We live in a world where a Boeing executive was forced to resign over a 33-year-old article opposing the idea of women in combat and a respected art curator was pushed out of the San Francisco Museum of Modern Art for saying he would “definitely still continue to collect white artists.” The editor of The New York Times opinion page left his job after publishing an article by Sen. Tom Cotton (R–Ark.) and TV host Nick Cannon was fired by ViacomCBS after voicing anti-Semitic comments on his podcast.

What is driving such instances of what many call “cancel culture”? To answer that question, Nick Gillespie turned to Jonathan Rauch—a fellow at the Brookings Institution, a contributing writer to The Atlantic, and a signatory to the recent open letter in Harper’s warning that “the free exchange of information and ideas, the lifeblood of a liberal society, is daily becoming more constricted.”

In 1993, Rauch wrote Kindly Inquisitors: The New Attacks on Free Thought, an influential defense of free speech and open inquiry that was excerpted in Reason. Is free thought under unprecedented attack? And if it is, what’s driving the repression? Rauch, who is currently working on a book tentatively titled The Constitution of Knowledge, answers those questions and discusses the best way to engage censors and cancelers.

Audio production by Ian Keyser.

from Latest – Reason.com https://ift.tt/30FypcT

via IFTTT

Via College Fix, the Rutgers English Department purports to challenge “the familiar dogma that writing instruction should limit emphasis on grammar/sentence-level issues so as to not put students from multilingual, non-standard ‘academic’ English backgrounds at a disadvantage.” So far so good. Helping students who struggle with standard English is exactly what an English Department that wants to helps disadvantaged students should do.

Instead, though, Rutgers goes even woker. Rather than merely deemphasizing standard grammar, the English Department declares that standard grammar is “biased,” and endorses “critical grammar,” which “encourages students to develop a critical awareness of the variety of choices available to them w/ regard to micro-level issues in order to empower them and equip them to push against biases based on ‘written’ accents.”

In short, the Rutgers English Department wants to make sure that students who come to Rutgers with a poor grasp of standard written English not only remain in that state, but come to believe that learning standard English is a concession to racism. I remember when keeping “people of color” ignorant was considered part of white supremacy.

from Latest – Reason.com https://ift.tt/2WJm5Hu

via IFTTT

Via College Fix, the Rutgers English Department purports to challenge “the familiar dogma that writing instruction should limit emphasis on grammar/sentence-level issues so as to not put students from multilingual, non-standard ‘academic’ English backgrounds at a disadvantage.” So far so good. Helping students who struggle with standard English is exactly what an English Department that wants to helps disadvantaged students should do.

Instead, though, Rutgers goes even woker. Rather than merely deemphasizing standard grammar, the English Department declares that standard grammar is “biased,” and endorses “critical grammar,” which “encourages students to develop a critical awareness of the variety of choices available to them w/ regard to micro-level issues in order to empower them and equip them to push against biases based on ‘written’ accents.”

In short, the Rutgers English Department wants to make sure that students who come to Rutgers with a poor grasp of standard written English not only remain in that state, but come to believe that learning standard English is a concession to racism. I remember when keeping “people of color” ignorant was considered part of white supremacy.

from Latest – Reason.com https://ift.tt/2WJm5Hu

via IFTTT

“Conventional Logic” No Longer Exists: What That Means For The Treasury Market Tyler Durden

Wed, 07/22/2020 – 14:25

By Ian Lyngen and Jon Hill of BMO Capital Markets

Two of the mainstays of investor anxiety are once again setting the tone in financial markets;

fears the pandemic is worsening and

devolving China/US relations.

The first has been highlighted by not only the recent surge in Covid-19 cases, but also a fresh round of concern that the autumn (and typical flu season) will represent an especially challenging period for the battle with the coronavirus. These worries have been combined with the reinstatement of lockdowns/closures and thereby undermined any lingering recovery optimism. Although to be fair, the extent of positive sentiment related to the bounce back of the global economy was already in short supply as the summer unfolds and a second fiscal stimulus deal from Washington begins to take on a more elusive quality than previously assumed. This isn’t to suggest the odds for a deal are low, rather that the scope and magnitude of the second round of stimulus appears poised to disappoint.

The State Department’s order to close China’s consulate in Houston “to protect American intellectual property and Americans’ private information” represents another step in the ongoing tension between Beijing and Washington. The Chinese Foreign Ministry spokesman characterized the move as an “unprecedented escalation” and investors are now awaiting details on any potential retaliation. It’s an all too familiar dynamic and one which the market has been relatively sanguine about, all things considered. While equity futures are off the highs, the -0.4% move is only a fraction of the reaction such a development would have triggered in January. This is, in part, due to the more significant economic ramifications from the pandemic, but it also reflects investors’ perception that a shift in the White House will make it easier for both sides to discount any escalation seen during the second half of 2020.

The Presidential election is quickly approaching on the horizon and as the nuances of Biden’s policy agenda come into focus we’ll be eager to see how resilient the bid for domestic equities remains. Conventional logic suggests if the White House is controlled by a Democrat, less pro-business policies will weigh on risk asset valuations; an influence which would only be exaggerated in the event of a blue sweep which similarly achieves control of Congress. If we’ve learned anything from 2020 (aside from the importance of washing our hands), it’s that “conventional logic” hasn’t been in the driver’s seat for a very long time.

In fact, it’s well within the set of potential outcomes that a blue sweep implies a welcome return to establishment politics which clears the way for US equities to rally into the end of the year; even if the kneejerk would be risk off. While this might initially sound somewhat counter-intuitive, the process of moving beyond the divisive political environment of the last several years could resolve into a net positive for the business community; particularly if combined with continued progress through the depths of the pandemic.

That said, the needed level of clarity on the political front will not be on offer in the Treasury market at this stage and instead, we’ll continue to trade off the incremental influences from risk assets as earnings season progresses. 10s have extended the stealth rally with yields dropping as low as 58.4 bp overnight. For context, since April 30 10-year rates have only been this low on one other occasion; July 10 – when 56.8 bp redefined the lower-bound. We’re focused on two sell levels; 56.8 bp and 53.9 bp (low from April 21). Our baseline expectation is that both levels will be sold on the first attempt and if yields manage to close above the floor, a second attempt isn’t a foregone conclusion. In the event of a shift in the macro narrative, a more durable bid could easily push through the bottom of the range and put a <50 bp 10-year yield on the table as the summer drags on.

In keeping with our range-trading thesis for Q3, we’re anticipating selling interest as rates creep lower and the fundamentals remain comparatively steady. The omnipresent uncertainties created by the pandemic will limit any significant selloff back toward 75 bp in 10s; even if low volumes and diminished risk-taking capacity clear the path for sharp price action.

via ZeroHedge News https://ift.tt/3eQKGA8 Tyler Durden

Facebook’s Neutral “Fact Checkers” Exposed As Ex-CNN Staffers And Democratic Donors Tyler Durden

Wed, 07/22/2020 – 14:05

Today in news about the radical left-wing censorship machines our social media companies have become, it was exposed this week that Facebook’s fact-checker, Lead Stories, is an outfit that is stocked to the brim with ex-CNN staffers.

The organization presents itself as neutral yet “most of its employees” have donated to the Democratic party, according to RT.

The National Pulse reached out to Facebook’s fact checkers this week after a story they published about Black Lives Matter was flagged as “partly false” by the platform. This led TNP to “do some digging” on who was behind the smear.

What they found was stunning: an organization “staffed almost entirely by Democratic donors, half of whom had worked for CNN in the past.”

THREAD #1:

So Facebook just put a “Partly False” flag on one of our @TheNatPulse exclusives. Except… it’s not false at all.

I called Alan Duke, the editor at the LeadStories website (I’ve never heard of it?) which apparently conducts fact checks for Facebook. pic.twitter.com/AwVFd1EO6Z

25% of the organization’s employees were recurring Democratic donors and Lead Stories’ founder, Perry Sanders, has donated over $10,000 to Democratic political campaigns – including Hillary Clinton and Barack Obama’s Presidential runs.

TNP also exposed that “several other writers” had Democratic contributions on their records. For example, one writer named Gita Smith, was listed in “99 separate small-dollar donations” to various Democratic candidates – in addition to contributions to ActBlue.

The org’s editor, Alan Duke, spent nearly three decades with CNN as a reporter and editor and the org’s senior editor, Monte Plott, spent over 10 years with CNN. Five other names at the organization were also found to have worked at CNN as some point.

Writer Jessica Ravitz spent 10 years with CNN and also spent “nearly four years with the Anti-Defamation League, a self-styled anti-‘hate’ watchdog that spends most of its considerable resources demonizing political voices that deviate from the neoliberal centrist mainstream-media line.”

TNP’s investigation followed Lead Stories taking exception with their article titled: “Black Lives Matter Website, ‘Defund the Police’ Donations Go to ‘Act Blue’, the ‘Biden for President’ Campaign’s Top Source of Donations”.

Facebook posted the story in the “Hoax Alert” section of its website as a result of Lead Stories’ flagging. The fact checked pointed out that “BLM’s donations go through, not to ActBlue, which is a payment processor for Democratic campaigns and not the ultimate source of the Biden campaign’s cash.”

TNP corrected the word “to” to “through” but claimed Lead Stories still would not lift the “partly false” flag on its story.

And so it appears to us what we have yet again is a social media platform clearly acting as a publisher yet not having to incur the legal liabilities that come with it. This slippery slope is going to continue – and only get worse, we predict – until at some point it gets even more blindingly obvious than it is now that these Silicon Valley firms are using their power to nudge the country toward the political ideologies they support, rather than providing unbiased “fact-checked” outlets for public discussion.

via ZeroHedge News https://ift.tt/32IEY0L Tyler Durden

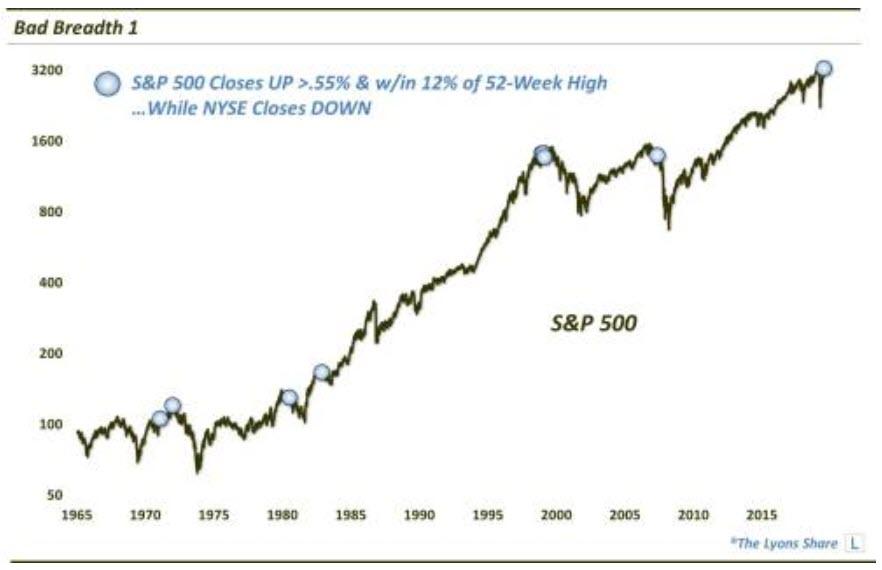

Monday’s market breadth was historically poor given the performance in the major averages.

Like a breath mint for halitosis, sometimes the performance in the popular, cap-weighted stock averages can mask underlying weakness in the overall market breadth (i.e., advancing vs. declining stocks). As such, market conditions may not be quite as robust as the indices would suggest. Monday’s action was a good example of that as market breadth was historically poor given the performance of the large-cap indices. To wit:

On Monday, the cap-weighted large-cap S&P 500 (SPX) gained 0.84%. Despite that solid gain, the broad NYSE Composite actually closed slightly down on the day as there were more declining issues than advancers on the exchange. In the 55 years of data in our database, that is just the 4th time – and the first in 40 years – that the SPX has gained that much on a day that the NYSE was down.

Relaxing the parameters a bit, we dove a little deeper into the data and identified all days during that period that saw the SPX gain at least 0.55%, while within 12% of a 52-week high, when the NYSE closed down on the day. This chart shows all 9 such days in the past 55 years.

As you can see, several of the previous incidents occurred at quite inauspicious times in the market – including near cyclical peaks in 1973, 1980, 2000 and 2008. History does not have to repeat, but these are not exactly optimistic precedents.

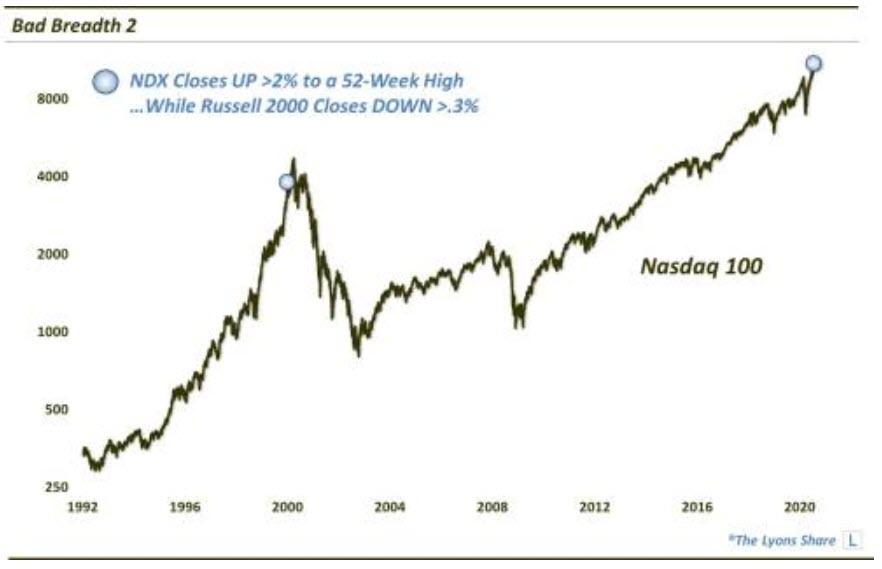

Another example of the disparity between the performance of the popular large-cap averages and those broader indices on Monday can be seen in a comparison between the large-cap Nasdaq 100 (NDX) and the Russell 2000 (RUT) small-cap index. Specifically, the NDX closed up nearly 3% on Monday to a new all-time high. On the flip side, the RUT actually closed down on the day by 0.36%. The only other date in our 30 years of data on the 2 indices that saw this combination of behavior was the 1st day of the millennium (also not a great time to be buying stocks).

So, what is the takeaway here? Is the stock market doomed? Well, we wouldn’t put a ton of stock into a 1-day phenomenon, despite the ominous precedents. There are certainly more important factors that go into our investment decision-making process, namely our objective, quantitative models. However, this is another among a growing collection of red flags – and it will definitely garner more attention from us should this pattern of “bad breadth” continue.

* * *

How much “stock” are we putting into this data point? How is it impacting out investment posture? If you’re interested in an “all-access” pass to all of our charts, research — and investment moves — please check out our site, The Lyons Share. You can follow our investment process and posture every day — including insights into what we’re looking to buy and sell and when. Thanks for reading!

via ZeroHedge News https://ift.tt/2WLoyRr Tyler Durden

Senate GOP Weighs Short-Term Extension For Unemployment Aid While Lawmakers Fight Over Stimulus Tyler Durden

Wed, 07/22/2020 – 13:25

With a $2.5 trillion gulf between Republican and Democratic stimulus packages – and ongoing negotiations between the White House and Senate GOP over issues such as a payroll tax cut favored by President Trump, chances of a successful negotiation happening anytime soon are fleeting at best – and will most likely continue beyond when the $600 weekly unemployment carved out under the Cares Act is set to lapse at the end of the month.

Mitch McConnell speaks at the U.S. Capitol. Photographer: Stefani Reynolds/Bloomberg

Notably, the Republicans are aiming for a $1 trillion stimulus package, while Democrats have a $3.5 trillion price tag on theirs.

In order to address what will undoubtedly be a protracted negotiation, lawmakers are considering a side-deal which would extend the unemployment bonus, according to Bloomberg.

While Republicans have criticized the $2,400 per month stipend as a disincentive to seek work, the plan to extend the benefits has drawn the support of GOP Senators, including Marco Rubio (R-FL), who acknowledged that lawmakers are considering the plan. That said, the size and scope of any extension is currently unknown.

Both parties also support extending supplemental unemployment benefits. Some Republicans have floated the idea of structuring it so that unemployment insurance replaces 70% to 75% of previous wages rather than the flat $600 per week boost to state benefits in the last stimulus. But others, including Finance Committee Chairman Chuck Grassley of Iowa, have insisted that the solution has to be simple enough for the states to easily implement. –Bloomberg Tax

Not in favor of the extension is House Majority Leader Steny Hoyer (D-MD), who said “I would prefer not to see a short-term extension,” adding that he wants “to give people the security they are not going to be let down and fall through the cracks in September and October.”

Meanwhile, the White House has softened its tone regarding amandatory payroll tax holiday, though on Tuesday Press Secretary Kayleigh McEnany said that President Trump is still in favor of the measures.

Chief of Staff Mark Meadows echoed this sentiment, saying in a Tuesday statement on Capitol Hill: “I don’t know that in any negotiation that there are red lines, but there are certainly high priorities and it will remain a very high priority for the president.“

Meadows and Treasury Secretary Steven Mnuchin are returning to the Capitol Wednesday after an initial round of talks with Senate Republicans ended without a clear outline or any lessening of GOP resistance to President Donald Trump’s desire for a payroll tax holiday. –Bloomberg

Also on Tuesday, Senate Majority Leader Mitch McConnell (R-KY) outlined some of his own priorities – namely extending the PPP loan program for small businesses, as well as another round of direct payments to individuals.

via ZeroHedge News https://ift.tt/2CXapcW Tyler Durden

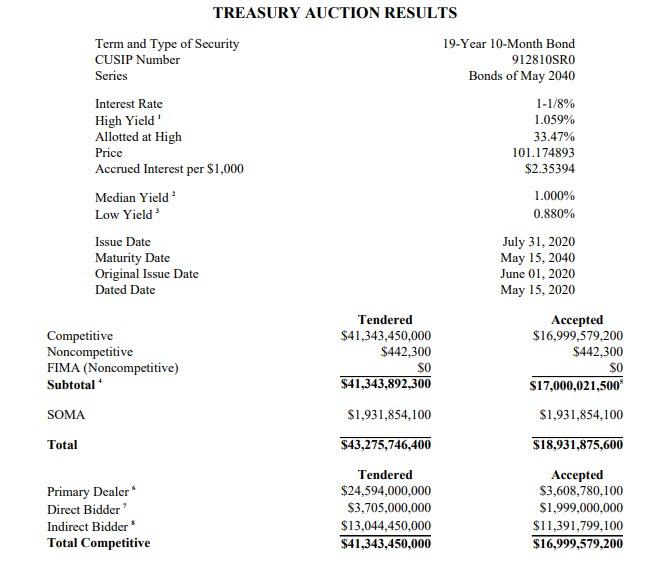

20Y Treasury Prices At Record Low Yield Amid Relentless Demand For Duration Tyler Durden

Wed, 07/22/2020 – 13:14

Two months after the first 20Y auction in 34 years priced at a yield of 1.22% amid surprisingly strong demand, moments ago the Treasury sold its third batch of the recently restarted 20Y Treasury in the form of a $17 billion reopening (19-years-10-months) of the original Cusip (SR0), which priced at a high yield of 1.059%, far below last month’s 1.314%, yet tailing modestly to the 1.050% When Issued.

The auction metrics are as follows:

Bid to Cover: 2.43x compared to 2.63x last month and below the 2.53x in the inaugural, May auction.

Indirects: 67.0%, well above both June’s 61.6% and May’s 60.7%

Directs: 11.8%, a bit drop from the 16.5% in June, and also below May’s 14.7%

Dealers: 21.2%, almost unchanged from last month’s 21.9%.

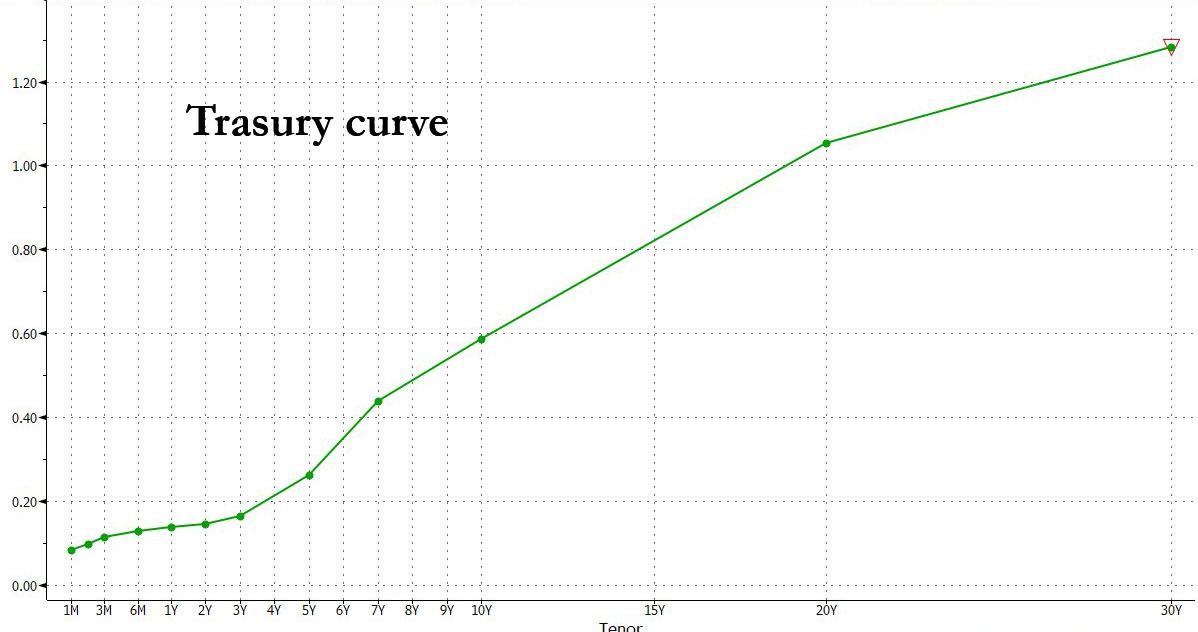

One possible reason for the modest tail is that the curve has been rallying, with 10Y trading below 0.59%, just shy of all time lows, thus providing little opportunity for concession.

Of course, since there is just one auction in recent history to compare today’s auction to, superficially the auction was quite strong, although one look at the curve shows that the 20Y is somewhat “kinky” on the curve.

via ZeroHedge News https://ift.tt/39hjObx Tyler Durden

Ciphertrace is tracking the stolen Bitcoin from the Twitter hack last week.

Hackers have shifted the funds through coin mixers, exchanges, and gambling sites to obscure its movement.

With the community’s eyes on the funds, it’s going to be difficult to cash out.

Last week hackers hijacked Twitter, taking control of the accounts of several high-profile individuals. But rather than start World War 3, they elected to run a simple Bitcoin scam – swindling a total of 12.5 Bitcoin ($120,000).

Now, the Bitcoin is on the move, and here’s how the hackers are trying to escape with their spoils.

According to blockchain analytics firm Ciphertrace, the hackers are using a combination of Bitcoin mixing services, gambling sites, exchanges—and even defunct addresses—in an attempt to both hide the money and turn it into other currency.

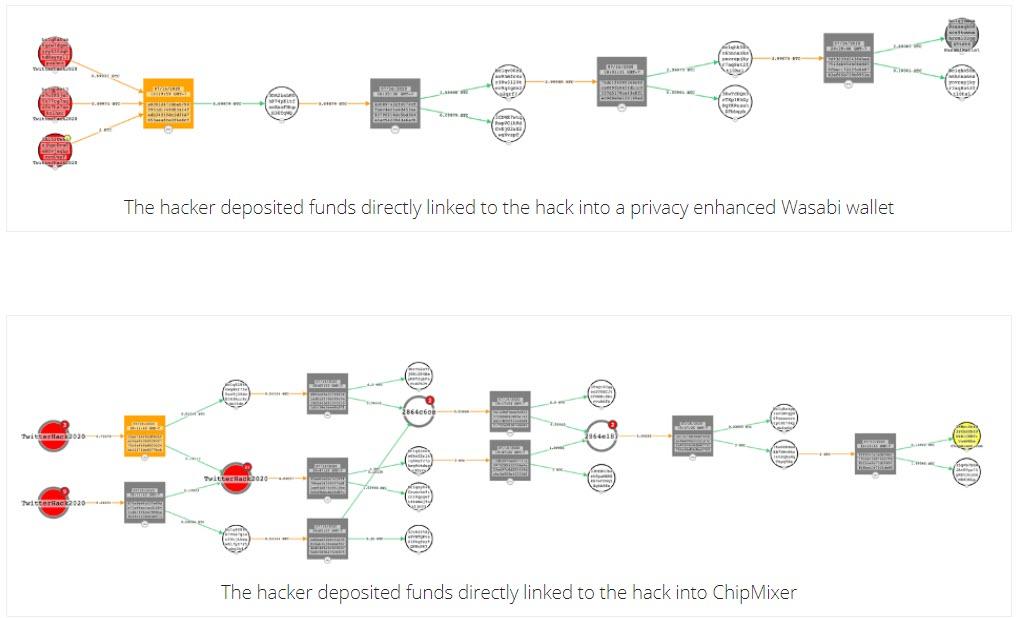

The first port of call was a Bitcoin mixing service. These let people swap their Bitcoin for someone else’s Bitcoin—while obscuring the identities of both parties. They’re often used to “clean” stolen Bitcoin.

On July 16, one day after the hack, attackers sent 2.89 Bitcoin (roughly 22.5% of the total haul) to Wasabi—a privacy-centric Bitcoin wallet with a built-in mixer. It’s a very effective way of stopping any observers from following the money trail.

A day later, a further 0.1022 BTC moved into another Bitcoin obfuscator, Chipmixer. Ciphertrace was unable to follow the Bitcoin any further.

Ciphertrace tracked the scammed funds to two coin mixers. Image: Ciphertrace

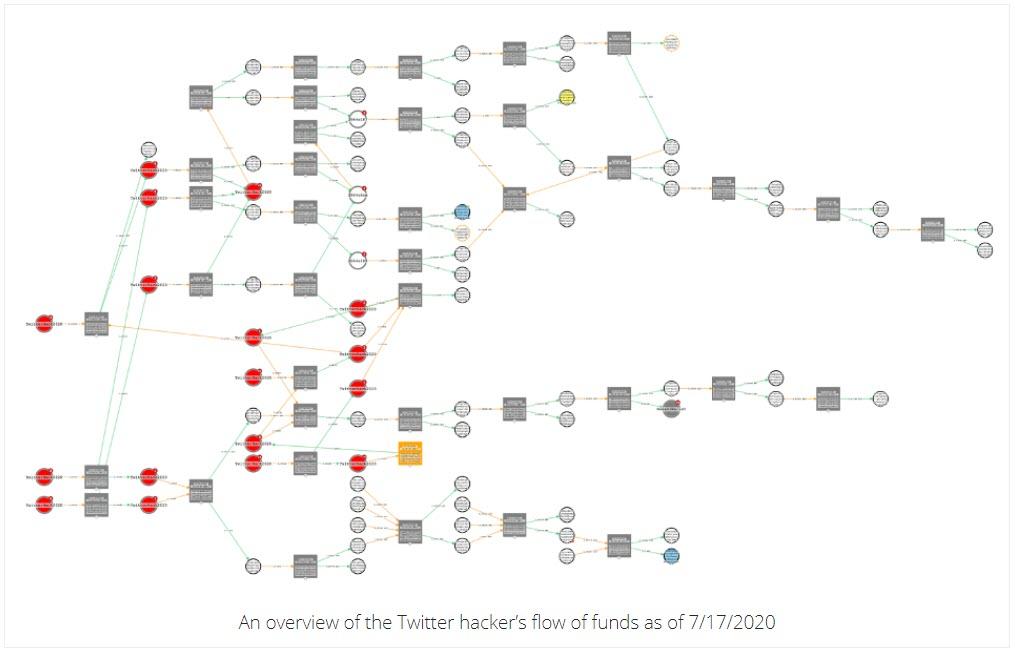

Over the next few days, Ciphertrace tracked piecemeal amounts of the rest of the scammed funds to peer-to-peer exchanges and gambling sites. Just over 1 Bitcoin—roughly 8.5% of the Twitter plunder—was sent to an unnamed Singapore-based crypto exchange.

Ciphertrace’s overview of the Twitter hacker’s flow of stolen Bitcoin. Image: Ciphertrace

An unspecified portion of Bitcoin then traveled to an inactive Binance cold wallet.

“CipherTrace believes that this transaction was not made to cash out funds, but rather to troll,” reads the reports. The idea being that the hackers know the funds are being watched and they just want to confuse or infuriate anyone watching.

Who hacked Twitter?

Per a report from the New York Times, contrary to conspiracies of elaborate schemings from a rival nation, the hack was purportedly initiated by a group of youths. The alleged adolescent attackers told the Times how they managed to gain access via information left on Twitter’s internal Slack channel.

Since then the person, known as Kirk, who had the access to Twitter has since disappeared.

via ZeroHedge News https://ift.tt/2ZObnBl Tyler Durden

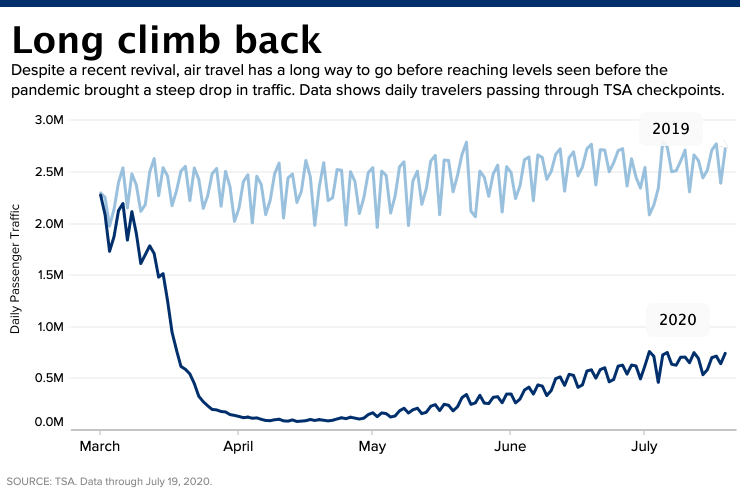

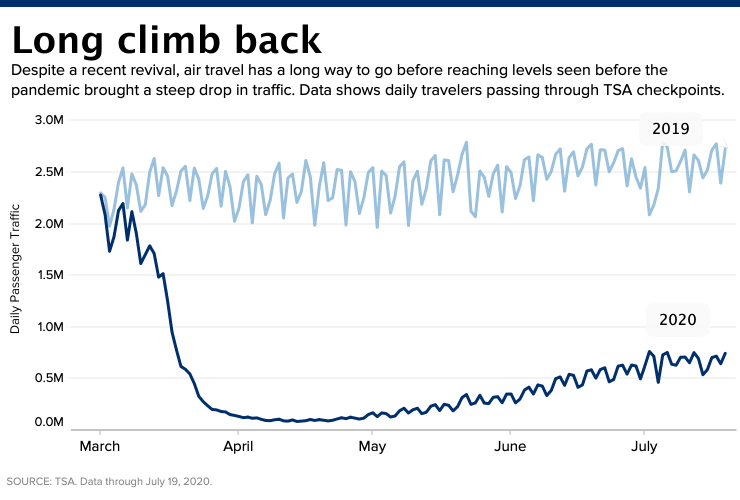

United Airlines Defers Plane Deliveries To Beyond 2022 As Air Travel Remains Muted Tyler Durden

Wed, 07/22/2020 – 12:50

United Airlines Holdings Inc. said Wednesday morning, all new aircraft deliveries due in 2022 have been deferred as air travel for the next several years will remain depressed. The Chicago-based company also said 32,000 employees have volunteered for a temporary leave of absence.

Earlier in the morning, United Airlines’ CEO Scott Kirby told CNBC that estimated sales would not recover in a V-shaped formation until there’s a proven vaccine for COVID-19.

“Our guess is that revenue will get to about 50% of what it was in 2019 in a pre-vaccine world,” Kirby told CNBC. Once we get past a vaccine and it is widely distributed, we will quickly recover towards 100%, but our guess is we are going to plateau at 50% until we get to a vaccine.”

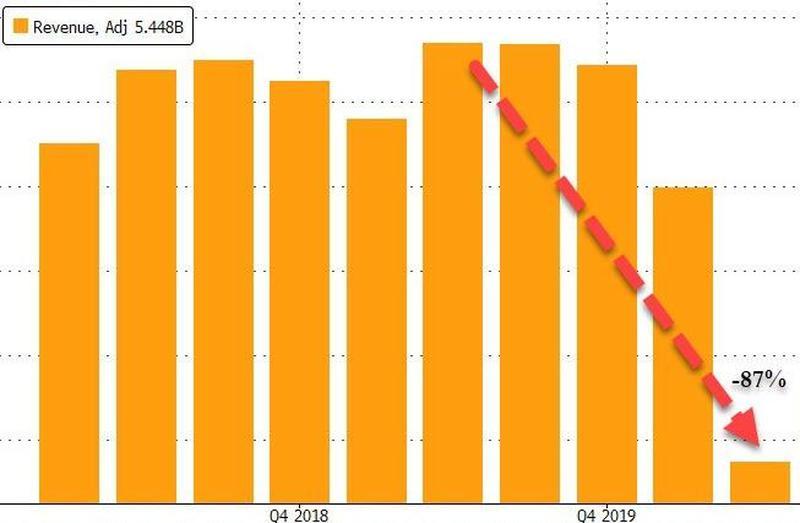

On Tuesday, the airliner reported revenues of $1.48 billion in 2Q20, an 87% crash from $11.4 billion during the same time last year. It said capacity in 3Q would be down 65% compared with the same quarter a year ago.

In early July, United Airlines warned 36,000 employees were at risk of losing their jobs in October when the federal payroll stimulus expires.

Shares of United Airlines slid nearly -2% on Wednesday.

On Monday, the Transportation Security Administration (TSA) published new passenger data from US airports, showing the first slump in weekly air travel since April.

h/t CNBC

United Airlines’ deferment of planes due in 2022 suggests the travel and tourism industry will remain muted for a couple of years. It also implies there’s no V-shaped recovery in the economy this year.

via ZeroHedge News https://ift.tt/3hphu52 Tyler Durden

{kind=link}

{kind=link}