces the absurd situation where forward P/E ratios are always far lower (currently 18.4 according to FactSet) than the actual P/E ratios (currently 24.6, highest since the Financial Crisis).

#4: “The revolving door between government and Wall Street – ‘the swamp.’” Drain it already.

#5: “The revolting door between government and Wall Street” – that would be one of Wolf’s infamous typos.

#6: “Exclusion of negative earnings from P/E calculations of broad indices.” The Russell 2000 does this. There are a large number of loss-making companies in the index. Excluding their negative earnings distorts earnings measures of the Russell 2000, such as the P/E ratio of the index. With losses included, the P/E ratio of the Russell 2000 would be about four times higher than the officially quoted P/E ratio without losses. It’s not a secret: FTSE Russell and iShares disclose that losses are excluded; but it’s the fake P/E ratio without losses that is being quoted all the time to rationalize high stock prices.

#7. “Bogus ‘Chinese Walls’ and other internal conflicts of interest.”

#8. “Arms-length Agreements” to describe veiled self-dealing.” Also see #7 above.

#9. “Mark-to-Fantasy accounting standards.” A common situation when an asset is valued on the balance sheet based on whatever (including wishful thinking) instead of market price because the market price would be too inconvenient.

#10. “‘Non-GAAP’ accounting metrics.” This might be fake income with all the bad stuff removed, producing a “non-GAAP” profit vs. a GAAP loss, a common feature in earnings reports by Corporate America. Or it might be homemade metrics that everyone has to pay attention to, while ignoring the GAAP accounting metrics.

In the same non-GAAP vein: “Use of EBITDA and subtracting all ‘nonrecurring items’” – which turn out to recur regularly.

#11: “GAAP accounting metrics…” ha, we knew that.

#12: “Debt-financed share buybacks” – a form of equity stripping.

#13: “Positive coverage of ‘share buy backs,’ ostensibly to enrich share ‘owners,’ but really to enrich share sellers and to recycle management stock options through the corporate treasury?”

In the same vein: “Mopping up overgenerous stock options by looting the treasury with share buybacks, described as “Returning Shareholder Value,” while never paying a dividend.”

#14: “Leveraged buyouts with asset-stripping.” This was a favorite in brick-and-mortar retail some years ago, leading to a massive pileup of bankruptcies by major retailers, such as Toys “R” Us.

#15: “Banging the Close.” This can occur in all markets, including cryptos. Here is a definition for the futures market, where it is illegal: “A manipulative or disruptive trading practice whereby a trader buys or sells a large number of futures contracts during the closing period of a futures contract (that is, the period during which the futures settlement price is determined) in order to benefit an even larger position in an option, swap, or other derivative that is cash settled based on the futures settlement price on that day.”

#16: “Citizens’ United”: The US Supreme Court case on campaign finance, Citizens United v. Federal Election Commission, as explained by SCOTUSblog: “Political spending is a form of protected speech under the First Amendment, and the government may not keep corporations or unions from spending money to support or denounce individual candidates in elections. While corporations or unions may not give money directly to campaigns, they may seek to persuade the voting public through other means, including ads, especially where these ads were not broadcast.”

#17: “Gimmicks to mask stock-compensation expenses.” Also see #13 above.

#18: “Cost-of-Business fines to punish corporate wrongdoing, rather than punitive damages plus jail time for responsible individuals.” This includes fining a company like Facebook what looks like a large amount for serious wrong-doing, but that represents only a fraction of its quarterly profit and just becomes part of the cost of doing business.

#19: “Perfectly Legal tax-avoidance schemes.”

#20: “Quarter-End Window Dressing.”

#21: “Pump-and-Dump” – which is a feature, not a bug in some of the reporting.

#22: “Front-Running and stop-loss harvesting from peeking at orders.”

#23: “Narrative Fraud (hyping fake news).”

#24: “The media conveniently forget to disclose the financial interests of guest speakers in their financial columns and misinformation shows. I wouldn’t put it past the MIC ‘swamp’ to purposely misinform the POTUS, as well. Rid us of the swamp already!”

#25: “Goodwill.” But wait… this is GAAP accounting. See #11 above.

#26: “High-frequency trading which evaporates whenever the market needs genuine liquidity.”

#27: “Wagging the Dog – manipulating markets via fake or incorrect headlines to trigger reactions from speed-reading algorithms.”

#28: “Wagging the Dog 2 – manipulating primary securities prices in liquid markets via small-scale trades in illiquid derivatives markets.”

#29: “Opinion presented as fact, especially on the front page rather than editorial pages.”

#30: “Machine-generated formulaic articles which aren’t labeled as such.” But wait… they’re so cheap and nearly instant to generate, and machines (trading algos) love reading machine-generated articles! No humans needed.

#31: “The mindset in which ‘If 2 sources say the same thing it must be published as if true,’ especially when the 2 sources are colluding behind-the-scenes.

#32: “The savings glut.” Yeah, that’ll be the day.

Target Shares Plunge After Holiday Sales Missed Forecasts

Target shares plunged as much as 8.8% on Wednesday morning after it cut its fourth-quarter comparable sales view due to a rather depressing holiday sales season, missing the average Wall Street estimates.

Erasing most of last quarter’s gains…

Target said same-store sales for the quarter were up just 1.4%, missing Wall Street estimates of 3.8%.

Sees 4Q comparable sales +1.4%, estimate +3.8% (Consensus Metrix, average of 20 estimates)

Still sees FY adjusted EPS $6.25 to $6.45, estimate $6.49 (range $5.95 to $7.01) (Bloomberg data)

“We faced challenges throughout November and December in key seasonal merchandise categories, and our holiday sales did not meet our expectations,” Chief Executive Brian Cornell said.

The company noted that apparel and beauty sales outperformed, while electronics, toys, and home goods offset those gains.

Digital sales jumped 19% over the period thanks to curbside pick when orders are placed online. The company said the online service increased by 50% during November and December compared with the same period in 2018.

Target shares plunged as much as 8.8% premarket on Wednesday due to weak holiday sales and missing Wall Street estimates. The decline in Target also sparked retail selling panic that has now spread into Walmart.

Macy’s, J.C. Penney, and Kohl’s have all reported same-store sales declines for the holiday season, which begs the question: Is the retail industry flashing a warning sign that could suggest the consumer isn’t as strong as Wall Street thinks?

There’s also another important question we must ask: Has the industrial recession, that has already triggered an employment slowdown, now starting to weigh on consumers?

If so, Target could be an important bellwether that suggests economic weakness could persist in 2020 – rather than a massive recovery the stock market has already priced in.

“A Fragile Truce”: Here’s What’s In Trump’s “Big Beautiful Monster” Of A Trade Deal

Earlier this month, President Trump referred to his ‘Phase 1’ trade pact as a “big, beautiful monster.” But for most of the trade hawks in his administration, it will likely be a disappointment – though hope remains for a more comprehensive ‘Phase 2’ pact after the election, assuming Trump wins a second term.

Rather than ending trade tensions with Beijing, the “hard fought” agreement will help establish a “fragile truce” between the world’s two largest economies, the FT reports. Indeed, many feel like the only reason we’re even getting a deal is thanks to escalating anxieties about slowing growth (in Beijing) and worries about a major market selloff heading into November (in Washington). Trump is worried because it’s an election year, and President Xi is worried because China’s powerful growth engine has started to slow, threatening to sow instability and discord among China’s population.

Based on what we know so far, this is the core of the agreement: The US has agreed to halve 15% tariffs on $120 billion in Chinese imports and an indefinite delay on further tariff hikes. In return, China has promised to make structural reforms, and buy an additional $200 billion over 2017 levels in goods and services over the next two years.

The agreement will be signed by Trump and Vice Premier Liu He during a White House ceremony at 11:30 am, and the full text is expected to be released on Wednesday, though some details will remain secret.

However, the deal leaves in place the bulk of tariffs imposed by Trump on $360 billion of Chinese imports – nearly all of the Chinese made products flowing into the country – while the top concerns of America’s trade negotiators remain unaddressed: China refused to offer concession on issues from state subsidies to rampant cyber theft. As one Communist Party functionary said this week: “If the policies are working, why should we change?”

Initial skepticism about the capacity for Beijing’s state-controlled companies to increase imports by such a large margin has been rebuffed by a team of analysts at Goldman Sachs, who now believe that China can fulfill its $200 billion promise as we reported yesterday. They even devised a sample scenario of what that might look like:

The trade deal with Beijing is essentially an informal agreement, not a treaty or an official trade pact (like USMCA), which means Trump doesn’t need Congress’s approval to sign off. At 86 pages, it’s pretty thin for a trade agreement. There’s something else about the deal that’s unique: As Bloomberg points out, it embraces a “socialist-style central planning” that might have been anathema to prior Republican administrations.

That’s because the deal sets fixed amounts for China’s purchases of American products. A classified part of the deal breaks down the planned purchases in detail.

The deal also embraces a level of Socialist-style central planning that would have made past American presidents wince. While trade pacts traditionally set the rules and leave the details of actual commerce to markets, the one that Trump’s team has negotiated includes a classified annex that details the $200 billion Chinese buying spree.

That includes some $32 billion in additional purchases of American farm exports and $50 billion in natural gas and crude oil, according to people briefed on its contents. The administration insists the different nature of the deal is by design and that it won’t need the approval of Congress. “

This is not a free trade agreement,” it told supporters in a memo last month. “Its purpose is to rectify unfair trade practices.”

One analyst argues that the deal, while a welcome development for the markets, does little to curb the economic rivalry between the two countries or even meaningfully reduce trade tensions (since most of the tariffs will remain in place until at least November as an enforcement measure). Moreover, significant uncertainties remain on the parameters of the purchase agreement.

It also does nothing to de-escalate the growing military tensions in the Pacific, tensions with Taiwan, and objections to Beijing’s internment of Muslims in Xinjiang.

“The signing of this truce, while welcome, does not obviate the reality that both countries view one another in increasingly antagonistic terms,” said Ali Wyne, a policy analyst at the Rand Corporation, a think-tank in Washington. “Washington regards Beijing’s economic ascendance as a threat to its national security and that of its allies and partners; Beijing, meanwhile, considers the acceleration of indigenous innovation and the cultivation of alternative export markets to be existential imperatives.”

As the administration began the process of selling the deal to the American public, Treasury Secretary Steven Mnuchin appeared on CNBC Wednesday morning to try and butter up the market.

And some analysts are already singing Trump’s praises.

“It’s a major victory for the president,” said Stephen Vaughn, who until last year helped oversee Trump’s trade policies as the general counsel and right-hand man to U.S. Trade Representative Robert Lighthizer. “He has gotten China to make stronger commitments than it has made in previous agreements.”

Will Trump’s ‘Phase 1’ deal finally break the ‘Trade War cycle’ that has partly dominated markets over the last two years?

If not, fear not: speaking on CNBC, Steven Mnuchin said that a Phase 2 deal could come in multiple steps, such as 2A, 2B, 2C and so on… in other words, whatever it takes to push stocks higher on constant “trade deal optimism.”

BofA Beats Boosted By Buybacks As FICC Revenue Rebounds While NIM Tumbles

Continuing the barrage of Q4 bank earnings reports started with better than expected results by JPMorgan and Citi, and offset by the latest dismal report from Wells Fargo, moments ago BofA reported so-so Q4 earnings, with better than expected earnings driven by a surge in FICC trading, while overall revenue disappointed as the bank’s consumer division disappointed as Net Interest Margin tumbled to a new all time low.

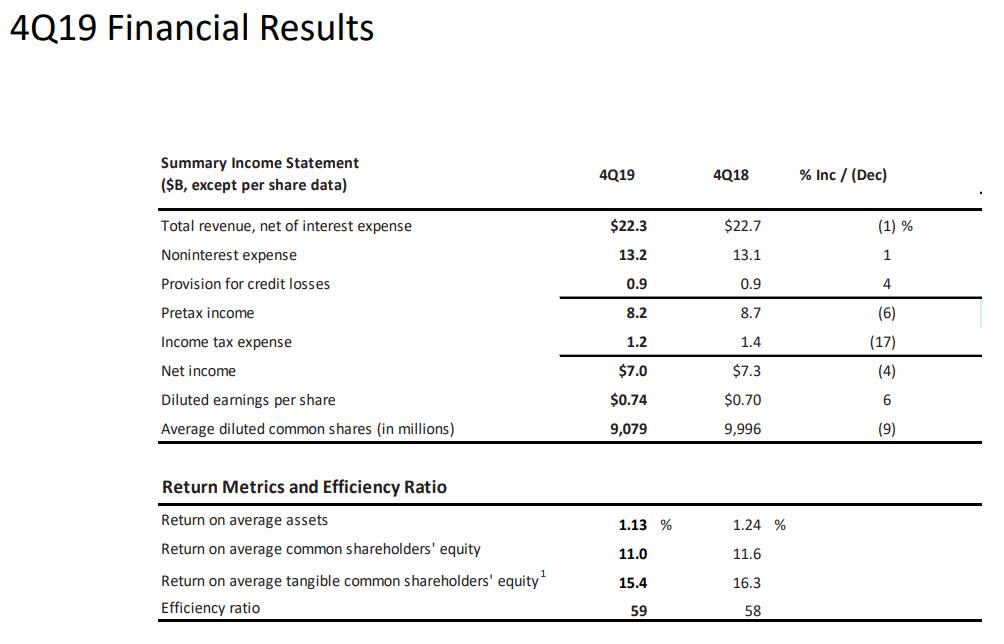

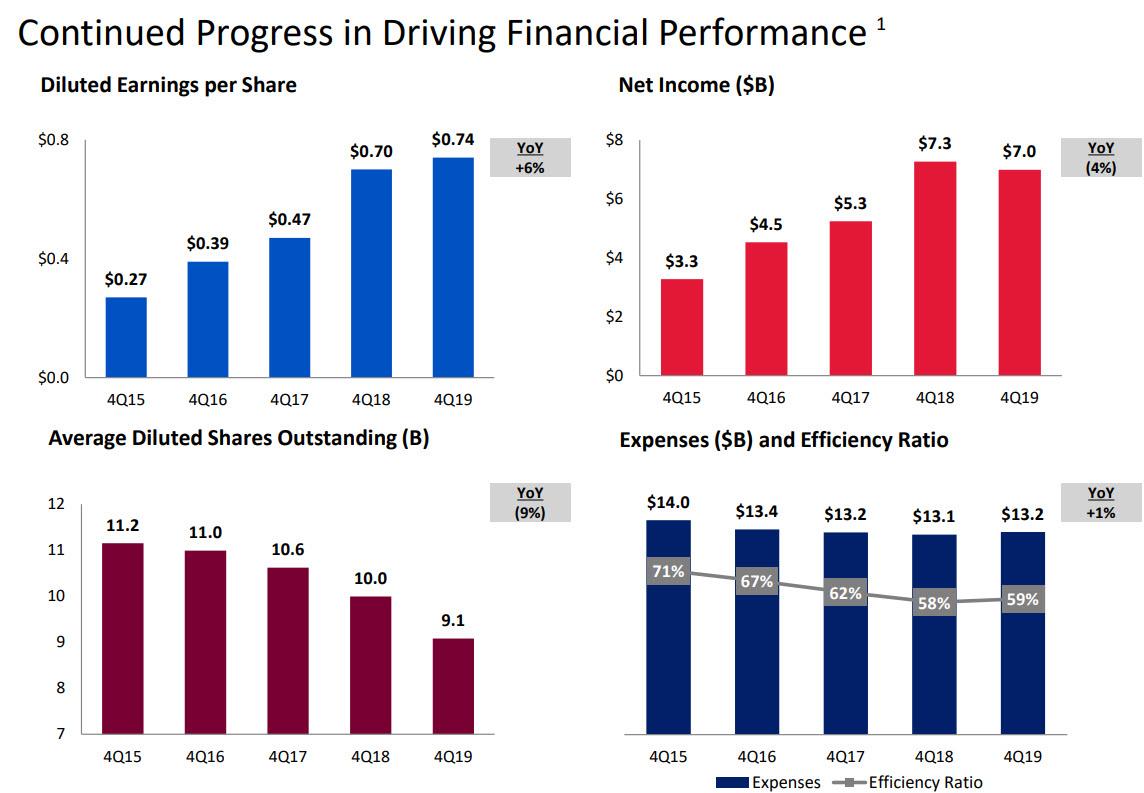

Starting at the top, BofA reported Q4 EPS of $0.74, beating expectations of $0.70, and up 6% from the prior year, even as revenues of $22.3BN declined 1% from $22.7BN one year ago, missing expectations of a $22.36BN print, with Net Income also declining to $7.0BN from $7.3BN.

But how did EPS rise 6% even as Net Income declined 4% Y/Y? Simple: the bank repurchased 9% of its shares outstanding, while keeping its expenses flat.

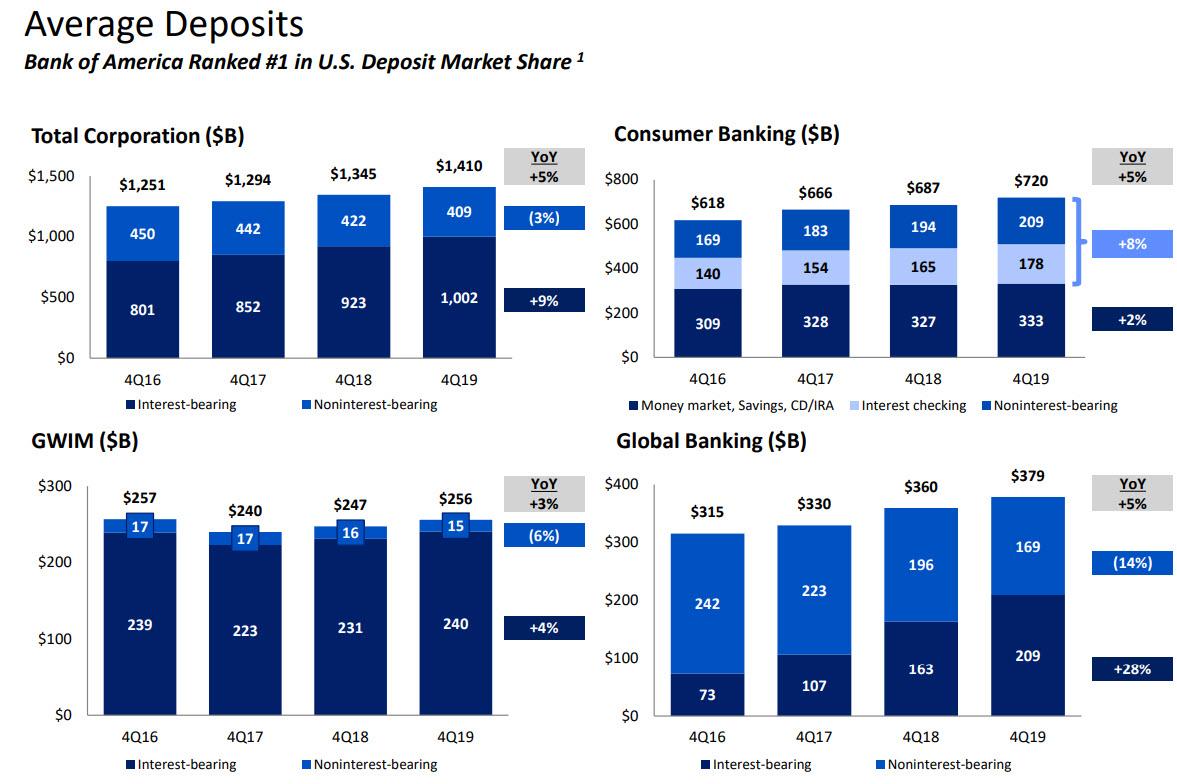

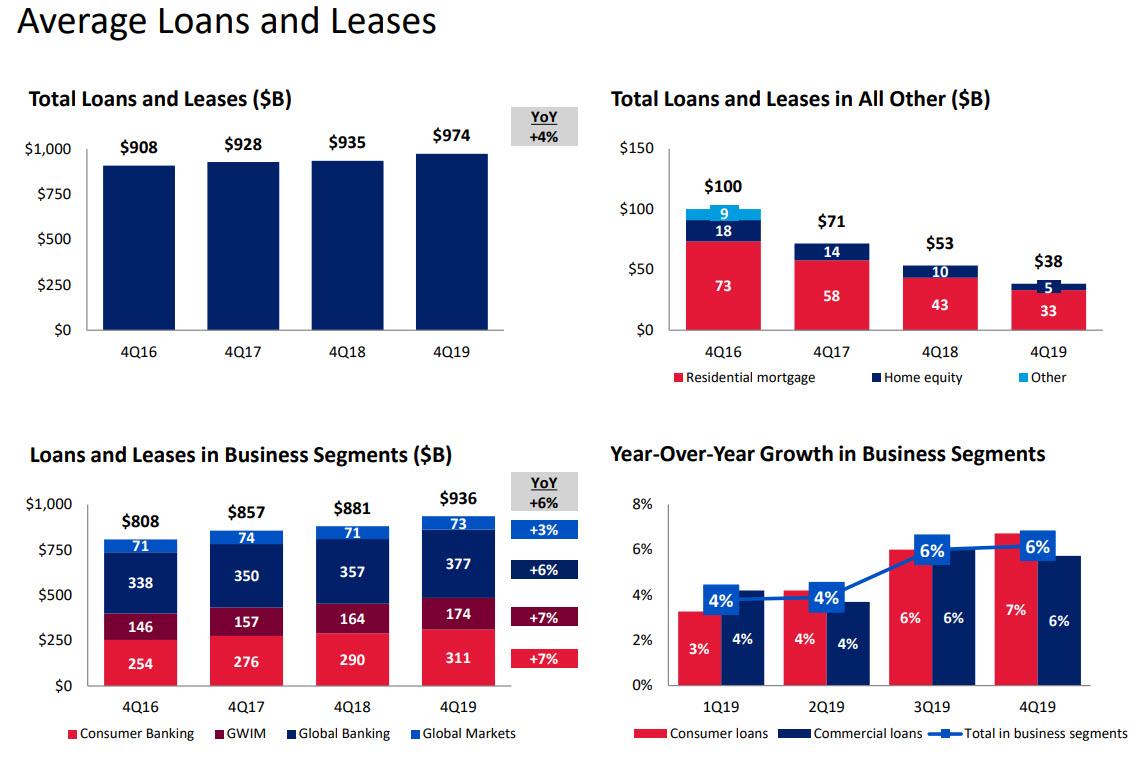

A quick look at the company’s balance sheet reveals a continuation of historical trends, with total deposits up 5%…

… while total loans and leases increased 4% Y/Y.

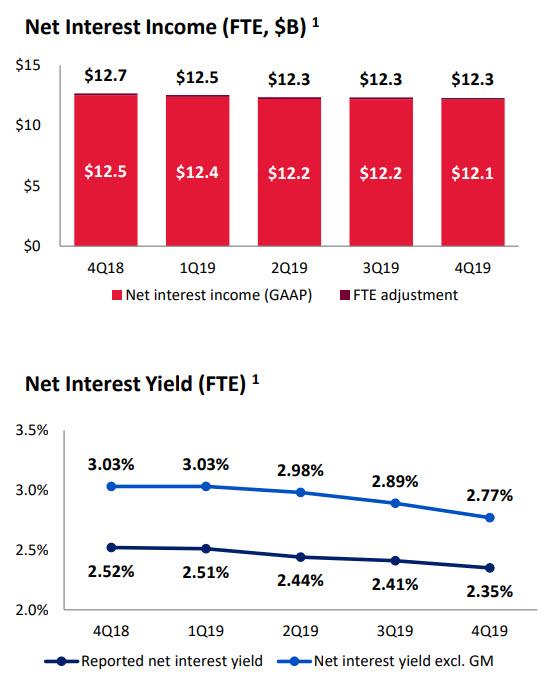

However, in a concerning similarity to Wells Fargo, BofA’s Net Interest Income declined once again, with its net interest margin sliding to 2.35% from 2.41%, a fresh all time low. The good news: despite the ongoing slowdown, the bank’s unadjusted net interest income of $12.1BN just barely beat expectations of $12.09BN. This is how the bank described this segment:

Net interest income of $12.1B ($12.3B FTE), “decreased $0.4B, or 3%, from 4Q18, driven primarily by lower interest rates, partially offset by loan and deposit growth.” The NII declined modestly from 3Q19, as lower asset yields were partially offset by lower funding costs as well as benefits of loan and deposit growth. Worse, the net interest yield of 2.35% decreased 17 bps from 4Q18 and decreased 6 bps from 3Q19. And is where the Fed’s rate cuts helped: the average rate paid on interest-bearing deposits declined 15 bps from 3Q19 to 0.61%.

“We enter 2020 with momentum,” CEO Brian Moynihan said in a statement, although one look at the chart below and one can see that he wasn’t referring to the company’s core Net Interest Income: indeed, the trend here shows NIM continuing to decline as the Fed is now terrified of ever again hiking rates.

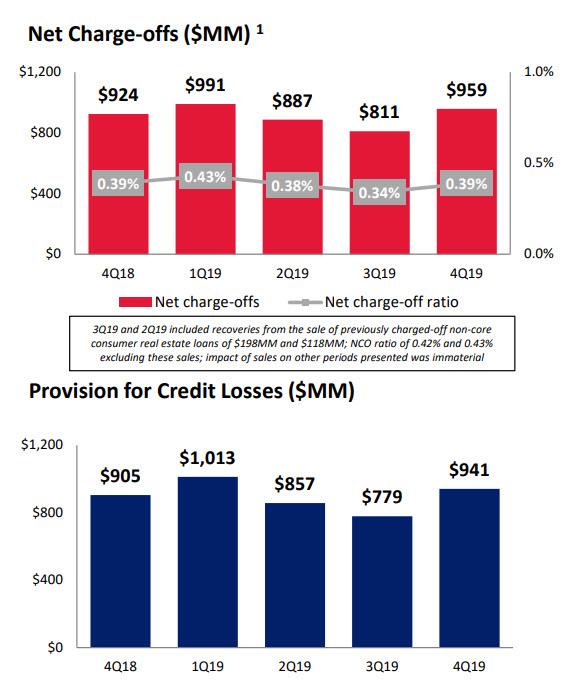

And balance sheet highlight: BofA’s total net charge-offs in Q4 jumped to $959MM from $811MM in Q3, if modestly down from 3Q19, although one should note that the 3Q19 and 2Q19 included recoveries from the sale of previously charged-off non-core consumer real estate loans of $198MM and $118MM, resulting in NCO ratio of 0.42% and 0.43%. Excluding the loan sales in 3Q19, net charge-off ratio decreased 3 bps to 39bps.

Putting this together revealed a rather unpleasant picture, as net income at the bank’s consumer division slid 9.7% to $3.11 billion as interest income fell, with revenue dropping 4% to $9.5B, driven primarily by lower NII.

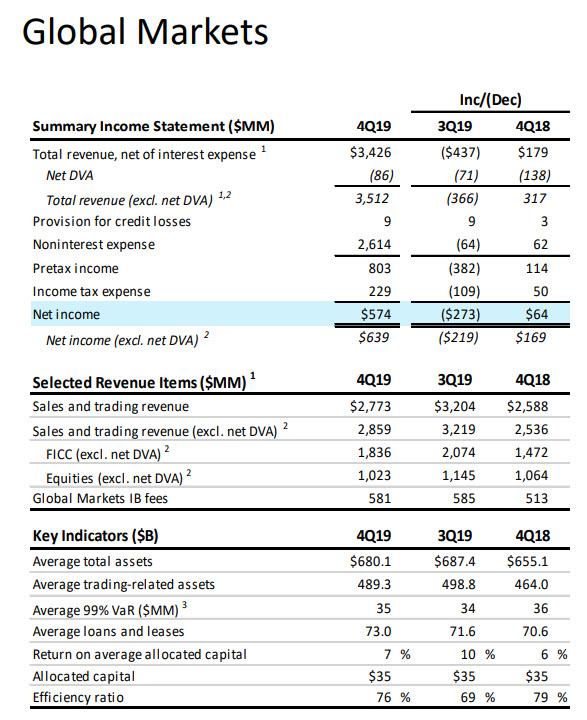

But if the bank’s core business was the bad news, this was more than offset by the bank’s Investment Banking and Markets results, as trading revenue climbed 13% to $2.86 billion, beating the estimate of $2.76 billion, helped by fixed-income activity even as equities trading disappointed. Here is the full breakdown:

4Q FICC trading revenue excluding DVA $1.84 billion estimate $1.68 billion, +25% y/y, “driven by an improvement in most products, particularly mortgages”

4Q equities trading revenue excluding DVA $1.02 billion vs estimate $1.08 billion, -3.3% y/y, “driven by lower levels of client activity in derivatives”

Meanwhile, Bank of America’s investment-banking fees rose 9.3% from a year earlier to $581 million after a blockbuster third quarter, with the investment-banking division continuing its turnaround under Matthew Koder.

As Bloomberg notes, the fourth-quarter markets results were similar to those of JPMorgan which posted a record performance in bond trading Tuesday, and Citigroup Inc., where debt trading jumped by more than double what analysts had forecast.

The bottom line: Bank of America, and other banks which have solid trading desks and benefited from the Fed’s launch of QE4 in the fourth quarter, managed to report (somewhat) stronger than expected results (also benefiting from massive stock buybacks), even as their core Net Interest Income continued to decline. Meanwhile, banks such as Wells which remain entirely dependent on NIM continue to sink as central banks have no choice but to cut rates ever lower to zero and below, and one should merely look to Deutsche Bank to find out how this all ends.

World Stocks Pause At Record High To Asses US-China Trade Deal

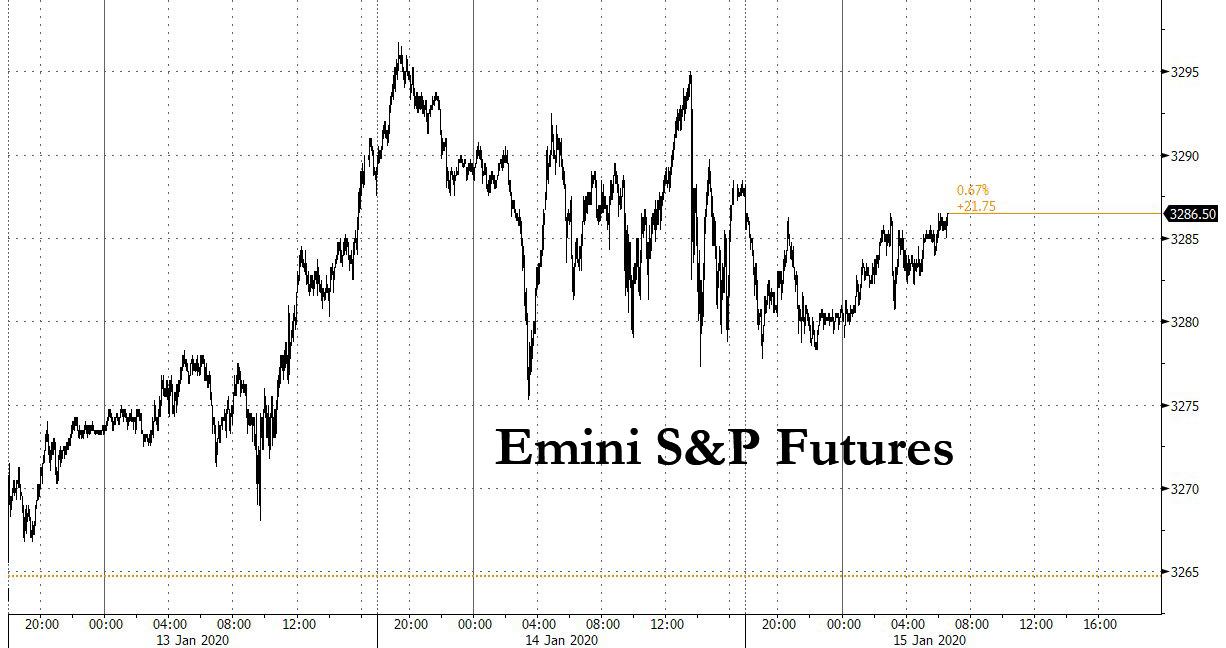

US equity futures dipped and world stocks eased off record highs on Wednesday with US and German bond yields slipping as euphoria over the US-China trade deal set to be announced today fizzled after Steven Mnuchin said tariffs on billions of dollars of Chinese goods coming into the U.S. are likely to stay in place until after the U.S. presidential election.

Today’s main event will be the phase one trade deal signing. As DB’s Jim Reid writes, the closely guarded text still remains a bit of a mystery and as such the devil will be in the detail. All will be revealed later though with a reminder that the signing is expected to take place at the White House at 11.30am EST. It’s said to be an 86 page document but for those of us used to 550 plus page Brexit agreements that were eventually voted down this is a walk in the park. Joking aside the main headline yesterday came after Europe went home as Bloomberg reported (after others had hinted earlier) that existing tariffs on billions of Chinese goods will remain until after the US election to allow the administration to review Chinese compliance before removing them. However, Treasury Secretary Steven Mnuchin said later that China won’t win US tariff relief until the two countries reach a Phase 2 accord and added that there was no link between the timeline for tariff reductions and the November election. So the US will maintain 25% tariffs on $250 billion of Chinese imports and 7.5% on a further $120 billion for now. This news wasn’t a big surprise really but markets lost traction and dipped into the red after the headlines offsetting the small positive momentum post the dovish US CPI and the bumper start to US bank earnings. Elsewhere, the top trade officials of the US, the EU and Japan struck a deal yesterday in Washington to expand the kinds of industrial subsidies prohibited by the WTO.

“Despite the landmark signing of the U.S.-Sino trade deal today, markets are unenthused,” said Rand Merchant Bank economist Nema Ramkhelawan-Bhana. “Phase One, though positive, is merely the start of a long process to undo the damage already inflicted on the global trade order.”

Share prices pulled back from recent highs on Wednesday after Wall Street closed weaker on Tuesday, with the Stoxx 600 index dipping in the red, with gains for health-care shares countered by drops in carmakers and insurers, triggered by Mnuchin’s comments that U.S. tariffs on Chinese goods would stay until the completion of a second phase of a U.S.-China trade agreement. Their eventual removal hinged on Beijing’s compliance with the Phase 1 accord, Bloomberg reported, citing sources.

Earlier in the session, MSCI’s index of Asian shares ex-Japan retreating from 19-month peaks and Japan’s benchmark Nikkei likewise falling 0.5%, off a four-week high, hours before the U.S. and China are due to sign their phase-one trade deal. The region’s benchmark MSCI Asia Pacific Index snapped a four-day winning streak. Philippine and Indonesia shares were among the biggest decliners, while Australia’s S&P/ASX 200 Index and the New Zealand Exchange 50 Gross Index hit new highs. Bourses in China, South Korea and Hong Kong lost between 0.5%-0.7% on the day. India’s Sensex also declined. Technology was the worst-performing sector. Heavyweights such as Taiwan Semiconductor Manufacturing Co. and Samsung Electronics Co. both retreated after recent rally. Here are some notable movers in the region:

European bonds held gains after data showed the German economy expanded at the slowest pace in six years in 2019…

… with gilts outperforming after U.K. inflation ebbed to a three-year low, virtually assuring more Bank of England interest-rate cuts.

The 18-month long trade feud between the US and China is set for a ceasefire in just hours as President Donald Trump and Chinese Vice Premier Liu He sign an initial agreement that would boost Chinese purchases of U.S. manufactured and agricultural goods, energy and services. Dubbed the Phase 1 deal, it may ease concerns about the economy, if not markets which are at all time highs on constant “trade war optimism”, as the conflict between the world’s two largest economies hit hundreds of billions of dollars in goods, uprooted supply chains and slowed economic growth.

Stocks stumbled after Mnuchin’s Tuesday comments that U.S. tariffs on Chinese goods would stay until the completion of a second phase of a U.S.-China trade agreement. Their eventual removal hinged on Beijing’s compliance with the Phase 1 accord. The news did not entirely surprise markets, however, and many attributed the pullback to profit-taking off the recent rally than to any turn in underlying sentiment.

“The Phase One deal had pretty much been priced in so (Mnuchin’s) comments took some steam out of the market last night and that’s feeding through into today,” said Justin Onuekwusi, a portfolio manager at Legal & General Investment Management.

The jittery mood gave a mild boost to safe-haven assets such as gold, with the precious metal ticking up 0.3% after two days of losses. The Japanese yen and high-grade bonds also firmed slightly, though the yen was only 0.1% higher versus the dollar and a whisker off 7-1/2-month lows of 110.22. The euro rose versus the dollar, which erased earlier gains against some of its biggest peers. The trade-reliant Australian dollar slipped 0.3% against the greenback while the euro was broadly flat.

The big mover was the British pound which is down almost 2% this month versus the dollar as dismal economic numbers and policymaker comments have fanned expectations of an interest rate cut as soon as this month. A quarter-point cut is now fully priced by end-2020.

Elsewhere, U.S. Treasury yields also ticked down, with the benchmark 10-year note yield falling more than 2 basis points to 1.7864%, hurt also by Tuesday’s data showing consumer prices undershooting expectations in December, which could allow interest rates to stay unchanged this year. German 10-year yields also eased 2 bps, having earlier hit two-week highs around minus 0.169% but their direction may hinge on 2019 German growth numbers which showed the biggest euro zone economy grew at its slowest since 2013.

The Market was also weighing the impact of the U.S. government nearing publication of a rule to vastly expand its powers to block shipments of foreign-made goods to China’s Huawei, as it seeks to squeeze the blacklisted telecoms firm.

“I think the Trump administration will continue to put pressure on China in this way or some other, even after signing a Phase 1 deal,” Yuichi Kodama, chief economist at Meiji Yasuda Life Insurance said.

And then there are earnings, with traders now focusing closely on company earnings from now, as Q4 EPS are expected to fall 0.6%. Big banks Goldman Sachs, Bank of America, BlackRock are among those reporting results later on Wednesday and expectations are high after JPMorgan posted record profits and Citi beat estimates, though Wells Fargo profits slumped.

“The market will see trade escalation taken off the table but it will start to focus on earnings. We saw huge multiple expansions in 2019 and that won’t happen again until we see earnings coming through,” Onuekwusi said.

In commodities, oil futures drifted, with West Texas Intermediate trading close to $58 a barrel. Gold nudged higher.

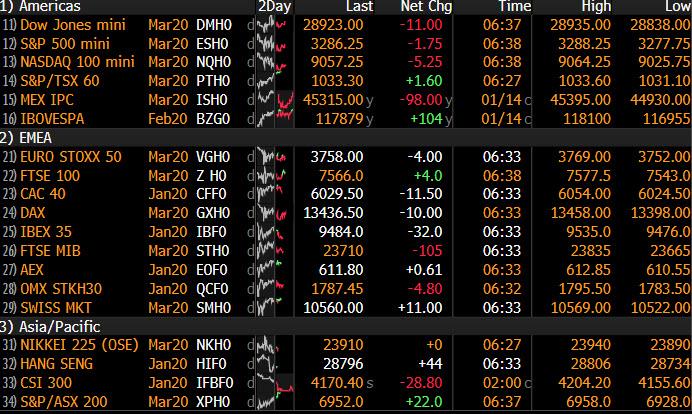

Market Snapshot

S&P 500 futures down 0.1% to 3,283.25

STOXX Europe 600 down 0.07% to 419.31

MXAP down 0.4% to 173.58

MXAPJ down 0.3% to 568.44

Nikkei down 0.5% to 23,916.58

Topix down 0.5% to 1,731.06

Hang Seng Index down 0.4% to 28,773.59

Shanghai Composite down 0.5% to 3,090.04

Sensex down 0.3% to 41,809.62

Australia S&P/ASX 200 up 0.5% to 6,994.84

Kospi down 0.4% to 2,230.98

German 10Y yield fell 3.0 bps to -0.201%

Euro up 0.04% to $1.1132

Brent Futures down 0.5% to $64.16/bbl

Italian 10Y yield rose 1.8 bps to 1.224%

Spanish 10Y yield fell 1.8 bps to 0.461%

Brent Futures down 0.5% to $64.16/bbl

Gold spot up 0.4% to $1,552.75

U.S. Dollar Index up 0.01% to 97.39

Top Overnight News from Bloomberg

Existing tariffs on billions of dollars of Chinese goods coming into the U.S. are likely to stay in place until after the U.S. presidential election, and any move to reduce them will hinge on Beijing’s compliance with the phase-one accord, people familiar said

President Donald Trump is poised to sign a deal with China on Wednesday that for the first time would punish Beijing if it fails to deliver on pledges related to its currency, intellectual property and the trade balance.

Germany’s economy expanded at the slowest pace in six years in 2019, when manufacturing took a battering and the country was dragged to the brink of a recession. Expansion was just 0.6% amid trade tensions and a broader slowdown in demand that added to fundamental structural challenges the country is battling

Qube Research & Technologies Ltd., the quant fund spun out from Credit Suisse Group AG with $1 billion in assets, has hired a trader from Barclays Plc as the firm expands into credit

University of Oxford, which traces its roots back to the 11th century, plans to sell sterling notes maturing in 2117, as pound investors seek out names likely to ride out Brexit risks

Ashmore Group Plc posted a 12th straight quarter of investor inflows, driving its assets to a record and bucking the downward trend among active asset managers

U.S. government is nearing publication of a rule that would vastly expand its powers to block shipments of foreign-made goods to China’s Huawei as it seeks to squeeze the blacklisted telecoms company, Reuters said, citing two sources

ECB officials see euro-area economy stabilizing at the start of 2020. Bank of France Governor Francois Villeroy de Galhau said recessions in the U.S. or Europe can practically be excluded this year. Executive Board member Yves Mersch said the 19-nation economy was “certainly giving good signs of stabilization”

China added liquidity to the financial system, helping to offset a cash squeeze ahead of the Lunar New Year holiday, while keeping interest rates on the loans unchanged.

Australian Prime Minister Scott Morrison said government will spend “as much as it takes” to help fire victims

U.S. House will vote Wednesday to send articles of impeachment against Donald Trump to the Senate for a trial that’s expected to begin early next week, but the president has yet to settle on either his defense strategy or the team that will represent him

Asian equity markets followed suit to the cautious performance on Wall St where there was a bias to the downside for most major indices on trade-related headwinds after US officials confirmed that China tariffs are to remain until after the US election despite the Phase 1 deal, although the DJIA remained afloat helped by banking names including JPMorgan at the start of earnings season. ASX 200 (+0.5%) extended on record highs and edged closer to the 7000 landmark amid mild gains in financials and as gold miners outperformed after a rebound in the precious metal, while Nikkei 225 (-0.5%) was lacklustre following the recent pullback from the 24k level and near its yearly high. Hang Seng (-0.4%) and Shanghai Comp. (-0.5%) also traded subdued on disappointment that the Phase 1 deal will not include a tariff rollback, which overshadowed the liquidity efforts by the PBoC that had announced CNY 300bln in MLF lending and to inject CNY 100bln through 14-day reverse repos ahead of the Lunar New Year scheduled next week. Finally, 10yr JGBs oscillated beneath the 152.00 level with participants sidelined ahead of a 5yr JGB auction and after BoJ Governor Kuroda failed to provide any fresh insights regarding monetary policy ahead of next week’s meeting, although prices later recovered as all metrics pointed to a stronger 5yr auction.

Top Asian News

MUFG Is Said to Appoint Kamezawa as CEO, Replacing Mike

China Adds $58 Billion Into Banking System as Holiday Nears

Bharti Airtel Raises $3 Billion for Fee Payment Due in a Week

Indonesia Makes Arrests as Scandal-Hit Insurer Probe Widens

European equities mostly see a relatively lacklustre session [Euro Stoxx 50 -0.1%] ahead of the much-anticipated Phase One deal signing with the region holding a more cautious bias. This follows on from a similar APAC performance which saw Chinese markets subdued on disappointment that US will not currently roll back on existing China tariffs. UK’s FTSE 100 outperforms on the back of a weaker Sterling boosting exporters in light of further dovish rhetoric from BoE dissenter Saunders coupled with sub-par UK CPI readings. Sectors are mixed with no clear reflection of the overall risk sentiment in the market. Healthcare outperforms with support from Roche (+0.6%) after the Pharma-giant announced commercial availability of a test which will help healthcare professionals better monitor and manage transplant patients at risk of infections. Elsewhere, the IT sector is underpinned by ASM International (+9.6%) whose share were bolstered by an upgrade to prior guidance. In terms of individual movers, Chr Hansen (-6.8%) fell to the foot of the Stoxx 600 following overall downbeat earnings and a downgraded outlook. Elsewhere, RBS (-2.7%), Eurazeo (+3.3%), Safran (+1.5%) have all been influenced by broker action.

Top European News

Aston Martin Needs at Least GBP400m of Equity, Jefferies Says

U.K.’s Flybe Rescue Shows It’s Tough for Governments to Go Green

In FX, the Pound wasn’t that perturbed about typically dovish commentary from BoE’s Saunders, but Cable subsequently retreated towards recent sub-1.3000 lows and Eur/Gbp rebounded to circa 0.8570 from just under 0.8540 when headline and core UK inflation both missed consensus by some distance. Indeed, the former printed at its weakest y/y pace in 3+ years and latter slowed to 1.4% from 1.7% previously and forecast to tip January easing expectations over 60% compared to less than evens ahead of remarks from one of the resident MPC rate cut dissenters.

AUD – Revelations that US-China trade deal Phase One will not come with any further tariff roll-backs or removal of existing levies on Chinese goods have undermined the Aussie more than most majors given its closer correlation to sentiment surrounding the issue and Yuan moves by proxy. Hence, Aud/Usd has reversed through 0.6900 again, as Usd/Cnh pares more losses and hovers above the latest lower Usd/Cny midpoint fix in contrast to the recent trend.

CHF/JPY/EUR/CAD/NZD/NOK/SEK – The Franc continues to outperform its G10 peers in wake of Switzerland’s inclusion on the list of currency manipulators compiled by the US Treasury, but Usd/Chf and Eur/Chf are also slipping on technical grounds and an element of safe-haven positioning to around 0.9655 and 1.0745 respectively. Similarly, Usd/Jpy is probing lower amidst an unwind of risk-on flows, and after topping out only a pip or so over 110.00 compared to 110.20 at one stage on Tuesday, while Eur/Usd is forging fresh 1.1150+ peaks after finally breaching aligning DMAs (21/200 marks both at 1.1138). Elsewhere, the Loonie remains softer within 1.3055-78 parameters against the backdrop of softer crude prices that are also niggling the Norwegian Krona, but not quite as much as its Swedish counterpart following a wider trade surplus vs broadly in line/benign CPI and CPIF metrics.

EM – Some respite for the Rand as SA retail sales exceed forecast, but little consolation for the Lira due to ongoing Libya angst.

In commodities, WTI and Brent front-month futures traded somewhat lacklustre after the Russian and UAE Energy Ministers dismissed source reports that the OPEC+ is to delay the March 5th/6th meeting to June. WTI Feb’20 futures reside just above the USD 58/bbl mark having dipped below the figure earlier in the session ahead of the 200DMA around USD 57.84/bbl. As a reminder, the OPEC Oil Market Report is to be released at 12:40GMT following yesterday’s EIA STEO which downgraded its 2020 world oil demand growth. Meanwhile, today will also see the weekly EIA crude stocks release after last night’s API figures printed a surprise build of 1.1mln barrels (vs. exp. draw of 500k barrels) which added selling pressure to the complex. Elsewhere, spot gold saw modest gains as APAC traders digested reports that US will not be rolling back existing China tariffs until after the election – with the yellow metal meandering around 1550/oz. Meanwhile, copper prices fell from 8-month highs on the aforementioned tariff reports which potentially dampens demand prospects for the red metal. Finally, Dalian iron ore futures swayed within tight ranges as traders juggled the US tariffs on China with lower port inventories.

US Event Calendar

7am: MBA Mortgage Applications, prior 13.5%

8:30am: PPI Final Demand MoM, est. 0.2%, prior 0.0%; PPI Final Demand YoY, est. 1.3%, prior 1.1%

8:30am: PPI Ex Food and Energy MoM, est. 0.2%, prior -0.2%; PPI Ex Food and Energy YoY, est. 1.3%, prior 1.3%

8:30am: PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.0%; PPI Ex Food, Energy, Trade YoY, prior 1.3%

8:30am: Empire Manufacturing, est. 3.6, prior 3.5

2pm: U.S. Federal Reserve Releases Beige Book

Central Banks

11am: Fed’s Harker Speaks in New York

11am: Fed’ Daly Speaks in San Ramon, CA.

12pm: Fed’s Kaplan Speaks to the Economic Club of New York

2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

The highlight today will likely be the phase one trade deal signing. The closely guarded text still remains a bit of a mystery and as such the devil will be in the detail. All will be revealed later though with a reminder that the signing is expected to take place at the White House at 11.30am EST. It’s said to be an 86 page document but for those of us used to 550 plus page Brexit agreements that were eventually voted down this is a walk in the park. Joking aside the main headline yesterday came after Europe went home as Bloomberg reported (after others had hinted earlier) that existing tariffs on billions of Chinese goods will remain until after the US election to allow the administration to review Chinese compliance before removing them. However, Treasury Secretary Steven Mnuchin said later that China won’t win US tariff relief until the two countries reach a Phase 2 accord and added that there was no link between the timeline for tariff reductions and the November election. So the US will maintain 25% tariffs on $250 billion of Chinese imports and 7.5% on a further $120 billion for now. This news wasn’t a big surprise really but markets lost traction and dipped into the red after the headlines offsetting the small positive momentum post the dovish US CPI and the bumper start to US bank earnings. Elsewhere, the top trade officials of the US, the EU and Japan struck a deal yesterday in Washington to expand the kinds of industrial subsidies prohibited by the WTO.

By the close of play the S&P 500 and NASDAQ ended -0.15% and -0.24% respectively with both pulling back from fresh intra-day all time highs again. This followed the STOXX 600 eking out a small gain of +0.29% before the trade headlines. Elsewhere 10y Treasury yields were -3.5bps lower following a slightly delayed reaction to the CPI report while the 2s10s curve flattened a couple of basis points. The 10y Treasury-Bund spread also broke below 200bps meaning the spread has tightened for five successive sessions. In commodities Gold (-0.09%) continued to edge lower while Brent rose +0.73%.

In an otherwise quiet session it was the big beats for JP Morgan and Citi which grabbed the headlines in the early going. In the case of the former, revenues were ahead of consensus by over $1bn driven by FICC while EPS of $2.57 also smashed expectations for $1.98. Similarly for Citi, strong FICC performance also boosted revenues above consensus to over $18bn while EPS came at $1.90 compared to expectations for $1.83. Elsewhere Wells Fargo did buck the trend somewhat after reporting earnings slightly below consensus. In response, the share prices for JPM and Citi were up +1.17% and +1.56% respectively but with Wells Fargo closing down -5.39%.

Back to trade and Reuters reported overnight that the US Commerce Department has drafted a rule that would allow it to block exports to Huawei specifically if US components make up more than 10% of the product value. Currently, the US can block exports of many high-tech products to China from other countries if US-made parts make up more than 25% of the value. The Commerce department has also drafted another rule that would subject foreign-made goods based on US technology to American oversight. This could be a sign that trade related tension are likely to linger even with a phase one deal signed today.

Asian markets are trading down this morning on the trade and tariff related news mentioned above. The Nikkei (-0.53), Hang Seng (-0.75%), Shanghai Comp (-0.69%), CSI (-0.81%) and Kospi (-0.54%) are all lower. The onshore Chinese yuan is also trading down -0.14% to 6.8936. Elsewhere, futures on the S&P 500 are down -0.24%.

Back to the details of the CPI data yesterday in the US. The core reading of +0.1% (+0.113% unrounded) was below expectations for +0.2% however the annual rate did still hold steady at +2.3% yoy. In the details personal care products had the fourth largest fall in history and lodging away and household furnishings were also significant detractors. On the positive side health insurance prices continued to grow while medical care commodities was a big contributor.

The only other print in the US was the December NFIB small business optimism reading which weakened 2pts to 102.7 (vs. 104.6 expected), albeit within the c.3pt range of the last three months. There was no data of note in Europe yesterday.

Before the day ahead a mention that yesterday Nick and Craig in my credit team published a report looking at current valuations for USD and EUR HY from the perspective of cash prices and analyse what current levels have historically meant for performance going forward. See the link to the full report here.

To the day ahead now, where all eyes will be on the signing of the first phase of the trade deal between the US and China and Washington. As for data, in the US we’re due to get the December PPI report and January Empire manufacturing reading. In Europe the main data of note are December inflation prints in France and the UK as well as November industrial production for the Euro Area. The 2019 GDP reading for Germany is also scheduled. Away from the data we get the Fed’s Beige Book while the Fed’s Daly, Harker and Kaplan are also due to speak. The ECB’s Holzmann and Villeroy, along with the BoE’s Saunders also speak. Finally, Bank of America and Goldman Sachs report earnings.

{kind=link}