Rabo: As Trump Challenges The Results, This Is Likely To Get Bumpy For Markets Tyler Durden

Fri, 11/06/2020 – 08:45

By Michael Every of Rabobank

What a nice end to the week. Front and center, obviously, is the ongoing chaos of the US election. The latest developments are that vote margins remain razor-thin in several states, with Trump’s lead declining in Pennsylvania and Georgia, but Biden’s lead narrowing in Arizona in tandem – potentially enough that the state could, perhaps, flip back to Trump when/if all votes are finally counted, if the current vote split being seen continues. Were that to occur, the narrative, and the market, could move quickly. Recounts seem likely, however.

More importantly, Trump himself was front and center, with unprecedented claims that the election is being stolen due to orchestrated Democrat voter fraud: with litigation pending, this suggests the election will end up with judicial action one way or the other. Mainstream and social media, and Bloomberg, report these claims –an unhappy echo of the infamous 1960 Nixon–Kennedy election– as “baseless” and “falsehoods”. That may well prove to be the case, but collecting evidence for litigation in such opaque matters takes time; until then, while the president’s remarks are obviously inflammatory, the (social) media stance, right or wrong in fact, will not help calm matters given Trump also stated he had ran against “suppression” pollsters, and the mainstream media, and Big Tech.

The key implication for markets is again that this is likely to get bumpy, and drag on, and through the courts – a process already now underway in a few states, and possibly at the federal level in short order. Notably, Nixon ultimately conceded to Kennedy after losing by just 112,000 votes from 68 million in total, despite being convinced that fraud had occurred, because he did not want the country to go through a constitutional crisis. This election looks like it could perhaps be decided by as few as 12,000 votes from more than double the 1968 total. Yet judging from Trump’s words, a Nixon-style concession does not look like it is going to be repeated.

Over in China, the Global Times makes clear that regardless of who wins, things continue to look bleak for US-China relations: more Trumpism is seen stemming from both the Democratic and the Republican parties. It’s true that the one area of bipartisan cooperation in the US is anything China-related. Moreover, watching the least partisan US political post-mortems finds loud voices from both the Democratic and Republican parties arguing that their future lies with appealing to the working class more – which is not going to sit well with free trade and free markets. Just don’t tell the donors of either party who, like the existing gerontocracies running both, like things just the way they are, thank you very much.

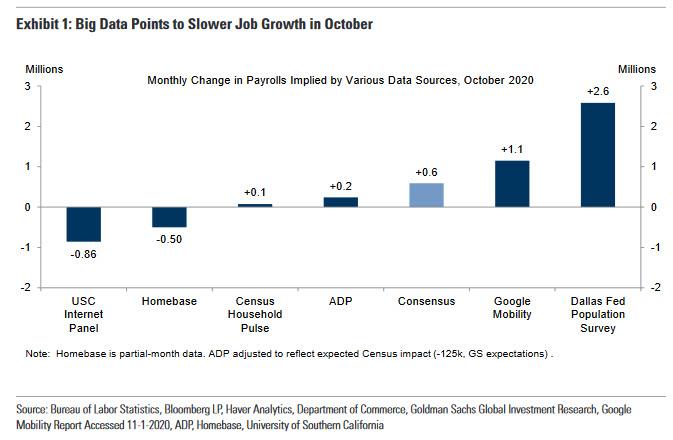

That’s a sentiment obviously shared by US stocks, which have been delighted by the prospect of constitutional chaos and/or political gridlock. Forget about institutional quality; forget about fiscal stimulus; lack of effective governance is obviously the secret sauce for success. That is regardless of initial claims falling just a little yesterday, suggesting the ‘v-shaped’ labour market recovery has now stalled far below where it needs to be, a hypothesis which is likely to be confirmed by the payrolls data today. It is also regardless of the US hitting a new daily record for Covid-19 infections of 120,000. Bond yields, just as obviously, track the other way to stocks and will keep doing so – and if stocks stumble, all the more so.

On that front, yesterday’s Fed meeting did nothing, as expected. As Philip Marey notes, even the statement regarding monetary policy was identical to last time. During his press conference, Fed Chair Powell noted that in recent months the pace of recovery has moderated; and now it appears that we should not count on fiscal policy to provide much support to the economic recovery in the next two years, leaving the FOMC on their own at a time when monetary policy options are almost depleted.

It’s similar glad tidings all over: the BOE voted unanimously to maintain rates at 0.10% and to increase QE by another GBP150bn, which was above our own and the consensus expectation of GBP100bn: the total size of the APF will now rise to GBP 895bn over the course of 2021. Their economic projections were also significantly downgraded: the BOE now sees GDP contracting 11% in 2020, then growing 7.25% in 2021, and another 6.25% in 2022. In our Brit-watcher Stefan Koopman’s view, this is way too optimistic. Indeed, the British government seems to agree, and has just carried out the latest in a series of U-turns, this time to extend the expensive and historically-unprecedented jobs furlough scheme to the end of March 2021. It’s a good job the BOE is paying for all this, isn’t it? It’s an even better job that GBP doesn’t seem to mind so far. Perhaps if the UK has its own constitutional crisis over Scotland, and before that Brexit, things will look different.

Meanwhile, Australia is bracing for de facto confirmation that from today Chinese importers will introduce an “import suspension” of various Aussie goods such as barley, sugar, red wine, logs, coal, lobster, and copper ore and concentrate. The South China Morning Post says “word from custom clearance has been filtering down to importers across China, telling them that shipments could be severely delayed after Friday.” Recall that there is a signed Australia-China Free Trade Agreement in effect; luckily, the Chinese authorities have already clarified that “relevant companies reducing imports from Australia are acting on their own initiative.” One wonders if this factored into the RBA’s latest set of quarterly economic projections released today along with its Statement on Monetary Policy.

In short, how much more happiness can we handle as we head into the weekend?

via ZeroHedge News https://ift.tt/351LKzu Tyler Durden

US Unemployment Rate Unexpectedly Tumbles Below 7% As October Payrolls Beat Expectations Tyler Durden

Fri, 11/06/2020 – 08:36

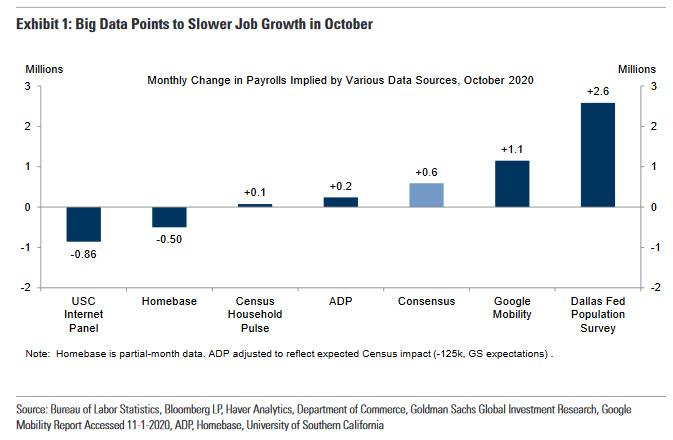

Heading into today’s payrolls report, the high frequency data showed a marked deceleration of employment-linked indicators as the benefits from the stimulus faded…

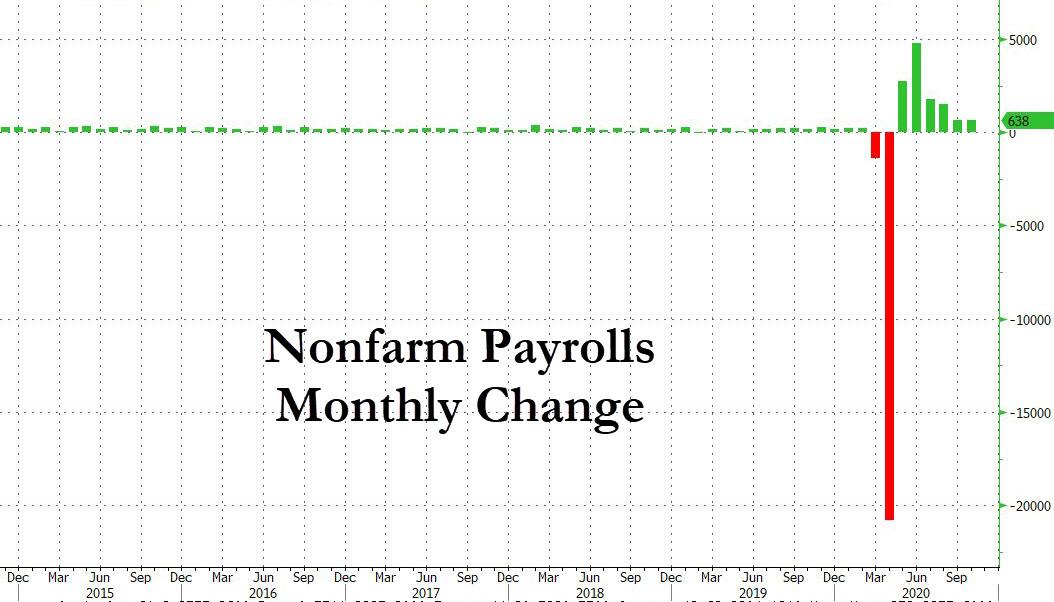

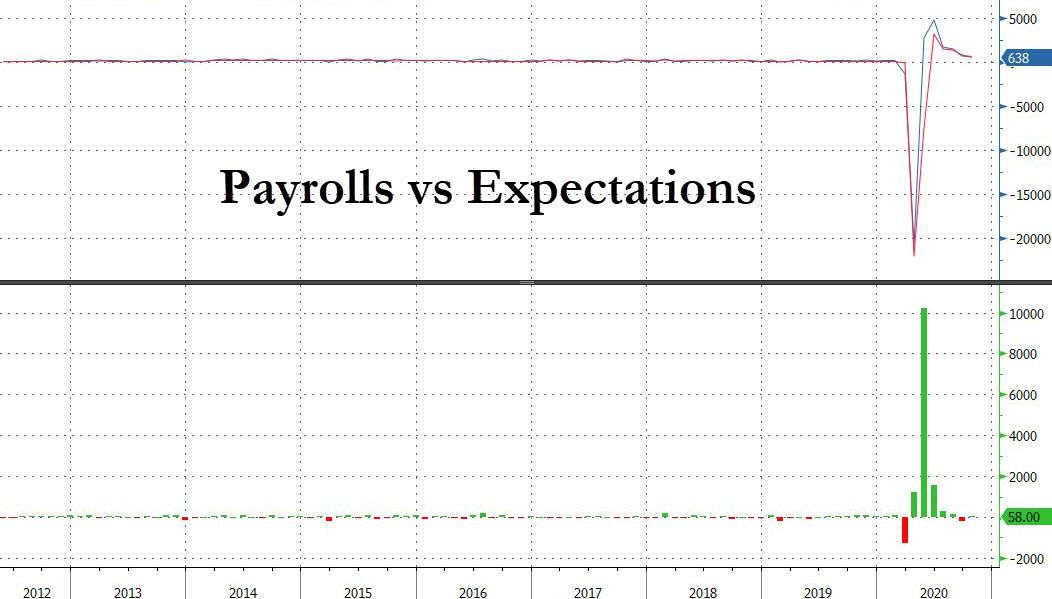

… with Goldman warning that the October payrolls result could be a substantial disappointment. However, that was not the case with the BLS reporting that in October, the US economy added a stronger than expected 638K jobs, which while below last month’s 672K (revised) payrolls…

… was a 58K beat relative to expectations of 593K.

But while the payrolls was indeed better than many had expected, and certainly stronger than the whisper number, it was the unemployment rate that had the most surprising move, tumbling by 1% from 7.9% to 6.9%, and far below the 7.6% expected.

This was as a result of a sharp drop in the number of people unemployed, which declined by 1.5 million from 12.580MM to 11.06MM in October, while the civilian labor force increased modestly from 160.1MM to 160.9MM.

Developing

via ZeroHedge News https://ift.tt/353Q3u7 Tyler Durden

UK Media Reports Putin To Step Down In January Amid Parkinson’s Disease Fears Tyler Durden

Fri, 11/06/2020 – 08:30

Overnight reports that 68-year old Russian President Vladimir Putin is set to unexpectedly step down early due to increasing debilitating health factors originated in the UK tabloid The Sun based in part on observations that he could be showing early symptoms of Parkinson’s disease.

“Observers who studied recent footage of Putin noted his legs appeared to be in constant motion and he looked to be in pain while clutching the armrest of a chair,” The Sun reported late last night. “His fingers are also seen to be twitching as he held a pen and gripped a cup believed to contain a cocktail of painkillers.”

However, responding to questions about the reports the Kremlin put out a statement Friday morning denying it. “No,” Kremlin Spokesman Dmitry Peskov said in response when asked about revelations from the story. “He is in excellent health,” Peskov added.

Via AFP

“There isn’t much to comment on here,” Peskov said specifically of The Sun’s article. “This is pure nonsense. The president is well.”

The initial claims were pushed in the media by a Moscow political scientist named Professor Valery Solovei, who underscored Putin is expected to retire as early as January at the urging of his family. Solovei had actually made similar claims back in 2016, which were also picked up in British media at the time. According to The Sun report:

The academic said he also understood Putin’s undisclosed partner Alina was pressuring him to quit – along with his daughters Maria Vorontsova , 35, Katerina Tikhonova, 34.

Solovei said: “There is a family, it has a great influence on him. He intends to make public his handover plans in January”.

What also fueled the speculation is that Putin introduced a new bill which would make his transition away from Russia’s highest office immediately easier. The bill would both make him a senator for life and grant of life-long immunity from any kind of prosecution, coming as part of the previously announced major shake-up and reworking of the Russian constitution under Putin.

The early retirement claims made a huge international splash, while close Kremlin observers attributed the reporting to a heap of usual fake and hyped reports on Russia that tend to originate in the West.

Oh Jesus. US/UK media has diagnosed Putin with a serious illness again. This time Parkinson’s disease.

Based on comments from Valery Solovey, a well-known Moscow-based conspiracy theorist.

As it currently stands Putin’s term ends in 2024, but for the past couple years it’s been widely believed the constitutional reforms would actually bestow the possibility of even another term – essentially allowing Putin to stay in office for life if he desired.

Interestingly, it doesn’t appear the Kremlin denial included a specific or narrowed detailed refutation of of the Parkinson’s claim in particular, though Peskov did refer overall to The Sun’s reporting as “nonsense” while noting the “excellent health” of the president. Should there be any truth to the speculation – and at this point there’s no real evidence or credible insider sources verifying it – it’s likely Moscow would want nothing of it prematurely leaked out to the world especially given the current sensitivity of the timing as related to the still stalled US presidential election results.

No doubt Russia during this time of American vulnerability would want to project strength, and certainly Putin would want to convey power and confidence should there be transition in Washington to a Biden presidency, or for Trump’s potential next term as well. But then again UK tabloids have been known to get a lot wrong, driven mostly by pure speculation and manufactured narratives and wishful thinking.

via ZeroHedge News https://ift.tt/3l5dJE6 Tyler Durden

I’m delighted that Prof. McConnell—one of the top Religion Clauses scholars in the country—was willing to pass along some thoughts on the Fulton oral argument:

The Supreme Court heard oral argument Wednesday in Fulton v. City of Philadelphia, a case asking whether Philadelphia violated the Free Exercise Clause by excluding Catholic Social Services (CSS) from the array of private groups connecting children without families with willing foster homes, on the ground that CSS’s religious beliefs prevent it from certifying same-sex or unmarried couples who want to become foster parents. Not that that ever happened. No same-sex couples have ever tried to foster through CSS. And not that CSS’s beliefs have any real effect on such couples: they can foster through any number of other organizations. The only concrete consequence of the exclusion is to leave hundreds of children in Philadelphia without foster homes.

One of the questions presented in Fulton is whether the Court should “revisit” (meaning overrule) the Court’s much-criticized 1990 decision, Employment Division v. Smith, in which the Court allowed criminal prosecution of Native American Church practitioners for ingesting peyote, their sacramental substance. That decision, written by the late lamented Justice Antonin Scalia, has been criticized by multiple Justices over the years as well as by a host of academics (though the ideological valence of the critique has shifted from left to right over the ensuing decades). My views on Smith are no secret; Justice Scalia called me Smith‘s most prominent academic critic. I hope and expect that the Court will revisit the decision, which without benefit of briefing or argument drastically narrowed the First Amendment protection for free exercise of religion in the teeth of constitutional text and precedent and what I consider the strong weight of historical evidence of original understanding.

Alas, during Wednesday’s oral argument the Justices showed no serious interest in the merits or demerits of Smith. The reason is obvious: the Petitioner, CSS, led with the argument that it should prevail even under Smith. The new Justice, Amy Coney Barrett, whom most people assume is not a friend to the Smith decision, pointedly asked CSS’s counsel:

[Y]ou argue in your brief that Smith should be overruled. But you also say that you win even under Smith because this policy is neither generally applicable nor neutral. So, if you’re right about that, why should we even entertain the question whether to overrule Smith?

It is of course likely that some of the Justices will concur on the ground that Smith should be overruled. Is has been common the last few years for the Court to render narrow decisions in an early case, declining invitations to overrule precedent, and then to grab the bull by the horns in a subsequent decision. And it is likely that a minority of the Court will vote against CSS—though exactly on what legal ground it is hard to predict. Probably not the unpersuasive logic of the court below.

Assuming for sake of argument that the Court will not overrule Smith, what is it likely to do? There are two most likely paths.

[1.] The Court could render a narrow, fact-specific decision based on the evident hostility shown by Philadelphia toward CSS’s religious beliefs. For example, the City Council passed a resolution labeling CSS’s actions “discrimination that occurs under the guise of religious freedom.” The Commissioner told CSS that “times have changed,” “attitudes have changed,” and that it was “not 100 years ago,” and that its policy on foster families conflicts with the teaching of the Pope. The Court could conclude that this “hostility on the part of the State” fell below the minimum requirements of the Free Exercise Clause. I think of this path as “Masterpiece 2.0,” because it is very similar to the Court’s ruling in Masterpiece Cakeshop v. Colorado Civil Rights Commission, which rested on “religious hostility on the part of the State itself,” and specifically on “the Commission’s consideration of Phillips’ case,” which the Court held “was neither tolerant nor respectful of Phillips’ religious beliefs.”

But this path, like the path of overruling Smith, drew little attention at oral argument in Fulton. And for good reason. Masterpiece didn’t help reduce the temperature on gay rights and religious freedom. If anything, it raised it by suggesting to lower courts and the government that punishing those who hold a minority view on marriage is fine as long as the government does a better job of hiding its hostility—ensuring that more cases like these will keep coming.

In fact, Masterpiece didn’t even resolve the baker’s own case, as he was immediately targeted again after the Court ruled in his favor. More generally, I think there is little appetite on the Court for making the subjective motivations of government actors central to constitutional law. If the Court wanted to go down the path of emphasizing subjective motivations, it would have decided Trump v. Hawaii the other way.

[2.] The other path, much better than Masterpiece 2.0, would be to use the case to correct the needlessly narrow way in which the Third Circuit interpreted the Smith doctrine. As shown by the Lukumi case, decided by a unanimous Court only a few years after Smith, Smith does not have to be a wrecking ball for religious freedom.

First, it can clarify the meaning of general applicability. The City wants the Court to focus narrowly on one portion of the regulatory scheme (the evaluations of foster families by foster parenting organizations) and ask whether the City lets other agencies engage in precisely the same conduct as CSS but for nonreligious reasons. Whether the City has actually allowed a secular organization to exclude same-sex couples should not be the question: the question should be whether, under the terms of its policy, the City retains the right to make exceptions.

It is undisputed that the City carves out other exceptions from its nondiscrimination policy, for other foster-care organizations; moreover, there is a catch-all exceptions policy big enough to drive a truck through. In Smith, in its discussion of Sherbert, the Court made clear that regulatory schemes that allow case-by-case discretion are not “generally applicable.”

Second, the Court can clarify Smith‘s neutrality standard. At the beginning of this saga, CSS provided foster care services in Philadelphia (as it had for 200 years—long before the City became involved) and the City had no policy that would exclude CSS. Philadelphia politicians read in the newspaper that CSS holds a religious objection to approving same-sex and unmarried couples for its foster care program, and instructed City lawyers to find a way to exclude entities that discriminate “under the guise of religious freedom.” The City then proceeded to craft a policy that would have the effect of excluding CSS without interfering with the ability of other foster care agencies to operate out of compliance with other aspects of the anti-discrimination policy.

The logic of Smith is that policies that apply to all parties are not unconstitutional when they happen to conflict with one party’s religious exercise. That does not license governments to craft policies to exclude religious entities and exempt others.

[3.] Even if a City policy burdens the free exercise of religion, it might nonetheless be constitutional if it serves a compelling governmental purpose in the least restrictive way. (If a religion commanded child sacrifice, the government could prohibit the exercise of that belief.) It is not likely that the City’s policy would satisfy this demanding standard.

The principal justification for the City’s policy seems to be communicative in nature; it wishes to prevent the insult to same-sex couples that is implied by their exclusion from CSS’s program. But pure communicative impacts are a parlous ground for compelling governmental interests; people have a free speech right to express disapproval of conduct the state approves of.

More important are the material effects. If CSS were the only foster-care organization or if there were any evidence that same-sex couples were hindered by CSS’s policy (issues Justice Kavanaugh asked about), the City might well have an argument. But this is contrary to the facts of the case.

Indeed, the real effect of the City’s policy is to reduce the availability of foster placements for all children. As Hashim Mooppan. Counselor to the Solicitor General arguing in support of CSS, put it: “what the City has done is worse than cutting off its nose to spite its face. What it is doing is cutting off homes from the most vulnerable children in the City to spite the Catholic Church.”

[4.] Finally, I was surprised to hear some Justices give credence to a late-made argument by the City that attempts to sidestep the First Amendment issue. According to the argument, the City did not exclude CSS from the foster care program in an exercise of its regulatory power but merely refused to enter into a contract with it. Both Chief Justice Roberts and Justice Kagan asked about this argument.

It is not obvious that this would be a winner for the City even if the argument applied; after all, governments cannot violate the Constitution in their contracting capacity any more than their regulatory capacity. But a simpler answer is that the City has never claimed it was imposing the policy in a managerial capacity. It has said throughout this dispute that it is enforcing the Fair Practices Ordinance, which applies across the board to private and business conduct, and has nothing to do with contracting. If upheld, the City’s broad rule could be stretched to apply to religious schools, hospitals, and homeless shelters (as the City admitted at oral argument)—not just entities required to “contract” with the City.

More importantly, the City’s argument is misguided as a matter of principle. As Lori Windham pointed out on behalf of CSS, it would mean “the Free Exercise Clause [would] shrink every time the government expands its reach.” Justice Barrett also seized on this problem, pressing Neal Katyal, counsel for the City, with a hypothetical in which the government expanded its authority over healthcare and attempted to force Catholic hospitals as a condition of their contracts to provide abortions. Although Neal is a great litigator and friend, he had no good answer to this hypothetical. That is where the City’s position on contracting leads.

[5.] The broader significance of this case, as a cultural matter, is whether it will exacerbate the conflict between LGBT rights and religious freedom, or lower the temperature. Many—probably most—Americans who supported same-sex marriage did so on the assumption that it would get the government out of the business of restricting the ability of same-sex couples to act on the basis of their own consciences and identities when deciding whom to marry and how to live their lives. That victory is won.

But the terrain has now shifted. The question in cases like Fulton and Masterpiece is whether dissenters from that capacious understanding of marriage can be coerced into retreating from their position, or pretending to do so, on penalty of being ostracized from the public sphere. In my opinion, such coercion perpetuates controversy and unnecessarily enflames the culture wars. I hope the Court will bear that in mind.

from Latest – Reason.com https://ift.tt/3exlQGV

via IFTTT

TUESDAY, NOVEMBER 10

Free Speech & Election Law

Rule of Law, or Just Making it Up? First Amendment Tiered Scrutiny

11:00 a.m. – 12:15 p.m.

Prof. Ashutosh Bhagwat, Boochever and Bird Endowed Chair for the Study and Teaching of Freedom and Equality; Martin Luther King Jr. Professor of Law, University of California, Davis School of Law

Prof. Genevieve Lakier, Assistant Professor of Law, Herbert and Marjorie Fried Teaching Scholar, University of Chicago Law School

Prof. Nicholas Quinn Rosenkranz, Professor of Law, Georgetown University Law Center

Prof. Eugene Volokh, Gary T. Schwartz Distinguished Professor of Law, University of California, Los Angeles School of Law

Moderator: Hon. David R. Stras, United States Court of Appeals, Eighth Circuit

As is usual with the Federalist Society, we try to provide balance on these panels; we invited Prof. Bhagwat and Lakier (leading scholars, both of whose work I much admire) to provide the non-Federalist-Society perspective, whatever that might mean here—I expect Nick and I will agree with them on some matters, and disagree with them on others.

At a Libertarian convention years ago, one of the party’s candidates started saying, “When I’m president of the United States.” I chuckled and responded: “Well, that isn’t going to happen.” We all knew then—and know now—that the Libertarian Party (L.P.) candidate has zero chance of ever sitting behind the Resolute Desk.

After former New Mexico Gov. Gary Johnson won the L.P. nomination in 2016, libertarian activists thought it was their year to put the party on the map. Well, that was the view of those who weren’t mad about Johnson’s lack of ideological purity and his not-particularly-libertarian running mate, former Republican Bill Weld.

At the time, some optimism seemed warranted. The race pitted an enormously unpopular Democratic candidate against a vulgar Republican one, which—in theory, anyway—should have created a hunger for an experienced ticket offering sensible limited-government solutions.

After the ticket garnered 3.27 percent of the vote, I received a press release celebrating that accomplishment, which was a record-setting vote haul for the Libertarian Party. That was perhaps 47 percent and 270 electors short of making any difference, but such are the small victories that keep libertarians going. I remember when state party leaders celebrated their elected officials, with a member of a water board leading the show.

After Tuesday’s vote, Libertarian Party nominee Jo Jorgensen drew around 1 percent of the vote. It has nothing to do with her personality, which is pleasant, or her campaign, which seemed fine. This year’s election was a referendum on Donald Trump. The major parties have convinced the nation that this was the Most Important Election Ever—and the wrong outcome would lead America into (pick one) socialism or fascism. Why “waste” a vote?

My goal isn’t to dump on the L.P., even though it wouldn’t take much research to chronicle its long-running failures. The two major parties dominate the national discussion. They have put impediments in the way of third-party ballot and debate access. Although libertarianism has deep roots within the nation’s history, most Americans are not libertarians. That makes party building a tough row to hoe.

Democrats and Republicans have evolved largely into warring cultural tribes rather than vessels of ideological consistency. As government grows and both parties fight over who controls the levers of power, it’s harder to stay relevant with our less-is-more approach toward governance. It’s difficult even to get our policy ideas onto the national stage.

To make matters worse, libertarians have irreconcilable disagreements. Many libertarian colleagues despise the president and view him as a wannabe authoritarian, while others are convinced that he’s the most libertarian president in ages. In 2014, Jeffrey Tucker wrote about two main libertarian camps, which he termed “humanitarians” and “brutalists.”

The humanitarians believe in liberty because it “allows peaceful human cooperation” and “keeps violence at bay,” he argued. “It allows for capital formation and prosperity. It protects human rights of all against invasion. It allows human associations of all sorts to flourish on their own terms.”

By contrast, brutalists like liberty because “it allows people to assert their individual preferences, to form homogeneous tribes, to work out their biases in action, to ostracize people based on ‘politically incorrect’ standards.” It allows them “to hate to their heart’s content so long as no violence is used as a means, to shout down people based on their demographics or political opinions.” I call them “get off my lawn” libertarians.

I count myself among the humanitarians, but my point is the chasm between these self-identified libertarian groups is as deep as the one separating progressive Democrats from nationalist conservatives. It’s hard to build a national movement that resonates with the public when our own movement is bitterly divided.

The Orange County Register recently interviewed Jorgensen and came away impressed. In a pre-election editorial, the newspaper argued that she “deserves to be heard.” While her overall ideas were worthy of discussion, she had nothing illuminating to say in response to my question about how we, as libertarians, should proceed in our increasingly non-libertarian world.

I’ve long argued that libertarians should focus their politicking on the local level, at building a bottom-up rather than top-down movement. California’s city council and supervisor races are nonpartisan, which gives third-party candidates real opportunities to actually win office. We shouldn’t underestimate how much we can achieve at that level.

For instance, former Calimesa Mayor Jeff Hewitt, now a Riverside County supervisor, led the reform of his city’s fire department to reduce pension liabilities—something officials in the Orange County city of Placentia officials echoed. The legislature then passed a law halting such reforms out of fear that it would spread (and endanger union pay packages), but this was a testament to how much change one elected libertarian can accomplish.

A libertarian has again failed to become president or to even seriously be in the running. Perhaps libertarians have a more promising future if we spend less time worrying about national elections and more time championing our good ideas—and working politically at the local level.

This column was first published in The Orange County Register.

from Latest – Reason.com https://ift.tt/3l9eyf6

via IFTTT

In a venom filled online rant, Keith Olbermann called for President Trump to be dragged out of the White House immediately in handcuffs.

“TRUMP HAS LOST HIS MIND AND MUST BE REMOVED, TONIGHT,” Olbermann tweeted, along with the video of him ranting on his online program literally titled Olbermann vs Trump.

“The coup attempt, we can survive. A mentally incompetent president, we may not. Instead, he will stay, and when he concedes he will simultaneously begin a campaign for 2024.” Olbermann stated.

Olbermann called Trump “President Karen” and a “lame duck president.”

TRUMP MUST BE REMOVED AND ARRESTED, TONIGHT. Gripped by a paranoid delusion, threatening the nation’s safety, this can’t wait any longer. It won’t happen; in fact he’ll probably concede and instantly announce he’s running in ’24.

Full video: https://t.co/pCaCgZdkbr

Brief version: pic.twitter.com/MpVatbGepW

Here is the full 10 minute mental breakdown, for those who can stomach it:

President Trump vowed last night to take the matter of election theft to the highest court in the land, noting “We think there’ll be a lot of litigation, because we cannot have an election stolen like this.”

Once a respected newsreader who espoused nuanced positions including opposition to illegal invasions in the Middle East, Olbermann is now completely unhinged, engaging in endless ‘orange man bad’ rants.

Last month Olbermann said Trump should be executed over the handling of the coronavirus:

Keith Olbermann calls for Trump to get the death penalty, one for every COVID death. Unhinged. pic.twitter.com/8JbY0pPu7p

I’m delighted that Prof. McConnell—one of the top Religion Clauses scholars in the country—was willing to pass along some thoughts on the Fulton oral argument:

The Supreme Court heard oral argument Wednesday in Fulton v. City of Philadelphia, a case asking whether Philadelphia violated the Free Exercise Clause by excluding Catholic Social Services (CSS) from the array of private groups connecting children without families with willing foster homes, on the ground that CSS’s religious beliefs prevent it from certifying same-sex or unmarried couples who want to become foster parents. Not that that ever happened. No same-sex couples have ever tried to foster through CSS. And not that CSS’s beliefs have any real effect on such couples: they can foster through any number of other organizations. The only concrete consequence of the exclusion is to leave hundreds of children in Philadelphia without foster homes.

One of the questions presented in Fulton is whether the Court should “revisit” (meaning overrule) the Court’s much-criticized 1990 decision, Employment Division v. Smith, in which the Court allowed criminal prosecution of Native American Church practitioners for ingesting peyote, their sacramental substance. That decision, written by the late lamented Justice Antonin Scalia, has been criticized by multiple Justices over the years as well as by a host of academics (though the ideological valence of the critique has shifted from left to right over the ensuing decades). My views on Smith are no secret; Justice Scalia called me Smith‘s most prominent academic critic. I hope and expect that the Court will revisit the decision, which without benefit of briefing or argument drastically narrowed the First Amendment protection for free exercise of religion in the teeth of constitutional text and precedent and what I consider the strong weight of historical evidence of original understanding.

Alas, during Wednesday’s oral argument the Justices showed no serious interest in the merits or demerits of Smith. The reason is obvious: the Petitioner, CSS, led with the argument that it should prevail even under Smith. The new Justice, Amy Coney Barrett, whom most people assume is not a friend to the Smith decision, pointedly asked CSS’s counsel:

[Y]ou argue in your brief that Smith should be overruled. But you also say that you win even under Smith because this policy is neither generally applicable nor neutral. So, if you’re right about that, why should we even entertain the question whether to overrule Smith?

It is of course likely that some of the Justices will concur on the ground that Smith should be overruled. Is has been common the last few years for the Court to render narrow decisions in an early case, declining invitations to overrule precedent, and then to grab the bull by the horns in a subsequent decision. And it is likely that a minority of the Court will vote against CSS—though exactly on what legal ground it is hard to predict. Probably not the unpersuasive logic of the court below.

Assuming for sake of argument that the Court will not overrule Smith, what is it likely to do? There are two most likely paths.

[1.] The Court could render a narrow, fact-specific decision based on the evident hostility shown by Philadelphia toward CSS’s religious beliefs. For example, the City Council passed a resolution labeling CSS’s actions “discrimination that occurs under the guise of religious freedom.” The Commissioner told CSS that “times have changed,” “attitudes have changed,” and that it was “not 100 years ago,” and that its policy on foster families conflicts with the teaching of the Pope. The Court could conclude that this “hostility on the part of the State” fell below the minimum requirements of the Free Exercise Clause. I think of this path as “Masterpiece 2.0,” because it is very similar to the Court’s ruling in Masterpiece Cakeshop v. Colorado Civil Rights Commission, which rested on “religious hostility on the part of the State itself,” and specifically on “the Commission’s consideration of Phillips’ case,” which the Court held “was neither tolerant nor respectful of Phillips’ religious beliefs.”

But this path, like the path of overruling Smith, drew little attention at oral argument in Fulton. And for good reason. Masterpiece didn’t help reduce the temperature on gay rights and religious freedom. If anything, it raised it by suggesting to lower courts and the government that punishing those who hold a minority view on marriage is fine as long as the government does a better job of hiding its hostility—ensuring that more cases like these will keep coming.

In fact, Masterpiece didn’t even resolve the baker’s own case, as he was immediately targeted again after the Court ruled in his favor. More generally, I think there is little appetite on the Court for making the subjective motivations of government actors central to constitutional law. If the Court wanted to go down the path of emphasizing subjective motivations, it would have decided Trump v. Hawaii the other way.

[2.] The other path, much better than Masterpiece 2.0, would be to use the case to correct the needlessly narrow way in which the Third Circuit interpreted the Smith doctrine. As shown by the Lukumi case, decided by a unanimous Court only a few years after Smith, Smith does not have to be a wrecking ball for religious freedom.

First, it can clarify the meaning of general applicability. The City wants the Court to focus narrowly on one portion of the regulatory scheme (the evaluations of foster families by foster parenting organizations) and ask whether the City lets other agencies engage in precisely the same conduct as CSS but for nonreligious reasons. Whether the City has actually allowed a secular organization to exclude same-sex couples should not be the question: the question should be whether, under the terms of its policy, the City retains the right to make exceptions.

It is undisputed that the City carves out other exceptions from its nondiscrimination policy, for other foster-care organizations; moreover, there is a catch-all exceptions policy big enough to drive a truck through. In Smith, in its discussion of Sherbert, the Court made clear that regulatory schemes that allow case-by-case discretion are not “generally applicable.”

Second, the Court can clarify Smith‘s neutrality standard. At the beginning of this saga, CSS provided foster care services in Philadelphia (as it had for 200 years—long before the City became involved) and the City had no policy that would exclude CSS. Philadelphia politicians read in the newspaper that CSS holds a religious objection to approving same-sex and unmarried couples for its foster care program, and instructed City lawyers to find a way to exclude entities that discriminate “under the guise of religious freedom.” The City then proceeded to craft a policy that would have the effect of excluding CSS without interfering with the ability of other foster care agencies to operate out of compliance with other aspects of the anti-discrimination policy.

The logic of Smith is that policies that apply to all parties are not unconstitutional when they happen to conflict with one party’s religious exercise. That does not license governments to craft policies to exclude religious entities and exempt others.

[3.] Even if a City policy burdens the free exercise of religion, it might nonetheless be constitutional if it serves a compelling governmental purpose in the least restrictive way. (If a religion commanded child sacrifice, the government could prohibit the exercise of that belief.) It is not likely that the City’s policy would satisfy this demanding standard.

The principal justification for the City’s policy seems to be communicative in nature; it wishes to prevent the insult to same-sex couples that is implied by their exclusion from CSS’s program. But pure communicative impacts are a parlous ground for compelling governmental interests; people have a free speech right to express disapproval of conduct the state approves of.

More important are the material effects. If CSS were the only foster-care organization or if there were any evidence that same-sex couples were hindered by CSS’s policy (issues Justice Kavanaugh asked about), the City might well have an argument. But this is contrary to the facts of the case.

Indeed, the real effect of the City’s policy is to reduce the availability of foster placements for all children. As Hashim Mooppan. Counselor to the Solicitor General arguing in support of CSS, put it: “what the City has done is worse than cutting off its nose to spite its face. What it is doing is cutting off homes from the most vulnerable children in the City to spite the Catholic Church.”

[4.] Finally, I was surprised to hear some Justices give credence to a late-made argument by the City that attempts to sidestep the First Amendment issue. According to the argument, the City did not exclude CSS from the foster care program in an exercise of its regulatory power but merely refused to enter into a contract with it. Both Chief Justice Roberts and Justice Kagan asked about this argument.

It is not obvious that this would be a winner for the City even if the argument applied; after all, governments cannot violate the Constitution in their contracting capacity any more than their regulatory capacity. But a simpler answer is that the City has never claimed it was imposing the policy in a managerial capacity. It has said throughout this dispute that it is enforcing the Fair Practices Ordinance, which applies across the board to private and business conduct, and has nothing to do with contracting. If upheld, the City’s broad rule could be stretched to apply to religious schools, hospitals, and homeless shelters (as the City admitted at oral argument)—not just entities required to “contract” with the City.

More importantly, the City’s argument is misguided as a matter of principle. As Lori Windham pointed out on behalf of CSS, it would mean “the Free Exercise Clause [would] shrink every time the government expands its reach.” Justice Barrett also seized on this problem, pressing Neal Katyal, counsel for the City, with a hypothetical in which the government expanded its authority over healthcare and attempted to force Catholic hospitals as a condition of their contracts to provide abortions. Although Neal is a great litigator and friend, he had no good answer to this hypothetical. That is where the City’s position on contracting leads.

[5.] The broader significance of this case, as a cultural matter, is whether it will exacerbate the conflict between LGBT rights and religious freedom, or lower the temperature. Many—probably most—Americans who supported same-sex marriage did so on the assumption that it would get the government out of the business of restricting the ability of same-sex couples to act on the basis of their own consciences and identities when deciding whom to marry and how to live their lives. That victory is won.

But the terrain has now shifted. The question in cases like Fulton and Masterpiece is whether dissenters from that capacious understanding of marriage can be coerced into retreating from their position, or pretending to do so, on penalty of being ostracized from the public sphere. In my opinion, such coercion perpetuates controversy and unnecessarily enflames the culture wars. I hope the Court will bear that in mind.

from Latest – Reason.com https://ift.tt/3exlQGV

via IFTTT

TUESDAY, NOVEMBER 10

Free Speech & Election Law

Rule of Law, or Just Making it Up? First Amendment Tiered Scrutiny

11:00 a.m. – 12:15 p.m.

Prof. Ashutosh Bhagwat, Boochever and Bird Endowed Chair for the Study and Teaching of Freedom and Equality; Martin Luther King Jr. Professor of Law, University of California, Davis School of Law

Prof. Genevieve Lakier, Assistant Professor of Law, Herbert and Marjorie Fried Teaching Scholar, University of Chicago Law School

Prof. Nicholas Quinn Rosenkranz, Professor of Law, Georgetown University Law Center

Prof. Eugene Volokh, Gary T. Schwartz Distinguished Professor of Law, University of California, Los Angeles School of Law

Moderator: Hon. David R. Stras, United States Court of Appeals, Eighth Circuit

As is usual with the Federalist Society, we try to provide balance on these panels; we invited Prof. Bhagwat and Lakier (leading scholars, both of whose work I much admire) to provide the non-Federalist-Society perspective, whatever that might mean here—I expect Nick and I will agree with them on some matters, and disagree with them on others.

Futures Drop, Record November Rally Fizzles As Election Gets Increasingly Contested Tyler Durden

Fri, 11/06/2020 – 08:01

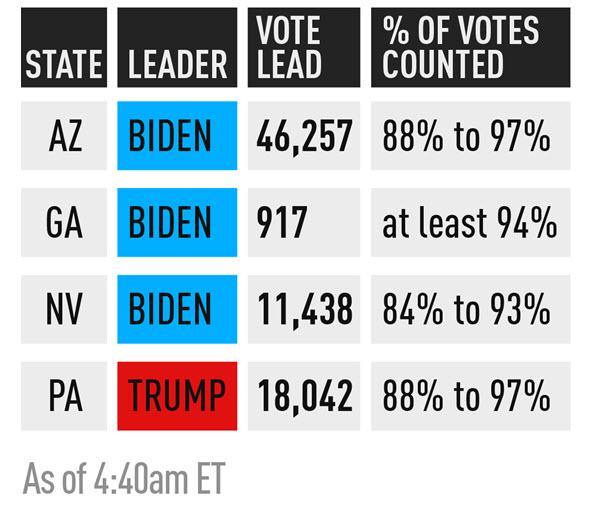

The blistering November rally, which pushed the S&P higher by nearly 8% in the first 4 days of the month, the biggest advance in the first days of the month on record, finally reversed and pared some of this week’s gains as the vote count continued but got increasingly more contested amid mounting legal complaints from President Donald Trump’s campaign. Meanwhile, just around 4am, Joe Biden edged ahead of Donald Trump in the latest batch of Georgia results, a major shift in the Republican stronghold that hasn’t backed a Democrat for president since 1992. Biden also got closer in Pennsylvania and is still ahead in Nevada and Arizona, though Trump is catching up.

S&P futures slid 25 points, or 0.7%, to 3,480 while global stocks were in the red but near all-time highs ahead of what some expect will be a downbeat jobs report underlining the scale of the economic challenge awaiting America’s next president (full preview here).

The dollar and U.S. bond yields remained subdued on Friday amid a “bullish” reversal in Blue Wave expectations according to which a divided Congress – previously seen as a doomsday scenario – would limit fiscal stimulus which would pave the way for even more central bank stimulus.

MSCI’s all-country index was fractionally red after gains earlier in the week, still close to the record reached in September. At 730 a.m. ET, Dow e-minis were down 171 points, or 0.6%, S&P 500 e-minis were down 24.5 points, or 0.7%, and Nasdaq 100 e-minis were down 127 points, or 1.1%. Tech mega-caps including the FAAMGs fell about a percent in premarket trading after logging strong gains this week. The drop follows the Fed’s Thursday announcement keeping its loose monetary policy intact and again pledging to do whatever it can to sustain an economy crippled by the COVID-19 pandemic. Cannabis-related stocks, which have been identified by analysts as potential winners under a Biden administration, were among the rare gainers in early premarket trading.

“It’s not that the market is expecting something dramatic to happen, but just de-risking after a strong performance,” said Ingo Schachel, head of equity research at Commerzbank in Germany.

Despite today’s soggy moody, the S&P 500 is on course for its best week since April, while the tech-heavy Nasdaq has jumped 6.5% since the Nov. 3 election as the prospect of a policy gridlock in Washington eased worries about tighter regulations on companies.

“From here, we believe the impact of the presidential result should be relatively small,” said Lars Kreckel, global equity strategist at LGIM. “Whether Biden or Trump are in the White House, governing with a Congress that is very likely to be divided would be difficult and mean very little policy that could significantly move equity markets would be passed.”

And with Biden having taken the lead in Georgia, absent a remarkable reversal of results in the courts, risk sentiment was also underpinned by a sense that a Biden presidency would be more predictable than Trump’s even though investors saw no quick rapprochement between the United States and China on trade and other issues.

Biden had a 253 to 214 lead in the state-by-state Electoral College vote that determines the winner, according to most major television networks, putting him closer to the 270 Electoral College votes needed to win. In Pennsylvania, which has 20 electoral votes, Biden cut Trump’s lead to just over 18,000 by the early hours of Friday. Shortly after 4am, Biden also went ahead in Georgia, which has 16 electoral votes, leading by some 900 votes.

“The market reaction to the unfolding election news suggests that financial markets would prefer to see a constrained Biden presidency,” said Paul O’Connor, head of multi-asset at Janus Henderson Investors. “The economic backdrop to this election is one of an incomplete global recovery that remains threatened by the continued spread of Covid-19 in many major economies as well as fast-fading fiscal support measures.“

Matt Sherwood, head of investment strategy at Perpetual in Sydney, said markets had already moved to price in a Biden presidency and a divided Congress: “We can get all of the good things about a Biden presidency, such as stable leadership and foreign policy, without any of the bad things from the far Left of his party, such as taxation,” he said.

Europe’s Stoxx 600 opened 0.4% lower, with investor sentiment dimmed by the economic toll of new lockdowns in Europe to contain the coronavirus. Italy and France registered record numbers of COVID-19 cases. Deutsche Lufthansa fell 7% amid a resurgence in coronavirus cases. IT services firm Netcompany slumped more than 6% after a downbeat earnings report. On the plus side, luxury goods maker Richemont surged as much as 12% after sales rebounded in China.

Earlier in the session, Asian stocks gained, led by the energy and materials sectors as MSCI’s index of Asian Pacific shares ex-Japan rising 0.3%, near a three-year high. Most markets in the region were up, with Indonesia’s Jakarta Composite advancing 1.4% and India’s S&P BSE Sensex Index rising 1.2%, while China’s Shanghai Composite slid 0.2%. Trading volume for MSCI Asia Pacific Index members was 27% above the monthly average for this time of the day. The Topix added 0.5%, with Daikin and Kubota contributing the most to the move. Japan’s Nikkei average rose 0.9% to a 29-year high while. The Shanghai Composite Index retreated 0.2%, driven by China Life and Kweichow Moutai

On the covid front, the US became the first country to top 100,000 coronavirus infections in a single day, with Fed Chair Powell warning that mounting infection rates are a risk to the recovery. Meanwhile, France warned of a “violent” second wave as it joined European countries including Italy and Poland in reporting new highs in daily infections.

The Labor Department’s closely watched report is likely to show U.S. employers hired the fewest workers in five months in October in the absence of new fiscal stimulus and as COVID-19 infections surged.

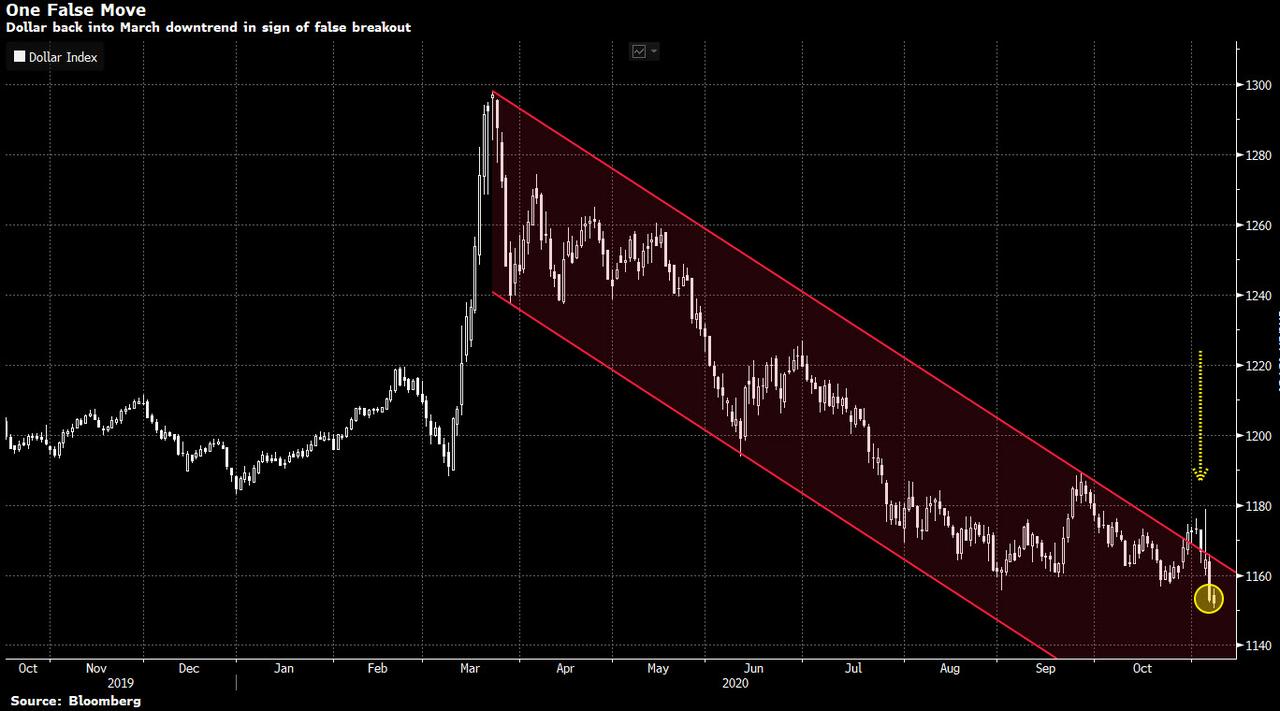

In FX, the Bloomberg Dollar Spot Index extended declines to the lowest since May 2018 as investors waited on results from narrowing vote races in key U.S. battleground states.

The dollar traded mixed versus Group-of-10 peers; the euro climbed for the fourth day, rising past $1.1850. The New Zealand dollar led G-10 gains on the back of an improved reading on the nation’s inflation expectations, while the Aussie weakened as trade tensions with China hurt sentiment. The pound fluctuated between modest gains and losses, as optimism that a Brexit trade deal will be reached offset concern over the negative impact of a nationwide lockdown. The yen hovered near the strongest level since March after breaching a key chart level from 2016 that had only been broken in March in the years since.

U.S. bond yields drifted lower, with the 10-year Treasury yield falling to 0.773%, below the pre-U.S. election level on Tuesday. It had struck a three-week low of 0.7180% on Thursday.

Elsewhere, crude oil declined and gold edged higher. Emerging-market stocks were on track for a fifth day of gains.

Looking at the day ahead, the US jobs report is likely to be the data highlight, but there’ll also be the Canadian employment report for October, along with German industrial production and Italian retail sales for September. From central banks, we’ll hear from Bank of Canada Governor Macklem and the ECB’s Holzmann.

Market Snapshot

S&P 500 futures down 1.2% to 3,461.75

STOXX Europe 600 down 0.6% to 365.10

German 10Y yield fell 0.8 bps to -0.645%

Euro up 0.2% to $1.1848

Italian 10Y yield fell 2.0 bps to 0.556%

Spanish 10Y yield fell 0.3 bps to 0.088%

MXAP up 0.5% to 181.98

MXAPJ up 0.4% to 603.59

Nikkei up 0.9% to 24,325.23

Topix up 0.5% to 1,658.49

Hang Seng Index up 0.07% to 25,712.97

Shanghai Composite down 0.2% to 3,312.16

Sensex up 1.3% to 41,874.76

Australia S&P/ASX 200 up 0.8% to 6,190.18

Kospi up 0.1% to 2,416.50

Brent futures down 2.4% to $39.97/bbl

Gold spot little changed at $1,947.97

U.S. Dollar Index little changed at 92.45

A quick look at global markets courtesy of NewsSquawk

Asian equity markets traded mixed with the region only partially sustaining the momentum from Wall Street where the post-election rally persisted despite no declared winner yet, although Biden does remain on the cusp with 6 electoral votes shy of victory at 264 votes vs. President Trump at 214 votes. The key states still to be declared include Nevada (6 votes), Georgia (16 votes), North Carolina (15 votes) and Pennsylvania (20 votes) with Biden leading in Nevada, while the former VP dramatically caught up with President Trump in Georgia and narrowed the gap in Pennsylvania. ASX 200 (+0.8%) was lifted by strength in mining names and as financials were kept afloat, with the largest-weighted sector and shares in Macquarie unfazed by the slump in the latter’s H1 earnings, while Nikkei 225 (+1.0%) extended on gains to breach October 2018 highs and briefly print its best levels in nearly 3 decades with slight encouragement from better than expected household spending. Conversely, Hang Seng (-+0.1%) and Shanghai Comp. (-0.2%) lagged after the PBoC refrained from open market operations which resulted to a net daily drain of CNY 100bln and weekly drain of CNY 590bln, while the central bank also set the strongest currency fix in more than 2 years. Finally, 10yr JGBs were flat as prices took a breather from the mid-week surge to above the 152.00 level and with further upside capped by the gains in stocks and mixed results at the 10yr inflation-indexed JGB auction.

Top Asian News

China Starts Thinking About Stimulus Exit as Economy Recovers

World’s Largest Pension Fund Gains With Assets Near Record

Japan’s Households Raise Quarterly Spending by Most Since 2000

Yuan Is Halfway Through Erasing Losses Since Trade War Began

Equities across Europe trade lower across the board (Euro Stoxx 50 -0.6%), albeit off worst levels following a mixed APAC session as sentiment deteriorates throughout the European morning – with the US Presidential race winner still undeclared but tilting further towards Biden. The latest update from some poll-watchers suggested a blue flip in the state of Georgia with over 99% of votes tallied. Assuming this tally corresponds with the final outcome for Georgia (16 EC votes) and if Arizona (11 EC votes) is awarded to Biden (as some desks have), this would place the Democratic candidate on 280 votes and thus surpassing the 270 required for Presidency. However, if you omit Arizona, then Biden would be on 269 electoral college votes. As a reminder, officials in the state have remarked that it could be several weeks before we get a final result given how close the race is regarding Georgia. Meanwhile, the latest implied probabilities from Betfair Exchange point to a +90% chance of a Biden victory. Elsewhere, the Senate rate remains neck and neck as each side clutch 48 seats, with 4 still hanging in the balance. US equity futures (ES -0.8%, NQ -1.2%, YM -0.6%, RTY -0.5%) have been drifting lower since European players entered the fray, with traders also weighing a contested outcome as Trump continues to condemn the legitimacy of the voting system. Back to Europe, the region conforms to the risk aversion as bourses extended on the downside seen at the cash open, whilst losses remain relatively broad-based across. Sectors are now all in the red after a mixed open, with Travel & Leisure at the bottom of the pile as it continues to bear the brunt of COVID-related lockdown measures, with IAG’s (-1.8%) British Airways also cancelling all flights from Gatwick airport for the month amid England’s restrictions. Meanwhile, losses in the Telecoms sectors are cushioned on the back of stellar earnings from T-Mobile (+6.4% pre-mkt) which in turn bolstered its majority shareholder Deutsche Telekom (+2.4%), who owns some 43.5% of TMUS. The insurance sector is also faring better than some of its peers as Allianz (+0.1%) rose post-earnings, but the stock has waned off highs. Other earnings-related movers include Richemont (+8.3%) who saw a positive trend in Q2 following the sharp decline in the prior month, in turn supporting its peer Swatch (+1.0%).

Top European News

German Industrial Production Rose for Fifth Month in September

EU’s Green Bonds Set to Preempt Rules That Will Govern Them

Novo Nordisk Agrees to Buy Emisphere in $1.8 Billion Deal

U.K. House Prices Climb Most Since 2016 Ahead of New Lockdown

In FX, the Kiwi is consolidating recent gains in the high 0.6700 zone vs its US counterpart and has peered just above 0.6800 in wake of an uptick in NZ Q4 inflation expectations overnight, but the Nzd is also benefiting from tailwinds via the Aussie cross amidst more angst between China and its Antipodean neighbour on the trade front. Indeed, Aud/Nzd has retreated to test 1.0700 from around 1.0760 at one stage and Aud/Usd is losing momentum have topped out a few pips over 0.7280 despite another firm PBoC Cny fix. For the record, the RBA’s SOMP merely underscored dovish guidance that came alongside Tuesday’s multi-pronged policy stimulus, so hardly impacted.

USD – Little respite for the Dollar or reprieve from the FOMC, as the wait to see final results of the US Presidential Election continues. In fact, the DXY has slipped into another lower range even though several major peers are losing momentum independently or in line with a downturn in broad risk sentiment. The index has bounced off worst levels within a 92.823-435 range, and perhaps looking idle sideways into NFP unless any of the last remaining states declare and push front-runner Biden technically through the tape.

CAD/GBP – The Loonie has lost traction from oil, but retaining grip of the 1.3000 handle vs its US rival in the run up to Canadian jobs data, but the Pound appears a bit more precarious above 1.3100 given latest Brexit updates from EU chief negotiator Barnier effectively laying the blame for no progress on fishing or the LPF at the UK’s door.

EUR/CHF/JPY – All firmer against the Buck, with the Euro still within striking distance of a cluster of late October peaks that stand in the way of last month’s apex circa 1.1880, while the Franc is hovering just shy of 0.9000 and Yen has accelerated beyond 103.50 following firmer than forecast Japanese household spending data and somewhat dismissive rhetoric from PM Suga on exchange rates aside from expressing the importance of stability.

SCANDI/EM – Collapsing crude prices and contagion in stocks, or vice-versa are obvious factors behind a rebound in Eur/Nok through 10.9000, but a fall in Norwegian manufacturing output hot on the heels of yesterday’s downbeat Norges Bank economic outlook is also weighing on the Crown. Elsewhere, the Rub is also weaker alongside Brent that has slipped under Usd 40/brl, but the Try is not gleaning any comfort from cheaper oil at all.

RBA Statement on Monetary Policy noted the board is prepared to expand bond buying if required and that it is not contemplating further lowering rates with little to be gained from moving to negative rates. Furthermore, it committed to not increase rates until inflation is sustainably in 2%-3% target band, Furthermore, it sees GDP Y/Y growth at -4% in Q4 2020, +5% in Q4 2021 and +4% in Q4 2022, while it sees Trimmed Mean CPI Y/Y at 1% in Q4 2020, 1% in Q4 2021 and 1.5% in Q4 2022. (Newswires)

In commodities, WTI and Brent front-month futures post losses in tandem with the overall sentiment across the market and with complex-specific news flow on the lighter side. Again, price action throughout the day is likely to be dictated by macro-themes in the absence of OPEC/OPEC+ updates as producers continue to balance supply and demand risks heading into a crucial month for the members. Consensus thus far points to an extension of current cuts through Q1 21, with some murmurs of deeper cuts, albeit this has not been agreed on nor confirmed by ministers. WTI Dec loses ground below USD 38/bbl (vs. high 38.61/bbl) while Brent Jan yielded the USD 40/bbl handle (vs. high 40.70/bbl). Elsewhere, spot gold and silver drift off worst levels on the back of a softer Buck, with the former now north of 1950/oz to the upside after climbing from a low of ~1935/oz, whilst spot silver gains ground above USD 25.50/oz. The softer Dollar has also benefitted LME copper, which remains around session highs heading into the US open.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 592,500, prior 661,000

Change in Private Payrolls, est. 685,000, prior 877,000

Change in Manufact. Payrolls, est. 55,000, prior 66,000

Unemployment Rate, est. 7.6%, prior 7.9%

Average Hourly Earnings MoM, est. 0.2%, prior 0.1%

Average Hourly Earnings YoY, est. 4.5%, prior 4.7%

Average Weekly Hours All Employees, est. 34.7, prior 34.7

Labor Force Participation Rate, est. 61.5%, prior 61.4%

Underemployment Rate, prior 12.8%

10am: Wholesale Inventories MoM, est. -0.1%, prior -0.1%; Wholesale Trade Sales MoM, est. 1.05%, prior 1.4%

3pm: Consumer Credit, est. $7.75b, prior $7.22b deficit

Top Overnight news from Bloomberg

The hard-fought presidential contest between Donald Trump and Joe Biden now depends on the outcomes of a handful of states, each with varying rules on counting votes and contesting results — delaying the declaration of a winner

The Justice Department is looking into allegations by President Donald Trump’s campaign of voter fraud in Nevada. Democratic nominee Joe Biden is closing in on the 270 electoral votes he needs to win the presidency, while Trump’s path to re-election has narrowed

U.K. house prices climbed the most since 2016 last month, pushing average values to a record ahead of the renewed restrictions to contain coronavirus

The U.K. is imposing a two-week quarantine on travelers from Denmark, following an outbreak of a rare mutation of Covid-19 in the Nordic country’s mink farms

The Bank of England and U.K. Treasury are both investigating a possible leak detailing the central bank’s plans to expand its bond buying by a surprising amount

Hard-pressed commodity traders will get no respite at all next week as the U.S. electoral drama plays out ahead of a very busy agenda. There’ll be key insights into energy markets, a raft of top central bank speakers, and the latest on crop markets just as foodstuffs stage a powerful rally. The backdrop is the rapidly escalating coronavirus pandemic

DB’s Jim Reid concludes the overnight wrap

On the third day of counting votes we saw Joe Biden continue to close the gap in Pennsylvania, now trailing President Trump by 0.6% with 6% of the vote to go. Yesterday at the same time Biden trailed by 3%, with 11% of the vote left to be counted. That vote continues to come from predominately Democratic counties and is almost entirely mail-in votes which Democratic voters favoured. A win in Pennsylvania would give Mr Biden over 270 electoral college votes and clinch the presidency, regardless of the outcomes in other states. We’re not sure if they’ll stop the count overnight but if not at this run rate Biden could be in front by around 8am London time and effectively called as the new President.

Biden has also made up ground in Georgia, where yesterday he was behind by 0.6% with 5% uncounted, he now is essentially tied – less than 0.1% behind – with under 2% of the vote to go. It is going to be very tight and likely go to a recount. Nevada drifted toward Biden as well with his lead moving from 0.6% to 0.9% in the last day, though 11% of the vote is still remaining and there may not be a full count until the end of the weekend. There was no movement from North Carolina but most continue to expect President Trump to carry the state. Lastly there was some positive movement for President Trump, who was down 3% to Biden in Arizona yesterday and has closed to within 1.5% as of now.

On the Senate front, we learned that the second Georgia Senate seat will go to a runoff in January. This means that both senate seats in that state will be in play on January 5th. While Republican candidates likely come in as slight favourites into those races, the Democrats could be competitive. Also without President Trump or Mr Biden at the top of the ticket there may be a very different level of voter enthusiasm and turnout. Either way they are likely to be heavily competitive and expensive Senate races as Democrats will see it as an outside shot at getting slim control of the Senate (50:50 with VP breaking the tie) if Mr Biden wins the presidency.

Back to normal life and yesterday’s Fed meeting received the lowest amount of fanfare in quite some time as attention remained on the election counts. The FOMC kept the fed funds target rate at 0-0.25%, where it’s been since March, while maintaining their bond purchases at $120bn per month. For a second meeting in a row, Fed Chair Powell stressed the need for further fiscal stimulus. “I think we’ll have a stronger recovery if we can just get at least some more fiscal support,” Powell said in the ensuing press conference. He also noted that the recent rise in covid-19 cases both domestically and abroad represent risks to the economic outlook over the medium term. Notably, market participants were clearly focused on the election count as there was little market movement on the back of the release and presser.

Against this backdrop, global equity markets continued to surge, with the S&P 500 up another +1.95% and to a 3-week high, while the VIX fell by a further -2.0pts to bring its decline since the start of the week to over 9pts (now 27.6). It was a similar story in Europe too, where the STOXX 600 climbed +1.05% with the DAX (+1.98%) and the CAC 40 (+1.24%) also seeing major advances. Over in sovereign bond markets, US Treasuries pared back early gains as 10yr yields closed flat at 0.763%, while in Europe, yields on 10yr bunds (+0.1bps) and gilts (+2.7bps) also moved higher. And in FX, the dollar continued to weaken, with the dollar index falling -0.94% in its worst day since July.

Overnight in Asia the rally has run out of a bit of steam with futures on the S&P 500 and Nasdaq down -0.61% and -1.08% respectively. Other markets are also largely trading lower outside of the Nikkei which is up +0.97%. The Hang Seng (-0.25%), Shanghai Comp (-0.75%) and Kospi (-0.13%) are all down. Elsewhere, crude oil prices are down c.-2.50%. In other news, the Daily Mail has reported that Russian President Putin could quit in January amidst reports that he has Parkinson’s disease.

Though it’s likely to get a lot less attention than usual thanks to the election, we do have the US jobs report for October coming out later. Our US economists expect that nonfarm payrolls will rise by +600k, which would imply ongoing improvements in the labour market, but also be the slowest pace of job growth since the labour market recovery began in May. That should also lower the unemployment rate down to a post-pandemic low of 7.7%.

Back on central banks, the Bank of England’s MPC voted unanimously to increase their asset purchases by a further £150bn, which was above the consensus expectation for an extra £100bn, and left Bank Rate unchanged at 0.1%. Our UK economists (link here) say that the policy statement was “undoubtedly dovish”, with lower growth forecasts and stronger language on forward guidance. Indeed in the BoE’s Monetary Policy Report that was also released yesterday, they forecasted a contraction in Q4 GDP, which comes as the UK entered its second lockdown yesterday, with non-essential shops along with bars and restaurants closed once again. Oh and Golf Courses! In response to the new lockdown, Chancellor Sunak also unveiled further support for affected workers, with the furlough scheme extended until the end of March, which pays workers 80% of their salary for hours not worked.

On the coronavirus, it was announced that a national lockdown would be imposed in Greece for 3 weeks starting Saturday morning in response to rising case numbers. As part of this, primary schools would remain open, but secondary schools would close. Elsewhere, a number of other European countries reported record case numbers, including France, Italy, Poland, Austria and Romania. France’s health minister said that Covid-19 patients now account for more than 85% of French hospitals’ initial intensive-care capacity. The US saw another record number of daily infections at 126,210 in the past 24 hours with Illinois, Ohio and Michigan reporting record number of new cases amongst other states, Ohio’s governor has called state’s numbers as “shockingly high.” Meanwhile, New York state reported a positivity rate of 1.86% on Wednesday, the highest since June. Across the other side of world, Japan recorded 1046 cases yesterday the highest since August. Hokkaido, the prefecture which is seeing the most number of cases is planning to raise its coronavirus alert as soon as tomorrow and will reportedly ask restaurants in the nightlife district of Susukino to close at 10 pm.

Looking at yesterday’s data, German factory orders for September grew by a smaller-than-expected +0.5% (vs. +2.0% expected), while Euro Area retail sales in September also fell by a more-than-expected -2.0% (vs. -1.5% expected). The figures came as the European Commission’s autumn economic forecast projected a smaller economic contraction this year of -7.8% for the Euro Area (vs. -8.7% in the summer), though they revised down their 2021 forecast to +4.2% (vs. +6.1% previously). Meanwhile in the US, the weekly initial jobless claims for the week through October 31 fell to 751k (vs. 735k expected), down from an upwardly revised 758k the previous week. The continuing claims reading for the week through October 24 also fell to 7.285m, which is a post-pandemic low.

To the day ahead now, and the aforementioned US jobs report is likely to be the data highlight, but there’ll also be the Canadian employment report for October, along with German industrial production and Italian retail sales for September. From central banks, we’ll hear from Bank of Canada Governor Macklem and the ECB’s Holzmann.

via ZeroHedge News https://ift.tt/2I83fFl Tyler Durden

{kind=link}