The global economy is already in the worst distress that we have seen since 2008, and it appears that the global slowdown is actually picking up pace as we head into 2020. And this is happening even though central banks around the world have been cutting interest rates and pumping massive amounts of money into their respective financial systems. The central bankers appear to be losing control, and it certainly wouldn’t take much of a push for this new crisis to evolve into a complete and utter nightmare. The U.S. economy hasn’t been hit quite as hard as economies in Asia and Europe have been, but without a doubt things are slowing down here too. Corporate earnings have been falling quarter after quarter, auto loan delinquencies just hit a record high, the Cass Freight Index has declined for 11 consecutive months, and we just witnessed the largest drop for U.S. industrial production since 2009. Everywhere around us there is bad economic news, but most Americans are still completely oblivious to what is happening.

In this article, I am going to share even more evidence that a global economic slowdown has already begun. When you add these numbers to all of the other numbers that I have been sharing in recent weeks, it becomes impossible to deny that something major is taking place.

The following are 5 more signs that the global economy is careening toward a recession…

#1 It is being projected that global auto sales will be down approximately 4 percent this year. According to CNN, this will be the second consecutive year that global auto sales have fallen…

With only a month left in the year, global auto sales are on track for a 3.1 million drop, about 4%, for the year, according to Fitch. That would be the biggest decline since 2008, when the financial crisis hit, and the second year in a row that sales have fallen. Fitch expects worldwide car sales to total 77.5 million in 2019.

#2 Global trade just keeps falling. According to Zero Hedge, total global trade has now declined on a year over year basis for four months in a row…

Global trade on a YoY basis contracted by 1.1% in September, marking the fourth consecutive YoY declines and the most extended period of subdued trade since the financial crisis in 2009.

The CPB said supply chain disruptions between the US and China, due mostly to the trade war, were the most significant drag on international trade volumes. US volumes fell 2.1% in September MoM. Though in China, imports plunged 6.9% MoM.

As you can see from those first two examples, we keep witnessing things happen that we haven’t seen since the last financial crisis. Over the past few months, I have used phrases such as “since 2008” and “since 2009” over and over again. We literally have not seen economic numbers this bad since the last recession, and we are still in the very early phases of this new downturn.

And in some cases, the numbers are actually even worse than anything that we saw during the last recession, and that brings us to our next sign…

China Industrial Enterprises total profits collapsed in October to CNY427.5bn from CNY575.6bn in September – a 9.9% YoY plunge, the biggest drop on record.

In fact, China’s Industrial sector has seen annual declines in its profits for 4 of the last 6 months.

The trade war has hit the Chinese economy really hard, but it doesn’t look like a trade deal will happen any time soon.

Consumer confidence dipped for a fourth straight month in November as economic conditions weaken toward the end of 2019, data released Tuesday by The Conference Board shows.

The board’s consumer confidence index dipped to 125.5 this month. That’s down from 126.1 in October. Economists polled by Dow Jones expected the index to rise to 126.6.

This wasn’t supposed to happen, and if it keeps happening that is going to have important implications for the 2020 election.

#5 Even the wealthy are cutting back on their spending. According to Yahoo Finance, this is a continuation of a trend that we have been seeing for the past three quarters…

Spending by the top 10% fell 1% in the second quarter from the same period last year, according to an analysis of Federal Reserve data by Moody’s Analytics. And a four-quarter average of outlays by the high earners has slipped on an annual basis the past three quarters, marking the first such declines since the Great Recession of 2007-09.

In recent years, global central banks have engaged in unprecedented intervention in an attempt to stave off another crisis, and for a while their efforts appeared to be successful.

But just because the coming crisis was delayed does not mean that it was canceled.

In fact, over the past few years our long-term financial problems have actually gotten a lot worse. We are facing the biggest debt bubble in the history of the planet, global financial markets are more primed for a crash than they have ever been before, and civil unrest is breaking out all over the world. The stage is certainly set for “the perfect storm” that I keep talking about, and most Americans have absolutely no idea what is coming.

In all the time that I have been writing about the global economy, things have never looked more ominous then they do right now.

So buckle up and hold on tight, because it certainly looks like we are in for a very bumpy ride in the months ahead.

Global Markets Grateful For Trade Deal Optimism, Levitate To All Time Highs

With little out there to threaten the melt-up in global stocks, and with hte occasional “trade deal optimism” trickling in from Trump’s tweets or Chinese soundbites, traders were thankful for yet another all time high in S&P futures while world markets made another push for a record high on Wednesday after Trump said Washington and Beijing were in the final throes of inking an initial trade deal.

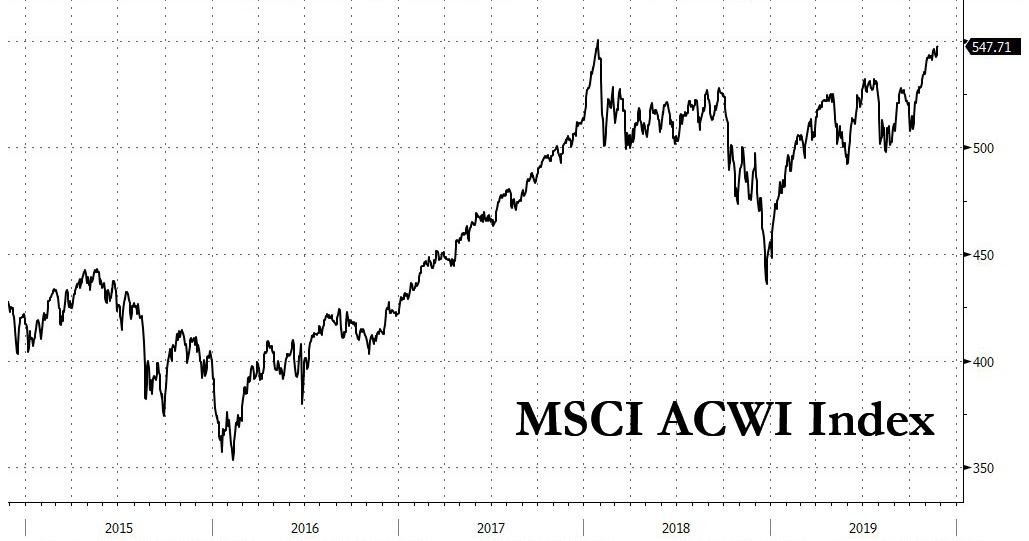

The MSCI’s all-country world index was just within 0.4%, or 2 points, of its record high from January 2018…

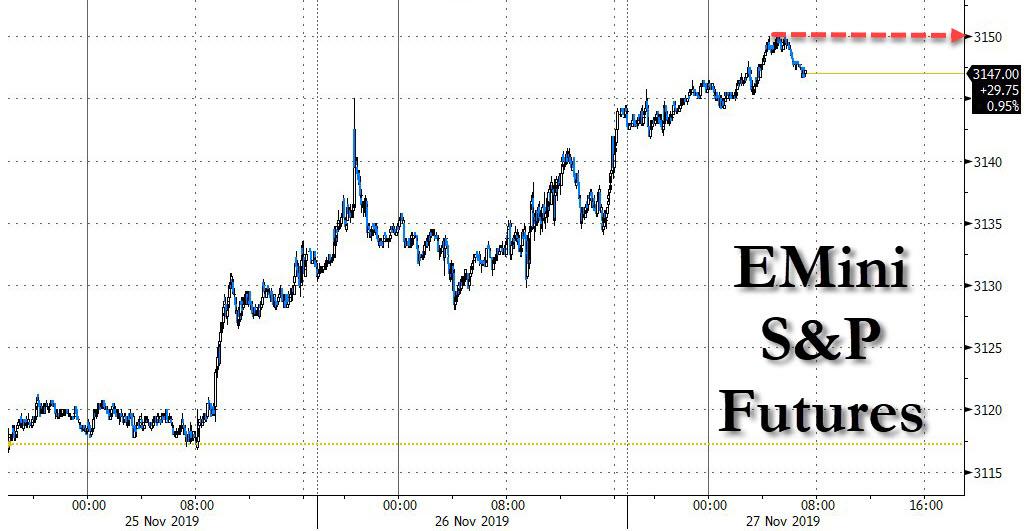

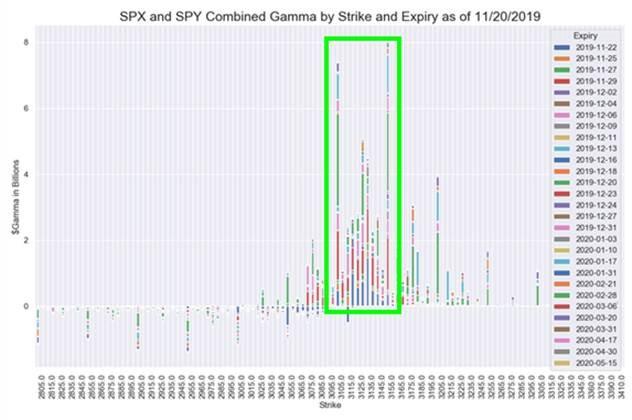

… while US equity futures rose all night until they rebounded off the giant gamma wall at 3,150…

… which we discussed previously has set the trading range for the S&P between 3,100 and 3,150. And so, having hit the top end of the dealer sweet spot, the S&P may now revert lower… but don’t hold your breath.

Europe’s Stoxx 600 index also rose to within 1% of its record close, with 15 of 19 sector groups advancing amid very subdued volumes.

Earlier in the session, Asian stocks advanced for a fourth day, led by tech firms, with the MSCI Asia Pacific index adding 0.3% in overall quiet trading, and while Shanghai struggled after Chinese industrial company profits plunged the most since 2011, Australian shares reached record highs and Japan’s Nikkei drew support from the growing likelihood of extra fiscal stimulus, while the Topix added 0.3%, driven by electronics and machinery makers, as foreigners extended their buying of Japan equities for a seventh week, its longest stretch in two years. A senior Japanese ruling party official said on Wednesday he believed the government was striving to compile a supportive spending package worth about 10 trillion yen ($92 billion).

The Shanghai Composite Index closed 0.1% lower, with China Yangtze Power and Ping An Insurance Group among the biggest drags. Profits at Chinese industrial companies fell for a third month, dropping by the most since at least 2011. India’s Sensex rose, heading for a fresh record, as Housing Development Finance and Kotak Mahindra Bank offered strong support.

As usual, the big topic of discussion, or rather diversion, was trade, even though China continues to slow not due to the trade war but its inability to stimulate a credit impulse, while the only reason why US stocks are at record highs is QE4.

“Something will come out of the phase one (Sino-U.S. trade) talks,” said TD Securities Senior Global Strategist James Rossiter. “Rolling back tariffs to where they were in August, with the December ones put on hold or canceled maybe.” But he said the two countries were unlikely to go beyond that, and China’s declining industrial profits underscored the economic strain exerted by the tensions.

Another signal of the rising market confidence was the VIX plunging to 7 month lows. It is now less than half the level it was in August, when U.S.-China talks looked close to collapsing, and a third of last December’s level when stock markets were pulled lower by trade angst and rising interest rates. Kay Van-Petersen, global macro strategist at Saxo Capital Markets in Singapore, said while Sino-U.S. trade headlines may be driving some tactical, near-term moves in the market, they were mostly just “noise”. And echoing what we said, the Saxo strategist said that the broader market direction is “about the accommodative Fed and accommodative monetary policy and the fact that structurally the meta-trend is still lower in yields and rates,” he said.

In FX, the dollar relentless levitation continued, and the greenback was stronger against developed and emerging currencies, with dollar/yen holding above 109 and euro/dollar steady at $1.10. That was despite softer-than-expected U.S. economic data on Tuesday, which showed a fourth straight monthly contraction in consumer confidence and an unexpected drop in new home sales in October. Sterling initially dropped then spiked as pre-election opinion polls showed some narrowing of the Conservative lead over opposition parties, although Prime Minister Boris Johnson is still favored gain an overall majority. The reaction to the polls squeeze has been modest as the prospect of another hung parliament raises the prospect of some form of coalition government made up of parties supporting a second Brexit referendum.

“So far, the market has been relatively complacent when it comes to the risks ahead,” said Thu Lan Nguyen, FX strategist at Commerzbank. “Yes, the Tories still have the lead, but they’re certainly not gaining.”

In emerging markets, traders were watching Brazil’s real, which fell to a record low, below the troughs of the 2015 recession, despite central bank intervention.

Among the main commodities, oil prices edged lower after reaching their highest since late September on the reassuring trade headlines. U.S. West Texas Intermediate crude was down 0.21% at $58.29 per barrel. Global benchmark Brent crude lost 0.11% to $64.20 per barrel.

Expected data include annualized GDP, durable-goods orders, and personal income and spending.

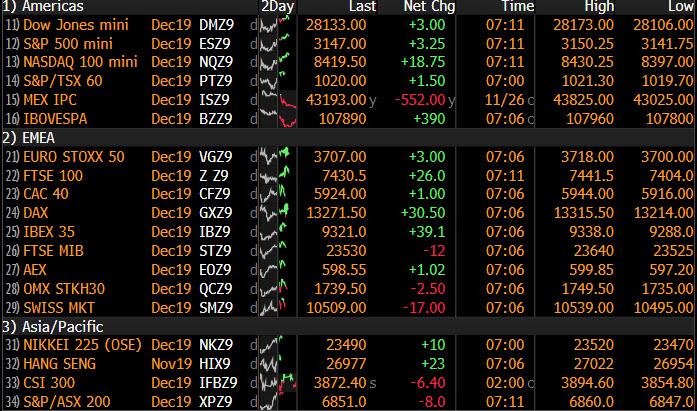

Market Snapshot

S&P 500 futures up 0.2% to 3,149.75

STOXX Europe 600 up 0.4% to 410.26

MXAP up 0.3% to 165.63

MXAPJ up 0.4% to 530.12

Nikkei up 0.3% to 23,437.77

Topix up 0.3% to 1,710.98

Hang Seng Index up 0.2% to 26,954.00

Shanghai Composite down 0.1% to 2,903.20

Sensex up 0.4% to 40,972.32

Australia S&P/ASX 200 up 0.9% to 6,850.60

Kospi up 0.3% to 2,127.85

German 10Y yield unchanged at -0.372%

Euro down 0.1% to $1.1006

Italian 10Y yield rose 0.6 bps to 0.824%

Spanish 10Y yield fell 0.7 bps to 0.382%

Brent futures up 0.3% to $64.46/bbl

Gold spot down 0.2% to $1,459.24

U.S. Dollar Index up 0.1% to 98.36

Top Overnight News

Global central banks are approaching the end of the year with a collective shudder at the risky behavior that their low interest-rate policies are encouraging. Policy makers from European Central Bank and the Federal Reserve are among those raising cautionary flags at potentially unsafe investing stoked by their efforts to flood economies with ultra-cheap money

President Donald Trump declared Tuesday that talks with China on the first phase of a trade deal were near completion after negotiators from both sides spoke by phone, signaling progress on an accord in the works for nearly two years

Profits at Chinese industrial enterprises fell for a third straight month, dropping by the most since at least 2011 as producer prices continue falling and domestic demand slows

China saw strong demand for its third offering of dollar bonds in three years, though U.S. investors largely left the deal alone amid the trade war. Fund managers were also a diminished presence from last year, with the bulk of the sale taken up by banks and the public sector — a group that includes central banks and sovereign wealth funds

The earliest-available indicators of China’s economic performance point to a continued slowdown in November. Economic growth was already the slowest in almost three decades in the third quarter

Elizabeth Warren’s steady rise in the polls has shifted into reverse as attacks from her Democratic rivals over her Medicare for All plan take a toll. A Quinnipiac poll released Tuesday found that Warren has dropped by 14 points since October, when she topped the field in the same poll. Joe Biden now has a clear lead and she is in a three-way statistical tie for second place with Pete Buttigieg and Bernie Sanders. Every other candidate had 3% support or less

A White House budget official said he warned his superiors that a hold on security assistance for Ukraine could be illegal, and he waited months for an explanation for the delay he described as unusual, according to transcripts released Tuesday

The road map for quantitative easing laid out by Reserve Bank of Australia Governor Philip Lowe is spurring a rally in the nation’s bonds as investors seize on his comments to bet on deeper interest-rate cuts

The earliest-available indicators of China’s economic performance point to a continued slowdown in November. Economic growth was already the slowest in almost three decades in the third quarter, and Bloomberg Economics’ gauge aggregating the earliest data from financial markets and businesses shows that continuing

U.K. Labour party leader Jeremy Corbyn accused Boris Johnson’s government of secretly negotiating with the U.S. over the National Health Service as he sought to shift the focus from a spat over antisemitism that has embroiled his campaign for next month’s election

Asian equity markets traded broadly firmer after Wall Street extended on record levels once again, but with gains capped given the lack of material breakthrough from the recent slew of optimistic US-China trade rhetoric and following a further slump in Chinese Industrial Profits. ASX 200 (+0.9%) and Nikkei 225 (+0.3%) were positive with notable strength in Australia’s telecoms sector as Telstra was boosted in anticipation of a stronger performance in H2 and with gold miners underpinned after the precious metal found relief from support at USD 1450/oz, while Tokyo sentiment rode on the recent upward trajectory in USD/JPY and with Toshiba lifted by prospects of a sooner return to the main market following reports the Tokyo Stock Exchange will ease requirements to fast-track promotion to the main board as soon as next year. Hang Seng (+0.2%) and Shanghai Comp. (-0.1%) were somewhat indecisive with Hong Kong kept afloat by hopes protests were waning and that the university siege may have drawn to an end, although the mainland was choppy due to continued PBoC liquidity inaction and after Industrial Profits further deteriorated with its largest decline since 2011. Finally, 10yr JGBs ignored the mostly positive tone in stocks and extended on the prior day’s post-40yr auction rebound to briefly test resistance at the 153.50 level, with prices also supported by the BoJ’s presence in the market today with the central bank’s Rinban operations heavily concentrated on 5yr-10yr maturities.

Top Asian News

Another Yield-Starved Japanese Bank Steps In to Buy CLOs

Westpac Still Under Fire as Advisers Say Directors Must Go

Investors in China Can’t Wait to Finally Own Alibaba Shares

Hong Kong Sets Record in $5 Billion Land Sale to Sun Hung Kai

Major European bourses (Euro Stoxx 50 +0.2%) are higher in quiet but choppy trade, as global equities continue to build on recent momentum amid elevated trade hopes since the latest US President Trump comments that trade talks are in the “final throes”. Meanwhile, month-end factors continue to distort price-action. Sectors are in the green across the board, with outperformance seen in Materials (+0.3%) and Consumer Discretionary (+0.3%). In terms of individual movers; British American Tobacco (+2.1%) nursed losses seen at the open after the Co. noted that it is on track for a strong year despite a slowdown in the US vaping market. Elsewhere today’s notable gainers include Aroundtown Properties (+2.5%) whose shares advanced after the Co. posted strong gains in both revenue and EBITDA. In terms of the laggards, Knorr Bremse (-3.5%) is under pressure after the Co. posted earnings that missed on top line expectations. Meanwhile, Rolls Royce (-1.5%) and Compass Group (-2.5%) are both lower following downgrades at Morgan Stanley and SocGen respectively. Taking a broader view, Barclays continue to see moderate upside for European equity markets in 2020, forecasting a further 9% of upside for the Euro Stoxx 50 by next year’s end. Although “the tactical risk-reward has become less appealing following the latest rally, as macro recovery and reducing policy uncertainty appear to be widely expected… light positioning, the relative expensiveness of ‘safe assets’, the positive delta in activity & earnings and the easier financial conditions argue for an extension of the equity bull market into 2020” the bank concludes.

Top European News

Better Macro Should Support European Stocks in 2020: Jefferies

Bain, Fortress, Apollo Consider Investing in Monte Paschi: MF

Lloyds to Cut Chief Executive Horta-Osorio’s Pension Award

Vodafone Wins German Court Backing in Price Fight With Elliott

In FX, The Dollar remains on a firm footing ahead of a packed US agenda with data front loaded and compressed due to Thursday’s Thanksgiving holiday. The Greenback is up vs most G10 rivals, albeit rangebound as the DXY meanders between 98.407-259 parameters, and just shy of resistance at 98.450. Back to today’s raft of releases, Q3 GDP and October core PCE are likely to headline, but durable goods may steal the limelight given the erratic nature of that series.

CAD/NZD/SEK/NOK – The major outliers and ‘outperformers’, as the Loonie maintains a degree of bullish technical momentum after Usd/Cad closed below the 200 DMA on Tuesday (1.3278) and the Kiwi benefits from favourable cross-winds with Aud/Nzd pivoting 1.0550 and Nzd/Usd holding relatively firmly above 0.6400 having largely shrugged off or taken in stride comments from RBNZ Governor Orr, the latest FSR and NZ trade data. Similarly, the Scandi Crowns have not really sustained serious or lasting damage from a dip in Swedish household lending, flip from trade surplus to a deficit twice the size or rise in the unofficial Norwegian survey-based jobless rate, as Eur/Sek tests support at 10.5500 and Eur/Nok straddles 10.1000.

GBP/AUD/JPY/CHF/EUR – The Pound has recovered pretty well if not impressively from early weakness and a breach of yesterday’s low (circa 1.2835) that seemed partly Eur/Gbp related amidst reports of RHS demand for the end of November. Indeed, Cable has bounced ahead of last Friday’s base (around 1.2822) towards 1.2885 and eclipsing the 21 DMA (1.2881) and the cross is back near 0.8650 having climbed to within a few pips of its 21 DMA (0.8587), as Eur/Usd hovers just above 1.1000. Note, hefty options expire close by (2 bn from 1.0995-1.1000 and 1.1 bn between 1.1035-40), while a key Fib (1.0994) is also keeping the single currency in narrow confines. Elsewhere, broadly risk-on sentiment amidst latest positive US-China trade chat (phase 1 deal in final throes per President Trump) is capping the Yen and Franc just under 109.00 and over parity respectively, with expiry interest also in proximity for Usd/Jpy (3.3 bn from 108.95-109.00 and 1 bn at 109.15). Back down under, a couple of dovish RBA calls vs 1 less dovish has weighed on Aud/Usd and protected a serious approach on 0.6800, but the pair is holding above 1bn expiries between 0.6760-75.

RBNZ Financial Stability Report noted that New Zealand’s financial system is resilient to a range of economic risks although global financial stability risks and domestic debt vulnerabilities remain, while it added that prolonged low long-term interest rates could generate excess leverage and overheated asset prices. Furthermore, the RBNZ stated negative OCR is not currently a central scenario in its published forecasts and it is considering potential impacts of unconventional monetary policy tools on bank profitability.

In commodities, the crude complex is slightly firmer, with Brent Feb’ 20 futures making fresh weekly highs above yesterday’s high (around USD 64.30/bbl) , as the market rebounds from overnight post bearish API inventory data lows as it opts to instead take its cue from better risk appetite spurred by trade hopes. Looking ahead, attention will be on EIA inventory data, where weekly crude stocks are seen drawing by 347k barrels, although if EIA crude stocks follow API’s lead and print a surprise build, this would mark a fifth straight week of builds. It is also the first day of the OPEC Economic Commission Board Meeting, which ends tomorrow, after which the board may provide policy recommendations to OPEC – although the recommendations are non-binding. Elsewhere, eyes turn to Libya following reports of military action around the El-Feel oilfield (circa. 100k BPD capacity), although no damage or production halts have been reported, the organisation stated that an escalation in violence could prompt evacuations and production shut-down. Looking at metals, gold prices continue to be subdued from lack of haven demand, with prices having briefly slipped below the USD 1460/oz mark. Meanwhile, copper prices continue to gain traction, as positive trade feels spur macro risk appetite, although prices did take a fleeting hit during overnight trade in the wake of abysmal IP data out of China.

US Event Calendar

8:30am: GDP Annualized QoQ, est. 1.9%, prior 1.9%

Personal Consumption, est. 2.8%, prior 2.9%

Core PCE QoQ, est. 2.2%, prior 2.2%

8:30am: Durable Goods Orders, est. -0.9%, prior -1.2%; Cap Goods Orders Nondef Ex Air, est. -0.2%, prior -0.6%

8:30am: Cap Goods Ship Nondef Ex Air, est. -0.2%, prior -0.7%

8:30am: Initial Jobless Claims, est. 220,500, prior 227,000; Continuing Claims, est. 1.69m, prior 1.7m

8:30am: Durables Ex Transportation, est. 0.1%, prior -0.4%

9:45am: MNI Chicago PMI, est. 47, prior 43.2

10am: Personal Income, est. 0.3%, prior 0.3%; Personal Spending, est. 0.3%, prior 0.2%

10am: PCE Deflator MoM, est. 0.27%, prior 0.0%; PCE Deflator YoY, est. 1.4%, prior 1.3%

10am: PCE Core Deflator MoM, est. 0.11%, prior 0.0%; PCE Core Deflator YoY, est. 1.7%, prior 1.7%

10am: Pending Home Sales MoM, est. 0.2%, prior 1.5%; Pending Home Sales NSA YoY, est. 6.0%, prior 6.3%

2pm: U.S. Federal Reserve Releases Beige Book

DB’s Jim Reid concludes the overnight wrap

I was on Bloomberg TV yesterday and one comment I made that had a few people asking me questions was the one where I said that I thought nominal yields will stay below nominal GDP for the rest of my career. I truly believe this is the only way of supporting the existing colossal global debt burden and what is likely to be more debt in the future. Central banks will end up being forced to own a lot more bonds as far as the eye can see to facilitate this but I do think both will eventually be forced higher by policy. Clearly for reasons of which I’m not aware of, my career might not have long left but given a new house this year, building renovations that cost the original estimate times Pi, and school/university fees into the 2040s that’s how long I might need to work and how long I think this period of financial repression might need to last. We talk about this a lot in this year’s long-term study on debt. See here for a reminder.

Today markets will wind down ahead of Thanksgiving tomorrow but this means that a number of important US releases are shoe-horned into one day. We’ll get the second reading for third-quarter GDP, which is expected to show no change to the headline number of 1.9% growth, though there are expectations for a 0.1pp downgrade to consumption. We’ll also get durable and capital goods orders for October, which are expected to decline a bit further month-on-month (by -0.9% and -0.2%, respectively) but watch for the impact of the GM strikes. Apart from the national accounts data, core PCE prices for October will be released, which should show below-target inflation of 1.7%, and the Chicago PMI is expected to rise +3.8pts to 47.0 after it hit its lowest level since 2015 last month at 43.2. We’ll also get the biggest opinion poll and subsequent seat model forecast of the U.K. election campaign so far tonight (more on this below).

Ahead of all this, it was another day of edging to fresh record highs for markets, with the S&P 500 (+0.22%), the NASDAQ (+0.18%) and the DOW (+0.20%) all advancing to new highs in response to yesterday’s news that there had been a phone call between the US and Chinese negotiators. It was a similar story in Europe, with the STOXX 600 up +0.10% at its highest level since May 2015. Trade-sensitive indices fell back, however, with the Philadelphia semiconductor index down -0.50%. That move came despite an assertion by President Trump that the two sides are in the “final throes” of negotiations, possibly as concerns intensified over the recently-passed Hong Kong bill, which President Trump has neither confirmed nor denied that he will sign. If he does not sign or veto the bill by December 3, it will become law regardless.

Meanwhile, after the US markets closed, President Trump said in an interview for former Fox News Bill O’Reilly’s website that he’s holding up the trade deal to ensure better terms for the US while saying, “We can’t make a deal that’s like, even. We have to make a deal where we do much better, because we have to catch up.” President Trump also spoke of Hong Kong in the interview and said that the US wanted to see things “go well in Hong Kong” while adding that he was confident of a good outcome.

Overnight, the US Department of Commerce has released an advanced notice for proposed rulemaking (ANPRM) that will implement last May’s executive order on information and communications technology and services supply chain security. Also of note is that it did not name China as an “adversary nation”, as suggested in an earlier draft.

A quick refresh of our screens this morning show that Asian markets are mostly trading up with the Nikkei (+0.45%), Shanghai Comp (+0.07%) and Kospi (+0.42%) all higher while the Hang Seng is trading flat. As for FX, all the G10 currencies are trading weak against the dollar with the Australian dollar (-0.21%) leading the declines. Elsewhere, futures on the S&P 500 are up +0.06% while WTI crude oil prices are down -0.21% after a report from the American Petroleum Institute indicated that US crude inventories increased by 3.64mn barrels last week. As for overnight data releases, China’s October industrial profits declined by -9.9% yoy (-5.3% yoy last month), the largest decline in the 8 years we can find data at this time of the morning. However, the series is quite volatile in nature.

In other news, S&P said in an overnight report that Australia’s AAA credit rating – one of only 11 in the world – would come under increased “downward pressure” if the government opted to deploy fiscal stimulus that changed the trajectory of the budget while adding that the top ranking is reliant on “strong fiscal outcomes.” This perhaps helps to explain the Australian government’s determination to return to a balanced budget in the backdrop of a slowing economy.

Back to yesterday and it’s worth highlighting that volatility has now returned to very low levels, with the VIX index down by -0.12pt to 11.75 – its lowest level since October 2018, while in Europe the V2X was down -0.29pts to 12.10pts – just 1.1pts off its low for the year.

Sovereign bonds also advanced on both sides of the Atlantic, with 10yr Treasury yields down -1.9bps to 1.736%. However, the 2s10s curve snapped a run of 9 successive sessions flatter as the curve steepened by +1.1bps with 2yr yields -2.8bps. Yields fell in Europe too, with 10yr bunds (-2.4bps), OATs (-2.3bps) and gilts (-4.4bps) all lower. Bank stocks underperformed as a result, with the STOXX Banks index down -0.66%, and the S&P Banks industry group down -0.31%.

Possibly supporting the bull steepening move were comments from Fed Governor Brainard, who explicitly said that she supports a form of yield curve control targeted at the front end of the yield curve. Her proposal would cap front-end Treasury yields to reinforce forward guidance and ideally drive down longer-end rates as a result. She says that this policy would be better than outright QE, though she did say that she would support QE in a severe downturn. Brainard also committed to supporting a flexible inflation target, to “anchor inflation expectations at 2 per cent by achieving inflation outcomes that average 2 per cent over time or over the cycle.” Such a change in the Fed’s target appears increasingly likely as a result of their ongoing policy review.

Earlier in the day, Dallas Fed President Kaplan said that “I think policy is in the right place now”, but also said that “We think the fourth quarter is going to be weak”. Kaplan is going to be a voting member on the FOMC next year. He expects growth around 2% for 2020, and would likely need to see a downside surprise versus that figure before supporting any change in policy.

In FX markets, sterling fell -0.26% yesterday as narrowing opinion poll leads for the Conservatives led to investor concern that there might be continued uncertainty over Brexit moving forward into next year. Following Monday’s ICM poll which had a 7pt Tory lead, yesterday morning saw another from Kantar with the lead falling from 18pts to 11pt lead in a week. As such sterling moved from being the best performing G10 currency on Monday to the worst yesterday. A YouGov poll later also showed an 11pt lead, only down 1pt since Friday.

Tonight, market attention will be on the release of YouGov’s MRP (multilevel regression and post-stratification) model at 10pm GMT, used to forecast the result. At the last election, this model predicted a hung Parliament over a week before the elections in contrast to expectations that there’d be a larger Conservative majority, so it’ll be fascinating to see if it’s forecasting any surprises this time round (albeit slightly further out from polling).

Staying with FX, the Brazilian Real depreciated -0.17% to its weakest-ever level against the dollar yesterday, in spite of intervention from the central bank. The move came after Brazil’s Economy Minister commented that a weaker currency is not a problem. Meanwhile, The Brazilian central bank has embarked on a series of rate cuts recently, with 50bp reductions at each of the last 3 meetings. Added to this has been general concerns over political stability in Latin America in light of recent protests across the continent, while former President Lula’s release from prison has raised the prospects of a more radical, populist left-wing government further down the line as he re-enters the political fray. Overnight, Brazil’s central bank chief Roberto Campos Neto has said that the central bank will intervene further if they need to normalize the foreign exchange market.

Sticking with LatAm, yesterday Chile’s central bank said that it will hold its next monetary policy decision two days earlier than scheduled in a bid to provide “timely information” about the country’s economic situation following weeks of social unrest. The central bank will now make the rate decision on December 4 (earlier December 6) and present their quarterly monetary policy report, known as the IPOM, the next day at 8:30 am (earlier December 9).

Elsewhere, the dollar weakened -0.07% after 5 days of gains, while bitcoin (-1.22%) fell for a 10th consecutive session against the dollar, with the latter falling to its lowest level since May.

In terms of data out yesterday, the Conference Board’s consumer confidence reading came in slightly below consensus at 125.5 (vs. 127.0 expected), although the previous month’s reading was revised up by two-tenths. The present situation reading fell to a 5-month low of 166.9, although the expectations indicator rose to 97.9. Looking at the labour market indicators, the differential between those saying jobs were “plentiful” and jobs were “hard to get” fell to 32.1 (vs. 36.1 previously), also at a 5-month low.

Other US data releases included new home sales beating expectations in October, coming in at a seasonally adjusted annual rate of 733k (vs. 705k expected), while the previous month was revised up by +37k to 738k. That means that new home sales have had their best two months in over 12 years and adds to a run of strong data on the US housing market. Elsewhere, the Richmond Fed’s manufacturing survey fell to -1 (vs. 5 expected), and amidst the ongoing trade war, the advanced goods trade deficit for the US fell to $66.5bn in October (vs. $71.0bn expected), its lowest level since May 2018.

In Europe, the main data out yesterday was the GfK consumer confidence reading from Germany, with the December forecast up to 9.7 (vs. 9.6 expected). More notable, however, was the expectations indicator, which rose to 1.7 in November, up from -13.8 the previous month, which was the biggest single-month increase in expectations since July 2010.

To the day ahead now, and this morning’s data include French consumer confidence for November, along with Italian consumer confidence, manufacturing confidence and economic sentiment for the month. Meanwhile, ahead of tomorrow’s Thanksgiving holiday we have a raft of US data releases, including the second reading of Q3 GDP, along with personal consumption and core PCE. Then there’s the preliminary October reading of durable goods orders and non-defence capital goods orders. And to round it off, there’s the MNI Chicago PMI reading for November, personal income and spending data for October, pending home sales for October, and the weekly initial jobless claims and MBA mortgage applications. Turning to central banks, the Fed will be releasing their Beige Book, while we’ll hear from the ECB’s Lane again.

Rabobank: “Global Central-Bankery Continues To Go Where No-One Has Gone Before”

Submitted by Michael Every of Rabobank

Stocks at new recorder record highs; bonds up (yields down); CNY up; broad USD DXY up; China issuing USD6bn of sovereign debt at a narrow spread over USTs….it’s all up, up, and away. And why not? Trump tells us the US is “in the final throes” of a phase one trade deal with China. Usually that language is used to imply something is dying, but hey ho, decimate is used to mean annihilation rather than killing one in ten of the enemy, and quantum leap is used to imply something big when it actually means something amazingly small. Suffice to say markets loved it. So much so in fact that it is a song we should keep singing over and over, like another ‘final’- “The Final Countdown”.

Three decades after Europe’s pop-metal kitsch classic first hit the charts, they are still out there playing it, and whenever anyone hears the keyboard intro “Deedle deedle….deedle dee”, everyone knows the song and joins in enthusiastically: how can you not? As such, I suggest that from now on, every time the White House talks about the impending phase one trade deal coming soon, to save time they just play the track for the press. Or just the keyboard intro. And rallying markets can continue to trade off the deep wisdom of the lyrics:

“We’re leaving together; But still it’s farewell; And maybe we’ll come back; To earth, who can tell?

I guess there is no one to blame; We’re leaving ground (leaving ground); Will things ever be the same again?

It’s the final countdown; The final countdown”

And indeed, will things ever be the same again in markets? Not just because of the constant dangled promise of a trade deal that the vast majority of those working in those same markets admit is unlikely to mean much of anything; but because global central-bankery continues to go where no-one has gone before. Mass asset-purchases; negative rates; ‘Not-QE’; yield curve control–Brainard says the Fed should use asset purchases to cap yields on short- and medium-term Treasuries, a-la BOJ, where it hasn’t worked, of course–and, shortly no doubt, solving the global climate crisis and inequality! In their special central-bank minds, *this* is the voyage all the rest of us are mere passengers on:

“We’re heading for Venus (Venus); And still we stand tall; ‘Cause maybe they’ve seen us (seen us); And welcome us all, yeah

With so many light years to go; And things to be found (to be found); I’m sure that we’ll all miss her so…”

But then back to that trade deal:

“It’s the final countdown; The final countdown; The final countdown; The final countdown; Oh, The final countdown, oh It’s the final count down; The final countdown; The final countdown; The final countdown; Oh; It’s the final count down.”

And then back to central banks and that trade deal working together:

“We’re leaving together; The final count down; We’ll all miss her so; It’s the final countdown; It’s the final countdown; Oh; It’s the final countdown, yeah.”

Schiff Hits The Fan: First House Democrat Publicly Opposes Impeachment

With public support for impeachment waning and the risk of a potentially disastrous Senate trial looming, House Democrats have suffered their first impeachment defection after Rep. Brenda Lawrence of Michigan said she no longer supports the effort.

“We are so close to an election. I will tell you, sitting here knowing how divided this country is, I don’t see the value of taking him out of office,” said Lawrence, who instead favors censuring President Trump over allegations that he withheld military aid in Ukraine for self-serving purposes, according to the Washington Examiner.

“I do see the value of putting down a marker saying his behavior is not acceptable.“

“I want to censure. I want it on the record that the House of Representatives did their job and they told this president and any president coming behind him that this is unacceptable behavior and, under our Constitution, we will not allow it,” Lawrence continued.

Lawrence backed the House inquiry as recently as early October, but changed her tune after recent polls reveal a drop in public support for impeachment following weeks of televised testimony from hand-picked witnesses who were unable to conclude that Trump withheld Ukraine aid in a quid pro quo, extortion, or any other phrase that polled well.

According to the FiveThirtyEight average of national polls, support for impeachment has shrunk from 50.3 percent in mid-October to 46.3 percent presently, while opposition has risen from 43.8 percent to 45.6 percent.

Among independents in the FiveThirtyEight average, support for impeachment topped out at 47.7 percent in late October but has sunk to 41 percent over the past three weeks. –The Hill

Maybe, but too many of them are afraid their offices and homes would soon be like halftime at the Yale-Harvard game. https://t.co/30lUkpX401

An impeachment in the House would mean a trial in the GOP-controlled Senate, where witnesses such as Joe and Hunter Biden, Devon Archer, John Kerry’s Stepson and Ukrainian officials would be fair game as Republicans slow-walk America through allegations that the former Vice President and his son were engaged in a pay-for-play political racket.

Base will melt if they don’t impeach. But it’s a political boondoggle if they do.

Mexico Pushes Back Against Trump Plan To Label Cartels Terror Groups

Mexican officials are sounding the alarm after President Trump told Bill O’Reilly during a radio interview that he would “absolutely” designate Mexico’s drug cartels as terror groups.

During the interview, which aired for the first time last night and will re-air on Thanksgiving Day, Trump told O’Reilly, who first raised the issue, that he has been working on getting the cartels designated a terror group for the past 90 days, which means the project began before the murder of 9 US citizens in a drug-cartel ambush that killed three mothers and six young children.

Here’s a clip from the interview:

After the attack on members of the LaBaron family – a Mormon community that has been living in Mexico since the 1940s – Trump tweeted an offer of assistance to Mexco’s president, saying the US would be happy to supply troops or ‘whatever it takes’ to wipe out the cartels once and for all.

Now, Trump is weighing a terrorist designation for the cartels, which could open the door for American cross-border attacks on cartel infrastructure and cartel personnel.

According to the Washington Post, under US law, any violent foreign group or individual who “threatens American security” can be designated a terror group and be subjected to sanctions that, in this case, could seriously disrupt commerce between American and Mexican companies.

It’s also a huge problem for the banks, as anybody who remembers the $900 million money laundering scandal involving UK-based HSBC back in 2012, when the bank got caught laundering money for the drug cartels (the incident is now the subject of a Netflix documentary) and paid a massive fine (the bank has also been subjected to several civil suits).

A terror designation would seriously raise the stakes for any banks who risk handling cartel money.

Unsurprisingly, Mexico is less than thrilled about the prospect of an American crackdown on the cartels.

Mexican Foreign Minister Marcelo Ebrard tweeted the government’s “position”: “Mexico will never accept any action that violates our national sovereignty…We will act firmly. I have sent our position to the US as well as our resolution on combating transnational organized crime.”

That’s hardly surprising, since turning to the Americans to fix Mexico’s problems would almost certainly be extremely politically unpopular for AMLO, whose popularity has already taken a dive since he took office. But with Mexico’s murder rate about to hit a new record high – a stunning development, since AMLO’s decision to end the government’s war on the cartels was supposed to lead to a deescalation of violence – the pressure is on for him to do something.

Of course, this wouldn’t be the first time President Trump has threatened to crack whip on Mexico (remember his threats to close the border, or his decision to send US troops to provide more support for border agents?).

It was long believed in the gold space that Western central banks are against gold, but things have changed, for quite some years now. Instead of discouraging people from buying gold, or convincing them that gold is an irrelevant asset, many of these central banks are increasingly honest about the true properties of this monetary metal. Stating that gold is the ultimate store of value, that it preserves its purchasing power through time and is a global means of payment. Such statements, combined with actions that will be discussed below, reveal that more and more central banks are preparing for plan B.

The Bundesbank (the German central bank) published a book last year named Germany’s Gold. In the introduction, written by the President of the Bundesbank Jens Weidmann, the view of this bank leaves no room for interpretation. Weidmann writes (emphasis mine):

Ask anyone in Germany what they associate with gold and, more often than not, they will say that it is synonymous with enduring value and economic prosperity.

Ask us at the Bundesbank what our gold holdings mean for us and we will tell you that, first and foremost, they make up a very large share of Germany’s reserve assets … [and they] are a major anchor underpinning confidence in the intrinsic value of the Bundesbank’s balance sheet.

The Bundesbank produced this publication to give a detailed account, the first of its kind, of how gold has grown in importance over the course of history, first as medium of payment, later as the bedrock of stability for the international monetary system.

Finally got my hands on an English copy of Gold, published by the German central bank. Something tells me the Bundesbank is pro gold.

For Keynesians these comments might read like the Bundesbank (BuBa) is a “goldbug.” Its remarks, however, are simply common sense. Gold has enduring value. The world over it is associated with economic prosperity. Every reserve currency in the world today is underpinned by vast gold reserves. Otherwise, monetary authorities wouldn’t trust holding the respective currencies, next to holding their own gold reserves. Gold truly is the bedrock of stability for the international monetary system.

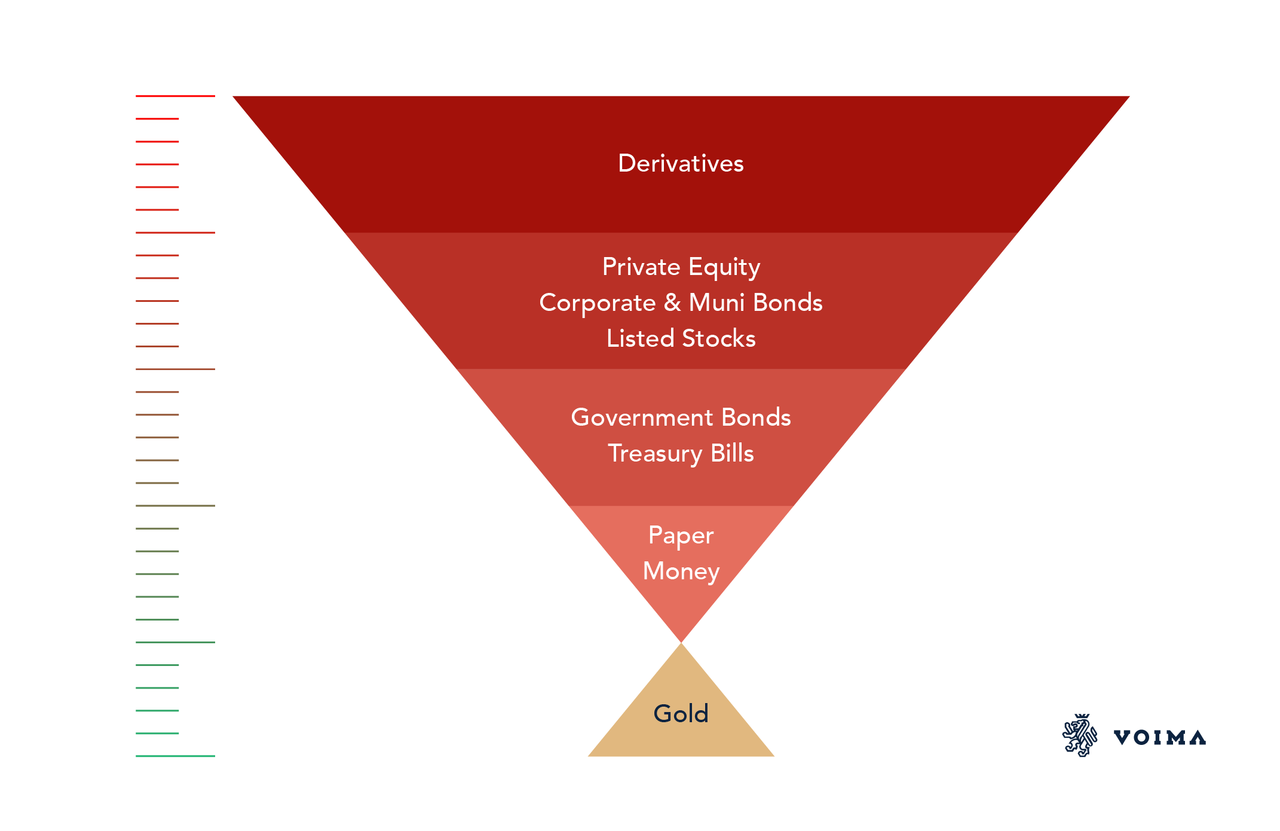

Central Banks and Exter’s Pyramid

What springs to mind when reading Weidmann’s statement is Exter’s Inverse Pyramid. John Exter was an American economist that in the 1960s conceived an upended pyramid of financial assets. Underneath the pyramid is gold that forms the base of most reliable value; all asset classes within the pyramid on progressively higher levels involve more risk. Exter would sometimes refer to his model as the debt pyramid; hence, he positioned gold outside of it as it’s the only asset that has no liability against it.

Tellingly, when Exter addressed the Economic Society of South Africa in Johannesburg on November 16, 1966, he said (source):

Gold is the hard core of our international monetary system.

“Bedrock” (Weidmann) and “hard core” (Exter) are similar, and both point to gold’s strength and what it can carry. An essential element of capitalism is investing—directly, indirectly, through bonds or equity—that involves risk. The higher the risk, the higher the return. The lower the risk, the lower the return. What falls outside of the investment realm has zero risk and no return, but provides the base that carries the debt system. This safe haven is gold, the only asset refuge that has no counterparty risk.

In the Balance of Payments and International Investment Position Manual (BPM6) drafted by the International Monetary Fund (IMF), we read:

Financial assets are economic assets that are financial instruments. Financial assets include financial claims and monetary gold held in the form of gold bullion … A financial claim is a financial instrument that has a counterpart liability. Gold bullion is not a claim and does not have a corresponding liability. It is treated as a financial asset, however, because of its special role as a means of financial exchange in international payments by monetary authorities and as a reserve asset held by monetary authorities.

The IMF considers all financial assets to have counterparty risk, except gold.

On page 112 of BPM6 the IMF lists all international reserve assets by descending order. Crowning the lineup is physical gold, followed by cash, debt securities, equity, and finally derivatives. Nearly an exact copy of Exter’s Pyramid.

Another appearance of the pyramid can be found on the website of the Dutch central bank, De Nederlandsche Bank (DNB). Since April 2019 DNB’s gold information page reads:

A bar of gold always retains its value, crisis or no crisis. This creates a sense of security.

Shares, bonds and other securities are not without risk, and prices can go down. But a bar of gold retains its value, even in times of crisis. That is why central banks, including DNB, have traditionally held considerable amounts of gold. Gold is the perfect piggy bank—it’s the anchor of trust for the financial system. If the system collapses, the gold stock can serve as a basis to build it up again. Gold bolsters confidence in the stability of the central bank’s balance sheet and creates a sense of security.

Exter’s pyramid all over. Kindly note the similarity between DNB’s and BuBa’s comments on gold providing essential confidence in their balance sheets. It goes to show these two central banks have a long history of cooperating.

I tweeted about DNB’s candid approach last April (a few months later, it went viral).

Remarkably candid stance on gold by Dutch central bank:

‘Gold is the perfect piggy bank – it’s the anchor of trust for the financial system. If the system collapses, the gold stock can serve as a basis to build it up again.’

Let’s continue with another quote, this time from the Bank of Finland (BOF):

Gold – The basis of a monetary system

Gold is called the eternal payment instrument and has been used as a medium of exchange for thousands of years. Gold is a genuinely global means of payment that has maintained its value throughout history.

Gold is a highly sought-after precious metal, considered to be the ultimate store of value.

All central banks quoted agree gold preserves its purchasing power through time.

Preparing for Plan B

Next to strong statements by central banks, they’re acting accordingly. Shortly after the Great Financial Crisis (GFC), central banks as a sector became net buyers; and Germany, the Netherlands, Austria, Hungary and Turkey, among others, repatriated gold. Mainly from the Bank of England in London and the Federal Reserve Bank of New York.

According to BuBa, their repatriation scheme had three objectives: cost efficiency, security, and liquidity. Cost efficiency is about the storage costs in every location. Security involves the safety of the vaults and where those vaults are. The current trend is to have a significant fraction of gold on home soil due to the geopolitical environment. Liquidity is about owning bars that adhere to prevailing industry standards and are located in liquid marketplaces such as London, i.e., to make payments in times of changes in the financial system. This latter aspect deserves special attention.

As we’ve seen, Western monetary authorities mention gold to be, “the anchor of trust for the financial system,” “the bedrock of stability for the international monetary system,” and, “a genuinely global means of payment.” They’re also saying that “if the system collapses, the gold stock can serve as a basis to build it up again.” One wonders if these entities are preparing for a new type of international gold standard. They see it as one possible outcome, as in recent years, several central banks have upgraded their gold reserves to current gold industry standards, also referred to as London Good Delivery.

Throughout history, bars of different purities were traded in wholesale markets. By 1954 every new bar accepted in the London Bullion Market—the center of gold trade since the 18th century—was required to be at least 995 parts per thousand fine and weighing in between 350 and 430 fine troy ounces. Although not every old bar was promptly upgraded. Some remained as they were, in vaults in London and other places. These bars now trade a at discount, usually equal to the cost of upgrading and, if necessary, transporting them to London.

After the GFC many central banks were holding bars that were cast before 1954, which are currently not liquid in wholesale markets. In response, the French, Swedish and German central bank, that I know of, have upgraded their gold reserves to solve this liquidity issue.

Since 2009, the Banque de France has been engaged in an ambitious programme to upgrade the quality of its gold reserves. The target is to ensure that all its bars comply with LBMA [London Bullion Market Association] standards so that they can be traded on an international market.

To ensure that the Riksbank has the most liquid gold reserve possible, in 2017 the Riksbank upgraded the part of its gold reserve that did not meet the LGD [London Good Delivery] standard by replacing these bars with new gold bars that do meet the standard.

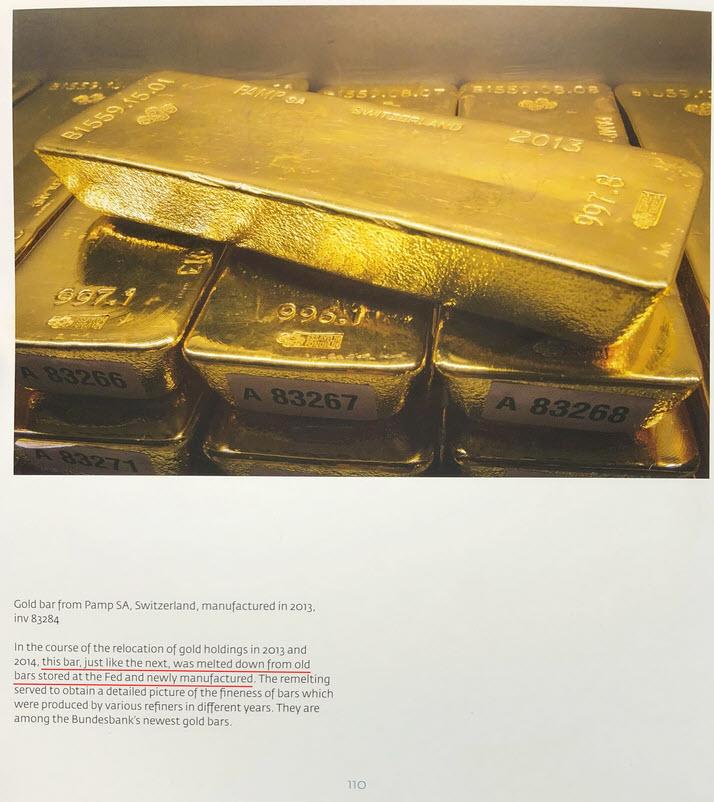

I don’t have a quote from BuBa itself on their upgrade operation. However, connecting a few dots uncovers when and how they did it. BuBa released a bar list in 2015 disclosing all their gold to be 995 fine or higher. In the book Germany’s Gold, a bar is displayed on page 110 with the subscription:

In the course of the relocation [repatriating] of gold holdings in 2013 and 2014, this bar … was melted down from old bars stored at the Fed and newly manufactured. The remelting served to obtain a detailed picture of the fineness of bars which were produced by various refiners in different years. They are among the Bundesbank’s newest gold bars.

While BuBa states this bar was melted for assaying purposes, in reality, it was part of making their entire stack at least 995 fine. One, because it doesn’t require melting a whole bar for assay testing. Two, on November 11, 2017, the Financial Times published an article on how BuBa repatriated its gold. The article states:

more than 4,400 bars transferred from New York were taken to Switzerland, where two smelters remoulded the bullion into bars that meet London Good Delivery standards for ease of handling.

Just like that one bar wasn’t melted to ‘obtain a detailed picture of the fineness,’ an additional 4,399 bars weren’t melted ‘for ease of handling.’ They were all refined for one reason: to meet London Good Delivery criteria and make Germany’s gold reserves wholly liquid.

Conclusion

According to John Exter, when the debt pyramid has grown in excess and becomes unstable, bubbles burst. Investors, seeking safety, will run down the ladder until they find solid ground (the bedrock). This foundation is gold, which can’t default or be arbitrarily devalued.

The GFC was caused by too much debt (a credit binge). When Lehman fell, and the house of cards came crumbling down, the quickest solution authorities could think of, ironically, was more debt. We went from “extend and pretend” to “delay and pray.” Central bank intervention can be effective, for a while, until the underlying problem resurfaces with a vengeance. Presently the world is more in debt than before the GFC. The Institute of International Finance estimates global debt to GDP is now 320%.

When reading the mainstream media, one can be persuaded to think all central banks are willing to “print” money to infinity and lower interest rates as far as they can—or launch a variety of the same—pushing us further into the abyss. Some of them, though, aren’t that ignorant and are actively preparing for when paper currencies are forced to be devalued by the weight of debt issued in said currencies.

There’s one more development at a Western central bank I like to share. The Banque de France—whose vaults were a vibrant part of the global gold market during the classical gold standard—has not only upgraded its metal but also enhanced its entire vaulting infrastructure since the GFC. From BDF:

Since the 2008 financial crisis, there has been renewed interest in gold from reserve managers.

As well as upgrading its stock, the Banque de France is taking various other steps to ensure it meets LBMA criteria [these standards apply for trading across the globe] … The renovation of the historical vaults housing the gold reserves has nearly been completed: the floor will be able to support heavy forklift trucks, and intermediary shelves have been inserted between the existing shelves to ensure the gold is only stacked five bars high, making handling easier. Other storage facilities will be available soon: either strong rooms for storing bare bars on shelves or large vaults to store sealed pallets, facilitate handling, transportation and auditing. By the end of the year, a new IT system will be in place to improve our ability to respond to market operation needs and other custody services.

So, after the GFC, not only have Western central banks changed the way they talk about gold—that is, they have become more honest regarding gold’s function as a safe haven—but, as a sector, central banks have also become net buyers. Many central banks have redistributed their gold, carefully considering all possible future risks and developments. A few central banks have upgraded their gold to current industry standards to be able to trade frictionless in international markets. One central bank, BDF, has even enhanced its entire vaulting infrastructure. And this is just based upon publicly available information.

We’re all too familiar with central banks in the East openly buying gold, stimulating citizens to buy gold, setting up new gold exchanges, and de-dollarizing. In the West, these subjects are more sensitive for political reasons. As a result, since the GFC, Western central banks gently started moving towards gold, not to cause any shocks in the market. In 2015, I called this “the slow development towards gold,” and it’s continuing still.

It’s beyond the scope of this article to discuss every probable international monetary development and attribute a percentage chance to each of them. I think it’s clear though, that many central banks are preparing for gold to play a resolving and pivotal role in future global finance. Why else buy, redistribute and upgrade gold, next to enhance trading facilities, increase transparency and then advertise gold’s financial features? Keep in mind what Pericles said around 500 BC, “the key is not to predict the future but to prepare for it.”

Currently, Exter’s Pyramid has grown too big and is unstable. The moment the pyramid falls, “gold will do its job.” History teaches us gold protects its owners through all types of weather, and central banks know this. Ever wondered why virtually every central bank owns gold? Because gold is physical. Immutable, yet divisible. Independent and without counterparty risk. It is the ultimate store of value—as it retains its purchasing power through time—and works as an eternal payment instrument.

The Santa Clara, California, district attorney’s office says it is investigating a prosecutor police say used his daughter as bait to find a man now charged with molesting her. Ali Mohammad Lajmiri has been charged with lewd and lascivious acts on a minor under the age of 14 years, lewd and lascivious acts on a minor under the age of 14 years by the use of force, violence, duress, menace or fear and false imprisonment for molesting the 13-year-old girl while she walked her dog. Police say that her father brought her back to the scene of the attack several times, hoping to catching Lajmiri. He finally succeeded, but not before Lajmiri reportedly pulled the girl onto a bench and kissed the top of her head before she was able to get away. According to the police report, the father directed his daughter to walk back and forth along a wooded trail and to let Lajmiri touch her if she encountered him again.

from Latest – Reason.com https://ift.tt/2DmXlKO

via IFTTT

Rare Jewels Stolen In Historic Heist Valued At More Than $1 Billion, German Police Say

Police in Dresden have finally released the first images of the jewels stolen in a brazen robbery of the Green Vault, which houses the Saxon Royal Collection, one of the most valuable collections of jewels on the planet.

At least two thieves participated in the heist, the biggest museum theft in Germany since the Second World War, and possibly the largest in German history. Police haven’t released much information, though they did say that two men smashed a display case, grabbed the jewels and ran. The two are also believed to have set a fire nearby to distract authorities.

Though the most of the invaluable collection remains intact, the thieves managed to abscond with a stash of jewels valued at more than $1 billion, according to the police.

Among other items, the stash includes a jewel- encrusted sword and scabbard, as well as bejeweled clasps, epaulettes, brooches, buckles and other essential 18th-cetury pieces.

Below are photos of some of the bigger pieces (via CNN):

Diamond hat clasp:

Comprised of 15 large diamonds and more than 100 smaller stones.

Diamond Epaulette:

Made for Frederick Augustus III, this piece is comprised of more than 200 diamonds.

Order of the White Eagle

A medal honoring a member of a prestigious Polish order.

Sword & Scabbard:

The pressure is on for the police to find the stolen jewels, since the Saxon state government neglected to insure the collection (very un-German of them), leaving the state on the hook for the loss unless the gems are recovered unharmed, according to Bloomberg.

Police are saying that the theft took just minutes, with the thieves simply smashing a display case and running.

Anyone with information about the heist, or the jewels’ current whereabouts, is encouraged to contact the Saxony Police.

The Santa Clara, California, district attorney’s office says it is investigating a prosecutor police say used his daughter as bait to find a man now charged with molesting her. Ali Mohammad Lajmiri has been charged with lewd and lascivious acts on a minor under the age of 14 years, lewd and lascivious acts on a minor under the age of 14 years by the use of force, violence, duress, menace or fear and false imprisonment for molesting the 13-year-old girl while she walked her dog. Police say that her father brought her back to the scene of the attack several times, hoping to catching Lajmiri. He finally succeeded, but not before Lajmiri reportedly pulled the girl onto a bench and kissed the top of her head before she was able to get away. According to the police report, the father directed his daughter to walk back and forth along a wooded trail and to let Lajmiri touch her if she encountered him again.

from Latest – Reason.com https://ift.tt/2DmXlKO

via IFTTT