CA Officials Topple Giant ‘TRUMP’ Sign Overlooking 405 Freeway, Citing ‘Life And Safety Hazard’ Tyler Durden

Wed, 10/07/2020 – 14:22

California officials were so triggered after someone erected a giant “TRUMP” sign on a hillside overlooking a Los Angeles freeway, that they promptly removed it from the private property within two hours of a caller reporting it.

The sign, visible on the hills near the Sepulveda Pass as Los Angeles drivers began their Tuesday commute, was first reported just before 7 a.m. by a driver who “was apparently concerned it could spark a blaze” after the state’s history of “destructive brush fires in the past few years.”

As such, the CA Highway Patrol noted the sign as a “traffic hazard” as drivers began to decelerate to take photos of the sign.

By 9 a.m., the sign was taken down by the California Department of Transportation (Caltrans), which entered private property and “laid it down so it wasn’t a visual distraction.” (h/t The Federalist).

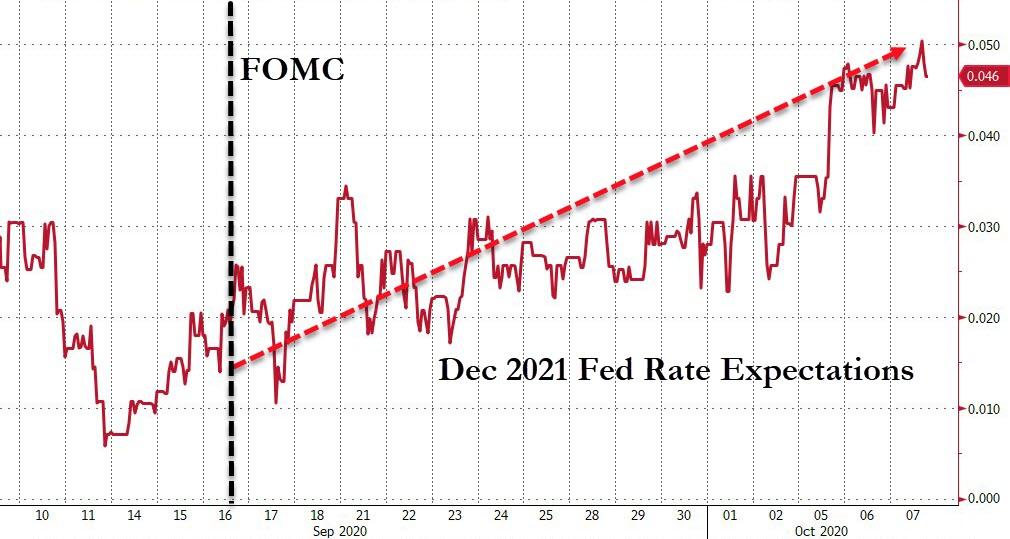

FOMC Minutes Show Fed Assumed More Fiscal Aid In 2020, “Some” See Need To Revise QE In The Future Tyler Durden

Wed, 10/07/2020 – 14:10

Since the last FOMC meeting on Sept 16th, gold has been the biggest loser while the USD managed modest gains…

Source: Bloomberg

Of course, the very modest gain in stocks was thanks to a huge short-squeeze…

Source: Bloomberg

Interestingly, despite The Fed promising that rates are on hold for pretty much ever, the market’s expectations for Dec 2021 have shifted hawkishly higher…

Source: Bloomberg

And real yields have risen significantly…

Source: Bloomberg

As we noted earlier, while the Minutes will likely reinforce the recent run of Fed commentary (more fiscal stimulus needed, uncertainties ahead, rates not going anywhere any time soon, etc) the market will be paying particular attention to any remarks on the Fed’s QE purchases, especially since the chances of fiscal help (and thus Treasury supply that would need to be monetized by The Fed) has all but evaporated.

Also, as a reminder, the meeting was unusually contentious with two dissents (one dovish – Kashkari, one hawkish – Kaplan).

One critical item in these minutes will be to see how reliant the Fed’s forecasts were on fiscal stimulus given the news in the last 24 hours on that front.

Reaffirming the lower-forever rates forecast, minutes show Fed officials laid out a three-part test that must be met before they consider lifting short-term rates from near zero.

First, they need to be satisfied that labor-market conditions meet their maximum employment goals, which weren’t spelled out.

Second, inflation must reach 2%.

Third, they will need some evidence—from forecasts or market-based measures—that inflation will continue to run moderately above 2%.

So essentially the “no change until at least 2023” takeaway that most had from the Fed decision last month isn’t set in stone.

“Participants generally noted that outcome-based forward guidance for the federal funds rate of this type was not an unconditional commitment to a particular path. Indeed, outcome-based guidance of this type would allow the public to infer changes in the Committee’s assessment of how long the target range for the federal funds rate would remain at its current setting.”

Additionally, and most notably, given ZIRP forever, some participants also noted that in future meetings it would be appropriate to further assess and communicate how the Committee’s asset purchase program could best support the achievement of the Committee’s maximum employment and price-stability goals.

Regarding asset purchases, participants judged that it would be appropriate over coming months for the Federal Reserve to increase its holdings of Treasury securities and agency MBS at least at the current pace. These actions would continue to help sustain smooth market functioning and would continue to help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

Most ominously, Fed staff and many officials forecasts did indeed assume some more fiscal aid in 2020.

The staff’s forecast assumed the enactment of some additional fiscal policy support this year; without that additional policy action, the pace of the economic recovery would likely be slower.

On bubble fears:

“a couple of participants indicated that highly accommodative financial market conditions could lead to excessive risk-taking and to a buildup of financial imbalances.”

With regard to COVID:

“In the staff’s medium-term projection, the baseline assumptions included that the current restrictions on social interactions and business operations, along with voluntary social distancing by individuals and firms, would ease gradually through next year.“

On Inflation:

“While the outlook for inflation was viewed as highly uncertain, a number of participants projected that inflation would run below the Committee’s 2 percent longer-run objective for a significant period before moving moderately above 2 percent for some time—consistent with the Committee’s revised consensus statement.

Participants still generally judged that the overall effect of the pandemic on prices was disinflationary.”

On Employment:

“The gains in employment over July and August were generally seen as larger than anticipated. Participants judged, however, that the labor market was a long way from being fully recovered.

They generally agreed that prospects for a further substantial improvement in the labor market would depend on a broad and sustained reopening of businesses, which in turn would depend importantly on how safe individuals felt to reengage in a wide range of activities.

Some participants noted that the majority of gains in employment so far reflected workers on temporary layoffs returning to work. These participants judged it as less likely for future job gains to continue at their recent pace, because a greater share of the remaining layoffs might become permanent.

Workers facing permanent layoffs were seen as more likely to need to find new jobs in different industries, and this process could take time, especially to the extent that these workers needed to be retrained.“

The Fed has suddenly become more ‘woke’ than normal, worrying about the effect of the pandemic lockdowns on minority workers:

“Participants observed that lower-paid workers had been disproportionally affected by the economic effects of the pandemic. Many of these workers were employed in the service sector or other industries most adversely affected by social-distancing measures.

With a disproportionate share of service-sector jobs held by African Americans, Hispanics, and women, these groups were seen as being especially hard hit by the economic hardships caused by the pandemic.

Participants viewed fiscal support from the CARES Act as having been very important in bolstering the financial situations of millions of families, and a number of participants judged that the absence of further fiscal support would exacerbate economic hardships in minority and lower-income communities.

In addition, several participants observed that the effects of the pandemic were disrupting the supply of labor because of the need to care for children, many of whom were attending school virtually from home.”

And finally, The Fed discovers the perils of ‘reflexivity’:

“Information pointing to a weaker outlook for the economy and inflation would tend to lead to public expectations for a longer period at the current setting of the target range while information suggesting a stronger outlook for the economy and inflation would tend to lead to expectations for a shorter period at the current setting.”

* * *

Full FOMC Minutes below:

via ZeroHedge News https://ift.tt/2I6fYZg Tyler Durden

The news, as it tends to be, has been dominated by President Donald Trump over the last several days, perhaps even more so with his recent COVID-19 diagnosis, which means one recent Trump tidbit largely flew under the radar: his requirement that billions of dollars in food aid packages for the needy arrive in tandem with a letter signed by him.

“As President, safeguarding the health and well-being of our citizens is one of my highest priorities,” the letter reads, referencing the U.S. Department of Agriculture’s $4 billion Farmers to Families Food Box Program. The initiative has purchased food typically bought by restaurants and rerouted it toward poor families, with over 100 million boxes sent since May. “As part of our response to the coronavirus, I prioritized sending nutritious food from our farmers to families in need throughout America.”

Reactions have not been uniformly positive, with some characterizing the letter as an overtly politicized election stunt. “In my 30 years of doing this work, I’ve never seen something this egregious,” Lisa Hamler-Fugitt, executive director of the Ohio Association of Food Banks, toldPolitico. “These are federally purchased boxes.”

Some food banks have begun removing the letters. Meanwhile, several people appear to be receiving the aid and corresponding letter even though they aren’t underserved. “Why would someone receiving this really need to know this?” said Matthew Killen of Miami Beach, who is not in need but received a package of food on his doorstep, according to The Miami Herald. He lives in a majority Hispanic neighborhood, which he feels the administration “targeted” so Trump could “win [the] area.”

Readers might remember a string of similar criticisms leveled at former President Barack Obama during the 2012 election after the “Obamaphone” video went viral. “Everybody in Cleveland—low, minority—got Obamaphones,” says a woman who had shown up to protest at a Mitt Romney rally. “Keep Obama in president [sic]. He gave us a phone. He’s gonna do more.”

In reality, that controversy was a farce. Under the spotlight was the Lifeline program, which provides subsidies for communications to eligible low-income recipients. The catch: It was implemented in 1985 during the Reagan administration, and the Obama administration had sought to reform what was seen as a program plagued by massive fraud. The changes reportedly saved $213 million.

That didn’t get in the way of a semi-popular claim, however, that Obama was passing out phones for votes. “She may not know who George Washington is or Abraham Lincoln,” opined radio host Rush Limbaugh, “but she knows how to get an Obamaphone.” Former Rep. Adam Putnam (R–Fla.) had more pointed words: “Early vote now so that you can wave signs on election day next Tuesday,” he said. “We’ve got to drag people to the polls. That’s what they’re doing. You don’t have to offer them cell phones like they’re doing.”

The Trump administration denies that his food aid work was at all politically-motivated. “Politics has played zero role in the Farmers to Families food box program,” the Department of Agriculture said in a statement. “It is purely about helping farmers and distributors get food to Americans in need during this unprecedented time.”

Trump similarly attached a letter to the stimulus checks doled out as part of the government’s coronavirus relief program, though that was a bipartisan measure negotiated through Congress. The two programs have something else in common, though: They are the very types of “socialist” policies that many right-wingers usually condemn, a la “Obamaphones.”

from Latest – Reason.com https://ift.tt/34C0CD8

via IFTTT

Four weeks before Election Day, third-party presidential candidates continue to lag in the polls compared to the spike year of 2016, when 5.7 percent of the electorate went nontraditional for POTUS. In the RealClearPolitics average of the last five national polls, Libertarian Jo Jorgensen sits at just 2 percent, while the Green Party’s Howie Hawkins is at a temporarily high 1.4 percent that will revert closer to 1 once the next poll rolls over. (Also, if Hawkins, in the face of near-fanatical Democratic voter motivation this year, tops 2016 nominee Jill Stein’s 1.1 percent, I will eat a Dodgers hat on live television.)

Still, there remains potential yet for Libertarians and even Greens to be labeled “spoilers” depending on how this high-intensity election plays out. Jorgensen is polling higher than the gap between President Donald Trump and Democratic nominee Joe Biden in four key states, each of which Trump won in 2016: Ohio and North Carolina, where Biden currently leads, and Iowa and Georgia, where the incumbent retains a tiny advantage.

Here are those state races, ranked by the percentage-point distance between the third-party candidate and the margin between the top two.

Forecast: Rated a toss-up by 12 out of 14 prognosticators, with the other two leaning Trump. “Ohio looked like a red state a year ago,” noted Cleveland.com last week. “Heading into the presidential debate, it’s clearly a toss-up.”

Polling percentages: Biden 45.8, Trump 44.6, Jorgensen 2.0, Hawkins 0.6, Constitution Party nominee Don Blankenship 0.4 (in eight polls), other/not voting/undecided 6.2 (17 polls)

Forecast: 13/14 toss-up, with one leaning Biden. “Most every political veteran in North Carolina, Democrat or Republican, is expecting a close race,” reported The New York Times on September 26. “Each of the last three presidential races in the state has been decided by less than four percentage points….[And] a number of people in the state have already voted: Absentee ballots began going out to the state’s voters three weeks ago.”

2016 results: Trump 49.8, Clinton 46.2, Johnson 2.7, Stein 0.3

Forecast: 9/14 rate it a toss-up, with five leaning Trump. Reports CNN this week: “Trump’s campaign canceled its planned television advertising in Iowa and Ohio this week, focusing its spending on states where Trump is behind even as polls show he is neck-and-neck with Democratic challenger Joe Biden in the two Midwestern states.”

2016 results: Trump 51.2, Clinton 41.7, Johnson 3.8, Evan McMullin 0.8, Stein 0.7, Darrell Castle (Constitution Party) 0.3, Lynn Kahn (New Independent) 0.1, Dan Vacek (Legal Marijuana Now) 0.1

Polling percentages: Trump 46.6, Biden 45.1, Jorgensen 2.1, Hawkins 1.0, other/not voting/undecided 5.6 (11 polls, four with Hawkins)

Forecast: 12/14 toss-up, with two leaning Trump. “In a wild 2020 election shaped by pandemic, protests and polarizing politics,” the Atlanta Journal-Constitution wrote last week, “suburban women could well determine the fate of Georgia’s presidential race, two U.S. Senate elections and down-ballot contests. And both parties have sharpened their pitches to win over the once-reliably Republican bloc.”

2016 results: Trump 50.4, Clinton 45.4, Johnson 3.0, Evan McMullin 0.3

That’s a question mark because for some foolish reason POLLSTERS AREN’T INCLUDING THIRD-PARTY CANDIDATES IN ALASKA, NOT EVEN ONCE. This is a particularly unwise tactic in the Last Frontier since voters there are as likely as any in the union to vote against the grain—a combined 12.2 percent for non-Dems/Repubs in 2016. Ralph Nader got 10.1 percent of the vote there in 2000; Ross Perot got 28.4 percent of the vote in 1992.

Forecast: 13/14 prognosticators peg this race as likely or leaning Republican, and fair enough—Alaska has voted for the last 13 consecutive GOP presidential nominees, and by at least 14 percentage points for the past six. “Alaska’s values are the values of the Libertarian Party,” Jorgensen told the Juneau Empire last month. “We believe in the individual, we believe that people have the right to make their own decisions and we shouldn’t be bossed around by the people in Washington. The federal government is too big, too nosy, too, bossy and the worst part is, they usually end up hurting the very people they’re trying to help.”

2016 results: Trump 51.3, Clinton 36.6, Johnson 5.9, Stein 1.8, Castle 1.2, Reform Party nominee Rocky De La Fuente 0.4

from Latest – Reason.com https://ift.tt/2SNyS9v

via IFTTT

France & Germany To Push For EU Sanctions On Russia’s GRU Over Navalny Tyler Durden

Wed, 10/07/2020 – 13:45

France and Germany announced Wednesday they will push for European sanctions on Russia – specifically Kremlin intelligence officials – over the alleged poisoning of Alexei Navalny with what German authorities believe was a Russian-produced nerve agent.

A joint statement essentially faulted lack of adequate Russian response giving “no credible explanation” to the allegations which many observers have seen as an eerily familiar repeat to the Skipral affair in the UK.

“No credible explanation has been provided by Russia so far. In this context, we consider that there is no other plausible explanation for Mr Navalny’s poisoning than a Russian involvement and responsibility,” Foreign Ministers Jean-Yves Le Drian and Heiko Maas said in their joint statement Wednesday.

Russian activist and opposition leader Alexei Navalny, AFP via Getty Images.

The proposal is expected during a meeting of 27 EU foreign ministers scheduled for next Monday. The sanctions are expected to target Russian GRU military intelligence officials.

“Drawing the necessary conclusions from these facts, France and Germany will share with European partners proposals for additional sanctions,” the two ministers added. “Proposals will target individuals deemed responsible for this crime and breach of international norms, based on their official function, as well as an entity involved in the Novichok program.”

Russia will no doubt see this as an ‘absence of evidence means Russia must have done it’ type charge which it’s been subject to the in the past amid a charged anti-Moscow atmosphere, spurned on also by the United States.

The allegation that Novichok was involved, again in a seeming replay of the Skipral case, is what has left skeptics scratching their heads, given it’s a Cold War era military grade nerve-agent which was developed only by the Soviet Union. This has left some to point out howbizarre the plot is, given how “obvious” Russian fingerprints behind such an “assassination attempt” would be.

Meanwhile Navalny in his first major interview since recovering and leaving the Berlin hospital told Der Spiegel: “I assert that Putin was behind the crime.”

The official Kremlin response was even more interesting, which said via state media sources that “Western intelligence agencies – in particular, agents from the American CIA – are working with Russian opposition figure Alexey Navalny,” according to Putin’s spokesman.

The Russian opposition leader Aleksei Navalny was poisoned with a nerve agent that had “similar structural characteristics” to Novichok, according to the world’s leading chemical weapons body.https://t.co/7l2dhRLWgO

Navalny has since his hospital release been making the media rounds, where he’s since repeated that the highest levels of the Russian government ordered his death.

In recent days, the Organization for the Prohibition of Chemical Weapons (OPCW) has gotten involved, saying its own tests confirmed the presence of toxic substances in Navalny’s blood and urine samples, however, which were “similar to Novichok”.

Russia has questioned the entire investigation given its own authorities have been blocked from accessing and inquiring of the evidence, even after repeat requests.

No doubt novichok nerve agent used to poison Alexey #Navalny. Any use of a banned chemical weapon is a matter of great concern to all #CWC States Parties

“Until the documents are provided… we will consider everything that’s happening around this incident an unbridled propaganda campaign of lies or, simply put, a low-grade provocation,” Moscow’s envoy Alexander Shulgin said at an OPCW session in The Hague.

“Russia owes nothing to anyone, not to Germany, not to other countries that categorically and without proof claim that Russia is allegedly guilty of poisoning Navalny,” he said.

via ZeroHedge News https://ift.tt/2Sycel1 Tyler Durden

The news, as it tends to be, has been dominated by President Donald Trump over the last several days, perhaps even more so with his recent COVID-19 diagnosis, which means one recent Trump tidbit largely flew under the radar: his requirement that billions of dollars in food aid packages for the needy arrive in tandem with a letter signed by him.

“As President, safeguarding the health and well-being of our citizens is one of my highest priorities,” the letter reads, referencing the Food and Drug Administration’s (FDA) $4 billion Farmers to Families Food Box Program. The initiative has purchased food typically bought by restaurants and rerouted it toward poor families, with over 100 million boxes sent since May. “As part of our response to the coronavirus, I prioritized sending nutritious food from our farmers to families in need throughout America.”

Reactions have not been uniformly positive, with some characterizing the letter as an overtly politicized election stunt. “In my 30 years of doing this work, I’ve never seen something this egregious,” Lisa Hamler-Fugitt, executive director of the Ohio Association of Food Banks, toldPolitico. “These are federally purchased boxes.”

Some food banks have begun removing the letters. Meanwhile, several people appear to be receiving the aid and corresponding letter even though they aren’t underserved. “Why would someone receiving this really need to know this?” said Matthew Killen of Miami Beach, who is not in need but received a package of food on his doorstep, according to The Miami Herald. He lives in a majority Hispanic neighborhood, which he feels the administration “targeted” so Trump could “win [the] area.”

Readers might remember a string of similar criticisms leveled at former President Barack Obama during the 2012 election after the “Obamaphone” video went viral. “Everybody in Cleveland—low, minority—got Obamaphones,” says a woman who had shown up to protest at a Mitt Romney rally. “Keep Obama in president [sic]. He gave us a phone. He’s gonna do more.”

In reality, that controversy was a farce. Under the spotlight was the Lifeline program, which provides subsidies for communications to eligible low-income recipients. The catch: It was implemented in 1985 during the Reagan administration, and the Obama administration had sought to reform what was seen as a program plagued by massive fraud. The changes reportedly saved $213 million.

That didn’t get in the way of a semi-popular claim, however, that Obama was passing out phones for votes. “She may not know who George Washington is or Abraham Lincoln,” opined radio host Rush Limbaugh, “but she knows how to get an Obamaphone.” Former Rep. Adam Putnam (R–Fla.) had more pointed words: “Early vote now so that you can wave signs on election day next Tuesday,” he said. “We’ve got to drag people to the polls. That’s what they’re doing. You don’t have to offer them cell phones like they’re doing.”

The Trump administration denies that his food aid work was at all politically-motivated. “Politics has played zero role in the Farmers to Families food box program,” the Department of Agriculture said in a statement. “It is purely about helping farmers and distributors get food to Americans in need during this unprecedented time.”

Trump similarly attached a letter to the stimulus checks doled out as part of the government’s coronavirus relief program, though that was a bipartisan measure negotiated through Congress. The two programs have something else in common, though: They are the very types of “socialist” policies that many right-wingers usually condemn, a la “Obamaphones.”

from Latest – Reason.com https://ift.tt/34C0CD8

via IFTTT

Four weeks before Election Day, third-party presidential candidates continue to lag in the polls compared to the spike year of 2016, when 5.7 percent of the electorate went nontraditional for POTUS. In the RealClearPolitics average of the last five national polls, Libertarian Jo Jorgensen sits at just 2 percent, while the Green Party’s Howie Hawkins is at a temporarily high 1.4 percent that will revert closer to 1 once the next poll rolls over. (Also, if Hawkins, in the face of near-fanatical Democratic voter motivation this year, tops 2016 nominee Jill Stein’s 1.1 percent, I will eat a Dodgers hat on live television.)

Still, there remains potential yet for Libertarians and even Greens to be labeled “spoilers” depending on how this high-intensity election plays out. Jorgensen is polling higher than the gap between President Donald Trump and Democratic nominee Joe Biden in four key states, each of which Trump won in 2016: Ohio and North Carolina, where Biden currently leads, and Iowa and Georgia, where the incumbent retains a tiny advantage.

Here are those state races, ranked by the percentage-point distance between the third-party candidate and the margin between the top two.

Forecast: Rated a toss-up by 12 out of 14 prognosticators, with the other two leaning Trump. “Ohio looked like a red state a year ago,” noted Cleveland.com last week. “Heading into the presidential debate, it’s clearly a toss-up.”

Polling percentages: Biden 45.8, Trump 44.6, Jorgensen 2.0, Hawkins 0.6, Constitution Party nominee Don Blankenship 0.4 (in eight polls), other/not voting/undecided 6.2 (17 polls)

Forecast: 13/14 toss-up, with one leaning Biden. “Most every political veteran in North Carolina, Democrat or Republican, is expecting a close race,” reported The New York Times on September 26. “Each of the last three presidential races in the state has been decided by less than four percentage points….[And] a number of people in the state have already voted: Absentee ballots began going out to the state’s voters three weeks ago.”

2016 results: Trump 49.8, Clinton 46.2, Johnson 2.7, Stein 0.3

Forecast: 9/14 rate it a toss-up, with five leaning Trump. Reports CNN this week: “Trump’s campaign canceled its planned television advertising in Iowa and Ohio this week, focusing its spending on states where Trump is behind even as polls show he is neck-and-neck with Democratic challenger Joe Biden in the two Midwestern states.”

2016 results: Trump 51.2, Clinton 41.7, Johnson 3.8, Evan McMullin 0.8, Stein 0.7, Darrell Castle (Constitution Party) 0.3, Lynn Kahn (New Independent) 0.1, Dan Vacek (Legal Marijuana Now) 0.1

Polling percentages: Trump 46.6, Biden 45.1, Jorgensen 2.1, Hawkins 1.0, other/not voting/undecided 5.6 (11 polls, four with Hawkins)

Forecast: 12/14 toss-up, with two leaning Trump. “In a wild 2020 election shaped by pandemic, protests and polarizing politics,” the Atlanta Journal-Constitution wrote last week, “suburban women could well determine the fate of Georgia’s presidential race, two U.S. Senate elections and down-ballot contests. And both parties have sharpened their pitches to win over the once-reliably Republican bloc.”

2016 results: Trump 50.4, Clinton 45.4, Johnson 3.0, Evan McMullin 0.3

That’s a question mark because for some foolish reason POLLSTERS AREN’T INCLUDING THIRD-PARTY CANDIDATES IN ALASKA, NOT EVEN ONCE. This is a particularly unwise tactic in the Last Frontier since voters there are as likely as any in the union to vote against the grain—a combined 12.2 percent for non-Dems/Repubs in 2016. Ralph Nader got 10.1 percent of the vote there in 2000; Ross Perot got 28.4 percent of the vote in 1992.

Forecast: 13/14 prognosticators peg this race as likely or leaning Republican, and fair enough—Alaska has voted for the last 13 consecutive GOP presidential nominees, and by at least 14 percentage points for the past six. “Alaska’s values are the values of the Libertarian Party,” Jorgensen told the Juneau Empire last month. “We believe in the individual, we believe that people have the right to make their own decisions and we shouldn’t be bossed around by the people in Washington. The federal government is too big, too nosy, too, bossy and the worst part is, they usually end up hurting the very people they’re trying to help.”

2016 results: Trump 51.3, Clinton 36.6, Johnson 5.9, Stein 1.8, Castle 1.2, Reform Party nominee Rocky De La Fuente 0.4

from Latest – Reason.com https://ift.tt/2SNyS9v

via IFTTT

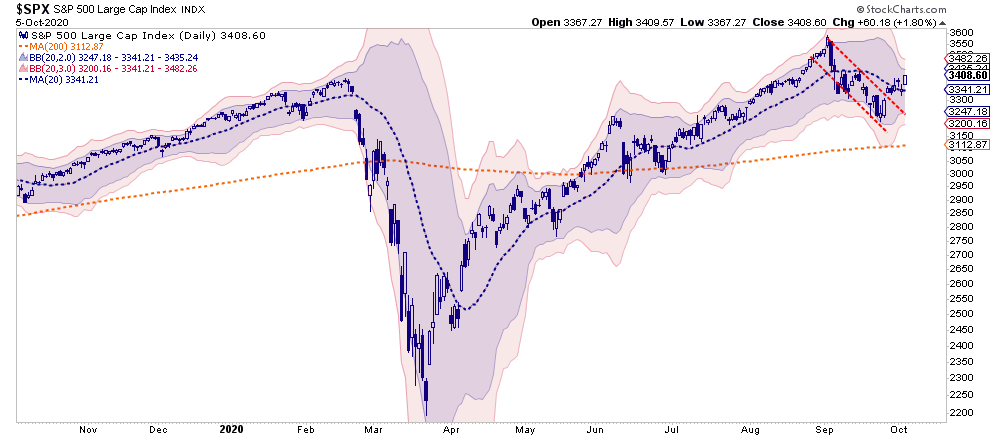

In this past weekend’s missive “Trump Infects Markets Bounce,” we discussed even though the market had bounced off support, we still consider it a “sellable rally,” for now. The comment generated quite a few emails, mainly since we also discussed that markets are generally positive in election years. To wit:

“Lance, I am confused. On one hand you say that investors should use any near-term rally to rebalance risks. But then discuss how markets tend to be positive the majority of the time during election years. I am not sure what to do.” – KC

It’s a great question that drives to the heart of our risk management process.

Let’s start with our comment from the newsletter:

“Notably, while the rally that we have witnessed from the recent lows has eaten up a fair bit of the previous oversold condition, the MACD “buy signal” was triggered on Friday.

Such suggests that we could see some additional buying next week. However, again, with the failure at the 50-dma, such means continuing to use rallies to rebalance risks accordingly.”

Chart updated through Monday’s close.

The good news is that we did indeed see a spurt of “additional buying” on Monday, which allowed the market to clear the 50-dma. Such puts the previous September highs back within the context of the rally that started two weeks ago.

The bad news is that investors chased the market on “hopes” for further stimulus and a “Biden” victory during the upcoming election. There is a reasonable probability that one or both of those outcomes will not occur.

Lastly, as shown below, while the very short-term technicals are bullish, the intermediate-term measures have not reversed yet. Such could limit upside potential from current levels.

Conflicting Information

If we break down the commentary and charts into critical points, we can gain some clarity.

The market broke above resistance (bullish)

MACD has crossed positively, issuing a “buy signal.” (bullish)

The market broke above the 50-dma. (bullish)

The overall trend from the September highs is negative (bearish)

MACD is back to overbought (neutral to bearish)

Intermediate-term “sell-signals” still firm (bearish)

Notably, the markets have returned to more neutral territory, and as noted previously, the correction has been orderly.

“Over the last couple of weeks, we have been discussing the ongoing market correction. As shown below, the sell-off has been orderly and not one of a ‘panic’ induced decline.“ –The Selloff Is Overdone,

So, why do we think this is still a “sellable rally?”

In the short-term, we remain “bullish-biased” in portfolios. However, there are several significant concerns we have over the intermediate to long-term.

Psychology:

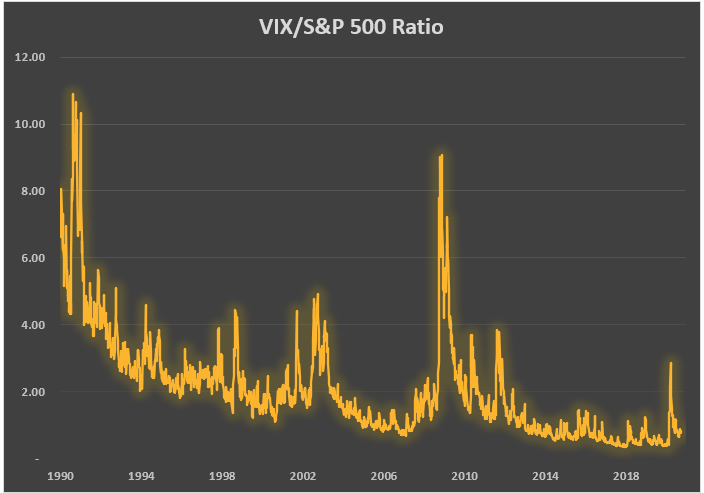

Despite the recent correction, volatility remains hugely suppressed. “Over-confidence” by investors in the market is a “contrarian” indicator we watch closely. As noted above, the recent decline has shown no signs of investors “panic selling,” instead they appear to have become even more complacent.

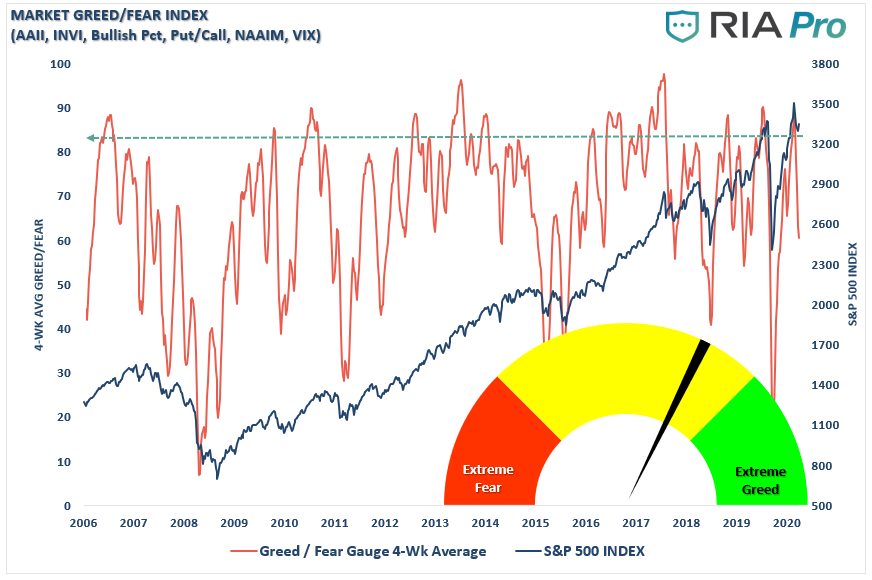

Notably, while the recent correction did reduce our fear-greed index somewhat, it remains elevated. Again, like volatility, overall investment positioning doesn’t show “fear” of a deeper correction. While the indicator is currently in more “neutral” territory, it suggests gains are likely limited short-term.

The same goes for positioning by professional investors. With positioning back to more neutral territory, any rally in the market is likely limited.

The current psychological conditions suggest the short-term bottom in the market remains intact. However, given that much of the more “bullish” exuberance was not displaced, the upside may get confined to previous highs.

As noted, much of the impetus for the rally was “hope” of more stimulus. However, currently, there is little evidence of another CARES Act occurring before the election, particularly with the Senate in recess. Such could wind up disappointing investors in the short-term, particularly as economic growth continues to wane.

Fundamental

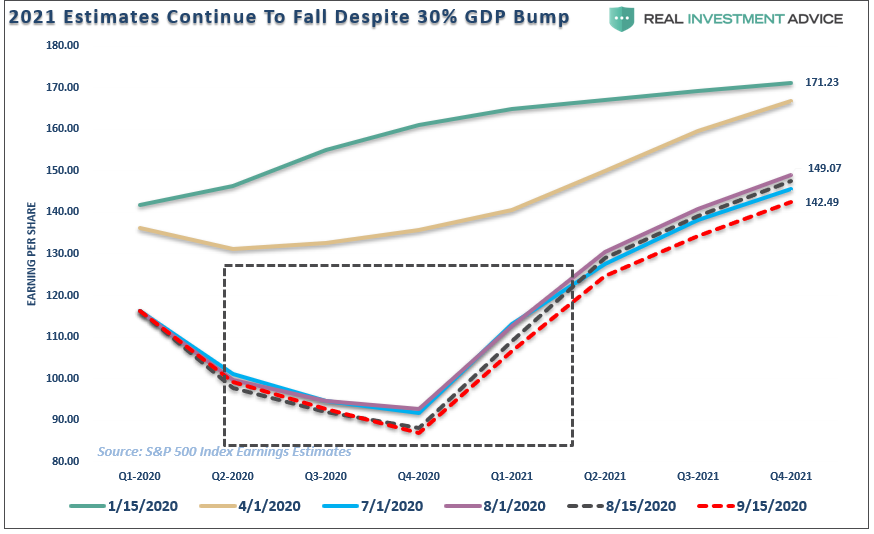

In “Earnings Don’t Support The Bullish Thesis,”I noted that while estimates were lowered by Standard & Poors (latest update was September 30th), the earnings revisions continue to fall despite media commentary about a strongly recovering economy.

Let me point out some critical points:

In January and February, investors were bidding up stocks to all-time highs based on REPORTEDearnings of $171/share by the end of 2021.

Today investors are paying roughly the same price for 2021 earnings that are near $30/share lower.

While earnings revisions did tick HIGHER at the beginning of August, estimates through the end of 2020 hit a new low just 2-weeks later.

A Simple Message

In January of 2020, investors bought stocks because valuations were cheap based on 2021 estimates.

In September of 2020, investors are buying on the same media spin, but are paying more for less.

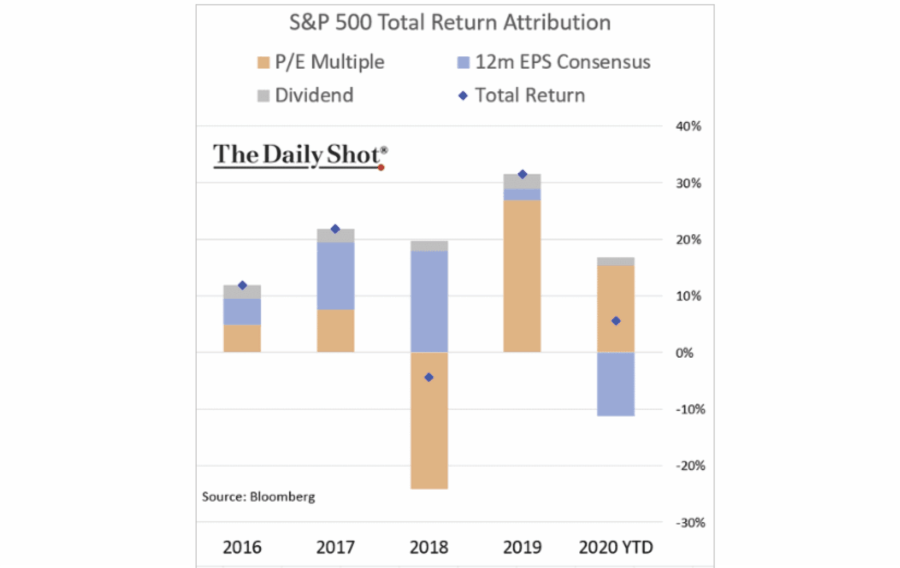

But this isn’t a new story, but one that existed over the last two years as shown by the S&P 500 total return attribution analysis.

Investors have been consistently “betting” on the promise of “stronger economic growth.” However, such has not been the case as corporate profits have weakened, economic growth has slowed, and valuations have only continued to expand.

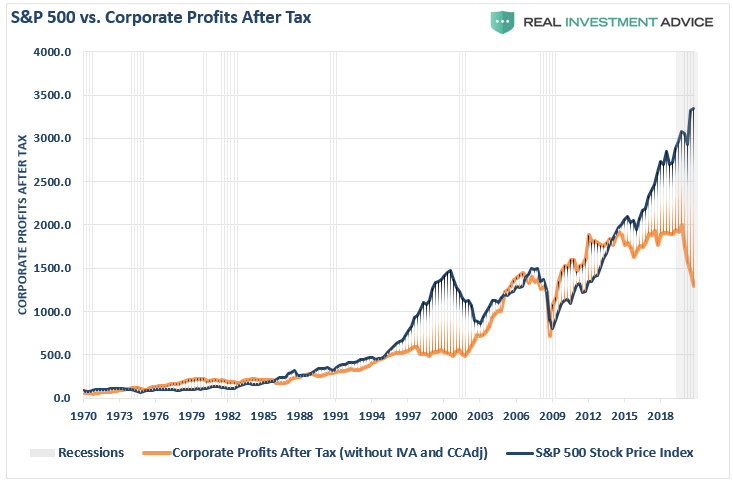

GAAP Earnings (actual real earnings), as compared to GDP, explains the problem. Not surprisingly, since “stocks are a function of the economy,” there is a decent correlation between economic growth and corporate earnings. Such is because, without economic growth, consumers don’t have paychecks with which to consume, which is where corporate profits come from.

Such is also reason to remain concerned about the persistent gap between “the stock market” and “corporate profits.”

Eventually, the two will reconnect either by:

Stock prices fall sharply as in 2008,

The market stagnates while profits catch up, or

A combination of both as in 2002-2003.

Technical Concerns

From a purely technical perspective, the market remains in a long-term deviation from historical trends. The problem with long-term trend analysis, much like valuations, is that markets can “remain irrational longer than logic would predict.” It is during these periods of “irrationality” where investors begin to believe “this time is different,” or “such and such” doesn’t matter any longer due to Central Bank interventions.

Those beliefs have, without exception, wound up costing investors more than they ever thought possible.

As noted above, on a short-term basis, if the market can clear the 50-dma, a subsequent rally back to all-time highs is certainly not out of the question.

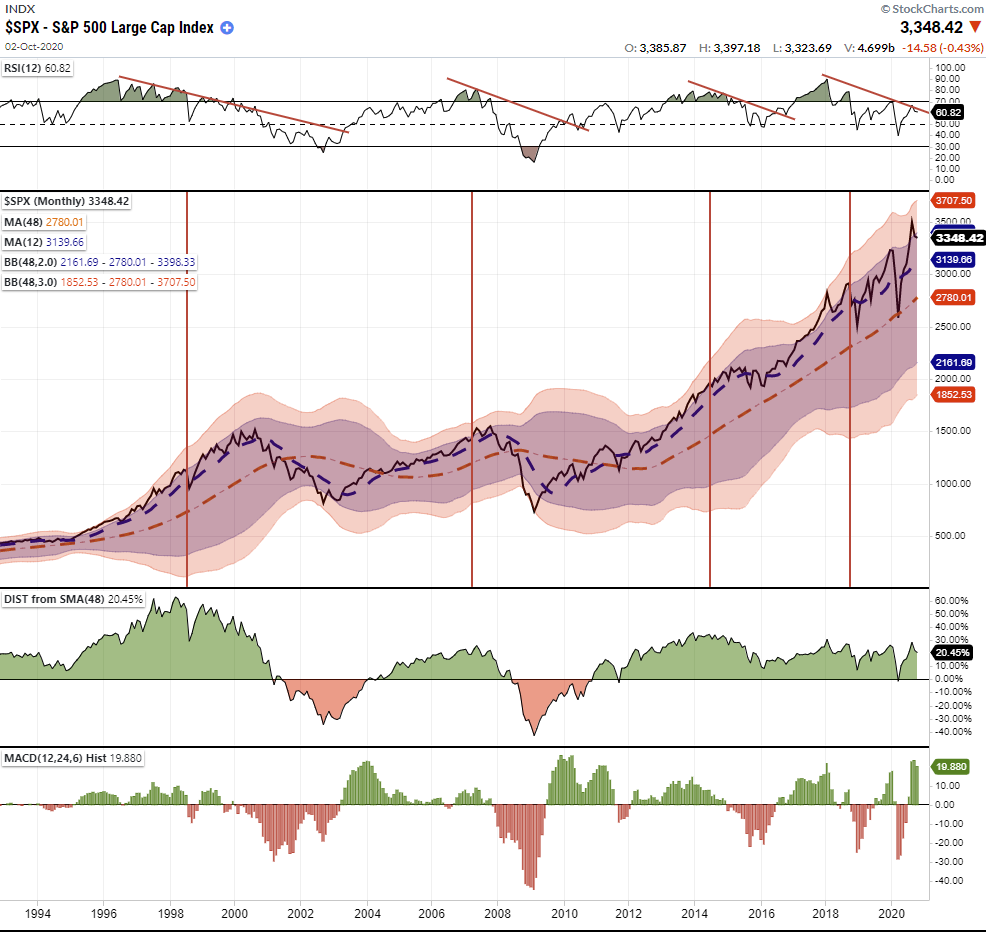

However, when viewing longer-term time frames, the risks become more evident. As shown in the “weekly” chart below, the deviation from long-term means remains at extreme levels. Historically, these deviations correct themselves. Such a “mean-reverting” event can occur over a drawn-out period, as seen in 2015-2016. Or, it occurs rapidly, as seen in both 2018 and 2020.

What is essential to understand is that while the short-term bullish “meme” is hard to resist, these “mean-reverting” events occur regularly. They also tend to happen when the media least expects them too.

If we take a long-term view, the “monthly” chart confirms the same. Relative-strength continues to diverge negatively, participation remains weak, and markets remain well deviated from long-term means.

Navigating The Dichotomy

For many, it is hard to understand how there can be two simultaneous but opposing views. In the short-term, markets are “bullishly” biased, which keeps portfolio allocations weighted toward equity risk. However, longer-term, there is a clear “bearish” backdrop to consider.

That dichotomy is what makes investing difficult for most investors. Since they become so focused on the “short-term” view, as that is where all the “action” is, they dismiss the long-term view entirely. Unfortunately, such repeatedly leads to poor outcomes.

For now, and for all of the reasons stated herein, our portfolio management processes change from “buying dips” to “selling rallies.”

Let me be clear. Such does not mean we are “selling everything and going to cash.”

The Rules

Instead, we will use rallies to:

Re-evaluate overall portfolio exposures. Are equity exposures aligned with current market dynamics and related risks?

Raise cash as needed. (Cash is a risk-free portfolio hedge when clear opportunities are not available.)

Review all positions (Sell losers/trim winners)

Look for opportunities in other markets and assets. (There is no rule you can only buy stocks. Bonds, commodities, currencies, alternative investments, annuities, etc. can all have places.)

Add hedges to portfolios.

Trade opportunistically. (There are always rotations which can be taken advantage of)

As we have discussed previously, momentum-driven markets are a tough thing to kill. However, when they do turn, the momentum works equally well in reverse.

If the bulls are right, then it is a simple process to remove hedges and reallocate back to equity risk accordingly.

However, if there is a risk to the bull market, a more conservative portfolio will protect capital in the short-term. The reduced volatility allows for a logical approach to making adjustments as the correction becomes more apparent. (The goal is not to get forced into a “panic selling” situation.)

It also allows you to buy at deeply discounted values.

For all of these reasons, we continue to use rallies as opportunities to rebalance risk, follow our portfolio management rules, and protect capital as needed.

via ZeroHedge News https://ift.tt/34tDW8g Tyler Durden

Tesla Has Officially “Dissolved” Its PR Department Tyler Durden

Wed, 10/07/2020 – 13:15

Tesla has once again added to its list of “firsts” and has apparently become the first automaker who “officially” doesn’t talk to the press anymore. The company has “dissolved” its PR department as of earlier this week, according to the pro-Tesla bloggers over at electrek.

“We no longer have a PR Team,” a Tesla source said.

After all, who needs a PR department when you constantly have Cathie Wood, Chamath and Ross Gerber singing your praises, live, on every financial news network 24 hours a day, 7 days a week. And who needs a PR department when “leaked e-mails” can make their way to the press, saying literally anything the company wants, at any time, and they are instantly reported on.

In fact, while we’re on that train of thought, who needs SEC disclosures in this case?

But we digress. According to electrek, it isn’t going to be a huge loss to begin with as Tesla “hasn’t responded to a press inquiry in months”.

Whether or not this is a savvy ploy of some sort remains to be seen. Tesla has grappled with the press, who has done a halfhearted job in trying to report the truth about the embattled automaker, for years. It also seems to us that, despite having a $400 billion market cap, Tesla still seems to be conserving their cash.

With Keely Sulprizio, the last contact at PR at Tesla leaving last December (and “virtually every other member” of the company’s PR team departing thereafter), it could also be that Tesla simply doesn’t have the manpower to run PR right now.

Electrek noted other departures from the same team:

Alan Cooper was the most senior member of Tesla’s communications team, and in February, his role was changed to director of demand generation, but he has now apparently left the company.

Gina Antonini, a senior manager on Tesla’s comms team for three years, saw her role changed to director of external relations and employee experience at Tesla in February.

Also in February, Tesla communications manager Alexander Ingram moved to a role as content lead for Design Studio at Tesla.

Danielle Meister, senior global communications manager at Tesla, left for WhatsApp in April.

Most recently, Rich Otto, who handled some of the latest PR projects at Tesla like exclusive videos with YouTubers and Jay Leno, is now a product manager, according to his LinkedIn profile.

Regardless, it appears Tesla’s relationship with the press is set to become even more cagey. Pretty soon Musk will be holding full-on assault style press conferences, a la Donald Trump, where we spends an hour berating the press and avoiding their questions.

Even electrek couldn’t get behind the idea, stating: “Ignoring the press, and thus the public and customers, which is basically what is happening without a PR department, is only adding to something that most Tesla owners would probably agree was already one of Tesla’s biggest weaknesses: communication.”

Between the press and regulators, it appears Musk seems hell bent on turning as many people in the public eye against him as possible. And, like an abused domestic partner, both the press and the regulators still seem hell bent on letting Musk get away with whatever he wants.

And hey, don’t worry – Musk can handle his own press:“Let me be clear, I do not respect the SEC. I do not respect them.”

via ZeroHedge News https://ift.tt/3jRcMhS Tyler Durden

{kind=link}