Senate Trial Likely To Start Next Week After Pelosi Ends Impeachment Impasse

President Trump’s Senate impeachment trial will likely begin Jan. 21, according to Sen. John Cornyn (R-TX).

The news comes as House Speaker Nancy Pelosi announced that that two articles will be transferred to the Senate, ending a three-week standoff over how the trial would be conducted, according to Bloomberg.

“Tuesday is what it’s feeling like,” Cornyn told reporters, adding that he expects the articles and the names of impeachment managers from the House this week (likely Jerrold Nadler of NY and Adam Schiff of CA).

Cornyn also says there will likely be a full trial, as there won’t be enough votes to dismiss the charges without one as Trump has suggested over Twitter.

“My understanding is that most Republicans want to have a full trial,” said Conryn.

Meanwhile, Bloomberg cites a Quinnipiac University poll which found that 2/3 of US voters want former White House National Security Adviser John Bolton to testify – a finding which may convince Republicans to join with Democrats in calling him as a witness.

Bolton’s offer to testify at the trial if subpoenaed has been central to attempts by House Speaker Nancy Pelosi and other Democrats to force the GOP-controlled Senate to allow witnesses. It would take just four Republican senators to vote with Democrats to get a majority on the question of witnesses. Maine Senator Susan Collins, one of the most vulnerable GOP incumbents in 2020, said last week she’s been talking with a small number of her colleagues about allowing new testimony.The poll, conducted Jan. 8-12 among self-identified registered voters, also found a bare majority, 51%, approved of the House vote to impeach Trump and 46% disapproved. Voters were divided on the verdict of a trial, with 48% saying the Senate should not vote to remove the president from office and 46% saying Trump should be removed.

The poll of 1,562 people nationwide has a margin of error of plus or minus 2.5 percentage points. –Bloomberg

According to the report, Nadler and Schiff are likely to be the top names on the prosecution team in the Senate trial, according to Rep. Dan Kildee of Michigan during a Monday interview with CNN, who said it would be a “Talented group, obviously with Adam Schiff and Nadler — one would expect them.”

There’s a fine line between legislation addressing deepfakes and legislation that is itself a deep fake. Nate Jones reports on the only federal legislation addressing the deepfake problem so far. I claim that it is well short of a serious regulatory effort – and pretty close to a fake itself.

In contrast, India seems serious about imposing liability on companies whose unbreakable end-to-end crypto causes harm, at least to judge from the howls of the usual defenders of such products. David Kris explains how the law will work. I ask why Silicon Valley gets to impose the externalities of encryption-facilitated crime on society when we’d never let Big Tech leave us with the tab for water or air pollution just because their products are so cool. In related news, the FBI may be turning the Pensacola military terrorism attack into a slow-motion replay of its San Bernardino fight with Apple, this time with more top cover (and probably better lawyering).

Poor Nate seems to draw all the fake legislation in this episode. He explains a 2020 appropriations rider requiring the State Department to report on how it issues export licenses for cyber espionage capabilities; this is a follow-up to investigative reporting on the way such capabilities ended up being used against human rights activists in the UAE. As we agree, it’s an interesting and likely unsolvable policy problem, so the legislation opts for the most meaningless of remedies, requiring the Directorate of Defense Trade Control to report “on cybertools and capabilities licensing, including licensing screening and approval procedures as well as compliance and enforcement mechanisms” within 90 days.

Nate also gets to cover some decidedly un-fake requirements in the 2019 NDAA limiting how defense contractors can use Chinese technology. The other shoe is about to drop, and if the first one was a baby shoe, the second is a Clydesdale’s horseshoe.

It’s hard to call it fake, but the latest export control rule restricting sales of AI could hardly be narrower. Maury Shenk and I speculate that this is because a long-term turf war has broken out again in export control policy circles. Maury’s money is on the business side of that fight, and the narrowness of the AI rule gives weight to his views.

And here’s some Christmas cheer for DOJ and national security officials: A federal district court put a lump of coal in Fast Eddie Snowden’s stocking, denying him royalties from a book that violated his nondisclosure agreement. Nate thinks it’s safe for me to buy a copy, but I’m waiting for appellate confirmation.

Less festive news comes from the European Court of Justice’s advocate general opinion in Schrems II, a case that could greatly complicate EU-US data transfers by purporting to put Europeans in charge of how the US defends itself from terrorism. Maury explains; I complain.

David unpacks with clarity a complex Second Circuit decision on the constitutionality of FISA 702 collection. On the whole, Judge Lynch did a creditable job with a messy and unprecedented set of claims, though I question the wisdom of erecting a baroque mansion of judge-made limits on a slippery and narrow foundation like the Fourth Amendment’s requirement that searches be “reasonable.”

Finally, to put everyone back in the Christmas spirit, LabMD won nearly a million dollars in fees from the Federal Trade Commission for the FTC’s bullheaded pursuit of the company despite the many flaws in its case. The master’s opinion makes clear just how badly the FTC erred in hounding LabMD.

As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect those of their spouses, children, clients, firms, or institutions.

from Latest – Reason.com https://ift.tt/3a6ZXMg

via IFTTT

A senator from Vermont recently proposed a total ban on cellphone use for anyone under 21-years-old. Democratic Sen. John Rodgers says that he is sponsoring the bill because “cellphones are just as dangerous as guns.”

While Rodgers says that he knows the bill will not make it past the judiciary committee, he is using the effort to draw a comparison between cellphones and firearms, which are illegal for anyone under the age of 21 to purchase in the state of Vermont.

“I’m not going to push for the bill to pass. I wouldn’t vote for the thing. This is just to make a point,” Rodgers said, according toCNN.

The text of the bill reads:

“It is clear that persons under 21 years of age are not developmentally mature enough to safely possess them.“

If the bill ever were actually voted into law violations could result in fines of up to $1,000 – or even up to a year in prison.

Rodgers said that he established the bill to intentionally parallel Vermont’s gun legislation. In the bill Rodgers references the dangers of texting and driving and calls attention to how the problems of bullying have evolved in the social media age. He even suggested that cellphones have played a role in mass shootings.

“The Internet and social media, accessed primarily through cellphones, are used to radicalize and recruit terrorists, fascists, and other extremists,” the text of the bill read.

When Vermont constituents reacted with understandable anger, Rodgers insisted that his bill was intended as somewhat of a troll which was intended to highlight the importance of the 2nd amendment.

“I think people need to think about what liberties they’re willing to give up for safety. My position is that no good can come from taking rights from good people,” Rogers said.

“People in rural areas are largely independent, and we take it upon ourselves to stay safe. Without the Second Amendment, we couldn’t do that,” he added.

There’s a fine line between legislation addressing deepfakes and legislation that is itself a deep fake. Nate Jones reports on the only federal legislation addressing the deepfake problem so far. I claim that it is well short of a serious regulatory effort – and pretty close to a fake itself.

In contrast, India seems serious about imposing liability on companies whose unbreakable end-to-end crypto causes harm, at least to judge from the howls of the usual defenders of such products. David Kris explains how the law will work. I ask why Silicon Valley gets to impose the externalities of encryption-facilitated crime on society when we’d never let Big Tech leave us with the tab for water or air pollution just because their products are so cool. In related news, the FBI may be turning the Pensacola military terrorism attack into a slow-motion replay of its San Bernardino fight with Apple, this time with more top cover (and probably better lawyering).

Poor Nate seems to draw all the fake legislation in this episode. He explains a 2020 appropriations rider requiring the State Department to report on how it issues export licenses for cyber espionage capabilities; this is a follow-up to investigative reporting on the way such capabilities ended up being used against human rights activists in the UAE. As we agree, it’s an interesting and likely unsolvable policy problem, so the legislation opts for the most meaningless of remedies, requiring the Directorate of Defense Trade Control to report “on cybertools and capabilities licensing, including licensing screening and approval procedures as well as compliance and enforcement mechanisms” within 90 days.

Nate also gets to cover some decidedly un-fake requirements in the 2019 NDAA limiting how defense contractors can use Chinese technology. The other shoe is about to drop, and if the first one was a baby shoe, the second is a Clydesdale’s horseshoe.

It’s hard to call it fake, but the latest export control rule restricting sales of AI could hardly be narrower. Maury Shenk and I speculate that this is because a long-term turf war has broken out again in export control policy circles. Maury’s money is on the business side of that fight, and the narrowness of the AI rule gives weight to his views.

And here’s some Christmas cheer for DOJ and national security officials: A federal district court put a lump of coal in Fast Eddie Snowden’s stocking, denying him royalties from a book that violated his nondisclosure agreement. Nate thinks it’s safe for me to buy a copy, but I’m waiting for appellate confirmation.

Less festive news comes from the European Court of Justice’s advocate general opinion in Schrems II, a case that could greatly complicate EU-US data transfers by purporting to put Europeans in charge of how the US defends itself from terrorism. Maury explains; I complain.

David unpacks with clarity a complex Second Circuit decision on the constitutionality of FISA 702 collection. On the whole, Judge Lynch did a creditable job with a messy and unprecedented set of claims, though I question the wisdom of erecting a baroque mansion of judge-made limits on a slippery and narrow foundation like the Fourth Amendment’s requirement that searches be “reasonable.”

Finally, to put everyone back in the Christmas spirit, LabMD won nearly a million dollars in fees from the Federal Trade Commission for the FTC’s bullheaded pursuit of the company despite the many flaws in its case. The master’s opinion makes clear just how badly the FTC erred in hounding LabMD.

As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect those of their spouses, children, clients, firms, or institutions.

from Latest – Reason.com https://ift.tt/3a6ZXMg

via IFTTT

Mueller Probe Witness Faces 30 Years In Jail After Guilty Plea To Second Child Porn Charge

Having been previously convicted of transporting child pornography in 1991, George Nader, a Lebanese-American businessman who served as a witness in special counsel Robert Mueller’s investigation, pleaded guilty to two charges relating to sexual exploitation of children on Monday, according to The Washington Post.

As we detailed in July 2019 when Nader was indicted, Mueller’s team discovered child pornography on his phone while interviewing him about a meeting between Blackwater founder Erik Prince, the brother of Education Secretary Betsy DeVos, and a high-level Russian official with ties to President Vladimir Putin, according to WaPo.

Soon after the images were discovered, prosecutors reportedly filed a criminal complaint against Nader over the images, but they kept the charges under seal, and Nader’s lawyers were never informed of his impending arrest all the while that he continued to cooperate with the Mueller probe.

That means Mueller kept a suspected child abuser and pornographer on the streets while it used him as a witness. And when Nader was no longer useful, he was finally being charged.

Nader has claimed the images were not child pornography but admitted to having received an email including violent sexual images of infants in 2012.

WaPo details the disgusting acts of this key Mueller witness, noting that according to Czech court documents, he paid at least five teenage boys to engage in sex acts, four of whom were under 15.

He engaged them through a boy he met at a Prague arcade, who said he “knew lots of boys who had been in elementary school with him who would be interested.”

Nader enticed the boys with “money, jewelry, mobile telephones, clothing, care and housing,” according to the court record, and took some to the city’s annual Matthew’s Fair.

While the serial pedophile’s charges carry a maximum penalty of 30 years, prosecutors (for reasons that are simply beyond our ken) in the Eastern District of Virginia agreed to recommend the mandatory minimum of 10 years.

Sentencing is set for April 10.

Additionally, as we reported previously, Nader was indicted in December on charges of illegally funneling campaign funds to Hillary Clinton’s 2016 campaign using straw donors, according to Politico.

Our favorite bank portfolio holding, U.S. Bancorp (NYSE:USB), closed Friday at 1.87x book value, down about 5% from the peak in December just over $60 and 2x book. Still a little too rich to add more to our portfolio of USB common, but we continue to accumulate a number of bank preferred issues. With the number of profitless unicorns dying at an accelerating rate, steady cash flow has a certain appeal right about now.

More important, credit default swap (CDS) spreads for high quality issuers are also at all time lows. JPMorganChase (NYSE:JPM) is inside 40bp or around a “A” rating for the largest bank in the US. In 2015, JPM’s CDS was trading close to 120bp over sovereign swaps. Question is, does the market know, really, how much risk sits on Jamie Dimon’s books in the world of corporate CDS and more obscure credit products, like “transformation repo.” We think not.

For those not familiar with the wonders of OTC derivatives and collateral swapping, see our 2019 comment “HELOCs and Transformational REPO.” We wrote in March of last year: “The dealer bank trades corporate debt for cash (for a fee), but uses its own government or agency collateral to meet the margin call for the customer. The bank holds the crap and all of the market and credit risk – sometimes for its own book, sometimes for clients. Tales of MF Global. Recall that the margin rules in Dodd-Frank and other laws and regulations around the world are meant to increase the proverbial “skin in da game” for swaps customers, especially the non-bank customers of banks.”

Outgoing Bank of England governor Mark Carney worries that the global economy is heading towards a “liquidity trap” that would undermine central banks’ efforts to avoid a future recession, according to the Financial Times. Former Fed Chairman Benjamin “QE” Bernanke is screaming for new fiscal policy measures to combat a non-existent recession – this as the negative after effects of “quantitative” monetary policy measures are growing.

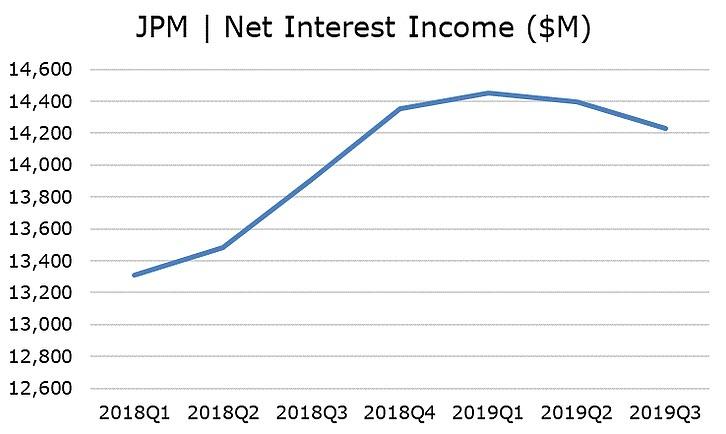

These central banksters may be right, but to us the bigger question is the unrecognized threat to the financial system from underpriced long-credit positions embedded on the balance sheets of global banks and bond funds. Bank interest earnings have long been subsidized by QE, but now banks are being squeezed by the same forces of market manipulation as credit starts to roll over. Suffice to say that the Street seems to finally understand that bank earnings are going to be a tad light, again, this quarter, due to the hangover from Uncle Ben’s QE electric KoolAid. The chart below shows net interest income for JPM.

Source: FFIEC

Despite the rosy economic outlook, bears continue to see reasons for despair in the world of credit – and we agree. The repo market sailed through year-end cushioned on a soft pillow of liquidity provided by Federal Open Market Committee. With the Fed announcing an end to the not-QE liquidity injection operations, though, we look forward to the next learning-by-doing adventure from Federal Reserve Chairman Jerome Powell.

Should the repo markets again start to seize up when the Fed ends its extraordinary liquidity injections, then Chairman Powell’s job may actually be on the line – and not because of President Donald Trump. The looming threat to Powell and other members of the FOMC is the tightly coiled but largely invisible long credit/short put positions on the books of major banks. This is a largely hidden risk that arises from years of market manipulation by global central banks. But hold that thought…

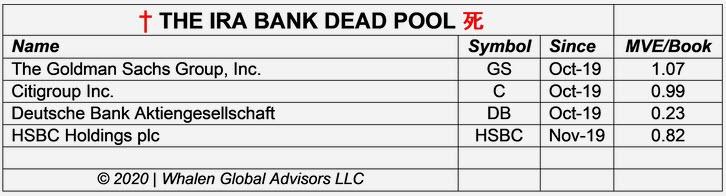

“We assign a negative outlook to DB and have little expectation that the situation will change in the near term. In our view, the most promising way to resolve what is an increasingly precarious situation would be for DB to sell its US operations in their entirety and wind up the remaining bank operations. Since Germany political leaders refuse to consider such a possibility, we expect that DB will stagger along, depleting capital and creating outsized risks, until such time as the bank’s poor management makes a mistake of sufficient magnitude to cause the bank to fail.”

Just to review, DB is one of four value destroyers in The IRA Bank Dead Pool. Banks that are members of the IRA Dead Bank Pool have poor financial performance, inferior equity market valuations and no apparent plan to correct these deficiencies. Even with US financials at the highest equity market valuations in a decade, the four institutions in the IRA Dead Pool – DB, Goldman Sachs (NYSE:GS), Citigroup (NYSE:C) and HSBC Holdings (NYSE:HSBC) – all trade at or below book value. DB has the lowest multiple of equity price to book value of any major bank.

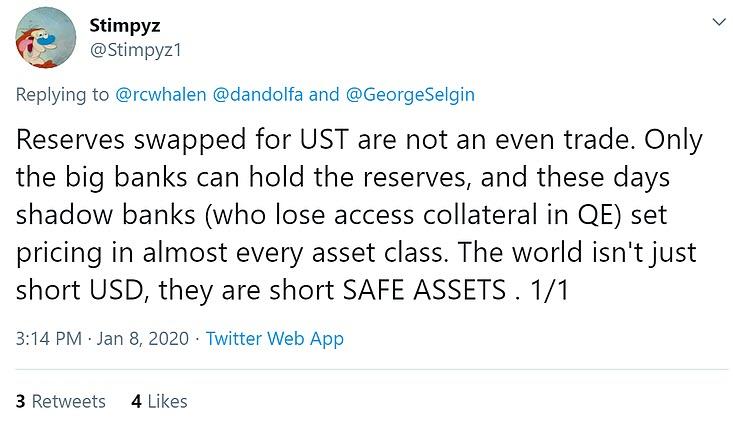

In a recent twitter post, our pal @Stimpyz1 reminds us that negative interest rates are not the only source of risk to global banks.

“Deutsche bank might be in the crosshairs, but don’t forget HSBC,” he avers. “Hong Kong is looking like a black hole, and HSBC exposure to real estate on the island makes the DB balance sheet look like Microsoft.”

Like DB, HSBC’s US operations are in pretty bad shape, with years of credit losses and poor operational performance. Once upon a time, HSBC was a good comp for Citigroup, but today we would not even bother running the numbers. But when it comes to risk, we are far more focused on the bond market than banks, which are generally under-leveraged but contain a lot of undisclosed credit risk.

The lingering negative effect of the Bernanke-Yellen monetary benevolence is so pronounced in fixed income that a number of institutional managers we know have begun to lighten up on investment grade (IG) exposures based on the belief that a ratings-driven correction is coming. Michael Carrion of TCW wrote before the holiday:

“Much ink has been spilled this year on the topic of how strong the technicals are within the investment grade credit market and for good reason as they have been the dominant underlying driver of overall IG spreads all year. The resurgent strength derives from this year’s re-expansion of central bank balance sheets, which has resulted in a relentless supply/demand imbalance for IG bonds. Demand for IG credit reached a year-to-date peak in November, particularly in the second half of month as the pace of primary market new issuance slowed.”

Patti Domm of CNBC, quoting a research report from Hans Mikkelsen, head of investment grade corporate strategy at BofA Securities, wrote after the close on Friday: “Lured by low rates, companies issue high grade debt at one of the fastest paces ever this week,” this as interest rates touched a three-year low. The combination of market reaction to political uncertainty and central bank purchases of risk-free debt has created a credit trap for global banks and bond investors.

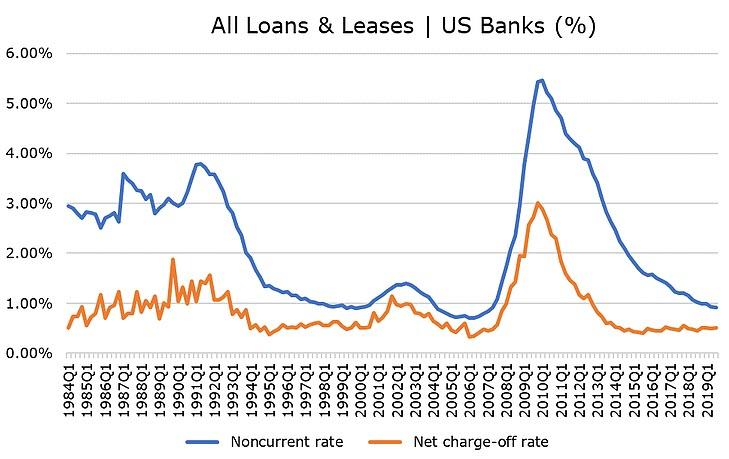

One of the things we learned from our colleague Dennis Santiago years ago at Institutional Risk Analytics is that when a credit spread looks to good to be true, it probably is. In those days, we’d convert the apparent default rate of a bank portfolio into a bond rating equivalent, then look at loss given default (LGD) to try to figure out how much the rate was understated. Today LGDs in the real estate sector are so skewed as to suggest that default rates are understated by at least 100%.

At the end of Q3 2019, the implied rating on the 0.51% of gross defaults for the $10.5 trillion in loans held by all US banks mapped to a “BBB” rating using the S&P default scale. If you believe that the aggregate rating of all obligors of US banks is investment grade, then we have some WeWork shares we’d like to sell you. Step right up.

Source: FDIC

The issuance of IG debt has set new records for the past several years, but most of this paper is clustered around “BBB” ratings. This suggests that the proverbial lemmings could fall off of the ratings cliff with little or no notice. As we all hopefully learned in the Adam McKay film “Big Short,” the major credit rating agencies don’t have the capacity or the courage to react quickly as and when economic and/or market conditions dictate a change for dozens of issuers. The investors that own long positions in underpriced corporate risk positions will be long dead before the ratings change.

The potential ratings volatility embedded in corporate debt has huge implications for banks, which have been “transforming” crap collateral into high IG in order to partially satiate the investor demand for low- or no-risk paper. TCW confirms our earlier colloquy with @Stimpyz1 on Twitter the other day:

This implies that there is an embedded credit put on the books of a lot of banks and funds as and when the QE party well and truly ends. Perhaps this is why John Carney and Ben Bernanke are so insistent of a shift to fiscal stimulus. But it needs to be said that no amount of fiscal push will fix the credit risk that the Fed and other central banks have created via “quantitative easing.”

We’ve been talking about the misalignment of credit ratings and corporate fundamentals for the past several years, but the continuation of QE in Europe and Asia has managed to prevent a reversion to the valuation mean. The divergence seen in junk rated collateral sold into collateralized loan obligations (CLOs) and superior credits suggests to us that an adjustment may finally be underway. The inferior assets always fall first. And to recall John Kenneth Galbraith’s great book about the 1920s: “Genius comes after the fall.”

While interest rate movements are suppressing net interest margins at major US banks, the prospect of a wholesale slip below investment grade for literally hundreds of weak bond issuers may be a far more worrisome problem. Bad ratings concealed the true risk in billions of dollars-worth of mortgage backed securities prior to the 2008 crisis. The new area for securities fraud and ratings malfeasance is the corporate bond market. If you think the liquidity problems we saw last summer in plain vanilla repo were bad, imagine what happens when margin calls on collateral swaps start to swamp the dealer banks.

California’s homeless population keeps skyrocketing, and so has the number of bills aiming at solving the homelessness problem. Last week, Gov. Gavin Newsom unveiled a billion-dollar plan designed to get more houses built for those who need it. But even that much money isn’t likely to help many people if the underlying problem remains unchanged. To solve California’s homelessness problem, you have to address inflexible zoning rules and ineffective municipal bureaucracies.

Newsom’s executive order allocates $750 million to build more affordable housing units and to establish a California Access to Housing and Services Fund within the state’s Department of Social Services. The goal is to pay rent for individuals facing homelessness and to make vacant state properties available immediately as shelter options. An additional $695 million will be used to boost preventative health care measures for the homeless through Medi-Cal Healthier California for All.

This follows 18 housing bills that Newsom signed into law last fall. The bills are supposed to accelerate housing production, but they don’t have much teeth. They require local jurisdictions to publicly share information about zoning ordinances and other building rules—not to roll the regs back, just to be more transparent about them. They also ask cities and counties to maintain an inventory of state surplus land sites suitable for residential development.

California voters also approved $4 billion in bonds last year for affordable housing programs.

“You can’t just throw money at homelessness and a lack of affordable housing and expect that you’re going to achieve the result that you’re hoping to achieve,” says David Wolfe, legislative director of the Howard Jarvis Taxpayers Association. After all, it hasn’t worked so far.

California is home to almost half of America’s homeless population, and the median price for a house there is more than twice the national level. Fixing that problem means building more houses, but zoning laws and anti-development activism make that difficult. Serious reform will require moves like modifying city codes to let developers build units that aren’t single-family homes. And dialing back rules, such as the California Environmental Quality Act, that let neighborhood activists block new construction with faux-environmental concerns. And, in general, clearing away the thicket of state and local regulations that get in the way of meeting the demand for housing.

“If you’re a city council,” San Francisco Assemblyman Phil Ting toldCurbed San Francisco, “the people who vote for you oppose the housing you’re creating, and you’re creating housing for the people who have yet to move in.”

Californians also have to contend with a perverse incentive built into Proposition 13, a measure that limits property-tax increases on homes until they’re sold. This gives cities a reason to encourage commercial instead of residential development.

As legislators continue to pour money into housing programs, perhaps they should think more about how to address the broken system responsible for the mess. In the meantime, others will look for ways to route around the system. Silicon Valley giants have begun to propose their own housing projects, underscoring the state government’s inability to move forwards with its own reforms.

from Latest – Reason.com https://ift.tt/3a15ofD

via IFTTT

US Budget Deficit Blows Out To Nine Year High In First Quarter Of Fiscal 2020

The gaping US budget deficit hole is getting bigger with each passing month.

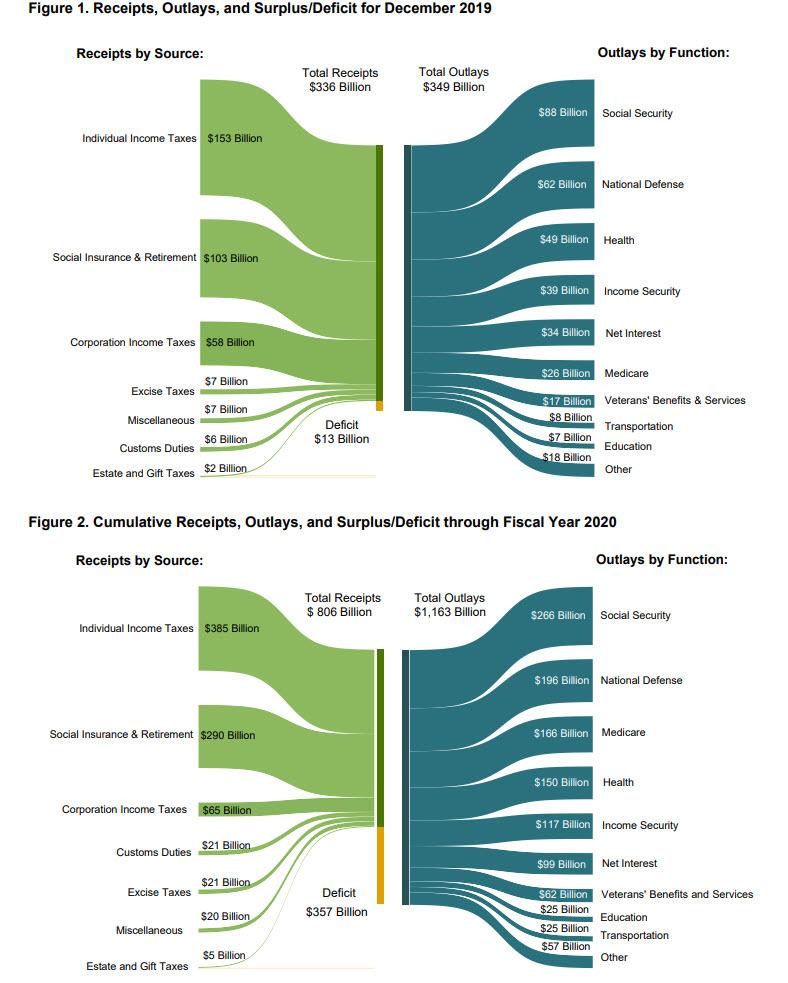

Earlier today, the US Treasury announced that in December (the third month of fiscal 2020), the US spent $13.3 billion more than it pulled in, and while the month’s budget deficit was modestly better than the $15 billion expected, it was virtually unchanged from the $13.5BN deficit recorded in Dec 2018.

Total December spending of $349billion, was 7.5% higher than a year earlier, with the biggest outlays for the month as follows: social security ($88BN), national defense ($62BN), Health ($49BN), Income Security ($39BN), Net Interest ($34BN), which was more than Medicare spending for the month ($26BN) and so forth. Meanwhile, receipts increased by an almost identical amount, rising 7.4% from $312.6BN to $335.8BN, thanks to $153BN in individual income taxes, $103BN in Social insurance and retirement receipts, and $58BN in corporate income taxes.

For the first three months of fiscal 2020, total Outlays rose to $1,163BN while Receipts were a far more modest $806BN, as broken out in the chart below.

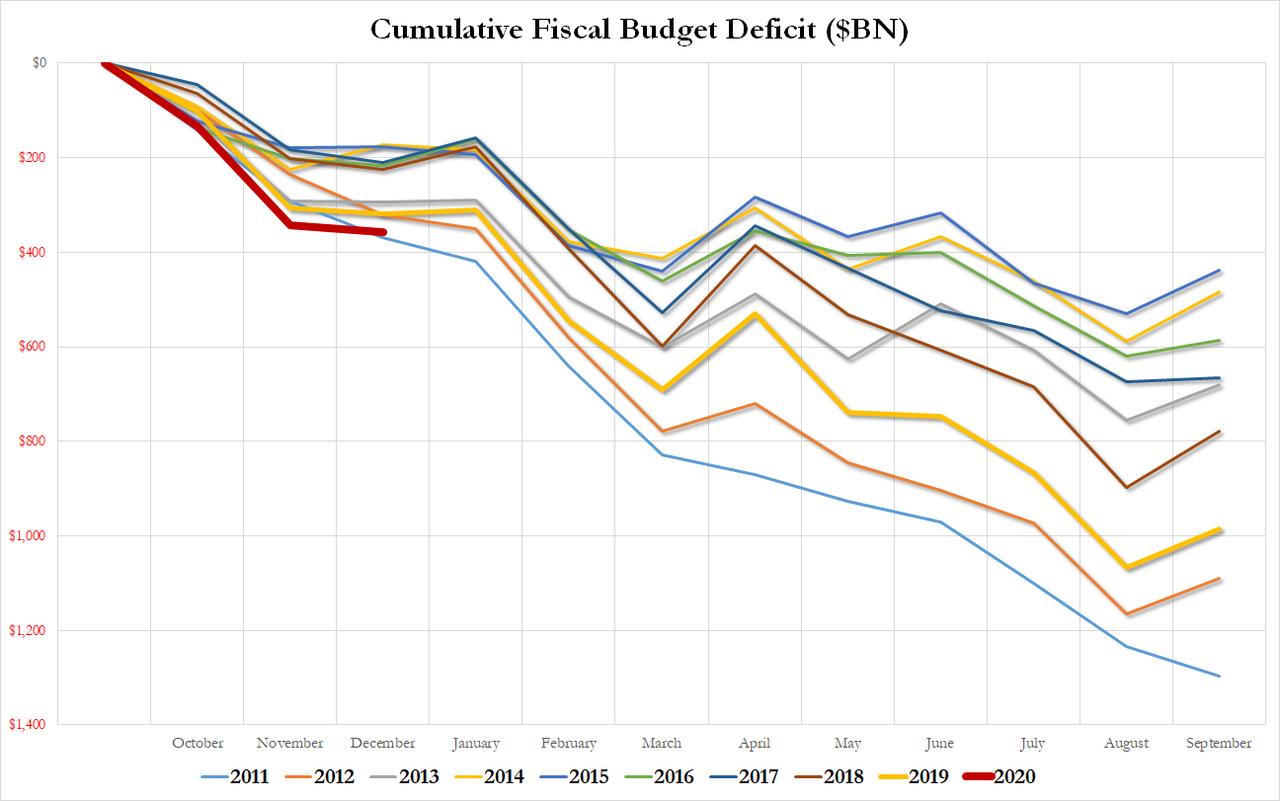

This means that the cumulative deficit for the first three months of the year has surged to $357BN.

It also means that the deficit after one quarter of fiscal 2020 is now in the history books, was the widest going back all the way to 2011, when the US was still spending like a drunken sailor under President Obama, in response to the financial crisis, and when the final deficit for the full year soared to $1.3 trillion.

And while in 2020 nobody is predicting a full-year hole as big as 2011’s, with every passing month we get closed to a number hinting that the US is spending as if it is emerging from a recession and a major economic crisis. That, or it is about to enter one. One more thing to keep in mind: if it wasn’t for $21BN in customs duties collected mostly from China as a result of the trade war tariffs, the cumulative US budget deficit through December would be even worse than that in 2011.

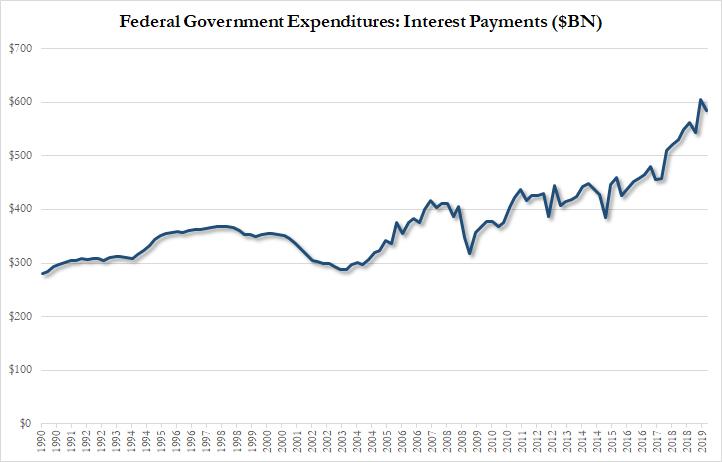

One final point: with US debt recently surpassing $23 trillion, it is no surprise that interest expense on this debt has also pushed to all time highs, and in the latest quarter it stabilized just shy of the prior record, dipping modestly to $585 billion, roughly double where its average for the two decade period from 1990 to 2010, at which point it soared. One can only imagine what the interest expense will be if and when rates are ever allowed to normalize.

But the actual demise of the authoritarian regime that’s been in power since 1979 will come more from acts like the one taken by Kimia Alizadeh, Iran’s only female Olympic medalist. Late last week, the bronze medalist in Taekwondo in the 2016 Summer Games announced via Instagram that she has fled her home country due to the systematic oppression of women. Via CNN:

“Let me start with a greeting, a farewell or condolences,” the 21-year-old wrote in an Instagram post explaining why she was defecting. “I am one of the millions of oppressed women in Iran who they have been playing with for years.”…

“They took me wherever they wanted. I wore whatever they said. Every sentence they ordered me to say, I repeated. Whenever they saw fit, they exploited me,” she wrote, adding that credit for her success always went to those in charge.

“I wasn’t important to them. None of us mattered to them, we were tools,” Alizadeh added, explaining that while the regime celebrated her medals, it criticized the sport she had chosen: “The virtue of a woman is not to stretch her legs!”

On the heels of Alizadeh’s self-imposed exile comes reports that two anchors for Iranian state broadcaster IRIB have quit over qualms about censorship and official lies. From The Guardian:

Zahra Khatami quit her role at IRIB, saying: “Thank you for accepting me as anchor until today. I will never get back to TV. Forgive me.”

Her fellow anchor Saba Rad said: “Thank you for your support in all years of my career. I announce that after 21 years working in radio and tv, I cannot continue my work in the media. I cannot.”

The journalists’ statements are part of a crisis of confidence following the initial attempts by state officials to deny that Ukrainian jetliner 752 had been shot down by mistake by members of the Islamic Revolutionary Guards Corp (IRGC) air defence force.

A third broadcaster, Gelare Jabbari, said she quit “some time ago” and asked Iranians to “forgive me for the 13 years I told you lies.”

This is all happening against the backdrop of massive protests in Iran following the accidental shooting down of a Ukrainian airliner that carried 176 people. Demonstrators protested rising gas prices late last year and in the years prior, there have been other protests and general strikes for a host of reasons, including increased dissatisfaction with theocratic rule. According to a Carnegie Endowment report, 150,000 educated Iranians emigrate each year, “costing the country over $150 billion per year” as relatively young and motivated residents leave for greener pastures elsewhere.

By all accounts, sanctions imposed by the United States in 2018 have hit Iran’s economy extremely hard and are playing a role in sparking protests. It’s never fully clear how those sorts of intervention, much less more militaristic actions such as the killing of Soleimani, play out—sometimes overt pressure applied by an outside power emboldens dissent and sometimes it decreases it. But when a country starts to get hollowed out from within, as seems to be the case with Alizadeh’s exile and other recent and ongoing domestic developments, autocrats should start sweating.

from Latest – Reason.com https://ift.tt/30iaShl

via IFTTT

California’s homeless population keeps skyrocketing, and so has the number of bills aiming at solving the homelessness problem. Last week, Gov. Gavin Newsom unveiled a billion-dollar plan designed to get more houses built for those who need it. But even that much money isn’t likely to help many people if the underlying problem remains unchanged. To solve California’s homelessness problem, you have to address inflexible zoning rules and ineffective municipal bureaucracies.

Newsom’s executive order allocates $750 million to build more affordable housing units and to establish a California Access to Housing and Services Fund within the state’s Department of Social Services. The goal is to pay rent for individuals facing homelessness and to make vacant state properties available immediately as shelter options. An additional $695 million will be used to boost preventative health care measures for the homeless through Medi-Cal Healthier California for All.

This follows 18 housing bills that Newsom signed into law last fall. The bills are supposed to accelerate housing production, but they don’t have much teeth. They require local jurisdictions to publicly share information about zoning ordinances and other building rules—not to roll the regs back, just to be more transparent about them. They also ask cities and counties to maintain an inventory of state surplus land sites suitable for residential development.

California voters also approved $4 billion in bonds last year for affordable housing programs.

“You can’t just throw money at homelessness and a lack of affordable housing and expect that you’re going to achieve the result that you’re hoping to achieve,” says David Wolfe, legislative director of the Howard Jarvis Taxpayers Association. After all, it hasn’t worked so far.

California is home to almost half of America’s homeless population, and the median price for a house there is more than twice the national level. Fixing that problem means building more houses, but zoning laws and anti-development activism make that difficult. Serious reform will require moves like modifying city codes to let developers build units that aren’t single-family homes. And dialing back rules, such as the California Environmental Quality Act, that let neighborhood activists block new construction with faux-environmental concerns. And, in general, clearing away the thicket of state and local regulations that get in the way of meeting the demand for housing.

“If you’re a city council,” San Francisco Assemblyman Phil Ting toldCurbed San Francisco, “the people who vote for you oppose the housing you’re creating, and you’re creating housing for the people who have yet to move in.”

Californians also have to contend with a perverse incentive built into Proposition 13, a measure that limits property-tax increases on homes until they’re sold. This gives cities a reason to encourage commercial instead of residential development.

As legislators continue to pour money into housing programs, perhaps they should think more about how to address the broken system responsible for the mess. In the meantime, others will look for ways to route around the system. Silicon Valley giants have begun to propose their own housing projects, underscoring the state government’s inability to move forwards with its own reforms.

from Latest – Reason.com https://ift.tt/3a15ofD

via IFTTT