Biggest US payrolls miss since 2008 and biggest collapse in China exports in years (after the biggest credit injection ever)…

Take your pick from China – tech-heavy small-cap dominated CHINEXT surged over 5% while megacap-heavy China 50 tumbled almost 5%…(SHCOMP ended the week marginally lower with the worst day since October and first losing week of the year)…

By the end of the week, only UK’s FTSE managed to hold on to gains as weakness rippled through global markets in the latte half of the week…

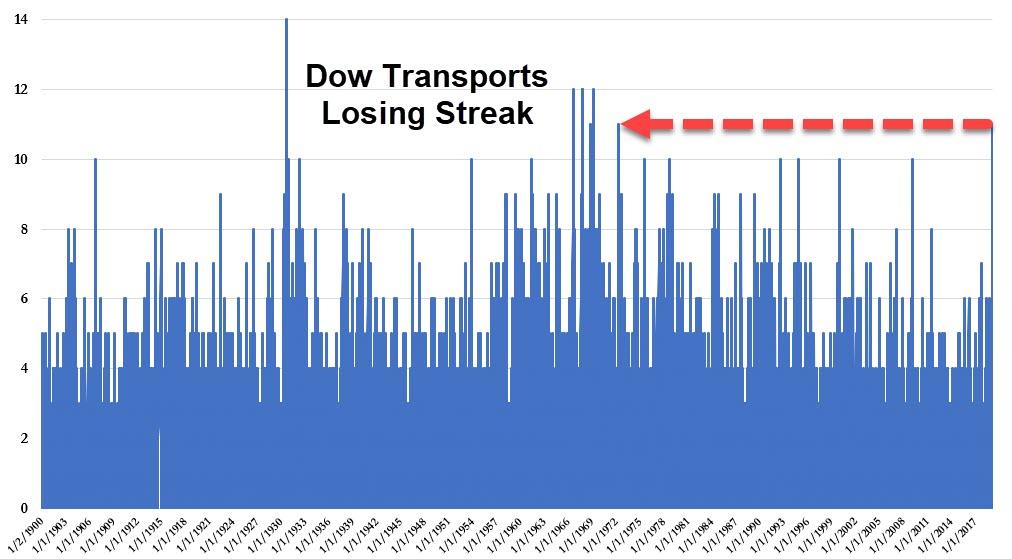

Dow, S&P, Nasdaq and Small Caps are down 5 days in a row but The Dow Transports is now down 11 days in a row – the longest losing streak since Nixon in 1972…

This week was the first down week for US stocks since 2018… Small Caps were the biggest laggards

The machines went wild as always, desperate to get stocks green on the day…

Everything green from the shitty payrolls print…

Stocks tried twice to accelerate and ignite momentum for a green push but China trade headlines in the last hour spoiled the party briefly before the panic bid ensued, pushing the market above the pre-payrolls levels…

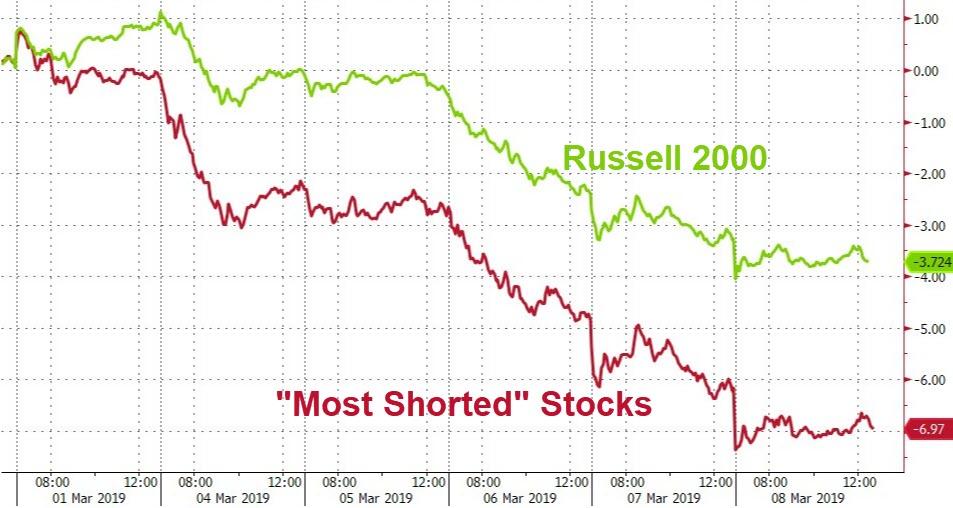

“Most Shorted” Stocks are down 7 days in a row (first down week of the year)

Buyback-related stocks are also down 8 of the last 9 days…

The S&P and Nasdaq both broke back below their 200DMA this week…

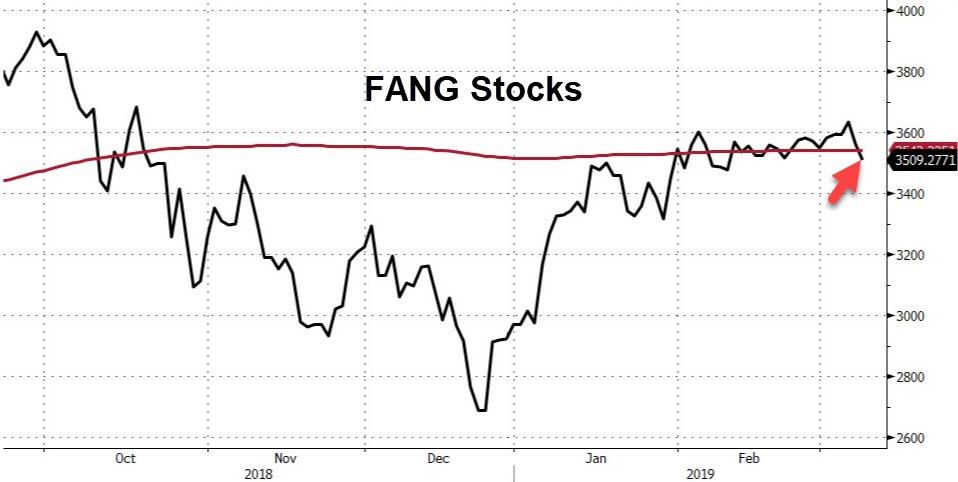

FANG Stocks suffered their biggest loss of 2019 this week…notably breaking back below its 200DMA

Semis were slaughtered – worst week of the year…

About two-thirds of its members are down, led by Marvell Tech after disappointing earnings. There was also a Nikkei report that the global semiconductor market contracted in January for the first time in 30 months. Momentum on the SOX is negative, as measured by the MACD. Falling below the 200-DMA could be an excuse for a broader selloff in stocks, I pointed out yesterday.

Credit spreads have widened 5 days in a row (and VIX is up 5 days in a row), blowing out by the most since Dec 21st…

The VIX term structure has re-inverted…

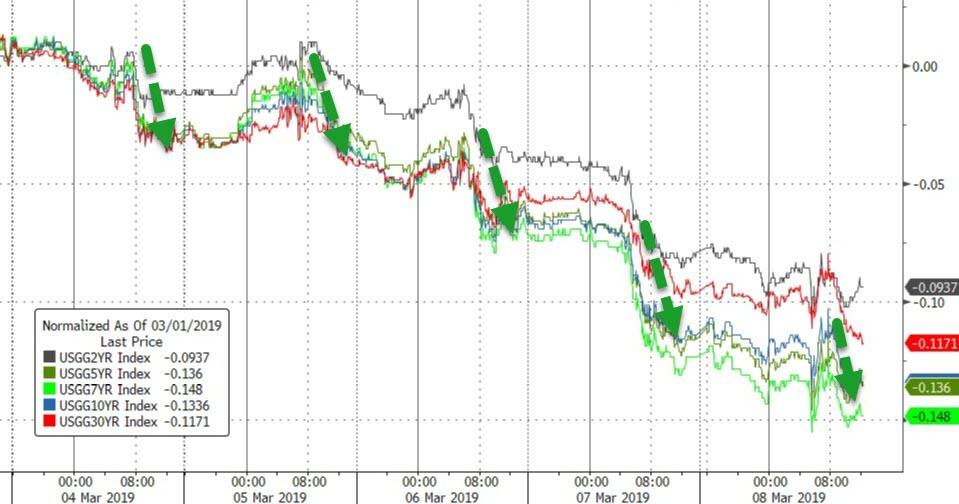

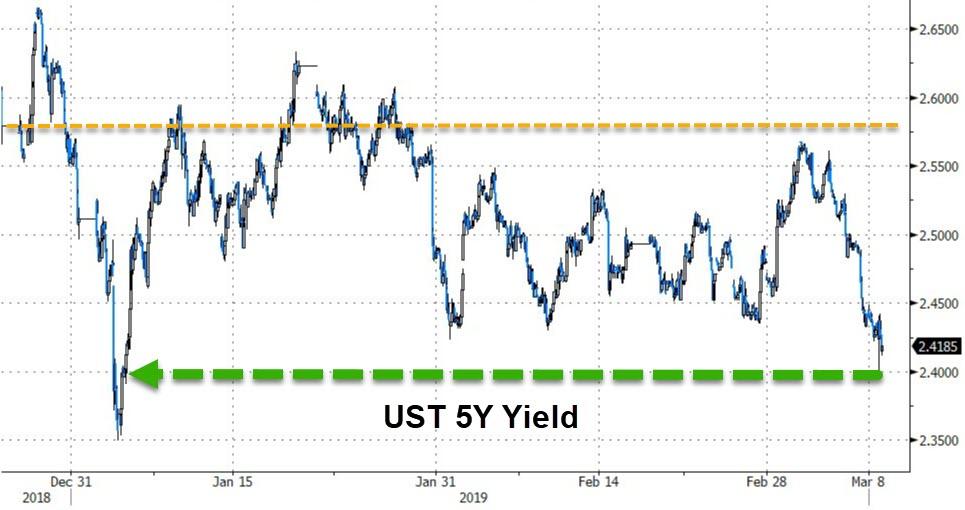

Treasury yields tumbled all week, with the belly outperforming…

The long-end dropped back to a 3.01 handle – erasing last week’s losses…

And the belly reached down to its lowest since the first day of the year…

In fact the belly is the richest it has been in years (5Y lowest relative to the 2s10s curve) as bond traders are no longer so concerned about a policy error, but still seem to be pricing in a major growth slowdown in the next few years.

And before we leave bond land, we note that 10Y CAD yields are now less than 2bps above the BOC policy rate!!!

After rising for 7 days straight, the dollar index tumbled today but remains above the key 97.00 level…

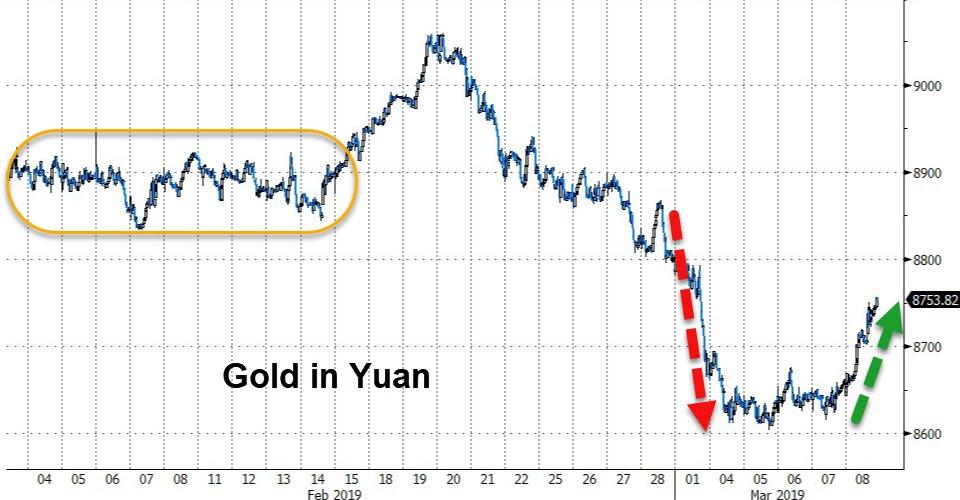

Yuan weakened – as you’d expect with USD gains – but closed at the lows of the week after Xi headlines…

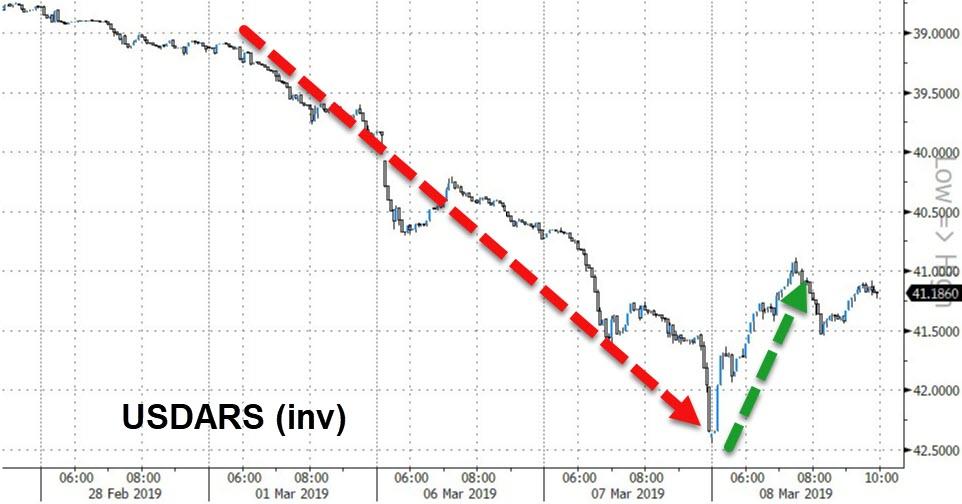

After yesterday’s bloodbath to a new record low, Argentina’s Peso rebounded notably as BCRA raised its benchmark rate by 500bps to 56.76%!!

Litecoin had a big week but the rest of Crypto was practically flat…

Despite the dollar surge on the week, PMs and oil gained on the week – rallying after the dismal jobs data…

WTI dropped off $57 and bounce back off $55…

Today’s dismal jobs data sparked a revival in gold – bouncing off unchanged for 2019…

And Gold rebounded notably against the Yuan…

Finally, deja vu all over again?

Because the gap to reality is wide…

via ZeroHedge News https://ift.tt/2HljBYR Tyler Durden

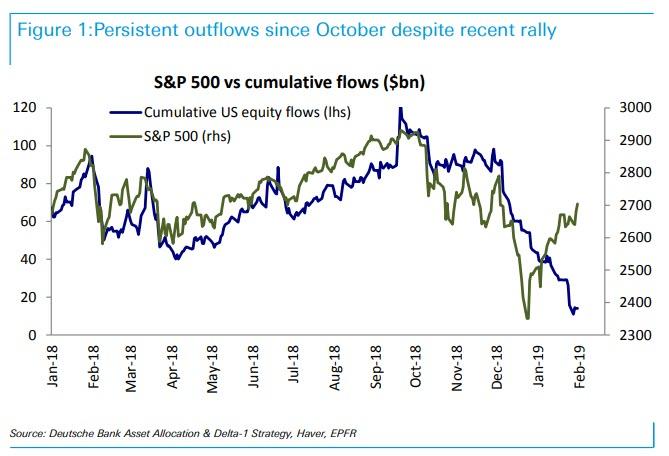

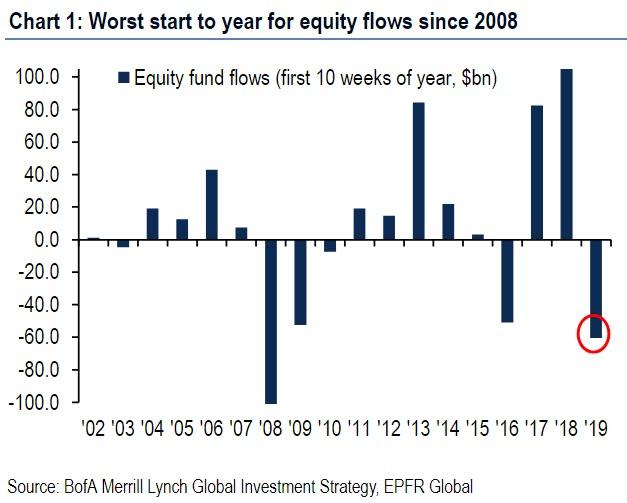

For the past two months, we have been highlighting what emerged as one of the greatest paradoxes of this market in 2019: even as stocks kept grinding higher, having almost wiped out all their Q4 losses as recently as last week, investors were locked in non-stop liquidation mode, selling stocks and pulling money out of equity funds week after week after week, for 12 consecutive weeks since December.

So now that the market appears to have finally reversed and the “goldilocks” rally is over, with BMO’s technician predicting that a retest of the December lows is now underway, it appears that all those skeptics who continued to sell even as stocks rose, were correct.

And sell they did again, because one week after it appeared that bearish investors had finally thrown in the towel with a modest inflow into US equity funds, EPFR reported that the latest week saw another $10.1 billion equity outflow ($1.7bn ETF outflows, $8.4bn mutual fund outflows), with the US seeing about half, or $5.5 billion, of this, while inflows into fixed income accelerated with $8.8bn flowing into bonds, $1.2bn pulled from gold.

But back to stocks, where the outflows have now entered historic territory and as Bank of America calculates, 2019 is now the worst start to year for equity outflows since 2008; of course, recall that it wasn’t until March 2008 that Bear collapsed and it was only in Q3 and Q4 that the financial crisis fireworks really erupted. Which means that for whatever reason, investors were well ahead of the curve in 2008 when they rushed to pull money out of the market. The question is whether lightning will strike twice, and the same financial Armageddon that hit in 2008 – when investors pulled some $100BN from stocks in the first 10 weeks – will strike again this year.

And while equity outflows may be the largest in 11 years, something which naturally does not jive with market action YTD, this week marks another historic anniversary, with BofA reminding us that on Saturday, the bull market turns 10 years old, with the market cap of US stocks up $21.3 trillion, or 3x the rise in US GDP of $6.5tn, with the 3 Dow performers Boeing, Apple, Unitedhealth Group; while the worst performers are Walgreen, Exxon, IBM.

But while the US remains a case study of how a central bank should inject trillions into its market, if not economy, the rest of the world remains lacking, and 10 years after the GFC, the Eurozone remains trapped in deflationary “Japanification” of growth & interest rates, with EU rates unlikely to rise ever and EU equities in “value trap” according to BofA.

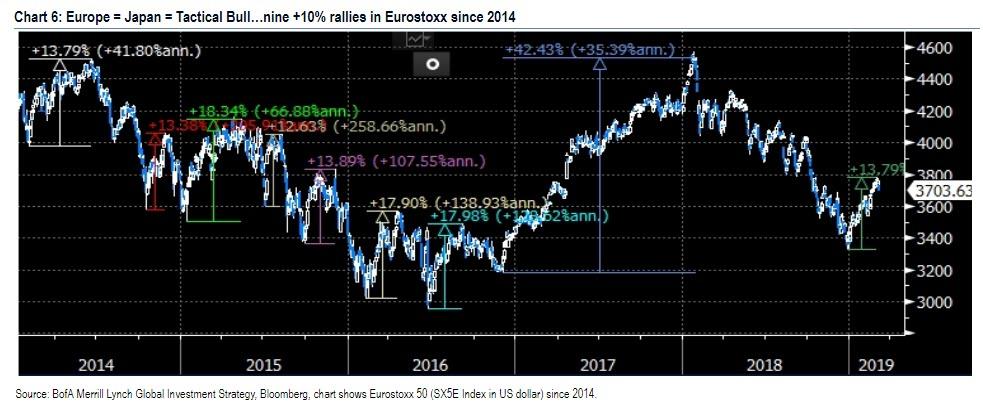

Ironically then, according to BofA “Europe = Japan” is now the most consensus trade in the world, with European stocks now the “ultimate contrarian trade”…

… which to BofA means they are likely to outperform in Q2’19 as: a) tightening Euro credit signaling Euro stocks higher; b) China “greenshoots” rally confirmed by rebound in March PMIs; c) dovish ECB = EUR @ 20-month low = boost for cheap, high beta Euro cyclicals.

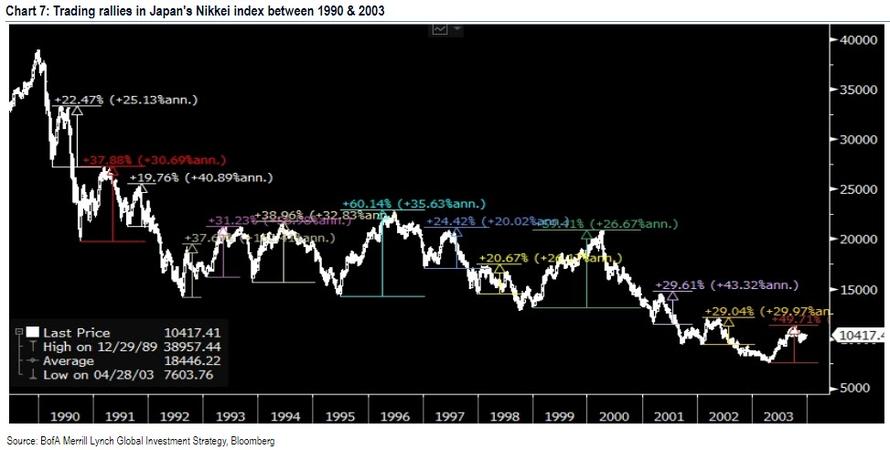

Finally, just as Hartnett showed that Japan “enjoyed” no less than 13 rallies that exceeded 20% during its secular bear market years from 1990 and 2003…

… he points out that in Europe too there have been nine +10% rallies in the Eurostoxx since ’14, with BofA confident that #10 is coming up.

via ZeroHedge News https://ift.tt/2XLgFdW Tyler Durden

As President Trump tries to push more positive trade talk on the markets, reports that China might be getting cold feet about a sweeping trade deal with the US just keep coming.

With barely 40 minutes left in the session and stocks in the midst of another intraday rally, Fox News poured cold water on the market’s party when it reported that President Xi had removed a tentatively-planned trip to Mar-a-Lago from his calendar. The report appeared to substantiate earlier reports taht the Chinese leader was wary of traveling all the way to Florida, only to leave without a deal.

Now we wait to see if the US manages to revive hopes for a trade deal before stocks close with their worst weekly drop of the year.

via ZeroHedge News https://ift.tt/2TxU3yf Tyler Durden

The co-founder and former president of Greenpeace, Patrick Moore, says that climate change is a “complete hoax and scam,” which has been “taking over science with superstition and a kind of toxic combination of religion and political ideology.”

Moore, who recently made headlines for calling Rep. Alexandria Ocasio-Cortez a “pompous little twit” and “garden-variety hypocrite” on climate change, sat down with SiriusXM’s Breitbart News Tonight with hosts Rebecca Mansour and Joel Pollak.

The Greenpeace co-founder’s message echoes that of John Coleman, the late Weather Channel founder who called global warming “the greatest scam in history.”

Moore told Breitbart how fear and guilt are driving the climate change argument, reports Breitbart News.

Fear has been used all through history to gain control of people’s minds and wallets and all else, and the climate catastrophe is strictly a fear campaign — well, fear and guilt — you’re afraid you’re killing your children because you’re driving them in your SUV and emitting carbon dioxide into the atmosphere and you feel guilty for doing that. There’s no stronger motivation than those two.

LISTEN:

According to Moore, the climate change movement has co-opted and corrupted politicans and bureaucracies in order to exert further control over people, Moore explained – noting that “green” companies only exist on the back of taxpayers.

And so you’ve got the green movement creating stories that instill fear in the public. You’ve got the media echo chamber — fake news — repeating it over and over and over again to everybody that they’re killing their children, and then you’ve got the green politicians who are buying scientists with government money to produce fear for them in the form of scientific-looking materials, and then you’ve got the green businesses, the rent-seekers and the crony capitalists who are taking advantage of massive subsidies, huge tax write-offs, and government mandates requiring their technologies to make a fortune on this, and then of course you’ve got the scientists who are willingly, they’re basically hooked on government grants.

When they talk about the 99 percent consensus [among scientists] on climate change, that’s a completely ridiculous and false numbers, but most of the scientists — put it in quotes, scientists — who are pushing this catastrophic theory are getting paid by public money. They are not being paid by General Electric or Dupont or 3M to do this research, where private companies expect to get something useful from their research that might produce a better product and make them a profit in the end because people want it — build a better mousetrap type of idea — but most of what these so-called scientists are doing is simply producing more fear so that politicians can use it control people’s mind and get their votes because some of the people are convinced, ‘Oh, this politician can save my kid from certain doom.’

Moore also warned that manmade climate change, known scientifically as anthropogenic global warming, threatens modern reasoning itself – much like the persecution of Galileo.

“But this abomination that is occurring today in the climate issue is the biggest threat to the Enlightenment that has occurred since Galileo,” said Moore. “Nothing else comes close to it. This is as bad a thing that has happened o science in the history of science.”

It is the biggest lie since people thought the Earth was at the center of the universe. This is Galileo-type stuff. If you remember, Galileo discovered that the sun was at the center of the solar system and the Earth revolved around it. He was sentenced to death by the Catholic Church, and only because he recanted was he allowed to live in house arrest for the rest of his life.

So this was around the beginning of what we call the Enlightenment, when science became the way in which we gained knowledge instead of using superstition and instead of using invisible demons and whatever else, we started to understand that you have to have observation of actual events and then you have to repeat those observations over and over again, and that is basically the scientific method.

“It’s taking over science with superstition and a kind of toxic combination of religion and political ideology. There is no truth to this. It is a complete hoax and scam,” Moore concluded.

via ZeroHedge News https://ift.tt/2EWqpdW Tyler Durden

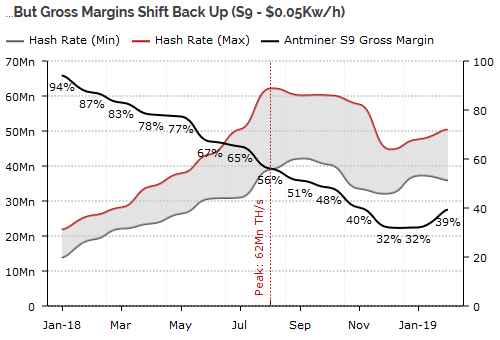

After over a year and a half of decreasing Bitcoin mining revenue, a new report shows a small yet significant recovery in the gross margins. Let’s take a look at what the mining industry has been through in recent years, and what this recovery could mean for the near future.

A dip in the industry

Last month, Bitcoin mining revenues fell to their lowest intake since August 2017. The total mining income in February 2019 totalled $195 million – a mere fraction compared to the $951 million peak of December 2017, and a 10 percent decline from the previous month.

The digital currency data analysis institution, Diar, reports the following statistics:

“In December 2017 fees alone earned miners over $295Mn. But along with the price drop and the adoption of SegWit rising from an average of 12 percent in January 2018 to over 43 percent in February this year, revenues from fees have become an afterthought.”

The downturn of the crypto-market towards the end 2018, which saw deflation of around 50 percent in the crypto-market, caused the mining industry to suffer. Smartereum reported last November that a great deal of bitcoin miners began leaving the network after BTC dropped 40 percent in price within two weeks. This was the point where the market valuation of bitcoin fell below $4000 for the first time since September 2017.

Even miners with an optimal set-up of equipment and electricity prices have been experiencing reduced growth margins, thus needing to deploy a great deal of the hashpower to remain afloat. Private miners and individuals who don’t have significant capital for investment would not be able to keep up. Only pools who can afford the newest equipment and have a cheap energy supply can profitably mine Bitcoin.

A shift into growth

However, this 18-month dip is seeing a small yet hopeful turn-around. Diar’s report showed us a rise in the mining gross margins of Bitcoin.

The gross margins of the miners went down from 94 percent at the beginning of 2018, to 32 percent at the beginning of 2019. But in February, the gross margins rose up slightly to 39 percent as shown in the graph below.

Another indication of things looking brighter for the mining industry is Bitmain’s recent success. Despite the recent hardships of the mining empire, some of their equipment sales show a growing interest in mining.

For example, their most recent flagship miner, the S15, has already sold out twice, with the next batch becoming ready for distribution in April. The S15 is expected to bring 84 percent more return compared to the older model. Furthermore, Bitmain introduced the next generation 7nm ASIC Chip for SHA256 mining which is supposed to be 28.6 percent more efficient.

What can we expect?

While there is a positive turn in the mining industry, we cannot make wild assumptions about the implications it may have on the market in the near future. The information here is not sufficient to conclude that an indication for a nearing bull market or an improvement of price stability.

Nonetheless, Smartereum reports a hopeful perspective on the matter:

“The total daily trade volumes for BTC have increased significantly since the beginning of the cryptocurrency winter hitting as high as 350,000 transactions in March. What this means is that people are beginning to focus less on the price of BTC and more on the BTC technology. So, even if the price isn’t at its best, the confidence of the true Bitcoin believers is still stronger than ever. It is this confidence that drives adoption.”

Another important point to note is that in May 2020, Bitcoin is going to be halving – namely, the bitcoin mining rewards will be algorithmically reduced by 50 percent. This means that the rewards per newly discovered block will drop from 12.5 to 6.25. Mining will be significantly less profitable if the Bitcoin price will not grow by then.

via ZeroHedge News https://ift.tt/2ENbjG5 Tyler Durden

The Financial Time’s “Lunch with the FT” is usually good for a few compelling anecdotes, particularly when they’ve got a good guest. And when it comes to consumable soundbites, there are few better than Bill Gross.

Fresh off a series of staggering post-retirement revelations, including telling Bloomberg that he had recently been diagnosed with Asperger’s, a form of autism, after reading about the symptoms experienced by hedge fund manager Michael Burry in the book “The Big Short”, Gross sat down with the FT’s US markets editor Robin Wigglesworth for a roving discussion about how Gross decided to pursue a career on Wall Street, the early days of Pimco, his ouster from the firm he built, his tabloid divorce, what it was like working with millennials and his plans for retirement. A common theme throughout the conversation was how Gross’s Asperger’s – and his insatiable lust for fame – influenced his decision-making.

As Gross puts it:

“I wanted to be famous because I wanted to be loved…pursued that obsessively,” he reflects at one point. “Shit, that’s why I’m talking to you today.”

Wigglesworth filled the interview with amusing color about Gross’s mannerisms, including his penchant for stabbing the air with his fork as a point of emphasis, and Gross’s order of his “usual” – what Wigglesworth described as “an unremarkable looking” tuna melt, which he didn’t finish.

Below, we’ve broken down a few key points:

His “defenestration” from Pimco:

While it likely contributed to his investing success, Gross suspects that his undiagnosed Asperger’s helped create some of the interpersonal friction with his senior managers that ultimately led to his ouster from the firm. Gross didn’t want to leave, and even suggested a demotion to some more minor role, but after the departure of Mohamed El-Erian, the firm’s other senior employees had apparently had enough of his shit.

At the end, Gross “was begging like a mongrel…I wanted to stay at Pimco…it was my family.”

He attributes his fall from grace at Pimco partly to his undiagnosed Asperger’s, which made him a “singular, dominating, angry, quiet, introverted person”. As Pimco grew bigger, and the average employee became younger, his “style of speaking my mind in a non-friendly way” started to cause friction. “Millennials like to hear good things, not bad things,” he says. Things came to the boil in 2014, when Mohamed El-Erian, Pimco’s chief executive and a vital Gross shock absorber, abruptly quit.

A subsequent rash of stories blamed El-Erian’s exit on the founder’s increasingly difficult behaviour – which in turn sent Gross on a witch-hunt for media leaks. Ultimately, faced with a possible exodus of frustrated senior fund managers, Pimco’s executive committee instead decided to oust Gross.

Gross offered to take on a reduced role. “I was begging like a mongrel, sniffing for titbits on the ground…I just wanted to stay at Pimco, it was my family,” he says, alternating between anger and sadness. “They looked at me, and said no…So I called up Janus.”

The early days of Pimco:

Gross’s big innovation after joining Pacific Mutual Life was to disrupt the staid world of fixed income with an aggressive style of trading, which helped Pimco earn a reputation as a bunch of “badasses” looking for “every penny we could find.”

The business came of age in an era of excess, but where the culture of Wall Street was reputedly fuelled by drink and drugs, Gross insists he never saw anything troubling at Pimco. Their main high, he says, was sugar – especially M&M’s. “It gave us all the false courage in the world to take on dealers and tell them to go f*** themselves,” Gross recalls wistfully, as he tucks into what looks like an unremarkable tuna melt.

Active, aggressive bond investing was Gross’ big innovation. Historically, insurers and pension funds were the big buyers of bonds. They rarely traded – in fact bonds were typically kept in a vault, and selling meant physically mailing them to the buyer – and enjoyed cordial, clubby relationships with Wall Street. Pimco, on the other hand, actively traded in and out of positions, expanded assertively into hot new areas like junk bonds and emerging markets, and used its increasing clout to cudgel banks into giving them better bids.

“Back then [we were] known as badasses. Between banks and insurers there was a friendly atmosphere, but we were definitely not friendly. We were looking for every penny we could get,” Gross says. The result was an investing empire that peaked at $2tn of assets under management in the wake of the financial crisis, which Pimco navigated with aplomb.

His messy tabloid divorce

Looking back, if Gross could re-do his divorce from his second wife, Sue Gross, after their 30-year marriage fell apart, there are a few things he would do differently…like maybe he wouldn’t have filled the house that went to his ex with fart spray. The acrimony has led to serious repercussions in his personal life: For example, he wasn’t invited to his son’s wedding in Italy.

Unfortunately, his private life offered little respite from the professional turmoil. In 2017 he split up with his second wife of over three decades, Sue Gross. The divorce was played out in the tabloids, reaching a tragicomic nadir with allegations that Gross had filled a house that went to his ex-wife with “fart spray”.

Gross admits this is true, but claims he was only responding in kind to what his ex had allegedly done to another home that he was taking over. “So I went to a drugstore and found smelly shit,” he says. “I don’t know why I did that. It got very ugly. It’s still ugly.” He quietly reveals that things are now so bad that he wasn’t invited to their son’s wedding in Italy — indeed he only found out about it from his dental hygienist. The downbeat turn in conversation clashes awkwardly with the clinks of wine glasses and chatter from a handful of wealthy Newport Beach “golf widows” lunching nearby.

Working with millennials

Among the factors that contributed to his fall from grace at Pimco, Gross included one big surprise. His management style didn’t exactly jive with millennials.

He attributes his fall from grace at Pimco partly to his undiagnosed Asperger’s, which made him a “singular, dominating, angry, quiet, introverted person”. As Pimco grew bigger, and the average employee became younger, his “style of speaking my mind in a non-friendly way” started to cause friction. “Millennials like to hear good things, not bad things,” he says.

His failures at Janus

After leaving Pimco, Gross sought to quickly revive his reputation by joining Janus Henderson, a much smaller rival. As anybody who has been following his exploits over the past few years probably already knows, that didn’t go so well. After a few years of sub-par returns, Gross announced his retirement earlier this year, marking an ignominious end for a man who had been one of Wall Street’s biggest luminaries.

One of the biggest factors that led to his downfall? Gross says he was hungry to prove himself outside Pimco and as a result took too much risk with his “unconstrained” investing strategy.

Unfortunately, his time at Janus Henderson provided no salvation. Desperate to prove that his golden touch hadn’t disappeared, Gross admits he ignored the lessons of a lifetime and took excessive risks with his new fund. It started out reasonably well, but suffered a 3.9 per cent loss last year, underperforming his benchmark and most other bond fund managers.

“I lost my bearings,” he says. “I wanted to prove that I could still do it, and do it quickly.” He wonders aloud whether it would have been better for his legacy if he had simply bowed out quietly from Pimco. “Eventually, as the Coldplay song goes, who would ever want to be king?” he says. His brain might tell him his legacy is intact. “But as you’ve observed, the emotional side of me says ‘people don’t love me any more’.”

But while Gross has certainly taken his fair share of blows in recent years, there is still much for him to find comfort in, as Wigglesworth readily notes. Gross followed up his lunch with a round of golf with his new girlfriend – a retired pro tennis player – and later departed for a retirement trip to Bora Bora.

Even though he’s no longer “the Bond King”, life is still pretty good.

via ZeroHedge News https://ift.tt/2VL4dsH Tyler Durden

2020 Democratic Presidential Candidate Andrew Yang has been making the rounds on talk shows and popular podcasts like the Joe Rogan Experience over the past month. The key platform of his candidacy is what his team has branded “The Freedom Dividend.” This promise of a $1,000/month government payout for every American adult over the age of 18 is nothing more than a rebranding of what is commonly known as the Universal Basic Income (UBI). Unfortunately for Yang, the basis of both the supposed need for his policy prescription and the prescription itself is built upon a foundation of economic fallacies and lies.

Yang is seeking to appeal to the same voters that helped Donald Trump rise to the presidency. He is explicitly targeting the struggling working class and what he claims are hordes of soon to be unemployed middle Americans with little education and job prospects. In other words, he’s looking to buy votes by paying those who have fallen upon hard times and by convincing others that they too will need government handouts in the future due to losing their jobs to technology. While it can be said that all politicians are buying votes in some form or another, to make handing out $12,000 a year to every American adult the basis of your presidential campaign would be to set an alarming precedent with perverse incentives and a slippery slope. When $12,000 fails to satiate the voting public or live up to the outcomes claimed – which it is certain to do – this figure can only surely rise in the future. And after enacted, how willing would voters be to simply give up their $12,000 payout?

Yang’s plan of giving the entire population of Americans over the age of 18 who aren’t already receiving more than $1,000 in government benefits per month would mean the Federal Government, which is already $22 trillion in debt, would be handing out nearly $2 trillion per year. His solution – funding the plan with a new value added tax (VAT). A VAT is nothing more than an elaborate consumption tax. As Rothbard noted, “Surely a sales tax, other things being equal, is manifestly both simpler, less distorting of resources, and enormously less bureaucratic and despotic than the VAT. Indeed the VAT seems to have no clear advantage over the sales tax, except of course, if multiplying bureaucracy and bureaucratic power is considered a benefit.”

As Yang has admitted, the “Freedom Dividend”, polls far better than the term “Universal Basic Income” with Americans. This alone should be reason for concern. Yang isn’t even an elected politician yet and he’s already relying on verbal sleight of hand to appeal to the population’s economic ignorance and patriotic tendencies in order to convince them that handing out $12,000 a year to every adult is a good idea even though it goes against their most basic instincts.

Yang invokes three common economic fallacies to support his proposal:

1. Technology destroys demand for labor and dooms future generations to economic misery

Yang’s claim that robots and automation are leaving less work for humans and dooming American’s to economic misery is an old and tired line that has existed as long as capital has been accumulated and utilized to make technological breakthroughs. This line of thinking is a continuation of the logic espoused by English Luddites of the 19th century which protested against the substitution of manual labor for employing even the most basic forms of machinery. This is the same line of thinking that leads to protectionist trade policies. After all, a robot or machine isn’t the only form of competition for labor. Free trade, which allows for accessing skills and goods for lower prices globally than can be had domestically was also claimed to be a job killer and economic death sentence. Over the past century, the protectionists have of course been proven wrong as the rise of global trade has led to both domestic and global economic growth resulting in staggering declines in poverty and rising standards of living.

Sure, instead of petitioning to end the use of technology in business Yang and the supporters of UBI are suggesting government handouts via redistribution, but their entire basis for the need for a UBI emerges from this view that Americans are doomed to be displaced by technology and left worthless in the labor market. It seems hard to believe that after witnessing the last two centuries of employing ever more technology in the workplace, and the commensurate rise in objective measures of standards of living over that time, that anyone could even make such a claim in good faith.

Yang invokes the labor force participation rate, which remains below pre-2008 recession levels, and claims this implies we need a UBI because those not in the work force are there due to technological displacement. And while it is true that the labor force participation rate remains marred below financial crisis levels, the 4% decline in labor force participation happened between January 2008 and September 2015 as the US economy entered recession and then languished from the government’s so-called economic remedies. You would have to be a fool (or conniving politician) to suggest that the labor force participation rate, which even as technology progressed was unchanged between 1990 and 2007, suddenly plummeted due to the employment of technology following 2007.

Yang tries to weave statistics into his justification for a UBI, and relies on hysterical “the sky is falling” forecasts of mass unemployment driven by technological advancement in near the future. However, oddly enough, he never mentions the fact that 40% of Americans were employed in agriculture at the turn of the 20th century and by the end of the 20 th century only 1% of the population was employed in the field and yet America rose to economic prominence over the period. Tractors and farm machinery made millions of jobs obsolete, and yet economic catastrophe did not follow. The same can be said for countless other industries. Yes, specific jobs are destroyed by innovation and technology, but this has always been the case and it does not lead to a general decline in the demand for labor. Furthermore, technology has historically displaced the most dangerous, monotonous and grueling tasks – which we should all be thankful for.

2. Maximizing employment as an economic goal rather than maximizing wealth

Yang claims the US needs a VAT to stick it to companies like Amazon who are innovating away the need for labor, so that this tax revenue can be used to fund the UBI and create millions of new jobs. Not only doempirical studies find that the rise of technology throughout history does not lead to a long term rise in unemployment, but this leads us directly to the second fallacy of making maximizing employment the measure of economic success and an economic goal in and of itself. Even if the labor force participation rate was set to decline due to the rise of technology, that isn’t something to necessarily fear. The fallacy arises in part due to the fact that the unemployment rate is discussed as being nearly synonymous with the strength of the economy.

Intuitively we should all know that we do not value work for work’s sake – we value wealth, not jobs per se. If simply employing the most labor and resources, instead of creating wealth is what is to be valued, then we would simply make every process as inefficient and labor intensive as possible. But we don’t. What makes people’s lives more enjoyable, what raises their standard of living, is that which makes food and other key goods and services more abundant. If an abundance of resources can be had with less hours worked surely we would all be in favor. In fact, it is clear by our very actions that we value wealth more than work for works sake.

People who speak alarmingly over the rise of automation and technology displacing human labor must be appalled by the fact that the average number of hours worked by full time workers declined by over 33% over the course of the 20th century as technology was increasingly utilized. After all, if employment of human labor is a good in and of itself, we should want to work more hours rather than less. But of course that’s not the case. At this point, surely the absurdity of such a fixation on maximizing employment is clear. We all want access to goods and services and we all want to expend as little time and energy as possible to attain them. Only masochists would want to labor away to attain things which could be attained with less effort.

The past century of progress in the growth of the material wealth of individuals has proven that the rise of technology allows humans to work less while simultaneously achieving greater degrees of material wellbeing. The employment of technology is not a plague to be feared. Alas, unfortunately we can’t all just set around and do as we please while robots do all of our work quite yet. People need to prepare for a changing economy and to learn new skills as they always have. The best thing we can do to make sure this happens is to get government out of the way of those willing to prepare.

3. Consumer spending is the basis of economic growth

Following the Keynesian framework, Yang employs the fallacy of consumer spending as the basis for economic growth. Of course, if you measure economic growth as a measure of spending like GDP, less spending necessarily means less growth. Under the current GPD fixated Keynesian framework, it is spending rather than savings that makes the economy grow. But this is merely a matter of the mathematical formula that makes up GDP and says nothing about the logical considerations or intertemporal allocation of resources that should actually be examined when trying to judge what determines economic success.

As Yang’s Keynesian consumption fixated model goes, putting cash in the hands of individuals gives them confidence to spend. And when they spend more money other people receive more money and their confidence rises and they spend more money. And this circular flow continues. Yang employs this narrative as justification to hand out money under the UBI. This is the foundation of the Keynesian framework, which suggests that aggregate demand for goods is what drives the economy and a lack of demand for goods is what causes economic contraction. He seems unaware that great thinkers like Henry Hazlitt intellectually destroyedthis framework many years ago.

This model for viewing the economy ignores the fundamental tradeoff between producing consumption goods and producing investment goods. That is to say, it ignores the very notion of scarcity. Before more of something can be consumed, more of that thing must be produced. Producing more of a good first requires investment in capital goods like tractors, or welders, or production facilities. Investment in those capital goods necessarily requires savings, which is to say consuming less than otherwise possible. You cannot save if you have already maximized consumption. So it is savings, not spending that allows for greater consumption in the future. The Keynesian framework to which Yang likely unknowingly subscribes sweeps this entire consideration aside. It focuses purely on the need to boost aggregate demand. The employment of this model by the US government has led to the justification for the disastrous deficit spending, bail outs, and money printing of the past century.

This begs the question – why stop at $12,000 a year? If scarcity need not be considered, if the UBI is such a great idea, if high aggregate demand is the key to economic success, and if government can simply print money with no consequence as is readily suggested today, why not just give everyone a UBI of $100,000 per year with money printed by the Federal Reserve? To suggest that this is a ludicrous suggestion is to admit that there is indeed an undisclosed cost to such a UBI proposal and for the entire Keynesian framework for that matter.

Conclusion

In the depths of the great depression, Keynes suggested that “the Government should have people dig up holes and then fill them up” so as to provide pay for anything no matter how fruitless in an effort to spur on consumption. A UBI is then nothing more than skipping the step of digging the hole. For the average man who is not corrupted and predisposed to the Keynesian model, the great pre-Keynesian economic insight of scarcity and of the need to produce before consuming is largely self-evident. The corollary to this insight is that any policy that hopes to help those rise up and better their material wellbeing should first help individuals be more productive.

Yang claims that the UBI will not cause people to quit their jobs, as $1,000 per month is too little to cause people to quit work. While this may be true in many instances, it still misses the point. Shouldn’t the goal of such a policy be to help individuals become financially independent? Have we completely given up on teaching a man to fish? Finland, which ran a trial of UBI for unemployed Fins from January 2017-December 2018 had hoped it would give people the financial security to allow them to receive education and build new skills needed to re-enter the workforce. But the study concluded that those on the UBI were no more likely to find employment than a control group who did not receive the payment. Yang’s proposal is far more sinister as he is not even singling out the unemployed. In this way, it is simply just expansionary fiscal policy that goes straight to individuals. Ironically, this is proposed by the same group of people that don’t want to cut taxes.

With UBI and Modern Monetary Theory rising to political prominence among the left’s young and hip, we should prepare for the onslaught of economic fallacies that will be employed to justify their enactment.

via ZeroHedge News https://ift.tt/2ELP0AR Tyler Durden

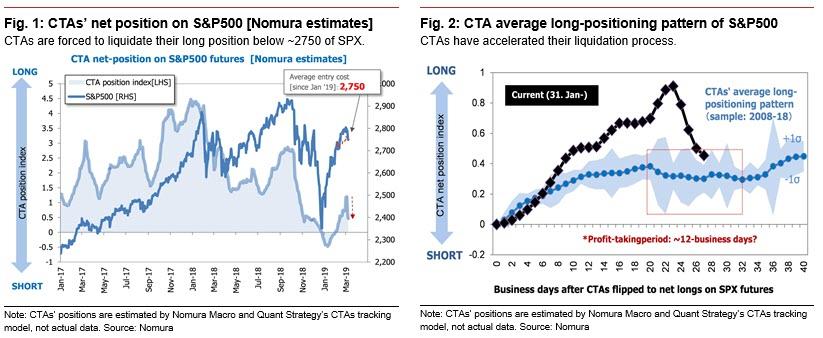

Earlier today, we explained why the technical picture for stocks is getting increasingly gloomy, when we noted that with the S&P dropping below 2,750, or a critical selling “trigger” for the trend-following community, CTAs have now started to sell.

And while the fundamentals have been turning increasingly more bearish in recent months (prompting every central bank to turn dovish in recent weeks), with the global economy rapidly slowing with Europe and Japan now effectively in recession, now not even the chartists can find a reason to remain bullish.

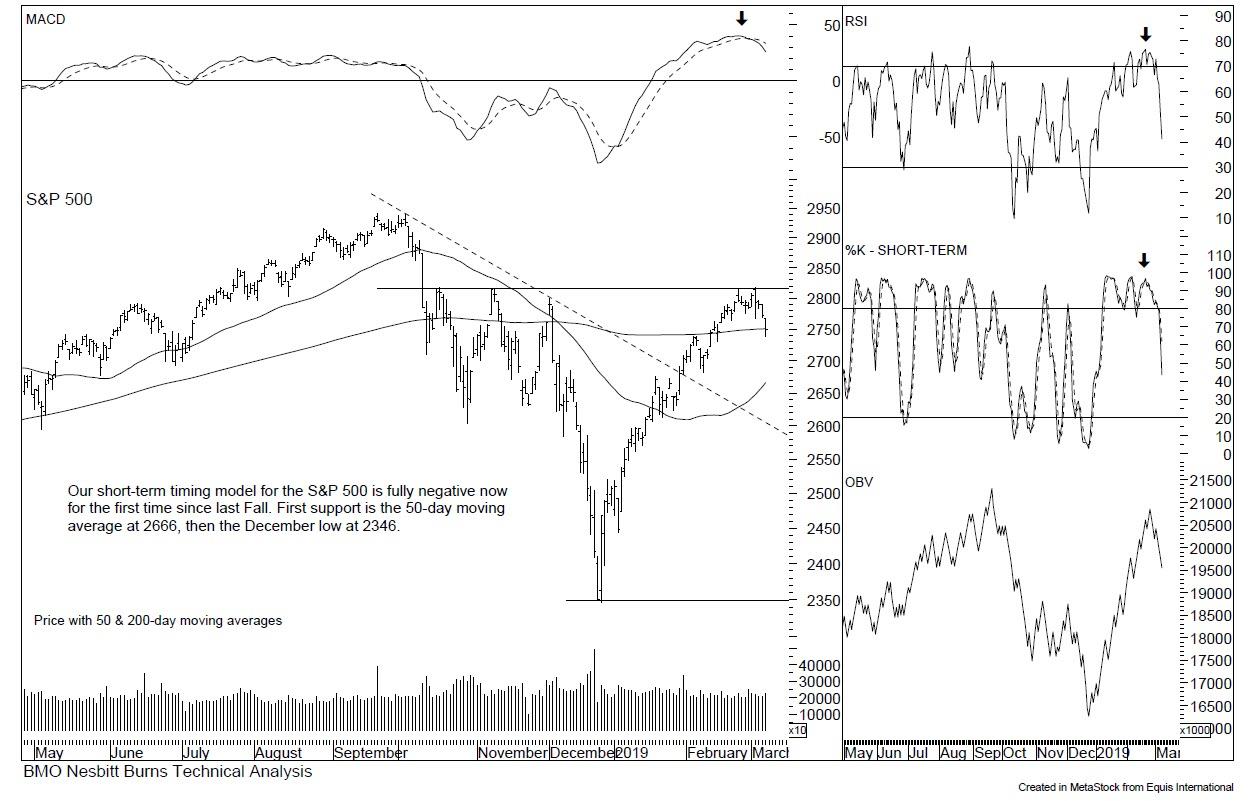

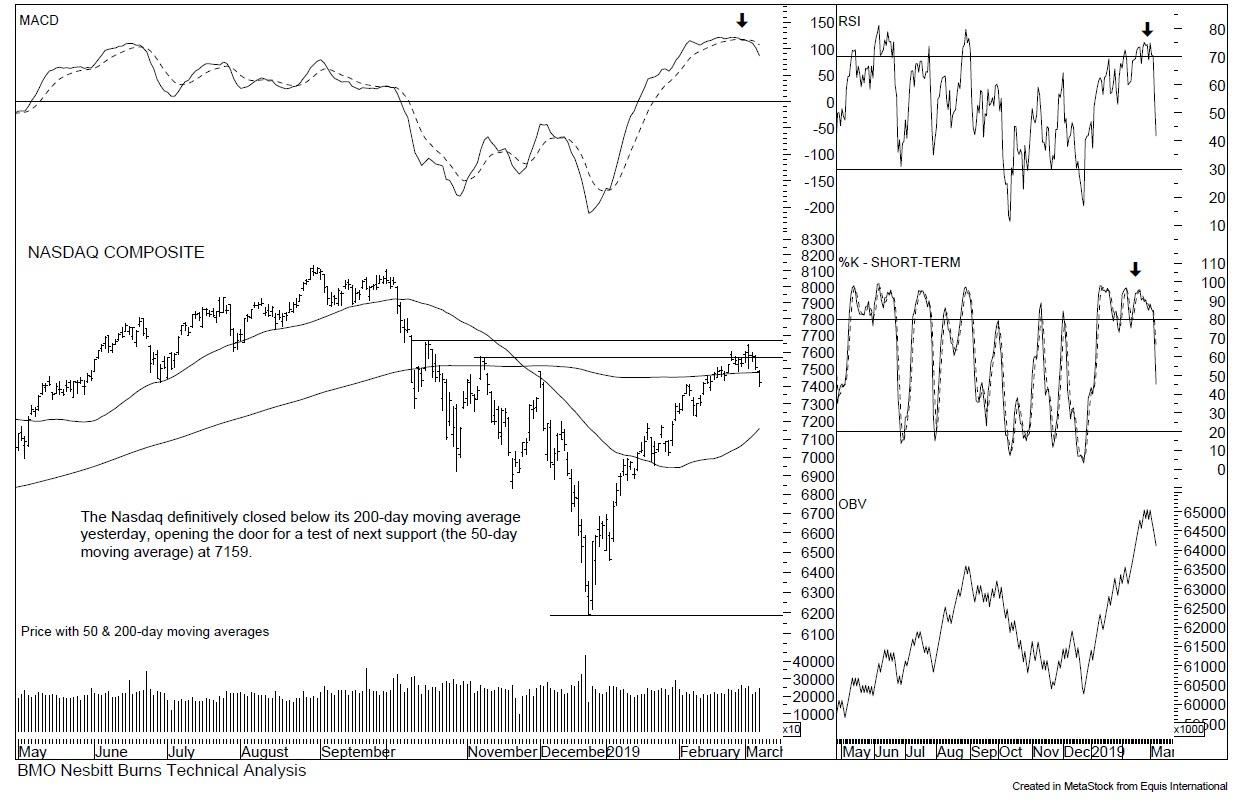

Case in point: BMOs chief technical analyst Russ Visch writes that after the “goldilocks” rally officially ended when the S&P failed to breach and hold 2800, “it appears as if the “re-test” phase of the “low, rally re-test” bottoming sequence is now underway in earnest as equity markets sold off sharply yet again yesterday, resulting in the S&P 500…

… and Nasdaq Composite closing below their 200-day moving averages again for the first time in nearly a month.”

With upside momentum broken, Visch says that the next support level from here is now the 50-day moving averages (S&P: 2666, Nasdaq: 7159) although, as the bearish technician has written in the past, he expects “a much deeper retracement than that.“

Additionally, and as Nomura warned previously, next Friday is “quadruple witching”, a day in which all four of the different types of options and futures contracts expire on the same day. This could be lead to even greater turbulence, as historically, markets have been prone to volatile price swings during expiry weeks as investors reposition large options and futures holdings so, as Visch notes, “it could get ugly pretty quickly.“

via ZeroHedge News https://ift.tt/2tVmPKF Tyler Durden

With the Italian government seemingly on the verge of collapse every few months, and with tensions between the two parties in the ruling coalition – Five Star and the League, especially as the former has been sliding in the polls at the expense of the latter’s rising popularity – escalating in recent weeks, it was only a matter of time before Italian bondholders had a PTSD flashback to May 2018 when the populist government first stormed on the stage, sending Italian bonds plunging. All that was missing was a catalyst.

Said catalyst emerged as a lingering dispute within Italy’s ruling coalition over the future of a train, or technically a high-speed rail link with France, escalated suddenly on Thursday, once again raising the risk of a government collapse, with the 5-Star chief accusing his partner of acting irresponsibly.

The Alpine rail line has been backed by the ruling League party but is fiercely opposed by its coalition partner, the 5-Star Movement, which argues Italy’s share of the funding would be better spent upgrading existing roads and bridges. And after League leader, the outspoken Matteo Salvini who continues to enjoy rising popularity with every new poll, said in an evening television interview he would not back down and his party would “never sign” a decree to block the project, 5-Star chief Luigi Di Maio accused him of threatening to bring down the government.

While the tensions between Di Maio and Salvini were for the most part contained before closed doors, the animosity between the two “equal” vice premiers erupted in public when Di Maio said in a statement that Salvini “will bear the responsibility before millions of Italians” adding that he considers “this to be irresponsible behavior” adding that he was “stunned by the threat of a government crisis” coming from Salvini.

The TAV project (Treno Alta Velocita) is a joint venture between the Italian and French states to link the cities of Turin and Lyon with a 58-km (36-mile) tunnel through the Alps on which work has already begun. According to Reuters, the EU has pledged to fund up to 40 percent of costs, Italy up to 35 percent and France up to 25 percent.

Earlier on Thursday, Italy’s Prime Minister Giuseppe Conte said that recently updated traffic projections for the line warranted a review of the project’s long-term viability and, if necessary, a renegotiation of the way the funding is split. Conte told reporters he had strong personal doubts about the validity of the venture and he would take responsibility for a final decision based on a cost-benefit analysis already carried out by the government.

That analysis, commissioned by Transport Minister Danilo Toninelli, a 5-Star politician, found the TAV was a waste of public money, estimating the economic return would be a negative balance of 7.0 billion-7.8 billion euros ($7.9 billion -$8.8 billion). Conte, who is technically not a member of either party but is closer to 5-Star, called the funding of the TAV “iniquitous” and said he would speak to France and the EU “to share our doubts and perplexities.”

However, as Reuters noted, despite his doubts, Conte acknowledged the ruling coalition remained “deadlocked” over the issue, as a Monday deadline approaches when the tenders must be launched to build or block key parts of the project.

And while Conte dismissed media speculation the Alpine rail link could be the issue that finally brings the government down as “absurd” saying that the dispute between the ruling parties was transparent and constructive, others disagree, and on Thursday night, Matteo Salvini who is currently Italy’s most popular politician and many believe can become Italy’s next premier outright without the need for a colaition, said he was ready “to go all the way” on the TAV dispute.

On Friday the spat continued, and the ruling coalition made no progress in defusing the dispute ahead of Monday’s looming deadline.

As Reuters updates, on Friday Salvini walked away from the negotiating table telling reporters he would not reopen discussion until after the weekend, in a move that seemed designed to allow the tenders, due to be opened on Monday, to go ahead.

In turn, a clearly displeased Di Maio said during a news conference that “(Salvini) can’t tell me ‘we’ll see each other on Monday’. This needs to be a weekend of work,” adding that he had asked Prime Minister Giuseppe Conte to do his best to block the tenders.

Some League politicians proposed that the tenders could be launched on schedule but with a clause that they could be revoked depending on the outcome of the coalition dispute. Di Maio rejected this, saying it made no sense to commit money to a project and then discuss whether to go ahead with it.

“Putting the government at risk over the TAV is absurd,” he said, appealing to Salvini to work with him for a deal, however as of this moment, Salvini has clearly refused to engage in negotiations, raising the probability that a government collapse could be imminent, and resulting in another episode of Italian bond volatility as the next Italian government will likely be even more populist than the current iteration.

For now markets, which have generally stopped responding to newsflow and instead are only focused on what central banks do next, have shrugged off the mounting coalition tensions, and on Friday Italian 10-year bond yields were heading for the biggest weekly drop since September, and the spread over German Bunds hovered around 245 basis points, compared with a recent high of 280 on Feb 22, on the back of the ECB’s TLTRO announcement which some have speculated makes the probability of a ruling crisis even greater as the risk of a market crash has been pushed back largely thanks to Draghi’s surprisingly dovish reversal unveiled on Thursday.

via ZeroHedge News https://ift.tt/2HltAgF Tyler Durden

The College of Charleston professor, a prolific digital-mob leader, has been active in trying to marginalize women who believe that men who identify as women should not be allowed to participate in women’s sports.

As noted by Red State‘s Sister Toldjah this week, McKinnon is claiming that women who want women’s sports to be limited to women are the functional equivalent of racists:

If Sharron Davies, Paula Radcliffe, or Martina Navratilova had said we need to keep black women out of sport to “protect it” and the “integrity of women’s sport”

That would be obviously racist

That’s why it’s obviously transphobic to exclude trans women now

If Sharron Davies, Paula Radcliffe, or Martina Navratilova had said we need to keep black women out of sport to “protect it” and the “integrity of women’s sport”

That would be obviously racist

That’s why it’s obviously transphobic to exclude trans women now

Not “name calling”

— Dr. Rachel McKinnon (@rachelvmckinnon) March 5, 2019

You’ve got to wonder how black women feel about being considered to vengeful white men such as McKinnon.

Toldjah reminds the professor that excluding a race from sports competition is “not even remotely comparable” to segregating the sexes in sporting competitions:

Black athletes were once viewed as inferior based on their race. Men’s and women’s competitions have always been separate because their bodies are different. It’s an indisputable scientific fact. …

This ain’t rocket science, y’all. Female athletes find losing to male athletes in female competition demoralizing, and they have legitimate reasons for feeling that way. Yet they’re being told to shut up, sit back, and take it.

[ZH: But it gets better…]

As BigLeaguePoilitcs.com reports, a British rapper briefly identified as female in order to break a weightlifting record and prove a point about transgender athletes.

“I keep hearing about how biological men don’t have any physical strength advantage over women in 2019… So watch me DESTROY the British Women’s deadlift record without trying. P.S. I identified as a woman whilst lifting the weight. Don’t be a bigot,” Zuby Tweeted, attaching a video of himself breaking the record.

I keep hearing about how biological men don’t have any physical strength advantage over women in 2019…

So watch me DESTROY the British Women’s deadlift record without trying.