Mueller Probe Witness Faces 30 Years In Jail After Guilty Plea To Second Child Porn Charge

Having been previously convicted of transporting child pornography in 1991, George Nader, a Lebanese-American businessman who served as a witness in special counsel Robert Mueller’s investigation, pleaded guilty to two charges relating to sexual exploitation of children on Monday, according to The Washington Post.

As we detailed in July 2019 when Nader was indicted, Mueller’s team discovered child pornography on his phone while interviewing him about a meeting between Blackwater founder Erik Prince, the brother of Education Secretary Betsy DeVos, and a high-level Russian official with ties to President Vladimir Putin, according to WaPo.

Soon after the images were discovered, prosecutors reportedly filed a criminal complaint against Nader over the images, but they kept the charges under seal, and Nader’s lawyers were never informed of his impending arrest all the while that he continued to cooperate with the Mueller probe.

That means Mueller kept a suspected child abuser and pornographer on the streets while it used him as a witness. And when Nader was no longer useful, he was finally being charged.

Nader has claimed the images were not child pornography but admitted to having received an email including violent sexual images of infants in 2012.

WaPo details the disgusting acts of this key Mueller witness, noting that according to Czech court documents, he paid at least five teenage boys to engage in sex acts, four of whom were under 15.

He engaged them through a boy he met at a Prague arcade, who said he “knew lots of boys who had been in elementary school with him who would be interested.”

Nader enticed the boys with “money, jewelry, mobile telephones, clothing, care and housing,” according to the court record, and took some to the city’s annual Matthew’s Fair.

While the serial pedophile’s charges carry a maximum penalty of 30 years, prosecutors (for reasons that are simply beyond our ken) in the Eastern District of Virginia agreed to recommend the mandatory minimum of 10 years.

Sentencing is set for April 10.

Additionally, as we reported previously, Nader was indicted in December on charges of illegally funneling campaign funds to Hillary Clinton’s 2016 campaign using straw donors, according to Politico.

Our favorite bank portfolio holding, U.S. Bancorp (NYSE:USB), closed Friday at 1.87x book value, down about 5% from the peak in December just over $60 and 2x book. Still a little too rich to add more to our portfolio of USB common, but we continue to accumulate a number of bank preferred issues. With the number of profitless unicorns dying at an accelerating rate, steady cash flow has a certain appeal right about now.

More important, credit default swap (CDS) spreads for high quality issuers are also at all time lows. JPMorganChase (NYSE:JPM) is inside 40bp or around a “A” rating for the largest bank in the US. In 2015, JPM’s CDS was trading close to 120bp over sovereign swaps. Question is, does the market know, really, how much risk sits on Jamie Dimon’s books in the world of corporate CDS and more obscure credit products, like “transformation repo.” We think not.

For those not familiar with the wonders of OTC derivatives and collateral swapping, see our 2019 comment “HELOCs and Transformational REPO.” We wrote in March of last year: “The dealer bank trades corporate debt for cash (for a fee), but uses its own government or agency collateral to meet the margin call for the customer. The bank holds the crap and all of the market and credit risk – sometimes for its own book, sometimes for clients. Tales of MF Global. Recall that the margin rules in Dodd-Frank and other laws and regulations around the world are meant to increase the proverbial “skin in da game” for swaps customers, especially the non-bank customers of banks.”

Outgoing Bank of England governor Mark Carney worries that the global economy is heading towards a “liquidity trap” that would undermine central banks’ efforts to avoid a future recession, according to the Financial Times. Former Fed Chairman Benjamin “QE” Bernanke is screaming for new fiscal policy measures to combat a non-existent recession – this as the negative after effects of “quantitative” monetary policy measures are growing.

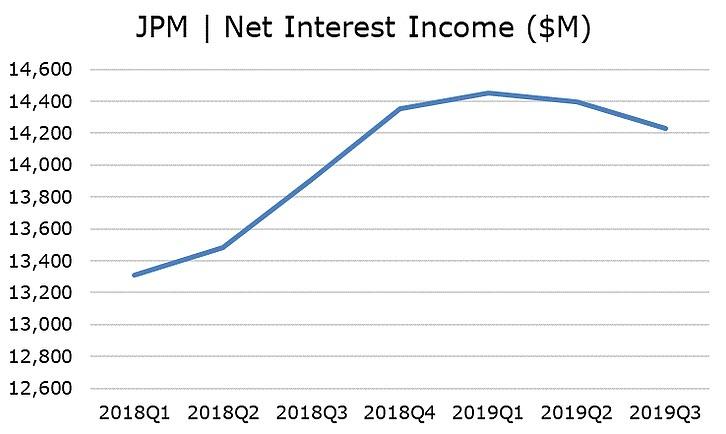

These central banksters may be right, but to us the bigger question is the unrecognized threat to the financial system from underpriced long-credit positions embedded on the balance sheets of global banks and bond funds. Bank interest earnings have long been subsidized by QE, but now banks are being squeezed by the same forces of market manipulation as credit starts to roll over. Suffice to say that the Street seems to finally understand that bank earnings are going to be a tad light, again, this quarter, due to the hangover from Uncle Ben’s QE electric KoolAid. The chart below shows net interest income for JPM.

Source: FFIEC

Despite the rosy economic outlook, bears continue to see reasons for despair in the world of credit – and we agree. The repo market sailed through year-end cushioned on a soft pillow of liquidity provided by Federal Open Market Committee. With the Fed announcing an end to the not-QE liquidity injection operations, though, we look forward to the next learning-by-doing adventure from Federal Reserve Chairman Jerome Powell.

Should the repo markets again start to seize up when the Fed ends its extraordinary liquidity injections, then Chairman Powell’s job may actually be on the line – and not because of President Donald Trump. The looming threat to Powell and other members of the FOMC is the tightly coiled but largely invisible long credit/short put positions on the books of major banks. This is a largely hidden risk that arises from years of market manipulation by global central banks. But hold that thought…

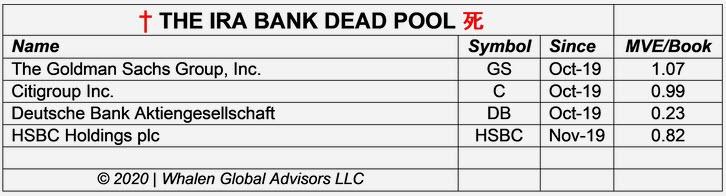

“We assign a negative outlook to DB and have little expectation that the situation will change in the near term. In our view, the most promising way to resolve what is an increasingly precarious situation would be for DB to sell its US operations in their entirety and wind up the remaining bank operations. Since Germany political leaders refuse to consider such a possibility, we expect that DB will stagger along, depleting capital and creating outsized risks, until such time as the bank’s poor management makes a mistake of sufficient magnitude to cause the bank to fail.”

Just to review, DB is one of four value destroyers in The IRA Bank Dead Pool. Banks that are members of the IRA Dead Bank Pool have poor financial performance, inferior equity market valuations and no apparent plan to correct these deficiencies. Even with US financials at the highest equity market valuations in a decade, the four institutions in the IRA Dead Pool – DB, Goldman Sachs (NYSE:GS), Citigroup (NYSE:C) and HSBC Holdings (NYSE:HSBC) – all trade at or below book value. DB has the lowest multiple of equity price to book value of any major bank.

In a recent twitter post, our pal @Stimpyz1 reminds us that negative interest rates are not the only source of risk to global banks.

“Deutsche bank might be in the crosshairs, but don’t forget HSBC,” he avers. “Hong Kong is looking like a black hole, and HSBC exposure to real estate on the island makes the DB balance sheet look like Microsoft.”

Like DB, HSBC’s US operations are in pretty bad shape, with years of credit losses and poor operational performance. Once upon a time, HSBC was a good comp for Citigroup, but today we would not even bother running the numbers. But when it comes to risk, we are far more focused on the bond market than banks, which are generally under-leveraged but contain a lot of undisclosed credit risk.

The lingering negative effect of the Bernanke-Yellen monetary benevolence is so pronounced in fixed income that a number of institutional managers we know have begun to lighten up on investment grade (IG) exposures based on the belief that a ratings-driven correction is coming. Michael Carrion of TCW wrote before the holiday:

“Much ink has been spilled this year on the topic of how strong the technicals are within the investment grade credit market and for good reason as they have been the dominant underlying driver of overall IG spreads all year. The resurgent strength derives from this year’s re-expansion of central bank balance sheets, which has resulted in a relentless supply/demand imbalance for IG bonds. Demand for IG credit reached a year-to-date peak in November, particularly in the second half of month as the pace of primary market new issuance slowed.”

Patti Domm of CNBC, quoting a research report from Hans Mikkelsen, head of investment grade corporate strategy at BofA Securities, wrote after the close on Friday: “Lured by low rates, companies issue high grade debt at one of the fastest paces ever this week,” this as interest rates touched a three-year low. The combination of market reaction to political uncertainty and central bank purchases of risk-free debt has created a credit trap for global banks and bond investors.

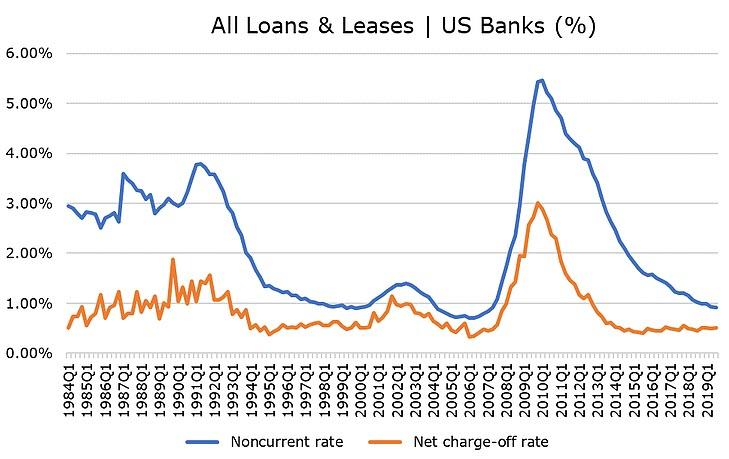

One of the things we learned from our colleague Dennis Santiago years ago at Institutional Risk Analytics is that when a credit spread looks to good to be true, it probably is. In those days, we’d convert the apparent default rate of a bank portfolio into a bond rating equivalent, then look at loss given default (LGD) to try to figure out how much the rate was understated. Today LGDs in the real estate sector are so skewed as to suggest that default rates are understated by at least 100%.

At the end of Q3 2019, the implied rating on the 0.51% of gross defaults for the $10.5 trillion in loans held by all US banks mapped to a “BBB” rating using the S&P default scale. If you believe that the aggregate rating of all obligors of US banks is investment grade, then we have some WeWork shares we’d like to sell you. Step right up.

Source: FDIC

The issuance of IG debt has set new records for the past several years, but most of this paper is clustered around “BBB” ratings. This suggests that the proverbial lemmings could fall off of the ratings cliff with little or no notice. As we all hopefully learned in the Adam McKay film “Big Short,” the major credit rating agencies don’t have the capacity or the courage to react quickly as and when economic and/or market conditions dictate a change for dozens of issuers. The investors that own long positions in underpriced corporate risk positions will be long dead before the ratings change.

The potential ratings volatility embedded in corporate debt has huge implications for banks, which have been “transforming” crap collateral into high IG in order to partially satiate the investor demand for low- or no-risk paper. TCW confirms our earlier colloquy with @Stimpyz1 on Twitter the other day:

This implies that there is an embedded credit put on the books of a lot of banks and funds as and when the QE party well and truly ends. Perhaps this is why John Carney and Ben Bernanke are so insistent of a shift to fiscal stimulus. But it needs to be said that no amount of fiscal push will fix the credit risk that the Fed and other central banks have created via “quantitative easing.”

We’ve been talking about the misalignment of credit ratings and corporate fundamentals for the past several years, but the continuation of QE in Europe and Asia has managed to prevent a reversion to the valuation mean. The divergence seen in junk rated collateral sold into collateralized loan obligations (CLOs) and superior credits suggests to us that an adjustment may finally be underway. The inferior assets always fall first. And to recall John Kenneth Galbraith’s great book about the 1920s: “Genius comes after the fall.”

While interest rate movements are suppressing net interest margins at major US banks, the prospect of a wholesale slip below investment grade for literally hundreds of weak bond issuers may be a far more worrisome problem. Bad ratings concealed the true risk in billions of dollars-worth of mortgage backed securities prior to the 2008 crisis. The new area for securities fraud and ratings malfeasance is the corporate bond market. If you think the liquidity problems we saw last summer in plain vanilla repo were bad, imagine what happens when margin calls on collateral swaps start to swamp the dealer banks.

California’s homeless population keeps skyrocketing, and so has the number of bills aiming at solving the homelessness problem. Last week, Gov. Gavin Newsom unveiled a billion-dollar plan designed to get more houses built for those who need it. But even that much money isn’t likely to help many people if the underlying problem remains unchanged. To solve California’s homelessness problem, you have to address inflexible zoning rules and ineffective municipal bureaucracies.

Newsom’s executive order allocates $750 million to build more affordable housing units and to establish a California Access to Housing and Services Fund within the state’s Department of Social Services. The goal is to pay rent for individuals facing homelessness and to make vacant state properties available immediately as shelter options. An additional $695 million will be used to boost preventative health care measures for the homeless through Medi-Cal Healthier California for All.

This follows 18 housing bills that Newsom signed into law last fall. The bills are supposed to accelerate housing production, but they don’t have much teeth. They require local jurisdictions to publicly share information about zoning ordinances and other building rules—not to roll the regs back, just to be more transparent about them. They also ask cities and counties to maintain an inventory of state surplus land sites suitable for residential development.

California voters also approved $4 billion in bonds last year for affordable housing programs.

“You can’t just throw money at homelessness and a lack of affordable housing and expect that you’re going to achieve the result that you’re hoping to achieve,” says David Wolfe, legislative director of the Howard Jarvis Taxpayers Association. After all, it hasn’t worked so far.

California is home to almost half of America’s homeless population, and the median price for a house there is more than twice the national level. Fixing that problem means building more houses, but zoning laws and anti-development activism make that difficult. Serious reform will require moves like modifying city codes to let developers build units that aren’t single-family homes. And dialing back rules, such as the California Environmental Quality Act, that let neighborhood activists block new construction with faux-environmental concerns. And, in general, clearing away the thicket of state and local regulations that get in the way of meeting the demand for housing.

“If you’re a city council,” San Francisco Assemblyman Phil Ting toldCurbed San Francisco, “the people who vote for you oppose the housing you’re creating, and you’re creating housing for the people who have yet to move in.”

Californians also have to contend with a perverse incentive built into Proposition 13, a measure that limits property-tax increases on homes until they’re sold. This gives cities a reason to encourage commercial instead of residential development.

As legislators continue to pour money into housing programs, perhaps they should think more about how to address the broken system responsible for the mess. In the meantime, others will look for ways to route around the system. Silicon Valley giants have begun to propose their own housing projects, underscoring the state government’s inability to move forwards with its own reforms.

from Latest – Reason.com https://ift.tt/3a15ofD

via IFTTT

US Budget Deficit Blows Out To Nine Year High In First Quarter Of Fiscal 2020

The gaping US budget deficit hole is getting bigger with each passing month.

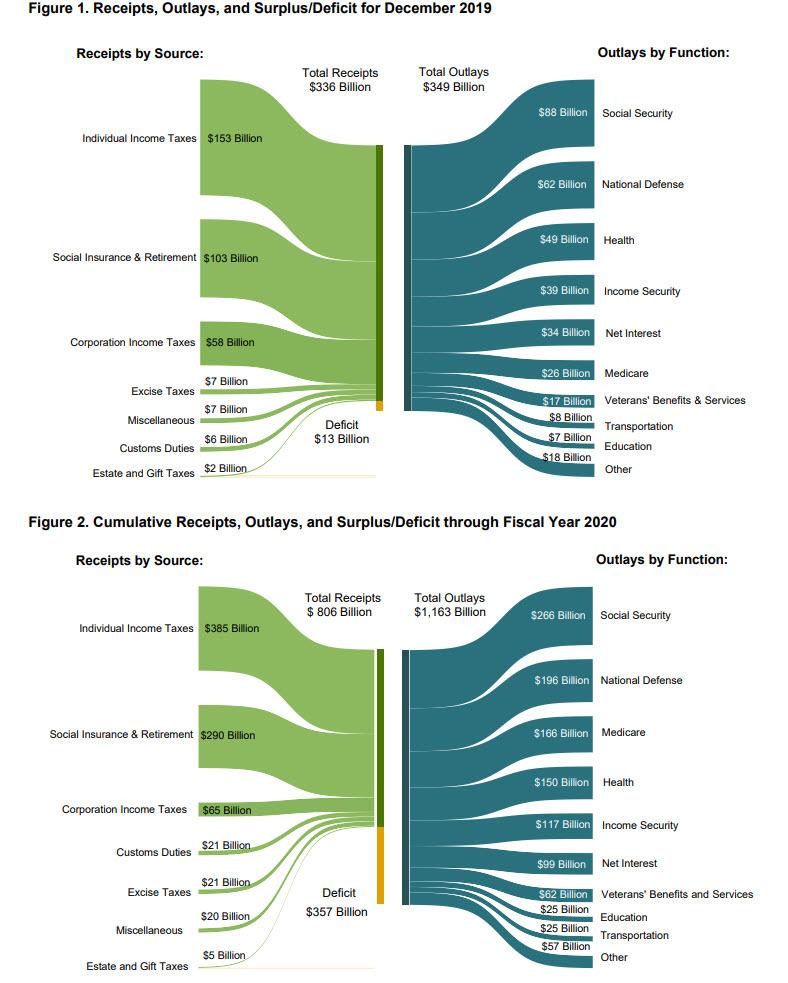

Earlier today, the US Treasury announced that in December (the third month of fiscal 2020), the US spent $13.3 billion more than it pulled in, and while the month’s budget deficit was modestly better than the $15 billion expected, it was virtually unchanged from the $13.5BN deficit recorded in Dec 2018.

Total December spending of $349billion, was 7.5% higher than a year earlier, with the biggest outlays for the month as follows: social security ($88BN), national defense ($62BN), Health ($49BN), Income Security ($39BN), Net Interest ($34BN), which was more than Medicare spending for the month ($26BN) and so forth. Meanwhile, receipts increased by an almost identical amount, rising 7.4% from $312.6BN to $335.8BN, thanks to $153BN in individual income taxes, $103BN in Social insurance and retirement receipts, and $58BN in corporate income taxes.

For the first three months of fiscal 2020, total Outlays rose to $1,163BN while Receipts were a far more modest $806BN, as broken out in the chart below.

This means that the cumulative deficit for the first three months of the year has surged to $357BN.

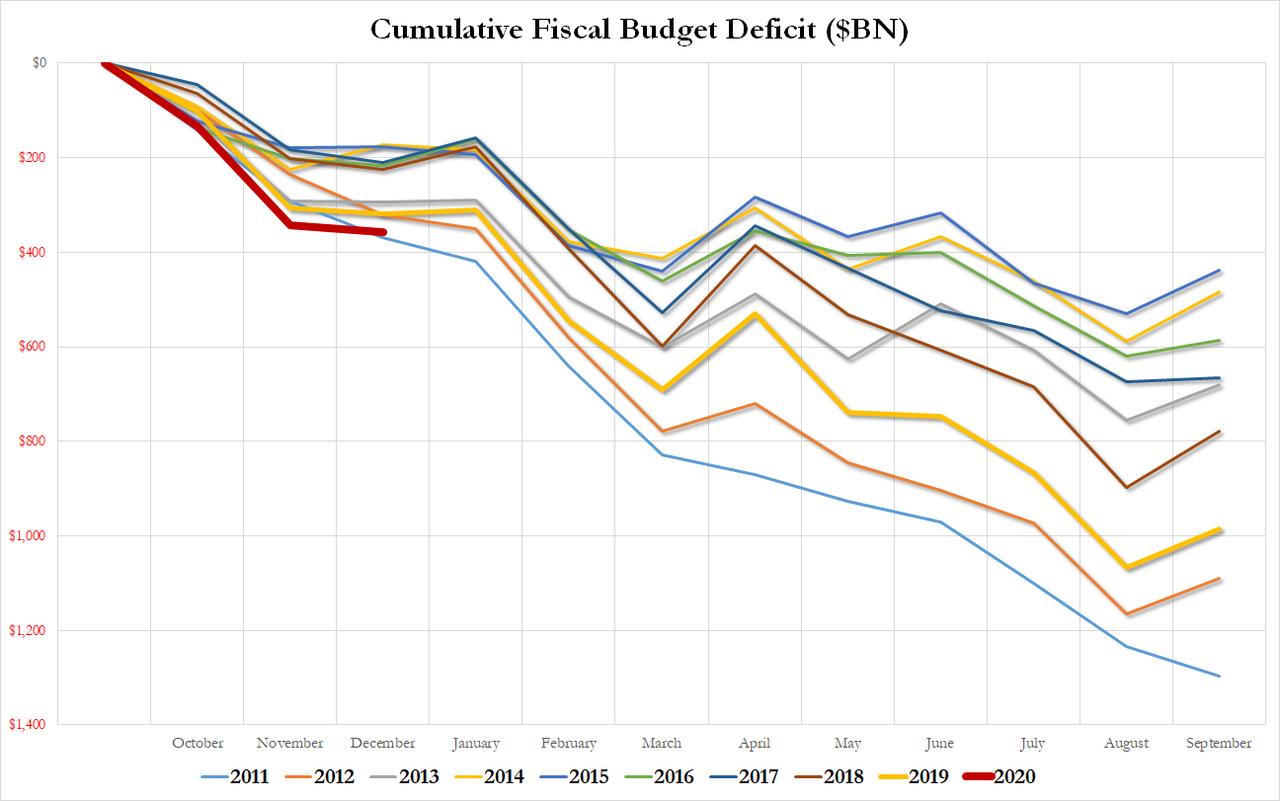

It also means that the deficit after one quarter of fiscal 2020 is now in the history books, was the widest going back all the way to 2011, when the US was still spending like a drunken sailor under President Obama, in response to the financial crisis, and when the final deficit for the full year soared to $1.3 trillion.

And while in 2020 nobody is predicting a full-year hole as big as 2011’s, with every passing month we get closed to a number hinting that the US is spending as if it is emerging from a recession and a major economic crisis. That, or it is about to enter one. One more thing to keep in mind: if it wasn’t for $21BN in customs duties collected mostly from China as a result of the trade war tariffs, the cumulative US budget deficit through December would be even worse than that in 2011.

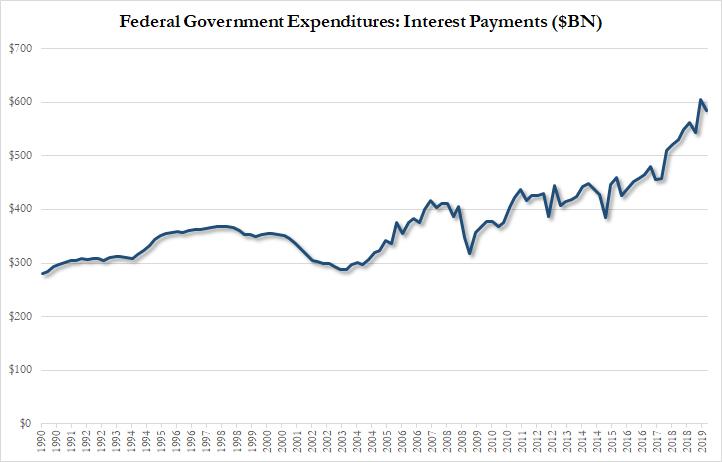

One final point: with US debt recently surpassing $23 trillion, it is no surprise that interest expense on this debt has also pushed to all time highs, and in the latest quarter it stabilized just shy of the prior record, dipping modestly to $585 billion, roughly double where its average for the two decade period from 1990 to 2010, at which point it soared. One can only imagine what the interest expense will be if and when rates are ever allowed to normalize.

But the actual demise of the authoritarian regime that’s been in power since 1979 will come more from acts like the one taken by Kimia Alizadeh, Iran’s only female Olympic medalist. Late last week, the bronze medalist in Taekwondo in the 2016 Summer Games announced via Instagram that she has fled her home country due to the systematic oppression of women. Via CNN:

“Let me start with a greeting, a farewell or condolences,” the 21-year-old wrote in an Instagram post explaining why she was defecting. “I am one of the millions of oppressed women in Iran who they have been playing with for years.”…

“They took me wherever they wanted. I wore whatever they said. Every sentence they ordered me to say, I repeated. Whenever they saw fit, they exploited me,” she wrote, adding that credit for her success always went to those in charge.

“I wasn’t important to them. None of us mattered to them, we were tools,” Alizadeh added, explaining that while the regime celebrated her medals, it criticized the sport she had chosen: “The virtue of a woman is not to stretch her legs!”

On the heels of Alizadeh’s self-imposed exile comes reports that two anchors for Iranian state broadcaster IRIB have quit over qualms about censorship and official lies. From The Guardian:

Zahra Khatami quit her role at IRIB, saying: “Thank you for accepting me as anchor until today. I will never get back to TV. Forgive me.”

Her fellow anchor Saba Rad said: “Thank you for your support in all years of my career. I announce that after 21 years working in radio and tv, I cannot continue my work in the media. I cannot.”

The journalists’ statements are part of a crisis of confidence following the initial attempts by state officials to deny that Ukrainian jetliner 752 had been shot down by mistake by members of the Islamic Revolutionary Guards Corp (IRGC) air defence force.

A third broadcaster, Gelare Jabbari, said she quit “some time ago” and asked Iranians to “forgive me for the 13 years I told you lies.”

This is all happening against the backdrop of massive protests in Iran following the accidental shooting down of a Ukrainian airliner that carried 176 people. Demonstrators protested rising gas prices late last year and in the years prior, there have been other protests and general strikes for a host of reasons, including increased dissatisfaction with theocratic rule. According to a Carnegie Endowment report, 150,000 educated Iranians emigrate each year, “costing the country over $150 billion per year” as relatively young and motivated residents leave for greener pastures elsewhere.

By all accounts, sanctions imposed by the United States in 2018 have hit Iran’s economy extremely hard and are playing a role in sparking protests. It’s never fully clear how those sorts of intervention, much less more militaristic actions such as the killing of Soleimani, play out—sometimes overt pressure applied by an outside power emboldens dissent and sometimes it decreases it. But when a country starts to get hollowed out from within, as seems to be the case with Alizadeh’s exile and other recent and ongoing domestic developments, autocrats should start sweating.

from Latest – Reason.com https://ift.tt/30iaShl

via IFTTT

California’s homeless population keeps skyrocketing, and so has the number of bills aiming at solving the homelessness problem. Last week, Gov. Gavin Newsom unveiled a billion-dollar plan designed to get more houses built for those who need it. But even that much money isn’t likely to help many people if the underlying problem remains unchanged. To solve California’s homelessness problem, you have to address inflexible zoning rules and ineffective municipal bureaucracies.

Newsom’s executive order allocates $750 million to build more affordable housing units and to establish a California Access to Housing and Services Fund within the state’s Department of Social Services. The goal is to pay rent for individuals facing homelessness and to make vacant state properties available immediately as shelter options. An additional $695 million will be used to boost preventative health care measures for the homeless through Medi-Cal Healthier California for All.

This follows 18 housing bills that Newsom signed into law last fall. The bills are supposed to accelerate housing production, but they don’t have much teeth. They require local jurisdictions to publicly share information about zoning ordinances and other building rules—not to roll the regs back, just to be more transparent about them. They also ask cities and counties to maintain an inventory of state surplus land sites suitable for residential development.

California voters also approved $4 billion in bonds last year for affordable housing programs.

“You can’t just throw money at homelessness and a lack of affordable housing and expect that you’re going to achieve the result that you’re hoping to achieve,” says David Wolfe, legislative director of the Howard Jarvis Taxpayers Association. After all, it hasn’t worked so far.

California is home to almost half of America’s homeless population, and the median price for a house there is more than twice the national level. Fixing that problem means building more houses, but zoning laws and anti-development activism make that difficult. Serious reform will require moves like modifying city codes to let developers build units that aren’t single-family homes. And dialing back rules, such as the California Environmental Quality Act, that let neighborhood activists block new construction with faux-environmental concerns. And, in general, clearing away the thicket of state and local regulations that get in the way of meeting the demand for housing.

“If you’re a city council,” San Francisco Assemblyman Phil Ting toldCurbed San Francisco, “the people who vote for you oppose the housing you’re creating, and you’re creating housing for the people who have yet to move in.”

Californians also have to contend with a perverse incentive built into Proposition 13, a measure that limits property-tax increases on homes until they’re sold. This gives cities a reason to encourage commercial instead of residential development.

As legislators continue to pour money into housing programs, perhaps they should think more about how to address the broken system responsible for the mess. In the meantime, others will look for ways to route around the system. Silicon Valley giants have begun to propose their own housing projects, underscoring the state government’s inability to move forwards with its own reforms.

from Latest – Reason.com https://ift.tt/3a15ofD

via IFTTT

“A shocking crime was committed on the unscrupulous initiative of few individuals, with the blessing of more, and amid the passive acquiescence of all.”

Tacitus, Publius Cornelius

The shocking crime being committed during this century under the unscrupulous initiative of a few evil men is ongoing and no longer hidden from those willing to open their eyes and see the truth. As conspiracy theorists have proven to be right through the sacrifice of Snowden, Assange, and other patriots for truth, the Deep State psychopaths have double downed and are blatantly flaunting their power and control over the levers of government, finance and media.

Never in the history of mankind have such devious, unscrupulous, arrogant, narcissistic and downright evil men seized hegemony over global finance, trade and politics. A minority of billionaire oligarchs and their highly compensated apparatchiks, ingrained in government bureaucracies, surveillance agencies and media outlets refuse to relinquish their dominance and would rather burn the world to the ground than loss their ill-gotten riches, un-Constitutional power and unlawful control.

When I started pondering a theme for 2020, the “year of living dangerously” immediately popped into my mind. But I had a feeling I’d used that title before. I did a search of my site and lo and behold I wrote 2012 – The Year of Living Dangerously eight years ago. As I reread my predictions for 2012, it was a humbling experience, as not only did most of my predictions not come to fruition in 2012, they haven’t materialized during the next eight years. My facts and reasoning were sound, but my naivety regarding the extreme measures the Deep State was willing to utilize, blinded me to how long they could keep this game going. In my year-end assessment of my 2012 predictions this was my conclusion:

“It seems I always underestimate the ability of sociopathic central bankers and their willingness to destroy the lives of hundreds of millions to benefit their oligarch masters. I always underestimate the rampant corruption that permeates Washington DC and the executive suites in mega-corporations across the land. And I always overestimate the intelligence, civic mindedness, and ability to understand math of the ignorant masses that pass for citizens in this country. It seems that issuing trillions of new debt to pay off trillions of bad debt, government sanctioned accounting fraud, mainstream media propaganda, government data manipulation and a populace blinded by mass delusion can stave off the inevitable consequences of an unsustainable economic system.”

This statement has been applicable for an inexplicable length of time, with no indication of changing in the near future. I thought the national debt reaching $16.5 trillion would surely trigger a crisis and recession. Here we are eight years later, $7 trillion more in debt and still no recession. I thought global debt, particularly in in Europe, would lead to a global contagion and breakup of the EU. Global debt has risen by $50 trillion, the EU is intact, and the world muddles on.

The coordinated efforts of central bankers in the U.S., Europe, Japan and China has produced a flood of liquidity, elevating all markets, enriching the .1%, impoverishing senior citizens, and creating inflation for average Americans – underreported by the BLS. By artificially propping up GDP, the economy has not officially gone into recession, which has supported the stock market going up 150% since 2011. Debt to GDP ratios and stock market valuations are meaningless when the Fed’s sole purpose is to enrich their Wall Street benefactors through money printing.

Home prices were still falling in 2011 and I expected it to continue in 2012. Again, I was unable to comprehend the lengths the ruling class would go to in order to reverse the verdict of free markets. Little did I know the Fed, Treasury, and Wall Street would conspire to buy up millions of foreclosed homes, renting them back to the people they kicked into the street, artificially suppress interest rates, and use Fannie and Freddie to again give mortgages to anyone who could fog a mirror. It worked like a charm, as home prices bottomed in 2012 and now have surpassed the 2005 peak.

The official unemployment rate in 2011 was 8.7% and I expected it to tick higher once the recession took hold. But, QE3 was unleashed, staving off recession, propelling the stock market, and driving “official” unemployment to record lows of 3.5% today, even though 101 million working age Americans aren’t working. The combination of QE to infinity and hundreds of billions in corporate stock buybacks have worked wonders for the .1%, despite lackluster GDP and corporate income growth.

Oil reached the highest level in history during 2012 and continued higher in 2013. This normally would have triggered a recession, but QE and zero interest rates kept it at bay. Then the “shale miracle” drove supply higher, oil prices crashed into the $30s, and have remained in the $60 range ever since. The shale miracle certainly created millions of new barrels per day, but the companies fracking for the oil haven’t made a dime in seven years. The “miracle” was created by the Fed’s easy money and Wall Street bankers financing companies with no possibility of ever being profitable. With prices still hovering around $60, frackers are going bankrupt in droves, output has peaked as new investment dollars dry up, and this boom goes bust, as all fraudulent schemes do when reality meets delusion.

As the presidential election approached, the Occupy Wall Street movement was at its height. Just like the Tea Party movement before it, the Occupy movement was co-opted and trivialized within months by the Deep State and their minions in government and the media. Bloomberg did his part and wiped out the Zuccotti Park encampment in one night. Ron Paul’s libertarian attempt to capture the Republican nomination was derailed by the GOP establishment and my dreams of a 3rd party run were dashed. The country’s last chance for redemption was lost.

My expectations of a war between Iran and Israel have still gone unfulfilled, with tensions continuing to grow. But at least the military industrial complex was able to profit from war in Syria, Yemen, and the never-ending war in Afghanistan. Trump’s taking out a key Iranian general with drone strikes have certainly increased the risk of something bigger in the Middle East, but will probably not result in a bigger shooting war.

Eight years of keeping the balls in the air, as their toxic “solutions” poison the system and ensure a cataclysmic demise to this debt-based Ponzi scheme, has convinced millions abnormality is actually normal. Living through my first and only Fourth Turning has proven to be more difficult than I realized. I expected it to proceed at a much faster pace than has materialized. Knowing the details of previous Fourth Turnings convinced me I could predict how this one would proceed.

But I failed to grasp the likely twenty-year length of this crisis and how actions and reactions will develop on their own timeline, not according to the annual forecast of prognosticators and pundits. The key factors driving this crisis: debt, civic decay, and global disorder, triggered this crisis in 2008, continue to gain momentum, and will ultimately merge into a lethal combination which will end the relatively short but eventful period of the American Empire.

My attempt at trying to predict what would happen in 2019, based on the Fourth Turning – 2019 From a Fourth Turning Perspective – turned out to be wrong once again. Not a shocker, since my timing has been off during the first eleven years of this Crisis. Nothing in my assessment has changed one year later. The three driving factors of this Fourth Turning continue to hasten towards a fateful climax. My assessment as we entered 2019 still applies as we enter 2020:

Debt, civic decay and global disorder are on center stage as we enter the fateful year of 2019. A madness seems to be gripping the nation, a melancholy realization all is not right. Everything has a chaotic feel, as financial markets are falling, politicians threaten and attack each other, government dysfunction is laid bare for all to see, Deep State snakes slither behind the scenes trying to bring down Trump, racial tensions grow, foreign governments topple, Russia and China challenge U.S. hegemony, and the global debt Ponzi scheme is entering its collapse phase.

The stock market was falling and signs of imminent recession were appearing as we entered 2019. My prediction that a Fed discount rate of 3% would trigger a recession, stock market collapse and a debt crisis looked solid, until the Treasury, Trump and Wall Street bankers pressured Powell to cease rate increases and corporate executives did their part by buying back their shares. Powell then folded like a cheap suit to Trump’s demands and lowered rates by .75% to goose the stock market over the summer.

When the repo market showed the true underlying distress in the financial system, Powell introduced QE4 and added $500 billion to the Fed balance sheet, with no sign of slowing down. This liquidity injection again boosted the wealth of the .1% to stratospheric levels as the stock market skyrockets to new records daily. There are clearly deep-seated structural issues with a financial system saturated with unpayable levels of debt. So, the Fed will continue to run their electronic printing presses at warp speed until the inevitable banquet of consequences is served to all.

The optimism among the financial class has reached all-time highs. As long as their sugar daddy Powell keeps the candy flowing, all is well on Wall Street. Meanwhile, most economic indicators continue to point downward and our national debt grows by $4 billion per day. Average Americans are up to their eyeballs in debt, as they need their credit cards to survive, student loan delinquencies soar, auto loan debt is going bad at a higher rate than the 2008 crisis, and home prices are now 15% above the previous bubble peak.

Rent and healthcare costs continue to grow at a much higher rate than reported by the government. It feels like something has to give. Reasonable, critical thinking, intelligent observers are flabbergasted by the outrageously blatant disregard for future generations being exhibited by the ruling class, as they pillage whatever is left of our national wealth. The children be damned.

The social distress I noted last year continues unabated today as the glorification of abnormality reaches new heights. The flames of division and disarray are fanned unceasingly by the left-wing media in order to distract from the true desperate financial situation of the country. As young generations, dumbed down and socially engineered in government run schools, are lured into believing socialism is the answer by corrupt lying politicians, they are willfully ignorant of what socialism has wrought in Venezuela and other 3rd world shitholes.

Rather than focus on how politicians of both parties, the Deep State and the Wall Street cabal have destroyed their financial futures through corrupt schemes and rigging the system for their benefit, they worship a thirteen year old regarding the climate change hoax. The puppeteers using Greta as their puppet seek control of your lives, more taxes, and the power to take away your liberties and freedom, while enriching themselves.

The political distress as we entered 2019 was already at looming civil war intensity. If possible, the decibel level has actually risen higher, to 11 on a 1 to 10 scale. The Mueller investigation turned into a big nothingburger as the ongoing Deep State coup against Trump relentlessly marches onward. The Democrats and their Surveillance State co-conspirators have determined the best way to cover-up their treasonous acts is to stay on the offensive by impeaching Trump on bogus charges. Their media mouthpieces produce prodigious levels of propaganda designed to convince the masses Trump should be removed from office. The majority of the public aren’t buying it, as the fake news media has lost its credibility after three years of lies and misinformation.

In Part II of this article I will examine some of the dynamics which will most impact the next year and remainder of this Fourth Turning.

* * * The corrupt establishment will do anything to suppress sites like the Burning Platform from revealing the truth. The corporate media does this by demonetizing sites like mine by blackballing the site from advertising revenue. If you get value from this site, please keep it running with a donation. [Jim Quinn – PO Box 1520 Kulpsville, PA 19443] or Paypal

“This Is Insanity!” – Jim Rogers Warns Of “Horrible Time” Ahead

The Fed has increased its balance sheet over 500% in the past decade; The Bank of Japan is printing money to buy bonds and stock ETFs; and The European Central Bank is mired in insane negative interests. And, according to legendary investor Jim Rogers, they will continue this “madness” as long as its necessary.

In an interview with RT’s Boom Bust, Rogers exclaims, that interest rates around the world have never been this low:

“… this is insanity, that’s not how sound economic systems are supposed to work.”

In 2008, Rogers notes that we had problems because of too much debt, however, “since then the debt has skyrocketed everywhere and it’s going higher and higher. We are going to have a horrible time when this all comes to an end.”

Adding that:

…eventually, the market is going to say: ‘We don’t want this, we don’t want to play this game anymore, and we don’t want your garbage paper anymore’.”

And when that happens, Rogers warns that central banks will print even more and buy even more assets.

“And that’s when we will have very serious problems… We all are going to pay a horrible price someday but in the meantime it’s a lot of fun for a lot of people.”

When it comes to an end, Rogers laments, “it will be the worst of my lifetime.”

But the actual demise of the authoritarian regime that’s been in power since 1979 will come more from acts like the one taken by Kimia Alizadeh, Iran’s only female Olympic medalist. Late last week, the bronze medalist in Taekwondo in the 2016 Summer Games announced via Instagram that she has fled her home country due to the systematic oppression of women. Via CNN:

“Let me start with a greeting, a farewell or condolences,” the 21-year-old wrote in an Instagram post explaining why she was defecting. “I am one of the millions of oppressed women in Iran who they have been playing with for years.”…

“They took me wherever they wanted. I wore whatever they said. Every sentence they ordered me to say, I repeated. Whenever they saw fit, they exploited me,” she wrote, adding that credit for her success always went to those in charge.

“I wasn’t important to them. None of us mattered to them, we were tools,” Alizadeh added, explaining that while the regime celebrated her medals, it criticized the sport she had chosen: “The virtue of a woman is not to stretch her legs!”

On the heels of Alizadeh’s self-imposed exile comes reports that two anchors for Iranian state broadcaster IRIB have quit over qualms about censorship and official lies. From The Guardian:

Zahra Khatami quit her role at IRIB, saying: “Thank you for accepting me as anchor until today. I will never get back to TV. Forgive me.”

Her fellow anchor Saba Rad said: “Thank you for your support in all years of my career. I announce that after 21 years working in radio and tv, I cannot continue my work in the media. I cannot.”

The journalists’ statements are part of a crisis of confidence following the initial attempts by state officials to deny that Ukrainian jetliner 752 had been shot down by mistake by members of the Islamic Revolutionary Guards Corp (IRGC) air defence force.

A third broadcaster, Gelare Jabbari, said she quit “some time ago” and asked Iranians to “forgive me for the 13 years I told you lies.”

This is all happening against the backdrop of massive protests in Iran following the accidental shooting down of a Ukrainian airliner that carried 176 people. Demonstrators protested rising gas prices late last year and in the years prior, there have been other protests and general strikes for a host of reasons, including increased dissatisfaction with theocratic rule. According to a Carnegie Endowment report, 150,000 educated Iranians emigrate each year, “costing the country over $150 billion per year” as relatively young and motivated residents leave for greener pastures elsewhere.

By all accounts, sanctions imposed by the United States in 2018 have hit Iran’s economy extremely hard and are playing a role in sparking protests. It’s never fully clear how those sorts of intervention, much less more militaristic actions such as the killing of Soleimani, play out—sometimes overt pressure applied by an outside power emboldens dissent and sometimes it decreases it. But when a country starts to get hollowed out from within, as seems to be the case with Alizadeh’s exile and other recent and ongoing domestic developments, autocrats should start sweating.

from Latest – Reason.com https://ift.tt/30iaShl

via IFTTT

There certainly hasn’t been a lack of seismic activity so far in 2020. Just a few days ago, I wrote about the horrific earthquake swarm that Puerto Rico is currently experiencing. More than 1,000 earthquakes have rattled Puerto Rico so far, and as you will see below, it was just hit by another very large earthquake. But right now volcanic eruptions have taken center stage. In particular, a massive eruption in the Philippines is making headlines all over the world, but what most people don’t realize is that several other volcanoes have also blown their tops in spectacular fashion within the past week. Suddenly, volcanoes all over the globe are shooting giant clouds of ash miles into the air, and this is greatly puzzling many of the experts.

Let’s review what we have witnessed over the past 7 days.

Last Tuesday, one of the most important volcanoes in Alaska shot hot ash 25,000 feet into the air…

Shishaldin Volcano erupted at 5 a.m. Tuesday, the Alaska Volcano Observatory announced, and sent up an initial ash cloud to 19,000 feet. Clouds initially obscured the mountain, but satellite imagery confirmed the ash cloud, U.S. Geological Survey geophysicist Hans Schwaiger said.

Seismicity diminished for a few hours, but it then increased again. During the increase, the volcano spewed an ash cloud to 25,000 feet, the observatory announced. The later eruption increased the volume of ash.

There are 5280 feet in a mile, and so we are talking about an ash cloud nearly 5 miles high.

Mexico’s Popocatépetl volcano burst to life on Thursday in a spectacular gush of lava and clouds of ash that hurled incandescent rock about 20,000 feet into the sky.

The dramatic explosion of the active stratovolcano, a little over 40 miles southeast of Mexico City, was captured on video by Mexico’s National Center for Disaster Prevention, CENAPRED.

Those that follow my work on a regular basis already know that I am deeply concerned about Mt. Popocatepetl. It has the potential to create the worst natural disaster in the modern history of North America, because it is quite close to Mexico City. The following summary of the potential threat that Mt. Popocatepetl poses comes from one of my previous articles…

Approximately 26 million people live within 60 miles of Popocatepetl’s crater, and so we are talking about the potential for death and destruction on a scale that is difficult to imagine. In ancient times, Mt. Popocatepetl buried entire Aztec cities in super-heated mud, but then it went to sleep for about 1,000 years. Unfortunately for us, it started waking up again in the 1990s, and now this is the most active that we have seen it ever since the volcano originally reawakened.

Let us hope that Mt. Popocatepetl settles down, because the death and destruction that a catastrophic eruption would cause would be off the charts.

Explosive activity continues. Volcanic Ash Advisory Center (VAAC) Buenos Aires warned about a volcanic ash plume that rose up to estimated 24000 ft (7300 m) altitude or flight level 240 and is moving at 15 kts in S direction.

But hardly anyone is paying any attention to what just took place in Peru because of what just happened in the Philippines.

According to USA Today, ash has already reached Manila, and “red-hot lava” has started gushing out of the volcano…

Red-hot lava gushed from of a Philippine volcano on Monday after a sudden eruption of ash and steam that forced villagers to flee and shut down Manila’s international airport, offices and schools.

There were no immediate reports of casualties or major damage from Taal volcano’s eruption south of the capital that began Sunday. But clouds of ash blew more than 100 kilometers (62 miles) north, reaching the bustling capital, Manila, and forcing the shutdown of the country’s main airport with more than 240 international and domestic flights cancelled so far.

Unfortunately, authorities are warning that the worst may still be yet to come.

“The earthquakes were strong, and it felt like there was a monster coming out” as in the movies, Cookie Siscar, who had left the area and was relaying a report from her husband, Emer, a poultry farmer, told the Times.

The Philippine Institute of Volcanology and Seismology increased its threat level for Taal Volcano to four out of five, saying that a “hazardous explosive eruption” could happen at any minute

Meanwhile, we continue to see unusual earthquake activity all over the globe.

After already experiencing more than 1,000 earthquakes since the beginning of 2020, Puerto Rico was hit by a magnitude 5.9 quake on Saturday…

A magnitude 5.9 quake shook Puerto Rico on Saturday, causing further damage along the island’s southern coast, where previous recent quakes have toppled homes and schools.

The U.S. Geological Survey said the 8:54 a.m. (1254 GMT) quake hit 8 miles (13 kilometers) southeast of Guanica at a shallow depth of 3 miles (5 kilometers).

For quite a while, I have been warning that our planet is becoming increasingly unstable and that the shaking is only going to get worse.

I know that a lot of people didn’t believe me at first, and that is okay.

After the events of the last few days, perhaps a few more people will start to understand what is going on.

There have always been earthquakes and volcanic eruptions, but for most of our lives we have been able to assume that our planet is generally stable.

Unfortunately, that is no longer a safe assumption.

We have entered a period of time when all of the old assumptions will no longer apply, and everything that can be shaken will be shaken.