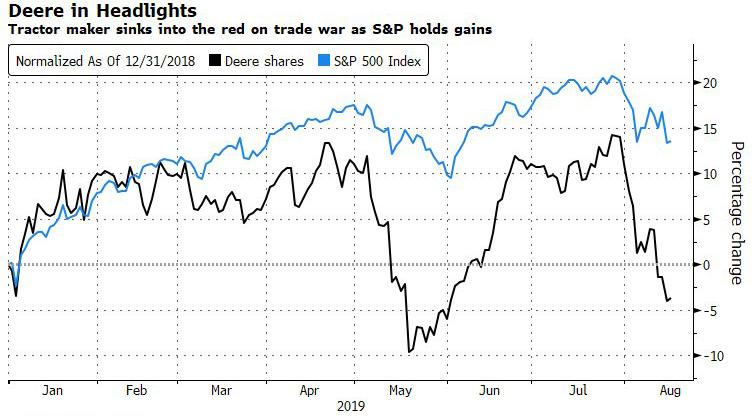

For those asking this morning if the US-China trade war is hurting the economy – and America’s farmers – look no further than heavy industrial equipment giant Deere which this morning cut its earnings guidance for a second straight quarter and announced a review of costs as U.S. farmers – battered by trade and weather disruptions – were unable to splurge on expensive new tractors.

While Deere’s Q3 results were dismal – with the company missing on both the top line, reporting 3Q net sales of $8.97 billion, down -3.4% y/y, and below the estimate of $9.38 billion, and the bottom line, with Q3 adjusted EPS of $2.71 missing estimates of $2.84 – its guidance was worse.

Deere cut its net income and its construction & forestry equipment sales forecasts for the full year, with the guidance missing the average analyst estimate. The company now sees FY net income about $3.2 billion, down from $3.3 billion previously, and below the sellside estimate of $3.29 billion. The company also cut its FY construction & forestry equipment sales forecast to +10%, from +11%, and below the +11% estimate. Deere also said it was “conducting a thorough assessment of its cost structure and initiating a series of actions to make the organization more structurally efficient and profitable.” For fiscal 2019, equipment sales are now projected to rise about 4%, with net income forecast at $3.2 billion, the Moline, Illinois-based company said. Three months ago, it predicted 5% equipment sales growth and $3.3 billion profit.

And so with fiscal Q3 earnings missing estimates and a sharp guidance cut, Deere shares fell 3.7% in pre-market trading on Friday before recovering some ground. The stock has badly underperformed the S&P since the start of the year.

The quarterly results “reflected the high degree of uncertainty that continues to overshadow the agricultural sector,” Chief Executive Officer Samuel Allen said in a statement Friday. “Concerns about export-market access, near-term demand for commodities such as soybeans, and overall crop conditions, have caused many farmers to postpone major equipment purchases.”

According to Bloomberg, the reason for the disappointing results was that US farmers were hesitating to upgrade their aging fleets of Deere’s iconic yellow and green tractors as the U.S.-China trade war stretches into a second year, undermining crop demand and fanning fears of recession. At the same time, record rainfall in the U.S. planting season gave way to hot, dry weather that has dimmed the outlook for yields and farmer incomes.

via ZeroHedge News https://ift.tt/2KNHDvz Tyler Durden

In a quiet end to an extremely tumultuous week (pending one or more shocking Trump tweets) there were no overnight trade war tape bombs from China, no additional curve inversions even as more than half of the world’s yield curves are now inverted…

… and so US equity futures surged and European stocks and most Asian shares posted modest gains on Friday, while Treasuries pared some of their recent blistering advance, taking advantage of the rare moment of quiet, as expectations grew of further stimulus by central banks, offsetting worries about slowing economic growth which intensified this week as the the US 2s10s yield curve inverted for the first time since 2007.

S&P 500 futures pushed above prior day’s highs amid renewed trade optimism after U.S. President Donald Trump said a call is planned very soon with Chinese leader Xi Jinping.

MSCI’s All Country World Index was up 0.2% on the day, although it was set for its third straight losing week, down 2.2%.

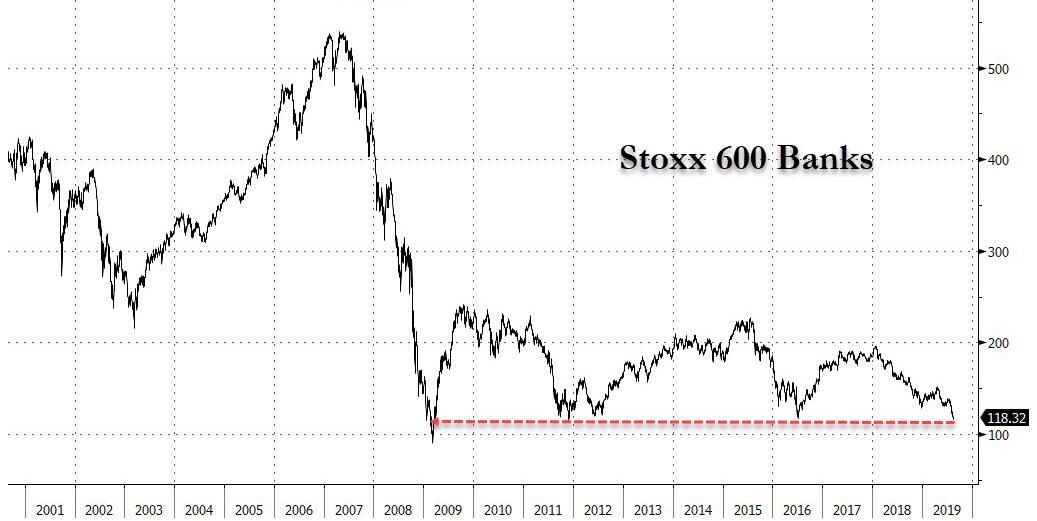

European shares rebounded from six-month lows, with the European Stoxx 600 index over 1% higher, drifting in low-volume trade in a morning devoid of fresh news flow or data. The Stoxx 600 Banks Index was one of Europe’s best-performing sectors today, gaining 1.1%, in contrast with other cyclical industries like autos and chemicals that lagged behind the broader market. Commerzbank was the biggest gainer in the index as the negative yield sentiment took a step back. The catalyst: the 10y Bund yield was slightly up Friday by 1bps as the benchmark’s bond is heading for the fifth weak of falling yields; somehow this was enough to launch a relief rally in Europe’s banks which have tumbled to near record low levels. Italian banks also among the top performers after the country’s market was closed for a holiday Thursday. The banks were also catching up on comments from ECB’s Olli Rehn about a potential “impactful and significant” stimulus package.

A technical glitch delayed the start of trading of the UK’s benchmark FTSE 100 and midcap stock indexes for almost two hours. It was the longest outage at one of the world’s top stock markets in eight years.

Earlier in the session, Asian shares were mostly higher, with Chinese stocks climbing and Korean shares dipping.

Treasuries drifted lower over Asia session and into early European session, paring some Thursday’s rally. Yields were up 0.5bp to 3.2bp across the curve in a bear steepening move with 2s10s wider by ~1bp and 5s30s by ~2bp; 10-year yields ~1.54% are cheaper by 1.5bp but remain towards richer end of 1.473% to 1.733% weekly range. In Europe, Bunds outperformed Treasuries, while gilts underperformed as money markets trim pricing on Bank of England easing; Chancellor Sajid Javid holds Brexit talks in Berlin later Friday.

To be sure, the bulk of the action this week was in the bond market, where with no trade war settlement in sight, investors hedged against a global slowdown by buying bonds. Yields on 30-year debt dropped to a record low 1.916% on Thursday, leaving them down 27 basis points for the week, the sharpest decline since mid-2012.

That means investors are willing to lend the government money for three decades for less than either the overnight rate or Libor. Which also means that all those who pegged their ARM mortgages to the 30Y instead of Libor are now winning.

Some analysts say the current bond market is a different beast than past markets and might not be sending a true recession signal: “The bond market may have got it wrong this time, but we would not dismiss the latest recession signals on grounds of distortions,” said Simon MacAdam, global economist at Capital Economics. “Rather, it is of some comfort for the world economy that unlike all previous U.S. yield curve inversions, the Fed has already begun loosening monetary policy this time.”

And so with the bond market screaming a recession is coming, the futures market is bracing for action from the Fed and the Fed Funds market now sees a one in three chance the Federal Reserve will cut rates by 50 basis points at its September meeting, and see rates reaching just 1% by the end of next year.

On Thursday, the ECB’s Olli Rehn flagged the need for even stronger easing in September. Markets currently anticipate a cut in the ECB’s deposit rate of at least 10 basis points and a resumption of bond buying, sending German 10-year bund yields to a record low of ‑0.71%.

“The underlying concern and drivers such as a recession and the expectation for an aggressive policy response, fueled by Rehn’s comments yesterday, has given the bond market another boost at already elevated levels,” said Commerzbank rates strategist Rainer Guntermann.

Meanwhile, Mexico overnight joined the global easing tide and became the latest country to surprise with a rate cut, the first in five years. Canada – whose yield curve inverted by the most in nearly two decades – is likely next to cut.

In other overnight news, President Trump said Fed Chair Powell should be cutting rates because other countries are lowering rates and we want to remain even. Meanwhile, Fed’s Kashkari (Non-Voter, Dove) said the Fed will debate what to do on rates and that he is leaning towards further rate reduction, while he added that Fed officials are committed to ignoring politics and focusing on jobs. Kashkari also noted that he sees some cautious signs as well as some signs of optimism and that it is definitely a nervous time.

Additionally, Trump said he doesn’t think China will retaliate to an increase in tariffs and understands the September meeting between negotiators is still on, while he added that he has a call scheduled with Chinese President Xi and will be speaking to him soon. Trump also stated that US consumers may have to pay something at some point to cover the cost of tariffs on Chinese goods, that China very much wants to make a deal and he thinks the trade war will be fairly short.

In FX, the talk of ECB easing knocked the euro lower for a fourth day back to a two-week low of $1.1075 and away from a top of $1.1230 early in the week. It was last down 0.3% at $1.1078, helping lift the dollar index to 98.283 and off the week’s low of 97.033. Australia’s dollar rose for a second day as U.S. President Donald Trump said he had a phone call coming soon with China’s Xi Jinping, boosting optimism trade tensions between the two nations will ease. The pound headed for its first weekly gain against the euro for three months, as opposition lawmakers sought to find a way to stop a no-deal Brexit, while Chancellor of the Exchequer Sajid Javid will become the first senior member of Boris Johnson’s government to hold Brexit talks with EU leaders when he flies to Berlin today to speak to German finance minister Olaf Scholz.

In commodities, gold fell 0.7% to $1,512.7, just off a six-year peak. Oil prices surged. Brent crude futures added 2% to $59.48 a barrel, while U.S. crude rose 2% to $55.60 a barrel.

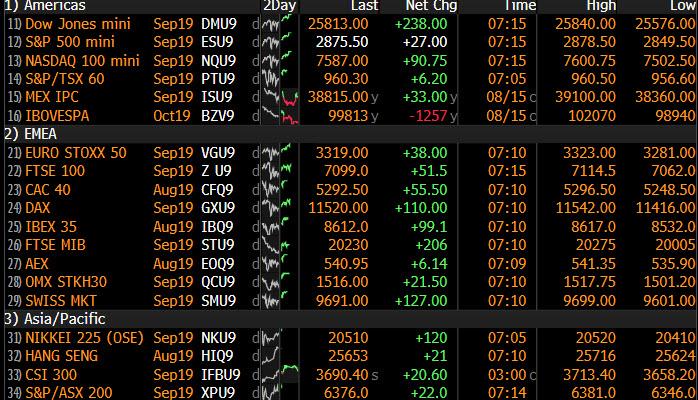

Market Snapshot

S&P 500 futures up 0.9% to 2,872.75

STOXX Europe 600 up 0.8% to 367.96

MXAP up 0.3% to 150.51

MXAPJ up 0.4% to 486.38

Nikkei up 0.06% to 20,418.81

Topix up 0.1% to 1,485.29

Hang Seng Index up 0.9% to 25,734.22

Shanghai Composite up 0.3% to 2,823.82

Sensex up 0.3% to 37,409.18

Australia S&P/ASX 200 down 0.04% to 6,405.53

Kospi down 0.6% to 1,927.17

German 10Y yield rose 0.6 bps to -0.707%

Euro down 0.2% to $1.1086

Italian 10Y yield fell 17.1 bps to 0.985%

Spanish 10Y yield unchanged at 0.034%

Brent futures up 1.5% to $59.09/bbl

Gold spot down 0.7% to $1,512.71

U.S. Dollar Index up 0.1% to 98.26

Top Overnight News

The European Central Bank is throwing every tool it has at the sluggish euro-zone economy. Starting in September, it’ll make a generous funding offer to lenders in the region, returning to an approach it’s used twice before in the past five years. It’s also considering tweaking its interest-rate policy to limit the punitive side effect of its stimulus.

Japanese investors bought a record amount of U.S. agency bonds in June, data from Department of Treasury showed Thursday. Purchases worth $14.3b were the highest in data going back to 1977

Labour Party leader Jeremy Corbyn’s appeal to other U.K. parties that he should become a caretaker prime minister to stop a no- deal Brexit looks to have already fallen flat, as even some in his own party apparently accepted an alternative plan was needed

Japan’s 10-year bond yield slipped to its lowest since July 2016, intensifying scrutiny over the central bank’s yield- curve control policy amid a global debt rally. New Zealand’s benchmark rate also fell to a new record low

The U.S. is gravely disappointed with the U.K. after a Gibraltar court allowed the release of an Iranian tanker suspected of hauling oil to Syria, and threatened sanctions against ports, banks and anyone else who does business with the ship or its crew, two administration officials said

“I’m leaning towards the camp of yes, we need to give more stimulus to the economy, more support, we need to continue the expansion and not allow a recession to hit us,” Minneapolis Fed President Neel Kashkari told Minnesota Public Radio

North Korea fired two unidentified projectiles on Friday into waters off its east coast between the Korean Peninsula and Japan, South Korea’s defense ministry said

Asian equity markets struggled for firm direction following the mixed lead from Wall St where most major indices eventually composed themselves after the recent sell-off but with price action tumultuous on continued US-China trade uncertainty. ASX 200 (Unch.) was subdued as upside in healthcare and financials counterbalanced weakness in commodities and telecoms, with a heavy slate of earnings adding to the mix. Nikkei 225 (Unch.) was restricted by an uneventful currency, while KOSPI (-0.6%) underperformed as it caught up to the recent rout on return from holiday and amid a deterioration in inter-Korean relations after North Korea fired 2 more projectiles and stated it has no intention to talk with South Korea again. Hang Seng (+0.9%) and Shanghai Comp. (+0.3%) were initially choppy amid conflicting rhetoric from both sides of the trade spat. In addition, policymakers later contributed to the outperformance in the mainland after the PBoC’s continued liquidity efforts resulted to a net weekly injection of CNY 300bln and with the NDRC announcing to roll out a plan to boost disposable incomes. Finally, 10yr JGBs initially edged higher to test the 155.00 level to the upside as 10yr yields fell to -0.25% which was the lowest since 2016, although prices then reversed in the aftermath of the BoJ’s Rinban operation in which it reduced purchases of 5yr-10yr bonds for the first time since December as speculated, to stem the decline in yields.

Top Asian News

BOJ Steps in With Cut to Bond Purchases as Yields Keep Sliding

Thailand Plans $10 Billion Economic Boost to Hit 3% Growth

Modi’s Kashmir Move Faces UN Test After Top Court Skips Pleas

European equities are higher across the board [Eurostoxx 50 +1.1%] following on from a mixed Asia-Pac session, with Europe continuing to feel tailwind from ECB’s Rehn, who yesterday hinted to a preference for a bazooka of Central Bank stimulus (in the form of rate cuts and APP) whilst stating its better to overshoot with stimulus than undershoot. UK’s FTSE 100 (+0.4%) fails to benefit from the prospect of EU stimulus and also encountered technical problems which delayed the bourse’s open by just over 90 minutes. Sectors are all in positive territory, whilst some early outperformance was seen in the IT sectors in light of NVIDIA’s (+5.3% pre-market) earnings which beat on both top and bottom lines and supported the likes of fellow chip names [AMS (+3.2%), Infineon (+2.2% and STMicroelectronics (+1.2%)]. Meanwhile, the EU banks saw a sudden sharp decline, although the current yield environment is not attractive, some are citing a technical break below 80 in the Euro Stoxx Bank Index (SX7E). In terms of individual movers, Bayer (+2.3%) rose on the back of an upgrade at BAML, whilst Ryanair (-2.6%) shares were impacted by a double downgrade.

Top European News

In Brave New World, U.K. Markets Don’t See Any BOE Hike, Forever

In FX, Sterling looks set to end the week on top of the G10 table after a run of firmer or better than expected UK data (average earnings, CPI and retail sales) and latest moves to block a no deal Brexit. Cable has reclaimed 1.2100+ status and inched above yesterday’s high (1.2150) even though the Dollar is also generally bid after Thursday’s strong US data/survey releases, while Eur/Gbp has reversed sharply from ytd highs of 0.9325 through Fib support at 0.9160 and 0.9150 amidst all round Euro weakness on the back of dovish ECB rhetoric and perhaps with some fix flow in the mix as well, as the cross probes 0.9125.

EUR – As noted, the single currency remains under pressure following yesterday’s aggressive policy pronouncements from ECB’s Rehn who is advocating conventional easing and substantial bond buying to be unveiled in September on the premise that too much is better than not enough in terms of stimulus. Hence, Eur/Usd is hovering just above the next sub-1.1100 target area or bidding zone between 1.1080-70 and at this stage expiry option interest at the big figure does not seem likely to factor (especially as there is less than 1 bn rolling off).

DXY – The index is inching closer to nearest chart resistance above 98.000 in wake of the aforementioned bullish US macro updates, at 98.301 vs 98.371, with the Greenback also gleaning momentum at the expense of other majors in contrast to EM currencies that are clawing back losses amidst an improved risk environment overall.

JPY/CHF/NZD – All on the back foot, with the Yen unable to breach 106.00 vs the Buck or threaten decent expiries below (1.1 bn from 105.80-70) and subsequently slipping to circa 106.50 as supply at 106.30 dried up, but holding in ahead of support via a Fib at 106.68 for now. Safe-haven unwinding is also weighing on the Franc that is hovering around 0.9800 and even lagging against the independently weak Euro, albeit still above 1.0900 and pivoting 1.0850. Elsewhere, the Kiwi has not derived any comfort from the upturn in risk sentiment after more deep RNBZ rate cut calls overnight (UBS looking for the OCR to hit 0.5% by February next yesr) and a sub-50 NZ manufacturing PMI, with Nzd/Usd closer to the base of 0.6450-25 parameters.

CAD/NOK – A decent rebound in crude prices has helped the Loonie pare some losses relative to its US counterpart within a 1.3325-1.3290 band, while 1.2 bn expiries at 1.3340 are also providing support ahead of 1.3350, and Eur/Nok has reversed from 10.0320 towards 9.9600 with the aid of oil’s recovery and ECB/Norges Bank policy divergence after the latter kept a 25 bp hike on the agenda for this year, albeit not necessarily next month as previously inferred.

EM – Regional currencies have extended their recoveries vs the Dollar as noted earlier, and irrespective of factors that would appear bearish or negative, like an unexpected 25 bp ease from Banxico and much weaker than forecast Turkish IP. However, Usd/Mxn and Usd/Try are both mid-range circa 19.5750 and 5.5500 respectively with the Peso and Lira getting traction from the wider pick-up in risk appetite.

In commodities, a positive session thus far for WTI and Brent futures as the benchmarks recover from yesterday’s losses with upside supported by constructive trade comments from US President Trump, who stated that a call is scheduled with his Chinese counterpart and the September meeting between the negotiators is still on. WTI reclaimed the 55/bbl handle during Asia-Pac hours whilst Brent prices moved north of 59/bbl in early EU trade; and both remain north of these marks. Looking ahead on the docket, OPEC are due to release its delayed Monthly Oil Market report with focus on any revisions to its global oil demand outlook following 2019 downgrades by both the EIA and IEA (to 1.1mln BPD and 1.0mln BPD respectively). Currently OPEC estimates that oil demand will grow by 1.4mln BPD in both 2019 and 2020. On a weekly basis, both benchmarks are poised to post mild gains, albeit this is very much subject to macro-newsflow heading into the final settlement of the week. Elsewhere, gold prices are retreating closer to the 1500/oz level as the Dollar index continues to gain ground above 98.000, whilst profit taking and an unwind in haven positions are contributing to the downside. Meanwhile, copper prices are little changed intraday and remain below the 2.60/lb level as a rise in Chinese refined copper output counterbalances some of the optimism from Trump’s latest China comments. Finally, Dalian iron ore futures are relatively flat as demand woes were neutralised by supply concerns after Brazil’s Vale halted operations at its Viga concentration plant, thus impacting some 330k tonnes of iron ore per month.

US Event Calendar

8:30am: Housing Starts, est. 1.26m, prior 1.25m; Housing Starts MoM, est. 0.24%, prior -0.9%

8:30am: Building Permits, est. 1.27m, prior 1.22m; Building Permits MoM, est. 3.08%, prior -6.1%

10am: U. of Mich. Sentiment, est. 97, prior 98.4; Current Conditions, prior 110.7; Expectations, prior 90.5

DB’s Craig Nicol concludes the overnight wrap

After running to stand still recently, yesterday felt almost like a rare day of calm for risk assets although we still had the usual intraday swings to deal with. Indeed, it wasn’t like there wasn’t much newsflow to digest. We had more trade headlines, strong US data, and ECB stimulus talk. By the end of play, the S&P 500 limped to a +0.25% gain while the DOW and NASDAQ ended +0.39% and -0.09%, respectively. Volumes were still above average and the VIX remained elevated around 21.18; however, it did feel a bit calmer certainly relative to recent days. That being said, Treasuries continued to rally with 2y, 10y and 30y yields ending -7.8bps, -5.1bps and -4.5bps lower, respectively. They did actually weaken a bit into the close as prior to that we saw 10y yields fall below 1.50% intraday. The moves also meant that the 2s10s slope ended slightly steeper at +2.3bps. So we’re still waiting for the first official negative print on a closing basis in this cycle. Cash HY credit spreads finished +3bps and +4bps wider in the US and Europe, respectively. US IG spreads also widened slightly, though they were impacted by the sharp move in GE’s benchmark 2035 bonds, which widened +45bps after reports circulated, accusing the company of “accounting fraud.” The company’s shares fell -11.30% for their worst day since April 2008.

Just on the trade headlines, they focused on China’s state council tariff committee saying that China “has no choice but to take necessary measures to retaliate” and that the US had violated the Xi-Trump consensus with the latest tariff announcement. The statement didn’t suggest what the countermeasures might be; however, Zhou Xiaoming – a former Ministry of Commerce official – suggested that the retaliation may not be limited to tariffs. President Trump also said that an agreement with China has to be on “our terms” while he also indicated that he has a call with Xi “very soon” and that “they would like to do something”.

Overnight most Asian markets are trading higher, with the Nikkei (+0.09%), Shanghai Comp (+0.69%) and the Hang Seng (+0.74%) all advancing. However, the Kospi (-0.70%), which is trading again after yesterday’s Liberation Day bank holiday, has fallen back as news has come through overnight from South Korea that North Korea fired two projectiles, the latest in a series of tests that North Korea has launched in recent weeks. Meanwhile in Japan, 10y JGB yields fell to -0.257% in trading earlier for the first time since 2016, although at time of writing have risen to -0.241%. We’ve also heard overnight that the BoJ reduced their purchases of 5- to 10-year bonds by 30bn yen, the first reduction in their purchases of that maturity since December.

Sticking with Asia, we also heard yesterday that Hong Kong revised down their growth forecasts for this year, down to 0-1%, having been 2-3% previously, while also announcing stimulus measures. This morning, we’ll get Hong Kong’s final Q2 GDP print, which follows the advance estimate last month that showed GDP contracting by -0.3% qoq in Q2, with a yoy growth rate of +0.6%. Looking ahead, S&P 500 futures are currently up +0.58%.

In terms of that US data yesterday that we mentioned at the top, front and centre was the July retail sales report, which was undoubtedly strong with above-market prints for the core (+0.9% mom vs. +0.5% expected) and control group (+1.0% mom vs. +0.4% expected) components. There was a small downward revision to the prior month; however, this was still the fifth straight monthly increase in retail sales, which underscores the solidity of consumer activity at the moment. In addition to that, both the August empire manufacturing (4.8 vs. 2.0 expected) and Philly Fed (16.8 vs. 9.5 expected) surveys surprised to the upside while jobless claims ticked up slightly to 220k but still remain historically low.

The flip side for risk was the upward revision to unit labor costs to +2.4% qoq, which points to some modest upside risk to core CPI over the next year. The other slightly negative print was misses for July industrial production (-0.2% mom vs +0.1% expected), and manufacturing production (-0.4% mom vs. -0.3% expected) albeit slightly offset by upward revisions to the prior. All in all, the general takeaway from the slew of data was that this might make it harder for the Fed to surprise with a more aggressive cut next month (50bps as opposed to 25bps) given the solid consumer data, resilient business sentiment especially in the face of the trade war escalation, and a firming of pricing pressure in the labour market. It’s worth noting that GDP trackers ticked higher yesterday, with the Atlanta Fed estimate now at 2.2% for the third quarter, up +0.3pp from its previous level.

Meanwhile, the ECB stimulus talk concerned comments from policymaker Rehn who said that ECB easing should include an “significant and impactful” stimulus package at its September meeting, in an interview with the WSJ. He went on to say that “when you’re working with financial markets, it’s often better to overshoot than undershoot.” That left the market pricing higher odds of a big QE announcement for the September ECB meeting. Bonds rallied across the continent, with 10y yields in Germany, France, and Italy dropping -6.2bps, -6.6bps, and -17.6bps. The euro weakened as much as -0.42% in response and ultimately closed -0.29% lower versus the dollar, though the pass-through to equities was not overly strong, as the STOXX 600 still closed -0.29% lower.

Across the pond, Fedspeak didn’t really move markets, though we did get confirmation that Chair Powell will speak at 3pm London time next Friday to kick off the Jackson Hole conference. The text of his speech will likely be released at the same time. There were also unsubstantiated reports that Powell is cracking down on Fed staff communicating with market participants and/or the media, though it’s hard to believe that they would change their communications policy without publicizing it. Separately, St. Louis Fed President Bullard spoke and sounded, at the margin, dovish. He said that the market’s inflation expectations were “not high enough to meet our target so that is something I will definitely take into account if it is sustained going forward”. Minneapolis Fed President Kashkari also said yesterday that “I’m leaning towards the camp of yes, we need to give more stimulus to the economy”.

In other news, the only other data worth flagging yesterday was in the UK where the July retail sales data was by and large surprisingly positive, with the core measure rising +0.2% mom versus expectations for a -0.2% mom decline. That took the year-on-year reading to +2.9% versus the expected +2.3%. As for other central banks, the global march toward more accommodation continued as the Norges Bank gave a surprisingly dovish statement, sending the krone -0.39% weaker versus the dollar. Mexico’s central bank also surprisingly cut interest rates by 25bps.

Finally to the day ahead, which is quiet for data this morning with only the June trade balance for the Euro Area due. Over in the US this afternoon, we’ll get July housing starts and building permits data before the preliminary University of Michigan consumer sentiment survey is released. It’s worth keeping an eye on the household inflation expectations component of this survey, which remains low despite a pickup last month and has been flagged as a concern by Fed officials. The only other release worth flagging is OPEC’s monthly oil market report.

via ZeroHedge News https://ift.tt/2KDh5OX Tyler Durden

“Summer Breeze makes me feel fine… blowing thru the jasmine on my mind..!

Run for the hills..? Nope.

How much more horrible does this need to get: Chinese Police Troops poised on the Hong Kong Border? Bond Yields inverted and tumbling lower? Germany sliding into recession? China hiding internal pain? Global Equity threatening to puke completely? Italy government about to fall? Brexit? Trade wars deepening? Political gridlock? Geopolitical uncertainty? A new banking crisis? The outlook looks horrible… but Relax. Just Do It! The sun will likely come up tomorrow. And don’t forget we are right in the Ides of August: the thinnest, most illiquid time of the year. Crashes usually happen in October!

We’ve also got a growing awareness from global regulators, central bankers, and politicians of just how badly flawed policy responses and their unintended consequences have been since 2008. None of them want to jeopardize their electoral chances or future careers. If crisis crunches into crash there is the reality of a rescue bailout to factor in. (How is the question – central banks are out of options on rates, so I guess they just buy everything and end the logic of free markets for ever…)

Plus, it’s a simple fact there is loads and loads of ready cash sitting waiting for the opportunity to invest on a market reset. When the whole street is waiting for a correction as the moment to buy… It doesn’t happen till you don’t expect it.

Let’s not be overly optimistic. There are clearly troubles ahead, but I suspect they are likely to be tactical in the short-run. The risk is a couple of tactical shocks could precipitate a strategic collapse. Let me explain – all it might take is a couple of key stock shocks to really crush market sentiment, and spin us into a situation where the “authorities” have to respond to crisis.

Let me give you the four stocks I think you should be watching for signs we’ve in the deep solids…

First up is HSBC. If Hong Kong kicks off, there has to be a massive sell off in the bank. It gets 90% of its profits from Hong Kong – which is already massively destabilised as a result of the tensions and protests. Money and skills are exiting the territory and heading towards Singapore. HSBC is already on the China sh*t-list over Huawai. If you think the Chinese will enable a foreign bank and signal of imperialism to flower in a New Hong Kong, then please can I have a quarter of whatever you are smoking. (And HSBC makes my blood boil: Yesterday I tried to pay money to my daughter’s new account in Oz. I gave the details to HSBC over the phone, but they refused to make any payments unless I answered a host of deeply personal questions about why – they knew it was daughter! I understand why, but they were so bloody rude and arrogant about it – treating me like a child. I gave up. I am also writing to the FCA to make formal complaint: they screwed up 3 credit card repayments in a row, and then promised to respond to my initial complaint within 8 weeks. They offered me a meeting in a Southampton branch to discuss. I said no – let’s meet in London when I live and work during the week. They considered that sufficient grounds to close the case. They are definitionally useless.)

Second stock to watch is GE – in the press yesterday because the guy that exposed Madoff says they are guilty of a $38 bln fraud in their insurance and Baker Hughes business. Ouch. Late last year I warned GE had a very limited time to fix itself – See “Is GE Going to Repay its Debt”. Now GE may be working round its problems, but another wobble and the kind of 15% stock crash we saw last night makes that path even more perilous. Bad news sticks.

Third is Boeing. I’ve written about its problems so many times – back in July warning that as the biggest component stock on the Dow, Boeing could be the name to trigger collapse. There is no idea when it gets the B 737 Max programme back in the air or if anyone will now fly it. The company is still in denial, and the likelihood of massive legal action as the scale of their regulatory capture of the FAA becomes apparent is growing. The sheer greed of their top management and how they pushed back safety in pursuit of bonueses and their pay packages could yet crush the company and force a policy response from US government that could totally change their position selling planes abroad.

And, then there is We-Work’s IPO. You really could not make it up how one sided the terms of the IPO are and what it actually says about the company’s “mission”, values and its boss – Adam Neumann. To buy this stock you would need to be insane. If it’s not the absolute top of the crazy tech IPO market, then the world needs a reset. To read the details try this from the Register: Authentic Tech Company Vibes, right down to billion in losses and admission it may never be profitable. And the thing is – its not a Tech company at all. It’s a rather poorly managed property play run by a snake oil salesman who’d bluffed some stupid money. Here’s what I said about We-Work back in January.

I am sure there are a host of other equity and bond stories that could provide the sparks that light a market conflaguration in coming weeks. Or maybe we will get lucky and the fires keep get put out before they take hold. We only need to be unlucky a few times….

Bottom line – I suspect we are at something of a wake-up and smell the coffee moment. It’s going to be painful and massive pressure on top level level stocks will trigger all kinds of post-shock consequences. It will likely trigger a regulatory reaction and a buying opportunity. I suppose the only strategy is stay awake and be a boy-scout: be prepared..

Meanwhile, back in Camelot… Blain’s Brexit Watch

When I get round to writing the definitive comedy about Brexit I am going to ask Jeremy Corbyn to play himself. He’s brilliant. An unchallenged masterof pathos, gormlessness, and a capacity for self-delusion that would be unbeatable if parliament didn’t already contain Hammond and the Liberals. However, his offer to lead the country might not be so stupid – he’s not saving No-Brexit. He’s strectching out the pain, promising Brexit Tomorrow, if you still want it. Bottom line on Brexit. Going to hurt. UK will feel pain, and recover. Not so sure about Europe.

via ZeroHedge News https://ift.tt/2N9ZWOq Tyler Durden

Alibaba Executive Chairman Joe Tsai is reportedly planning to pay $3.5 billion to buy out Mikhail Prokhorov’s stake in the Brooklyn Nets and the Barclays Center, swapping ownership of the NYC franchise just after it acquired two superstar players who have greatly improved the team’s prospects for the upcoming season.

According to Bloomberg, the deal to buy the sports franchise could be announced as soon as Friday. Taiwan-born Tsai is a Yale Law Graduate, and was corporate tax lawyer at venerated white-shoe firm Sullivan & Cromwell when Jack Ma persuaded Tsai to leave and become one of the 8 founding members of Alibaba. He’s know worth some $10 billion.

Joe Tsai

Tsai bought a 49% stake in the team at a $2.3 billion valuation a few years ago – a record for a US pro sports franchise – and he had until 2021 to exercise the option to take control of the club. And after the events of this off-season (acquiring Kyrie Irving and Kevin Durant), which have left the club in a much better position to make the playoffs or possibly become a championship contender, the timing for buying out the team was just right.

That isn’t to say Prokhorov is getting shorted – quite the opposite.

Prokhorov’s Onexim Sports & Entertainment paid $223 million in 2010 for an 80% stake in the team and a 45% stake in the arena. In 2015, Prokhorov bought out the team and the arena (the league prefers it when one owner controls both) in a deal valuing the assets at a combined $1.7 billion.

The oligarch made his money in minerals, but bought the team in 2009 after losing favor with Putin. At the time, he paid less than $400 million for the struggling New Jersey Nets and a piece of the stadium.

He then proceeded to be a terrible NBA owner in every way except the one that counts: making a massive profit when you sell the team. The sale qualifies as the richest in NBC history, according to SB Nation.

Asians have been buying up professional sports teams in Europe and around the world, but buying an NBA team is rare.

Indonesian Erick Thohir, chairman of the Mahaka Group, once owned a stake in the Philadelphia 76’ers, but he has since sold it.

Chinese investors typically prefer European soccer teams, including Aston Villa, West Bromwich Albion, Wolverhampton Wanderers and Southampton in England, Italy’s A.C. Milan and Inter Milan, Spain’s Atletico Madrid, and Slavia Prague in the Czech Republic, according to Bloomberg.

But if the Nets have a breakout season, outshine the Knicks and maybe even make it deep in the playoffs, Tsai’s reign would be off to a great start.

via ZeroHedge News https://ift.tt/2TBLO1A Tyler Durden

Rupert Hogg, the CEO of Hong Kong-based airline Cathay Pacific has reportedly resigned on Friday, and though no official reason has been given, many suspect it was due to his slow-to-respond and at times seemingly sympathetic treatment of the protest movement, according to BBG.

A report about the Cathay board accepting Hogg’s resignation appeared on China state TV. No sources were given, but the story was later confirmed by Hong Kong Exchanges and Clearing.

What’s more, SCMP reports Paul Loo, Cathay’s chief customer and commercial officer and a known Hogg deputy, has also stepped down, in what’s beginning to look like a purge.

Both men resigned to “take responsibility as a leader of the company in view of recent events,” the company said in a statement.

“The Board of Directors believes that it is the right time for new leadership to take Cathay Pacific forward,” the airline said in a statement.

Augustus Tang Kin-wing, 60, the CEO of maintenance and engineering company Haeco, was appointed interim CEO of the airline. Haeco is owned by Cathay Pacific’s parent company, Swire Pacific.

Newly appointed HK Express CEO Ronald Lam Siu-por will take Loo’s place as the new chief customer and commercial officer. Cathay Pacific said it would eventually find a new CEO.

The airline said Tang and Lam were “highly experienced executives with long careers at Cathay Pacific” and were “ideally suited to lead the company”.

Cathay was criticized by the mainland government for being to slow to punish employees who chose to participate in the protests, a sign of disloyalty that the Party was not willing to let go. Two employees, and two pilots were fired last week as pressure came to a head, but state-owned companies had started a boycott of Cathay and voiced their displeasure in other ways, making leadership change unavoidable.

via ZeroHedge News https://ift.tt/2z1QSTt Tyler Durden

Inflation? Deflation? Stagflation? Consecutively? Concurrently?… or from a great height (apologies to Tom Stoppard).

We’ve reached a pivotal moment where all of the narratives of what is actually happening have come together. And it feels confusing. But it really isn’t.

The central banks have run out of room to battle deflation. QE, ZIRP, NIRP, OMT, TARGET2, QT, ZOMG, BBQSauce! It all amounts to the same thing.

How can we stuff fake money onto more fake balance sheets to maintain the illusion of price stability?

The consequences of this coordinated policy to save the banking system from itself has resulted in massive populist uprisings around the world thanks to a hollowing out of the middle class to pay for it all.

The central banks’ only move here is to inflate to the high heavens, because the civil unrest from a massive deflation would sweep them from power quicker.

For all of their faults leaders like Donald Trump, Matteo Salvini and even Boris Johnson understand that to regain the confidence of the people they will have to wrest control of their governments from the central banks and the technocratic institutions that back them.

That fear will keep the central banks from deflating the global money supply because politicians like Trump and Salvini understand that their central banks are enemies of the people. As populists this would feed their domestic reform agendas.

So, the central banks will do what they’ve always done — protect the banks and that means inflation, bailouts and the rest.

At the same time the powers that be, whom I like to call The Davos Crowd, are dead set on completing their journey to the Dark Side and create their transnational superstructure of treaties and corporate informational hegemony which they ironically call The Open Society.

This means continuing to use whatever powers are at their disposal to marginalize, silence and outright kill anyone who gets in their way, c.f. Jeffrey Epstein.

But all of this is a consequence of the faulty foundation of the global financial system built on fraud, Ponzi schemes and debt leverage… but I repeat myself.

And once the Ponzi scheme reaches its terminal state, once there are no more containers to stuff more fake money into the virtual mattresses nominally known as banks, confidence in the entire system collapses.

It’s staring us in the face every day. The markets keep telling us this. Oil can’t rally on war threats. Equity markets tread water violently as currencies break down technically. Gold is in a bull market. Billions flow through Bitcoin to avoid insane capital controls.

Any existential threat to the current order is to be squashed. It’s reflexive behavior at this point. But, as the Epstein murder spotlights so brilliantly, this reflexive behavior is now a Hobson’s Choice.

They either kill Epstein or he cuts a deal or stands trial and hundreds of very powerful people are exposed along with the honeypot programs that are the source of so much of the bad policy we all live with every day.

These operations are the lifeblood of the power structure, without it glitches in the Matrix occur. People get elected to power who can’t be easily controlled.

The central banks are faced with the same problem. To deflate is worse than inflating therefore there is no real choice. So, inflation it is. Inflation extends their control another day, another week.

Whenever I analyze situations like this I think of a man falling out of a building. In that state he will do anything to find a solution to his problem, grasp onto any hope and use that as a means to prolong his life and avoid hitting the ground for as long as possible.

Desperate people do desperate and stupid things. So as the mother of all Battles of the ‘Flations unfolds over the next two years, remember it’s not your job to take sides because they will take you with them.

This is not a battle you win, but rather survive. Like Godzilla and Mothra destroying the city. If Epstein’s murder tells you anything, there’s a war going on for control of what’s left of the crumbling power structure.

And since inflation is the only choice that choice will undermine what little faith there is in the current crop of institutions we’ve charged with maintaining societal order.

As those crumble that feeds the inflation to be unleashed.

For the smart investor, the best choice is not to play. Wealth preservation is the key to survival. That means holding assets whose value may fluctuate but which cannot be taken from you during a crisis.

It means having productive assets and being efficient with your time.

It means minimizing your counter-party risk. Getting out of debt. Buying gold and cryptos on program or on pullbacks. Most importantly, it means keeping your skills up to date and your value to your employer(s) high.

And if you’re really smart, diversifying your income streams to keep your options open.

Deflation and inflation are two sides of the same coin (or the same side of two coins). Both are just as destructive.

* * *

Join my Patreon is you want help offsetting inflation risks. Install Brave if you want to ensure you’ll still be allowed to talk such heresy.

via ZeroHedge News https://ift.tt/2OVh1Oy Tyler Durden

The United Kingdom’s Ministry of Social Justice ad regulator has stricken two advertisements from the approved list for following longstanding gender stereotypes.

On Wednesday, the Advertising Standards Authority (ASA) announced that they “drew the line” over ads by Volkswagen and cream cheese maker Philadelphia for perpetuating the offensive stereotypes, according to DW.com.

In Volkswagen’s case, their ad featured men participating in adventurous activities, while women sat on a beach next to a baby buggy. According to the ASA, “images of men in extraordinary environments and carrying out adventurous activities” vs. “women who appeared passive” were stereotypical and not nice.

Volkswagen pushed back against the judgement, arguing that their advertisement featured men and women “taking part in challenging situations.”

The Philadelphia cream cheese advert, meanwhile, featured two men easily distracted by the snack while forgetting about their babies, which the ASA said “implied that the fathers had failed to look after the children properly because of their gender,” and “relied on the stereotype that men were unable to care for children as well as women.”

Philadelphia’s parent company, Mondelez UK, said that they are “extremely disappointed with the ruling.”

UK authorities introduced the new rules in June, after pressure from campaigners focusing on sexism. The new rules focused on banning “gender stereotypes which are likely to cause harm or serious or widespread offense.”

A spokeswoman for the women’s rights group the Fawcett Society, Ella Smillie, told the Reuters news agency advertisers need to “wake up and stop reinforcing lazy, outmoded gender stereotypes.”

“We know that children internalize [gender stereotypes] in a way that limits their aspirations and potential in life,” she added.

A study by data and consultancy firm Kantar showed less than one in ten adverts have an authoritative female in it, despite research which shows consumers respond better to women than men in adverts. –DW.com

While the ASA cannot fine Volkswagen and Philadelphia, the advertisements won’t be able to taint impressionable UK minds anymore.

via ZeroHedge News https://ift.tt/2Zbkjgl Tyler Durden

The Mexican government is reportedly considering banning cash purchases of gasoline and the use of cash to pay highway tolls. The goal is to reduce tax evasion and money laundering and to identify stations that are selling stolen gas. Cash is used for 80 to 90 percent of purchases in the country.

from Latest – Reason.com https://ift.tt/2KS6ApB

via IFTTT

The Mexican government is reportedly considering banning cash purchases of gasoline and the use of cash to pay highway tolls. The goal is to reduce tax evasion and money laundering and to identify stations that are selling stolen gas. Cash is used for 80 to 90 percent of purchases in the country.

from Latest – Reason.com https://ift.tt/2KS6ApB

via IFTTT

Muslim taxi drivers in Austria are refusing to transport blind people with guide dogs because dogs are seen as being unclean in Islamic culture.

Tiroler Tageszeitung reports on how a former board member of the Association for the Blind, who is totally blind herself, ordered a taxi to drop her off at Innsbruck airport.

However, when the taxi arrived, the driver refused to take her dog.

Taxi operators Anton Eberl and Harald Flecker apologized for the incident but stressed that they only mediate calls and do not own the taxis.

“We try to make it clear to the drivers again and again that this is not the case for us and that these trips have to be carried out exactly like any other job. Unfortunately, at the moment we are not in a position to solve this problem satisfactorily, ” said Flecker,

…adding that drivers had to be told “again and again” about the rules.

According to the Tiroler Tageszeitung newspaper, “80 percent of drivers now have a migrant background – and Muslims traditionally often regard dogs as “impure”.

Gabriele Jandrasits also tried to order a taxi to transport her and her Beagle-Jack Russell dog to the airport. Despite the fact that the dog was contained inside a transport cage, she was told that “most drivers would refuse to take dogs for reasons of faith.”

Local laws state the drivers must accept guide dogs for the blind, although many of them simply seem to be ignoring this mandate.

Meanwhile, diversity continues to be a strength.

* * *

There is a war on free speech. Without your support, my voice will be silenced. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

via ZeroHedge News https://ift.tt/33BbuA6 Tyler Durden