My coauthor Cassandra Burke Robertson and I have an article coming out in the Vanderbilt Law Review entitled “Litigating Citizenship“, which follows in the footsteps of our article “(Un)Civil Denaturalization” that appeared in the NYU Law Review earlier this year. Here is the abstract of our new piece:

By what standard of proof—and by what procedures—can the U.S. government challenge citizenship status? That question has taken on greater urgency in recent years. News reports discuss cases of individuals whose passports were suddenly denied, even after the government had previously recognized their citizenship for years or even decades. The government has also stepped up efforts to re-evaluate the naturalization files of other citizens and has asked for funding to litigate more than a thousand denaturalization cases. Likewise, citizens have gotten swept up in immigration enforcement actions, and thousands of citizens have been erroneously detained or removed from the United States. Most scholarly treatment of citizenship rights has focused on the substantive protection of those rights. But the procedures by which citizenship cases are litigated are just as important—and sometimes more important—to ensure that citizenship rights are safe.

This Article analyzes the due-process implications of citizenship litigation in the United States. It examines different stages at which the citizenship question is judicially resolved, including denaturalization, removal and exclusion, and restrictions on the exercise of citizenship rights such as voting, working, and traveling. The Article concludes that the structure of U.S. democracy relies on the stability of citizenship and requires heightened procedural protections when the government challenges an individual’s citizenship. In the words of Justice Felix Frankfurter, “The history of liberty has largely been the history of observance of procedural safeguards.” Those procedural safeguards are needed to ensure that the judicial branch can remain the stalwart protector of a key pillar of our constitutional democracy.

from Latest – Reason.com https://ift.tt/2Lno6Td

via IFTTT

Huawei accused the US government on Tuesday of harassing its employees and orchestrating a campaign of cyberattacks to try and infiltrate its internal network, Bloomberg reports. The company made these claims in an official statement, but didn’t say how it got this information.

The accusations are the latest in a back-and-forth conflict between Huawei and the US government, which has been accused of trying to use its influence to stop the Chinese telecoms giant from gaining supremacy in the market for fifth generation wireless gear.

The Trump Administration has notoriously blacklisted the Chinese company, banning American companies from doing business with it (potentially depriving it of critical components like microchips manufactured by Qualcomm). Trump has accused the company of aiding Beijing by carrying out espionage against its clients, making Huawei a “threat to national security.”

In its letter, Huawei accused Washington of using “every tool at its disposal”to try and undermine the company, including ordering law enforcement to harass current and former employees.

“It has been using every tool at its disposal – including both judicial and administrative powers, as well as a host of other unscrupulous means – to disrupt the normal business operations of Huawei and its partners,” the company said. Other measures included “instructing law enforcement to threaten, menace, coerce, entice, and incite both current and former Huawei employees to turn against the company and work for them.”

It added that “no company becomes a global leader in its field through theft.”

“We strongly condemn the malign, concerted effort by the U.S. government to discredit Huawei and curb its leadership position in the industry,” the company said. “No company becomes a global leader in their field through theft.”

Regarded by some as a “bargaining chip” in the US-China trade talks (indeed, President Trump has often treated it like one, most recently promising President Xi the US would back down from its harassment of Huawei as an overture to Beijing, though the next round of talks didn’t pan out so well).

The American military has launched an international campaign to convince its allies to reject Huawei technology in their next generation of wireless networks, warning allies that using Huawei equipment could put the data of citizens and the military at risk.

Though Huawei remains the world leader in 5G, Washington’s efforts have been a hindrance to the company. Huawei’s Billionaire founder, Ren Zhengfei, warned in an internal memo in August his company faced a “live or die moment.”

Huawei’s accusations follow a report by the Wall Street Journal published last week claiming that the DoJ was expanding its investigation into Huawei’s efforts to steal technology from American firms.

via ZeroHedge News https://ift.tt/2LjVPhz Tyler Durden

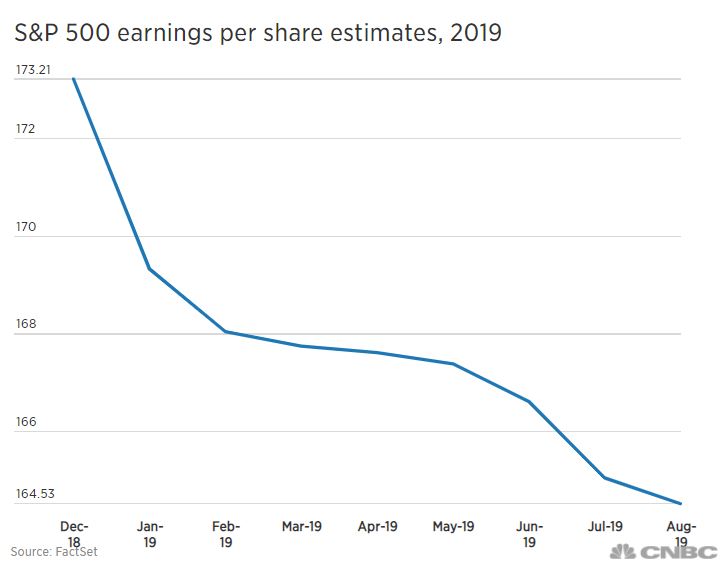

Since the end of the last recession, the outlook for the U.S. economy has never been as dire as it is right now. Everywhere you look, economic red flags are popping up, and the mainstream media is suddenly full of stories about “the coming recession”. After several years of relative economic stability, things appear to be changing dramatically for the U.S. economy and the global economy as a whole. Over and over again, we are seeing things happen that we have not witnessed since the last recession, and many analysts expect our troubles to accelerate as we head into the final months of 2019.

We should certainly hope that things will soon turn around, but at this point that does not appear likely. The following are 28 signs of economic doom as the pivotal month of September begins…

#1 The U.S. and China just slapped painful new tariffs on one another, thus escalating the trade war to an entirely new level.

#2 JPMorgan Chase is projecting that the trade war will cost “the average U.S. household” $1,000 per year.

#3 Yield curve inversions have preceded every single U.S. recession since the 1950s, and the fact that it has happened again is one of the big reasons why Wall Street is freaking out so much lately.

#4 We just witnessed the largest decline in U.S. consumer sentiment in 7 years.

#6 Sales of luxury homes valued at $1.5 million or higher were down five percentduring the second quarter of 2019.

#7 The U.S. manufacturing sector has contracted for the very first time since September 2009.

#8 The Cass Freight Index has been falling for a number of months. According to CNBC, it fell “5.9% in July, following a 5.3% decline in June and a 6% drop in May.”

#9 Gross private domestic investment in the United States was down 5.5 percentduring the second quarter of 2019.

#10 Crude oil processing at U.S. refiners has fallen by the most that we have seen since the last recession.

#11 The price of copper often gives us a clear indication of where the economy is heading, and it is now down 13 percent over the last six months.

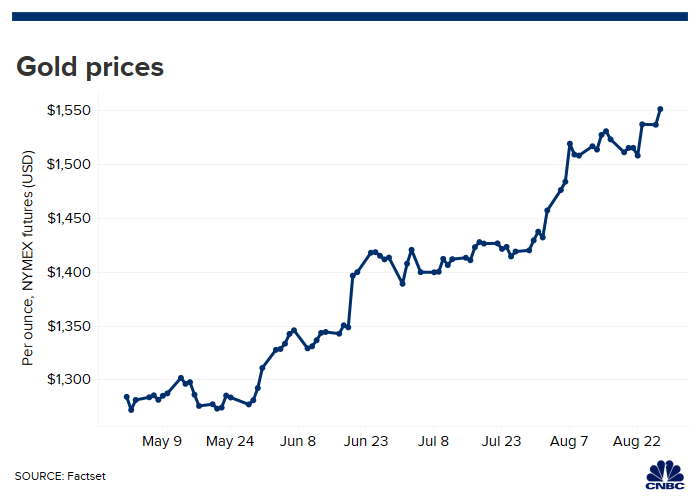

#12 When it looks like an economic crisis is coming, investors often flock to precious metals. So it is very interesting to note that the price of gold is up more than 20 percent since May.

#21 According to CNBC, the S&P 500 “just sent a screaming sell signal” to U.S. investors.

#22 Masanari Takada is warning that we could soon see a “Lehman-like” plunge in the stock market.

#23 Corporate insiders are dumping stocks at a pace that we haven’t seen in more than a decade.

#24 Apple CEO Tim Cook has been dumping millions of dollars worth of Apple stock.

#25 Instead of pumping his company’s funds into the stock market, Warren Buffett has decided to hoard 122 billion dollars in cash. This appears to be a clear indication that he believes that a crisis is coming.

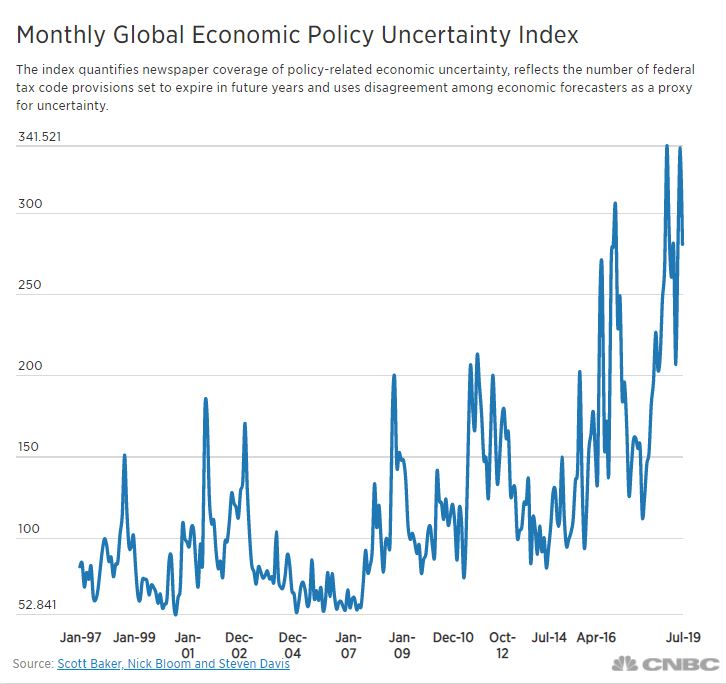

#27 The Economic Policy Uncertainty Index hit the highest level that we have ever seen in the month of June.

#28 Americans are searching Google for the term “recession” more frequently than we have seen at any time since 2009.

The signs are very clear, but unfortunately we live at a time when “normalcy bias” is rampant in our society.

If you are not familiar with “normalcy bias”, the following is how Wikipedia defines it…

The normalcy bias, or normality bias, is a belief people hold when considering the possibility of a disaster. It causes people to underestimate both the likelihood of a disaster and its possible effects, because people believe that things will always function the way things normally have functioned. This may result in situations where people fail to adequately prepare themselves for disasters, and on a larger scale, the failure of governments to include the populace in its disaster preparations. About 70% of people reportedly display normalcy bias in disasters.[1]

For most Americans, the crisis of 2008 and 2009 is now a distant memory, and the vast majority of the population seems confident that brighter days are ahead even if we must weather a short-term economic recession first. As a result, most people are not preparing for a major economic crisis, and that makes us extremely vulnerable.

In 2008 and 2009, the horrible financial crisis and the bitter recession that followed took most Americans completely by surprise.

It will be the same this time around, even though the warning signs are there for all to see.

via ZeroHedge News https://ift.tt/34j7owP Tyler Durden

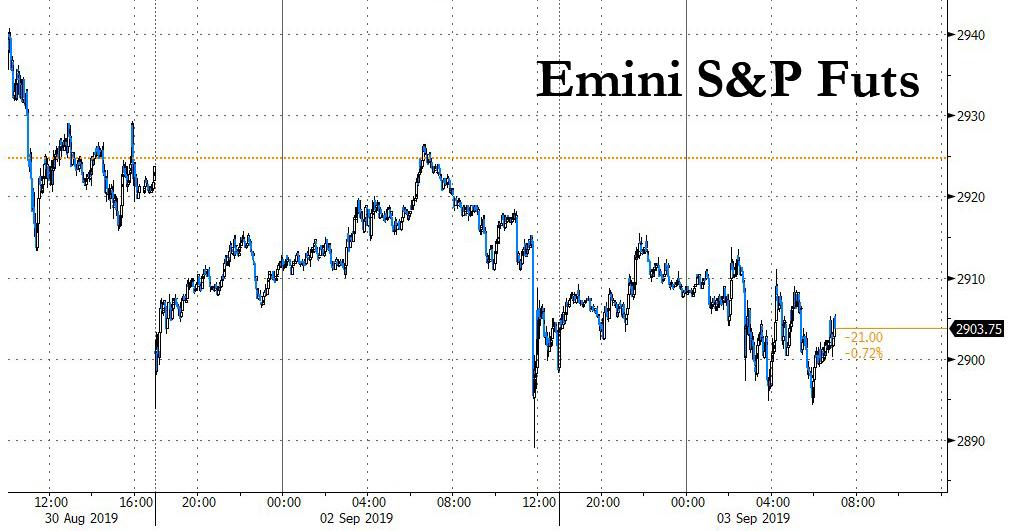

One day after stocks first tumbled, when the US and China launched a new round of sanctions over the weekend, then rebounded for no comprehensible reason, then tumbled again following a Bloomberg report of difficulties in setting a schedule as both sides had failed to agree on a date for Chinese officials to meet their U.S. counterparts in Washington, S&P futures once again magically recovered all losses but not for long and have since sunk again, sliding 0.8% to just above 2,900 as investors awaited the next batch of news on trade talks.

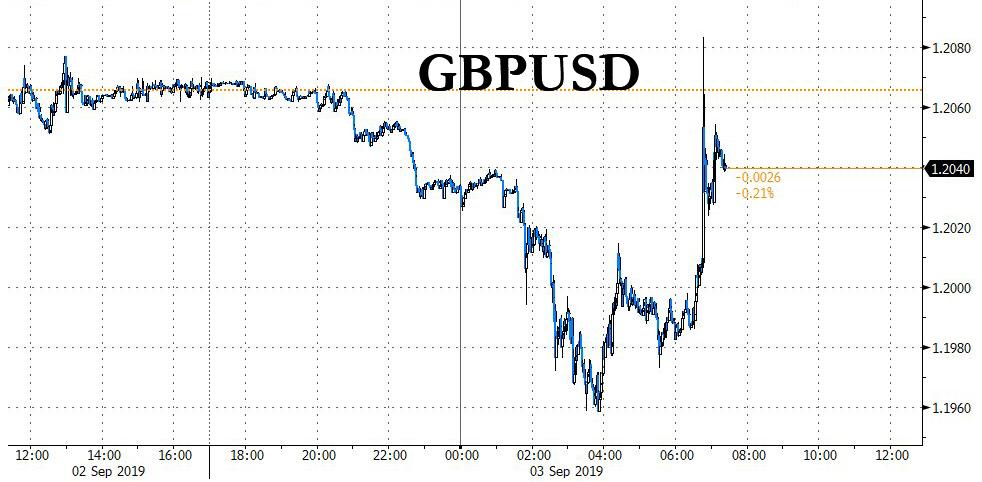

US futures dragged the world lower and global stocks slipped toward a recent two-month low on Tuesday, as U.S.-China trade tensions drove investors to the relative shelter of gold, the Japanese yen and government debt; as a result treasuries advanced, while the pound first sank below 1.20 against the dollar for the first time in three years as Brexit brinkmanship raised the possibility of an early election in the U.K, only to surge shortly after for reasons not exactly clear.

To be sure, September has been off to a rocky start for risk assets as traders remained sensitive to the twists and turns of the Sino-U.S. trade war. With mistrust on both sides, officials from the world’s two largest economies are struggling to agree on basic terms of re-engagement and even when to hold meetings planned for this month, Bloolmberg reported while violent confrontations in Hong Kong and the risk of an imminent Chinese incursion continue to weigh on sentiment.

With U.S. markets closed on Monday, global markets took their cue from weak PMI survey data in Europe and China which raised concerns the global economy was struggling on many fronts. An index of global stocks slipped 0.2% on Tuesday, heading toward a two-month low hit in early August. An index of Asian stocks was down 0.7%. In the trade war between Washington and Beijing, tensions have shown little sign of abating even though U.S. President Donald Trump has said they would meet for talks this month.

“Since the trade dispute has become the driving force behind equity markets, we advise against adding significantly to equity exposure, particularly for those with an adequate strategic allocation,” Mark Haefele, chief investment officer at UBS Global Wealth Management said.

European stocks were on the back foot as investors locked in profits from a three-day streak that saw indices scale near one-month highs, with the Stoxx Europe 600 Basic Resources Index falling for a second day, down as much as 1.4%, on news Chinese and American officials were struggling to schedule trade talks; metals retreated with copper hitting a 2-year low as diversified miners fall, with Rio Tinto -0.7%, BHP Group -0.5%, Anglo American -1.4%, Glencore -1.3%. Steelmakers also dropped: ArcelorMittal -1.2%, Evraz -1.7%, Voestalpine -1.3%, hit after Fitch analysts cut their 2019 global steel price forecast to $600/t from $650/t, as global prices continue to be hammered by poor sentiment from the ongoing U.S.-China trade tensions, increasing downside risks to the global economy. Base metals also fell in London, with copper -0.6%, zinc -1.5%, nickel little changed; aluminum -0.5%; iron ore -1.6% in Singapore.

Earlier in the session, Asian stocks dropped for a second day, led by energy producers, as Beijing and Washington struggled to set a meeting schedule for trade negotiations. Markets in the region were mixed, with Japan advancing and India retreating. The Topix climbed 0.4% in thin trading, supported by automakers and chemical producers. The Shanghai Composite Index closed 0.2% higher, with Foxconn Industrial Internet and China Yangtze Power among the biggest boosts. Sports-related shares jumped after China announced a plan to boost athletic development. India’s Sensex fell 1.4%, dragged down by financial shares, amid concerns that the biggest bank overhaul in decades may hurt the nation’s bad loan cleanup and slow lending approvals.

The move away from equities boosted demand for government debt with yields on benchmark U.S. Treasury debt tumbling to toward a three-year low hit last week as investors also ramped up their bets the global economy is headed toward a recession. Market watchers are hoping that U.S. data would undermine some of those bearish bets on the global economy with surveys from the Institute for Supply Management due later in the day while U.S. payrolls data is due on Friday.

“The ISM … is going to be (a) particular important market mover as those who have been buying bonds strongly, suggesting that the U.S. is on course for recession, need to see some sort of justification,” said Andrew Milligan, head of global strategy at Aberdeen Standard Investments.

The yield on 10-year U.S. Treasuries fell 2 basis points to 1.4876%, off a three-year low of 1.443% touched last week. The yield dropped more than 50 basis points last month, the biggest monthly drop since August 2011. U.K. gilts and Italian debt led the rally in European sovereign bonds.

In FX, Sterling was the big mover in currency markets, nearing a three-year low with British Prime Minister Boris Johnson set for a showdown with Parliament over a no-deal Brexit. On the opposite performance end, the Bloomberg Dollar Spot Index touched the highest since May 2017 as uncertainty over the planning of U.S.-China trade talks supported the greenback; its seven-day winning streak is the longest since March. The dollar strengthened against all G-10 peers barring havens – the yen and the Swiss franc – as risk sentiment deteriorated; the biggest declines were seen in the NZ dollar and Norwegian krone.

After dropping to a record low on Monday, the offshore yuan failed to stage a rebound overnight as China and the U.S. struggled to set a date for planned trade talks this month. The onshore currency extended its decline Tuesday to the lowest level since February 2008, after news emerged that both sides had failed to agree on a date for Chinese officials to meet their U.S. counterparts in Washington. The offshore yuan fell as much as 0.47% overnight on the news, inching closer to 7.2 per dollar, before rising 0.2% as of 5:20 p.m. in Hong Kong. “The yuan will remain bearish, but the People’s Bank of China has been tightening its grip in the onshore yuan fixing and may attempt to anchor trading at the 7.1-7.2/USD range,” said Ken Cheung, chief Asian FX strategist at Mizuho Bank. The central bank set its daily yuan fix at a level stronger than market watchers expected for a 10th straight day, the longest stretch since June. When the onshore currency breaches the 7.2 level, the PBOC may step up measures such as issuing verbal comments to reinforce its intention to smooth the pace of the depreciating yuan, Cheung said.

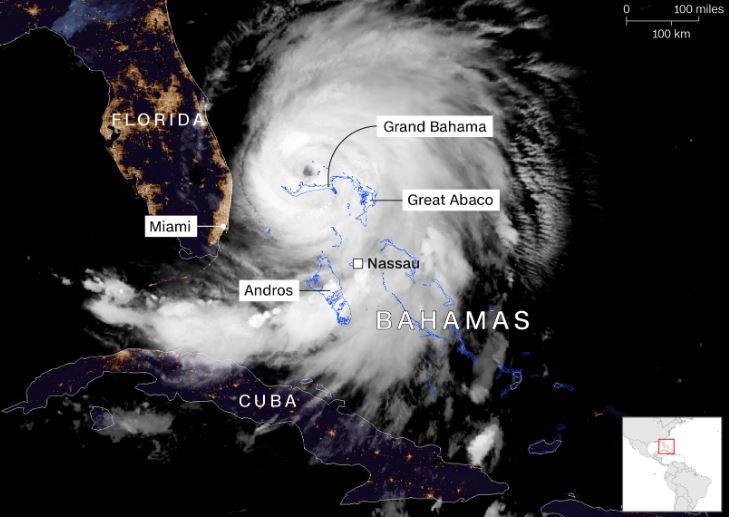

In commodities, oil prices were also dented by trade war concerns. U.S. West Texas Intermediate crude lost 0.47% to $54.84 per barrel. Brent futures dipped 0.05% to $58.63 per barrel amid concerns an economic slowdown from the trade war may dent demand. Forecasters are looking for signs a weakening Hurricane Dorian will turn north from the Bahamas rather than slamming head on into Florida.

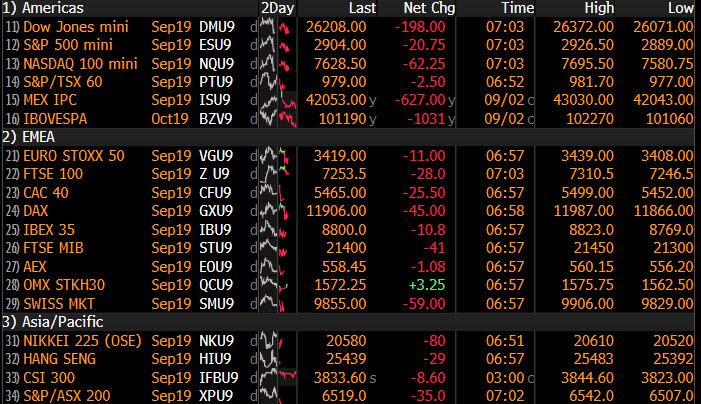

Market Snapshot

S&P 500 futures down 0.8% to 2,901.50

STOXX Europe 600 down 0.5% to 378.78

German 10Y yield fell 3.4 bps to -0.736%

Euro down 0.2% to $1.0945

Brent Futures down 1% to $58.07/bbl

Italian 10Y yield fell 3.1 bps to 0.626%

Spanish 10Y yield fell 4.0 bps to 0.088%

Brent Futures down 1% to $58.07/bbl

MXAP down 0.3% to 152.31

MXAPJ down 0.7% to 490.16

Nikkei up 0.02% to 20,625.16

Topix up 0.4% to 1,510.79

Hang Seng Index down 0.4% to 25,527.85

Shanghai Composite up 0.2% to 2,930.15

Sensex down 1.6% to 36,743.43

Australia S&P/ASX 200 down 0.09% to 6,573.40

Kospi down 0.2% to 1,965.69

Gold spot up 0.2% to $1,532.04

U.S. Dollar Index up 0.3% to 99.25

Top Overnight News from Bloomberg

Britain faces its third election in just over four years after Johnson said he would rather risk losing office than have his negotiations with the EU undermined. In a dramatic ultimatum, Johnson will try to trigger a snap vote on Oct. 14 if he loses a crunch vote in Parliament on Tuesday evening

BOE Governor Mark Carney is running out of opportunities to warn lawmakers just how much a no-deal Brexit will harm the economy. With Parliament set to be suspended next week, Carney’s appearance before the Treasury Committee Wednesday could be one of his last chances to publicly address MPs before Oct. 31

Chinese and U.S. officials are struggling to agree on the schedule for a planned meeting this month to continue trade talks after Washington rejected Beijing’s request to delay tariffs that took effect over the weekend, according to people familiar with the discussions

Italy’s new government would push through an expansionary 2020 budget and demand a review of European Union fiscal rules, according to a draft program seen by Bloomberg

France is taking advantage of record-low borrowing costs to plan its biggest-ever debt sale this week, just as signs emerge that investor sentiment may be faltering after a global rally

The U.S. East Coast from Florida to the Carolinas was bracing for devastating winds and a life-threatening storm surge from Hurricane Dorianas the Category 3 storm wreaks havoc on the Bahamas

Asian equity markets traded indecisively following a non-existent lead from Wall St due to the Labor Day holiday and as upcoming key risk events, as well as reports US and China are struggling to set a meeting for trade talks this month, added to the non-committal tone. ASX 200 (U/C) and Nikkei 225 (+0.1%) were choppy with upside in Australia limited by mixed data and amid the RBA rate decision where the central bank kept rates unchanged as expected, while advances in Tokyo were restricted by a mixed currency. Hang Seng (-0.4%) and Shanghai Comp. (+0.2%) conformed to the indecisive tone after reports noted difficulty in setting up planned US-China trade talks and after MOFCOM lodged a case against the US at the WTO, with PBoC inaction and a net daily liquidity drain of CNY 80bln also contributing to the lacklustre sentiment in China. Finally, 10yr JGBs were subdued after the pullback in T-notes but then gradually recovered after mixed 10yr JGB auction results.

Top Asian News

Japan Companies Are Sitting on Record $4.8 Trillion in Cash

Hong Kong’s Lam Says She Never Asked China’s Permission to Quit

China Sees Some Positive Signs in Hong Kong Despite Violence

European indices are marginally lower on the day [Eurostoxx 50 -0.4%] following on from a mostly subdued Asia-Pac lead and ahead of US markets’ first chance to react to the implementation of further US/China tariffs. UK’s FTSE 100 (-0.2%) derives some modest support, but remains in negative territory, from the weaker Pound as UK Parliament returns from their summer recess to challenge PM Johnson’s attempt to prorogue Parliament until 14th October. Sectors are mostly in the red, albeit defensive sectors are less dented than cyclicals. Turning to individual movers, easyJet (-3.9%) rests at the foot of the Stoxx 600 index due to a broker downgrade at Kepler Cheuvreux, whilst Iliad (-4.3%) is not far behind on the back of earnings. On the flip side, Renault (+1.2%) and Fiat Chrysler (+2.5%) shares spiked higher amid source reports that Renault and Nissan are seeking ways to end their alliances discord, a resolution may potentially lead to a Fiat Chrysler deal.

Top European News

U.K. Construction Shrinks Again as Brexit Sees New Work Dry Up

Moscow Police Detain Opposition Activists After Orderly Protests

Italy’s Draft Government Plan Pledges Expansionary 2020 Budget

Lego Reports 12% Drop in Profit Dragged Down by Asian Investment

In FX, the Pound has racked up more losses in advance of UK Parliament reconvening after the Summer break and in anticipation of a showdown between anti-no deal politicians across party divides and PM Johnson’s pro-Brexiteers. Like yesterday, stops were triggered in Cable once the previous 1.2015 ytd low was breached and again through the psychological 1.2000 before another round was tripped on a break of 1.1980 that sat just below 1.1986-83 ‘support’ from mid-May 2017. The selling has subsequently abated even though construction PMI missed expectations in line with Monday’s manufacturing headline print, but Sterling remains weak and extending relative declines vs G10 pears with Eur/Gbp firmly above 0.9100 and Gbp/Jpy hovering around 127.00 after an order driven lurch to circa 126.70 at one stage.

AUD/JPY/CHF – In contrast to the underperforming Pound, and despite ongoing strength in the Greenback (ie DXY up to 99.356 at best), the Aussie and Yen are at the top of the major ranks, as Aud/Usd reclaims 0.6700+ status and Usd/Jpy slips back to test underlying bids/support around 106.00. No change in rates or wait-and-see guidance from the RBA overnight has helped the Aussie stabilise amidst the ongoing US-China trade stalemate and further Yuan weakness, while a broader downturn in risk sentiment is keeping the Yen underpinned alongside Gold, but not the Franc uniformly. Indeed, Usd/Chf is still holding above 0.9900, while Eur/Chf creeps deeper below 1.0850, albeit largely due to Euro depreciation on top of no verbal intervention from the SNB, so far.

CAD/NZD/EUR – The Loonie and Kiwi have both lost more ground relative to their US peer (and latter against the aforementioned recovering Aussie as Aud/Nzd eyes 1.0700), with Usd/Cad climbing above 1.3350 ahead of NA Markit manufacturing PMIs, and ISM in the US, while Nzd/Usd has pulled back under 0.6300 into the latest GDT auction and not really gleaning support from NZ Finance Minister Robertson noting some robust domestic data and firm economic fundamentals, as he also stated that the Government is ready to react in the case of a shock. Elsewhere, the single currency continues to decline as noted above, and closer to 1.0923 support ahead of 1.0900, but may find some traction from hefty option expiries close by (2 bn between 1.0945-50).

EM – The Rand and Lira look technically and fundamentally ripe to claw back ground vs the Buck, with Usd/Zar reversing from almost 15.2900 towards 15.1250 and Usd/Try touching 5.7650 compared to 5.8220 at the other extreme in wake of SA GDP and Turkish CPI that confounded forecasts on the upside and downside respectively.

RBA kept the Cash Rate unchanged at 1.00% as expected. RBA stated the outlook for global economy is reasonable and that it is to ease policy if needed to support sustainable growth, while it added rates are to remain low for an extended period. RBA reiterated that it will monitor developments in labour market closely and that signs of a turnaround in housing market but sees inflation likely to be subdued for some time and noted the outlook for consumption remains the main domestic uncertainty.

In commodities, WTI and Brent futures are on the backfoot in early EU trade, with prices around 54/bbl and under 58/bbl respectively. Prices may also see divergence as WTI had no settlement yesterday due to the US Labor Day Holiday, which will also see the weekly API and DoE inventory data pushed back by a day. Price action has largely been dictated by sentiment thus far, with ongoing US/China, Brexit and Hong Kong woes weighing on risk appetite. State-side, NHC said a tropical cyclone is expected to form later today over SW Gulf of Mexico, tropical storm warnings have been issued for portions of NE Mexico. The potential tropical cyclone Seven is located about 220 miles East of La Pesca, Mexico, with maximum sustained winds of 35mph. Meanwhile, Hurricane Dorian is reportedly stationary and is expected to drift North/Northwest later, away from the Gulf of Mexico. Elsewhere, gold is relatively flat but off of intra-day lows and in positive territory despite the DXY printing fresh YTD highs as investors increase positions in safe-haven assets. Conversely, the risk aversion has taken a toll on copper prices which currently reside below the 2.50/lb level. Finally, Dalian iron ore futures rose in excess of 4% amid a rosier demand outlook for the base metal as steel mills restock their supplies.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 50, prior 49.9

10am: ISM Manufacturing, est. 51.2, prior 51.2;

10am: Construction Spending MoM, est. 0.3%, prior -1.3%

DB’s Jim Reid concludes the overnight wrap

For a brief moment yesterday the main headline out of No.10 Downing Street yesterday was the arrival of a very cute new adopted Jack Russell puppy named Dilyn. However fast moving political events soon overshadowed this. Although before moving on I can’t help wonder what Larry the Downing Street cat made of the new arrival.

The news quickly moved from puppies to polling as speculation intensified as the day progressed that a government commitment to a general election was imminent. PM Boris Johnson spoke outside No.10 just after 6pm UK time and suggested that if Parliament blocks no deal this week and votes for a delay, they are making his negotiations with the EU impossible. This move comes in the wake of news that lawmakers plan to raise a motion today to take over the order paper tomorrow and raise a bill to force the government to extend A50. It specifies the government must seek an extension to 31st January 2020 or agree to any extension EU27 provides. It also says this must be complied with by 19th October. The vote will likely take place tomorrow evening. Mr Johnson didn’t actually say that an election will follow a loss in tomorrow’s vote as was expected beforehand but it’s hard to see what the alternative is and there are plenty of well respected and connected journalists suggesting that an election on October 14th is being lined up. Interestingly this is a Monday as the crucial EU summit takes place on the 17-18th and takes the usual Thursday UK election slot. The last non-Thursday general election was in 1931. Apparently historically Fridays were always ruled out as politicians were worried that burgeoning end of the week pay packets were likely to lead to drunken voting. Insert your own jokes here but people from both sides of the Brexit debate might need a stiff drink at the end of this week! We should also add that with fixed term parliaments the PM can’t automatically call an election as 2/3rds of the House requires to vote for it. However this is surely a formality if the PM supports it as the opposition party has been calling for one. The most interesting scenario though is that the PM loses the vote tomorrow and the opposition refuse to vote for an election or insist on it being held after October 31st thus leaving the PM trapped. One to watch.

Sterling had a tough day on continuous speculation about the day’s likely news and weakened about -0.80% by the afternoon and was then relatively unmoved by the PM’s statement, partly helped by no US trading. It is trading down a further -0.27% this morning though.

In light of yesterday’s developments, it’s worth noting where the latest polls are. YouGov has run two separate polls in the last week with the 28-29 Aug poll showing a 33% versus 22% Conservatives-Labour split. The poll from 27-28 August in conjunction with the Times had a 34% versus 22% split. The Brexit Party picked up 12% and 13% respectively and Lib Dems 21% and 17% respectively. Since then the Survation/Daily Mail poll conducted over 29-30 August had a slimmer lead for the Conservatives over Labour at 31% versus 24% (albeit with a much smaller sample size). Most recently, the Deltapoll/Mail on Sunday poll had a 35% versus 24% split. It feels to me that the country is still very close to being 50/50 split on Brexit and the key to any election is which side unites more around one party than the other side. With Boris Johnson doing everything he can to win back a high proportion of the those who flocked to the Brexit Party, the Labour and Liberals are probably going to need a plan as how they can avoid splitting the remain vote.

So expect there to be a lot more focus on the polls in light of yesterday’s news, especially if the government lose tomorrow’s vote as expected. Over in markets 10y Gilts (-6.7bps) tracked the move in Sterling however most other European bond markets were a shade weaker to unchanged after the manufacturing PMIs broadly printed in line with expectations (more on those below). Indeed 10y Bund (-0.1bps) and OAT (+0.6bps) yields were flat to slightly higher along with 10y yields in Spain (+2.3bps) and Portugal (+0.9bps) although BTPs (-3.0bps) extended their strong recent run with the spread over Bunds now down to 167bps. To think that spread was closer to 240bps in early August.

In equity markets, with the US off on holiday, volumes were down some 50% or so however markets did finish slightly on the positive side with small gains for the STOXX 600 (+0.32%) and DAX (+0.12%). The FTSE 100 (+1.13%) was a standout thanks to the currency move while Italy’s FTSE MIB also closed up +0.50%. In EM the Argentinian Peso strengthened +6.21% after the nation imposed capital controls while in commodities Gold (+0.59%) closed up but is trading down -0.30% this morning while Brent oil futures were down -2.90% yesterday.

In other news, yesterday late afternoon Bloomberg reported that the US and China were struggling to agree on a date to meet this month. S&P futures after being flattish at around Europe’s lunchtime traded as low as -1% down after headlines. They are down -0.54% as we type.

Bourses in Asia are trading flat to down amidst low volumes this morning. The Nikkei (+0.04%) and Shanghai Comp (-0.05%) are trading broadly unchanged while the Hang Seng (-0.10%) and Kospi (-0.17%) are slightly lower. In Fx, all G10 currencies are trading weak (range c. -0.1% – -0.5%) with the US dollar index trading up +0.37% at 99.281, the highest level since May 2017. Asian EM Fx is also trading weak with the onshore Chinese yuan down -0.15% to 7.1824 with the Indian rupee leading the declines (-0.88%). Meanwhile the 10y UST yield is up +2.9 bps this morning and the 2y yield up +1.5bps bringing the 2s10s curve back in marginally positive territory (+0.4bps). The yields on the 30y UST is up +3.9bps. As for overnight data releases, South Korea’s August inflation printed at 0% yoy (vs. +0.2% yoy expected and +0.6% yoy last month) – a record low – and core inflation printed in line with expectations at +0.9% yoy (vs. +1.0% yoy last month) while the final Q2 GDP was revised down one tenth from the initial read at +2.0% yoy. Separately, the BoK said that the recent low inflation is mainly due to supply-side factors and government’s policies on welfare and it’s hard to say it’s the precursor of deflation while adding that inflation will quickly rebound around the end of this year.

Back to yesterday, where with the ECB meeting now just a stone’s throw away, the PMIs were always going to be a bit more peripheral than normal and the fact that they were broadly close to consensus only furthered that argument. Indeed the manufacturing reading for the Euro Area was confirmed at 47.0 and unrevised from the flash with a slight upward revision for France (51.1 from 51.0) offset by a slight downward revision for Germany (43.5 from 43.6). There were however slight positive surprises for Italy (48.7 vs. 48.5 expected) and Spain (48.8 vs. 48.5 expected) although this needs to be taken in context of both still being in contractionary territory.

Meanwhile, the UK’s manufacturing PMI (47.4 vs. 48.4 expected) hardly made for pretty reading. The market is obviously more focused on Brexit developments however this was still the lowest reading in 85 months with new orders also at the lowest level in over 7 years. Most of the forward-looking indicators were fairly weak too with the data still very much consistent with the manufacturing sector in recession.

So the baton passes to the US today where we’ll get the August ISM manufacturing and final manufacturing PMI revisions. The market expects the ISM to have held steady at 51.2 which as a reminder was the lowest since August 2016. The reading has also dropped for 4 consecutive months and 8 of the last 11 months. We should flag that our US economists expect a temporary bounce in today’s ISM to 52.5 in light of the regional survey data however they do expect further downside risks in the near term owing to trade uncertainty.

To the day ahead now, where the only data of note this morning is the July PPI print for the Euro Area. In the US this afternoon the highlight is likely to be the August ISM manufacturing report, while the final August manufacturing PMI revisions will also be made. The July construction spending print is the only other data of note. Away from that the Fed’s Rosengren is due to speak late this evening.

via ZeroHedge News https://ift.tt/34ntBd1 Tyler Durden

If you were a KGB agent in the heyday of Cold War surveillance, how would you design the perfect snooping system?

This system should gather good dirt on all people within the Soviet Union. We want to identify people and their habits to build behavioral profiles and keep tabs on their comings and goings. And it should it be as unobtrusive as possible; we wouldn’t want the masses to start making a fuss about our valiant civic undertaking. What would you do?

This was the question posed to a group of academics attending a 1971 conference at the Center for Strategic and International Studies at Georgetown University. They had two days to dream up a perfectly evil surveillance architecture.

Their answer? “This group decided that if you wanted to build an unobtrusive system for surveillance, you couldn’t do much better than an electronic funds transfer system.”

So told former RAND analyst and self-described “computer-nik” Paul Armer to the Senate in a 1975 testimony. He elaborates:

The system not only collects and files a great deal of data about your financial transactions—and that means a great deal of data about your life—but the system knows where you are every time you make such a transaction. [emphasis original]

It’s genius, really. No spies, clunky camera and microphone equipment, or random checkpoints are needed. All you have to do to get a detailed surveillance picture of a population is to hand them a payment card and send them on their way.

Armer was prescient. At the time he wrote, our modern payments system was still being built. “National BankAmericard” and “Master Charge”—now known as Visa and Mastercard—were young pups and only served a tiny portion of the population. But Armer and his colleagues quickly intuited how the structures these new ventures were building could be exploited for ill ends.

The problem is that such technologies could only work if users entrusted lots of sensitive information to service providers. The bank would need to know your personal identity and financial information. This would be shared with the payments network. The retailer would report what you bought and when to the network and bank. It would be trivial to build a detailed profile on your known locations and consumption habits. And since the whole operation would be digitized, this information would be quickly updated and easy to obtain.

It’s not that financial institutions set out to build a super snooper for Uncle Sam. It’s just that the infrastructure needed to operate a third party-provided payment system is coincidentally the same architecture that allows for constant spying. And all we see is convenience!

The happy accident of surveillance as a by-product of modern payments technology quickly attracted government interest. Peter van Valkenburgh of Coin Center describes how case law and legislation like the Bank Secrecy Act targeted third-party financial providers as holders of coveted personal information. Financial institutions can and do turn over information on certain exchanges to governments every day.

But really, Armer was a bit of an optimist. While he was spot on in articulating the surveillance dangers of a pervasive third party-based payment network, his article didn’t foresee how advertisers and data brokers could get looped in and make an even bigger mess of things. Our payments system poses a greater surveillance risk because advertising is how most platforms make money online.

Consider this recent feature from the Washington Post, which traces how companies share transaction data when you make a card purchase. The columnist, Geoffrey Fowler, tried to track down exactly how many firms got his information when he purchased a humble banana. While companies are tight-lipped on how they share data, he was able to get a general picture of the records life of a card-based transaction.

Each time you swipe your card to buy a piece of fruit, at least six categories of corporations can receive your data, depending on how you pay: your bank, the payments network, the store itself, the point-of-sale system, mobile wallets like Google Pay, and financial apps like Mint.

And all of these groups love to share. Take your bank. The Gramm-Leach-Bliley Act of 1999 empowers banks to share customer data with “affiliates” for marketing purposes—so long as your bank tells you in the fine print of one of the many junk letters you toss out without reading and gives you the ability to opt out.

And share they do—ever wonder why you get Facebook ads for a product that you just purchased? Nonaffiliate marketing may be the culprit.

Fowler discovered that payment networks, too, will share information with businesses like Google, packaged as “data insights.” Mastercard says it scrubs any identifiable information from the data. Does that make you feel any better?

Even if these groups didn’t decide to share, they can do creepy things with the data we give them. I’ve written before about how Target—coincidentally Fowler’s banana-peddler of choice—builds behavioral profiles of their customers to more effectively market to them. In one incident, Target flagged a teen mother-to-be’s pregnancy based on her activities before her family even knew. The barrage of advertisements for diapers and formula tipped the poor girl’s father off.

The insidious thing about this kind of private surveillance system is that it’s just so convenient. Most people—yours truly included—regularly swipe away without thought to the trail of breadcrumbs that our transaction graph reveals each day. Marketing is annoying, sure. And everyone knows that if we do something illegal, our transactions can be evidence in court.

But we rarely, if ever, consider just what a perfect surveillance system our payments network could be, as those Cold War theoreticians first brilliantly surmised in 1971.

The nice thing about this kind of private surveillance system is that we don’t need to participate. The KGB does not force us to use Visa. We have the freedom to use cash or even cryptocurrency to preserve our privacy if we choose. Most people don’t, of course. But we still have that right, and cryptocurrency transactions, while still maturing, are becoming more accessible and private all the time.

The freedom to use physical and digital cash is precious, but it is unfortunately not guaranteed. As Jerry Brito of Coin Center has pointed out, there is a movement to do away with cash altogether. Many commentators see it primarily as a way to facilitate crime or thwart central bank plans. Others attack cryptocurrency for similar reasons.

But as the recent protests in Hong Kong demonstrate, doing away with cash would leave us at the mercy of governments and financial institutions that do not always have our best interests in mind. Even if you don’t use cash or cryptocurrency in your day-to-day life, it’s an important exit option to appreciate and defend.

Maybe this Cold War thought experiment won’t convince you to cut your cards altogether. But it should give us all food for thought of what we have to lose if the alternatives to our payments infrastructure are taken away from us.

from Latest – Reason.com https://ift.tt/2ZHbrj7

via IFTTT

Hurricane Dorian has weakened from a Category 4 storm down to Category 3, now with winds of 120 miles per hour, but experts and officials say it’s too soon for Floridians to relax.

The storm stalled over the island of Grand Bahama for a day, staying in roughly the same position for 12 hours. Prime Minister Hubert Minnis described the storm as a “historic tragedy,” with five people confirmed to have died. Roughly 13,000 homes have been destroyed or seriously damaged.

Now, it’s setting its sights on the Eastern seaboard. There are already reports of flooding in Miami.

We have a report of ongoing coastal flooding on NE 30th Street at Biscayne Bay in Miami early this morning. Remember to never drive through flooded roadways. #TurnAroundDontDrown#FLwxpic.twitter.com/Pu3zIdL8Nr

Millions have been ordered to evacuate across Florida, Georgia, and the Carolinas. In Florida, where many people have been preparing for the hurricane since last week, many families have built up stockpiles of emergency supplies and food, according to CNN.

Some hurricane shelters in Stuart, Florida have already stopped accepting evacuees. “If they haven’t evacuated yet, it’s too late,” said CNN meteorologist Derek Van Dam in Stuart.

“In fact, the shelters, the evacuation centers here in Martin County are no longer accepting evacuees. The causeway that connects the barrier islands where the mandatory evacuations have been under way since 1 p.m. yesterday are now closed,” Van Dam said.

Coastal areas like Stuart are already experiencing bands of rain and wind, though the storm is still roughly 100 miles away. The National Hurricane Center’s latest update is still focused on the Bahamas. Gusts north of 60 mph have been reported in Florida, and they will likely strengthen throughout the day on Tuesday as the storm moves closer.

If you were a KGB agent in the heyday of Cold War surveillance, how would you design the perfect snooping system?

This system should gather good dirt on all people within the Soviet Union. We want to identify people and their habits to build behavioral profiles and keep tabs on their comings and goings. And it should it be as unobtrusive as possible; we wouldn’t want the masses to start making a fuss about our valiant civic undertaking. What would you do?

This was the question posed to a group of academics attending a 1971 conference at the Center for Strategic and International Studies at Georgetown University. They had two days to dream up a perfectly evil surveillance architecture.

Their answer? “This group decided that if you wanted to build an unobtrusive system for surveillance, you couldn’t do much better than an electronic funds transfer system.”

So told former RAND analyst and self-described “computer-nik” Paul Armer to the Senate in a 1975 testimony. He elaborates:

The system not only collects and files a great deal of data about your financial transactions—and that means a great deal of data about your life—but the system knows where you are every time you make such a transaction. [emphasis original]

It’s genius, really. No spies, clunky camera and microphone equipment, or random checkpoints are needed. All you have to do to get a detailed surveillance picture of a population is to hand them a payment card and send them on their way.

Armer was prescient. At the time he wrote, our modern payments system was still being built. “National BankAmericard” and “Master Charge”—now known as Visa and Mastercard—were young pups and only served a tiny portion of the population. But Armer and his colleagues quickly intuited how the structures these new ventures were building could be exploited for ill ends.

The problem is that such technologies could only work if users entrusted lots of sensitive information to service providers. The bank would need to know your personal identity and financial information. This would be shared with the payments network. The retailer would report what you bought and when to the network and bank. It would be trivial to build a detailed profile on your known locations and consumption habits. And since the whole operation would be digitized, this information would be quickly updated and easy to obtain.

It’s not that financial institutions set out to build a super snooper for Uncle Sam. It’s just that the infrastructure needed to operate a third party-provided payment system is coincidentally the same architecture that allows for constant spying. And all we see is convenience!

The happy accident of surveillance as a by-product of modern payments technology quickly attracted government interest. Peter van Valkenburgh of Coin Center describes how case law and legislation like the Bank Secrecy Act targeted third-party financial providers as holders of coveted personal information. Financial institutions can and do turn over information on certain exchanges to governments every day.

But really, Armer was a bit of an optimist. While he was spot on in articulating the surveillance dangers of a pervasive third party-based payment network, his article didn’t foresee how advertisers and data brokers could get looped in and make an even bigger mess of things. Our payments system poses a greater surveillance risk because advertising is how most platforms make money online.

Consider this recent feature from the Washington Post, which traces how companies share transaction data when you make a card purchase. The columnist, Geoffrey Fowler, tried to track down exactly how many firms got his information when he purchased a humble banana. While companies are tight-lipped on how they share data, he was able to get a general picture of the records life of a card-based transaction.

Each time you swipe your card to buy a piece of fruit, at least six categories of corporations can receive your data, depending on how you pay: your bank, the payments network, the store itself, the point-of-sale system, mobile wallets like Google Pay, and financial apps like Mint.

And all of these groups love to share. Take your bank. The Gramm-Leach-Bliley Act of 1999 empowers banks to share customer data with “affiliates” for marketing purposes—so long as your bank tells you in the fine print of one of the many junk letters you toss out without reading and gives you the ability to opt out.

And share they do—ever wonder why you get Facebook ads for a product that you just purchased? Nonaffiliate marketing may be the culprit.

Fowler discovered that payment networks, too, will share information with businesses like Google, packaged as “data insights.” Mastercard says it scrubs any identifiable information from the data. Does that make you feel any better?

Even if these groups didn’t decide to share, they can do creepy things with the data we give them. I’ve written before about how Target—coincidentally Fowler’s banana-peddler of choice—builds behavioral profiles of their customers to more effectively market to them. In one incident, Target flagged a teen mother-to-be’s pregnancy based on her activities before her family even knew. The barrage of advertisements for diapers and formula tipped the poor girl’s father off.

The insidious thing about this kind of private surveillance system is that it’s just so convenient. Most people—yours truly included—regularly swipe away without thought to the trail of breadcrumbs that our transaction graph reveals each day. Marketing is annoying, sure. And everyone knows that if we do something illegal, our transactions can be evidence in court.

But we rarely, if ever, consider just what a perfect surveillance system our payments network could be, as those Cold War theoreticians first brilliantly surmised in 1971.

The nice thing about this kind of private surveillance system is that we don’t need to participate. The KGB does not force us to use Visa. We have the freedom to use cash or even cryptocurrency to preserve our privacy if we choose. Most people don’t, of course. But we still have that right, and cryptocurrency transactions, while still maturing, are becoming more accessible and private all the time.

The freedom to use physical and digital cash is precious, but it is unfortunately not guaranteed. As Jerry Brito of Coin Center has pointed out, there is a movement to do away with cash altogether. Many commentators see it primarily as a way to facilitate crime or thwart central bank plans. Others attack cryptocurrency for similar reasons.

But as the recent protests in Hong Kong demonstrate, doing away with cash would leave us at the mercy of governments and financial institutions that do not always have our best interests in mind. Even if you don’t use cash or cryptocurrency in your day-to-day life, it’s an important exit option to appreciate and defend.

Maybe this Cold War thought experiment won’t convince you to cut your cards altogether. But it should give us all food for thought of what we have to lose if the alternatives to our payments infrastructure are taken away from us.

from Latest – Reason.com https://ift.tt/2ZHbrj7

via IFTTT

“I believe in public education, and I believe in public charter schools,” explained Sen. Bernie Sanders (I–Vt.) at a CNN town hall in March. What the candidate for the Democratic presidential nomination doesn’t believe in, he said, are “privately controlled charter schools.”

The problem with that distinction is that all charters are privately controlled to some degree. They are also all public schools, funded with taxpayer money. That dual nature is what distinguishes charter schools from every other kind.

Sanders clarified his stance when he released an education plan in May. While he wants more “accountability” for nonprofit charters, he would entirely ban their for-profit counterparts.

According to data obtained from the National Alliance for Charter Schools, schools run by for-profit companies make up roughly 12 percent of charters nationwide. One of the goals of these schools—at least on paper—is to make money. Regardless of what they do for their students, that makes for-profit charters a perfect target in the eyes of democratic socialists like Sanders.

How well they serve students matters, however. Such charters exist because parents prefer them to the state-run alternative. “Charter schools are held accountable by parents, who can choose or not choose to enroll their children there,” says Lindsey Burke, the Will Skillman Fellow in Education at the Heritage Foundation. “Charters only receive [public] funding if families are selecting into them.”

By contrast, Burke says, “public schools are in the position of near-monopolies that receive students—and funding—regardless of how poorly they perform. Those interested in ‘accountability’ should start by turning a critical eye toward the traditional public school system, where fraud and financial mismanagement is, unfortunately, a reality for districts across the country.”

Sanders would likely counter that for-profit charters are partiallyresponsible for low student achievement. Online charter schools, in particular, present a conundrum for charter devotees: Studies show that those students exhibit weaker academic performance in both reading and math.

But even that model has its place, argues Burke. “Online charters are serving the needs of students who in some cases cannot attend a brick-and-mortar school, or who want to try an individual course, or who have been completely left behind by the traditional public school system,” she says. “In some cases, online options are providing important credit recovery options and drop-out prevention tools.”

These educational alternatives have become scapegoats for poor outcomes in traditional public schools, from whom charters supposedly siphon difference-making dollars. But charter schools collect just 64 percent of the funds that traditional public schools receive. Students enrolled in the latter cost an average of $13,764 in state funding per year, or nearly $170,000 for each individual who receives a K–12 education. Yet only one-third of high schoolers are able to read proficiently.

from Latest – Reason.com https://ift.tt/2PC8AYV

via IFTTT

“I believe in public education, and I believe in public charter schools,” explained Sen. Bernie Sanders (I–Vt.) at a CNN town hall in March. What the candidate for the Democratic presidential nomination doesn’t believe in, he said, are “privately controlled charter schools.”

The problem with that distinction is that all charters are privately controlled to some degree. They are also all public schools, funded with taxpayer money. That dual nature is what distinguishes charter schools from every other kind.

Sanders clarified his stance when he released an education plan in May. While he wants more “accountability” for nonprofit charters, he would entirely ban their for-profit counterparts.

According to data obtained from the National Alliance for Charter Schools, schools run by for-profit companies make up roughly 12 percent of charters nationwide. One of the goals of these schools—at least on paper—is to make money. Regardless of what they do for their students, that makes for-profit charters a perfect target in the eyes of democratic socialists like Sanders.

How well they serve students matters, however. Such charters exist because parents prefer them to the state-run alternative. “Charter schools are held accountable by parents, who can choose or not choose to enroll their children there,” says Lindsey Burke, the Will Skillman Fellow in Education at the Heritage Foundation. “Charters only receive [public] funding if families are selecting into them.”

By contrast, Burke says, “public schools are in the position of near-monopolies that receive students—and funding—regardless of how poorly they perform. Those interested in ‘accountability’ should start by turning a critical eye toward the traditional public school system, where fraud and financial mismanagement is, unfortunately, a reality for districts across the country.”

Sanders would likely counter that for-profit charters are partiallyresponsible for low student achievement. Online charter schools, in particular, present a conundrum for charter devotees: Studies show that those students exhibit weaker academic performance in both reading and math.

But even that model has its place, argues Burke. “Online charters are serving the needs of students who in some cases cannot attend a brick-and-mortar school, or who want to try an individual course, or who have been completely left behind by the traditional public school system,” she says. “In some cases, online options are providing important credit recovery options and drop-out prevention tools.”

These educational alternatives have become scapegoats for poor outcomes in traditional public schools, from whom charters supposedly siphon difference-making dollars. But charter schools collect just 64 percent of the funds that traditional public schools receive. Students enrolled in the latter cost an average of $13,764 in state funding per year, or nearly $170,000 for each individual who receives a K–12 education. Yet only one-third of high schoolers are able to read proficiently.

from Latest – Reason.com https://ift.tt/2PC8AYV

via IFTTT

Norway has been hailed as a model for electric vehicles adoption with EV sales exceeding 57% of new car sales in June of this year. This accomplishment stands at odds with the rest of the world, where despite substantial subsidies, EV sales have lingered in the low single digits. The reality of Norway’s EV sales success is rooted in the simple fact that Norway has created an extremely distorted car market.

Norway’s cold weather makes the country one of the least suitable markets for electric cars since freezing temperatures tend to reduce an EV range by up to 40%. This fact alone makes Norway a less likely market for wide EV adoption. EVs high price tag, range limitations, slow charging time and limited second market makes them a niche product in many markets, said another way, EVs practical inferiority to internal combustion engine (ICE) cars has discouraged their adoption at a wide scale. To counter EVs inherent inferiority, the Norwegian government has introduced a host of market distorting – stick and carrot – initiatives to force EVs adoption:

EV Carrots:

EVs are exempt from VAT and other taxes on car purchases and sales.

Parking in public parking spaces is free.

EVs can use most toll roads and several ferry connections free of charge.

EVs are allowed to use bus and collective traffic lanes.

The company car tax is 50 per cent lower on EVs, and the annual motor vehicle tax/road tax is also lower.

Battery charging is free at a rapidly growing number of publicly funded charging stations.

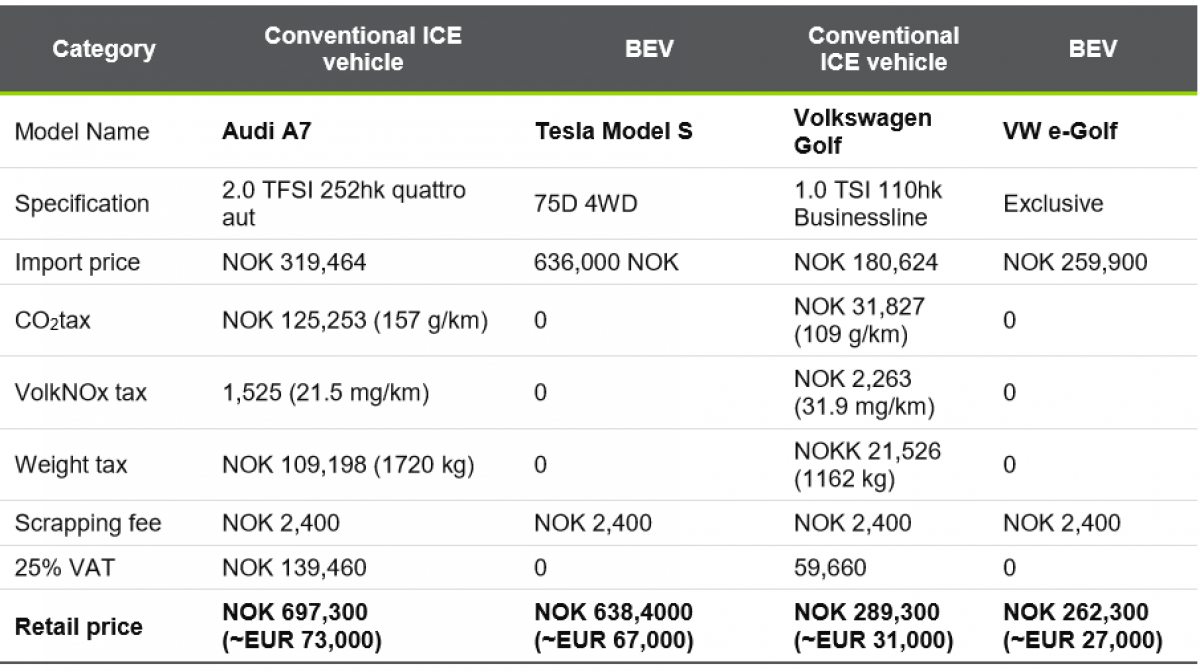

As result of the above distortions, ICE cars cost more to purchase in Norway and are up to 75% more expensive to operate. Thus, it is no wonder that EV sales have been growing at a brisk rate in Norway. As a matter of fact, it is mind boggling as to why anyone would even purchase an ICE car in Norway under these conditions.

(Source: Norsk Elbilforening)

Having these many incentives come at a great cost to the Norwegian treasury, or more precisely these incentives come at a great cost to the Norwegian taxpayer. Governments may create the conditions for wealth creation, but they don’t create wealth per se, wealth is created by private enterprise and is taxed and redistributed by governments for the public good. The Norwegian government seems to be believe that a switch to EVs (due their supposed CO2 emissions reduction) is in the public interest.

At what cost?

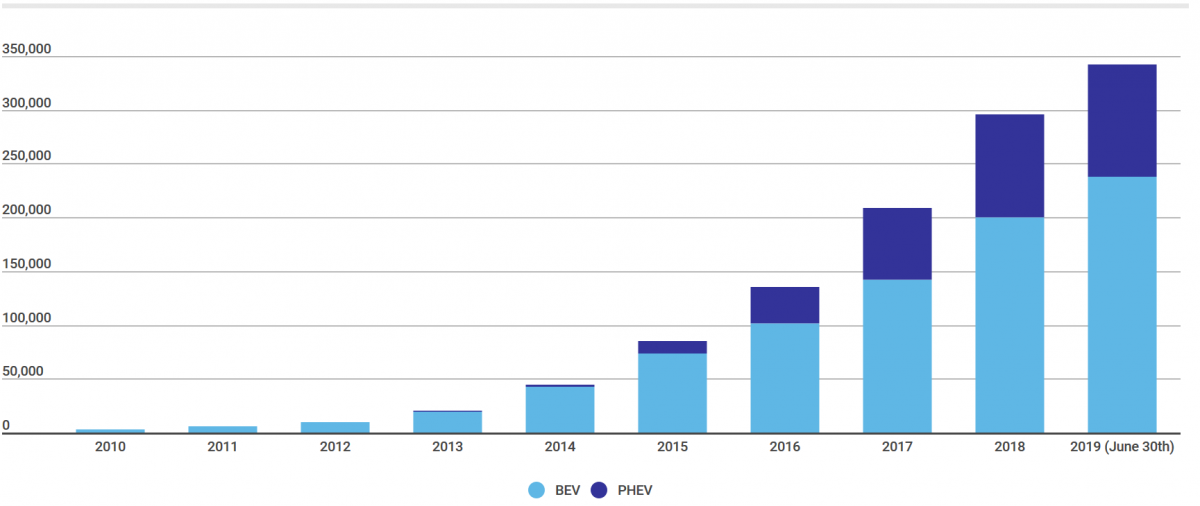

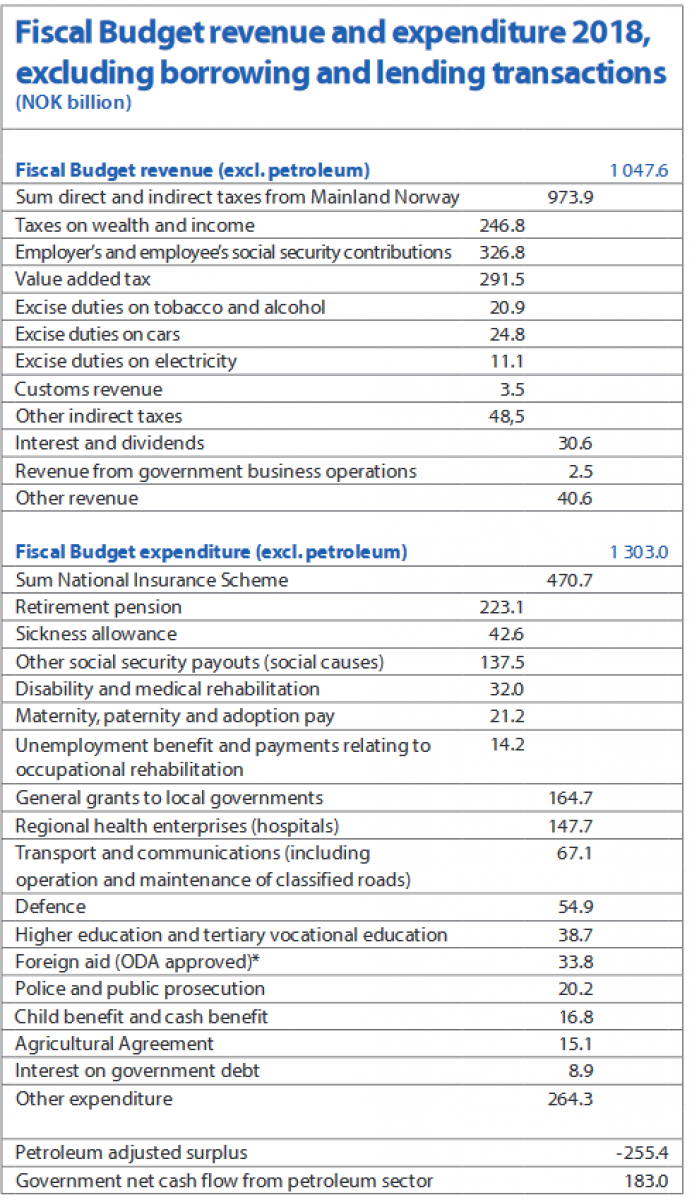

In 2014, Bjart Holtsmark (Statistics Norway) and Anders Skonhoft (Department of Economics, Norwegian University of Science and Technology) answered this question in an excellent research paper. According to that independent study, the annual EV incentives cost to the Norwegian treasury stands at a staggering $8100 per EV (excluding the value of free charging and bus lane access). At the end of 2018, Norway had 200,000 registered EVs (I am excluding PHEVs from the calculation since they have different incentives), this means the total annual EV subsidy cost to the Norwegian treasury stands at $1.62 billion dollars (14.6B NOK) per year as of the end of 2018. The annual subsidy has grown to around $1.95 billion dollars (21.6B NOK) as of June 30th due to the rapid growth in the EV fleet. Norway has a total of 2.7M private cars, if the country were to convert all of them to EVs under the same incentives scheme, the total annual cost to the Norwegian treasury would reach $22 billion dollars per year (198B NOK). To put these numbers in prospective, here is the breakdown of Norway’s 2018 fiscal budget:

(Source: Government of Norway)

Based on the above, we can see that the annual cost of Norway’s EV support scheme already exceeds the annual cost of Maternity and Paternity leave pay (21.2B NOK) and also exceeds the annual Unemployment Benefit budget (14.2B NOK) and the Child Benefit budget (16.8B NOK). As a matter of fact, if Norway were to convert all its cars to EVs, the country EV budget would become the second largest government expenditure at 198B NOK, only behind the retirement pension budget at 223B NOK. It is worth noting that Norway is running a sizable 20% primary budget deficit (excluding oil revenues) and 7% deficit including oil revenues. Norway’s EV support is already having a material impact on Norway’s finances, the excise duties on cars and petrol have declined by 25.9B NOK in 5 years from 50.7B NOK in 2013 to 24.8B NOK in 2018. If this revenue item had remained constant, Norway’s budget deficit for 2018 would have shrunk to 4.2% from 7%.

Emissions and social costs

At this stage one may ask what Norway is getting out of all of this? EVs are not a goal into themselves, EVs are a mean to an end, namely, reducing gasoline and diesel consumption, which ultimately means a reduction in CO2 emissions. Let’s take a look at Norway’s petroleum consumption since 2014:

(Source: Statistics Norway)

In 2014, Norway consumed a total of 5M liters of auto diesel and gasoline (tax and untaxed), by 2018 that number increased to 5.06M liters or a 1.2% increase. More damming still is that last year alone Norway’s CO2 road traffic emissions increased by 2.8% (excluding EVs CO2 lifecycle emissions). To be fair, road traffic emissions (although increased in 2018) did decline by about 10% from 9.9M tons in 2014 to 9M tons in 2018. Norwegian road traffic emissions statistics don’t capture a vehicle lifecycle emissions which are much higher at the outset for an EV due to the heavy CO2 emissions associated with battery production. This lifecycle gap in the data exaggerates the amount of CO2 emission reduction due to the displacement of emissions from where the car is driven to where it is produced. Another factor we need to consider is the continued improvement in fuel efficiency of newer ICE cars, which means as the ICE car fleet is renewed associated CO2 emissions are reduced naturally. Thus, when we take in consideration these factors, it is probable that the actual four-year reduction in Norwegian CO2 road emissions due to EVs is in the low single digits at best.

In light of the above, it is fair to say that Norway’s massive investment in EVs in eliminating a negligible amount of CO2 comes at a great financial cost. One reason for the muted impact of EVs on Norwegian gasoline and diesel consumption is that 64% of Norwegian households that own an EV also own an ICE car. Two cars households used ICE cars for 60% of their driving needs and EVs for 40%. The second car effect is apparent in the passenger car data: In 2014, Norway had 2.55M passenger cars (including 50K EVs and PHEVs) as compared to 2.76M passenger cars (Including 300K EVs and PHEVs) in 2018. This shows that the ICE fleet has remained constant and that EVs are supplementing ICE cars and not replacing them.

Another interesting feature of the Norwegian EV market is the split between the have and the have nots. The likelihood of purchasing an EV is 15 times higher for the richest 25% of Norwegian households as compared to the bottom 25%. Since the purchase price of an EV is cheaper than an ICE car in Norway that discrepancy can not be explained by the initial cost barrier. The fact that 84% of the richest households own at least one additional ICE car against only 21% of the poorest households seems to indicate that without access to a second ICE car, owning an EV – despite all the incentives – is less appealing to the average person. This is most likely due to EVs inherent limitations as compared to ICE cars. In many ways, Norway’s EV support policy is a second car discount and living cost subsidy mechanism for the rich.

Cited research by Halvorsen and Froyen Indicates that such an extreme support for EVs is encouraging Norwegians to rely less on public transport and on walking and cycling. Only 14% of EV owners use public transport, cycle, or walk, as compared to more than 50% for non-EV owners.

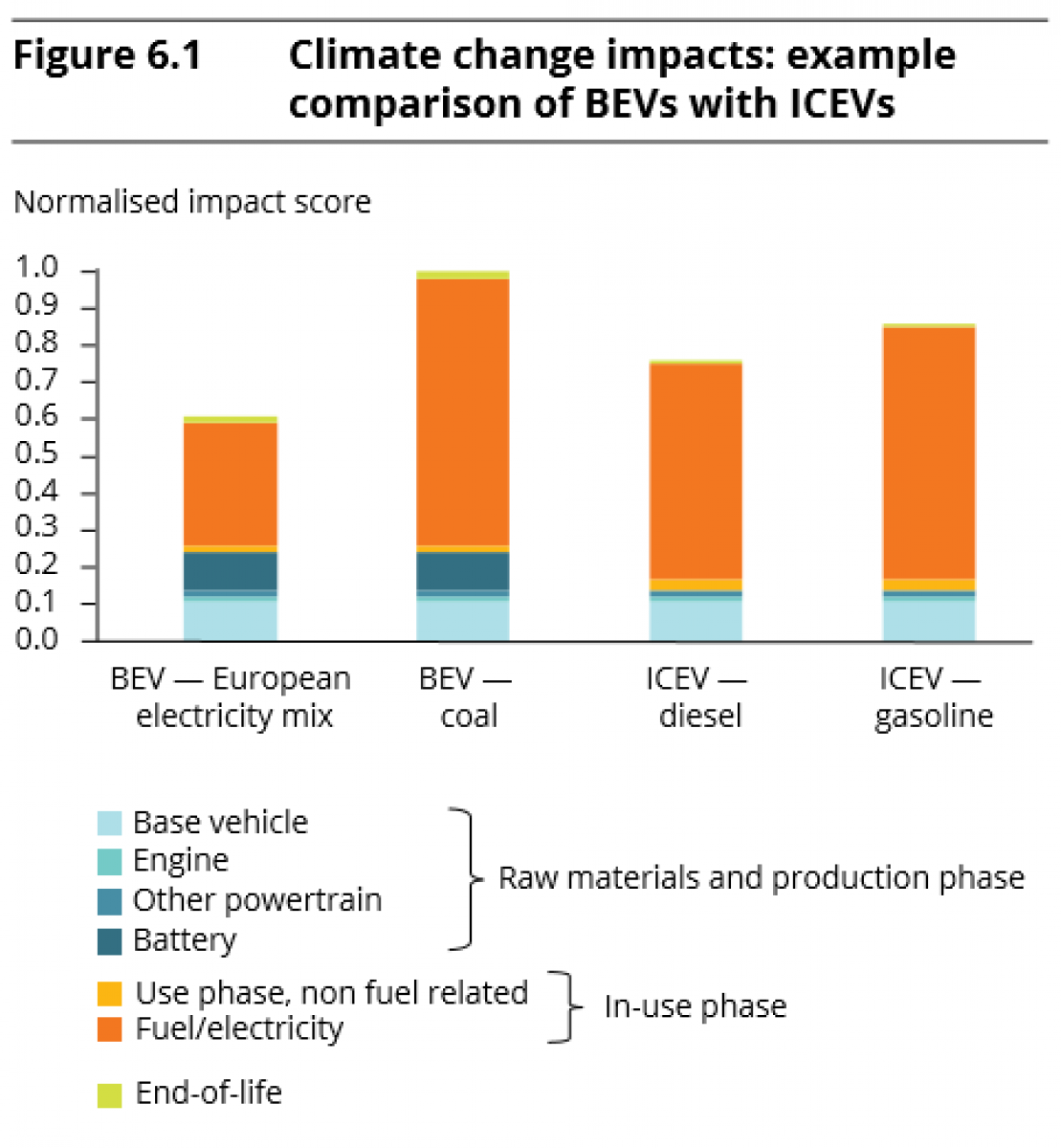

Favoring EVs as a policy to reduce CO2 emissions is marginally effective at best and very expensive. The policy creates a number of perverse incentives and contributes to an increase in economic inequality. In the aforementioned research paper on Norway’s EV policy, the authors conclude that the reduction in Norway’s CO2 emissions through EV adoption comes at the extraordinary cost of $13500 per ton of CO2. Considering that Norwegian road traffic emissions stood at 9M tons as of 2018. You can do that math as what it would cost to bring these emissions to zero at $13500 per ton. Several studies have shown that EVs have a relatively limited (17% to 30%) CO2 emissions reduction impact – on lifecycle basis – under the current European electricity mix:

(Source: European Environment Agency)

While it is likely that European electricity will become increasingly emission free in the coming decades, a larger decrease in CO2 transport emissions today can probably be achieved faster (and for a much lower cost) through a policy mix focused on public transport and highly efficient ICE vehicles. A recent study by the respected IFO Institute in Germany concluded that a switch to EVs would actually increase German CO2 road emission in comparison to a policy favoring fuel efficient diesel cars. My point here is not to promote a specific drive train technology, the point is that as a society we need to adapt effective and sustainable environmental and economic policies that will lead to tangible reductions in CO2 emissions. Norway’s model is absolutely not the one to follow. I will state for the record that once Norway reduces its generous EV incentives in 2020/2021, the country multi-year growth in EVs sales will likely reverse as was the case in Denmark in 2017.

Norway has pursued its extreme EV support policy due to the seemingly mistaken belief that one can both fight climate change and maintain a car culture. Considering the limits of of today’s personal vehicle technology and the limitations of public finances, the simultaneous pursuit of these two conflicting objectives is perhaps a well-intentioned folly.

via ZeroHedge News https://ift.tt/2LeUMzk Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}