Repo Shrinkage Begins In February: That’s When Fed Cuts Each Term Repo By $5 Billion

With everyone (grudgingly or otherwise) now admitting that the Fed’s repo and QE4 was responsible for the miraculous surge in stocks since the start of Q4 2019, traders were especially focused on today’s release of the next monthly schedule of repo operations to see if the Fed would, as Powell hinted, start reducing the liquidity injection via repo. And sure enough, that’s precisely what happened when the NY Fed announced that starting February, the term repo, which had been kept constant at a level of $35 billion since mid-December, would be reduced by $5 billion to $30 billion for every new term repo.

As shown in the latest schedule below, the New York Fed announced that overnight repos would remain at their prior limit of “at least $120 billion”, but it was the term repos where the Fed confirmed that the massive liquidity glut triggered by JPMorgan the Sept repo crisis would finally being to taper, starting with the Feb 4 two-week term repo, which would decline from $35BN to $30BN.

In the aggregate this is a modest drop, reducing overall liquidity by just $20 BN over the month of February as existing repos roll into smaller operations, but assuming there are no incidents, one assumes that in March (and then April, and May), the shrinkage will continue apace, with the total amount declining by a similar or greater amount.

Of course, on net the total liquidity will actually increase as in February the Fed will inject at least $60BN in liquidity via T-Bill monetizations courtsy of “NOT QE 4”, and then another $60BN in March, then April and so on. In other words, while there Fed confirmed a modest repo shrinkage starting in two weeks, this will be more than offset by permanent open market operations which will see the Fed continuing to grow its balance sheet, in the words of UBS, “indefinitely.”

Yes, It’s Possible: This Is How China Can Boost US Imports By $200 Billion

Almost one month ago we showed in one chart why the core concession in the Phase One trade deal by China – namely the promise for a “best effort” to purchase $40 billion in agricultural products from the US – appeared impossible. In short, assuming a similar export mix as in 2017, this would translate into an unprecedented 235% volumetric increase in 2020 US agricultural exports to China over 2019. The problem is that while US exports to China had declined sharply in 2018, other nations stepped in, in many cases with long-term bilateral contracts in place ensuring the long-term delivery of ag products from mostly Latin American substitute markets. This, as Goldman points out, means that such an increase in Chinese purchases from the US “would likely be hugely disruptive to global agriculture markets, primarily crowding out Argentine and Brazilian supplies that have taken substantial market share since 2017 due to the trade war and much weaker currencies.“

Fast forward to today when Reuters writes that commodity traders and analysts are similarly struggling to map out how China will reach the “eye-popping” amounts it is committing to buy from the United States under Phase 1 of their trade deal.

As we reported previously, China has pledged to buy $50 billion more in U.S. energy supplies, and will raise US agriculture purchases by some $32 billion over two years above 2017’s $24 billion baseline, according to a source briefed on the deal to be signed on Wednesday. The deal also stipulates purchases of an additional $80 billion in manufactured goods, although details still remain scarce. Overall, it was reported that, as a part of the deal, China will buy $200bn more US goods and services than 2017 cumulatively over the next two years.

Those totals would certainly trim the roughly $300 billion annual trade gap between the countries. However, analysts who study Chinese commodity flows remain skeptical that Beijing can absorb such quantities of U.S. goods without threatening trade ties with other suppliers, hurting its own domestic producers, and making substantial changes to import standards and quotas.

“Either China massively increases imports and reduces current account surplus from the current 1.5% of GDP, or it engages in trade diversion away from current providers of goods which compete with the U.S.” said Alicia Garcia Herrero, Chief Economist Asia Pacific at Natixis in Hong Kong. “I see this second scenario as much more likely.”

According to Chinese trade sources and analysts, China will have to include U.S. crude, liquefied natural gas (LNG) shipments and imports of petrochemical raw materials such as ethane and liquefied petroleum gas (LPG) to meet the target. But it would still struggle unless new supply deals are signed that displace other exporters.

The $50 billion target is “too aggressive and unlikely to achieve”, said Seng Yick Tee, an analyst at SIA Energy in Beijing, adding that energy product exports from the United States to China were about $8 billion in 2017 and 2018. “To achieve $25 billion a year, all the imports need to be tripled.”

Gavin Thompson, Vice Chair for Asia Pacific at Wood Mackenzie, was surprised by the energy figure since it would mean tariffs on U.S. crude and LNG imports would have to be removed, particularly for LNG to be competitive. Quality, rather than quantity, may be another hurdle.

“Most of the Chinese refineries were designed to process medium-sour crude, but U.S. oil is mostly light, sweet,” SIA’s Tee said, referring to the density and the sulfur amounts in crude, which dictate the types of fuels that can be refined from an oil.

But it’s China’s agricultural pledge that most found laughable: the pledge to boost U.S. farm imports by over $30 billion over two years is “shocking” since that increment is more than the value of farm products it has purchased from the U.S. in a single year, said a China-based grains trader quoted by Reuters. “It would make (more) sense if the $32 billion is the total number, not the increased number.”

Such a large fixed dollar-figure from one producer would also risk supply disruptions and distort international crop prices, said Iris Pang, Greater China economist at ING in Hong Kong. “Prices of agri (commodities) from the rest of the world could be cheaper, especially after China cut import tariffs (in January). So even after retaliatory tariffs are removed, the U.S. will not have a competitive advantage over other economies,” she said.

Traders also questioned what products China could buy from the United States since African swine fever has dented demand for soybeans for animal feed and quotas to protect domestic farmers limit grain imports. “China will, for sure, buy more soybeans, let’s say, 30 to 40 million tonnes. (For) wheat, maybe we can increase purchases within the import quota,” said a trader with a Chinese grain importer. A third grains trader said: “If such volume (of products) come to China, it will be a disaster for us (in the domestic market).”

* * *

Not everyone is a cynical skeptic, however.

Goldman Sachs has emerged as a believer that what China has promised can actually be done, and in a note published over the weekend writes that “given the size of the total Chinese imports and US exports, there should be sufficient room in theory for China to increase its purchases from the US by $200bn. However, doing so within two years would likely require policy assistance such as lower tariffs and more SOE buying under administrative measures. Commodities and commodity-like goods that are fungible and easy to substitute from one supplier to another probably will feature prominently in the list.”

A quick look at the math: Chinese policymakers have agreed to increase imports from the US by $200bn cumulatively over the next two years relative to the 2017 levels. To put this number in context, an additional $100bn per year would account for 70bp of China’s 2018 nominal GDP and would imply a doubling of China’s 2019 imports of US goods. Which is why many investors have asked Goldman (and everyone else) whether such a large amount of purchases in such a short period of time is achievable, what China is most likely to buy, and what the implications are for the economy and markets.

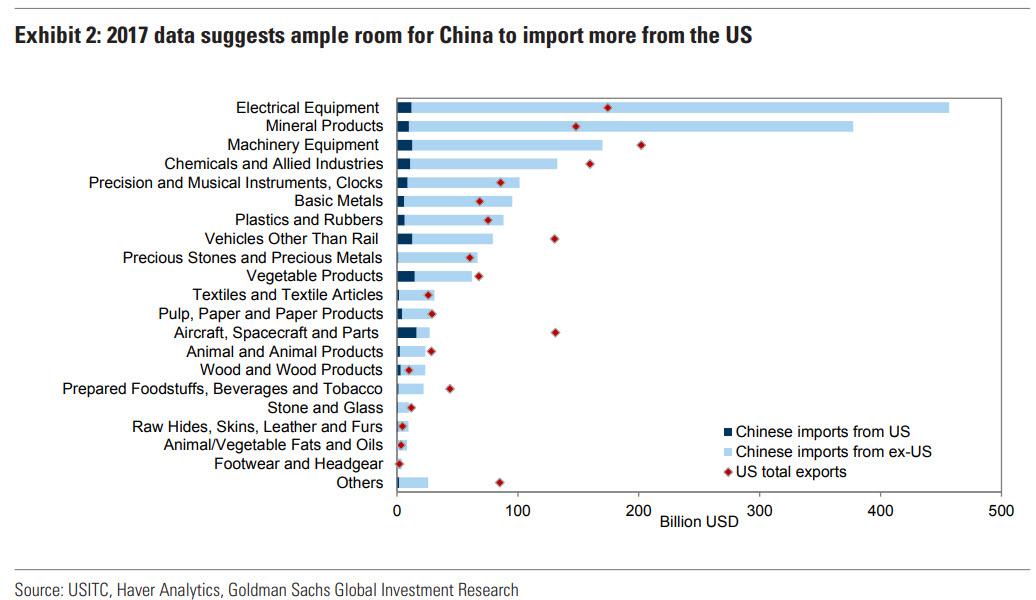

Annual Chinese total imports and US total exports each exceed $2tn, so increasing the bilateral trade flows by $200bn over the next two years, looks theoretically achievable. However, doing so will not be easy without policy support,due to the lack of economic competitiveness. In Exhibit 1, assuming China is going to buy an additional $200bn of US goods and services in 2020-21, Goldman constructs a potential scenario of how this may be achieved based on product fungibility and hard constraints in major markets.

As Goldman’s analysis suggests, much of the additional purchases would result in trade diversion of commodities and commodity-like goods. However, such re-directing of trade flows, even for the most homogeneous commodities, may not happen instantaneously. Moreover, hard physical constraints such as the sharp decline in US soybean production and the grounding of Boeing’s 737MAX will likely make the purchase ramp-up especially difficult in 2020 compared to 2021.

The parameters of the deal

While not much detail is known – one day before the official signing – a few key parameters have been reported by multiple news outlets. As a part of the Phase 1 deal, China has reportedly agreed to buy $200bn more in US goods and services over two years, focusing on manufacturing, energy, agriculture and services. In particular, per the press reports, US officials have emphasized that at least $40bn of American farm products will be bought per year, and China will make “best efforts” to increase its purchases by another $5bn annually, adding up to the $40-50bn number that President Trump announced on October 11. Wheat, corn and rice are the specific agricultural products mentioned. According to the US Trade Representative Robert Lighthizer, there would be specific targets for Chinese purchases of specific products, but those would not be made public to avoid distorting markets

Based on aggregate numbers alone, there appears to be ample room for Chinese imports from the US to double. For example, the US exported $2.4tn goods and services in 2017 and only 8% went to China ($186bn). Similarly, China imported $2.2tn goods and services in 2017 and only 8% came from the US. Of course, there do exist notable mismatches between what China demands and what the US supplies. For example, China imports $75bn iron ore annually but the total US exports are less than $1bn per year. However, even after taking into account such supply and demand mismatches which impose physical constraints to how much China can buy from the US, the headroom seems wide enough for China to fulfill the $200bn list (Exhibit 2).

A more detailed list of what China may buy

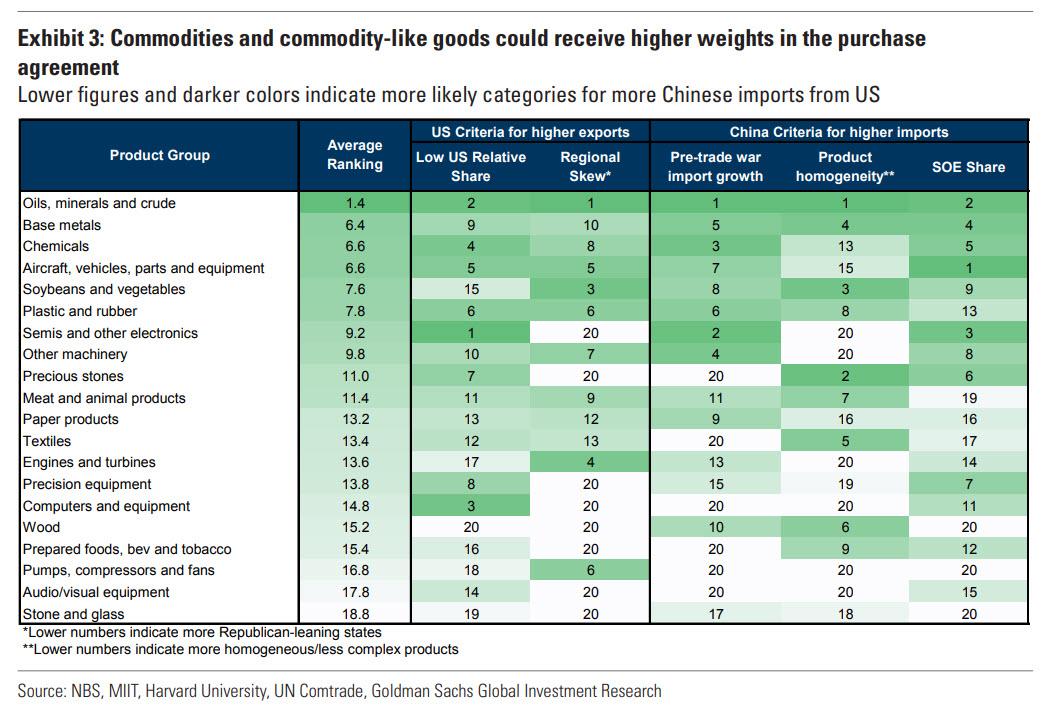

Commodities are most easily diverted in trade flows due to product homogeneity, effectively muting the impact of tariffs on the real economy. In addition to product homogeneity, we have also looked at factors such as regional skew on the US side (e.g., goods produced in Republican-/Democrat-leaning states may receive different weights in the trade deal) and SOE share on the China side (e.g., a higher SOE concentration makes it easier to implement trade policies) to assess which products could feature prominently in the purchase list. Based on an average rank across five factors, Exhibit 3 shows that commodities and commodity-like goods such as chemicals, aircraft, plastics and semiconductors stand at the top of the list.

What about Services

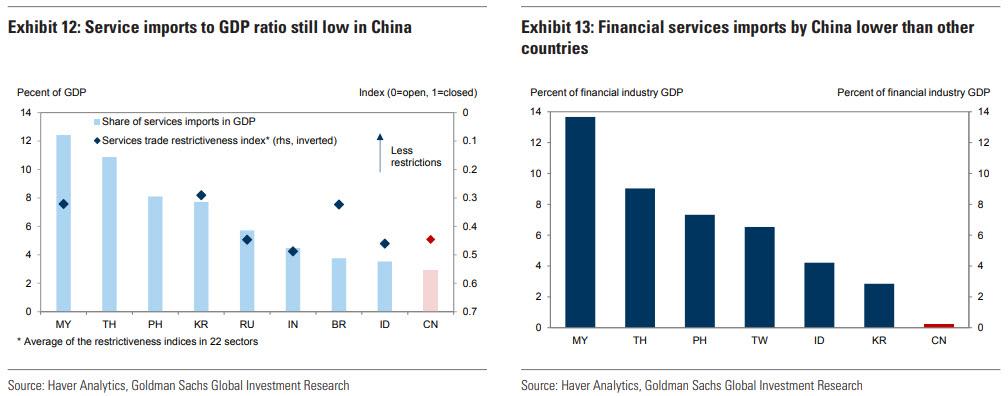

After adjusting for capital outflows disguised as travel spending in the Chinese balance of payment data, China imported $363bn in services in 2017. US data shows that service exports to China totaled $56bn in 2017, with travel services constituting the largest share (59%) followed by charges for use of intellectual property (11%), financial services (6%) and other business services (6%). Compared to other developing countries, service imports by China are still low relative to its GDP (Exhibit 12). We calculate that, if the service imports to GDP ratio in China (2.9%) were to increase to Indonesia’s level (3.5%), Chinese service imports would increase by $30bn. The OECD Services Trade Restrictiveness Index, which summarizes information on regulations affecting trade in services, shows that there is indeed room for the Chinese government to lessen service trade restrictions. Imports of financial services, for example, are significantly lower in China than in other countries when compared to the size of the country’s financial industry (Exhibit 13). More recently, discussions about financial opening have been gathering steam in China. But this is likely to be a gradual process. Overall, we think it is feasible for total Chinese imports of US services to increase $15bn in 2020 and $30bn in 2021.

If US Wins, who Loses?

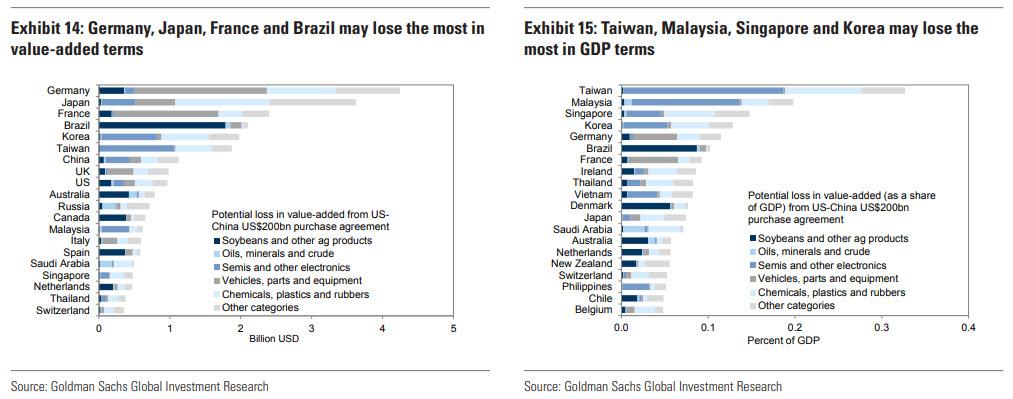

As for China’s other trading partners, Goldman applies the same methodology used in its previous research to estimate the GDP impact by combining the type of goods China may buy from the US, the likelihood and patterns of trade diversion, and the world input-output table. Exhibits 14 and 15 show that the effects would be mostly moderate, with Germany, Japan, France and Brazil estimated to experience the largest negative impact in value-added terms and Taiwan, Malaysia, Singapore and Korea in GDP terms.

Market Implications

There are two key potential market implications. First, given the unfavorable economics of raising imports from the US significantly and quickly, the Chinese government may want to keep CNY on the stronger side relative to USD to maintain its purchasing power. Second, there may be price divergence between US and ex-US prices to incentivize diversion of trade flows. Possible examples include US outperforming Brazil soybean price and WTI outperforming Brent crude oil price.

In parting, some caveats.

First, it is worth emphasizing that significant uncertainties remain on the parameters of the purchase agreement. For example, it is unclear whether multi-year contracts can be counted as a part of the $200bn package even when they do not lead to actual trade flows in 2020 and 2021. In the case of LNG, there are several large LNG projects where Chinese companies could potentially sign long-term contracts with the US. Assuming a combined volume of 50mtpa – not too aggressive an assumption based on China’s demand trajectory, the value could be $20bn per year, or $200bn for 10 years. But the actual delivery is unlikely to begin before 2023.

Second, the evaluation of GDP impact on China’s trading partners as shown above is solely based on economic factors such as similarity to the goods exported by the US and the ease of trade diversion. It leaves out political considerations which could be important in practice. For example, China’s state-run newspaper has been quoted saying that “entities from countries which are friendly to China will be favored by the Chinese people” when asked about foreign institutions who might benefit from China’s financial opening. Such political factors could affect the eventual trade outcomes above and beyond a US-China purchase agreement.

Warren, Van Hollen Ask SEC To Investigate Insider Trading By Mar-A-Lago Guests Before Soleimani Airstrike

Presidential contender Sen. Elizabeth Warren and Sen. Chris Van Hollen co-wrote a letter on Monday to the Securities and Exchange Commission (SEC) requesting an “investigation into whether there may have been any illegal trading in defense company stocks or commodities related to individuals’ advance knowledge of the United States attack on January 2, 2020, that killed Iranian Major General Qasem Soleimani.”

Warren, Van Hollen ask SEC and CFTC to investigate possible insider trading by Mar-a-Lago members reportedly given advance notice on Iran action.

Letter references rise in $NOC, $LMT, $RTN shares and the price of crude oil after strike.

The letter alleges that President Trump told guests at the Mar-A-Lago resort that military action was pending in the Middle East.

The senators pulled a quote from a story that was featured on the left-leaning Daily Beast that detailed how three unnamed sources at the resort heard President Trump talking to guests about an upcoming military operation:

“In the five days prior to launching a strike that killed Iran’s most important military leader, Donald Trump roamed the halls of Mar-a-Lago, his private resort in Florida, and started dropping hints to close associates and club-goers that something huge was coming … Trump began telling friends and allies hanging at his perennial vacation getaway that he was working on a ~big’ response to the Iranian regime that they would be hearing or reading about very •soon.’ [T]he president specifically mentioned he’d been in close contact with his top national security and military advisers on gaming out options for an aggressive action that could quickly materialize.”

The letter went onto say that “guests at President Trump’s resort may have obtained confidential market-moving information and had the opportunity to trade defense industry stocks or commodities or make other trades based on this information.”

It also said, “Between January 2, 2020, before the announcement of the attack, and the end of the day on January 3, 2020, Northrop Grumman stock prices increased by over 5%; Lockheed Martin’s stock prices increased by 3.6%… Additionally, immediately following the killing of Soleimani, the price of crude oil increased by over 4%.”

However, as the charts below show, defense stocks were actually down ahead of the attack on the embassy, which triggered the first push higher, and then surged on Soleimani’s death headlines…

We’ve noted in the past how left-leaning news organizations have played politics and tried to suggest President Trump and his associates were front-running equity futures, commodities, and or stocks ahead of trade headlines.

The Chicago Mercantile Exchange (CME) called the infamous Vanity Fair piece titled – “The Fantastically Profitable Mystery of the Trump Chaos Trades” – a “fantastical” story:

“CME Group regularly monitors its markets for suspicious activity.

As it relates to the Vanity Fair article published on October 17, 2019, regarding activities in the E-mini S&P 500 futures contract, the allegations about the trading activity are patently false.

These transactions were entered into by a significant number of diverse market participants.”

And at the time the Vanity Fair piece was released, we did not run a comment on the article because of our initial skepticism of the reporting, and as Bloomberg reported, experts who examined the story said any implication that people traded on inside information fell short of being proven.

Contrary to popular opinion, I think a loss of faith in Washington D.C. and its institutions is entirely rational and healthy. Maintaining faith in something due to tradition or the fumes of hope won’t lead to anything productive, rather, it’s preferable to honestly assess the reality of whatever situation you’re in and reorient your worldview and priorities accordingly.

Whether the issue relates to above the law criminal bankers, a Federal Reserve which systematically funnels free money to the already wealthy and powerful, the societal dominance of free speech and privacy-despising tech giant monopolies, or the national security state’s undeclared forever wars for empire, there’s no good reason to maintain any faith in the federal government and the oligarchs/special interests who control it.

Philosophically speaking, I’ve come to conclude the only way to truly have self-government where community life reflects the desires and needs of the people who live there is by concentrating decision making at the local level. I’ve become increasingly interested in the general idea of localism not just because I agree with it in theory, but because it seems more and more people will begin to gravitate toward this perspective and life strategy out of necessity and frustration.

Fed Considering Lending Cash Directly To Hedge Funds In Next Repo Market Crisis

At the beginning of December, the Bank of International Settlements, presented a formerly unknown explanation for the September repocalypse, one which in addition to a sharp drop in liquidity by the “Top 4” banks, was amplified by an imbalance in demand for repo by hedge funds: “High demand for secured (repo) funding from non-financial institutions, such as hedge funds heavily engaged in leveraging up relative value trades,” was a key factor behind the chaos, said Claudio Borio, head of the monetary and economic department at the BIS.

The BIS’s finding was novel, and surprising, as it highlighted the “growing clout of hedge funds in the repo market” which in retrospect is to be expected: as we noted over a year ago, hedge funds such as Millennium, Citadel and Point 72 are not only active in the repo market, they are also the most heavily leveraged multi-strat funds in the world, taking something like $20-$30 billion in net AUM and levering it up to $200 billion. They achieve said leverage using repo.

In short, and as shown in the chart above, some of the world’s biggest hedge funds are active in the repo market to boost their returns. The problem is what happens when repo rates get unhinged as happened on September 16: for the best example of how market players react when their underlying correlations go tilt, look no further than what happened to LTCM in 1998.

This also explains why the Fed panicked in response to the GC repo rate blowing out to 10% on Sept 16, and instantly implemented repos as well as rushed to launch QE 4: not only was Fed Chair Powell facing an LTCM like situation, but because the repo-funded arb was (ab)used by most multi-strat funds, the Federal Reserve was suddenly facing a constellation of multiple LTCM blow-ups that could have started an avalanche that would have resulted in trillions of assets being forcefully liquidated as a tsunami of margin calls hit the hedge funds world.

So with hedge funds now emerging as the weakest market transmission link in any future repo market flare up, the Fed has to act, and sure enough, as the WSJ reports, in order to minimize risk during any and all upcoming repo market crises, Fed officials are considering a new tool to ease repo market stress: namely bypassing the existing system entirely, and lending cash directly to smaller banks, securities dealers and hedge funds through the repo market’s clearinghouse, the Fixed Income Clearing Corp., or FICC.

How is this different from the current system?

Well, as the BIS explained last month, hedge funds currently borrow through a process called sponsored repo, in which a large bank effectively act as a middleman or guarantor, pairing their government bonds with money-market funds willing to lend cash. The bank then guarantees that the parties will fulfill their obligations—repaying the cash or returning the securities. In the new proposal, firms trading through the FICC, would contribute to a fund that would cover a borrower’s default. However, as the WSJ notes, critics of the new plan say if the Fed lends cash directly through the clearinghouse, it could end up contributing to a hedge-fund bailout.

Which, of course is moot: when the Fed stepped in to launch repos for the first time since the crisis in September, followed by QE4 in October, bailing out hedge funds (in addition to banks, and prop desks, such as JPMorgan’s) is precisely what it did then goo. It is also hardly surprising that following the massive liquidity injection in October that continues to this day, that stocks have soared in what is virtually a straight line.

Yet while the former regime is so convolulted only a few individuals, and the BIS, get it, the new approach makes the Fed’s backstop of hedge funds far more explicit, and could also political problems for policy makers. The problem, as the WSJ notes, “centers on the central bank lending directly to hedge funds”, which already only cater to ultra high net worth clients.

Are they really the ones that so desperately need a bailout when the next crisis hits?

It doesn’y really matter because hedge fund leverage is now so intertwined with the repo market, any bailout of the banks or the financial system, also explicitly bails out hedge funds, even though “some fear that lending directly to hedge funds could lead to the perception the Fed is fueling risky bets.”

“There’s a strong aversion to fat cat bailouts,” said Glenn Havlicek, chief executive of GLMX, which provides technology to repo trading desks. Actually, Glenn, that’s news to us: the Fed did just such a bailout in September, and nobody said or thing, or noticed. Perhaps because the pathway that leads from repo to markets to hedge funds is so complex that nobody actually gets it.

Furthermore, as the WSJ notes, many, if not a vast majority, of hedge funds trade in the cash market through sponsored repos. The clearinghouse sits between buyers and sellers to ensure that neither party backs out of the transaction. Records of cleared trades also are publicly available, improving the market’s transparency.

The idea of using the clearinghouse appeals to some investors and analysts because the Fed has had trouble getting cash into the hands of the smaller banks, securities dealers and investors who need it the most. That is because the Fed trades exclusively with a small group of large banks and securities firms, known as primary dealers. Even among these firms, activity is tightly concentrated. A study recently published by the Bank for International Settlements said that liquidity in the repo market rests in the hands of the four largest banks in the U.S. system.

Incidentally, clearinghouses are also what Horseman’s Russell Clark believes will be the weakest link during the next crisis, and is how the market crash will spread (as we discussed last month). It may also explain why the Fed is quietly tiptoeing to directly backstopping clearinghouses, as it realizes that while it may backstop every bank, unless it can also save the linkages between them, the system is still in trouble.

Of course, if hedge funds at least used the repo funding for some noble, original purposes, that could at least put some favorable spin on this debate. Alas, hedge funds mostly use the borrowed repo funds just to boost leverage and increase potential gains from investments, as shown in the top chart. Of course, such leverage can also magnify losses. And while policy makers typically haven’t encouraged the use of levered investment strategies, the wide availability of repo has made it the preferred means for hedge funds to leverage up as much as 10x.

Finally, as the WSJ correctly notes, some investors say the connections between firms involved with sponsored repos make the distinction between lending to one or the other meaningless. Gang Hu, a hedge-fund manager at WinShore Capital Partners, said he borrows cash in the repo market to increase the impact of his investments in Treasury-bond futures and other interest-rate products.

“They are reluctant to provide a tool that would allow” overall leverage to increase beyond current levels, Mr. Hu said. “The system cannot work without leverage, but a system with too much leverage is unstable.”

And since we are now deep inside the “too much leverage” phase, the only option for the Fed is to quietly come in and backstop every repo market player, including the billionaires that get richer by the year simply be levering up on the Fed’s ongoing liquidity injections in the stock market.

The day Speaker Nancy Pelosi announced she would open up impeachment proceedings against President Trump I called it a coup. It was obvious to me then and more obvious to me today that we are headed to a dangerous place (a dangerous place).

Trump’s impeachment trial in the Senate begins next week and it’s clear that this will not be a walk in the park for the President. Anyone dismissing this because the Republicans hold the Senate simply do not understand why this impeachment exists in the first place.

It is the ultimate form of leverage over a President whose desire to end the wars in the Middle East is anathema to the entrenched powers in the D.C. Swamp.

The Democrats would not be pushing for this if they didn’t think they have the votes in the House and the Senate to get this done. Ignore the conventional wisdom on this. They were wrong in the UK.[about the courts upholding Johnson proroguing Parliament]

They will be wrong here, unless Trump has something else up his sleeve.

His removing John Bolton and refusal to attack Iran is driving the neoconservatives to apoplexy. They want their holy war against the apostate Shi’ites and they will get it. Mike Pence will be their avatar until such time as he can be removed through a sham election in 2020.

If this wasn’t the case they wouldn’t be risking what’s left of their political future defending a senile old man, Joe Biden, who they don’t actually want to be the candidate anyway.

It’s a coup folks.

Take this one step farther. You don’t start this process if you aren’t going to use what it gives you. Thinking only in terms of the Democrats’ horrific slate of challengers to Trump betrays the myopia of most political analysts.

They see things, wrongly, in terms of partisanship. This isn’t primarily about Democrat v. Republican. This isn’t even just about Clinton v. Trump and a temper tantrum.

Many believe that by the Senate giving credence to a trial based on the no evidence, no crime, read the transcripts, “no pressure” Impeachment Hoax, rather than an outright dismissal, it gives the partisan Democrat Witch Hunt credibility that it otherwise does not have. I agree!

And you have to ask yourself the question why would Senate Majority Leader Mitch McConnell go along with a real trial unless the fix was in?

Because, as Trump rightly points out, he’s got the approval rating nationally and within his own party. He’s a lock for re-election. So, given the clear unconstitutionality of these impeachment articles (which I discussed previously) why is this even still a thing?

Because Trump is going to be taken out.

The events of the past twelve days since Trump murdered IRGC General Qassem Soleimani prove this beyond any doubt. Impeachment was the leverage point to drive open a wedge between Republicans and Trump through Iran.

Pelosi slow-walking the articles of impeachment to the Senate was all part of the pantomime, folks. She gets what she wants: Congress asserting more power and the Democrats shoring up their base by taking out an eyesore in Trump.

She waits just long enough for Trump to do something questionable and for it to be made known publicly.

The neocons in the Senate get what they want — further escalation of pressure on Iran with the hope of destroying them. Moreover, they prove to Trump, Israel, the MIC and the world that they are still fully in charge of U.S. foreign policy.

The Swamp Strikes Back and puts Trump in a no-win situation.

The Wall St. Journal article from this weekend which intimated that Trump made the decision to kill Soleimani was motivated by shoring up his support in the Israeli Occupied Senate is further proof.

“Mr. Trump, after the strike, told associates he was under pressure to deal with Gen. Soleimani from GOP senators he views as important supporters in his coming impeachment trial in the Senate, associates said,” the newspaper reported.

It’s not like Trump hasn’t let missiles fly to appease the Neocons in the past. He did it with the bombing of the Al Shairat airbase in Syria back in April of 2017. Remember, that was the night the MSM and Congress declared Trump suitably “Presidential.”

Now Pelosi wants to add more charges to the docket and McConnell is going for a trial, when he should just outright dismiss these charges. I told you that this all comes down to McConnell and how he handles the terms of the trial.

He sets the table for this. And if he’s not tilting it in Trump’s favor, Donald is right to be worried.

Trump’s killing Soleimani gives them plenty of cover to do so. His lack of consistency in defending the act will be used against him. That’s why Esper told the world Trump didn’t have proof of an imminent threat.

So, Trump, often his own worst enemy, then defends himself by saying Soleimani just needed killin’.

The Fake News Media and their Democrat Partners are working hard to determine whether or not the future attack by terrorist Soleimani was “imminent” or not, & was my team in agreement. The answer to both is a strong YES., but it doesn’t really matter because of his horrible past!

It’s all being stage-managed by a nearly rogue Secretary of State Mike Pompeo and facilitated through Lindsey Graham. The events that led up to Iran’s missile attack on our bases in Iraq should not be taken at face value.

Killing one U.S. oil contractor does not justify attacks on five PMU bases ringing the Iraqi/Syrian border crossing between Al Qaim and Al Bukamai.

It certainly doesn’t necessitate taking the conflict all the way to the point of Iran firing missiles at our airbases in Iraq.

Don’t think for a second that if Graham feels Trump isn’t sufficiently controlled at this point that he won’t, in the end, wring his hands and vote for his removal from office because the President’s decision-making skills are questionable.

If the Swamp truly wants Trump removed from office then this impeachment trial is their best chance of getting that done. At this point we have a handful of open Republican turncoats. Swelling that number to twenty in the Senate is not that hard.

Remember, twenty is a helluva lot smaller than the millions of voters that would have to turn against Trump to elect Hillary Clinton waiting in the wings to emerge from a brokered Democratic convention this summer.

That’s what’s fundamentally wrong with representative forms of government.

And even then, Pence v. Clinton would be a close affair because of the deep divisions within the electorate and Hillary’s fundamental evil. Either way, the Swamp wins.

Nothing happens in D.C. that doesn’t become a weapon in these people’s hands.

To think Pelosi wouldn’t use this to its fullest is terminally naive. To think Trump is savvy enough to see the game board in all its complexity having not one truly loyal staff (or family) member is also naive.

To think McConnell is anything more than an order-taker from those above him is the height of naivete.

I give Trump credit for navigating things to this point and keeping the violence to a minimum, but if he’s going to go down, he better be prepared to go scorched earth in the process.

It’s his only chance at survival and fulfilling even one of his many campaign promises.

Either way, the U.S. electorate will not stand for removing Trump over this. And they shouldn’t. I may be angry with Trump for his recent actions, but this impeachment is the height of lunacy. And when something this ludicrous goes this far, it means the fix is in.

The Flying Monkeys have taken over the asylum. The existence of this trial is itself an inflection point in history.

The rest is just a chase scene.

* * *

Join my Patreon if you support honest analysis of world events and their effect on capital markets Install the Brave Browser to begin clawing back our right to speak freely about them

Kerri Hand became a chicken owner for the eggs, but then she fell in love. A retired cop who lives in rural southern California, Hand and her children came to view their flock as part of the family.

In late 2018, Hand returned home to find a notice stuck on her door from the California Department of Food and Agriculture stating that there was an outbreak of a highly deadly avian virus in her neighborhood, which can wipe out massive flocks. State and federal health officials had ordered all birds across several counties under immediate quarantine, including Hand’s.

To date, officials have searched thousands of homes and farms and identified just under 500 infections. After determining that quarantine wasn’t enough, they ordered the mandatory euthanasia of over 1.2 million birds in high-risk areas surrounding the infections, including healthy birds. The euthanasia campaign may be necessary to prevent the spread of the Newcastle disease, but according to the bird owners who spoke with Reason, health officials have carried out their duties in a cruel manner, leaving bird-owning families with lasting emotional scars.

Hand complied with the state’s quarantine orders for months, and paid to have her birds tested by a veterinarian—tests that came back negative for Virulent Newcastle Disease. But as she and her family were preparing to celebrate Good Friday, a team of police and state workers dressed in biohazard suits unexpectedly arrived at her house, with a search warrant and an order to kill her family’s flock. Hand’s children watched their pets die.

Workers kill birds by breaking their necks, shooting them with firearms, or suffocating them with CO2 gas—methods that officials maintain are humane. But Hand disagrees. She recalls that workers placed her birds in a trash can with no viewing window, forcing them to lift the lid to check if the birds had died. Each time, oxygen leaked in, prolonging the process.

Hand recorded and shared live video of the slaughter in a Facebook group she created called Save Our Birds, and it went viral. The group gained thousands of members, and Hand began organizing volunteers to show up at kills and film on their phones. She alleges they’ve documented scores of abuses by state workers and police.

Produced, written, shot, and edited by Justin Monticello

Camera by John Osterhoudt

Music: “White Hats” by Wayne Jones; “I’ve Just Had an Apostrophe!” by Spazz Cardigan; “Butchers” by Silent Partner; “Versace Beat” by Yung Logos; “Gaia in Fog” by Dan Bodan; “Grasshopper” by Quincas Moreira; “Pinckney” by The 126ers

from Latest – Reason.com https://ift.tt/2RjZ4qK

via IFTTT

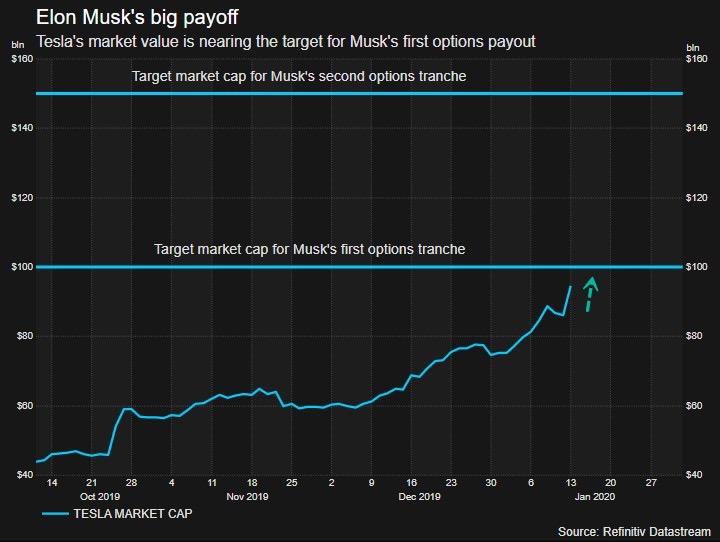

Tesla shares on Tuesday morning were trading around $542 – or about +150% from the levels when the Federal Reserve’s ‘Not QE’ started the dash-for-trash and provided liquidity to hedge funds to bid up stocks.

Tesla has been a significant beneficiary of the Fed’s money-printing as it resulted in a monstrous squeeze that allowed Elon Musk to wage nuclear war on short sellers.

At the same time, Musk has come close to a whopping $346 million payday, in the form of equity options, if Tesla shares sustain a $100 billion valuation, or $554.80 per share, for a one-month and six-month average, according to Reuters.

Musk is nearing his first big payday:

We noted in early 2018 that Musk agreed to remain at the helm of Tesla for at least another 10 years. And in exchange for this commitment, the company’s board granted him 12 tranches of options to buy Tesla stock.

Musk currently owns 34 million Tesla shares, or about 19% of the company. His compensation package would allow him to purchase another 20.3 million shares if all options were vested.

When Tesla first unveiled Musk’s package in early 2018, it said Musk could make at least $56 billion if all milestones were reached.

The combination of Fed’s liquidity and a massive short squeeze has propelled Tesla’s stock to achieve a valuation higher than Ford and General Motors combined and could eclipse VW’s market cap (as the largest global automaker) if higher highs are seen.

In recent weeks, Tesla has had some good news of expansion in China. Still, in a period when the Fed and other major central banks are printing trillions of dollars and cutting rates at the fastest speed since the last recession, valuations and fundamentals don’t matter – it’s all about central bank liquidity.

Bloomberg reports that existing tariffs on billions of dollars of Chinese goods coming into the U.S. are likely to stay in place until after the American presidential election, and any move to reduce them will hinge on Beijing’s compliance with the terms of a phase-one trade accord, people familiar with the matter said.

The two sides have an understanding that no sooner than 10 months after the signing of the agreement at the White House Wednesday, the U.S. will review progress and potentially trim tariffs now in place on $360 billion of imports from China, the people said, declining to be identified because the matter is private.

And the reaction was instant… Dow dumped back below 29k…

And yuan weakened significantly…

Source: Bloomberg

Hogs and cotton futures prices also slipped on the headline.

As a reminder, only the then-imminent September tariffs were actually removed (before they hit) in the phase one deal, so this should not be a total shock. However, it appears the assumption was that the rest of the tariffs would be lifted sooner rather than later.

In the run-up to tonight’s Democratic presidential debate in Iowa, the last such contest before primary voting begins, one of the big storylines is about who won’t be among the half-dozen candidates on stage.

“This debate is so white, it’s not allowed to bring the potato salad,” crackedMediaite‘s Tommy Christopher. “The smallest, whitest one yet,” concurred Politico.

With Sen. Cory Booker (D–N.J.) exiting the race Monday, and both Andrew Yang and Rep. Tulsi Gabbard (D–Hawaii) failing to meet the qualification thresholds, the resulting lineup is not just pale, it’s ancient—the three highest-polling of the six debaters would each be the oldest president ever sworn into office. A fourth, Tom Steyer, is a hedge fund billionaire who literally bought his way to the podium, after an entire season in which Democrats debated whether billionaires should even exist. (An even older white billionaire, Michael Bloomberg, currently sits fifth in national polls, but is not bothering with early primary/caucus states.)

So you can see why the younger, more progressive voices who punch above their weight in Democratic political discourse would be dismayed. “Bad for democracy,” pronouncedSalon‘s David Daley. “The system they have designed has suppressed the most loyal base of the Democratic Party,” charged Color of Change Executive Director Rashad Robinson in The Washington Post. “Anyone with an understanding of civil rights law understands how the rules can be set up to benefit some communities. The Democratic Party should look at the impact of these rules and question the results.”

That is certainly one theory. But I would suggest at least considering another. Cory Booker was one of five Gen X candidates (only one white male among them) who came into the race with ideologically mixed pedigrees—including not a small amount of what progressives would deride as “neoliberal” policy positions on deficits, trade, and education—but then competed with varying levels of believability on being the most woke, before eventually collapsing.

First Sen. Kirsten Gillibrand (D–N.Y.), then Beto O’Rourke, Sen. Kamala Harris (D–Calif.), Julián Castro, and now Booker all made the affirmative choice to either tack heavily left on economics or just downplay their past heresies in favor of talking up issues such as slavery reparations, Medicare for all illegal immigrants, and the racism/sexism of President Donald Trump. The abject failure of this approach is one of the greater under-explored storylines of the 2020 presidential nominating season.

Eleven months ago, this group accounted for about one-quarter of voter support in national polls: Around 12 percent for Harris, 6 percent for O’Rourke, 5 percent for Booker, and 1 percent each for Castro and Gillibrand. Sen. Elizabeth Warren (D–Mass.), who would eventually vault herself up to near-frontrunner status, was then just a face in this crowd: 7 percent. Democrats were making similar murmurs of pride about their energetic and historically diverse field that you heard among Republicans in the first half of 2015.

What happened next? While Warren went on a white-paper spree of policy “plans” for every economic and regulatory issue under the sun, the Gen X Five engaged in more identity-politics emoting than a campus struggle session, only with less sincerity. O’Rourke agonized publicly about his ancestors owning slaves. Harris the cop tried gruesomely to rebrand herself as a hip Jamaican pot smoker. Gillibrand spent valuable debate-stage time talking about the need to educate people about her white privilege. Booker pushed for reparations and policed Joe Biden’s language, while Castro was busy shaking his damn head that all these leftward lurches didn’t go nearly left enough.

The late-night comedy skits wrote themselves. And by August, Warren was out-polling all five whippersnappers combined.

It’s not that the more successful septuagenarian progressives shied away from calling Trump a racist—far from it. But voters did not have to guess about what got the northeastern senators up early every morning: It’s the economic policy, stupid. What, exactly, was Kirsten Gillibrand’s selling proposition? Why were O’Rourke and Booker (at least until the last of the latter‘s debates) running away from much of the stuff that made them interesting in the first place?

What makes their choice that much more curious is the persistent math of this race: The progressive bloc in the 2020 Democratic field has persistently lagged the centrists by about 10 percentage points. The RealClearPolitics running national averages for Biden (27.4 percent), Pete Buttigieg (7.8 percent) and Bloomberg (6.2), and Sen. Amy Klobuchar (3.0) (D–Minn.) combine for 44.4 percent; Sanders (18.8 percent) + Warren (16.8) + Steyer (2.2) = 37.8. Instead of using their ideological dexterity to compete against a very old-looking frontrunner for the scared-of-socialists vote, the Gen Xers chased whatever progressive crumbs hadn’t already been hoovered by two strong candidates.

The great irony of this blown strategy playing out even today is that Elizabeth Warren, after benefiting directly from her competitors’ stumbles, seems to be making the exact same tactical mistake. By leaking a private conversation with Sanders in a not-particularly-convincing attempt to make him look possibly sexist, Warren’s campaign is engaging in the same kind of bad-faith word-policing that so many voters find off-putting. Tonight’s debate may well feature several minutes of linguistic hair-splitting and I’m-not-saying/I’m-just saying, in place of conversations about what the federal government should and shouldn’t do. That is not what got Warren into the top three.

Donald Trump, like successful populists worldwide, campaigned and won in part by railing against the perceived political correctness of the country’s political, journalistic, and cultural elites. Continuing to mash that button is one way he strengthens his grip on the Republican Party, though there’s some evidence that the attendant crude manners and cruel policies are driving away suburban voters, especially women.

Democrats and other Trump-averse political actors thus face a challenge: How to forcefully oppose the president’s malodorous actions without alienating fence-sitters via in-group jargon and out-group condescension? The now-vanished field of Gen X candidates already tried out I-am-Spartacus histrionics, serial F-bombery, and even a bizarre if fleeting attempt to make school busing a litmus test. Forget the general election; none of this worked in the Democratic primary.

How Democrats react to #DebatesSoWhite might give us a hint of how they’re approaching the Trump problem. Black voters have overwhelmingly preferred Joe Biden; Bernie Sanders has drawn strong Latino support. Those who pin such preferences onto structural racism are wandering directly into the briar patch of false consciousness, which is rarely a good look.

In a season where electability is the primary Democratic virtue, Democratic voters have been sending a consistent message: Identity politics ain’t the ticket. Maybe next time around the Gen X candidates of all hues and genders will run as how they really are, as opposed to how Brooklyn Twitter wants them to be.

from Latest – Reason.com https://ift.tt/35SupWT

via IFTTT