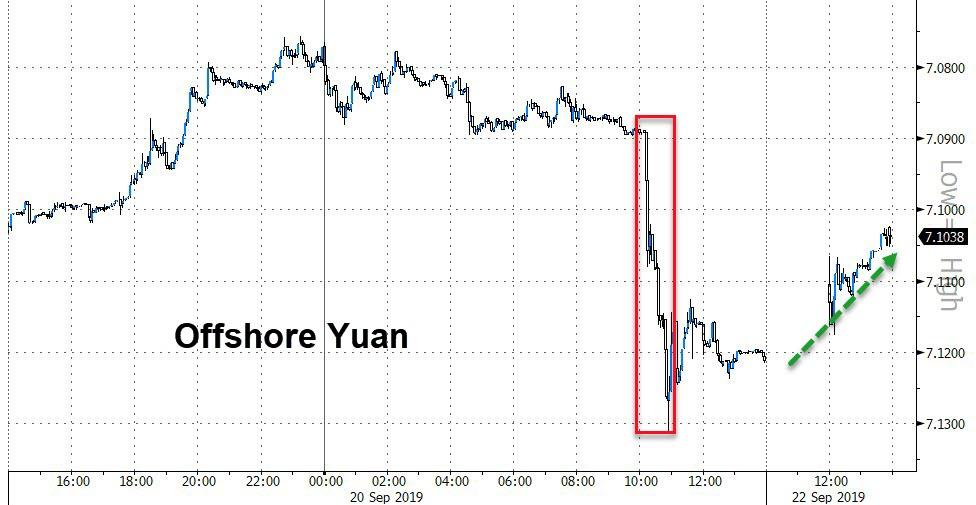

‘Vaguely Troubling’: BIS Warns Of Financial Disaster Amid $17 Trillion In Negative-Yield Debt

When the central bank for central banks publishes its quarterly review, the world should take note.

Claudio Borio, Head of the Monetary and Economic Department at the BIS, published the BIS Quarterly Review, September 2019on Sunday, revealing how the increasing acceptance of negative interest rates has reached “vaguely troubling” levels.

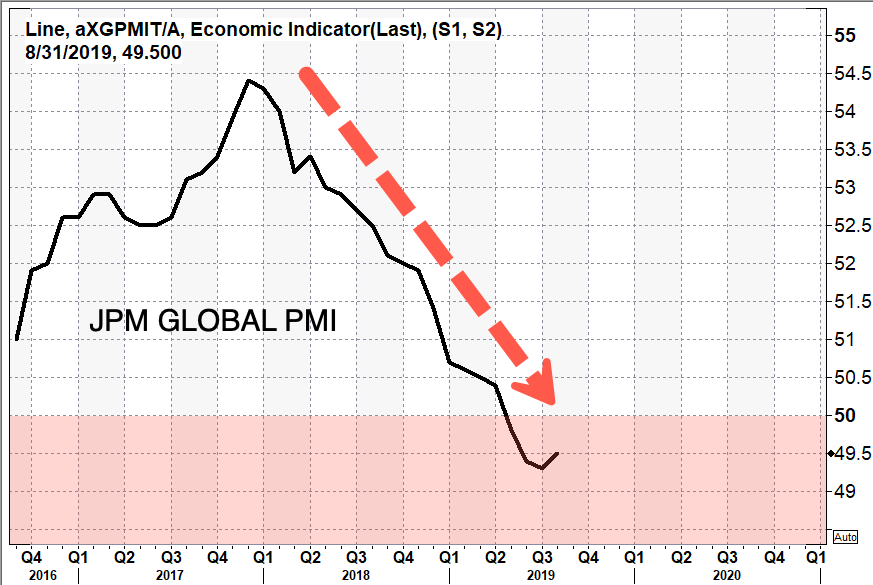

The statement comes after the Federal Reserve and European Central Bank (ECB) cut interest rates to flight a global manufacturing slowdown — Borio said that the effectiveness of monetary policy is severely waning and might not be able to counter the global downturn, in other words, JPMorgan Global Composite PMI might print sub 50 for a considerable period of time.

“The room for monetary policy maneuver has narrowed further. Should a downturn materialize, monetary policy will need a helping hand, not least from a wise use of fiscal policy in those countries where there is still room for maneuver.”

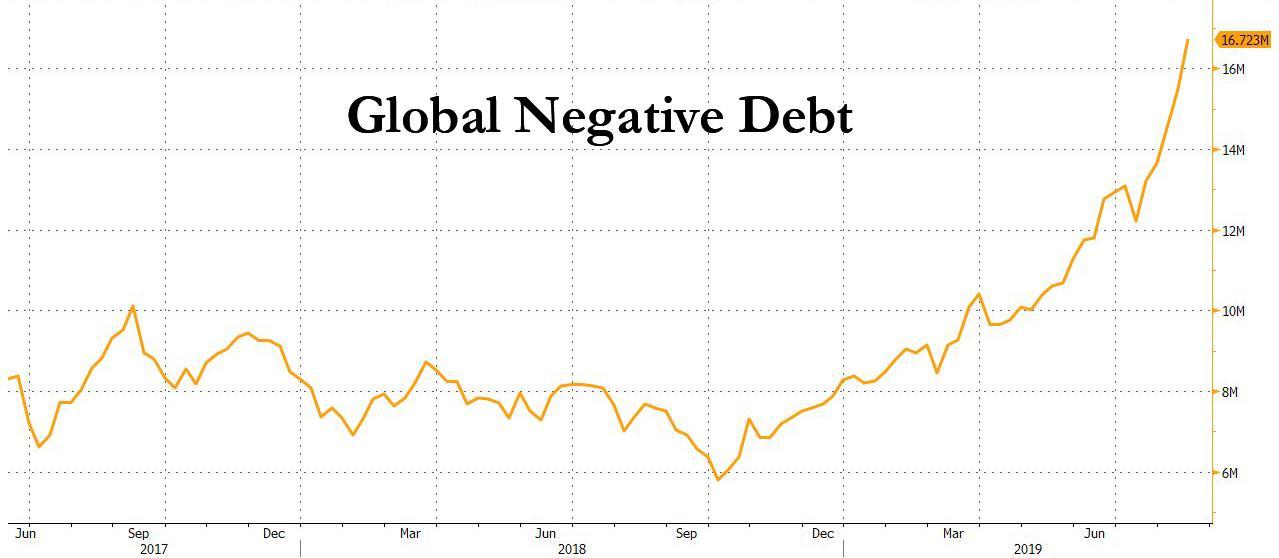

The BIS, known as the ‘central bankers’ bank,’ said the recent easing by the Fed, ECB, and PBOC, has pushed yields lower across the world, contributing to the more than $17 trillion in negative-yielding tradeable bonds.

From Germany to Japan, 10-year government debt rates have plunged into negative territory, in recent times.

“Against this backdrop, sovereign bond yields naturally declined further, at times driven by the prospect of slower economic activity and heightened risks, at others by central banks’ reassuring easing measures. At one point, before the recent uptick in yields, the amount of sovereign and even corporate bonds trading at negative rates hit a new record, over USD 17 trillion according to certain estimates, equivalent to roughly 20% of world GDP. Indeed, some households, too, could borrow at negative rates. A growing number of investors are paying for the privilege of parting with their money. Even at the height of the Great Financial Crisis (GFC) of 2007-09, this would have been unthinkable. There is something vaguely troubling when the unthinkable becomes routine,” Borio warned.

Central bankers have already acknowledged that the flurry of recent rate cuts had continued to deplete their already-limited firepower – which would make their ability to fight a prolonged downturn less effective than ever before.

ECB President Mario Draghi said earlier this month that “it’s high time for the fiscal policy to take charge,” an indirect admittance that monetary policy has run its course.

“Almost all the things that you see in Europe, the creation of more than 11 million jobs in a short period of time, the recovery, the sustained growth for several quarters, were by and large produced by our monetary policy. There was very little else… Now it’s high time for the fiscal policy to take charge.”

Draghi: We are very concerned about the pension industry and related services. Negative rates are necessary instruments of monetary policy. It has created a lot of positive effects. How do we speed up these effects so that interest rates can go up? The answer is fiscal policy.

Borio said global markets were alarmed this summer by the inversion of the US and other major countries’ bond yield curves.

He also warned about the corporate debt market, specifically major imbalances in leveraged loans known as collateralized loan obligations (CLOs) which “represent a clear vulnerability” to the global financial system.

And perhaps gold is ‘fearing’ the same “unthinkable” status quo that Borio warns of as it rises alongside negative rates…

Iran is an enigma to most American policymakers. Iranian foreign and defense policies, according to Kenneth Katzman, are “products of overlapping, and sometimes contradictory, motivations.” The key question is whether Iran is an expansionist, theocratic, Shia-chauvinist state, or a rational, defensive bulwark with only limited regional aspirations. While it is a bit of both, it is generally more defensive and decidedly not a strategic or existential threat to the United States.

Iran’s role in the region is not entirely negative. Particularly in Iraq, Iran and the United States have recently found themselves on the same side. Both states opposed the Islamic State. Iraq’s Popular Mobilization Units, a largely Shia Iraqi militia network, were critical in stopping the spread of ISIS and then fighting back against them. These militias have enjoyed significant Iranian support, without becoming a totally Iranian initiative. At the same time, they have been significant drivers of sectarianism and have raised worries that they will undermine the Iraqi government’s authority at Iran’s behest. Iran and the United States also both opposed the independence referendum in Iraqi Kurdistan and the attempted coup in Turkey. Those areas of overlapping interest are narrow and often temporary, yet they highlight the danger of viewing U.S.-Iranian relations as a zero-sum competition.

There are also limits on the threat Iran poses to vital U.S. interests in the Middle East. Thanks to the 2016 nuclear agreement, the prospect of an Iranian nuclear weapon has been delayed for a number of years. Iran would have to either develop covert facilities, which the agreement’s inspection regime makes more difficult; or signal its intentions to weaponize by expelling inspectors, an act that would quickly isolate it diplomatically.

Overestimating Iran’s power

For all the standard neocon alarmism of the Trump team, Iran’s conventional military power is actually quite limited, especially in comparison with the United States’. In order to achieve control of the key oil regions at the western end of the Persian Gulf, Iran would have to advance over the same open desert terrain where American air power and ground forces crushed Saddam Hussein’s army in 1991. Even before being confronted by America, Iranian invaders would have to defeat the Gulf Arab militaries, which enjoy better equipment than Iran and are more capable than the forces Iraq routed in Kuwait. Iran’s military is not built to engage in offensives, but to defend against attackers by means of a “mosaic” of independent military commands across the country. Any shift to include some offensive elements will take many years to realize — years in which Iran’s neighbors can strengthen their defenses.

Iran’s threat to the Gulf oil flow is also overstated. In order to stop oil shipments, Iran would have to deploy large numbers of mines, swarming small craft, and missile launchers. Strategically, the global economic impact of choking the oil flow would isolate Iran, a very negative outcome that Iranian policymakers would have to consider in deciding whether to launch a Gulf offensive. Thus, there are many reasons to suspect Iranian action in the Strait would be focused more on harassment than on achieving a sustained interruption in the oil flow. And a harassment campaign, while it would boost oil prices, would allow much oil to get through, limiting the impact on the U.S. economy.

Even Iran’s most dastardly activity, its support for terrorism, has a measure of predictability. Iranian terror attacks have often been not bolts from the blue, but responses to attacks by others. For example, between 2010 and 2012, Iran faced a wave of assassinations of nuclear scientists and the use of the U.S./Israeli-created Stuxnet cyber weapon against Iranian centrifuge facilities. Outside Iran, there was a similar uptick in Iranian-backed terror attacks and plots against Israeli, American, and Saudi targets, along with a major cyberattack on Saudi Arabia’s state oil company. The 1992 bombing of the Israeli embassy in Argentina came one month after an Israeli airstrike killed the leader of Hezbollah; the terrorists explicitly stated that their action was a response to that killing. This is not to excuse such activity, but rather illuminates that there are two sides to this, and every, story.

Iran and its neighbors

In general, Iran’s (limited) assertiveness has only damaged its relations with its neighbors. Their fear of Tehran, coupled with a perceived U.S. withdrawal during the Obama administration, encouraged them to strengthen their militaries, including advanced missile defense systems. That was by far preferable to the United States’ taking the lead to check Iran which, as recent history demonstrates, only increases tensions.

Iran’s support for Syria has only compounded its own regional isolation. Sending Shia militias to back a tyrannical non-Sunni regime in its brutal war against a largely Sunni opposition has turned Sunnis against Iran in large numbers. While the West favors Iran’s current president, Hassan Rouhani, far more than his predecessor, Mahmoud Ahmadinejad, the Syria war has helped make the reverse true in the Arab world. Iran’s best proxy, Hezbollah, has had a similar experience — it went from great popular support after fighting Israel to a draw in 2006 to growing isolation as it became entangled in Syria.

At the same time, Iran has been able to cooperate successfully with Russia, particularly in Syria. Given Iran’s strong nationalistic tendencies — including a constitution that forbids any foreign military base to be established on its soil — it is noteworthy that Iran has allowed Russian aircraft and cruise missiles to overfly Iran on their way to Syria, and even allowed Russian bombers to temporarily operate from an airbase in western Iran for operations in Syria. That arrangement fell apart after a week because of Iranian frustration with Russia’s giving it major publicity, amplifying controversy in Iran. Russia also sold Iran the S-300 air defense missile system, a relatively advanced system that could significantly complicate any U.S. or Israeli attack on Iran. However, the Iranian-Russian relationship has many complexities. Roughly a decade elapsed between Russia’s selling Iran the S-300 and the system’s being delivered and going operational, in part because of a Russian decision to withhold the weapons. That was above and beyond its obligations under Security Council restrictions on weapons sales to Iran, signaling a potential hesitation on the part of Russia to empower Iran with the technology.

Russia has long had a friendly relationship with the Kurds, and responded to Iraqi Kurdistan’s independence referendum ambiguously, contrasting sharply with Iran’s opposition to the referendum and support for Iraqi military operations against the Kurds. Russia’s oil giant, Rosneft, a firm majority-owned by the Russian government, has provided the Kurds with significant financial support and expanded its position in Kurdistan, even during the height of the crisis with Baghdad.

In Syria, Russia favors a strong, central Syrian state, and Iran favors another Lebanon, with local sectarian proxies loyal to Tehran, not Damascus. Russia fears Sunni jihadism, and can reasonably expect that the Iranian tendency to sectarianize conflicts would strengthen such jihadism in Syria. Moreover, Russia has at times worked to limit Iranian influence in key areas of Syria, and has a close relationship with Iran’s bitter rival, Israel.

Iran’s influence in Iraq, Syria, and Lebanon is clearly greater than it was prior to the Iraq War and the Arab Spring. Iraq, in particular, went from being Iran’s firmest foe and a serious check on its power to being an area where Iranian-backed militias and political factions have a notable impact. That was the ultimate outcome of America’s invasion of Iraq, and should give policymakers pause before repeating the folly in Iran. Iran has a greater ability to shape events in Syria, thanks to its growing weakness, and in Lebanon, thanks to its perennial divisions. The key question for U.S. interests is whether it will lead to Iranian dominance of the region — and specifically, of the region’s oil exports. It won’t!

In the near-to-medium term, Iraq and Syria are unlikely to be great assets for Iran, since both states have been wrecked, divided, and destabilized by war. Syria in particular will require tremendous reconstruction in order to be a source of strength for those who control it. The proxy forces and foreign militiamen Iran has used to expand its regional influence aren’t likely to be effective at governance, especially in the inclusive and professional way that would foster reconciliation. Moreover, given the ethnic and sectarian divisions in Iraq and Syria, fearful local powers will find many potential partners as they seek to raise the costs of Iranian rule in the area. Thus, it is possible that American allies in the region will empower radical jihadist groups in their efforts to build resistance to Iran, or that they will unwittingly cause a regional conflict while trying to counter Iran.

Over the last few months, Trump’s team — led, apparently, by John Bolton — has edged the United States to the brink of war by provoking Iran’s insecure and defensive leaders. Re-imposed U.S. sanctions on Tehran hurt the people more than they hurt the governing elites of Iran and serve mainly to drive the populace into the arms of the nationalist mullahs. Then the United States declared an official portion of Iran’s military — the Revolutionary Guards Corps (IRGC) — a “terrorist” organization. That unnecessary and absurd decision prompted Tehran to counter (with some validity) that the U.S. military command in the Middle East, USCENTCOM, was the actual terrorist organization.

Iran, strangled by sanctions, and threatened by public pronouncements of U.S. bellicosity as well as American troops based in a veritable ring around the country, then proceeded to “act out.” Trump’s response to these modest provocations has brought the United States to the edge of war — something Bolton has long desired. When various oil tankers in the Persian Gulf were attacked, Trump immediately (with little evidence) blamed Iran. Then, when Iran shot down an unmanned American drone in the Gulf, Trump claimed that he’d come within ten minutes of bombing Iran before standing down. He has not, however, ruled out future use of military force against Tehran, and, with Iran now declaring its intent to enrich more uranium than was allowed by the JCPOA — which admittedly the United States dropped out of — the war drums have certainly not ceased to beat.

Exit and engage.

For most of its history, the United States has not been deeply involved in the Middle East. However, with the Persian Gulf intervention in 1991, America shifted to an active, interventionist (even hegemonic) role. Aided by a large military presence posted throughout the Gulf region, the United States attempted to actively manage Gulf security. That new strategy has entangled the United States in constant conflict, from enforcing the Iraqi no-fly zones, to overthrowing Saddam, to a system of deadly sanctions on Iraq, to attempts to stabilize Iraq, to driving back ISIS in Syria, and to containing Iran. All that has proven disastrous for the American republic and for the region as a whole.

We should generally expect Iran’s neighbors to respond to Iranian pressure with resistance, not acquiescence. The United States does not need to play any role in the region. Indeed, a policy of nonintervention on the part of the United States would give them stronger incentives to work together and to bear more of the burden of their own defense. Conversely, increased U.S. support for Iran’s neighbors against Iran may yield less cooperation among them and greater dependency on the United States. The recent Qatar crisis, which broke out days after a firm U.S. declaration of support for Saudi Arabia, highlights the danger that stronger U.S. backing can suppress regional cooperation.

Iran must be given some breathing space and an assurance of security. An American pledge not to undertake a regime-change operation in Tehran would be a solid start. Let us remember that matters in the Persian Gulf, the Arab world, and Central Asia are vital strategic interests and potentially existential threats to the Islamic Republic. U.S. presence and interests in the area are but distant and tangential by comparison. Courage and statesmanship do not need to mean war. Context and nuance ought to reign, and Trump must realize that even the loss of a drone, potential attacks on foreign oil tankers, and Iranian support for regional proxies — even if all that is true — ought not to reach the threshold of war. It is time, in short, for the “dealmaker” to strike a deal with Iran.

Avoiding catastrophe or destabilization

Given the chaos that followed regime change in Iraq and Libya, the U.S. government should not pursue regime change in Iran and should simply get out of the Middle East entirely. It should not engage in a war with Iran. Period. An invasion of the large, mountainous, nationalistic Iranian plateau would be a military and diplomatic disaster. Instead, America should offer Iran a path to better relations, even under its current regime. The United States must accept the world and region as it is, not as it would like it to be. That requires an understanding of two inconvenient truths: that the view from Tehran demonstrates the United States has often been the aggressor in the bilateral relationship, and furthermore, that Iran is not the monster of the hawkish imagination. Iran is complex and nuanced — there are no simple solutions. America’s favorite policy tool, its military, has the least efficacy in the current situation. Every president from Jimmy Carter to Barack Obama to Donald Trump has refused to take U.S. military options “off the table,” but that’s precisely what prudence requires.

“What Were You Like At 17?”: Bill Maher Defends Brett Kavanaugh In Fiery Exchange With Guest

On his show Friday night, Bill Maher and his panel wound up getting into a heated debate over the “new” allegations about Brett Kavanaugh –yes, the ones even his accuser can’t remember.

Maher surprisingly turned on his liberal comrades, adopting the position that rehashing events from when Kavanaugh was 17 years old hurt the Democrats in 2018 – and could hurt them again. Citing polling from 2018, Maher said that Democrats could have done better in the midterm elections had it not been for the Kavanaugh hearings.

“People did not like going after a guy for what he did in high school. It looked bad and now Democrats are talking about impeaching him again?” Maher said.

Guest Andrew Sullivan seemed to agree. “He probably did some shitty things in high school drunk,” he said.

And when liberal guest Heather McGhee tried to jump in, asking “May the woman please speak about what this felt like?”, Sullivan shot her down immediately: “Please don’t play that card. You’re making my point.”

When Kavanaugh’s temperament was brought up, Sullivan responded:

“You try maintaining a good temperament when you’re being accused of something, you had no idea it was coming at you, came at the last minute, and that happened years and years and years ago.”

As McGhee tried to make the point that being a Supreme Court justice isn’t just a “normal job”, Maher immediately fired back: “So you’re saying at 17 you have to have your fully formed character?”

He continued:

“Live in reality, man! That’s who they put up. We don’t have the votes, and now we lost seats! Are we gonna do it again? Ruth Bader Ginsburg said glowing things about him… What were you like at 17?”

South Korean Exports Collapse 21% – Biggest Drop In A Decade

Having “stabilized” at a dismal level on contraction, South Korean exports’ collapse just took another leg lower as the battle with Japan sparks the biggest drop in trade since 2009.

Exports (for the first 20 days of September):

to China -29.8%;

to U.S. -20.7%;

to EU -12.9%;

But as the trade war crushes chip exports (contracting 39.8%), the ongoing dispute with Japan is accelerating the overall collapse:

Exports to Japan -13.5%

Imports from Japan -16.6%

Sending overall exports (for the first 20 days of September) down 21.8% YoY…

Source: Bloomberg

The Won has tumbled at the open…

Source: Bloomberg

South Korea is the first major exporter to report trade data each month, so provides an early reading of global trade; and as the world’s leading exporter of computer chips, ships, cars and petroleum products, September’s data is a major red flag for the global economy’s accelerating downturn (and global stocks’ earnings expectations).

The Federal Reserve did exactly what the markets expected this week, cutting interest rates by another 25 basis points, but the central bank sent out mixed signals about what will happen next.

Markets widely construed the Fed’s messaging as somewhat hawkish. In its policy statement, the Fed said the US economy is growing at a “moderate” rate and the labor market “remains strong. It cut rates, “in light of the implications of global developments for the economic outlook as well as muted inflation pressures.”

In his podcast, Peter Schiff reiterated this was just another step toward zero and said whatever the Fed wants to call its mechanizations, they’re going to stink to high heaven.

Fed Chair Jerome Powell was specifically asked about negative rates during his press conference. He said the Fed wasn’t really thinking about that, but Peter said, “Of course, we’ll see what happens when we get to zero and problems aren’t solved.”

The rate cut vote was 7-3. Two members of the FOMC didn’t want any cuts and Jim Bullard wanted a 0.5% cut.

As Peter pointed out, the Fed met market expectations, as it usually does.

It’s too afraid of provoking an adverse reaction. If they don’t cut enough, the markets could sell off. Or maybe if they cut too much, the markets could be thinking, ‘Oh my God, what are they worried about, why are they panicking?’ So, the Fed always wants to play it safe and it pretty much does what the markets expect, what the markets want. And that’s exactly what we got.”

Markets didn’t react significantly to the Fed’s move. Stocks initially sold off. The Dow was down close to 200 points after the announcement, but recovered to close slightly positive. Gold fell below $1,500 but was back above that level Thursday morning. The dollar gained slightly.

Peter said the more significant move that the mainstream didn’t pay much attention to was the repo operations that the Fed ran Tuesday and Wednesday mornings. In a nutshell, there wasn’t enough liquidity in the financial system. There weren’t enough lenders to meet the needs of the borrowers and the repo rate skyrocketed. So, the Fed stepped in and injected billions of dollars into the system to push interest rates back down. Peter said this is a “big deal.”

It shows that the Fed is losing control of the short end of the curve, that market forces are beginning to overwhelm the Fed’s attempts to artificially suppress interest rates.”

Ironically, during the post-FOMC meeting Q&A, Powell wondered out loud why interest rates – particularly on the long end – are so low.

It hasn’t dawned on Powell that the reason interest rates are low is because of the Fed. It’s not because of some weird thing going on in the economy. Interest rates are low because central banks around the world are artificially suppressing them. It makes no sense fundamentally to be as low as they are, especially in the United States where we have minimal savings and everybody is loaded up with debt.”

Powell continues to insist the economy is strong and the last two rate cuts are merely precautionary.

The markets are seeing the recession that the Fed is denying. And of course, even if the Fed sees it, it thinks its job is to deny it because it wants to engender confidence to delay the onset of the recession as long as possible. But the markets are seeing this recession and they are bringing rates down in advance to front-run the Fed because they know exactly how the Fed is going to react the next recession. In fact, the Fed is telling you. If they are surprised, if their rosy forecast proves wrong, they are slashing rates, they’re doing more QE and the bond traders have been trying to front-run.”

Peter said QE is the problem. The problem is that interest rates are too low. And the longer the central banks keep them this low, the worse the problems are going to get. Peter compared the central bankers to medieval doctors bleeding their patients.

But the Fed doesn’t want to deal with the problems that allowing interest rates to normalize would cause. So, they continue to work to keep them down. This is exactly what the Fed did with its repo operations earlier in the week. It essentially created money out of thin air and injected it into the financial system.

In effect, that was like a return to quantitative easing. I mean, they’re not calling it quantitative easing, but what did the Federal Reserve do? They created money and they bought government debt and they expanded their balance sheet.”

During his press conference, Powell actually said the Fed may have to resume balance sheet expansion. That’s basically an admission that QE4 is on the horizon. They probably won’t call it quantitative easing. The current term being tossed about is POMO (Permanent Open Market Operations). Peter said it’s all semantics. When you boil it all down, it’s really just debt monetization.

Basically, it doesn’t matter. Debt monetization, quantitative easing, by any other name, it still stinks. And whatever the Fed is going to do, it’s going to stink to high heaven.”

It’s Official: Bank of America Now Calls What Is Coming “QE4”

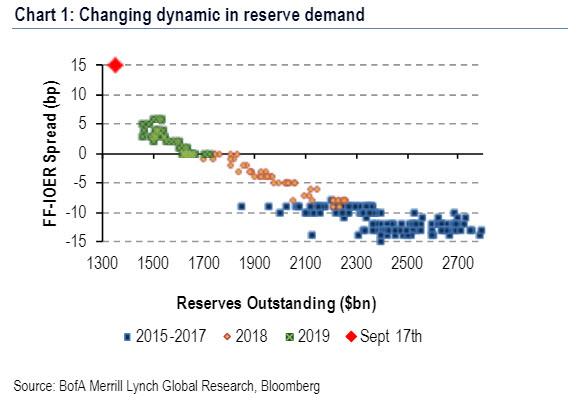

One of the reasons for the sharply hawkish initial response to Wedensday’s FOMC meeting – one which saw both the dollar and yields spike – is that as we pointed out just before Powell’s statement, in the hours ahead of Powell’s press conference, Wall Street consensus quickly shifted with many expecting the Fed to announce some form of permanent repo facility or restart of POMO (or QE for those who call a spade a spade) to push reserves back to a level where the funding market is stable. This, as we showed with the following chart, would require some $400 billion in new reserves for the FF-IOER spread to normalize.

To the disappointment of many, Powell did not do that, and instead, the FOMC realigned both interest on excess reserves (IOER) and the reverse repo (RRP) rate lower by 5bp, resulting in 30bp cuts to both rates. Powell also noted during his press conference that the Fed would use temporary open market operations (OMOs) “for the foreseeable future” to address pressures in funding markets.

However, and the reason why stocks shot up just before 3pm ET on Wednesday, is that that’s when Powell added that “it’s possible that we’ll need to resume the organic growth of the balance sheet, earlier than we thought. … We’ll be looking at this carefully in coming days and taking it up at the next meeting” in late October. Said otherwise, while the Fed may not have announced QE4 yesterday, but it will likely announce it in the very near future.

And while the Fed also moved to broadly expand its balance sheet late on Friday by preannouncing continued daily open market repo operations, together with at least three, $30 billion term repos to ease funding conditions around quarter end, which confirms that the rebound in the Fed’s balance sheet – the first in almost five years – is anything but temporary…

As a reminder, Goldman now assumes a roughly $15bn/month rate of permanent OMOs, enough to support trend growth of the balance sheet plus some additional padding over the first two years to increase the size of the balance sheet by $150bn, restoring the reserve buffer and eliminating the current need for temporary OMOs.

And while Simon Potter did not lay out a timeframe for his prediction, he agreed that the Fed “may have to expand the central bank’s balance sheet through outright purchases of U.S. Treasury securities, to ensure stable liquidity conditions at the end of the quarter as well as at year-end.”

The bottom line from the flurry of events which took place in the last week is that after just under two years of Quantitative Tightening, which shrank the Fed’s balance sheet from $4.5 trillion to $3.8 trillion, the current level of liquidity in the financial system is once again insufficient.

Which addresses the question that everyone has been quietly asking: if the current level of reserves, at roughly $1.4 trillion as broken out by bank cash levels which we discussed last night, is too low…

… then what is a sufficient level of reserves?

That’s the question addressed by JPMorgan’s “other” quant, Nick Panagirtzoglou in his latest weekly Flows and Liquidity letter, in which he writes that “the liquidity effects from the Fed’s balance sheet shrinkage have been manifesting themselves over the past year via a reduction in both broad or non-bank liquidity and narrow or banking sector liquidity” and reminds readers that recently he also warned that that “liquidity will likely continue to tighten in the US banking system even after the Fed stops its balance sheet shrinkage, and, as a result, in order to stop this liquidity tightening from advancing further, the Fed may need to start open market operations sooner rather than later to inject reserves into the US banking system.“

As we said last week (and above): QE, which until recently nobody thought was possible again, is now a foregone conclusion.

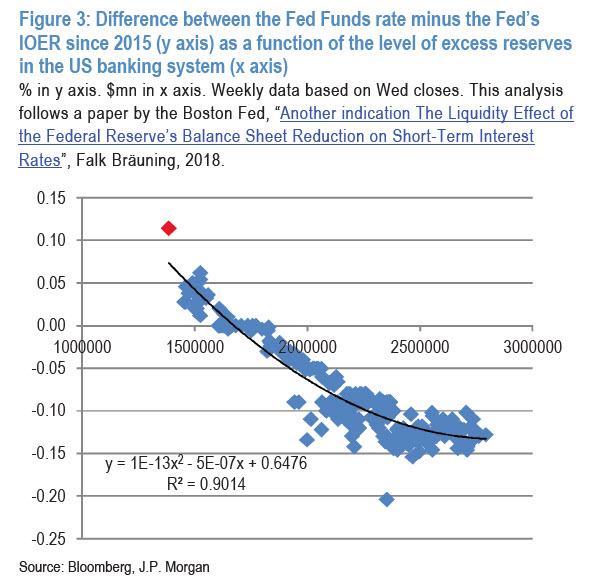

So how does the JPM quant justify his view that more POMOs are just around the corner? Largely the same way as BofA, by depicting the sensitivity of the Fed Funds rate to the level of reserves. The chart below plots the effective Fed Funds rate over the Fed’s policy rate i.e. the IOER or Interest On Excess Reserves, with Panagirtzoglou noting that “the steepening of this relationship over the past year is consistent with the idea that the level of reserves has been shifting towards tighter territory. When reserves are abundant, the line in Figure 3 should be relatively flat, i.e. any change in reserves should have little impact on interest rates, which was the case when reserves were above $2tr. But when liquidity conditions become tighter and reserve drainage starts “biting”, the sensitivity of interest rates to changes in reserves increases.” In other words, and as the chart at the top showed, “the steeper this sensitivity, the more the tightening in liquidity conditions.“

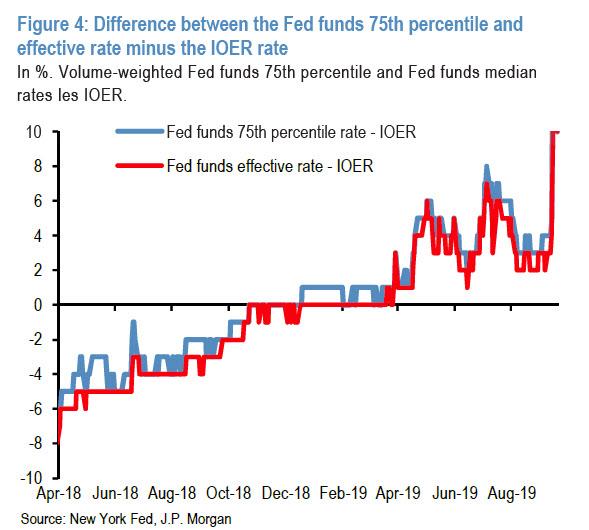

The chart above suggests that the steepening (i.e., tightening) began when the level of reserves started falling below the $2tr mark in the middle of 2018 and intensified since last December as reserves fell below the $1.75tr mark. This steepening of the sensitivity of interest rates to reserve changes became more acute more recently, when reserves fell below $1.6tr in April and below $1.4tr this past week. The response of interbank rates, both secured and unsecured has been forcefully as shown in the chart below demonstrating the relationship between Fed Funds and IOER…

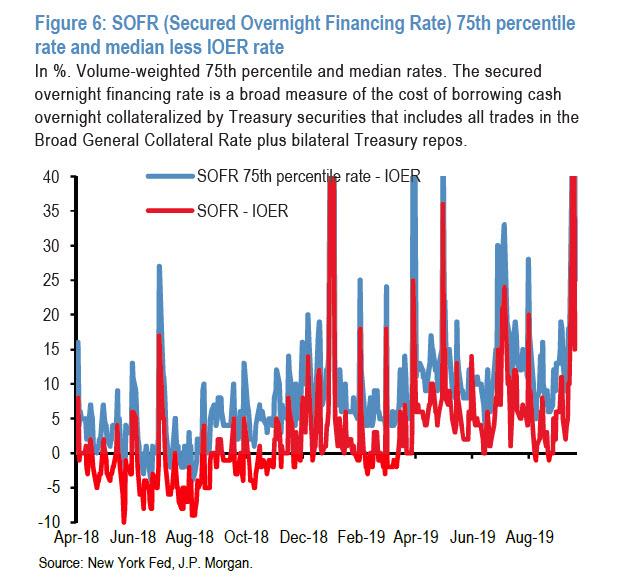

… and also the chart showing the spread between SOFR and IOER.

The first chart above, depicting the gap between the IOER and the Fed Funds rate, shows that the increases over the past week’s reserve drainage episode were more pronounced than last April’s episode, consistent with the idea that we are currently at a steeper part of the reserve demand curve than last April, according to JPM.

The second chart shows a similar tightening trend in the secured interbank market, in this case measured by the SOFR (Secured Overnight Financing Rate), a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities that include all trades in the Broad General Collateral Rate plus bilateral Treasury repos. The secured overnight interbank market is much bigger than the unsecured one. But what is troubling is that secured overnight interbank market rates are more volatile, as the experience of this past week reminded us. Here too the increases in SOFR over the past week’s reserve drainage episode were more pronounced that last April’s episode, consistent with the idea that we are currently at a steeper part of the reserve demand curve than last April (it also begs the question just how valid of a replacement to LIBOR will SOFR be, if its volatility is so high as to rattle the hundreds of trillions in floating-rate debt linked currently to Libor and, started in 2020, to SOFR).

One final observation: the ratio of reserves to banking system assets has collapsed over the past five years to its lowest level since the end of 2009 i.e. a ten year low… although of course, prior to that it was 0% so this is only a financial crisis artifact, in large part sprung by changes to the regulatory regime demanding banks hold on to much more reserves.

The bottom line here is clear: despite $1.4 trillion in “excess” reserves, despite a $3.8 trillion Fed balance sheet, the liquidity in the system is not enough.

So what is the proper level of liquidity measured by bank reserves?

To answer that question, Panigirtzoglou asks rhetorically, what if the current ratio of 7.9% is too low and a ratio of around 10% seen at the beginning of the year is more appropriate? His answer: a 10% ratio would imply a level of reserves of $1.75tr, $360bn above current levels, which is in line with our calculation of $400 billion more reserves needed. This, to the JPM analyst, “is an important decision the Fed would have to make in its October meeting”, as well as the following question: “Is there currently a need for an upfront and permanent injection of reserves, before dealing with the longer term issue of $160bn per annum balance sheet expansion perhaps needed over time due to banknotes in circulation and the organic expansion of the banking system?“

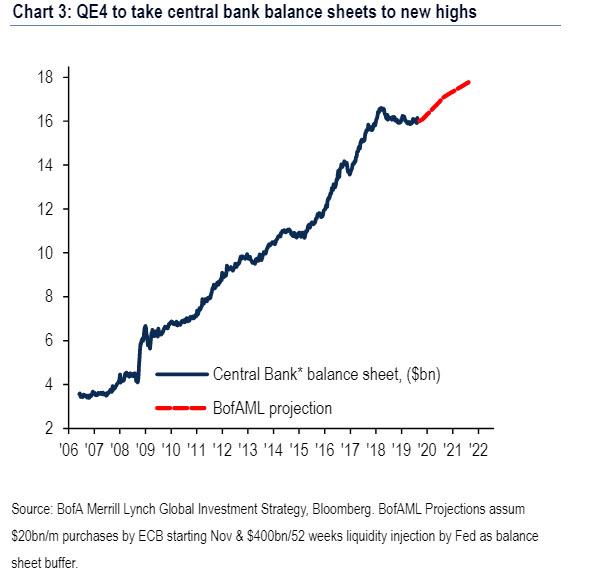

As of this moment, Bank of America, Nomura, JPMorgan, Goldman and, last but not least, Simon Potter are all convinced that there is now a need for an “upfront and permanent injection of reserves.” Which means it is just a matter of time before QE4 – as Bank of America’s CIO Michael Hartnett now openly calls it – arrives, and pushes central bank balance sheets to new all time highs, to wit:.

QE4: Fed makes it 43 rate cuts YTD (751 since Lehman); ECB QE (€20bn/m from Nov’19) + Fed liquidity operations (est. $400bn next 12-months) = new high in G5 central bank balance sheet by Apr’20 (prior peak was $16.6bn in Mar’18); G5 central banks have bought $13tn of financial assets since 2008 (Chart 3).

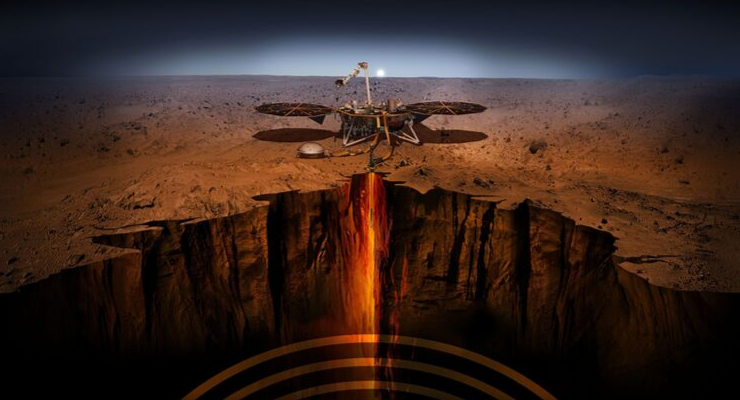

NASA’s robotic space rover has made a shocking discovery on Mars which, while puzzling to researchers so far, may be key to understanding the unique environment of the Red Planet.

The InSight space rover designated to study Mars has discovered strange magnetic pulsations on the surface of the planet at midnight. The bizarre bursts of magnetic energy were detected by the magnetometer attached to the cutting-edge spacecraft, reportsNational Geographic.

Since last November, the InSight capsule has gathered information about the planet’s evolution and make-up, as well as recording its tremendous “Marsquakes,” measuring its upper crust’s temperature, and gauging the planet’s magnetic field.

But at a joint meeting of the American Astronomical Society and European Planetary Science Congress (EPSC), it was revealed that not only were there these strange pulses that “jiggled” the magnetic field, but the crust of Mars is also far more magnetic than researchers had expected.

The lander’s data also revealed that about 62 miles below the planet’s surface lies a 2.5-mile-thick layer of some electrically conductive substance. While scientists are less than certain, some are speculating that the layer could potentially be a massive body of water, either consisting of dissolved solids, or water and ice—and it may even be possible that the layer stretches across the entire planet.

Preliminary data from the InSight lander’s magnometer suggest that the red planet’s magnetic field wobbles in inexplicable ways at night. https://t.co/Tbi4LAW68P

Dave Brain, an atmospheric and space physics scientist at the University of Colorado who is familiar with InSight’s data, noted that because the rover can only dig as deep as 16 feet below the surface, it remains to be proven whether or not such vast water reserves exist. In the future, however, scientists will hopefully find other ways to find out what is causing the signals from the potential watery layer.

What also makes the discovery especially enticing for space scientists is the fact that Mars, unlike our planet Earth, suffered a collapse in its global magnetic field roughly four billion years. Lacking that crucial shield to defend itself from the sun’s solar winds, the planet was stripped of its atmosphere and became what it is now: a cold desert with bone-dry water reservoirs that’s incapable of supporting life.

However, InSight has been able to measure strong magnetic signals from the rocks lying near it which are both more stable and up to 20 times stronger than what had been predicted based on past measurements taken from orbit.

The scientists involved with the work haven’t yet identified whether these rocks lie deep underground or are closer to the surface—an important distinction to make, because if the rocks are younger and near the surface, this would mean that Mars’s magnetic field lasted far longer than scientists currently believe.

While the data hasn’t yet undergone a peer review, the information gained in less than a year before the InSight robot landed on Mars has been stunning.

Paul Byrne, a planetary geologist at North Carolina State University who wasn’t involved with the NASA probe’s work, commented:

“We’re getting an insight into Mars’s magnetic history in a way we’ve never had before.”

Secret FBI Subpoenas For Personal Data Go Far Beyond Previously Known

Secret subpoenas issued by the FBI for personal data go far deeper than previously known, according to new documents obtained by the Electronic Frontier Foundation through a Freedom of Information Act (FOIA) lawsuit, according to the New York Times.

The agency says the sweeping requests are crucial to counterterrorism efforts – however the new records reveal that the FBI requests go far beyond Silicon Valley; “encompassing scores of banks, credit agencies, cellphone carriers and even universities,” according to the report.

The demands can scoop up a variety of information, including usernames, locations, IP addresses and records of purchases. They don’t require a judge’s approval and usually come with a gag order, leaving them shrouded in secrecy. Fewer than 20 entities, most of them tech companies, have ever revealed that they’ve received the subpoenas, known as national security letters. –New York Times

“This is a pretty potent authority for the government,” said University of Texas law professor, Stephen Vladeck. “The question is: Do we have a right to know when the government is collecting information on us?”

According to the documents – which contain information covering about 750 of the subpoenas “representing a small but telling fraction of the half-million issued since 2001” – credit agencies Experian, TransUnion and Equifax received a large number of national security letters. Also included were Western Union and the Federal Reserve Bank of New York.

Equifax, Experian and AT&T received the most termination letters: more than 50 each. TransUnion, T-Mobile and Verizon each received more than 40. Yahoo, Google and Microsoft got more than 20 apiece. Over 60 companies received just one. -NYT

Aside from these new names – we’ve long known about tech companies receiving national security letters, including Verizon, AT&T, Google and Facebook “which have acknowledgedreceivingthe letters in the past” per the Times.

The Federal Bureau of Investigation determined that information on the roughly 750 letters could be disclosed under a 2015 law, the USA Freedom Act, that requires the government to review the secrecy orders “at appropriate intervals.”

The Justice Department’s interpretation of those instructions has left many letters secret indefinitely. Department guidelines say the gag orders must be evaluated three years after an investigation starts and also when an investigation is closed. But a federal judgenoted “several large loopholes,” suggesting that “a large swath” of gag orders might never be reviewed.

According to the new documents, the F.B.I. evaluated 11,874 orders between early 2016, when the rules went into effect, and September 2017, when the Electronic Frontier Foundation, a digital rights group, requested the information. –New York Times

“We are not sure the F.B.I. is taking its obligations under USA Freedom seriously,” said EFF lawyer Andrew Crocker. “There still is a huge problem with permanent gag orders.”

National Security letters have been the subject of controversy for decades. Issued since the 1980s, the agency is required to show “specific and articulable facts” that the target of such letters was an agent of a foreign power. That criterion has since been eroded to a target simple needing to be “relevant” to a terrorism, counterterrorism or a leak investigation.

“NSLs are an indispensable investigative tool,” said the DOJ while replying to the FOIA case – adding that information contained in the letters both helps identify criminals while clearing the innocent of suspicion.

A.I. driven social scores to supplant constitution?

Professor Larry Backer of Penn State University writes in a 2018 paper that resistance to social credit systems in the west could be dissolved when the masses are “socialized… as a collective” and “…the great culture management machinery of Western society develop a narrative in which such activity is naturalized within Western culture”

A 2018 paper written by prominent law professor Larry Backer of Penn State discussed the ways in which a social credit system could be implemented in the west. Backer writes that the shift in law with this system will “…change the focus of public law from constitution and rule of law to analytics and algorithm…”

Backer proposes that the “great culture management machinery” of the west normalize the idea of social credit and sharing private data. Backer writes:

“But is it possible to socialize the masses, or even mass democracy as a collective, to embrace this pattern of data disclosure beyond these immediately self-serving closed loop systems? Would it be possible for the state to develop systems for the enforcement of laws (criminal and regulatory) that depends on intelligence by inducing the masses to serve as positive contributors of data necessary for enforcement or regulation? The answer, in Western liberal democracies, may depend on the ability of the great culture management machinery of Western society – its television, movies and other related media – to develop a narrative in which such activity is naturalized within Western culture“.

As Big Tech and artificial intelligence creep further into our lives, a grid of high tech surveillance has entangled us. As if to pacify resistance, these systems (Google home, Apple watches, Amazon Alexa) offer “convenience” in the form of targeted ads, personalized content and other features.

In reality, this system is meant to determine whether or not you will be allowed to function in modern society.

The Trump admin is reportedly considering using this surveillance grid to monitor the population for signs of mental illness, triggering authorities to confiscate firearms from “dangerous individuals”.

“…already knows whether you’ve been taking your meds, getting your teeth cleaned and going for regular medical checkups. Now some employers or their insurance companies are tracking what staffers eat, where they shop and how much weight they’re putting on — and taking action to keep them in line.”

Artificial Intelligence, programmed by power hungry individuals, is steadily taking over our society. It is already censoring political opinions. It will be making medical, education, and financial decisions. Humans are to be sidelined. The social credit system will be watching you closely for any deviant behavior. If you arent careful, you will become an outcast. Access to food, transportation and medical care will be denied.

As we noted earlier, Saturday’s news from the NYT that the “the delegation of Chinese agriculture officials that had planned to travel to Montana and Nebraska in the coming week didn’t cancel the trip because of any new difficulty in the trade talks” but “instead, the trip was canceled out of concern that it would turn into a media circus and give the misimpression that China was trying to meddle in American domestic politics”, oil too is likely to catch a bid after the WSJ reported that it may take “up to eight month”, rather than 10 weeks company executives had previously promised, to fully restore operations at Aramco damaged Abqaiq facility, suggesting the crude oil shortfall will last far longer than originally expected.

US Futures have indeed spiked… with S&P Futs back at the Maginot Line of 3,000…