In 2011, the USA Network introduced a truly preposterous legal comedy-drama called Suits, in which one of the name partners at a powerhouse Manhattan law firm makes an exception to its older-than-God employment policy of hiring only Harvard Law grads.

The precedent-smashing candidate not only didn’t go to Harvard, he didn’t go to law school at all, and he literally stumbled into the job interview while fleeing a police bust of one of his dope deliveries. Aside from the weed biz, the only entry on his resume was for fraudulently taking bar exams for nitwits, which he always passed because of his photographic memory.

Most of the next six seasons or so consisted of everybody at the firm running around trying to keep the outside world from finding out one of their fellow lawyers was a fake. This was surprisingly entertaining—I’ve met a lot of attorneys who confided that Suits was their second-favorite guilty pleasure after billing clients for on-line backgammon games. But eventually the premise wore itself out and in recent years, Suits has been mostly known as the place where Meghan Markle worked before she turned into a lumpen proletariat mole in the British royal family.

Never one to forget a (even temporarily) winning formula, USA is spinning off a Suits sequel, Pearson, based on an even more ludicrous proposition: The mayor of Chicago, on the verge of losing a poverty-pimp lawsuit over a public-housing development that could expose his shady financial machinations, gets the opposing attorney disbarred, then hires her as his No. 2 aide.

The person she has to work most closely with is the very city attorney who led the legal fight to revoke her law license, and whom she angrily (and, as it turns out, correctly) accused of sleeping with the mayor. If you’re thinking this is a thought problem from a Human Rights Regulations on the Ninth Circle of Hell handbook, we must have similar bookshelves.

The disbarred attorney at the heart of this massive goat-fornicative scenario is Jessica Pearson (Gina Torres), the former head of the big New York law firm in Suits. Having lost that firm—though not, apparently the income that supported her haute couture wardrobe—through her inability to manage its intricate and savage politics, she’s decided to take on the simpler task of managing the city that produced Richard Daley, Al Capone, and Rod Blagojevich.

Her new boss, Mayor Bobby Novak (Morgan Spector, Homeland), seems to fit right into the job’s slimeball traditions—dirty money, scummy pals, using the police for after-hours hardball—but Pearson sniffs “Pshaw!” to friends and family concerned about her new job: “All politicians are professional liars.” Yet not two minutes later, she proclaims herself on a moral crusade: “I spent years doing nothing but making money and trying to keep my name up on a [law firm] wall. I’d like this to be about more.”

There you see the real danger confronting Ms. Pearson: not endemic corruption or grinding poverty or police brutality, but serial-killer hackery on her writing staff, which can’t remember what it’s had coming out of its characters’ mouths from one scene to the next.

In Suits, Pearson was largely a supporting character whose main job was to keep her weird, temperamental staff of attorneys from killing one another. In this show, however, her responsibilities have increased. She has to sell a badly written character, juggle a hellish number of barely comprehensible storylines, and—unlike in Suits—do it all without cracking a smile. The weird obsessions that made Suits wildly more entertaining than your standard legal drama—with mud baths, incontinence, and pronunciation of the word “sheee-it”—have all disappeared.

Instead, there’s an endless parade of political soap opera. Pearson’s boyfriend, disgusted by her job, takes on a long out-of-town project. The mayor is extramaritally conferring with his cute-as-a-button city attorney (Bethany Joy Lenz, Colony), and not about tax millage. And the mayor’s illegitimate brother with the patronage job at the police department—is he spying on the cops for the mayor, or on the mayor for the cops?

If Pearson gets anything right, it’s the mind-numbingly redistributive nature of big-city government, where literally every minute of every day is spent slicing and re-slicing the revenue pie in hope of the momentary pacification of one shrieking pressure group or another. The public schools, the police union, the housing activists, they all want theirs, and not one moment is spent evaluating their demands on public money except in terms of how much hell they can potentially raise.

But Pearson—neither the show nor the character—makes no attempt to analyze or comprehend its squalid environment beyond the occasional sloganeering like “Closing schools is a hate crime.” Pearson simply proclaims herself right and rolls along, too good to be true, and too sanctimoniously arrogant to be fun.

If we had to have a drama about Chicago politics, why couldn’t it have been a reality show set in the office of velvet-voiced Jerry Butler, who retired from the city commission last year after 32 years in office? He may not have done much about the murder rate, but when he sang, who cared?

from Latest – Reason.com https://ift.tt/30z8DW1

via IFTTT

Japanese crypto exchange Bitpoint has suspended all services after losing $32 million in a hack involving XRP, Bitcoin (BTC) and other cryptocurrencies.

In an official announcement on July 12, Bitpoint revealed that it had lost around 3.5 billion yen (~$32 million) — 2.5 billion yen (~$23 million) of which belonged to customers and 1 billion (~$9.2 million) to the exchange.

Bloomberg reports that shares of Bitpoint’s parent firm Remixpoint Inc. shed 19% following news of the incident, and were untraded in Tokyo as of 1:44 p.m. “on a glut of sell orders.”

Alongside XRP and Bitcoin, a total five different cryptocurrencies had been stored in the affected hot wallets, including Litecoin (LTC) and Ether (ETH).

The exchange’s cold wallets are not reportedly thought to have been compromised, Bitpoint’s announcement indicates.

Bitpoint was one of multiple domestic crypto exchanges to have been served a business improvement order from Japan’s financial regulator, the Financial Service Agency (FSA), during its wide-ranginginspections of industry businesses, per Bloomberg.

As previously reported, the industry record-breaking hack of $534 million of NEM from Japan’s Coincheck exchange in January 2018 had been attributed to the fact that the coins were stored in a low-security hot wallet.

In 2019, May’s $40 million hack of top crypto exchange Binance has loomed large over the industry – at least eight crypto exchanges have been the target of large-scale hacking incidents in the first half of this year, most recently Singapore-based Bitrue.

via ZeroHedge News https://ift.tt/2jEIhlA Tyler Durden

What do you do if you are a major Japanese investor, whose mandate is to invest in safe assets, yet the yield on Japanese govvies is too low to cover the cost of your liabilities?

That’s the question that Japan Post Bank Co., the banking unit of Japan Post Holdings, has been grappling with. Its answer: buy and hold over half a trillion dollars, or $577 billion to be precise, worth of foreign corporate bonds. That, as Bloomberg notes, is “more than the investment-grade portfolio at Fidelity Investments or the fixed-income holdings at Britain’s Standard Life Aberdeen Plc.” And since Japan Post is a public company, majority-owned by the government, it means that one Japanese bank (really, Japan, due to its state-ownership) is directly funding countless US-based corporations, resulting in hundreds of billions in stock buybacks , and this bank is also indirectly funding the hiring of thousands of US workers. In this “new normal” era of super low rates, this represents a major change from just a decade ago, when the foreign bond portfolio at Japan Post Bank was virtually nil.

This new global bond market “whale” did not emerge voluntarily: as a result of decades of ZIRP and NIRP, Japan Post was effectively pushed out Japan’s bond market and forced to look for investment opportunities elsewhere. Long-term yields in Japan are around 0%, far below even the exceptionally slim rates in the U.S, crippling the business model the postal bank used for more than a century.

Some background: as Bloomberg details, Japan’s postal system set up savings accounts in 1875, which at one point grew to become the world’s largest deposit-taking institution. However, to maintain an especially safe risk profile, the bank was barred from making loans like those of a normal commercial bank, and so the banking unit plowed those deposits into government bonds. Which, when yields were well north of 1%, that made for a boring, yet profitable, enterprise, and helped the bank grow its deposits to a whopping $1.7 trillion, comprising the savings of millions of Japanese households in big cities and remote villages. And, being a bank, it has to invest this money somewhere. But with Japan’s bond yields too low to cover the cost of servicing the bank’s funds, which according to S&P is 0.57%, the bank had to look to other assets.

“It’s a road to insolvency” for the postal bank to invest in Japanese government bonds now, says David Threadgold, a Keefe, Bruyette & Woods analyst in Tokyo who’s followed banks there for more than three decades. And with no other domestic asset class big enough to pour deposits into other than equities, which would require the bank to keep higher capital reserves, “they have to turn themselves into an overseas investment vehicle,” he says.

Such as corporate bonds.

To be sure, the majority of the bank’s investments are still boring enough: Instead of buying supersafe Japanese government bonds paying essentially nothing, it buys supersafe U.S. Treasuries yielding about 2%, which should be sufficient to leave the bank comfortably profitable; the main risk is currency fluctuation, although investors can hedge that risk, even as the cost of doing so has climbed in recent years due to rate differentials between the US and Japan.

Still, its profit margins remain razor thin, and so to boost its profits, the Postal bank has been on the hunt for new kinds of assets. However, with $539 billion of domestic government bonds still on the books and set to mature over time, and deposits continuing to grow, “that’s no simple task.”

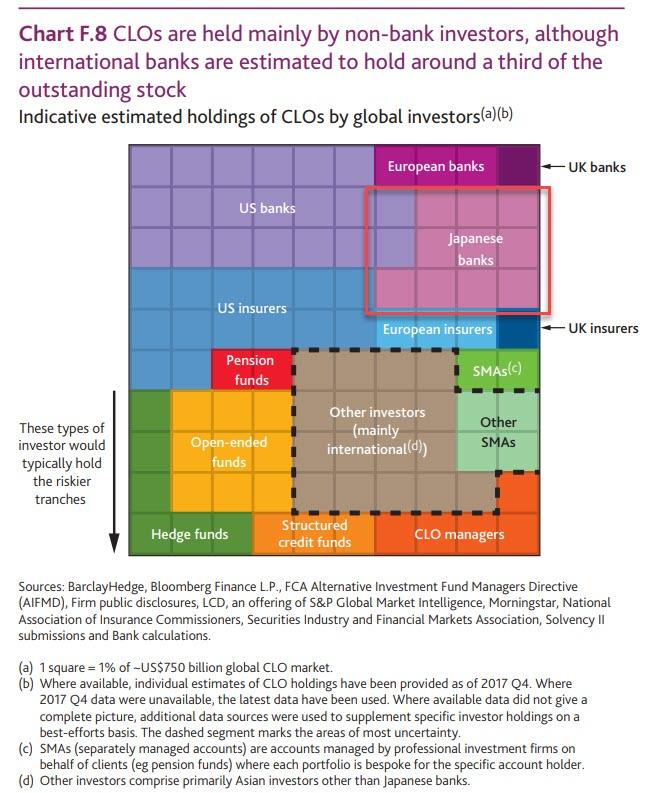

To broaden its universe of possible investments, the bank aims to direct some funds to private equity and real estate. It’s also gone into credit investments, including U.S. collateralized loan obligations—which bundle together loans made to riskier companies. Of course, it isn’t the only Japanese savings institution diving into CLOs in search of better yield. Norinchukin Bank, a cooperative that invests the deposits of millions of Japanese farmers and fishermen – and which has recently emerged as a CLO whale – is too. Norinchukin bought $10 billion of CLOs in the U.S. and Europe in the last three months of 2018, accounting for almost half of the top-rated issuance for the period, according to estimates compiled by Bloomberg (more on this later).

So are Japanese savers and pensioners going to be the next financial crisis’ German “widows and orphans“, i.e., bagholders of the trillions in fallen angel corporate bonds and “safe” CLO tranches?

While Bloomberg notes that observers are confident Japan Post doesn’t have major time bombs on its balance sheet, the sad record of Japanese investment overseas is replete with missteps; just two examples:

In March, Japan’s No. 3 bank, Mizuho Financial Group Inc., surprised investors by booking 150 billion yen ($1.4 billion) of losses on its foreign bond holdings.

Norinchukin posted a $6 billion loss during the financial crisis because of its purchases of toxic assets in the U.S.

“You are asking if we are comfortable with this? I don’t think everything is fine. There are risks,” a resigned Japan Post Holdings CEO Masatsugu Nagato said about the need to invest abroad at a June press briefing. He also said: “We are very careful, but foreign bond investment will increase” for one simple reason: he is forced to buy the next generation of “toxic assets” because the BOJ assures the bank’s insolvency, as Keefe, Bruyette said, if it sticks with Japanese assets.

To be sure, this is not the first time questions have been asked about Japan seemingly price-insensitive investments around the world, and mostly in US corporate bonds and CLOs (see “A Japanese Tsunami Out Of US CLOs Is Coming“). Aware of the growing concerns about its massively levered financial system, financial regulators say they are keeping an eye on lenders’ investments in CLOs and other loans, so the postal bank’s freedom to pile into particularly risky assets may be limited (although who can forget that according to none other than Ben Bernanke, “subprime was contained”).

Yet even so, another risk is on the horizon: what if even more Japanese investors scramble for the “high yield” of US Treasurys and corporate bonds? If U.S. Treasury yields fall? “The scary thing really is that they are all depending on the U.S. market,” Michael Makdad, a Morningstar analyst said of Japan Post Bank and its peers.

Indeed, prompting speculation that US Treasuries have become a Giffen Good, 10Y Treasury yields have tumbled by more than a percentage point over the past nine months, as investors have bought up government debt expecting central banks to become even more dovish as economic growth slows; and yet foreign demand appears to be stable, if not rising. On the other hand, with the Fed set to cut rates, Treasury yields are expected to slide well below 2%. Of course, the euro region hardly offers a better option, with much of the area’s debt trading with negative yields. “If you turn the rest of the world into Japan, then there’s no escape,” Threadgold says.

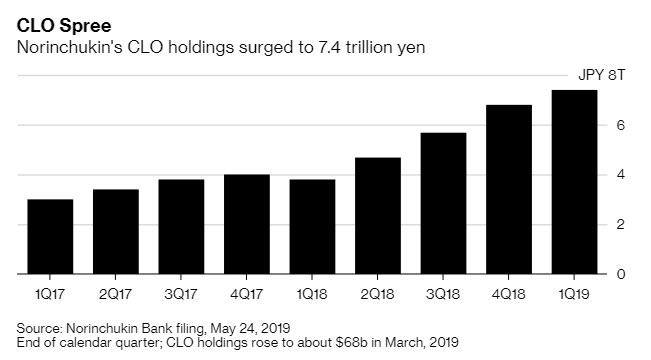

Meanwhile, as the scramble for yield comes back with a vengeance now that all global central banks have turned dovish again, Japanese mega-buyer Norinchukin Bank – better known as Nochu – and lender to Japan’s farmers and fisherman, has re-started purchasing CLOs after dramatically cutting back around April amid heightened market scrutiny, Bloomberg reported separately.

How big is Nochu in the US CLO market? Let’s just say there is no single bigger player, because until very recently it was a massive presence in the $600 billion CLO market, buying as much as half of the highest-rated bonds in the fourth quarter in Europe and the U.S.

That helped sustain record growth which in turn sparked regulatory scrutiny and diverted attention to the bank’s outsized role in the market, prompting its recent retrenchment. And after taking a brief sabbatical, the bank is back yet even in its absence, CLO sales held near record pace, underscoring their popularity with investors starved of yield; indeed, even with a largely absent Nochu, sales hit $35.9 billion in the second quarter of 2019, compared with $29.5 billion in the first three months of the year.

“We aim to build a portfolio of bonds, equities and credit with healthy risk balances by exercising necessary checks,” a representative for Nochu told Bloomberg. “CLOs are credit assets that we will invest in based on this concept.”

The silver lining is that Japanese banks invest mostly in the super-senior, AAA-tranches. Yet even so, it is only a matter of time before they too are forced to buy riskier tranches. Consider that even with Nochu’s brief absence, average spreads on the triple-A rated bonds sold by top-tier managers tightened to roughly 130 basis points across May and June, compared with about 138 basis points in the first quarter, according to data compiled by Bloomberg. Market participants point to the tightening as proof of the CLO market’s resilience. Of course, the other, more correct explanation, is that with central banks herding investors into increasingly riskier assets, CLOs had nowhere to go but up.

On the other hand, CLO risk premia have been more resistant to tightening than other asset classes in 2019, so the increase in Japanese buyers will likely result in a spike in demand for the bundled loans. That would lower borrowing costs for junk-rated companies and help increase the volume of leveraged buyouts, but could also add air to a market that regulators worry is already over-inflated.

Meanwhile, as Japanese banks seek to allocate trillions in local savings, they have emerged as some of the world’s largest bond, and CLO, investors: Nochu alone held more than 18% of all triple A-rated CLO bonds outstanding at the end of March 31, according to research by Citigroup. Wells Fargo held around 9.5% while Japan Post Bank Co. owned approximately 2.9%, the Citi research showed (of course, Japan Post appears far more interested in buying corporate bonds outright).

“The basic concept of Norinchukin Bank’s investment is global diversification,” the bank’s representative said in its email, written in response to questions from Bloomberg News. As a reminder “diversification” is how you try to justify a reckless investment just after the crash.

And speaking of growing concentration risk, Japanese regulators – and millions of Japanese savers – appear to have no choice but to see more investments into increasingly risky fixed income.

One option to mitigate such risk, according to Bloomberg, would be to wind down balance sheets of banks such as Post Bank and make it smaller. But Japan Post is sometimes the only provider of financial services in areas where the population is shrinking. And the banking unit subsidizes the postal business, so it is a monopolistic Catch 22. Furthermore, the idea of turning customers away or discouraging deposits by adding fees is difficult for any national policymaker to embrace. Japan Post Bank is “a national brand,” says Rie Nishihara, a senior analyst at JPMorgan Chase & Co. in Tokyo. “They face a more challenging yield cycle and credit challenges, and that’s very difficult while also supporting 24,000 branches” across the postal system, she says.

So, as Bloomberg concludes, “the fortunes of this mammoth institution may rely on the U.S. avoiding the same low-rates-forever dynamic that has driven the bank overseas.” Yes, but that’s just half the story, because if instead of dreaded low-rates, yields on the US investments in which Japan has invested trillions suddenly were to suddenly soar, then neither Post Bank nor Nochu would survive absent full-blown nationalization. While it is unclear if such an option is amenable to Japan’s taxpayers, the alternative is for tens of millions of pensioners and savers in the demographically crippled country to one day wake up and upon checking their retirement account finding that it’s gone… it’s all gone.

Or, as Threadgold said earlier, for Japan “there’s truly no escape.”

via ZeroHedge News https://ift.tt/2LVatMZ Tyler Durden

With some $13 trillion of bonds worldwide yielding less than zero percent, it would be easy to characterize fixed-income assets as nothing more than a giant bubble waiting to burst. Those who agree probably haven’t heard of the concept of a “Giffen good.”

Simply put, a Giffen good is a paradox of economics where rising prices lead to higher demand, which is in contrast to the negatively sloped demand curve that students learn in Economics 101. Named after 19th century Scottish economist Sir Robert Giffen, a Giffen good is typically an essential item that, because of its higher price, leaves less resources to purchase other items. (To be sure, many economists debate whether a Giffen good actually exists.)

In terms of the bond market, it’s important to understand that the rapid plunge in yields, especially for sovereign debt, reflects increased concern about the state of the global economy. Those concerns, in turn, only fuel demand for the safest assets even at negative yields, which pushes prices higher and yields even lower.

There are three more reasons why sovereign bonds have become a Giffen good.

First, inflation rates have been low or declining in the U.S., euro zone and Japan, encouraging investors to allocate more resources to fixed-income assets despite falling yields. High rates of inflation reduce the purchasing power of bond holders, but low rates of inflation do the opposite.

The Federal Reserve’s target of a 2% inflation rate has not been consistently met for more than a decade, and we learned Friday that average hourly earnings of U.S. workers over the past year increased by only 3.1%, less than consensus and continuing to decelerate from a rate of 3.4% earlier this year. The European Central Bank’s 2% inflation target remains a distant dream with prices rising by 1.2%. Japanese consumer prices rose by a mere 0.7% in May.

Second, expectations for central bank monetary policy have been kind to bond investors. Ten-year yields have fallen below policy rates in the U.S., Germany and Japan, providing a reason – and pressure – for monetary authorities to reduce rates. Fed Chairman Jerome Powell bluntly stated in his testimony to Congress this week that the latest month employment report, which showed that the economy added a healthy and greater-than-forecast 224,000 jobs in June, would not prevent the central bank from cutting rates in the near future.

In Europe, the nomination of International Monetary Fund Managing Director Christine Lagarde to become the next President of the ECB was a factor in last week’s drop in yields. Lagarde has been supportive of asset purchases by the ECB, and is widely expected to commence a new quantitative easing program when she assumes her new role on Nov. 1.

Third, the steep decline in U.S. and German risk-free yields have increased the attractiveness of lower-rated sovereign credits. As investors reached for returns, Greek five-year yields have fallen from 1.66% to 1.24% over the past month. Even more dramatic was the draw of Italian 10-year notes, whose yields dropped by 66 basis points over the past month to 1.70%.

And as the Fed, ECB and the Bank of Japan lower interest rates or accelerate asset purchases, don’t expect the global economy to respond positively. Instead, such moves are only likely to increase investor concern about the health of the global economy, which could become a sort of self-fulfilling prophecy and tamp down inflation expectations even further. Such a scenario would cause central bankers to lean toward even more easing, raising the odds of a “Japanification” of the global economy.

Investors would be better off ignoring advice that suggests today’s low bond yields make them unattractive relative to equities. The high prices and low yields of bonds acts as a magnet and is likely to be a gift that keeps on giving for the bulls.

via ZeroHedge News https://ift.tt/2l7plw3 Tyler Durden

After explaining, “I don’t think it is right and fair for this administration’s Labor Department to have [Jeffrey] Epstein as the focus rather than the incredible economy we have today,” Labor Secretary Alexander Acosta announced this morning he would be resigning from President Donald Trump’s administration, effective in one week.

Acosta has been in the crosshairs ever since billionaire Jeffrey Epstein was arrested last weekend on federal sex trafficking charges. When Acosta was a U.S. attorney in Miami, he signed off on what’s been seen as an extremely lenient plea agreement with Epstein in 2007 with a remarkably short part-time jail sentence over allegations of sex with underaged girls.

The deal wasn’t just unusual. Ken “Popehat” White, a former federal prosecutor and current Reason contributing editor, explains over at The Atlantic that it was pretty much unheard of:

Epstein’s team secured the deal of the millennium, one utterly unlike anything else I’ve seen in 25 years of practicing federal criminal law. Epstein agreed to plead guilty to state charges, register as a sex offender, and spend 13 months in county jail, during which time he was allowed to spend 12 hours a day, 6 days a week, out of the jail on “work release.” In exchange, the Southern District of Florida abandoned its criminal investigation of Epstein’s conduct, agreed not to prosecute him federally, and—incredibly—agreed not to prosecute anyone else who helped him procure underage girls for sex. This is not normal; it is astounding.

Acosta had been put on the defensive over the deal, and as this scandal played out, his resignation became pretty much inevitable.

Watch Trump and Acosta’s public announcement this morning below:

And here’s Acosta’s resignation letter, which he tweeted out:

Elizabeth Nolan-Brown took an early look at the new indictment against Epstein. Read her analysis from earlier in the week here. And she explored Esptein’s past friendship with Trump himself here.

from Latest – Reason.com https://ift.tt/2xVGYCx

via IFTTT

After explaining, “I don’t think it is right and fair for this administration’s Labor Department to have [Jeffrey] Epstein as the focus rather than the incredible economy we have today,” Labor Secretary Alexander Acosta announced this morning he would be resigning from President Donald Trump’s administration, effective in one week.

Acosta has been in the crosshairs ever since billionaire Jeffrey Epstein was arrested last weekend on federal sex trafficking charges. When Acosta was a U.S. attorney in Miami, he signed off on what’s been seen as an extremely lenient plea agreement with Epstein in 2007 with a remarkably short part-time jail sentence over allegations of sex with underaged girls.

The deal wasn’t just unusual. Ken “Popehat” White, a former federal prosecutor and current Reason contributing editor, explains over at The Atlantic that it was pretty much unheard of:

Epstein’s team secured the deal of the millennium, one utterly unlike anything else I’ve seen in 25 years of practicing federal criminal law. Epstein agreed to plead guilty to state charges, register as a sex offender, and spend 13 months in county jail, during which time he was allowed to spend 12 hours a day, 6 days a week, out of the jail on “work release.” In exchange, the Southern District of Florida abandoned its criminal investigation of Epstein’s conduct, agreed not to prosecute him federally, and—incredibly—agreed not to prosecute anyone else who helped him procure underage girls for sex. This is not normal; it is astounding.

Acosta had been put on the defensive over the deal, and as this scandal played out, his resignation became pretty much inevitable.

Watch Trump and Acosta’s public announcement this morning below:

And here’s Acosta’s resignation letter, which he tweeted out:

Elizabeth Nolan-Brown took an early look at the new indictment against Epstein. Read her analysis from earlier in the week here. And she explored Esptein’s past friendship with Trump himself here.

from Latest – Reason.com https://ift.tt/2xVGYCx

via IFTTT

Most people would be hard-pressed to remember every candidate who showed up at last month’s two-night Democratic presidential debate, must less the candidates who didn’t appear. But one contender who did not make the qualifying threshold was Mike Gravel, the 89-year-old former Alaskan senator. And all things considered, Gravel is pretty memorable: What he lacks in name recognition, he makes up for with an unorthodox and deliberately outrageous approach to politics. (His campaign, for example, is being run by two teenagers.)

Now the former senator is proposing a constitutional amendment to remove marijuana as a Schedule 1 drug, thus legalizing it recreationally on the federal level. It’s an unconventional approach to drug reform befitting of an unconventional presidential candidate, but Gravel argues that it would be the easiest way given the current congressional gridlock.

“Congress hasn’t done anything at this point in time, and it’s tough to realize whether we’re looking at another year, two years,” he tells Reason. “From my experience in the Congress, they could pretty well screw it up, and this is already unbelievably screwed up. We could immediately get a law passed in the next 30 days, but we’ve been waiting 30 days for the past three years.”

In times past, constitutional amendments have been implemented with a two-thirds vote of approval in both the House and the Senate, which then must be ratified by three-fourths of the states. But Gravel acknowledges that his plan would be a near-impossible sell if Republicans maintain control of the Senate. In that case, he says, he would take advantage of a second avenue—a constitutional convention—in which 34 states would need to gather on their own accord and agree to adopt the amendment. That route has never before been used.

Gravel compares the harmful effects of marijuana bans to the harmful effects of alcohol Prohibition. And Prohibition, he reminds us, was repealed by constitutional amendment—though only because it started with one. The 21st Amendment nullified the 18th.

“It’s an option is really what I’m saying,” says Gravel. The candidate doesn’t rule out the chance that Congress could act—in fact, he muses that the pressure of a convention could force lawmakers to come together. But he doubts that would happen. And even it if does, he worries about the poison bills and bargaining chips that could pollute the legislation.

However it pans out, Gravel sees federal action as a necessary way forward. The current state-by-state approach is a “mess,” he says, “promulgated by the fact that the federal Damocles hangs over” their heads. (When former Attorney General Jeff Sessions took office, he threatened to crack down on marijuana using federal jurisdiction, even in states that legalized it.) Gravel also rails against sky-high pot taxes, which he says have sometimes “been so horrendous that people have stayed with the underground supply rather than the legal supply.” Schedule 1 substances are subject to heavy federal income taxation, as the government prohibits (fully legal) state businesses of the weed variety from deducting a slew of business expenses. So his amendment also declares that the drug will be regulated like alcohol and tobacco.

While Gravel limits his proposed amendment to marijuana, he supports the decriminalization of all drugs. “We treat all of these drugs as criminal problems,” he explains. “They’re not. They’re public health problems.” He speaks fondly of the approach taken by Portugal, a fairly conservative country that in 2001 decriminalized all illicit substances, including heroin and cocaine. Drug trafficking there is still a criminal offense, but those caught with less than a 10-day supply get no more than a slap on wrist—a fine, for instance. The problem is otherwise considered a medical one, where individuals meet with a local commission to discuss possible treatment options. The method has been widely successful, with the nation seeing a decrease in overdoses, drug-related crime, HIV infections, and adolescent drug use.

Gravel hopes his amendment will help put the U.S. on track to something like the Portuguese model. “Once you see the success of cannabis and addressing that problem in society, then society matures with these experiences and reacts differently,” the former senator says. “If we were to succeed with this, then I think it would really lead to a legislative approach.”

Although the campaign recently announced that it might be coming to an end in the near future, it received new life with a fundraising plea made by Marianne Williamson—a fellow contender for the Democratic nomination—on Gravel’s behalf, putting him in striking distance of the 65,000-donor threshold required to make the July debates. (At the time of this writing, he is less than 3,000 short.) If it doesn’t happen, he concedes that he won’t be heartbroken. His campaign, he says, was less about ascending to the Oval Office and more about starting a conversation about the issues—something that only became a reality when David Oks and Henry Williams, the two teens at the heart of his effort, urged him to run.

“Do you realize how old I am?” he asked the boys when they approached him.

“Doesn’t make any difference,” they replied. “It’s the positions you have on the issues that are so vital to communicate.”

In addition to drug reform, Gravel wants to cut military spending in half. He also supports single-payer health care and calls for the abolition of private insurance companies.

The deadline to qualify for the next Democratic debate is July 16. If Gravel makes it, his debate appearance will represent a major shift in his campaign—and not just because he’ll have a big platform for an evening. Up until now, he has not left his house in the pursuit of his 2020 ambitions. And until the next debate, he plans to stay put.

“No party’s gonna carry me other than these kids,” he says, referring to Oks and Williams. “But I’m gonna have a patio campaign. I’m gonna sit on my patio, and see what happens.”

from Latest – Reason.com https://ift.tt/2l7jk2r

via IFTTT

Most people would be hard-pressed to remember every candidate who showed up at last month’s two-night Democratic presidential debate, must less the candidates who didn’t appear. But one contender who did not make the qualifying threshold was Mike Gravel, the 89-year-old former Alaskan senator. And all things considered, Gravel is pretty memorable: What he lacks in name recognition, he makes up for with an unorthodox and deliberately outrageous approach to politics. (His campaign, for example, is being run by two teenagers.)

Now the former senator is proposing a constitutional amendment to remove marijuana as a Schedule 1 drug, thus legalizing it recreationally on the federal level. It’s an unconventional approach to drug reform befitting of an unconventional presidential candidate, but Gravel argues that it would be the easiest way given the current congressional gridlock.

“Congress hasn’t done anything at this point in time, and it’s tough to realize whether we’re looking at another year, two years,” he tells Reason. “From my experience in the Congress, they could pretty well screw it up, and this is already unbelievably screwed up. We could immediately get a law passed in the next 30 days, but we’ve been waiting 30 days for the past three years.”

In times past, constitutional amendments have been implemented with a two-thirds vote of approval in both the House and the Senate, which then must be ratified by three-fourths of the states. But Gravel acknowledges that his plan would be a near-impossible sell if Republicans maintain control of the Senate. In that case, he says, he would take advantage of a second avenue—a constitutional convention—in which 34 states would need to gather on their own accord and agree to adopt the amendment. That route has never before been used.

Gravel compares the harmful effects of marijuana bans to the harmful effects of alcohol Prohibition. And Prohibition, he reminds us, was repealed by constitutional amendment—though only because it started with one. The 21st Amendment nullified the 18th.

“It’s an option is really what I’m saying,” says Gravel. The candidate doesn’t rule out the chance that Congress could act—in fact, he muses that the pressure of a convention could force lawmakers to come together. But he doubts that would happen. And even it if does, he worries about the poison bills and bargaining chips that could pollute the legislation.

However it pans out, Gravel sees federal action as a necessary way forward. The current state-by-state approach is a “mess,” he says, “promulgated by the fact that the federal Damocles hangs over” their heads. (When former Attorney General Jeff Sessions took office, he threatened to crack down on marijuana using federal jurisdiction, even in states that legalized it.) Gravel also rails against sky-high pot taxes, which he says have sometimes “been so horrendous that people have stayed with the underground supply rather than the legal supply.” Schedule 1 substances are subject to heavy federal income taxation, as the government prohibits (fully legal) state businesses of the weed variety from deducting a slew of business expenses. So his amendment also declares that the drug will be regulated like alcohol and tobacco.

While Gravel limits his proposed amendment to marijuana, he supports the decriminalization of all drugs. “We treat all of these drugs as criminal problems,” he explains. “They’re not. They’re public health problems.” He speaks fondly of the approach taken by Portugal, a fairly conservative country that in 2001 decriminalized all illicit substances, including heroin and cocaine. Drug trafficking there is still a criminal offense, but those caught with less than a 10-day supply get no more than a slap on wrist—a fine, for instance. The problem is otherwise considered a medical one, where individuals meet with a local commission to discuss possible treatment options. The method has been widely successful, with the nation seeing a decrease in overdoses, drug-related crime, HIV infections, and adolescent drug use.

Gravel hopes his amendment will help put the U.S. on track to something like the Portuguese model. “Once you see the success of cannabis and addressing that problem in society, then society matures with these experiences and reacts differently,” the former senator says. “If we were to succeed with this, then I think it would really lead to a legislative approach.”

Although the campaign recently announced that it might be coming to an end in the near future, it received new life with a fundraising plea made by Marianne Williamson—a fellow contender for the Democratic nomination—on Gravel’s behalf, putting him in striking distance of the 65,000-donor threshold required to make the July debates. (At the time of this writing, he is less than 3,000 short.) If it doesn’t happen, he concedes that he won’t be heartbroken. His campaign, he says, was less about ascending to the Oval Office and more about starting a conversation about the issues—something that only became a reality when David Oks and Henry Williams, the two teens at the heart of his effort, urged him to run.

“Do you realize how old I am?” he asked the boys when they approached him.

“Doesn’t make any difference,” they replied. “It’s the positions you have on the issues that are so vital to communicate.”

In addition to drug reform, Gravel wants to cut military spending in half. He also supports single-payer health care and calls for the abolition of private insurance companies.

The deadline to qualify for the next Democratic debate is July 16. If Gravel makes it, his debate appearance will represent a major shift in his campaign—and not just because he’ll have a big platform for an evening. Up until now, he has not left his house in the pursuit of his 2020 ambitions. And until the next debate, he plans to stay put.

“No party’s gonna carry me other than these kids,” he says, referring to Oks and Williams. “But I’m gonna have a patio campaign. I’m gonna sit on my patio, and see what happens.”

from Latest – Reason.com https://ift.tt/2l7jk2r

via IFTTT

The Democrat-led House voted Friday to block President Trump from taking military actions against Iran without first seeking Congressional approval – a vote which had the support of more than two dozen Republicans, much to John Bolton’s chagrin.

According to the Washington Post, the vote will likely ensure a showdown with the GOP-controlled Senate over whether the restriction will be included in the final bill negotiated between the two chambers. Of note, the House version contains an exception for cases of self-defense.

Republicans in both the House and Senate have argued that such language would embolden Tehran amid a ‘divided’ Congress.

“Our national security is not a game. But that is exactly how Democrats are treating it,” said House Minority Leader Kevin McCarthy (R-CA) on Friday morning.

House Armed Services Committee Chairman Rep. Adam Smith (D-WA) pushed back, saying that Republicans “can opposite it, that’s fine, but to say we don’t care about national security . . . is a baldfaced lie.”

“In fact, our bill isn’t just good, it’s better than the ones that the Republican Party has put together, because we believe the Pentagon should be accountable,” added Smith.

At the center of the Iran amendment is a dispute over how much money should be allocated to the Pentagon and military this year. While Trump and the Republicans want $750 billion, the House bill limits it to $733 billion – a figure Smith says military leaders have previously endorse.

The Iran amendment is just one of several high-profile measures that lawmakers voted this week to include in the first defense authorization bill Democrats have steered through the House since taking over the majority earlier this year. Those measures, which range from ending U.S. participation in Saudi Arabia’s military campaign in Yemen to undoing President Trump’s ban on transgender troops, helped secure the support of liberal Democrats from the congressional Progressive Caucus, who had previously warned that they might vote against the defense bill. –Washington Post

Liberal Democrats, meanwhile say $733 billion is still too steep vs. the current fiscal year’s $717 billion allocation, and have proposed a $16.8 billion reduction to war funding – an effort which failed in the House.

via ZeroHedge News https://ift.tt/2l5MAH4 Tyler Durden

Submitted by Joseph Carson, Former Director of Global Economic Research, Alliance Bernstein.

Preemptive or Bubble-Making Monetary Policy

Preemptive actions is an important feature of monetary policy, but policymakers have never made a preemptive move when the economy’s actual performance has been so closely aligned with the Fed’s own expectations or when the financial markets were so robust. If the Federal Reserve lowers official rates at it’s July 30-31 Federal Open Market Committee meeting it would be done based on the view that a modest “preemptive” move now would obviate the need for larger actions later. Yet, the counterargument is that adding liquidity against a backdrop of overly accommodative financial conditions is precisely the tinder that ignites bubbles.

At the December 18-19 2018 Federal Open Market Committee meeting policymakers revealed their forecasts for 2019; 2.3% gain in real GDP, a 3.5% end of year unemployment rate and core inflation of 2%. And based on those economic and inflation forecasts policymakers had anticipated hiking official rates twice (in increments of 25 basis points) over the course of 2019.

During the first half of 2019 the real economy grew 2.3% annualized (averaging the 3.1% growth of Q1 with the 1.4% estimate for Q2 based on GDPNOW forecasting model of the Federal Reserve Bank of Atlanta), the unemployment rate sat at 3.7% in June and the core consumer price inflation increased at an annualized rate of 2.1%. Despite a near home run in all of its forecasts policymakers are now considering lowering official rates. What changed?

One of the arguments that has been advanced is that some policymakers are worried that the consistent undershoot of the 2% inflation target creates the potential for consumer inflation expectations to become unhinged, hindering the effectiveness of monetary policy.

The first problem with that argument is that monetary policy can influence the degree of liquidity in the system, but it cannot guide its direction. The fact that of the monetary liquidity is being channeled into the asset markets (which are not part of the targeted inflation index) does not mean policy is ineffective or that rates need to be lowered to hit an arbitrary inflation target. Given the complexity of the economy and the imprecision in price measurement hitting a 2% target would occur more by luck than by design.

The second problem with that argument is that either consumer’s are unaware of the Fed’s 2% target or that their actual experienced inflation consistently runs higher than reported inflation. Surveys of consumer inflation expectations have consistently shown that people expect more inflation than the 2% target, and only twice (for a very short spell) in the past 20 years did expectations dip below 2% mark and both of those occurred during a crisis (9/11 and Great Financial Recession).

Another argument advanced by the Fed Chairman Jerome Powell is that the economy is facing a lot of crosscurrents. Crosscurrent is another way of saying that some sectors and industries in the economy are growing and others are not. But that’s always true. The Bureau of Labor Statistics includes in its monthly employment report a diffusion index, measuring how many industries are hiring month over month. In normal times the diffusion index runs between 60% to 65% —-which implies an increase in hiring for a broad range of industries but also a large group that are not hiring as well. The June 2019 diffusion index reading stood at 60.7. Normal times?

* * *

Monetary policy is about to enter uncharted territory. Preemptive easing policy actions in the past have been taken when sharp sell-offs in equity markets or stress in the credit markets had the potential to generate adverse economic outcomes. None of those conditions exist today; if anything, financial conditions are too relaxed.

Preemptive policymaking requires a constant and broad assessment of economic and financial conditions so not to risk over doing it one way or the other. Equity prices should figure prominently in this monitoring process since equity prices offer signals on future growth but they are also a receptacle for excess liquidity. The sharp rise in equity prices over the first half of 2019 should tell policymakers that the problems the economy faces are non-monetary related and lowering official rates is not the appropriate policy response. The danger in promising more easy money is that equity prices rise to unsustainable levels creating bigger adjustment risks to the economy that presently exists in low inflation and crosscurrents.

via ZeroHedge News https://ift.tt/2jEv3W8 Tyler Durden