NBC is reporting that President Donald Trump was mulling the hit on Iranian Maj. Gen. Qassem Soleimani seven months ago, with war hawks such as John Bolton urging him to go for it. This further erodes the administration’s claim that the assassination was done to stop an “imminent” attack on U.S. lives.

“According to five current and senior administration officials,” NBC reports, Trump gave the order in June 2019, “with the condition that Trump would have final signoff on any specific operation to kill Soleimani.” Trump said that signoff would come if any Americans were killed, their sources said, which “explains why assassinating Soleimani was on the menu of options that the military presented to Trump two weeks ago for responding to an attack by Iranian proxies in Iraq.” That proxy attack killed a U.S. contractor.

The strike was carried out on January 3. Secretary of State Mike Pompeo quickly and repeatedly attributed it not to retribution but to an alleged imminent threat to dozens (sometimes “hundreds”) of American lives.

The killing looked like something former National Security Advisor John Bolton would have hatced, but Bolton has been gone since September. Now it seems that Bolton’s imprint may have been on this operation after all. From NBC:

After Iran shot down a U.S. drone in June, John Bolton, Trump’s national security adviser at the time, urged Trump to retaliate by signing off on an operation to kill Soleimani, officials said. Secretary of State Mike Pompeo also wanted Trump to authorize the assassination, officials said.

Yesterday, Defense Secretary Mark Esper told Face the Nation that he knew of no “specific evidence” to support the claim that Iran was planning embassy attacks. Rep. Justin Amash (I–Mich.) has been blasting the Trump administration for continuing to push this story:

The administration didn’t present evidence to Congress regarding even one embassy. The four embassies claim seems to be totally made up. And they have never presented evidence of imminence—a necessary condition to act without congressional approval—with respect to any of this. https://t.co/Eg0vaCnqFd

Anti-Catholic law in Montana comes to Supreme Court. When it considers Espinoza v. Montana Department of Revenuelater this month, the U.S. Supreme Court “has the opportunity to do more than just settle the fate of one controversial tax credit; it could also junk Montana’s Blaine Amendment, finding it in violation of the Constitution’s religious-freedom and equal-protection clauses,” writes Nick Sibilla at The Atlantic. “In doing so, it would set a strong precedent against any law born of bigotry.”

The case concerns “a modest tax-credit scholarship program in Montana,” notes Sibilla, but it “could have major ramifications for educational-choice programs across America, which help nearly half a million students attend private schools.”

FREE MARKETS

Times editorial board lays out plans to “fortify” the FDA. On Sunday, the New York Times editorial board praised the Food and Drug Administration while worrying over its (lack of) leadership and admitting that it often fails. Its proposed solutions for “fortifying” the agency? Giving it even more power, of course. (Sigh.) To fix the FDA’s flaws, the paper claims, “the agency needs to be made stronger, not weaker.”

“Fortunately,” they write, “options for fortifying the F.D.A. abound”:

For instance, laws that would make it easier for regulators to police the cosmetics industry and to hold medical device companies to account have been floating through Congress for years. A group of former F.D.A. commissioners last year proposed an even bolder fix: Restore the agency’s autonomy by extracting it from the Department of Health and Human Services. The F.D.A.’s decisions used to be final, but for decades now they have been subject to layers of political interference. Making the agency independent, as the Federal Reserve and the Social Security Administration are, could help reverse that trend.

ELECTION 2020

Vermin Supreme won the New Hampshire Libertarian Party convention’s pick for the party’s presidential nomination.Heavyexplains what this means:

The Libertarian Party hosts a series of primaries and caucuses where non-binding votes are cast, indicating a state party’s preference for its presidential candidate. These preferences are not binding and delegates who are sent to the national convention can vote for whichever candidate they prefer. New Hampshire had the first primary. This self-funded presidential preference primary was actually conducted by mail, with results announced on January 11….

So the voting of Vermin Supreme was a statement of preference, but it does not bind the delegates when they vote at the national convention on May 21-25, 2020 in Austin, Texas.

Presumably, it’s a picture from earlier last week, when it did snow, although the conspiracy theorists of Twitter are having a field day:

I don’t want to sound like Alex Jones here but is this some sort of secret communication? Racking my brain to make any sort of sense of this. It nearly hit 70 degrees in DC today. https://t.co/aLwOz5HKVD

Now that we have an open admission from the Fed that their balance sheet expansion is exacerbating asset prices and creating excess and imbalances (see Ghosts of 2000) the term bubble can no longer be dismissed as some fringe rantings by cranks like me, but rather a recognition for what any bubble is: An overpricing of asset prices far above where they should be based on earnings, fundamentals or the growth basis of the economy.

The question on everybody’s mind of course: When does the rally end, when will the bubble get popped? You know it’s bad when even bulls call for corrections but can’t get any. In December what seemed an aggressive call for 3,333 $SPX by March 3rd by BAML already looks overly conservative as $SPX got within a stone’s throw of 3,300 on January 10.

Current sentiment:

And that’s the sentiment in every bubble. Until it pops.

But for now there’s little doubt that the Fed’s liquidity machine maintains full control over the asset price inflation equation seeing again multiple daily repo operations this week in the $70B to $100B range.

Yet this week also offered an example of how quickly the bid can disappear.

You couldn’t tell by the $VIX closing at 12.56 at the end of the week, nor by the cash charts, but this week was actually pretty wild:

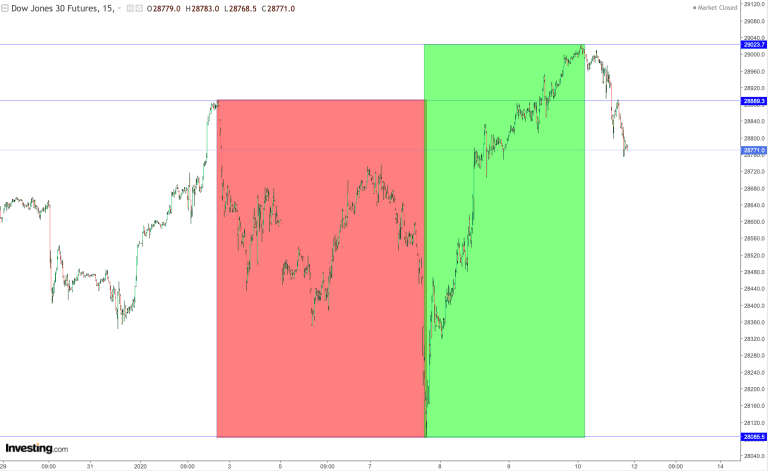

An 800 point drop in the $DJIA followed by a 1,000 point rally.

While all focus was on the again swift recovery lost in the shuffle was how quickly markets can drop out of the blue for any reason. Unprotected investors (as evidenced by extreme low put/call ratios and the lowest $SPY short position since January 2018) could take comfort in that the aggressive drop in overnight was erased in overnight and markets gapped up and raced higher in what can only be described as indiscriminate panic buying. Classic bubble behavior. The desperation to buy.

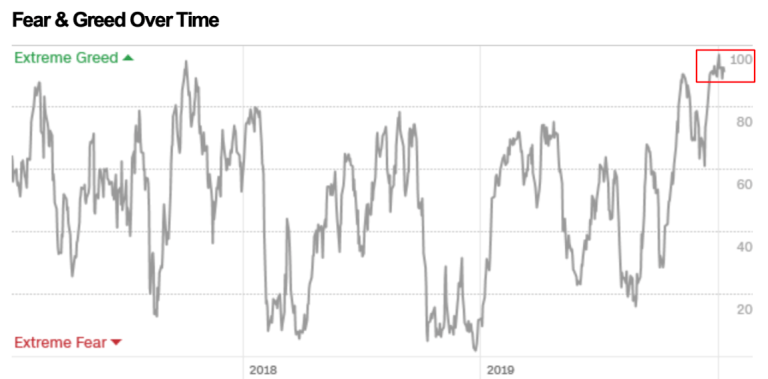

None of this is new. We’ve seen bubbles before that brought about major pain when the excess and imbalances were wrought out following a period of extreme greed and complacency.

And it’s fair to say that this the environment we’re in now as CNN’s fear and greed model appears to now have settled into what seems an unprecedented permanent full greed mode:

What can we learn from the bubbles of the past? What do the technicals suggest how this might unfold? What are the risks to the upside and downside?

Join me for the latest market review offering perspective on all of these questions:

* * *

To get notified of future videos feel free to subscribe to our YouTube Channel. For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

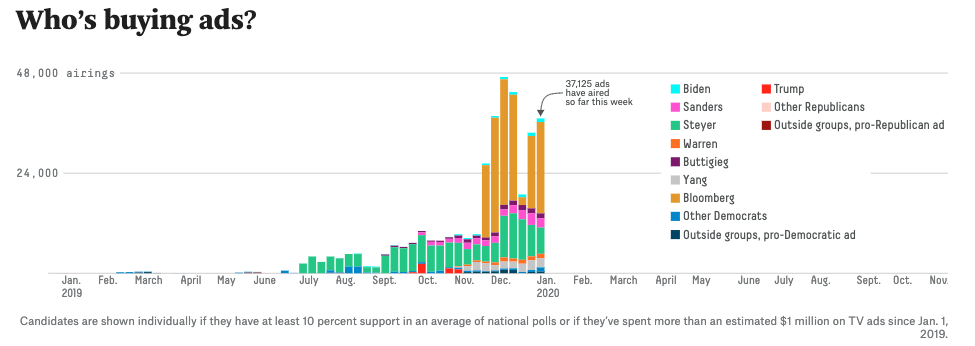

Having spent more money on ads than the rest of the Democrat field combined (as we noted , Bloomberg admitted over the weekend that he’s “spending all his money to beat Trump”, Mike Bloomberg’s media presence may be starting to get to President Trump.

Mini Mike Bloomberg is spending a lot of money on False Advertising.

I was the person who saved Pre-Existing Conditions in your Healthcare, you have it now, while at the same time winning the fight to rid you of the expensive, unfair and very unpopular Individual Mandate, and, if Republicans win in court and take back the House of Represenatives, your healthcare, that I have now brought to the best place in many years, will become the best ever, by far.

I will always protect your Pre-Existing Conditions, the Dems will not!

But Bloomberg (or rather his team we suspect), responded, calling for the president to address them directly next time…

Phase One And Done: Key Events In The Busy Week Ahead

With the market’s fascination with events in the middle east appears to be fading fast in the absence of any material escalation, the main highlights for the week ahead will be the signing of the Phase One trade deal between the US and China (Wednesday). Even though Steven Mnuchin said over the weekend that an English-language version of the agreement will be released this week, DB’s Jim Reid notes that it’s quite remarkable that we still don’t know much in the way of details so eyes will be on this.

We’ll also see the start of US earnings season with a number of banks reporting. On Tuesday we’ll hear from JPMorgan Chase, Wells Fargo and Citigroup. Then on Wednesday we’ll get Bank of America, UnitedHealth Group, Goldman Sachs, US Bancorp and BlackRock. Finally on Thursday, we’ll hear from Morgan Stanley and BNY Mellon.

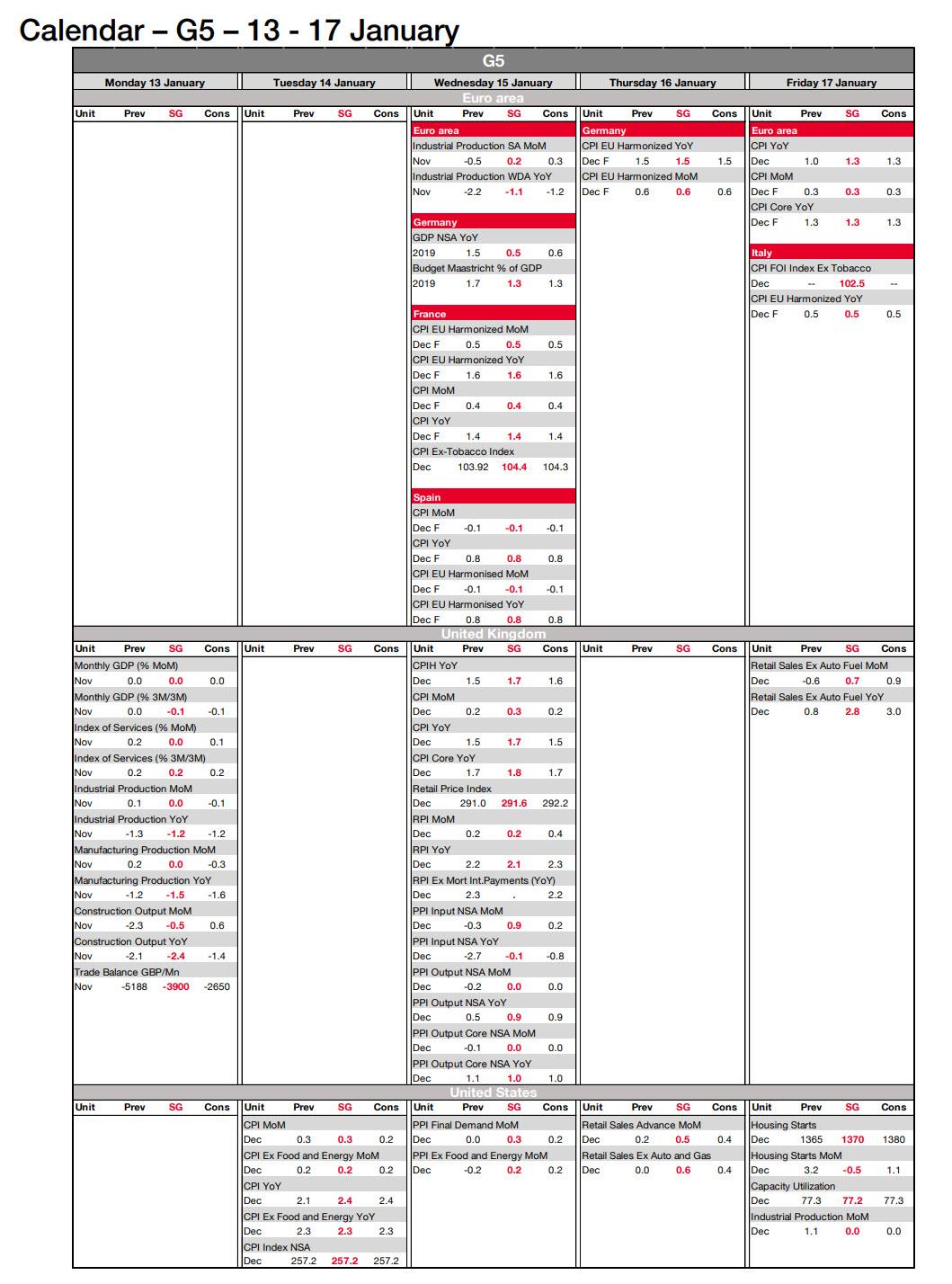

In terms of data CPI (Tuesday), retail sales (Thursday), and consumer confidence (Friday) are the main highlights in the US. In China we have trade data (Tuesday) and Q4 GDP/retail sales/industrial production (Friday). So we’ll have quite a good idea about momentum in the Chinese economy by the end of the week. In Europe industrial production numbers (Tuesday), and the flash CPI (Friday) are the highlights. The UK also sees CPI (Wednesday) and retail sales (Friday).

In terms of central banks over the coming week, publications to watch for include the Beige Book from the Fed on Wednesday, and then the ECB’s monetary policy account of its December meeting (and Christine Lagarde’s first as ECB President) on Thursday.

Over to politics now, and there’s a number of upcoming events this week. In the US, it’s the last Democratic primary debate on Tuesday before primary voting kicks off in February. Former Vice President Biden is currently ahead in the national polling according to the average on RealClear Politics. However, the polls in the first two states to vote in February, Iowa and New Hampshire, are much tighter, with the RealClear Politics average putting the 3 top candidates in Iowa between 20% and 22%, so it’s a tight race going into the caucuses there on 3rd February.

A Des Moines Register/Mediacom/CNN poll out from Iowa (the first state to vote) put Senator Bernie Sanders in first place on 20%, a 5-point jump for Sanders since their last poll in November. Elizabeth Warren was in 2nd place on 17%, while Pete Buttigieg was on 16%, and Joe Biden on 15%. As discussed above, nationally Biden remains the frontrunner, but the big question will be whether he can maintain his momentum were he not to win either of the first 2 states. Given how quickly Warren’s support has fallen, and also the impressive rally in Sanders’s ratings over a relatively short period of time, its clear that it remains all to play for in this race.

Below is a day by day guide to the week ahead, courtesy of Deutsche Bank:

Monday

Data: UK November GDP, trade balance, industrial production, manufacturing production, US December monthly budget statement, Japan November current account balance

Central Banks: Fed’s Rosengren and Bostic speak

Politics: House of Lords begins debate on Brexit Withdrawal Agreement Bill, deadline for UK Labour leadership contenders to receive nominations from at least 10% of MPs and MEPs

Tuesday

Data: US December NFIB small business optimism index, December CPI, Japan December M2 money stock, M3 money stock, China December trade balance

Central Banks: ECB’s Mersch, Fed’s Williams and George speak

Politics: US Democratic primary debate

Earnings: JPMorgan Chase, Wells Fargo, Citigroup

Wednesday

Data: Japan preliminary December machine tool orders, France final December CPI, UK December CPI, RPI, PPI, Euro Area November industrial production, trade balance, US weekly MBA mortgage applications, US December PPI

Central Banks: BoJ’s Kuroda, ECB’s Holzmann, BoE’s Saunders and Fed’s Harker and Kaplan speak, Federal Reserve releases Beige Book

Earnings: Bank of America, UnitedHealth Group, Goldman Sachs, US Bancorp, BlackRock

Other: Signing of the US-China Phase One trade deal

Thursday

Data: EU27 December new car registrations, Germany final December CPI, US December retail sales, January Philadelphia Fed business outlook, weekly initial jobless claims, November business inventories, January NAHB housing market index, November net long-term TIC flows

Central Banks: Policy decisions from the Central Bank of Turkey and the South African Reserve Bank, monetary policy account of the ECB’s December meeting released

Earnings: Morgan Stanley, BNY Mellon

Friday

Data: China Q4 GDP, retail sales, industrial production, Japan November tertiary industry index, Euro Area November current account, Italy November trade balance, UK December retail sales, Euro Area December CPI, Canada November international securities transactions, US December building permits, housing starts, capacity utilisation, industrial production, preliminary January University of Michigan sentiment, November job openings

Central Banks: Policy decision from the Bank of Korea, Fed’s Harker speaks

Finally, looking at the key economic data releases in the US, Goldman notes that this week all eyes are on the CPI report on Tuesday and the retail sales report on Thursday. There are several scheduled speaking engagements by Fed officials this week.

Monday, January 13

10:00 AM Boston Fed President Rosengren (FOMC non-voter) speaks: Boston Fed President Eric Rosengren will speak at a Connecticut Business and Industry Association event in Hartford, Connecticut. Prepared text and audience Q&A are expected.

12:40 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will discuss the economic outlook and monetary policy with the Rotary Club of Atlanta. Audience and media Q&A are expected.

Tuesday, January 14

06:00 AM NFIB small business optimism, January (consensus 104.8, last 104.7)

08:30 AM CPI (mom), December (GS +0.33%, consensus +0.3%, last +0.3%); Core CPI (mom), December (GS +0.16%, consensus +0.2%, last +0.2%); CPI (yoy), December (GS +2.41%, consensus +2.4%, last +2.1%); Core CPI (yoy), December (GS +2.30%, consensus +2.3%, last +2.3%): We estimate a 0.16% increase in December core CPI (mom sa), which would leave the year-on-year rate unchanged at +2.3%. Our monthly core inflation forecast reflects a pullback in used car prices and a holiday-season-related decline in household furnishing prices. On the positive side, we expect a rebound in apparel and footwear prices reflecting residual seasonality and Nike price increases. We estimate a 0.33% increase in headline CPI (mom sa), mainly reflecting higher energy prices.

09:00 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will discuss behavioral science and organizational culture at an event organized by the Banking Standards Board, the New York Fed, and the London School of Economics. Prepared text and audience Q&A are expected.

1:00 PM Kansas City Fed President Esther George (FOMC non-voter) speaks: Kansas City Fed President Esther George will discuss the economic outlook and monetary policy at an event hosted by the Kansas City Fed. Audience Q&A is expected.

Wednesday, January 15

08:30 AM PPI final demand, December (GS +0.2%, consensus +0.2%, last flat); PPI ex-food and energy, December (GS +0.1%, consensus +0.2%, last -0.2%); PPI ex-food, energy, and trade, December (GS +0.1%, consensus +0.2%, last flat); We estimate that headline PPI increased 0.2% in December, reflecting stronger energy prices but somewhat softer core prices. We expect a 0.1% increase in the core measure excluding food and energy, and also a 0.1% increase in the core measure excluding food, energy, and trade.

08:30 AM Empire State manufacturing index, January (consensus +3.6, last +3.5)

11:00 AM Philadelphia Fed President Harker (FOMC voter) speaks; Philadelphia Fed President Patrick Harker will discuss “Monetary Policy Normalization: Low Interest Rates and the New Normal” at the Harvard Club of New York. Prepared text and audience Q&A are expected.

12:00 PM Dallas Fed President Kaplan (FOMC voter) speaks; Dallas Fed President Robert Kaplan will speak to the Economic Club of New York. Audience and media Q&A are expected.

02:00 PM Beige Book, January FOMC meeting period; The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. In the January Beige Book, we look for anecdotes related to growth, labor markets, wages, price inflation, and trade policy.

Thursday, January 16

08:30 AM Retail sales, December (GS +0.5%, consensus +0.3%, last +0.2%); Retail sales ex-auto, December (GS +0.6%, consensus +0.5%, last +0.1%); Retail sales ex-auto & gas, December (GS +0.5%, consensus +0.4%, last flat); Core retail sales, December (GS +0.5%, consensus +0.3%, last +0.1%): We estimate that core retail sales (ex-autos, gasoline, and building materials) increased 0.5% in December (mom sa), reflecting the solid monthly sales results of general merchandisers as well as a boost from the late Thanksgiving holiday, which may have shifted some holiday shopping into December. That being said, we believe uncertainty around this report is higher than usual, as the underlying cause of last December’s sharp and short-lived drop in retail spending remains unclear (potential explanations include the government shutdown, a particularly early Thanksgiving, and the secular trend towards earlier holiday shopping). We estimate a 0.5% increase in the headline measure in this week’s report, reflecting a rise in gas prices but a pullback in auto sales.

08:30 AM Philadelphia Fed manufacturing index, January (GS +4.4, consensus +3.1, last +2.4): We estimate that the Philadelphia Fed manufacturing index rebounded by 2.0pt to +4.4 in January after declining by 6.0pt in the prior month.

08:30 AM Initial jobless claims, week ended January 11 (GS 220k, consensus 217k, last 214k): Continuing jobless claims, week ended January 4 (last 1,803k); We estimate jobless claims ticked up 6k to 220k in the week that ended January 11. We expect a persistent winter seasonal bias to continue to exert upward pressure on the continuing claims measure between now and February.

08:30 AM Import price index, December (consensus +0.4%, last +0.2%)

10:00 AM Business inventories, November (consensus -0.1%, last +0.2%)

10:00 AM NAHB housing market index, January (consensus 74, last 76)

Friday, January 17

08:30 AM Housing starts, December (GS +2.5%, consensus +1.1%, last +3.2%); Building permits, December (consensus -1.5%, last +1.4%): We estimate housing starts increased by 2.5% in December. Our forecast incorporates stronger construction job growth but a drag from likely mean reversion in the noisy multifamily category.

09:00 AM Philadelphia Fed President Patrick Harker (FOMC voter) speaks: Philadelphia Fed President Patrick Harker will discuss the economic outlook at the New Jersey Bankers Association Leader Forum in Somerset, New Jersey. Prepared text and audience Q&A are expected.

09:15 AM Industrial production, December (GS -0.2%, consensus -0.1%, last +1.1%); Manufacturing production, December (GS flat, consensus +0.1%, last +1.1%); Capacity utilization, December (GS 77.0%, consensus 77.1%, last 77.3%): We estimate industrial production declined modestly in December, reflecting a pullback in the utilities category and a slight decrease in auto manufacturing. We estimate capacity utilization declined by three tenths in November to 77.0%.

10:00 AM University of Michigan consumer sentiment, January preliminary (GS 99.6, consensus 99.3, last 99.3): We expect University of Michigan consumer sentiment edged 0.3pt higher in the preliminary January reading to 99.6, reflecting increases in other confidence measures and higher stock prices.

10:00 AM JOLTS Job Openings, May (consensus 7,267k, last 7,267k)

The Trump Administration’s decision to include a citizenship question in the 2020 Census provoked substantial outrage. Many feared that inclusion of the question would depress response rates, leading to an inaccurate Census, and that it would produce a substantial undercount of people in immigrant communities, particularly in households containing noncitizens. Indeed, many suspected that was the whole point.

Fears of a significant undercount, and its consequent effects on political representation and the distribution of federal funds, prompted many states and interest groups to file suit against the Trump Administration. As the Supreme Court explained when it discussed the plaintiffs’ claim of standing to bring the suit:

Respondents assert a number of injuries—diminishment of political representation, loss of federal funds, degradation of census data, and diversion of resources—all of which turn on their expectation that reinstating a citizenship question will depress the census response rate and lead to an inaccurate population count. Several States with a disproportionate share of noncitizens, for example, anticipate losing a seat in Congress or qualifying for less federal funding if their populations are undercounted. . . .

Several state respondents here have shown that if noncitizen households are undercounted by as little as 2%—lower than the District Court’s 5.8% prediction—they will lose out on federal funds that are distributed on the basis of state population. . . .

Justice Breyer’s separate opinion also stressed the arbitrariness of including a question that would produce a less accurate enumeration of people within the country.

How can an agency support the decision to add a question to the short form, thereby risking a significant undercount of the population, on the ground that it will improve the accuracy of citizenship data, when in fact the evidence indicates that adding the question will harm the accuracy of citizenship data?

As readers know, the Court decided, 5-4, that inclusion of the citizenship question was unlawful because the Administration’s explanation for why the question was to be added seemed “contrived” and did not match the available evidence.

In 2019, the Census nonetheless conducted a significant test of the effects of including a citizenship question, and the results were not what anyone (including the Census’s own experts) expected, as documented in a recently released report. As noted by Lyman Stone, the report tells a quite different story about the effects of a citizenship question than that upon which the Census case was litigated.

In 2018, the U.S. Census Bureau decided to test the operational implications of a proposed question on citizenship status on the 2020 Census. In particular, experts and stakeholders raised concerns that such a question could depress self-response rates, increase cost, and reduce the quality of the 2020 population count. An indirect study by Census Bureau researchers predicted that “adding a citizenship question to the 2020 Census would lead to lower self-response rates in households potentially containing noncitizens…” compared to households with all citizens (Brown, Heggeness, Dorinski, Warren, & Yi, 2018). However, the authors recommended the ideal analysis would be to conduct a randomized controlled experiment to compare response rates on questionnaires with and without a citizenship question. . . .

The major finding of the 2019 Census Test was that there was no statistically significant difference in overall self-response rates between treatments. The test questionnaire with the citizenship question had a self-response rate of 51.5 percent; the test questionnaire without the citizenship question had a self-response rate of 52.0 percent. Although these results differ from the predicted rates in Brown’s et al. study, the results of the two studies are not

comparable since this study benefits from the randomized controlled design, which isolates the treatment effect.

The Report also found statistically significant declines in response rates among some areas and among subgroups, including areas where more than are 4.9 percent noncitizens or more than 49.5 percent are Hispanic, as well as in the New York and Los Angeles metropolitan areas. This decline, however, was far lower than the Census and other experts had predicted. Whereas Census experts and the Administration’s critics had expected a greater-than-five percentage point decline (or more) among particular subgroups, the actual drop as in the neighborhood of one percent. According to the report, these differences are small enough that they would not have required staffing changes for the Census’ routine follow-up responses. It’s also lower than the point at which plaintiff states claimed they would lose out on federal funding.

While these findings challenge some of the assumptions upon which the legal challenge to inclusion of the citizenship question was based, they don’t undermine the Court’s ultimate holding, which was based upon the arbitrariness and lack of candor of the Commerce Department (of which the Census is a part), not any particular assumptions about the effect of including the question. They do, however, challenge some of the assumptions that caused so many to file suit against the Census in the first place, and will make it easier for a future administration to include a citizenship question in the decennial Census, if it should so choose.

from Latest – Reason.com https://ift.tt/2tStZTa

via IFTTT

Phase 1 Trade Deal “Stops Bleeding,” Does Not Resolve Trade War, Says US Chamber Of Commerce

President Trump is expected to sign a Phase 1 trade agreement with China this week that “stops the bleeding” but is no resolution to the trade war, a senior U.S. Chamber of Commerce official said on Monday, quoted by Reuters.

Reuters: Myron Brilliant, the chamber’s Executive Vice President, told a media briefings in the Chinese capital that there is “clearly a sigh of relief from both sides” with the agreement and that the depth of the Phase 1 was more positive than initially thought.

Myron Brilliant, the chamber’s Executive Vice President, told reporters at a press conference in Beijing on Monday that there are significant challenges ahead, and a temporary trade agreement is “clearly a sigh of relief from both sides.”

“Implementation of Phase 1 will be important to building trust and certainty, building off the success of the negotiation,” said Brilliant, who said the deal could be signed as soon as Wednesday.

As Phase 1 “stops the bleeding”, he said. “at the same time, it’s important that the two sides demonstrate a commitment to moving forward on the Phase 2 negotiations”.

Brilliant warned that “significant challenges” remain ahead-considering structural issues at the heart of the trade war are unresolved.

Brilliant said he’s been briefed on the text of the trade deal but hasn’t been allowed to view it.

U.S. Treasury Secretary Steven Mnuchin told Fox News on Sunday that China’s commitments on agriculture products haven’t changed during the translation process, and he said the text of the trade deal could be released this week.

Mnuchin said China is expected to buy $40 billion to $50 billion worth of U.S. farm goods per year and total around $200 billion in two years.

The Global Times said Sunday that the upcoming trade deal between the U.S. and China would cover agriculture purchases to intellectual property rights (IPR) to enforcement mechanisms.

Chinese officials have said the Phase 1 agreement will include nine chapters, including sections on IPR, technology transfers, food and agricultural products, financial services, foreign exchange rates, transparency, and two-way assessment.

A source told the Global Times that “balance is a highlight of the phase one deal.” “You will see what I mean by this when you see the final text of the agreement,” the source said.

The Phase 1 trade deal is optically pleasing for President Trump during an election year and could further be a catalyst for higher stock market prices. However, the deal hasn’t been made public and there are doubts about how comprehensive the deal is. There’s also concern whether the agreement will be implemented in full by both countries. A full resolution of the trade war could take years.

The worship of mortals as demi-gods and faith in Golden Idols triggers a turn in the karmic wheel as near-infinite hubris invites divine retribution.

In case you missed it, here’s a snapshot of the most recent Federal Reserve board meeting:

It’s certainly a peculiar moment in history when the President chides everyone who hasn’t gained 90% in their 409K (sic), seemingly unaware that only the top 5% have enough in a 409K to make a difference.

President Trump and the Federal Reserve agree: the “solution” to inequality and malaise is to boost the 409Ks of the top 5%, leaving the rest of the American workforce as glorified servants of the few who benefit from a record-setting stock market.

Note to the Prez and the Fed: goosing the stock market only increases wealth/income inequality. There’s only so many dogs owned by the top 5% the peasantry can walk, only so many Priuses and Teslas to wash, only so many preciously over-scheduled children to tutor, only so many $50 steak dinners to bus, only so many bedpans of the top 5%’s parents to empty. The top 5% who benefit from the stock market’s relentless melt-up can’t generate a tide that raises all ships; all they can do is further enrich themselves on the debt-serfdom of their servants.

Then there’s the whole triumphal tone of the Fed’s self-satisfied service of the super-wealthy and the President’s boosterism taunting the bottom 95% who don’t own enough stocks in their 409Ks to reverse their deteriorating financial condition. This reflects an openly quasi-religious faith in the omnipotence of the Fed which we can chart:

The worship of mortals as demi-gods and faith in Golden Idols triggers a turn in the karmic wheel as near-infinite hubris invites divine retribution. Call it the loss of the Mandate of Heaven for lack of a better term, but those who taunt the unprivileged, worship false idols and rig the system to benefit the few at the expense of the many are in effect claiming to hold the Ultimate Power in the Universe.

For a suitable warning about the consequences of this unlimited hubris, let’s turn to Darth Vader, in paraphrase:

Don’t be too proud of this financial terror you’ve constructed. The ability to control a market is insignificant next to the power of the Force.

Put another way: Those whom the gods would destroy they first make powerful.

(In case you were wondering: the chart is of TSLA, courtesy of www.slopeofhope.com)

The Trump Administration’s decision to include a citizenship question in the 2020 Census provoked substantial outrage. Many feared that inclusion of the question would depress response rates, leading to an inaccurate Census, and that it would produce a substantial undercount of people in immigrant communities, particularly in households containing noncitizens. Indeed, many suspected that was the whole point.

Fears of a significant undercount, and its consequent effects on political representation and the distribution of federal funds, prompted many states and interest groups to file suit against the Trump Administration. As the Supreme Court explained when it discussed the plaintiffs’ claim of standing to bring the suit:

Respondents assert a number of injuries—diminishment of political representation, loss of federal funds, degradation of census data, and diversion of resources—all of which turn on their expectation that reinstating a citizenship question will depress the census response rate and lead to an inaccurate population count. Several States with a disproportionate share of noncitizens, for example, anticipate losing a seat in Congress or qualifying for less federal funding if their populations are undercounted. . . .

Several state respondents here have shown that if noncitizen households are undercounted by as little as 2%—lower than the District Court’s 5.8% prediction—they will lose out on federal funds that are distributed on the basis of state population. . . .

Justice Breyer’s separate opinion also stressed the arbitrariness of including a question that would produce a less accurate enumeration of people within the country.

How can an agency support the decision to add a question to the short form, thereby risking a significant undercount of the population, on the ground that it will improve the accuracy of citizenship data, when in fact the evidence indicates that adding the question will harm the accuracy of citizenship data?

As readers know, the Court decided, 5-4, that inclusion of the citizenship question was unlawful because the Administration’s explanation for why the question was to be added seemed “contrived” and did not match the available evidence.

In 2019, the Census nonetheless conducted a significant test of the effects of including a citizenship question, and the results were not what anyone (including the Census’s own experts) expected, as documented in a recently released report. As noted by Lyman Stone, the report tells a quite different story about the effects of a citizenship question than that upon which the Census case was litigated.

In 2018, the U.S. Census Bureau decided to test the operational implications of a proposed question on citizenship status on the 2020 Census. In particular, experts and stakeholders raised concerns that such a question could depress self-response rates, increase cost, and reduce the quality of the 2020 population count. An indirect study by Census Bureau researchers predicted that “adding a citizenship question to the 2020 Census would lead to lower self-response rates in households potentially containing noncitizens…” compared to households with all citizens (Brown, Heggeness, Dorinski, Warren, & Yi, 2018). However, the authors recommended the ideal analysis would be to conduct a randomized controlled experiment to compare response rates on questionnaires with and without a citizenship question. . . .

The major finding of the 2019 Census Test was that there was no statistically significant difference in overall self-response rates between treatments. The test questionnaire with the citizenship question had a self-response rate of 51.5 percent; the test questionnaire without the citizenship question had a self-response rate of 52.0 percent. Although these results differ from the predicted rates in Brown’s et al. study, the results of the two studies are not

comparable since this study benefits from the randomized controlled design, which isolates the treatment effect.

The Report also found statistically significant declines in response rates among some areas and among subgroups, including areas where more than are 4.9 percent noncitizens or more than 49.5 percent are Hispanic, as well as in the New York and Los Angeles metropolitan areas. This decline, however, was far lower than the Census and other experts had predicted. Whereas Census experts and the Administration’s critics had expected a greater-than-five percentage point decline (or more) among particular subgroups, the actual drop as in the neighborhood of one percent. According to the report, these differences are small enough that they would not have required staffing changes for the Census’ routine follow-up responses. It’s also lower than the point at which plaintiff states claimed they would lose out on federal funding.

While these findings challenge some of the assumptions upon which the legal challenge to inclusion of the citizenship question was based, they don’t undermine the Court’s ultimate holding, which was based upon the arbitrariness and lack of candor of the Commerce Department (of which the Census is a part), not any particular assumptions about the effect of including the question. They do, however, challenge some of the assumptions that caused so many to file suit against the Census in the first place, and will make it easier for a future administration to include a citizenship question in the decennial Census, if it should so choose.

from Latest – Reason.com https://ift.tt/2tStZTa

via IFTTT

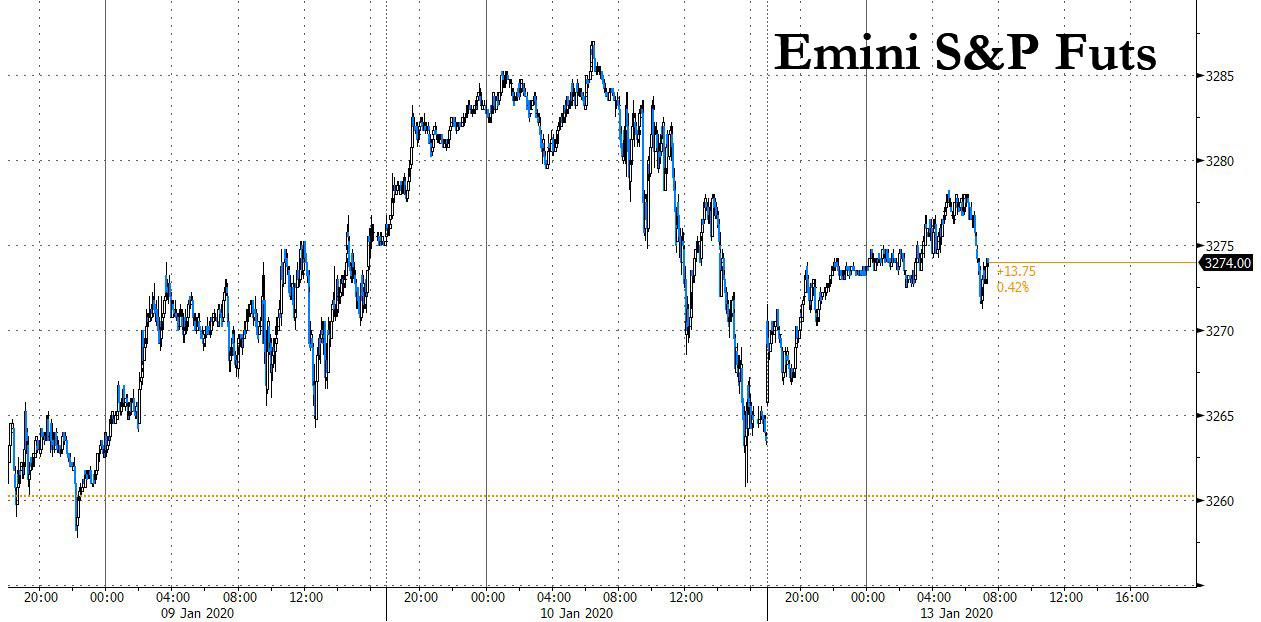

Futures Jump On “Trade Optimism” As Phase 1 Deal Signing Looms

With the Fed’s liquidity deluge ongoing, stocks predictably are up on Monday and back to all time highs and since traders always need a “narrative” what better time to use the old standby “U.S. Stock-Index Futures Gain Amid Trade Optimism” (which is how Bloomberg “explained” the market action) especially since the signing of a Phase 1 China-U.S. trade deal is set for this Wednesday, even though markets have yet to see details of the agreement.

With December’s disappointing nonfarm payrolls report largely forgotten, half the Friday drop was erased overnight in very thin volume, and the S&P e-mini stock futures rose 0.31% to 3,274.8, just 10 points shy from reclaiming its all time high.

Ironically, Friday’s market reaction to the poor payrolls report was bizarre: as DB’s global FX strategy head Alan Ruskin said, “This is the perfect employment report for the Fed to continue to run the economy ‘hot’, as views on the natural rate of unemployment continue to drop,” adding “this is perfect for risky assets.”

MSCI’s All Country World Index was up 0.02%, also just short of a record high hit last week. After rising in early trade, European shares were last down 0.2% by midday. Germany’s DAX fell 0.3%, France’s CAC 40 gained 0.05% and Britain’s FTSE 100 added 0.19% amid speculation for rate cuts by the BOE. Europe’s Stoxx 600 index fell 0.22%.

In Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan was up 0.64%, touching its highest level since June 2018. South Korea’s trade-sensitive Kospi added 1.04% and Hong Kong’s Hang Seng was up 1.11%, while Taiwan shares increased 0.74% in the first trading day after Taiwan re-elected President Tsai Ing-wen by a landslide on Saturday. Mainland Chinese shares lagged the regional index after China’s major equity indexes logged their sixth consecutive weekly rise last week, the longest such streak since the first quarter of 2019. The benchmark Shanghai Composite Index was up 0.8% in the afternoon, turning around from losses earlier in the session. Investors in China are looking ahead to trade and economic growth data due this week, which is expected to shed more light on early signs of economic improvement after the country logged its slowest pace of growth in nearly three decades in the third quarter. China’s fourth-quarter and 2019 full-year GDP figures, due on Friday, are also likely to draw scrutiny as investors look for signs that improvements seen in recent manufacturing surveys are reflected in broader growth and investment figures.

Japan’s Nikkei was closed for a holiday. It fell sharply early last week when Iran attacked bases hosting U.S. military in Iraq, only to rally almost a thousand points when the two countries stepped back from hostilities.

Trading in stocks, bonds and currencies was suspended in the Philippines because the Taal volcano to the south of the capital is belching out ash.

It wasn’t just Japan: tensions between the U.S. and Iran after the U.S. killing of a top Iranian general put investors on guard against risk last week, knocking global stocks off a record high set in the first trading week of the year. But with no further escalation in conflict and focus shifting toward this week’s trade deal, markets have rebounded.

“Last week there was a lot of focus on the conflict between Iran and the U.S. However, the ‘modest’ Iranian response to the killing of Suleimani and even some more conciliatory comments from Trump have taken the U.S.-Iran conflict more or less away from the financial agenda,” said Arne Rasmussen, chief analyst at Danske Bank in a note to clients.

And so, with optimism over a potential World War III surging, attention turned to Trade War I, where Reuters reported that China’s commitments in the Phase 1 trade deal with the United States were not changed during a lengthy translation process and will be released this week as the document is signed in Washington, U.S. Treasury Secretary Steven Mnuchin said on Sunday.

“Even getting to this phase-one agreement, when we weren’t sure we would get here, really shows that there’s political will to de-escalate trade tensions between China and the U.S.,” Lucy Meagher, investment adviser at Evan’s & Partners Pty., told Bloomberg Television. “We expect that to be a positive.”

To be sure, the main event of the week will be the signing of the Phase 1 trade deal between the United States and China on Wednesday. The Trump administration has invited at least 200 people to the White House for the ceremony.

“A calmer geopolitical backdrop and the signing of the U.S.‑China Phase 1 agreement is, on balance, favorable for global growth,” said Joseph Capurso, an FX strategist at CBA. “However, the 86-page Phase 1 agreement has not yet been made public. There are doubts how comprehensive the deal is, and whether the Phase 1 agreement will be implemented in full by both governments.”

Yet while geopolitics simmers in the background, Trump tweeted his support for protesters in Iran angered at their country’s mistaken downing of a Ukrainian jet, which could potentially add to middle east instability. Additionally, earnings from some of the biggest U.S. companies are due, amid forecasts they will show the smallest growth in three years.

Elsewhere, Germany’s benchmark bund yield headed for its least negative closing level since May. The offshore yuan strengthened past 6.9 per dollar for the first time since July in both onshore and offshore markets, as the signing of a preliminary trade deal with the U.S. nears. The People’s Bank of China set its daily fixing at the strongest level since August, nearly matching estimates by analysts and traders. The dollar rose and Treasuries fell across the curve as the completion of the first trade deal nears. President Donald Trump has said the U.S. and China will sign the accord on Wednesday.

The euro was flat on Monday at 1.1121, up from a $1.1083 low on Friday. Support comes in around $1.1060, while the recent peak at $1.1239 marks stiff resistance. The dollar rose 0.14% against a basket of currencies, up to 97.488, well within the recent trading range of 96.355 to 97.817; it was firmer on the yen at 109.87 but faces tough resistance around 109.70 where rallies have repeatedly failed in the past couple of months according to Reuters. The pound slipped 0.86% to $1.2963 after Bank of England policymaker Gertjan Vlieghe said he will vote for a cut in interest rates later this month, barring an “imminent and significant” improvement in the growth data.

In commodities, oil prices were slightly firmer after suffering their first weekly loss since late November. Brent crude futures were down 0.25% at $64.82 a barrel, while U.S. crude fell 0.15% to $58.96 a barrel. Spot gold slipped 0.6% to $1,552.30 per ounce, having hit a seven-year top last week of $1,610.90 at the height of Iran-U.S. tensions.

Fed’s Rosengren and Bostic are set to speak, economic data include monthly budget statement. Shaw Communications is due to report

Market Snapshot

S&P 500 futures up 0.3% to 3,275.75

MXAP up 0.4% to 173.67

MXAPJ up 0.7% to 568.36

Nikkei up 0.5% to 23,850.57

Topix up 0.4% to 1,735.16

Hang Seng Index up 1.1% to 28,954.94

Shanghai Composite up 0.8% to 3,115.57

Sensex up 0.6% to 41,832.58

Australia S&P/ASX 200 down 0.4% to 6,903.67

Kospi up 1% to 2,229.26

STOXX Europe 600 up 0.1% to 419.66

German 10Y yield rose 2.1 bps to -0.178%

Euro down 0.01% to $1.1120

Italian 10Y yield fell 5.7 bps to 1.151%

Spanish 10Y yield rose 2.5 bps to 0.466%

Brent Futures up 0.2% to $65.11/bbl

Gold spot down 0.9% to $1,547.98

U.S. Dollar Index up 0.1% to 97.49

Top Overnight News from Bloomberg

Iran witnessed a second night of protests, some violent, after the governmentadmitted it had mistakenly downed a Ukrainian passenger jet

Riksbank Deputy Governor Per Jansson says his reservation against the rate hike in Dec. doesn’t necessarily mean he will advocate a cut if development ahead is in line with forecasts

The U.K. economy unexpectedly shrank ahead of the general election, casting doubt over whether there was any growth at all in the fourth quarter

Conditions boiled over as Iranians gathered for a second night of protests after the governmentadmitted it had mistakenly downed a Ukrainian passenger jet, triggering global outrage as well as internal dissent

Oil was steady after the biggest weekly drop since July as an easing of geopolitical tension in the Middle East turned attention back to a flood of new supply set to hit the market this year

Argentine President Alberto Fernandez said in an interview with local media that his administration aims to “resolve” how much external debt the country needed to repay by March 31

Troubles at aircraft maker Boeing could trim about half a point from U.S. GDP in 2020 but economic growth should still come in at about 2.5%, said Treasury Secretary Steven Mnuchin

U.K. job postings fell by the most in a decade last year as Brexit uncertainty whipsawed business planning, according to a report from BD

Xi Jinping’s goal of bringing Taiwan under his control moved further out of his grasp as the island re-elected a president who has vowed to defend its sovereignty

Prime Minister Scott Morrison’s personal ratings have tumbled over his handling of Australia’s wildfire crisis, adding to pressure on his government to shift course on its climate change policies

The executive director of campaign group Human Rights Watch said Sunday that he was prevented from entering Hong Kong, where he intended to release a report critical of the Chinese government

Asian equity markets began the week somewhat mixed with the region indecisive and Japanese participants away for a national holiday, with this week’s US-China Phase 1 deal signing adding to the tentativeness. ASX 200 (-0.4%) suffered from broad losses across its sectors led by underperformance in energy and defensives, while Westpac recently estimated losses from the ongoing bushfires at AUD 5bln and a total impact to domestic GDP of between 0.2%-0.5%. The TAIEX (+0.7%) was lifted following a landslide victory by Taiwanese President Tsai and with several encouraging monthly revenue updates including Acer, Pegatron and TSMC. Shanghai Comp. (+0.8%) and Hang Seng (+1.1%) were varied with early underperformance in the mainland after the PBoC once again refrained from open market operations and as the looming Phase 1 signing kept participants on the fence. Furthermore, the sides were said to have agreed to launch a new semi-annual dialogue mechanism, although not also was rosy with the US to drop its civilian drone programme amid security concerns regarding Chinese tech and with officials to visit the UK in which they are expected to pressure the UK against the use of Huawei equipment.

Top Asian News

New SARS-Like Virus Found in Traveler From China, Thailand Says

Blackstone Is Said to Near Deal to Buy Allcargo’s Unit Stake

Trump Trade Deal Raises Issue of Trusting China to Deliver

‘Digital Currency for Cadres’ Is China’s Latest How-To Book Hit

A tentative start to the week for European equities thus far [Euro Stoxx 50 +0.1%], following on from a similarly mixed APAC session ahead of the looming US-China Phase One deal signing. UK’s FTSE 100 [+0.5%] outperforms its regional peers as a weaker GBP bolsters exporters in the index following further dovish comments from BoE MPC members – this time Vlieghe – in the run up to the Jan 30th BoE confab; as well as UK today’s poor UK GDP numbers. Sectors are relatively mixed with no clear under/outperform in a reflection of the broad overall sentiment. The tech sector [+0.6%] outperforms with some tailwind heading into the Phase One deal signing as US business executives suggest the deal shows some advances on some sticking points such as intellectual property protection, significant agricultural purchases and recued export barriers. In terms of individual movers, UCB (+3.1%) remains one of the winners in the Stoxx 600 after the Co. upgraded its FY19 core EPS and revenue outlooks. Wirecard (+1.7%) is the top gainer in the DAX after Chairman Matthais and the supervisory board chairman stepped down. On the other end of the spectrum, Renault (-3.8%) shares fell to the foot of the pan-European index amid reports that Senior Nissan executives have stepped up the contingency planning regarding a possible split from Renault.

Top European News

Pound Falls After Vlieghe Joins BOE Chorus on Potential Rate Cut

Aston Martin Said to Hold Funding Talks With Stroll, Geely

Norway’s Arctic Oil Vision Suffers Another Blow From Lundin

New German Coal Plant Could Threaten Merkel’s Final Climate Push

In FX, the Pound was already under pressure and underperforming G10 peers after BoE’s Vlieghe joined the growing ranks of dovish MPC members by signalling his leaning towards a rate cut as soon as this month barring an imminent and significant pick-up in UK growth. However, November GDP fell 0.3% m/m vs the flat consensus to lift January and 2020 easing expectations and push Sterling down further through 1.3000 vs the Dollar and through 0.8570 against the Euro, with the former testing December 27 lows circa 1.2970 and latter approaching Xmas Eve peaks after breaching the 55 DMA (0.8534) and 0.8550.

JPY – The next weakest major link, as stops set around mid and early December highs were tripped to leave the Yen eyeing lows not seen since May 30 last year (109.93) ahead of big 110.00 barriers and technically bearish having fallen below the 200 WMA (109.70). From a fundamental perspective, broadly risk on sentiment awaiting the signing of US-China trade pact Phase 1 and no further US-Iran hostilities has prompted Jpy selling, while Usd/CNH has continued its downtrend to multi-month lows under 6.9000.

AUD/EUR/NZD/CHF/CAD – All narrowly mixed vs the Greenback, as the DXY regains more composure off post-NFP lows within a 97.327-535 range, albeit partly on the aforementioned Pound and Yen depreciation. Aud/Usd is pivoting 0.6900, Eur/Usd is hovering above 1.1100 flanked by hefty options (1.6 bn between 1.1095-1.1100 and the same size from 1.1120-40), Nzd/Usd is meandering within 0.6625-52 parameters in the run up to NZIER confidence and building consensts, Usd/Chf is sitting tight in a 0.9723-36 band and Usd/Cad is equally restrained between 1.3046-67 ahead of Canada’s LEI and the BoC’s outlook survey.

SCANDI/EM – The Norwegian Krona has weakened further alongside oil prices and from a chart perspective as Eur/Nok trades above the 200 DMA to 9.9100+ at one stage, while its Swedish counterpart is also on the back foot close to 10.5900 in wake of comments from Riksbank’s Jansson reiterating his opposition to December’s 25 bp repo hike. However, the Turkish Lira is consolidating recovery gains vs the Buck through 5.9000 even though the current account balance swung into arrears in November and the CBRT is widely forecast to ease again this week, with the Try still cheering cheaper crude costs and the overall appetite for risk noted above.

Commodities are largely mixed with WTI and Brent front-month futures choppy but ultimately flat in intraday trade, following last week’s vehement price action amid the heating and then cooling of geopolitical tensions in the Middle East. Over the weekend, focus somewhat shifted from the US/Iran conflict after Iran admitted it unintentionally shot down the Ukrainian Boeing 737-800 – which prompted mass protests in Tehran. WTI futures oscillate on either side of USD 59.0/bbl having already dipped below its 50 DMA at USD 58.81/bbl. Meanwhile, Brent Mar’20 contracts fell below the USD 65/bbl level and briefly dipped below Friday’s low of USD 64.88/bbl ahead of the current 2020 low-print at USD 64.58/bbl. SocGen notes that if the 200DMA (~USD 64.30/bbl) fails to hold, then oil will be put in ranges seen last September- after Saudi managed to put production back online surprisingly quickly after the attacks on Aramco facilities. Elsewhere, spot gold continues to trickle lower and prices temporarily lost the USD 1550/oz psychological figure amid a firmer Buck. Technicians will be eyeing USD 1540/oz for support marks the current YTD low. The firmer Dollar also provoked copper prices, which eased from highs north of USD 2.81/lb+ back to ~USD 2.80/lb – with the red metal on standby for the US-Sino deal signing later this week.

US Event Calendar

2pm: Monthly Budget Statement, est. $15.0b deficit, prior $13.5b deficit

Central Banks

10am: Boston Fed’s Rosengren Discusses Economic Outlook

12:40pm: Fed’s Bostic Discusses Economic Outlook and Monetary Policy

DB’s Jim Reid concludes the overnight wrap

I will be in Davos next week at the annual World Economic Forum. I’m still hopeful that Bono will want to come to one of my presentations one year on the off chance that he still hasn’t found what he’s looking for. With or without Bono, today’s new piece will be the basis of our conversations in Davos and is on the subject of growth. The general premise is that economic growth has been a wonderful game changing development for humans but only started with the first industrial revolution (c.250 years ago). Health, life expectancy, poverty etc. hardly improved for centuries before this and only saw huge improvements once the second industrial revolution (c.100 years later) changed sanitation and medicine forever. So the last 100-150 years has seen a rate of progress like nothing in history for the human race. The development has been near exponential since. However the side effects of this has been increasingly seen over the last few decades in terms of debt, regional inequality and most importantly the climate. The climate gets special focus in the note and we conclude that while the awareness of human’s impact on the environment has reached a tipping point, we feel that there is limited appreciation of the economic and personal trade-offs and sacrifices that will be needed if we want to seriously limit global warming. Will human’s sacrifice economic growth and even human development to halt environmental damage? That will probably be the question of our age but we shouldn’t lose stock of the uncomfortable truth that polluting growth has been essential for human progress after centuries (perhaps longer) of it going nowhere. Without it none of us would be here.

As discussed the first and last question in this month’s survey (link here) ) is related to climate change and asks how much economic growth you would be prepared to give up to help the environment and at the end asks whether you’ve changed your behaviour in a number of activities to limit the damage. It’s totally anonymous so feel free to be honest. Alongside this there are the usual market related questions. Results will be published on Thursday morning. We’d be grateful to get as many replies as possible before we close it at 5pm Wednesday. You only have to answer the questions you want and can skip any you don’t. Last month’s results are here.

The main highlights for the week ahead will be the signing of the Phase One trade deal between the US and China (Wednesday). US Treasury Secretary Steven Mnuchin said over the weekend that an English-language version of the agreement will be released this week. It’s quite remarkable that we still don’t know much in the way of details so eyes will be on this. We’ll also see the start of US earnings season with a number of banks reporting. On Tuesday we’ll hear from JPMorgan Chase, Wells Fargo and Citigroup. Then on Wednesday we’ll get Bank of America, UnitedHealth Group, Goldman Sachs, US Bancorp and BlackRock. Finally on Thursday, we’ll hear from Morgan Stanley and BNY Mellon. In terms of data CPI (Tuesday), retail sales (Thursday), and consumer confidence (Friday) are the main highlights in the US. In China we have trade data (Tuesday) and Q4 GDP/retail sales/industrial production (Friday). So we’ll have quite a good idea about momentum in the Chinese economy by the end of the week. In Europe industrial production numbers (Tuesday), and the flash CPI (Friday) are the highlights. The UK also sees CPI (Wednesday) and retail sales (Friday).

In terms of central banks over the coming week, publications to watch for include the Beige Book from the Fed on Wednesday, and then the ECB’s monetary policy account of its December meeting (and Christine Lagarde’s first as ECB President) on Thursday.

Over to politics now, and there’s a number of upcoming events this week. In the US, it’s the last Democratic primary debate on Tuesday before primary voting kicks off in February. Former Vice President Biden is currently ahead in the national polling according to the average on RealClear Politics. However, the polls in the first two states to vote in February, Iowa and New Hampshire, are much tighter, with the RealClear Politics average putting the 3 top candidates in Iowa between 20% and 22%, so it’s a tight race going into the caucuses there on 3rd February.

A Des Moines Register/Mediacom/CNN poll out from Iowa (the first state to vote) put Senator Bernie Sanders in first place on 20%, a 5-point jump for Sanders since their last poll in November. Elizabeth Warren was in 2nd place on 17%, while Pete Buttigieg was on 16%, and Joe Biden on 15%. As discussed above, nationally Biden remains the frontrunner, but the big question will be whether he can maintain his momentum were he not to win either of the first 2 states. Given how quickly Warren’s support has fallen, and also the impressive rally in Sanders’s ratings over a relatively short period of time, its clear that it remains all to play for in this race.

A quick refresh of our screens this morning shows that most Asian markets are trading higher with the Hang Seng (+0.82%), Shanghai Comp (+0.30%) and Kospi (+0.87%) all making advances. Japan’s markets are closed for a holiday. As for Fx, the Chinese onshore yuan is up +0.293% to 6.8990, the highest since July, ahead of the signing of the Phase 1 deal. Elsewhere, futures on the S&P 500 are up +0.28%.

In weekend news the Financial Times reported that the BoE’s Gertjan Vlieghe said that he will vote for an interest-rate cut from 0.75% to 0.5% this month if there are no signs of the economy improving after the general election. He said, “I really need to see an imminent and significant improvement in the U.K. data to justify waiting a little bit longer.” His comments echo those from the BoE Governor Carney made earlier in the past week while, the MPC member Silvana Tenreyro has also said that she may support an interest-rate cut in the next few months if sluggish global growth and Brexit uncertainty persist. Meanwhile, the FT also reported overnight that the CBI has urged the UK government to include businesses in the UK’s post-Brexit trade talks with the EU and US.

Turning to geopolitics, Iran has faced significant internal protests over the weekend after the Iranian government admitted that it had mistakenly downed the Ukrainian jet last week.

Recapping last week now, and the theme was very much the return of investor risk appetite, thanks to declining tensions between the US and Iran. Brent Crude was down -5.28% last week (-0.60% Friday) to just below $65/barrel, putting it clearly below the pre-US strike price. Meanwhile US equities were just shy of record highs, thanks to a slight pullback on Friday following the jobs report (more on that below). The S&P 500 ended the week +0.94% (-0.29% Friday), while the STOXX 600 also advanced +0.19% (-0.12% Friday). Volatility was also down, with the Vix index -1.46pts last week (+0.02pts Friday). Investors continued to move out of safe havens, with the Japanese Yen ending the week -1.24% (+0.06% Friday) against the US dollar, while sovereign debt also sold off, with 10yr Treasury yields +3.1bps (-3.4bps Friday) and 10yr bunds +7.9bps (-2.0ps Friday).

Looking at the jobs report, the headline numbers were a little below expectations, as nonfarm payrolls grew by +145k in December (vs. +160k expected), though there was a downward revision of -14k to the prior 2 months. The unemployment rate remained at 3.5%, in line with expectations and remaining at its joint lowest level since 1969. The more negative news for the economy (but positive for carry) came from average hourly earnings growth, which rose by +2.9% (vs. +3.1% expected), the first time it’s fallen below 3% since July 2018. That said, in somewhat brighter news, the broader U6 measure that also includes the underemployed and those marginally attached to the labour force fell to 6.7%, its lowest level since the data series began in 1994. From the Fed’s perspective, the report could be taken as a sign that there’s still slack in the labour market, particularly with the declines in U6 and wage growth falling back somewhat.

During the protests, which erupted out of anger over the regime’s initial lies about Flight 752 (it initially insisted that a “mechanical error” was responsible despite video evidence suggesting a missile strike), ranian security forces fired both live ammunition and tear gas into crowds of demonstrators furious over the government’s denials.

Some of the video and images have shown what appear to be casualties, though death tolls and counts on the number of injured have been difficult to pin down.

As Reuters explains, the protests against the regime “are the latest twist” in the Trump Administration’s campaign of maximum pressure against Iran and its government. Over the weekend, President Trump tweeted a couple of messages of support for the protesters on the ground, including one tweet sent in Arabic.

مشاور امنیت ملی امروز عنوان کرد كه تحریم ها و اعتراضات، ایران را«به شدت تحت فشار»قرار داده است و آنها را مجبور به مذاكره می كند.در واقع، اصلا برایم اهمیتی نداردکه آیا آنها مذاکره می کنند یا نه.این کاملاً به عهده ی خودشان است، اما سلاح هسته ای نداشته باشیدو«معترضان خود را نکشید.» https://t.co/DBGGs8QFcJ

To the leaders of Iran – DO NOT KILL YOUR PROTESTERS. Thousands have already been killed or imprisoned by you, and the World is watching. More importantly, the USA is watching. Turn your internet back on and let reporters roam free! Stop the killing of your great Iranian people!

Videos posted to social media on Sunday recorded gunshots in the vicinity of protests in Tehran’s Azadi Square. The wounded could be seen being carried off on stretchers as riot police fired what looked like rubber bullets. Other videos showed riot police beating protesters with batons, while others nearby screamed “Don’t beat them!”

Moreover, shouts of “Death to the dictator” could be heard in footage circulating on social media. It showed protesters shouting, directing their fury at Supreme Leader Ayatollah Ali Khamenei and the system of clerical rule.

“They killed our geniuses and replaced them with clerics,” demonstrators chanted at a one protest outside a university on Monday, a reference to the dozens of Iranian students who were returning to school in Canada who were aboard the flight.

This is a brand new chant – never heard before. It’s in response to the caliber of people killed on #UkranianPlaneCrash & the people killed 40 years ago during Iran revolution

The chief of police in Tehran insisted that Iranian police didn’t shoot any protesters…

“At protests, police absolutely did not shoot because the capital’s police officers have been given orders to show restraint,” Hossein Rahimi, head of the Tehran police, said in a statement carried by the state broadcaster’s website.

…Despite photos that appear to show individuals who have been shot with live ammo.

In one of the more dramatic chants, students at Tehran University reportedly shouted on Saturday that “They are lying that our enemy is America! Our enemy is right here!”

The regime is facing a tremendous backlash to the accidental shoot-down of Flight 752, a strike that killed 176 passengers and crew, including 60 Canadians. It’s thought that a misfiring of Iran’s Russian-made missile defense system brought down the passenger plane. Aside from the protests, some Iranian artists have spoke out against the regime. One famed director, Masoud Kimiai, withdrew from an upcoming international film festival. Two state TV reporters resigned in protest over the regime’s initial dissembling about the cause of the accident.

Though we didn’t see the level of violence that characterized protests in nearby Iraq last year, the Iranian regime came out in force. Uniformed police officers were only one arm of Iran’s vast security forces.

Riot police in black uniforms and helmets gathered earlier Sunday in Vali-e Asr Square, at Tehran University and elsewhere. Revolutionary Guard members patrolled the city on motorbikes, and plainclothes security men were also out in force.

It’s just the latest indication that the killing of General Suleimani and Iran’s response was truly an advantageous move for Washington and the West, as the Iranian regime hasn’t looked this fragile, or faced this much international condemnation in years.

So we probably can’t blame Tehran for its vicious crackdown, as the possibility of another revolution hangs in the balance.